flexible rollover product pds jan 2018 redesign eliza - … · flexible rollover product > pds...

TRANSCRIPT

Member guide:

Flexible Rollover Product

Date of issue: 7 May 2018

SUPER SA

Product disclosurestatement

> 2

Flexible Rollover Product > PDS

This Product Disclosure Statement (PDS) is a summary of signifi cant information and contains a number of references to important information (each of which forms part of the PDS). You should consider this information before making any decisions about the Super SA Flexible Rollover Product.

The information provided in this PDS is general information only and does not take into account your personal fi nancial situation or needs. You should therefore obtain fi nancial advice that is tailored to your personal circumstances.

1. About the Super SA Flexible Rollover Product 3

2. How super works 4

3. Benefi ts of investing with the Flexible Rollover Product 6

4. Risks of super 8

5. How we invest your money 9

6. Fees and costs 12

7. How super is taxed 16

8. Insurance in your super 19

9. How to open an account 23

10. Extra information 25

Up to date copies of this PDS and incorporated documents are available at www.supersa.sa.gov.au or by calling 1300 369 315.

Super SA reserves the right to change the information in this PDS from time to time where the change:

– only gives additional rights to investors and does not derogate from their existing rights,or

– is necessary or desirable, in the opinion of Super SA, to ensure that Super SA, as administrator of the Flexible Rollover Product, complies with applicable laws, or

– in the opinion of Super SA, is in the best interests of investors generally.

Changes to the information in this PDS will be notifi ed on the Super SA website. Where changes are of a materially adverse nature, Super SA will also issue a replacement PDS.

Contents

> 3

1. About the Super SA

Flexible Rollover Product

The Super SA Flexible Rollover Product is a low-cost place to invest your super money while giving you access to some, or all, of your money at any time1.

This product is designed to help meet your needs during your working life and into retirement.

If you cease working in the SA public sector, with the Super SA Flexible Rollover Product, you can avoid the inconvenience of having to fi nd a new fund administrator.

With the Super SA Flexible Rollover Product you can choose to grow your super while maintaining access to it and consolidate your retirement savings in preparation for purchasing an income stream. All within a tax-effective environment.

The Super SA Flexible Rollover Product is a not for profi t product and that means it’s here solely for the benefi t of its investors.

1 Subject to Commonwealth Government preservation rules.

Across all schemes and products, Super SA manages the super of:

– over 213,0002 members and

– has over $26.6 billion2 funds under management.

2 Figures current at 31 March 2018.

> 4

Flexible Rollover Product > PDS

Super is a tax-effective way of saving for your retirement. It’s an investment in your future!

The Commonwealth Government’s tax concessions and incentives are there to help boost your super savings. They also make super one of the best long-term investments around.

Whilst you are working it’s compulsory for your employer to make contributions of 9.5% of your salary into your super scheme, otherwise known as the Superannuation Guarantee (SG).

While most people can choose which super fund they would like their super paid into, SA public sector employees are members of a State Government super scheme.

For more information about how super works visit the Government website www.moneysmart.gov.au.

About the Flexible Rollover Product

As a current member (active or preserved) of one of the SA public sector super schemes you can invest in the Super SA Flexible Rollover Product.

Types of contributions

Within the Super SA Flexible Rollover Product you can make the following types of contributions:

– After-tax contribution: paying money into your super from your take-home pay.

– Government Co-contribution: a payment you could receive from the Commonwealth Government, if you qualify, for making after-tax contributions to your super.

The Super SA Flexible Rollover Product cannot accept contributions from employers.

2. How super works

> 5

It’s easy to contribute to your super!As a Super SA Flexible Rollover Product investor you can:

– Make a lump sum payment of $1,000 or more by cheque, money order or BPAY.

– Transfer super you have in another fund into your Super SA Flexible Rollover account.

Bringing your money together

If you have super invested in several funds, you can bring it all together by rolling it into the Super SA Flexible Rollover Product.

Any part of your rollover that was subject to preservation before it was transferred to the Flexible Rollover Product will remain preserved until you reach your Commonwealth Government preservation age, which you’ll fi nd in the Extra Information section of this PDS.

You can fi nd out more about consolidating your super and download the Easy Roll In form at www.supersa.sa.gov.au.

Withdrawals

You can make withdrawals from your account. Each withdrawal must be $1,000 or more and is subject to Commonwealth preservation rules. A balance of at least $1,500 must be maintained in the FRP at all times.

Contribution limits

There is a limit on the total value of after-tax contributions you can make to your super. Exceeding this limit means you may have to pay extra tax.

Further information on tax rates and contribution limits is available in the How super is taxed section of this PDS.

2. How super works (cont.)

You should read the important information about how super works in the Grow Your Super fact sheet and Accessing Your Super fact sheet before making a decision. Go to www.supersa.sa.gov.au to view these fact sheets. The material relating to growing and accessing your super may change between the time when you read this PDS and the day when you acquire the product.

> 6

Flexible Rollover Product > PDS

The Super SA Flexible Rollover Product can help you make the most of your super!Low fees and competitive insurance

– Low administration fee: Just $1.35 a week! (minimum annual fee of $70.20)

– No contribution fees.

– Access to Death and Total and Permanent Disablement Insurance or Death Only Insurance.

Great ways to grow your super

– The option to contribute non-super monies.

– Choice of investment options: you can choose to invest your super in any number of the eight available investment options. Choose one, or a combination of options.

Leave your super to your Estate

– You can nominate a legal personal representative (estate) so that your death benefi t is paid to your Estate, and distributed according to your Will.

Options for your spouse

– Spouse Account: You have the option to open an account for your spouse or putative spouse1.

Access to your super while you’re working

– Early Access to Super: You have the option to access your super when you reach your Commonwealth preservation age using an income stream – even if you’re still working.

Take advantage of award winning products

– The Super SA Income Stream has been awarded the AAA Selecting Super Quality Assessment and the highest possible rating of 5 Apples by Chant West.2 Both the Income Stream and Flexible Rollover Product have also been given a Gold rating by SuperRatings.

Range of member services

– Free education seminars on a variety of topics.

– Industry Fund Services offer fee for service personal fi nancial advice, or you can consult your own independent fi nancial adviser.

– Access the latest super info via our website and mobile site. You also have 24 hour secure access to your account online.

3. Benefi ts of investing with the

Super SA Flexible Rollover Product

1 For defi nition refer to the Glossary on the Super SA website.2 For further information about the ratings methodology used by Chant West, see www.chantwest.com.au.

> 7

Retiring from the SA public sector

Investing your money in the Super SA Flexible Rollover Product allows you to keep your money invested in a tax-effective super environment with Super SA, while still giving you the freedom to withdraw part or all of your money, subject to Commonwealth Government preservation rules. You’ll fi nd your preservation age in the Extra Information section of this PDS.

Because you are keeping your money within the super environment, the Super SA Flexible Rollover Product is the perfect way to consolidate your super before moving it into an income stream.

Under age 55 and leaving the SA public sector

Investing your super in the Super SA Flexible Rollover Product means you continue to enjoy Super SA’s products and services. This includes an option to keep your current level of insurance through Super SA.

Still employed in the SA public sector

You are also eligible to invest in the Super SA Flexible Rollover Product if you are a current member of an SA public sector super scheme. However, you cannot roll the money held in your current scheme into the Super SA Flexible Rollover Product until you cease employment with the SA public sector.

Super fl exibility… whether you are leaving the SA public sector or leaving the workforce, the Super SA Flexible Rollover Product is designed to be fl exible enough to meet your needs.

3. Benefi ts of investing with the

Super SA Flexible Rollover Product (cont.)

You should read the important information about super benefi ts before making a decision. Go to the Accessing

Your Super fact sheet at www.supersa.sa.gov.au. The material relating to super benefi ts may change between the time when you read this PDS and the day when you acquire the product.

> 8

Flexible Rollover Product > PDS

4. Risks of super

All investments have some type of risk and super is no different.

Different investment options may carry different levels of risk, depending on the assets that make up that option.

Generally, the investment options that offer the highest long-term returns may also carry the highest level of short-term risk.

When it comes to your super, it’s important to know that:

– the value of your super investment may go up and down

– the level of your returns will vary

– returns are not guaranteed and you may lose some of your money

– future returns may differ from past returns

– laws affecting super may change.

Your choice of risk level will vary depending on a range of factors including your age, investment time frame, your other investments and your risk tolerance.

As a Super SA Flexible Rollover Product investor, you should be aware that capital losses are possible, depending on the investment options you choose and their performance over time. This is due to the volatility of investment markets.

It’s also important to keep in mind that your future super savings, including contributions and investment earnings, might not be enough to provide you with the lifestyle you want in retirement.

You should read the important information about risks of super before making a decision. Go to the Investment fact sheet at www.supersa.sa.gov.au. The material relating to risks of super may change between the time when you read this PDS and the day when you acquire the product.

> 9

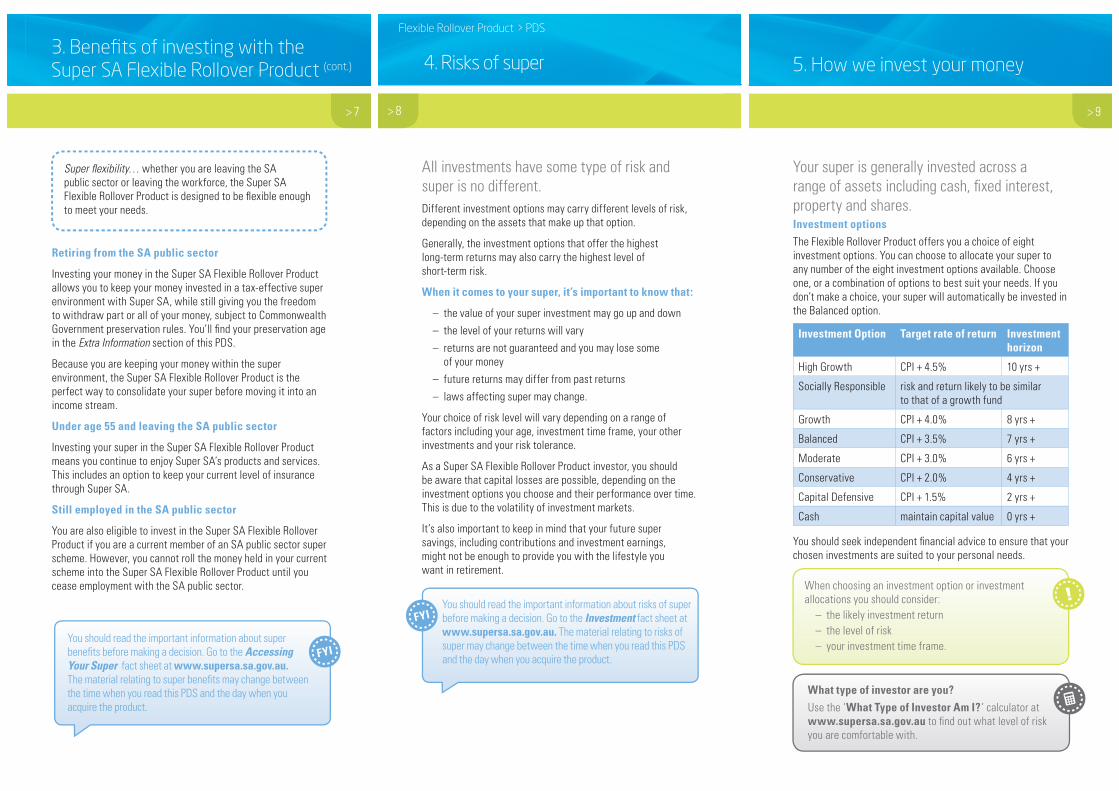

5. How we invest your money

Your super is generally invested across a range of assets including cash, fi xed interest, property and shares. Investment options

The Flexible Rollover Product offers you a choice of eight investment options. You can choose to allocate your super to any number of the eight investment options available. Choose one, or a combination of options to best suit your needs. If you don’t make a choice, your super will automatically be invested in the Balanced option.

Investment Option Target rate of return Investment horizon

High Growth CPI + 4.5% 10 yrs +

Socially Responsible risk and return likely to be similarto that of a growth fund

Growth CPI + 4.0% 8 yrs +

Balanced CPI + 3.5% 7 yrs +

Moderate CPI + 3.0% 6 yrs +

Conservative CPI + 2.0% 4 yrs +

Capital Defensive CPI + 1.5% 2 yrs +

Cash maintain capital value 0 yrs +

You should seek independent fi nancial advice to ensure that your chosen investments are suited to your personal needs.

When choosing an investment option or investment allocations you should consider:

– the likely investment return

– the level of risk

– your investment time frame.

What type of investor are you?

Use the ‘What Type of Investor Am I? ’ calculator at www.supersa.sa.gov.au to fi nd out what level of riskyou are comfortable with.

> 10

Flexible Rollover Product > PDS

5. How we invest your money (cont.)

Switching options

To switch investment options log into our online member portal or complete the Investment Choice form and return it to Super SA.

You can choose to switch your super across any number of the eight available investment options.

You can nominate different investment options for your current super balance and your future contributions.

The fi rst switch in any fi nancial year is free and there’s a $20 fee for subsequent switches in the same fi nancial year. There’s no switching fee for redirecting the investment of future contributions.

Switching investment options is an important decision and you should seek professional fi nancial advice.

If you decide to switch your investment options you need to keep in mind that you can’t switch within seven business days of opening your account or investing additional funds in excess of $5,000 (by rollover, contribution or other method).

Switching timeframes

The unit price applied to a switch will represent the market value of an investment option calculated after the request to switch is received.

A request to switch your current super balance received before 5pm on a business day will generally be processed on the third business day following the date of receipt. If switching via the member portal, a switch made to future contributions will take effect immediately. Check the Super SA website for any variation to this.

> 11

Investment details for the Balanced (default) option1

Description This option is structured for investors with an investment time horizon of at least seven years. Annual returns may be volatile.

Investment return objective

Infl ation + 3.5%

Asset allocation

This option is invested in the range of 55% – 75% in Growth assets (shares, certain types of property, private equity and other growth opportunities) and the balance in Defensive assets (such as cash and fi xed interest).

Strategic Asset Allocation

Australian Equities 23%

International Equities 19%

Property 12%

Diversifi ed Strategies Growth 8%

Diversifi ed Strategies Income 16%

Infl ation Linked Securities 9%

Fixed Interest 11%

Cash 2%

Min suggested time frame

7 years

Summary risk level

It is likely that a negative return might be expected to occur between three and four years in 20.

Risk classifi cation

Medium to high risk (Risk Band 5)2

5. How we invest your money (cont.)

You should read the important information about investments, including each of the other investment options, responsible investing, and how investment options may be changed, before making a decision. Go to the Investment fact sheet at www.supersa.sa.gov.au. The material relating to investments may change between the time when you read this PDS and the day when you acquire the product.

1 Figures current at 1 July 2017.2 The Standard Risk Measure is based on industry guidance.

> 12

Flexible Rollover Product > PDS

6. Fees and costs

Fees and other costs for the Balanced investment option

The table on the next page shows fees and costs that you may be charged for the Balanced investment option and can be used to compare costs between different super products.

These fees and costs are paid directly from your super account or deducted from your investment earnings, depending on the fee or cost.

Did you know?

Small differences in both investment performance and fees and costs can have a substantial impact on your long-term returns.

For example, total annual fees and costs of 2% of your account balance rather than 1% could reduce your fi nal return by up to 20% over a 30 year period. For example reduce it from $100,000 to $80,000.

You should consider whether features such as superior investment performance or the provision of better member services justify higher fees and costs.

To fi nd out moreIf you would like to fi nd out more, or see the impact of fees based on your own circumstances, the Australian Securities and Investments Commission (ASIC) website, www.moneysmart.gov.au has a superannuation calculator to help you check out different fee options.

CONSUMER ADVISORY WARNING

> 13

6. Fees and costs (cont.)

Flexible Rollover Product Balanced

Type of Fee Amount How and when paid

Investment fee Nil The applicable investment costs are included in the indirect cost ratio below.

Administration fee

$1.35 per week subject to a minimum annual fee of $70.20

Deducted from your account on a weekly basis.

Buy-sell spread Nil Not applicable

Switching fee1 $20 for each switch (cost of the fi rst switch waived each fi nancial year).

Deducted from your account at the time of the switch.

Exit Fee (partial withdrawal only)

$20 for each withdrawal(cost of the fi rst waived each fi nancial year).

Deducted from your account at the time of the withdrawal.

Advice fees Nil You will only be charged an Adviser fee if you agree to receive fi nancial advice. These fees will be discussed and agreed with you.

See over the page for information on other fees and costs.

1There is no switching fee for redirecting future contributions.

> 14

Flexible Rollover Product > PDS

6. Fees and costs (cont.)

Balanced option – fee example

This table gives an example of how the fees and costs in the Balanced option for this product can affect your super investment over a one year period.

You should use this table to compare this product with other superannuation products.

Example:Balanced Option

Balance of $50,000

Investment fees

Nil For every $50,000 you have in Balanced you will be charged $0 each year.

PLUS: Administration fees

$70.20 ($1.35 per week)

And, you will be charged $70.20 in administration fees regardless of your balance.

PLUS: Indirect costs for Balanced

0.93% And, indirect costs of $465 each year will be deducted from your investment.

EQUALS: Cost of product

$535.20 If your balance was $50,000, then for that year you will be charged fees of $535.20 for the Balanced investment option.

– Additional fees may apply.

– Super SA does not charge commissions or receive commissions from fi nancial advisers, sales agents or any other person or entity.

Other fees and costs1

Indirect cost

ratio2 (ICR)0.93% Fee deducted from the

product’s investment returns before earnings are allocated to your account which occurs through twice weekly determined unit prices (not deducted directly from your account).

1 For information on other fees and costs such as activity fees (Family Law) and insurance fees refer to the Additional Explanation of Fees and Costs in the Fees and Costs Fact Sheet.2 The ICR represents investment management costs for the 2016-17 year and varies across investment options. Investment costs vary from year to year.

> 15

You should read the important information about fees and costs including the fees applicable to each of the other investment options in the Fees and Costs fact sheet at www.supersa.sa.gov.au before making a decision. Further information about the defi ned fees can be found at www.supersa.sa.gov.au/knowledge_centre/glossary. The material relating to fees and costs may change between the time when you read this PDS and the day when you acquire the product.

6. Fees and costs (cont.)

Changes to fees and costs

The Flexible Rollover Product is a not for profi t product and Super SA endeavours to keep fees and costs low for investors.

As our fees are already as low as possible, it’s not possible to negotiate lower fees.

Occasionally, fees might need to rise to cover costs without your consent. If this happens, we’ll give you 30 days’ prior written notice.

Fees paid to Financial Advisers

If you consult a fi nancial adviser additional fees may be payable. For more information refer to the Statement of Advice (SOA) received from your fi nancial adviser. If you get fi nancial advice from Industry Fund Services (IFS) you can pay for the fi nancial planning service direct from your Triple S account. Fees to fi nancial planners may be paid from your account if you close your account.

To see how fees and costs may affect your account balance use the calculator on the ASIC website at www.moneysmart.gov.au.

> 16

Flexible Rollover Product > PDS

7. How super is taxed

Unlike many other forms of savings super is concessionally taxed. Your super is generally taxed at three different stages.

1. Tax on contributions

A contributions tax of 15% is usually deducted from most employer contributions at the time they are paid into super (includes salary sacrifi ce contributions).

Please note: The Super SA Flexible Rollover Product cannot accept employer contributions and salary sacrifi ce contributions.

However some government schemes, such as the Triple S, Lump Sum Scheme and Pension Scheme are “untaxed funds”, which means that contributions tax is not deducted from contributions as they are paid into the scheme. When money from these schemes is rolled over into another scheme (such as the Super SA Flexible Rollover Product), contributions tax of 15% will be deducted by the new fund. Any after-tax contributions you have made to your super are tax free when you withdraw your super.

2. Tax on investment earnings

As with most other super schemes, the Super SA Flexible Rollover Product is required to pay up to 15% tax on its investment earnings. The tax will be applied to the product as a whole and will be refl ected in the unit price of each investment option.

3. Tax on withdrawals and lump sum payments

Withdrawals from your account may be taxed if you’re under age 60 (refer to table on page 17). Once you turn 60, generally no tax will apply to withdrawals.

> 17

7. How super is taxed (cont.)

Your age Tax on taxable (taxed) component

Under Commonwealth preservation age1

20% maximum rate (no limit)

Commonwealth Preservation Age up to age 591

Taxed at 0% up to $200,0002

15% tax on balance (no limit)

60 or over Tax free

Please note: Assumes tax fi le number (TFN) provided. If you do not provide your TFN, you will be taxed at the highest marginal tax rate plus Medicare levy. The 2% Medicare levy is also deducted when tax is payable if you take your entitlement in cash.

1 Commonwealth Government preservation ages are listed in the “Extra

Information” section of this PDS.

2 From 1 July 2017

Tax treatment of lump sum withdrawals when taken in cash

The tax that applies to lump sum withdrawals from your Super SA Flexible Rollover Product will depend on your age and the different components that make up your super. You cannot select which components you withdraw as a lump sum. Tax components will be calculated in the same proportion as the components that make up your total account balance.

The following table sets out the taxation on the most common components of your superannuation lump sum.

> 18

Flexible Rollover Product > PDS

7. How super is taxed (cont.)

Tax and breach of caps and limits

The Commonwealth Government has set certain caps and limits on the amount of super contributions you can make or receive. Exceeding these will incur the highest marginal rate plus Medicare levy on the excess amount:

– After tax contributions are limited to $100,000 each fi nancial year or, if you are under age 65 during the fi nancial year, you can bring forward the limit for two years to contribute up to $300,000 in one year1.

Exceeding caps and limits

If you exceed the caps and limits you will incur the highest marginal rate plus Medicare levy on the excess amount.

Providing your TFN

To ensure your entitlement is taxed at concessional rates, you should provide your tax fi le number (TFN) to Super SA. If you do not, you will be taxed at the highest marginal tax rate plus 2% Medicare levy.

Online: log into our online member portal at www.supersa.sa.gov.au and type your TFN into the My Details page.

Post: Download the Tax File Number Notifi cation form and send it to Super SA.

You should read the important information about how super is taxed before making a decision. Go to the Tax fact sheet at www.supersa.sa.gov.au and read how taxation affects Triple S. The material relating to how super is taxed may change between the time when you read this PDS and the day when you acquire the product.

1Subject to transitional arrangements. Please visitwww.ato.gov.au for more information.

> 19

8. Insurance in your super

Having adequate insurance will help ensure that you and those close to you are fi nancially protected should the unexpected happen.

In the Super SA Flexible Rollover Product you’ve got the option of purchasing cost-effective insurance cover.

Types of cover

You can choose Death Only Insurance or Death and Total and Permanent Disablement Insurance. Providing you meet the eligibility criteria, you can apply for either. The cost of your insurance will depend on which type you choose.

Eligibility for Insurance

Death and Total and Permanent Disablement cover

If you are under 65 and working 20 hours or more per week on a regular basis, you can apply for Death and Total and Permanent Disablement (TPD) Insurance.

To be able to make a TPD claim, you must have averaged 20 hours per week of paid employment for the 12 months preceding your date of incapacity as confi rmed by your employer.

Death Only cover

If you are under 65 and working less than 20 hours per week on a regular basis you can apply for Death Only insurance but not Death and TPD Insurance.

If you are a Spouse investor you can only apply for Death Only Insurance.

For more information on Death Only insurance go to the Insurance fact sheet at www.supersa.sa.gov.au.

The type of insurance available is referred to as Standard cover.

> 20

Flexible Rollover Product > PDS

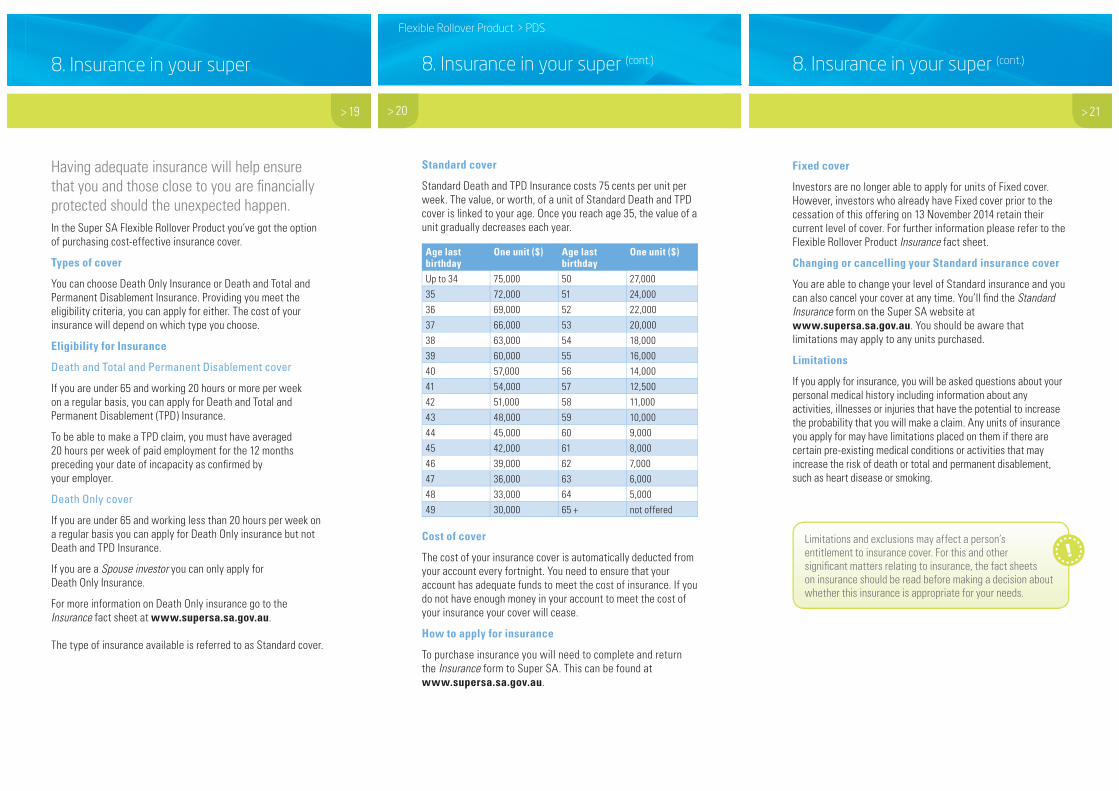

Standard cover

Standard Death and TPD Insurance costs 75 cents per unit per week. The value, or worth, of a unit of Standard Death and TPD cover is linked to your age. Once you reach age 35, the value of a unit gradually decreases each year.

Age last birthday

One unit ($) Age last birthday

One unit ($)

Up to 34 75,000 50 27,000

35 72,000 51 24,000

36 69,000 52 22,000

37 66,000 53 20,000

38 63,000 54 18,000

39 60,000 55 16,000

40 57,000 56 14,000

41 54,000 57 12,500

42 51,000 58 11,000

43 48,000 59 10,000

44 45,000 60 9,000

45 42,000 61 8,000

46 39,000 62 7,000

47 36,000 63 6,000

48 33,000 64 5,000

49 30,000 65 + not offered

Cost of cover

The cost of your insurance cover is automatically deducted from your account every fortnight. You need to ensure that your account has adequate funds to meet the cost of insurance. If you do not have enough money in your account to meet the cost of your insurance your cover will cease.

How to apply for insurance

To purchase insurance you will need to complete and return the Insurance form to Super SA. This can be found atwww.supersa.sa.gov.au.

8. Insurance in your super (cont.)

> 21

8. Insurance in your super (cont.)

Fixed cover

Investors are no longer able to apply for units of Fixed cover. However, investors who already have Fixed cover prior to the cessation of this offering on 13 November 2014 retain their current level of cover. For further information please refer to the Flexible Rollover Product Insurance fact sheet.

Changing or cancelling your Standard insurance cover

You are able to change your level of Standard insurance and you can also cancel your cover at any time. You’ll fi nd the Standard

Insurance form on the Super SA website at www.supersa.sa.gov.au. You should be aware that limitations may apply to any units purchased.

Limitations

If you apply for insurance, you will be asked questions about your personal medical history including information about any activities, illnesses or injuries that have the potential to increase the probability that you will make a claim. Any units of insurance you apply for may have limitations placed on them if there are certain pre-existing medical conditions or activities that may increase the risk of death or total and permanent disablement, such as heart disease or smoking.

Limitations and exclusions may affect a person’s entitlement to insurance cover. For this and other signifi cant matters relating to insurance, the fact sheets on insurance should be read before making a decision about whether this insurance is appropriate for your needs.

> 22

Flexible Rollover Product > PDS

8. Insurance in your super (cont.)

You should read the important information about Death and TPD insurance and Death Only insurance, including eligibility and limitations, before making a decision. Go to the Insurance fact sheet and the Insurance and

Leaving the Public Sector fact sheet at www.supersa.sa.gov.au. The material relating to insurance may change between the time when you read this PDS and the day when you acquire the product.

Continuation of Triple S insurance when ceasing employment

If you invest in the Flexible Rollover Product within 60 days of ceasing SA public sector employment and you held Triple S insurance cover on the last day you worked, you can elect to continue the same type and level of Death and TPD insurance in the Super SA Flexible Rollover Product without having to provide further medical information, provided you meet the required age and employment conditions.

> 23

Joining the Super SA Flexible Rollover Product is only three steps away!

1. Complete the Application to purchase form available in the hardcopy or printable PDF version of this PDS.

2. Complete an Investor contribution form available in the hardcopy or printable PDF version of this PDS.

3. A $1,500 payment must accompany your forms. You can make your payment by cheque or money order. For more information go to the ways to pay page of the website located at www.supersa.sa.gov.au.

You can also establish a Flexible Rollover Product account by rolling in your Triple S entitlement (if you have resigned or retired from the SA public sector).

Want an account for your spouse?

You have the option to create a Super SA Flexible Rollover account for your spouse or putative spouse. You can do so by completing the Application to purchase form available in the hardcopy or printable PDF version of this PDS (the Setting up a

Spouse Account fact sheet available on the website can assist you in completing the form).

Spouse members can receive spouse contributions, Commonwealth Government Co-contributions, rollovers, make personal after-tax contributions and apply for voluntary Death Only Insurance.

A Spouse Account can be established by any of the following methods (as long as the minimum starting balance is $1,500):

– a personal contribution by the spouse (by cheque or money order)

– a spouse contribution made to the Spouse Account, or

– a rollover from the spouse’s previous super fund.

9. How to open an account

> 24

Flexible Rollover Product > PDS

Cooling off

You have 14 days from the date we acknowledge receipt of your application to decide if the Super SA Flexible Rollover Product is the right choice for you. During this time you can cancel your membership.

If you cancel, any administration fees applied to your account will be reversed and the amount returned will be calculated using the unit price effective at the date of cancellation.

The amount you receive will also be less any withdrawals made during your membership and any taxes payable.

To close your account during the cooling-off period, you need to send a written request to Super SA at the address shown on the back cover of this PDS.

9. How to open an account (cont.)

> 25

Commonweath Government preservation age

Your Commonwealth Government preservation age depends on

your date of birth:

Date of birth Commonwealth Government preservation age

Before 1 July 1960 55

1 July 1960 to 30 June 1961 56

1 July 1961 to 30 June 1962 57

1 July 1962 to 30 June 1963 58

1 July 1963 to 30 June 1964 59

After 30 June 1964 60

Complaints resolution process

Super SA aims to resolve all matters through its internal enquiry and complaints processes.

If you have any concerns with a product or service provided by Super SA and our Member Service Centre has not been able to provide a satisfactory response, you can escalate the matter by lodging a formal complaint with Super SA. Complaints need to be in writing and may be submitted in the following ways:

Online: Complete and submit the online Member Complaint Form.

Download from the website: Download, complete and send the Member Complaint Form to Super SA.

Mail: Complaints Offi cer, Super SA, GPO Box 48, Adelaide SA 5001.

Email: [email protected]

If the Complaints Offi cer cannot resolve the issue you may choose to lodge an appeal with the Super SA Board or have the matter investigated by the State Ombudsman.

10. Extra information

Cover photographs:

Adelaide Oval, South Australian Tourism Commission

DECD; SA Water; SA Ambulance

To fi nd out more visit supersa.sa.gov.au

Public - I1 - A1

Website

supersa.sa.gov.au

Member Services

Ground Floor

151 Pirie Street

(enter from Pulteney Street)

Adelaide SA 5000

Postal address

GPO Box 48, Adelaide, SA 5001

Telephone

(08) 8207 2094

or 1300 369 315

(for regional callers)

Facsimile

(08) 8115 1296

ABN

11 635 839 852

USI

11635839852001

If you require further information please contact Super SA:

Flexible Rollover Product ratings:

SuperRatings does not issue, sell, guarantee or underwrite this product. Go to superratings.com.au for details of its ratings criteria.

Account IDSuper ID

Please complete all the details on this form in BLOCK LETTERS and return it to Super SA.

1. PERSONAL DETAILS

Mr Ms Miss Mrs Dr Prof

Surname

Given name(s)

Residential address

Postcode

Postal address (if different from above)

Postcode

Date of birth / / Male Female

Telephone WORK

HOME

MOBILE

When establishing a Spouse Account, please provide spouse details in Section 1 above and Super SA member details below.

Name of partner (Super SA member)

When entitlement was received

Super SA member’s Super/Investor ID

Date of birth / /

You are required to provide proof of identity documents with this application. Please see the Proof of Identity fact sheet for more information.

2. INVESTMENT OPTIONSPlease refer to the Investment section of the Super SA Flexible Rollover Product – Product Disclosure Statement (PDS) to assist you in selecting investment options. Select the percentage you wish to invest in each option below in whole percentages. If you do not select an option your money will be invested in the Balanced option.

High Growth %

Socially Responsible %

Growth %

Balanced %

Moderate %

Conservative %

Capital Defensive %

Cash %

Total =100%

3. TRANSFER DETAILSPlease indicate from which SA public sector scheme if any, you are transferring your funds:

Triple S Lump Sum Pension

Other Government super fund (please specify):

4. FINANCIAL ADVISER AUTHORISATION –optional

I authorise my financial adviser to enquire about my Super SA Flexible Rollover Product details.

I understand that this authorisation will be effective for two years, unless revoked in writing by me before that time.

Financial adviser details:Name Company name

Address Postcode

Telephone

Fax

Important: – You will need to complete an Application for Payment of Entitlement form to release entitlements from your previous Super SA scheme.

– Cheques should be made payable to Super SA Flexible Rollover Product.

– If you are an active member of a Super SA scheme (eg Triple S, Lump Sum Scheme, Pension Scheme) you cannot roll money out of that account into the Flexible Rollover Product.

– Employer contributions cannot be paid into the Super SA Flexible Rollover Product.

Account IDAccount ID

Form updated May 2018 Sensitive: Personal (when completed) -I2-A1 Page 1 of 2

Please complete all the details on this form in BLOCK LETTERS and return it to Super SA.

SUPER SA FLEXIBLE ROLLOVER PRODUCT FRP17

APPLICATION TO PURCHASE FORM

5. INSURANCE OPTIONTo apply for insurance through the Super SA Flexible Rollover Product you need to complete the Insurance form found at the back of this PDS.

I wish to apply for insurance and have completed the Insurance form.

6. LEGAL PERSONAL REPRESENTATIVE (ESTATE) – optionalYour death benefit is automatically paid to your spouse (if any). If you would prefer your death benefit to be paid to your Estate, and distributed according to your Will, you can nominate a legal personal representative (estate).

I wish to nominate a legal personal representative (estate) and have completed the Binding Death Nomination – Legal Personal Representative (Estate) form (available to download from the Super SA website).

7. TAX FILE NUMBERSupplying your TFN to Super SA is optional. However, if you choose not to supply your TFN, you may pay more tax on your entitlements than you have to. If we do not have your TFN, tax will be deducted from every withdrawal at the highest marginal rate.

My tax file number is:

8. RECIPIENT DECLARATIONI hereby apply to become an investor in the Super SA Flexible Rollover Product and declare that:

– I understand that the Super SA Flexible Rollover Product PDS is a general guide and does not contain financial advice.

– I understand that Super SA will invest my super according to my choice of investment option and I accept full responsibility for my investment choice and acknowledge that I am aware of the consequences of making such an election.

– The information supplied on this form is true and correct. – I understand that the Super SA Flexible Rollover Product PDS dated 7 May 2018 represents

the terms and conditions under which the Super SA Board offers this Flexible Rollover Product. The terms and conditions are subject to any changes in Commonwealth Acts and Regulations.

– I have read the Super SA Flexible Rollover Product PDS dated 7 May 2018 and I fully understand its contents and accept the terms and conditions set out in it.

Signature Date / /

Please complete all the details on this form and return the signed original to Super SA.

Contact details

Websitewww.supersa.sa.gov.au

Telephone(08) 8207 2094 or 1300 781 874 (for regional callers)

MailGPO Box 48, Adelaide SA 5001

In personGround Floor 151 Pirie Street(enter from Pulteney Street)Adelaide SA 5000

Form updated May 2018 Sensitive: Personal (when completed) -I2-A1 Page 2 of 2

SUPER SA FLEXIBLE ROLLOVER PRODUCT FRP17

APPLICATION TO PURCHASE FORM

Account ID

Contact details Website www.supersa.sa.gov.au

Email [email protected]

Telephone (08) 8207 2094 1300 369 315 (for regional callers)

Mail GPO Box 48, Adelaide SA 5001

Visit Ground Floor (enter from Pulteney Street)

151 Pirie Street ADELAIDE SA 5000

2. PERSONAL CONTRIBUTIONI wish to contribute the amount of $ . I enclose a cheque made payable to “Super SA Flexible Rollover Product”.

(Minimum $1,500 for establishing a Super SA Flexible Rollover Product account. Minimum of $1,000 for additional contributions once an account has been established.)

In order to make a personal contribution you must meet one of the following conditions:

I am under the age of 65. I am over the age of 65 and under the age of 75 and in the

current financial year have worked in paid employment for at least 40 hours in a period of no more than 30 consecutive days.

If you are unable to tick one of the above boxes then you may not be eligible to contribute. Please contact Super SA for further information.

3. ELIGIBLE SPOUSE CONTRIBUTION*Please complete this section if you want to make an eligible spouse contribution to your spouse’s account.My spouse wishes to contribute the amount of $ to my Super SA Flexible Rollover Product account. I enclose a cheque made payable to “Super SA Flexible Rollover Product”.

(Minimum $1,500 for establishing a Spouse Account. Minimum of $1,000 for additional contributions once an account has been established.)

To receive an eligible spouse contribution you must meet one of the following conditions:

I am under the age of 65. I am over the age of 65 and under the age of 70 and in the

current financial year have worked in paid employment for at least 40 hours in a period of no more than 30 consecutive days.

If you are unable to tick one of the above boxes then you may not be eligible to receive an eligible spouse contribution. Please contact Super SA for more information.

*An eligible spouse is defined in Commonwealth Government Legislation as your:– Legal spouse that you are currently living with.– De facto spouse that you are living with on a genuine domestic basis as a couple.

1. PERSONAL DETAILS

Mr Ms Miss Mrs Dr Prof

Surname

Given name(s)

Residential address

Postcode

Postal address (if different from above)

Postcode

Date of birth / / Male Female

Telephone WORK

HOME

MOBILE

When establishing a Spouse Account, please provide spouse details in Section 1 above and Super SA member details below.

Name of partner (Super SA member)

When entitlement was received

Super SA member’s Account ID

Date of birth / /

Account ID

SUPER SA FLEXIBLE ROLLOVER PRODUCT FRP15

INVESTOR CONTRIBUTION FORM

Please complete all the details on this form in BLOCK LETTERS and return it to Super SA.

Form updated 7 May 2018 Sensitive: Personal (when completed) -I2-A1 Page 1 of 2

Please complete all the details on this form and return the signed original to Super SA.

4. INVESTOR DECLARATION– I declare that the information I have provided on this form is true and correct. – I understand that my contribution and any eligible spouse contribution will be invested in

the Super SA Flexible Rollover Product according to the specified investment option.– If I wish to change my investment option I will complete an Investment Choice form.– I understand that this contribution is preserved and generally cannot be cashed until

age 65 or genuine retirement after I reach my Commonwealth Government preservation age.– If I wish to claim a personal superannuation deducation for this contribution, I will complete

and lodge a Notice of Intent to Claim form (available from www.ATO.gov.au).

Signature Date

SUPER SA FLEXIBLE ROLLOVER PRODUCT FRP15

INVESTOR CONTRIBUTION FORM

Form updated 7 May 2018 Sensitive: Personal (when completed) -I2-A1 Page 2 of 2

Account ID

1. PERSONAL DETAILS

Mr Ms Miss Mrs Dr Prof

Surname

Given name(s)

Residential address

Postcode

Postal address (if different from above)

Postcode

Date of birth / / Male Female

Telephone WORK

HOME

MOBILE

Complete this form if you wish to:– apply for Standard cover in the Flexible Rollover Product;

or– continue your Triple S cover in the Flexible Rollover

Product.

How to use this form– Complete Sections 1 and 2.– If you are applying to continue your Triple S insurance cover,

complete Section 3.– Complete Section 4.– If you are applying for Death and TPD Insurance, complete

Section 5. – If you are applying for Death Only Insurance, complete Section 6.– Complete Section 7 (unless you are applying to continue your

Triple S insurance).– Complete Section 8.

If you have changed your type of cover or purchased additional units, new conditions may apply to these units of insurance.

2. INVESTOR TYPE I am a standard investor in the Super SA Flexible Rollover Product or I am a spouse investor* in the Super SA Flexible Rollover Product

3. CONTINUATION OF COVER FROM TRIPLE S

(Applicable only to members who roll over from Triple S within 60 days of ceasing SA public sector employment)

I am under the age of 65 and have ceased employment with the SA public sector and am making this application within 60 days of my last day at work, and

I am applying to continue the same units of cover that I held in Triple S, and

I understand that any limitations that applied to my Triple S cover will apply to my cover in the Super SA Flexible Rollover Product.

If you have ticked all three boxes above, please complete Section 4, read, sign and date the Investor Declaration at Section 8 and return this form to Super SA.

*Please note that spouse investors can apply for Death Only Insurance but not Death and TPD Insurance.

Office use only: Previous cover: Standard Fixed Limitations: Yes No Limitations:

New cover: Standard Fixed Limitations: Yes No Limitations:

Date commenced: Age: Cost p/w: New value:

Contact details Website www.supersa.sa.gov.au Email [email protected] Telephone (08) 8207 2094 1300 369 315 (for regional callers) Mail GPO Box 48, Adelaide SA 5001 Visit Ground Floor (enter from Pulteney Street)

151 Pirie Street ADELAIDE SA 5000

Account ID

SUPER SA FLEXIBLE ROLLOVER PRODUCT FRP10

INSURANCE FORM FOR NEW INVESTORS

Please complete all the details on this form in BLOCK LETTERS and return it to Super SA.

Form updated 7 May 2018 Sensitive: Medical (when completed) -I2-A1 Page 1 of 4

Please complete all the details on this form and return the signed original to Super SA.

4. AGE AND WORK DECLARATION I am under age 65 and have been working 20 or more hours per week on a regular basis during the past 12 months (please now complete either section 5 or section 6), or I am under age 65 and have NOT been working 20 or more hours per week on a regular basis during the past 12 months (please now

complete section 6) I have not ceased work due to total and permanent disablement and have not received a TPD entitlement from my former Super SA super

scheme. (If you have received a TPD entitlement, please contact Super SA to discuss your insurance options.)

5. LEVEL OF COVER FOR DEATH AND TPD Notes: – To apply for Death and TPD Insurance you must be a standard member of the Super SA Flexible Rollover Product working 20 or more hours on a

regular basis during the last 12 months and have not received an entitlement for TPD from your former SA public sector fund.– If you are also an active member of Triple S, the combined value of your insurance through both Triple S and the

Super SA Flexible Rollover Product must not exceed $1,500,000.

I require a total number of Standard unit(s) of cover equal to the following number of units.

1 2 3 4 5 6

7 8 9 10 Other (please state )

Please now complete:– Section 7: Personal Statement – Section 8: Investor Declaration

6. LEVEL OF COVER FOR DEATH ONLY Notes: – If you are also an active member of Triple S, the combined value of your insurance through both Triple S and the

Super SA Flexible Rollover Product must not exceed $1,500,000.

I require a total number of Standard unit(s) of cover equal to the following number of units:

1 2 3 4 5 6

7 8 9 10 Other (please state )

Please now complete: Section 7: Personal Statement & Section 8: Investor Declaration

SUPER SA FLEXIBLE ROLLOVER PRODUCT FRP10

INSURANCE FORM FOR NEW INVESTORS

Form updated 7 May 2018 Sensitive: Medical (when completed) -I2-A1 Page 2 of 4

Please complete all the details on this form and return the signed original to Super SA. Note: You must answer all questions.

7. PERSONAL STATEMENTIf you have elected to buy additional units of Standard cover you are required to complete this Personal Statement regarding your health. If you need more space please attach additional pages.

1. Height (in cm): Weight (in kg):

2. Are you, or have you been, a smoker in the last five years? Yes No

3. Do you have an illness/medical condition(s)* or disability? Yes No If NO, please proceed to question 7.

4. What is the exact nature of the existing illness/medical condition(s)*? If more than one condition, please attach additional information.

5. a) When did you first suffer from the above illness/medical condition(s)*?

b) Have you had any recurrence or symptoms arising from the illness/medical condition(s)*? Yes No

c) Is/are the illness/medical condition(s)* getting worse? Yes No

6. a) What was the nature of any treatment?

b) Are you still receiving treatment (including medication) for the illness/medical condition(s)*? Yes No If YES, please give details:

7. Have you ever consulted a doctor about some other illness/medical condition(s)* or disability which is not an existing medical condition? Yes No If YES, you are required to provide the following details: a) What was the exact nature of the illness/medical condition(s)*? If more than one condition, please attach additional information.

b) When did you first suffer from the above illness/medical condition(s)*?

c) Have you had any recurrence or symptoms arising from the illness/medical condition(s)*?

d) What was the nature of the treatment?

*A “medical condition” is any disease, injury, disability, disorder, syndrome, infection, behaviour and atypical variations of structure and function that impact on or affect the physical and/or mental condition, and impairs normal function.

SUPER SA FLEXIBLE ROLLOVER PRODUCT FRP10

INSURANCE FORM FOR NEW INVESTORS

Form updated 7 May 2018 Sensitive: Medical (when completed) -I2-A1 Page 3 of 4

Please complete all the details on this form and return the signed original to Super SA. Note: You must answer all questions.

8. Please provide the name(s) of doctor(s) for your most recent consultation due to all illnesses/medical condition(s)*.

Doctor’s name: Doctor’s name:

Doctor’s address: Doctor’s address:

Postcode: Postcode:

Date of last consultation: Date of last consultation:

Doctor’s name: Doctor’s name:

Doctor’s address: Doctor’s address:

Postcode: Postcode:

Date of last consultation: Date of last consultation:

9. Have you ever had any surgical procedures in relation Yes No to any illness/medical condition(s)* or disability? If YES, please give details:

8. INVESTOR DECLARATION – I have never been approved a TPD entitlement in any Super SA super scheme (eg Triple S, the Lump Sum Scheme, the Pension Scheme,

SA Ambulance Superannuation Scheme). – I understand that I am required to disclose every matter that could reasonably be expected to be known by me, which may be relevant in

Super SA’s decision whether to accept the risk of insuring me.– I understand that an insurance entitlement may be reduced or not payable if the cause of my death or disability is caused wholly or partly by

a pre-existing illness/medical condition(s)* or disability, or an illness/medical condition(s)* or disability arising out of a pre-existing illness/medical condition(s)* or disability, or a prescribed activity.

– I acknowledge, if I am applying for Death and TPD Insurance, that I am a standard investor in the Super SA Flexible Rollover Product under age 65 and have been working at least 20 hours per week for the last 12 months.

– I acknowledge that if I am applying for Death Only cover that I am under age 65.– I understand that non-disclosure will result in my insurance entitlement being withheld or reduced.– I authorise any hospital, doctor or other person who has treated or examined me to provide Super SA with any further information or medical

reports on my illness/medical condition(s)* or injury, medical history, consultations, prescriptions or treatment. A photocopy of this authorisation is as valid as the original.

– I understand that Super SA and its medical adviser(s) will use this information for the purpose of considering my application for insurance.

Signature Date / /

*A “medical condition” is any disease, injury, disability, disorder, syndrome, infection, behaviour and atypical variations of structure and function that impact on or affect the physical and/or mental condition, and impairs normal function.

SUPER SA FLEXIBLE ROLLOVER PRODUCT FRP10

INSURANCE FORM FOR NEW INVESTORS

Form updated 7 May 2018 Sensitive: Medical (when completed) -I2-A1 Page 4 of 4