florida's ocean and coastal economies report phase 2

TRANSCRIPT

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 1/219

Phase IIFlorida’s Ocean and Coastal

Economies ReportJudith Kildow, Principal InvestigatorMonterey Bay Aquarium Research Institute

June 2008

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 2/219

Acknowledgments The National Ocean Economics Program research team prepared this report incollaboration with the following people named below along with their contributions tothis work. Judith Kildow was Principal Investigator and led the team. Charles Colgan,

University of Maine, provided oversight for the Ocean Economy sectors: Real Estate,Cruise Industry, Fishing Industry and Transportation. Linwood Pendleton, Fellow at theOcean Foundation, provided oversight for the Coastal Recreation chapters. Othermembers of the NOEP research team who contributed to many of the chapters andpreparation of the report included Bonnie Lockwood, Pat Johnston, Scott Norris, KirstinCsik, Nick Rome, Elizabeth Rogers, Bethany Taylor, and Nat Miller.

Research teams at Florida Atlantic University were led by Principal Investigator LenoreAlpert from the Center for Urban and Environmental Solutions at Florida AtlanticUniversity; William B. Stronge, Professor Emeritus and Senior Fellow; M.J. Matthews,Senior Research Associate; and Angela Grooms, Research Associate; who were

responsible for the following chapters: 1) The Cruise Industry, 2) Real Estate, 3) TouristReal Estate, and 4) Coastal Recreation. Other research assistants who contributed to thesechapters were Lauren Schild, Marc Miller, Ian Singer, and Jose Mena.

The research team at the University of Florida, Gainesville, responsible for information inthe Fisheries Industry chapter included Charles Adams, Principal Investigator andChristopher de Bodisco, post-doctoral assistant.

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 3/219

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 4/219

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 5/219

Florida’s Ocean and Coastal Economies

Phase II

Table of Contents

Part I — Introduction and Background...........................................................................................................1

Chapter 1 Context for the Study..........................................................................................................1

Chapter 2 Glossary of Terms and Definitions....................................................................................3

Part II — Executive Summary and Update.....................................................................................................7

Chapter 3 Executive Summary ............................................................................................................7

Chapter 4 Updates from Phase I Report .............................................................................................9 4.1 Florida Coastal Economy 2006.......... ........... ........... .......... ........... ........... .......... ........... ........ 10 4.2 Coastal Economy Growth 2003-2006.......... ........... .......... ........... ........... .......... ........... ......... 11 4.3 Economic Growth at the County Level 2003-2006...............................................................11 4.4 Population and Housing ........................................................................................................16 4.5 Conclusion ............................................................................................................................23

Part III — Ocean Economy: Sector Supplements.........................................................................................25

Chapter 5 Fishing Industry ...............................................................................................................26 5.1 Fishing Industry Overview....................................................................................................26 Commercial Fisheries..........................................................................................................................27 5.3 Recreational Fisheries ...........................................................................................................35 5.4 Imports and Exports ..............................................................................................................39 5.5 Seafood Processors and Wholesalers ........... .......... ........... .......... ........... .......... ........... .......... 42 5.6 Commercial and Pleasure Water Vessel Registrations .......... ........... ........... ........... ........... ...44 5.7 Conclusion ............................................................................................................................45

Chapter 6 Marine Transportation including Ports ...........................................................................46 6.1 Introduction..........................................................................................................................46 6.2 National and State Comparisons..........................................................................................47 6.3 Conclusion ...........................................................................................................................56

Chapter 7 Marine Construction – Beach Nourishment.....................................................................58 7.1 Dredging Operations.............................................................................................................58 7.2 Beach Nourishment...............................................................................................................60 7.3 Conclusion ............................................................................................................................70

Chapter 8 Coastal Tourism and Recreation – The Cruise Industry ..................................................72 8.1 Introduction to Florida’s Cruise Industry..............................................................................72 8.2 Overview of Florida’s Cruise Economy.......... .......... ........... ........... .......... ........... .......... .......72

8.3 National Comparisons of the Cruise Tourism Industry................... ........... .......... ........... ......74 8.4 State Economic Impacts of the Cruise Industry ......... ........... .......... ........... .......... ........... ......75 8.5 Analysis of Individual Florida Cruise Ports ........... ........... .......... ........... ........... .......... .......... 78 8.6 Conclusion ............................................................................................................................81

Chapter 9 Coastal Real Estate ..........................................................................................................82 9.1 Coastal Real Estate Values....................................................................................................82 9.2 Tourist-Oriented Coastal Property in Florida......................................................................116 9.3 Seasonal Housing................................................................................................................127

i

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 6/219

9.4 Conclusion ..........................................................................................................................136

Chapter 10 Marine Research and Education....................................................................................137 10.1 Introduction.........................................................................................................................137 10.2 Marine Institutions Survey Results ........... .......... ........... ........... ........... ........... .......... .......... 137 Conclusion.........................................................................................................................................143

Part IV Coastal Recreation Activities and Assets ........... .......... ........... ........... ........... ........... ......144 Chapter 11 Introduction and Overview............................................................................................144

11.1 Non-Market Values.............................................................................................................144 11.2 Organization of this Report............ .......... ........... ........... ........... ........... .......... ........... .......... 145 11.3 Impacts of the 2004 and 2005 Hurricane Seasons in Florida.......... ........... ........... ........... ...148 11.4 Coastal Recreation in Florida............... ........... .......... ........... ........... ........... .......... ........... ....149

Chapter 12 Park Visitation and Attendance.....................................................................................156 12.1 Introduction.........................................................................................................................156 12.2 Florida’s State Parks ...........................................................................................................158 12.3 State and National Park Attendance................ ........... ........... .......... ........... ........... .......... ....161 12.4 Recreational Reef Use.........................................................................................................164 12.5 Data Gaps in Coastal Park Visitation............. .......... ........... ........... .......... ........... ........... .....166

Chapter 13 Recreational Boating in Florida................................................................................168 13.1 Introduction.........................................................................................................................168 13.2 Boating within Florida’s Park System .......... ........... ........... .......... ........... ........... .......... ......169 13.3 Boating Activity..................................................................................................................170 13.4 Boating and Recreational Reef Use ....................................................................................172 13.5 Data Gaps............................................................................................................................173

Chapter 14 Recreational Fishing in Florida.....................................................................................174 14.1 Introduction.........................................................................................................................174 14.2 Fishing and Recreational Reef Use by Anglers.......... ........... ........... .......... ........... ........... ...177 14.3 Data Gaps............................................................................................................................178

Chapter 15 Scuba Diving and Snorkeling in Florida........................................................................179 15.1 Introduction.........................................................................................................................179

15.2 Recreational Reef Use............... .......... ........... .......... ........... .......... ........... .......... ........... ......179 15.3 Data Gaps............................................................................................................................181

Chapter 16 Beach Activities in Florida.............................................................................................182 16.1 Introduction.........................................................................................................................182 16.2 Beach Regions.....................................................................................................................182 16.3 Beach Attendance ...............................................................................................................184 16.4 State Beach Parks................................................................................................................186 16.5 Selected Studies of Florida Beaches ...................................................................................187 16.6 Surfing in Florida ................................................................................................................189 16.7 Data Gaps............................................................................................................................191

Chapter 17 Conclusion......................................................................................................................192

Part V References......................................................................................................................193

ii

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 7/219

List of Tables

Sectors and Industries of the Ocean Economy................. ........... .......... ........... ........... ........... .......... ........... .......... ........ 4

Table 4.1 Florida’s Ocean Economy, 2005................ ........... .......... ........... ........... .......... ........... ........... ........... ........... .. 9

Table 4.2 Florida’s Coastal Economy, 2006 (shoreline counties only) ........... .......... ........... ........... ........... .......... ........ 9

Table 4.3 Florida Economy Total Regional Values and Contribution to State Economy, 2006......... ............ ........... . 10 Table 4.4 Florida Regional Coastal Economy 2003-2006 .......... .......... ........... ........... .......... ........... ........... .......... ...... 11

Table 4.5 Top Five Counties by Percent Change................ ........... .......... ........... ........... ........... ........... .......... .......... ... 12

Table 4.6 Top Five Counties by Real Change ............................................................................................................ 12

Table 4.7 Bottom Five Counties by Percent Change .................................................................................................. 13

Table 4.8 Bottom Five Counties by Real Change.......... ........... ........... ........... .......... ........... ........... ............ .......... ...... 14

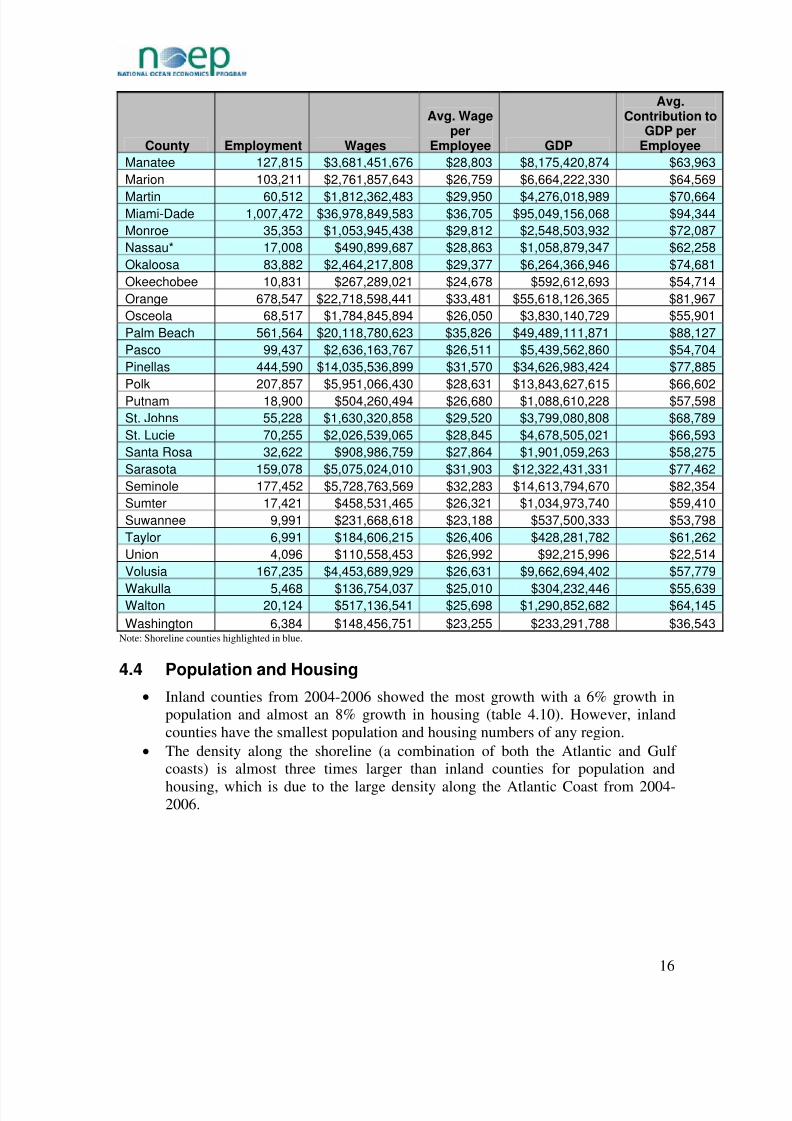

Table 4.9 Florida County Comparisons of Economic Indicators, 2006 .......... ........... ........... ........... .......... ........... ...... 15

Table 4.10 Florida’s Regional Population and Housing 2004-2006 ........... ........... ........... .......... ........... ........... ......... 17

Table 4.11 Distribution of Florida’s Population, 2006 ..............................................................................................17

Table 4.12 Distribution of Florida’s Housing, 2006 .......... ........... ........... ........... ........... .......... ........... .......... ........... .. 17

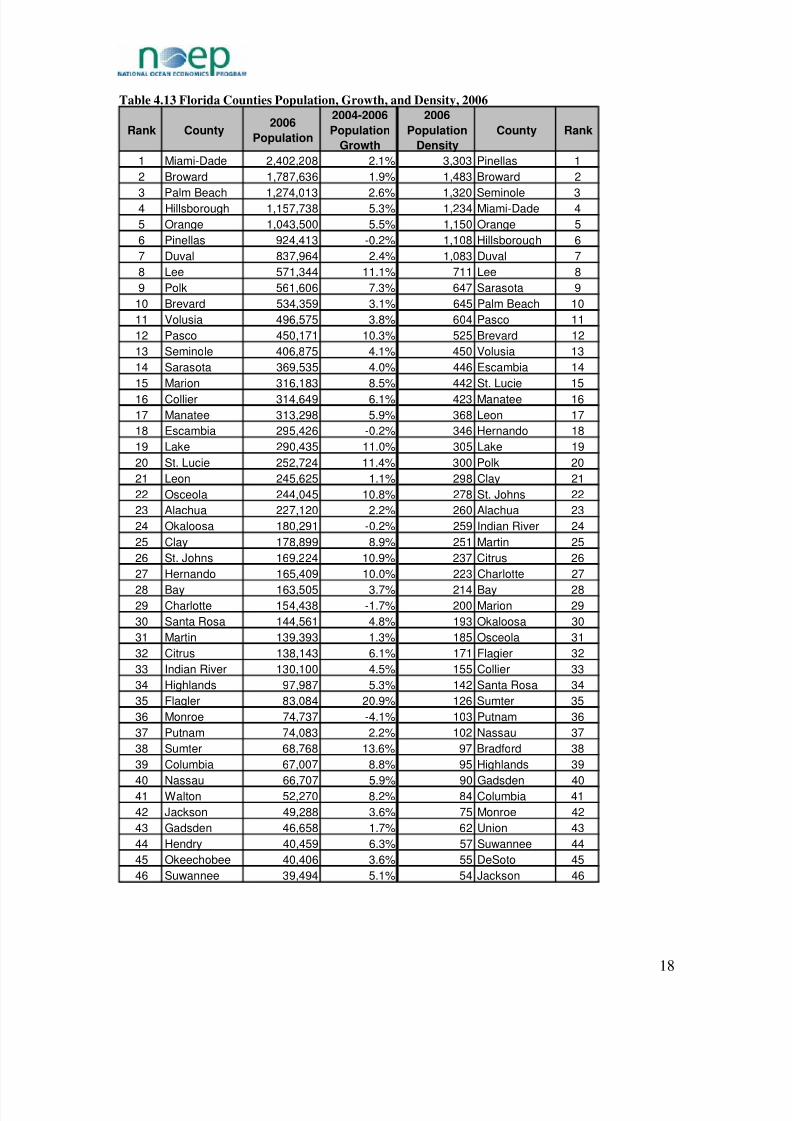

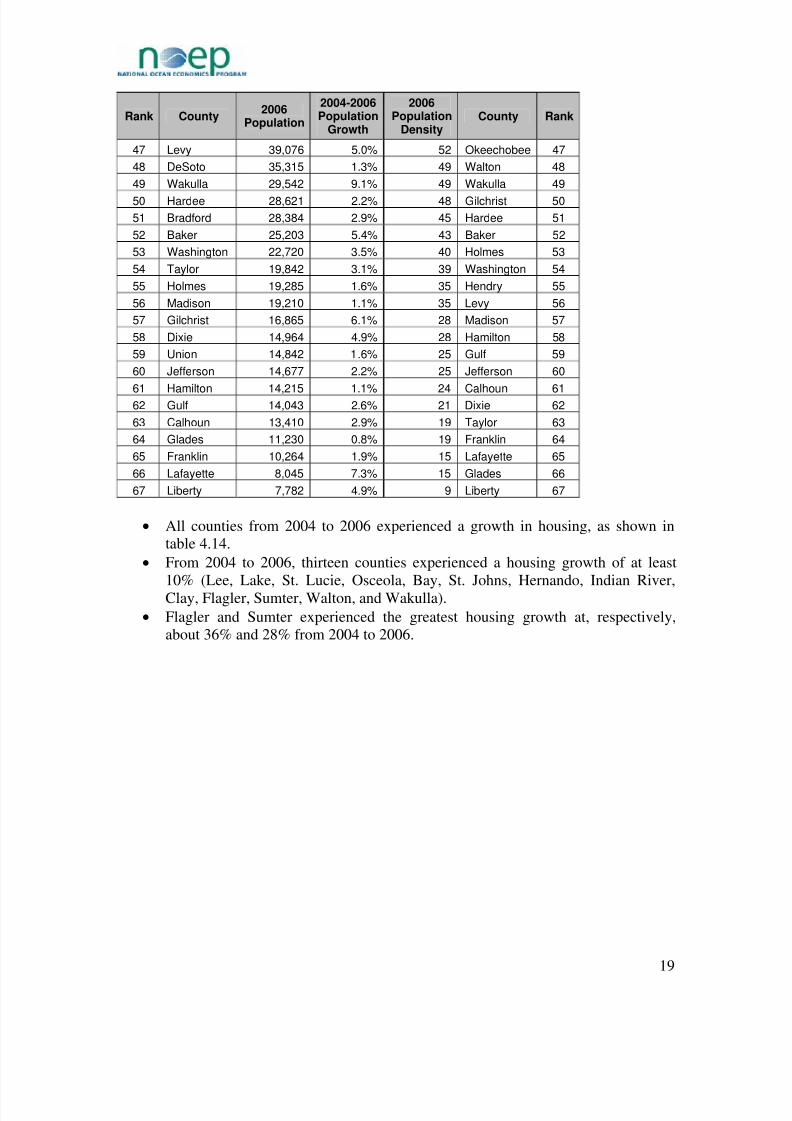

Table 4.13 Florida Counties Population, Growth, and Density, 2006 .......... ........... .......... ........... ........... .......... ......... 18

Table 4.14 Florida Counties Housing, Growth, and Density, 2006 ........... ........... ........... ........... ........... ........... ......... 20

Table 4.15 Coastal States Coastal Population and Density, 2006.......... ........... ........... ........... ........... .......... .......... .... 22

Table 4.16 Coastal States Coastal Housing and Density, 2006......... ........... .......... ........... ........... .......... ............ ......... 23

Table 5.1 Commercial Seafood Harvests, 1990, 1994, 2007 ........... ........... .......... ........... ........... ........... .......... .......... . 28

Table 5.2 Commercial Seafood Groups, 2007........................................................................................................... 29

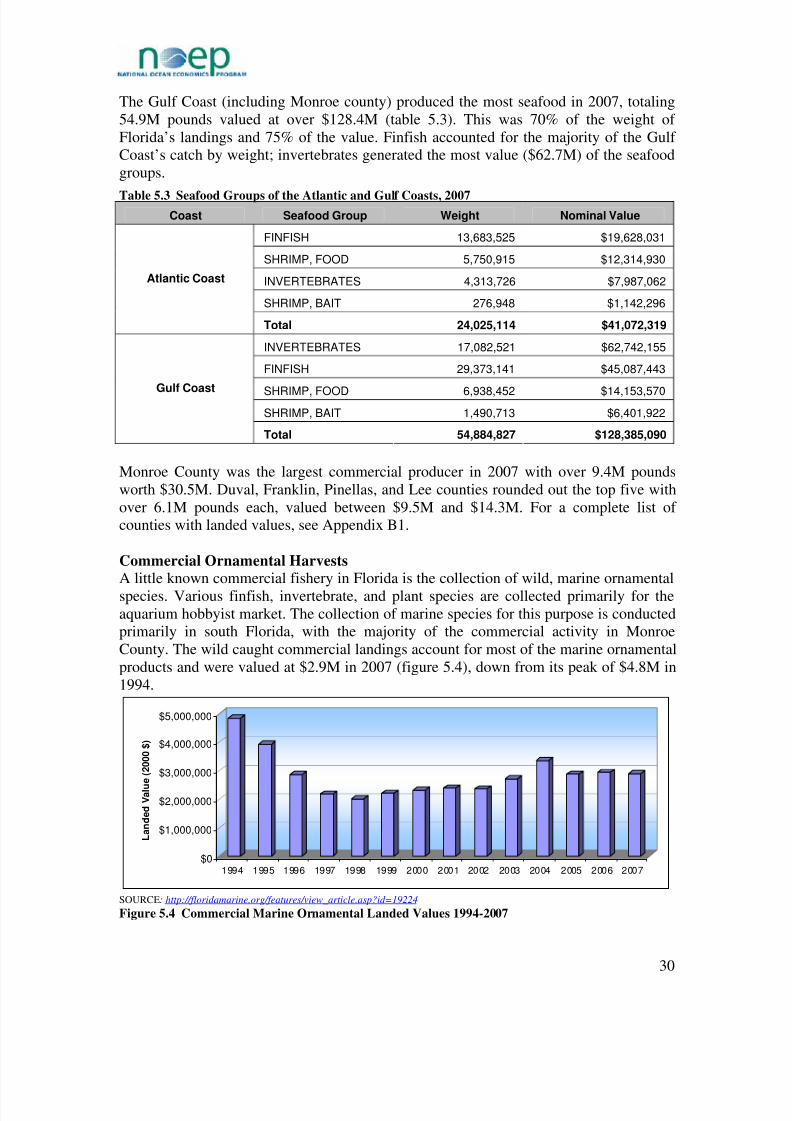

Table 5.3 Seafood Groups of the Atlantic and Gulf Coasts, 2007 ........... .......... ........... ........... ........... .......... ........... .. 30

Table 5.4 Recreational License Sales 2004-2007 ...................................................................................................... 38

Table 5.5 Recreational Marine Fishing Values, 2006.......... ........... .......... ........... ........... .......... ........... ........... .......... . 39

Table 6.1 U.S. Port Container Volumes, 1997, 2006, and 2007 ........... ........... ........... .......... ........... ........... .......... ...... 47

Table 6.2 Gulf vs. Atlantic, Trade Values ................................................................................................................. 48

Table 6.3 Gulf vs. Atlantic, Trade Volume.................. ........... ........... ........... ........... .......... ........... ........... .......... ........ 49

Table 6.4 Associated Counties of the Individual Florida Ports........ ........... ........... ........... ........... ........... ........... ......... 49

Table 6.5 Total Value and Containerized Cargo Value .............................................................................................. 50

Table 6.6 Dollar Value of Florida’s Exports and Imports by Port, 2007.......... ........... ........... .......... ........... ........... .... 50

Table 6.7 Florida’s Total Waterborne Trade, Tons.................. .......... ........... ........... .......... ........... ........... .......... ........ 52

Table 6.8 Cargo Types Carried at Florida’s Seaports FY 2007 .......... .......... ........... ........... ........... .......... .......... ........ 53

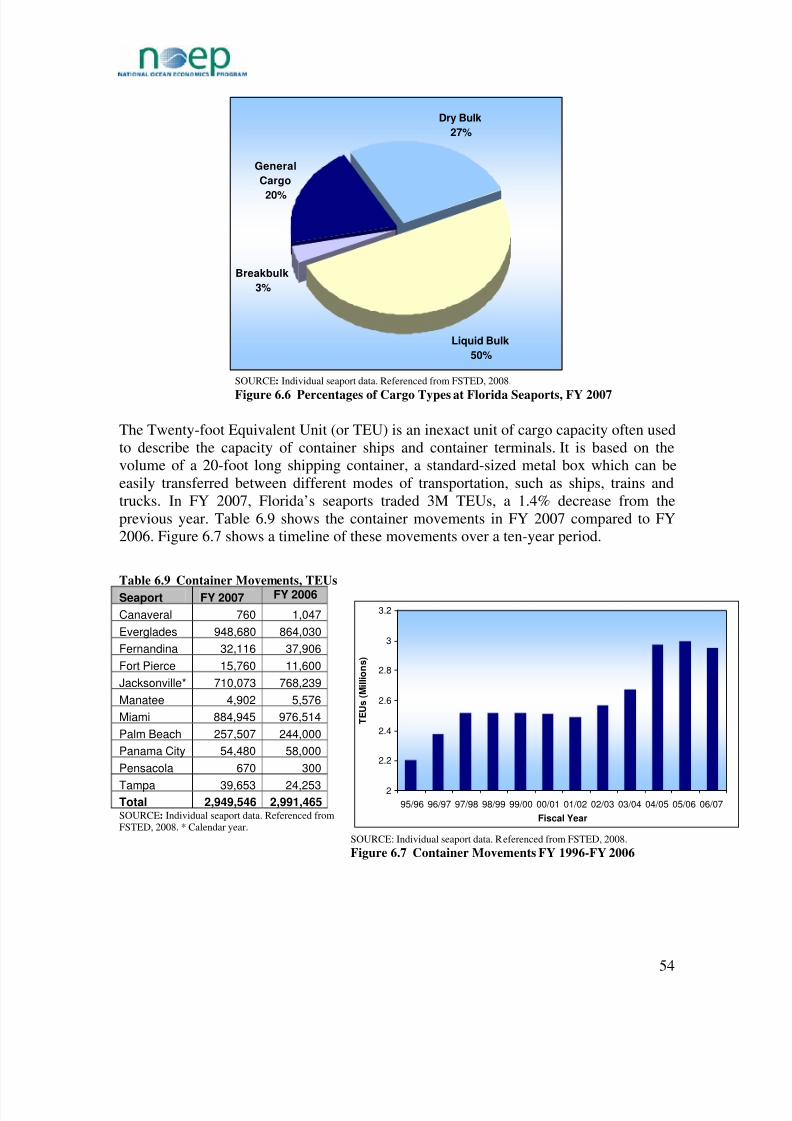

Table 6.9 Container Movements, TEUs..................................................................................................................... 54

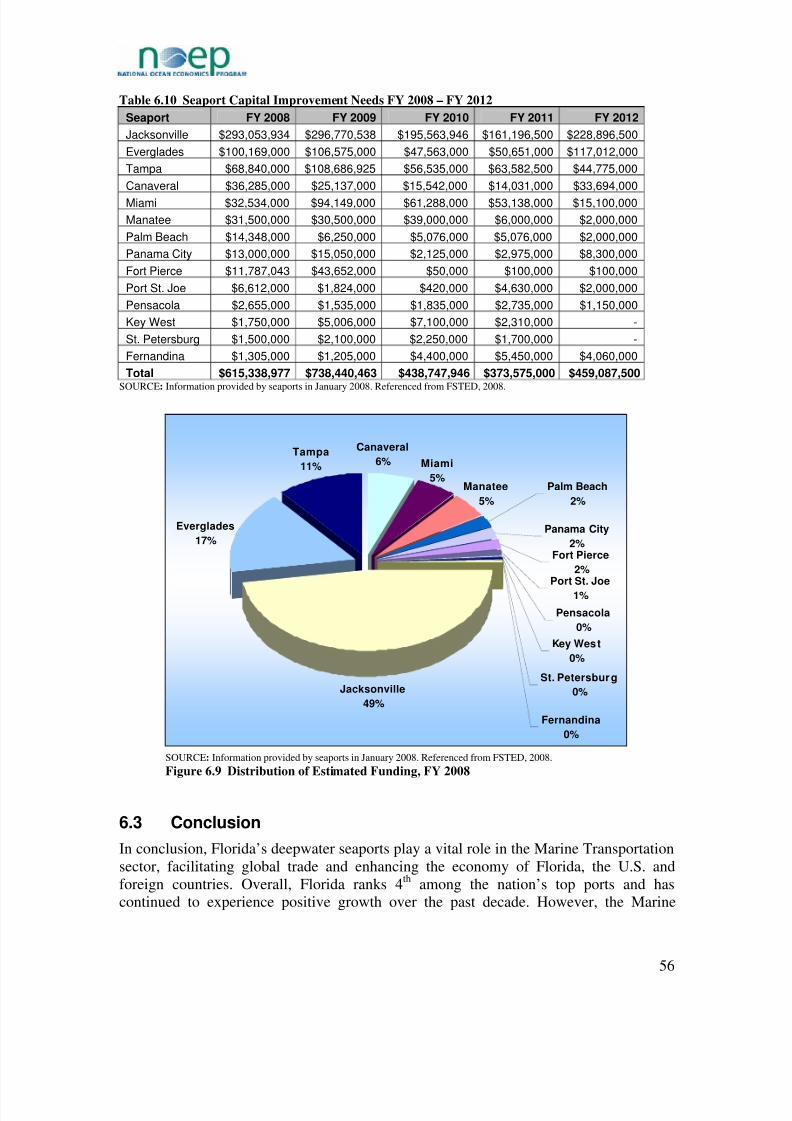

Table 6.10 Seaport Capital Improvement Needs FY 2008 – FY 2012 .......... ........... ........... ........... ........... .......... ...... 56 Table 7.1 Time Series of Contracted Dredging by the USACE in Florida 1990-2005........... ........... .......... ........... ... 59

Table 7.2 Volume of Beach Nourishment Projects by County 1944-2006........... ........... ........... ........... .......... .......... 63

Table 7.3 Funding Sources for Total Volume and Cost of Beach Nourishment 1960-2005................... ........... ........ 65

Table 7.4 Breakdown of Federal Funding Type for Total Volume 1960-2005 .......... ........... ........... ........... ........... ... 66

Table 7.5 Department of Environmental Protection Regional Erosion, 2003............. .......... ........... ........... ........... ..... 66

iii

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 8/219

Table 7.6 Counties in Department of Environmental Protection Regions for Reference ........... .......... ........... .......... 67

Table 8.1 Florida Ocean Tourism & Recreation Industries - Excluding Cruise Line, 2004........... .......... ........... ...... 72

Table 8.2 Embarkations by Port 2004-2006 ..............................................................................................................74

Table 8.3 Florida's Share of U.S. Cruise Industry, 2006................. ........... ........... ........... .......... ........... .......... .......... . 75

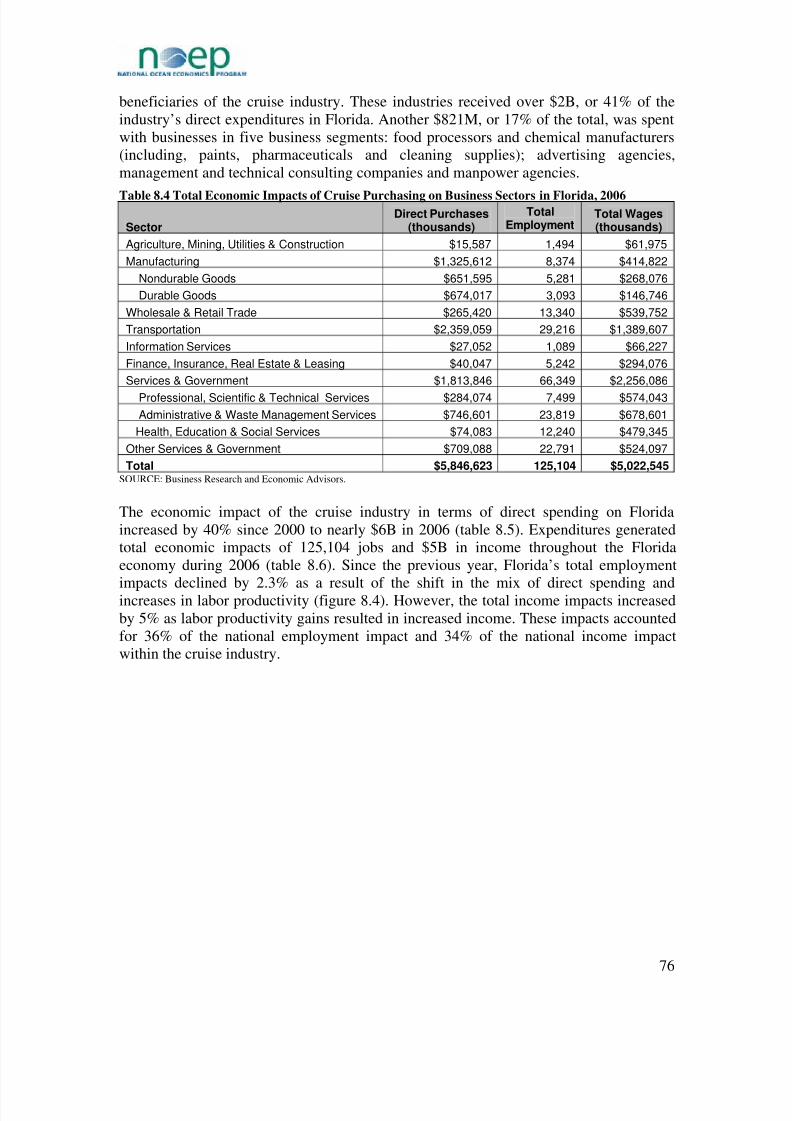

Table 8.4 Total Economic Impacts of Cruise Purchasing on Business Sectors in Florida, 2006................. ........... .... 76

Table 8.5 Economic Impact of Cruise Industry on Direct Spending in Florida 2000-2006............... ........... ............ 77

Table 8.6 Economic Impact of Cruise Industry on Florida Spending 2000-2006................ ........... ........... .......... ..... 77

Table 8.7 Cruise Operations, Embarkations and Disembarkations FY 2005 – FY 2007............. ........... ........... ......... 80

Table 9.1 Seasonal Homes by State, 1990 and 2006 ............................................................................................... 128

Table 9.2 Percentage of Seasonal Homes, 1990 and 2006.................. .......... ........... .......... ........... ........... ........... ..... 129

Table 10.1 Florida Marine Economic Indicators ..................................................................................................... 138

Table 10.2 Major Marine and Coastal Research and Education Institutions in Florida, 2007................... ........... ... 140

Table 12.1 National Estuarine Research Reserves Attendance 2002 - 2007................ ........... .......... ........... ........... .. 163

Table 15.1 Expenditures for Scuba Diving and Snorkeling in Florida ......... ........... ........... .......... ........... ............ ..... 180

iv

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 9/219

List of Figures

Figure 5.1 Commercial Seafood Harvests 1990-2007 ................................................................................................28

Figure 5.2 Commercial Seafood Landings by Coast 1990-2007 .......... .......... ........... ........... ........... ........... ......... ...... 29

Figure 5.3 Commercial Seafood Groups 1990-2007 ................................................................................................. 29

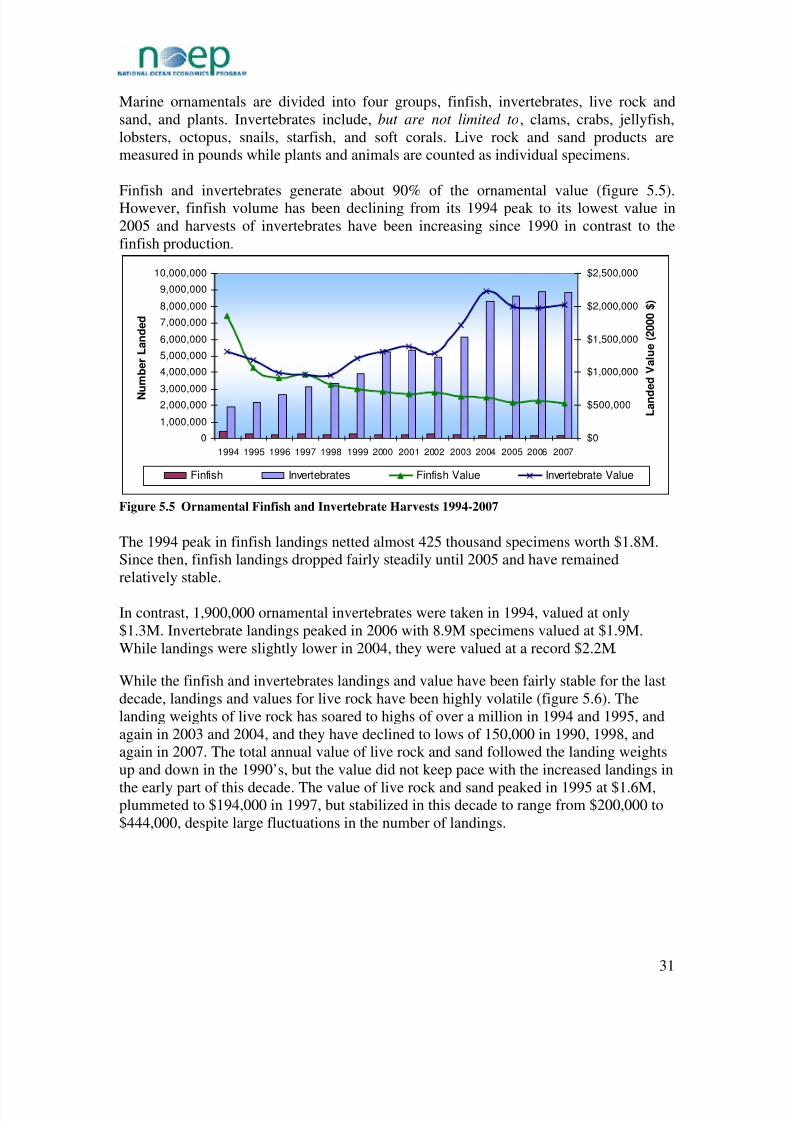

Figure 5.4 Commercial Marine Ornamental Landed Values 1994-2007 .......... ........... ........... ........... ........... ........... .. 30 Figure 5.5 Ornamental Finfish and Invertebrate Harvests 1994-2007........... ........... ........... ........... ........... .......... ...... 31

Figure 5.6 Marine Ornamental Live Rock and Sand 1994-2007 ........... ........... ........... .......... ........... ........... .......... .... 32

Figure 5.7 Commercial Marine Fishing Licenses FY 1994-95 to FY2006-07 ........... ........... ........... .......... ........... .... 33

Figure 5.8 Commercial Fishing License Types FY 1994-95 to 2006-07............ ........... ........... ........... ........... .......... . 33

Figure 5.9 Aquaculture Operations, Workers, and Sales 1987-2005.......... ........... ........... ........... .......... ........... ......... 34

Figure 5.10 Aquaculture Product Sales 1987-2005 ................................................................................................... 35

Figure 5.11 Recreational Fish Landings 1990-2006 .................................................................................................. 36

Figure 5.12 Top Ten Recreation Fish 1990-2006 ....................................................................................................... 37

Figure 5.13 Saltwater Fishing Licenses Sold 2004-2007................ ........... .......... ........... ........... .......... ........... .......... . 37 Figure 5.14 Individual Recreational Fishing Licenses, Resident and Non-Resident 2004-2007 ............ ........... ........ 38

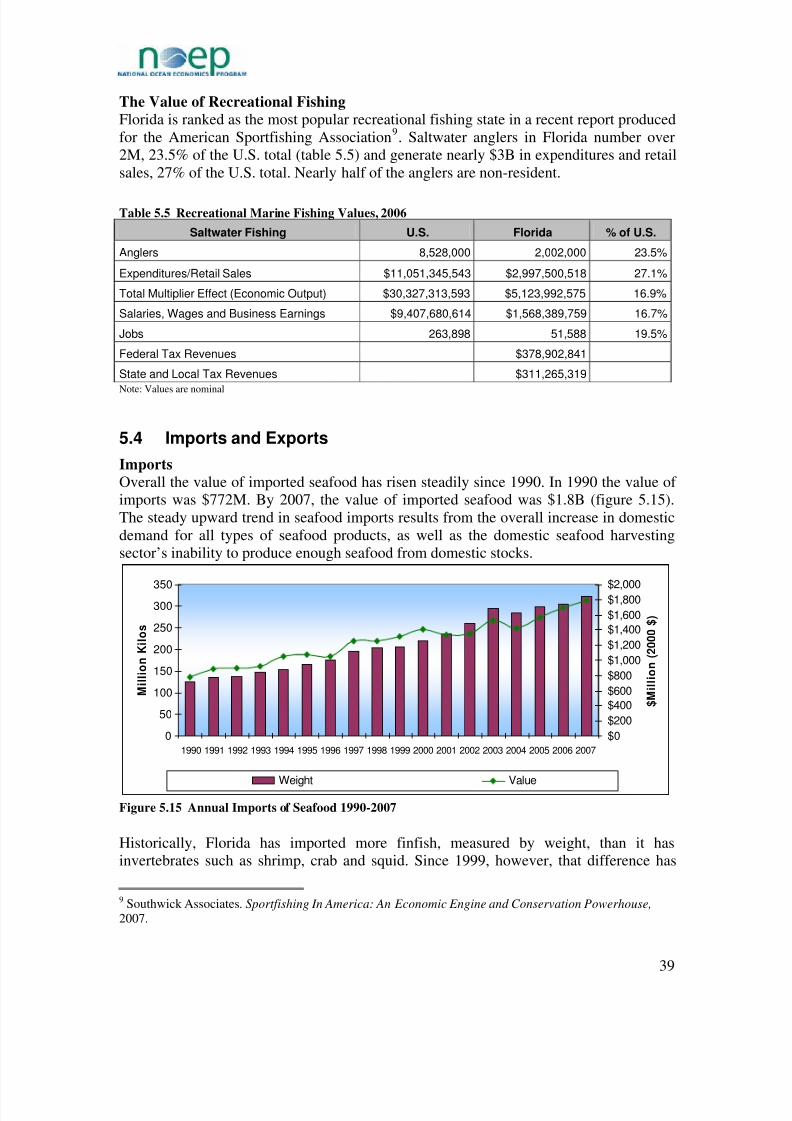

Figure 5.15 Annual Imports of Seafood 1990-2007 .................................................................................................. 39

Figure 5.16 Imports of Finfish and Shellfish 1990-2007 .......... ........... .......... ........... ........... ........... ........... .......... ...... 40

Figure 5.17 Seafood Exports 1990-2007 ................................................................................................................... 40

Figure 5.18 Exports of Finfish and Invertebrates 1990-2007 .......... ........... ........... .......... ........... ........... .......... .......... 41

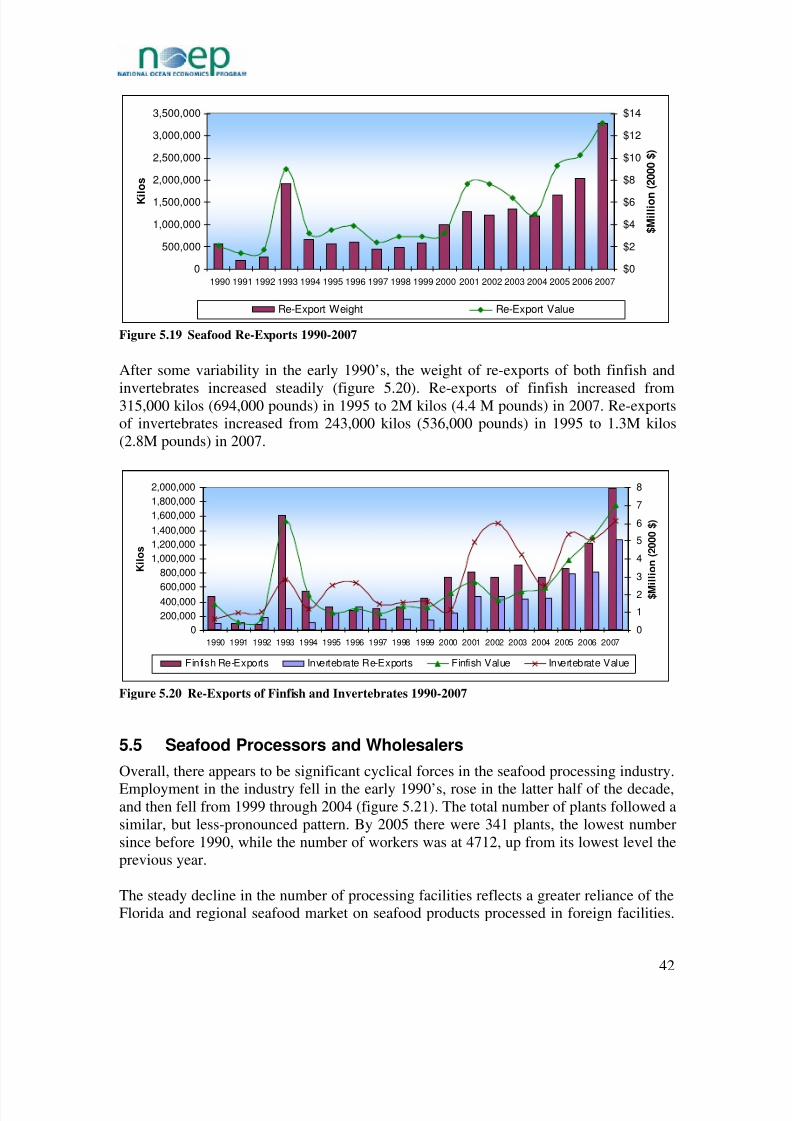

Figure 5.19 Seafood Re-Exports 1990-2007.................. ........... .......... ........... ........... ........... ........... ......... .......... ........ 42

Figure 5.20 Re-Exports of Finfish and Invertebrates 1990-2007................ ........... ........... ........... ........... .......... ......... 42

Figure 5.21 Seafood Processing and Wholesale Plants 1990-2005 ........... ........... ........... ........... ........... ........... ......... 43

Figure 5.22 Seafood Processing and Wholesale Plants 1990-2007 ........... ........... ........... ........... ........... ........... ......... 43

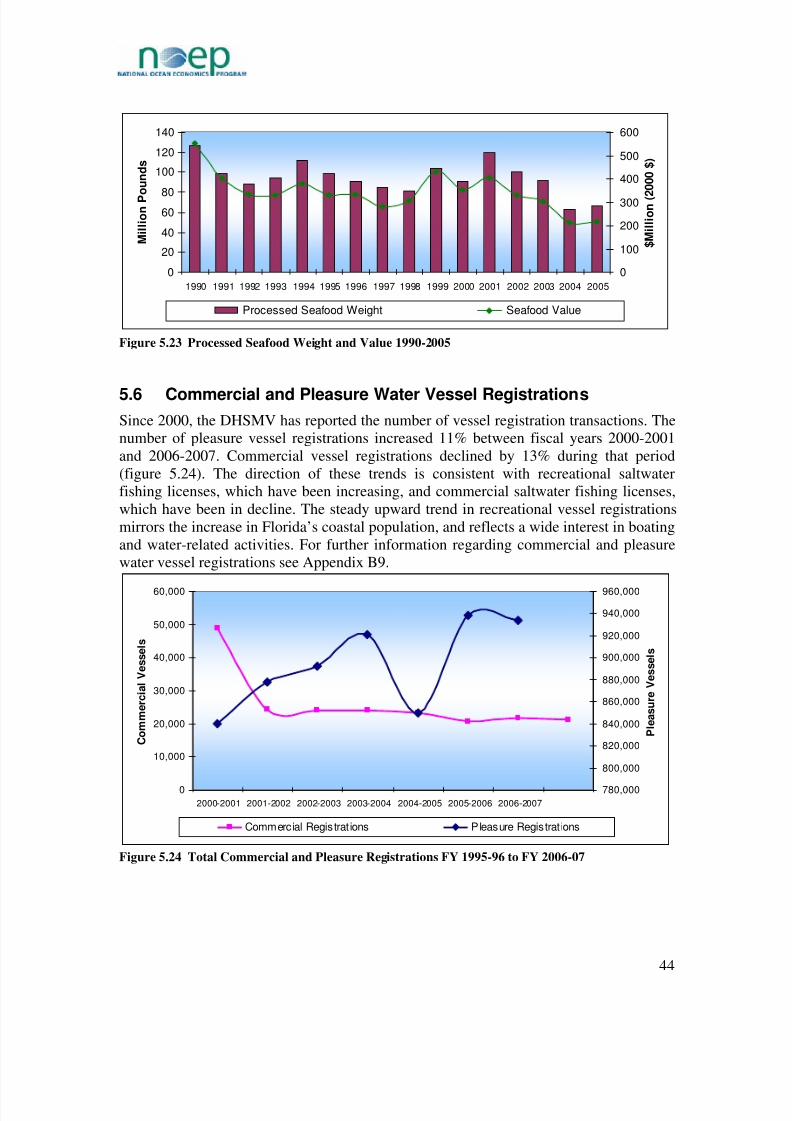

Figure 5.23 Processed Seafood Weight and Value 1990-2005 ........... .......... ........... ........... .......... ........... ........... ....... 44

Figure 5.24 Total Commercial and Pleasure Registrations FY 1995-96 to FY 2006-07........... .......... ........... .......... . 44

Figure 5.25 Commercial Fish Landings vs. Seafood Imports.............. .......... ........... ........... ........... .......... ........... ...... 45

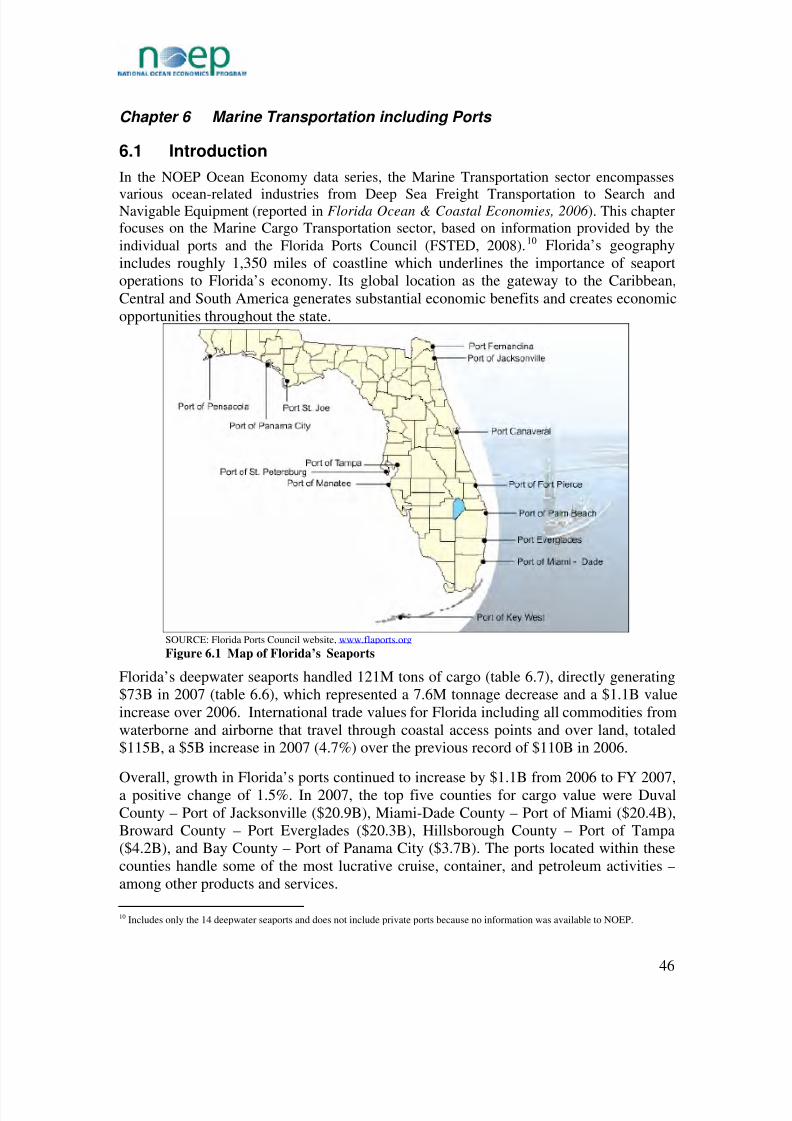

Figure 6.1 Map of Florida’s Seaports ....................................................................................................................... 46

Figure 6.2 Percentage Changes of Cargo Values and Volume 2005-2007 .......... ........... ........... ........... ........... ......... . 49

Figure 6.3 Distribution of Florida Seaports based on Total Value, FY 2006........... ........... .......... ........... .......... ........ 51

Figure 6.4 Distribution of Florida’s Seaports by Tons, FY 2007......... ........... ........... ........... .......... ........... .......... ...... 52

Figure 6.5 Florida Ports Import vs. Export Tonnage, FY 2007 .......... ........... .......... ........... ........... .......... .......... ........ 53

Figure 6.6 Percentages of Cargo Types at Florida Seaports, FY 2007 ........... .......... ........... ........... ........... .......... ...... 54

Figure 6.7 Container Movements FY 1996-FY 2006 ................................................................................................54

Figure 6.8 Distribution of Florida Seaports based on Container Movements, 2007 ........... .......... ........... ........... ....... 55

Figure 6.9 Distribution of Estimated Funding, FY 2008 ........................................................................................... 56

Figure 7.1 Time Series of Contracted Dredging by the USACE in Florida 1990-2005............... ........... ........... ........ 60

Figure 7.2 Top Ten Beach Nourishment States in the U.S. by Cost 1960-2007........... ........... ........... ........... .......... .. 61

v

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 10/219

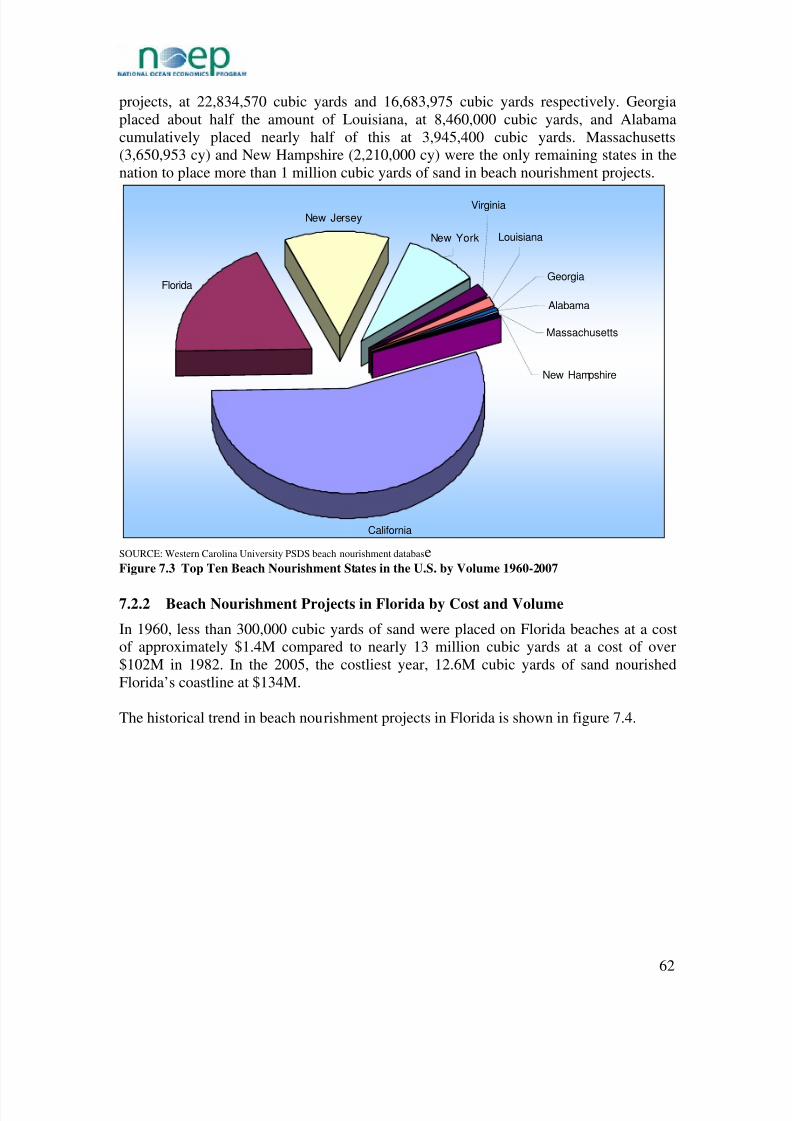

Figure 7.3 Top Ten Beach Nourishment States in the U.S. by Volume 1960-2007 .......... ........... ........... ........... ....... 62

Figure 7.4 Cost and Volume of Beach Nourishment Projects in Florida 1960-2005................ ........... ........... ........... . 63

Figure 7.5 Funding Sources for Total Volume and Cost of Beach Nourishment 1960-2005 ........... ........... ........... .. 65

Figure 7.6 Main Sources of Funding for Beach Nourishment 1992-2002.......... ........... ........... ........... .......... ........... . 67

Figure 7.7 Regional Funding for Beach Nourishment Projects 1992-2002 .......... ........... ........... ........... .......... .......... 68

Figure 7.8 Map of Critical Erosion Areas in Florida .................................................................................................. 69

Figure 7.9 Map of the Florida State Coastal Construction Control Line .......... ........... .......... ........... ........... .......... .... 70

Figure 8.1 Map of Florida’s Cruise Ports........... ........... ........... .......... ........... ........... .......... ............ .......... .......... ........ 73

Figure 8.2 Embarkations by Port 2004-2006..............................................................................................................74

Figure 8.3 Florida's Percentage Share of U.S. Cruise Industry, 2006.......... ........... ........... ........... ........... .......... ......... 75

Figure 8.4 Employment, Income, and Direct Spending: Florida Cruise Industry 2000-2006.......... ........... ........... ..... 77

Figure 8.5 Total Global Embarkations 1990-2006.......... ........... ........... ........... ........... .......... ........... ........... .......... ...... 78

Figure 8.6 Percent of Global Cruise Embarkations, 2006.................. ........... ........... .......... ........... ........... .......... ........ 78

Figure 8.7 Total Embarkations from Florida Ports 1990-2006 ........... ........... .......... ........... ........... ........... .......... ....... 79

Figure 8.8 Percentage Share of Florida Cruise Embarkations by Port 1990-2006........... ........... .......... ........... .......... 79

Figure 8.9 Percentage Growth in Cruising at Florida Ports 2001-2006.......... .......... ........... ........... ........... .......... ...... 80

Figure 8.10 Embarkations and Disembarkations from Florida Ports by Length of Cruise.......... ........... ........... ......... 81

Figure 9.1 Number of Florida Coastal Properties by Land Use.......... .......... ........... ........... .......... ........... .......... ........ 84

Figure 9.2 Value of Florida Coastal Properties by Land Use .................................................................................... 84

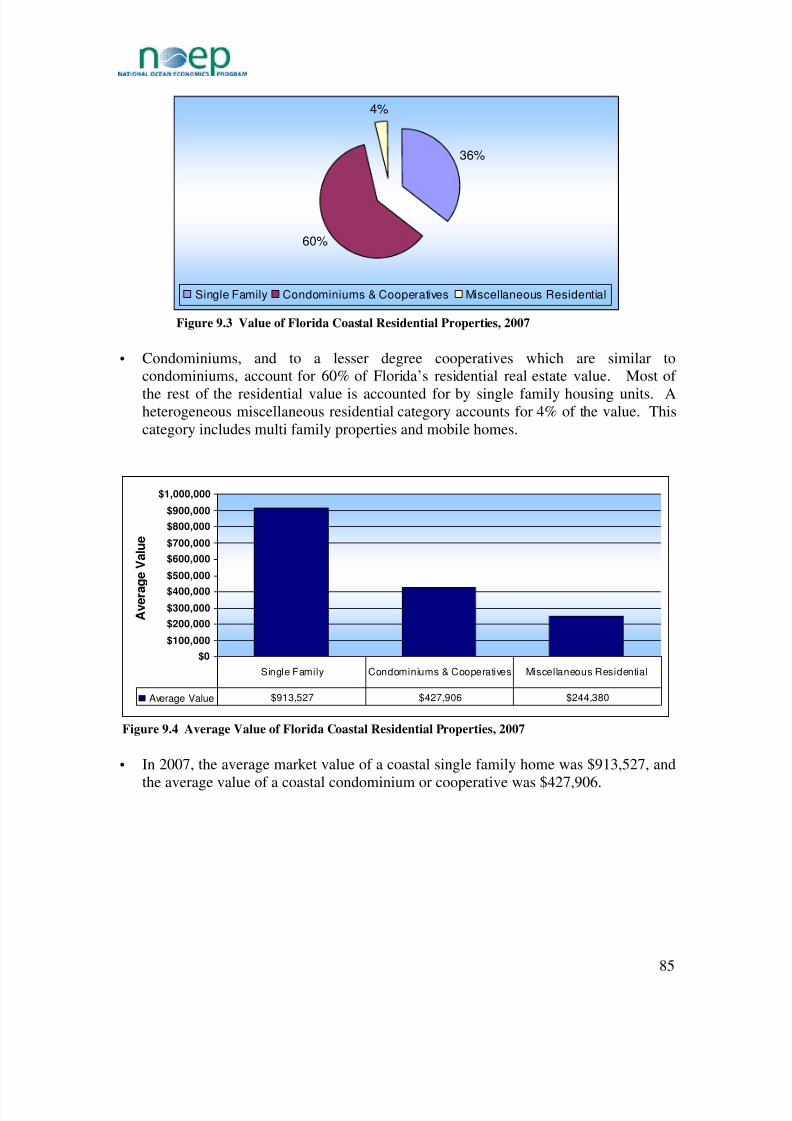

Figure 9.3 Value of Florida Coastal Residential Properties, 2007 ........... ........... ........... ........... .......... .......... ........... .. 85

Figure 9.4 Average Value of Florida Coastal Residential Properties, 2007........... .......... ........... ........... ........... ......... 85

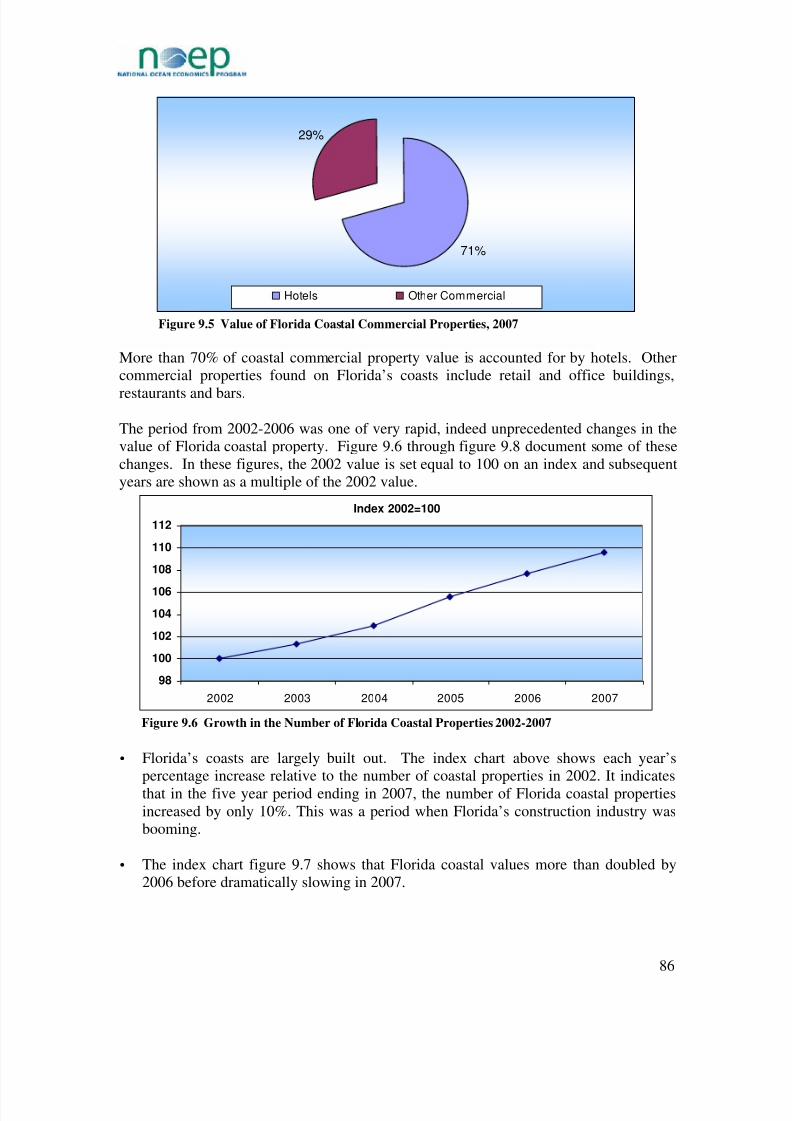

Figure 9.5 Value of Florida Coastal Commercial Properties, 2007 ........... ........... ........... .......... ........... .......... .......... . 86

Figure 9.6 Growth in the Number of Florida Coastal Properties 2002-2007.......... ........... ........... ........... ........... ....... 86

Figure 9.7 Growth in the Value of Florida Coastal Properties 2002-2007............ ........... ........... ........... .......... .......... 87 Figure 9.8 Growth in the Average Value of Florida Coastal Properties 2002-2007 ........... ........... ........... ........... ...... 87

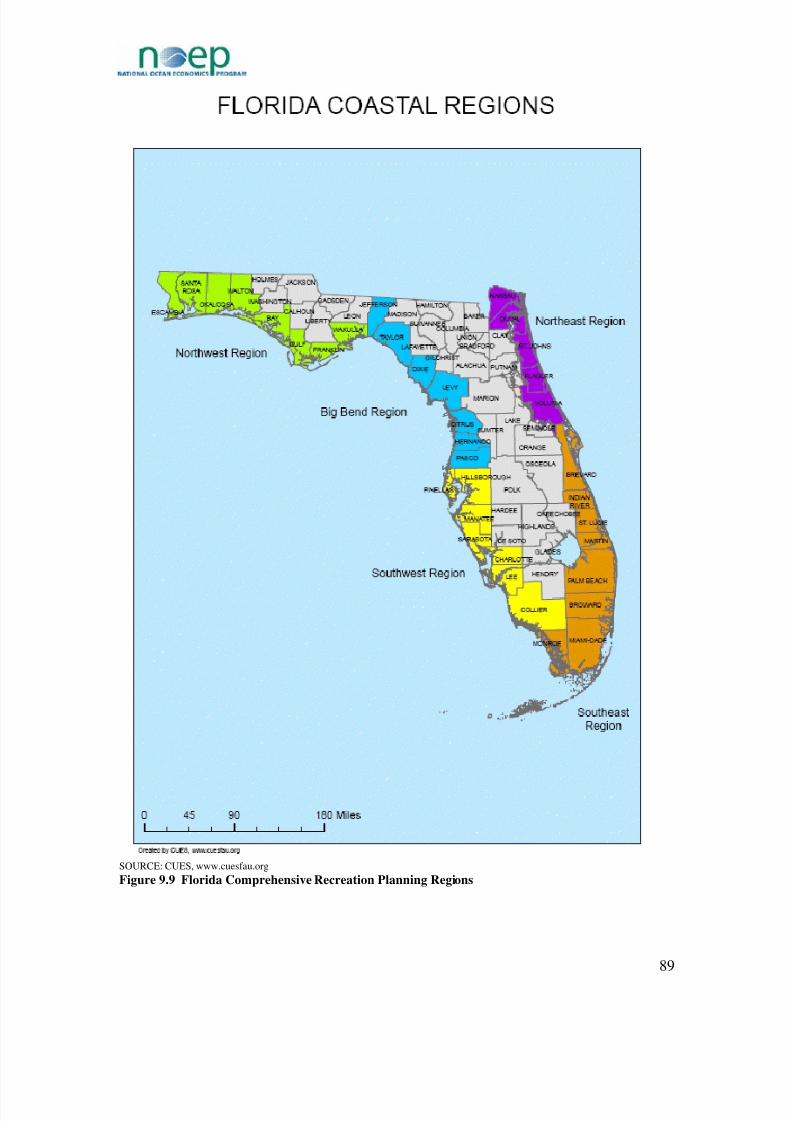

Figure 9.9 Florida Comprehensive Recreation Planning Regions ........... .......... ........... .......... ........... ........... ........... .. 89

Figure 9.10 Distribution of the Number of Coastal Properties by Coastal Region, 2007........... ........... ........... ......... 90

Figure 9.11 Distribution of Coastal Property Values by Coastal Region, 2007............. .......... ........... ........... .......... .. 90

Figure 9.12 Distribution of Average Coastal Property Values by Coastal Region, 2007 ........... ........... ........... ......... 91

Figure 9.13 Distribution of Property Values by Land Use in Coastal Regions, 2007............. ........... ........... ........... .. 91

Figure 9.14 Average Coastal Property Values by Land Use in Coastal Regions, 2007........... .......... ........... ........... .. 92

Figure 9.15 Coastal Value as a Percent of Total Value in Coastal Regions, 2006.............. ........... ........... ........... ...... 92

Figure 9.16 Percent Growth in Coastal Values in Coastal Regions 2002-2007............. ........... ........... .......... ............ 93 Figure 9.17 Property Tax Revenues from Coastal Parcels by Region .......... ........... ........... ........... ........... ........... ...... 93

Figure 9.18 Distribution of the Number of Coastal Properties by County Northeast Region, 2007.............. ............ 94

Figure 9.19 Distribution of Coastal Property Values by County Northeast Region, 2007 .......... ........... ........... ........ 95

Figure 9.20 Distribution of Average Coastal Property Values in Northeast Coastal Region, 2007.................. .......... 95

Figure 9.21 Coastal Value as a Percent of Total Value in Northeast Coastal Region, 2006.......... ........... ........... ...... 96

vi

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 11/219

Figure 9.22 Percent Growth in Coastal Value in Northeast Coastal Region 2002-2007 ........... ........... ........... .......... 96

Figure 9.23 Distribution of Coastal Property Values by Land Use in Northeast Coastal Region, 2007.................... 97

Figure 9.24 Average Value of Coastal Properties by Land Use in Northeast Coastal Region, 2007................ .......... 97

Figure 9.25 Property Tax Revenues from Coastal Parcels by County in Northeast Coastal Region, 2007 ............ .... 98

Figure 9.26 Distribution of the Number of Coastal Properties by County Southeast Region, 2007.............. ........... . 99

Figure 9.27 Distribution of Coastal Property Values by County in Southeast Region, 2007 ........... ........... ........... ... 99

Figure 9.28 Distribution of Average Coastal Property Values in Southeast Coastal Region, 2007......... ........... ..... 100

Figure 9.29 Coastal Value as Percent of Total Value in Southeast Coastal Region, 2006 ........... ........... .......... ...... 100

Figure 9.30 Percent Growth in Coastal Value in Southeast Coastal Region 2002-2007 .......... ........... ........... ......... 101

Figure 9.31 Distribution of Coastal Property Values by Land Use in Southeast Coastal Region, 2007........... ....... 101

Figure 9.32 Average Coastal Property Values by Land Use in Southeast Coastal Region, 2007............ .......... ...... 102

Figure 9.33 Property Tax Revenue from Coastal Parcels by County in Southeast Coastal Region, 2007............... 102

Figure 9.34 Distribution of Number of Coastal Properties by County Southwest Region, 2007................ ........... .. 103

Figure 9.35 Distribution of Coastal Property Values by County in Southwest Region, 2007 .......... ............ ........... 104

Figure 9.36 Distribution of Average Coastal Property Values in Southwest Coastal Region, 2007............. ........... 104

Figure 9.37 Coastal Values as Percent of Total Value in Southwest Coastal Region, 2006........... ........... ........... ... 105

Figure 9.38 Percent Growth in Coastal Value in Southwest Coastal Region 2002-2007 ........... ........... ........... ....... 105

Figure 9.39 Distribution of Coastal Property Values by Land Use in Southwest Coastal Region, 2007.................. 106

Figure 9.40 Average Coastal Property Values by Land Use in Southwest Coastal Region, 2007.......... ........... ....... 106

Figure 9.41 Property Tax Revenues from Coastal Parcels by County in Southwest Coastal Region, 2007............ 107

Figure 9.42 Distribution of the Number of Coastal Properties by County Big Bend Region, 2007 ........... ........... .. 107

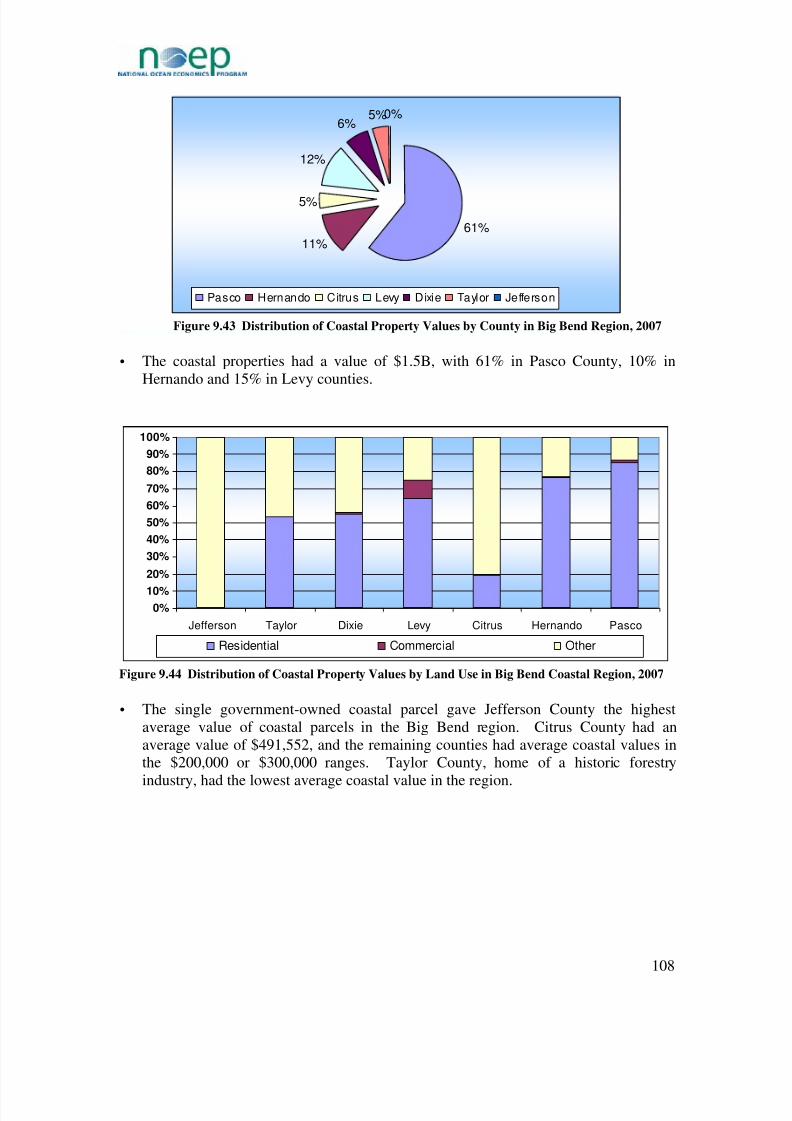

Figure 9.43 Distribution of Coastal Property Values by County in Big Bend Region, 2007.......... ........... ........... ... 108

Figure 9.44 Distribution of Coastal Property Values by Land Use in Big Bend Coastal Region, 2007........... ....... 108

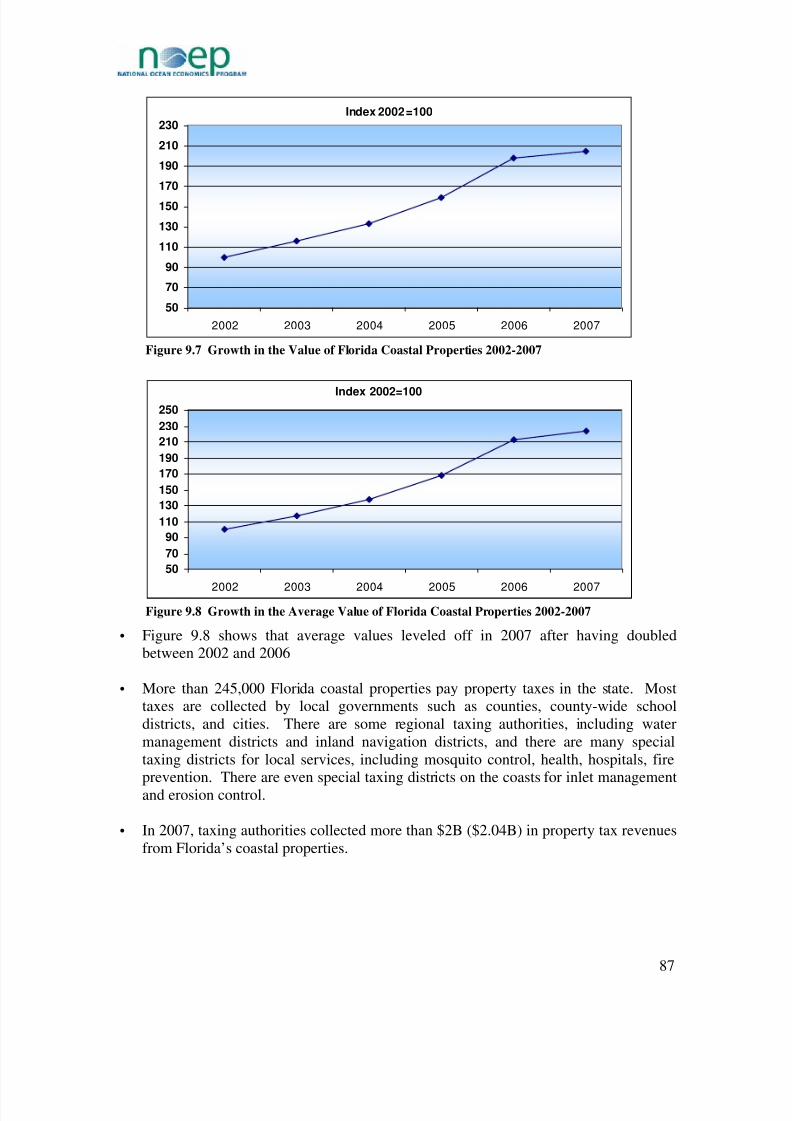

Figure 9.45 Coastal Value as Percent of Total Value in Big Bend Coastal Region, 2006................ ........... ........... . 109 Figure 9.46 Percent Growth in Coastal Value in Big Bend Coastal Region 2002-2007........... ........... ........... ......... 109

Figure 9.47 Distribution of Coastal Property Values by Land Use in Big Bend Coastal Region, 2007........... ....... 110

Figure 9.48 Average Coastal Property Values by Land Use in Big Bend Coastal Region, 2007 .......... ........... ....... 110

Figure 9.49 Property Tax Revenues from Coastal Parcels by County in Big Bend Coastal Region, 2007.............. 111

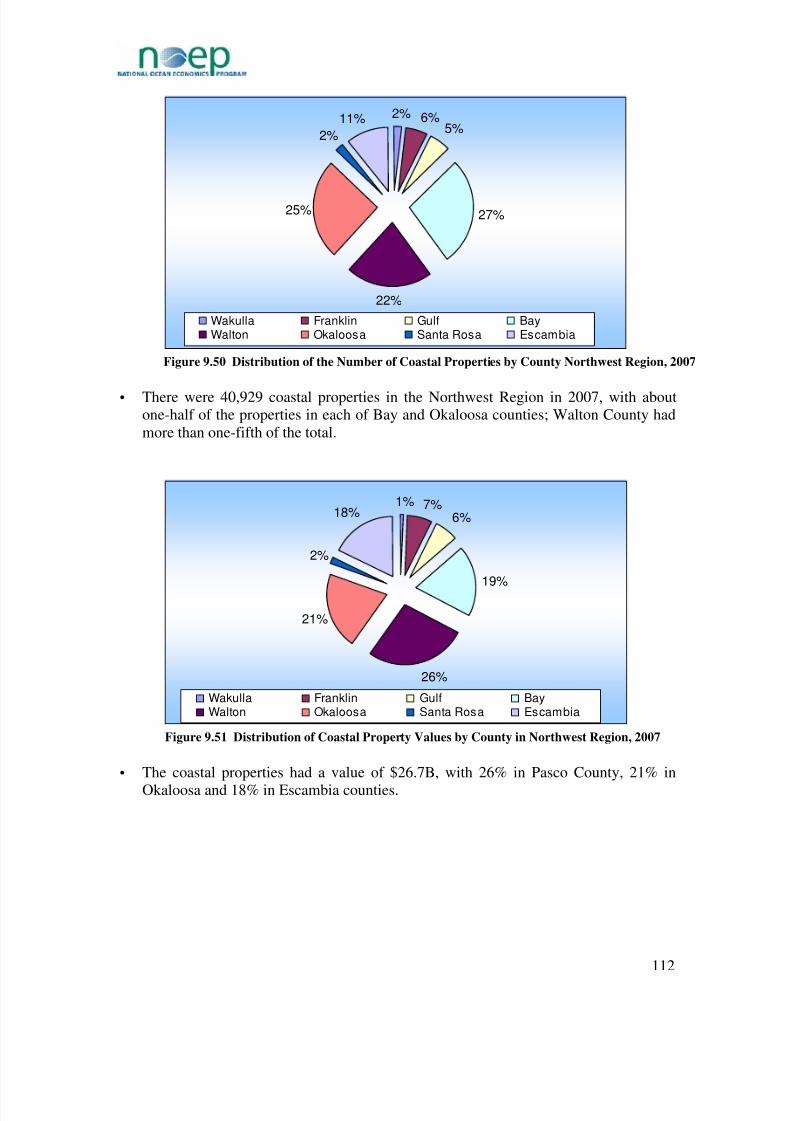

Figure 9.50 Distribution of the Number of Coastal Properties by County Northwest Region, 2007................ ....... 112

Figure 9.51 Distribution of Coastal Property Values by County in Northwest Region, 2007 .......... ........... .......... .. 112

Figure 9.52 Distribution of Average Coastal Property Values in Northwest Coastal Region, 2007............. ........... 113

Figure 9.53 Coastal Value as Percent of Total Value in Northwest Coastal Region, 2006 .......... ........... ........... ..... 113

Figure 9.54 Percent Growth in Coastal Value in Northwest Coastal Region 2002-2007 ........... ........... ........... ....... 114 Figure 9.55 Distribution of Coastal Property Values by Land Use in Northwest Coastal Region, 2007............ ..... 114

Figure 9.56 Average Coastal Property Values by Land Use in Northwest Coastal Region, 2007............ ........... .... 115

Figure 9.57 Property Tax Revenues from Coastal Parcels by County Northwest Coastal Region, 2007 ............ .... 115

Figure 9.58 Type of Accommodations Used by Domestic Visitors to Florida............ ........... ........... .......... ........... .. 116

Figure 9.59 Licenses for Tourist and Transient Housing in Florida, 2008 ........... ........... ........... ........... ........... ........ 117

vii

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 12/219

Figure 9.60 Value of Coastal Retail and Entertainment Properties, 2007.................. ........... .......... ........... ........... ... 118

Figure 9.61 Entertainment & Recreation in Florida Coastal Properties, 2007............ ........... ........... ........... .......... .. 118

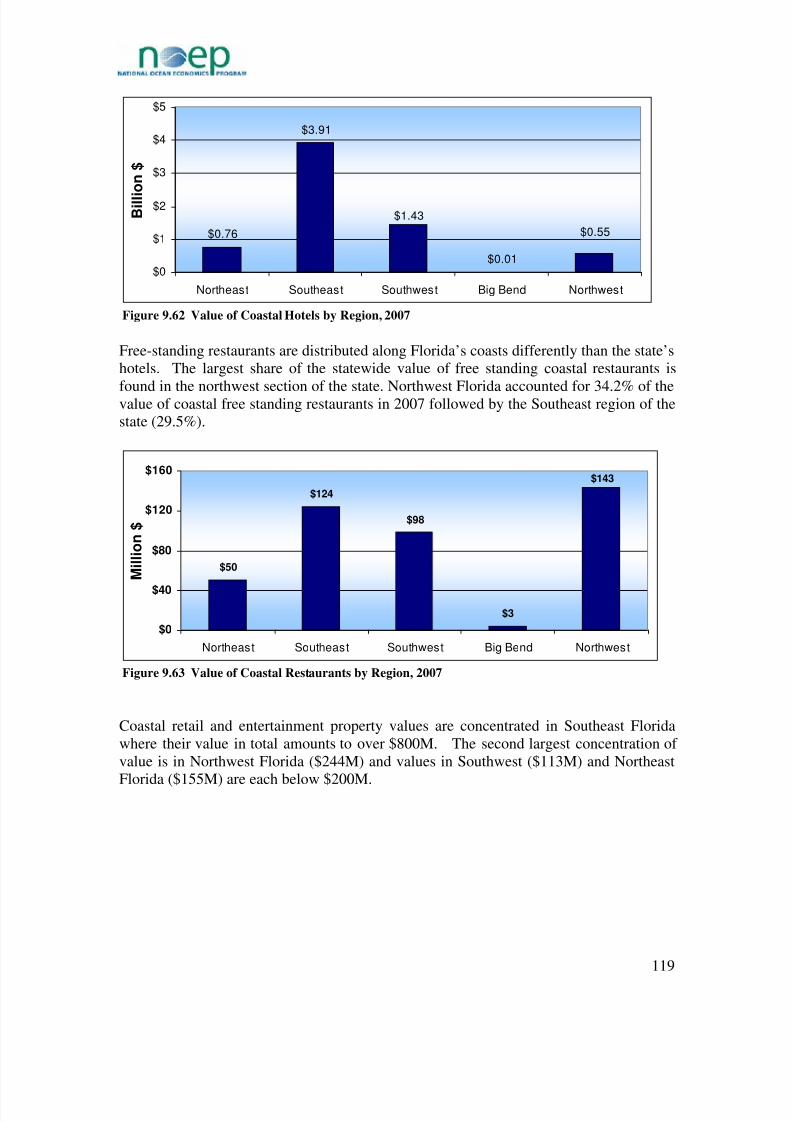

Figure 9.62 Value of Coastal Hotels by Region, 2007......... ........... .......... ........... ........... ........... .......... ........... ......... 119

Figure 9.63 Value of Coastal Restaurants by Region, 2007 .................................................................................... 119

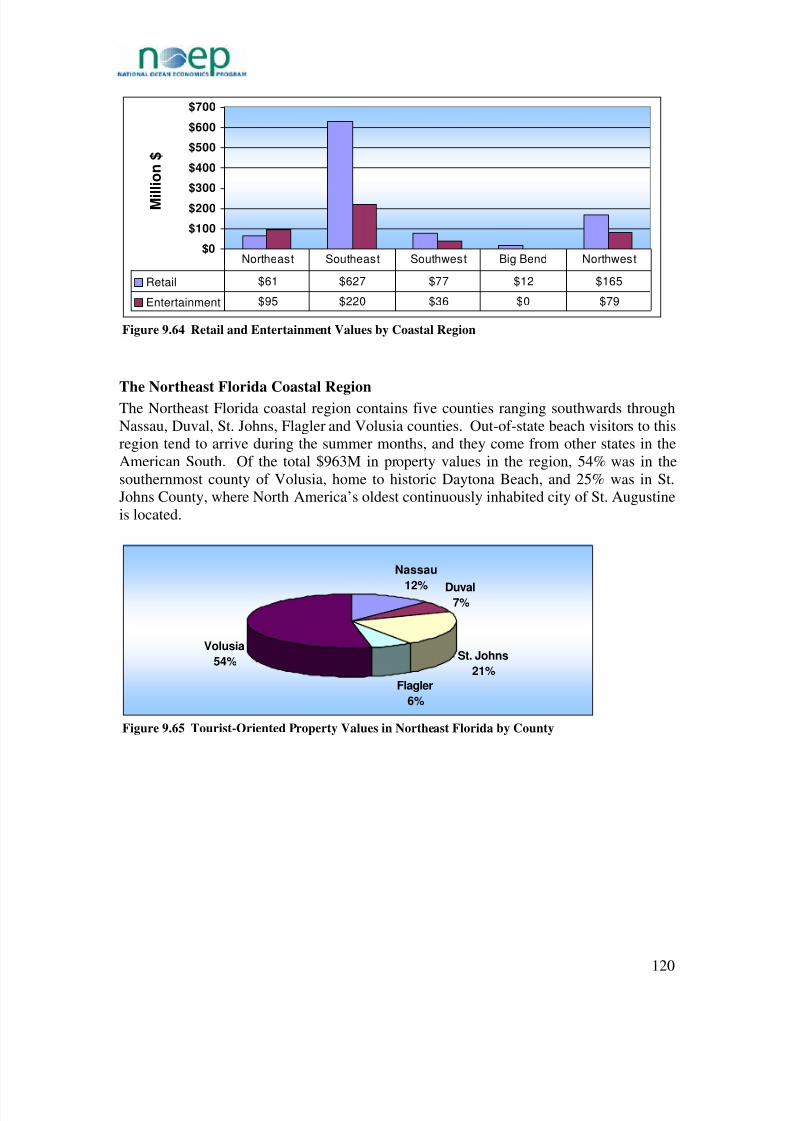

Figure 9.64 Retail and Entertainment Values by Coastal Region.......... .......... ........... ........... ........... ........... .......... .. 120

Figure 9.65 Tourist-Oriented Property Values in Northeast Florida by County ........... ........... ........... .......... ........... 120

Figure 9.66 Tourist-Oriented Property Values in Northeast Florida by Type.................... ........... ........... ........... ..... 121

Figure 9.67 Value of Tourist-Oriented Property in Northeast Florida by County, 2007 .......... ........... ........... ......... 121

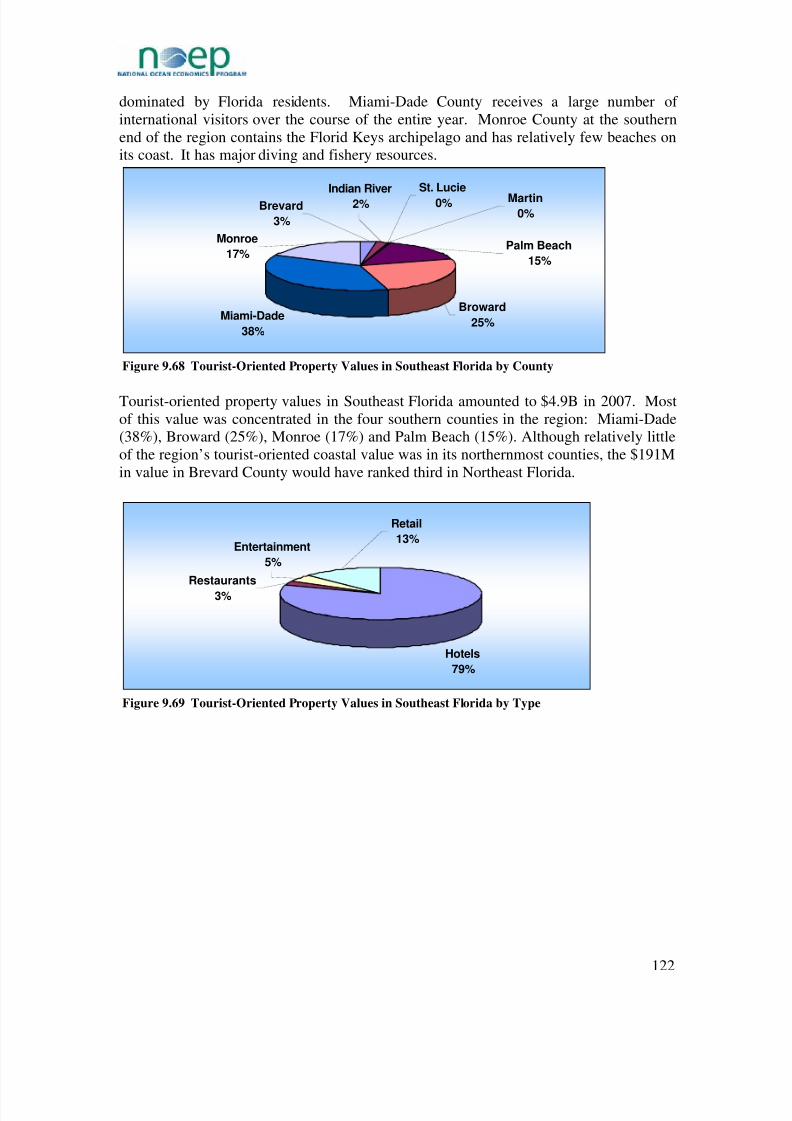

Figure 9.68 Tourist-Oriented Property Values in Southeast Florida by County ........... ........... ........... .......... ........... 122

Figure 9.69 Tourist-Oriented Property Values in Southeast Florida by Type........... ........... ........... ........... .......... .... 122

Figure 9.70 Value of Tourist-Oriented Properties in Southeast Florida by County, 2007.............. ........... ............ .. 123

Figure 9.71 Tourist-Oriented Property Values in Southwest Florida by County................... ........... .......... ........... .. 123

Figure 9.72 Tourist-Oriented Property Values in Southwest Florida by Type ........... ........... .......... ........... ........... .. 124

Figure 9.73 Value of Tourist-Oriented Properties by County in Southwest Florida, 2007.................. ........... ......... 124

Figure 9.74 Tourist-Orientated Property Values in the Big Bend Region by County......... ........... ........... .......... ...... 125

Figure 9.75 Tourist-Oriented Property Values in the Big Bend Region by Type .......... ........... .......... ........... .......... 125

Figure 9.76 Value of Tourist-Oriented Properties by County in the Big Bend Region, 2007 ........... ........... ........... 126

Figure 9.77 Tourist-Oriented Property Values in Northwest Florida by County.................. ........... ........... ........... .. 126

Figure 9.78 Tourist-Oriented Property Values in Northwest Florida by Type ........... ........... .......... ........... ........... .. 127

Figure 9.79 Value of Tourist-Oriented Properties by County in Northwest Florida, 2007.......... ........... ........... ..... 127

Figure 9.80 Percentage Seasonal Homes within Select Counties, 1990 and 2006............... .......... ........... ........... ..... 130

Figure 9.81 Seasonal Homes for Select Counties, 1990 and 2006 (arranged by population) ........... ........... ........... .. 131

Figure 9.82 Change in Number of Seasonal Homes for Select Counties 1990-2006............ ........... ........... ........... ... 132

Figure 9.83 Rate of Change of Seasonal Homes 1990-2006 .................................................................................... 133 Figure 9.84 Changes in Seasonal Homes for Selected Counties................. ........... ........... ........... ........... ........... ....... 134

Figures 9.85 and 9.86 Growth in Seasonal Homes (percent change), 2000-2006 and 1990-2006................ ........... 135

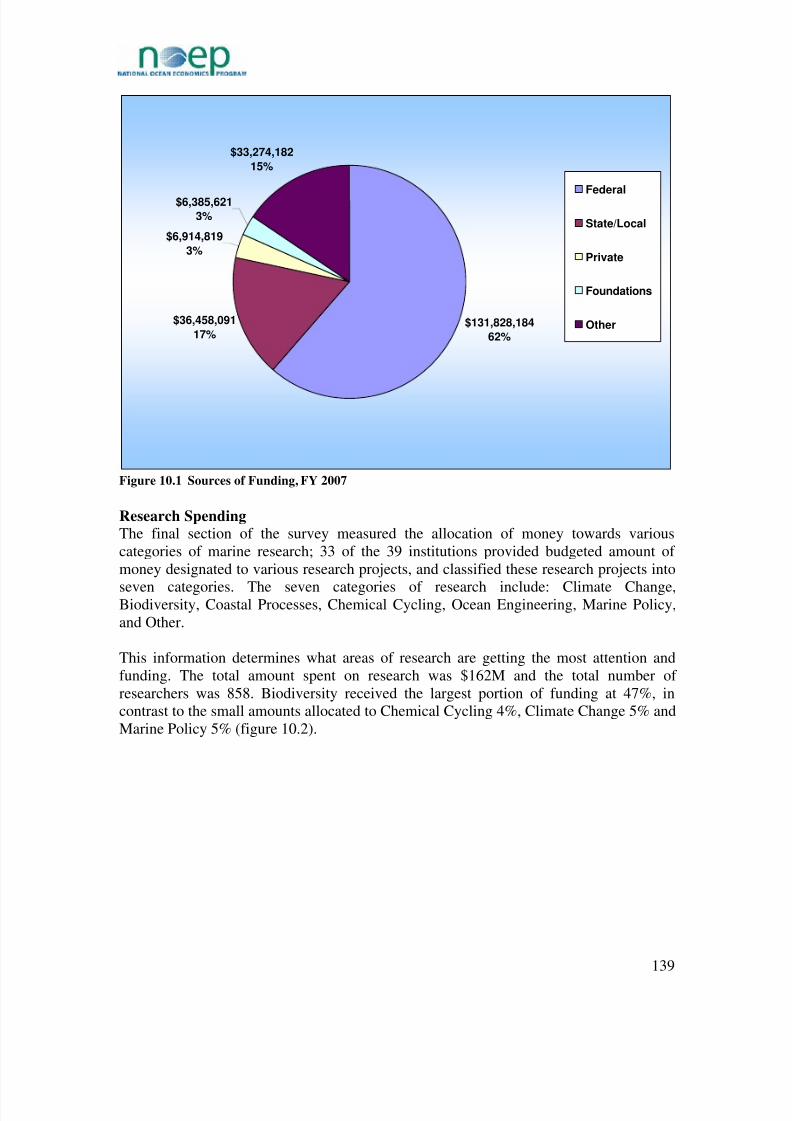

Figure 10.1 Sources of Funding, FY 2007............................................................................................................... 139

Figure 10.2 Areas of Research Spending, FY 2007.......... ........... ........... .......... ........... ........... ........... .......... .......... .. 140

Figure 11.1 Florida Coastal Regions Map ............................................................................................................... 147

Figure 11.2 Map of Public Beaches by County ........................................................................................................ 151

Figure 11.3 Map of Public Parks by County............................................................................................................. 152

Figure 11.4 Map of Marine Facilities by County.............. .......... ........... ........... .......... ........... ........... .......... .......... .... 153

Figure 11.5 Map of Boat Ramps by County ............................................................................................................154 Figure 11.6 Map of Piers by County........................................................................................................................ 155

Figure 12.1 Florida Comprehensive Recreation Planning Regions .......... ........... ........... .......... ........... ........... ......... 157

Figure 12.2 Map of Florida State Park Districts ....................................................................................................... 160

Figure 12.3 Attendance at Florida State Parks, FY2001-02 to FY 2006-07........... ........... .......... ........... .......... ........ 161

Figure 12.4 Attendance at Florida State Parks by District, FY2001-02 to FY 2006-07 ........... .......... ........... ........... 161

viii

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 13/219

Figure 12.5 Attendance at National Parks in Florida 2001-2006............ ........... ........... .......... ........... ........... .......... .. 162

Figure 12.6 Attendance by Region at National Parks in Florida 2001-2006 .......... ........... ........... ........... ........... ...... 163

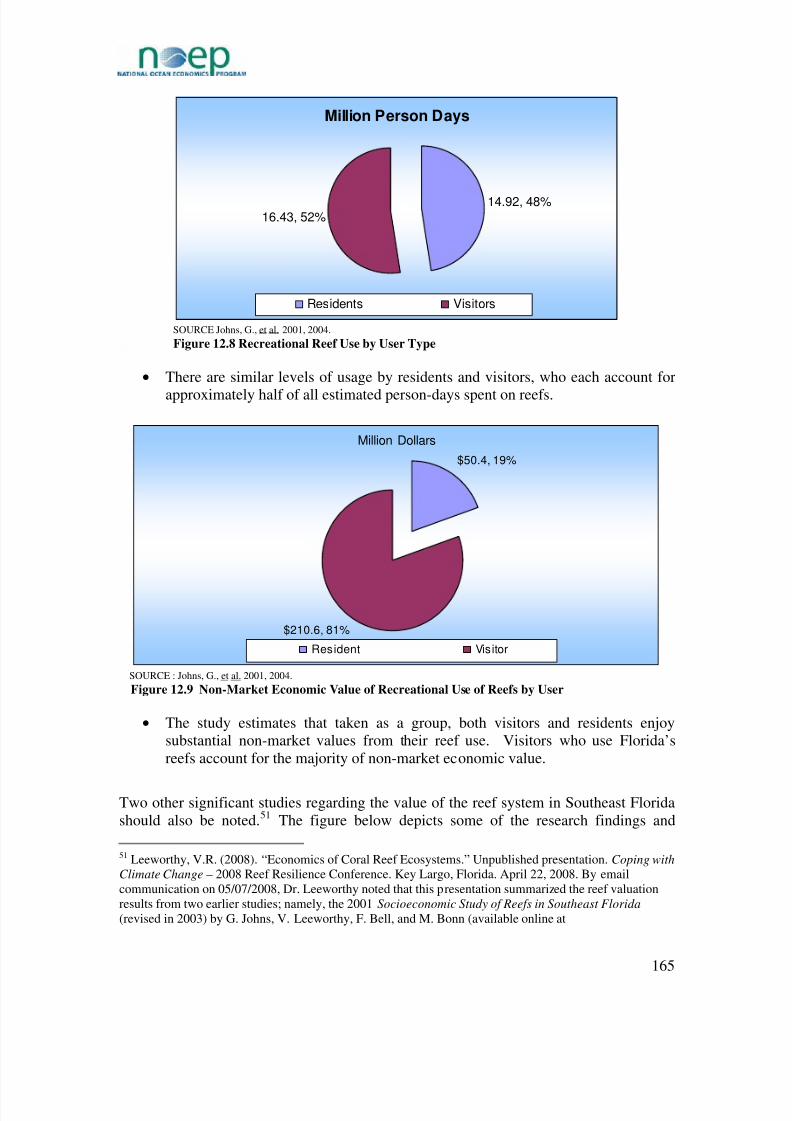

Figure 12.7 Recreational Reef Use by Counties ...................................................................................................... 164

Figure 12.8 Recreational Reef Use by User Type................. ........... ........... ........... .......... ........... ........... .......... ......... 165

Figure 12.9 Non-Market Economic Value of Recreational Use of Reefs by User........... ........... ........... ........... ....... 165

Figure 12.10 Reef Use by Activity ........................................................................................................................... 166

Figure 13.1 Florida Vessel Registration FY 2000-01 to FY 2005-06........... .......... ........... ........... .......... ........... ....... 169

Figure 13.2 Estimated Recreational Boating Activity FY 2000-01 to FY 2005-06................ ........... .......... ........... .. 171

Figure 13.3 Estimated Recreational Boating Activity by Region FY 2000-01 to FY 2005-06 .......... ........... ........... 171

Figure 14.1 Saltwater Fishing and Sportsman Licenses for Residents and Non-Residents FY 2004-05 to FY 2005-06 .............................................................................................................................................................................. 174

Figure 14.2 Saltwater Fishing and Sportsman Licenses for Residents and Non-Residents FY 2004-05 to FY 2005-06, Coastal Regions Only .........................................................................................................................................175

Figure 14.3 Saltwater Fishing and Sportsman Licenses for Residents and Non-Residents by Region FY 2004-05 toFY 2005-06............................................................................................................................................................... 175

Figure 14.4 Saltwater Fishing and Sportsman Licenses for Counties in Southwest Region, FY 2005/2006............ 177

Figure 16.1 Estimated Annual Activity Days 2003 - 2007 .......... ........... ........... ........... .......... ........... ........... .......... .. 184

Figure 16.2 Estimated Beach Activity Days by Region 2003 - 2007 ........... .......... ........... ........... .......... ........... ....... 185

Figure 16.3 Estimated Beach Activity Days by Geographic Origin 2003 - 2007.......... ........... ........... ........... .......... 185

Figure 16.4 Florida State Parks Attendance by Beach Region FY 2002-03 to FY 2006-07................... ........... ....... 186

Figure 16.5 Characteristics of Beach Visits to Cocoa Beach, Winter 2007......... ........... ........... ........... ........... ......... 190

Figure 16.6 Beach Visits by Purpose of Activity in Cocoa Beach, Winter 2007............... ........... ........... ........... ...... 190

ix

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 14/219

x

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 15/219

Part I — Introduction and Background

Chapter 1 Context for the Study

Phase II of Florida’s Ocean and Coastal Economics Report was prepared for the FloridaOceans and Coastal Council and funded under contract #RM077 by the FloridaDepartment of Environmental Protection. The Phase I report of Florida’s Ocean andCoastal Economies provided basic information that the NOEP compiles for all coastalstates about employment, wages and output of those activities located geographicallyalong Florida’s shoreline (Coastal Economy) as well as those activities directlydependent upon the oceans (Ocean Economy). That information not only described thestatus and trends of Florida’s Coastal and Ocean Economy but allowed comparison toeconomies in other states as well as comparisons among counties in Florida. It alsoprovides basic data about fisheries productivity and estimates of the non-market value of coastal recreation.

The Phase II report is in three volumes: this report, Phase II, Florida’s Ocean and

Coastal Economies, a smaller summary version, Phase II Facts and Figures, and Phase

II Appendices. Phase II expands and provides more detailed information about additionaleconomic activities that particularly define Florida’s Ocean Economy that were notincluded in Phase I. These include: the passenger cruise industry, the commercial andrecreational fishing, coastal real estate – the value of coastal real estate, value of touristreal estate and data on seasonal housing; marine research and education institutions,coastal construction activities including beach nourishment and dredging, and finallymarine transportation and port activities. In addition, an expanded marine recreationsection provides detail about the location of Florida’s coastal recreational assets, the

number provides information on the number of people using them, and estimates of thevalue of numerous recreational activities such as boating, surfing, etc. A major study onboating and marinas is currently underway for the state of Florida by other contractors

1.

To provide context for the expanded descriptions of economic activities, the NOEP hasalso prepared an update of the Phase I report using a summary of the most recentnumbers available for Florida’s Coastal and Ocean economic contributions, e.g. asummary update of the estimates from the Phase I report.

Background

Florida’s economy has been strongly tied to the oceans through tourism and recreationfor decades. Yet, there are many facets of its economy that are also dependent on its longand lovely coastline, but don’t get reported in any single document or coherent report.

1 Urban Harbors Institute, et al. (forthcoming in 2008).

Boating Access Facilities Inventory and Economic Study. University of Massachusetts-Boston, Mass.Prepared for Florida Fish and Wildlife Conservation Commission.

1

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 16/219

That is the purpose of this effort. The combination of these activities adds up to a diverseeconomy that sustains Florida. Marine industries, for example, are a major economicengine for the state of Florida. In 2005 it was reported that the marine-related industrystatewide generated $18.4 billion in annual economic impact and 220,000 jobs in theareas of seaports, boating and marinas, fishing, and marine science research. Almost

100,000 of these jobs were in manufacturing.

2

This report attempts to provide important details, some of which can be found in separatereports and separate websites which were our sources and reported throughout thefollowing pages, and some of which were generated specifically for this report, such asthe real estate values and those for the marine research and education sector, two newsectors that NOEP added to its data series with the anticipation that these sectors willsoon be measured in other states as well. These newly added sectors are also importantto report because they add an important dimension to Florida’s economy. Coastal realestate carries a high price tag with various tax revenues that flow to the state. At thesame time, that market has gone through volatile times recently, leaving the state with farlower revenues as a result of lower values. It is instructive to be able to track thesevalues so that contingencies can be created with more accurate forecasting. The researchand education sector chapter provides a window into the potential effectiveness of Florida’s efforts to attract research institutions as a way of diversifying its economy to aless volatile service sector. The Marine Research and Education sector provides aninteresting microcosm, and only three-fifths of the institutions actually responded, so thischapter is still underestimating values.

Dollar values in this report are reported in current dollars when only one year is availableand in real dollars (2000 base year) for multiple years.

For those who have not read Phase I, we include a description of the two types of

economies we have measured in both reports: Ocean and Coastal Economies. SeeGlossary.

The Coastal and Ocean Economies Are Not the Same

Economic ActivityLocated Along the Coast

Economic Activity Using theOcean as an Input

Coastal Economy Ocean Economy

2 Murray, Thomas & Associates, Inc. (2005). Florida’s Recreational Marine Industry – Economic Impactand Growth: 1980-2005. p. iii. Cited in Marine Industries Association of Florida. Boating is Big Businessin Florida. Retrieved 11/15/2007 http://www.boatflorida.org/custom_pages/site_page_2708/index.html.

2

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 17/219

Chapter 2 Glossary of Terms and Definitions

To avoid repetition and for clarification purposes, the following terms and definitionsregarding economic indicators and valuation categories are found in the beginning of thisreport, so that the reader can fully understand what is intended throughout the text.

Coastal Economy: The sum of all economic activity occurring in counties defined by states as part of their coastal zone management program or part of a coastal watershed as definedby the U.S. Geological Survey. For purposes of analyzing the Florida CoastalEconomy, counties are divided between shore-adjacent and inland counties tobetter illuminate the differences between the shoreline and inland regions. Unlessotherwise noted, coastal counties will indicate shoreline counties in thisdocument.

Ocean Economy:

The concept of the Ocean Economy derives from the ocean (or Great Lakes) andits resources being a direct or indirect input of goods and/or services to aneconomic activity: a) an industry whose definition explicitly ties the activity tothe ocean, or b) which is partially related to the ocean and is located in a shoreadjacent zip code. This is defined in part by the definition of a sector, such as Maritime Transportation in the North American Industrial Classification System

3

or an industry that is part of the sector (for example, Deep Sea FreightTransportation) and partly by geographic location (for example, a hotel in acoastal town).

North American Industrial Classification System (NAICS):

NOEP Economic statistics are grouped by a classification system known as theNorth American Industrial Classification System (NAICS), which imperfectlyreflects the relationship between economic activity and the ocean. The NAICS isthe successor to the Standard Industrial Classification. It was developed in the1990s as a part of the North American Free Trade Agreement (NAFTA) toprovide a common basis for the United States, Canada, and Mexico to measuretheir economic activity. The definition of the Ocean Economy industries isderived from the NAICS classifications for the following industries (see Table 1).

3 As of 2000, all industries are classified using the North American Industry Classification System (NAICS)rather than the Standard Industrial Classification (SIC by BLS). NAICS focuses on how products and servicesare created, as opposed to SIC which focuses on what is produced. Using NAICS yields significantly differentindustry groupings from those produced using SIC.

3

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 18/219

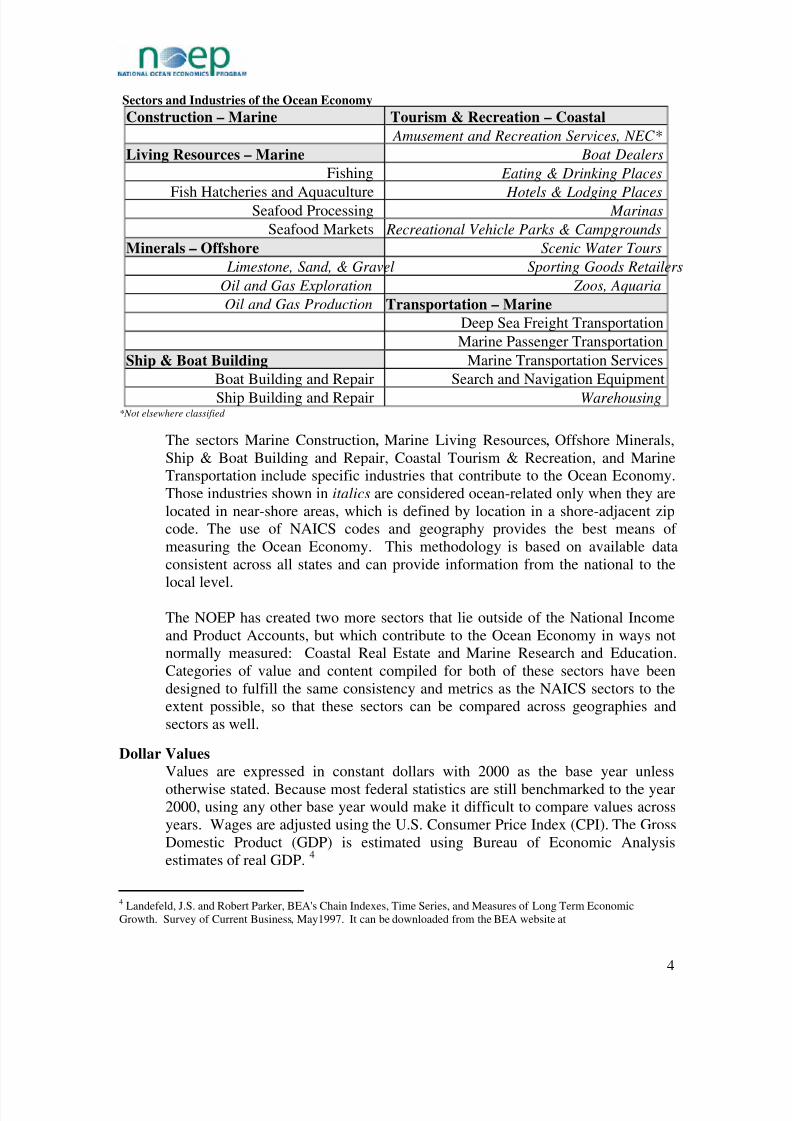

Sectors and Industries of the Ocean Economy

Construction – Marine Tourism & Recreation – Coastal

Amusement and Recreation Services, NEC*

Living Resources – Marine Boat Dealers

Fishing Eating & Drinking Places

Fish Hatcheries and Aquaculture Hotels & Lodging PlacesSeafood Processing Marinas

Seafood Markets Recreational Vehicle Parks & Campgrounds

Minerals – Offshore Scenic Water Tours

Limestone, Sand, & Gravel Sporting Goods Retailers

Oil and Gas Exploration Zoos, Aquaria

Oil and Gas Production Transportation – Marine

Deep Sea Freight Transportation

Marine Passenger Transportation

Ship & Boat Building Marine Transportation Services

Boat Building and Repair Search and Navigation Equipment

Ship Building and Repair Warehousing*Not elsewhere classified

The sectors Marine Construction, Marine Living Resources, Offshore Minerals,Ship & Boat Building and Repair, Coastal Tourism & Recreation, and MarineTransportation include specific industries that contribute to the Ocean Economy.Those industries shown in italics are considered ocean-related only when they arelocated in near-shore areas, which is defined by location in a shore-adjacent zipcode. The use of NAICS codes and geography provides the best means of measuring the Ocean Economy. This methodology is based on available dataconsistent across all states and can provide information from the national to the

local level.

The NOEP has created two more sectors that lie outside of the National Incomeand Product Accounts, but which contribute to the Ocean Economy in ways notnormally measured: Coastal Real Estate and Marine Research and Education.Categories of value and content compiled for both of these sectors have beendesigned to fulfill the same consistency and metrics as the NAICS sectors to theextent possible, so that these sectors can be compared across geographies andsectors as well.

Dollar Values Values are expressed in constant dollars with 2000 as the base year unless

otherwise stated. Because most federal statistics are still benchmarked to the year2000, using any other base year would make it difficult to compare values acrossyears. Wages are adjusted using the U.S. Consumer Price Index (CPI). The GrossDomestic Product (GDP) is estimated using Bureau of Economic Analysisestimates of real GDP.

4

4 Landefeld, J.S. and Robert Parker, BEA's Chain Indexes, Time Series, and Measures of Long Term EconomicGrowth. Survey of Current Business, May1997. It can be downloaded from the BEA website at

4

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 19/219

• Dollar values are estimated as direct and indirect values. Indirect values includeinduced values.

• Direct values are those activities associated only with the designated oceansectors such as Recreation & Tourism and Living Resources (examples include

labor and capital costs associated with fish processing or ship building.• Multipliers are indirect and induced values. Multipliers affect the estimates of

employment, wages, and output within the region. Indirect effects include boththe change in economic activity in industries within the region that buy or sellfrom ocean industries (examples include sales of food to restaurants and hotelsand the activities of travel agents booking trips) and the change in economicactivity resulting from the spending of the wages earned by those employed of theocean industries within the region (induced). All indirect values or multipliereffects are based on IMPLAN, a standard and widely used economic impactmodel.

• Unless otherwise indicated, all measures are stated as direct values.

Employment Employment is the annual average wage and salary employment (excluding self-employment) as reported in the Quarterly Census of Employment and Wages(formerly known as the ES-202 employment series). This definition covers about90% of employment in the U.S. It excludes farm employment, the military,railroads, and self-employment. Wage and salary employment measuresemployment by place of work, not by place of residence. It also measures jobs,not people. It does not distinguish between full and part time work, and year-round and part-year jobs. The data in the NOEP database is annual averageemployment. Employment in the fisheries harvesting sector is generally excludedfrom the unemployment insurance laws and thus is not included in the NOEPdata.

Gross Domestic Product (GDP)

GDP is a measure of the contribution of the sector to the value of goods andservices in the economy. GDP is a measure of value-added, or sales, minus the cost of inputs. Using this measure eliminates “double counting,” among sectors.5

GDP data is published only at the state level and for industry aggregations greaterthan used in the Ocean Economy definition. In order to estimate a share of GDPin an Ocean or Coastal Economy industry, the proportion of the GDP for a givensector is calculated based on the proportion of total wages paid in that sector by a

given establishment. Since wages often account for as much as 60% of GSP, this

http://www.bea.gov/bea/regional/gsp/help/OnlineHelp.htm5 Bureau of Economic Analysis defines GDP as “the value added in production by the labor and property located in astate. GDP for a State is derived as the sum of the gross state product originating in all industries in a State. In concept,an industry's GDP, referred to as its "value added", is equivalent to its gross output (sales or receipts and otheroperating income, commodity taxes, and inventory change) minus its intermediate inputs (consumption of goods andservices purchased from other U.S. industries or imported). Thus, GDP is often considered the state counterpart of thenation's gross domestic product (GDP), BEA's featured measure of U.S. output. In practice, GDP estimates aremeasured as the sum of the costs incurred and incomes earned in the production of GDP.”

5

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 20/219

method is a reasonable approximation of individual establishments’ contributionto GDP.

Housing Patterns and Trends

These include both single and multi-family housing units including seasonal andyear round, owner occupied and rental. The U.S. Bureau of Census is the sourcefor these data.

National Ocean Economics Program (NOEP):

Externally funded program to understand and estimate changes in the nature andvalue of the coastal and ocean-based economy of the United States.

Wages and Salaries: Total wages and salaries paid; all wages are shown in year 2000 dollars

6

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 21/219

Part II — Executive Summary and Update

Chapter 3 Executive Summary

• Florida’s Coastal Economy generated almost $562B in 2006.

• Florida’s Ocean Economy contributed $25B in 2005.

Fishing Industry

• Commercial saltwater landings generated $143M in inflation-adjusted docksidesales in 2007, compared to $247.5M in 1990.

• Annual commercial saltwater landings declined 66% by weight and 56% inconstant value between 1990 and 2007.

• Commercial vessel registrations declined 13.3% from 1990 to 2007, whilepleasure craft registrations increased by 11%.

• Seafood Imports totaled $2.1B in 2007, an annual growth of 5.7% since 1990.

• Seafood Exports were $89.1B in 2007.

• In 2006, over 2M saltwater anglers contributed $3B in retail sales with over 180Mfish landed, making Florida the number one recreational fishing state in theUnited States.

Marine Transportation

• Florida's international trade value, including both waterborne and airbornecommodities moving through coastal access points and over land, totaled $115B,a $5B increase in 2007 (4.7%) over the previous record of $110B in 2006.

• Florida’s 14 deepwater seaports managed 121 million tons of cargo, generating an

overall $73B economic contribution.Coastal Construction

• Dredging costs increased during the period 1990-2000, but declined sharply since,with a peak in 2000 at $41.2M, and value in 2005 being $3.3M.

• 59% of Florida’s beaches (485 miles) are experiencing erosion; of these, 192miles are nourished beaches managed by federal entities.

• $1.1B was spent from 1960 through 2007 on beach nourishment activities inFlorida.

Tourism and Recreation – The Cruise Industry

• More than 9M cruise passengers embarked on cruises from U.S. ports in 2006.

• The top three Florida ports accounted for over 4M of the 9M passengers thatembarked on cruises from U.S. ports in 2006 or an estimated 50% of all U.S.cruise embarkations.

• Florida businesses received almost $6B in 2006, or one-third of the directexpenditures generated by the cruise industry in the United States.

7

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 22/219

Real Estate

• Florida’s 367,000 coastal properties were valued for tax purposes in 2006 at$181B, yielding $2B in property tax revenues.

• Coastal parcels made up 7.5% of the value of all real estate in Florida.

•

From 2002-2006, the number of coastal parcels grew by about 10%, but the valueof coastal parcels more than doubled reflecting the strong demand for coastal realestate in the early part of this decade.

Seasonal Housing

• Florida ranks first in the nation for number of seasonal housing units.

• In 1990 Florida accounted for 14% of all seasonal housing units in the UnitedStates with 417,670. In 2006 Florida accounted for 16% of U.S. seasonal housingunits with 655,647.

• From 1990-2006 Florida added 237,977 seasonal housing units, a 57% growthrate, compared to an overall U.S growth in seasonal housing units of 37%.

Marine Research and Education, 39 of 55 institutions reporting

• Annual Budgets totaled $272.5M.

• Annual Wages totaled $154M.

• Annual Employment totaled 2,925.

• Number of degree students totaled 2,234.

Coastal Recreation

• In Fiscal Year 2007, the Florida system of State Parks provided a direct economicimpact of over $936M to local economies throughout the state.

• For every 1,000 persons attending a State Park, total direct economic impactexceeded $43,200. On average, if a State Park were closed for one year, a loss of nearly $5.9M would impact the state economy. Similarly, if the State Park systemincreased annual attendance by 10% during the next fiscal year, the state’seconomy would rise by an additional $65M.

• In 2005, the recreational marine-related industry statewide generated $18.4B inannual economic impact, 220,000 jobs in the areas of boating and marinas,fishing, and marine science research. Almost 100,000 of these jobs were inmanufacturing. 6

6 Murray, Thomas & Associates, Inc. (2005). Florida’s Recreational Marine Industry – Economic Impact

and Growth: 1980-2005. p. iii. Cited in Marine Industries Association of Florida. Boating is Big Business

in Florida. Retrieved 11/15/2007 http://www.boatflorida.org/custom_pages/site_page_2708/index.html.

8

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 23/219

Chapter 4 Updates from Phase I Report

To set the stage for the economic studies included in this report, the most recent estimatesavailable for both the Ocean and Coastal economies for Florida are present below.

• Florida’s Ocean Economy contributed $25B to state GDP during 2005. Thiscomprised 4% of the total GDP.

• Without the multiplier effects, the Ocean Economy produced direct output of more than $14B.

Table 4.1 Florida’s Ocean Economy, 2005

Ocean Economy Employment, 2005

Sector Direct Indirect & Induced Total

Construction 3,580 3,077 6,657

Living Resources 4,135 4,419 8,554

Minerals 475 390 865

Ship & Boat Building 13,556 11,960 25,516

Tourism & Recreation 261,204 100,669 361,873

Transportation 32,049 75,659 107,708

Ocean Economy 314,999 196,174 511,173

Ocean Economy Wages, 2005

Sector Direct Indirect & Induced Total

Construction $163,800,810 137,166,798 $300,967,608

Living Resources $122,450,157 161,230,122 $283,680,279

Minerals $20,717,729 66,319,522 $87,037,251

Ship & Boat Building $497,270,170 347,392,941 $844,663,111

Tourism & Recreation $4,786,359,214 2,935,474,106 $7,721,833,320

Transportation $1,615,599,892 2,610,163,186 $4,225,763,078

Ocean Economy $7,206,197,972 6,257,746,675 $13,463,944,647

Ocean Economy GDP, 2005Sector Direct Indirect & Induced Total

Construction $365,690,000 333,436,142 $699,126,142

Living Resources $354,640,000 292,507,072 $647,147,072

Minerals $68,900,000 49,311,730 $118,211,730

Ship & Boat Building $396,090,000 262,053,144 $658,143,144

Tourism & Recreation $10,512,590,000 7,697,318,398 $18,209,908,398

Transportation $2,322,960,000 2,200,307,712 $4,523,267,712

Ocean Economy $14,020,870,000 10,834,934,198 $24,855,804,198

Florida’s coastal (shoreline counties) contributed almost $562B to state GDP for 2006.This was 82% of state GDP.

Table 4.2 Florida’s Coastal Economy, 2006 (shoreline counties only)

Supersector Establishments Employment Wages GDP

Construction 55,448 473,960 $19,370,199,234 $43,098,844,063

Financial Activities 55,503 428,621 $23,727,596,107 $141,238,751,050

Education and Health Services 41,650 891,115 $36,270,400,396 $44,543,391,374

Information 7,062 122,939 $6,915,884,613 $22,581,285,553

9

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 24/219

Supersector Establishments Employment Wages GDP

Leisure and Hospitality 33,988 641,340 $12,812,829,992 $26,402,075,726

Manufacturing 13,132 302,599 $13,852,457,530 $27,480,902,806

Natural Resources and Mining 2,908 58,923 $1,384,373,389 $4,351,546,699

Other Services 38,141 191,734 $5,157,590,478 $14,166,289,754

Professional and Business

Services 91,849 898,109 $39,061,614,696 $72,180,894,146

Public Administration 2,822 323,459 $15,733,744,365 $60,070,901,103

Trade, Transportation, andUtilities 97,711 1,226,712 $43,642,006,508 $105,637,428,623

Total, all industries 445,634 5,782,478 $226,403,461,926 $561,752,310,896

4.1 Florida Coastal Economy 2006

This section provides an update of Florida’s Coastal Economy for 2006. It includes themost recent values of industries within the shoreline region, for the Atlantic and Gulf coasts, and their contribution to Florida’s economy overall. Comparisons are made to the

2003 values, which were the most recent data available in NOEP’s Florida Ocean and Coastal Economies, 2006 report. Percent changes from 2003 are shown on a state,regional, and county level.

Overall, economic growth from 2003-2006 was strong, with the smallest growth rates foremployment at 10% increase, and the highest growth for GDP at 17.5%. While the finalnumbers for 2007 and 2008 are not yet available, initial evaluations show a reversal of the growth seen leading up to 2006, with declines in 2007 and 2008. Florida’s shorelineand coastal regions’ contribution to the state economy in 2006 are provided in table 4.3.Florida’s shoreline makes up over 75% of economic activity whether measured by GDP,wages, employment, or establishments, yet the shoreline counties make up only 56% of

land area. Both coastal regions showed economic contributions that were inverselyproportional to their land area. While the Gulf Coast makes up 34% of land area, itcontributed approximately 30% of economic activity in Florida; however, the AtlanticCoast takes up 21% of land area and showed a range of economic activity from 45% of Florida’s employment to almost 50% contribution to Florida’s GDP. Thisdisproportionate division of economic distribution is due to the urban counties such asMiami-Dade, Broward, Palm Beach, and Duval along the Atlantic Coast. These fourcounties alone make up 42% of Florida’s overall GDP.

Table 4.3 Florida Economy Total Regional Values and Contribution to State Economy, 2006

Establishments % of FL Total Employment % of FL Total

Florida Total 560,589 100.0% 7,632,992 100.0%

Shoreline Total 445,634 79.5% 5,782,478 75.8%

Atlantic Shoreline 273,503 48.8% 3,425,730 44.9%

Gulf Shoreline 172,131 30.7% 2,356,748 30.9%

Wages % of FL Total GDP % of FL Total

Florida Total $291,926,053,544 100.0% $713,504,000,000 100.0%

Shoreline Total $226,403,461,926 77.6% $561,752,310,896 78.7%

Atlantic Shoreline $139,954,527,968 47.9% $352,075,624,974 49.3%

Gulf Shoreline $86,448,933,958 29.6% $209,676,685,922 29.4%

10

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 25/219

4.2 Coastal Economy Growth 2003-2006

Florida experienced large economic growth rates from 2003-2006 despite this short timeperiod. The smallest changes were seen in employment, with the Atlantic Coast at 8.8%and the Gulf Coast at 9.8%, compared to the Florida state overall growth of 10% (shownin table 4.4). Combined, shoreline counties lagged the overall state growth trends

somewhat, reflecting both the mature economies of the urban coastal areas and continuedstrong growth in central Florida around the Orlando area. However, the Gulf of Mexicoshoreline counties did show somewhat faster growth than the state rates.

Table 4.4 Florida Regional Coastal Economy 2003-2006

% Change 2003-2006

Establishments Employment Wages GDP

Florida Total 17.36% 10.07% 14.51% 17.47%

Shoreline Total 16.16% 9.22% 13.91% 16.91%

Atlantic Shoreline 13.76% 8.83% 13.43% 16.26%

Gulf Shoreline 20.20% 9.81% 14.71% 18.01%

4.3 Economic Growth at the County Level 2003-2006

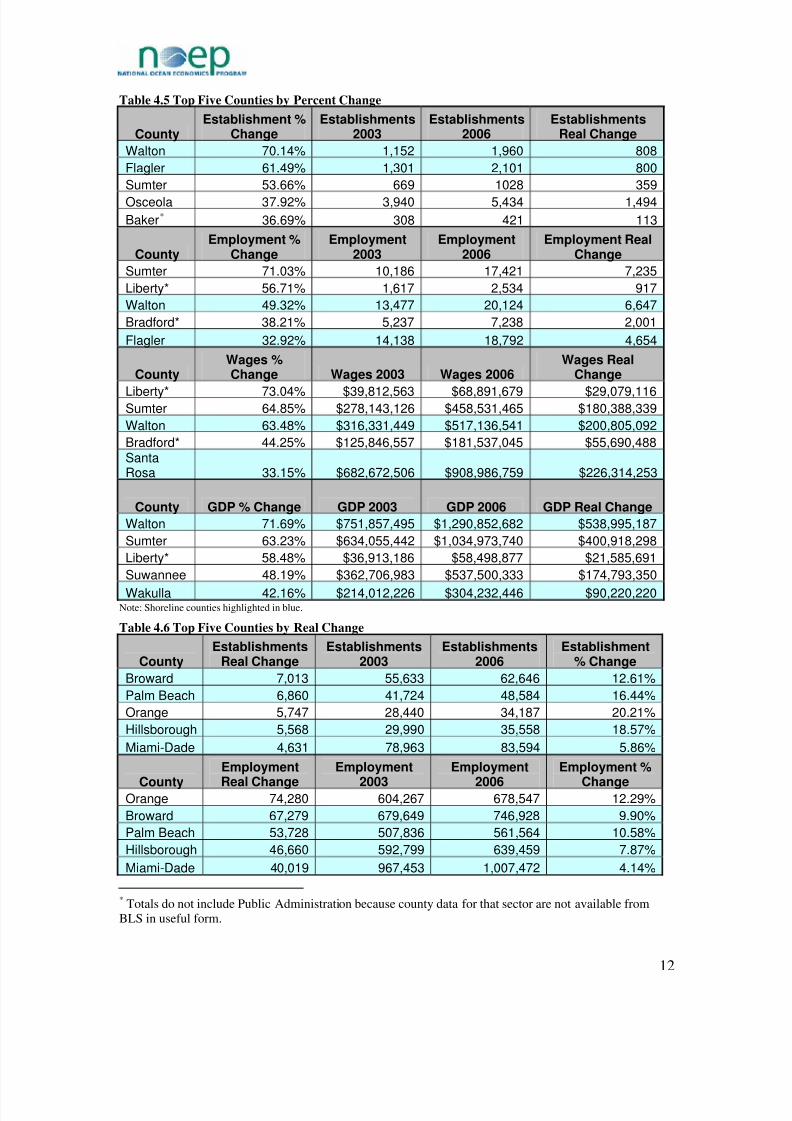

At the county level, growth over 2003-2006 was uneven. Although state numbers showgreater growth inland, more individual shoreline counties ranked among the top counties,in particular by real change, while more inland counties ranked among the bottomcounties (tables 4.5 through 4.8). While this is the case, the actual change and percentchange helps to identify the overall impact throughout the state for growth in bothshoreline and inland counties. Without an indication of what the actual change or baselinefor change is, percent change can not tell a complete story. For instance, differentshoreline counties rank highest in growth when measured by percent change or by realchange (tables 4.5 and 4.6). This demonstrates that while more significant changes areoccurring in shoreline counties such as Flagler, Santa Rosa, Wakulla, and Walton(reflected in percent change), strong growth is still occurring in major shoreline countiessuch as Broward, Hillsborough, Miami-Dade, and Palm Beach (reflected in real change).While these latter counties do not rank high in percentage change, their real growth ishigh because they are some of the largest economic producers in the state, and anysignificant growth will produce the largest real change in value. On the other hand, inlandcounties such as Sumter, Liberty, and Baker counties have relatively small contributionsto the overall state economy. However, growth in these inland counties has beenconsistently strong when measured by percent change, and these are some of the fastestgrowing counties in the state. This county comparison helps to explain why inlandcounties are showing a stronger percent change in state data than the shoreline; thecoastal region consists of matured economies which, while contributing more to theoverall state economy, show less growth than inland counties. Even though the inlandcounties contribute less to the state economy, they exhibit larger percent change.

11

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2

http://slidepdf.com/reader/full/floridas-ocean-and-coastal-economies-report-phase-2 26/219

Table 4.5 Top Five Counties by Percent Change

CountyEstablishment %

ChangeEstablishments

2003Establishments

2006Establishments

Real Change

Walton 70.14% 1,152 1,960 808

Flagler 61.49% 1,301 2,101 800

Sumter 53.66% 669 1028 359

Osceola 37.92% 3,940 5,434 1,494

Baker* 36.69% 308 421 113

CountyEmployment %

ChangeEmployment

2003Employment

2006Employment Real

Change

Sumter 71.03% 10,186 17,421 7,235

Liberty* 56.71% 1,617 2,534 917

Walton 49.32% 13,477 20,124 6,647

Bradford* 38.21% 5,237 7,238 2,001

Flagler 32.92% 14,138 18,792 4,654

CountyWages %Change Wages 2003 Wages 2006

Wages RealChange

Liberty* 73.04% $39,812,563 $68,891,679 $29,079,116Sumter 64.85% $278,143,126 $458,531,465 $180,388,339

Walton 63.48% $316,331,449 $517,136,541 $200,805,092

Bradford* 44.25% $125,846,557 $181,537,045 $55,690,488SantaRosa 33.15% $682,672,506 $908,986,759 $226,314,253

County GDP % Change GDP 2003 GDP 2006 GDP Real Change

Walton 71.69% $751,857,495 $1,290,852,682 $538,995,187

Sumter 63.23% $634,055,442 $1,034,973,740 $400,918,298

Liberty* 58.48% $36,913,186 $58,498,877 $21,585,691

Suwannee 48.19% $362,706,983 $537,500,333 $174,793,350

Wakulla 42.16% $214,012,226 $304,232,446 $90,220,220Note: Shoreline counties highlighted in blue.

Table 4.6 Top Five Counties by Real Change

CountyEstablishments

Real ChangeEstablishments

2003Establishments

2006Establishment

% Change

Broward 7,013 55,633 62,646 12.61%

Palm Beach 6,860 41,724 48,584 16.44%

Orange 5,747 28,440 34,187 20.21%

Hillsborough 5,568 29,990 35,558 18.57%

Miami-Dade 4,631 78,963 83,594 5.86%

County

Employment

Real Change

Employment

2003

Employment

2006

Employment %

ChangeOrange 74,280 604,267 678,547 12.29%

Broward 67,279 679,649 746,928 9.90%

Palm Beach 53,728 507,836 561,564 10.58%

Hillsborough 46,660 592,799 639,459 7.87%

Miami-Dade 40,019 967,453 1,007,472 4.14%

* Totals do not include Public Administration because county data for that sector are not available fromBLS in useful form.

12

8/9/2019 Florida's Ocean and Coastal Economies Report Phase 2