fm blbs059-engle june 11, 2010 14:14 trim: 246mm x 189mm printer name ... economics and...

TRANSCRIPT

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

Aquaculture Economics andFinancing

Management and Analysis

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

Aquaculture Economics andFinancing

Management and Analysis

Carole R. EngleAquaculture/Fisheries Center

University of Arkansas at Pine Bluff

A John Wiley & Sons, Ltd., Publication

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

Edition first published 2010C© 2010 Carole R. Engle

Blackwell Publishing was acquired by John Wiley & Sons in February 2007. Blackwell’s publishing program has beenmerged with Wiley’s global Scientific, Technical, and Medical business to form Wiley-Blackwell.

Editorial Office2121 State Avenue, Ames, Iowa 50014–8300, USA

For details of our global editorial offices, for customer services, and for information about how to apply for permission toreuse the copyright material in this book, please see our Website at www.wiley.com/wiley-blackwell.

Authorization to photocopy items for internal or personal use, or the internal or personal use of specific clients, is granted byBlackwell Publishing, provided that the base fee is paid directly to the Copyright Clearance Center, 222 Rosewood Drive,Danvers, MA 01923. For those organizations that have been granted a photocopy license by CCC, a separate system ofpayments has been arranged. The fee code for users of the Transactional Reporting Service is ISBN-13:978–0-8138–1301-1/2010.

Designations used by companies to distinguish their products are often claimed as trademarks. All brand names and productnames used in this book are trade names, service marks, trademarks or registered trademarks of their respective owners. Thepublisher is not associated with any product or vendor mentioned in this book. This publication is designed to provideaccurate and authoritative information in regard to the subject matter covered. It is sold on the understanding that thepublisher is not engaged in rendering professional services. If professional advice or other expert assistance is required, theservices of a competent professional should be sought.

Library of Congress Cataloging-in-Publication Data

Engle, Carole Ruth, 1952–Aquaculture economics and financing : management and analysis / Carole R. Engle. – 1st ed.

p. cm.Includes bibliographical references and index.ISBN 978-0-8138-1301-1 (pbk. : alk. paper) 1. Aquaculture industry. 2. Aquaculture–Economic aspects.

3. Aquaculture–Finance. I. Title.HD9450.5.E53 2010338.3–dc22

2010013917

A catalog record for this book is available from the U.S. Library of Congress.

Set in 9.5/11.5 pt Times by Aptara R© Inc., New Delhi, IndiaPrinted in Singapore

1 2010

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

This book is dedicated to my parents, Mildred Evelyn Orris Engle Wambold,Glenn Wambold, and Morris Engle, Jr.; my husband, Nathan Stone;

our children Reina, Eric, and Cody; andto the fish farmers of Arkansas.

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

Contents

Preface ix

Acknowledgments xi

I Managing Aquaculture Businesses 1

1 Starting an Aquaculture Business 3

2 Marketing Aquaculture Products 13

3 Developing a Business Plan for Aquaculture 23

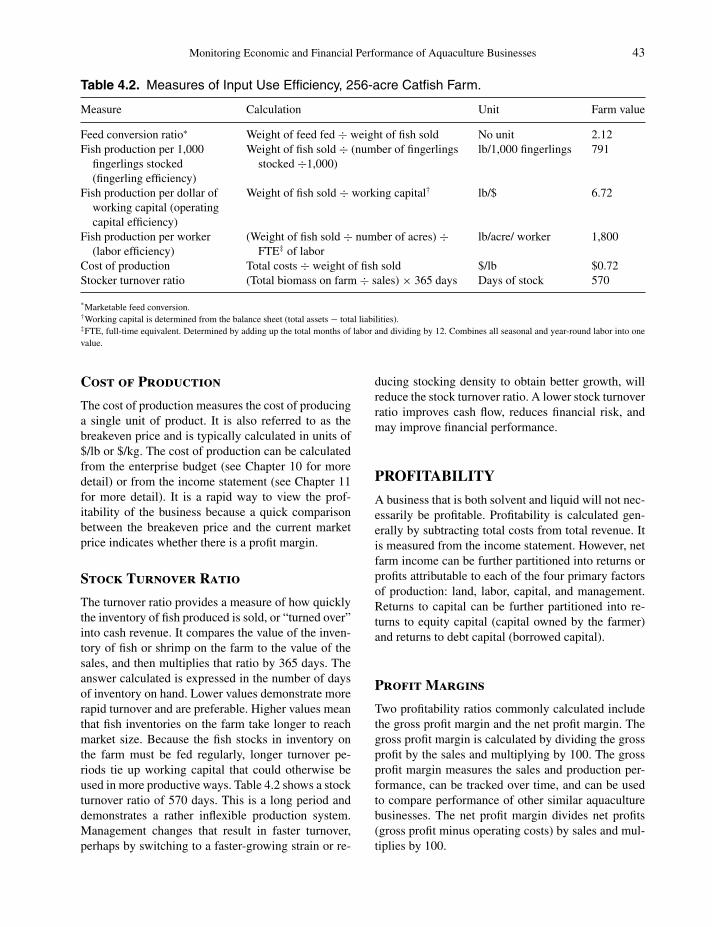

4 Monitoring Economic and Financial Performance of Aquaculture Businesses 41

5 Financing an Aquaculture Business 57

6 Managing Cash Flow 67

7 Managing Capital Assets in Aquaculture Businesses 81

8 Managing Risk in Aquaculture Businesses 93

9 Managing Labor 105

II Economic and Financial Analysis of Aquaculture Businesses 115

10 The Enterprise Budget and Partial Budgeting in Aquaculture 117

11 Financial Statements: Balance Sheet and Income Statement in Aquaculture 131

12 Cash Flow Analyses in Aquaculture 143

13 Investment Analysis (Capital Budgeting) in Aquaculture 159

14 Lending in Aquaculture 173

vii

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

viii Contents

III Research Techniques to Analyze Farm-Level Decision-Making 183

15 Use and Misuse of Enterprise and Partial Budgets 185

16 Risk Analysis in Production Aquaculture Research 197

17 Whole-Farm Modeling of Aquaculture 207

18 Managing Government Policies and Regulation in Aquaculture Businesses 219

Bibliography 231

Webliography 235

Glossary 241

Index 255

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

Preface

The volume of aquaculture production worldwide hasgrown at a rate of approximately 8% per year overthe last decade. Continued growth is expected due toincreases in world population and the apparent lev-eling off of the capture of many commercial fish-eries species. Farmed salmon and shrimp productionhave grown to dominate their respective world mar-kets over the last several decades. More recently, newglobal markets have emerged for farmed species suchas tilapia (Oreochromis sp.), channel catfish (Ictaluruspunctatus) and the basa/tra species (Pangasius sp.).Continued growth, however, depends not just on de-mand but also on the economic and financial viabilityof the businesses developed.

Aquaculture production presents some unique chal-lenges for economic analysis. While there are manybooks that address the theory and methodology of eco-nomic and financial analysis, there are few that presentclear details on applications to aquaculture businesses.The few that do are quite general in nature and rely onhypothetical examples that omit the often-messy de-tails of the real world. The difficulties posed by aqua-culture businesses are rarely discussed or addressed.The problem is exacerbated by the lack of practicalknowledge and experience in aquaculture on the partof many economists. Simplifying assumptions makeanalyses more tractable, but too often obscure the prob-lems and challenges faced by those attempting to makea living from aquaculture.

As a result, researchers who wish to add an eco-nomics component to a production aquaculture trialhave little guidance. The unfortunate result is that keycosts are too often ignored, invalid assumptions aremade, and analytical tools are applied incorrectly.These errors degrade the quality of the work and maylead to erroneous or misleading conclusions.

The intent of this book is to provide a detailed andspecific set of guidelines for both aquaculture busi-nessmen and women and researchers related to the use

of economic and financial analysis of aquaculture. Thegoal of the book is to remove the mystery or “voodoo”from economic analysis as it is applied to aquacultureand to provide a guide for its accurate application.

This book discusses key issues related to bothfinancing and planning for aquaculture businesses,how to monitor and evaluate economic and financialprogress, and how to manage the capital, labor, andrisk in the business. The book works through the spe-cific application of farm management and financialanalysis tools for aquaculture. Particular attention ispaid to those line items and valuation methods thatare most often confused or in error in aquaculture. Asection on use and misuse of budgeting techniques inresearch should assist aquaculture researchers to avoidcommon mistakes. Additional chapters on risk analy-sis and whole-farm modeling provide a sense of moreadvanced techniques and their applicability. Finally,a chapter on managing government regulations pro-vides guidance for adjusting to an increased numberof regulatory activities.

The book is based entirely on aquaculture examplesand literature with an emphasis on farm-level data andanalysis. It is written in terminology that aquacultureresearchers and business persons will readily followand understand. The section on the application of eco-nomic analysis in aquaculture research is unique; noother book outlines how to value parameters measuredin aquaculture field trials.

The book includes a specific, detailed example ofa practical application in each chapter. A section onother applications in aquaculture is included to paint abroad picture of the economics of aquaculture aroundthe world while providing comprehensive guidance oneach particular topic.

The three principal audiences for this book are: (1)aquaculture business owners and managers; (2) thosewho conduct research on aquaculture production sys-tems, strategies, equipment, or management practices;

ix

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

x Preface

and (3) students preparing for careers either in the in-dustry or in aquaculture research. The book shouldappeal to practitioners in a number of different coun-tries, but especially those with aquaculture industries.

Aquaculture business owners and managers willlikely be most interested in Section I: Managing Aqua-culture Businesses. The chapters in this section are de-signed for those who are likely to hire an accountant todevelop the analyses, but need to know what questionsto ask and how to interpret the answers. This sectionworks through the key questions related to starting anaquaculture business, some basic marketing consider-ations, business planning, understanding how to inter-pret the financial statements prepared by accountantsfor businesses, cash flow, financing, and managementof capital assets, labor, and risk. The key focus in thissection is on the use of information to make man-agement decisions. Those aspects of aquaculture busi-nesses that are unusual or different from other typesof businesses are emphasized from the perspective ofmanaging the business effectively for profit. Chapter18 on managing government policies and regulationswill also be of interest to aquaculture business owners.

Section II, Economic and Financial Analysis ofAquaculture Businesses, is for students and thosewho wish to understand the details of how to develop

and complete the various types of economic analysesthat are commonly used in the economic analysisof aquaculture. Each chapter presents in detail themechanics and methodology for developing enterprisebudgets, partial budgets, balance sheets, income state-ments, cash flow budgets, and investment analyses.Challenges and common pitfalls associated with useof each of these methodologies are discussed in eachchapter.

Section III, Research Techniques to Analyze Farm-Level Decision-Making, is written especially for thosewho conduct research on aquaculture production sys-tems, strategies, equipment, or management prac-tices. Misleading assumptions, omitted costs, over-estimating revenues, and misapplication of researchdata can be common in economic analysis based onaquaculture research. This section reviews these chal-lenges and describes detailed approaches to developingaccurate economic analyses with production researchdata.

The book includes an annotated bibliography and awebliography of resources. Software products avail-able for economic and financial analyses are listed anddescribed. It is my hope that you will find this bookuseful and that it will help aquaculture businesses tobe efficient, viable, and profitable.

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

Acknowledgments

There are many people who contributed either directlyor indirectly to the content of this book. Some of thismaterial was drawn from earlier training programsdeveloped with the assistance of Diego Valderrama,Steeve Pomerleau, and Ivano Neira. Ganesh Kumarhas provided invaluable assistance throughout. In-sightful and useful review comments were provided

by Diego Valderrama, Anita Kelly, Madan Dey, andGeorge Selden. Umesh Bastola, Pratikshya Sapkota,and Abed Rabbani also provided suggestions. Finally,fish farmers throughout Arkansas and other statesprovided the continuous ground truthing of theeconomics and financing of aquaculture.

xi

P1: SFK/UKS P2: SFK/UKS QC: SFK/UKS T1: SFK

fm BLBS059-Engle June 11, 2010 14:14 Trim: 246mm X 189mm Printer Name: Yet to Come

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

Section IManaging Aquaculture Businesses

INTRODUCTION TO SECTION I:MANAGING AQUACULTUREBUSINESSES

This section focuses on the use and application of eco-nomic tools and interpretation of their results. It isdesigned primarily for owners and managers who hireothers to prepare financial statements and analyses. Atthe same time, those who are trained to conduct eco-nomic and financial analysis but who are not familiarwith aquaculture should also find this section useful.

Aquaculture is a management-intensive business.The need for intensive and skilled management stemsfrom the high level of capital invested in the facil-ities, and in the high levels of operating capital re-quired to operate a competitive and profitable business.Throughout aquaculture, undercapitalization (not hav-ing enough capital to make payments and survive the

sometimes lengthy startup periods) has been a consis-tent problem.

Individual companies must answer a series of ques-tions that involve pricing, output, and market posi-tioning. Key questions that the manager must answerinclude: (1) how much should be produced; (2) howmuch input should be used; (3) what is the optimalsize of the business; (4) how should cash flow be man-aged; (5) how should risk be managed; (6) how will thebusiness be financed; and (7) how can business perfor-mance be optimized? Thus, it is the manager who mustdevelop the business plan, monitor economic and fi-nancial performance of the business, and manage cash,capital, labor, and risk. Each of the following chaptersdiscuss specific aspects of the types of managementfunctions and decisions that need to be made by themanager.

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

1Starting an Aquaculture Business

Aquaculture has grown rapidly in volume and in com-plexity around the world in the last several decades.While aquaculture has a centuries-long history as asource of food for households in Asia and Africa, themost dramatic change in more recent years has beenthe development of aquaculture businesses into com-plex industries. These industries operate on nationaland international levels.

Development of efficient and viable businesses re-quires careful evaluation and thorough planning for thenew business. This book presents details on the pro-cess of business planning (see Chapter 3) as well ason how to prepare the various types of financial state-ments needed for thorough planning (see Chapters 10through 14). Chapter 1 begins by outlining steps to beconsidered before starting the business.

The new business owner must think carefully aboutwhat will set his or her business apart, both from otherexisting businesses and from other future businesses. Itis critical to identify the strengths, abilities, and skillsowned and available that will help the farm owner tobe successful. This chapter discusses the motivationand goals for starting an aquaculture business, andthe capital- and management-intensive nature of aqua-culture. Marketing challenges and trade-offs associ-ated with various organizational structures, financing,and the availability of resources are contrasted. It con-cludes with a discussion of permits, regulations, andsources of assistance. Figure 1.1 illustrates the varioussteps that will be needed to start a successful aquacul-ture business.

MOTIVATION AND GOALS

The first step to starting an aquaculture business is tocarefully consider one’s goals and motivation. An in-

dividual interested in starting an aquaculture businessmust fully understand why he or she wants to do this.Some individuals enjoy working outdoors with fish anddislike office work and paperwork. These individualsmay do an admirable job like raising fish on the farm.However, inadequate attention to the business aspectsof the aquaculture business will result in financial fail-ure. If the owner spends all his or her time caring forthe fish, who will take care of the permits, regulations,financial statements, and economic performance of thebusiness?

Others who wish to start an aquaculture businessmay view it as a way to make a great deal of money.There certainly are success stories of aquaculture busi-nesses that have become profitable businesses. How-ever, aquaculture businesses are intensive businessesthat require management committed to working longhours under often difficult conditions. Who will pro-vide that level of management?

Still others view aquaculture as the wave of the fu-ture and want to get in on the ground floor. However,businesses developed to raise the latest “hot” specieswith the newest production technology frequently arebeset with substantial levels of financial, price, andyield risk. Aquaculture entrepreneurs must be preparedto manage the degree of risk associated with their busi-ness model and plan.

It is important to develop clear and specific goals forthe business from the beginning. For example, what isadequate revenue for one individual may not be suf-ficient to entice another to invest the necessary timeand money. The effects of starting a new business onthe farmer’s family must be considered carefully. Willfamily members be supportive and helpful or will theyresent the time that must be invested in the business?The early years of an aquaculture business may gener-ate minimal revenue, and the family may be requiredto live for a time on reduced income.Aquaculture Economics and Financing: Management and

Analysis, Carole R. Engle, C© 2010 Carole R. Engle.

3

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

4 Managing Aquaculture Businesses

Assess available resources, strengths, and weaknessesSelect production system and species to raise

Find

Markets

Financing

Management

Develop a detailed business plan:

• Marketing plan• Organizational and management plan• Labor plan• Financial plan

Acquire permitsDevelop support network

Construct facilitiesInitiate production

Figure 1.1. Starting an aquaculture business.

AQUACULTURE IS ACAPITAL-INTENSIVE BUSINESS

The majority of aquaculture businesses require sub-stantial amounts of both operating and investmentcapital. One of the largest problems encountered instarting an aquaculture business often is to acquire suf-ficient capital. Undercapitalized farms and processingplants rarely survive. Careful thought and planningneed to go into determining the amount of capitalneeded to operate at an efficient level and to identi-fying sources for the needed capital.

Capital requirements begin with the investment cap-ital needed to purchase land, build production facili-ties, and purchase equipment. Depending on the spe-cific location, new roads may need to be constructed,electric power lines may need to be installed, or theremay be additional infrastructure required that will in-crease the total amount of investment capital needed.Capital required for marketing facilities must be in-cluded in the planning. Is a shed needed to hold, grade,and sell the fish? If so, a water supply system to fillhauling trucks will also be required. Perhaps an icemachine is required, depending on the form of theproducts sold. If the farm will do its own hauling and

transportation, then the trucks, tanks, oxygen systems,and loading equipment will also be needed. In all, in-vestment capital for an aquaculture business typicallywill be several thousand dollars an acre of produc-tion for pond systems, and can range from $0.30 to$7.00/lb across the many different types of speciesand production systems. More information on invest-ment capital requirements can be found in Chapter 10,and techniques to measure the profitability of such aninvestment can be found in Chapter 13.

The high level of investment capital required for anaquaculture business results in high levels of annualfixed costs (see Chapter 10 for more details on whatconstitute annual fixed costs). The best way to reducethe fixed cost portion of the cost of producing fishis to produce at an intensive level with high yields.High yields spread the annual fixed costs over a greaterlevel of production and lower the cost per pound ofproduction.

Operating capital requirements often are as substan-tial as investment capital requirements for aquaculturebusinesses. Frequently, this is because high yields areneeded to lower the per-pound annual fixed costs andkeep production costs at a competitive level. Achievinghigh yields requires high numbers of fingerlings, largeamounts of feed, greater electricity for aeration, andcorresponding amounts of other inputs such as labor,repairs and maintenance, and fuel. Operating costs fre-quently can be $2,000–$5,000/acre for pond systemsand $33,000–$150,000/acre for intensive systems suchas raceways and indoor systems.

Operating cost requirements are compounded by thefact that some types of fish raised do not reach marketsize in one growing season. Thus, the prospective fishfarmer often must prepare to operate the business formore than a year without receiving revenue from thebusiness. Careful financial planning and good commu-nication with one’s banker are keys to having accessto sufficient amounts of capital with which to build thebusiness until it reaches its full production capacity.

The high levels of capital required for many aquacul-ture businesses result in substantial amounts of finan-cial risk (see Chapters 8 and 16). The profit potential isoften accompanied by a variety of risks, and the largesums of money invested in an aquaculture businesscan be lost quickly. The best method to prevent suchlosses is adequate and thorough planning, monitoring,and assessment of the economics and finances of theaquaculture business throughout its life. If the owner isnot willing to spend the time to monitor the business’financial performance, then it is essential to hire or

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

Starting an Aquaculture Business 5

retain an expert to keep a constant and close eye on itseconomic aspects. Otherwise, the likelihood of failureand severe financial losses is high.

AQUACULTURE IS AMANAGEMENT-INTENSIVEBUSINESS

The high levels of investment and operating capital re-quired in aquaculture businesses, along with the inten-sive nature of production of aquatic animals requiresa high degree of management. When aquatic animalsare confined in a production unit, constant attentionis needed to the quality of the growing conditions forthe fish. Maintaining adequate levels of oxygen andother critical water quality parameters, and prevent-ing problems associated with the breakdown of wasteproducts in the system, takes careful and constantmonitoring. Diseases spread rapidly when animals aremaintained in close confinement. Thus, attention mustbe paid to monitoring the health of the animals andtaking necessary actions when there are indications ofdisease.

Marketing and sales of aquatic products can repre-sent management challenges depending upon the na-ture of the target market. Farms engaged in direct saleswill require a great deal of management attention tomarketing functions and activities. Even farms thatsell directly to a processing plant must have managerswho pay close attention to the requirements of pro-cessors. These requirements include quality standardsand delivery requirements, among others, to minimizedockages from fish that do not meet specifications.Top managers ensure that their farm is considered tobe a preferred supplier, one that consistently deliversquality fish, within specification, and on time.

Management must keep a close eye on costs andproduction efficiencies throughout the production pro-cess. This includes monitoring the efficiency of labor,feed usage, use of electricity and fuel, and use andcare of equipment. Feed, for example, is frequentlythe largest single component of the cost of raising anaquaculture crop. Feeding carefully and appropriatelywill ensure a better feed conversion ratio and will re-sult in more pounds of fish produced per pound offeed applied. Similarly, judicious use of aeration canprovide adequate oxygen levels by turning aerators onsequentially, as needed, rather than turning on moreaerators than are needed at one time. Taking time tokeep equipment well maintained and to ensure that itis operated correctly will reduce the costs of repairs

and will extend its life. This will reduce the cost ofequipment as a percentage of the total cost of produc-tion.

Moreover, the manager must be able to think andplan strategically. Preparing to stay ahead of fu-ture challenges requires examination of the business’sstrategic plan from a variety of different perspectives.

MARKETING CHALLENGES

Many individuals who wish to start an aquaculturebusiness are captivated by the animals and plants thatthey wish to raise and will spend many hours talkingabout their biology and growing requirements. How-ever, the marketing challenges of starting a new aqua-culture business often are greater than the productionchallenges and ultimately more important. Successfulaquaculture businesses are managed and owned by in-dividuals who spend as much time exploring marketingoptions and trends as they do working on productionefficiencies. Chapter 2 of this book discusses market-ing issues and strategies related to aquaculture prod-ucts in greater detail and Chapter 3 outlines steps inthe development of marketing plans as part of an over-all business plan. This chapter discusses some generalconcepts.

There are a number of overarching trends and chal-lenges that prospective aquaculture business ownersshould consider. Most species that are being aquacul-tured at one time were primarily a wild-caught species.Many of these species have existing markets and de-mand that were based originally on supply from cap-ture fisheries. Preferences for wild-caught as comparedto farmed fish vary by region. Care must be taken to un-derstand these preferences in the market targeted forthe business’s product. As farmed product becomesavailable in the market, it frequently must competewith wild-caught product that is already well estab-lished in the market. However, the cost of producingfarmed fish, especially in the early years of startupbusinesses, requires a price that often is higher thanthat of wild-caught fish. To establish a new product inthe market often requires differentiating it from wild-caught and other similar products to capture a pricethat will cover production costs.

The seafood market has undergone dramaticchanges in the last several decades. The possible ef-fects of current and emerging trends must be consid-ered carefully in planning for successful marketingprograms. Seafood in earlier decades was primarilya locally sourced, fresh product supplied by either

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

6 Managing Aquaculture Businesses

fishermen or specialized jobbers and small-scalewholesalers. Changes in packaging and freezing tech-nologies have opened the door for global trade inseafood that has continued to increase dramatically.The increase in global trade in seafood has resultedin a number of conflicts and competition with fishraised domestically. All types of fish and seafoodare now shipped around the world to satisfy variousmarkets.

Dynamic markets like those for seafood, while chal-lenging, can also offer opportunities for entrepreneurs.For example, the shrimp and salmon industries world-wide have benefited from the increase in global tradeand technology. These segments of aquaculture havegrown to dominate shrimp and salmon markets world-wide.

Food marketing in general has undergone dramaticchanges in recent decades that have resulted in changesalong the supply chain. The driving force has beenthe emergence of strong market power at the levelof the large hypermarket discount retail sector, exem-plified by companies like Wal-Mart. In response tothis concentration of market power, wholesalers andfood service distributors have also become more con-centrated. This has increased pressure on growers toeither consolidate by integrating vertically to capturemarket power, or to form cooperative or other formsof organizations to be able to compete.

Startup aquaculture businesses must identify thespecific market that the business plans to target. Theoverall marketing plan (see also Chapter 3) must alsoidentify the competition and the unique position thecompany’s product will occupy in the market. Theproduct must be defined well and must match the wayit is positioned in the market for the targeted customers.Careful attention should be paid to the size of the mar-ket, long-term price trends, and distribution patternsof similar products.

The marketing plan must lay out an effective pro-motion and advertising plan. Even the smallest-scaleaquaculture farms must have a plan to spread the wordabout their products. Promotion is a way to transmit in-formation about the attributes of the product, the price,and why the consumer should purchase it.

Appropriate and effective market channels must bedeveloped. Is the farmer planning to transport all thefish produced to the various markets? The amount oftime needed to transport fish to markets must be deter-mined and adequate personnel included in the businessplan. The length of round trips that can be undertakenfeasibly can be an important factor. If the farmer doesnot intend to transport his or her own fish, relationships

and agreements will be needed with a wholesaler ordistributor.

ORGANIZATIONAL STRUCTUREFOR THE AQUACULTURE BUSINESS

Most farms in the United States have a single ownerand are classified as sole proprietorships. In a soleproprietorship, the farmer is self-employed and haslegal title to the property. This is the simplest form ofbusiness structure, but it also entails the greatest risk.Risk results from the liability for any debt obligationsor accidents that falls entirely on the owner in a singleproprietorship. Moreover, the liability is not limitedto what the farmer has invested in the business. Thefarmer can lose his or her land and home as a result ofsevere adverse situations.

Some farmers form partnerships with family mem-bers or others to gain access to additional resourcessuch as land, equipment, labor, or management. Part-nerships can be either general or limited. Partners sharein all ownership, management, and liability in a generalpartnership. Limited partners share in the profits andlosses of the business but not in the management. Inthis way, the limited partner provides resources suchas capital, but management decisions are under thecontrol of the principal owner.

Some segments of aquaculture have integrated verti-cally and have developed into corporations. In a corpo-ration, capital is provided by shares of stock, and themanagement and control are provided by the stock-holders, the board of directors, and the officers. Theboard sets policies, and the officers manage the dailyactivities of the company. Stockholders, while ownersof the company, are not personally liable for actionsof the corporation. Their liability is limited to theirinvestment in stocks.

There are also subchapter C and subchapter S cor-porations. With C corporations, dividends received bystockholders are taxed as income, while S corporationsare taxed as limited partnerships. The officers are paidbefore the remaining profits are distributed.

AVAILABLE RESOURCES

An important step in starting an aquaculture businessis to develop a frank assessment of the resources avail-able for the business. New businesses fail more oftenthan they succeed, often due to the lack of adequateresources. The assessment of available resources be-gins with the individual. The owner must be inno-vative, persistent, resourceful, and determined to find

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

Starting an Aquaculture Business 7

solutions to the many problems that will arise. Theassessment should extend to physical resources avail-able that include land, existing ponds, wells or othertypes of water supply, farm equipment, and buildings.The assessment must be thorough and detailed. Forexample, the individual may have an adequate quan-tity of land available, but current or impending zoningregulations may prohibit its use for aquaculture. Waterand soil analyses should be done to check the suitabil-ity for the species to be considered. Some freshwatershave enough salinity to consider some crops like ma-rine shrimp that can tolerate low levels of salinity.There must also be adequate backup equipment in theevent of breakdowns, generators for power outages andbackup aeration equipment. Resources also include theavailability of adequate quantities of seedstock.

The availability of labor resources can be an impor-tant factor in the success or failure of a new business.The assessment of labor availability should include anyfamily labor that is available to assist with the farm.A realistic assessment must be made of the local laborsupply and the availability of adequately trained la-bor that can be hired for the aquaculture business. Thetype of labor is also an important consideration. Aqua-culture businesses often require more skill than someother types of agriculture, and the ability of workersto handle the new responsibilities must be evaluatedcarefully. For example, workers who cannot swim orwho are afraid of the water may have difficulty adjust-ing to working around it constantly. Much aquaculturerequires long and irregular hours during the maingrowing season. Workers may or may not be willing towork such hours. The degree of equipment on the farmrequires a great deal of maintenance. An aquaculturebusiness requires either a mechanic hired on the farmor the business must be prepared to have higher repairand maintenance costs.

The availability of management resources must beassessed. The level of expertise and skill of the ownerto manage the production, marketing, and financingof the aquaculture business must be evaluated frankly.If the owner has excellent aquaculture skills but isweak in financial analysis, an appropriate accountantor financial analyst will need to be hired, contracted,or retained. Similarly, if the owner has good businessskills in marketing and financing, but lacks experiencein culturing aquatic animals, hiring a production man-ager with adequate aquaculture skill and expertise willbe essential.

Sufficient capital resources must be available aswell. Both investment and operating capital are re-quired in necessary quantities to be received at ap-

propriate times. The operating line of credit must bestructured to continue the business throughout the en-tire startup period during which the business beginsto generate returns. Depending on the type of busi-ness, this may be a period of 2–3 years before sub-stantial revenue can be generated from the aquaculturebusiness. The investment capital must be available insufficient quantities to provide facilities to minimizerisk. This includes sufficient redundancy in equipmentto cover power outages, breakdowns, and unantici-pated extended periods of adverse weather conditions.Maintenance requirements must be accounted for infinancial planning. This includes the capital to be ableto replace all equipment and facilities when necessary.

The availability of adequate credit will depend inpart on the ability of the owner to finance the opera-tion through equity or to have the credit capacity toborrow the necessary amounts of capital. This in turnwill depend upon the individual’s balance sheet, avail-ability of collateral, and overall credit worthiness.

The particular species selected and their productforms are critical decisions. These must match theprojected price point and the quantity demanded forthat product form for that species. In selecting thespecies to be raised, thought must be given to whetherthere is competition from imported species or capturefisheries, or both. Diversifying farm production withseveral species also serves to spread the market risk ofprice downturns for one specific species.

The key to starting a successful aquaculture busi-ness is to match the species to be produced, the pro-duction system to be used, and the scale and scopeof operation with the available markets and resources(labor, land, capital, and management). Mismatchesare likely to result in business failure. For example, aparticular species and production system may exhibitstrong economies of scale. If the owner is unlikely tobe able to acquire sufficient capital to construct andoperate a farm of a large size, it is better to rethink thebusiness plan to develop one that is workable with thecapital resources available. Undercapitalization is of-ten a major reason for failure of aquaculture farms andprocessing plants. Mismatches between projected andactual capital requirements result in financial failure.

FINANCING

Adequate financial resources are essential to a suc-cessful business, and the ability to acquire sufficientcapital is a key factor. One of the first steps is to identifythe sources of capital that are available. Venture cap-ital can be difficult for aquaculture and often follows

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

8 Managing Aquaculture Businesses

certain patterns and trends that may not always favorfinancing aquaculture businesses. Private capital frompartners, whether active or silent, can be considered inestablishing the business. However, private lenders fi-nance most aquaculture businesses. Many lenders maybe skeptical about aquaculture and view it as a riskybusiness. Perceptions of high risk in aquaculture maylead to less favorable terms of lending, requirementsfor greater owner equity in the business, higher inter-est rates, or refusal to consider loans for aquacultureventures.

Financing from private lenders can also be com-plicated by the fact that many lenders may not havesubstantial experience with aquaculture. Lack of fa-miliarity with the business can result in unwillingnessto assess business loan proposals; the loan officer maynot be comfortable with the estimates of yields, costs,or efficiency measures that form the basis of the pro-posal. It may be necessary to spend a great deal oftime working with a lender to help them understandthe basics of aquaculture, introduce them to peoplewho are knowledgeable about successful aquaculturebusinesses and the keys to their success, and to keepthem informed of the most recent trends in aquacul-ture. It is important to plan for adequate capital toprovide for the family through the very difficult earlyyears of the business.

HARVESTING AND PROCESSING

Decisions must be made early on in the developmentof an aquaculture business on how the fish or otheranimals will be harvested and whether they will beprocessed, stored, and transported by the farm busi-ness. If not, these services will need to be contracted.Serious thought needs to be given to the implicationsof these decisions. In areas with little aquaculture pro-duction, these services may not be available. If thefarm owner must hire a seining crew, process the prod-uct, and store and transport it, the owner likely willneed to operate on a relatively large scale. There aresome examples of small-scale aquaculture businessesthat perform these functions, but typically these willrequire a larger scale of business. Processing in par-ticular has substantial economies of scale that must beconsidered before proposing this type of componentto the business.

Product handling throughout transportation and pro-cessing will affect the end quality of the product. Ifproper conditions are not maintained during harvestand transport, the quality of the fillet may suffer. Sim-

ilarly, if processed fillets are not stored or packagedproperly, the result will be a poor quality product. Ad-equate planning for these functions is necessary.

PERMITS AND REGULATIONS

Part of a careful assessment for a startup business in-cludes identifying the permits and regulations that willaffect the new business both currently and in the fu-ture. Chapter 18 discusses the role of regulations andpreparing to manage them in greater detail.

There are a wide variety of types of permits that arerequired in different states, provinces, and countries.These permits may refer to the site, the business, ac-cess to water supplies, discharges, predator control, orprocessing.

All legal and regulatory statutes relevant to the busi-ness must be understood and planned for. Some typesof permits may require lengthy application periods thatmay delay startup of the business.

SOURCES OF HELP

There are a number of sources of help and techni-cal assistance available to the individual consideringa startup aquaculture business. Table 1.1 summarizesseveral types of assistance available. It is advisable todevelop an excellent relationship with these groups.Universities, extension agents, trade associations, anddiagnostic laboratories are all essential sources of sup-port, technical assistance, and help. Joining the rele-vant trade association and inclusion on the mailing listof the local extension office will ensure that the newfarmer receives the latest updates on permits, regula-tions, issues, and research.

Plans must include developing contacts with the lo-cal diagnostic laboratories, pathologists, and techni-cians. Understanding the best way to submit samplesfor diagnosis and training workers in the proceduresrequired will reduce the time to initiate appropriatetreatments.

International sources of help include internationalnetworks that promote aquaculture such as the Net-work of Aquaculture Centres in Asia-Pacific (NACA).A network in Eastern Europe, the Network of Aqua-culture Centres of Central-Eastern Europe (NACEE),similarly promotes aquaculture and provides informa-tion to industry.

In the United States, available help includes per-sonnel of United States Department of Agriculture-

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

Starting an Aquaculture Business 9

Table 1.1. Sources of Help and Assistance for New Aquaculture Businesses.

Type of organization Type of assistance

Extension services Research-based informationDisease and water quality diagnostics laboratories Diagnosis of disease and water quality problemsIndustry trade associations Updates on issues

State Political actionNational Trade journalsInternational NewsSpecies specific Updates on issues, meetingsMultispecies Updates on issues, meetings

Government agencies Information on permits and programsState Information on permits and programsFederal Information on permits and programs

Related industry segments Information on trends, costs, productsEquipment suppliers Information on trends, costs, equipmentFeed manufacturers Information on trends, costs, productsSupply company representatives Information on trends, costs, products, permitsBank Information on financial position and trends

Local government entities Information on trends and permitsChambers of commerce News and local eventsEconomic development offices Business and financial assistance and new programs

Animal Plant and Health Inspection Service/WildlifeServices. Permits are required in the United States tocontrol fish-eating birds. Severe fines and penaltiescan be levied on farmers who have not obtained thenecessary permits. Wildlife Services personnel have avariety of programs to provide assistance in the controlof fish-eating birds and in the process of obtaining thenecessary permits.

Local and state aquaculture associations can be ofgreat help. Subscriptions to aquaculture journals, mag-azines, and newsletters help to keep abreast of currentnews and impending legislation.

Extension professionals are some of the best sourcesof information. These are trained scientists who areskilled in techniques to disseminate information effec-tively. They also have the latest research results at theirfingertips and may offer opportunities for farmers tocooperate in on-farm or verification trials.

Some states and provinces have government officesthat will assist aquaculture growers. Equipment sup-pliers, feed manufacturers, supply company represen-tatives, and restaurant owners can be good sources ofinformation on trends, costs, and market data. Localchambers of commerce, economic development of-fices, and banks can also provide relevant and usefulinformation.

RECORD-KEEPING FORAQUACULTURE BUSINESSES

The intensive nature of successful businesses requiresmanagers to maintain detailed records. Those contem-plating starting an aquaculture business should prepareto spend time to maintain records and to analyze themperiodically throughout the year. This level of man-agement can make the difference between success andfailure.

Records required will include complete records oninput purchases, use, and inventory. Labor and salesrecords that indicate the quantity sold, the price re-ceived, and any dockages incurred with each sale mustbe maintained. The ability to sort records into feedamounts and fish sales by pond or other fish cultureunit will provide the manager with a means to evaluatepond-level performance and relate this back to man-agement changes in that pond. Reports from diagnosticlaboratories on disease incidence by pond will enablethe manager to search for ways to minimize lossesdue to disease. Financial records must be maintainedfor each loan along with depreciation schedules forall equipment in the business. All paperwork relatedto permits and compliance with regulations must bemaintained over time along with all chemical use onthe farm.

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

10 Managing Aquaculture Businesses

Each of the following chapters presents detailedsuggestions on how to organize and use records tomonitor and evaluate farm performance relevant to thetopic discussed in each chapter. Management decisionsmade from detailed farm records will be more effec-tive and have greater positive results over time if basedon detailed historical performance records of the farmbusiness.

PRACTICAL APPLICATION

Throughout this book, each chapter includes an exam-ple of an application of the material presented in eachchapter to the case of a fish farm. To start such a farm,the owner will need to begin to address the criticalissues related to acquiring the necessary managementskills and capital. If the owner is not skilled and expe-rienced in managing a fish farm, it will be necessary torecruit and hire a skilled manager. Careful thought asto how to obtain the capital that will be needed mustbe given from the very beginning. Preliminary contactswith lenders will be necessary to identify those morelikely to loan to fish farmers and to identify the levelsof lending that each bank can provide.

Decisions related to the overall structure of the busi-ness can affect the supply of capital available forthe fish farm. Developing a partnership or joint ven-ture with a friend or family member can provide asource of capital. The overall financial plan needsto detail the capital that will be available from theowner and any partners and how much will need to beborrowed.

Marketing decisions also will need to be made earlyon in the planning process for the business. Overviewsof the market for that particular business and analysisof its position in the market can be important. Therest of this book provides details of each componentand analysis that is required to start and maintain asuccessful aquaculture business.

OTHER APPLICATIONS INAQUACULTURE

Engle and Valderrama (2001) developed a trainingmanual designed to assist shrimp growers to beginto develop business plans. The Engle and Valder-rama (2001) document emphasizes the financial state-ments needed for a comprehensive business plan forshrimp farming in Honduras. A CD is provided withspreadsheet templates to assist those who wish to de-

velop comprehensive business plans for their shrimpoperations. Self-guided tutorials and exercises areincluded.

SUMMARY

Aquaculture businesses should be entered into only af-ter considerable thought and analysis. Greater capital,more intensive labor, and high levels of managementare required to be successful in aquaculture regardlesswhether the business is large or small.

Comprehensive business and marketing planningis necessary. However, other considerations such aseffects on the family, personal motivations, and theavailability of adequate resources must also be ana-lyzed carefully. The remaining chapters in this bookpresent detailed information on the steps needed bothto start up and to maintain a successful aquaculturebusiness.

REVIEW QUESTIONS

1. What types of specific goals must be set whenstarting an aquaculture business?

2. Why is it important to assess one’s motivation toenter into an aquaculture business?

3. Why is aquaculture considered to be a capital-intensive business? Identify some specific exam-ples of the capital requirements for various aqua-culture businesses.

4. Where does financial risk come from?

5. Why is aquaculture considered to be amanagement-intensive business? Give some spe-cific examples for various types of aquacultureproduction.

6. What are some of the marketing challenges in-volved in starting up aquaculture business? Givesome specific examples.

7. What types of resources must be available for dif-ferent types of aquaculture businesses? Pick twodifferent aquaculture production systems and con-trast the differences in resource availability thatwould be required.

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

Starting an Aquaculture Business 11

8. List three types of organizational structures thatcan be used for aquaculture businesses and com-pare the advantages and disadvantages.

9. What are some of the key considerations relatedto financing new aquaculture businesses?

10. What are some sources of help and assistance fornew aquaculture businesses?

REFERENCE

Engle, Carole R. and Diego Valderrama. 2001. Eco-nomics and management of shrimp farms trainingmanual. In: M.C. Haws and C.E. Boyd (eds). Meth-ods for Improving Shrimp Culture in Central Amer-ica. Managua, Nicaragua: Editorial-imprenta, Uni-versidad Centroamericana. pp. 231–261. ( in Englishand Spanish)

P1: SFK/UKS P2: SFK

c01 BLBS059-Engle June 11, 2010 9:22 Trim: 246mm X 189mm Printer Name: Yet to Come

P1: SFK/UKS P2: SFK

c02 BLBS059-Engle June 11, 2010 10:17 Trim: 246mm X 189mm Printer Name: Yet to Come

2Marketing Aquaculture Products

The focus of this book is on the economics and financeof aquaculture businesses. However, an aquaculturebusiness will not be successful without a marketingprogram and plan that is appropriate and workablefor that particular business. This chapter summarizescritical factors involved in identifying and developingmarkets for aquaculture products. For a completediscussion and presentation of marketing aquacultureproducts, readers are referred to Engle and Quagrainie(2006).

THE ESSENCE OF SUCCESSFULMARKETING

The first essential point to understand about market-ing is that marketing is not synonymous with “sales.”A salesman may or may not be a marketer. Success-ful marketing results in sales, but product sales donot always mean that there is a successful market-ing program in place. Aquaculture businesses will notsucceed without a successful marketing program intoday’s food market.

Successful marketing involves development of acomplete plan that is cohesive and meshes seamlesslywith a number of factors. A successful business mustidentify which specific set of customers the businessis seeking to attract and what that group of customerswants to buy. Moreover, the business must find a wayto meet those customers’ wants and needs better thanany other business. The price charged needs to matchthe customers’ expectations in such a way that theybelieve they receive enough value to justify what theypay for the product. This type of price/quality positionfor the product must be at a price point that resultsin a profit for the business. The business’ promotionalstrategy must effectively communicate how the prod-

uct uniquely meets the preferences of the targeted con-sumer groups. Lastly, the aquaculture business mustidentify the most convenient locations for the exchangeof product to occur for their targeted consumer group.These factors must all mesh and function together as asingle company concept to be successful.

The Importance of DemandCharacteristics

Quantitatively measured characteristics of consumerdemand can shed some light on how some of thesefactors interact. Economists measure demand quanti-tatively by regressing the price of a product againstindependent variables that often include the quantitysold of the product, incomes, and tastes and prefer-ences, among others. Economists then use the esti-mated demand relationships to calculate elasticity, theproportional change in quantity demanded in responseto a change in price. Elasticity is important to a discus-sion of markets because, if demand is elastic, an in-crease in price will result in a relatively larger decreasein the quantity demanded, such that total revenue tothe producer will go down. However, with inelasticdemand, the price increase may still result in a lowerquantity demanded, but the quantity response is pro-portionately less than the change in price. When thisoccurs, the total revenue to the grower will increaseas prices increase. Development of specialty marketstypically depends upon inelastic demand to success-fully command the higher prices common in specialtymarkets.

One characteristic of products with inelastic demandis that there are few close substitutes for the prod-uct. After all, if all shrimp sold (imported, domestic,farmed, wild-caught) are identical, why would a buyerpay a higher price for one particular farm’s shrimp?Thus, one key to developing a product for a specialtymarket is to differentiate it from the competition.

Aquaculture Economics and Financing: Management andAnalysis, Carole R. Engle, C© 2010 Carole R. Engle.

13

P1: SFK/UKS P2: SFK

c02 BLBS059-Engle June 11, 2010 10:17 Trim: 246mm X 189mm Printer Name: Yet to Come

14 Managing Aquaculture Business

Product Differentiation andPositioning

Efforts to develop a differentiated product must care-fully consider where the product needs to be positionedin the marketplace. This decision must consider thecosts of production, the competition, consumer per-ceptions of the product, and closely competing prod-ucts. A product-space map (Figure 2.1) can be usedto help make this decision. Products can be positionedas a high-quality and high-priced product or, at theother end of the spectrum, a low-quality and low-pricedproduct. The key is to match consumers’ expectationswith the price. Certain market segments are willing andable to pay high prices for a product that is expectedto be of high quality.

Product positioning reflects the combination of thespecies, product form, packaging, and its price. Anyattribute that adds value, such as a spice package, mari-nade, or the package size, may affect the way a productcan be positioned and how it can be differentiated fromother products.

Aquaculture growers, particularly smaller-scalegrowers, often prefer to target specialty markets be-cause prices frequently are higher. Specialty marketingis a choice to produce a high-quality product to capturea high price. To be successful, the marketer must havea clear understanding of which attributes will entice aconsumer to pay a higher price. Equally important is

Low quality

Lo

w p

rice

High quality

Hig

h p

rice

Lobster

Trout

Jumboshrimp

Freshwaterprawns

Tilapia

Atlanticsalmon

Mackerel

Carp

Bullhead

Frozen crab legs

Refrozenshrimp in grocery

stores

Jumbo shrimp held past shelf life

Figure 2.1. Generalized example of a product-space map with various types of seafood species. The exact positionof a product will reflect not only the species, but product form, size, and handling.

how the specific product embodies those attributes to agreater extent than the competition. Why should some-one pay more for your product? What is it specificallythat uniquely presents the value that the consumer issearching for? Products must be positioned to be dif-ferentiated from other products in such a way that thevalue of the product is worth what the consumer mustpay for it.

Successful products attract competition over time.Other companies will learn to produce similar productsand perhaps extend the product concept and line. Whenthis happens, the product will no longer be unique. Thebusiness needs to be prepared for competition that willcome if the new products are successful. Each productthat becomes established in the market goes through atype of life cycle (Figure 2.2). In the early stages fol-lowing the introduction of product, sales grow rapidlyas customers become aware of the product and begin toexperiment with it. However, at some point, the prod-uct reaches a stage of maturity when it attracts com-petition. The rate of growth of product sales begins toslow as the sales volume reaches a maximum. Productsales then begin to decline. Companies with productsin the maturity stage must begin to either search outnew markets (either new geographic markets or newmarket segments) or begin to develop new products.

The price point of the product as the business haspositioned it in the market must be adequate to covernot just production costs, but marketing costs as well.

P1: SFK/UKS P2: SFK

c02 BLBS059-Engle June 11, 2010 10:17 Trim: 246mm X 189mm Printer Name: Yet to Come

Marketing Aquaculture Products 15

Growth Maturity Decline

Introduction

Time

Fin

anci

al p

erfo

rman

ce

Sales revenue

Figure 2.2. A theoretical diagram of a product life cycle indicating its various stages.

A high price is meaningless if total costs of productionand marketing are higher still. The business will not beprofitable. If the business plan requires the producerto carry out all marketing functions and activities,these costs must be included in the financial analysesof the plan. Marketing costs can be considerable andcan frequently include the costs of hauling live fishor transporting processed fish, off-flavor checking,marketing equipment such as baskets, dip nets, andoxygen systems, supplies like ice and bags, andcommunication systems that include telephone, fax,and Internet charges. Unfortunately, farmers oftenignore such marketing costs. An often-overlookedcost is the fish or shrimp that are produced but notsold (Engle and Stone 2008). Few farmers sell all thatthey produce. This is particularly true of newer farmsand those that target higher-risk markets like specialtymarkets.

Successful market development must also place theproduct where it is easy for the targeted consumersto purchase it. Successful marketing managers under-stand where and when their customers prefer to shop.Product is then supplied to those physical locationswith the greatest likelihood of being available to thetarget consumers. For example, it would be unwiseto attempt to sell a high-valued specialty product in adiscount store.

The last essential component of successful market-ing is how products will be promoted. Promotion is theeffort by the company to provide information on theproduct. The customer has to understand the benefitsof the product, appreciate its value, and realize whythey need to purchase it.

SUCCESSFUL MARKETINGREQUIRES DETAILED PLANNING

Marketing plans must evolve constantly to stay aheadof lifestyle and consumer trends. A complete mar-keting strategy involves development of the product,careful pricing, identifying the most promising loca-tions for sales, and developing an effective and tar-geted promotion program. Customer segments shouldbe selected on the basis of whether the firm can ad-dress their needs effectively. The business’s image andlogo must reflect and communicate the unique andspecific attributes of its products to not only justifybut also validate its higher price. No one businesscan service everyone. The key is to identify whichcustomer segments work best for that particular com-pany and its product line. Long-term success dependsupon how well the company understands its customers.Why should someone buy that farms’ product? Is it thefreshest? Is it locally grown? Is it the highest quality?Is it because that farm treats the animals in the mosthumane manner? How does the farm create an “expe-rience” that will bring people back?

Table 2.1 outlines what needs to be included in athorough and comprehensive marketing plan. It is along outline, but shortcutting the various componentslisted is a good way to ensure business failure. Themarket summary requires research and careful assess-ment of current demographics such as the size of thegeographic area, age groups, family structure, gen-der, income, education, lifestyle factors, and spendinghabits. Out of this assessment must come a clear under-standing of what products are needed, how they need

P1: SFK/UKS P2: SFK

c02 BLBS059-Engle June 11, 2010 10:17 Trim: 246mm X 189mm Printer Name: Yet to Come

16 Managing Aquaculture Business

Table 2.1. Outline for a Marketing Plan.

I. Executive summaryII. Overall market situation analysis

A. Market summary1. Consumer demographics

a. Geographic areab. Age groupsc. Family structured. Gendere. Incomef. Educationg. Lifestyle factorsh. Spending habits

2. Supermarket demographicsa. Geographic areasb. Age groupsc. Family structured. Gendere. Incomef. Educationg. Lifestyle factorsh. Spending habits of customers

3. Restaurant demographicsa. Geographic areasb. Age groupsc. Family structured. Gendere. Incomef. Educationg. Lifestyle factorsh. Spending habits of customers

4. Market needsa. Product(s)b. Convenience/servicec. Pricing

5. Market trendsa. Supplyb. Packagingc. Health consciousness

6. Market growthB. Analysis of strengths and weaknesses of business

1. Strengths2. Weaknesses3. Opportunities4. Threats

C. CompetitionD. Product offeringE. Keys to successF. Critical issues

III. Marketing strategyA. MissionB. Marketing objectivesC. Financial objectivesD. Target marketsE. Distribution channelsF. PositioningG. StrategiesH. Marketing mixI. Marketing research

IV. Financial analysisA. Planned expenses

1. Sales force requirements2. Advertising expenditures

B. Sales forecastC. Break-even analysis

V. ControlsA. ImplementationB. Marketing organizationC. Contingency planning

to be packaged and supplied, and how they need to bepriced.

The strengths and weaknesses of the business mustbe identified and described objectively along with op-portunities and threats facing it. The business must po-sition itself to produce those products identified in themarket assessment for which it has a unique advantageand for which it can do a better job than the compe-tition. The specific factors that will have the greatesteffect on the success or failure must be identified.

The steps outlined above should have resulted inidentification of the specific target markets, productsand packaging, and pricing that mesh well with thecompany’s unique strengths and advantages. The nextstep is to lay out the specific marketing, sales, and

financial objectives for the business. The detailed fi-nancial analysis develops detailed projections of pro-duction, costs, sales force requirements, advertisingexpenditures, sales forecasts, and a break-even anal-ysis. Chapter 3 provides additional detail on businessplanning.

PRICING

Pricing strategies used by the company are clearly im-portant determinants of the success or failure of thebusiness. Prices received must cover costs of produc-tion for the business to survive. As obvious as thisis, there are many examples of aquaculture businessesdumping product on the market at low prices when

P1: SFK/UKS P2: SFK

c02 BLBS059-Engle June 11, 2010 10:17 Trim: 246mm X 189mm Printer Name: Yet to Come

Marketing Aquaculture Products 17

cash flow deficits require immediate receipts. Thistype of behavior reflects poor business planning andanalysis, inadequate liquidity, and perhaps inadequatecapitalization. Dumping product is not a pricing strat-egy but rather a symptom of a company with a poorfinancial structure. In this book, Chapter 3 discussesproper and thorough business planning, Chapter 4presents detailed measures of how to monitor and con-trol financial performance, and Chapters 11 and 12illustrate what constitutes adequate liquidity and cap-italization.

Engle and Quagrainie (2006) discuss various pricingsystems and strategies and factors that affect marketprices. What is most important is to identify a pricelevel that reflects the value to be derived by the con-sumer. Consumers must perceive that what they spendto acquire the product is worth that amount of money.The market planning process, if done well, should re-sult in clear understanding of what consumers want,how the company’s product uniquely meets those par-ticular needs and solves those consumers’ problems,and how much value consumers will receive from pur-chasing that product. That value is what the price needsto be. If the price is not high enough to cover produc-tion costs, the business is not feasible and additionalplanning is needed to identify a product that can beproduced at a cost that also provides adequate value tothe consumer.

MARKETING ISSUES SPECIFIC TOVARIOUS SIZES OF FARMS

Large-Scale Growers

Large-scale growers clearly need to identify a high-volume market outlet such as a processing plant. It isessential that a potential grower invest the time to meetwith the processing plant buyers before constructionof production facilities.

There are a number of important considerationstaken into account when considering sales to a pro-cessing plant. Information on historical prices paid tofish farmers for fish from this plant should be com-pared to historical prices paid to fish farmers fromother plants. The plant’s policies on dockage rates(poundage or percentage deducted from the total de-livery amount for trash fish, out-of-size fish, turtles, orother reasons) should also be compared across process-ing plants. Some plants pay based on dressout yield.Some plants provide harvesting and transportation ser-vices while others expect the farmer to make arrange-ments to harvest and transport fish. There is a great

deal of variation on contracting arrangements betweenprocessors and fish farmers. Details of the agreementshould be examined carefully. The farmer should askspecific questions related to delivery volume require-ments and seasonality issues that may affect delivery tothe plant. Size requirements can be important. For ex-ample, some plants will not pay for fish that are smalleror larger than a specified size range while other plantsmay dock a percentage off the entire load if the pro-portion of out-of-size fish is higher than the plant’sstandard. The grower must fully understand the pro-cessor’s expectations with regard to quality standards,flavor sales, and meat quality.

Payment frequency to growers and typical lengthof time between the time of delivery of fish and re-ceipt of payment should be compared across plants.Some states require that bonds be posted by process-ing companies to ensure that farmers are paid for fishdelivered. The processor’s record of payment shouldbe reviewed.

Small-Scale Growers

Small-scale producers will need to identify higher-priced alternative marketing outlets to maintain a prof-itable operation. This is because economies of scaleresult in higher costs of production on smaller as com-pared to larger farms. The prices paid to farmers byprocessors frequently fall below the break-even priceson smaller-scale farms. Alternative market outlets forsmall-scale growers can include the following: livesales with custom processing, fee-fishing or pay lakeoperations, or sales to local grocery stores and restau-rants, and sales to live haulers.

In areas with populations exhibiting regular fish con-sumption, sales of live fish can be a means of achievinghigher prices. The capability to process fish accordingto preferences of the customer may attract a broaderclientele. State and local health codes, permits, andHazard Analysis of Critical Control Points (HACCP)plans must be considered before developing this typeof marketing plan.

Fee-fishing or pay lake operations essentially sell arecreational opportunity to their customers. If locatedwithin 30–50 miles of a major population center, fee-fishing may offer a viable market outlet for farm-raisedfish. Pay lake operators also purchase fish for stock-ing. Increased interest in urban and community fishingprograms managed by state game and fish agenciesmay provide marketing opportunities for fish farmers.Sales to pay lakes may require arrangements with alivehauler to transport fish. Livehaulers are firms or

P1: SFK/UKS P2: SFK

c02 BLBS059-Engle June 11, 2010 10:17 Trim: 246mm X 189mm Printer Name: Yet to Come

18 Managing Aquaculture Business

individuals who truck live fish to pay lakes or live salemarkets. Larger fish frequently are required for paylake outlets. For catfish, a larger (2–3 lb) fish typicallyis required.

Sales to local grocery stores and restaurants re-quire on-site processing unless restaurant personnelclean the fish. Typically, only managers of very ex-clusive seafood restaurants will purchase whole fish tobe cleaned by their personnel. State and local healthcodes, permits, and HACCP plans must be consideredbefore developing this type of marketing outlet.

Targeting any of these sales outlets requires care-ful estimates of volumes, size preferences, and costsassociated with the sales. Moreover, state and localregulations must be evaluated carefully, and implica-tions for costs of the business must be assessed.

HOW DOES A GROWER BEGIN TOASSESS THE MARKET?

Fish and shellfish markets are dynamic. Each marketsegment has its own buying patterns, quantities pur-chased, product forms, pricing schemes, and deliveryrequirements. The specific needs of buyers must be de-termined in detail. To do so, it is important to talk to asmany different buyers as possible. Prospective grow-ers can also talk to growers already in the business andto buyers in regions where the product is already beingsold. This will provide a good idea of how the productis positioned, priced, and promoted in that area. Pay-ing attention to the current level of competition willalso provide insight into whether it is time to begin todevelop new products.

It is more difficult to assess the market potential foran innovative new product not currently sold. One ap-proach is to gather information on substitute productssold locally and inquire about the market for these sub-stitutes. For example, someone interested in a marketfor freshwater prawns could evaluate the market forshrimp in a particular area and attempt to find a nichewithin the overall line of shrimp products sold that isnot currently being met. These efforts should result inan overall view of the types of needs that buyers have.

The next step is to quantitatively estimate the po-tential size and volume of the market. Secondary datacan be collected on the overall population demograph-ics. Consumer census data and business or economicdevelopment data from local chambers of commercecan be used to estimate the number of potential buy-ers and the total expected sales in the targeted marketarea. With the market assessment data, the aquaculture

business can then set specific market objectives. Theseobjectives would include specifying target sales goalsby market segment.

As an example, a targeted population might be cou-ples without children in an age range of 25–40 yearswith income levels above $40,000. The target marketarea includes 20,000 households that can be classi-fied within this demographic segment. The aquaculturebusiness believes that 10%, or 2,000, of these house-holds will purchase their product each year. If thesehouseholds are expected to purchase product once amonth, there will be 24,000 purchases a year. If cus-tomers are expected to purchase 2 lb of fish at eachpurchase, the business will project sales of 48,000 lbof product/year.

A key component of the marketing plan is to in-clude strategies to adapt to changing market condi-tions. Prices, consumer preferences, product contami-nation, and safety issues can have drastic effects on afarm business, and the farm must be prepared to reactquickly to these.

MARKET POWER AND WHAT ITCAN MEAN TO AQUACULTUREBUSINESSES

One of the striking trends in food marketing has beenthe trend toward increased concentration in the retailand wholesale sectors. The emergence of very largesupermarket chains such as Wal-Mart, Tesco, and Car-refour has been accompanied by consolidation in thefood service distribution sector as well. This increasedconsolidation has led to increased market power on thepart of these large companies.

Market power is a term used to refer to the abil-ity of an individual company to affect exchanges inthe market. A single large buyer often is in a posi-tion to strongly influence price of the product, qualitystandards, and how products flow to consumers. Theability to affect market exchanges constitutes power inthe marketplace.

Many aquaculture businesses are small relative tobuyers like Wal-Mart, Tesco, and Sysco. Thus, in ne-gotiations related to price, products, and volume, thelarge buyer typically will be in a position of strengthand will be better able to negotiate for favorableterms.

There are three broad strategies that can be usedby farming businesses to position themselves morefavorably in this type of environment. The best-known strategy is to integrate vertically. A vertically

P1: SFK/UKS P2: SFK

c02 BLBS059-Engle June 11, 2010 10:17 Trim: 246mm X 189mm Printer Name: Yet to Come

Marketing Aquaculture Products 19

integrated company is one that controls various stagesin the supply chain or the stages that a product movesthrough to reach the end consumer. Examples in aqua-culture include Marine Harvest (salmon) and ClearSprings, Inc. (trout). Vertically integrated companiesoften control both production and processing stages,and sometimes also control feed manufacturing orother activities. As a result, vertically integrated com-panies are large enough to be able to negotiate moreeffectively on price, product, and volume because theycontrol many of the various components and are largeenough to control a substantial volume of production.

A second strategy that can be used by farming busi-nesses when confronted by a high degree of concen-tration in their markets is to integrate horizontally.There are many examples of horizontal integration inagriculture. By definition, horizontal integration refersto the formation of business relationships with othercompanies that operate at the same level in the sup-ply chain. Horizontal integration can take many formsthat can include cooperatives, bargaining associations,marketing orders, marketing agreements, and others.In integrating horizontally, care must be taken not toviolate laws designed to prevent unfair pricing prac-tices. Often, these take the form of antitrust legislationwithin a particular country, or can constitute provi-sions of international treaties such as the World TradeOrganization.

Farmers who organize to integrate horizontally togain parity in the market (when faced with dispro-portionately greater market power by buyers) may beexempted from charges of antitrust violations. In theUnited States, such an exemption is provided on alimited basis by the Capper-Volstead Act of 1922.The Fishermen’s Collective Marketing Act of 1934extended the provisions of the Capper-Volstead Actto aquaculture. Specific provisions of the Capper-Volstead Act include: (1) associations must be operatedfor the mutual benefit of the members; (2) all mem-bers (voters) must be agricultural producers; (3) eachmember must have one vote or there must be a capon stock dividends of 8% per year; and (4) the valueof business conducted with members must exceed thatwith nonmembers. Forming a cooperative or creating amarketing agreement or order allows for that organiza-tion to control a greater amount of supply that can leadto greater influence over price, products, and volumeswhen negotiating with larger buyers.

The third strategy, which can be used by an individ-ual farm when there is a high degree of concentrationin the market, is to form an alliance with other com-