food agribusiness saudi arabia ireland

TRANSCRIPT

Food & Agribusiness Trade & Investment Opportunities Saudi Arabia & Ireland

© Farrelly & Mitchell 2013

Malachy Mitchell, Managing Director

Riyadh, Saudi Arabia, October 2013

In association with:

www.FARRELLYMITCHELL.ie

M&A » Buy & Sell Mandates » Strategic Partnerships & Joint Ventures » Funding » Commercial and Operational Due Diligence » IPO Preparation / Vendor Support » Business Valuations

Advisory » Operations Consulting » Commercial Consulting » Financial & Strategy Consulting » HR & Reorganisation Consulting

Our Services include: “We help companies to grow profits, increase efficiencies or invest or divest a business”

Presentation:

1: Quick Facts & Figures

2: Supply & Demand

3: Retail Landscape

4: Challenges & Opportunities

5: Where’s the Growth?

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

s

1) Quick Facts & Figures

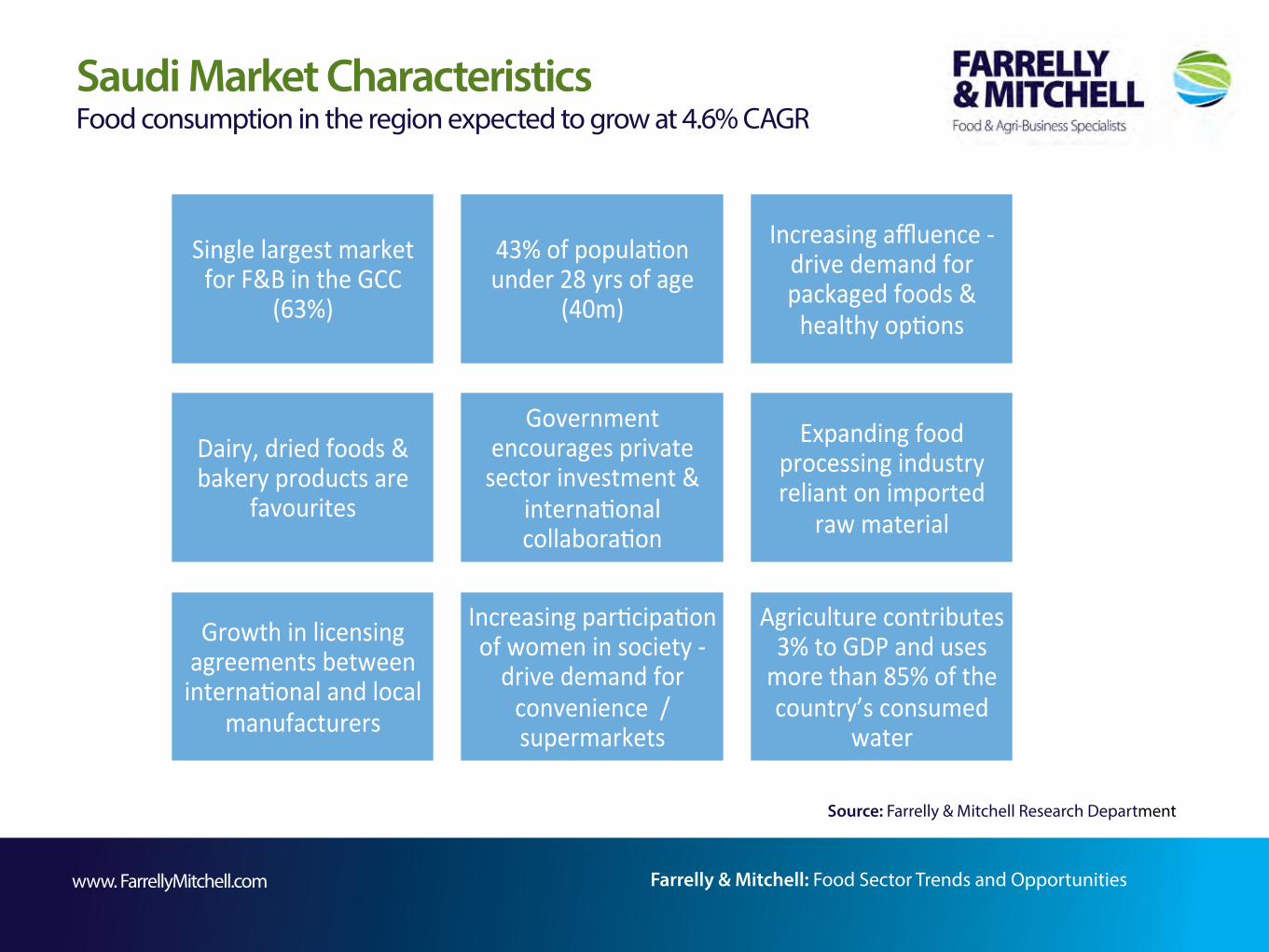

Saudi Market Characteristics Food consumption in the region expected to grow at 4.6% CAGR

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

Source: Farrelly & Mitchell Research Department

Single largest market for F&B in the GCC

(63%)

43% of popula>on under 28 yrs of age

(40m)

Increasing affluence -‐drive demand for packaged foods & healthy op>ons

Dairy, dried foods & bakery products are

favourites

Government encourages private sector investment &

interna>onal collabora>on

Expanding food processing industry reliant on imported

raw material

Growth in licensing agreements between interna>onal and local

manufacturers

Increasing par>cipa>on of women in society -‐ drive demand for convenience / supermarkets

Agriculture contributes 3% to GDP and uses more than 85% of the country’s consumed

water

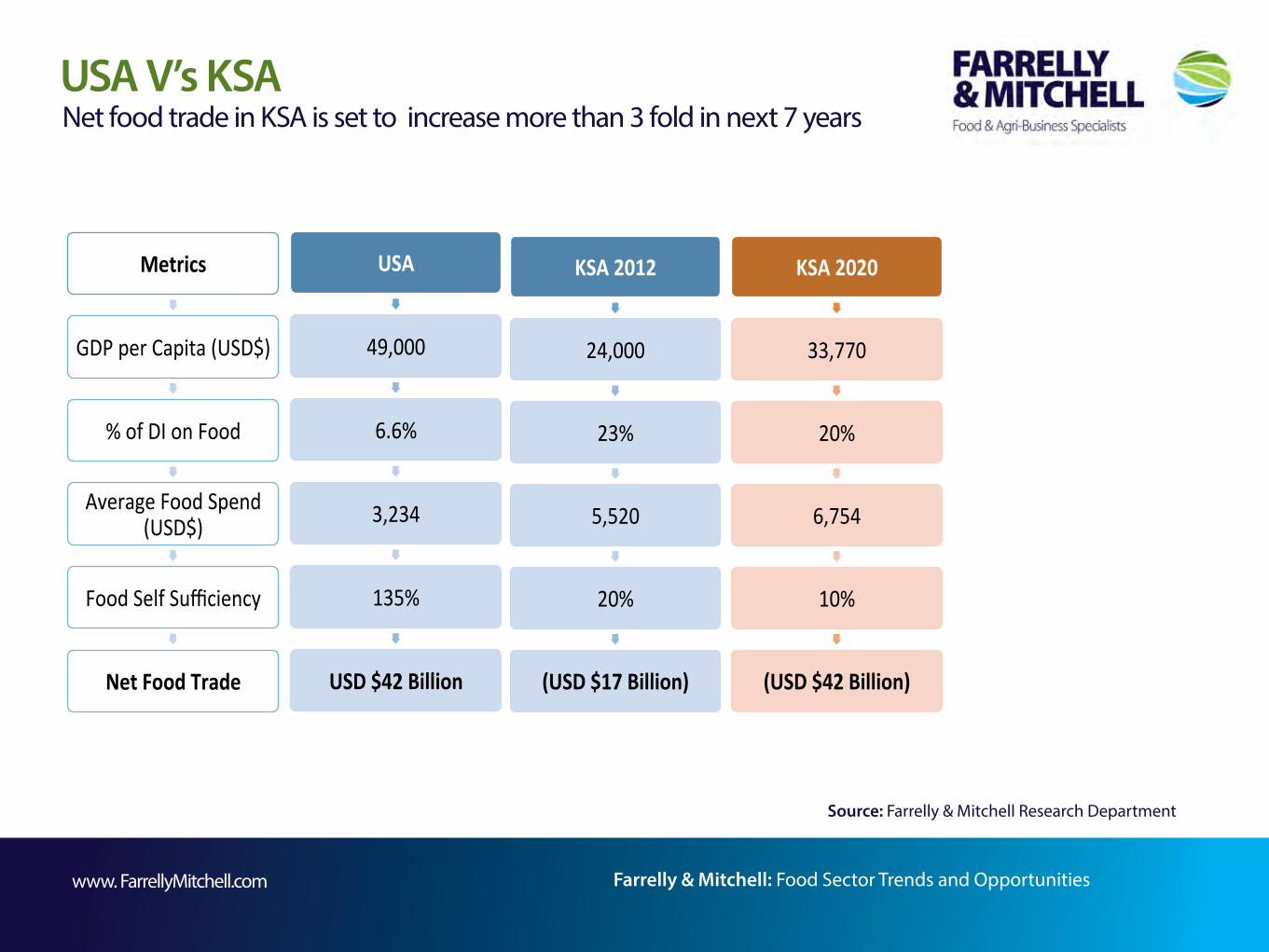

USA V’s KSA Net food trade in KSA is set to increase more than 3 fold in next 7 years

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

Source: Farrelly & Mitchell Research Department

Metrics

GDP per Capita (USD$)

% of DI on Food

Average Food Spend (USD$)

Food Self Sufficiency

Net Food Trade

USA

49,000

6.6%

3,234

135%

USD $42 Billion

KSA 2012

24,000

23%

5,520

20%

(USD $17 Billion)

KSA 2020

33,770

20%

6,754

10%

(USD $42 Billion)

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

2) Supply & Demand

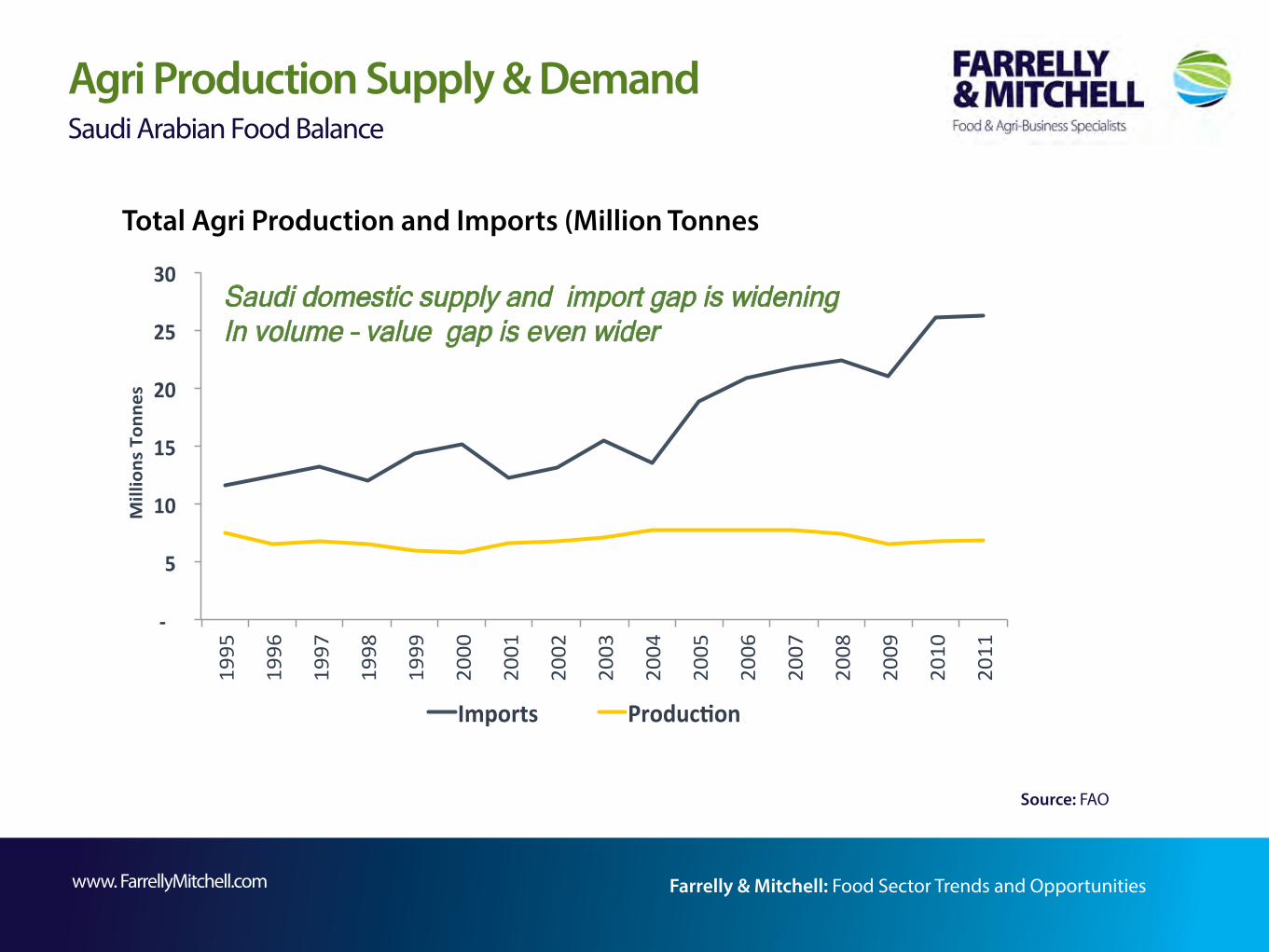

Agri Production Supply & Demand Saudi Arabian Food Balance

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

-‐

5

10

15

20

25

30

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Millions Ton

nes

Imports Produc9on

Saudi domestic supply and import gap is widening In volume – value gap is even wider

Total Agri Production and Imports (Million Tonnes

Source: FAO

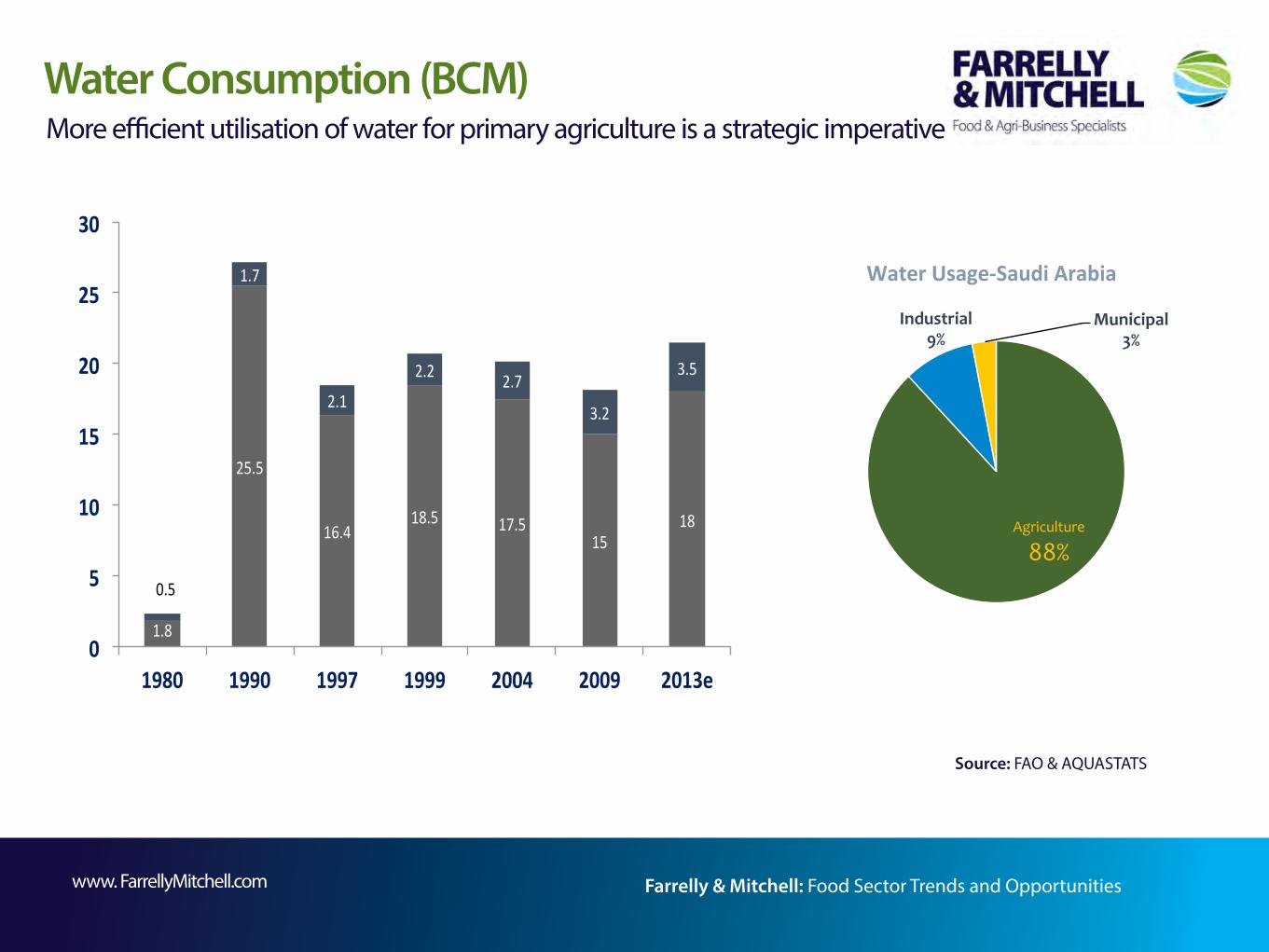

Water Consumption (BCM) More efficient utilisation of water for primary agriculture is a strategic imperative

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

1.8

25.5

16.4 18.5 17.5

15 18

0.5

1.7

2.1

2.2 2.7

3.2

3.5

0

5

10

15

20

25

30

1980 1990 1997 1999 2004 2009 2013e

Agriculture

88%

Industrial 9%

Municipal 3%

Water Usage-‐Saudi Arabia

Source: FAO & AQUASTATS

Key Resource Pressures Supply side factors

Food security agenda being developed by:

» Investing in farm land overseas

» Water efficient agriculture

» Promoting the domestic food processing industry

(to reduce imports of processed foods

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

Food Security

Food Self Sufficiency

Water Resources

Agriculture, despite food security aims, only produces 25% of food demand due to:

» Dwindling arable resources (2%) » Water constraints » Inefficiencies in supply and logistics » Rising cost of inputs

Balancing demand generation and ensuring supplies to meet demand is key - Government is a vital link to production capacity with various support schemes

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

3) Retail Landscape

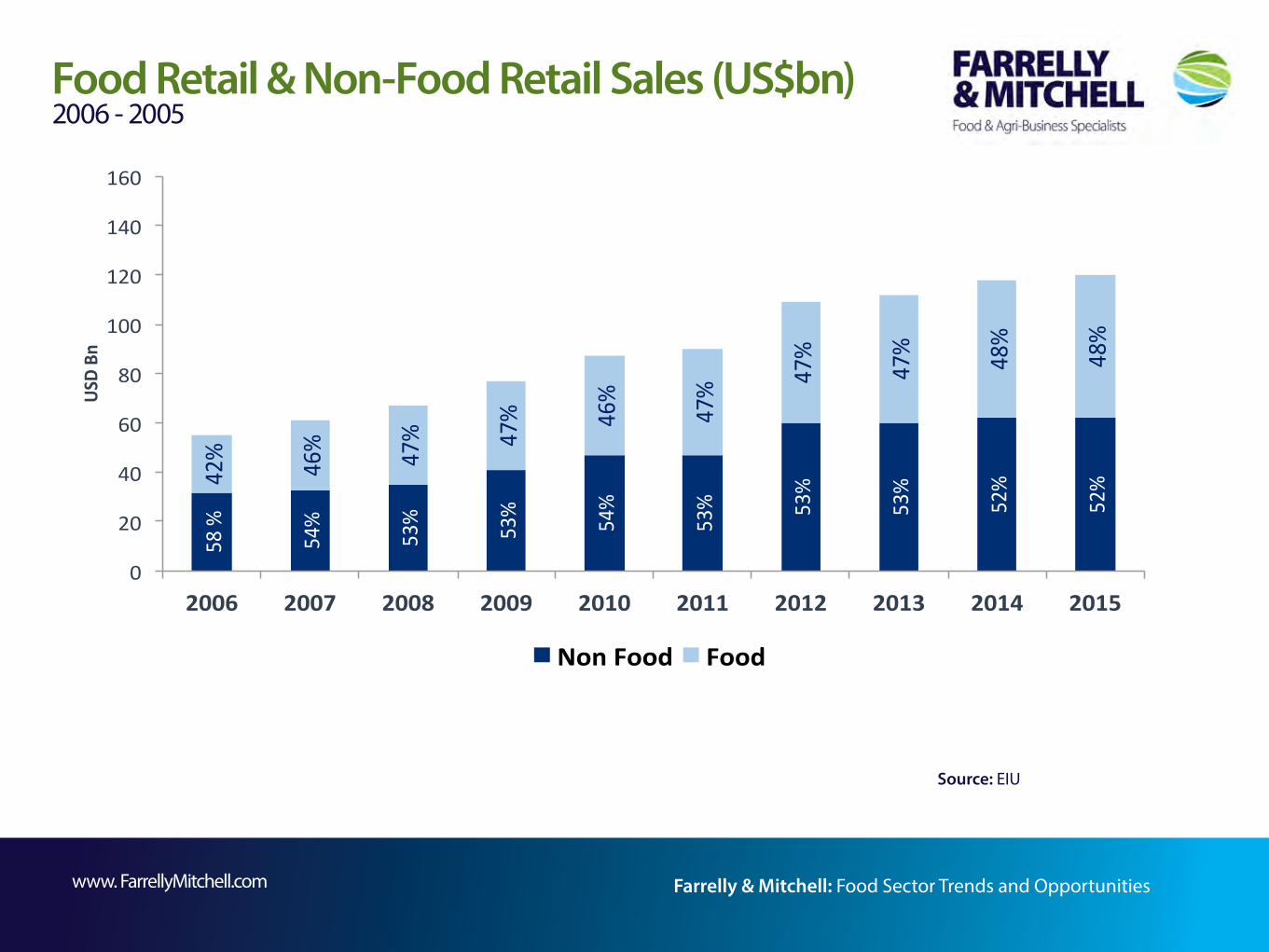

Food Retail & Non-Food Retail Sales (US$bn) 2006 - 2005

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

58 %

54%

53%

53%

54%

53%

53%

53%

52%

52% 42%

46%

47%

47%

46%

47% 47%

47%

48%

48%

0

20

40

60

80

100

120

140

160

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

USD Bn

Non Food Food

Source: EIU

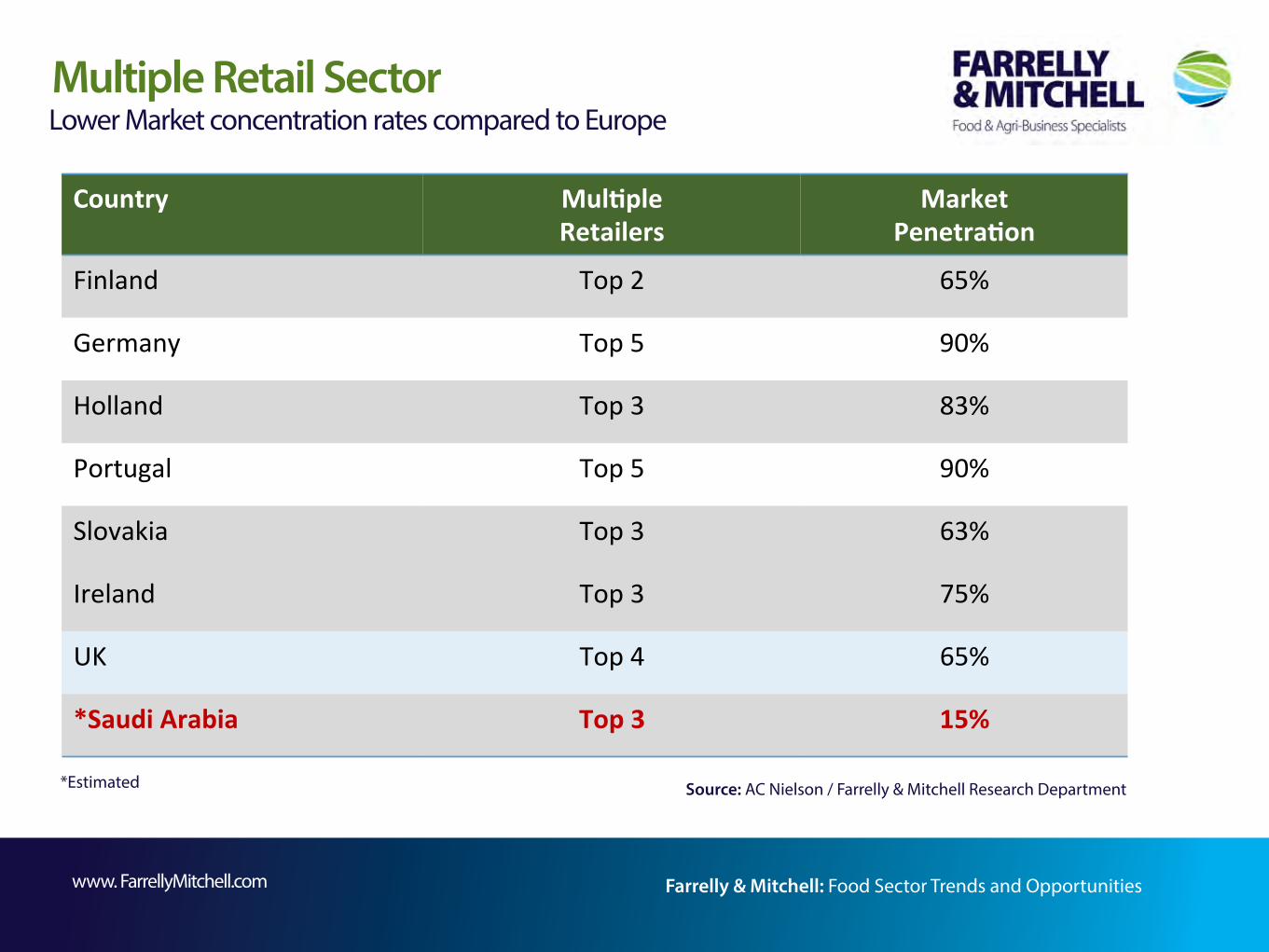

Multiple Retail Sector Lower Market concentration rates compared to Europe

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

Country Mul+ple Retailers

Market Penetra+on

Finland Top 2 65%

Germany Top 5 90%

Holland Top 3 83%

Portugal Top 5 90%

Slovakia Top 3 63%

Ireland Top 3 75%

UK Top 4 65%

*Saudi Arabia Top 3 15%

*Estimated Source: AC Nielson / Farrelly & Mitchell Research Department

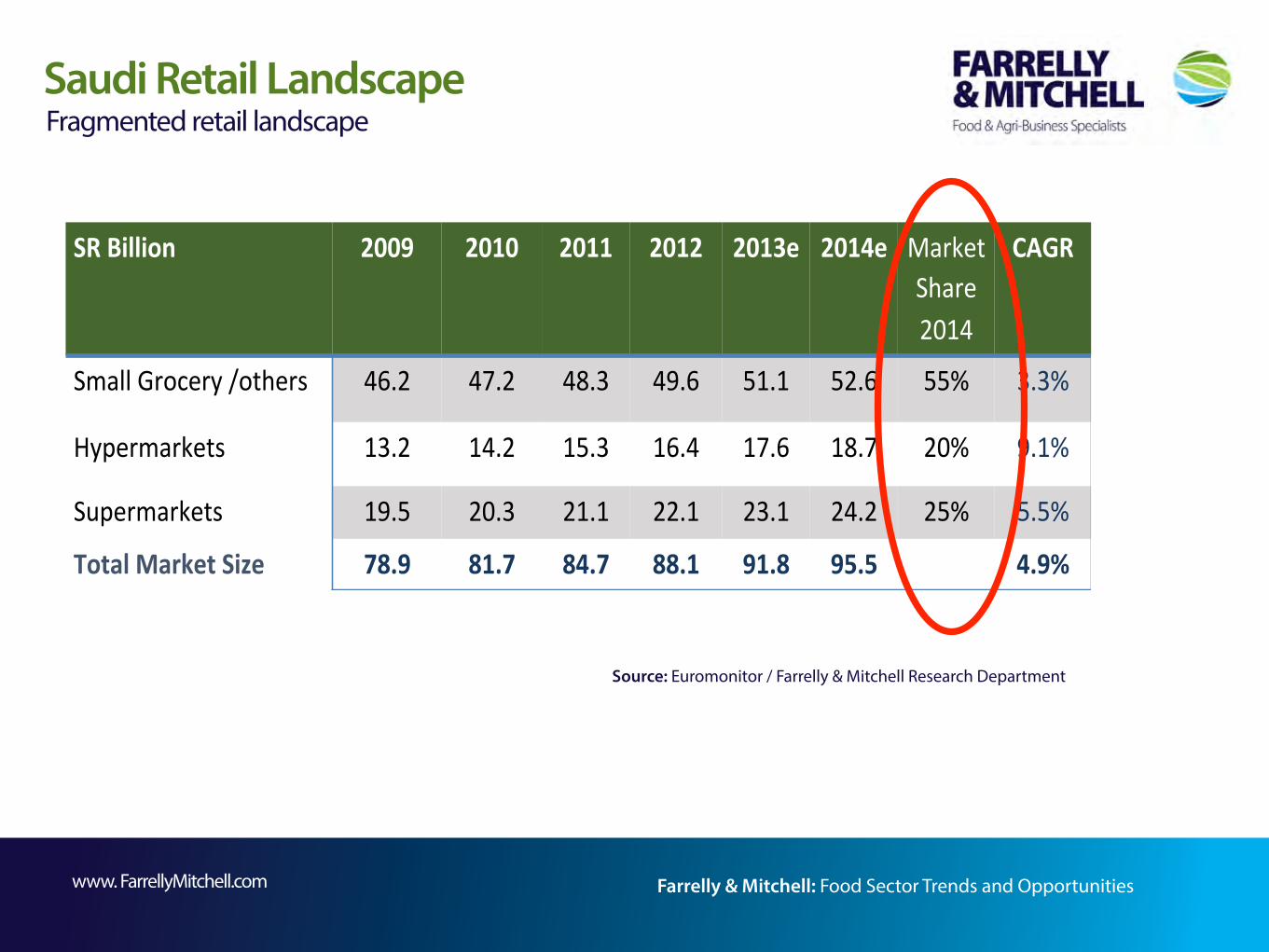

Saudi Retail Landscape Fragmented retail landscape

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

SR Billion 2009 2010 2011 2012 2013e 2014e Market Share 2014

CAGR

Small Grocery /others 46.2 47.2 48.3 49.6 51.1 52.6 55% 3.3%

Hypermarkets 13.2 14.2 15.3 16.4 17.6 18.7 20% 9.1%

Supermarkets 19.5 20.3 21.1 22.1 23.1 24.2 25% 5.5%

Total Market Size 78.9 81.7 84.7 88.1 91.8 95.5 4.9%

Source: Euromonitor / Farrelly & Mitchell Research Department

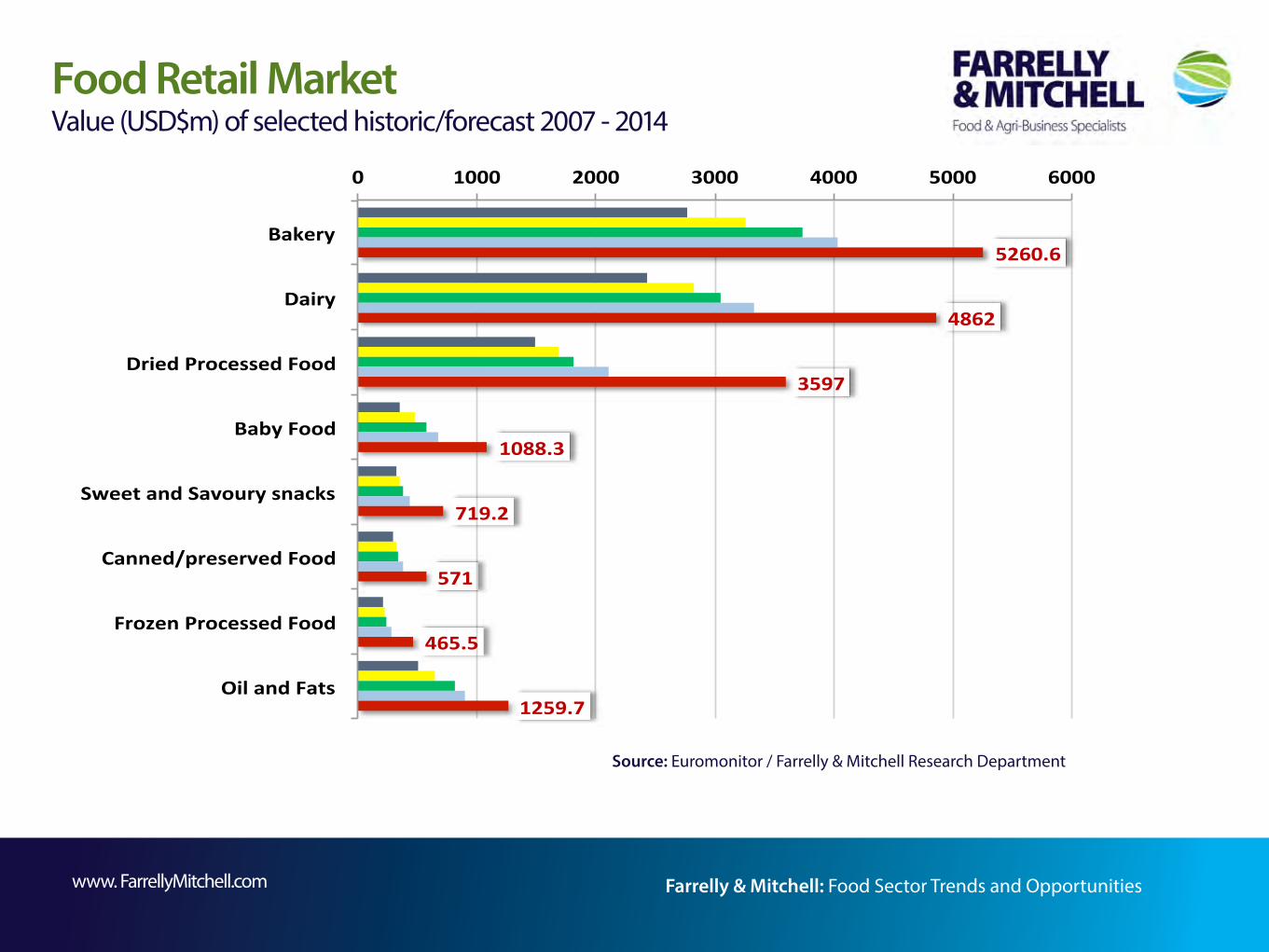

Food Retail Market Value (USD$m) of selected historic/forecast 2007 - 2014

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

5260.6

4862

3597

1088.3

719.2

571

465.5

1259.7

0 1000 2000 3000 4000 5000 6000

Bakery

Dairy

Dried Processed Food

Baby Food

Sweet and Savoury snacks

Canned/preserved Food

Frozen Processed Food

Oil and Fats

Source: Euromonitor / Farrelly & Mitchell Research Department

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

4) Challenges & Opportunities

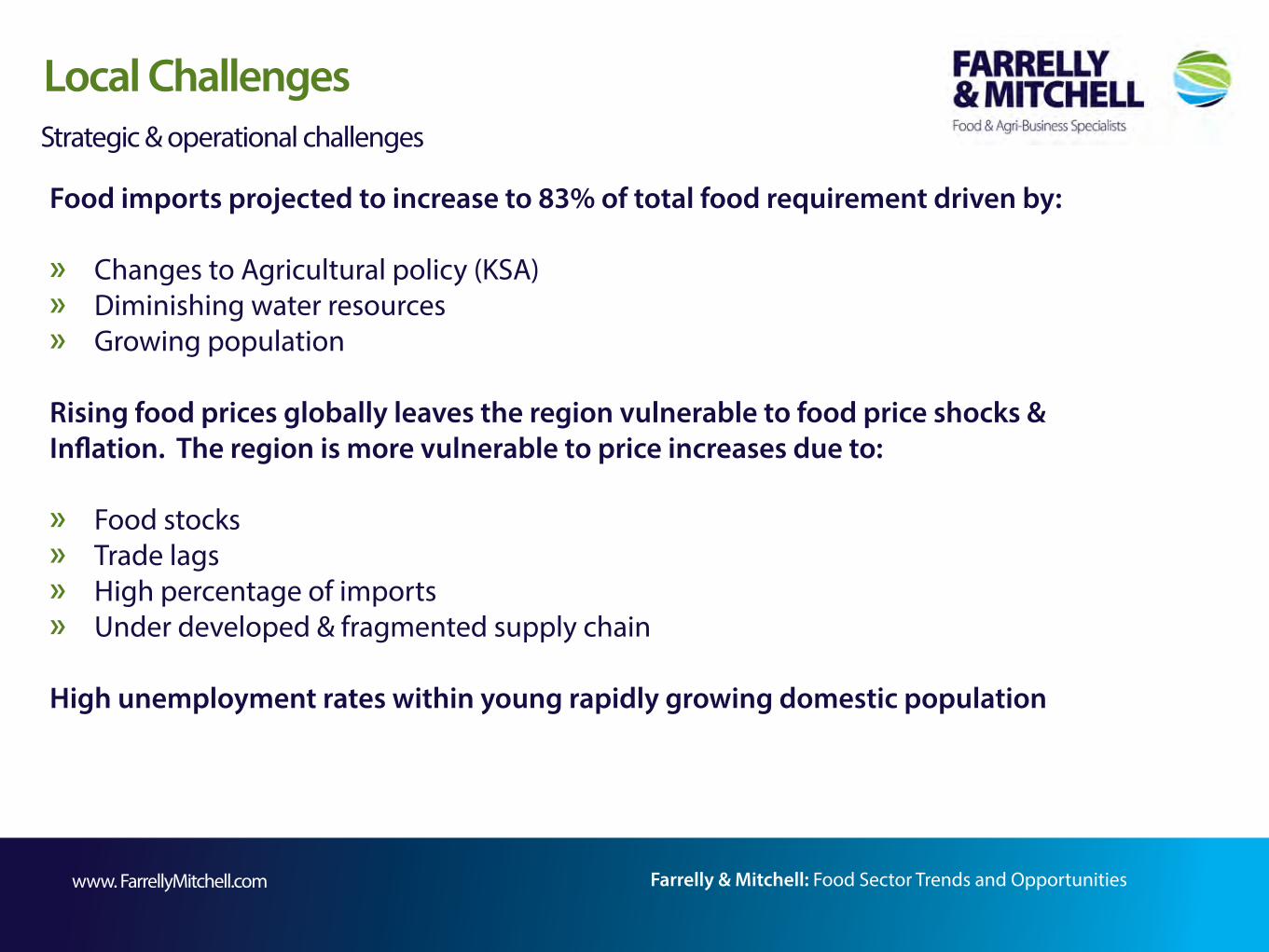

Local Challenges Strategic & operational challenges

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

Food imports projected to increase to 83% of total food requirement driven by:

» Changes to Agricultural policy (KSA) » Diminishing water resources » Growing population

Rising food prices globally leaves the region vulnerable to food price shocks & Inflation. The region is more vulnerable to price increases due to:

» Food stocks » Trade lags » High percentage of imports » Under developed & fragmented supply chain

High unemployment rates within young rapidly growing domestic population

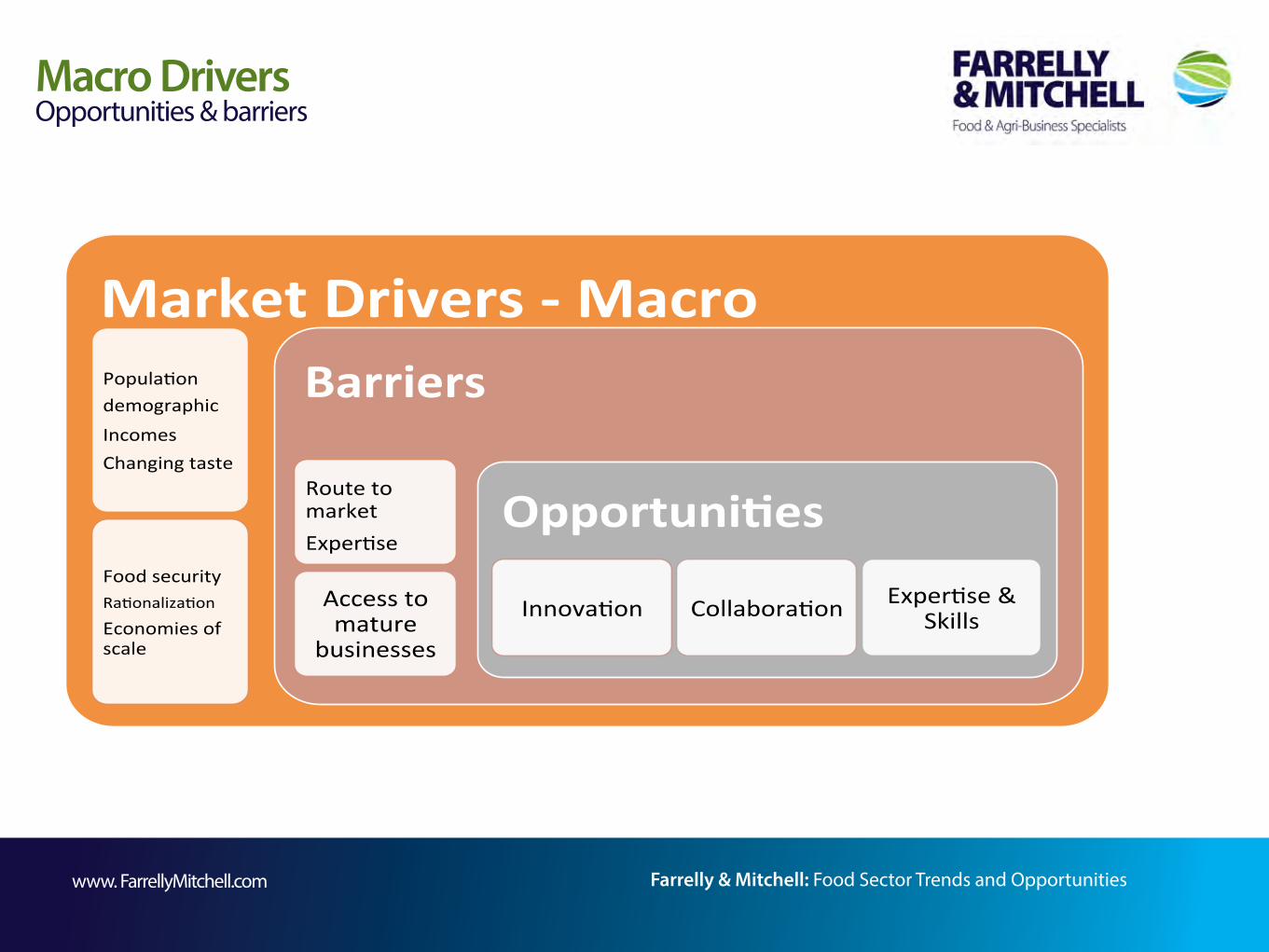

Macro DriversOpportunities & barriers

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

Market Drivers -‐ Macro Popula'on demographic Incomes Changing taste

Food security Ra'onaliza'on

Economies of scale

Barriers Route to market Exper'se

Access to mature

businesses

Opportuni4es

Innova'on Collabora'on Exper'se & Skills

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

5) Where’s the Growth?

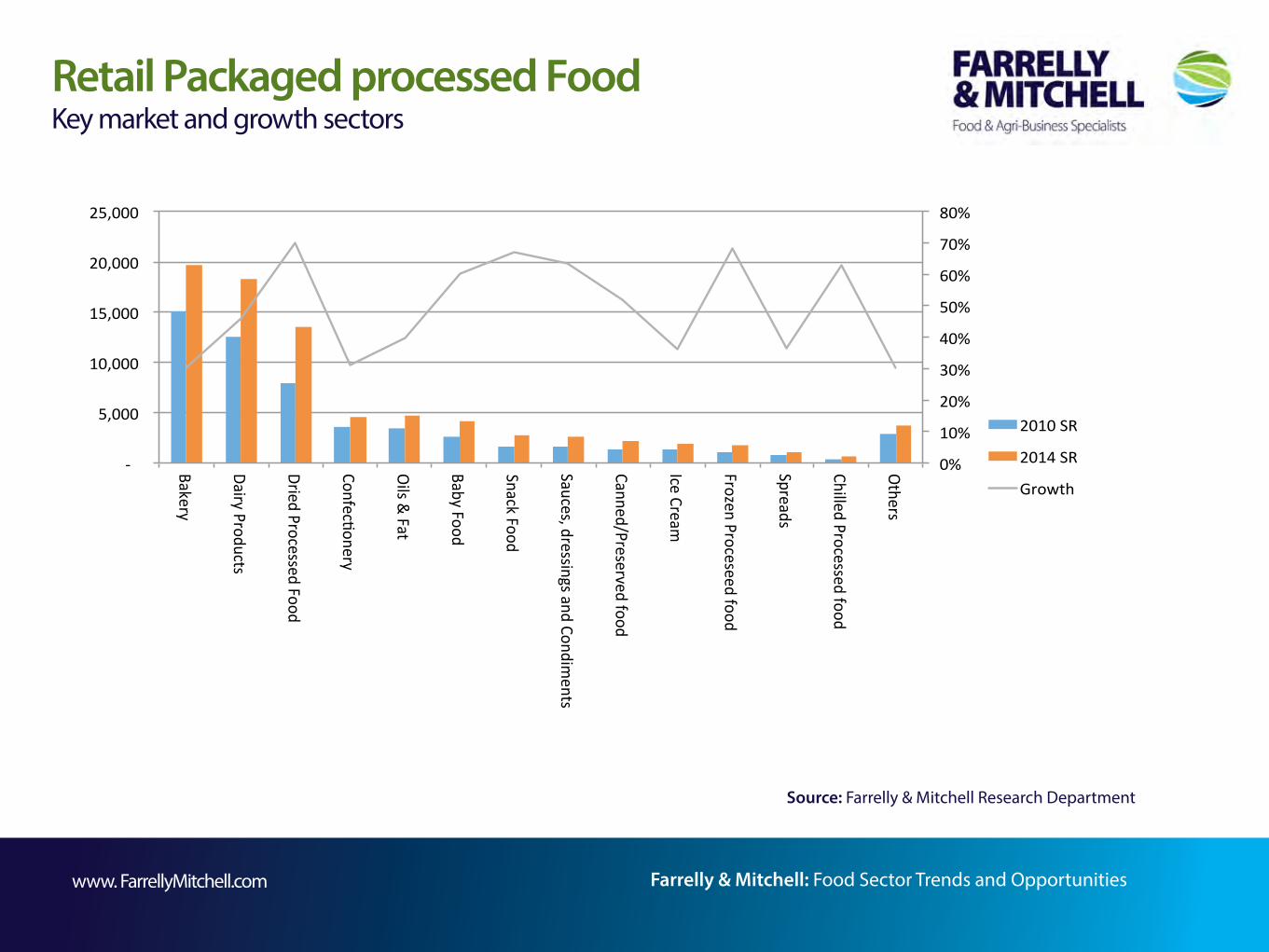

Retail Packaged processed Food Key market and growth sectors

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

Source: Farrelly & Mitchell Research Department

0%

10%

20%

30%

40%

50%

60%

70%

80%

-‐

5,000

10,000

15,000

20,000

25,000

Bakery

Dairy Products

Dried Processed Food

ConfecAonery

Oils & Fat

Baby Food

Snack Food

Sauces, dressings and Condiments

Canned/Preserved food

Ice Cream

Frozen Proceseed food

Spreads

Chilled Processed food

Others

2010 SR

2014 SR

Growth

Key High Growth Sectors Forecasted growth rates over the next 5 years (CAGR)

www. FarrellyMitchell.com Farrelly & Mitchell: Food Sector Trends and Opportunities

Frozen Processed Meats, Poultry

and Seafood 8%

Processed Baby Food 9.8%

Bakery & Confec:onery

Retail 7.2%

Cheese Manufacturing

7.9%

Dried Processed Foods Trading

8.3%

Source: Farrelly & Mitchell Research Department

Thank YouQ&A

Head Office:

Malachy MitchellManaging Director

Unit 5A Fingal Bay Business ParkBalbrigganCo. DublinIreland

Tel: 00 353 1 690 6550Fax: 00 353 1 883 4910Mobile: 00 353 86 806 0843Email: [email protected] Web: www.farrellymitchell.com

Middle East Office:

Mohammed HajjarRegional Director

Al-Rusais BuildingSuite 510Olaya Main RoadP.O. Box 616, Riyadh 11421Kingdom of Saudi Arabia

Tel: 00 966 11 4634406Fax: 00 966 11 4648952 Mobile: 00 966 54 338 7199Email: [email protected] Web: www.farrellymitchell.com

Please Note:The information in this presentation is intended to give information in general nature, great efforts has been exerted to ensure the accuracy of this data at the time the initial presentation was made. Farrelly & Mitchell Business Consultants Ltd. and its Branch offices or affiliates does not provide any implicit or explicit guarantees on the validity, timing or completeness of any data or information in this presentation. Also we assume no responsibility on the appropriateness of the data and information for suiting any particular purpose or reliability in trading or investing. Unless provided otherwise and in writing from us, all information contained in this presentation, including logo, pictures and drawings, are considered property of Farrelly & Mitchell Business Consultants Ltd.