for institutional client use only the cash manager's survival guide are you equipped for...

TRANSCRIPT

For institutional client use only

The Cash Manager's Survival GuideAre You Equipped for Unprecedented Volatility?

May 2012

Not FDIC insured. May lose value. No bank guarantee.

Michael Morin, CFA®Director of Institutional Portfolio Management, Liquidity Management Solutions Fidelity Investments

2

© 2012 FMR LLC. All rights reserved.

For Institutional Client Use Only

1. Assessing Risk: Current Market Conditions

2. The Impact From Regulatory Reform

3. Cash Practitioner’s Best Practices: Formulating the Survival Guide

4. Asset Manager’s Best Practices: Developing a Robust Investment Process

Agenda

For institutional client use only

Assessing Risk: Current Market Conditions

© 2012 FMR LLC. All rights reserved

4 For Institutional Use Only

© 2012 FMR LLC. All rights reserved.

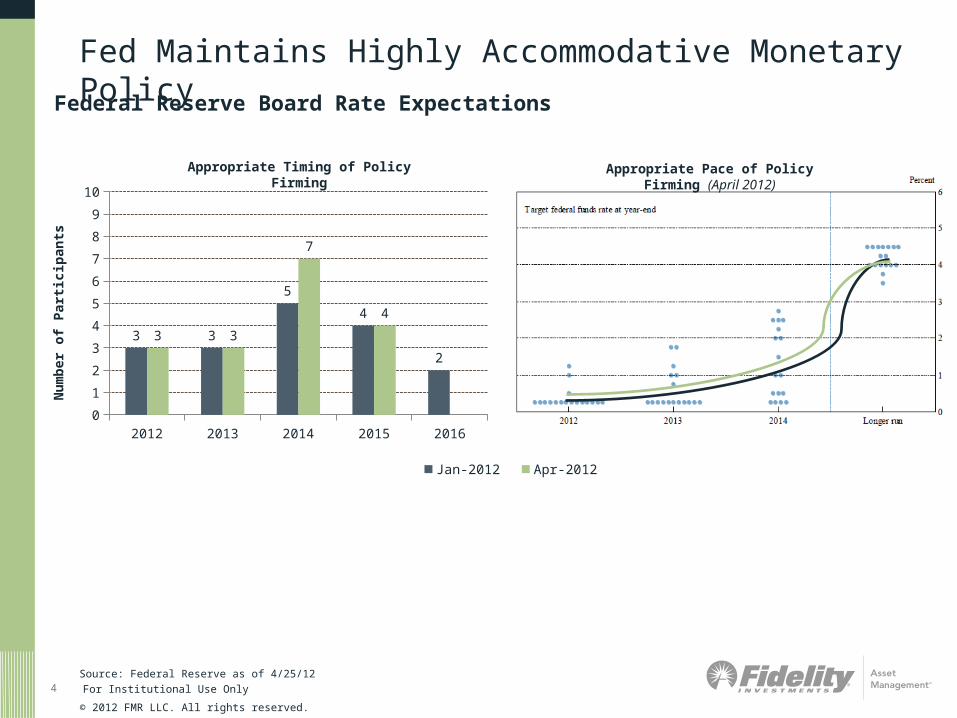

Source: Federal Reserve as of 4/25/12

Fed Maintains Highly Accommodative Monetary Policy

Federal Reserve Board Rate Expectations

2012 2013 2014 2015 20160

1

2

3

4

5

6

7

8

9

10

3 3

5

4

2

3 3

7

4

Jan-2012 Apr-2012

Nu

mb

er o

f P

arti

cip

ants

Appropriate Timing of Policy Firming Appropriate Pace of Policy Firming (April 2012)

Market Expectations in Line with Fed Statement

Sources: FMR, Bloomberg as of 3/31/12

Mar-10 May-10Jul-10 Oct-10 Dec-10 Feb-11 Apr-11 Jun-11 Aug-11 Oct-11 Dec-11 Feb-12 Apr-12 Jun-12 Aug-12 Oct-12 Dec-12 Feb-13

0.00

0.25

0.50

0.75

1.00

Yield (%)

Futures 12/31/08

Futures 12/31/10

Futures 6/30/11Fed Funds Target Rate

Futures 12/31/11

Futures 3/31/12

Fed Funds Target Rate and Fed Funds Futures Levels

For Institutional Client Use Only

0.0

1.0

2.0

3.0

4.0

5.0

Aug

-08

Oct

-08

Dec

-08

Feb

-09

Ap

r-09

Jun-

09

Aug

-09

Oct

-09

Dec

-09

Feb

-10

Ap

r-10

Jun-

10

Aug

-10

Oct

-10

Dec

-10

Feb

-11

Ap

r-11

Jun-

11

Aug

-11

Oct

-11

Dec

-11

Feb

-12

Ap

r-12

Yie

ld (%

)

3 Month LIBOR 3 Month Treasury

6 For Institutional Client Use Only

Short-Term Credit Spreads Stabilize

Past performance is no guarantee of future results. It is not possible to invest directly in an index. Index performance is not meant to represent that of any Fidelity mutual fund.Source: Bloomberg as of 4/30/12

3-MONTH LIBOR VS. 3-MONTH TREASURIES

TED Spread High:10/10/08: 464 bps

TED Spread Low:3/16/10: 11 bps

TED Spread Current:4/30/12: 38 bps

© 2012 FMR LLC. All rights reserved.

7 For Institutional Use Only

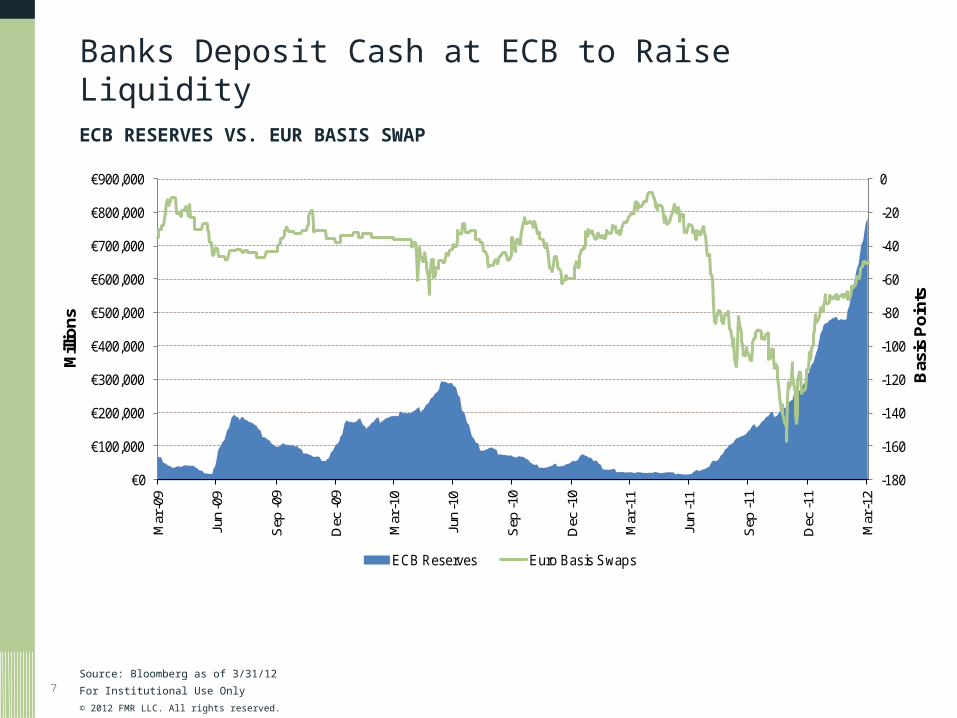

Banks Deposit Cash at ECB to Raise Liquidity

Source: Bloomberg as of 3/31/12

ECB RESERVES VS. EUR BASIS SWAP

© 2012 FMR LLC. All rights reserved.

-180

-160

-140

-120

-100

-80

-60

-40

-20

0

€0

€100,000

€200,000

€300,000

€400,000

€500,000

€600,000

€700,000

€800,000

€900,000

Mar

-09

Jun

-09

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Mar

-12

Bas

is P

oin

ts

Mill

ion

s

ECB Reserves Euro Basis Swaps

For institutional client use only

May 2011

European Council approves €78 billion bailout program for Portugal

March 2011

European Banking Authority publishes provisional details of second EU-wide bank stress test with results expected to be released in July 2011

Apr 2011

Portugal asks for a bailout

European Central Bank raises policy rate 25 basis points to 1.25%

Dec 2009

Statement by Commissioner Almunia on Greece:

"We take note of the fact that the sustainability of public finances in Greece draws the attention of financial markets and rating agencies."

Jan 2010

Eurostat report on Greek deficit and debt statisticsquestions the reliability of Greek figures in general and recent Greek revisions of excessive deficit procedure notifications

Feb 2010

European Commission adopts recommendations to ensure that the budget deficit of Greece was to be brought below 3% of GDP by 2012

May 2010

ECB and IMF agree to €110B Greek bailout

€440B European Financial Stability Facility (EFSF) established

Additional funding through IMF bilateral loans brings total support to €860B

July 2010

Committee of European Banking Supervisors (CEBS) announces results of first European bank stress test of which seven banks failed

Aug 2010

The European Financial Stability Facility (EFSF) becomes fully operational

Dec 2010

European Council and IMF agree to provide €85 billion to Ireland

The EC agrees to replace EFSF with European Stability Mechanism (ESM)

European Debt Crisis – A Timeline of Events

Source: FMR, European Economic and Financial Affairs as of 2/29/12

July 2011

Greece receives 5th installment (€12 B) of original € 110B bailout

Discussions begin for additional €100B bailout

EBA releases results of second stress test

June 2011

Greek Prime Minister George Papandreou receives vote of confidence and €78B of austerity approved

© 2012 FMR LLC. All rights reserved

Dec 2011

ECB cuts overnight refinancing rate 25 basis points to 1.00%

Euro area holds summit and agrees to more consolidated fiscal union,

Oct 2011

European Council and Euro area hold summit to discuss fiscal unity and integration of the Euro area

Nov 2011

Italian 10-year bond yields soar to 7%

Greek President Papandreou replaced by Lucas Papademos

ECB President Claude Trichet replaced by Mario Draghi

Aug 2011

French President Sarkozy and German Chancellor Merkel propose common efforts to strengthen the governance of the euro area

Dec 2011

ECB provides banks with €489B of 3-year loans through LTRO

8

Feb – Mar 2012

ECB provides second LTRO installment

Greece receives second bailout through Private Sector Involvement

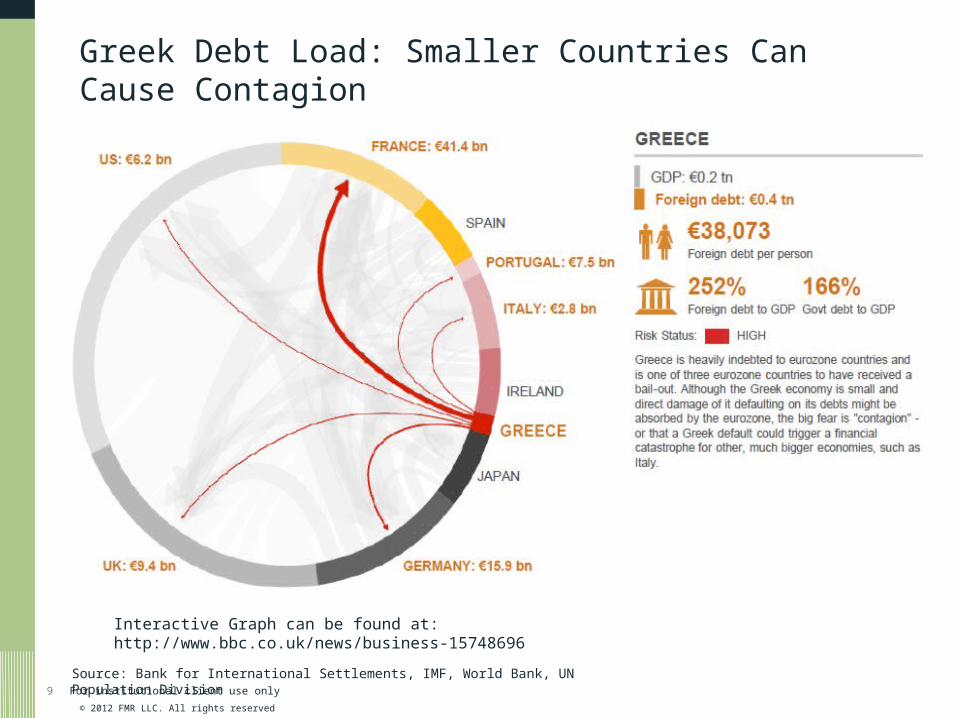

Greek Debt Load: Smaller Countries Can Cause Contagion

9

© 2012 FMR LLC. All rights reserved

For institutional client use only

Interactive Graph can be found at: http://www.bbc.co.uk/news/business-15748696

Source: Bank for International Settlements, IMF, World Bank, UN Population Division

Italian Debt Load: Large Versus Growth Expectations

10

© 2012 FMR LLC. All rights reserved

For institutional client use only

Interactive Graph can be found at: http://www.bbc.co.uk/news/business-15748696

Source: Bank for International Settlements, IMF, World Bank, UN Population Division

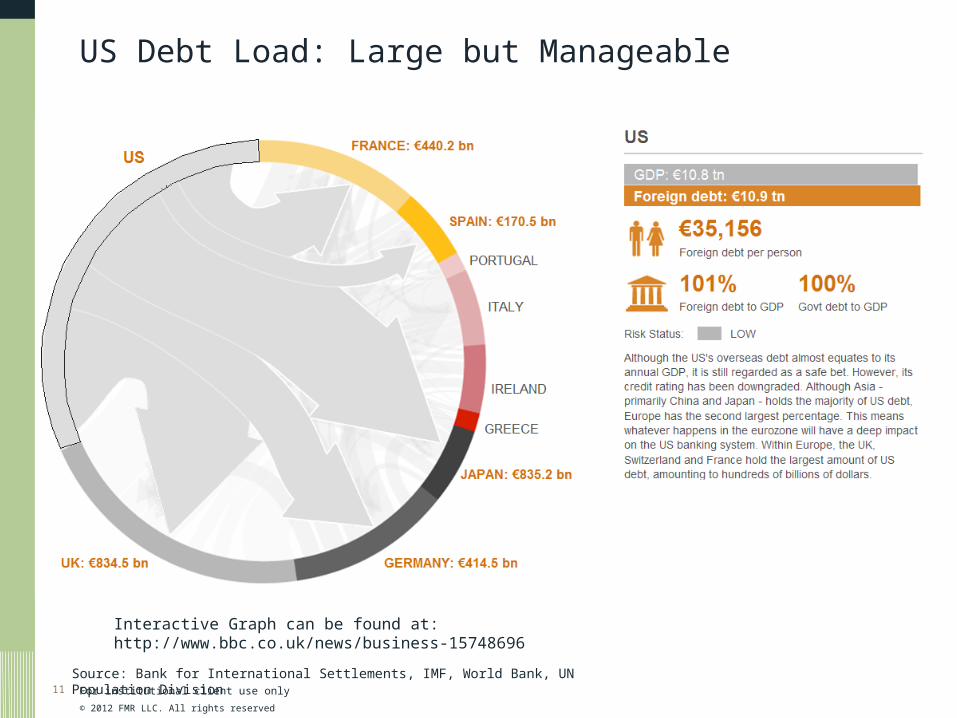

US Debt Load: Large but Manageable

11

© 2012 FMR LLC. All rights reserved

For institutional client use only

Interactive Graph can be found at: http://www.bbc.co.uk/news/business-15748696

Source: Bank for International Settlements, IMF, World Bank, UN Population Division

12 For Institutional Client Use Only

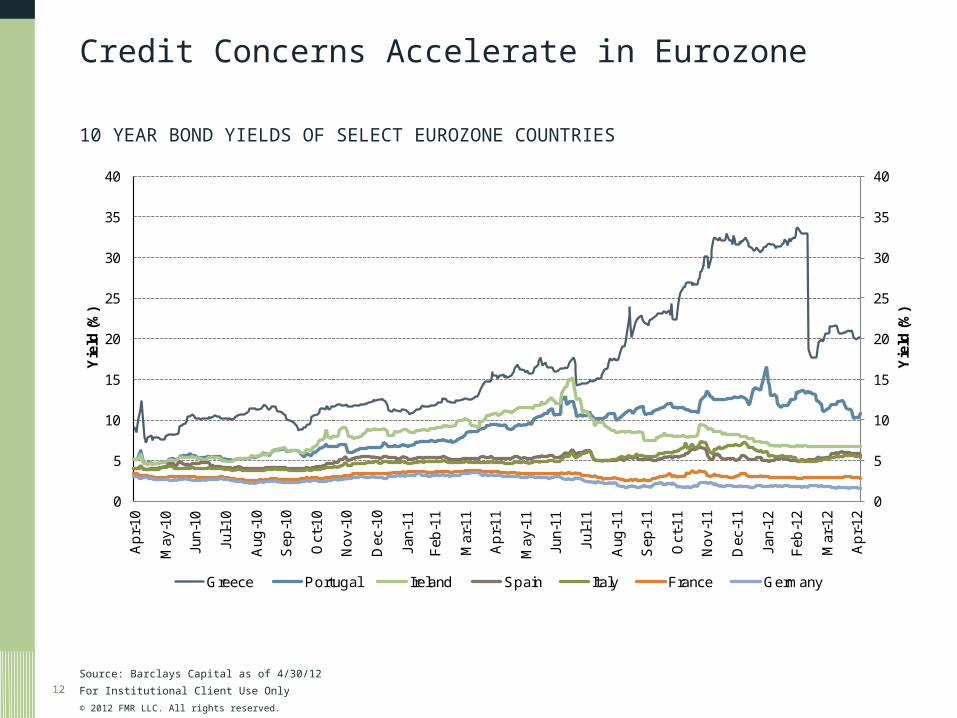

Credit Concerns Accelerate in Eurozone

Source: Barclays Capital as of 4/30/12

10 YEAR BOND YIELDS OF SELECT EUROZONE COUNTRIES

© 2012 FMR LLC. All rights reserved.

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

Ap

r-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

No

v-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Ap

r-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Oct

-11

No

v-11

Dec

-11

Jan-

12

Feb

-12

Mar

-12

Ap

r-12

Yie

ld (%

)

Yie

ld (%

)

Greece Portugal Ireland Spain Italy France Germany

The Next Six Months

For Institutional Client Use Only

BASE CASE• Europe remains in mild recession. Liquidity effect fades and weak fundamentals come to

dominate again Questions about debt sustainability remain, but growth outlook becomes key issue for international markets and anti-austerity voice becomes louder and more mainstream.

• Election risks are manageable – new French president provides limited upsets while Greek government post May 6th elections broadly toes the line on reform.

• Spain comes under greater scrutiny and market pressure increases as budget targets remain elusive and contingent liabilities rise– but manages to maintain market access despite talk of Troika programme

• Italy continues to make progress on reform. Yields move in a fairly wide range as some contagion from worsening Spanish situation is felt. No failed auctions.

ADVERSE CASE• French president seeks change in fiscal pact and raises tensions with Germany

• Greek government abandons reform and process of EUR exit starts – EU authorities will manage this process carefully

• Spain deteriorates and a rescue package is needed – ECB intervention takes place in run up to package

• Italy struggles with the market but manages to raise funding via increased financial ‘repression’

• Deposit flight picks up in periphery, credit conditions deteriorate and additional ECB liquidity is constrained by collateral availability

13

For institutional client use only

The Impact from Regulatory Reform

Regulatory Reform Impacts Financial Markets

15 For Institutional Client Use Only

© 2012 FMR LLC. All rights reserved

• Dodd Frank Act• Full FDIC insurance on non-interest bearing US accounts causes cash to leave money

market funds for bank products. Program set to expire at end of 2012• Repeal of Regulation Q has not influenced flows between banks and money market funds• Systemically Important Financial Institution (SIFI) designations• Volcker Rule could significantly impact the banking industry

• Basel III impacts bank leverage, liquidity coverage, and capital ratios

• Changes to SEC Rule 2a-7 has increased the resilience of money market funds

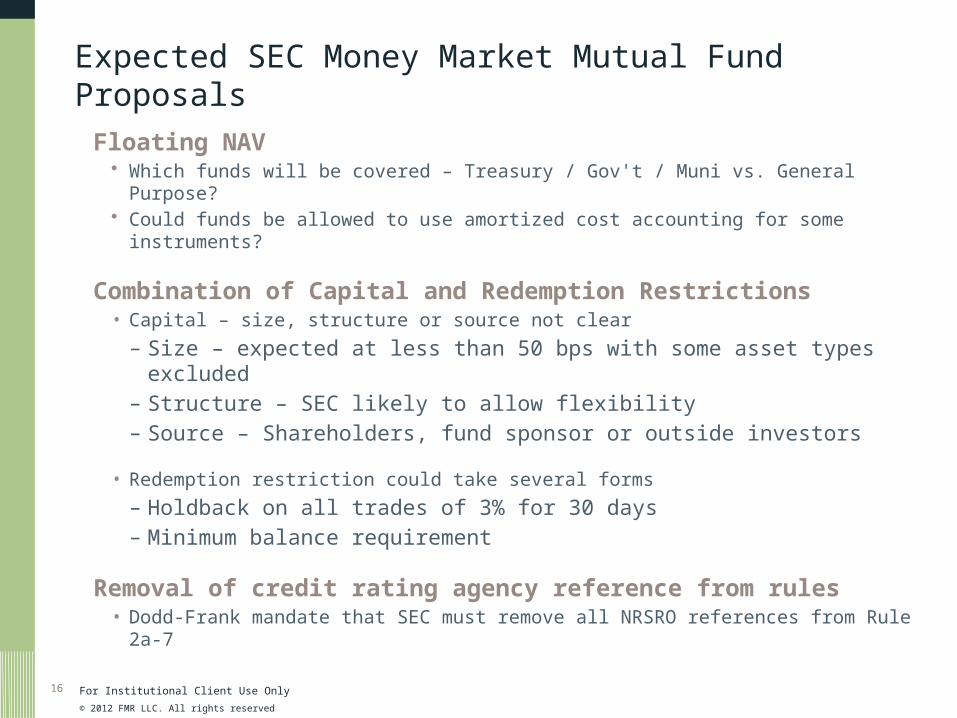

Expected SEC Money Market Mutual Fund Proposals

Floating NAV• Which funds will be covered – Treasury / Gov't / Muni vs. General Purpose?• Could funds be allowed to use amortized cost accounting for some instruments?

Combination of Capital and Redemption Restrictions• Capital – size, structure or source not clear

– Size – expected at less than 50 bps with some asset types excluded– Structure – SEC likely to allow flexibility– Source – Shareholders, fund sponsor or outside investors

• Redemption restriction could take several forms

– Holdback on all trades of 3% for 30 days– Minimum balance requirement

Removal of credit rating agency reference from rules• Dodd-Frank mandate that SEC must remove all NRSRO references from Rule 2a-7

16 For Institutional Client Use Only

© 2012 FMR LLC. All rights reserved

Response to erroneous allegations

17

While many say [the SEC’s] 2010 reforms did the trick… I disagree

[Rule 2a-7 reforms] don’t protect against a credit event

[Money market mutual funds operate] without a safety net

[Investors] think there’s no way to lose money

Money market funds remain susceptible to runs

Following Rule 2a-7 amendments, boards have ability to suspend redemptions.

A vast majority of investors realize money market mutual funds are not guaranteed and the funds’ prospectus’ contain appropriate disclosures.

Funds are required to hold roughly $800 billion in liquid assets, far surpassing amounts available to the funds thru the past Fed/Treasury programs.

Funds have stringent investment requirements; 97% of holdings must be first tier securities.

Money market mutual funds are investment products whose assets fluctuate in value; money market funds only hold very safe investments

Charge Response

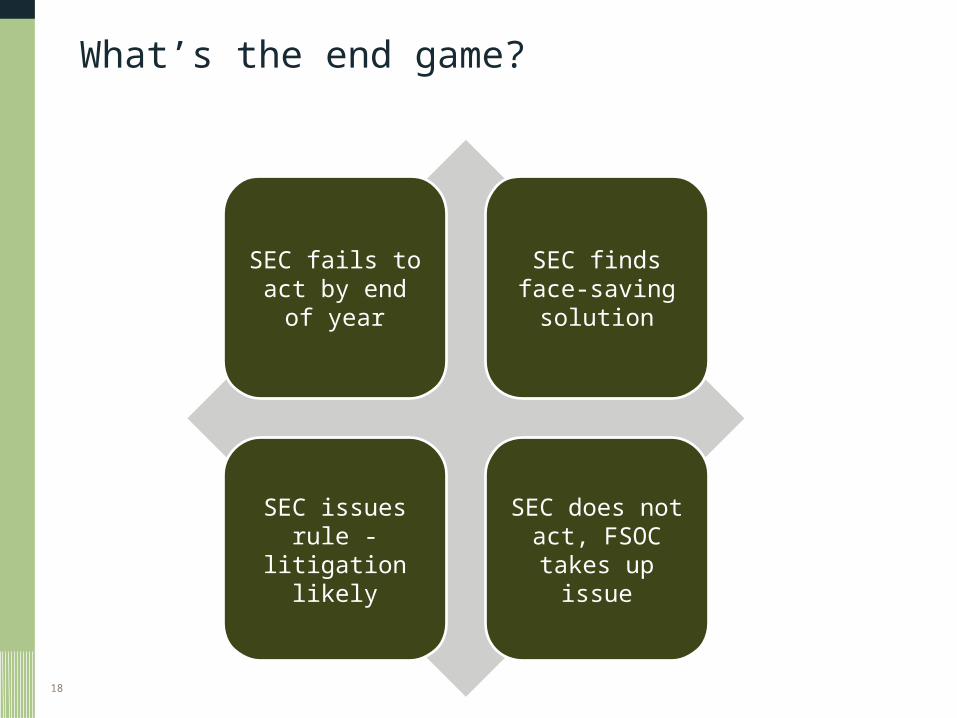

What’s the end game?

18

SEC fails to act by end of year

SEC finds face-saving solution

SEC issues rule - litigation likely

SEC does not act, FSOC takes

up issue

For institutional client use only

Formulating The Survival Guide

© 2012 FMR LLC. All rights reserved

Formulating the Survival Guide

I. Establish / update an investment policy Scope: US dollar centric or multi-currency portfolio Define Investment Objective: Capital preservation, liquidity, yield Identify permissible instruments List prohibited investments Set credit quality constraints, maturity targets, concentration limits Responsibilities

II. Analyze projected cash flows Potential Uses

Dividend payout Stock repurchase plan Debt retirement Merger & Acquisition strategy

Potential Sources Cash from operations Secured lending facilities Lines of credit

20

© 2012 FMR LLC. All rights reserved

For institutional client use only

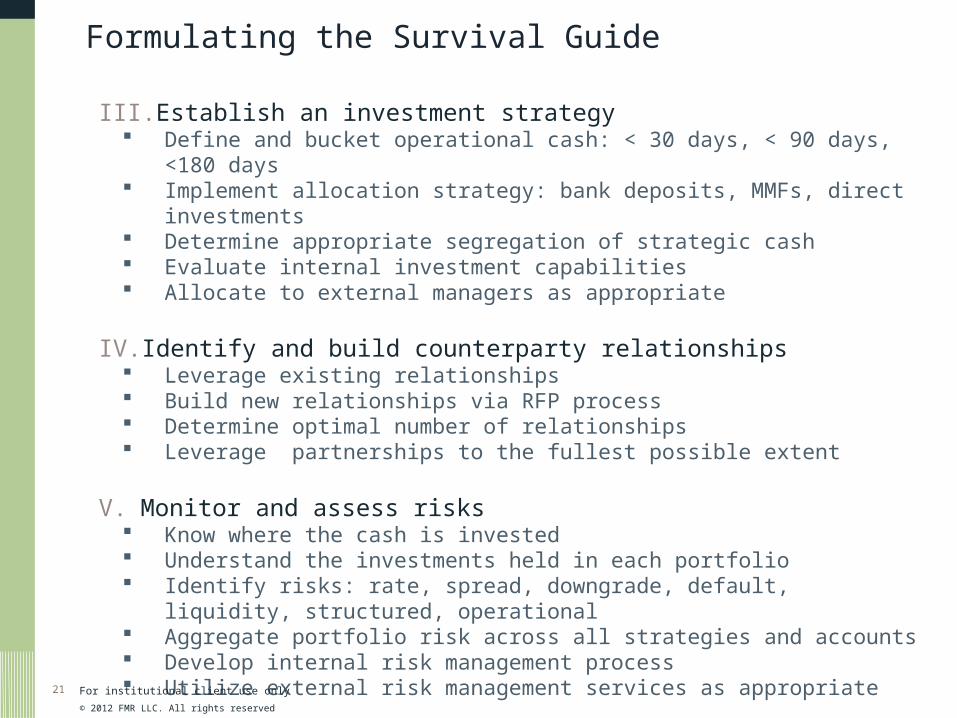

Formulating the Survival Guide

III. Establish an investment strategy Define and bucket operational cash: < 30 days, < 90 days, <180 days Implement allocation strategy: bank deposits, MMFs, direct investments Determine appropriate segregation of strategic cash Evaluate internal investment capabilities Allocate to external managers as appropriate

IV. Identify and build counterparty relationships Leverage existing relationships Build new relationships via RFP process Determine optimal number of relationships Leverage partnerships to the fullest possible extent

V. Monitor and assess risks Know where the cash is invested Understand the investments held in each portfolio Identify risks: rate, spread, downgrade, default, liquidity, structured, operational Aggregate portfolio risk across all strategies and accounts Develop internal risk management process Utilize external risk management services as appropriate

VI. Modify / update the survival guide (Maintain flexibility)21

© 2012 FMR LLC. All rights reserved

For institutional client use only

For institutional client use only

Asset Management Perspective: Robust Investment Process

Identify and Measure Relevant Risk Parameters

23 For institutional client use only

Investment Risks Significance of Risk Exposure Benefits of a Multi-Dimensional Research Process

Credit RiskPrincipal depreciation through price volatility or default

Non-reliance on Nationally Recognized Statistical Rating Organizations

Interest Rate RiskPrincipal depreciation through rising interest rates and widening spreads

Quantitative Risk Management Framework

Liquidity Risk Lost access to cash holdings Thorough analysis of underlying liquidity provisions

Structural Risk Complex documentation contains embedded risksDedicated legal team with specialized securities knowledge

© 2012 FMR LLC. All rights reserved

For Institutional Use Only

Bottom Up Foundation• Fundamental Analysis

– Fundamental foundation– Relative value assessment

• Quantitative Analysis– Proprietary risk modeling– Security and portfolio level

• Structured Analysis– Capital structure analysis– Complements fundamentals

• Value-Added Trading– Relative value assessment– Across curve and structure– Macro trends/technicals

Top Down Perspectives• Macroeconomic Inputs

– Federal Reserve expectations– Sovereign landscape– Tail risk/scenario modeling

• Sector– Basis call: transparency– Fundamental and relative value

• Yield Curve– Breakeven analysis– Slope and volatility– Relative value opportunities

• Interest Rate– Duration views– Volatility perspectives

201101-8963

For institutional client use only

© 2012 FMR LLC. All rights reserved

24

ConsistentRisk-Adjusted

Alpha

Objective:Consistent

Risk-AdjustedAlpha

Bottom-up, fundamental Investment platform complemented by top-down inputs, results in a robust and durable process.

Multi-Dimensional Investment Approach

Liquidity Management Priorities Change over time

25

© 2012 FMR LLC. All rights reserved

For institutional client use only

Summarizing the Survival Guide

• A currently vetted investment policy is the foundation of robust liquidity management

• It is critical to understand both asset and liability dynamics for accurate cashflow forecasting

• Investment goals and objectives are independent of current market conditions– Capital Preservation– Liquidity– Returns

• Cash Management is a time consuming, resource intensive multi-dimensional process– Develop a Risk vs. Return profile– Segment cash into appropriate allocations (operating, strategic, reserves)– Understand all aspects of the investible universe– Perform timely portfolio review

• Establish relationships with asset managers– Align investment priorities of asset manager with your investment goals– Investment process must be time-tested– State of the art risk management and compliance engines are key– Investment strategy communicated through monthly commentary, white papers, statements

• Continuously monitor and update your guidelines

26

© 2012 FMR LLC. All rights reserved

For institutional client use only