for official use only - all documents

TRANSCRIPT

FILE COPYReport No. 1219-BD

Bangladesh: Survey of Steel, Pulp and Paper andLeather Tanning IndustriesNovember 30, 1976

Industrial Projects Department

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may nototherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

The value of the Bangladesh Taka (Tk.) is officially setrelative to the Pound Sterling. From Ma 17, 1975 throughApril 25, 1976, the official value was 30.0 to the PoundSterling. Since the latter date the value has been changedon three occasiona, the most recent being on November 3, 1976,when it was set at 25.45 to the Pound Sterling. The Pound isfloating relative to the U.S. dollar and consequently the Taka-USdollar rate is subject to change. The exchange rate used in pre-paring the data for this report is Tk.15 - U.S.$1.

PRINCIPAL ABBREVIATIONS USED

BJMC - Bangladesh Jute Hills CorporationBTMC - Bangladesh Textile Hills CorporationTCB Trading Corporation of BangladeshBStMC - Bangladesh Steel Mill CorporationBTC - Bangladesh Tanneries CorporationBPBC - Bangladesh Paper and Board CorporationBFCPC - Bangladesh Fertilizer, Chemical and

Pharmaceutical CorporationBESC - Bangladesh Engineering and Ship-

building CorporationECIC - Bangladesh Chemical Industries

CorporationBSEC - Bangladesh Steel and Engineering

Corporation

FISCAL YEAR

July 1 through June 30

This report is based on the findings of an industrialsector mission which was in the field in December 1975, witha follow-up visit to Bangladesh in March 1976. Participatingin the work of the mission were Irwin Baskind (Chief),Ernst Bolte, Hugh McFarlane (IBRD/FAO Cooperative Program),L.F. Graham (Consultant), Ounnar Lunden (Conaultant) andRobert H. Parker (Consultant).

FOR OFFICIAL USE ONLY

BANGLADESH

SURVEY OF STEEL, PULP AND PAPER ANDLEATHER TANNING INDUSTRIES

TABLE OF CONTENTS

Page No.

SUMMARY OF CONCLUSIONS AND PRINCIPAL RECOMMENDATIONS i-ix

PART I: THE PRIMARY STEEL PRODUCING AND CONSUMING INDUJSTRIES

I. GENERAL CHARACTERISTICS OF THE BANGLADESHSTEEL INDUSTRY 1

Historical Background ........................... 1Company Structure, Ownership and Location ....... 1Current Consumption of Steel Products .... ....... 2Domestic Production and Imports .... ............. 4Steel Users: Current Total Consumption .... ..... 5Current Demand-Supply Situation .... ............. 6

II. CHITTAGONG STEEL MILL - STATUS AND CAPABILITY ............. 8

Plant Production Facilities ..................... 8Production Capacities and Capabilities .... ...... 9Costs, Prices and Profitability .... ............. 12Other Steel Products ............................ 14

III. RE-ROLLING MILLS - STATUS AND CAPABILITY .... ............. 16

Re-Rolling Mill Facilities and Products .... ..... 16Production Output and Capacity Utilization ...... 16Factors Affecting Performance .... ............... 17Structure of Costs .............................. 18Financial Results ............................... 19

IV. MEDIUM-TERM DEVELOPMENT PROSPECTS ........................ 21

Domestic Consumption Trends ..... ................ 21Improving Production Efficiency .... ............. 22Other Organizational Matters ..... ............... 25Strengthening CSM Management ..... ............... 26Proposed Expansion Project ..... ................. 27

This document has a rmtricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

-2-

Page No.

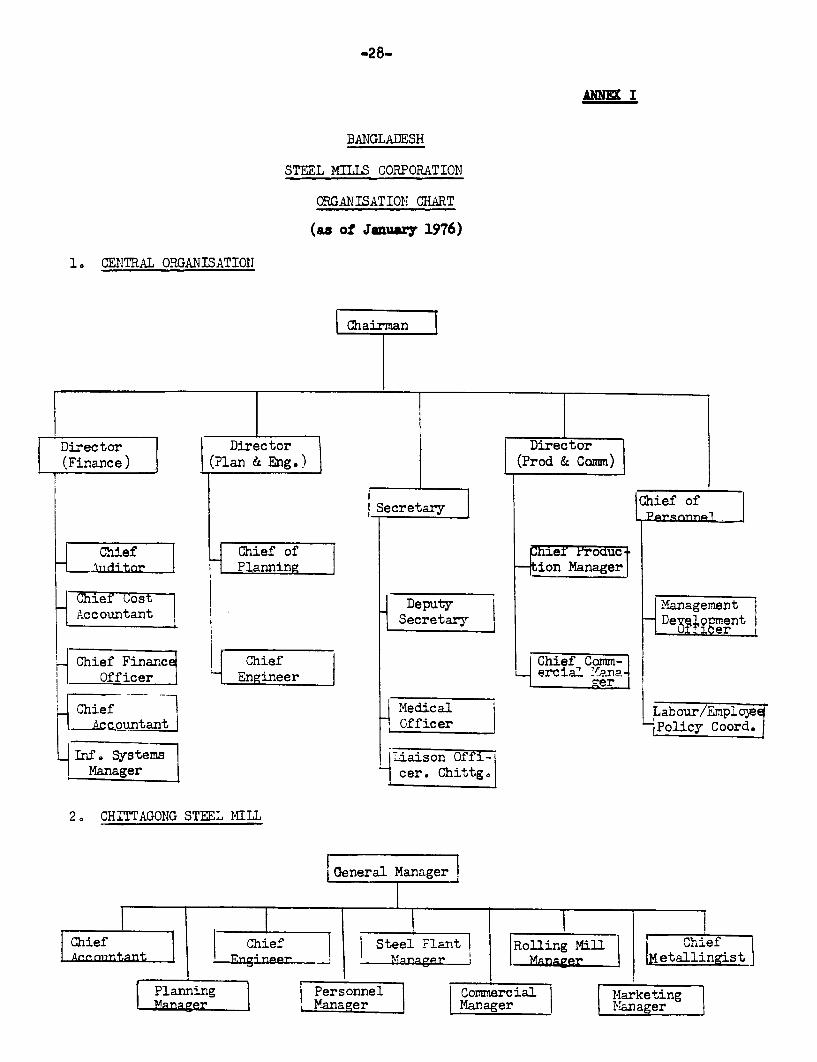

ANNEX I Bangladesh Steel Mills Corporation - OrganizationChart . ............................................ 28

ANNEX II Flow Diagram of Chittagong Steel Mill .... ........ 29ANNEX III Bangladesh Steel Mills Corporation - Enterprises,

Products, Employees and Sales Value .30ANNEX IV Bangladesh Steel Mills Corporation - Re-rolling

Mills, Installed Capacity and Actual Capability 32ANNEX V Private Sector Re-rolling Mills - Production

and Capacity Utilization .......................... 33ANNEX VI Principal Public Sector Consumers of Steel ....... 34ANNEX VII Proposal for a Sponge Iron Project .... ........... 37

STATISTICAL APPENDIX

Table 1 Chittagong Steel Mill - Production and CapacityUtilization .39

Table 2 Chittagong Steel Mill - Net Sales and Stockby Product Type .40

Table 3 Chittagong Steel Mill - Requirement of SpareParts and Consumables .41

Table 4 Chittagong Steel Mill - Analysis of Reasons forLost Production Time .42

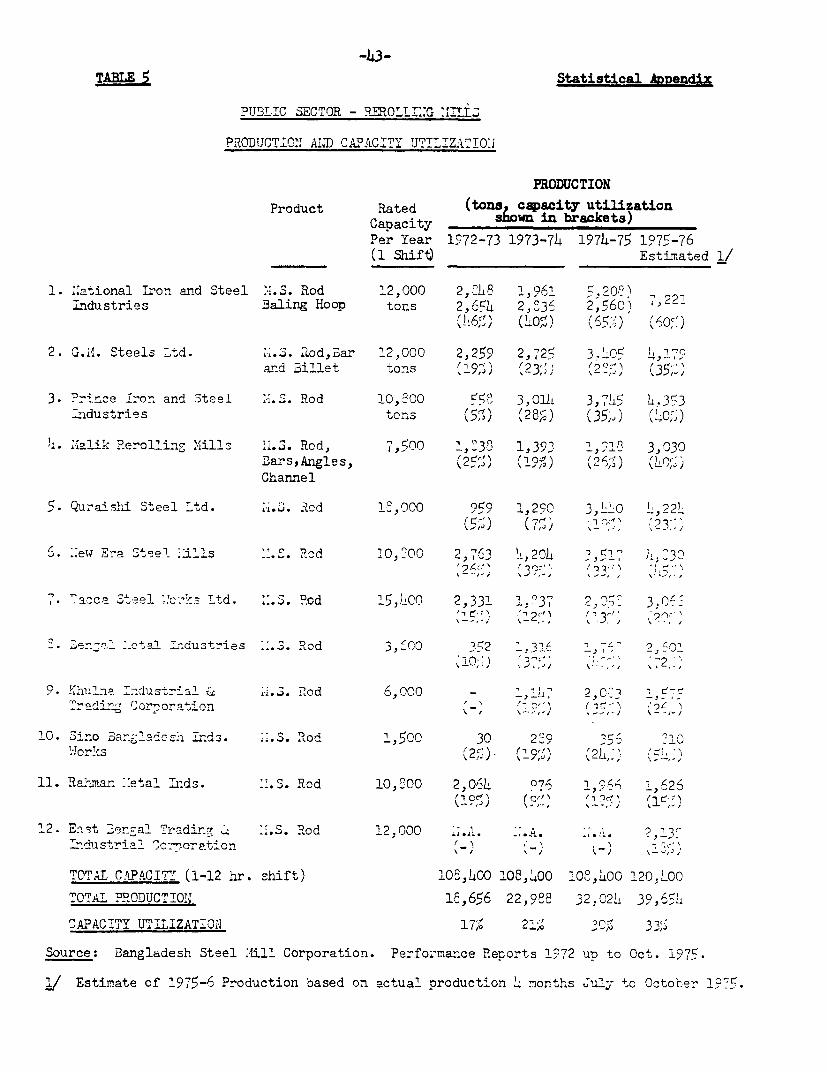

Table 5 Public Sector Re-rolling Mills - Productionand Capacity Utilization .43

Table 6 Imports of Primary Iron and Steel Goods,1973/74 and 1974/75 .44

Table 7 Imports of Iron and Steel Products, 1973/74and 1974/75 .45

Table 8 Import of Complex Iron and Steel Products,1973/74 and 1974/75 .47

Table 9 Bangladesh Steel Mills Corporation - Re-rollingMills Sales and Profits, 1972 to 1975 .48

PART II: THE PULP AND PAPER INDUSTRY

I. HISTORICAL BACKGROUND AND CURRENT STATISTICS .49

II. GENERAL MARKET CONDITIONS AND PRICES

Newsprint .52Printing and Writing Papers .54Other Paper Grades .56Pulp .56

-3-

Page No.

III. FACTORS AFFECTING PERFORMANCE

Utilization of Capacity ............................... 58

Mill Productivity ...................................... 58

Maintenance ................................. 58

Spare Parts ................................. 59Management .................................. 59

Labor ....................................... 60

Production Costs .................---------------- 60

Financial Results .63Fibrous Raw Materials .64

IV. MEASURES TO IMPROVE PERFORMANCE

Pricing Policy .66Technical Considerations .67Raw Material Supply .68Spare Parts .70Marketing .71

Printings and Writings .71Newsprint .71Pulp .72Changes in Product Line .72

Management .73

Industry Organization .74

ANNEX I Description of Mills .76ANNEX II Draft Terms of Reference for a Consultant .82

STATISTICAL APPENDIX

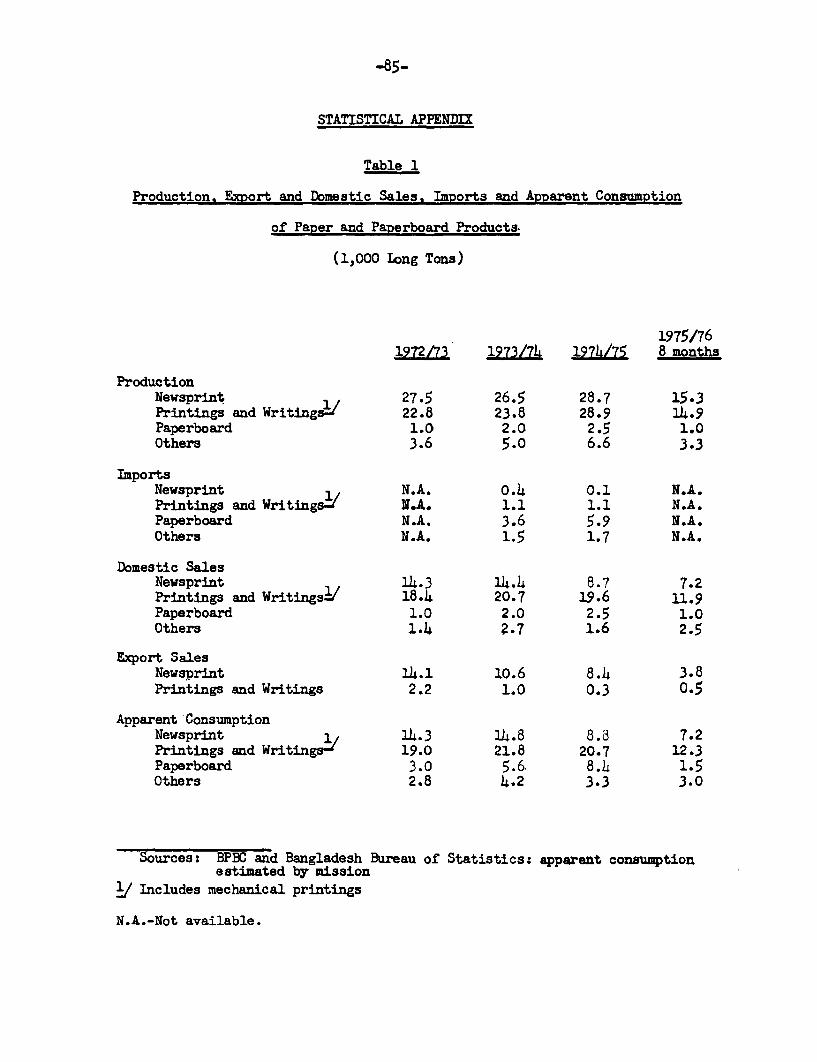

Table 1 Production, Export and Domestic Sales, Imports andApparent Consumption of Paper and Paperboard Products.. 85

Table 2 Imports of Newsprint in Selected Countries (1969-1973). 86

Table 3 Imports of Printings and Writings in SelectedCountries (1969-1973) ................................. 87

Table 4 Production of Printings and Writings in SelectedCountries (1969-1973) ................................. 88

Table 5 Average Direct Production Costs, Khulna NewsprintMlills ................................................. 89

-4-

Page No.

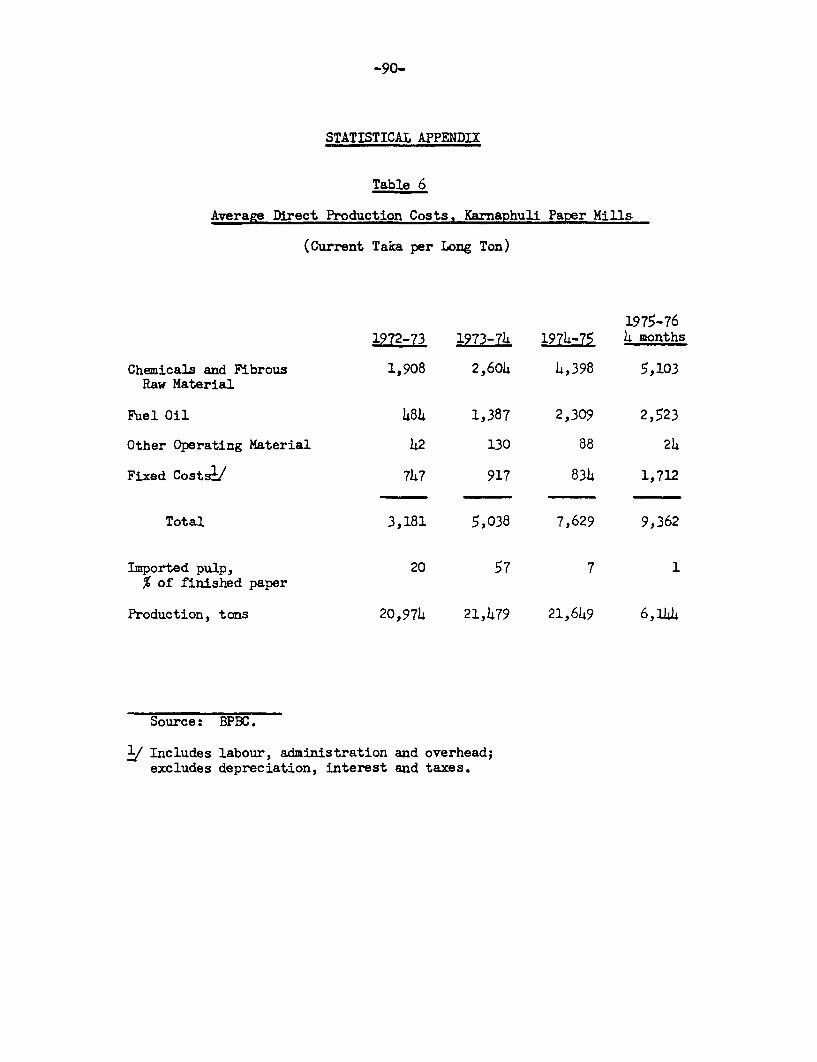

Table 6 Average Direct Production Costs, Karnaphuli PaperMills . ................................................. 90

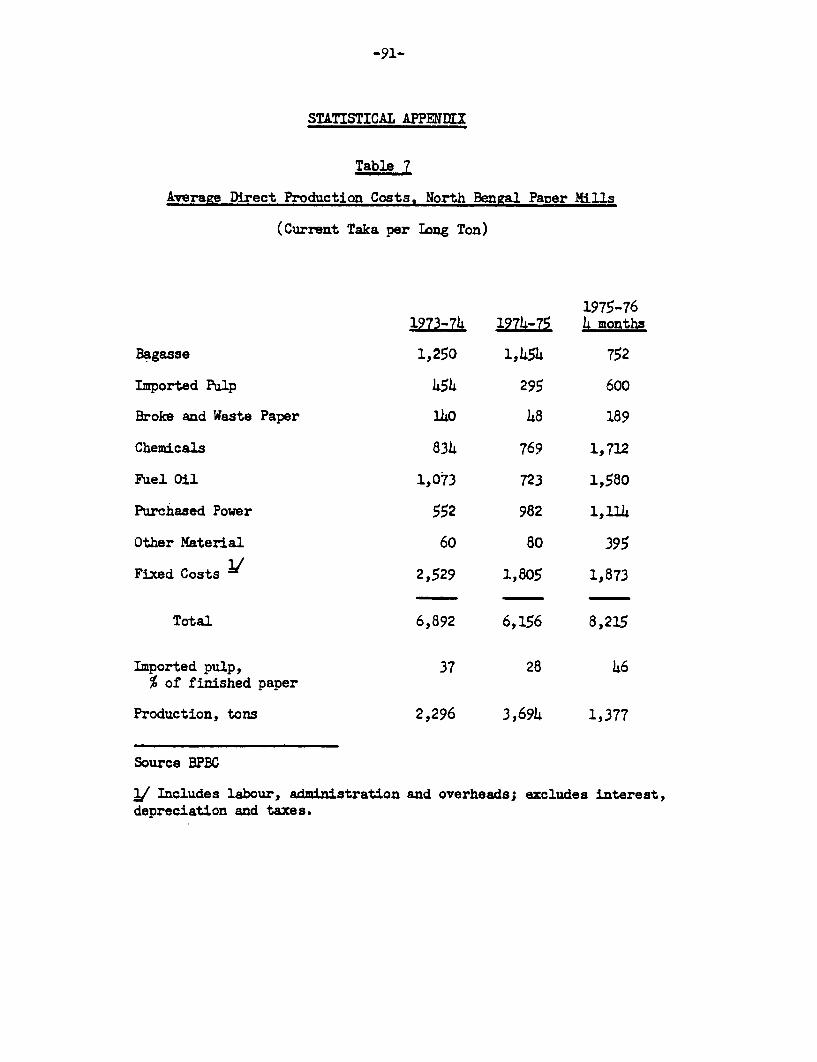

Table 7 Average Direct Production Costs, North Bengal PaperMills . ................................................. 91

PART III: THE LEATHER TANNING INDUSTRY

I. PAST DEVELOPMENT OF THE TANNING INDUSTRY .... ............... 92

II. PRESENT STATUS OF THE TANNING INDUSTRY ..................... 94

Production Capacity ................................... 94Production and Exports ................................ 95Raw Material Supply ................................... 95

III. EFFICIENCY OF THE TANNING INDUSTRY ......................... 98

Utilization of Capacity ............................... 98Technical Conditions and Performance of Tanneries ..... 98Labor and Management .................................. 99Cost Structure ........................................ 100Financial Performance ................................. 101

IV. MEASURES FOR FUTURE DEVELOPMENT ............................ 103

Supply of Raw Hides ................................... 103Price Increases ....................................... 103Processing of Finished Leather ........................ 104Change of Sector Organization ......................... 106Training Program ...................................... 106Incentives ............................................ 106

ANNEX I Tannery Processes .108

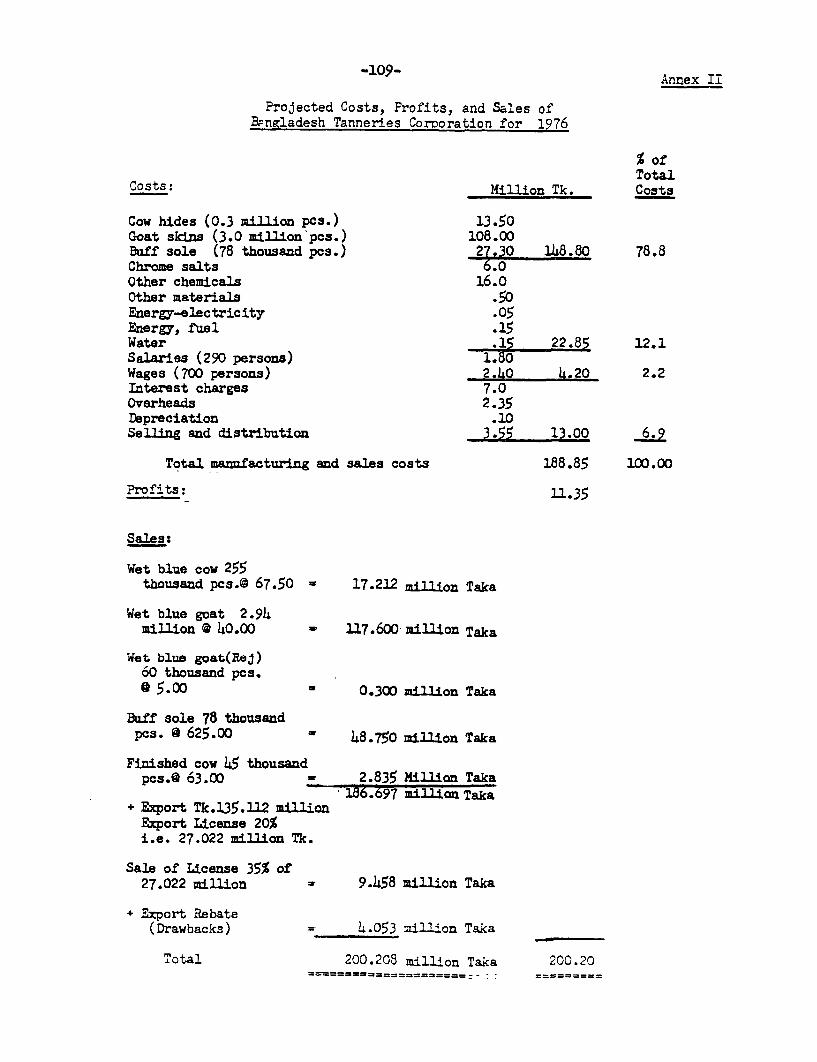

ANNEX II Projected Costs, Profits, and Sales of BangladeshTanneries Corporation for 1976 .109

ANNEX III Research, Development and Training Institutionsfor the Tanning Industry .110

SUMMARY OF CONCLUSIONS AND PRINCIPAL RECOMMENDATIONS

I. Steel Producing and Consuming Industries

i. The origins of the present day Bangladesh steel production arefound in the policies followed and measures taken during the 1960s by thePakistan Government to encourage the development of import substitutionindustries to serve the East and West Pakistan integrated market. Thelargest single enterprise in the steel sub-sector is the Chittagong SteelMill (CSM) which is publicly owned, under the control of the BangladeshSteel Mills Corporation (BStMC).l/ This mill, which converts pig iron andscrap, initiated operations in 1967 with capacity of 150,000 tons (steelingots) but was expanded to a rated capacity of 250,000 tons (steel ingots) in1970. In expectation of demand from the area of West Pakistan, the mill wasdesigned with a relatively large capacity for flat products (for both sheetand plate) along with a bar/billet shop of only some 55,000 tons.

ii. In addition to CSM, there are 29 re-rolling mills, of which 12are in the public sector (also controlled by BStMC) representing enter-prises which had been abandoned by their non-Bengali owners at the timeof independence. On a two shift-22 hour basis, the total capacity ofthese mills is estimated at almost 500,000 tons of which about 40% belongsto the public sector enterprises.

iii. CSM, both prior to and following independence, has operated atwell below rated capacity. In the first place, there are serious technicaldesign deficiencies in the melting shop which make it virtually impossibleto achieve full utilization of the four existing furnaces; effective capa-city for producing ingot steel appears to be no more than two-thirds of ratedcapacity. Since independence, and until this past year, foreign exchangeshortages, limiting availability of raw materials and spare parts practi-cally all of which are imported, have been the main constraints on produc-tion. The inappropriate product-mix design in relation to the pattern ofactaal demand in Bangladesh also has presented difficulties; as a conse-quence, utilization of capacity for producing sheet and plate has onlyoccasionally reached as high as 15 to 20% but the bar/billet shop, pro-ducing primarily billets, has been more fully utilized.

iv. Overall capacity utilization in the re-rolling mills has been ofthe order of 15% about the same as reached prior to independence. The publicsector units have had access to CSM billets and have been able to achievehigher rates; private sector mills have been completely dependent upon bil-let imports and have not fared as well due to the limited foreign exchangeallocated to meet their needs. Since late 1975, however, both sectors haveexperienced reduced demand; in spite of improving raw material supplies theynevertheless have had to cut back on production.

1/ On July 1, 1976, BStMC was merged with the Bangladesh Engineering andShipbuilding Corporation to create the Bangladesh Steel and EngineeringCorporation (BSEC).

- ii -

v. Steel consumption has been heavily concentrated in the publicsector, which accounts directly or indirectly for 80%; a major portion ofthis are non-flat rolled products for construction purposes. In 1974/75,there was a sharp decline in steel availability largely due to the foreign ex-change crisis of mid-1974. As a result of increased allocations and declinesin world prices for basic materials, output was able to expand in 1975/76.Preliminary data for that year, however, indicate only a small increase inpublic demand for steel, although measures taken to stimulate the economy andthe improved availability of cement appear to have increased demand in theprivate sector, mainly for construction. With stocks of finished steelproducts growing steadily in recent months, plans by the mills for furtheroutput expansion, as raw material supplies continued to improve, have had tobe modified.

vi. With demand heavily concentrated in the non-flat r 2lled products,CSM has modified its output mix and by specializing in 50 mm billet produc-tion in the bar/billet mill, it has been able to improve its performance.Nevertheless, December 1975 estimates of unit costs of billets (some US$295/ton excluding taxes and tariffs) exceed estimated c.i.f. imported billetsprices by about 50%.

vii. Existing official price policy permits BStMC to price its productsat average cost plus 10% without providing appropriate incentives to minimizecosts. As a consequence, CSM and the Corporation's re-rollers have earnedsubstantial profits; in turn, however, the high price levels have played arole in the current generally depressed demand situation. Little is knownof cost-price relationships among the private sector mills but with thecurrent capacity utilization at no more than 10%, some of the plants areprobably only marginally profitable.

viii. Steel consumption has declined sharply since independence and intotal is below that achieved during the 1960s. At 2 kg. per capita, it isone of the lowest levels in the world. While it is difficult to projectfuture consumption levels in view of the situation facing the country, a5% per annum increase would bring the total level by 1980 to that achievedprior to independence. It is also anticipated that the composition ofdemand will continue to favor non-flat rolled products which will in turnincrease demand for billets from CSM.

ix. The mill's existing capacity appears adequate to meet most of thesebillet needs, even without full utilization of effective capacity for ingotsteel production. There is, however, a question as to the economic justifica-tion of this production as compared to the alternative of importing billets.Under the particular price conditions obtaining for pig iron, scrap and steelbillets in December 1975 in world markets, CSM steel production may haveresulted in net foreign exchange dissavings. This would not be the case,however, if the analysis were to be undertaken using prices prevailing throughmost of the early years of the present decade; moreover, recent price quotationsfor pig iron and scrap suggest a favorable foreign exchange position again.

- iii -

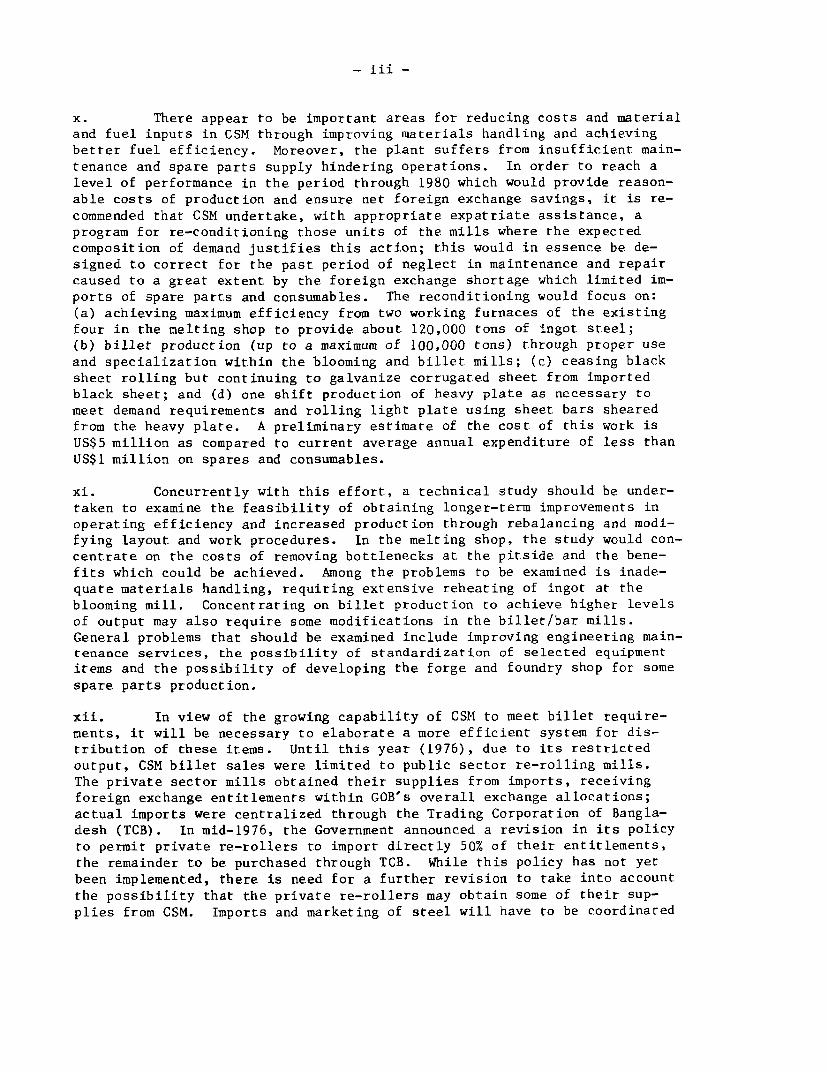

x. There appear to be important areas for reducing costs and materialand fuel inputs in CSM through improving materials handling and achievingbetter fuel efficiency. Moreover, the plant suffers from insufficient main-tenance and spare parts supply hindering operations. In order to reach alevel of performance in the period through 1980 which would provide reason-able costs of production and ensure net foreign exchange savings, it is re-commended that CSM undertake, with appropriate expatriate assistance, aprogram for re-conditioning those units of the mills where the expectedcomposition of demand justifies this action; this would in essence be de-signed to correct for the past period of neglect in maintenance and repaircaused to a great extent by the foreign exchange shortage which limited im-ports of spare parts and consumables. The reconditioning would focus on:(a) achieving maximum efficiency from two working furnaces of the existingfour in the melting shop to provide about 120,000 tons of ingot steel;(b) billet production (up to a maximum of 100,000 tons) through proper useand specialization within the blooming and billet mills; (c) ceasing blacksheet rolling but continuing to galvanize corrugated sheet from importedblack sheet; and (d) one shift production of heavy plate as necessary tomeet demand requirements and rolling light plate using sheet bars shearedfrom the heavy plate. A preliminary estimate of the cost of this work isUS$5 million as compared to current average annual expenditure of less thanUS$1 million on spares and consumables.

xi. Concurrently with this effort, a technical study should be under-taken to examine the feasibility of obtaining longer-term improvements inoperating efficiency and increased production through rebalancing and modi-fying layout and work procedures. In the melting shop, the study would con-centrate on the costs of removing bottlenecks at the pitside and the bene-fits which could be achieved. Among the problems to be examined is inade-quate materials handling, requiring extensive reheating of ingot at theblooming mill. Concentrating on billet production to achieve higher levelsof output may also require some modifications in the billet/bar mills.General problems that should be examined include improving engineering main-tenance services, the possibility of standardization of selected equipmentitems and the possibility of developing the forge and foundry shop for somespare parts production.

xii. In view of the growing capability of CSM to meet billet require-ments, it will be necessary to elaborate a more efficient system for dis-tribution of these items. Until this year (1976), due to its restrictedoutput, CSM billet sales were limited to public sector re-rolling mills.The private sector mills obtained their supplies from imports, receivingforeign exchange entitlements within GOB's overall exchange allocations;actual imports were centralized through the Trading Corporation of Bangla-desh (TCB). In mid-1976, the Government announced a revision in its policyto permit private re-rollers to import directly 50% of their entitlements,the remainder to be purchased through TCB. While this policy has not yetbeen implemented, there is need for a further revision to take into accountthe possibility that the private re-rollers may obtain some of their sup-plies from CSM. Imports and marketing of steel will have to be coordinated

- iv -

in such a manner that CSM would appear as the primary source of supply as-suming that it has taken steps to raise its efficiency as outlined in para x;imports would be undertaken to cover that part of demand which cannot besatisfied by CSM.

xiii. CSM management has demonstrated considerable competence in over-coming technical difficulties in increasing production and in modifyingoutput mix to achieve better utilization of capacity in face of emergingsteel requirements of Bangladesh. However, there is need for intensifyingand broadening management training in areas other than production engineer-ing. There is particular need to strengthen the Marketing Department topermit it to play a role in production planning; one of the priority tasksof this group would be to prepare a detailed market study of the country'sprimary steel needs in the immediate future.

xiv. There appears to be no particular advantage in retaining in thepublic sector the 12 re-rolling mills which represent "abandoned" proper-ties previously owned by non-Bengalis. In view of the stated policy ofthe Government to disinvest small and medium enterprises in this situation,these mills would qualify for such disinvestment. Given the considerableexcess capacity in re-rolling, measures for disinvestment need to be com-bined with measures for concentrating production in the most efficientunits, particularly in view of the fact that a number of the mills in boththe public and private sector are obsolete.

II. Pulp and Paper Industry

xv. The Bangladesh pulp and paper industry consists primarily of fourmajor mills. The oldest installation established in 1953 is at Karnaphuli(KPM) with a rated capacity of 30,000 tons/year of printing and writingpaper. A newsprint mill was constructed at Khulna (KNM) in 1959 with arated capacity of 40,000 tons/year of newsprint to which was added in 1965capacity for 10,000 tons/year of mechanical printing paper. The North BengalPaper Mill (NBPM) was commissioned in 1970 but was not able to actually beginproduction for sale until 1973; its rated capacity is 18,000 tons/year ofprinting and writing paper. The most recent installation is a pulp mill atSylhet (SPPM) construction of which was initiated in 1970; trial productionof this mill began in 1975 but it has not yet begun production for sale. Itsrated capacity is 24,000 tons/year of reed or bamboo pulp and 6,000 tons/yearof jute pulp.

xvi. The industry was originally conceived to serve both the East andWest Pakistan markets. Consumption in Bangladesh accounts for less than 25%of installed capacity for newsprint and 30-40% of installed capacity for

- v -

printing and writing papers. With the loss of the West Pakistan markets, 1/the country has had difficulty in finding alternative export markets, althoughduring the period of tight world supply in 1973-74 it was able to export rela-tively substantial quantities, particularly of newsprint. However, recentdeclines in international demand have resulted in sharp reduction of exportsales.

xvii. Even during the period of high demand, the industry's output wasunable to reach more than 50% of capacity due primarily to the poor operat-ing conditions of the three mills concerned. In the case of the older mills(Khulna and Karnaphuli), their physical conditions have deteriorated to thepoint where substantial expenditure will probably be necessary (particularlyat the latter) to rehabilitate them to achieve current rated capacity. Atthe North Bengal mill, serious difficulties have already been encountered inwater, power and raw material supplies to the extent that output has beenable to reach only 25% of capacity.

xviii. The study has concluded that before any action program can beformulated to ensure the future viability of this industry, major effortswill have to be made to re-assess market conditions for the various productsand to appraise the actual operating conditions of the three units which arein operation.

xix. In the case of Karnaphuli (KPM) the necessary feasibility studyto determine rehabilitation needs is being undertaken by a consultant teamfinanced under the IDA First Technical Assistance Credit (409-BD). Itsreport is expected by the end of 1976. For Khulna (KNM), the CanadianInternational Development Agency (CIDA) is providing assistance; in a firstphase, a technical expert was sent (September) to assess immediate spare partsrequirements for maintaining a reasonable level of output for the next sixmonths. Later this year, a team will analyze the overall situation of themill to determine the extent of rehabilitation requirements in the light ofits assessment of market developments and raw material and other supplyconditions. An extensive management assistance program is being provided byKreditanstadt fur Wiederaufbau (KfW) to the Sylhet pulp mill in the first twoyears of its operations including technical production and marketing aspects.

xx. The only major installation which is not currently receiving assis-tance in solving operational and associated problems is the North BengalPaper Mill (NBPM). The Government has agreed to employ qualified consul-tants to re-assess the overall situation of the mill. Given expected develop-ments in world demand for paper and newsprint, and especially the conditionsprevailing in potential nearby markets, there appear to be excellent prospectsfor developing exports of newsprint and, to a lesser extent, paper products.Improvements in quality are essential and will have to be accompanied by

1/ In the trade agreement with Pakistan completed in May 1976, there isprovision for some paper exports from Bangladesh. This is presumablya short-term arrangement and prospects for longer-term development ofthis trade require further analysis.

- vi -

aggressive marketing efforts. CIDA is considering providing technical assis-tance in the marketi.ng field at Khulna while a marketing advisor is beingprovided by KfW to Sylhet.

xxi. Because of their poor physical and/or operating conditions andlow capacity utilization, the three paper and newsprint mills have incurredhigh unit operating costs since independence. The situation was aggravatedby the policy adopted by the Government which fixed selling prices, particu-larly for domestically marketed newsprint, at well below costs of production.In April 1976 the Government announced an increase in the local newsprintprice to a level above current operating costs (from an average of about3,300 taka/ton to 5,600 taka/ton) and its intention to raise other paperprices (from an average of about 7,100 taka/ton to an expected level of9,400 taka/ton). The Government also acted to ease somewhat the criticalcash shortage of the Corporation by converting some of the existing short-term debt of KPM to equity. The operating deficits resulting from theprevious price policy had created a serious cash flow problem such thatthe mills had on occasion not been able to cover the local counterpart cur-rency requirements for imported spare parts made available through foreignassistance programs.

xxii. The main fibrous raw materials of the industry are bamboo (usedat Sylhet and KPM), bagasse (at NBPM) and indigenous hardwoods (used at KNMand KPM). The quality of the bamboo has deteriorated somewhat and while thesupply does not create major difficulties at this time, should mill produc-tion rise, there could be fiber supply problems at KPM. The supply ofbagasse for NBPM will require re-assessment. Some concern is also beingexpressed over hardwood supplies. The CIDA team to assess Khulna will includea review of this problem; the i.mprovement in raw material supplies for Karnap-huli is one of the objectives of a major regional development program in thatarea being undertaken by the Swedish International Development Agency (SIDA).In connection with these aspects, consideration is being given by these millsto using pulp produced at Sylhet which originally had been expected to beexported to West Pakistan; SPPM anticipates no difficulty in exporting itsproduction of high grade jute pulp for which external demand is relativelystrong.

xxii.i. The organization of the industry has also presented various prob-lems hindering efficient performance of the mi.lls. Since independence thethree paper and newsprint mills have been controlled by the Bangladesh Paperand Board Corporation (BPBC) which also controlled some small related enter-prises. On the other hand, the Sylhet pulp mill was controlled by theBangladesh Forest Industries Development Corporation (BFIDC). In January1976, the Government announced its intention to transfer Sylhet to BPBCwhile at the same time announcing the merger of BPBC with two other Corpora-tions (Bangladesh, Fertilizer, Chemical and Pharmaceutical Corporation andBangladesh Tanning Corporation).I/ The transfer of the Sylhet mill was delayed

1/ The formal merger of these three corporations, to create the BangladeshChemical Industries Corporation, (BCIC), occurred on July 1, 1976.

- vii -

causing considerable confusion over organizational responsibilities and delay-ing the completion of arrangements for external assistance.

xxiv. In accordance with the recently published guidelines definingthe relationships among the Government, the Public Sector Corporations andthe individual enterprises, it is expected that the mills will be givenconsiderable operational autonomy. As the new merged Corporation controllingthese mills includes a very large number of units producing heterogenousitems, there is some concern that the coordination required to make thepulp and paper industry a viable one will be made even more difficult. TheGovernment has agreed that, within the Planning Cell of the new merged cor-poration, a special unit for the industry will be established to monitorlong-term developments. This unit will be responsible for periodic reportingon the developments of the industry and for keeping the Association informedof the progress achieved under the current assistance programs.

xxv. In the meantime, given the fact that studies are underway orplanned to appraise performance at the four major mills, it is essentialthat steps be taken to ensure the coordination of these efforts. In partic-ular, it is necessary that the decisions made as a result of the recommenda-tions of the individual studies take into account the overall developmentstrategy of the industry. For this purpose, the Government has agreed to theappointment of a senior pulp and paper industry consultant to assist in theevaluation of the individual studies, in the overall assessment of fibrousmaterial supplies (including possible transfers among mills) and of marketpossibilities, and in the elaboration of a longer-term development plan forthe industry. The adviser will be attached to the Planning Cell mentioned inthe previous paragraph.

xxvi. In addition to reviewing the existing product mix of the industry,the advisor will assist in reviewing new product possibilities; particularimportance is attached to an assessment of potential for producing highgrade dissolving pulp to be used in manufacturing polynosic fibers for thelocal textile industry which could reduce the import requirements of thelatter.

III. Leather Tanning Industry

xxvii. The tanning industry in Bangladesh produces semi-finished "wetblue" leather for exports and finished leather for the local market. Leatherexports reached Tk 219 million in 1974/75 and for 1975/76 are provisionallyestimated at Tk 350 million, taking a third place in export earnings afterjute and jute products. Revenues from exports of goat leather are about Tk250 million and Tk 100 million result from exports of cow leather. Domesticconsumption of finished leather (practically all cow leather) is small, atabout Tk 20 million per year.

- viii -

xxviii. There are over 200 tanneries in the country, most of them smalland with primitive tanning equipment. Only about 40 mechanized larger tan-neries are exporting their products. Twenty-four, mostly large tannerieswhich have been nationalized as abandoned property after independence, formpart of the Bangladesh Tanneries Corporation (BTC), a public sector corpora-tion;1/ the remaining tanneries are privately owned. Recently, the Govern-ment put up for sale some of its facilities.

xxix. Utilization of installed tanning capacity has been extremely lowat about 30%. Tanneries in the public sector have utilized less than 20%of their capacity due to poor operating condition of equipment, inexperienceof management and staff and lack of working capital to buy raw materials;private tanneries have reached about 50% capacity utilization on average.In May 1975, all public tanneries were closed down; eight tanneries werereopened in January 1976. The Government plans to sell 12 of its tanneries;however, considering the past performance of public tanneries it may beadvisable to return all tanneries to private ownership. The new tanneryplanned by the Government with external assistance will represent an importantstep toward production and export of finished leather.

xxx. The tanneries are generally in poor physical condition due to inade-quate maintenance and improper operation of equipment. The staff is mostlyinexperienced and the different chemical and mechanical operations of thetanning process are performed without the necessary understanding and preci-sion. However, while the local market for finished leather has sufferedfrom bad product quality, export demand has been strong due to the highquality of the raw hides, particularly goatskins.

xxxi. About 95% on average of the total production costs of wet blueleather for export are raw material costs for hides and imported chemicals.The value added in tanning is extremely low, demonstrating the present limitedeconomic function of the industry.

xxxii. The organization of the hide trade has an adverse effect on quan-tity, quality and costs of production of the tanning industry. Slaughteringis widely dispersed throughout the country and costs associated with collec-tion and transport are high. Thus, producers get a small share of the revenuesfrom skin sales and receive little price incentives to supply a maximumquantity of hides of good quality. Many hides, particularly from cows, do notreach the tanneries or are damaged due to improper flaying and insufficientcuring. Ways to improve operations of the hide trade should be studied with aview to a possible involvement of cooperatives or similar organizations.

1/ In July 1976, BTC was merged with the Bangladesh Paper and BoardCorporation and the Bangladesh Fertilizer, Chemical and PharmaceuticalCorporation to form the Bangladesh Chemical Industries Corporation(BCIC).

- ix -

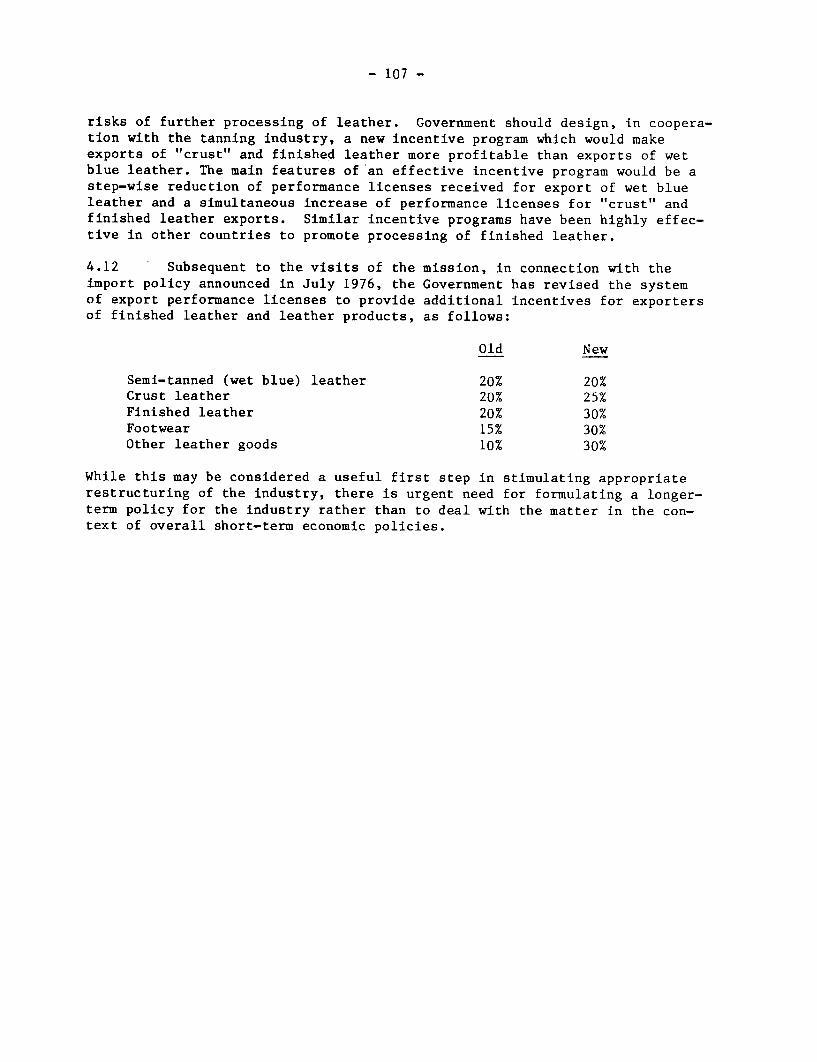

xxxiii. Private tanneries are highly profitable, while tanneries in thepublic sector are losing money. Direct revenues from exports of semi-finishedwet blue leather do not cover costs of production, but the systems of exportperformance licenses and rebates make leather exports profitable. Productionof finished leather for the local market is also profitable. The present(March 1976) export performance license system gives no incentive to improveoperations of the tanneries or to process finished leather for export. A moreefficient export promotion system would provide for a phased program forreduced incentives for export of wet blue leather and relatively higherincentives for export of finished leather.

xxxiv. There are excellent prospects to increase earnings of foreignexchange from leather exports. A program should be developed to increasethe degree of processing from wet blue to "crust" and finished leather forexport. This program would-include a change in the export incentive system,disinvestment of public tanneries, foreign technical assistance and localefforts to train tanners of the necessary high technical standard, and prep-arations for joint ventures with foreign tanners and importers of leatherwho would supply technical and marketing expertise.

xxxv. In connection with the import policy for July-December 1976 whichwas issued in July, the Government announced an increase in export incentivesfor finished leather and leather products; export performance licenses forthese items have been raised above the level granted for semi-finished lea-ther. While these are useful first steps in the required restructuring of theindustry, it is necessary to elaborate a longer-term policy to achieve thispurpose.

PART I: THE PRIMARY STEEL PRODUCING AND CONSUMING INDUSTRIES

CHAPTER I. GENERAL CHARACTERISTICS OF THEBANGLADESH STEEL INDUSTRY

A. Historical Background

1.1 In the late 1950's, the area now Bangladesh had only eight enter-prises in the basic metals industries. These were re-rolling mills producingin total about 8,000 tons per year of rolled products from imported billets.The output of the plants covered only a small percentage of the country'srequirements at the time.

1.2 As part of the second Five Year Plan, it was decided to expand theiron and steel industry to meet the internal demand. In 1963 an agreement wasreached between the government-owned East Pakistan Industrial DevelopmentCorporation's Iron and Steel Works, now the Chittagong Steel Mills Limited(CSM), and Kobe Steel Limited of Japan to set up a steel melting plant, basedon three open hearth furnaces using imported pig iron and scrap, with acapacity of 150,000 tons of steel ingot per year and steel rolling mills andgalvanizing plant. The first open hearth furnace was commissioned in February1967 and the other two shortly thereafter. In the same year a contract forexpansion up to a capacity of 250,000 tons per year of steel ingot was signedwhich was completed by the end of 1970. Total investment cost of the plantwas Tk 500 million or approximately US$100 million based on the exchange rateapplicable at that time; about half the expenditure was in foreign exchange.

1.3 For a variety of reasons, including serious layout defects, technicalproduction problems and over-optimistic assessment of continuous running time,the steel plant capacity utilization in its first four years of operationdropped from 45% in the first year to 27%, or 40,100 tons in 1970/71. Thedisturbances experienced at the time of the struggle for independence alsocontributed to the poor performance in that year.

1.4 During the 1960's there was also a substantial expansion of pri-vate sector re-rolling mills and for production of a variety of metal products,including simple fabricated items such as nails and baling. This growthlargely reflected the Government's incentive and other policies for promotingcapital investment and resulted in considerable excess capacity (see ChapterIII).

B. Company Structure, Ownership and Location

Public Sector

1.5 The steel industry of Bangladesh currently revolves mainlyaround the Bangladesh Steel Mills Corporation (BStMC) which is government

- 2 -

owned. 1/ This Corporation controls the steel mill, 12 re-rolling plants(which were abandoned by their non-Bengali owners at the time of indepen-dence), several foundries and steel fabrication units and two aluminum pro-ducts enterprises. In 1974/75 the Corporation employed about 7,000 wage andsalary earners and had sales of Tk. 591.1 million. Approximately 50% of bothemployees and sales are related to the Chittagong Steel Mill. A detailedbreakdown of the Corporation's enterprises showing locations, products, numberof employees and sales is in Annex III.

1.6 Although each of the Corporation's enterprises has a manager re-sponsible for achieving production and financial targets and an accountantto control finance and costs, there is a strong centralized control. Market-ing also has been centralized in the Corporation, and in programming produc-tion of re-rolling mills account is taken of customer destination of products.Production targets, which are set centrally, have in the past been largely aquestion of allocating available billets according to past performance andcapacity. Products pricing is also carried out centrally by submission ofrecommendations to the Price Advisory Board of the Ministry of Commerce.While CSM has some capacity for producing rolled products, most of its salesare in the form of billets supplied to the public sector re-rolling mills.The private sector mills obtain their billet supplies from the governmentimporting agency, the Trading Corporation of Bangladesh (TCB).

Private Sector

1.7 In the absence of a recent census of industry it is difficultto be certain of the actual position in the private sector. However, dis-cussions with the General Secretary of the Re-rolling Mills Associationindicated that there are 17 re-rolling mills operating in the private sector.Five are located in Chittagong, ten in Dacca and two in Khulna. Their totaloutput has been at an average annual level of 22,500 tons over the past threeyears. No information on employment or sales was available for the privatesector, but based on public sector ratios the mission estimates employmentat about 1,100 and sales at some Tk 150 million. A list of the private sectorre-rolling mills together with details of products and capacities is shown asAnnex V.

C. Current Consumption of Steel Products

1.8 Based on import data provided by the Bangladesh Bureau of Statis-tics and information from the Bangladesh Steel Mills Corporation and theRe-Rolling Mills Association, an estimate has been made of total apparentconsumption of both primary steel products and the steel content of finished

1/ In July, 1976, BStMC was merged with the Bangladesh Engineeringand Ship-building Corporation (BESC) to form the Bangladesh Steel andEngineering Corporation (BSEC).

- 3 -

steel products for the periods 1973/74 and 1974/75. 1/ These consumptionfigures are for steel only, excluding cast iron pipes and foundry products,and are as follows:

(in thousand tons)1973/74 1974/75

Sales of goods produced from domestic steel 49.4 47.4Sales of goods from re-rolling of importedbillet 30.9 12.9

Import of finished steel goods (sheet,rail, plate, etc.) 67.0 53.3

Sub-total primary steel products 147.3 113.6

Simple semi-finished products (structuralparts, nuts, bolts, tooling) 12.7 7.7

Intermediate finished products (locksmithwares, chains, springs and leaves) 0.7 0.6

Complex products (pump, truck chains,bicycle parts, etc.) 27.0 12.5

Sub-total finished and semi-finished 40.4 20.8

TOTAL 187.7 134.4

Source: Mission estimates.

1.9 A study prepared by BStMC has estimated average primary steelconsumption in the country during the period 1965-71 at 160,000 tons peryear; the 1974/75 level of consumption of about 134,000 tons thus representsa substantial decline from pre-independence. At less than two kilograms percapita, this level represents one of the lowest in the world.

1/ Publi-shed dat-aawn steel pr otuction->i-n-;angl'adesh tend to be mislead-ing. For extamp1res, the Bangila'cresn Montnly Statistics Bulletin showeda total-production of steel i-n:,the vear 1973/74 of 125,526 tons.How-ever, closer-.-examination reveals' that there is a considerable amountof double countine such that the billet, sheet bar and slab outputs areincluded as well as tne proaucts produced 'from these, including sheet,reinforcing bars and flat bars.

- 4-

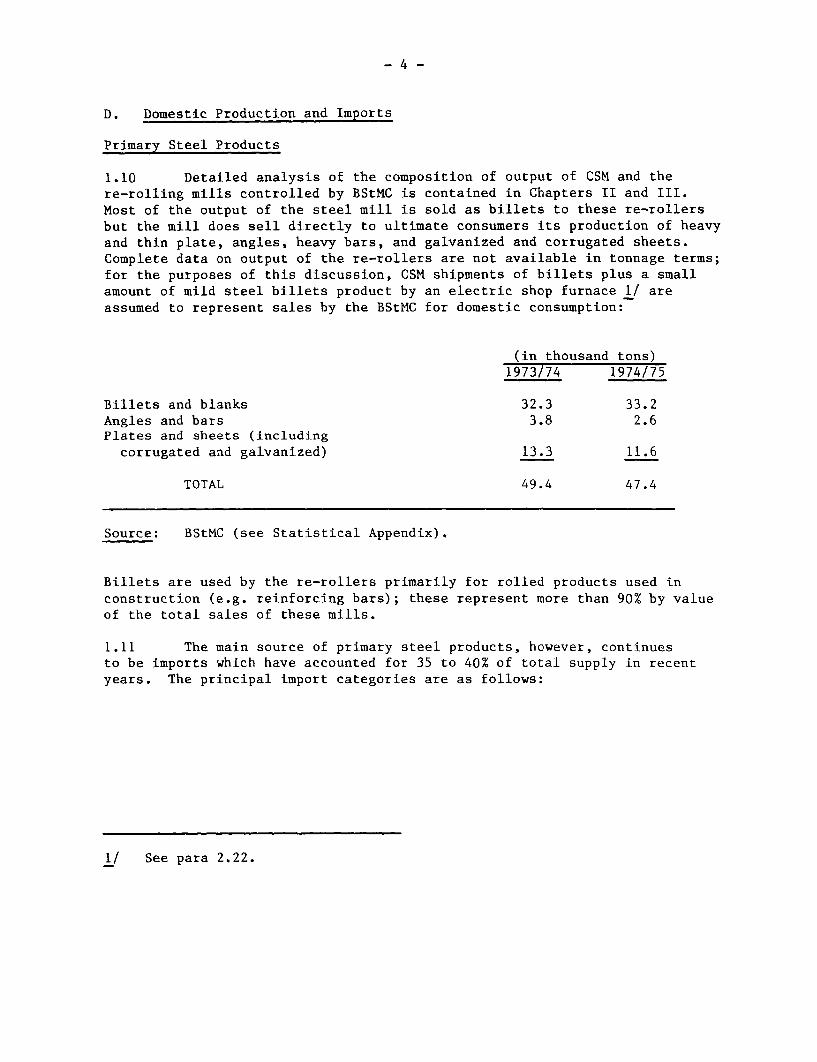

D. Domestic Production and Imports

Primary Steel Products

1.10 Detailed analysis of the composition of output of CSM and there-rolling mills controlled by BStMC is contained in Chapters II and III.Most of the output of the steel mill is sold as billets to these re-rollersbut the mill does sell directly to ultimate consumers its production of heavyand thin plate, angles, heavy bars, and galvanized and corrugated sheets.Complete data on output of the re-rollers are not available in tonnage terms;for the purposes of this discussion, CSM shipments of billets plus a smallamount of mild steel billets product by an electric shop furnace 1/ areassumed to represent sales by the BStMC for domestic consumption:

(in thousand tons)1973/74 1974/75

Billets and blanks 32.3 33.2Angles and bars 3.8 2.6Plates and sheets (including

corrugated and galvanized) 13.3 11.6

TOTAL 49.4 47*4

Source: BStMC (see Statistical Appendix).

Billets are used by the re-rollers primarily for rolled products used inconstruction (e.g. reinforcing bars); these represent more than 90% by valueof the total sales of these mills.

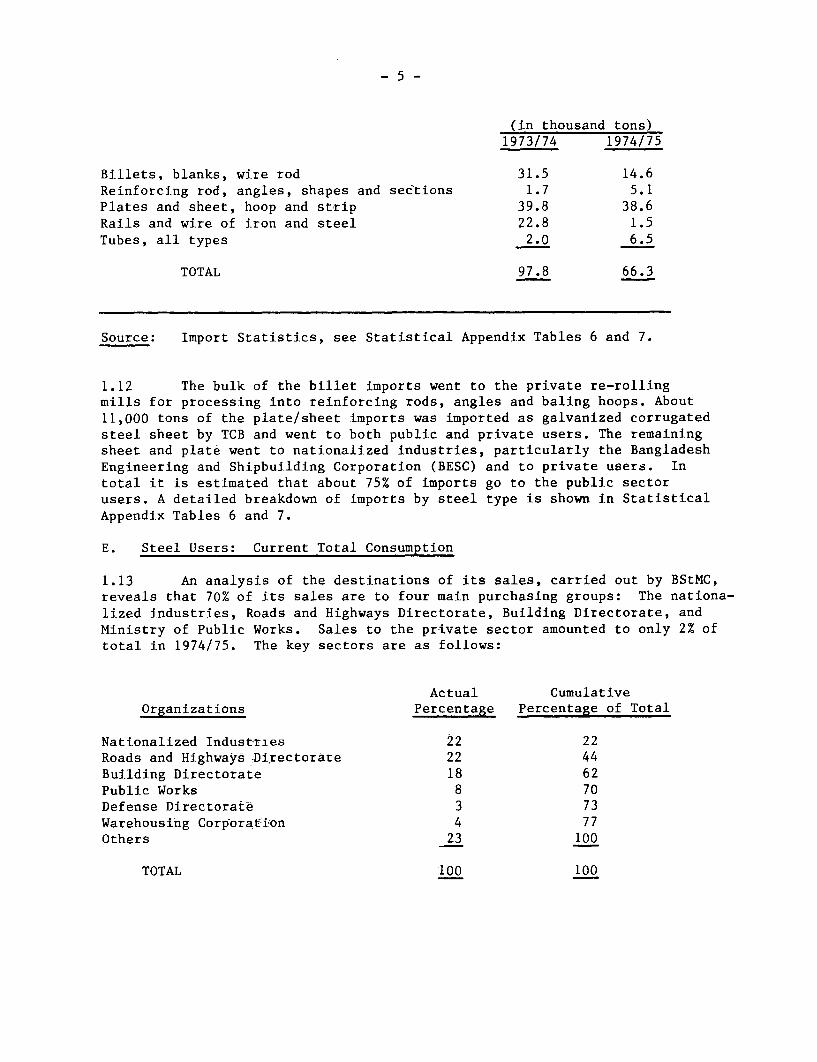

1.11 The main source of primary steel products, however, continuesto be imports which have accounted for 35 to 40% of total supply in recentyears. The principal import categories are as follows:

1/ See para 2.22.

-5-

(in thousand tons)1973/74 1974/75

Billets, blanks, wire rod 31.5 14.6Reinforcing rod, angles, shapes and sections 1.7 5.1Plates and sheet, hoop and strip 39.8 38.6Rails and wire of iron and steel 22.8 1.5Tubes, all types 2.0 6.5

TOTAL 97.8 66.3

Source: Import Statistics, see Statistical Appendix Tables 6 and 7.

1.12 The bulk of the billet imports went to the private re-rollingmills for processing into reinforcing rods, angles and baling hoops. About11,000 tons of the plate/sheet imports was imported as galvanized corrugatedsteel sheet by TCB and went to both public and private users. The remainingsheet and plate went to nationalized industries, particularly the BangladeshEngineering and Shipbuilding Corporation (BESC) and to private users. Intotal it is estimated that about 75% of imports go to the public sectorusers. A detailed breakdown of imports by steel type is shown in StatisticalAppendix Tables 6 and 7.

E. Steel Users: Current Total Consumption

1.13 An analysis of the destinations of its sales, carried out by BStMC,reveals that 70% of its sales are to four main purchasing groups: The nationa-lized industries, Roads and Highways Directorate, Building Directorate, andMinistry of Public Works. Sales to the private sector amounted to only 2% oftotal in 1974/75. The key sectors are as follows:

Actual CumulativeOrganizations Percentage Percentage of Total

Nationalized Industties 22 22Roads and Highways ,Di.rectorare 22 44Building Directorate 18 62Public Works 8 70Defense Directorat-e 3 73Warehousing Corporat4-on 4 77Others 23 100

TOTAL 100 100

- 6 -

1.14 The private sector Re-Rolling Mills Association did not have anydetailed information on the destinations of sales of its members but estimatedthat 85% of its sales were linked to the public sector even though theydelivered large quantitites to private construction firms. The reason forthis was that the bulk of the work of private construction companies was forpublic enterprises who contract for labor and organization and supply thematerials themselves. The destination of sales in the public sector weremainly to the following:

Roads and HighwaysBuilding DirectorateAgricultural Inputs CorporationMinistry of CommunicationPort Authority

1.15 Of domestic primary steel production, 93% is directly or indirectlylinked with the public sector. If imports are taken into account, then 84% ofthe total consumption of primary steel goods in Bangladesh goes to the publicsector, mostly in construction. In view of this finding, it is clear thatfuture demand for steel in Bangladesh will be closely linked with the levelsof Government development expenditure on bridges'and highways, public buildingsand factories, and houses.

F. Current Demand-Supply Situation

1.16 Based essentially on imported inputs, the Bangladesh steel industryhas been extremely sensitive to foreign exchange availabiliti.es. From thetime of independence through 1974, the major constraint on output was thelimited supply of raw materials due mainly to the low level of foreign ex-change made available to the industry; rising prices starting in 1973 in worldmarkets for these inputs and delays in obtaining shipments presented addi-tional difficulties. At the same time, labor unrest, spare parts shortagesand the loss of some technical and management personnel also played somerole in the failure of output to rise above pre-independence levels.

1.17 Beginning in early 1975, there was a marked change in the environ-ment. Some liberalization of imports was undertaken by the Government, allo-cating increased foreign exchange to the sub-sector while raw material pricesin world markets began to decline and delays in shipping were reduced.In November 1975, CSM achieved its peak production level at an annual rateof 150,000 tons of ingot.

1.18 At the same time, however, demand conditions for finished goodsbegan to deteriorate, largely as a result of a reduced volume of purchases bythe government agencies accounting for the bulk of primary steel consumption.As shown in the tables in previous sections, the total volume of sales ofboth public and private sector enterprises declined in 1974/75 as comparedto 1973/74. Stocks of billets of CSM rose by more than 2,000 tons betweenJune 1974 and June 1975, and an additional 6,000 tons in the period July1975 through February 1976, reaching a level of over 12,000 tons.

1.19 Preliminary estimates of output in 1975/76 indicate a somewhathigher level of production as compared to the previous year at CSM as well asamong the re-rollers:. But sales have failed to increase as much as produc-tion. Towards the end of the fiscal year, CSM cut back sharply on its acti-vity in the face of growing stocks.

CHAPTER II. CHITTAGONG STEEL MILL - STATUS AND CAPABILITY

A. Plant Production Facilities

2.1 The Chittagong Steel Mill began operations in 1967 having beenconstructed on a turn-key basis by Kobe Steel of Japan with an initial capa-city of 150,000 tons per year of steel ingots and steel rolling mill facili-ties. In 1970, the steel melting capacity was raised to 250,000 tons per yearof steel ingots, by adding an additional 60 ton open hearth furnace to thethree initially installed. Operated on full capacity these facilities couldturn out 172,000 tons of finished steel products in the form of billets,bars, angles, sheets and plates. A flow diagram of the process from receiptof the raw material to production of finished steel is shown in Annex II.

2.2 The principal elements in the designed capacity of CSM are sum-marized as follows:

Shop Products Rated Capacity

Melting Shop Steel Ingots 250,000 tonsper year - threeshifts

Blooming Mill Billets, Sheet 146,000 tonsBars, Slabs and per year - threeAngles shifts

Heavy Plate 6mm-25mm MS 57,000 tonsMill Plate

Billet & Bar Billets - 50mm ; 55,000 tonsMill M.S. Bar - per year - three

12 to 50 mm shifts

Sheet Mill Thin Plate 15,000 tons3 to 6 mm per year

BP Sheet 16 45,000 tonsto 30 g. per year

Galvanizing Mill Galvanized 60,000 tonsSheet or Corru-gated G Sheet

-9-

B. Production Capacities and Capabilities

Melting Shop

2.3 Over the first eight months of 1975/76 the melting shop has beenworking at the highest level of utillization of installed capacity achievedsince 1967/68, which was the first full year of operation. Details of pastproduction and utilization are as follows:

1975/76Installed Est. based onCapacity 1969/70 1972/73 1973/74 1974/75 July to Feb.

Crude SteelIngot 250,000 54,138 67,968 73,670 76,410 103,000 1/

CapacityUtili-zation (three-shifts) (22%) (27%) (30%) (31%) (41%)

2.4 In its basic design the melting shop has an installed capacityof 250,000 tons per year of steel ingots from its four open hearth furnaces.However, its effective capacity is less than 200,000 tons per year basedon continuous operation of three furnaces, in three shifts. Four furnacescannot all be operated to their maximum capacity due to congestion in thepitside where cross travel cranes obstruct simultaneous operation and to thelimited space available for teeming, stripping, cooling and resetting theingot moulds.

2.5 The recent upturn in production is directly attributable to twofactors, i.e. removal of the raw material constraint and the initiativetaken by CSM management to relieve the problem of congestion and handlingin the steel casting bay by casting larger ingots.

Ingot Rolling Plant

2.6 There are two ro±itng rn1Lis that are teca direct by steel ingots,the blooming mill :and the heavy plate mill;'-utilization of the bloomingmill has steaaL-Ly i-ncreased sirnce independence, and currently it is runningat the highest-leveFl sihce 1968T/69. On the orner hand, the heavy platemill after reacning a utilllation of 16% -in 19-:73/74 has fallen off badlydue to a lack of demand for its prdoducts. Details of past production andutilization are shown below:

1/ More recent data from CSM indicate a crude steel output of 90,000tons for the year.

- 10 -

19 75/76

Installed Est. based onCapacity 1969/70 1972/73 1973/74 1974/75 July to Feb.

Blooming Mill(tons) 146,000 50,505 48,236 46,175 56,654 79,000

(CapacityUtilization) (three shift) (35%) (33%) (32%) (39%) (54%)

Heavy PlateMill (tons) 57,000 - 6,168 8,852 6,838 -

(CapacityUtilization) (three shift) NIL (11%) (16%) (12%) NIL

Total IngotRolling(tons) 203,000 50,505 54,404 55,027 63,492 79,000

(CapacityUtilization) (25%) (27%) (27%) (32%) (39%)

2.7 The blooming mill installed capacity is 146,000 tons per yearbased on a three shift-25 day/month operation. Capacity utilization has

been affected by a high rate of breakdowns due to shortage of spares. In

1974/75 the percentage of delay time to total available working time was 47%and just over half of downtime was attributable to machinery breakdown. The

mill has been working on a two shift-16 hour day operation, which represents

an effective capacity of 85,000 tons per year, due in the early part of

1975 to a shortage of material but currently due to inadequate demand.

2.8 Production of heavy plate at CSM was started in 1971/72 to meetthe demands of a reconstruction program for ships and barges, destroyed

during the war of independence. Most of the production was of Lloyds qualityheavy plate and the peak was reached in 1973/74 when 8,852 tons were produced.However, since July 1975 there has been no production as stocks had risen at

that time to 7,000 tons, which is over one year's demand based on 1974/75sales. In 1974/75 it was running mainly on a one shift-8 hour basis.

Other Rolling Plant

2.9 A small amount of angles and large billets are directly rolledin the blooming mill. But most of the output of that mill is fed in largebillet form to the bar/billet mill and in sheet bar and slab to the sheet/

thin plate mills. Capacity utilization of the billet/bar mill has prog-ressively increased since independence and is currently operating at a pro-

duction level nearly 90% higher than in 1968/69 which was the highest achieved

prior to independence. On the other hand capacity utilization of the sheet/thin plate mills has been declining since independence. Details of past

production and utilization are shown below:

1975/76Installed Est. based onCapacity 1969/70 1972/73 1973/74 1974/75 July to Feb.

Bar and BilletMill (tons) 55,000 23,801 27,935 31,460 39,606 53,000

(CapacityUtilization) (43%) (51%) (57%) (72%) (96%)

Sheet and ThinPlate (tons) 60,000 12,511 11,623 8,200 8,570 8,000

(CapacityUtilization) (21%) (19%) (14%) (14%) (13%)

Total (tons) 115,000 36,312 39,558 39,660 48,176 61,000(CapacityUtilization) (32%) (34%) (34%) (42%) (53%)

2.10 The calculation of the installed capacity of the bar and billetmill was based originally on rods and billets of mixed sizes with rods pre-dominating and was given as 55,000 tons per year. Howeve5, the pattern ofdemand has altered and the major requirement is for 50 mm billet for rollingmills. CSM management has specialized in producing standard billets andrecently was able to exceed rated capacity for short periods of time. Effec-tive capacity basid on a higher operating ratio would be about 100,000 tonsper year of 50 mm billet. But at the present time with a high breakdownrate due to shortage of spares, the maximum possible output would be 85,000tons based on a three shift operation.

2.11 Although a 45,000 ton installed capacity is quoted for the BlackPlate (BP) sheet mill, parts of two of the three sheet mill lines have beenremoved and used as spares to keep one line running. Effective nominalcapacity of the sheet line is therefore only 15,000 tons, but with a highaverage of 35% delay time, of which over a third was due to machinery break-down, a more realistic estimate of capacity is 12,000 tons, operating one lineon a three shift basis. Based on this effective capacity estimate, utili-zation is currently running at 55%. The plant has a high material wastagerate, using an obsolete process, which makes its cost and price uncompetitivein relation to imports.

2.12 The installed capacity of the thin sheet mill, which can alsoproduce BP sheets, depending on demand, is 15,000 tons per year. The lowcapacity utilization of this mill in the past and estimate for 1975/76is attributable to low demand.

- 12 -

Galvanizing Shop

2.13 Output of the galvanizing shop has been severely curtailed by thelimited one line operation of the BP sheet mill that feeds it. Details ofproduction and utilization are shown below:

1975/76Installed Est. based onCapacity 1969/70 1972/73 1973/74 1974/75 July to Feb.

GalvanizingShop (tons) 60,000 7,343 6,888 4,731 4,139 8,000

(CapacityUtilization) (12%) (11%) (8%) (7%) (13%)

2.14 Although on a three shift basis the installed capacity of the threegalvanizing lines is 60,000 tons per year, output is limited if fed from theone line BP sheet mill. To increase utilization of this equipment it mightbe economic to import BP sheet for galvanizing; economic justification forallocating foreign exchange for this purpose would have to be examined andwould be dependent on differences in prices and in foreign exchange costs.

C. Costs, Prices and Profitability

Structure and Level of Costs

2.15 The costs of production of CSM products and their sales prices areconsiderably above world market levels. Proluction costs for the principalsaleable item of CSM, steel billets of 50 mm , were estimated by the mill inDecember 1975 at Tk 4728/ton (US$325) and the sales price was US$375 (Tk5450); the average European f.o.b. export quotation for the 4th quarter of1975 was US$170. 1/ The structure of CSM costs for that period has beenestimated as follows:

1/ Source: Metal Bulletin.

- 13 -

% of Total Cost

Pig iron and scrap 49.5Other raw materials (imported) 23.1

of which refractories (13.3)Consumables and spares 16.5

of which fuel and electricity (9.5)Manufacturing overhead 9.4

of which depreciation (2.6)Administrative overhead 1.6

a!100i.0

Source: BStMC; details do not add to total due to rounding.

a/ Does not include financial charges; on total sales,these are estimated at around 3%.

2.16 As a consequence of the accounting practices used by BStMC, thesedata are based on imported raw material prices and costs prior to devaluationsince these purchases were made before May 1975. However, it appears likelythat these costs have not substantially increased due to devaluation. In thefirst place, imports had been subject to a 20% tariff surcharge which waseliminated when the Taka was devalued. Secondly, pig iron and scrap priceshave experienced further declines as compared to the prices used in this cal-culation.

2.17 Based on the general structure of billet costs, these data suggesta high weight in total costs of fuel and other raw materials, particularlyrefractories. Much of this is apparently due to design deficiencies requiringexcessive re-heating and to the high scrap factor, due particularly to thediscontinuous nature of the billet casting but reflecting as well some in-efficiencies in the furnaces due to poor maintenance. As noted earlier, theseproblems are even more serious in the BP and in the plate mills where thescrap rate is considerably higher than in the billet mill.

2.18 Another factor contributing to high costs has been the inefficientmethods of unloading ships in Chittagong narbor, which restricts also thecontinuous flow of raw materials.

2.19 The cost data include a considerable proportion of sales taxes andimport duties paid to the Government; for example, import duties (including

- 14 -

the 20% surcharge removed after the May devaluation) amount to some Tk 7001/ or 16% of unit costs for billets. In addition, there are sales and othertaxes and duties. Overall for the entire BStMC, the total of these pay-ments amounted to 15% of total sales value in 1974/75.

2.20 In evaluating these data, one must also note the peculiar structureof import duties. A 10% duty is imposed on pig iron, while 40% is imposedon imported scrap and as much as 150% on imported dolomite. These rateswere originally established by the Government of Pakistan prior to indepen-dence and have not been modified since that time (except for the surcharges).

Prices and Profitability

2.21 Under current pricing policy, recommendations on prices for prod-ucts sold by the mill are submitted by the Corporation to a Price AdvisoryCommission which gives final approval. Current guidelines permit pricecalculations based on cost of production plus a 10% "profit" factor. Inthis situation it is not surprising that the mill has recorded substantialprofits in the last two years:

1972/73 1973/74 1974/75

Sales value (million Taka) 108.7 157.6 257.0Net profit (loss) (million Taka) (26.1) 28.3 25.0Profits/sales % (24.0) 18.0 9.7

D. Other Steel Products

2.22 In addition to the cast steel ingots produced by CSM, the MohammadiIron and Steel Works, a public sector enterprise, has an electric furnacewhich converts scrap to mild steel cast billets. It has a 6,000 ton peryear installed capacity and its effective capability is the same, based on athree shift operation. In 1974/75, production was at the level of 2,048 tons,giving a capacity utilization of 34%. Most of the output goes to localre-rolling mills in Chittagong. In 1974/75 net profits were only 2.5% ofsales.

2.23 BStMC also has under its control Husein Industries Limited, whichproduces black steel pipe of 1/2 to 1-1/2 inch diameter. It has a capacityof 3,000 ton per year which was built with the West Pakistan market in mindand consequently its utilization was only 3% in 1974/75; it has been makingcontinuous losses since being taken over after independence.

1/ Excluding the 20% surcharge, the normal tariffs on pig iron and scrapamount to Tk 200; duties paid for other imports are not separatelyidentified.

- 15 -

2.24 Prior to independence, two of the re-rolling mills now under thejurisdiction of BStMC had ordered small electric arc furnaces which weredelivered but never installed and remain in packing cases at the plants. TheCorporation has been considering setting up this machinery in one plantalong with ancillary equipment for heat treatment and forging. Consultantsare studying the feasibility of producing special steels.

- 16 -

CHAPTER III. RE-ROLLING MILLS - STATUS AND CAPABILITY

A. Re-rolling Mill Facilities and Products

3.1 Prior to independence all of the re-rolling mills in Bangladeshwere privately owned. At the present time, 12 re-rolling mills abandonedby their non-Bengali owners are controlled by the BStMC, leaving 17 re-rollingmills in the private sector. The output mix of the re-rolling mills variesfrom plant to plant but includes mild steel reinforcing rods, flats, angles,channel, and baling hoops. In addition, wire rods are made from billets foruse in wire drawing plants making nails, wood screws, barbed wire, etc.

B. Production Output and Capacity Utilization

3.2 Even before independence there seems to have been excessive capac-ity in the re-rolling sector; capacity utilization was only about 15% of themaximum two shift capacity in the area now Bangladesh; in West Pakistancapacity utilization was 13%. In 1974/75 the estimated output of 54,000 tonsrepresented 11% utilization of the two shift-22 hours maximum capacity of490,000 tons per year, or based on single shift operation a 20% utilization of275,000 tons per year capacity; of this output, about 60% was provided byBStMC mills. The table below, based on single shift capacity, shows that ofthe 29 re-rolling mills only 4 have capacity above 16,000 tons per year andaccount for 29% of total.

Installed Capacity Number of Mills(one shift-tons/year) Public Private % of Total Capacity

0- 2,000 1 - 12,000- 4,000 1 1 34,000- 8,000 2 9 208,000-16,000 7 4 4716,000-32,000 1 3 29

Total 12 17 100

Public Sector

3.3 In the public sector nine of the re-rolling mills are dependenton manual handling and are rather antiquated. Three are more modern semi-auto-matic units which are at Dacca Steel Works Ltd., Quraishi Steel Ltd (Khulna)and New Era Steel Mills Ltd. Chittagong. Most of the mills prior to inde-pendence ran on a one shift 12-hour basis and this gave a capacity of 120,400tons per year, but all the mills could be run for a maximum capacity oftwo shift-22 hours giving a 206,500 ton capacity. A detailed list of publicsector enterprises, type of mill, production products, installed and effec-tive capacity is shown in Annex IV.

- 17 -

3.4 Many of the mills taken over after independence by BStMC actuallyremained closed in the early years. For example Khulna IndustrLal and TradingCorporatLon remained closed through 1972/73 and Sino Bangladesh only operatedfor a month in that period. In addition, some mills, such as the East BengalTrading and Industrial Corporation, were only placed officially under theCorporation at the end of the 1974/75 period. It is not surprising there-fore that, in 1972/73, utilization of available capacity (one shift) wasonly at the level of 17% by comparison with the 26% achieved by those samemills in the 1969-71 period prior to independence. However, since then,capacity utilizatLon has improved to a level higher than the pre-independenceperiod as follows:

1969-71 1975/76Average 1972/73 1973/74 1974/75 (Estimated)

Total Capacity(one 12 hr Shift)(tons) 108,400 108,400 108,400 108,400 120,000

Total Produc-tion (tons) 28,410 18,656 22,988 32,024 44,000

CapacityUtilization 26% 17% 21% 30% 37%

A detailed analysis of production and capacity utilization trends for eachof the public sector re-rolling mill enterprises is shown in StatisticalAppendix Table 5.

Private Sector

3.5 Information on the private sector re-rolling mills was not soreadily available as in the public sector. However, based on discussionsand information provided by the General Secretary of the Re-rolling MillsAssociation the 17 re-rolling mills in the private sector have an installedcapacity based on one 12 hour shift of 154,300 tons per year. Over thelast three years, 1972-1975, production output has averaged 22,540 tons peryear, a capacity utilization of about 15%, which is about half the utili-zation figure currently being achieved by the public sector. A list ofthe prLvate sector re-rolling mills together with details of products andcapacities is shown in Annex V.

C. Factors Affecting Performance

3.6 Since independence the main constraint in improving productionoutput and capacity utilization in both the public and private sectors hasbeen a shortage of raw materials in the form of M.S. billets, due to limitedforeign exchange allocations. On the basts of their registered capacity,private re-rollers receive "entitlements" for Lmported steel billets in accor-dance with the overall foreign exchange allocations made by the Government;

- 18 -

actual import is undertaken by TCB after these entitlements are turned overto it. 1/ With CSM billets reserved, until recently, for the public sectormills, those enterprises have been able to achieve a higher capacity utiliza-tion than the private sector. However, capacity values provided by the privatesector may have been inflated to gain a higher entitlement.

3.7 Another constraint up to January 1974 had been labor unrest, but

this now seems to have been resolved in both the public and private sectors.The private sector seems to have had less trouble in the past and this mightbe related to the higher rates of pay relative to the public sector. Althoughin some private factories visited Tk 300-500 per month were being paid forunskilled workers, there were some that paid the public sector basic sal-ary of Tk 150 per month; thus factors such as continuity of management andlong-term good industrial relations could be relevant for the differencein the incidence of labor unrest.

3.8 Since early 1975, the constraints on production have changed.Demand has not kept pace with production increases of re-rolled products;consequently finished goods stocks have risen for the public sector millsfrom 5,442 tons at the end of June 1974 to 7,725 tons at the end of June 1975and 8,415 tons at the end of February 1976. The last stock position is equalto five months of sales. The reduced volume of government purchases and thecurrent depressed level of private consumption are considered to be the maincauses of lack of demand. Although no data are available, private mills alsoappear to be facing reduced demand.

D. Structure of Costs

3.9 For most mills using commercial grade billets, the current (December1975) average input cost has been Tk 5,450 per ton plus transport cost fromCSM. This price applies to both public and private sector re-rolling mills.

3.10 Each public enterprise attempts to achieve a 10% margin over costs,but selling prices are set centrally so the main variable is conversion costs.An example of the structure of costs of reinforcing bar at one mill is shownbelow:

1/ TCB fixes its own prices on these supplies, adding tariffs, taxes andadministrative costs to the c.i.f. import price.

- 19 -

TakatTon US$/Ton

Input of Billets 5,450 375Transport Cost 50Conversion/Manufacturing Cost 480Administration 132

TOTAL COST/TON 6,112 420SELLING PRICE 7,000 481

European Export Quotation,F.O.B. Avg. Oct. to Dec. 1975 195

Clearly with 90% of the cost linked with the input cost of billet, the re-rolling mills have little leeway in reducing overall costs and prices, butsome rationalization of this sector to achieve higher capacity utilizationcould assist in maintaining existing selling price levels.

E. Financial Results

3.11 In 1972/73, six of the 11 re-rolling mills in the public sectorrecorded losses. By 1974/75 only one of the re-rolling mills was in deficitand this was an enterprise that was only taken over physically in the latterpart of the 1974/75 period. In total, these public sector re-rolling millshave been profitable, in the early days because one mill, the National Ironand Steel Industries, was making sufficient profits to cover the lossesof other mills and later because of improvements in capacity utilizationand price increases; as noted earlier, official price policy sets prices onthe basis of average costs plus a "profit" factor with no efficiency criteria.Details of sales, profits in prices per ton are shown below:

1972/73 1973/74 1974/75

Sales Value (Tk million) 45.2 104.0 214.1Net Profit (Tk million) 2.5 13.1 15.6Net Profit on Sales 5.5% 12.6% 7.3%Sales (Tons) 21,047 24,895 31,451Revenue per ton (Tk) 2,146 4,176 6,807

3.12 There is a wide range of performance between re-rolling millsin the public sector, with profits in 1974/75 ranging from 2% up to 17%of sales, with one company making a loss. At the top end of performance,three companies, the National Iron and Steel Industries, New Era Steel Millsand Dacca Steel Works, have achieved good results over the past two years,while others have only been marginally profitable such as Quraishi SteelLtd., Sino Banglade-sh Industrial Works. A detailed list of enterprisesshowing sales, net profit and net profit on sales is given in StatisticalAppendix Table 9. In view of the overcapacity in relation to demand, somerationalization is desirable and the less healthy enterprises should bethoroughly reviewed in relation to long-term economic viability.

- 20 -

3.13 Little financial information was available on the private sectorre-rolling enterprises but it is estimated that the sales value in 1974/75was about Tk 152.5 million for sales of 22,540 tons of re-rolled products.With the low capacity utilization based on single shift working, a numberof the private sector mills are probably only marginally profitable.

Iron Foundries

3.14 Although the main concern of the mission was to look at steelrather than iron products, a number of iron foundries were visited in both thepublic and private sectors. Imports of foundry pig iron over the three years

1972/73-1974/75 averaged 6,890 tons per year (through TCB) for supply toprivate sector units. The public sector imports are done directly via the

nationalized industries, and no information is available on these imports aspig iron is not divided into foundry and steel making grades.

3.15 A strong entrepreneurial drive was in evidence in the privatesector iron foundries and many new products were being developed to add to thestandard range of cisterns, pumps, soil pipes and pipe couplings. One companyhad purchased, at an auction, a foundry and workshop previously under worker

management control and had introduced a range of products including dieselengines, small lathes, centrifugal pumps and shaping machines and was making

a variety of spares. Prices of these products appear to be competitivewith imports and quality is good. These entrepreneurial skills could bemore effectively utilized if there was a better awareness within the countryof the products and services available. The compiling of a Buyers' Guidewould greatly assist in this process.

- 21 -

CHAPTER IV. MEDIUM-TERM DEVELOPMENT PROSPECTS

A. Domestic Consumption Trends

4.1 In the light of recent developments, it is extremely difficultto forecast steel consumption for the immediate future. The Five-Year Develop-ment Program prepared in 1973, basing its forecasts on increases to pre-Independence per-capita consumption levels, projected an annual steel require-ment of 776,000 tons by 1977/78. But the severe balance of payments andfiscal constraints have considerably limited consumption; total use hasnot even reached that achieved in the 1960's with a resulting per capitause at one of the lowest levels in the world.

4.2 As detailed in Chapter I, the major consumer of steel at presentis the public sector, accounting for about 80% of total. Recent overalleconomic measures of the Government have been designed to give more latitudeto the private sector and there already appears to be some-expansion inits demand for steel products, particularly for residential construction.As regards the public sector, some details on the composition of its require-ments is provided in Annex VI. The total level of its future consumptionwill clearly depend upon both the size and composition of development expendi-tures.

4.3 To provide some indication of the implications of any future growthin steel consumption for the existing domestic steel producing facilities,calculations have been made for two alternative growth rates, 5% and 10%:

(in thousand tons)Average

1973/74-1974/75 1975/76 1976/77 1977/78 1978/79 1979/80

5% per year 130.4 136.9 143.8 151.0 158.5 166.410% per year 130.4 143.5 157.8 173.6 190.9 210.0

On the assumption of a 5% growth rate, total use will not reach pre-inde-pendence levels until 1980 1/, but per capita consumption will still remainbelow the previous level.

4.4 Assuming an identical structure of consumption as has prevailedin recent years, the product mix in 1980 under these two growth assumptionswould be as follows:

1/ Annual consumption during 1965-70 was about 160,000 tons; see Chapter I.

- 22 -

Projection of Primary Steel Demand in 1980

(In thousand tons)5% growth 10% growth

Billets and blanks (for rods, etc.) 71.6 90.3Wire and wire rod 1.7 2.1Reinforcing rod, angles and sections 8.3 10.5Rails and heavy sections 13.3 16.8Plate, sheet, strip, corrugated sheet 58.1 73.5Tinned plate 8.3 10.5Welded tube 3.3 4.2Other tube 1.7 2.1

4.5 With current capacity, re-rolling mills would have little diffi-culty in providing the total of such items (except for large sections). Totalbillet demand would be of the order of 80,000 tons under the smaller growthrate assumption and 100,000 under the larger. As pointed oyt in Chapter II,by concentrating its billet shop on a single product (50 mm billets) CSMcapacity would be sufficient to cover the lower requirements but would fallslightly short of the larger. The question which now must be addressed is theeconomic justification for that production as opposed to the alternative ofimporting all billets.

B. Improving Production Efficiency

CSM

4.6 The cost data presented earlier showed that in December 1975 CSMbillets were being produced at the equivalent of US$325 per ton as com-pared to typical export f.o.b. prices of US$170 per ton; assuming some US$25/ton in freight charges, local costs were more than 50% over competitiveimports. There exists wide scope to reduce local production costs, throughmeasures to reduce high scrap rates and to improve efficiency of fuel use.For purposes of comparison one would also have to exclude from productioncosts tariffs and taxes paid (which could not be separately identified)estimated to amount to some 12-15%. Taking into account these factors itappears that a domestic production cost of US$250-275 per ton would be achiev-able, still some 30 to 40% above the December 1975 price of imported billets.

4.7 The basic problem is the margin between the pig iron price and thesteel billet price. Under world market conditions prevailing in December 1975pig iron was available (c.i.f. basis) at some US$150/ton and billets at US$195/ton, a differential of some US$45 or 30% of the pig iron price. There isreason to believe that this situation is rather unique and does not necessarilyreflect longer-term relationships. Thus at the peak of the recent inflationaryperiod in late 1973 and 1974, steel billets were being imported at US$300 toUS$360 per ton while pig iron was being purchased for US$185 to US$200 per ton. 1/

1/ However, detailed cost data for that period show production costs (excludingtaxes) above imported billets prices, largely due to the relatively lowlevel of plant utilization at that time because of raw material shortages.

- 23 -

4.8 The determination of the appropriate price for imported steelbillets is not without its difficulties, as a number of Bank studies con-cerned with steel projects have indicated. Wiorld steel trade, while sub-stantially large in volume and value, represents no more than 10% of steeloutput. It is "in great part dependent on the extent to which local demandabsorbs local production capacity. In such a relatively small and uncer-tain marginal market, actual export trading prices are not meaningful forlong-term planning." I/ The same study concludes that, in 1974 prices,US$225/ton represents "a considered judgment of the long-term price steelproducts (in the major steel producing countries) would have to realize tocover costs and get an adequate return on their investments."