for official use only - world bank official use only report no. 27068-co international bank for...

TRANSCRIPT

Document of The World Bank

FOR OFFICIAL USE ONLY

Report No. 27068-CO

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

PROGRAM DOCUMENT FOR A PROPOSED

SECOND PROGRAMMATIC FISCAL AND INSTITUTIONAL STRUCTURAL ADJUSTMENT LOAN

IN THE AMOUNT OF US$lSO MILLION

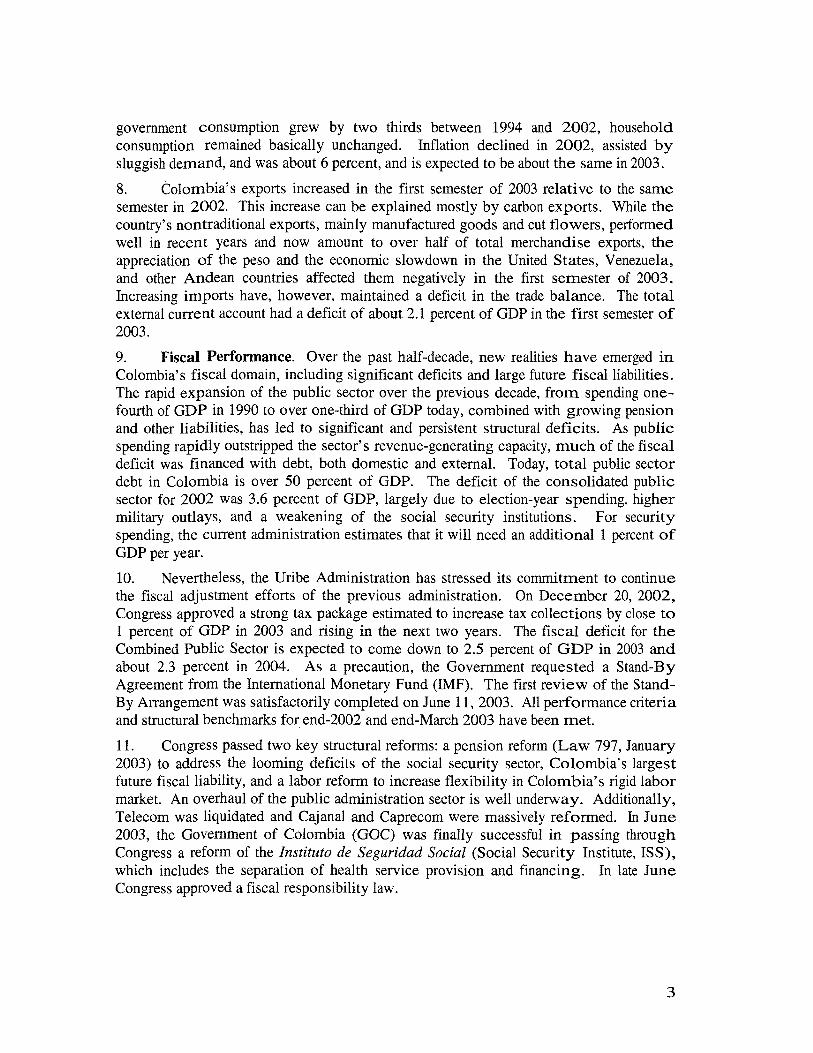

FOR

THE REPUBLIC OF COLOMBIA

OCTOBER 23,2003

Colombia-Mexico Country Management Unit Poverty Reduction and Economic Management Unit Latin America and the Caribbean Region

This document has a restricted distribution and may be used by recipients only in the performance o f their duties. I t s contents may not be otherwise disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

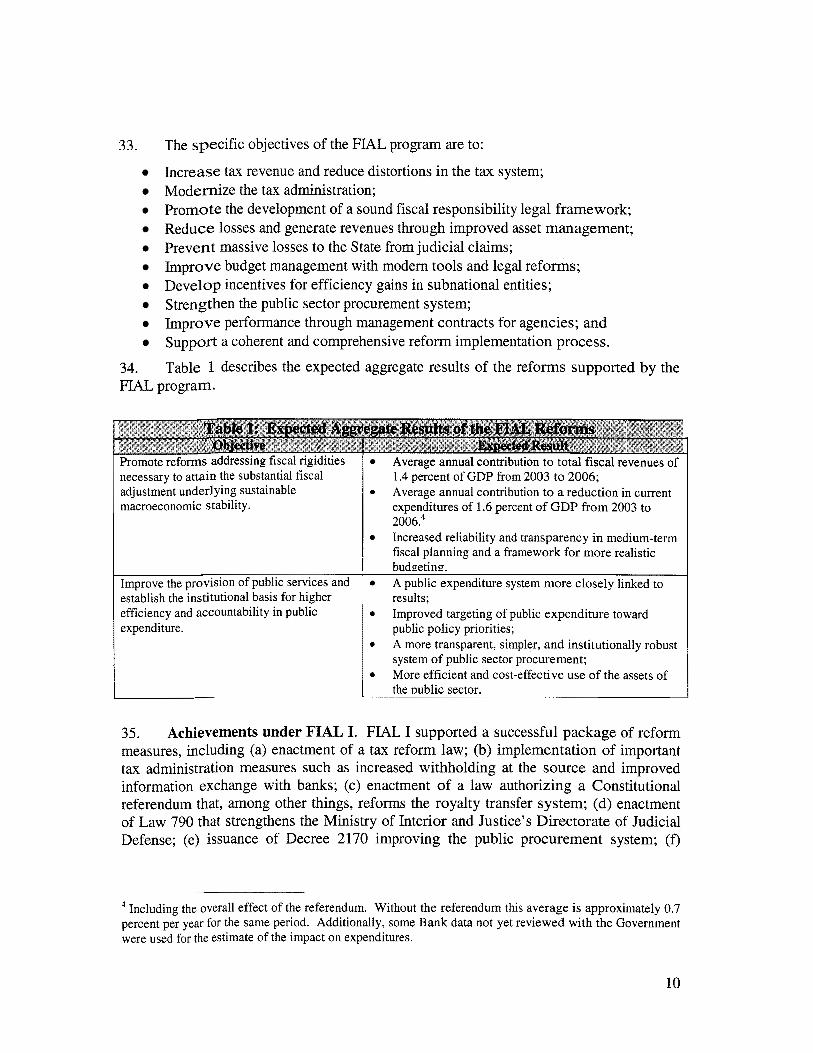

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

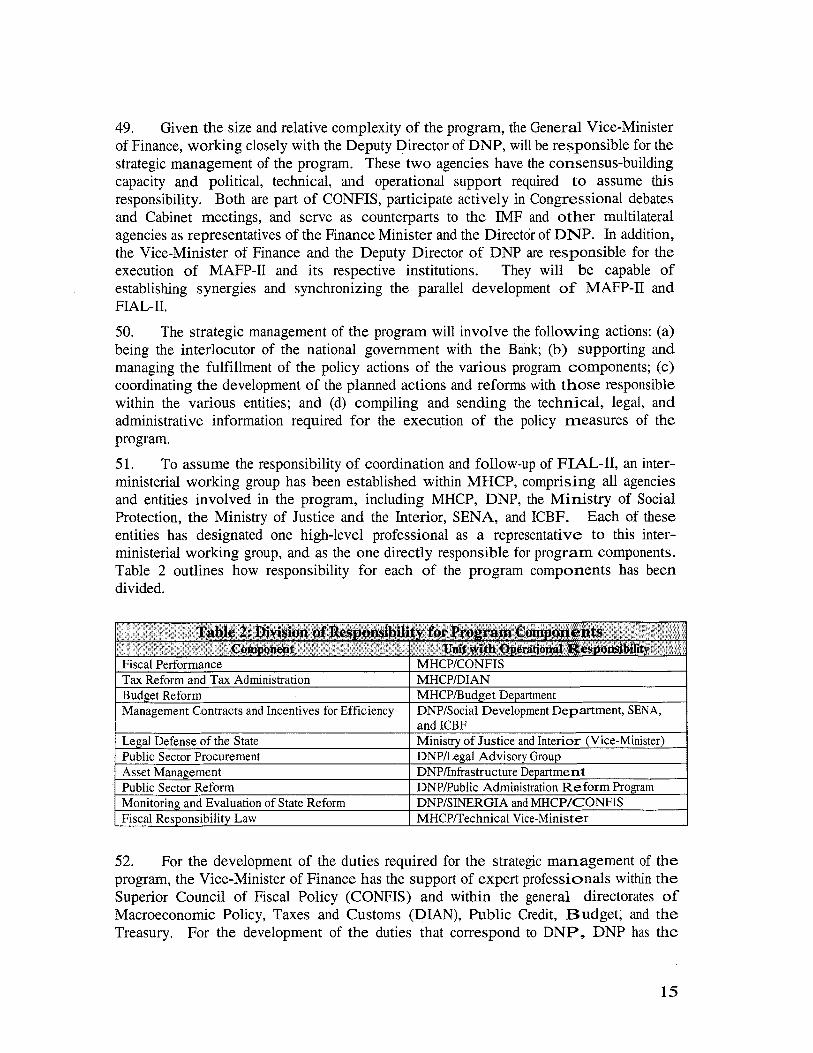

iscl

osur

e A

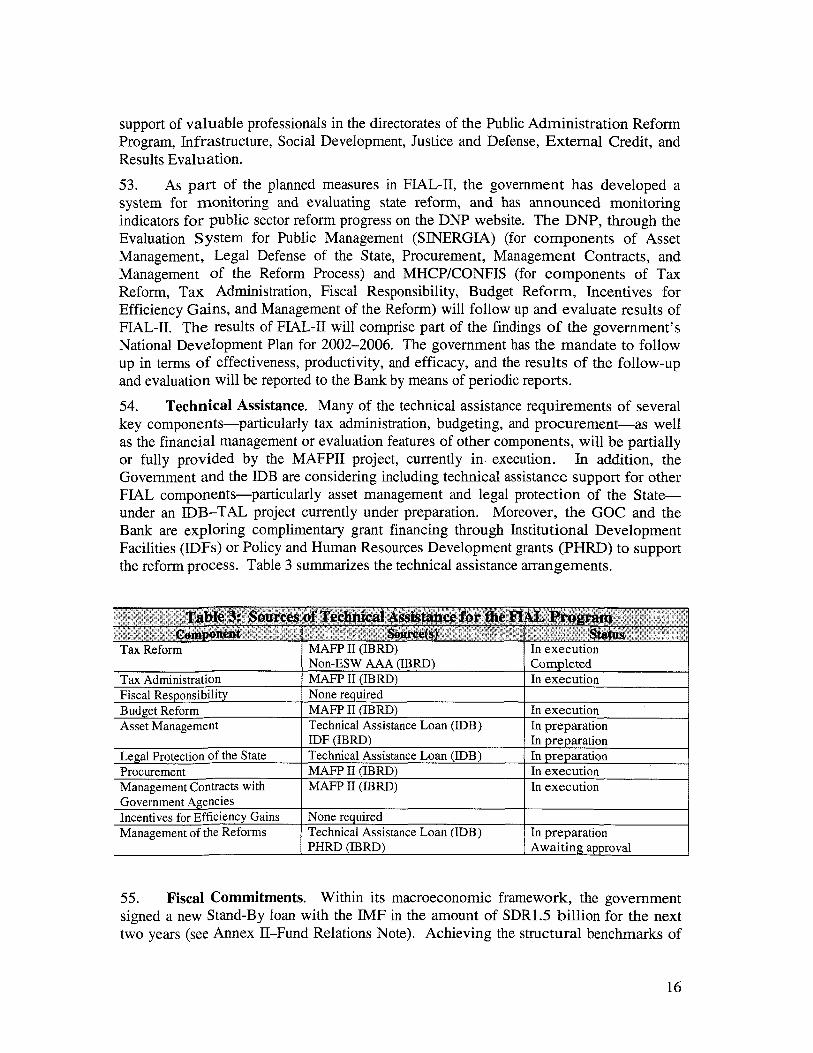

utho

rized

Pub

lic D

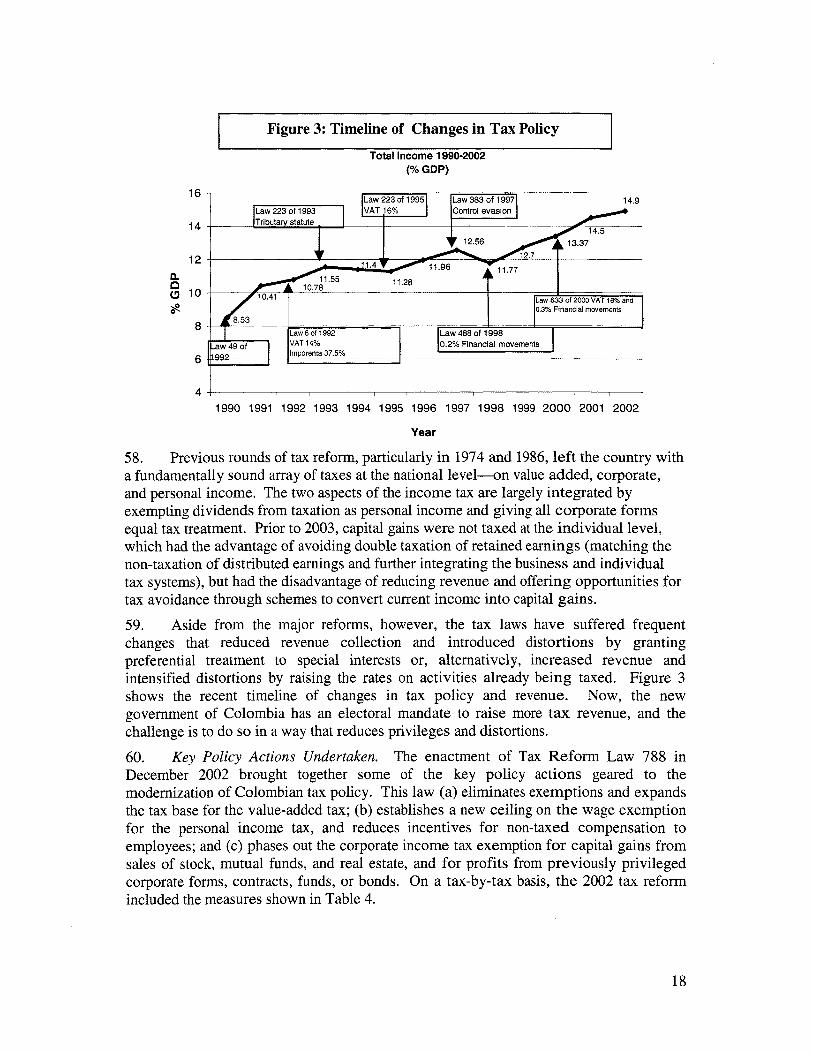

iscl

osur

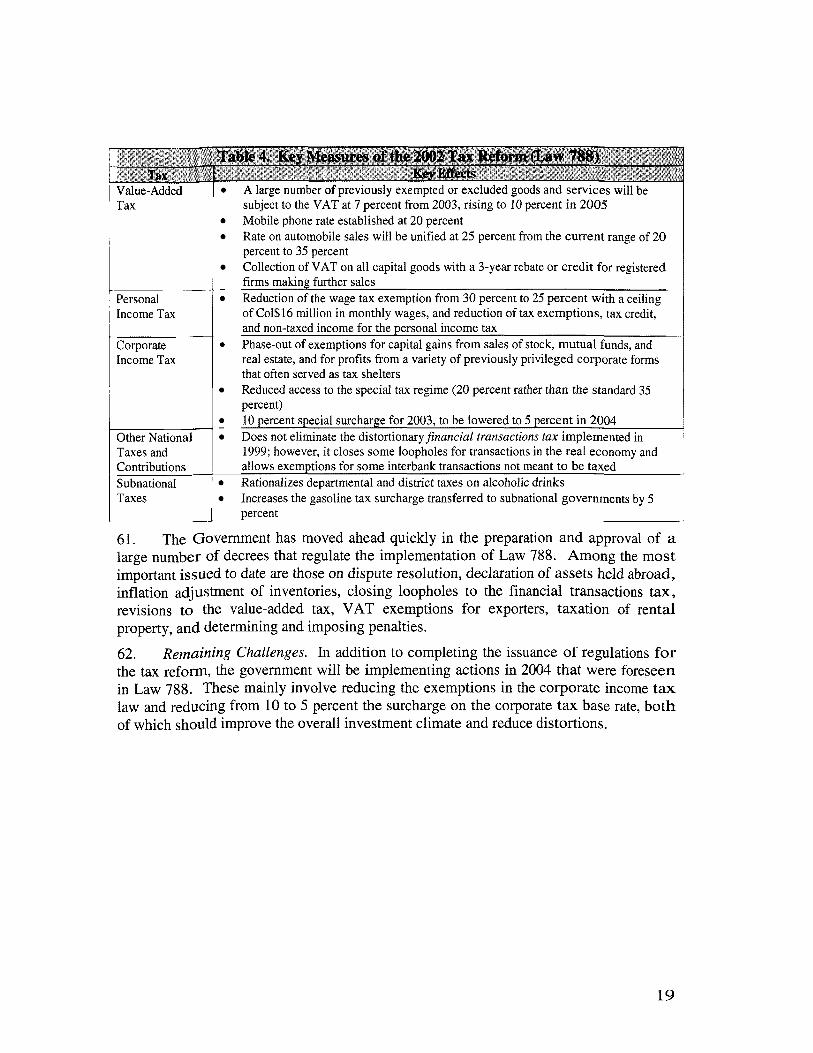

e A

utho

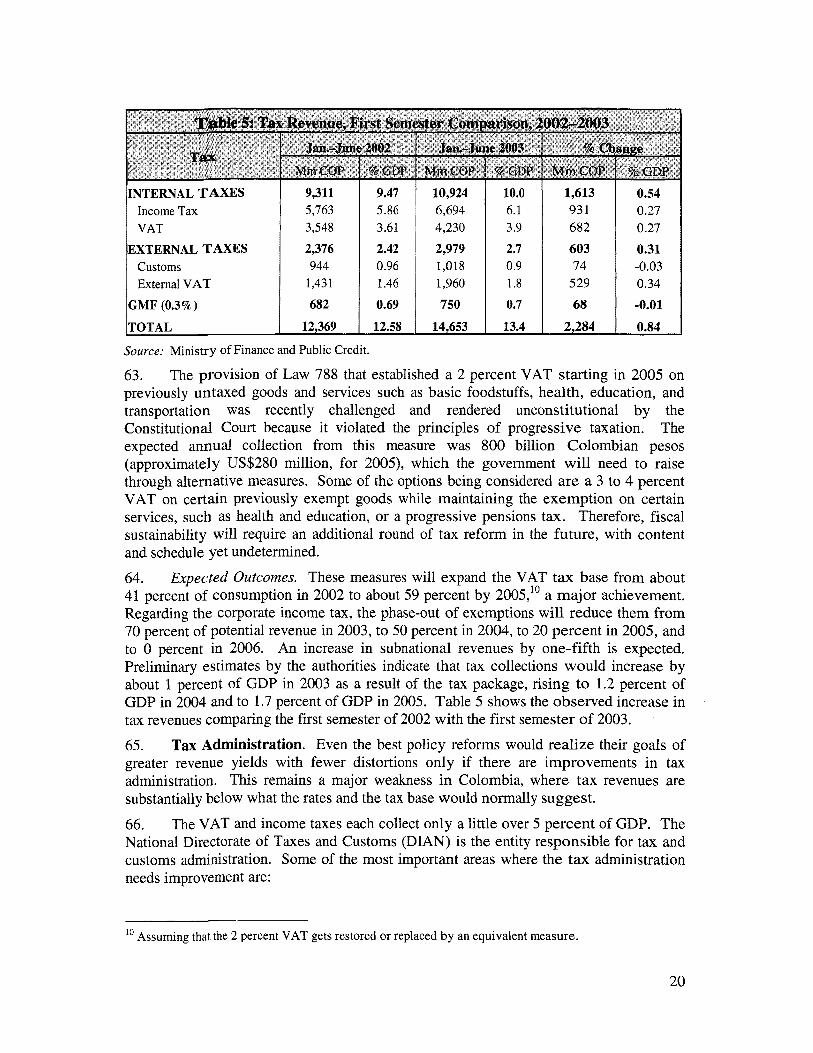

rized

Pub

lic D

iscl

osur

e A

utho

rized

CAS CFAA

CGN

CONFIS

CONPES

CPAR CSR DAFP

DIAN

DNP

FIAL

FNR

FRL GDP lBRD

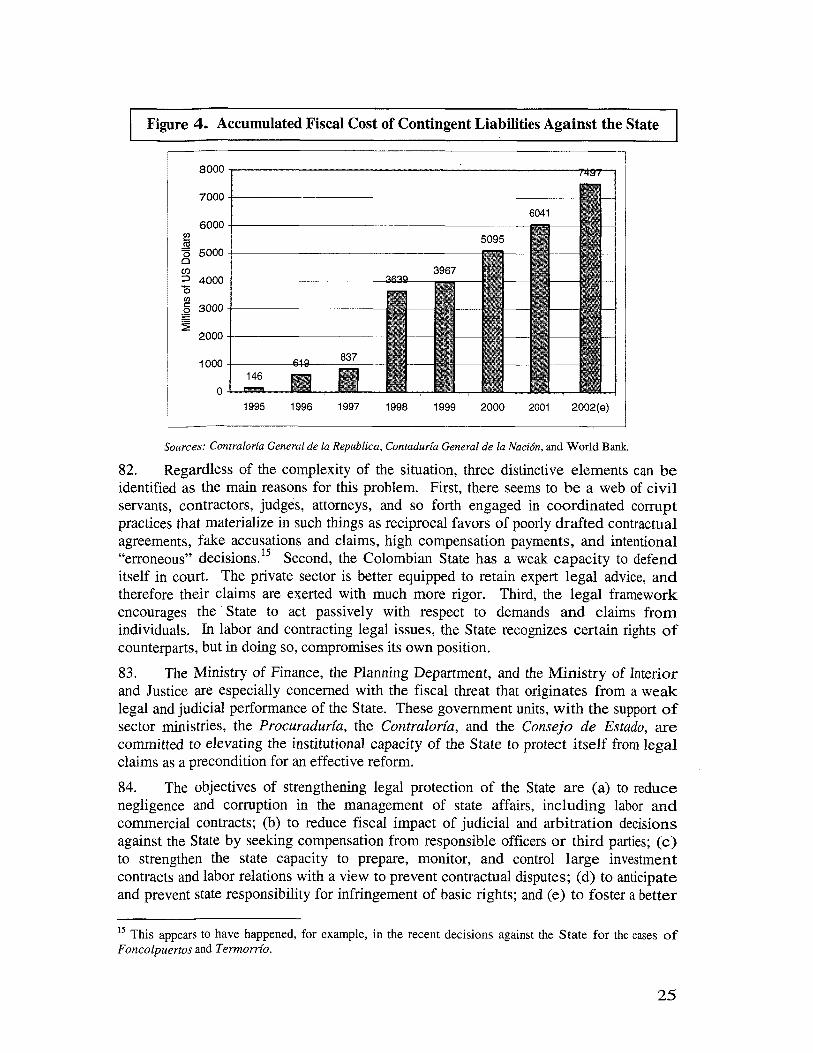

ICBF

IDB

REPUBLIC OF COLOMBIA-FISCAL YEAR January 1-December 3 1

CURRENCY EOUIVALENTS (as of 20 February 2003) CurrencyUnit = Peso

2,903.00 Pesos = US$1 0.92Euros = US$1

WEIGHTS AND MEASURES Metric System

Country Assistance Strategy Country Financial Accountability Assessment Contadurfa General de la Naci6n (Accountant General’s Office) Consejo Superior de Polftica Fiscal (Superior Council of Fiscal Policy) Consejo Nacional de Politica Econ6mica y Social (National Council of Economic and Social Policy) Country Procurement Assessment Report Commission for State Reform Departamento Administratho de la Funci6n Pliblica (Public Service Administrative Department) Direcci6n de Impuestos y Aduanas Nacionales (National Directorate of Taxes and Customs) Departamento Nacional de Planeach (National Planning Department) Programmatic Fiscal and Institutional Adjustment Loan Fondo Nacional de Regalias (National Royalty Fund) Fiscal Responsibility Law Gross Domestic Product Intemational Bank for Reconstruction and Development Instituto Colombian0 de Bienestar Familiar (Colombian Family Welfare Institute) Inter-American Development Bank

IDF JMF ISS

IVA LIL MAFP

MDGs MHCP

MU

MTEF NFPS OBC PHRD PLaRSSAL

PRAP

SENA

SIIF

SINERGIA

TAL VAT

Institutional Development Facility Intemational Monetary Fund Instituto de Seguridad Social (Social Security Institute) Impuesto a1 Valor Agregado (Value-added tax) Leaming and Innovation Loan Modemizaci6n de la Administracidn Financiera Pdblica (Public Financial Management Project) Millennium Development Goals Ministerio de Hacienda y Crkdito Pdblico (Ministry of Finance and Public Credit) Ministerio del Interior y Justicia (Ministry of Interior and Justice) Medium Term Expenditure Framework Non-Financial Public Sector Organic Budget Code Policy and Human Resources Development Programmatic Labor Reform and Social Sector Adjustment Loan Programa de Renovaci6n de la Administracidn Pdblica (Public Administration Renovation Program) Servicio Nacional de Aprendizaje (National Training Service) Sistema Integrado de Informaci6n Financiera (Integrated Financial Information System) Sistema Nacional de Evaluaci6n de Resultados (Evaluation System for Public Management) Technical Assistance Loan Value-added Tax

IBRD Vice President: David de Ferranti Chief Economist: Guillermo Perry Director, LCSPR: Ernesto May Sector Manager, LCSPS: Ronald E. Myers Country Director: Isabel M. Guerrero Lead Economist: Joaquin A. Cottani Task Manager: Mario F. Sanginks Sr. Counsel and Country Lawyer: Eduardo Brito

Th is operation was prepared by a World Bank team composed o f MessrsMmes. Del Villar, Leytbn, Mosqueira, Rojas, Sangin&, and Solana (LCSPS), Gonzhlez and Webb (LCSPE), Romhn (LCOPR), and Uribe (Consultant). The team was led by Mr. Sanginks (LCSPS) and worked under the general guidance of Mr. Ronald Myers (Sector Manager, LCSPS), Mr. Ernesto May (Director, LCSPR), and Mrs. Isabel Guerrero (Director, LCClC).

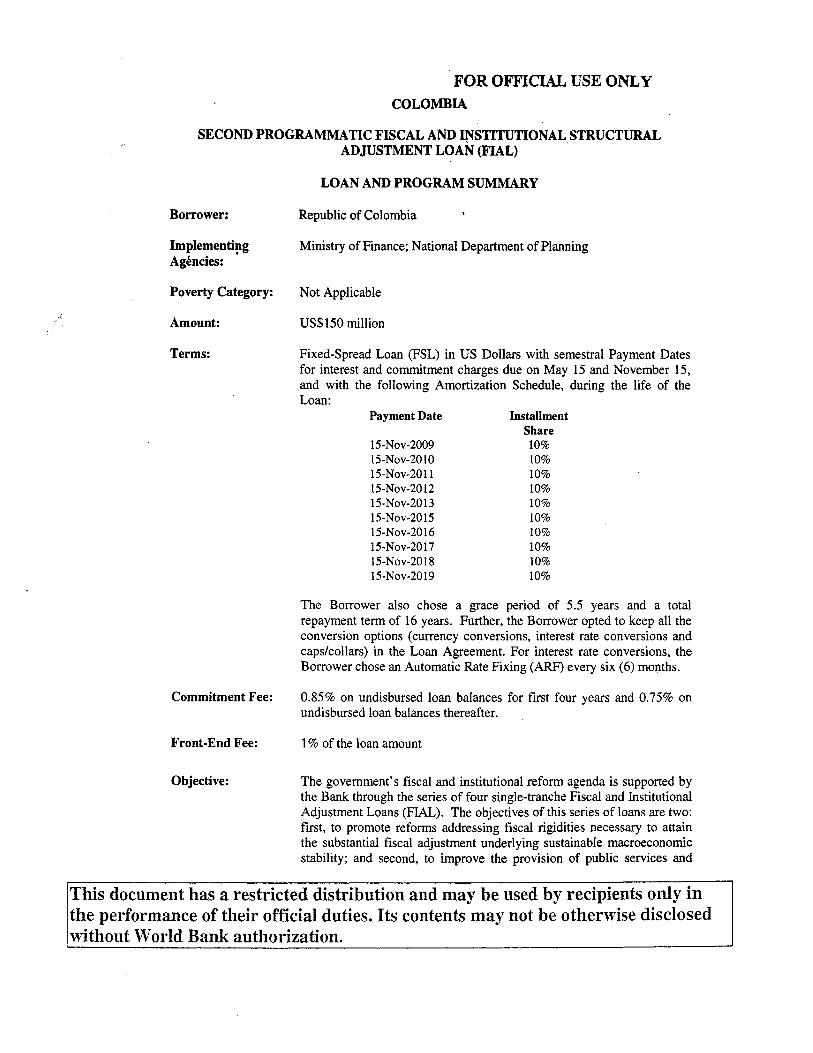

FOR OFFICIAL USE ONLY COLOMBIA

SECOND PROGRAMMATIC FISCAL AND I?NTITUTIONAL STRUCTURAL ADJUSTMENT LOAN (FIAL)

LOAN AND PROGRAM SUMMARY

Borrower:

Implementipg Agkncies:

Poverty Category:

Amount:

Terms:

Commitment Fee:

Front-End Fee:

Objective:

Republic o f Colombia 1

Ministry o f Finance; National Department o f Planning

Not Applicable

US$l50 million

Fixed-Spread Loan (FSL) in U S Dollars with semestral Payment Dates for interest and commitment charges due on May 15 and November 15, and with the following Amortization Schedule, during the l ife o f the Loan:

Payment Date Installment Share

15-NOV-2009 10% 1 5-NOV-20 10 10% 15-NOV-2011 10% 15-NOV-2012 10% 15-NOV-20 13 10% 15-NOV-20 15 10% 15-NOV-2016 10% 15-NOV-2017 10% 15-NOV-2018 10% 1 5-NOV-2019 10%

The Borrower also chose a grace period o f 5.5 years and a total repayment term o f 16 years. Further, the Borrower opted to keep all the conversion options (currency conversions, interest rate conversions and capskollars) in the Loan Agreement. For interest rate conversions, the Borrower chose an Automatic Rate Fixing (ARF) every six (6) months.

0.85% on undisbursed loan balances for f i rst four years and 0.75% on undisbursed loan balances thereafter. ,

1 % of the loan amount

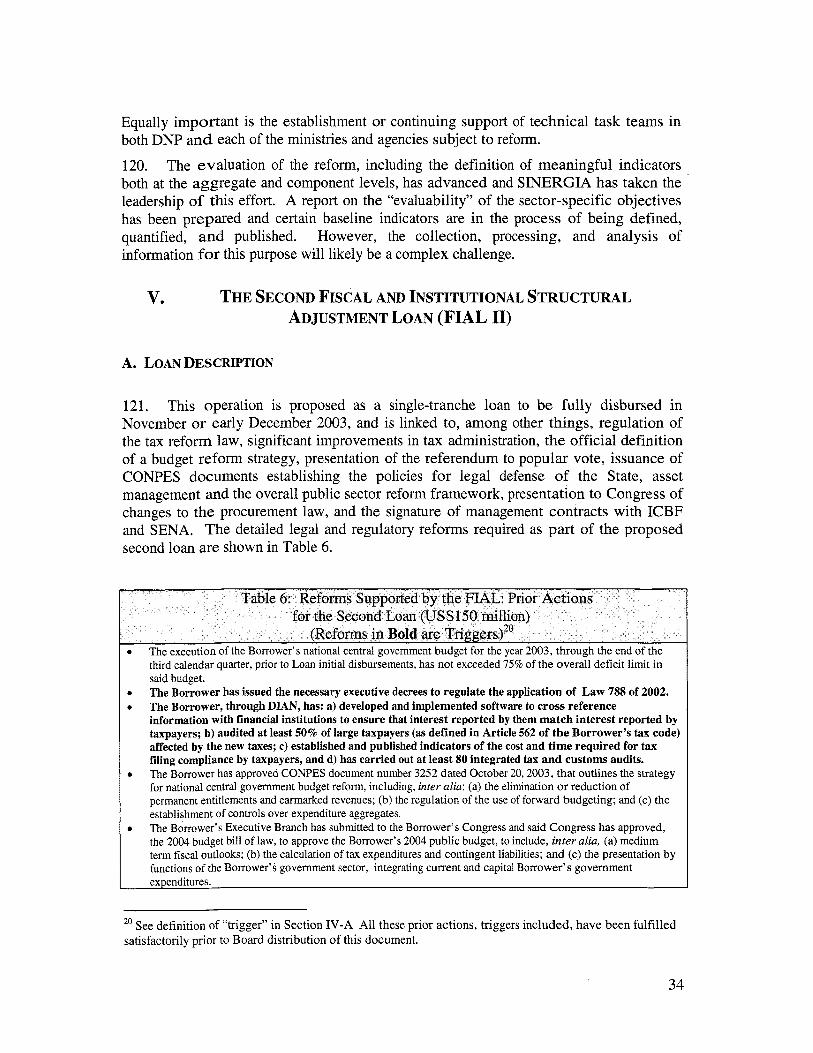

The government’s fiscal and institutional reform agenda i s supported by the Bank through the series o f four single-tranche Fiscal and Institutional Adjustment Loans (FIAL). The objectives o f this series o f loans are two: first, to promote reforms addressing fiscal rigidities necessary to attain the substantial fiscal adjustment underlying sustainable macroeconomic stability; and second, to improve the provision o f public services and

This document has a restricted distribution and may be used b y recipients only in the performance of their official duties. I t s contents may not be otherwise disclosed

Description:

Benefits:

Risks:

establish the institutional basis for higher efficiency and accountability in public expenditure.

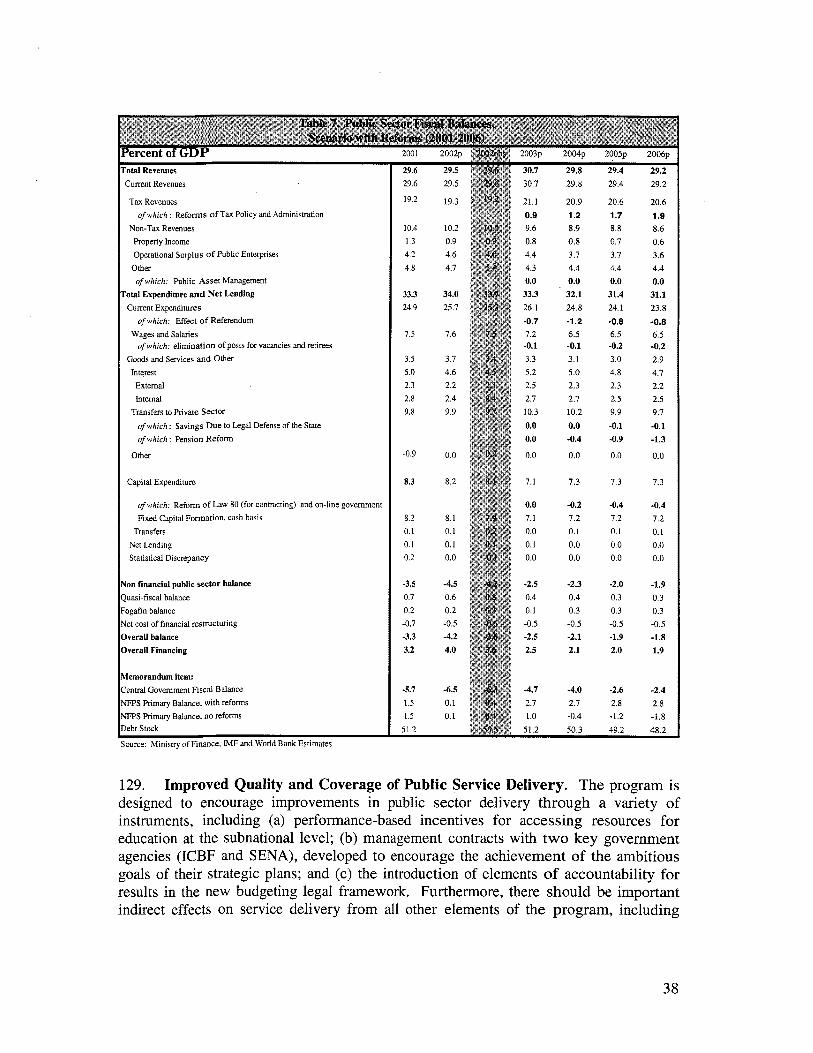

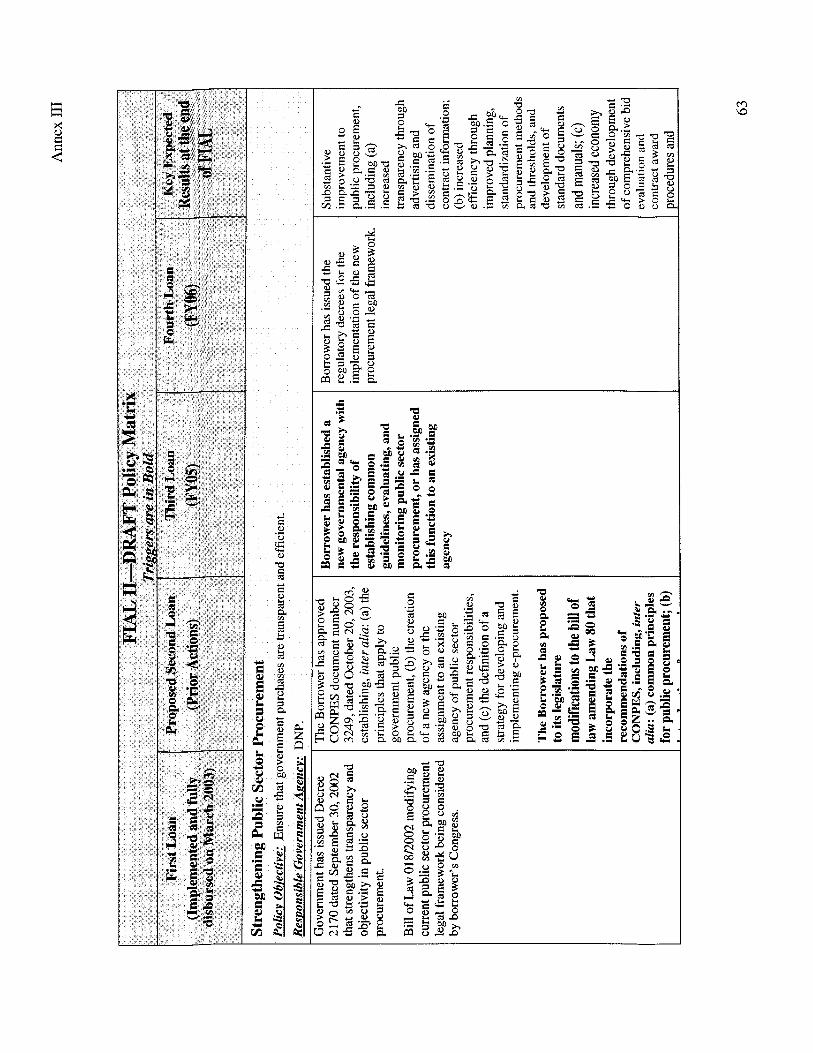

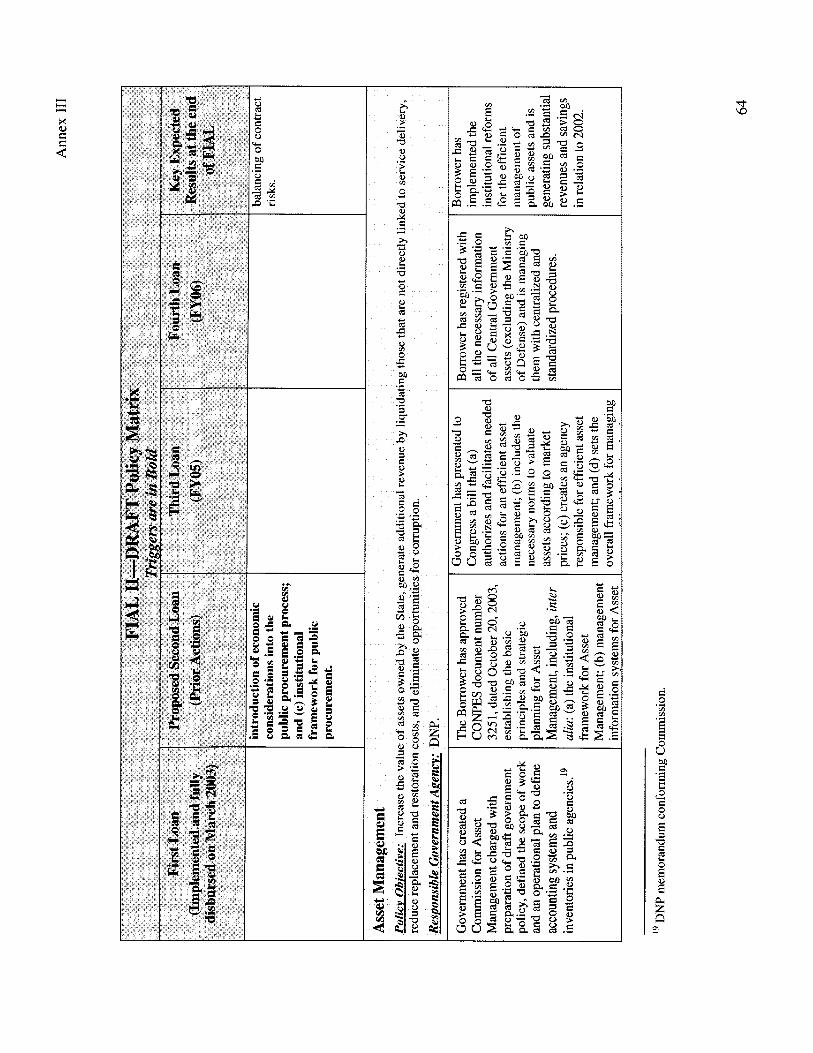

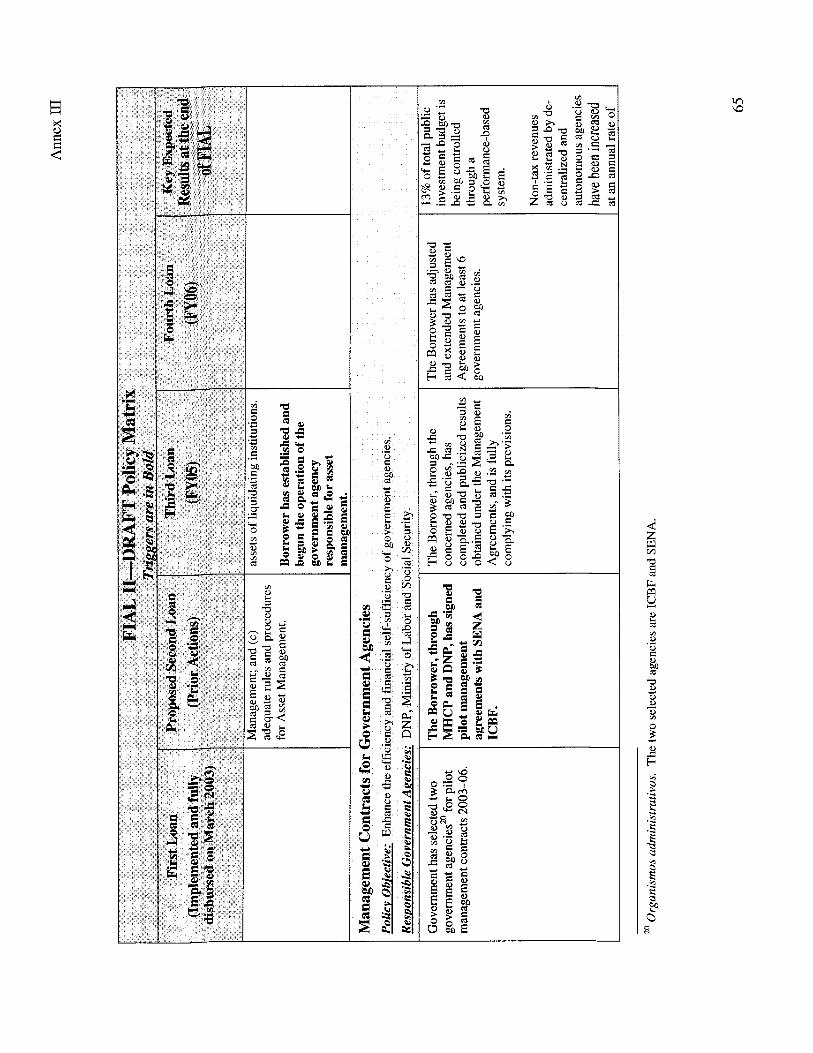

The specific objectives o f the FIAL program are to: (i) increase tax revenue and reduce distortions in the tax system; (ii) modernize the tax administration; (iii) promote the development o f a sound fiscal responsibility legal framework; (iv) reduce losses and generate revenues through improved asset management; (v) prevent massive losses to the State from judicial claims; (vi) improve budget management with modem tools and legal reforms; (vii) develop incentives for efficiency gains in subnational entities; (viii) strengthen the public sector procurement system; (ix) improve performance through management contracts for agencies; and (x) support a coherent and comprehensive reform implementation process.

This second loan of the program wi l l focus on the following elements: (i) issuance o f all legislation to regulate the application o f the tax reform law; (ii) further improvements in tax administration, including specific audit targets and the implementation of integrated tax-customs audits; (iii) approval o f an official budget reform strategy; (iv) Congressional approval of an improved 2004 Annual Budget Law; (v) presentation to popular vote o f the Constitutional referendum; (vi) issuance o f a new policy for legal defense o f the state; (vii) presentation to Congress o f reforms to the public procurement law; (viii) approval o f an official asset management policy and the achievement o f specific revenue targets; (ix) signature o f management contracts with two government agencies; and (x) enactment o f a Fiscal Responsibility Law.

The key benefits expected from the program are: (i) an average annual contribution to total fiscal revenues o f 1.4 percent o f GDP from 2003 to 2006; (ii) an average annual contribution to a reduction in current expenditures of 1.6 percent o f GDP from 2003 to 2006: (iii) increased reliability and transparency in medium-term fiscal planning and a framework for more realistic budgeting: (iv) a public expenditure system more closely linked to results; (v) improved targeting o f public expenditure toward public policy priorities; (vi) a more transparent, simpler, and institutionally robust system o f public sector procurement; and (vii) a more efficient and cost-effective use o f the assets o f the public sector. These achievements would translate directly into fiscal sustainability, improved quality and coverage o f public services, and improved governance and transparency.

The most important r isks faced by the program are: (i) the challenges faced by the government stemming from the overall political context, in particular the internal conflict and violence associated with illegal drug activity, which could negatively impact the continued implementation o f the program; (ii) possible attempts at derailing the reform process by special interest groups affected by it; (iii) the weakening o f the government’s overall policy agenda by the non-approval o f the Referendum; and (iv) the deterioration o f the fiscal and macroeconomic environment.

Project Identification Number: PO83905

REPUBLIC OF COLOMBIA SECOND PROGRAMMATIC FISCAL AND INSTITUTIONAL STRUCTURAL ADJUSTMENT

LOAN (FIAL 11)

Table of Contents

I . INTRODUCTION .................................................................................................. 2 CONTEXT OF THE OPERATION ..................................................................... 2

A . RELEVANT SOCIOECONOMIC BACKGROUND ............................................................ 2 B . FISCAL AND Ir\iSTITUTIONAL ISSUES ......................................................................... 5

I11 . THE G O V E R N M E N T ’ S REFORM PROGRAM .............................................. 8 I V . THE FISCAL AND I N S T I T U T I O N A L REFORM PROGRAM ...................... 9

A . OVERVIEW ............................................................................................................... 9 B . COMPONENTS OF THE PROGRAM ........................................................................... 17

A D J U S T M E N T LOAN (FIAL 11) ............................................................................... 34

I1 .

V . THE SECOND F I S C A L AND INSTITUTIONAL STRUCTURAL

A . LOAN DESCRIPTION ............................................................................................... 34 B . FIDUCIARY POLICIES ............................................................................................. 36 C . ENVIRONMENTAL ASPECTS .................................................................................... 36

F . SOCIAL IMPACT OF THE REFORMS .......................................................................... 40

D . BENEFITS ............................................................................................................... 37 E . RISKS ..................................................................................................................... 39

ANNEX I . LETTER OF DEVELOPMENT POLICY TO THE WORLD BANK ....................... 43 ANNEX 11 . INTERNATIONAL MONETARY FUND RELATIONS NOTE .............................. 54 ANNEX 111 . POLICY MATRIX ........................................................................................ 56 ANNEX I V . COLOMBIA AT GLANCE ............................................................................. 69

Figure 1 . Figure 2 . Figure 3 . Figure 4 .

Table 1 . Table 2 . Table 3 . Table 4 . Table 5 . Table 6 . Table 7 .

Figures Fiscal Deficit 1994-2002 ........................................................................................ 4 Colombian Debt Spreads ......................................................................................... 4 Timeline o f Changes in Tax Policy .......................................................................... 18 Accumulated Fiscal Cost o f Contingent Liabilities Against the State ..................... 25

Expected Aggregate Impact of the FIAL Reforms .................................................. 10 Division of Responsibility for Program Components .............................................. 15 Sources o f Technical Assistance for FIAL Program ................................................ 16 Key Measures ofthe 2002 Tax Reform (Law 788) ................................................. 19

Reforms Supported by the FIAL ............................................................................. 34 Tax Revenue. First Semester Comparison. 2002-2003 ........................................... 20

Public Sector Fiscal Balances, Scenario with Reforms (2001-2006) ...................... 38

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT PROGRAM DOCUMENT FOR A PROPOSED SECOND PROGRAMMATIC FISCAL AND

INSTITUTIONAL STRUCTURAL ADJUSTMENT LOAN TO THE REPUBLIC OF COLOMBIA

I. INTRODUCTION

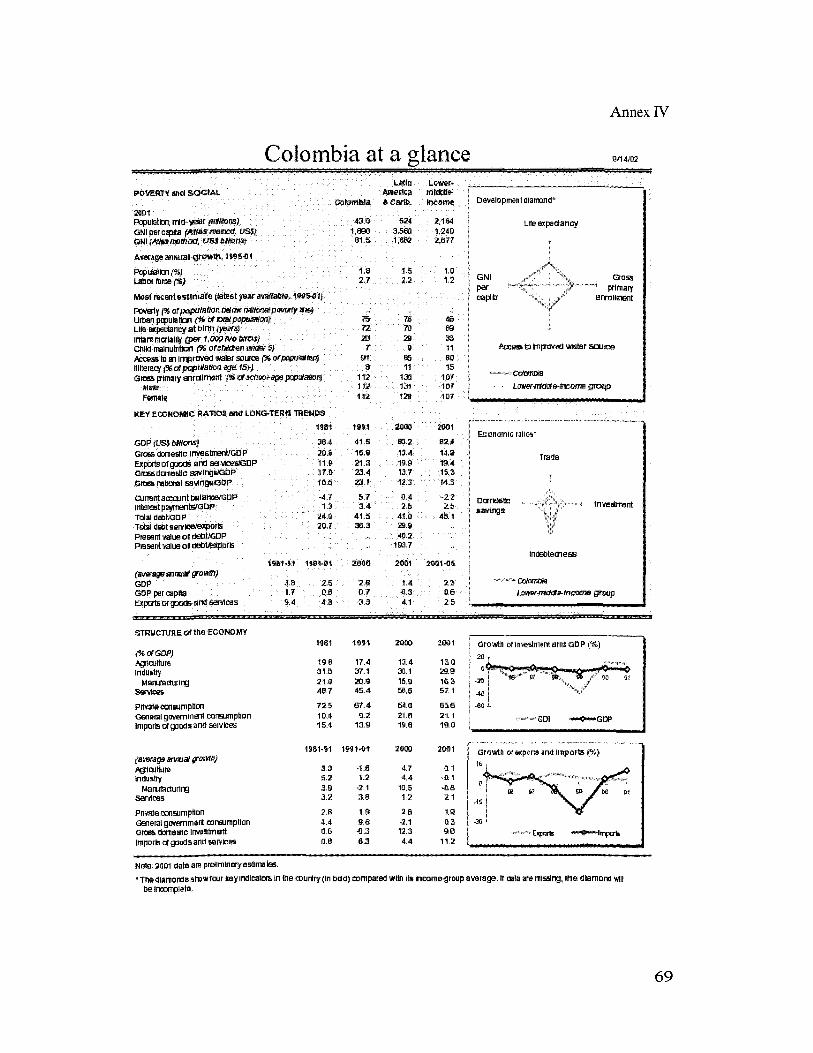

1. Colombia, a country o f 43 mill ion inhabitants with a history of sustained economic growth and fiscal stability, reached the end o f last decade with an almost unprecedented economic contraction and high levels o f c iv i l unrest. Facing a difficult fiscal outlook and popular disappointment with the peace process, President Alvaro Uribe took office in August 2002 on a platform of restoring security, fighting corruption, and delivering sustained economic growth. In i t s first year the Uribe administration has embarked on a path of fiscal prudence, ambitious public sector reform, and determination to end the 40-year armed struggle that makes Colombia one o f the most unsafe countries in the hemisphere.’

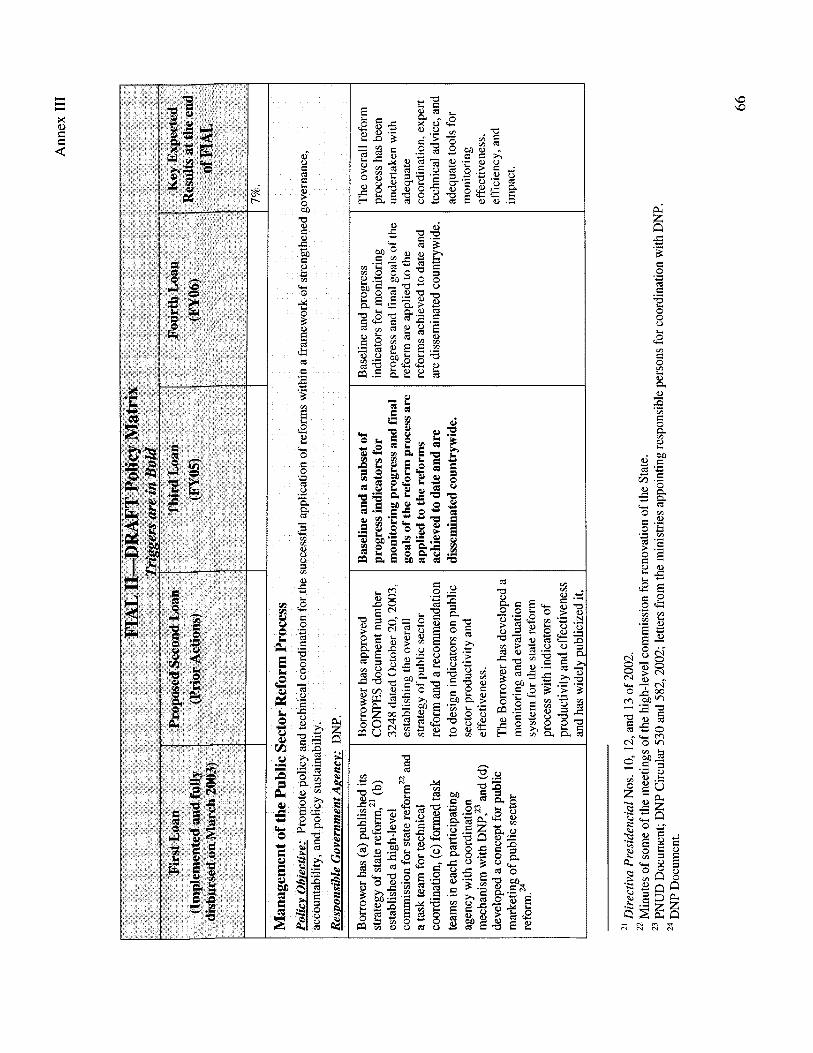

2. The backbone of the public sector reform process i s the Progruma de Renovacio’n de Zu Administrucio’n Pu’bZicu (PRAP), led by the National Planning Department (DNP) and based upon Presidential Directive 10 of October 2002. This program has so-called “vertical” reforms, which are basically sector- or entity-specific institutional restructuring actions that seek to reduce excess public sector employment and enhance quality and cost-effectiveness of public services; and “horizontal” reforms, which encompass cross- sector issues o f public administration, such as asset management, procurement, and others. This modernization effort i s coupled with substantial reforms in fiscal management, led by the Ministry of Finance and Public Credit (MHCP). These include a substantive tax reform, a major overhaul of the tax administration, budget reform, and the enactment of fiscal responsibility regulations. Together, these measures add up to a broad package meant to lay the foundations for improved service delivery and sustained fiscal balance. 3. During the second semester of 2002, the government agreed wi th the multilateral banks that the public sector reform process would be supported by structural adjustment loans from both the International Bank for Reconstruction and Development (IBRD) and the Inter-American Development Bank (IDB). The Bank focused on the issue of fiscal rigidities that make the implementation o f public policy extremely difficult, both from the revenue perspective and through the achievement of efficiency gains in the “horizontal” elements of the reform process. The IDB, on the other hand, focused i t s adjustment lending on the “vertical” elements of reform, and some horizontal elements not covered by the Bank, and i s also preparing an investment operation to support the pol icy reforms.

4. On March 18, 2003, the Bank approved the f i rs t Fiscal and Institutional Adjustment Loan (FIAL) to supp‘ort the government’s reform efforts. Th is f i rs t single- tranche structural adjustment loan, in an amount o f US$300 million, laid out the

The approval rating of the current administration has remained high. The latest polls indicate that 70 percent of Colombians have a favorable image o f the President, and his j ob approval rating i s 64 percent.

principles o f a programmatic operation that would total an estimated US$900 mill ion and would conclude in FY 2006. This program has two objectives: First, to promote reforms addressing fiscal rigidities necessary to attain the substantial fiscal adjustment underlying sustainable macroeconomic stability; and second, to improve the provision of public services and establish the institutional basis for higher efficiency and accountability in public expenditure. The focus of the reform program will gradually shift from tax and fiscal responsibility at the beginning, to expenditure and public expenditure reform in the later stages.

5. This Program Document presents the second loan o f the FIAL program (FIAL 11) for an amount of US$lSO million in a single tranche. Each of the loans in the FIAL program has a particular thrust within the overall scope of the reform; while FIAL I was heavily weighted toward tax policy as the initial and most urgent effort toward fiscal sustainability, the primary emphasis of the proposed FIAL I1 i s on establishing the legal and normative framework of the key elements of public sector reform, including procurement, royalty transfers, and fiscal responsibility, and the implementation of management contracts with two government agencies and the definition o f the budget reform strategy. FIAL I11 i s expected to focus mainly on the results o f the tax administration efforts, the operation of a framework o f legal defense of the State, new asset management legislation, and the effective implementation o f the mandates o f the procurement and fiscal responsibility laws. The fourth and final FIAL I V wil l emphasize the full implementation of the tax reform, the enactment of the budget reform, the expansion o f the management contracts scheme, additional performance management tools, and the overall evaluation of the reform process.

6. As shown later in this document, progress in the reform program has been satisfactory, and there have been significant accomplishments derived from the first FIAL loan. Most notably, the government has enacted a substantial tax reform package that i s expected to yield an additional 1 percent o f GDP in revenue this calendar year, as well as the initial steps of several key initiatives of public sector reform. The FIAL II loan i s well synchronized with the accomplishments to date, and sets the stage for further reforms during the remaining three years of this government’s administration.

11. CONTEXT OF THE OPERATION

A. RELEVANT SOCIOECONOMIC BACKGROUND

7. Macroeconomic Performance. During 1998-2002, the economy suffered from stagnation, but today confidence in the economy i s slowly returning, as signs o f recovery and growth continue. The economy grew by 3.3 percent in the first semester o f 2003, which i s the biggest gain in GDP in five years, and i s expected to grow by about 2.5 to 3 percent this calendar year and by 3 to 3.5 percent in 2004. Although the unemployment rate fell from 16 percent in the first quarter of 2003 to 14 percent in the second quarter of the same year, i t remains to be seen whether the economy i s now firmly established on a path of growth and stability. Total investment now stands at about 14 percent o f GDP, with private investment under 6 percent, which w i l l not sustain significant growth. While

2

government consumption grew by two thirds between 1994 and 2002, household consumption remained basically unchanged. Inflation declined in 2002, assisted by sluggish demand, and was about 6 percent, and i s expected to be about the same in 2003.

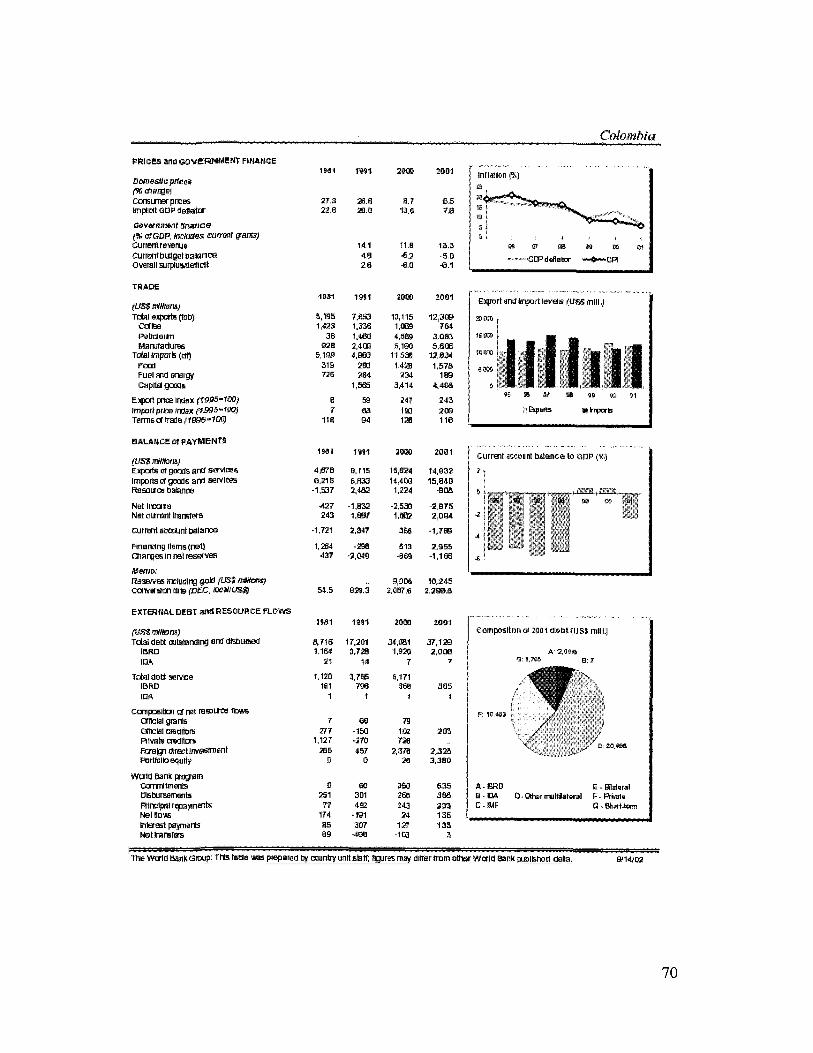

8. Colombia’s exports increased in the f irst semester o f 2003 relative to the same semester in 2002. This increase can be explained mostly by carbon exports. While the country’s nontraditional exports, mainly manufactured goods and cut flowers, performed well in recent years and now amount to over half o f total merchandise exports, the appreciation of the peso and the economic slowdown in the United States, Venezuela, and other Andean countries affected them negatively in the first semester of 2003. Increasing imports have, however, maintained a deficit in the trade balance. The total external current account had a deficit o f about 2.1 percent o f GDP in the f i r s t semester o f 2003. 9. Fiscal Performance. Over the past half-decade, new realities have emerged in Colombia’s fiscal domain, including significant deficits and large future fiscal liabilities. The rapid expansion of the public sector over the previous decade, from spending one- fourth of GDP in 1990 to over one-third of GDP today, combined with growing pension and other liabilities, has led to significant and persistent structural deficits. As public spending rapidly outstripped the sector’s revenue-generating capacity, m u c h of the fiscal deficit was financed with debt, both domestic and external. Today, total public sector debt in Colombia i s over 50 percent of GDP. The deficit of the consolidated public sector for 2002 was 3.6 percent of GDP, largely due to election-year spending, higher military outlays, and a weakening o f the social security institutions. For security spending, the current administration estimates that i t w i l l need an additional 1 percent o f GDP per year. 10. Nevertheless, the Uribe Administration has stressed i t s commitment to continue the fiscal adjustment efforts o f the previous administration. On December 20, 2002, Congress approved a strong tax package estimated to increase tax collections by close to 1 percent of GDP in 2003 and rising in the next two years. The fiscal deficit for the Combined Public Sector i s expected to come down to 2.5 percent of GDP in 2003 and about 2.3 percent in 2004. As a precaution, the Government requested a Stand-By Agreement from the International Monetary Fund (IMF). The first review of the Stand- B y Arrangement was satisfactorily completed on June 11, 2003. A l l performance criteria and structural benchmarks for end-2002 and end-March 2003 have been met.

11. Congress passed two key structural reforms: a pension reform (Law 797, January 2003) to address the looming deficits o f the social security sector, Colombia’s largest future fiscal liability, and a labor reform to increase flexibility in Colombia’s rigid labor market. An overhaul of the public administration sector i s well underway. Additionally, Telecom was liquidated and Cajanal and Caprecom were massively reformed. In June 2003, the Government of Colombia (GOC) was finally successful in passing through Congress a reform of the Znstituto de Seguridad Social (Social Security Institute, ISS), which includes the separation o f health service provision and financing. In late June Congress approved a fiscal responsibility law.

3

Figure 1: Fiscal Deficit 1994-2002 (Percentage of GDP)

40%

23

Source: Superior Council for Fiscal Policy (CONFIS).

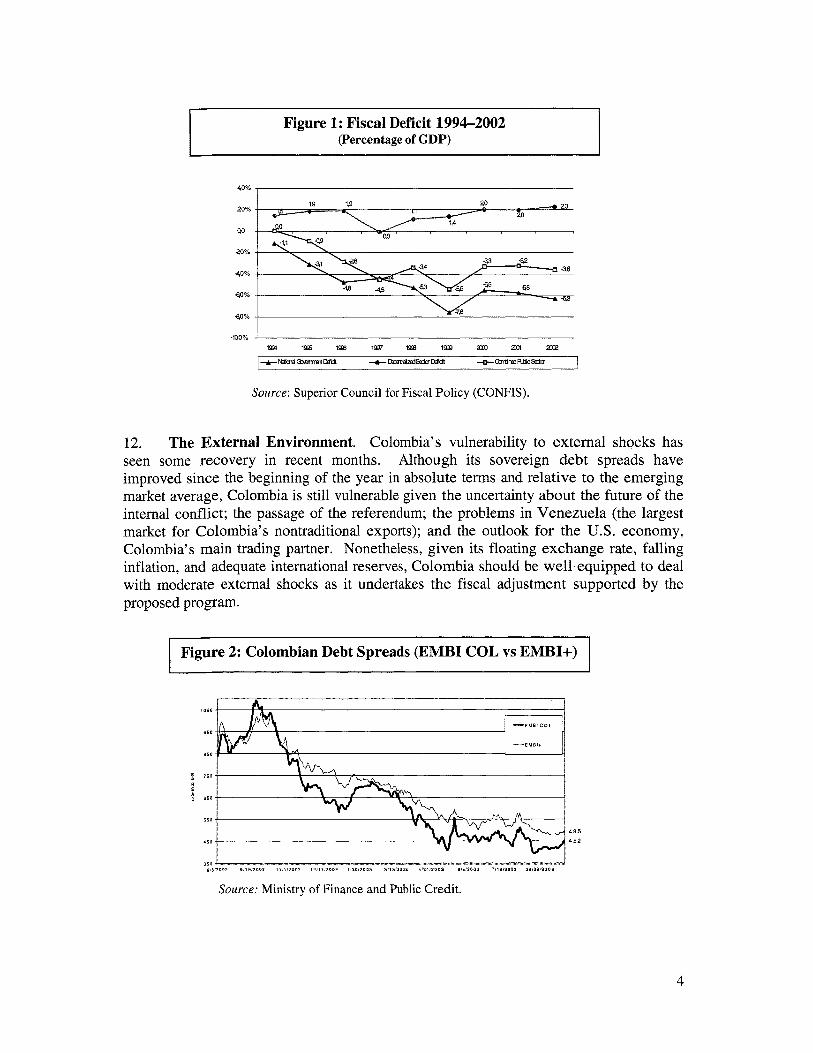

12. The External Environment. Colombia's vulnerability to external shocks has seen some recovery in recent months. Although i t s sovereign debt spreads have improved since the beginning of the year in absolute terms and relative to the emerging market average, Colombia i s s t i l l vulnerable given the uncertainty about the future o f the internal conflict; the passage of the referendum; the problems in Venezuela (the largest market for Colombia's nontraditional exports); and the outlook for the U.S. economy, Colombia's main trading partner. Nonetheless, given i t s floating exchange rate, falling inflation, and adequate international reserves, Colombia should be we l l equipped to deal with moderate external shocks as i t undertakes the fiscal adjustment supported by the proposed program.

Figure 2: Colombian Debt Spreads (EMBI COL vs EMBI+)

818,2002 011912002 ,11112882 ,21,,12002 t11012003 3,1912011 112412003 bi i i210, 1118,2003 * o I $ 1 * e o P

Source: Ministry of Finance and Public Credit.

4

13. Poverty. In Colombia, there has been a close positive correlation among fiscal balance, g rowth , and poverty reduction. During periods of positive growth (and fiscal balance), C o l o m b i a enjoyed substantial declines in poverty (even though inequality increased). Specifically, from 1988 to 1995, as GDP grew on average at about 4.2 percent per year, poverty rates declined from about 65 to 60 percent o f the population. This reduction, and the government’s efforts that helped achieve it, w e r e completely wiped out by the 1998-99 recession. Poverty levels today are not substantially different from what they were in the late 1980s. Although unemployment has dropped from around 15.7 percent last year to 14 percent during the second quarter o f 2003, i t i s yet not clear whether the economy has stabilized to sustain this level. Put differently, the evidence suggests that sustainable growth and fiscal balance have been Colombia’s best social safety net. A fiscal balance program that increases revenue and makes expenditure more efficient, and within prudent l imi ts, i s a sine qua non for Colombia’s attaining the human development Millennium Development Goals (MDGs). 14. Insecurity and Violence. Colombia has captured headlines around the world for its alarming indexes of violence. Since the 1980s, the multidimensional problem of violence has become more widespread and i s exacting an increasing economic and social toll. From 1 9 9 9 to 2002, the number o f attacks on petroleum infrastructure increased by 160 percent, on electric infrastructure by 680 percent, and kidnappings by 126 percent over the average o f the previous 13 years. I t i s estimated that the conf l ic t reduces the annual economic growth rate by at least 2 percent. The conflict places the country in a particularly vulnerable and difficult position; i ts repercussions for the economy and the overwhelming social demand for i t s settlement make peace the paramount priority of the government’s public policy agenda.’ As crucial complements to the direct counterinsurgency measures, the government recognizes the need to sustain fiscal balances and improve the quality and efficiency of public services. 15. In h i s 2003 report to Congress delivered on July 20, President Ur ibe presented encouraging signs that the government’s strategy on democratic security i s yielding positive results. During the f i rst semester o f 2003 there were 24 v io len t attacks on populations, the lowest in 10 years and just over one-third of the number for the f irst semester of 2002; attacks on economic infrastructure are down 58 percent over the same period, and homicides declined by 21 percent and kidnappings by 34.2 percent. Although there i s st i l l significant uncertainty over the evolution of the armed conflict, a n d paramount challenges s t i l l remain ahead, the statistics for the first half o f 2003 could show the beginning of a reversal in the trend toward increased violence that began in the late 1990s.

B. FISCAL AND INSTITUTIONAL ISSUES

16. The fundamental issue that constrains the effective implementation of publ ic policy in Colombia i s the inability of the Government to access the necessary budgetary resources to attend policy priorities. Regardless of the political commitment to promote

’ It has been estimated, for instance, that war-related additional public expenditures w i l l reach 1.5 percent o f GDP by 2006.

5

peace and development, there i s little that can be done without resources. Budgetary shortfalls are clearly not uncommon; fiscal adjustment i s a worldwide reality. However, the nature of the Colombian fiscal imbalance i s particularly complex due to the interplay of insufficient tax revenue, inefficient and rigid expenditure, and the lack o f an adequate legal framework for fiscal responsibility.

17. Some of the key issues that make up the spectrum of constraints to effective public policy that were faced by the incoming Uribe administration in August 2002 are:

18. Insufficient Resources for the Implementation of Public Policy. The Colombian Central Government tax burden has hovered under 20 percent o f GDP for the last few years,2 which was insufficient to undertake the ambitious government agenda, and substantial reforms in both tax policy and administration were required. A Bank- supported tax reform law enacted in December 2002 significantly broadened the tax base and reduced a number of exemptions. I t has already had visible impact on the revenues in the first semester of 2003, although the Constitutional Court challenged some key elements scheduled to go into effect in 2005. Tax administration measures are underway with support f rom the Bank, but most o f the challenges in this area s t i l l l i e ahead and involve efficient information usage, improved auditing, and a revision o f bylaws and regulations.

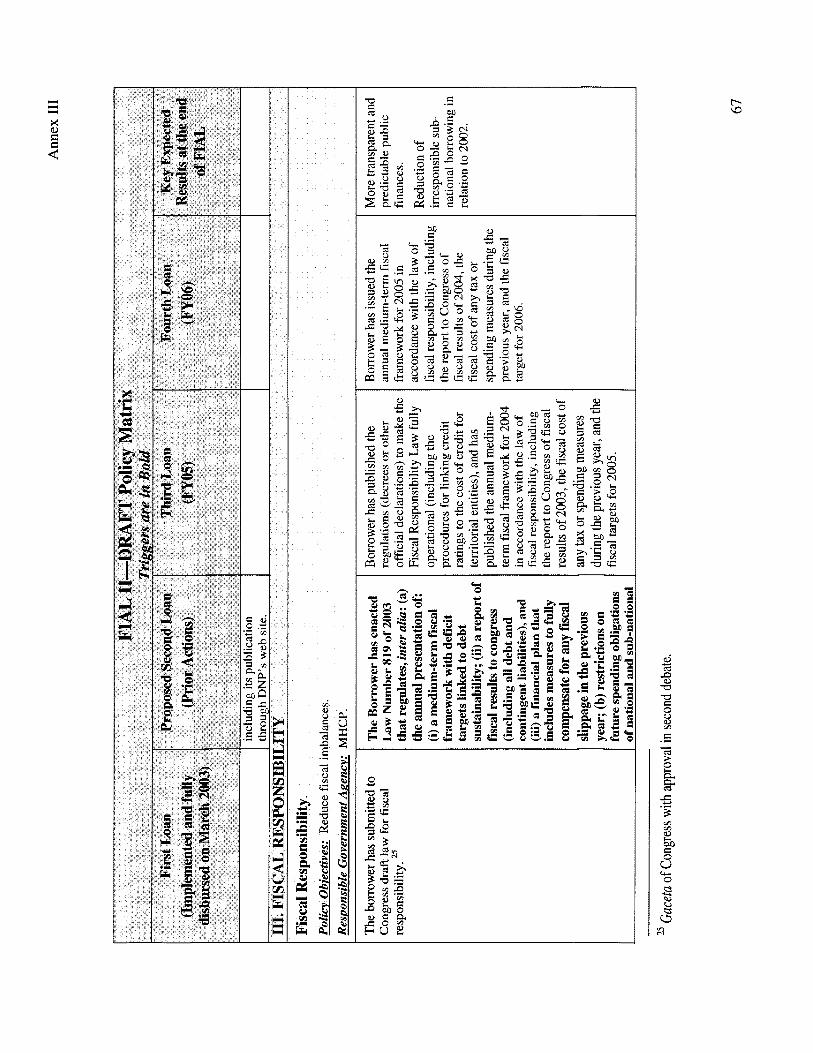

19. Lack o f a Fiscal Responsibility Framework. Many countries in the region have increased the odds of fiscal sustainability by approving laws that establish certain basic fiscal responsibility guidelines. These guidelines pertain to matters such as debt ceilings, subnational borrowing, medium-term fiscal planning, and reporting and accountability. The lack of such framework at the national level in Colombia made i t diff icult to align expenditures to within affordable and sustainable l imits. In June 2003, the government enacted the Fiscal Responsibility Law, which i s one o f the key benchmarks under the FIAL program.

20. The Colombian public sector lacks the institutional and legal framework to appropriately identify, assess, value, regularize the titling, and if necessary dispose o f assets-particularly real estate-that are part o f i t s capital stock. Not only are unnecessary expenditures generated when assets cannot be easily transferred from one activity to another, but a potential source of capital revenue i s not realized when assets unrelated to public policy priorities cannot be sold. Not having the appropriate mechanisms for asset management costs the public sector hundreds of millions of U.S. dollars.

21, Inordinate Growth of Liabilities against the State. Although reliable estimates s t i l l do not exist, contingent liabilities to the State that arise from legal action could reach as much as 2 percent o f GDP if current trends continue. The legal claims that generate such massive losses to the State have varied origins, including labor or administrative disputes, but the most significant source are contracts in areas such as concessions or public works that have gone into arbitration. Significant efforts need to be invested to strengthen the public sector’s capacity to defend itself, in parallel to an overhaul of the administrative processes (such as procurement) that lead to poorly designed contracts.

Inefficient use of Public Assets.

* Source: Directorate o f National Taxes and Customs (DIAN).

6

22. Inadequate Budgeting. The Colombian budgeting system i s plagued by numerous structural problems that are unquestionably key contributors to the difficulties in policy implementation, such as (a) the large number o f legally mandated expenditure entitlements eliminates the fiscal space needed to accommodate revenue shock or changes in expenditure priorities; (b) a budget structure that i s incompatible with economic, functional, or performance analyses; (c) a Ministry of Finance with limited authority to regulate public expenditure aggregates; (d) complex institutional arrangements that in effect divide the budget process into separate current expenditure and investment processes; (e) budgeting definitions that do not fall under internationally accepted standards; (0 a lack o f instruments to develop a medium-term vision of fiscal policy; and (g) a lack of substantial evaluation of public expenditure results, among others.

23. Inefficient System of Royalty Transfers. The Constitution establishes a rigid system of royalty transfers through the National Royalty Fund (FNR) that does not promote efficiency in their use. In order to obtain higher value-for-money in some of the key areas to which the royalties are directed, such as education, it i s important to improve the targeting mechanisms via constitutional reform if necessary in order to achieve higher impact from limited resources.

24. Complex and Ineffective Public Procurement System. There i s a high fiscal cost associated with an inadequate public procurement system. Not on ly are the costs o f government contracts higher than they would otherwise be, but poorly designed contracts (intentionally or not) find their way directly into litigation and generate large liabilities for the State. The Colombian procurement system i s not only ineffective in overseeing potentially conflictive contracts, but i s also plagued with complexities that raise the cost to bidders and cloud an effective application of modem procurement principles.

25. Lack of Incentives for Performance. The Colombian budget system does not have adequate mechanisms to promote performance at the agency level. Furthermore, the administrative regulations (such as human resource management) are fairly rigid and make i t difficult for public sector managers to be empowered with more flexibility. Under this scenario, i t i s difficult to have a serious system of performance evaluation that carries real consequences for both the agency and the government. Within a n environment of severe fiscal constraints, i t i s imperative to develop instruments to promote enhanced performance in the short term.

26. Past Government Responses. All recent governments have attempted to reverse these negative trends. However, the responses primarily addressed revenue and were partially ineffective with respect to the expenditure side, that is, reform of the public sector. To attempt to deal with excessive spending, previous administrations had launched several public sector reform programs. Yet these in i t ia t ives4ur ing 1992 and 1994, during 1998 and 1999, and in 200O-did not fully reach their desired outcomes. The limited success of these past reforms was primarily due to (a) some reforms, especially those between 1998 and 1999-though explicitly focused o n expenditure reduction-faced legal or political obstacles; and (b) other reforms were not primarily targeted to expenditure reduction or to effectively tackle the inner roots of rigid growth in fiscal transfers or legal claims against the State. After these attempts at reform, the

7

Colombian pub l ic sector still requires a significant effort to reduce inefficiencies, align responsibilities, foster transparency, and improve management and accountability.

111. THE GOVERNMENT’S REFORM PROGRAM

27. General Framework: The Estado Comunitario and the Future of the Colombian Public Sector. The idea of Estudo Comuniturio l ies at the heart o f this government’s public sector reform program. The Estudo Comuniturio i s a set o f basic reform guidelines put together and demonstrated in practice by President Uribe at the time he was governor of the department of Antioquia, perhaps the most developed intermediate-level administration in Colombia. Already elaborated and announced during President Uribe’s campaign, the concept of Estudo Comuniturio inspired criteria for the selection of entry points and impact evaluation o f public sector reform under the current administration. Although s t i l l evolving as a guiding concept of public sector reform, the Estudo Comuniturio incorporates and adapts to Colombia a number of widely accepted, contemporary principles of public sector reform that wi l l guide the renovation of the Colombian public sector under the current administration.

28. The concept of the Estudo Comuniturio i s the foundation of the National Development Plan 2002-2006. The fundamental principle underlying the concept is that the State should exist for the service of i t s citizens and not for the benefit o f special interests. The Estudo Comuniturio involves c iv i l society in the attainment o f social objectives; i t i s a modern State where scarce resources are invested wisely and efficiently; and i t i s a decentralized State that stands for regional autonomy with transparency, political responsibility, and community participation.

29. The National Development Plan proposes the development o f the Estudo Comunitario through four basic pillars:

0

0

0

e

30.

Democratic Security. The State must provide security and protection to all Colombians, without political, ideological, religious, or socioeconomic distinctions. Sustainable Development and Employment. Economic growth stagnated during the last few years and unemployment has grown by around 10 percent since 1999. The State must provide the conditions to recover the path to economic growth. Social Equity. The State must ensure that the fruits o f economic growth are enjoyed by all Colombians. Renovation of the State. The State must modernize i t s administration and reform intergovernmental relations. The ultimate goal i s to build a managerial, participatory, and decentralized public sector.

The Estado Comunitario and the Fiscal and Institutional Reform Program. The fundamental purpose o f the Fiscal and Institutional Reform Program i s to liberate resources for the effective implementation of public policy and to generate efficiency and transparency gains that wi l l contribute to fiscal sustainability and the improvement of service delivery. In this sense, the Program i s a necessary condition for the attainment of

8

the goals of the National Development Plan as described above. Democratic Security hinges upon the availability of untied fiscal resources, within a framework of macroeconomic stability, to invest in restoring peace to the country; Sustainable Development requires a sound macroeconomic framework and effective fiscal policy; Social Equity requires ability to deliver improved services to the poor and increase their ability to benefit from economic growth; and the Renovation ofthe State clearly entails efficiency and transparency gains and the necessary institutional strengthening actions to deliver more and better public services in a fiscally sustainable way. The reform program designed to implement this vision involves a wide array of constitutional, legal, and administrative measures that, together, represent the most significant reform effort since the Constitution of 1991.3 3 1. Concept and Structure of the Public Sector Reform Program. The core of the reforms i s contained in two reform packages known as the Tax Reform and the Renovation of Public Administration. These two packages are framed within and supplemented by other government reforms in such a way that the magnitude and expected impact of the former cannot be adequately grasped without reference to the latter. The program i s both coherent with and strengthened by the constitutional and legal reforms courageously undertaken by the current administration, involving a popular referendum scheduled for October 2003, a resubmission of a constitutional reform that was struck down by the Senate in July 2003, a pension reform, the reform of the Central Government structure, and a fiscal responsibility law enacted in June 2003. Al l these reforms have significant fiscal implications and should establish the necessary basis for Colombia’s political reconstruction and economic recovery.

Iv. THE FISCAL AND INSTITUTIONAL REFORM PROGRAM

A. OVERVIEW

32. Objectives of the Program. The Fiscal and Institutional Reform Program i s supported by the Bank through the series of four single-tranche Fiscal and Institutional Adjustment Loans (FIAL). The Bank approved the f i rs t loan of the program in March 2003 for an amount of US$300 mill ion out o f an estimated total of US$900 million for the entire program. This program has two objectives: first, to promote reforms addressing fiscal rigidities necessary to attain the substantial fiscal adjustment underlying sustainable macroeconomic stability; and second, to improve the provision of pub l i c services and establish the institutional basis for higher efficiency and accountability in public expenditure. The focus o f the reform program w i l l gradually shift from tax and fiscal responsibility at the beginning, to expenditure and public expenditure reform in the later stages.

World Bank projects are supporting these reform efforts through a combined package of structural reform projects that include overall rationalization o f public expenditures (including pension and social security expenditures), labor reform, tax reform and tax administration, financial reform, and improvement of health, education, and family services.

9

33.

34.

The specific objectives o f the FIAL program are to:

Increase tax revenue and reduce distortions in the tax system; Modernize the tax administration; Promote the development of a sound fiscal responsibility legal framework; Reduce losses and generate revenues through improved asset management; Prevent massive losses to the State from judicial claims; Improve budget management with modern tools and legal reforms; Develop incentives for efficiency gains in subnational entities; Strengthen the public sector procurement system; Improve performance through management contracts for agencies; and Support a coherent and comprehensive reform implementation process.

Table 1 describes the expected aggregate results of the reforms supported b y the FIAL program.

Table 1: Expected Aggregate Results of the FIAL Reforms Objective I Expected Resalt

Promote reforms addressing fiscal rigidities 1 Average annual contribution to total fiscal revenues of necessary to attain the substantial fiscal adjustment underlying sustainable macroeconomic stability.

1.4 percent of GDP from 2003 to 2006; Average annual contribution to a reduction in current expenditures of 1.6 percent o f GDP from 2003 to 2006.4 Increased reliability and transparency in medium-term fiscal planning and a framework for more realistic

0

0

I budgetinn. Improve the provision of public services and establish the institutional basis for higher

A public expenditure system more closely linked to results;

efficiency and accountability in public expenditure.

0

0

0

Improved targeting of public expenditure toward public policy priorities; A more transparent, simpler, and institutionally robust system o f public sector procurement; More efficient and cost-effective use of the assets of the D u b k sector.

35. Achievements under FIAL I. FIAL I supported a successful package of reform measures, including (a) enactment of a tax reform law; (b) implementation o f important tax administration measures such as increased withholding at the source and improved information exchange with banks; (c) enactment of a law authorizing a Constitutional referendum that, among other things, reforms the royalty transfer system; (d) enactment of Law 790 that strengthens the Ministry of Interior and Justice’s Directorate of Judicial Defense; (e) issuance o f Decree 2170 improving the public procurement system; (f)

Including the overall effect of the referendum. Without the referendum this average i s approximately 0.7 percent per year for the same period. Additionally, some Bank data not yet reviewed with the Government were used for the estimate of the impact on expenditures.

10

creation of a commission for asset management; and (g) selection of two pilot agencies for the implementation of a management contracts scheme.

36. Changes in the FIAL Program Since the Approval of FIAL I. The program has not undergone substantial changes since the approval o f the first operation. The structure of t he program and both the general and specific objectives remain unchanged, although the policy matrix has undergone a process of clarification and streamlining while still ful ly reflecting the scope of the reform program. On the contrary, the matrix has been strengthened by the establishment o f specific quantitative targets in some components that in most cases go beyond those established originally, and reflect the strong pace of the reform program led by the Government.

37. Of the subset of prior actions for FIAL I1 that have been defined as a trigger^"^ in the FIAL I document, there have been three components where the sequence and measurement of the reforms have been changed:

0 Budget Reform. The original FIAL matrix called for the presentation of the Organic Budget Code to Congress as for FIAL 11. However, the political environment surrounding the .referendum, coupled with the potentially controversial nature of the Code (primarily because i t seeks to reduce politically attractive permanent expenditure entitlements and revenue earmarks), has forced the government to take a more cautious and deliberate process of presentation of the bill to Congress. This wi l l now take place before FIAL 111 goes to the Board, while the approval of a policy document outlining the elements of budgetary reform wi l l be approved for FIAL I1 and the Organic Budget Code approved for FIAL IV.

Tax Administration. The original FIAL matrix called for the operation of an integrated tdcustoms taxpayer current account system for the largest taxpayers during 2003. However, DIAN adopted a new information technology strategy during th is year that calls for the development o f a platform that will provide integrated accounts for al l taxpayers, but which w i l l not be ready until mid-2004. This new strategy i s being supported and partially financed through the Bank- financed Public Financial Management Project I1 (MAFP 11). Therefore, the original policy action has been removed from FIAL I1 and introduced into FIAL 111 with a broader coverage.

0 Asset Management. The original FIAL matrix used revenue targets to measure the progress of the asset management program. Following expert advice, the program now measures this with both institutional development indicators and coverage in terms o f assets by the asset management system, wh i l e the revenue targets have been discarded.

0

The triggers defined for this operation are a subset of the policy matrix and are prior actions that need to be fulfilled for the approval of this loan by the Bank. They have been identified as the key elements of the reform process and serve as guideposts of the progress o f the program. As part of the prior actions, these triggers are included in the loan agreement and are part o f the package o f policy measures that sustain the loan. As this i s not standard practice in programmatic lending, special authorization was received from the Legal Department.

11

38. Expected Results under FIAL 11. The measures supported b y FIAL I1 are expected to y ie ld important results, including (a) issuance o f all legislation to regulate the application of the tax reform law; (b) further improvements in tax administration, including specific audit targets and the implementation o f integrated tax-customs audits; (c) approval of an official budget reform strategy; (d) Congressional approval o f an improved 2004 Annual Budget Law; (e) presentation to popular vote of the Constitutional referendum; (0 issuance of a new policy for legal defense o f the state; (g) presentation to Congress o f reforms to the public procurement law; (h) approval of an official asset management policy and the achievement of specific revenue targets; (i) signature of management contracts with two government agencies; and (i) enactment o f a Fiscal Responsibility Law.

39. Foreseen Results of FIAL I11 and IV. FIAL I11 i s expected to focus primarily on the following key policy actions: (a) achievement of specific targets of the tax reform; (b) unification of taxpayer accounts; (c) presentation o f the Organic Budget Code to Congress; (d) full implementation of revised royalty transfer scheme; (e) establishment of the institutional arrangements of the procurement system; (f) evaluation of the pilot management contract scheme; and (g) full implementation of the Fiscal Responsibility Law. FIAL I V wi l l focus on actual results from the tax policy and administration measures and the approval of the Organic Budget Code, implementation of medium-term budgeting, extension of the management contract scheme, and the effective implementation of the procurement, fiscal responsibility, asset management, and legal defense policies.

40. Overall Assessment of the Reforms. The Government has shown a high level of commitment and resiliency in pursuing the objectives o f the reform, which i s largely based upon the President's campaign platform and his initial presidential directives for public sector modernization.6 During the f i rst year of the Uribe Administration, the executive has worked with Congress for the enactment o f over 100 laws, including major reforms in tax policy, pensions, labor, fiscal responsibility, and most important, the approval to present a referendum to the population with significant measures for fiscal sustainability and reduction in the levels o f cor r~p t ion .~

41. The tax reform supported by FIAL I (and i t s full regulation by FIAL 11) has shown important results and statistics show that revenue has increased according to expectations. Nonetheless, the government i s s t i l l considering further measures to raise revenue while observing international best practices in tax policy. To complement the tax reform and as a prelude to the upcoming budget reform, Congress approved the Fiscal Responsibility Law, which sets out important principles for fiscal sustainability and transparency. Expenditure-side reforms of the kind supported by the FIAL are more complex and some of them show results only in the medium or long term; however, some indicators that show that the reform process i s on track are the following: (i) The

On July 26th, President Uribe held his first live, televised cabinet meeting where the Ministers presented reports on their accomplishments to date. Most of the objectives o f the FIAL, notably in taxation, budgeting, procurement, and fiscal responsibility, were explained and discussed at length.

The Constitutional Court recently ruled that most of the questions in the referendum are constitutional, including all related to the FIAL. Shortly afterward, the Government set the date of October 25" for the vote.

12

government has taken the overhaul o f i ts budgeting system very seriously and has obtained assistance from the Bank, the IMF, and other entities in the design of a new budget law; (ii) The 2004 Budget Bill was submitted to Congress and approved incorporating substantial improvements in terms of medium-term planning and the provision o f useful information for fiscal analysis; (iii) Strategies have been defined and institutional arrangements established to oversee areas such as asset management, legal defense of the state, and public sector procurement; (iv) A novel management system i s being piloted to enhance accountability for results; and (v) A referendum to consult the population on key issues involving fiscal, political, and institutional issues has been scheduled for October 25.

42. The FIAL Program within the Bank’s Country Assistance Strategy (CAS). Under i ts objective of achieving fast and sustainable growth, the CAS approved in December 2002 indicates that, “The main objective o f the IBRD’s strategy in terms of the macroeconomic framework would be to support Colombia’s continued fiscal adjustment, including the quality of the adjustment, as key for achieving faster and sustainable growth. To support this, the IBRD, in close collaboration with the IMF and the IDB, w i l l prepare a Programmatic series of Fiscal and Institutional Adjustment Loans (total US$900 million) to support fiscal adjustment, including reforming the tax system, strengthening the tax administration, implementing a fiscal responsibility law and reforming the public sector.” The CAS scheduled the first loan of the program for FY03 in the amount of US$300 million, followed by two loans o f US$l50 mi l l ion each in FY04 and FY05, and a final US$300 mill ion loan in FY06.

43. Linkage between the Programmatic Fiscal and Institutional Adjustment Program and other Bank Operations and Activities. The proposed Programmatic series of Fiscal and Institutional Adjustment Loans to support public sector reform and fiscal adjustment i s the core of the Bank’s support to the reform efforts of the government, and wi l l provide the basis upon which complementary policy-based operations wil l be developed. These include support to the financial sector in the form o f Programmatic Financial Sector Adjustment Loans (FY03 and FY04) that aims to promote the development of a well-functioning financial system that can provide adequate services to all segments of the productive sector and the population at large. In addition, building on the achievements o f the Financial Sector Adjustment Loan (FYOO), it w i l l address the remaining agenda to ensure the health and financial sustainability of the banking system and to foster capital markets development.

44. The anticipated Sustainable Development Sector Adjustment Loan (FY05) w i l l support the mainstreaming of the environment in practically a l l infrastructure sectors, including water and sanitation, energy, transport, and disaster management. The tools for mainstreaming environment include policy setting, strategic environmental assessments, land use planning @lanes de ordenamiento territorial), permits and licensing, environmental regulation, economic and fiscal instruments, social impact analysis and valuation, assessment and linkage with global environmental goals, participation a n d conflict-resolution mechanisms, and development o f sector-environment indicators l inked to health impacts. These tools are currently being used in most sectors, however, this operation aims to enhance effectiveness and impact by providing a more rational

13

application based on priority-setting and institutional analysis (how the environmental management institutions set priorities, receive budgets, and function).

45. The FIAL program shares some areas of mutual interest wi th the Programmatic Labor Reform and Social Sector Adjustment Loan (PLaRSSAL) approved by the Bank during the second quarter of FY2004. The task teams have worked in coordination, and the two main areas of interaction are (a) Management Contracts for Government Agencies. Both programs seek to improve the efficiency and effectiveness o f Colombian Family Welfare Institute (ICBF) and the National Training Service (SENA). The FIAL approaches t h i s issue through the creation o f a new instrument for improving management that can then be replicated to other entities and sectors. PLaRSSAL, on the other hand, i s concerned with the substantive impact of the managerial reforms on quality and coverage of service delivery.8 (b) Incentives for Efficiency Gains. This FIAL component has the objective of introducing incentives that promote the use of results- based management to improve efficiency and effectiveness of fiscal transfers to the subnational levels, particularly in the education sector, and wi l l support the presentation of the referendum to popular vote which includes a provision to assign 56 percent of the National Royalty Fund to education projects exclusively to increase school attendance in vulnerable groups. Other quantitative and qualitative sector-specific outcomes and indicators are considered in the PLaRSSAL.

46. In addition, the FIAL program i s highly interrelated with the current Public Financial Management Project II (MAFPII), aimed at strengthening budgeting, tax administration, public investment management, procurement, and results management. This Bank-financed Technical Assistance Loan (TAL), in implementation since August 2001, i s the most important source of technical assistance funding for the implementation of the FIAL policy actions. Although i t was approved before the FIAL discussions began, i t s objectives are fully consistent with the FIAL policy matrix. The components that are within i t s scope and are receiving assistance are tax policy, tax administration, budgeting, and procurement. Support for management contracts for government agencies and the monitoring of the overall reform process also fall within i t s scope, and technical assistance w i l l be made available shortly.

47. Complementarities with other Institutions’ Operations. The IDB i s preparing an investment operation of approximately US$18.3 million, designed to support the implementation of the overall reform program and specific support to asset management, legal defense of the State, and information technology. Both task teams are working in close coordination since the IDB’s components of asset management and legal defense of the state wi l l support and be consistent with the FIAL’s policy matrix. This loan i s expected to go to the IDB’s Board o f Directors during the last quarter of 2003.

48. Institutional Assessment. The FIAL program i s being executed b y the Ministry of Finance (MHCP) with the support of the National Planning Department (DNP). MHCP wi l l ensure the full execution o f the policy measures and “triggers” established in the program. These activities wi l l be carried out in close coordination with DNP.

In other words, the FIAL i s concerned with the success of the “instrument,” whereas the PLaRSSAL i s concerned with the “substance” of the reforms in ICBF and SENA.

14

49. Given the size and relative complexity of the program, the General Vice-Minister of Finance, working closely wi th the Deputy Director of DNP, will be responsible for the strategic management of the program. These two agencies have the consensus-building capacity and political, technical, and operational support required to assume this responsibility. Both are part o f CONFIS, participate actively in Congressional debates and Cabinet meetings, and serve as counterparts to the IMF and other multilateral agencies as representatives of the Finance Minister and the Director of DNP. In addition, the Vice-Minister of Finance and the Deputy Director of DNP are responsible for the execution of MAFP-TI[ and i t s respective institutions. They w i l l be capable o f establishing synergies and synchronizing the parallel development of MAFP-11 and

50. The strategic management of the program will involve the fol lowing actions: (a) being the interlocutor of the national government with the Bank; (b) supporting and managing the fulfillment of the policy actions of the various program components; (c) coordinating the development o f the planned actions and reforms with those responsible within the various entities; and (d) compiling and sending the technical, legal, and administrative information required for the execution o f the policy measures of the program.

5 1. To assume the responsibility o f coordination and follow-up of FIAL-11, an inter- ministerial working group has been established within MHCP, comprising all agencies and entities involved in the program, including MHCP, DNP, the M in i s t r y of Social Protection, the Ministry of Justice and the Interior, SENA, and ICBF. Each of these entities has designated one high-level professional as a representative to this inter- ministerial working group, and as the one directly responsible for program components. Table 2 outlines how responsibility for each of the program components has been divided.

FIAL-II.

Legal Defense of the State Public Sector Procurement Asset Management Public Sector Reform Monitoring and Evaluation of State Reform Fiscal Resoonsibilitv Law

and ICBF Ministry o f Justice and Interior (Vice-Minister) DNPLegal Advisory Group DNPLnfrastructure Department DNPPublic Administration R e f o r m Program DNP/SINERGIA and MHCP/CONFIS MHCPRechnical Vice-Minister

52. For the development o f the duties required for the strategic management of the program, the Vice-Minister of Finance has the support of expert professionals within the Superior Council o f Fiscal Policy (CONFIS) and within the general directorates o f Macroeconomic Policy, Taxes and Customs (DUN), Public Credit, Budget, and the Treasury. For the development of the duties that correspond to DNP, DNP has the

15

support of valuable professionals in the directorates of the Public Administration Reform Program, Infrastructure, Social Development, Justice and Defense, External Credit, and Results Evaluation.

53. As part of the planned measures in FIAL-11, the government has developed a system for monitoring and evaluating state reform, and has announced monitoring indicators for public sector reform progress on the DNP website. The DNP, through the Evaluation System for Public Management (SINERGIA) (for components o f Asset Management, Legal Defense of the State, Procurement, Management Contracts, and Management of the Reform Process) and MHCPKONFIS (for components o f Tax Reform, Tax Administration, Fiscal Responsibility, Budget Reform, Incentives for Efficiency Gains, and Management of the Reform) wi l l follow up and evaluate results of FIAL-II. The results of FIAL-I1 wi l l comprise part of the findings of the government's National Development Plan for 2002-2006. The government has the mandate to follow up in terms of effectiveness, productivity, and efficacy, and the results o f the follow-up and evaluation w i l l be reported to the Bank by means of periodic reports.

54. Technical Assistance. Many of the technical assistance requirements o f several key components-particularly tax administration, budgeting, and procurement-as well as the financial management or evaluation features of other components, w i l l be partially or fully provided by the MAFPII project, currently in execution. In addition, the Government and the IDB are considering including technical assistance support for other FIAL components-particularly asset management and legal protection o f the State- under an IDB-TAL project currently under preparation. Moreover, the GOC and the Bank are exploring complimentary grant financing through Institutional Development Facilities (IDFs) or Policy and Human Resources Development grants (PHRD) to support the reform process. Table 3 summarizes the technical assistance arrangements.

Table 3: Sources of Technical Assistance for the M A L Program Component t Source(s) I status

Tax Reform I MAFP I1 (IBRD) I In execution

55. Fiscal Commitments. Within i t s macroeconomic framework, the government signed a new Stand-By loan with the IMF in the amount o f SDR1.5 b i l l ion for the next two years (see Annex 11-Fund Relations Note). Achieving the structural benchmarks of

16

the agreement will constitute an overarching pol icy condition for the FIAL. Some of the targets of the IMF-backed program for 2003 are a Combined Public Sector deficit of 2.5 percent of GDP, a current account deficit o f 0.8 percent of GDP, and an inflation rate between 5 and 6 percent.

56. Although fiscal performance has remained within the framework o f the IMF agreement through the first semester, there i s widespread expectation that the year-end deficit w i l l b e above 2.5 percent of GDP. This will be fueled by several factors, among them the seasonality o f expenditures and a supplemental budget to be considered by Congress that includes unforeseen debt payment obligations, pensions, a n d the cost of the referendum. An IMF mission wil l review the progress in the agreement during the last week of October.

B. COMPONENTS OF THE PROGRAM

57. Colombia gets i ts fiscal revenue from three main sources-oi l royalties, customs duties, and domestic taxes. The value of oil revenues depends largely on world market factors beyond the government’s control, although there i s scope for reform of how these revenues are allocated and shared between di f ferent levels of government.’ Customs revenues have generally declined over recent years, with trade liberalization, and this trend should continue for the sake of economic development. The main opportunity for increasing revenues comes from domestic taxation, w h i c h i s also an important area for reducing economic distortions and administrative complexities.

Tax Policy.

For the last 15 years the value o f oil revenues has also suffered from attacks on the p ipe l i nes .

17

Figure 3: Timeline of Changes in Tax Policy Total Income 1990-2002

(‘76 GDP)

16

14

12 n :: 10

6

4 1 , , , 1

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Year

Previous rounds of tax reform, particularly in 1974 and 1986, l e f t the country with 58. a fundamentally sound array of taxes at the national level-on value added, corporate, and personal income. The two aspects of the income tax are largely integrated by exempting dividends from taxation as personal income and giving all corporate forms equal tax treatment. Prior to 2003, capital gains were not taxed at the individual level, which had the advantage o f avoiding double taxation of retained earnings (matching the non-taxation o f distributed earnings and further integrating the business and individual tax systems), but had the disadvantage of reducing revenue and offering opportunities for tax avoidance through schemes to convert current income into capital gains.

59. Aside from the major reforms, however, the tax laws have suffered frequent changes that reduced revenue collection and introduced distortions by granting preferential treatment to special interests or, alternatively, increased revenue and intensified distortions by raising the rates on activities already being taxed. Figure 3 shows the recent timeline of changes in tax policy and revenue. Now, the new government of Colombia has an electoral mandate to raise more tax revenue, and the challenge i s to do so in a way that reduces privileges and distortions.

60. The enactment of Tax Reform Law 788 in December 2002 brought together some of the key policy actions geared to the modernization of Colombian tax policy. This law (a) eliminates exemptions and expands the tax base for the value-added tax; (b) establishes a new ceiling on the wage exemption for the personal income tax, and reduces incentives for non-taxed compensation to employees; and (c) phases out the corporate income tax exemption for capital gains from sales of stock, mutual funds, and real estate, and for profits from previously privileged corporate forms, contracts, funds, or bonds. On a tax-by-tax basis, the 2002 tax reform included the measures shown in Table 4.

Key Policy Actions Undertaken.

18

Table 4. Key Measures of tbe 2002 Tax Reform (Law 788) Tax I Key Effects

Value-Added I A large number of previously exempted or excluded goods and services wil l be Tax

Personal Income Tax

Corporate Income Tax

Other National Taxes and Contributions Subnational Taxes

subject to the V A T at 7 percent from 2003, rising to 10 percent in 2005 Mobile phone rate established at 20 percent Rate on automobile sales wi l l be unified at 25 percent from the current range of 20 percent to 35 percent Collection of VAT on al l capital goods with a 3-year rebate or credit for registered firms making further sales Reduction o f the wage tax exemption from 30 percent to 25 percent with a ceiling of Co1$16 million in monthly wages, and reduction of tax exemptions, tax credit, and non-taxed income for the personal income tax Phase-out of exemptions for capital gains from sales of stock, mutual funds, and real estate, and for profits from a variety of previously privileged corporate forms that often served as tax shelters Reduced access to the special tax regime (20 percent rather than the standard 35 percent) 10 percent special surcharge for 2003, to be lowered to 5 percent in 2004 Does not eliminate the distortionaryfinancial transactions tux implemented in 1999; however, it closes some loopholes for transactions in the real economy and allows exemptions for some interbank transactions not meant to be taxed Rationalizes departmental and district taxes on alcoholic drinks Increases the gasoline tax surcharge transferred to subnational governments by 5

0

percent

61. The Government has moved ahead quickly in the preparation and approval of a large number o f decrees that regulate the implementation of Law 788. Among the most important issued to date are those on dispute resolution, declaration of assets held abroad, inflation adjustment of inventories, closing loopholes to the financial transactions tax, revisions to the value-added tax, VAT exemptions for exporters, taxation of rental property, and determining and imposing penalties.

62. Remaining Challenges. In addition to completing the issuance of regulations for the tax refom, the government w i l l be implementing actions in 2004 that were foreseen in Law 788. These mainly involve reducing the exemptions in the corporate income tax law and reducing from 10 to 5 percent the surcharge on the corporate tax base rate, both of which should improve the overall investment climate and reduce distortions.

19

Table 5: Ta EE INTERNAL TAXES

Income Tax VAT

EXTERNAL TAXES Customs External VAT

GMF (0.3%) TOTAL

9,311 5,763 3,548 2,376 944 1,43 1 682

12,369

9.47 5.86 3.61 2.42 0.96 1.46 0.69 12.58

10,924 6,694 4,230 2,979 1,018 1,960 750

14,653

10.0 6.1 3.9 2.7 0.9 1.8 0.7 13.4

1,613 93 1 682 603 74

5 29 68

2,284

0.54 0.27 0.27 0.31

0.34 -0.01 0.84

-0.03

Source: Ministry of Finance and Public Credit.

63. The provision of Law 788 that established a 2 percent VAT starting in 2005 on previously untaxed goods and services such as basic foodstuffs, health, education, and transportation was recently challenged and rendered unconstitutional by the Constitutional Court because i t violated the principles o f progressive taxation. The expected annual collection from this measure was 800 billion Colombian pesos (approximately US$280 million, for 2005), which the government wil l need to raise through alternative measures. Some of the options being considered are a 3 to 4 percent VAT on certain previously exempt goods while maintaining the exemption on certain services, such as health and education, or a progressive pensions tax. Therefore, fiscal sustainability wil l require an additional round of tax reform in the future, with content and schedule yet undetermined.

64. Expected Outcomes. These measures w i l l expand the VAT tax base from about 41 percent o f consumption in 2002 to about 59 percent by 2005," a major achievement. Regarding the corporate income tax, the phase-out of exemptions w i l l reduce them from 70 percent of potential revenue in 2003, to 50 percent in 2004, to 20 percent in 2005, and to 0 percent in 2006. An increase in subnational revenues by one-fifth i s expected. Preliminary estimates by the authorities indicate that tax collections would increase by about 1 percent of GDP in 2003 as a result of the tax package, rising to 1.2 percent o f GDP in 2004 and to 1.7 percent of GDP in 2005. Table 5 shows the observed increase in tax revenues comparing the f i rs t semester o f 2002 with the f i rs t semester of 2003.

65. Tax Administration. Even the best policy reforms would realize their goals o f greater revenue yields with fewer distortions only i f there are improvements in tax administration. This remains a major weakness in Colombia, where tax revenues are substantially below what the rates and the tax base would normally suggest.

66. The VAT and income taxes each collect only a little over 5 percent of GDP. The National Directorate o f Taxes and Customs (DIAN) i s the entity responsible for tax and customs administration. Some o f the most important areas where the tax administration needs improvement are:

.

lo Assuming that the 2 percent VAT gets restored or replaced by an equivalent measure.

20

0 Revision of the relationship with the banking system in order to standardize information flows and reduce the period during which funds are held by banks (now 14 days); Improved coverage of withholdings of interest income on individuals, now only at 7 percent and from large accounts only; Increased integration between the areas of internal revenue and customs, especially in processes such as auditing and information management; Reduced costs of enforcing compliance.

0

0

0

67. Key Policy Actions Undertaken. The DIAN has undertaken a major modernization effort and i s working hard to meet the revenue targets for 2003.'' I t has established regulations to reduce the threshold o f interest income revenue to be withheld at the source, enhanced reporting by financial institutions, established a p lan to collect tax debt, and defined indicators to monitor customs processes in Bogota and Medellin. I t has improved the cross-referencing of information with financial institutions, audited a majority of the large taxpayers that were brought into the new tax regime, established performance indicators for tax administration, and carried out over 200 integrated audits (taxes and customs), which i s well above the commitment in the policy matrix. The MHCP wi l l present to Congress a draft law to regulate the penalization o f tax evasion. Furthermore, DIAN has increased i t s auditing activities dramatically and has embarked on an ambitious modernization effort with the support o f the Govemment of Spain and the Bank. 68. Remaining Challenges. Many challenges to tax administration st i l l l ie ahead, In the medium term, DUN knows i t needs to make significant efforts in systems development, and reengineering of processes and procedures, and that improved regulations of and relationships with the banking system are necessary, which are in turn expected to yield a reduction in administrative costs per peso collected of 10 percent, a collection o f 75 percent of potential revenue from previously exempted corporate income taxes, and marked improvements in a broad set o f performance indicators. These w i l l be accomplished with the support o f FIAL I11 and IV. 69. Fiscal Responsibility. The fiscal situation in Colombia reflects the extent of excess demand on the State, i t s inability to meet those demands, and the urgency of achieving sustainable balances. A sound fiscal framework i s essential for the national security effort, for the social programs that sustain the State's legitimacy, and for the protection o f common citizens against the ravages of inflation. Achieving that w i l l require, among other things, institutional reform o f the formulation of macroeconomic policy, and close monitoring and control to meet short- and long-term fiscal targets.

70. Behind the unavoidable fiscal arithmetic b y which spending in excess of revenue has led to deficits and the accumulation of debt in Colombia, there l i e budgeting a n d fiscal management procedures that gave rise to the unsustainable fiscal tendencies. Colombia has given increasing attention, therefore, to changing i t s rules o f the game for fiscal policy at al l levels of government. Until recently, the Constitution and legal rules for budgeting and treasury have done l i t t le to restrain Central Govemment deficits a n d

In the televised cabinet meeting, DIAN announced that it had collected over 99 percent of the revenue target set for the first seven months o f 2003, which was COPI7,582,000 million.

21

debt, and in some ways they encouraged them. For example, vigencias futuras make commitment for future expenditure and the allowance for arrears based on ad hoc promises for future payment of current expenditures.

71. In the 1990s, the new Constitution broadened political participation, increased spending impulses, and weakened the tax base o f the national government (automatically sharing i t with subnational governments), all o f which compromised overall fiscal prudence. T h e Acto Legislativo (constitutional reform) o f 2001 sought to put ex ante limits on some of the spending impulse coming from transfers to subnational governments.

72. Despite these reforms, the national government believes that at all levels of government there remains too much discretion affecting fiscal deficits and not enough assurance o f fiscal sustainability. DNP evidence to this effect i s the fact that Central Government expenditures have increased steadily from 9.4 percent of GDP in 1990 to 20.8 percent of GDP in 2002.

73. The Colombian Congress approved a Fiscal Responsibility Law (FRL) in June 2003 that sets the stage for fiscal sustainability. After several rounds o f revisions and consultations with the Bank, the bill was enacted into law. The bill had been discussed within the government and Congress since the previous administration, and it came through Congress without any ad hoc amendments or cumbersome transition clauses. The FRL contains rules for fiscal stability, transparency and macroeconomic consistency, fiscal discipline, and subnational debt l i m i t s that reinforce and expand the measures previously taken with Law 617. The Law contains rules for (a) setting fiscal targets linked to debt sustainability and primary balance for the Non-Financial Public Sector (NFPS); (b) publication o f the financial plan; (c) annual reports of fiscal results to Congress; and (d) the obligation to include the fiscal impact and source o f financing within any new law that affects taxes or expenditures.