for personal use only - asx · 2017-02-15 · markets australia emerging markets frontier markets...

TRANSCRIPT

For

per

sona

l use

onl

y

Investment updateFebruary 2017

For

per

sona

l use

onl

y

DisclaimerThis presentation has been prepared by Walsh & Company Asset Management Pty Limited as Investment Manager of the Emerging Markets Masters Fund (Fund).

The information in this presentation is of a general nature and does not purport to be complete, nor does it contain all information which would be required in a

product disclosure statement (PDS) prepared in accordance with the requirements of the Corporations Act.

An investment in units of the Fund is subject to various risks, many of which are beyond the control of the Investment Manager. The past performance of the Fund is

not a guarantee of the future performance of the Fund.

This presentation contains statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those

assumptions may or may not prove to be correct. None of the Responsible Entity, the Investment Manager, their respective officers, employees, agents, advisers nor

any other person named in this presentation makes any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the

assumptions upon which they are based.

This presentation may contain general advice. Any general advice provided has been prepared without taking into account your objectives, financial situation or

needs. Before acting on the advice, you should consider the appropriateness of the advice with regard to your objectives, financial situation and needs. Where the

presentation relates to the purchase of a particular product, you should obtain a copy of the relevant product disclosure statement or offer document before making

any decisions in relation to the product.

Any opinions expressed reflect the Fund’s position at the date of this presentation and are subject to change. The information is taken from sources which are

believed to be accurate, but the Responsible Entity accepts no liability of any kind to any person who relies on the information contained in this presentation. Unless

expressly stated, none of the information should be taken to be a recommendation. You are acting independently at your own risk.

To the extent permitted by law, the Responsible Entity, the Investment Manager or their respective officers, employees, agents and advisers give no warranty,

representation or guarantee as to the accuracy or completeness or reliability of the information contained in this presentation. Further, none of the Responsible

Entity, the Investment Manager or their respective officers, employees, agents and advisers accept, except to the extent permitted by law, responsibility for any loss,

claim, damages, costs or expenses arising out of, or in connection with, the information contained in this presentation. Any recipient of this presentation should

independently satisfy themselves as to the accuracy of all information contained herein.

MSCI indices source: MSCI. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied

warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all

warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any such data. Without limiting any of the

foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any

direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution

or dissemination of the MSCI data is permitted without MSCI’s express written consent.

3 Investor update 2017

For

per

sona

l use

onl

y

Walsh & Company

Asset Management

• Walsh & Co is a Sydney-based specialist global fund manager

co-founded by Max Walsh in 2007

• Walsh & Co has approximately A$3.1 billion client assets under

management across global equities, residential and commercial

property, private equity, fixed income, and sustainable and social

investments

• We believe the best investment opportunities are often not readily

accessible to investors. We provide investors with access to market

segments that are often beyond reach, helping them build high quality

diversified portfolios

• Offices in Australia and New York

4 Investor update 2017

For

per

sona

l use

onl

y

Emerging Markets Masters Fund

• Diversified approach to emerging market equity investing,

through a multi-manager approach

• Differentiated exposure – over 60% of underlying portfolio

holdings not represented in the MSCI Emerging Markets Index.

Significant exposure to frontier markets

• Solid performance since launch

• Oversight by highly experienced, majority independent advisory

board

• Focus on emerging middle class

5 Investor update 2017

For

per

sona

l use

onl

y

1. 2016 Review

For

per

sona

l use

onl

y

2016 – a year of rotation

• Chinese stabilisation after concerns over debt and capital

outflows

• Recovery of energy and commodity prices

• Significant dispersion across country and sector returns

– Commodity and energy dependent markets (Brazil and

Russia) performed best

• Significant style rotation

– Recovery of cyclicals and value stocks

– Quality and growth lagged

• India demonetisation caused short-term shock

7 Investor update 2017

For

per

sona

l use

onl

y

2. Emerging market

considerations

For

per

sona

l use

onl

y

-4

-2

0

2

4

6

8

10

1987 1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

GD

P g

row

th (

%yo

y)

Developed Markets Emerging Markets

3.4

EM economies have grown faster

than DM

Source: IMF World Economic Outlook October 2016

2.6

9 Investor update 2017

For

per

sona

l use

onl

y

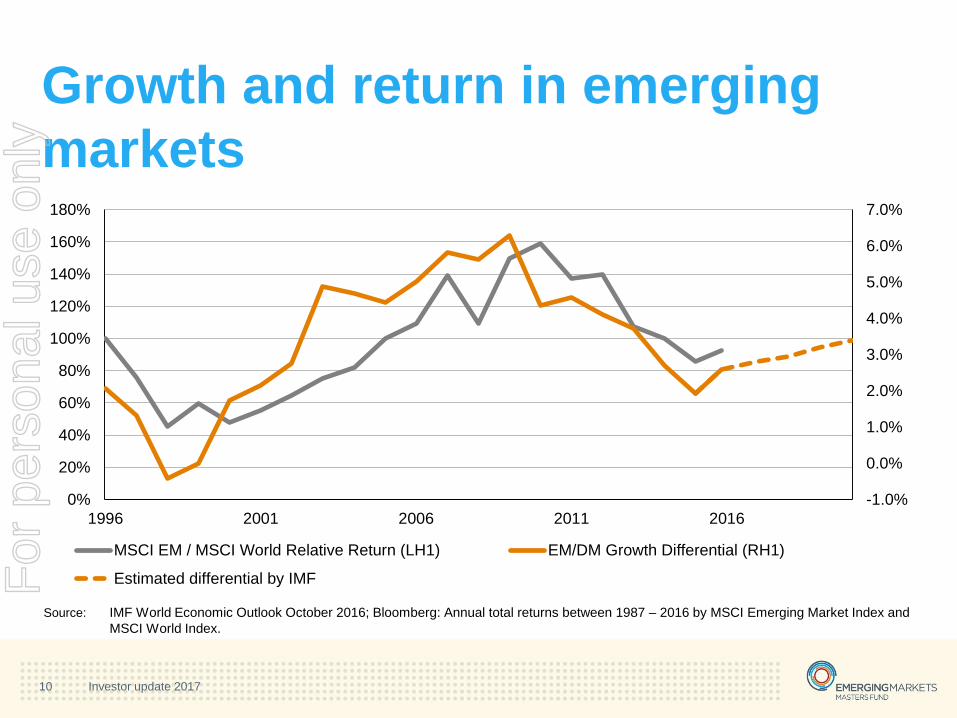

Growth and return in emerging

markets

Source: IMF World Economic Outlook October 2016; Bloomberg: Annual total returns between 1987 – 2016 by MSCI Emerging Market Index and

MSCI World Index.

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

1996 2001 2006 2011 2016

MSCI EM / MSCI World Relative Return (LH1) EM/DM Growth Differential (RH1)

Estimated differential by IMF

10 Investor update 2017

For

per

sona

l use

onl

y

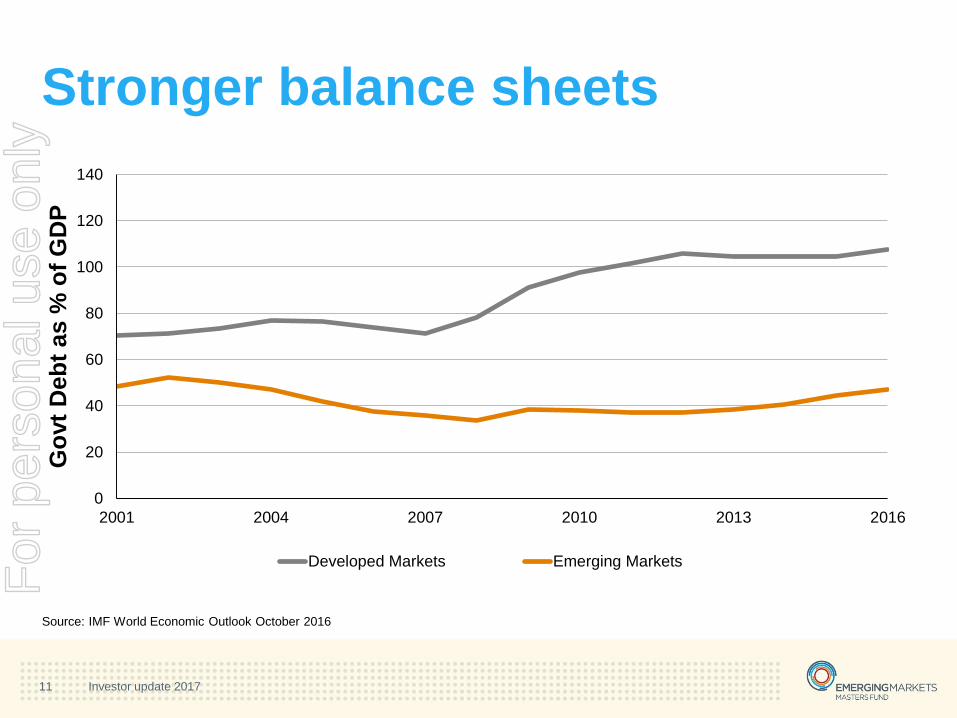

Stronger balance sheets

Source: IMF World Economic Outlook October 2016

0

20

40

60

80

100

120

140

2001 2004 2007 2010 2013 2016

Go

vt

Deb

t as %

of

GD

P

Developed Markets Emerging Markets

11 Investor update 2017

For

per

sona

l use

onl

y

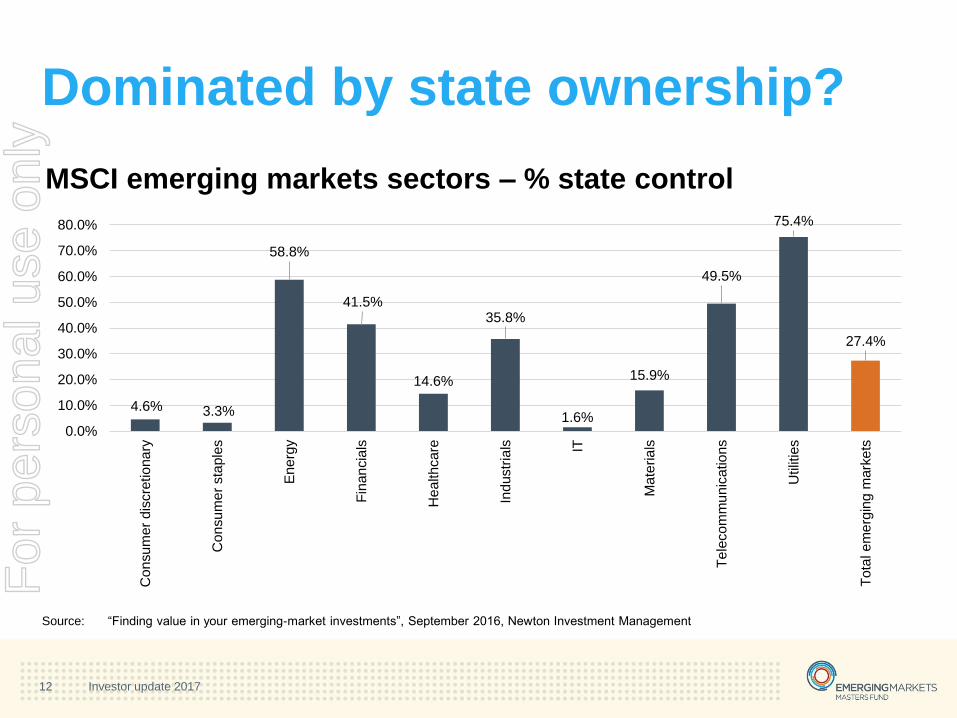

MSCI emerging markets sectors – % state control

Source: “Finding value in your emerging-market investments”, September 2016, Newton Investment Management

Dominated by state ownership?

12 Investor update 2017

4.6% 3.3%

58.8%

41.5%

14.6%

35.8%

1.6%

15.9%

49.5%

75.4%

27.4%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Co

nsu

me

r d

iscre

tio

na

ry

Co

nsu

me

r sta

ple

s

En

erg

y

Fin

an

cia

ls

He

alth

care

Ind

ustr

ials IT

Ma

teria

ls

Te

leco

mm

un

ica

tio

ns

Utilit

ies

To

tal e

me

rgin

g m

ark

ets

For

per

sona

l use

onl

y

Emerging markets leapfrogging

developed markets in usageCountries with the largest % of internet users that

shop online

0%

10%

20%

30%

40%

50%

60%

70%

80%

China Germany SouthKorea

India Brazil UK Ireland Turkey Taiwan Indonesia

Source: eMarket Services, 2015

13 Investor update 2017

For

per

sona

l use

onl

y

Source: Raghuram Rajan, Former

Governor of the Reserve

Bank of India. Image IMF.

Source: Elvira Nabiullina, Economist and

Head of the Central Bank of Russia.

WTO. Photo: Studio Casagrande (Jay

Louvion/Kryvosheiev Nikita).

Source: Sri Mulyani Indrawati, Finance Minister of

Indonesia. Image by Patrick Tsui/FCO.

Reform

14 Investor update 2017

For

per

sona

l use

onl

y

Key takeaways

The reality is more nuanced than the press would have

you believe

Disposable income growth is driving changes in behaviour

Requires specialist knowledge …and a dynamic approach to

managing strategy

Invest in these markets with professionals who know the market

well

15 Investor update 2017

For

per

sona

l use

onl

y

3. Outlook

For

per

sona

l use

onl

y

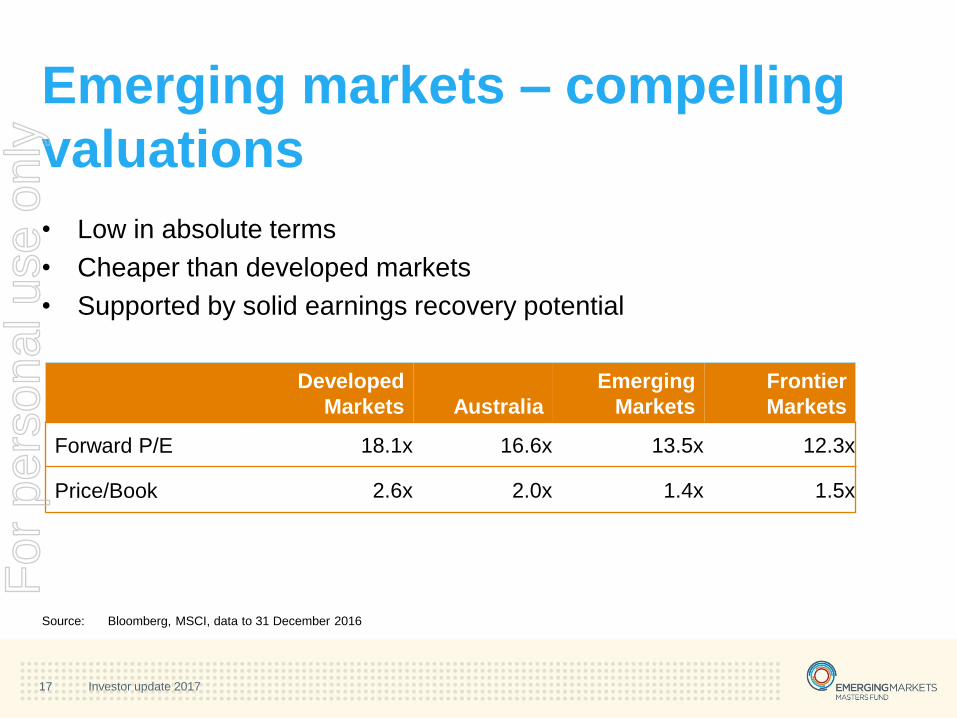

Developed

Markets Australia

Emerging

Markets

Frontier

Markets

Forward P/E 18.1x 16.6x 13.5x 12.3x

Price/Book 2.6x 2.0x 1.4x 1.5x

Emerging markets – compelling

valuations

• Low in absolute terms

• Cheaper than developed markets

• Supported by solid earnings recovery potential

Source: Bloomberg, MSCI, data to 31 December 2016

17 Investor update 2017

For

per

sona

l use

onl

y

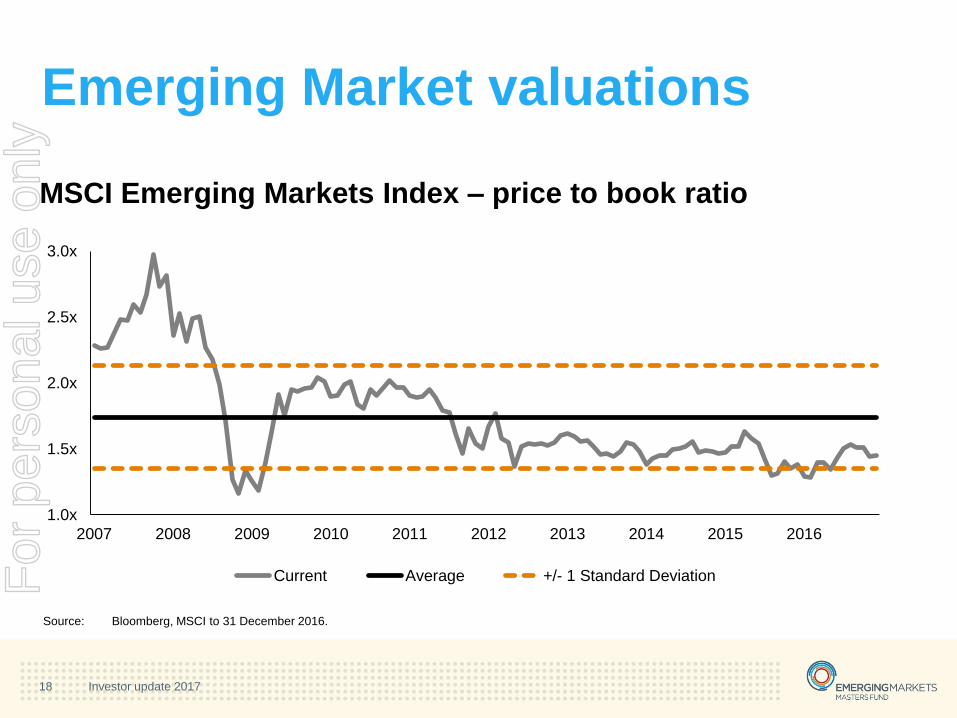

Emerging Market valuations

Source: Bloomberg, MSCI to 31 December 2016.

1.0x

1.5x

2.0x

2.5x

3.0x

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Current Average +/- 1 Standard Deviation

MSCI Emerging Markets Index – price to book ratio

18 Investor update 2017

For

per

sona

l use

onl

y

Frontier markets

• >20% of EMF is invested in frontier markets

• Unique underlying exposure – otherwise extremely difficult for retail

investors to access

• Uncorrelated markets

• Inefficient, providing great opportunities for active management

Correlations FM EM World

MSCI Frontier Markets Index 1

MSCI Emerging Markets Index 0.84 1

MSCI World Index 0.37 0.84 1

Source: Bloomberg, Walsh & Co. Asset Management, MSCI data (correlation calculated based on index weekly gross returns from May

2002 to Dec 2016

19 Investor update 2017

For

per

sona

l use

onl

y

Emerging Market Outlook

• Trump – Volatility and uncertainty

• Key risks are China and Mexico

• Domestic focused markets should be more resilient to Trump

risks

• Improving fundamentals

• Reforms – mixed picture short-term, but long-term positive

• Focus on domestic demand

• Expect significant divergence across emerging markets

• Frontier markets continue to look compelling

20 Investor update 2017

For

per

sona

l use

onl

y

4. Appendix

For

per

sona

l use

onl

y

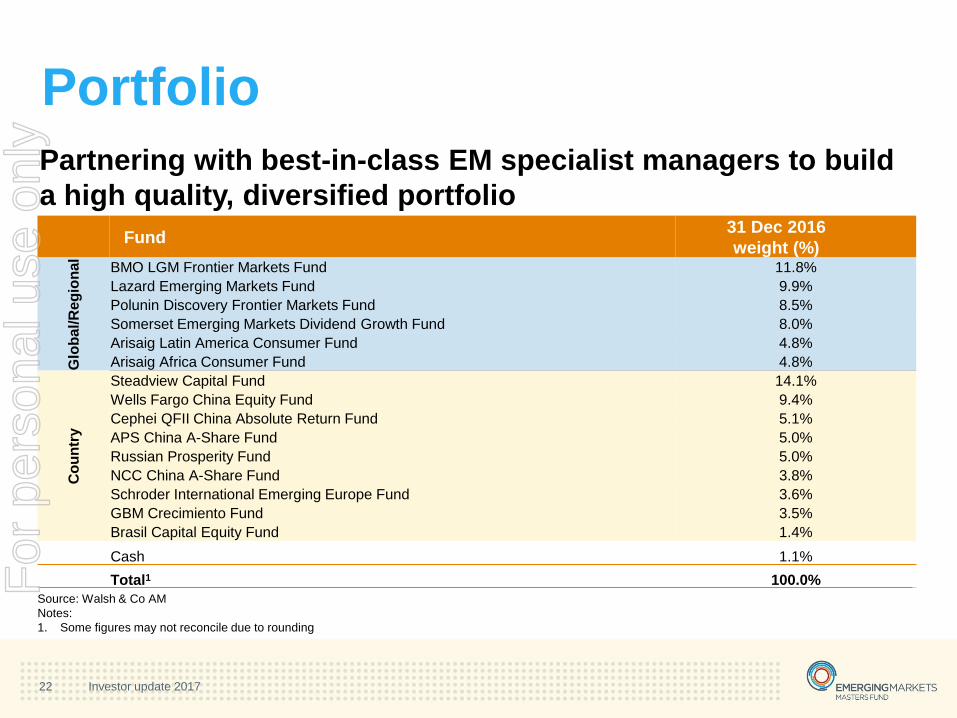

Portfolio

Fund31 Dec 2016

weight (%)

Glo

ba

l/R

eg

ion

al

BMO LGM Frontier Markets Fund 11.8%

Lazard Emerging Markets Fund 9.9%

Polunin Discovery Frontier Markets Fund 8.5%

Somerset Emerging Markets Dividend Growth Fund 8.0%

Arisaig Latin America Consumer Fund 4.8%

Arisaig Africa Consumer Fund 4.8%

Co

un

try

Steadview Capital Fund 14.1%

Wells Fargo China Equity Fund 9.4%

Cephei QFII China Absolute Return Fund 5.1%

APS China A-Share Fund 5.0%

Russian Prosperity Fund 5.0%

NCC China A-Share Fund 3.8%

Schroder International Emerging Europe Fund 3.6%

GBM Crecimiento Fund 3.5%

Brasil Capital Equity Fund 1.4%

Cash 1.1%

Total1 100.0%

Source: Walsh & Co AM

Notes:

1. Some figures may not reconcile due to rounding

Partnering with best-in-class EM specialist managers to build

a high quality, diversified portfolio

22 Investor update 2017

For

per

sona

l use

onl

y

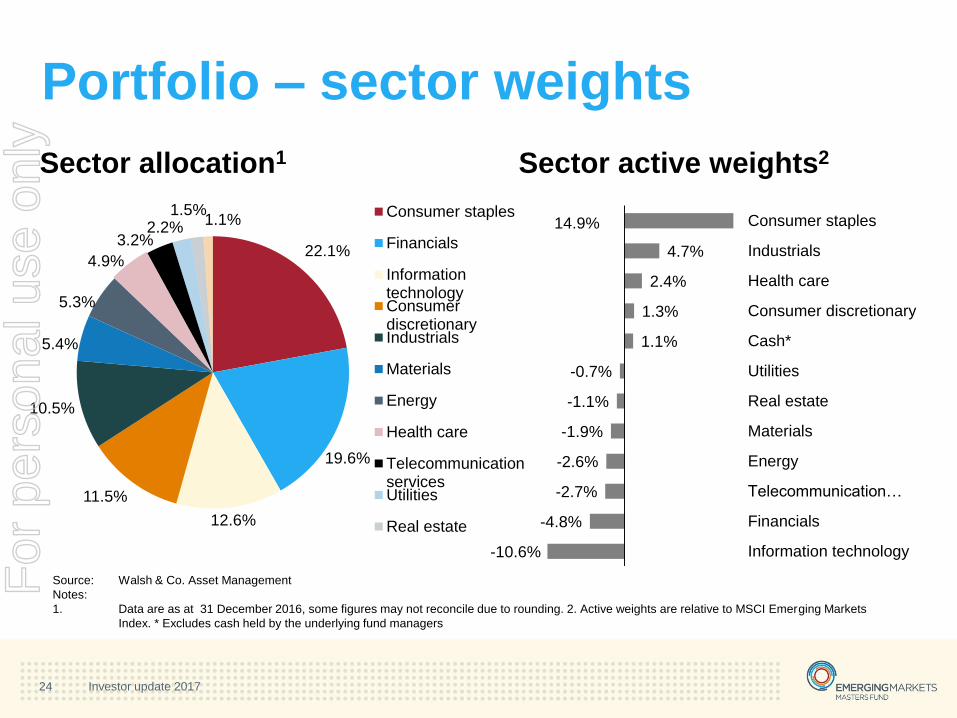

Source: Walsh & Co. Asset Management

Notes:

1. Data are as at 31 December 2016, some figures may not reconcile due to rounding. 2. Active weights are relative to MSCI Emerging Markets Index. *

Excludes cash held by the underlying fund managers

24.2%

21.7%16.3%

15.9%

7.8%

5.8%

4.6%2.5% 1.1%

China

Frontier

India

Other

Russia

Mexico

Brazil

South Africa

Cash* -26.4%

-4.6%

-3.0%

-2.3%

1.1%

2.2%

3.3%

7.9%

21.7%

Other

South Africa

Brazil

China

Cash*

Mexico

Russia

India

Frontier

Portfolio – country weights

Country allocation1 Country active weights2

23 Investor update 2017

For

per

sona

l use

onl

y

Source: Walsh & Co. Asset Management

Notes:

1. Data are as at 31 December 2016, some figures may not reconcile due to rounding. 2. Active weights are relative to MSCI Emerging Markets

Index. * Excludes cash held by the underlying fund managers

-10.6%

-4.8%

-2.7%

-2.6%

-1.9%

-1.1%

-0.7%

1.1%

1.3%

2.4%

4.7%

14.9%

Information technology

Financials

Telecommunication…

Energy

Materials

Real estate

Utilities

Cash*

Consumer discretionary

Health care

Industrials

Consumer staples

22.1%

19.6%

12.6%

11.5%

10.5%

5.4%

5.3%

4.9%

3.2%2.2%

1.5%1.1%

Consumer staples

Financials

InformationtechnologyConsumerdiscretionaryIndustrials

Materials

Energy

Health care

TelecommunicationservicesUtilities

Real estate

Portfolio – sector weights

Sector allocation1 Sector active weights2

24 Investor update 2017

For

per

sona

l use

onl

y

Consumer exposure

25 Investor update 2017

For

per

sona

l use

onl

y

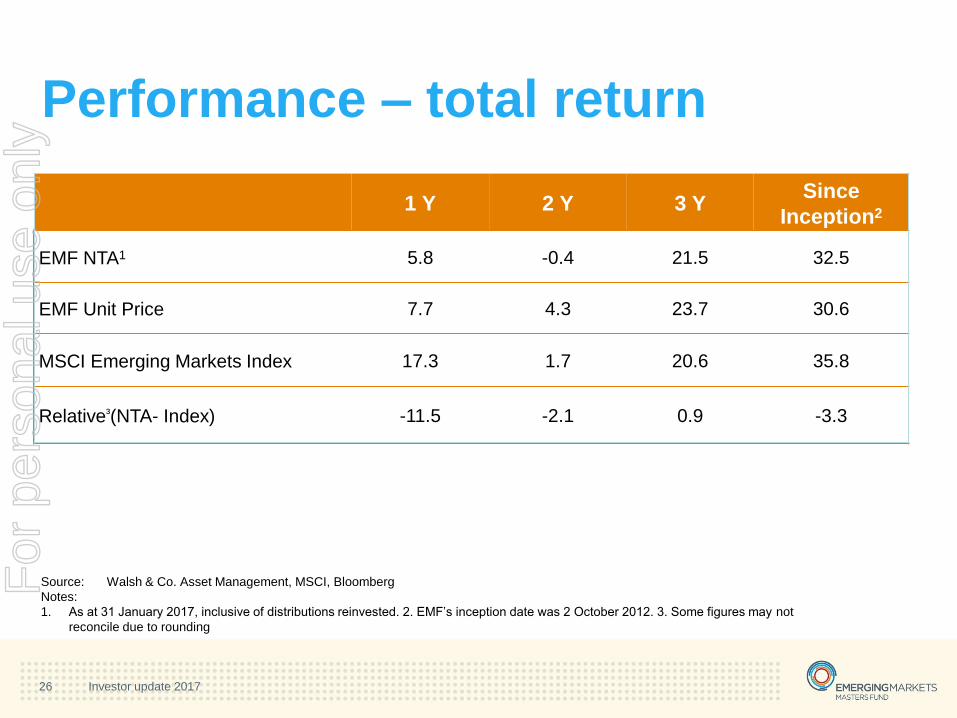

1 Y 2 Y 3 YSince

Inception2

EMF NTA1 5.8 -0.4 21.5 32.5

EMF Unit Price 7.7 4.3 23.7 30.6

MSCI Emerging Markets Index 17.3 1.7 20.6 35.8

Relative³(NTA- Index) -11.5 -2.1 0.9 -3.3

Source: Walsh & Co. Asset Management, MSCI, Bloomberg

Notes:

1. As at 31 January 2017, inclusive of distributions reinvested. 2. EMF’s inception date was 2 October 2012. 3. Some figures may not

reconcile due to rounding

Performance – total return

26 Investor update 2017

For

per

sona

l use

onl

y

Performance commentary

• Significant dispersion of returns made 2016 challenging

• Domestic Chinese (A-shares) and Indian exposure weighed on

performance

• Lack of exposure to cyclical markets such as Brazil was a

missed opportunity

• Index returns driven by cyclical sectors, Energy & Materials,

sectors which EMF has limited exposure to

• Frontier markets made a small positive contribution

27 Investor update 2017

For

per

sona

l use

onl

y

Emerging Markets

Masters Fund

Contact

Adam Coughlan - Head of Distribution

T 02 8662 9792 | M 0418 653 560 | W walshandco.com.au

28 Investor update 2017

For

per

sona

l use

onl

y