for the period may 14, 2018 may 18, 2018 · sbp approval sought for meezan ank’s ... karachi 1 ....

TRANSCRIPT

The Week in Review For the period May 14, 2018 – May 18, 2018

News This Week

Foreign exchange: SBP's reserves plunge 3.26% to USD10.8bn

FDI increases 2.4% to USD2.24bn in 10 months

Services sector exports fall 11% in nine months

Bank borrowings rise by 15.6%

To service maturing debt, Pakistan to borrow PKR22trn in FY19

Auto sales soar 40% in April; Suzuki hits record

Banks allowed to finance USD940mn telecom towers deal

SBP approval sought for Meezan Bank’s stake sale

KSE-100 – Volumes dry up amid Ramadan

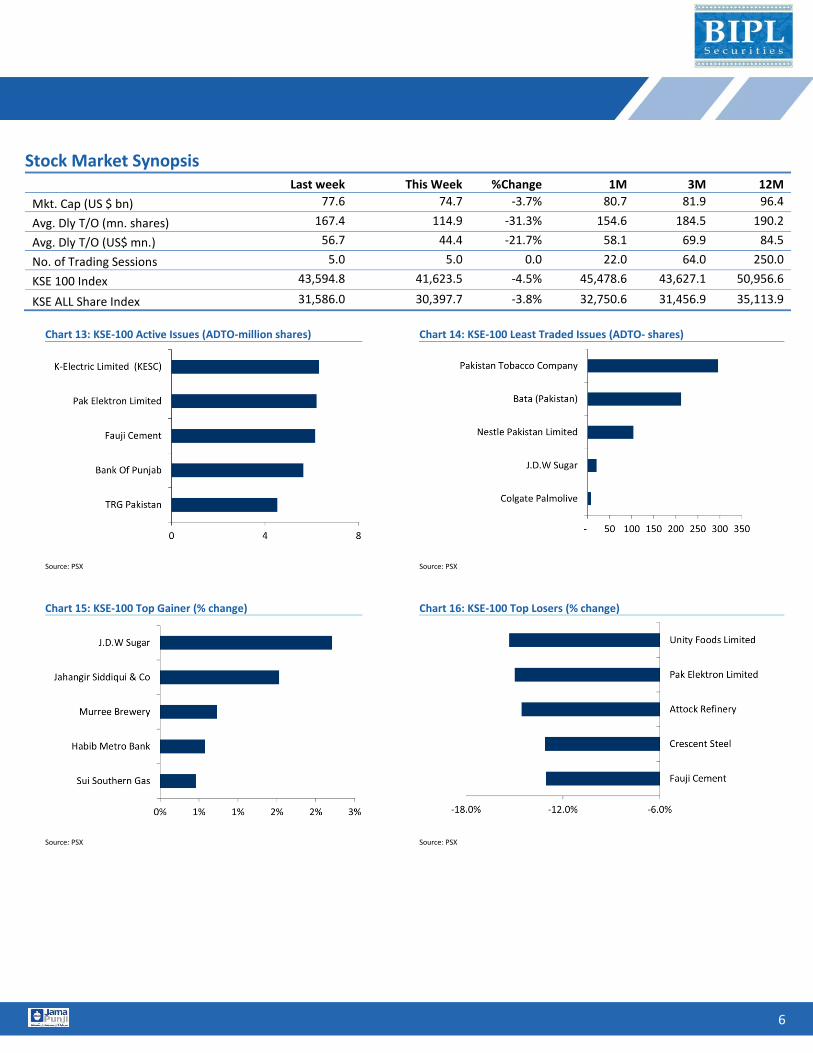

Stock Market Overview

The benchmark index continued its negative momentum throughout the week as political noise in the country rose given Civil-Military tensions over ousted PM's remarks. Moreover, persistent foreign selling, uncertainty over macroeconomics and lack of positive triggers led to the broader market meltdown whereby index settled down at 41,624pts, a decrease of 4.5%WoW. Resultantly, market participation exhibited a decline of 31%WoW and 22%WoW in ADT and ADTV, respectively. Additionally, foreign investors exhibited a net outflow of USD20mn.

JDWS, JSCL, MUREB, HMB and SSGC were the major gainers while UNITY, PAEL, ATRL, CSAP, and FCCL were the major losers in the benchmark KSE-100 this week.

REP 039 BIPL Securities Limited 5thFloor, Trade Centre, I.I. Chundrigar Road, Karachi 1

www.jamapunji.pk

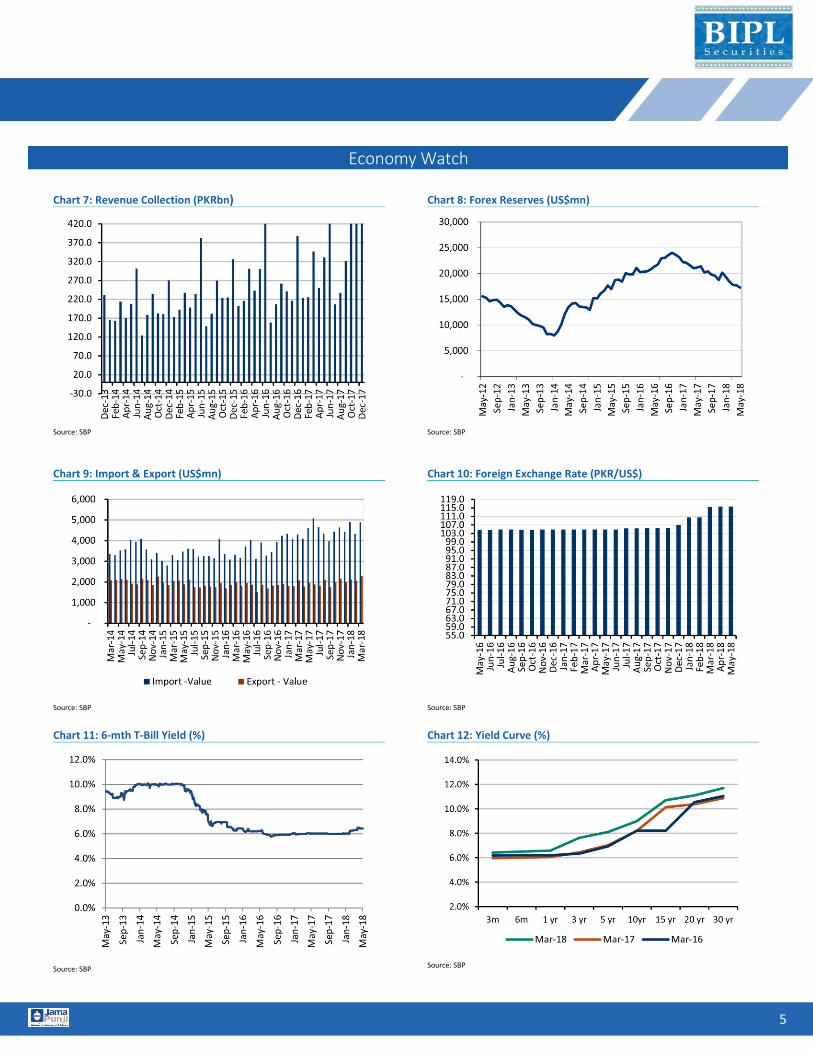

Market Review The benchmark index continued its negative momentum throughout the week as political noise in the country rose given Civil-Military tensions over ousted PM's remarks. Moreover, persistent foreign selling, uncertainty over macroeconomics and lack of positive triggers led to the broader market meltdown whereby index settled down at 41,624pts, a decrease of 4.5%WoW. Resultantly, market participation exhibited a decline of 31%WoW and 22%WoW in ADT and ADTV, respectively. Additionally, foreign investors exhibited a net outflow of USD20mn. During the week, PAMA released automobiles data for Apr’18 that clocked in at 25,567 units, posting a growth of 40%YoY/14%MoM. Furthermore, Edotco Pakistan Private Limited (Edotco PK) successfully obtained approval from the SBP, allowing local lenders to fund the acquisition of 13,000 tower by Edotco currently under Deodar Private Limited (Deodar). On the macro front, country’s foreign exchange reserves held by SBP decreased to USD10.8bn, down by 3.3%WoW, owing to the external debt servicing. Pakistan’s external debt soared to USD91.8bn as of Mar’18 which suggests that the figure may touch USD100bn as the country faces grave challenges in meeting growing external financing requirements. On the other hand, foreign direct investment (FDI) in Pakistan increased by 2.4%YoY to USD2.2bn in 10MFY18 mainly on the back of energy and construction projects.

Outlook We expect political situation to take the front seat and dictate the market direction. Furthermore, market participation is expected to remain dull during the month of Ramadan. Moreover, we expect status quo monetary policy which is due to be released next week.

KSE-100 – Volumes dry up amid Ramadan

Date Open High Low Close Change Vol (mn)

14-May-18 43,516 43,595 42,431 42,499 -2.5% 176

15-May-18 42,510 42,608 41,845 42,460 -0.1% 181

16-May-18 42,483 42,580 42,199 42,301 -0.4% 78

17-May-18 42,273 42,301 41,834 41,870 -1.0% 57

18-May-18 41,887 41,974 41,458 41,624 -0.6% 83

2 2

3

News This Week

Economic highlights & Data points

Foreign exchange: SBP's reserves plunge 3.26% to USD10.8bn| (Tribune): Foreign exchange reserves held by the State Bank of Pakistan (SBP) again came under pressure, falling 3.26% on a weekly basis, according to data released by the central bank on Thursday. On May 11, foreign currency reserves held by the central bank were recorded at USD10.8bn, down USD364.1mn or 3.26% compared with USD11.2bn in the previous week. FDI increases 2.4% to USD2.24bn in 10 months| (The News): : Foreign direct investment (FDI) in Pakistan increased 2.4% to USD2.24bn in 10MFY18, the central bank data showed on Tuesday, mainly on the back of energy and construction projects. Services sector exports fall 11% in nine months| (The News): Pakistan’s exports of services declined 11% to USD3.86bn during the 9MFY18, the Pakistan Bureaus of Statistics (PBS) said. Services exports stood at USD4.31bn in the corresponding period last year. In 9MFY18, services sector’s imports surged 7.17% to USD7.71bn. Trade deficit in services increased 34% to USD3.84bn during the nine-month period, according to PBS. Bank borrowings rise by 15.6%| (Dawn): According to the weekly statement of position of all scheduled banks for the week ended April 27, 2018 deposits and other accounts of all scheduled banks stood at PKR12,276bn after a 0.74% decrease over the preceding week’s figure of PKR12,186bn. Compared with last year’s corresponding figure of PKR11,214bn, the current week’s figure was higher by 9.47%. To service maturing debt, Pakistan to borrow PKR22trn in FY19| (Tribune): As the country falls deeper into payments obligation, the federal government has sought the National Assembly’s approval to borrow a record PKR22trn in the next financial year to serv ice its maturing public debt, an amount 44% or PKR6.7trn higher than the figure for the ongoing year.

Sector and Corporate highlights

Auto sales soar 40% in April; Suzuki hits record| (The News): Automakers on Friday reported robust sales growth in April, with Suzuki posting a record for monthly sales, as low cost consumer finance and high demand from ride-hailing services pulled buyers into showrooms. Auto sales jumped 40% in the month of April 2018 compared to the same period last fiscal, Pakistan Automotive Manufacturers Association (PAMA) data showed. Banks allowed to finance USD940mn telecom towers deal| (The News): The central bank allowed local lenders to fund a joint venture firm between a Malaysian telco and a local conglomerate to acquire an estimated USD940mn worth of telecom towers in Pakistan. “Edotco Pakistan Private Limited (Edotco PK) has successfully obtained approval from the State Bank of Pakistan (SBP), allowing local lenders to fund the acquisition by Edotco PK of Jazz’s portfolio of 13,000 tower assets currently under Deodar Private Limited (Deodar),” SBP approval sought for Meezan Bank’s stake sale| (The News): Kuwait-based Noor Financial Investment Company (NFIC) plans to sell 9.59% of its 49.1% stake in Meezan Bank Limited (MEBL), seeking approval from the State Bank of Pakistan, a statement said Wednesday. The MEBL in statement to Pakistan Stock Exchange said the company owns 522.03mn shares in the bank representing 49.1% of the issued and paid-up capital, lying in a blocked account maintained by Central Depository Company (CDC).

4

Stock Market – Last week in pictorals

Chart 1: KSE-100 Index

Source: PSX

Chart 2: KSE Advance/Decline Ratio

Source: PSX

Chart 3: Pak Foreign Portfolio Flows (US$mn; US$=PKR115)

Source: NCCPL

Chart 4: KSE- Volumes & Values

Source: PSX

Chart 5: Price to Money Ratio

Source: NCCPL

Chart 6: Off market activity

Source: PSX

Economy Watch

Chart 7: Revenue Collection (PKRbn)

Source: SBP

Chart 8: Forex Reserves (US$mn)

Source: SBP

Chart 9: Import & Export (US$mn)

Source: SBP

Chart 10: Foreign Exchange Rate (PKR/US$)

Source: SBP

Chart 11: 6-mth T-Bill Yield (%)

Source: SBP

Chart 12: Yield Curve (%)

Source: SBP

5

Stock Market Synopsis Last week This Week %Change 1M 3M 12M

Mkt. Cap (US $ bn) 77.6 74.7 -3.7% 80.7 81.9 96.4

Avg. Dly T/O (mn. shares) 167.4 114.9 -31.3% 154.6 184.5 190.2

Avg. Dly T/O (US$ mn.) 56.7 44.4 -21.7% 58.1 69.9 84.5

No. of Trading Sessions 5.0 5.0 0.0 22.0 64.0 250.0

KSE 100 Index 43,594.8 41,623.5 -4.5% 45,478.6 43,627.1 50,956.6

KSE ALL Share Index 31,586.0 30,397.7 -3.8% 32,750.6 31,456.9 35,113.9

Chart 13: KSE-100 Active Issues (ADTO-million shares)

Source: PSX

Chart 14: KSE-100 Least Traded Issues (ADTO- shares)

Source: PSX

Chart 15: KSE-100 Top Gainer (% change)

Source: PSX

Chart 16: KSE-100 Top Losers (% change)

Source: PSX

6

Disclaimer

This research report is for information purposes only and does not constitute nor is it intended as an offer or solicitation for the purchase or sale of securities or other financial instruments. Neither the

information contained in this research report nor any future information made available with the subject matter contained herein will form the basis of any contract. Information and opinions contained

herein have been compiled or arrived at by BIPL Securities Limited from publicly available information and sources that BIPL Securities Limited believed to be reliable. Whilst every care has been taken in

preparing this research report, no research analyst, director, officer, employee, agent or adviser of any member of BIPL Securities Limited gives or makes any representation, warranty or undertaking,

whether express or implied, and accepts no responsibility or liability as to the reliability, accuracy or completeness of the information set out in this research report. Any responsibility or liability for any

information contained herein is expressly disclaimed. All information contained herein is subject to change at any time without notice. No member of BIPL Securities Limited has an obligation to update,

modify or amend this research report or to otherwise notify a reader thereof in the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or

subsequently becomes inaccurate, or if research on the subject company is withdrawn. Furthermore, past performance is not indicative of future results.

The investments and strategies discussed herein may not be suitable for all investors or any particular class of investor. Investors should make their own investment decisions using their own

independent advisors as they believe necessary and based upon their specific financial situations and investment objectives when investing. Investors should consult their independent advisors if they

have any doubts as to the applicability to their business or investment objectives of the information and the strategies discussed herein. This research report is being furnished to certain persons as

permitted by applicable law, and accordingly may not be reproduced or circulated to any other person without the prior written consent of a member of BIPL Securities Limited. This research report may

not be relied upon by any retail customers or person to whom this research report may not be provided by law. Unauthorized use or disclosure of this research report is strictly prohibited. Members of

BIPL Securities and/or their respective principals, directors, officers, and employees and their families may own, have positions or affect transactions in the securities or financial instruments referred

herein or in the investments of any issuers discussed herein, may engage in securities transactions in a manner inconsistent with the research contained in this research report and with respect to

securities or financial instruments covered by this research report, may sell to or buy from customers on a principal basis and may serve or act as director, placement agent, advisor or lender, or make a

market in, or may have been a manager or a co-manager of the most recent public offering in respect of any investments or issuers of such securities or financial instruments referenced in this research

report or may perform any other investment banking or other services for, or solicit investment banking or other business from any company mentioned in this research report. Investing in Pakistan

involves a high degree of risk and many persons, physical and legal, may be restricted from dealing in the securities market of Pakistan. Investors should perform their own due diligence before investing.

No part of the compensation of the authors of this research report was, is or will be directly or indirectly related to the specific recommendations or views contained in the research report. By accepting

this research report, you agree to be bound by the foregoing limitations.

BIPL Securities Limited and / or any of its affiliates, which operate outside Pakistan, do and seek to do business with the company(s) covered in this research document. Investors should consider this

research report as only a single factor in making their investment decision. BIPL Securities Limited prohibits research personnel from disclosing a recommendation, investment rating, or investment

thesis for review by an issuer/company prior to the publication of a research report containing such rating, recommendation or investment thesis.

BIPL Securities Limited endeavors to make all reasonable efforts to disseminate its publication to all eligible clients in a timely manner through either physical or electronic distribution such as mail, fax

and/or email. Nevertheless, not all clients may receive the material at the same time.