forecast 2016 - · pdf fileforecast 2016. berkadia is an ... berkadia’s 2015 loan...

TRANSCRIPT

N AT I O N A L A PA R T M E N T R E S E A R C H R E P O R T

a Berkshire Hathaway and Leucadia National company

FORECAST 2016

Berkadia is an industry-leading real estate company. We provide comprehensive capital solutions and

investment sales advisory and research services for multifamily and commercial properties, and

rank among the largest, highest rated and most respected primary, master

and special servicers in the industry.

$26 BILLIONBerkadia’s 2015 loan origination volume surpassed $20 billion, while investment sales exceeded $6 billion.

$18 BILLIONSince 2012, our investment sales division has closed more than 1,700 transactions, totaling $18 billion.

16,500 TRANSACTIONSOver 16,500 transactions financed throughout our history.

$86 BILLIONTotal historical sales by our investment sales advisors exceed $86 billion.

$235 BILLIONOne of the largest loan and servicing portfolios worldwide at $235 billion.

65 OFFICES65 offices nationwide, covering all major markets.

a Berkshire Hathaway and Leucadia National company

The Value of Certainty®

NATIONAL TRENDS 2

ALBUQUERQUE 4

ATLANTA 5

AUSTIN 6

BATON ROUGE 7

BIRMINGHAM 8

BOSTON 9

CENTRAL VALLEY | CA 10

CHARLESTON 11

CHATTANOOGA 12

CHICAGO 13

COLUMBUS 14

DALLAS-FORT WORTH 15

DENVER 16

DETROIT 17

HOUSTON 18

INLAND EMPIRE | CA 19

JACKSONVILLE 20

KANSAS CITY 21

LAS VEGAS 22

LOS ANGELES-NORTH 23

LOS ANGELES-SOUTH 24

LOS ANGELES-WEST 25

MEMPHIS 26

NEW YORK-NEW JERSEY 27

OKLAHOMA CITY 28

ORANGE COUNTY | CA 29

ORLANDO 30

PHILADELPHIA 31

PHOENIX 32

PORTLAND 33

RALEIGH-DURHAM 34

SACRAMENTO 35

SALT LAKE CITY 36

SAN ANTONIO 37

SAN DIEGO 38

SAN FRANCISCO-OAKLAND 39

SEATTLE-TACOMA 40

SOUTH FLORIDA 41

ST. LOUIS 42

TAMPA-ST. PETERSBURG 43

TUCSON 44

TULSA 45

VIRGINIA BEACH 46

WASHINGTON, D.C. 47

DISCLAIMER AND SOURCES 48

TABLE OF CONTENTS

FORECAST 2016

-4%

-2%

0%

2%

4%

-6

-4

-2

0

2

4

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

Employment Percentage Change

U.S. EMPLOYMENT GROWTH

Em

plo

ym

en

t C

han

ge (

mil) E

mp

loym

en

t Ch

an

ge

2 Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. Apartment market data criteria and methodologies vary by market.

The U.S. economy closed 2015 on a strong note with healthy late-year job creation, despite international headwinds and the milder pace of hiring earlier in the fall. National employment expanded by approximately 2.5 million jobs in 2015. Staffing additions came in lower than the 3.1 million workers added in 2014; though, rising wages indicate ancillary employment-market strength despite the dip in the headline reading. Third-quarter GDP registered a 2.1% increase, following a stout 3.9% midyear gain. The U.S. consumer buoyed the economy in the face of international distress such as weakness in the Chinese economy that is stifling emerging foreign markets. U.S. hourly wages surged 2.5% annually in October, compared to a 1.8% rise in 2014. Additionally, consumer credit notched the largest increase on record by ascending $28.9 billion in September. With healthy consumer activity expected to persist, private consumption will soften downside risks from abroad in 2016, with U.S. payrolls forecast to rise by 2.4 million jobs.

The New York-New Jersey and Dallas-Fort Worth markets again claimed the top spots in job creation in 2015, adding 119,000 and 88,900 workers, respectively. Los Angeles employers, meanwhile, hired 85,600 personnel, as the impact of plunging oil prices pushed Houston out of third place and limited gains to 16,700 positions in 2015. The San Francisco-Oakland, Salt Lake City and San Antonio markets led in percent growth, each expanding 4.2% or more last year. In 2016, the Bay Area, Austin and San Antonio are projected to lead employment gains, all on pace to rise by 2.8% or more.

ECONOMY AND APARTMENT SUPPLY

The employment-driven apartment demand was met with significant supply-side pressure last year. Developers added 355,000 market-rate units to inventory over the course of 2015, putting upward pressure on vacancy in some metros. The Dallas-Fort Worth and Houston metros led inventory expansion, registering 19,200 and 16,700 new units, respectively. Deliveries were also elevated in primary, barrier-to-entry markets, with 9,900 rentals in Washington, D.C., 9,200 apartments in the New York-New Jersey area and 7,400 units in Los Angeles. Supply growth will moderate in 2016 yet remain elevated. Builders are on pace to complete 340,000 units this year, with New York-New Jersey, Dallas-Fort Worth and Houston each adding 15,000 rentals or more.

2015 PERFORMANCE HIGHLIGHTS

0 BPS YOY

VACANCY5.2%

21.4% YOY

CONSTRUCTION355,000 UNITS

1.8% YOY

EMPLOYMENTCHANGE

2,500,000

4.9% YOY

ASKING RENTS$1,250

*Estimate | Source: Berkadia, BLS, Moody’s Analytics

0%

1%

2%

3%

4%

0

30

60

90

120

N.Y

.-N

.J.

Dal

las-

Fo

rt W

ort

h

L.A

.

Atl

anta

D.C

.

Sea

ttle

Bo

sto

n

Inla

nd E

mp

ire

So

. Flo

rid

a

Chi

cag

o

Employment Percentage Change

TOP METROS: EMPLOYMENT GROWTH

Em

plo

ym

en

t C

han

ge 2

015

(th

s)*

Em

plo

ym

en

t Ch

an

ge 2

015

*

*Estimate; **Forecast | Source: Berkadia, BLS, Moody’s Analytics

0%

2%

4%

6%

0

5

10

15

20 Units Vacancy

Dal

las-

Fo

rt W

ort

h

Ho

ust

on

D.C

.

Den

ver

Atl

anta

N.Y

.-N

.J.

Au

stin

Sea

ttle

L.A

.

So

. Flo

rid

a

TOP METROS: SUPPLY GROWTH

Un

its

Co

mp

lete

d 2

015

(th

s)*

Vaca

ncy 2

015

*

*Estimate | Source: Berkadia Research, Axiometrics

0

100

200

300

400

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

U.S. CONSTRUCTION PIPELINE

Un

its

Co

mp

lete

d (

ths)

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

NATIONAL TRENDS

3Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. Apartment market data criteria and methodologies vary by market.

0%$1,330 $2,776 $1,373 $1,598 $1,254 $1,852 $1,390 $1,088 $914 $2,250

3%

6%

9%

12%

Po

rtla

nd

Den

ver

Sea

ttle

Sac

ram

ento

San

Die

go

Inla

nd

Em

pir

e

Orl

and

o

Ph

oen

ix

Bo

sto

n

San

Fra

nci

sco

-Oak

lan

d

TOP METROS: ASKING RENT GROWTH

Ask

ing

Re

nt

Gro

wth

20

15*

VACANCY, RENTS AND INVESTMENT TRENDS

Persistent apartment absorption and job creation facilitated robust rent gains. National asking rents appreciated 4.9% to $1,250 per month in the past four quarters. Moreover, national effective rents rose at a quicker rate, ascending 5.3% to $1,244 per month. The effective rent improvement put the concessions gap at 0.5% of asking rents at year-end 2015, 50 basis points below the previous year and the lowest in a decade. With vacancy edging higher this year, operators will begin to expand renter incentives. Asking and effective rents are projected to rise 3.7% and 3.4% to $1,296 and $1,286 per month, respectively. As a result, concessions will tick up to 0.8% of asking rents by year-end.

Historically low interest rates and favorable apartment fundamentals bolstered multifamily investment activity in 2015; preliminary sales data indicates a 12% rise in the number of apartment transactions. Buyer competition was evident with the average cap rate compressing 30 basis points to 5.9% nationwide. Meanwhile, the average price increased 9% to $124,500 per unit. Demand for Class A assets was evident, though values for middle- and lower-tier communities advanced more rapidly. The average price per unit for B-grade apartments advanced 12% to $120,200, dropping first-year yields 40 basis points to an average of 5.9%. Class C pricing surged 15% to $84,200 per unit as cap rates descended 40 basis points to 6.2%. Class A initial yields receded 20 basis points to 5.4% due to the 5% rise in per-unit pricing to $187,700.

Despite the sharp rise in apartment stock, pent-up demand from previous years’ limited supply increases mitigated the impact of new units in many markets. Consequently, nationwide apartment vacancy ended 2015 at 5.2%, unchanged year over year. Operators in Detroit recorded the steepest decline in vacancy, which plunged 150 basis points to 4.6% as local builders added just 400 rentals last year. Among metros with considerable supply growth, resilient demand resulted in 80-basis-point vacancy decreases in Dallas-Fort Worth and Atlanta, to 4.3% and 5%, respectively. A second-consecutive year of steep supply additions, however, will cause U.S. apartment vacancy to tick up 10 basis points to 5.3% in 2016.

5%

6%

7%

8%

$1,000

$1,075

$1,150

$1,225

$1,300

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

Asking Rents Vacancy

U.S. VACANCY AND RENT

*Estimate; **Forecast | Source: Berkadia, Axiometrics

5.5%

6.0%

6.5%

7.0%

7.5%

$50,000

$75,000

$100,000

$125,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Price Per Unit Cap Rate

U.S. APARTMENT INVESTMENT

*Estimate; Property Sale +$5 Million and +100 Units | Source: Berkadia, CoStar Group, Inc.

*Estimate | Source: Berkadia, Axiometrics

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

N.Y

.-N

.J.

Po

rtla

nd

Sac

ram

en

to

L.A

. Ora

ng

e C

o. |

CA

So

. Flo

rid

a

Orl

and

o Dal

las

Ce

n. V

alle

y |

CA

San

Fra

nci

sco

-Oak

lan

d

2014 Vacancy 2015 Vacancy*

TOP METROS: LOWEST VACANCY

*Estimate | Source: Berkadia, Axiometrics

2016 PERFORMANCE HIGHLIGHTS

VACANCY5.3%

-4.2% YOY

CONSTRUCTION340,000 UNITS

1.7% YOY

EMPLOYMENTCHANGE

2,400,000

3.7% YOY

ASKING RENTS$1,296

10 BPS YOY

5.0%

6.0%

7.0%

8.0%

$700

$750

$800

$850

2012 2013 2014 2015* 2016**

Albuquerque payrolls expanded 1.7% in 2015, marking the fourth-consecutive year of job growth. Approximately 3,400 of the 6,500 total jobs created last year were in the professional and business services sector, supported by the new Convergys call center in Rio Rancho that hired the first of 250 workers in June. Sustained economic expansion lifted apartment demand as vacancy fell 80 basis points to 5.9%. Builders moved to satisfy this demand with 860 completions in 2015, two-thirds of which came online in the northwest quadrant of the metro. Renters gravitated to the new product as more than 50% of leasing activity occurred in the Northwest submarket. Robust apartment absorption was also present in the Southeast submarket, where vacancy plummeted 340 basis points, though asking rents dipped 0.5%. Operators took advantage of heightened demand, raising asking rents 2.5% metrowide to $826 per month.

2015 REVIEW

Limited completions and persistent leasing activity will push down multifamily vacancy in 2016. Prompted by favorable demand, multifamily developers will request permits for 410 apartments by year-end, while an additional 370 units are in various stages of the planning process. In the near term, builders are slated to deliver 180 apartments in 2016. Of those new apartments, approximately 100 units at the Broadstone Promenade in the North Central submarket are scheduled to come online by mid-year. Renters are expected to absorb 490 apartments metrowide, depressing vacancy 60 basis points to 5.3%. Rent appreciation of 2.1% is anticipated during this time, with asking rents reaching $843 per month by December. Effective rents will rise at a faster rate, 2.5% growth, to $834 per month. Consequently, concessions will fall from an average of 1.5% to 1.1% of asking rents. The improved apartment fundamentals will be supported by 1.5% employment growth as 5,800 workers are added to local payrolls. Call-center expansion will once again boost professional and business services sector employment as S&P Data LLC hires 425 workers in Rio Rancho in the next few years.

2016 PREVIEW

4

2015 PERFORMANCE HIGHLIGHTS

1.7% YOY

EMPLOYMENT6,500

2.5% YOY

ASKING RENTS$826

-80 BPS YOY

VACANCY5.9%

139.2% YOY

CONSTRUCTION860 Units

-10 BPS YOY

UNEMPLOYMENT RATE5.8%

-120 BPS YOY

CONCESSIONS1.5%

MARKET FACTS

POPULATION905,000

MEDIANHOUSEHOLD

INCOME$51,100

HOUSEHOLDS357,600

RENTSHARE OFWALLET19.4%

-15,000

-10,000

-5,000

0

5,000

10,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$50,000

$70,000

$90,000

$110,000

5.5%

6.0%

6.5%

7.0%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

500

1,000

1,500

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

400

800

1,200

2012 2013 2014 2015* 2016**

EMPLOYMENT CHANGE

YE 2015 0.1% YOY YE 2015 0.2% YOY YE 2015 1.6% YOY YE 2015 20 BPS YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

ALBUQUERQUE

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

3.5%

4.5%

5.5%

6.5%

7.5%

$800

$900

$1,000

$1,100

2012 2013 2014 2015* 2016**

Intense multifamily development and planning occurred last year amid a robust local economy. Developers requested permits for 10,000 apartments, the most since 2007. Similarly, deliveries were the greatest in seven years as builders completed 9,350 units. The brisk pace of development, however, lagged demand, causing vacancy to fall 80 basis points to 5%. Market rents increased 5.5% to $1,041 per month as operators noted reduced availability. These healthy advances in apartment fundamentals were supported by 82,200 new jobs in 2015, a 3.2% year-over-year gain. Nearly one-third of the increase came from the professional and business services sector, where 26,200 jobs were created, 5.6% expansion. Another significant contributor to growth was the trade, transportation and utilities segment with 16,600 workers recruited for a 2.9% gain. The greatest rate of growth was a 6.5% surge, with the addition of 6,700 workers in the construction industry.

2015 REVIEW

Metro employment is projected to grow 2.7% in 2016 with 71,000 new workers. Construction payrolls will expand with approximately 5,000 jobs at the Atlanta Braves SunTrust Park development. Another 5,000 workers will be added through corporate expansions from State Farm, Mercedes-Benz, Kaiser Permanente, Stefanini and Sage Group over the next several years. The aggressive hiring will push down vacancy 50 basis points this year. Asking rents are expected to rise 4.7% to $1,090 per month. The favorable conditions will continue to attract investors in 2016. The most aggressive buyers will look to Gwinnett and Cobb counties, where cap rates are in the high-5% to high-6% range, depending on location and quality. Additionally, many Class B/C investors seek value-add properties among 1970s- through 1990s-vintage stock, where cap rates are compressing. Properties built in the 1970s and 1980s are frequently trading with cap rates in the mid-6% range, while 1990s inventory is averaging roughly 5.5%. Meanwhile, conservative investors are targeting Class A product in Buckhead and Midtown, often at first-year yields below 5%.

2016 PREVIEW

5

2015 PERFORMANCE HIGHLIGHTS

5.5% YOY

3.2% YOY

EMPLOYMENT82,200

ASKING RENTS$1,041

-80 BPS YOY

VACANCY5.0%

63.5% YOY

CONSTRUCTION9,350 Units

-100 BPS YOY

UNEMPLOYMENT RATE5.3%

-40 BPS YOY

CONCESSIONS0.4%

MARKET FACTS

POPULATION5,763,700

MEDIANHOUSEHOLD

INCOME$58,900

HOUSEHOLDS2,119,600

RENTSHARE OFWALLET21.2%

-150,000

-100,000

-50,000

0

50,000

100,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$30,000

$50,000

$70,000

$90,000

6.0%

6.5%

7.0%

7.5%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

400

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

4,000

8,000

12,000

2012 2013 2014 2015* 2016**

YE 2015 1.8% YOY YE 2015 2.0% YOY YE 2015 2.6% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 60 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

ATLANTA

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

3.5%

4.0%

4.5%

5.0%

$1,000

$1,050

$1,100

$1,150

$1,200

$1,250

2012 2013 2014 2015* 2016**

Austin employers accelerated hiring in 2015, driving apartment demand. Headcounts swelled 3.7%, or by 34,200 positions, in the prior four quarters, up from a 3.2% increase in 2014. The local rise outpaced the 1.8% national average during the last 12 months. The metro-leading 10,300 positions created in the professional and business services sector contributed to the upswing. With steady population growth and more job opportunities, household formation rose 2.9% in 2015. As a result, occupied stock grew by 8,750 apartments in 2015, the highest annual absorption in more than 15 years. Leasing exceeded the 8,590 deliveries since January, resulting in vacancy tightening 30 basis points to 4.6%. Heightened demand for apartments spurred operators to accelerate rent growth. After rising 3.8% in 2014, asking rents advanced 4.4% to $1,154 per month in December. Simultaneously, average concessions lowered from 0.5% to 0.3% of asking rents.

2015 REVIEW

With unemployment dropping below 3% in 2015, Austin is nearing full employment this year. As such, hiring will decelerate, though remain healthy in 2016. Headcounts are forecast to rise by 27,800 positions for a 2.9% increase. Technology companies will provide a boost to the metro, highlighted by the scheduled completion of the $304 million expansion of the Apple campus this year. The 1.1 million-square-foot addition will hold 3,600 more employees. The campus growth will help drive demand in the Far Northwest submarket, where vacancy fell 30 basis points to 4.9% last year and should continue to lower as limited new inventory comes online in 2016. Overall, vacancy is expected to decrease 20 basis points to 4.4% by December as elevated demand surpasses additions. Of the 8,010 apartments scheduled to come online this year, the largest community is the 444-unit Pearl Lantana in the West submarket. Operators will advance rents at a healthy clip, while moderately increasing concessions amid greater competition for renters. Asking rents will rise 4.3% to $1,204 per month in 2016 as concessions reach an average of two days of free rent.

2016 PREVIEW

6

2015 PERFORMANCE HIGHLIGHTS

3.7% YOY

EMPLOYMENT34,200

4.4% YOY

ASKING RENTS$1,154

-30 BPS YOY

VACANCY4.6%

8.2% YOY

CONSTRUCTION8,590 Units

-90 BPS YOY

UNEMPLOYMENT RATE2.9%

-20 BPS YOY

CONCESSIONS0.3%

MARKET FACTS

POPULATION2,031,600

MEDIANHOUSEHOLD

INCOME$65,200

HOUSEHOLDS770,000

RENTSHARE OFWALLET21.2%

-20,000

0

20,000

40,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY PERMITS AND DELIVERIES

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$50,000

$75,000

$100,000

$125,000

5.5%

6.0%

6.5%

7.0%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

400

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

YE 2015 3.0% YOY YE 2015 2.9% YOY YE 2015 1.9% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

0

4,000

8,000

12,000

2012 2013 2014 2015* 2016**

YE 2015 50 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

AUSTIN

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

4.0%

6.0%

8.0%

10.0%

$1,000

$1,025

$1,050

$1,075

$1,100

2012 2013 2014 2015* 2016**

Companies in Baton Rouge advanced headcounts by 10,400 workers last year, an increase of 2.6%. The construction industry added 3,600 workers, a 6.9% gain. Supporting the robust sector hiring was a significant number of industrial projects that progressed in 2015, including the $55 million IBM Technology Center, Thermaldyne’s $19 million waste remediation facility and the $45 million Water Campus project. Employment gains were also brisk among the professional and business services sector which expanded payrolls by 4,000 employees. Multifamily builders, attempting to take advantage of the surging economic development, stepped up supply, delivering 360 apartments. However, positive net absorption fell to 300 units last year. Consequently, vacancy edged up 10 basis points annually to 5.7% in December. Operators advanced asking rents, nevertheless, up 2.1% to $1,063 per month.

2015 REVIEW

Employment growth is forecast to reach 2.1% with 8,600 job additions by year-end. Shintech expects to break ground in the second quarter on a $1.4 billion ethylene plant at its Iberville Parish facility, creating work for 2,100 tradesmen; completion is slated for early 2018. Florida Fuel Connection will build a $75 million petroleum terminal in East Feliciana Parish and plans to recruit 250 total workers before completion in 2017. These industrial expansions, coupled with the ongoing downtown development, will bolster construction payrolls. Apartment developers will complete 890 units this year, the highest annual output since 2009. Absorption will again trail deliveries, causing vacancy to expand 20 basis points to 5.9%. Asking rents will appreciate 1.9% to $1,083 per month by December. In the investment arena, annual sales prices have varied greatly due to a small sample of sales and differing quality and size of assets trading hands. Despite the uneven year-over-year sales investment landscape, it is clear that buyers, particularly from out of state, will continue to pursue both Class A and value-add investments in Baton Rouge throughout 2016.

2016 PREVIEW

7

2015 PERFORMANCE HIGHLIGHTS

2.6% YOY

EMPLOYMENT10,400

2.1% YOY

ASKING RENTS$1,063

10 BPS YOY

VACANCY5.7%

123.3% YOY

CONSTRUCTION360 Units

-110 BPS YOY

UNEMPLOYMENT RATE5.5%

-20 BPS YOY

CONCESSIONS1.0%

MARKET FACTS

POPULATION828,800

MEDIANHOUSEHOLD

INCOME$53,600

HOUSEHOLDS311,900

RENTSHARE OFWALLET23.8%

-12,000

-6,000

0

6,000

12,000

18,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$0

$50,000

$100,000

$150,000

6.5%

7.0%

7.5%

8.0%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

400

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

300

600

900

2012 2013 2014 2015* 2016**

YE 2015 0.3% YOY YE 2015 1.0% YOY YE 2015 0.9% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 30 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

BATON ROUGE

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

6.5%

7.0%

7.5%

8.0%

$800

$850

$900

$950

2012 2013 2014 2015* 2016**

The local labor force expanded by 4,100 workers in the past 12 months, adding onto the 5,000 jobs created in 2014. Companies in the construction sector led job creation in which 1,700 positions were added, a 6.8% increase. Augmenting construction jobs was the development of Oxford Pharmaceuticals’ $29 million manufacturing plant which broke ground in the third quarter. An upswing in hiring among employers in the trade, transportation and utilities sector, as well as the education and health services segment, resulted in 2,300 combined new hires. Employment gains helped reduce metrowide apartment vacancy, ending the year down 20 basis points annually at 7.4%. Meanwhile, effective rents ascended 2% to $886 per month. After builders completed 1,110 units in 2014, supply growth eased to 830 rentals in 2015. Nevertheless, developers were particularly active in the Highway 280 and downtown areas.

2015 REVIEW

Blue-collar hiring will help lift overall payrolls this year. Kamtek is planning a $530 million expansion that will create 350 manufacturing jobs. Meanwhile, Publix will invest $34 million to build a distribution facility staffed with 200 trade and transportation workers. These additions will help boost metrowide employment by 3,500 jobs in 2016. Despite the modest slowdown in hiring, developers will ramp up completions to 1,120 units. Sturdy rental demand will outweigh deliveries, compressing vacancy another 20 basis points to 7.2%. Owners will raise asking rents 1.3% to $910 per month.

Robust demand for Class B/C apartment assets will drive deal flow this year. With fewer top-tier assets trading, annual pricing declined; however, acute competition for Class B/C apartment product is pulling down cap rates both in this segment and overall. Going-in rates for Class A communities are in the broad 5% range, though best-in-class properties will average 5.25%. Among middle- and lower-tier assets, cap rates typically start at 6% for ideally located, operationally sound communities, but can exceed 7% for more aggressive investments.

2016 PREVIEW

8

2015 PERFORMANCE HIGHLIGHTS

0.8% YOY

EMPLOYMENT4,100

2.0% YOY

ASKING RENTS$898

-20 BPS YOY

VACANCY7.4%

-25.1% YOY

CONSTRUCTION830 Units

0 BPS YOY

UNEMPLOYMENT RATE5.3%

10 BPS YOY

CONCESSIONS1.3%

MARKET FACTS

POPULATION1,153,200

MEDIANHOUSEHOLD

INCOME$50,700

HOUSEHOLDS457,100

RENTSHARE OFWALLET21.3%

-30,000

-20,000

-10,000

0

10,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$40,000

$50,000

$60,000

$70,000

$80,000

6.0%

6.5%

7.0%

7.5%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

200

400

600

800

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

500

1,000

1,500

2012 2013 2014 2015* 2016**

YE 2015 0.6% YOY YE 2015 1.1% YOY YE 2015 2.0% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 0 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

BIRMINGHAM

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

3.5%

4.0%

4.5%

5.0%

5.5%

$2,000

$2,100

$2,200

$2,300

$2,400

2012 2013 2014 2015* 2016**

More than 49,200 workers were added to local payrolls last year as employment expanded 1.9%. Professional and business services companies hired 18,100 workers. Aggressive recruiting at Liberty Mutual Insurance supported expansion in the financial activities segment where 2,300 staffers were recruited. Economic resiliency extended to the manufacturing industry, aided by 1366 Technologies, which began filling the first of 150 newly created positions. Healthy job growth supported multifamily absorption, which advanced 5.9% during 2015 with 6,480 newly occupied apartments. Vacancy was unchanged year over year at 4.6%. New inventory filled quickly as vacancy fell in the Cambridge/Watertown/Waltham and Central City/Back Bay/Beacon Hill submarkets, the two areas with the greatest number of completions. Operators across the metro area took advantage of heightened apartment demand, raising asking rents 5.9% to $2,250 per month.

2015 REVIEW

Favorable economic conditions and apartment fundamentals are expected to persist in the Boston metro area in 2016. Robust multifamily deliveries are anticipated, despite a projected 39.5% annual decrease to 4,110 units. Approximately 20% of new inventory in the metro will come online among several mid-rise apartment communities in the Mystic River North/Route 128 submarket. Significant completions are also scheduled in the Cambridge/Watertown/Waltham and Boston City submarkets. Brisk leasing activity is predicted with the absorption of 5,640 apartments marketwide. Demand will outpace completions by 37.3%, resulting in vacancy falling 40 basis points to 4.2% by December, the lowest year-end rate since 2000. The elevated leasing activity will be supported by the addition of 44,900 workers to the labor force, a 1.7% annual increase, and the seventh-consecutive year of job growth. Developers, anticipating sustained apartment demand, will augment the planning pipeline with 8,470 permits this year. Meanwhile, multifamily operators will capitalize on economic expansion and shrinking apartment availability by raising asking rents 3.4% to $2,327 per month.

2016 PREVIEW

9

2015 PERFORMANCE HIGHLIGHTS

1.9% YOY

EMPLOYMENT49,200

5.9% YOY

ASKING RENTS$2,250

0 BPS YOY

VACANCY4.6%

22.5% YOY

CONSTRUCTION6,800 Units

-80 BPS YOY

UNEMPLOYMENT RATE4.0%

-20 BPS YOY

CONCESSIONS0.2%

MARKET FACTS

POPULATION4,783,700

MEDIANHOUSEHOLD

INCOME$77,200

HOUSEHOLDS1,853,100

RENTSHARE OFWALLET35.0%

-75,000

-50,000

-25,000

0

25,000

50,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$125,000

$150,000

$175,000

$200,000

4.0%

5.0%

6.0%

7.0%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

3,000

6,000

9,000

2012 2013 2014 2015* 2016**

YE 2015 0.7% YOY YE 2015 1.3% YOY YE 2015 2.1% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 130 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

BOSTON

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

3.0%

4.0%

5.0%

6.0%

$800

$850

$900

$950

2012 2013 2014 2015* 2016**

Central Valley total nonfarm employment increased 1.6%, or by 18,800 workers, in 2015. With Amazon and Walmart expanding their presence in the area by creating more than 1,000 combined jobs, the trade, transportation and utilities sector was a major economic boost. The sector expanded 1.6% with 4,000 positions since January. The leisure and hospitality industry led hiring with 5,800 additions for a 5% increase. An improving job market led to leasing activity at twice the pace of inventory growth as vacancy lowered 50 basis points to 3.5%, the lowest year-end rate since 2001 when vacancy was 3.1%. A total of 750 apartments came online in 2015, up from 240 deliveries during the prior year. Spurred by rising demand, the average asking rent advanced 3.3% annually to $918 per month in December. Simultaneously, effective rents increased 3.9% to $913 per month, lowering concessions to an average of two days of free rent.

2015 REVIEW

After an ease in hiring in 2015, Central Valley businesses will again accelerate job creation to 1.9% with 22,700 new hires this year, as more warehouse and distribution centers emerge. The first phase of the International Park of Commerce development in Tracy is scheduled to open this year, which includes FedEx as a tenant. Development of the high-speed rail will boost employment, which already supported a sharp drop in vacancy in Fresno County last year. Central Valley could grow as a transportation hub as Hyperloop Transportation Technologies announced a plan to launch a five-mile Hyperloop test track in Kings County this year. Developers are focusing construction around these potential transportation hubs, with nearly three quarters of the 590 metrowide completions scheduled for this year in Fresno and San Joaquin counties. Rental demand will persist throughout Central Valley, as vacancy lowers 20 basis points to 3.3% by December. Operators will capitalize on heightened leasing activity by lifting asking rents 2.8% annually to $944 per month, while holding concessions at an average of two days of free rent.

2016 PREVIEW

10

2015 PERFORMANCE HIGHLIGHTS

1.6% YOY

EMPLOYMENT18,800

3.3% YOY

ASKING RENTS$918

-50 BPS YOY

VACANCY3.5%

206.1% YOY

CONSTRUCTION750 Units

-100 BPS YOY

UNEMPLOYMENT RATE10.1%

-60 BPS YOY

CONCESSIONS0.5%

MARKET FACTS

POPULATION4,038,100

MEDIANHOUSEHOLD

INCOME$47,500

HOUSEHOLDS1,240,500

RENTSHARE OFWALLET23.2%

-75,000

-50,000

-25,000

0

25,000

50,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$35,000

$45,000

$55,000

$65,000

6.5%

7.0%

7.5%

8.0%

8.5%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

200

400

600

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

500

1,000

1,500

2012 2013 2014 2015* 2016**

YE 2015 1.3% YOY YE 2015 1.7% YOY YE 2015 2.4% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 20 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

CENTRAL VALLEY | CA

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

4.5%

5.5%

6.5%

7.5%

$800

$900

$1,000

$1,100

2012 2013 2014 2015* 2016**

Apartment construction was well paced throughout 2015, allowing supply and demand to remain relatively balanced. Apartment developers added 1,620 units, boosting inventory by 3.1%. Builders concentrated deliveries in the submarkets of Berkeley County/Other and Central Charleston where there was ample demand. Brisk leasing provided vacancy improvements in both submarkets, where Berkeley County/Other vacancy tightened 90 basis points to 5.1% and Central Charleston rates compressed 80 basis points to 4.1%. The metrowide rate was 5.2%, the lowest year-end vacancy in nine years. Amid the vacancy decline, asking rents in Charleston elevated 5% to $1,031 per month. Underpinning the multifamily improvements was an annual employment gain of 1.6% in which employers added 5,300 total positions. Companies in the leisure and hospitality industry, along with education and health services employers, led hiring, collectively adding 3,800 workers.

2015 REVIEW

Hiring will accelerate in 2016, helping ameliorate supply-side vacancy pressure. Builders will complete 2,610 units this year, which is forecast to lift vacancy 70 basis points to 5.9% by December. Following recent robust rent gains, annual asking rent appreciation will slow to a still-healthy 3.1%, reaching $1,063 per month. Additionally, concessions will increase 50 basis points to 1.3% of asking rents. On the job front, payrolls will expand by 6,600 workers. Mercedes-Benz Vans and Volvo will separately begin construction in 2016 on assembly factories, bringing 3,300 manufacturing jobs to Charleston.

Meanwhile, investment activity will persist at a healthy pace due to demand for Class A and B apartment assets. Both in-state and East Coast buyers are driving velocity for top-tier assets. In this segment, cap rates are pushing toward the low- to mid-5% range, with pricing gravitating to $140,000 per unit, though values can rise by 50% for best-in-class communities. For middle-tier product, initial yields for well-run and located communities will near 6%, but rise to the high-6% range for B-minus assets.

2016 PREVIEW

11

2015 PERFORMANCE HIGHLIGHTS

1.6% YOY

EMPLOYMENT5,300

5.0% YOY

ASKING RENTS$1,031

-10 BPS YOY

VACANCY5.2%

-11.6% YOY

CONSTRUCTION1,620 Units

-50 BPS YOY

UNEMPLOYMENT RATE5.3%

30 BPS YOY

CONCESSIONS0.8%

MARKET FACTS

POPULATION746,500

MEDIANHOUSEHOLD

INCOME$54,700

HOUSEHOLDS293,700

RENTSHARE OFWALLET22.6%

-18,000

-12,000

-6,000

0

6,000

12,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$60,000

$80,000

$100,000

$120,000

5.0%

5.5%

6.0%

6.5%

7.0%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

300

600

900

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

1,000

2,000

3,000

2012 2013 2014 2015* 2016**

YE 2015 1.7% YOY YE 2015 2.5% YOY YE 2015 2.4% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 60 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

CHARLESTON

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

3.5%

4.5%

5.5%

6.5%

$800

$825

$850

$875

$900

2012 2013 2014 2015* 2016**

Aggressive hiring in the trade, transportation and utilities sector accounted for nearly one-third of the 4,000 jobs created in the metro area in 2015 as overall employment expanded 1.7%. Amazon filled 500 positions during this time, the primary contributor to 1,300 new jobs in the sector. The greatest rate of growth, however, occurred in the professional and business services segment, which advanced 4.3% with 1,200 workers added. Multifamily developers, confident in sustained economic expansion, requested permits for 750 apartments. The broad-based job growth supported a 16.3% increase in absorption. Renters had a broader choice of apartments last year as 870 units came online, a 3.2% annual increase in rental inventory. Builders concentrated much of the new stock in the southern portion of the metro. By year-end, overall vacancy was 4.8%, 30 basis points lower than one year prior. Market rents advanced 2.7% to $866 per month as vacancy decreased.

2015 REVIEW

Fallout from Volkswagen’s emissions scandal poses modest downside risk to job creation due to the company’s large presence in the metro. Nevertheless, at the close of 2015, the automaker remained committed to expanding local manufacturing operations. With no imminent autoworker layoffs on the horizon, metrowide employment is forecast to rise by 3,600 workers this year, a gain of 1.5% that will support apartment absorption of 460 units. Vacancy will descend 50 basis points to 4.3%, while operators lift market rents 2.1% to $884 per month by year-end. Similarly, effective rents are on pace to appreciate 2.1% to $878 per month. Improving apartment fundamentals will encourage developers to increase planning activity as they request permits for 940 apartments, a 24.9% increase over issuance in 2015. Meanwhile, 340 units are scheduled to come online. Approximately half of the deliveries will be completed among two mid-rise developments in the Central submarket, The Mission at Main and Vista Cameron Harbor apartment communities. Additionally, more than a dozen multifamily developments with nearly 3,500 total units are in various stages of the planning process.

2016 PREVIEW

12

2015 PERFORMANCE HIGHLIGHTS

1.7% YOY

EMPLOYMENT4,000

2.7% YOY

ASKING RENTS$866

-30 BPS YOY

VACANCY4.8%

68.2% YOY

CONSTRUCTION870 Units

-80 BPS YOY

UNEMPLOYMENT RATE5.5%

-70 BPS YOY

CONCESSIONS0.7%

MARKET FACTS

POPULATION549,800

MEDIANHOUSEHOLD

INCOME$51,300

HOUSEHOLDS222,600

RENTSHARE OFWALLET20.3%

-15,000

-10,000

-5,000

0

5,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$40,000

$50,000

$60,000

$70,000

$80,000

6.0%

6.5%

7.0%

7.5%

8.0%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

400

800

1,200

2012 2013 2014 2015* 2016**

YE 2015 0.6% YOY YE 2015 1.2% YOY YE 2015 2.6% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 0 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

CHATTANOOGA

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

4.0%

4.5%

5.0%

5.5%

6.0%

$1,350

$1,400

$1,450

$1,500

$1,550

2012 2013 2014 2015* 2016**

Despite contracting manufacturing payrolls, hiring in several other sectors helped lift overall employment and maintain apartment demand. Chicago-area payrolls expanded by 44,000 positions in the past 12 months. The 18,600 workers added in the professional and business services segment led the metro in 2015. The education and health services and the trade, transportation and utilities industries, meanwhile, combined to recruit 18,100 personnel. Conversely, the reduction of 5,500 manufacturing jobs was the largest drag on the economy. Despite this decline, overall hiring was sufficient to depress vacancy amid a 29.5% year-over-year rise in completions. The 4,770 apartment units that came online marketwide in 2015 trailed absorption of 7,120 units, underpinning a 30-basis-point annual decline in vacancy to 4.7%. Occupancy improvements supported operators’ ability to raise rents, with asking rents advancing 3.4% annually to $1,504 per month at the end of 2015.

2015 REVIEW

Although the ease in job creation this year will be modest, completions will accelerate causing vacancy to edge higher. The 41,200 new hires expected this year will increase Chicago-area payrolls by 0.9%. Meanwhile, metrowide inventory will rise by 7,740 units, a 62.3% annual increase in deliveries. Supply growth will be greatest within the city, with The Loop, City West and Gold Coast/River North submarkets expected to register more than 3,900 total new apartments this year. In the suburbs, at least 500 units will come online in the near-in Glenview/Evanston submarket.

While vacancy will rise in 2016, the supply imbalance will be modest and temporary. Marketwide vacancy will tick up 20 basis points to 4.9% by December. In comparison, vacancy averaged 6.3% in the three years preceding the recession. The mild vacancy rise will allow operators to continue to raise rents, though concessions will expand. Asking rents are forecast to rise 2.9% to $1,547 per month this year. Effective rents will advance 2.3% to $1,525 per month, expanding average concessions to 1.4% of asking rents.

2016 PREVIEW

13

2015 PERFORMANCE HIGHLIGHTS

1.0% YOY

EMPLOYMENT44,000

3.4% YOY

ASKING RENTS$1,504

-30 BPS YOY

VACANCY4.7%

29.5% YOY

CONSTRUCTION4,770 Units

-90 BPS YOY

UNEMPLOYMENT RATE5.3%

-10 BPS YOY

CONCESSIONS0.9%

MARKET FACTS

POPULATION9,598,800

MEDIANHOUSEHOLD

INCOME$64,400

HOUSEHOLDS3,557,600

RENTSHARE OFWALLET28.0%

-240,000

-160,000

-80,000

0

80,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$80,000

$90,000

$100,000

$110,000

$120,000

6.5%

7.0%

7.5%

8.0%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

3,000

6,000

9,000

2012 2013 2014 2015* 2016**

YE 2015 0.3% YOY YE 2015 0.9% YOY YE 2015 2.9% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 10 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

CHICAGO

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

4.0%

4.5%

5.0%

5.5%

$750

$800

$850

$900

2012 2013 2014 2015* 2016**

Education and health services employment surged 6.8% in 2015 with the addition of 10,500 workers. The sector was the largest contributor to 23,500 new jobs in the metro, equating to 2.3% annual growth. Substantial increases were also recorded in the professional and business services segment as 4,300 jobs were created. In the trade, transportation and utilities sector, 4,200 workers were hired, supported by 120 new positions at online pet retailer BarkBox. The broad-based hiring fueled healthy apartment demand in step with supply growth, keeping vacancy at 4.9%, the same as one year earlier. Builders finished 3,300 apartments last year, the greatest annual completions since 2004. Monthly asking rents appreciated at a quicker 3% rate in 2015, compared to 2.9% in the prior year, reaching $845 by December. Meanwhile, effective rents advanced 3.1% to $833 per month.

2015 REVIEW

Metrowide employment is projected to expand 1.8% this year with the addition of 18,900 workers. Apartment fundamentals will continue to improve with the sustained economic growth. Renters are forecast to occupy 1,650 additional units this year, outpacing the 1,080 rentals that come online. More than one-quarter of the new stock is slated for the University/Downtown submarket. Builders will deliver an even assortment of garden and mid-rise communities across the metro. The largest development, the three-story, 326-unit District at Linworth, is slated for completion late in the year. As deliveries trail absorption, metrowide vacancy is predicted to fall 40 basis points to 4.5% by December, the lowest year-end rate since 2000. The downward trend in availability will enable further rent appreciation. Landlords are expected to increase market rents 2.6% to $867 per month, while effective rents reach $857 per month, a 2.9% gain. Operators will generate additional revenue by cutting average concessions from 1.4% to 1.2% of asking rents over the course of the year.

2016 PREVIEW

14

2015 PERFORMANCE HIGHLIGHTS

2.3% YOY

EMPLOYMENT23,500

3.0% YOY

ASKING RENTS$845

0 BPS YOY

VACANCY4.9%

59.9% YOY

CONSTRUCTION3,300 Units

-80 BPS YOY

UNEMPLOYMENT RATE3.6%

-10 BPS YOY

CONCESSIONS1.4%

MARKET FACTS

POPULATION2,029,900

MEDIANHOUSEHOLD

INCOME$56,700

HOUSEHOLDS802,600

RENTSHARE OFWALLET17.9%

-40,000

-20,000

0

20,000

40,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$30,000

$40,000

$50,000

$60,000

7.0%

7.5%

8.0%

8.5%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

400

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

2,000

4,000

6,000

2012 2013 2014 2015* 2016**

YE 2015 1.2% YOY YE 2015 2.0% YOY YE 2015 1.1% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 30 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

COLUMBUS

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

3.0%

4.0%

5.0%

6.0%

$800

$900

$1,000

$1,100

2012 2013 2014 2015* 2016**

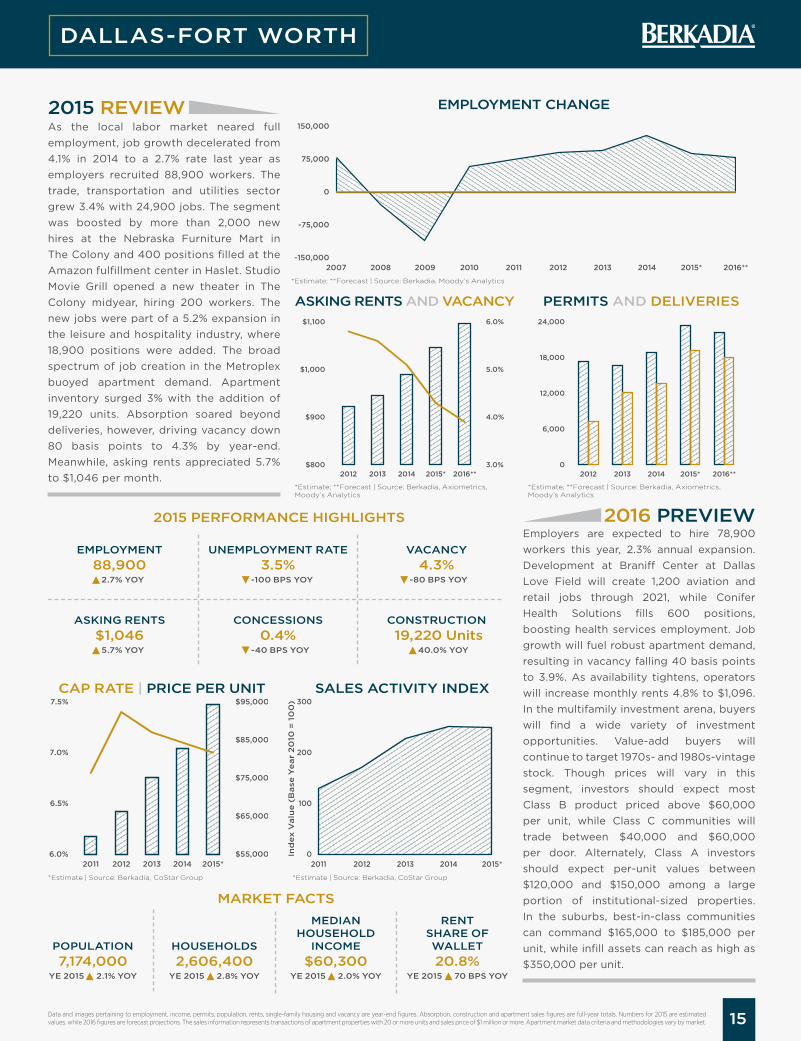

As the local labor market neared full employment, job growth decelerated from 4.1% in 2014 to a 2.7% rate last year as employers recruited 88,900 workers. The trade, transportation and utilities sector grew 3.4% with 24,900 jobs. The segment was boosted by more than 2,000 new hires at the Nebraska Furniture Mart in The Colony and 400 positions filled at the Amazon fulfillment center in Haslet. Studio Movie Grill opened a new theater in The Colony midyear, hiring 200 workers. The new jobs were part of a 5.2% expansion in the leisure and hospitality industry, where 18,900 positions were added. The broad spectrum of job creation in the Metroplex buoyed apartment demand. Apartment inventory surged 3% with the addition of 19,220 units. Absorption soared beyond deliveries, however, driving vacancy down 80 basis points to 4.3% by year-end. Meanwhile, asking rents appreciated 5.7% to $1,046 per month.

2015 REVIEW

Employers are expected to hire 78,900 workers this year, 2.3% annual expansion. Development at Braniff Center at Dallas Love Field will create 1,200 aviation and retail jobs through 2021, while Conifer Health Solutions fills 600 positions, boosting health services employment. Job growth will fuel robust apartment demand, resulting in vacancy falling 40 basis points to 3.9%. As availability tightens, operators will increase monthly rents 4.8% to $1,096. In the multifamily investment arena, buyers will find a wide variety of investment opportunities. Value-add buyers will continue to target 1970s- and 1980s-vintage stock. Though prices will vary in this segment, investors should expect most Class B product priced above $60,000 per unit, while Class C communities will trade between $40,000 and $60,000 per door. Alternately, Class A investors should expect per-unit values between $120,000 and $150,000 among a large portion of institutional-sized properties. In the suburbs, best-in-class communities can command $165,000 to $185,000 per unit, while infill assets can reach as high as $350,000 per unit.

2016 PREVIEW

15

2015 PERFORMANCE HIGHLIGHTS

2.7% YOY

EMPLOYMENT88,900

5.7% YOY

ASKING RENTS$1,046

-80 BPS YOY

VACANCY4.3%

-100 BPS YOY

UNEMPLOYMENT RATE3.5%

-40 BPS YOY

CONCESSIONS0.4%

MARKET FACTS

POPULATION7,174,000

MEDIANHOUSEHOLD

INCOME$60,300

HOUSEHOLDS2,606,400

RENTSHARE OFWALLET20.8%

-150,000

-75,000

0

75,000

150,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$55,000

$65,000

$75,000

$85,000

$95,000

6.0%

6.5%

7.0%

7.5%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

6,000

12,000

18,000

24,000

2012 2013 2014 2015* 2016**

YE 2015 2.1% YOY YE 2015 2.8% YOY YE 2015 2.0% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

40.0% YOY

CONSTRUCTION19,220 Units

YE 2015 70 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

DALLAS-FORT WORTH

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

4.0%

4.5%

5.0%

5.5%

$1,000

$1,200

$1,400

$1,600

2012 2013 2014 2015* 2016**

Denver headcounts expanded 2.1%, or by 29,200 jobs, in 2015, as the pace of growth eased with metro-area payrolls approaching full employment. The latest increase was the sixth year of rising staffing levels. Sustained hiring spurred developers to elevate multifamily permitting activity beginning in 2012, supporting the 9,790 apartments coming online in 2015, and nearing the past peak of 10,480 additions during 2002. Development remained concentrated in the Denver-Downtown submarket, accounting for more than one out of every four metrowide additions during the last 12 months. Overall, vacancy lifted 50 basis points to 4.7% by year-end 2015, as the influx of inventory exceeded healthy demand by 24.3%. With vacancy still lower than the 4.8% five-year average, asking rents surged 9% to $1,373 per month by December. Simultaneously, operators lifted effective rents 9.1% to $1,371 per month.

2015 REVIEW

Several employers committed to expanding their presence in the Denver metropolitan area during the upcoming years, the largest announcements coming from the financial activities sector. Charles Schwab plans to hire more than 500 workers by 2018, while OnDeck Capital Inc. committed to add 400 jobs by 2019. In the near term, total nonfarm employment is forecast to elevate 2% year over year with 28,000 additions by December. As job creation remains healthy, so will leasing activity. Residents will newly occupy 6,460 units during the next four quarters, 30.1% higher than the five-year average. Builders are working to meet the demand by adding 9,060 apartments to market inventory, with 3,680 apartments scheduled to come online in the Denver-Downtown submarket. Metrowide supply growth will again exceed the elevated leasing activity, resulting in vacancy increasing 70 basis points annually to 5.4%. As operators increase efforts to entice renters amid stiff competition, average concessions will increase to six days of free rent. Nevertheless, operators are projected to lift asking rents 5.6% to $1,450 per month during the next four quarters.

2016 PREVIEW

16

2015 PERFORMANCE HIGHLIGHTS

2.1% YOY

EMPLOYMENT29,200

9.0% YOY

ASKING RENTS$1,373

50 BPS YOY

VACANCY4.7%

60.6% YOY

CONSTRUCTION9,790 Units

-30 BPS YOY

UNEMPLOYMENT RATE3.8%

-10 BPS YOY

CONCESSIONS0.1%

MARKET FACTS

POPULATION2,829,900

MEDIANHOUSEHOLD

INCOME$68,500

HOUSEHOLDS1,135,700

RENTSHARE OFWALLET24.1%

-60,000

-30,000

0

30,000

60,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$0

$50,000

$100,000

$150,000

5.5%

6.0%

6.5%

7.0%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

400

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

2,500

5,000

7,500

10,000

2012 2013 2014 2015* 2016**

YE 2015 1.7% YOY YE 2015 2.5% YOY YE 2015 3.0% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 130 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

DENVER

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

3.5%

4.5%

5.5%

6.5%

$850

$875

$900

$925

$950

2012 2013 2014 2015* 2016**

Apartment fundamentals continued to improve in the Detroit metro area last year as payrolls grew. Developers added 400 units to local inventory, more than 80% of which came online downtown. Metrowide, the vacancy rate plunged 150 basis points to 4.6%, while asking rents advanced to $924 per month, 3% annual appreciation. Apartment demand surged with 4,620 newly occupied units last year, the greatest annual absorption since 2010, when foreclosures propped up leasing activity. The sturdy demand was supported by a 1.6% increase in employment as businesses recruited 30,600 workers. The largest contributor to growth was the trade, transportation and utilities sector, where 9,400 workers were recruited, a 2.5% increase. The manufacturing industry followed with 7,800 new hires, a gain of 3.2%. Rounding out the high-growth sectors was the professional and business services segment, which expanded 1.9% with 7,100 newly created jobs.

2015 REVIEW

Manufacturing will be a major driver in the local economy in 2016. General Motors will continue adding hundreds of technicians at its Warren Tech Center as part of a five-year expansion resulting in 2,600 new jobs. During the same period, up to 10,000 research and manufacturing jobs in metallurgy, stamping and casting will be created in the area through public-private initiatives administered through the American Lightweight Materials Manufacturing Innovation Institute in Canton, Michigan. Significant hiring will also occur in the financial activities sector as Quicken fills 1,100 positions following rehabilitation of the Detroit Media Partnership building in downtown Detroit. These additions will be part of 27,200 newly created jobs in 2016, 1.4% annual growth. The sustained expansion will spur already elevated apartment demand, which developers will accommodate with 1,050 new units. Renters are projected to absorb 2,710 apartments, resulting in a 60-basis-point decrease in vacancy to 4%. As availability diminishes, operators are expected to boost asking rents 2.6% to $948 per month and reduce concessions to 0.4% of average asking rents.

2016 PREVIEW

17

2015 PERFORMANCE HIGHLIGHTS

1.6% YOY

EMPLOYMENT30,600

3.0% YOY

ASKING RENTS$924

-150 BPS YOY

VACANCY4.6%

28.6% YOY

CONSTRUCTION400 Units

-260 BPS YOY

UNEMPLOYMENT RATE5.1%

-30 BPS YOY

CONCESSIONS0.9%

MARKET FACTS

POPULATION4,301,800

MEDIANHOUSEHOLD

INCOME$56,900

HOUSEHOLDS1,716,500

RENTSHARE OFWALLET19.5%

-180,000

-120,000

-60,000

0

60,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$20,000

$30,000

$40,000

$50,000

7.5%

8.0%

8.5%

9.0%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

400

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

1,000

2,000

3,000

2012 2013 2014 2015* 2016**

YE 2015 0.1% YOY YE 2015 1.1% YOY YE 2015 4.2% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 -20 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

DETROIT

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

5.0%

5.5%

6.0%

6.5%

7.0%

$950

$1,000

$1,050

$1,100

$1,150

2012 2013 2014 2015* 2016**

After years of rising multifamily permitting issuance, 16,660 apartments came online in Houston during 2015. Deliveries were more than double the five-year average. Construction was focused in the Montrose/River Oaks submarket, accounting for more than one out of every four new apartments in the metro added during the last 12 months. Resilient demand in the area resulted in vacancy decreasing 60 basis points annually to 5.4%. Conversely, metrowide vacancy ticked up 10 basis points to 5.8% as hiring slowed amid losses in the energy industry when the manufacturing and the natural resources and mining sectors shed a combined 16,300 jobs since January. Overall, employers added 16,700 positions, a modest 0.6% year-over-year expansion, following a 3.8% rise in payrolls in 2014. Even with the slowdown, asking rents advanced 3.4% annually to $1,091 per month in December, while concessions held at an average of three days of free rent.

2015 REVIEW

Hiring will remain moderate this year as headcounts grow by 12,000 positions, for a 0.4% increase by year-end. The opening of the $417 million heating, ventilation and air conditioning manufacturing facility for Daikin Industries Ltd. is scheduled for mid-year and will create 500 jobs in the previously contracting manufacturing sector. Despite the rising payrolls, leasing activity should ease amid an influx of new inventory. Renters, especially millennials, will continue to seek apartments near employment hubs in the east side of Houston where the health care and technology industries are growing. The largest community to come online in the area is the 361-unit Catalyst Houston in the Interloop/South Houston submarket. Overall, demand will not keep pace with the 15,450 apartments scheduled to come online metrowide, as vacancy elevates 40 basis points to 6.2%. Even with the increase, vacancy will remain well below the 7.3% 10-year average. With vacancy rising, annual effective rent growth will slow to 1.7% and reach $1,099 per month by December, resulting in a rise in concessions to an average of six days of free rent. The move will allow asking rents to rise 2.4% simultaneously to $1,117 per month.

2016 PREVIEW

18

2015 PERFORMANCE HIGHLIGHTS

0.6% YOY

EMPLOYMENT16,700

3.4% YOY

ASKING RENTS$1,091

10 BPS YOY

VACANCY5.8%

18.6% YOY

CONSTRUCTION16,660 Units

-20 BPS YOY

UNEMPLOYMENT RATE4.2%

0 BPS YOY

CONCESSIONS0.9%

MARKET FACTS

POPULATION6,688,000

MEDIANHOUSEHOLD

INCOME$61,000

HOUSEHOLDS2,336,300

RENTSHARE OFWALLET21.5%

-120,000

-60,000

0

60,000

120,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$50,000

$70,000

$90,000

$110,000

6.5%

7.0%

7.5%

8.0%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

9,000

18,000

27,000

2012 2013 2014 2015* 2016**

YE 2015 2.0% YOY YE 2015 2.7% YOY YE 2015 1.8% YOY

Ind

ex

Valu

e (

Base

Ye

ar

20

10 =

10

0)

YE 2015 30 BPS YOY

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

*Estimate; **Forecast | Source: Berkadia, Axiometrics, Moody’s Analytics

PERMITS AND DELIVERIES

HOUSTON

Data and images pertaining to employment, income, permits, population, rents, single-family housing and vacancy are year-end figures. Absorption, construction and apartment sales figures are full-year totals. Numbers for 2015 are estimated values, while 2016 figures are forecast projections. The sales information represents transactions of apartment properties with 20 or more units and sales price of $1 million or more. Apartment market data criteria and methodologies vary by market.

EMPLOYMENT CHANGE

4.0%

4.5%

5.0%

5.5%

$1,200

$1,300

$1,400

$1,500

2012 2013 2014 2015* 2016**

The local economic revitalization that began in 2012 continued in 2015. Employers augmented payrolls 3.7% year over year in Riverside and San Bernardino counties with the creation of 48,300 jobs. The largest contributor to this growth was the trade, transportation and utilities sector, gaining 10,000 workers, an increase of 3.1%. A significant portion of expansion in the sector was attributed to hundreds of jobs created among retail operators Smart & Final Extra! in Moreno Valley, The Fresh Market in Palm Desert and Mountain Grove Citrus Plaza in Redlands. Brisk job growth enabled multifamily operators to boost asking rents 6.5% to $1,390 per month by year-end. Robust rent appreciation occurred despite a 20-basis-point rise in vacancy to a still-healthy 4.5%. Completions numbering 1,690 units were the highest-recorded annual total since 2009, a factor in the uptick in vacancy. Long-term planning activity remained elevated as developers requested permits for 2,830 apartments.

2015 REVIEW

An additional 35,200 job seekers will procure employment this year, equating to a 2.6% gain. Logistics expansion in the two-county area will be a key contributor to overall growth. Australian-based Goodman Group has more than 4.9 million square feet of light-industrial space in various stages of development that, when completed, will provide space for numerous logistics companies, creating thousands of jobs. In the manufacturing industry, Fisker Automotive Inc. will open an assembly plant in Moreno Valley, hiring 150 workers. Economic expansion will sustain apartment demand with 1,300 additional units occupied by year-end. During this time, builders will deliver 1,760 rentals, more than 80% of which will be concentrated in the western portion of the metro. With the short-term supply imbalance, vacancy is forecast to edge up 20 basis points to 4.7%. Despite the upturn in vacancy, multifamily operators are expected to raise asking rents 5.2% this year to $1,462 per month. Meanwhile, effective rents will appreciate 4.9% to $1,455 per month as concessions rise from 0.2% to 0.5% of average asking rents.

2016 PREVIEW

19

2015 PERFORMANCE HIGHLIGHTS

3.7% YOY

EMPLOYMENT48,300

6.5% YOY

ASKING RENTS$1,390

20 BPS YOY

VACANCY4.5%

30.0% YOY

CONSTRUCTION1,690 Units

-150 BPS YOY

UNEMPLOYMENT RATE6.1%

-30 BPS YOY

CONCESSIONS0.2%

MARKET FACTS

POPULATION4,526,400

MEDIANHOUSEHOLD

INCOME$56,000

HOUSEHOLDS1,405,200

RENTSHARE OFWALLET29.8%

-80,000

-40,000

0

40,000

80,000

2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016**

ASKING RENTS AND VACANCY

*Estimate; **Forecast | Source: Berkadia, Moody’s Analytics

$0

$40,000

$80,000

$120,000

5.0%

5.5%

6.0%

6.5%

2011 2012 2013 2014 2015*

CAP RATE | PRICE PER UNIT

*Estimate | Source: Berkadia, CoStar Group

0

100

200

300

2011 2012 2013 2014 2015*

SALES ACTIVITY INDEX

*Estimate | Source: Berkadia, CoStar Group

0

1,000

2,000

3,000

4,000

2012 2013 2014 2015* 2016**