foreclosure & mortgage debt forgiveness what are they? why are we concerned? irs pub 4702 irs...

TRANSCRIPT

FORECLOSURE & MORTGAGE DEBT FORGIVENESS

WHAT ARE THEY?

WHY ARE WE CONCERNED?IRS Pub 4702

IRS Pub 970

DEFINITIONS• Foreclosure: Takeover of property by lender,

court process involved– Reportable ON Sched D; Possible Capital Gain may

be Reduced by Exclusion

• Cancellation of Debt; Reduction in Liability of Debtor due to Foreclosure, Repossession, or Negotiation.

• Debt Forgiveness: Cancelled Debt which the taxpayer may exclude from income.

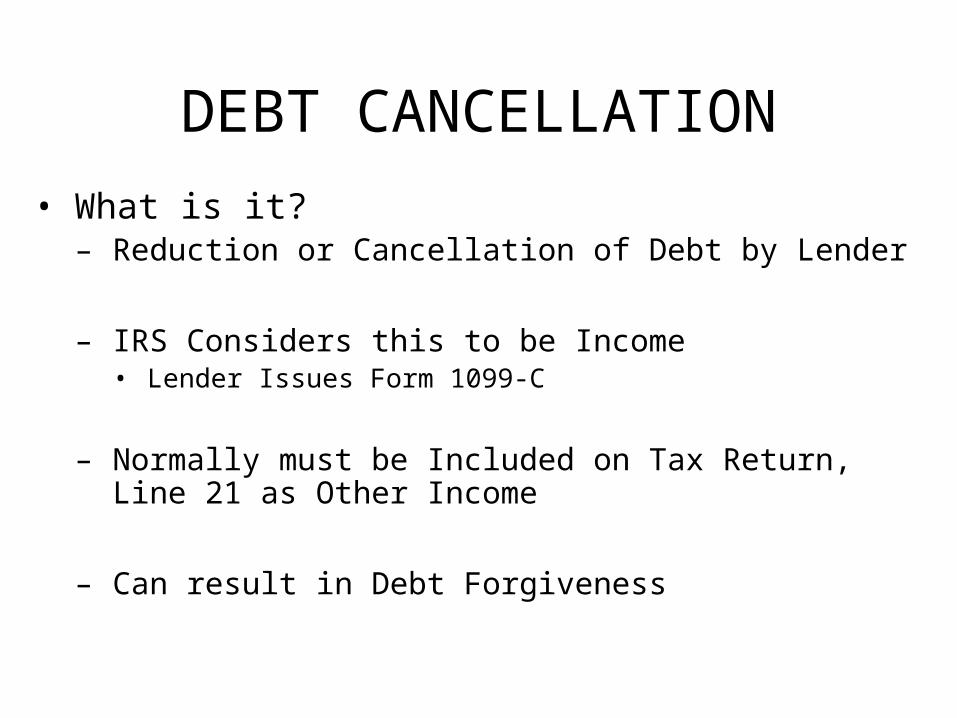

DEBT CANCELLATION

• What is it?– Reduction or Cancellation of Debt by Lender

– IRS Considers this to be Income• Lender Issues Form 1099-C

– Normally must be Included on Tax Return, Line 21 as Other Income

– Can result in Debt Forgiveness

IN-SCOPE• Foreclosure Reported as a sale of home from

1099-A –Must be reported on Schedule D– (May be only 1099-C if foreclosure and debt forgiveness in same

year)

• Cancellation of Debt Reported on Form 982 (if Recourse Debt)– 1099-A, Box 5 is YES

• No Cancellation of Debt if Non-Recourse Debt– 1099-A Box 5 is NO– Selling Price is Full Amount of Debt owed

Possible Gain Due to “Sale” of Property (1099-A)

Foreclosure –Real Property

• Foreclosure –Results in a Sale of Property from debtor to creditor (Form 1099-A)

• May have Capital Gain or Loss– If Personal Residence, No Loss Allowed

• Taxpayer will Receive Form 1099-A from creditor

• May also have Income from Cancelled Debt– Will Receive Form 1099-C

• RECOURSE (Borrower Personally Responsible) - Taxpayer should have Form 1099-A– Box 2 Shows Balance of Debt Outstanding– Box 4 Shows FMV of Property– Lesser Value is Sales Price listed on Sched D

• NON-RECOURSE (will not see ,very rare)

1099-A (example: Hyundai ad )– Box 2 is always Sales Price (Bal of Debt)

Foreclosure –Real Property

CANCELLATION OF DEBT REPORTING - RECOURSE DEBT

• Taxpayer will Receive Form 1099-C– Box 2 Shows Amount of Debt Forgiven.

• Must complete Form 982 and attach to Return– If Foreclosure, Complete only Boxes 1E and 2.– If Ownership retained, also complete Box 10b

• No Income Reported on Line 21, Form 1040

EXAMPLE• Mary Smith purchased her main home in June 2003 for

$175,000. • In 2008 she lost her job and was no longer able to make her

payments on this recourse mortgage. • In July, Mary moved out of the home to live with relatives. • On July 15, 2008 the bank foreclosed on the home and

canceled the remaining amount owed on the home. • The fair market value at the time was $100,000 because of

the poor housing market, but Mary still owed $150,000 on the mortgage.

• None of the loan proceeds were used for any purpose other than to buy, build, or substantially improve the principal residence.

1099-C

50,00007/15/2008

Home Mortgage Loan

FORM 982

FORM 982

• If Debt Forgiven and Ownership Retained: – Reduce Basis by Amount of Forgiven Debt

FORM 982, LINE 10B

FORM 1099-A

(RECOURSE) x

150,000

100,000

Home Mortgage Loan

07/15/08

• In Taxwise,– Select Sched D Wksht 2 from Forms List

• 1099-A, Box 1 is Date of Sale• 1099-A, Box 2 or Box 4 is Sale Price (Lesser)

– Complete Wksht 2, “Sale of Your Home” through Ln 14

– Ln 14 value must be entered Manually on Sched D. Does NOT Carry over from Worksheet

Foreclosure –Real Property

MARY SMITH FORECLOSURESCHED D, WORKSHEET 2

MARY SMITH FORECLOSURECAP GAIN WORKSHEET - LOSS

MUST OVERRIDE to 0

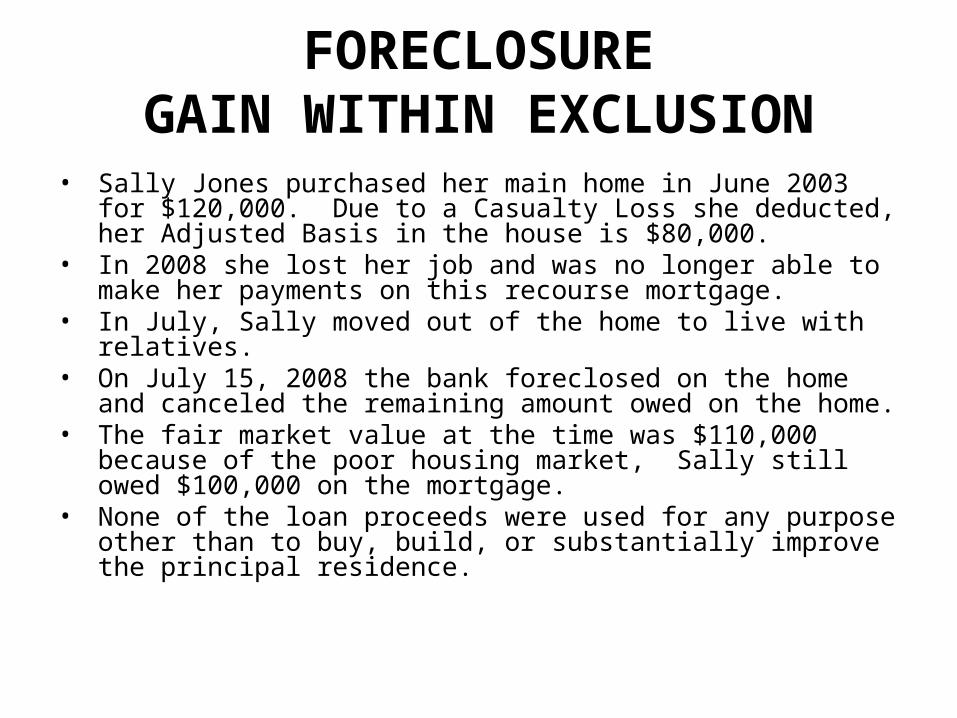

FORECLOSUREGAIN WITHIN EXCLUSION

• Sally Jones purchased her main home in June 2003 for $120,000. Due to a Casualty Loss she deducted, her Adjusted Basis in the house is $80,000.

• In 2008 she lost her job and was no longer able to make her payments on this recourse mortgage.

• In July, Sally moved out of the home to live with relatives. • On July 15, 2008 the bank foreclosed on the home and

canceled the remaining amount owed on the home. • The fair market value at the time was $110,000 because

of the poor housing market, Sally still owed $100,000 on the mortgage.

• None of the loan proceeds were used for any purpose other than to buy, build, or substantially improve the principal residence.

FORM 1099-A

x

100,000

110,000Sally Jones

Home Mortgage Loan

SALLY JONES FORECLOSURESCHED D, WORKSHEET 2 - GAIN

SALLY JONES FORECLOSURENON-TAXABLE GAIN

F3 TO “GET RED OUT

Schedule D Reporting of NonRecourse Debt

• To compute the realized gain or loss due to a Foreclosure of a nonrecourse debt, the amount of Debt cancelled is the Sale Price.

• A gain can be offset by Section 121 if the conditions are met for exclusion.

• If loss occurs due to foreclosure of Personal residence, it is a nondeductible loss.

Non Recourse Debt

No Cancellation of Debt if Non-Recourse

*1099-A Box 5 is NO

*No 1099-C issued

* Do not complete form 982

*Selling Price on Schedule D is Box 2 of 1099-A (Full Amount of Debt Cancelled)

Non Recourse Debt George Wilson paid $200,000 for his home.

He borrowed $190,000 from a bank. He is not personally liable for the loan (nonrecourse debt). He pledges the house as security.

Due to lack of payments, the bank foreclosed on the house. The loan balance was $180,000 and the FMV was $170,000.

The amount realized on foreclosure is $180,000 (debt cancelled) and there is no Cancellation of Debt to be reported.