forefield asset protection

TRANSCRIPT

Miles B. Kessler, CFP®Investment Representative

870 Kipling StreetSuite A

Lakewood, CO 80215-5826Direct: 303-290-8942

Branch: [email protected]

Asset Protection

January 28, 2016Page 1 of 10, see disclaimer on final page

Asset Protection

Introduction

If you haven't done any asset protectionplanning, your wealth is vulnerable to potentialfuture creditors and, should the worst happen,you could lose everything.

Lawsuits, taxes, accidents, and other financialrisks are facts of everyday life. And thoughyou'd like to believe that you're safe,misfortune can befall even the most carefulperson. What can you do? First, identify yourpotential loss exposure, then implementstrategies that are designed to help reducethat exposure without compromising yourother estate and financial planning objectives.

First, a word about fraudulenttransfers

Part of your overall asset protection plan mightinclude repositioning assets to make it legallydifficult for potential future creditors to reachthem. This does not, however, extend toactions that hide assets or defraud creditors. Ifa court finds that your asset protection planswere made with the intent to defraud, it willdisregard those plans and make the assetsavailable to creditors. How can you avoidrunning afoul of the fraudulent transfer laws?

• Make sure your plans are made forlegitimate business purposes or toaccomplish legitimate estate planningobjectives

• Carefully document the legitimate businessand estate planning purposes of anyarrangements you make

• Put your plans into effect before you haveany problems with creditors

• Do not implement a plan at a time when alawsuit is imminent or pending or at a timewhen you have an outstanding debt thatyou believe you may be unable to pay

Where the dangers lie

Unexpected liability can come from just aboutanywhere:

• The IRS and other tax authorities• Accident victims, including victims whose

injuries were caused by the actions ofminor children or employees

• Doctors, hospitals, nursing homes, andother health-care providers

• Credit card companies

• Business creditors, including employeesand former employees, governmentalagencies, suppliers, customers, partners,shareholders, and the general public

• Creditors of other individuals, where youhave cosigned or guaranteed obligationsfor those individuals

• Marital or other live-in partners

Asset Protection Techniques

There are three basic asset protectiontechniques: insurance, statutory protection,and asset placement. None of thesetechniques is a complete solution by itself, butmay make sense as one limited component ofan asset protection plan.

Insurance

The simplest way to cope with risk is to shiftthe risk to an insurance company. This shouldbe your first line of defense. Before you doanything else, review your existing coverage.Then consider purchasing or increasingcoverage on your insurance policies asappropriate. You should be adequatelyinsured against:

• Death and disability• Medical risk, including long-term care• Liability and property loss (both personal

and business)• Other business losses

Statutory protection

Creditors can't enforce a lien or judgmentagainst property that is exempt under federalor state law. While exemption planning can'toffer total protection, it can offer some shelterfor certain assets.

Both federal and state laws govern whetherproperty is exempt or nonexempt innonbankruptcy proceedings (separate federaland state laws govern whether property isexempt or nonexempt in bankruptcyproceedings). Generally, you can choosewhether the federal exemption or the stateexemption applies. When looking atexemption laws, be sure to find out how muchof an exemption is allowed for a particular typeof property--it may be completely exempt, orexempt only up to a certain amount orrestricted in some way. Types of propertyoften receiving an exemption include:

If you haven't done anyasset protection planning,your wealth is vulnerable topotential future creditorsand, should the worsthappen, you could loseeverything.

The simplest way to copewith risk is to shift the riskto an insurance company.This should be your firstline of defense.

Page 2 of 10, see disclaimer on final page

• Homestead (principal residence)• Personal property• Motor vehicle• IRAs, pension plans, and Keogh plans• Prepaid college tuition plans• Life insurance benefits and cash value• Proceeds of life insurance• Proceeds of annuities• Wages

Tip: In those jurisdictions that recognizeownership by tenancy by the entirety (TBE),creditors of the husband or creditors of thewife cannot reach TBE assets.

Asset placement

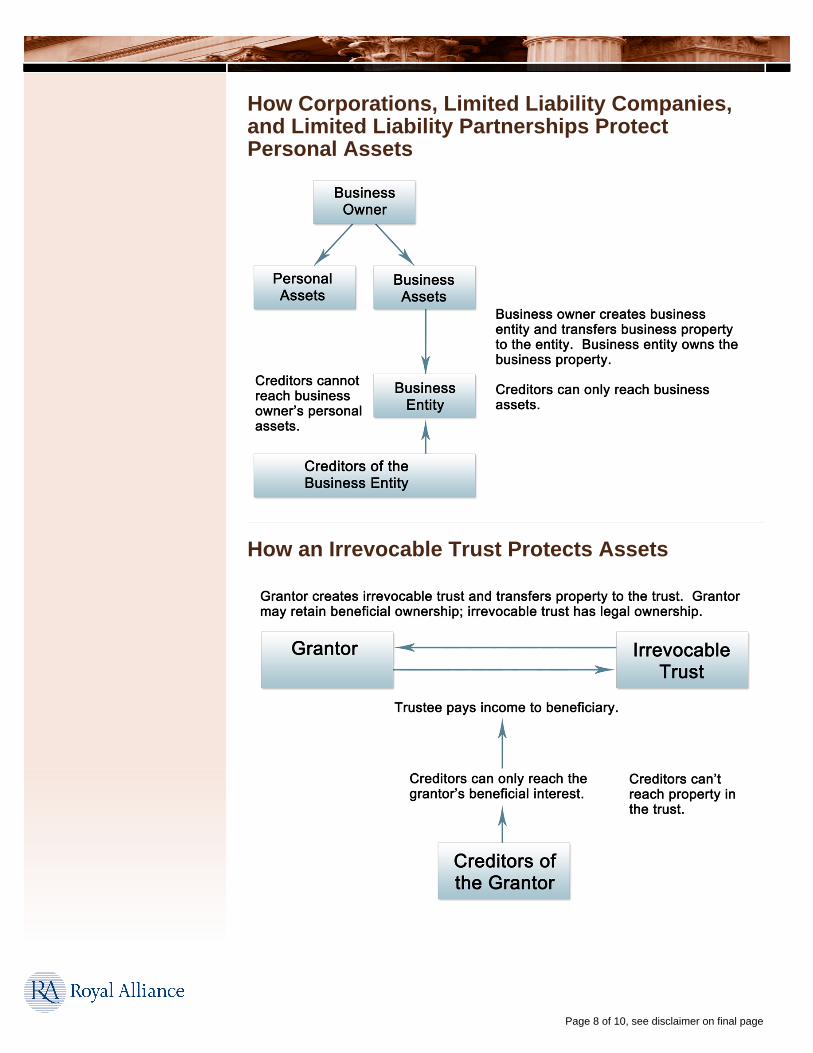

Asset placement refers to transferring legalownership of assets to other persons orentities, such as corporations, limitedpartnerships, and trusts. The basis for thistechnique is simple--creditors can't reachproperty that you do not own or control.

Shifting assets to the spouse who is lessexposed to claims

If you have high exposure to potential liabilitybecause of your occupation or business, itmay be advisable for you to shift assets toyour spouse. Your spouse would retain theassets that are subject to the exposure as hisor her separate property, and you would retainassets that enjoy statutory protection, such asthe homestead, life insurance, and annuities,as separate property. Furthermore, the shiftingof assets to a spouse or children may helpaccomplish other estate planning goals.

Caution: To avoid complications in the eventthat your marriage ends in divorce, both youand your spouse should agree to the divisionof assets in writing. This is especiallyimportant in community property states.

Corporations

If you own a business and aren't already acorporation, changing your business structureto a corporation will make it a separate legalentity in the eyes of the law. As such, acorporation owns the business assets and isresponsible for all business debts. Thus,incorporating your business separates yourbusiness assets from your personal assets, soyour personal assets will generally not be atrisk for the acts of the business.

Caution: The limited liability feature may be

lost if, for example, the corporation acts in badfaith, fails to observe corporate formalities(e.g., organizational meetings), has its assetsdrained (e.g., unreasonably high salaries paidto shareholder-employees), is inadequatelyfunded, or has its funds commingled withshareholders' funds.

Caution: A number of issues should beconsidered when selecting a form of businessentity, including tax considerations. With a Ccorporation, taxation may occur at both thecorporate and shareholder level; with an Scorporation, income and tax liabilities passthrough to the shareholders. Consult anattorney and tax professional.

Limited liability companies (LLCs) andpartnerships (LLPs and FLPs)

An LLC is a hybrid of a general partnershipand a corporation. Like a partnership, incomeand tax liabilities pass through to themembers, and the LLC is not double-taxed asa separate entity. And, like a corporation, anLLC is considered a separate legal entity thatcan be used to own business assets and incurdebt, protecting your personal assets fromother nontax claims against the LLC.

Professionals (e.g., doctors, lawyers, andaccountants) face liability for damages thatresult from the performance of theirprofessional duties. While no businessstructure will protect you from personal liabilityfor your professional activities, an LLP willprotect you from the professional mistakes ofyour partners. That is, if one of your partnersis sued, and the LLP is also named in thelawsuit, any malpractice judgment is thepersonal liability of the partner who's beensued, but a business liability for you and theother partners. Your personal assets aren't atstake if your partner commits malpractice,although your investment in the business maystill be at risk.

An FLP is a limited liability partnership formedby family members only. At least one familymember is a general partner; the others arelimited partners. A creditor can't obtain ajudgment against the FLP--it can only obtain acharging order. The charging order only allowsthe creditor to receive any income distributedby the general partner. It does not allow thecreditor access to the assets of the FLP. Thus,a charging order is not an attractive remedy tomost creditors. As a result, the limitation toseeking a charging order can often convince acreditor to settle on more reasonable termsthan might otherwise be possible.

Page 3 of 10, see disclaimer on final page

Protective trusts in general

A protective trust can protect both businessand personal assets from most creditors'claims. A trust works because it splitsownership of trust assets; the trustee hasequity ownership and the beneficiaries havebeneficial ownership. Essentially, a protectivetrust works like this:

Example: Harry would like to leave propertyto Wendy. However, Harry is afraid that hiscreditors might claim the property before hedies and that Wendy will receive none of it.Harry establishes a trust with both himself andWendy as the beneficiaries. The trustee isinstructed to allow Harry to receive incomefrom the trust until Harry dies and then todistribute the remaining assets to Wendy. Thetrust assets are then safe from being claimedby Harry's creditors, so long as the debt wasentered into after the trust's creation.

Under these circumstances, any of Harry'screditors would be able to reach assets in thetrust only to the extent of Harry's beneficialinterest in the trust. Say that Harry's interest inthe trust is a fixed income distribution eachmonth in the amount of $1,000. AssumingHarry's creditors obtained a judgment, theywould only be entitled to the $1,000 permonth.

Irrevocable trusts

As the name implies, an irrevocable trust is atrust that you can't revoke or change. Onceyou have established the trust, you can'tdissolve the trust, change the beneficiaries,remove assets from the trust, or change itsterms. In short, you lose control of the assetsonce they become part of the trust. But,because the assets are out of your control,they're generally beyond the reach of creditorstoo. You may further protect those assets fromyour beneficiaries' creditors by using speciallanguage (known as a spendthrift clause) inthe trust.

Caution: Unlike an irrevocable trust, arevocable trust provides the assets in the trustwith absolutely no legal protection from yourcreditors.

Offshore (foreign) trusts

It's possible to transfer assets to trusts that areformed in foreign countries (certain countriesare preferred). While the laws of each countryare different, they share one similarity--they

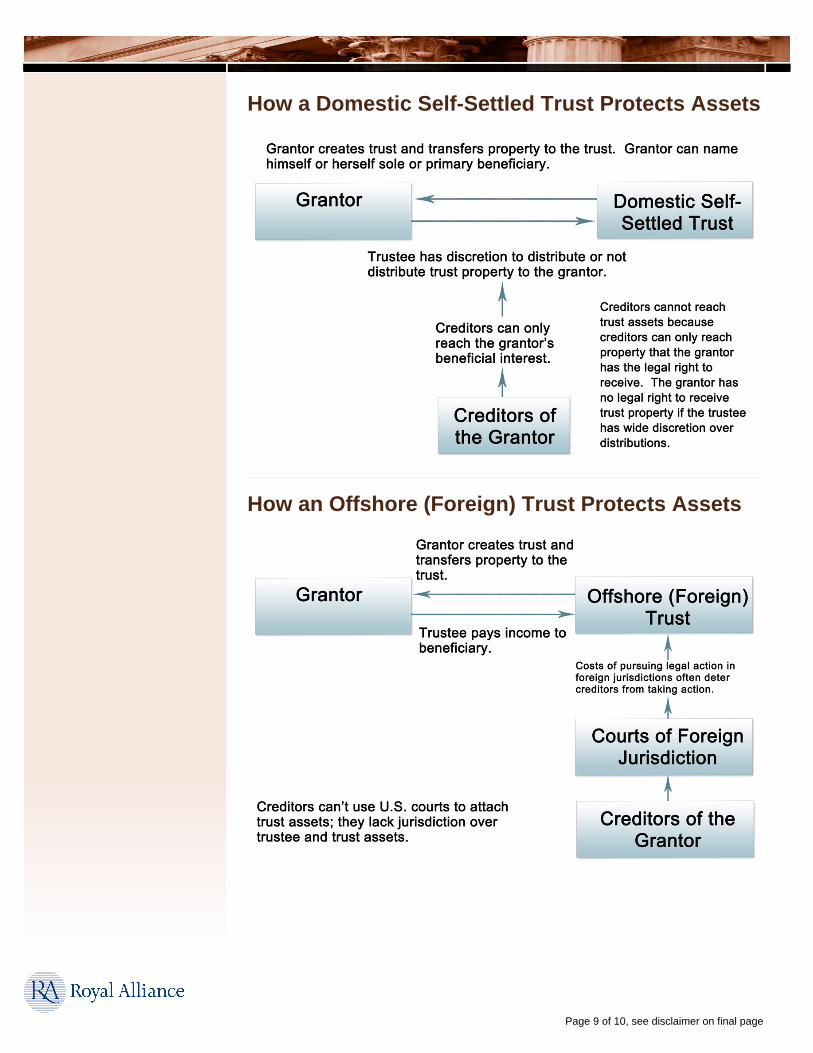

Here's how it works: In order for a creditor tobe able to reach assets held in a trust, a courtmust have jurisdiction over the trustee or thetrust assets. Where the trust is properlyestablished in a foreign country, obtainingjurisdiction over the trustee in a U.S. courtaction will not be possible. Thus, a U.S. courtwill be unable to exert any of its powers overthe offshore trustee.

So, the creditor must commence the suit in theoffshore jurisdiction. The creditor can't use itsU.S. attorney; it must use a local attorney.Typically, a local attorney will not take thecase on a contingency fee basis. Therefore, ifa creditor wants to pursue litigation in theoffshore jurisdiction, it must be prepared topay the foreign attorney up front. To makematters even less convenient, manyjurisdictions require the creditor to post a bondor other surety to guarantee the payment ofany costs that the court may impose againstthe creditor if it is unsuccessful. Taken as awhole, these obstacles have the general effectof deterring creditors from pursuing action.

Domestic self-settled trusts

The laws in Alaska, Delaware, Nevada, and afew other states enable you to set up aself-settled trust. Alaska was the first state toenact such an anti-creditor trust act, andDelaware quickly followed. Hence, this type oftrust is often called an Alaska/Delaware trust(sometimes also referred to as a domesticasset protection trust, or DAPT). A self-settledtrust is a trust in which the person who createsthe trust (the grantor) can name himself orherself primary, or even sole, beneficiary.These trusts give the trustee wide latitude topay as much or as little of the trust assets toany or all of the eligible beneficiaries as thetrustee deems appropriate. The key to thistype of protective trust is that the trustee hasthe discretion to distribute or not distribute thetrust property. Creditors can only reachproperty that the beneficiary has the legal rightto receive. Therefore, the trust property willnot be considered the beneficiary's property,and any creditors of the beneficiary will beunable to reach it.

Caution: Domestic self-settled trusts may notbe as effective as a foreign trust, because ajudgment from an individual state must behonored by another state under the UnitedStates Constitution.

make it more difficult for creditors to reachtrust assets.

A protective trust canprotect both business andpersonal assets from mostcreditors' claims. A trustworks because it splitsownership of trust assets;the trustee has equityownership and thebeneficiaries have beneficialownership.

Page 4 of 10, see disclaimer on final page

State Homestead Laws

The origin of state homesteadlaws

The federal Homestead Act, which wasenacted in 1862, offered free 160-acre parcelsof land to anyone willing to settle on them.After five years, these "homesteaders" wouldbecome the owners of the land, as long ascertain conditions were met (such as buildinga house and living on the property). Thoughthis act was repealed in 1976, many stateshave enacted their own homestead laws. Ifyour state has one, it may protect some or allof the equity in your home against certaincreditor claims.

Caution: A homestead filing will protect yourhome from most debts (including judgments)that arise after the homestead becomeseffective. It generally will not protect a homefrom debts incurred before the homesteadstatus attaches.

Caution: While the homestead laws in somestates may substantially protect yourresidence from unsecured creditor claims,even through a bankruptcy filing, this is notalways the case. You should consult anattorney about the protection offered by yourstate's homestead laws and other assetprotection strategies.

What homestead laws do

State homestead laws vary widely from stateto state. Some offer property tax relief or otherspecific tax considerations to real estateowners. Generally speaking, however, moststate homestead laws allow you to exempt aspecified amount of the equity in yourhomestead property from attachment andseizure efforts by certain unsecured creditors.The intent of these laws is to ensure that youwon't be forced to sell your home if you'reotherwise unable to pay certain debts.

How to obtain protection

The process of acquiring homestead lawprotection varies from state to state. Somestates require you to live in the state for acertain length of time before you becomeeligible for homestead law protection. In a fewstates, coverage is automatic. In most states,however, someone who is named on the deedto the property and who lives there must file anotarized declaration of homestead form witha local government office, such as a registry ofdeeds.

Generally, the property you homestead mustbe property that you own and occupy as yourprimary residence. In most states, propertyeligible for homestead law protection includesa single-family or multifamily home (and itslot), a condominium unit, or a mobile home.

Protection limits

Homestead laws exempt from attachment acertain amount of the equity value in thehomestead property. A few states offerunlimited protection; in Florida, for example,the homestead law completely exempts amultimillion-dollar mansion's total value fromattachment by certain unsecured creditors.Most states, however, assign a limit to theamount of protection offered by theirhomestead laws. These limits vary widely. Forinstance, an individual homeowner inCalifornia may be eligible for only $75,000 inexemption protection, while the samehomeowner in Massachusetts would receive$500,000 in protection.

Example: You are a single individual, yourhome is valued at $450,000, and it carries amortgage lien of $200,000 against it. Yourequity is then $250,000 ($450,000 -$200,000). If you live in California, you mayuse the homestead law there to protect$75,000 of that equity, leaving $175,000unprotected. However, if you live inMassachusetts, your state's homesteaddeclaration exempts all $250,000 of yourequity from unsecured creditor attachment.

Homestead laws do not automatically preventa forced sale of your primary residence tosatisfy a creditor claim. In the example above,if you live in California, the sale of your homecould be forced to satisfy such a claim, sincethe creditor could be paid from the sale'sequity proceeds over and above the amountthe homestead law exempts from attachment.If you live in Massachusetts, however, thehomestead law would exempt up to $500,000of a sale's equity proceeds from attachment; inthis case, there would be no point in a creditorforcing a sale of the property to satisfy a claim.

Caution: If the equity value of your propertyincreases over time (as your mortgagebalance decreases and/or property valuesrise), it may exceed the exemption protectionallowed by your state's homestead law. In thatevent, should a forced sale occur to satisfy acreditor claim, the homestead law wouldprotect some, but not all, of the equity in yourhome.

Page 5 of 10, see disclaimer on final page

Some creditors are not subjectto homestead law protections

Homestead laws do not protect your homefrom all creditors. Generally, these lawsexempt a portion of the equity in your principalresidence from attachment by creditors towhom you owe unsecured debts (e.g., medicalbills, credit card balances, and personalloans), even if the creditor has obtained acourt judgment against you.

Other debts are simply not subject to theexemption protection homestead laws offer.These include:

• Mortgages, second mortgages, homeequity loans or lines of credit secured bythe property

• Mechanic's liens for labor and/or materialsprovided to construct, alter, improve, orrepair the property

• Federal, state, or local income taxes;property taxes; or other assessments

• Debts owed to government agencies, suchas federal student loans or state Medicaidliens

• Court-ordered support of a spouse or minorchildren

Homestead laws andbankruptcy

State homestead laws can profoundly affectwhether or not you may keep your home inbankruptcy. In bankruptcy, you are notrequired to surrender exempt property tosatisfy the claims of creditors. The federalgovernment allows individuals a $22,975 (asof April 1, 2013) exemption in bankruptcy forreal estate used as a primary residence. Thisfederal exemption can vary significantly fromwhat you may be allowed to keep under yourstate's exemption laws.

Some states require you to follow theirexemption laws when filing for bankruptcy. Insuch cases, you'll have no choice about theamount of your home exemption; you'll beable to keep what your state's homestead lawallows. Other states allow you to choosebetween the federal and state exemption laws.In states where you have a choice, yourdecision about how to file for bankruptcy mayturn in part on which set of rules allows you tokeep the greatest amount of your home'svalue. In such cases, if your state homesteadlaw allows a more liberal home exemptionthan the one allowed by the federal law, filingfor bankruptcy under the state exemption lawsmay increase the probability that you'll keep

your home, particularly if you have substantialequity in it.

Example: Jimmy, a single individual, lives instate X, where he owns a modest homevalued at $100,000. When he files for Chapter7 bankruptcy against $97,000 in unsecureddebt, he is required to do so under the state Xexemption laws, which allow him to keep ahomestead worth only $5,000. Since the valueof his home exceeds that amount, he must sellhis home, keep $5,000 of the sale proceedsas allowed by the state exemption laws, anddistribute the remainder to the creditorsnamed in his bankruptcy petition to partiallysatisfy their claims.

Meanwhile, George, a single individual, livesin Texas, where he owns a ranch valued at$750,000. When he files for Chapter 7bankruptcy against $325,000 in unsecureddebt, he is allowed to elect either the federalor the state exemption laws. Since Texashomestead law exempts a residence ofunlimited value, George chooses to file underthe state exemption laws. He is not required tosell his ranch to raise money to satisfy thecreditors named in his bankruptcy petition.

For bankruptcy filings made on or after April20, 2005, the Bankruptcy Abuse Preventionand Consumer Protection Act of 2005imposes certain restrictions on statehomestead exemptions.

• Even if your state allows for a largerexemption, you may only exempt up to$155,675 (as of April 1, 2013) if youacquired your home within the 1,215-dayperiod (about 3 years, 4 months) prior tofiling bankruptcy. This limit does not applyto equity you rolled over from one home toanother within the same state during thisperiod.

• If you made an addition to your home in the10-year period prior to filing with the intentto hinder, delay, or defraud creditors, yourallowable exemption is reduced by thevalue of the addition.

• An absolute cap of $155,675 applies if you(a) have been convicted of a felony thatdemonstrates that the bankruptcy is"abusive," or (b) owe a debt arising fromviolations of securities laws, fiduciary fraud,racketeering, or crimes or intentional tortsthat caused death or serious bodily injury inthe preceding five years. This provision,however, will not apply if the homestead isreasonably necessary for your support andthe support of your dependents.

A Note of Caution

For bankruptcy filings made onor after October 17, 2005,there is a two-year residencyrequirement for using statehomestead exemptions.Specifically, to use a state'sexemption, you must haveresided there for 730 days(about 2 years) prior to filingbankruptcy. If you resided inmore than one state during this730-day period, the governingexemption law will be the statein which you resided for themajority of the 180-day period(about 6 months) preceding the730-day period.

Page 6 of 10, see disclaimer on final page

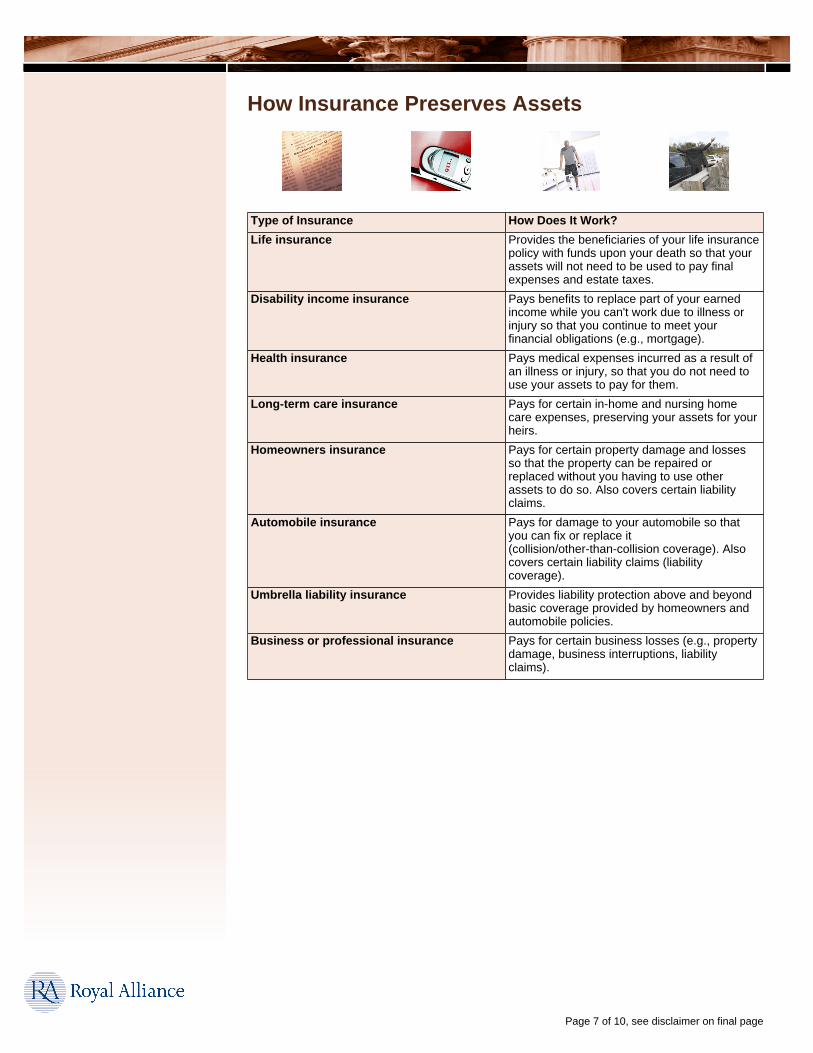

How Insurance Preserves Assets

Type of Insurance How Does It Work?

Life insurance Provides the beneficiaries of your life insurancepolicy with funds upon your death so that yourassets will not need to be used to pay finalexpenses and estate taxes.

Disability income insurance Pays benefits to replace part of your earnedincome while you can't work due to illness orinjury so that you continue to meet yourfinancial obligations (e.g., mortgage).

Health insurance Pays medical expenses incurred as a result ofan illness or injury, so that you do not need touse your assets to pay for them.

Long-term care insurance Pays for certain in-home and nursing homecare expenses, preserving your assets for yourheirs.

Homeowners insurance Pays for certain property damage and lossesso that the property can be repaired orreplaced without you having to use otherassets to do so. Also covers certain liabilityclaims.

Automobile insurance Pays for damage to your automobile so thatyou can fix or replace it(collision/other-than-collision coverage). Alsocovers certain liability claims (liabilitycoverage).

Umbrella liability insurance Provides liability protection above and beyondbasic coverage provided by homeowners andautomobile policies.

Business or professional insurance Pays for certain business losses (e.g., propertydamage, business interruptions, liabilityclaims).

Page 7 of 10, see disclaimer on final page

How Corporations, Limited Liability Companies,and Limited Liability Partnerships ProtectPersonal Assets

How an Irrevocable Trust Protects Assets

Page 8 of 10, see disclaimer on final page

How a Domestic Self-Settled Trust Protects Assets

How an Offshore (Foreign) Trust Protects Assets

Page 9 of 10, see disclaimer on final page

Miles B. Kessler, CFP®Investment Representative

870 Kipling StreetSuite A

Lakewood, CO 80215-5826Direct: 303-290-8942

Branch: [email protected]

January 28, 2016Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2016

Specializing in benefits and retirement strategies for Federal employees.Personalized financial services designed to meet your individual needs and objectives.

Securities and investment advisory services offered through Royal Alliance Associates, Inc., memberFINRA/SIPC and a registered investment advisor. Insurance services offered through Kessler & Associates,Inc., which is not affiliated with Royal Alliance Associates, Inc.

This message and any attachments hereto contain information that is confidential and is intended foruse only by the addressee. If you are not the intended recipient, or the employee or agent of the intendedrecipient responsible for delivering the message, you are notified that any review, copying, distribution oruse of this transmission is strictly prohibited. If you have received this transmission in error, please notify thesender immediately by email or telephone and destroy all copies of this message.

Page 10 of 10