foreign contribution (regulation) act, … contribution (regulation) act, 2010 (as applicable to...

TRANSCRIPT

FOREIGN CONTRIBUTION (REGULATION) ACT, 2010

(as applicable to Charitable Institutions)

by

CA Rajesh Kadakia

Half Day Workshop on Charitable Trusts

Organized jointly by BCAS & CTC

Mumbai

13th February, 2015

13-02-2015 Foreign Contribution (Regulation) Act, 2010 2

Synopsis

1. Introduction

2. Meaning of charitable institution for FCRA

3. Receipt of contributions by charitable institution – When is FCRA applicable?

4. Foreign source

5. Foreign contribution

6. Registration with the Central Government

7. Prior permission from Central Government

8. Post registration / prior permission

9. Renewal of registration

13-02-2015 Foreign Contribution (Regulation) Act, 2010 3

Introduction

1. Foreign Contribution (Regulation) Act, 1976

2. Foreign Contribution (Regulation) Act, 2010 (FCRA)

3. Purpose

To regulate acceptance and utilization of foreign contribution … by certain … associations or companies and to prohibit acceptance and utilization of foreign contribution … for any activities detrimental to the national interest... (Preamble to FCRA)

4. Interpretation of FCRA:

(a) FAQs on FCRA(b) Rules and Forms

13-02-2015 Foreign Contribution (Regulation) Act, 2010 4

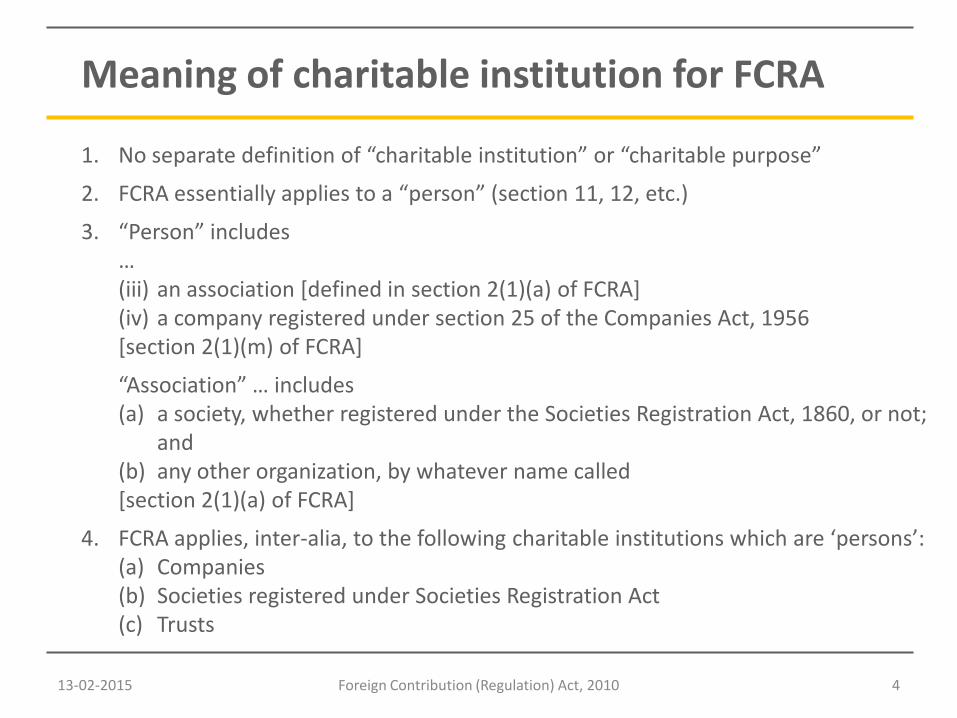

Meaning of charitable institution for FCRA

1. No separate definition of “charitable institution” or “charitable purpose”

2. FCRA essentially applies to a “person” (section 11, 12, etc.)

3. “Person” includes …(iii) an association [defined in section 2(1)(a) of FCRA](iv) a company registered under section 25 of the Companies Act, 1956[section 2(1)(m) of FCRA]

“Association” … includes(a) a society, whether registered under the Societies Registration Act, 1860, or not;

and(b) any other organization, by whatever name called [section 2(1)(a) of FCRA]

4. FCRA applies, inter-alia, to the following charitable institutions which are ‘persons’:(a) Companies(b) Societies registered under Societies Registration Act(c) Trusts

13-02-2015 Foreign Contribution (Regulation) Act, 2010 5

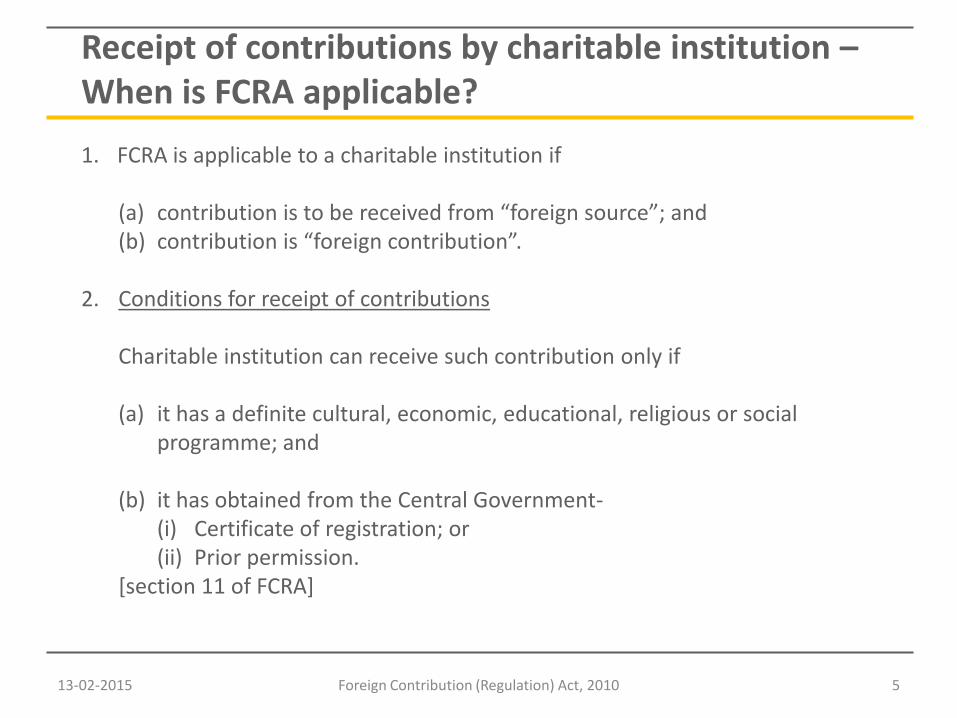

Receipt of contributions by charitable institution –When is FCRA applicable?

1. FCRA is applicable to a charitable institution if

(a) contribution is to be received from “foreign source”; and(b) contribution is “foreign contribution”.

2. Conditions for receipt of contributions

Charitable institution can receive such contribution only if

(a) it has a definite cultural, economic, educational, religious or social programme; and

(b) it has obtained from the Central Government-(i) Certificate of registration; or(ii) Prior permission.

[section 11 of FCRA]

13-02-2015 Foreign Contribution (Regulation) Act, 2010 6

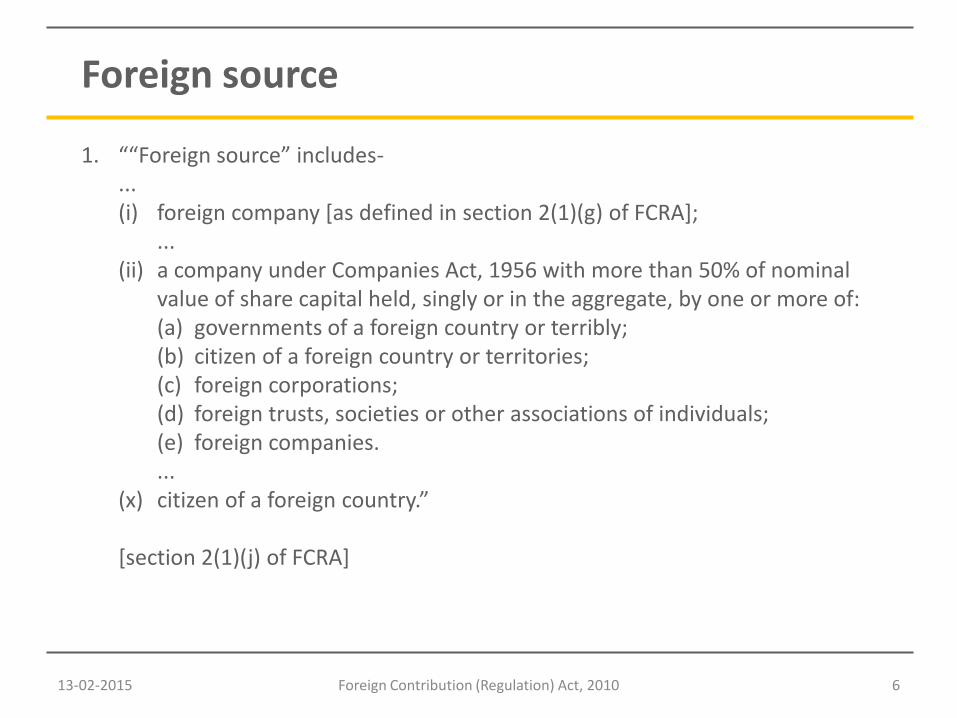

Foreign source

1. ““Foreign source” includes-...(i) foreign company [as defined in section 2(1)(g) of FCRA];

...(ii) a company under Companies Act, 1956 with more than 50% of nominal

value of share capital held, singly or in the aggregate, by one or more of:(a) governments of a foreign country or terribly;(b) citizen of a foreign country or territories;(c) foreign corporations;(d) foreign trusts, societies or other associations of individuals;(e) foreign companies....

(x) citizen of a foreign country.”

[section 2(1)(j) of FCRA]

13-02-2015 Foreign Contribution (Regulation) Act, 2010 7

Foreign source (cont.)

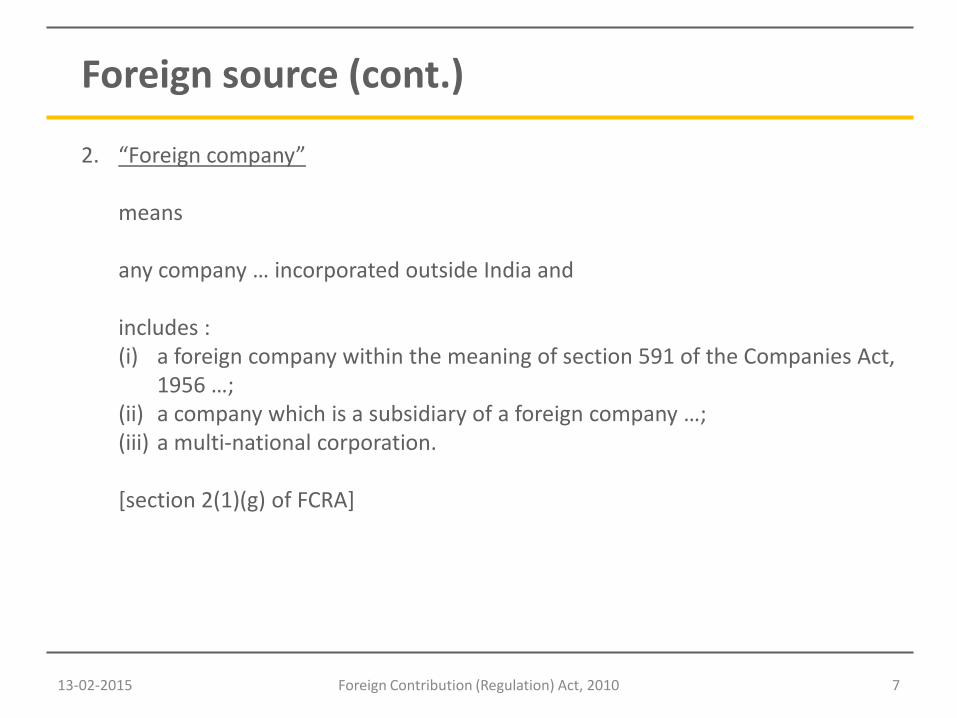

2. “Foreign company”

means

any company … incorporated outside India and

includes :(i) a foreign company within the meaning of section 591 of the Companies Act,

1956 …;(ii) a company which is a subsidiary of a foreign company …;(iii) a multi-national corporation.

[section 2(1)(g) of FCRA]

13-02-2015 Foreign Contribution (Regulation) Act, 2010 8

Foreign source (cont.)

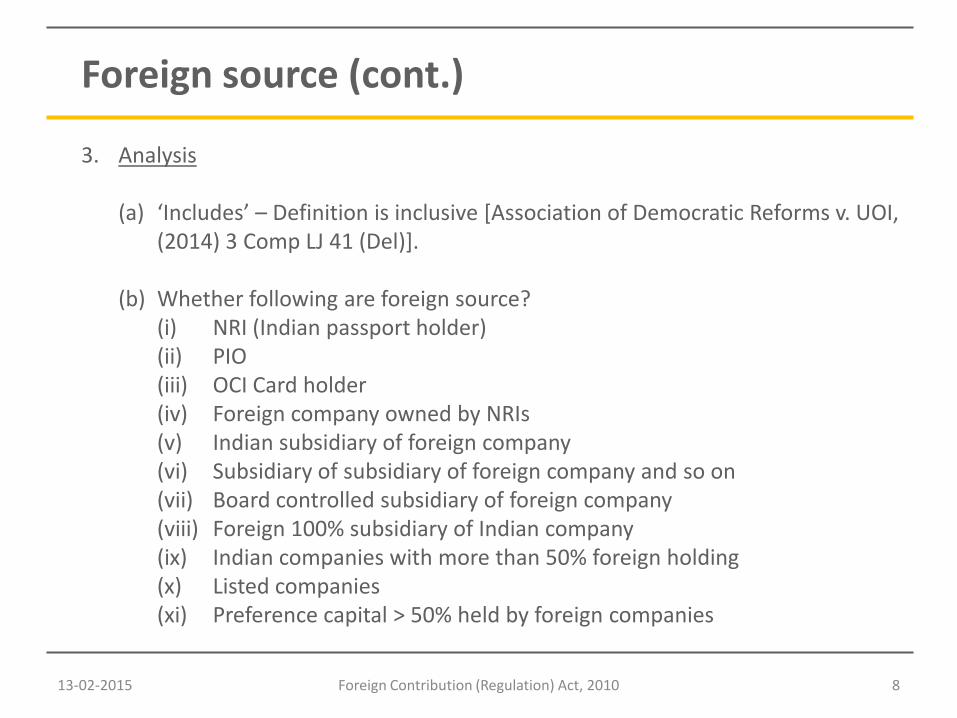

3. Analysis

(a) ‘Includes’ – Definition is inclusive [Association of Democratic Reforms v. UOI, (2014) 3 Comp LJ 41 (Del)].

(b) Whether following are foreign source?(i) NRI (Indian passport holder)(ii) PIO(iii) OCI Card holder(iv) Foreign company owned by NRIs(v) Indian subsidiary of foreign company(vi) Subsidiary of subsidiary of foreign company and so on(vii) Board controlled subsidiary of foreign company(viii) Foreign 100% subsidiary of Indian company (ix) Indian companies with more than 50% foreign holding (x) Listed companies(xi) Preference capital > 50% held by foreign companies

13-02-2015 Foreign Contribution (Regulation) Act, 2010 9

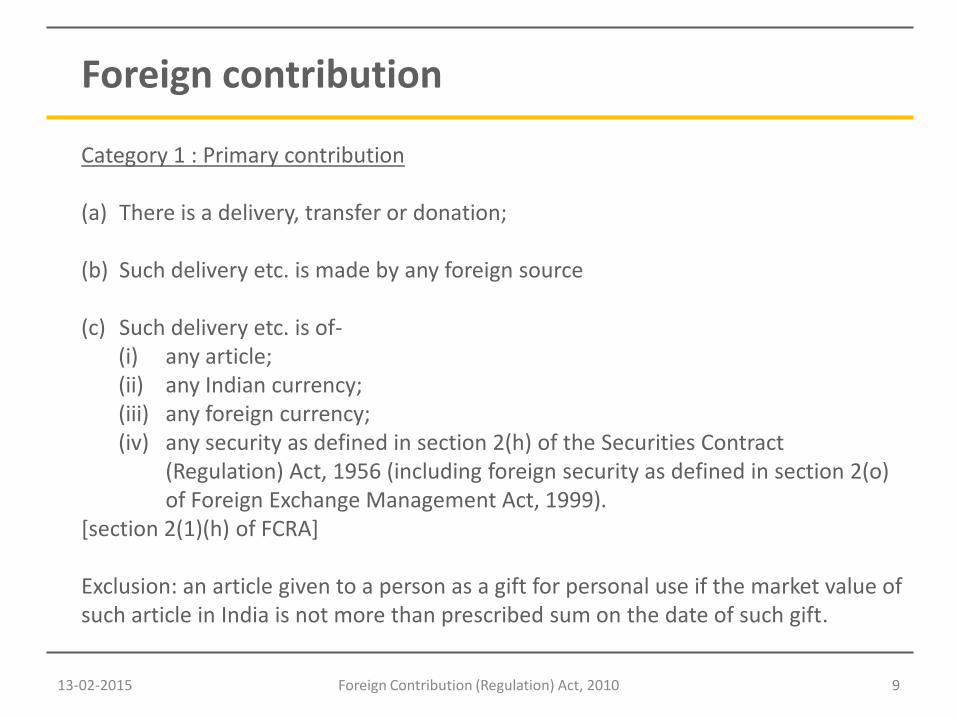

Foreign contribution

Category 1 : Primary contribution

(a) There is a delivery, transfer or donation;

(b) Such delivery etc. is made by any foreign source

(c) Such delivery etc. is of-(i) any article;(ii) any Indian currency; (iii) any foreign currency;(iv) any security as defined in section 2(h) of the Securities Contract

(Regulation) Act, 1956 (including foreign security as defined in section 2(o) of Foreign Exchange Management Act, 1999).

[section 2(1)(h) of FCRA]

Exclusion: an article given to a person as a gift for personal use if the market value of such article in India is not more than prescribed sum on the date of such gift.

13-02-2015 Foreign Contribution (Regulation) Act, 2010 10

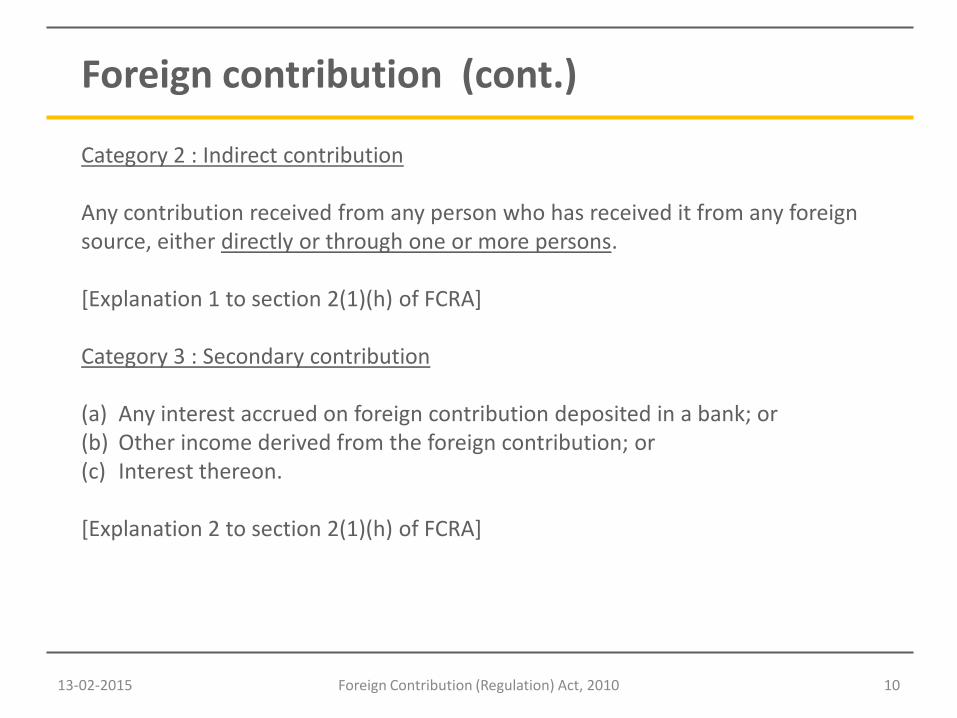

Foreign contribution (cont.)

Category 2 : Indirect contribution

Any contribution received from any person who has received it from any foreign source, either directly or through one or more persons.

[Explanation 1 to section 2(1)(h) of FCRA]

Category 3 : Secondary contribution

(a) Any interest accrued on foreign contribution deposited in a bank; or (b) Other income derived from the foreign contribution; or(c) Interest thereon.

[Explanation 2 to section 2(1)(h) of FCRA]

13-02-2015 Foreign Contribution (Regulation) Act, 2010 11

Foreign contribution (cont.)

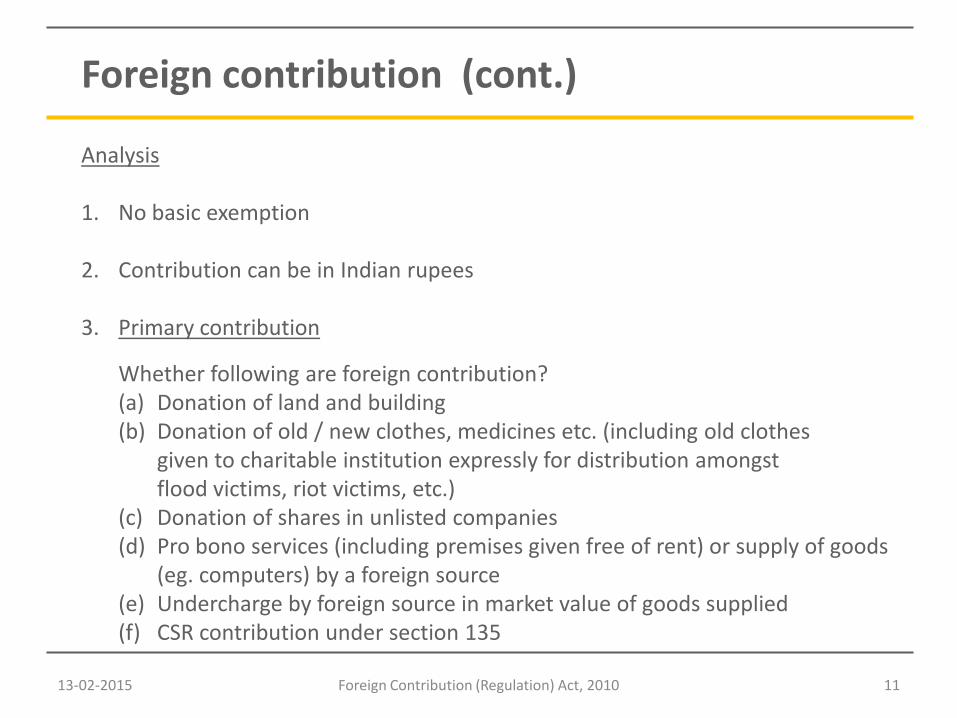

Analysis

1. No basic exemption

2. Contribution can be in Indian rupees

3. Primary contribution

Whether following are foreign contribution?(a) Donation of land and building(b) Donation of old / new clothes, medicines etc. (including old clothes

given to charitable institution expressly for distribution amongst flood victims, riot victims, etc.)

(c) Donation of shares in unlisted companies(d) Pro bono services (including premises given free of rent) or supply of goods

(eg. computers) by a foreign source(e) Undercharge by foreign source in market value of goods supplied(f) CSR contribution under section 135

13-02-2015 Foreign Contribution (Regulation) Act, 2010 12

Foreign contribution (cont.)

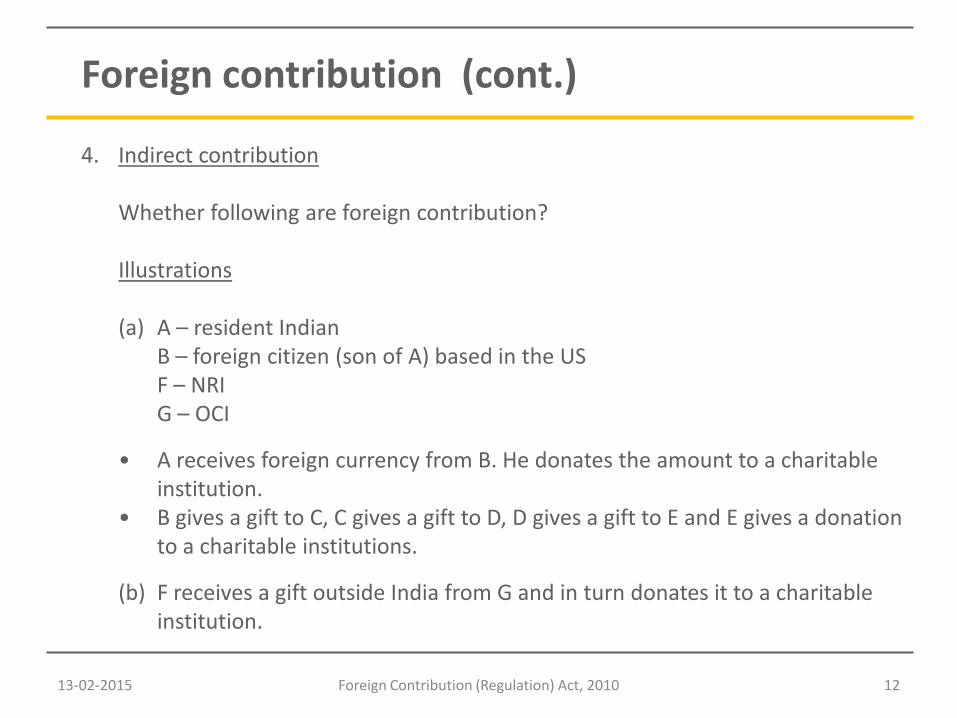

4. Indirect contribution

Whether following are foreign contribution?

Illustrations

(a) A – resident IndianB – foreign citizen (son of A) based in the USF – NRI G – OCI

• A receives foreign currency from B. He donates the amount to a charitable institution.

• B gives a gift to C, C gives a gift to D, D gives a gift to E and E gives a donation to a charitable institutions.

(b) F receives a gift outside India from G and in turn donates it to a charitable institution.

13-02-2015 Foreign Contribution (Regulation) Act, 2010 13

Foreign contribution (cont.)

5. Secondary contribution

What is the meaning of “income derived from any foreign contribution” in Explanation 2 of section 2(1)(h) of FCRA?

13-02-2015 Foreign Contribution (Regulation) Act, 2010 14

Foreign contribution (cont.)

Excluded contribution

1. Receipt of fees in India (including fees charged from foreign student)

2. Receipt towards cost in lieu of goods of services rendered by charitable institution in the ordinary course of its business, trade or commerce

3. Contribution received from an agent of a foreign source towards 1. or 2. above.

[Explanation 3 to section 2(1)(h) of FCRA]

13-02-2015 Foreign Contribution (Regulation) Act, 2010 15

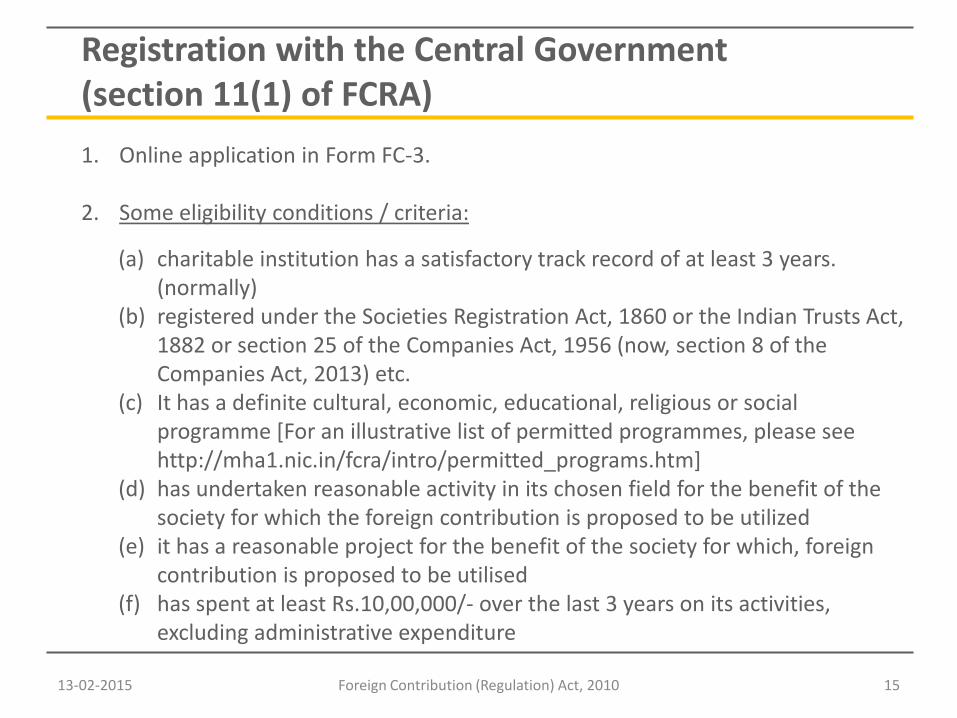

Registration with the Central Government(section 11(1) of FCRA)

1. Online application in Form FC-3.

2. Some eligibility conditions / criteria:

(a) charitable institution has a satisfactory track record of at least 3 years. (normally)

(b) registered under the Societies Registration Act, 1860 or the Indian Trusts Act, 1882 or section 25 of the Companies Act, 1956 (now, section 8 of the Companies Act, 2013) etc.

(c) It has a definite cultural, economic, educational, religious or social programme [For an illustrative list of permitted programmes, please see http://mha1.nic.in/fcra/intro/permitted_programs.htm]

(d) has undertaken reasonable activity in its chosen field for the benefit of the society for which the foreign contribution is proposed to be utilized

(e) it has a reasonable project for the benefit of the society for which, foreign contribution is proposed to be utilised

(f) has spent at least Rs.10,00,000/- over the last 3 years on its activities, excluding administrative expenditure

13-02-2015 Foreign Contribution (Regulation) Act, 2010 16

Registration with the Central Government(section 11(1) of FCRA) (cont.)

(f) does not have any office bearer who is a foreign national of non-Indian origin*

(g) It (or any of its office bearers) is not prosecuted or convicted for creating communal tension or disharmony, conversion, etc. ;

(h) the acceptance of foreign contribution by the charitable institution is not likely to affect prejudicially – the sovereignty and integrity of India, religious harmony, etc.

[Section 12(4) of FCRA; FAQs on FCRA; Form FC-3]

3. Statutory time limit for registration : 90 days, extendable after communication [section 12(3) of FCRA]

* relaxation made on a case to case basis.

13-02-2015 Foreign Contribution (Regulation) Act, 2010 17

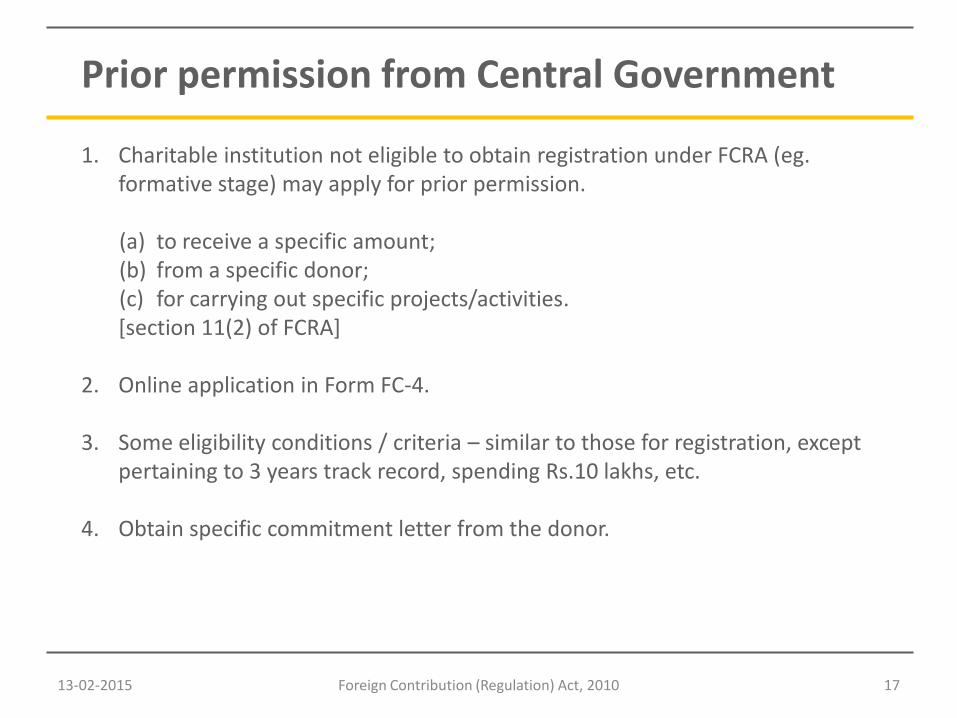

Prior permission from Central Government

1. Charitable institution not eligible to obtain registration under FCRA (eg. formative stage) may apply for prior permission.

(a) to receive a specific amount;(b) from a specific donor;(c) for carrying out specific projects/activities.[section 11(2) of FCRA]

2. Online application in Form FC-4.

3. Some eligibility conditions / criteria – similar to those for registration, except pertaining to 3 years track record, spending Rs.10 lakhs, etc.

4. Obtain specific commitment letter from the donor.

13-02-2015 Foreign Contribution (Regulation) Act, 2010 18

Post registration / prior permission

1. Receipt in designated account

(a) Deposit of the foreign contribution in a single bank account exclusively designated and specified in the order of registration or prior permission [section 17(1) of FCRA].

(b) No funds other than such foreign contributions can be transferred into such bank account [section 17(1) of FCRA].

2. Utilisation

(a) Utilisation only for the purposes for which the contribution has been received [section 8(1)(a) of FCRA].

(b) Institution has to be engaged in reasonable activity in its chosen field for the benefit of the society for two consecutive years [section 14(1)(e) of FCRA].

13-02-2015 Foreign Contribution (Regulation) Act, 2010 19

Post registration / prior permission (cont.)

3. Prohibition against investment / use for speculative activities

(a) Foreign contribution cannot be invested in any speculative business or activities [section 8(1)(a) of FCRA].

(b) Activities treated as speculative activities:(i) any activity or investment that has an element of risk of appreciation or

depreciation of the original investment linked to market forces including investment in mutual funds or shares;

(ii) participation in any scheme that promises high returns like investment in chits or land or similar assets not directly linked to the declared aims and objectives of the charitable institution.

[rule 4 of FCR Rules]

(c) Exceptions(i) debt-based secure investments [rule 4(2) of FCR Rules];(ii) fixed deposits in any bank or government approved financial institution[Question No. 17 of FAQs on FCRA]

13-02-2015 Foreign Contribution (Regulation) Act, 2010 20

Post registration / prior permission (cont.)

4. Register of investments

Every charitable institution must maintain a separate register of investments and submit it for audit (rule 4 of FCR Rules).

5. Restriction on utilisation of foreign contribution for administrative purpose

(a) Only up to 50% of foreign contribution received during a financial year can be used to meet administrative expenses.To defray more than 50%, prior approval of the Central Government is required [section 8(1)(b) of FCRA].

(b) Administrative expenses (see rule 5 of FCR Rules).(c) Some exclusions:

(i) Expenses incurred directly in furtherance of the objectives of the welfare oriented organization (such as salaries to doctors of hospital, salaries to teachers of school, etc.)

(ii) Interest paid to bank, bank charges, hospitality, etc.[rule 5 of FCR Rules]

13-02-2015 Foreign Contribution (Regulation) Act, 2010 21

Post registration / prior permission (cont.)

6. Transfer to another institution

A charitable institution is allowed to transfer the foreign donations to another charitable institution.

Situation 1: Recipient has obtained registration / prior permission

Transfer only if :

(a) Recipient has not been proceeded against under any provisions of the FCRA (It would be advisable to obtain a written undertaking from the recipient organization).

(b) The Central Government approves the transfer after application by Donor in Form FC-10;

(c) The amount of foreign contribution is reflected by the donor charitable institution in Form FC-6.

13-02-2015 Foreign Contribution (Regulation) Act, 2010 22

Post registration / prior permission (cont.)

Situation 2: Recipient has not obtained registration / prior permission

Transfer only if-

(a) The amount to be transferred ≤ 10% of total value of the foreign contribution received during the financial year;

(b) The donor makes application in Form FC-10, and gets it countersigned by the District Magistrate having jurisdiction in the place where the transferred funds are sought to be utilised;

(c) The Central Government approves the transfer;(d) The amount of foreign contribution is reflected in Form FC-6 as well as

Form-10.

(section 7 of FCRA; rule 24 of FCR Rules; FAQs on FCRA)

13-02-2015 Foreign Contribution (Regulation) Act, 2010 23

Post registration / prior permission (cont.)

7. Other matters requiring procedural compliance

(a) Change of members / trustees on governing body

Situation 1 - Change of members causing replacement of 50% or more of the members

(i) Prior permission of the Central Government required to replace the office-bearers.

(ii) Cannot accept any foreign contribution until• the permission to replace the office-bearers is granted; or• prior permission of the Central Government to receive contribution is

obtained.

Situation 2 - Change of members causing replacement of less than 50% of the members

Not required to obtain prior permission; advisable to intimate the Central Government about the change (Question 48 of FAQs on FCRA)

13-02-2015 Foreign Contribution (Regulation) Act, 2010 24

Post registration / prior permission (cont.)

(b) Change in name / address of charitable institution

Inform the Central Government within 30 days of such change in the prescribed form available on the Ministry’s website (Question 46 of FAQs on FCRA).

(c) Change in registration / nature / aims and objects of charitable institution

(i) inform the Central Government within 30 days of such change (‘Declaration and Undertaking’ given in the Application for registration in Form FC-3).

(ii) no prescribed form for such intimation.

(iii) reasonable to assume that the procedure to be followed would be similar to intimation in case of change of name / address.

13-02-2015 Foreign Contribution (Regulation) Act, 2010 25

Post registration / prior permission (cont.)

(d) Change in the designated bank / branch for receiving foreign contributions

(i) Charitable institution can change its designated bank / branch only after obtaining prior permission of the Central Government.

(ii) The reason for change of bank or branch of the bank has to be relevant and justifiable.

(iii) The charitable institution must apply to the Central Government in the prescribed form available on the website of Ministry of Home Affairs.

(Question 47 of FAQs on FCRA)

(e) Transfer to another bank account for utilisation:

(i) the other bank account is opened exclusively for the purpose of utilizing foreign contributions [section 17(1) of FCRA];

(ii) no funds other than such foreign contributions can be transferred into such bank account [section 17(1) of FCRA];

(iii) intimation to be sent to the Central Government within 15 days of the opening of such account [rule 9(1)(e) of FCR Rules].

13-02-2015 Foreign Contribution (Regulation) Act, 2010 26

Post registration / prior permission (cont.)

8. CA certificate

(a) Accounts to be audited by a Chartered Accountant.(b) Certificate from Chartered Accountant required in the format given in

Form FC-6.[rule 17(5) of FCR Rules]

9. Annual return

A charitable institution registered under FCRA is required to submit a report in Form FC-6 within 9 months of the closure of the financial year, i.e. by 31st

December each year [rule 17(1) of FCR Rules].

13-02-2015 Foreign Contribution (Regulation) Act, 2010 27

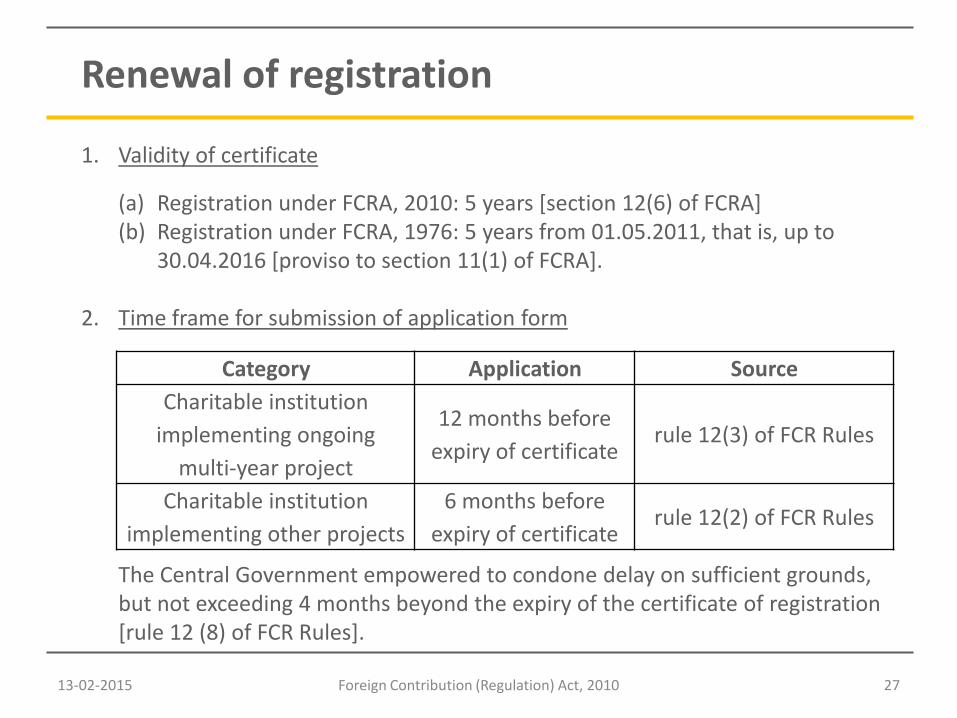

Renewal of registration

1. Validity of certificate

(a) Registration under FCRA, 2010: 5 years [section 12(6) of FCRA](b) Registration under FCRA, 1976: 5 years from 01.05.2011, that is, up to

30.04.2016 [proviso to section 11(1) of FCRA].

2. Time frame for submission of application form

Category Application Source

Charitable institution

implementing ongoing

multi-year project

12 months before

expiry of certificaterule 12(3) of FCR Rules

Charitable institution

implementing other projects

6 months before

expiry of certificaterule 12(2) of FCR Rules

The Central Government empowered to condone delay on sufficient grounds, but not exceeding 4 months beyond the expiry of the certificate of registration[rule 12 (8) of FCR Rules].

13-02-2015 Foreign Contribution (Regulation) Act, 2010 28

Renewal of registration (cont.)

3. Application to the Central Government in Form FC-5.

4. Time frame for granting renewal

Statutory time limit for registration : 90 days, extendable after communication [section 12(3) of FCRA]

13-02-2015 Foreign Contribution (Regulation) Act, 2010 29

“We know what aid from Country X means.It amounts in the end to X’s influence, if not X’s rule added to the British.”

- Mahatma Gandhi, Harijan, April 26, 1942

13-02-2015 Foreign Contribution (Regulation) Act, 2010 30

Thank You