foreign contribution regulation act ppt

TRANSCRIPT

1

WELCOME TO THE DISCUSSION ON

FOREIGN CONTRIBUTION (REGULATION) BILL 2010

1 MARK D' SOUZA & CO.

INTRODUCTION

• FCRA was enacted in 1976.

• The main purpose was to curb the use of foreign funds and hospitality for nefarious and anti-national purposes.

• FCRA is an internal security legislation and is not regulated by RBI.

• It is regulated by the Ministry of Home Affairs, Government of India.

2 MARK D' SOUZA & CO.

2

FOREIGN EXCHANGE MANAGEMENT ACT, 1999 - FEMA

• An Act to consolidate and amend the law

relating to foreign exchange

• with the objective of facilitating external trade and payments and

• for promoting the orderly development and maintenance of foreign exchange market in India

3 MARK D' SOUZA & CO.

Foreign Contribution Regulation Act, 1976

• An act to regulate the acceptance and utilization of foreign contribution or foreign hospitality by certain persons or associations,

• with a view to ensuring that parliamentary institutions, political associations and academic & other voluntary organizations as well as individuals working in the important areas of national life

• may function in a manner consistent with the values of a sovereign democratic republic, and for matters connected therewith or incidental thereto.

4 MARK D' SOUZA & CO.

3

Need for Foreign Contribution Regulation Act

• Regulating Foreign contribution meant for influencing elections or individuals or associations working in important areas of national life.

• Not meant to prohibit receipt of foreign contribution for genuine purposes.

• Security considerations.

5 MARK D' SOUZA & CO.

INTRODUCTION

• In 1985, FCRA was amended and certain important changes were made: (a) Funds received by subsequent recipient were brought under the purview of the act. (b) Definition of political parties was enlarged.

6 MARK D' SOUZA & CO.

4

INTRODUCTION

• (c) Section 6(1) was amended to ensure that foreign funds were received only after registration, and only through designated bank accounts.

• (d) Section 15A was inserted to empower Central Government to inspect and audit books of accounts of organisations.

• (e) Section 25A was inserted to ensure that acceptance of foreign funds was prohibited for 3 years after second conviction.

7 MARK D' SOUZA & CO.

INTRODUCTION

• The Foreign Contribution (Regulation) Bill 2010 has been passed by both houses of the Parliament recently.

• Now it awaits the assent from the President. .

• We discuss the main amendments and the implications thereof

8 MARK D' SOUZA & CO.

5

INTRODUCTION

• The inflow of foreign contribution through FCRA has increased from Rs. 24 crores in 1968 to Rs. Rs. 9,663.46 crore in 2008.

• The provisions of FCRA extends to the whole of India including the State of Jammu and Kashmir.

9 MARK D' SOUZA & CO.

Foreign Contribution

• Foreign contribution means the donation, delivery or transfer, made by any foreign source of any

• a) article, not given to a person as a gift, for personal use, if the market value in India of such article is not more than such sum as may be specified form time to time… ( words exceeds one thousand rupees are replaced)

• b) currency, whether Indian or foreign;

• c) foreign security as defined in clause 2(i) of the Foreign Exchange Regulation Act, 1973.

• NOTE : Contributions made by a citizen of India living in another country, from his personal savings, through the normal banking channels, is not treated as foreign contribution.

• It is advisable to obtain the passport details of the concerned citizen of India before accepting such contributions.

10 MARK D' SOUZA & CO.

6

Foreign Source

•Government of foreign country or any agency of such Government.

• International agencies, not being of

a) United Nations or its specialized agencies

b) World Bank

c) International Monetary Fund

d) Such other agencies as so notified by the Central Government.

11 MARK D' SOUZA & CO.

Foreign Source

• Foreign company or Corporation incorporated in foreign country

• Trade Union in a foreign country

• Foreign Trust or Foundation or Society or Club formed or registered outside India

• Company where more than half of shareholding held by foreign Govt., foreign citizens, foreign corporations

• Citizens of foreign countries

12 MARK D' SOUZA & CO.

7

Foreign Source …Contd

• The existing FCRA 1976 considers Indian companies, where more than 50% of equity is held by foreigners, as foreign source.

• For example : companies like ICICI Bank, Infosys etc. are foreign source and donations can not be accepted from them without FCRA registration.

• Unfortunately this provision has been retained in the proposed FCRA 2010, though the stated intent of the Government was to exclude such companies. This provision could be a drafting error and needs to be corrected

13 MARK D' SOUZA & CO.

Foreign Source …Contd • The FCRA 2010 has defined a foreign company under

clause (g) of Section 2, which does not include Indian Companies.

• This clause is apparently inserted to exclude Indian companies having more than 50% of Foreign equity holding.

• However section 2(j) which defines the term „foreign source‟ includes an Indian company under the category of foreign source if more than 50% of its equity is held by foreigners.

• Concern : Section 2(j)(vi) of the FCRA 2010 should have been amended to exclude Indian Companies.

14 MARK D' SOUZA & CO.

8

BUSINESS / CONSULTANCY INCOME OF AN NGO

• The definition of „foreign contribution‟ includes all kinds of foreign receipts. It does not distinguish between a commercial receipt or a voluntary contribution.

• This definition has largely been retained as per the existing FCRA 1976.

• However explanation 3 to section 2(h) excludes income from business, trade or commerce. This amendment was necessary but it comes with a lot of potent controversies and trouble for the NGOs.

15 MARK D' SOUZA & CO.

BUSINESS / CONSULTANCY INCOME OF AN NGO

• This section states that any fee or cost against business, trade or commerce shall not be considered as foreign contribution.

• In other words, such receipts can be treated as local income.

• However the problem is that this provision is in contradiction with the amended section 2(15) of the Income Tax Act which prohibits trade or business related receipts beyond Rs.10 lakh.

• Therefore, NGOs should be careful in treating consultancy income and other receipts as local income even though it is now permissible under the proposed Act.

16 MARK D' SOUZA & CO.

9

Who cannot accept Foreign Contribution

a) Candidate for elections.

b) Correspondents, columnists, cartoonists, editor, owner, printer.

c) Judge, Government servant or employee of any corporation

d) Member of any Legislature

e) Political party or office-bearer thereof.

17 MARK D' SOUZA & CO.

Who cannot accept Foreign Contribution

• it may be noted that the category of persons debarred from receiving foreign funds have been increased.

• The clause (f), (g) and (h) have been added by the FCRA 2010.

• (f) Organisation of a political nature.

• (g) Association or company engaged in broadcast of audio or visual news.

• (h) Correspondent, columnist etc. related with the company referred in clause (g)

• The above mentioned persons cannot receive foreign contribution subject to certain exceptions specified in section 4 which are as under:

18 MARK D' SOUZA & CO.

10

Who cannot accept Foreign Contribution

• salary, wages or remuneration for services rendered,

• Payment is received as an agent of a foreign source of organisation in relation to any transaction made by such foreign organisation with the central or state government.

• If the payment is received by way of gift or presentation as a part of any Indian delegation within the norms of acceptance described by Central Government.

• From his / her relative.

• By remittance under normal course under FEMA 1999.

• By way of Scholarship, stipend etc.”

19 MARK D' SOUZA & CO.

Does FCRA apply to commercial or business organization?

• Movement of foreign funds in the normal course of commerce and business is outside the purview of FCRA.

• Therefore, business organizations are not covered by FCRA 2010 also.

• However, the provision of Foreign Exchange Management Act, 1999, which is a financial legislation, would be applicable.

20 MARK D' SOUZA & CO.

11

RESTRICTION ON UTILISATION OF ADMINSTRATIVE EXPENSES

• Section 8 of FCRA 2010 provides that FC funds cannot be used for speculative business.

• The government will notify the meaning of speculative business through rules which are yet to be framed.

• Further section 8 also states that the administrative expenses shall not exceed 50%

• any expenditure of administrative nature in excess of 50% shall be defrayed with prior approval of the central government

21 MARK D' SOUZA & CO.

SUBSEQUENT RECEPIENT – TRANSFER OF FC FUNDS TO NON FC ORGNISATIONS

• Section 7 of FCRA 2010 provides that foreign contribution can be transferred only to those organisations which also possess FC registration or prior permission.

• Hence, it is not possible to transfer FC funds to non FC organisation.

• However the FCRA 2010 provides a clause wherein transfer to non FC organisation can be made with prior approval.

• The rules in this regard are to be framed.

22 MARK D' SOUZA & CO.

12

SUBSEQUENT RECEPIENT – TRANSFER OF FC FUNDS TO NON FC ORGNISATIONS

• The original idea was to exempt small CBOs and village level organisations from the vagaries of FCRA, as one can not expect small village level organisations to have FC registration.

• There is an urgent need to exempt CBOs and other village level organisations up to a certain limit, without any requirement of prior approval.

23 MARK D' SOUZA & CO.

Types of permission

• An association having a definite cultural, economic, educational, religious or social programme can receive foreign contribution .

• After it obtains the prior permission of the

Central Government, or gets itself registered

with the Central Government.

24 MARK D' SOUZA & CO.

13

Registration • Means permanent permission to accept foreign contribution from any

foreign source.

• Granted to associations with proven track record having definite cultural, economic, educational, religious, social programme.

Reasons for rejection of Registration Applications

• Association being in formative stage

• Association formed for personal gain

• Members of Executive Committee involved in illegal/criminal activities

• Sister association prohibited under the act

• Applicant association prohibited

• Association involved in anti-national activities

• Stated objects of the association not being pursued.

• Applicant having close links with another association with doubtful credentials

• Incomplete application.

25 MARK D' SOUZA & CO.

REGISTRATION - RENEWAL EVERY 5 YEARS

• The FCRA 2010 provides for renewal of registration of NGOs every 5 years.

• However, the Act has provided relief to all the existing NGOs for the first 5 years from the date of enactment.

• So, all existing NGOs have to renew their registration at the end of the period of 5 years from the date of enactment of FCRA 2010.

• As per Section 16 of the proposed Act, all NGOs should apply for renewal of the certificate within 6 months prior to the expiry of the five year period.

26 MARK D' SOUZA & CO.

14

RENEWAL OF REGISTRATION EVERY 5 YEARS – CONCERN

• This provision will create undue hardship to genuine NGOs and will perpetuate Inspector Raj, where every 5 years one has to manage the renewal.

• The Government probably should have kept only the defaulting NGOs under this category.

• The organisations which are already under scrutiny and assessment of the department on yearly basis and duly comply with the law, should not be subjected to yet another five yearly ritual.

27 MARK D' SOUZA & CO.

TIME LIMIT FOR PROCESSING THE APPLICATION FOR REGISTRATION

• There was no time limit mentioned under the FCRA 1976 either for granting or rejecting the application.

• FCRA 2010 provides that both regular registration and prior permission shall be granted or rejected within a period of 90 days from the date of receipt of application.

• The 90 days time limit is a very positive change.

• However, the Act is silent about the way forward if an order is not passed within 90 days.

• It is necessary that either a deemed permission or an redressal/appeal mechanism should be there within the FCRA Department if the application is not processed within 90 days.

28 MARK D' SOUZA & CO.

15

Prior Permission

When required

• Where the association does not have a FCRA registration

• Where the association is placed under prior permission category

• Where registration is frozen

• Associations of political nature, not being political party

Essentials of prior permission

• Donor specific

• Donee specific

• Amount specific – within overall limits

• Purpose specific

29 MARK D' SOUZA & CO.

No deemed Prior Permission

• FCRA 2010 provides that application for „prior permission‟ shall be granted or rejected within a period of 90 days from the date of receipt of application.

• It may be noted that under the FCRA 1976 there is a provision for deemed prior permission if the application is not processed within 120 days.

• The new FCRA 2010 does not have any provision of deemed prior permission.

• In other words, now onwards organisations, can not receive foreign funds in case of delay in processing of a „prior permission‟ application.

30 MARK D' SOUZA & CO.

16

QUESTIONABLE POWERS FOR REJECTING THE APPLICATION

• The FCRA 2010 has provided sweeping powers to the authorities for rejecting an application for prior permission or registration.

• Under Section 12 various strict conditions have been provided which include that the applicant should not have been prosecuted or convicted for indulging in activities aimed at conversion or creating communal tension.

• It may be noted that the word „prosecuted‟ has been used which implies that even if there is a false Court proceeding is pending, then also FCRA registration could be denied.

31 MARK D' SOUZA & CO.

QUESTIONABLE POWERS FOR REJECTING THE APPLICATION

• The power to deny FC registration or prior approval merely because some prosecution for any offence is pending seems very harsh, arbitrary and unconstitutional.

• Further FCRA 2010 also provides that in case of rejection the Central Government shall provide reasons in writing to the applicant.

• The reasons to be provided by the Central Government shall be restricted to the obligations as provided under Right to Information Act, 2005.

32 MARK D' SOUZA & CO.

17

POWER TO PROHIBIT SOURCES FORM WHICH FC CAN BE ACCEPTED

• The Act provides power to the Central Government under section 11(3)(iv) to notify such source(s) from which foreign contribution shall be accepted with prior permission only.

• It implies that the Central Govt. may notify specific donors or countries from which foreign funds could not be received or shall be received with prior permission only.

33 MARK D' SOUZA & CO.

POWER TO CANCEL REGISTRATION & NIL RETURNS

• The FCRA Department may cancel the certificate under Section 14 under various circumstances

• including lack of activity for a period of 2 years.

• now onwards NGOs cannot retain their FC registration just by filing NIL returns,

• because the registration certificate can be cancelled if there are no reasonable activities for a period of 2 years.

• The reasons for cancelling the certificate are :

34 MARK D' SOUZA & CO.

18

POWER TO CANCEL REGISTRATION & NIL RETURNS

• (i)Providing false information

• (ii) Violating the terms and conditions like filing of return, etc.

• (iii) Violating the Act or the Rules

• (iv) Acting against public interest

• (v) No reasonable activity for 2 years.

• Any person whose certificate has been cancelled shall not be eligible for registration or prior permission for a period of 3 years from the date of cancellation.

35 MARK D' SOUZA & CO.

POWER TO CANCEL REGISTRATION & NIL RETURNS -CONCERN

• The term “reasonable activity” has not been defined.

• It may so happen that an NGO may have activity from local sources.

• Therefore, it should be provided that reasonable activity whether from FC or local sources should be there for retaining FC registration.

36 MARK D' SOUZA & CO.

19

POWER TO MANGE FC AFTER CANCELLATION OF CERTIFICATE

• FCRA 2010 provides that after cancellation of registration certificate all the foreign contribution and assets thereof shall vest with such authority as may be prescribed.

• The government authorities shall take charge of the foreign contribution and the FC assets till the registration is restored.

• This seems to be a very harsh provision because it is open ended.

• Hence, FC assets created since the inception of the organisation can be implicated if the registration certificate is cancelled.

37 MARK D' SOUZA & CO.

POWER TO MANGE FC AFTER CANCELLATION OF CERTIFICATE -

CONCERN • The section 15 of the FCRA 2010 should be

supported by appropriate rules so that FC assets would not come under the purview of the Govt. authorities

• as it will create needless complications and controversies.

• The Government managing fixed assets created since inception will be practically not possible and would create hardship.

38 MARK D' SOUZA & CO.

20

MULTIPLE BANK ACCOUNTS

• Section 17 of FCRA 2010 provides that multiple bank accounts can be opened for the purposes of utilisation

• Provided only one bank account is maintained for receiving foreign contribution.

• This amendment provides a great relief to all the NGOs which were struggling under the arbitrary disallowance of multiple bank accounts under current FCRA.

39 MARK D' SOUZA & CO.

DISPOSAL OF FIXED ASSETS ON DISSOLUTION

• Section 22 of the FCRA 2010 provides that, in case of dissolution, the Central Govt. shall have the power to determine the process of disposal of FC assets.

• The Central Govt. may specify the manner and procedure in which such asset shall be disposed off.

40 MARK D' SOUZA & CO.

21

Must Do’s for the Registered Association

• Designated exclusive Bank account for receipt and utilization of foreign contribution.

• Submission of annual FC-3 returns.

• Change in members, home, address, objectives of the association to be reported to Central Government within 30 days.

• Change in the O.B‟s by 50% or more with prior permission only

• Exclusive accounts for utilisation of foreign contribution and audit by the Chartered Accountant.

• Exclusive accounts for receipt and utilization of foreign contribution .

• Substantial proportion of foreign contribution to be spent on welfare activities

• Reduction in Administrative expenses

41 MARK D' SOUZA & CO.

Penalties

• Prohibition

• Placing the association in prior permission category

• Fine

• Seizure/confiscation of the foreign contribution

• Imprisonment up to 5 years

42 MARK D' SOUZA & CO.

22

Role of Banks

• Prime source for receipt and utilization

• Can keep a watch over activities of doubtful associations

• Information about foreign contribution

• Not to allow receipt and utilization of foreign contribution without Registration or prior permission.

43 MARK D' SOUZA & CO.

ISSUES IN THE FUNCTIONING OF NGO‟S

Non-existent regulatory mechanism

Accountability

No perspective planning for NGO SECTOR

Proliferation of paper organisations

No National NGO policy

Comprehensive National Legislation Required

44 MARK D' SOUZA & CO.

23

STATISTICS

• A total of 34803 associations have been registered under the Foreign Contribution (Regulation) Act, 1976 up to 31.3.2008.

• During the year 2007-08, 866 associations were granted registration and 367 associations were granted prior permission to receive foreign contribution.

• 18796, associations reported a total receipt of foreign contribution of an amount of Rs. 9,663.46 crore. This includes Association which received Nil amount.

45 MARK D' SOUZA & CO.

STATISTICS • Among the States and Union Territories, the highest

receipt of foreign contribution was reported by Delhi (Rs. 1,716.57 crore), followed by Tamil Nadu (Rs 1,670.93 crore) and Andhra Pradesh (Rs 1,167.21 crore).

• Among the districts, the highest receipt of foreign contribution was reported by Chennai (Rs 731.22 crore), followed by Bangalore (Rs. 669.76 crore) and Mumbai (Rs. 469.90 crore).

• The list of donor countries is headed by the USA (Rs.2,928.30 crore) followed by UK (Rs. 1,268.59 crore) and Germany (Rs. 971.02 crore).

46 MARK D' SOUZA & CO.

24

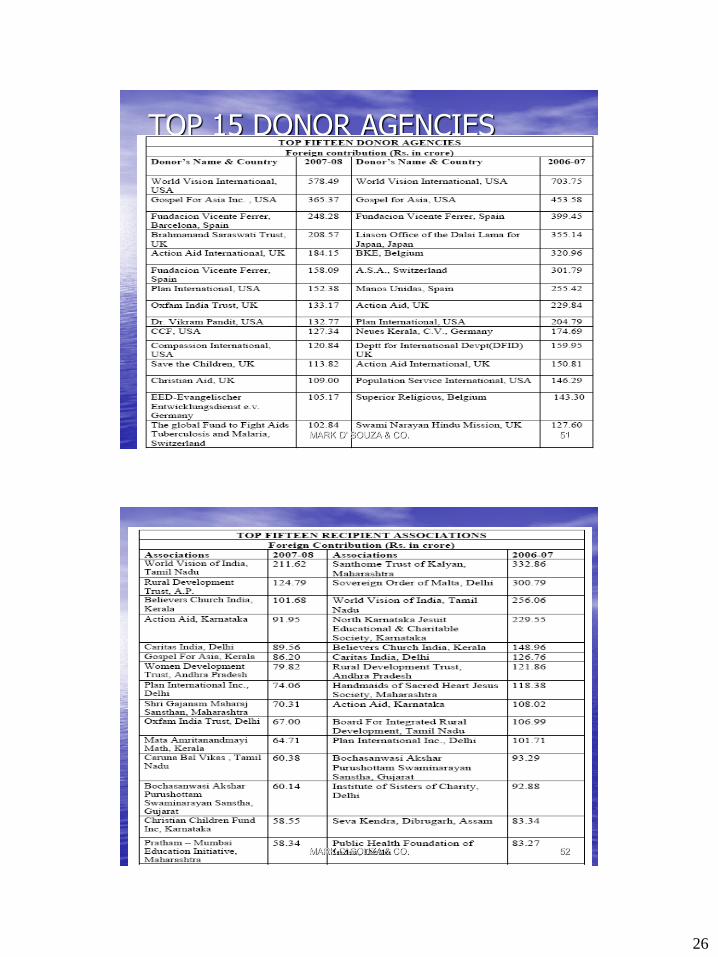

STATISTICS • The list of foreign donors is topped by World Vision

International, USA (Rs.578.49 crore) followed by Gospel For Asia Inc, USA (Rs. 365.37 crore) and Foundation Vicente Ferrer, Barcelona, Spain (Rs. 248.28 crore).

• Among the associations which reported receipt of foreign contribution, the highest amount of foreign contribution was received by World Vision of India, Chennai, Tamil Nadu (Rs. 211.62 crore), followed by Rural Development Trust, Ananthapur, A.P. (Rs.124.79 crore) and Believers Church India, Pathanamthitta, Kerala (Rs. 101.68 crore).

47 MARK D' SOUZA & CO.

STATISTICS • The highest amount of foreign contribution was received

and utilized for

• Establishment Expenses (Rs 3,421.95 crore),

• followed by Rural Development (Rs 1,781.38 crore),

• Relief/Rehabilitation of victims of natural calamities (Rs 1,689.08 crore),

• Welfare of Children (Rs 1,333.40 crore) and

• Construction and Maintenance of school/college (Rs 1,206.47 crore).

48 MARK D' SOUZA & CO.

25

NUMBER OF REGD. ASSOCIATIONS – 2007-08

49 MARK D' SOUZA & CO.

TOP 15 DONOER COUNTRIES -2007-08

50 MARK D' SOUZA & CO.

26

TOP 15 DONOR AGENCIES

51 MARK D' SOUZA & CO.

52 MARK D' SOUZA & CO.

27

53 MARK D' SOUZA & CO.