foreign exchange market - nov 2011

TRANSCRIPT

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 1/21

Foreign Exchange Market

Presented by

Mesia Ilomo

November 2011University of Dar es Salaam

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 2/21

Outline Of the Presentation

• Introduction to Foreign Exchange Market

• Characteristics of the Foreign Exchange

Market

• Types of Transactions in the Foreign Exchange

Market

• Participants in Foreign Exchange Market

• Quotation in the Foreign Exchange Market

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 3/21

Foreign Exchange Market: Introduction

The market where the commodity traded isCurrencies.

The market where one buys (or sells) the currency of countryA with (or for) the currency of country B

Price of each currency is determined in term of othercurrencies.

Major currencies of the World: USD, EURO, YEN andPOUND STERLING

A currency exchange rate – Is simply the ratio of a unit of currency of country A to a

unit of the currency of country B at the time of the buy orsell transaction

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 4/21

Foreign Exchange Market: Introduction

Currency conversion in the foreign exchange market

– Is necessary to complete private and commercialtransactions across borders

– A tourist needs to pay expenses on the road in localcurrency

–

A firm• Buys/sells goods and services in the other country’s local currency

• Uses the foreign exchange market to invest excess funds

Is used to speculate on currency movements

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 5/21

Foreign Exchange Market: Introduction

Minimizes foreign exchange risk (unpredictable rate

swings) There are different ways to trade currencies (spot

and forward)

The market is “open” 24 hours…

Arbitrage: buying low and selling high … given slightlydifferent exchange rate quotes in one location vsanother (e.g., London vs Tokyo)

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 6/21

Function of Foreign Exchange Market

The foreign exchange market is the mechanism

by which participants:

– transfer purchasing power between countries;

–

obtain or provide credit for international tradetransactions, and

– minimize exposure to the risks of exchange rate

changes.

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 7/21

Characteristics of Foreign Exchange Market

Largest of all financial markets with average

daily turnover of over $2 trillion!

66% of all foreign exchange transactionsinvolve cross-border counterparties.

London is the largest FX market.

US dollar involved in 87% of all transactions.

Telecommunication networks have a big role

to play in this market

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 8/21

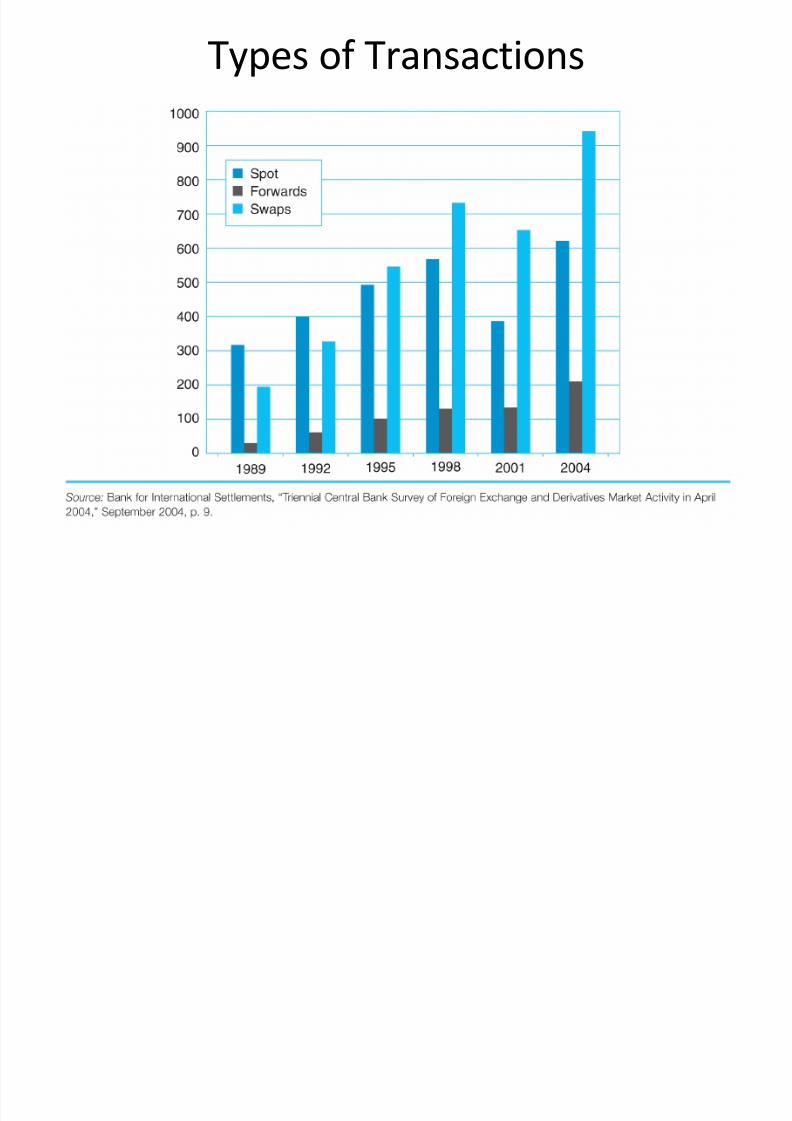

Types of Transactions

A Spot transaction in the interbank market is

the purchase of foreign exchange, with

delivery and payment between banks to take

place, normally, on the second followingbusiness day.

The date of settlement is referred to as the

value date.

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 9/21

Types of Transactions An outright forward transaction (usually called

just “forward”) requires delivery at a futurevalue date of a specified amount of onecurrency for a specified amount of anothercurrency.

The exchange rate is established at the time of the agreement, but payment and delivery arenot required until maturity.

Forward exchange rates are usually quoted forvalue dates of one, two, three, six and twelvemonths.

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 10/21

Types of Transactions

A swap transaction in the interbank market is thesimultaneous purchase and sale of a given amount of foreign exchange for two different value dates.

Both purchase and sale are conducted with the same

counterparty.

Some different types of swaps are:

spot against forward,

forward-forward,Also: nondeliverable forwards (NDF) … (forward contract

but settlement is done in USD).

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 11/21

Types of Transactions

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 12/21

Market Participants

The foreign exchange market consists of two tiers:

– the interbank or wholesale market (multiples of $1M US orequivalent in transaction size), and

–

the client or retail market (specific, smaller amounts).

Five broad categories of participants operate withinthese two tiers: bank and nonbank foreign exchange

dealers, individuals and firms, speculators andarbitragers, central banks and treasuries, and foreignexchange brokers.

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 13/21

Market Participants Banks and a few nonbank foreign exchange

dealers operate in both the interbank and clientmarkets.

They profit from buying foreign exchange at a“bid” price and reselling it at a slightly higher

“offer” or “ask” price. Dealers in the foreign exchange department of

large international banks often function as“market makers.”

These dealers stand willing at all times to buy andsell those currencies in which they specialize andthus maintain an “inventory” position in thosecurrencies.

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 14/21

Market Participants

Individuals (such as tourists) and firms (such

as importers, exporters and MNEs) conductcommercial and investment transactions inthe foreign exchange market.

Their use of the foreign exchange market isnecessary but nevertheless incidental to theirunderlying commercial or investmentpurpose.

Some of the participants use the market to“hedge” their foreign exchange risk.

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 15/21

Market Participants Speculators and arbitragers seek to profit from

trading in the market itself.

They operate in their own interest, without aneed or obligation to serve clients or ensure a

continuous market.

While dealers seek the bid/ask spread,speculators seek all the profit from exchange rate

changes and arbitragers try to profit fromsimultaneous exchange rate differences indifferent markets.

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 16/21

Market Participants Central banks and treasuries use the market to acquire

or spend their country’s foreign exchange reserves aswell as to influence the price at which their owncurrency is traded.

They may act to support the value of their owncurrency because of policies adopted at the nationallevel or because of commitments entered into through

membership in joint agreements such as the EuropeanMonetary System.

The motive is not to earn a profit as such, but rather toinfluence the foreign exchange value of their currencyin a manner that will benefit the interests of theircitizens.

As willing loss takers, central banks and treasuriesdiffer in motive from all other market participants.

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 17/21

Market Participants• Foreign Exchange Brokers ; these facilitate trading

between dealers without themselves becoming

principals in the transaction.

• They benefit in the form of commission

•

They maintain access to hundreds of dealers worldwidevia open telephone line

• It is their business to know at any point in time to know

which dealers wants to sell or buy any currency.

• They provide their client, the bank, with the informationabout the exchange rates at which banks are willing to

buy or sell a particular currency

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 18/21

Types of Activities

Speculation An activity that leaves one open to exchange rate

fluctuations where one aims to make a profit.

Hedging

Allows the firm to transfer exchange rate risk inherentin foreign currency transactions or positions.

Arbitrage – take advantage of inconsistent prices tomake risk-free profits. These profits are unlikely to

last long. Spatial (or Locational ) Arbitrage

Triangular Arbitrage

Covered Interest Arbitrage

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 19/21

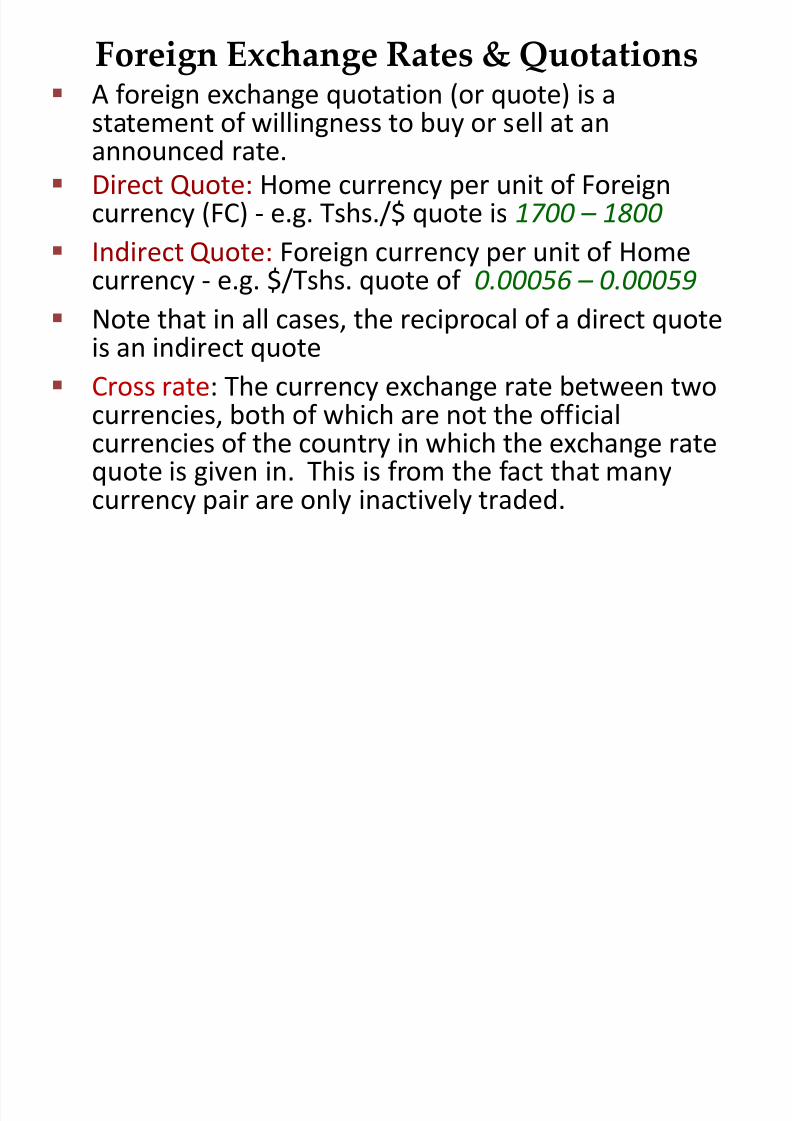

Foreign Exchange Rates & Quotations A foreign exchange quotation (or quote) is a

statement of willingness to buy or sell at anannounced rate.

Direct Quote: Home currency per unit of Foreigncurrency (FC) - e.g. Tshs./$ quote is 1700 – 1800

Indirect Quote: Foreign currency per unit of Home

currency - e.g. $/Tshs. quote of 0.00056–

0.00059 Note that in all cases, the reciprocal of a direct quote

is an indirect quote

Cross rate: The currency exchange rate between two

currencies, both of which are not the officialcurrencies of the country in which the exchange ratequote is given in. This is from the fact that manycurrency pair are only inactively traded.

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 20/21

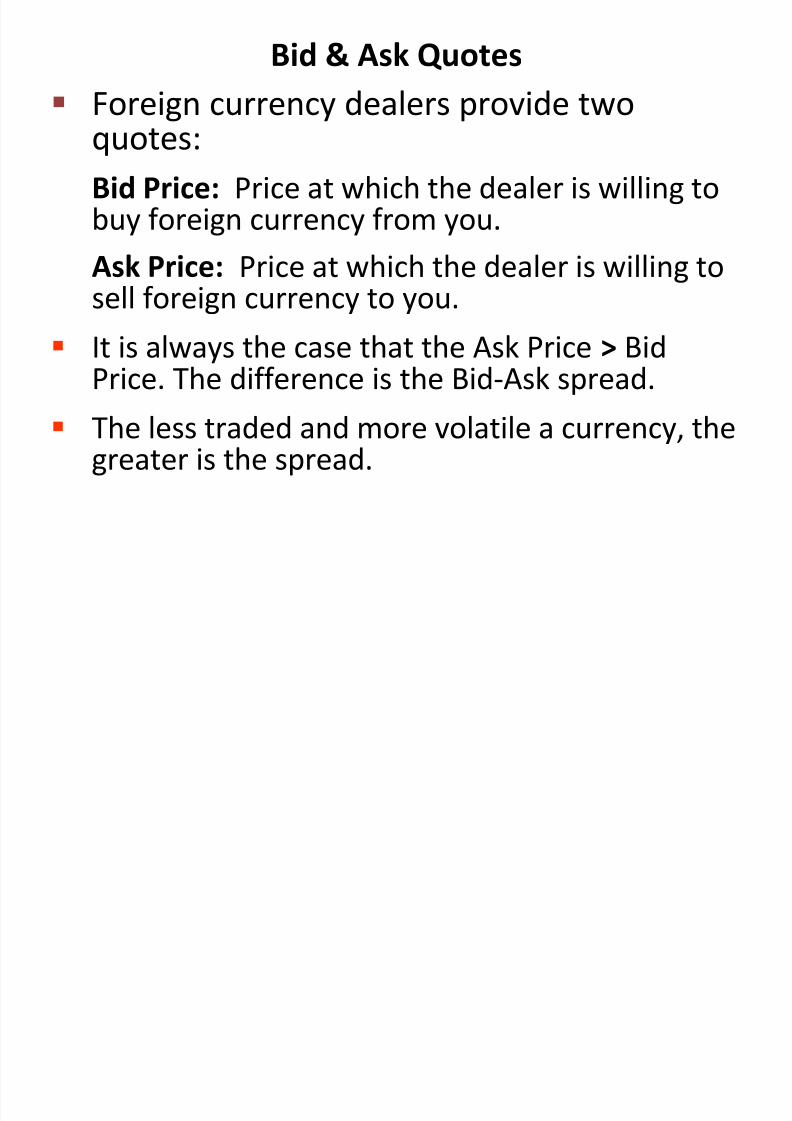

Bid & Ask Quotes

Foreign currency dealers provide two

quotes:Bid Price: Price at which the dealer is willing tobuy foreign currency from you.

Ask Price: Price at which the dealer is willing tosell foreign currency to you.

It is always the case that the Ask Price > BidPrice. The difference is the Bid-Ask spread.

The less traded and more volatile a currency, thegreater is the spread.

7/30/2019 Foreign Exchange Market - Nov 2011

http://slidepdf.com/reader/full/foreign-exchange-market-nov-2011 21/21

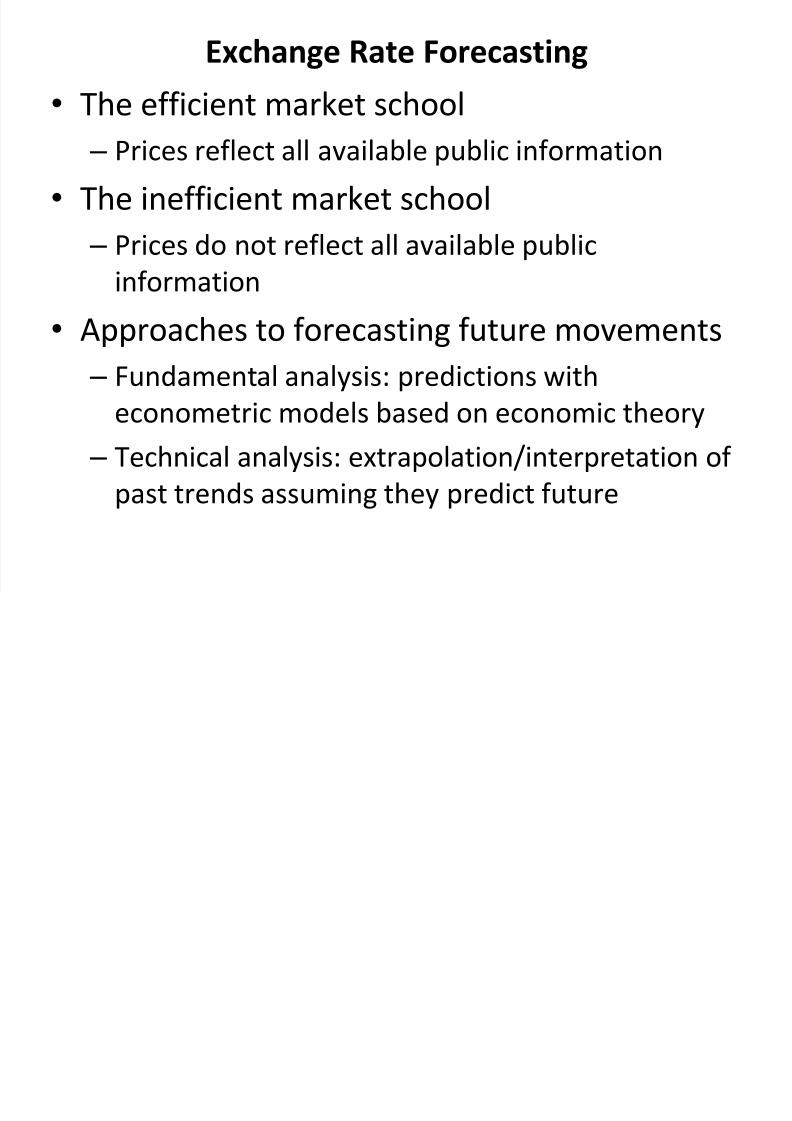

Exchange Rate Forecasting

• The efficient market school

– Prices reflect all available public information

• The inefficient market school

– Prices do not reflect all available public

information

• Approaches to forecasting future movements

– Fundamental analysis: predictions with

econometric models based on economic theory – Technical analysis: extrapolation/interpretation of

past trends assuming they predict future