foreign exchange risk management by swedish and...

TRANSCRIPT

Pacific-Basin Finance Journal 13 (2005) 343–366

www.elsevier.com/locate/econbase

Foreign exchange risk management by Swedish and

Korean nonfinancial firms: A comparative survey

Bengt Pramborg*

Stockholm University School of Business, SE-106 91 Stockholm, Sweden

Received 3 September 2003; accepted 23 April 2004

Available online 30 December 2004

Abstract

This study compares the hedging practices of Swedish and Korean nonfinancial firms. Our

findings suggest that the aim of hedging differed between firms in the two countries. Korean firms

mostly focused on reducing fluctuations in cash flows, while Swedish firms more commonly

emphasized reducing fluctuations of accounting numbers. The proportion of firms that used

derivatives was significantly lower in the Korean than in the Swedish sample, a finding that may

stem from the relative immaturity of the Korean derivatives markets. The evidence suggests that

Korean firms hedged as much as Swedish firms but substituted foreign debt for derivatives.

Furthermore, Korean firms appeared to be less rigorous than Swedish firms in overseeing risk

management activity. Finally, a large proportion of firms in both countries used a profit-based

approach to evaluating the risk management function.

D 2004 Elsevier B.V. All rights reserved.

JEL classification: F23; F31

Keywords: Hedging; Foreign exchange exposure; Risk management

1. Introduction

This paper uses survey evidence to compare Swedish and Korean firms’ foreign

exchange risk management practices. This is of interest because, as Lel’s (2003) findings

suggest, country-level and internal corporate governance structures and a country’s degree

of financial market development influence the hedging decisions of corporations. Notably,

0927-538X/$

doi:10.1016/j.

* Tel.: +46 8

E-mail add

- see front matter D 2004 Elsevier B.V. All rights reserved.

pacfin.2004.04.003

674 7427; fax: +46 8 674 7440.

ress: [email protected].

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366344

La Porta et al. (1998) reported that Korea lags Sweden in terms of law enforcement,

antidirector rights, cash-flow rights, and accounting standards. These differences may

cause Korean and Swedish firms to adopt different hedging policies and practices; by

studying these, we may improve our understanding of firms’ risk management practices.

Several methods are available for managing foreign exchange exposure, including the

use of financial derivatives such as forward contracts and currency options, foreign-

denominated debt, and internal methods such as leading and lagging. Prior survey

evidence pertaining to hedging primarily focused on the use of derivatives by firms in

local markets,1 while a few studies, notably those of Berkman et al. (1997), Alkeback and

Hagelin (1999), Bodnar and Gebhardt (1999), Sheedy (2001), and Bodnar et al. (2003),

also compared derivatives use between countries. Recent studies have presented survey

evidence pertaining to other hedging techniques, such as the use of foreign-denominated

debt and internal hedging techniques. Such studies include those of Hakkarainen et al.

(1998), who surveyed Finnish firms; Joseph (2000), who analyzed British firms; Marshall

(2000), who analyzed regional differences between Asia-Pacific and Western multinational

corporations (MNCs); and Allayannis et al. (2003), who investigated the hedging practices

of East Asian firms during the recent East Asian financial crisis.

This paper adds to existing research by analyzing country differences in foreign

exchange risk-management practices between Swedish and Korean firms. The focus is on

descriptive data comparing hedging practices; these data are complemented by direct tests

in order to investigate the potential of firm characteristics to explain differences. Korea and

Sweden are both export-oriented countries, heavily dependent on foreign trade, suggesting

that their markets would be suitable for this type of study. The countries’ markets differ in

other ways, such as their stage of economic and financial development. While Swedish

derivatives markets are well developed, comparable Korean markets have been heavily

regulated until very recently; this may have reduced firms access to, and consequently,

knowledge of derivative instruments.

Use of derivatives and other hedging techniques are investigated, using survey evidence

pertaining to the foreign exchange exposure and hedging practices of 163 firms in the two

countries that replied to a survey distributed in September 2000. In contrast to Marshall

(2000), who investigated only large multinational corporations, we sent our survey to all

nonfinancial firms listed on the major stock exchange in each country. In view of the

findings of Lel (2003) and Bartram et al. (2003), this is an important difference. Lel (2003)

investigated large, international firms listed via ADRs in the US and found that country-

specific factors were relatively more important than firm-specific factors in explaining the

probability of hedging. Bartram et al. (2003) used a larger sample including smaller firms

and found that firm-specific factors were relatively more important than country-specific

factors. The survey procedure used in our research produced a representative sample of

both large and small firms in Korea and Sweden, which may enhance our general

understanding of firms’ hedging practices.

Our findings suggest that while there are similarities between the hedging practices of

firms in the two countries, there are notable differences as well. Firms in both countries

1 See Batten et al. (1993), Nance et al. (1993), Bodnar et al. (1996, 1998), Berkman et al. (1997), and Alkeback

et al. (2004).

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366 345

were equally likely to decide to hedge foreign exchange exposure, this decision being

dependent of level of exposure and firm size. However, the aim of hedging activities

differed. Korean firms were more likely to focus on minimizing fluctuations of cash flow

rather than accounting earnings, while Swedish firms were more likely to focus on

accounting numbers. This is in line with the findings of Alkeback and Hagelin (1999)

and Alkeback et al. (in press) concerning Swedish firms. Perhaps our most striking

finding is that the proportion of firms that used derivatives was significantly lower in the

Korean than in the Swedish sample. This could not be accounted for by firm

characteristics such as foreign exchange exposure, size, liquidity, or leverage. A possible

explanation for this difference is that derivatives markets in Korea have been heavily

regulated until very recently, which would support the finding of Lel (2003) that the

degree of financial market development influences hedging policies. In line with this,

Korean firms were more likely to use foreign-denominated debt and used it more

extensively than did Swedish firms, suggesting a substitution effect. Furthermore, Korean

firms were less rigorous in monitoring their risk exposure positions than were Swedish

firms. This is in accordance with the findings of Sheedy (2001) and suggests that Asian

firms lag Western firms in this regard. An absolute majority of firms in both countries

used a profit-based approach to evaluate the risk management function. This contradicts

theoretical assumptions and adds to the findings of Bodnar et al. (1998) and Sheedy

(2001).

The paper is organized as follows: Section 2 presents prior research, Section 3 presents

the sample description and variable definitions, Section 4 presents the empirical results,

and Section 5 concludes the report. Throughout the paper, the findings are compared with

evidence from other studies wherever possible.

2. Prior survey evidence

Prior survey evidence pertaining to regional and country differences in hedging

practices has revealed significant differences in terms of hedging practices between US

and New Zealand firms (Berkman et al., 1997), between US and Swedish firms (Alkeback

and Hagelin, 1999), between US and German firms (Bodnar and Gebhardt, 1999),

between large MNCs in the Asia-Pacific region and in the US and the UK (Marshall,

2000), between US firms and firms in Hong Kong and Singapore (Sheedy, 2001), and

between Dutch and US firms (Bodnar et al., 2003).

Berkman et al. (1997) and Alkeback and Hagelin (1999) found similar differences in

the hedging practices of New Zealand and Swedish firms as compared to firms in the US.

The evidence presented in these studies shows a positive relationship between firm size

and derivatives use in all markets, suggesting that there are economies of scale in the use

of derivatives. Furthermore, the use of foreign exchange (FX) derivatives was more

common than the use of interest rate derivatives, commodity derivatives, and equity

derivatives in all three countries, which underlines the relative importance of FX exposure

to firms in most countries. The use of FX derivatives was more common in New Zealand

and Sweden than in the US, possibly because of the relative size and international

dependency of these markets.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366346

Bodnar and Gebhardt (1999) provided evidence suggesting that German firms were

more likely than US firms to use derivatives. They were also more comfortable with

derivatives use, indicating significantly less concern about issues related to derivatives

than is the case in US firms. It was suggested that this might stem from the German firms’

consistently stricter policies governing the control and monitoring of derivatives use

within the firm. Alkeback and Hagelin (1999) produced similar results when comparing

their Swedish sample to the US sample of Bodnar et al. (1996).

Marshall (2000) investigated the FX hedging practices of MNCs in the Asia Pacific

region, the US, and the UK and found similarities as well as differences among MNCs

from the different regions. The MNCs were similar in their use of internal hedging

techniques, but there were differences between the Asia Pacific MNCs and those from the

other regions in terms of the emphasis on FX risk management. FX risk management was

found to be significantly more important for the Asia Pacific MNCs than for MNCs from

the US and the UK, and the author suggested that this might be explained by the Asian

financial crisis.

Sheedy (2001) surveyed firms in Hong Kong and Singapore and compared their

derivatives use to that of US firms. She found that a higher proportion of the Asian firms

studied used derivatives than did the US firms, and moreover, that they did so with greater

frequency. The evidence suggested that the Asian firms exercised less rigorous oversight

of derivatives use than did the US firms, indicated partly by a lower proportion of firms

that had a set schedule for evaluating derivatives positions.

3. Sample description and variable definitions

The data for this study were collected through a survey. In September 2000, a

questionnaire was sent to Korean and Swedish nonfinancial firms (excluding utilities).

Three hundred and eighty-seven Korean firms listed on the Korean Stock Exchange and

250 Swedish firms listed on the Swedish Stock Exchange received the questionnaire,

which was sent in either a Korean or Swedish version as appropriate to increase the

response rate. In January 2001, a reminder was sent to firms that did not respond to the

first mailing. A total of 163 responses were received, 60 from Korean firms and 103 from

Swedish firms. This represents a total response rate of 26%: 16% for the Korean and 41%

for the Swedish sample. To check for response bias, responding firms were compared with

those that did not respond to the survey, and the result suggested that the sample is

unbiased (see Appendix A).

The use of a survey was necessary since information on firms’ exposures and hedging

practices is not publicly available. One caveat to bear in mind is that, although the

information provided is unique and may provide important insights, surveys have several

general shortcomings, such as the risk that survey subjects may give inaccurate or

dishonest responses. In addition, because in our case the respondents are from two

different countries with different cultures and languages, there is the additional problem of

how respondents interpret the questions from Korean- and Swedish-language versions of

the questionnaires. Firms operate under business conditions that differ in many respects

between these two countries, and it should be noted that this survey, like other similar

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366 347

surveys, can only document a limited set of characteristics and differences. It should be

taken into account that other not included variables could add to, or explain, some of the

results.

The questionnaire contained questions regarding (1) the respondent’s exposure to

foreign exchange rates and whether the respondent firm hedges; (2) the respondent’s use of

foreign currency derivatives (types of instruments, frequency of use, concerns); (3) the

respondent’s use of other foreign exchange risk management methods (foreign debt,

internal techniques); and (4) the respondent’s control and reporting procedures (decision-

making process, evaluation).2 Our decision to focus on only one type of exposure—FX

exposure—and the hedging of this exposure has the downside that possible correlations

with the hedging of other exposures are ignored. However, one important benefit is that

the survey is kept shorter, possibly improving response rates and allowing for a deeper

analysis of one exposure.

Summary statistics pertaining to the FX exposure of the sampled Swedish and Korean

firms are shown in Table 1, panel (A). Swedish firms are characterized by higher levels of

FX exposure for revenues, costs, and net assets as compared to Korean firms, although the

percentage of firms with FX exposure is similar for each category. Also, the percentage of

firms that indicated no exposure is similar in both countries. Furthermore, as can be seen in

panel (B), larger proportions of Korean firms hedged, used foreign debt, and used internal

methods, but these differences are not significant at a 10% level. However, the proportion

of Korean firms that used derivatives was significantly lower.

Reported differences, or the lack of such, may result from firm characteristics,

differences between national markets, or a combination of the two factors. This is

investigated further using logit regressions, as was done by Geczy et al. (1997), including

firm characteristics as control variables. The dependent variables are decision variables

representing firms’ decisions regarding hedging policy and choice of instruments. Three

decision variables are used, defined as follows:3

(a) Hedging (H), a dummy variable representing the decision to hedge. This variable is

assigned a value of 1 in the case of a firm that hedged (using currency derivatives,

foreign-denominated debt, internal methods, or a combination of the three) and 0

otherwise. All responding firms that indicated FX exposure are included in the

analysis.

(b) Currency derivatives (CD), a dummy variable representing the decision to use

currency derivatives to hedge. This variable is assigned a value of 1 in the case of a

firm that used derivatives to hedge and 0 otherwise. Only firms that hedged are

included in the analysis. Thus, this decision is defined as incremental to the decision

to hedge.

(c) Foreign debt (FD), a dummy variable representing the decision to use foreign-

denominated debt to hedge. This variable is assigned a value of 1 in the case of a

2 An English version of the questionnaire is available from the author on request.3 A fourth decision variable is possible: a dummy representing the decision to use internal methods. However,

since only nine firms did not use internal methods, inference from this variable is unreliable and this variable is

therefore not included.

Table 1

Exposure and hedging practices

Panel (A) Exposure to foreign exchange rates

Revenues Costs Net assets Zero exposure

Sweden

Mean 43.5 34.3 26.6

Max 100 100 100

3rd quartile 85 50 40

Median 40 30 15

1st quartile 5 10 0

No. of firms exposed 74 78 64 15

Percentage of firms exposed 75 80 68 16

No. of answers 99 98 94

Korea

Mean 28.8 20.9 13.4

Max 90 90 90

3rd quartile 45 30 30

Median 20 10 10

1st quartile 10 10 0

No. of firms exposed 49 47 38 8

Percentage of firms exposed 83 80 66 14

No. of answers 59 59 58

Panel (B) Hedging practices

Hedging Derivatives Foreign debt Internal methods

Sweden

Yes 54 44 37 44

No. of firms 88 54 52 51

Percentage 61 81 71 86

Korea

Yes 38 21 33 37

No. of firms 52 41 39 40

Percentage 73 51 85 93

Total

Yes 92 65 70 81

No. of firms 140 95 91 91

Percentage 66 68 77 89

Test for difference ( p-value)

0.158 0.002 0.131 0.346

The table contains descriptive statistics for firmsT foreign exchange exposure and hedging practices. Panel (A)

presents the foreign exchange exposure of revenues, costs, and net assets for the sampled firms, where the

exposure is calculated as the percentage of the total denominated in foreign currency. The last column presents the

number and percentage of firms that had no exposure. bNo. of firms exposedQ represents the total number of firms

with exposures of more than zero, bPercentage of firms exposedQ is calculated as the percentage of responding

firms with exposures of more than zero, and bNo. of answersQ is the total number of firms that answered each

question. Panel (B) presents descriptive statistics for sample firmsT hedging practices. For the first reporting

column, bYesQ represents the number of firms that answered that they hedged, bNo. of firmsQ represents the totalnumber of firms that responded, while bPercentageQ represents the proportion of responding firms that indicated

that they hedged. The last row presents the p-value from a Pearson Chi-square test for country difference in the

proportion of firms that hedged. Reporting columns 2 to 4 follow the same logic.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366348

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366 349

firm that used foreign-denominated debt to hedge and 0 otherwise. As for the

variable CD, only firms that hedged were included in the analysis.

The explanatory variables for these regressions include a country dummy as well as

proxies for FX exposure, size, growth opportunities, leverage, and liquidity. The reasons

for including these variables and how proxies are defined are as follows (predicted signs

for the model with dependent variable H appear in parentheses):

(i) Country dummy. This dummy measures the difference between the likelihood of

finding a Swedish firm and that of finding a Korean firm that, for example, hedges,

given that all other variables are controlled for. The dummy is set to 1 for Swedish

and to 0 for Korean firms (F0).

(ii) FX exposure. It is expected that direct exposure to FX rates is positively related to

the use of hedging instruments (see, e.g., Nance et al., 1993; Hagelin, 2003). The

proxy for FX exposure is defined as the average of the share of total revenues and

share of total costs that are denominated in foreign currency (+).4

(iii) Size. Empirical evidence suggests that economies of scale may influence the

decision to use derivatives (see, e.g., Hagelin, 2003). This may carry over to this

setting, as, for example, the implementation of a hedging program may be expected

to exhibit economies of scale. The proxy for size is the logarithm of total revenues

(+).5

(iv) Growth opportunities. Theoretical findings suggest that hedging reduces the

incentive to underinvest (see Myers, 1977; Bessembinder, 1991). Because firms

with more valuable growth opportunities are more likely to be affected by the

underinvestment problem, these firms may be more likely to hedge. The proxy for

growth opportunities is the book-to-market ratio. A lower value of this proxy

variable suggests more valuable growth opportunities (�).

(v) Leverage. Hedging can reduce the variance of the value of the firm and thereby the

expected cost of financial distress (see Smith and Stulz, 1985). Leverage can thus be

hypothesized as positively related to hedging. The proxy for leverage is the book

value of debt-to-equity ratio (+).

(vi) Liquidity. Hedging could increase the value of the firm by lowering the expected

costs of financial distress (see Smith and Stulz, 1985). Nance et al. (1993)

hypothesized that the probability of encountering financial distress may be reduced

by maintaining more liquid assets, thereby reducing the need to hedge. The proxy for

liquidity is the current ratio (�).

Data for creating the dependent and explanatory variables (i) and (ii) were taken from

the survey responses. The financial data required to calculate explanatory variables (iii)–

(vi) were collected from stock market guides: for the Korean firms from the Korea

4 An alternative proxy is the difference between revenues and costs denominated in foreign currency. As a

robustness test, this measure was used in all regressions producing similar results.5 Another proxy for corporate size is the logarithm of book value of total assets. This measure was also used,

producing similar results.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366350

Company Handbook (Asia-Pacific Infoserv, 2000) and for the Swedish firms from the

Nordbankens Aktieguide (Delphi Economics, 2000). All financial variables were as of the

beginning of year 2000.

In addition to the reported regressions, we also used alternative specifications which

included industry dummies, with industries classified according to Bodnar et al. (1996),

Berkman et al. (1997), and Alkeback and Hagelin (1999). This did not change the

results. Lel (2003) found that internal corporate governance structures influenced the

hedging decision. Thus, it may be expected that the hedging practices of Korean

chaebols (large conglomerates, such as Daewoo, Hyundai, and Samsung, usually

dominated by a founding family) would differ from those of other firms (for studies on

Korean chaebols see, e.g., Campbell and Keys, 2002; Ferris et al., 2001; Lim, 2001).

Three different classification systems for chaebols were included: the classification

system from Korea Listed Companies, 1999 (KLC), (Hyundai Securities), the

classification system from the Korean Fair Trade Law (FTL; as used by Lim, 2001),

and a more detailed classification system devised by Lim (2001). According to the

classification system presented in KLC, 22 of the 60 surveyed Korean firms were

chaebols, while according to the FTL system, only 14 of the 60 firms were chaebols.6

The inclusion of dummy variables for chaebols did not change the results, but the small

sample size means that no inference should be drawn from this inconclusive result. Further

research is needed to determine possible differences in hedging behavior between chaebols

and other firms.

4. Empirical results

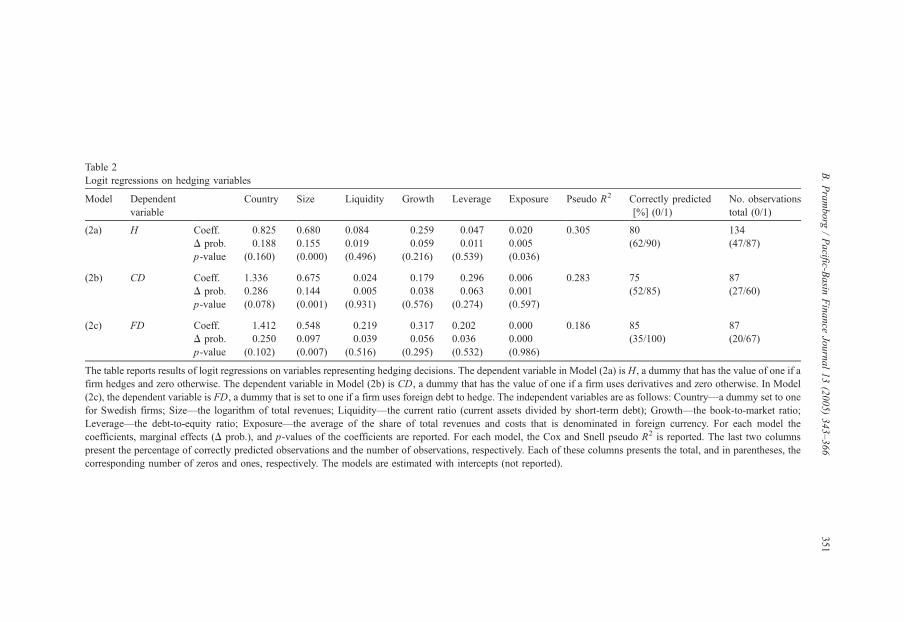

This section presents the empirical results. The results of the three logit regressions,

representing the decision variables discussed in Section 3, appear in Table 2. Before

proceeding, a comment on the organization of this section is in order. Subsection 4.1

discusses various aspects of the hedging decision as represented by Model (2a) in Table 2.

Subsection 4.2 presents findings regarding the use of derivatives and discusses Model

(2b). Subsection 4.3 presents findings pertaining to foreign-denominated debt, represented

by Model (2c), and internal hedging methods. Subsection 4.4, the last subsection, treats

control and reporting procedures.

At least two shortcomings of the logit regression models in Table 2 should be noted.

The first is that our classification of firms by means of dummy variables is crude. For

example, the decision whether to hedge or not, represented by Model (2a), may conceal

other relevant information, such as how much is hedged in each currency, whether or not

exposures in various currencies are hedged, and how long the hedge horizon is. The

second shortcoming is that the sample is small, especially for Models (2b) and (2c). Thus,

6 Lim (2001) classified chaebols according to whether they displayed pyramidal or horizontal ownership and

whether the controlling family retained a high or low stake, resulting in four classes of chaebols. Using this

classification, nine firms were classified as a type 4 chaebols (chaebols with pyramidal ownership and low family

stake) and five firms as type 1 (chaebols with horizontal ownership and high family stake). The inclusion of

dummies representing these types of chaebols did not alter the results.

Table 2

Logit regressions on hedging variables

Model Dependent

variable

Country Size Liquidity Growth Leverage Exposure Pseudo R2 Correctly predicted

[%] (0/1)

No. observations

total (0/1)

(2a) H Coeff. �0.825 0.680 0.084 �0.259 �0.047 0.020 0.305 80 134

D prob. �0.188 0.155 0.019 �0.059 �0.011 0.005 (62/90) (47/87)

p-value (0.160) (0.000) (0.496) (0.216) (0.539) (0.036)

(2b) CD Coeff. 1.336 0.675 �0.024 �0.179 �0.296 0.006 0.283 75 87

D prob. 0.286 0.144 �0.005 �0.038 �0.063 0.001 (52/85) (27/60)

p-value (0.078) (0.001) (0.931) (0.576) (0.274) (0.597)

(2c) FD Coeff. �1.412 0.548 �0.219 �0.317 0.202 0.000 0.186 85 87

D prob. �0.250 0.097 �0.039 �0.056 0.036 0.000 (35/100) (20/67)

p-value (0.102) (0.007) (0.516) (0.295) (0.532) (0.986)

The table reports results of logit regressions on variables representing hedging decisions. The dependent variable in Model (2a) is H, a dummy that has the value of one if a

firm hedges and zero otherwise. The dependent variable in Model (2b) is CD, a dummy that has the value of one if a firm uses derivatives and zero otherwise. In Model

(2c), the dependent variable is FD, a dummy that is set to one if a firm uses foreign debt to hedge. The independent variables are as follows: Country—a dummy set to one

for Swedish firms; Size—the logarithm of total revenues; Liquidity—the current ratio (current assets divided by short-term debt); Growth—the book-to-market ratio;

Leverage—the debt-to-equity ratio; Exposure—the average of the share of total revenues and costs that is denominated in foreign currency. For each model the

coefficients, marginal effects (D prob.), and p-values of the coefficients are reported. For each model, the Cox and Snell pseudo R2 is reported. The last two columns

present the percentage of correctly predicted observations and the number of observations, respectively. Each of these columns presents the total, and in parentheses, the

corresponding number of zeros and ones, respectively. The models are estimated with intercepts (not reported).

B.Pramborg

/Pacific-B

asin

Finance

Journal13(2005)343–366

351

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366352

we should use caution when interpreting the regression results. However, it should be

noted that various relevant information is provided by the surveys and presented in

conjunction with the regression results, enriching the information concerning the

regression results. Furthermore, the regressions are valuable in the sense that they indicate

possible country effects that cannot be explained by the exposure of individual firms or

other firm characteristics (included in the regressions).

4.1. Hedging

Model (2a) in Table 2 contains the dependent variable, H, which is set to 1 if a

firm hedges and to 0 otherwise. The coefficients for size and exposure are both

positive and statistically significant, suggesting that the decision to hedge FX exposure

is strongly influenced by both the size of the firm and its FX exposure. This is in line

with earlier studies that found support for economies of scale in the use of derivatives,

which would translate in this setting into economies of scale in setting up a hedging

program. Though the country dummy is negative, suggesting that Korean firms hedged

more, it is not statistically significant; thus, the null hypothesis of no country effect

cannot be rejected. Overall, the results are supported by the responses from firms that

did not hedge. The nonhedgers were asked to rank the factors influencing their

decision not to hedge (not reported). The responses suggest that insignificant FX

exposure, difficulties in estimating the FX exposure, and the costs of setting up a

hedging program were important determinants of the decision not to hedge for firms in

both countries.

Firms that hedged were asked to rank three prespecified objectives for hedging FX

exposure. The results suggest differences between Korean and Swedish firms, as

displayed in Fig. 1. Korean firms hedged primarily to reduce cash flow volatility, while

Swedish firms primarily hedged to reduce fluctuations in accounting earnings.

Korean firms ranked the latter alternative about as highly as did Swedish firms.

The results can be compared to Berkman et al. (1997) and Bodnar and Gebhardt

(1999), who found similar differences between New Zealand or German firms and US

firms. US firms emphasized cash flows as well as earnings, while firms in New

Zealand and Germany focused relatively more on earnings. Also, Marshall (2000)

found that Asian MNCs, like German and New Zealand firms, largely focused on

earnings.7 Berkman et al. (1997) and Bodnar and Gebhardt (1999) argued that the

differences may be attributed to differences in accounting regulations, where accounting

rules in the non-US countries made a stronger link between accounting earnings and cash

flows. This link is due to the comparatively strong connection between earnings, taxes,

and dividend payments. Swedish accounting regulation is tax related and somewhat

similar to German regulation (see Hung, 2001), while Korean accounting has, since the

Asian crisis in 1997, been heavily influenced by US GAAP, which would support these

7 Korean firms differ substantially from the Asian MNCs in the sample of Marshall (2000), where an absolute

majority considered minimizing earnings fluctuations to be the most important reason for hedging. However, only

three of the 53 Asian MNCs in Marshall’s sample were Korean firms.

2,14

2,40

1,09

2,37

1,771,69

1,0

1,2

1,4

1,6

1,8

2,0

2,2

2,4

2,6

a. Minimize fluctuations inaccounting earnings

b. Minimize fluctuations in realcash flows

c. Protect the appearance of thebalance sheet

Mea

n R

ank

Korea Sweden

Fig. 1. Objectives of hedging. The figure displays the answers to a question where firms were asked to rank what

they were trying to achieve by hedging. The possible ranks available were 3 =most important, 2 = next most

important, 1 = least important, and 0 = not at all important. A total of 88 answers was obtained, of which 36 were

from Korean and 52 were from Swedish firms. The vertical axis displays the mean rank calculated from the

responses from Korean and Swedish firms, respectively.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366 353

arguments. However, La Porta et al. (1998) reported that Korean accounting standards lag

Swedish standards considerably. Therefore, an alternative and perhaps more plausible

explanation is that Korean firms focus on cash flows because earnings are manipulated

extensively by, for example, backward accounting practices, and in the case of chaebols,

the transfer of profits within these large conglomerates.8 From Fig. 1, it is also evident that

Swedish firms ranked hedging of the balance sheet as about as important as hedging cash

flows, ranking it considerably higher than did Korean firms. As compared to firms in the

US and Europe (Bodnar et al., 1998, 2003; Bodnar and Gebhardt, 1999), Swedish firms

seem to focus relatively more on balance sheet hedging. This practice is not supported by

theory since it is aimed at accounting numbers and not cash flows. However, if this

hedging is a proxy for economic exposure (see Oxelheim and Wihlborg, 1997; Hagelin

and Pramborg, 2004a) or if firms have loan covenants expressed in accounting ratios (see

Hagelin and Pramborg, 2004b), such hedging may be rational.

4.2. Currency derivatives

4.2.1. The decision to use derivatives

Table 2, Model (2b), presents the results of a logit regression on the decision to use

derivatives. The dependent variable is CD, a dummy that is set to 1 if a firm uses

currency derivatives and to 0 otherwise. This model includes hedgers only, so the

8 The author is grateful to an anonymous referee for pointing this out.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366354

implicit assumption is that the choice to use derivatives is subsequent to the decision to

hedge. It is suggested that derivatives use differs significantly between firms in the two

countries, Swedish firms being more likely to use derivatives to hedge FX exposure than

are Korean firms. Furthermore, firm size is positively related to the decision to use

derivatives, confirming earlier findings that there are economies of scale in the use of

derivatives.

This country difference may be due to a number of factors. It may partly be a

consequence of the maturity of the two markets. The Swedish derivatives market was

established relatively early on, when the options exchange began trading in 1986; in

Korea, derivatives trading on exchanges began as recently as 1996 for stock index futures

and 1997 for stock index options. The trading of FX derivatives in Korea began as recently

as 1999, when the Korean Futures Exchange opened for trading in standardized USD

futures and options. The longer history of the Swedish market suggests that Swedish firms

have more experience using these types of instruments. However, Korean firms have long

been able to use, for example, nondelivered forwards in Singapore for their US dollar–won

exposure, so this difference in experience may thus be of less significance. A related, and

perhaps more important, reason for the difference between Korean and Swedish firms is

that in Korea, OTC derivatives have until recently been heavily regulated by the

authorities (due to the potential risk in derivative products, despite their positive economic

role as risk-hedging instruments). This heavy regulation can be expected to have

discouraged Korean firms from using derivatives. It was only in April 1999 that

government regulation changed, freeing up derivatives trading.9 If this interpretation of the

country difference is correct, the relative reluctance of Korean firms to use derivatives may

be a transitory phenomenon.

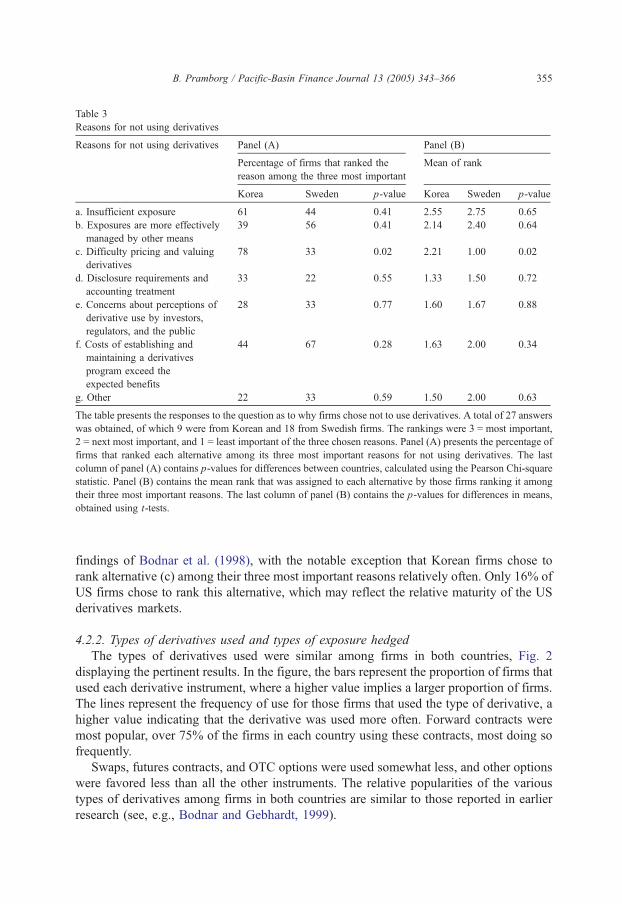

The above discussion is supported by the responses displayed in Table 3, regarding

reasons for not using derivatives. This question asked firms to rank three of seven

alternatives, assigning them the following values: 3 = most important, 2 = next most

important, and 1 = least important. Panel (A) displays the percentages of firms that

assigned each alternative a btop threeQ ranking. Panel (B) displays the mean rank of each

alternative, where the results include only the responses of those firms that ranked the

alternative among their top three reasons. Thus, the values in panel (B) could range from

1.00 (if all firms that ranked the alternative ranked it as least important) to 3.00 (if all

firms that ranked the alternative ranked it as most important). The only significant

difference between the countries is in their ranking of alternative (c), bDifficulty pricing

and valuing derivatives,Q suggesting that Korean firms have relatively less experience

with derivatives.

The proportion of firms that chose to rank this alternative, (c), as well as the average

rank assigned differs significantly between the two countries. This was the most important

reason for Korean firms (78% ranked this alternative, with a mean rank of 2.21), while for

Swedish firms, this alternative was ranked low (33% ranked this alternative, with the

lowest possible mean rank of 1.00). It should be noted that the number of responses to this

question was relatively low. In general, the results presented in Table 3 are in line with the

9 Source: Bank of Korea, http://www.bok.or.kr.

Table 3

Reasons for not using derivatives

Reasons for not using derivatives Panel (A) Panel (B)

Percentage of firms that ranked the

reason among the three most important

Mean of rank

Korea Sweden p-value Korea Sweden p-value

a. Insufficient exposure 61 44 0.41 2.55 2.75 0.65

b. Exposures are more effectively

managed by other means

39 56 0.41 2.14 2.40 0.64

c. Difficulty pricing and valuing

derivatives

78 33 0.02 2.21 1.00 0.02

d. Disclosure requirements and

accounting treatment

33 22 0.55 1.33 1.50 0.72

e. Concerns about perceptions of

derivative use by investors,

regulators, and the public

28 33 0.77 1.60 1.67 0.88

f. Costs of establishing and

maintaining a derivatives

program exceed the

expected benefits

44 67 0.28 1.63 2.00 0.34

g. Other 22 33 0.59 1.50 2.00 0.63

The table presents the responses to the question as to why firms chose not to use derivatives. A total of 27 answers

was obtained, of which 9 were from Korean and 18 from Swedish firms. The rankings were 3 = most important,

2 = next most important, and 1 = least important of the three chosen reasons. Panel (A) presents the percentage of

firms that ranked each alternative among its three most important reasons for not using derivatives. The last

column of panel (A) contains p-values for differences between countries, calculated using the Pearson Chi-square

statistic. Panel (B) contains the mean rank that was assigned to each alternative by those firms ranking it among

their three most important reasons. The last column of panel (B) contains the p-values for differences in means,

obtained using t-tests.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366 355

findings of Bodnar et al. (1998), with the notable exception that Korean firms chose to

rank alternative (c) among their three most important reasons relatively often. Only 16% of

US firms chose to rank this alternative, which may reflect the relative maturity of the US

derivatives markets.

4.2.2. Types of derivatives used and types of exposure hedged

The types of derivatives used were similar among firms in both countries, Fig. 2

displaying the pertinent results. In the figure, the bars represent the proportion of firms that

used each derivative instrument, where a higher value implies a larger proportion of firms.

The lines represent the frequency of use for those firms that used the type of derivative, a

higher value indicating that the derivative was used more often. Forward contracts were

most popular, over 75% of the firms in each country using these contracts, most doing so

frequently.

Swaps, futures contracts, and OTC options were used somewhat less, and other options

were favored less than all the other instruments. The relative popularities of the various

types of derivatives among firms in both countries are similar to those reported in earlier

research (see, e.g., Bodnar and Gebhardt, 1999).

0

20

40

60

80

100

a. Forwardcontracts (OTC)

b. Futurescontracts

(Exchange-traded)

c. Swaps d. Options onfutures

e. OTC options f. Exchange-traded options

Per

cent

age

that

use

d in

stru

men

t

0

20

40

60

80

100

Per

cent

age

(of u

sers

) th

at u

sed

freq

uent

ly

Korea (%) Sweden (%) Korea frequently Sweden frequently

Fig. 2. Types of derivatives used. The figure displays the answers to a question where firms were asked to indicate

how often they used various types of currency derivatives. The options available were 3 = frequently, 2 = seldom,

and 1 = never. A total of 88 answers was obtained, of which 36 were from Korean and 52 were from Swedish

firms. The left vertical axis refers to the bars in the figure and displays the percentage of firms that indicated that

they used an instrument at least seldom (rank 2 or 3). The right vertical axis refers to the lines in the figure and

displays the percentage of firms that used the instrument frequently, calculated from firms that responded that they

used the instrument.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366356

The types of exposures that were hedged using derivatives are similar among the firms

in the two countries. Table 4 displays the responses to the question about this, adding to

the evidence presented in Fig. 1 regarding the ultimate reasons for hedging (cash flows,

accounting earnings, and translation hedging).

There is no systematic difference in the use of derivatives between firms in the two

countries. Thus, the documented differences in the stated purposes of hedging FX

exposure (Fig. 1) do not necessarily result in practical differences in hedging behavior

between firms in the two countries. Note, for example, that a relatively large proportion of

the sampled firms in both countries used derivatives to hedge the translation of foreign

accounting statements, despite the difference suggested in Fig. 1. Thus, although the

relative emphasis on various objectives of hedging, as suggested in Fig. 1, may differ

between firms in the two countries, in practice, all the objectives may be of some concern,

and thus be hedged. One interesting observation is that Swedish firms were likely to

engage in speculation. About a third of the Swedish respondents indicated that they

speculated, and half of those firms did so frequently. These proportions are similar to those

found by Alkeback and Hagelin (1999).

4.2.3. Concerns about derivatives use

Concerns about the use of derivatives differ substantially in degree, as reported in

Table 5. Korean firms are more concerned across the board and significantly so for

alternatives (a)–(e). This may help explain why the Korean firms sampled are less likely

to use derivatives than are the Swedish firms. Other studies examining concerns with

Table 4

Frequency of derivatives use for various purposes

Frequency of derivatives Panel (A) Panel (B)

use for various purposesPercentage of firms that

used derivatives for the

stated purposes

Percentage of derivatives users

that used derivatives frequently

for the stated purposes

Korea Sweden p-value Korea Sweden p-value

a. Hedge translation of foreign

accounting statements?

62 72 0.41 46 55 0.60

b. Hedge foreign repatriations? 76 69 0.55 50 48 0.91

c. Hedge contractual commitments? 71 86 0.16 27 70 0.00

d. Hedge anticipated transactions

(b12 months)?

95 79 0.09 60 82 0.07

e. Hedge anticipated transactions

(N12 months)?

43 65 0.09 11 21 0.41

f. Arbitrage? 38 35 0.80 13 47 0.10

g. Speculate? 10 33 0.06 0 50 0.18

The table presents the responses to the question as to what purposes firms used derivatives. A total of 64 answers

was obtained, of which 21 were from Korean and 43 from Swedish firms. The rankings were 3 = frequently,

2 = seldom, 1 = never, and 0 = don’t know. Panel (A) contains the percentage of firms that assigned the

alternative a rank of at least 2, thus indicating that they used derivatives at least seldom for this purpose. Panel (B)

contains the percentage of derivatives users that assigned the alternative the rank of 3, thus indicating that they

used derivatives frequently. The last columns of panels (A and B) contain p-values for the differences between

countries, calculated using the Pearson Chi-square statistic.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366 357

derivatives use have also found significant differences between firms from different

countries; Bodnar and Gebhardt (1999) reported differences between German and US

firms, with German firms displaying less concern; Alkeback and Hagelin (1999)

presented evidence from a comparison of Swedish and US firms, suggesting that Swedish

firms are less concerned than US firms; and Bodnar et al. (2003) found differences

between Dutch and US firms, with Dutch firms displaying less concern. Differences may

arise from a number of factors, such as firm-level differences in policies towards

controlling and monitoring derivatives-related activities within the firm (Bodnar and

Gebhardt, 1999), or as a consequence of differences in disclosure requirements regarding

derivatives and the relative risk of corporate litigation for insufficient fiduciary care

(Bodnar et al., 2003).

The difference between Korean and Swedish firms could, at least to some

extent, be due to differences in disclosure requirements. Since the Asian crisis of

1997, Korean accounting regulation has primarily been based on US GAAP,

while Swedish accounting is similar to German and Dutch accounting. However,

Korean accounting had until recently been similar to German and Japanese

accounting, and the accounting standards of Korea are substantially lower than

those of Sweden according to La Porta et al. (1998).10 This suggests that Korean

10 After the 1997 financial crisis, IMF and World Bank pressure led to Korean accounting standards being

upgraded in an attempt to harmonize them with best practice, defined as requirements from the IAS and, above

all, US GAAP (see Choi, 1999).

Table 5

Concerns about the use of derivatives

Concerns about the use of derivatives Panel (A) Panel (B)

Percentage of firms that

ranked each item as a

bmoderateQ or bhighQ concern

Mean of rank

Korea Sweden p-value Korea Sweden p-value

a. Credit risk 62 23 0.00 1.86 0.91 0.00

b. Accounting treatment 67 33 0.01 1.86 0.95 0.00

c. Transaction cost (bankersT fees) 81 28 0.00 2.19 1.05 0.00

d. Liquidity risk 81 38 0.00 2.10 1.26 0.00

e. Lack of knowledge about

derivatives within my firm

62 23 0.00 1.71 0.93 0.00

f. Difficulty understanding the

firm’s exposure

38 24 0.24 1.19 0.93 0.26

The table presents the responses to the question about concerns regarding derivatives use. A total of 90 answers

was obtained, of which 39 were from Korean and 51 from Swedish firms. The rankings were 3 = high,

2 = moderate, 1 = low, and 0 = no concern. Panel (A) contains the percentage of firms that assigned each

alternative a rank of at least 2, indicating a moderate or high degree of concern. The last column of panel (A)

contains p-values for the differences between countries, calculated using the Pearson Chi-square statistic. Panel

(B) contains the mean rank assigned to each alternative. The last column of panel (B) contains p-values for

differences in means, calculated using t-tests.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366358

firms’ great concerns regarding derivatives, and consequent reluctance to use them, may

rather be a consequence of their relative inexperience with these instruments, as discussed

above.

4.3. Other foreign exchange risk management methods

4.3.1. Foreign-denominated debt

Model (2c) in Table 2 reports the results of a logit regression on the decision to

use foreign-denominated debt to hedge. The dependent variable is FD, a dummy that

is set to 1 if a firm uses foreign debt and to 0 otherwise. Using a 10% level of

significance, the results of this regression suggest that there is a positive relationship

between the size of a firm and the use of foreign debt. Also note that the sign of the

country dummy is opposite to that of the country dummy in Model (2b) with a p-

value of 0.102, thus marginally above statistical significance. Given that Korean firms

are more concerned about the use of derivatives, they may be inclined to use foreign

debt instead of currency derivatives.11

Firms were asked in the questionnaire to report the types of exposure they hedged using

foreign-denominated debt and the frequency of such hedging. Table 6 displays the

responses to this question.

11 The findings of Elliot et al. (2003) support the notion that firms may use foreign debt as a substitute for

derivatives.

Table 6

Frequency of foreign debt use for various purposes

Purposes of foreign debt use Panel (A) Panel (B)

Percentage of firms that

used foreign-denominated

debt for the purpose

Percentage of foreign debt

users that used frequently

for the purpose

Korea Sweden p-value Korea Sweden p-value

a. Hedge translation of foreign

accounting statements?

39 58 0.09 7 57 0.00

b. Hedge foreign repatriations? 54 27 0.01 48 14 0.04

c. Hedge contractual commitments? 44 25 0.06 24 46 0.19

d. Hedge anticipated transactions

(b12 months)?

67 19 0.00 35 20 0.39

e. Hedge anticipated transactions

(N12 months)?

41 8 0.00 13 25 0.53

f. Arbitrage? 26 33 0.47 40 18 0.20

g. Speculate? 3 12 0.12 0 17 0.66

The table presents the responses to the question as to what purposes firms used foreign-denominated debt. A total

of 64 answers was obtained, of which 21 were from Korean and 43 from Swedish firms. The rankings were

3 = frequently, 2 = seldom, 1 = never, and 0 = don’t know. Panel (A) contains the percentage of firms that gave an

alternative a rank of at least 2, indicating that they used foreign debt for the purpose. Panel (B) contains the

percentage of foreign debt users that assigned the alternative a rank of 3, indicating that they used foreign debt

frequently for the purpose. The last columns of panels (A and B) contain p-values for differences between

countries, calculated using the Pearson Chi-square statistic.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366 359

It is evident that significant proportions of firms in both countries used foreign-

denominated debt for hedging purposes. This underscores the importance of foreign-

denominated debt as a hedging instrument and suggests that research aimed at explaining

hedging decisions by firms should examine the use of foreign-denominated debt.

Importantly, Korean firms used foreign debt significantly more often to hedge cash flow

transactions than did Swedish firms. This finding suggests that once the decision was

taken to use foreign debt, Korean firms used this instrument extensively. It also supports

the finding in Table 2 that Korean firms were more likely to use foreign-denominated debt

to hedge than were Swedish firms. One caveat, however, is that there may be alternative

motives for extensive use of foreign-denominated debt. Allayannis et al. (2003) found

evidence that firms make trade-offs between the benefits of lower foreign borrowing costs

and a probable increase in financial risk due to exchange rate uncertainty. The higher the

positive interest rate differential between domestic and foreign debt, the more likely firms

are to use foreign-denominated debt. Accordingly, the high level of foreign-denominated

debt use by Korean firms may be a symptom of high overall debt use and their attempt to

attract foreign capital to retire high-interest domestic debt in the aftermath of the Asian

financial crisis. This is one way of arbitraging in the debt market, but one finding

contradicts whether such arbitrage was the primary intention here: in responding to

question (d) in Table 6, Korean firms were somewhat less likely to indicate that they

arbitraged with foreign-denominated debt. Nevertheless, it is possible that Korean firms

chose foreign-denominated debt not only driven by hedging demands and a reluctance to

use derivatives, but also for financing purposes.

0

20

40

60

80

100

a. Leading andlagging

b. Matchinginflows and

outflows (timing ofsettlement)

c. Inter-companynetting of receipts

and payments

d. Domesticcurrency invoicing

e. Adjustmentclause in sales

contracts

f. Transfer pricingagreements

Per

cent

age

that

use

d te

chni

que

0

20

40

60

80

100

Per

cent

age

(of u

sers

) th

at u

sed

freq

uent

ly

Korea (%) Sweden (%) Korea frequently Sweden frequently

Fig. 3. Types of internal hedging techniques used. The figure displays the answers to a question where firms were

asked to indicate how often they used various types of internal hedging. The options available were 3 = frequently,

2 = seldom, 1 = never, and 0 = do not know. A total of 90 answers was obtained, of which 39 were from Korean

and 51 were from Swedish firms. The left vertical axis refers to the bars in the figure and displays the percentage

of firms that indicated that they used a technique at least seldom (rank 2 or 3). The right vertical axis refers to the

lines in the figure and displays the percentage of firms that used the technique frequently, calculated from firms

that responded that they used the technique.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366360

In sum, the results indicate that foreign-denominated debt is used for hedging purposes

by a large proportion of firms in both countries, that there is a country difference, and

possibly that foreign debt is used as a substitute for derivatives, especially by Korean firms.

4.3.2. Internal methods

In the literature, most research has focused on derivatives and/or foreign-denominated

debt. Internal methods are often overlooked but are likely to be an important part of firms’

risk management strategies.12 In fact, the use of internal hedging techniques has been

found to be very common among firms (see, e.g., Hakkarainen et al., 1998; Joseph, 2000;

Marshall, 2000). Internal hedging techniques include leading and lagging of revenues and

costs, netting of trade receivables and payables among associated companies, and

domestic currency invoicing.

Firms were asked in our survey how often they used various internal hedging

techniques. An important finding is that most hedgers in the sample used internal methods

(only nine firms indicated that they did not). This finding, together with those of the

12 The findings of Choi and Kim (2003) are consistent with the notion that there is an interaction between

operational and financial strategies.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366 361

studies cited in the previous paragraph, suggests that firms across a range of markets make

extensive use of internal hedging methods.

Fig. 3 displays the responses to this question. Note that the methods surveyed in

this study primarily reflect the hedging demands of relatively short-term exposures

(implicitly assuming a static organization structure) and exclude long-term strategic

considerations, such as the shifting of production or plant location. See Marshall

(2000) for survey evidence concerning strategies for hedging longer term economic

exposures.13

The bars in Fig. 3 represent the proportion of firms that used each technique, where a

higher value implies a larger proportion of firms. The lines represent the frequency of use

on the part of those firms that used each technique, where a higher value indicates that the

technique was used more often. The relative popularity of various techniques in the two

countries was broadly similar. Matching inflows and outflows was the most common

technique in both countries, followed by inter-company netting for Swedish firms, and

leading and lagging for Korean firms. As suggested by the lines in Fig. 3, when adopting a

technique, Swedish firms used it more often than did Korean firms, except for leading and

lagging. Our findings regarding the Swedish firms are in line with the findings of

Hakkarainen et al. (1998), Joseph (2000), and Marshall (2000);14 our findings, however,

differ somewhat from theirs in terms of the relatively common use of leading and lagging

we found among Korean firms.

4.4. Control and reporting procedures

In the questionnaire, firms were asked about their control and reporting procedures.

They were specifically asked how often they evaluated their FX risk position, and how

they evaluated their risk management function.15

Fig. 4 shows how often the risk position was evaluated. Swedish firms were more likely

to have a set schedule, with less than 10% of Swedish firms having no set schedule.

Korean firms, on the other hand, were much more likely to evaluate as needed, adhering to

no set schedule. Earlier surveys have asked about the evaluation of derivatives positions

and not, as here, about the total risk position. However, both types of questions may

produce very similar answers, since it is likely that these two valuations are made

simultaneously. If so, the Swedish sample conforms to earlier results pertaining to Sweden,

Germany, and the US (see Alkeback and Hagelin, 1999; Bodnar and Gebhardt, 1999),

while Korean firms in this comparison stand out by the high proportion (41%) of them that

14 Joseph (2000) and Marshall (2000) studied different types of exposure. The utilization rates presented in Fig.

3 are compared to the figures for the hedging of transaction exposure, the dominant form of hedging used by the

firms studied.15 Firms were also asked whether the decision-making process concerning policy, strategy, and execution was

centralized or decentralized. The proportion of Swedish firms using a centralized decision-making process was

significantly higher, regardless as to whether the decision concerned policy, strategy, or the execution of risk

management.

13 For this question, firms could also choose alternative g—bother.Q However, since only 18 of the 90 firms that

answered the question responded to this particular alternative, this alternative is not included.

41,0

17,9 17,920,5

0,0

2,6

9,6

34,6

21,2

26,9

1,9

5,8

0

5

10

15

20

25

30

35

40

45

50

As needed/NoSchedule

Daily Weekly Monthly Quarterly Annually

Per

cent

age

of fi

rms

Korea Sweden

Fig. 4. Frequency of evaluating FX risk position. The figure displays the answers to a question where firms were

asked how frequently they evaluated their foreign exchange risk position. A total of 92 answers was obtained, of

which 39 were from Korean and 52 were from Swedish firms.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366362

evaluate as needed or have no evaluation schedule. However, Sheedy (2001) found that

36% of the studied firms from Hong Kong and Singapore did not have a schedule for

evaluating their derivatives positions. It seems that Asian firms are less likely to have

scheduled evaluations of risk positions than do Western firms. Two robustness tests were

performed. First, a logit regression on the decision as to whether or not to have scheduled

evaluations suggests that the country difference is robust and also that the greater the

exposure, the more likely firms were to conduct scheduled evaluations. Second, an ordered

probit regression on the frequency of reporting suggests that larger firms evaluated more

often, firms with greater FX exposure evaluated more often, and that Swedish firms

evaluated their positions more often than did Korean firms. This corroborates Sheedy

(2001) who found that the Asian firms in her sample lagged US firms in their oversight of

derivatives activity.

Fig. 5 presents findings regarding the method used to evaluate the FX risk

management function within firms. These findings suggest that firms in both Korea

and Sweden primarily evaluated the risk management function by absolute profit/loss.

This supports earlier results (see, e.g., Bodnar et al., 1998; Sheedy, 2001) but is

nonetheless somewhat puzzling, since risk management should, theoretically, be aimed

at reducing risk and not at seeking economic rents. Bodnar et al. (1998) reported that

about 40% of their sample used a profit-based approach, and about the same

proportion of firms used risk-adjusted measures. Sheedy (2001) reported similar

numbers for firms in Hong Kong and Singapore, and Bodnar et al. (2003) reported that

57% of Dutch firms used a profit-based approach. For the Korean and Swedish firms

7,3

14,6

56,1

22,0

0,0

21,4

10,7

50,0

5,4

12,5

0

10

20

30

40

50

60

70

a. Reducedvolatility relative to

a benchmark

b. Increased profit(reduced costs)

relative to abenchmark

c. Absoluteprofit/loss

d. Risk-adjustedperformance

(profits or savingsadjusted for

volatility)

e. Other

Per

cent

age

of fi

rms

Korea Sweden

Fig. 5. Evaluation of FX risk management. The figure displays the answers to a question where firms were asked

how they evaluated their FX risk management. A total of 97 answers was obtained, of which 41 were from

Korean and 56 were from Swedish firms.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366 363

we surveyed, the proportions of firms using a profit-based approach—alternatives (b)

and (c) in Fig. 5—are even higher at 71% and 61%, respectively.16 One possible effect

of this is that managers could be more inclined to speculate in order to increase profits, or,

alternatively, that firms that speculate are more likely to adopt a profit-based approach to

evaluate the risk management function. Supporting this link is a significant and positive

correlation between speculation with derivatives and the evaluation of the risk function

using a profit-based approach.17

5. Conclusions

This paper surveys Swedish and Korean nonfinancial firms on their foreign exchange

risk exposure and hedging practices. The findings suggest similarities between firms in the

two countries, with notable exceptions.

The aim of hedging activity differed between the countries, Korean firms being

more likely to focus on minimizing fluctuations of cash flows, while Swedish firms

17 Using a logit regression with the decision to speculate with derivatives as a dependent variable suggests that

speculation is positively associated with firm size and with a profit-based approach ( P-value of 0.059). The

country effect suggested in Table 6 is also confirmed, in that Swedish firms were significantly more likely to

engage in speculation.

16 A logit regression, where the dependent variable is a dummy that takes the value of 1 if the firm uses a profit-

based approach and 0 otherwise, suggests that this may not be explained by firm characteristics. The difference

between firms in the two countries is not significant.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366364

favored minimizing fluctuations of earnings or protecting the appearance of the

balance sheet. The proportion of firms that used derivatives was significantly lower in

the Korean than in the Swedish sample. This could not be captured by firm

characteristics such as FX exposure, size, liquidity, or leverage. This may be due to

the higher fixed costs incurred by Korean firms initiating derivatives programs. These

higher costs could result from the relative immaturity of Korean derivatives markets

and, perhaps more importantly, from Korean authorities’ heavy regulation of OTC

derivatives use. Korean firms relied to a larger extent on alternative hedging methods,

suggesting that the decision to hedge was not country specific but rather driven by

firm-specific variables, such as the level of FX exposure and firm size. It is further

suggested that Korean firms were less rigorous in monitoring their risk positions than

were Swedish firms. Finally, a large proportion of firms in both countries used a

profit-based approach to evaluate the risk management function, which is counter to

theoretical recommendations and bolsters the findings of Bodnar et al. (1998) and

Sheedy (2001).

Acknowledgements

The paper has benefited substantially from the suggestions of an anonymous

referee, and the author gratefully acknowledges his/her contribution. The author would

also like to thank Hossein Asgharian, Niclas Hagelin, Martin Holmen, Lars Norden,

and Clas Wihlborg for their valuable comments. Comments from participants in the

EAMSA annual meeting in Stockholm, 2003, and from seminar participants at the

Stockholm University School of Business are also acknowledged. The author is

grateful to Mika Sarkkinen, Hyun Park, and Olivia Kang for their help in translating

the Korean-language questionnaire and to the Center for Pacific Asia Studies at

Stockholm University and the Jan Wallander and Tom Hedelius Foundation for

financial support.

Appendix A. Summary statistics and tests for unbiasedness

The table contains descriptive statistics for the sampled firms and significance tests

for the differences in means and medians between responding and nonresponding firms.

The variables are defined as follows: bLeverageQ is measured as the debt-to-equity ratio,

bLiquidityQ is measured as short-term debt divided by current assets (current ratio),

bSizeQ is proxied by total sales, and bProfitabilityQ is proxied by return on equity. The

bExport ratioQ is measured as foreign sales divided by total sales, and bOwnershipconcentrationQ is measured as the proportion of shares owned by the five (three) largest

shareholders for the Swedish (Korean) sample. The significance test for the mean is a t-

test, and for the median is the Wilcoxson/Mann–Whitney test. The data are for financial

years ending in 1999. Values are translated to USD using the exchange rates as of

December 31, 1999.

Leverage Liquidity Size

(USD million)

Profitability Export ratio Ownership

concentration

Panel (A) Korean firms

Responding firms

Mean 1.77 1.41 615 4.1 32.1 31.8

Median 1.18 1.35 161 6.3 19.6 30.8

No. firms 60 60 61 58 60 60

Nonresponding firms

Mean 1.44 1.45 975 4.4 32.3 33.0

Median 1.14 1.23 158 6.8 23.2 30.1

No. firms 326 327 327 302 326 325

Test for difference ( p-value)

mean 0.64 0.77 0.41 0.94 0.97 0.59

median 0.93 0.38 0.73 0.83 0.71 0.99

Panel (B) Swedish firms

Responding firms

Mean 1.94 1.13 1120 �7.12 44.8 44.2

Median 1.29 0.57 98 10.4 45.0 42.0

No. firms 103 103 103 103 67 101

Nonresponding firms

Mean 1.74 0.79 557 �0.94 41.0 48.7

Median 1.26 0.54 93 8.9 37.0 49.0

No. firms 147 147 147 147 97 144

Test for difference ( p-value)

mean 0.60 0.18 0.10 0.35 0.48 0.06

median 0.99 0.48 0.31 0.72 0.53 0.05

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366 365

References

Alkeb7ck, P., Hagelin, N., 1999. Derivative use by nonfinancial firms in Sweden with an international

comparison. Journal of International Finance and Management Accounting 10, 105–120.

Alkeb7ck, P., Hagelin, N., Pramborg, B., 2004. Derivative usage by non-financial firms in Sweden 1996 and

2003: What has changed? Managerial Finance (in press).

Allayannis, G., Brown, G.W., Klapper, L.F., 2003. Capital structure and financial risk: Evidence from foreign

debt use in East Asia. Journal of Finance 58, 2667–2709.

Bartram, S.M., Brown, G.W., Fehle, R.F., 2003, International evidence on financial derivatives usage. Working

paper, Kenan-Flagler Business School, University of North Carolina at Chapel Hill.

Batten, J., Mellor, R., Wan, V., 1993. Foreign exchange risk management practices and products used by

Australian firms. Journal of International Business Studies 24, 557–573.

Berkman, H., Bradbury, M.E., Magan, S., 1997. An international comparison of derivatives use. Financial

Management 26, 69–73.

Bessembinder, H., 1991. Forward contracts and firm value: investment incentive and contracting effects. Journal

of Financial and Quantitative Analysis 26, 519–532.

Bodnar, G.M., Gebhardt, G., 1999. Derivatives usage in risk management by US and German non-financial firms:

A comparative survey. Journal of International Finance and Management Accounting 10, 153–187.

Bodnar, G.M., Hayt, G.S., Marston, R.C., 1996. 1995 Wharton survey of derivatives usage by U.S. non-financial

firms. Financial Management 25, 113–133.

Bodnar, G.M., Hayt, G.S., Marston, R.C., 1998. 1998 Wharton survey of financial risk management by U.S. non-

financial firms. Financial Management 27, 70–91.

B. Pramborg / Pacific-Basin Finance Journal 13 (2005) 343–366366

Bodnar, G.M., De Jong, A., Marcae, V., 2003. The impact of institutional differences on derivative usage: A

comparative study of US and Dutch firms. European Financial Management 9, 271–297.

Campbell, T.L., Keys, P.Y., 2002. Corporate governance in South Korea: The chaebol experience. Journal of

Corporate Finance 8, 373–391.

Choi, J.H., 1999, Transforming accounting standards, The AMCHAM Journal May/June issue, The American

Chamber of Commerce in Korea.

Choi, J.J., Kim, Y.-C., 2003. The Asian exposure of U.S. firms: Operational and risk management strategies.

Pacific-Basin Finance Journal 11, 121–138.

Elliot, W.B., Huffman, S.P., Makar, S.D., 2003. Foreign-denominated debt and foreign currency derivatives:

Complements or substitutes in hedging foreign currency risk? Journal of Multinational Financial Management

13, 123–139.

Ferris, S.P., Kim, K.A., Kitsabunnarat, P., 2001, The costs and benefits of diversified business groups: The case of

Korean chaebols, Working paper, University of Wisconsin-Milwaukee.

Geczy, C.G., Minton, B.A., Schrand, C., 1997. Why firms use currency derivatives. Journal of Finance 52,

1323–1354.

Hagelin, N., 2003. Why firms hedge with currency derivatives: An examination of transaction and translation

exposure. Applied Financial Economics 13, 55–69.

Hagelin, N., Pramborg, B., 2004a. Hedging foreign exchange exposure: Risk reduction from transaction and

translation hedging. Journal of International Finance and Management Accounting 15, 1–20.

Hagelin, N., Pramborg, B., 2004b. Empirical evidence on the incentives to hedge transaction and translation

exposure. Working paper, Stockholm University.

Hakkarainen, A., Joseph, N., Kasanen, E., Puttonen, V., 1998. The foreign-exchange exposure

management techniques of Finnish industrial firms. Journal of International Finance and Management

Accounting 9, 34–57.

Hung, M., 2001. Accounting standards and value relevance of financial statements: An international analysis.

Journal of Accounting and Economics 30, 401–420.

Joseph, N.L., 2000. The choice of hedging techniques and the characteristics of UK industrial firms. Journal of

Multinational Financial Management 10, 161–184.

La Porta, R., Lopez-de-Silanes, F., Schleifer, A., Vishny, R.W., 1998. Law and finance. Journal of Political

Economy 106, 1113–1155.

Lel, U., 2003. Currency risk management, corporate governance, and financial market development. Working

paper, Kelley School of Business, Indiana University.

Lim, U., 2001, The choice of ownership structure in conglomerates: An empirical study on the case of chaebols in

Korea. Working paper, Yonsei University.

Marshall, A.P., 2000. Foreign exchange risk management in UK, USA and Asia Pacific multinational companies.

Journal of Multinational Financial Management 10, 185–211.

Myers, S., 1977. The determinants of corporate borrowing. Journal of Financial Economics 5, 147–175.

Nance, D.R., Smith Jr., C.W., Smithson, C.W., 1993. On the determinants of corporate hedging. Journal of

Finance 48, 267–284.

Oxelheim, L., Wihlborg, C., 1997. Managing in the Turbulent World Economy: Corporate Performance and Risk

Exposure. John Wiley and Sons, New York.

Sheedy, E., 2001. Corporate use of derivatives in Hong Kong and Singapore: A survey. Working paper,

Macquarie University.

Smith, C.W., Stulz, R.M., 1985. The determinants of firms’ hedging policies. Journal of Financial and

Quantitative Analysis 20, 391–405.