foreign exchange transaction processing: execution-to ... · pdf fileforeign exchange...

TRANSCRIPT

NondealerParticipants

11

for

Foreign Exchange Transaction Processing:Execution-to-SettlementRecommendations

Introduction ....................................13The Foreign Exchange Market .........................13The Changing Marketplace .............................13What Is the Foreign Exchange Committee

and What Are the Best Practices? .................14How to Use This Document ...........................14

Pre-Trade Preparationand Documentation .........................15

Process Description .........................................15Recommendation No. 1: Determine Foreign

Exchange Needs and DevelopAppropriate Infrastructure ............................15

Recommendation No. 2: EnsureSegregation of Duties....................................16

Recommendation No. 3: DetermineAppropriate Documentation........................16

Trade Execution and Capture ...........18Process Description.........................................18Recommendation No. 4: Establish

Appropriate Trading Policiesand Procedures .............................................18

Recommendation No. 5: Clearly IdentifyCounterparties...............................................19

Recommendation No. 6: Establishand Control System Access..........................20

Recommendation No. 7: Enter Tradesin a Timely Manner.......................................20

Confirmation...................................21

Process Description..............................................21Recommendation No. 8: Confirm Trades

in a Timely Manner........................................21Recommendation No. 9: Block Trades

Should Be Confirmed in a Timely Manner ....22Recommendation No. 10: Resolve

Confirmation Discrepanciesin a Timely Manner .......................................22

Recommendation No. 11: Unique Featuresof Foreign Exchange Options .......................23

Recommendation No. 12: Unique Featuresof Non-deliverable Forwards .......................24

Netting and Settlement ...................25Process Description ........................................25Recommendation No. 13: Net Payments

and Confirm Bilateral Amounts ....................25Recommendation No. 14: Provide Accurate

and Complete Settlement Instructions........26Recommendation No. 15: Use Standing

Settlement Instructions.................................27Recommendation No. 16: Understand Risks

Associated with Third-Party Payments .........27

Account Reconciliation....................28Process Description ........................................28Recommendation No. 17: Perform Timely

Account Reconciliation................................28Recommendation No. 18: Identify

Nonreceipt of Payments and SubmitCompensation Claims in a Timely Manner...29

Accounting and Control...................29Process Description ........................................29Recommendation No. 19: Conduct Daily

General Ledger, Position, and P&LReconciliation...............................................30

Recommendation No. 20: Conduct DailyPosition Valuation.........................................30

Other..............................................31Recommendation No. 21: Develop and Test

Contingency Plans .........................................31Recommendation No. 22: Ensure Service

Outsourcing Conforms to Best Practices......31

Acknowledgments ...........................33

Recommended Readings ..................34

12 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT12

Table of Contents

Execution-to-SettlementForeign Exchange Transaction Processing:

13

Introduction

The Foreign Exchange MarketThe foreign exchange (FX) market is the largest and most liquid sector of the globalfinancial system. According to the Bank for International Settlements’ TriennialCentral Bank Survey of Foreign Exchange and Derivatives Market Activity 2004, FXturnover averages USD 1.9 trillion per day in the cash exchange market and an addi-tional USD 1.2 trillion per day in the over-the-counter (OTC) FX and interest ratederivatives market.1 The FX market serves as the primary mechanism for makingpayments across borders, transferring funds, and determining exchange ratesbetween different national currencies.

The Changing MarketplaceOver the past decade, the FX market has grown in terms of both volume and diversityof participants and products. Although commercial banks have historically domi-nated the market, today’s participants also include investment banks, brokeragecompanies, multinational corporations, money managers, commodity trading advisors,insurance companies, governments, central banks, and pension and hedge funds.In addition, the size of the FX market has grown as the economy has continued toglobalize. The value of transactions that are settled globally each day has risenexponentially—from USD 1 billion in 1974 to USD 1.9 trillion in 2004.

NondealerParticipants

forRecommendations

14 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT

What Is the Foreign ExchangeCommittee and What Are the BestPractices?The Foreign Exchange Committee is an industrygroup sponsored by the Federal Reserve Bankof New York that has been providing guid-ance and leadership to the global FX marketsince its founding in 1978. In all its work, theCommittee seeks to improve the efficienciesof the FX market, to encourage steps toreduce settlement risk, and to supportactions that enhance the legal certainty of FXcontracts.

In 1998, the Committee recognized theneed for a checklist of best practices thatcould help nondealer participants enteringthe FX market to develop internal guidelinesand procedures for managing risk. Theoriginal version of Foreign ExchangeTransaction Processing: Execution-to-SettlementRecommendations for Nondealer Participantswas published in 1999 by the Committee’sOperations Managers Working Group toserve as a resource for market participants asthey evaluate their policies and proceduresregarding FX transactions. This 2004 updatetakes into account market practices that haveevolved since the paper’s original publicationand supersedes previous recommendationsby the Committee regarding nondealerparticipants.

The purpose of this paper is to share theexperiences of financial institutions that areactive in the growing FX market with non-dealer participants that may participate in the

FX market on a more occasional basis. Thetwenty-two issues highlighted are meant topromote risk awareness and provide “bestpractice” recommendations for nondealers.Participants in prime brokerage or similararrangements should also be familiar withthese recommendations. The implementationof these practices may mitigate some of thetrading and operational risks that are specific tothe FX industry. It may also help limit potentialfinancial losses and reduce operational costs.

This document is primarily oriented towardnondealer participants with moderate FXactivities. However, those nondealer parti-cipants that are particularly active in the FXmarket are encouraged to review theCommittee’s guidance to other marketparticipants, specifically the Guidelines forForeign Exchange Trading Activities and theManagement of Operational Risk in ForeignExchange. These documents provide a moredetailed discussion of the business practicesand operational guidelines appropriate toinstitutions with larger or more complex FXactivities. Copies of these papers areavailable on the Committee’s website at<www.newyorkfed.org/fxc>.

How to Use This DocumentThis document is divided into sections basedon the five steps of the FX trade process flow:1) pre-trade preparation, 2) trade executionand capture, 3) confirmation, 4) netting andsettlement, and 5) account reconciliation andaccounting/financial control processes. How

1 Bank for International Settlements, Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity 2004 (Basel: Bank forInternational Settlements, 2004).

15FOREIGN EXCHANGE TRANSACTION PROCESSING

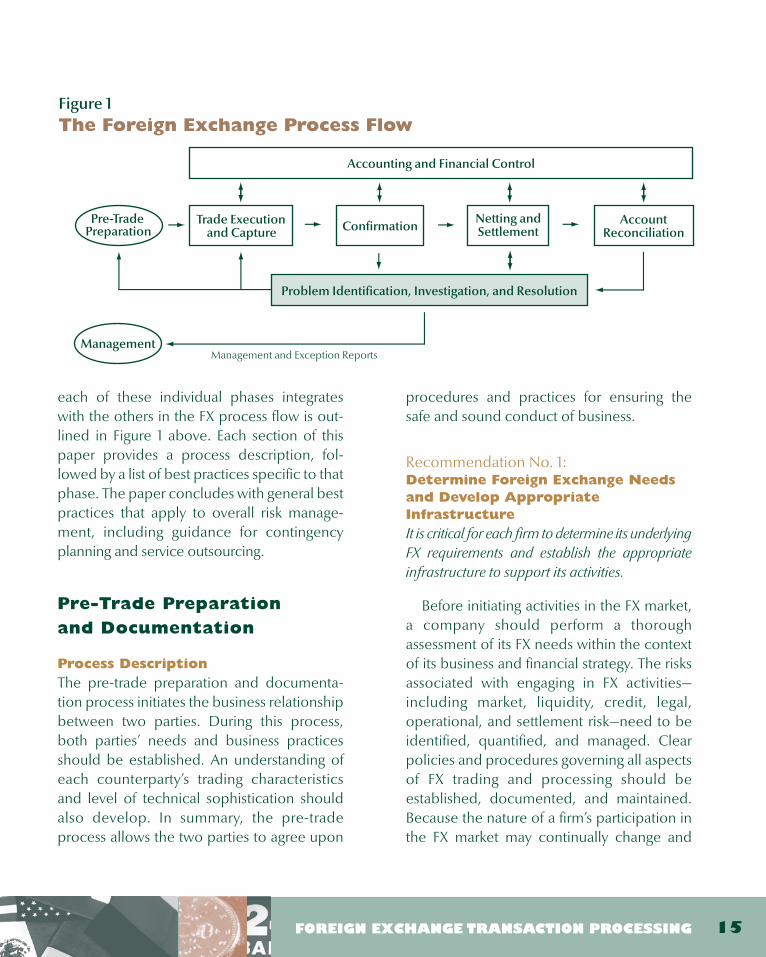

each of these individual phases integrateswith the others in the FX process flow is out-lined in Figure 1 above. Each section of thispaper provides a process description, fol-lowed by a list of best practices specific to thatphase. The paper concludes with general bestpractices that apply to overall risk manage-ment, including guidance for contingencyplanning and service outsourcing.

Pre-Trade Preparationand Documentation

Process DescriptionThe pre-trade preparation and documenta-tion process initiates the business relationshipbetween two parties. During this process,both parties’ needs and business practicesshould be established. An understanding ofeach counterparty’s trading characteristicsand level of technical sophistication shouldalso develop. In summary, the pre-tradeprocess allows the two parties to agree upon

procedures and practices for ensuring thesafe and sound conduct of business.

Recommendation No. 1:Determine Foreign Exchange Needsand Develop AppropriateInfrastructureIt is critical for each firm to determine its underlyingFX requirements and establish the appropriateinfrastructure to support its activities.

Before initiating activities in the FX market,a company should perform a thoroughassessment of its FX needs within the contextof its business and financial strategy. The risksassociated with engaging in FX activities—including market, liquidity, credit, legal,operational, and settlement risk—need to beidentified, quantified, and managed. Clearpolicies and procedures governing all aspectsof FX trading and processing should beestablished, documented, and maintained.Because the nature of a firm’s participation inthe FX market may continually change and

Figure 1The Foreign Exchange Process Flow

Accounting and Financial Control

AccountReconciliation

Netting andSettlementConfirmationTrade Execution

and CapturePre-Trade

Preparation

Problem Identification, Investigation, and Resolution

ManagementManagement and Exception Reports

evolve, policies and procedures should beperiodically reviewed and updated.

All market participants should ensure thatthey engage sufficient experienced personnelto execute the firm’s FX mandate. Each groupor individual playing a role in the FX processflow should have a complete understandingof how FX trades are initiated, recorded,confirmed, settled, and accounted for.Insufficient knowledge of the overall FXprocess, or the role played by each individualor group, can lead to an improper segregationof duties, inadequate controls, and increasedrisk. All market participants should provideongoing employee education regardingbusiness strategies, roles, responsibilities, andpolicies and procedures.

A clear policy on ethics should beestablished, such as a code of conduct thatconforms to applicable laws, good convention,and corporate policies. In particular, theguidelines should address the issue of thereceipt of entertainment and gifts on the partof trading staff and others in a position toinfluence the firm’s choice of counterparties.Senior management should ensure that thepolicies are well circulated, understood, andperiodically reviewed by all personnel. Suchpolicies should be updated regularly toensure they cover new business initiatives andmarket developments.

Recommendation No. 2:Ensure Segregation of DutiesNondealer participants should preclude individualsfrom having concurrent trading, confirmation,payment, and general ledger reconciliation

responsibilities. Reporting lines for trading andoperational personnel should be independent,and management should ensure that appropriatesegregation of duties exists between operationsand other business lines and within operations.

Responsibility for trade execution, tradeconfirmation, payments, and general ledgerreconciliation should be segregated to thegreatest extent possible. At a minimum,responsibility for trade execution should besegregated from responsibility for subsequentprocessing steps. When such duties are notsegregated, the potential for fraud mightincrease. An individual may be able tocomplete unauthorized trades and hide anyresultant losses.

Individuals responsible for confirmation,settlement, and reconciliation must be able toreport any and all issues to managementindependent of the trading function. To do so,operations staff must have a reporting line thatis not subject to an organizational hierarchythat could lead to a compromise of control.Firms with small treasury staffs and an overlapin employee responsibilities should establishand document workflows and systems toprevent unauthorized activities. Such arrange-ments should be periodically verified by anindependent audit function.

Recommendation No. 3:Determine AppropriateDocumentationAn institution should determine its documentationrequirements and know whether those require-ments have been met prior to trading.

16 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT

An institution should begin FX tradingactivities only if it has the proper documen-tation in place. The use of industry standarddocuments is strongly encouraged to provide asound mutual basis for conducting financialmarket transactions. A variety of documentsensure the smooth functioning of the marketsand protect participants in these markets:

� Authority documents address capacity—the right of an institution to enter into atransaction—and authority—permissionfor an individual to act on the institution’sbehalf.

� Confirmations summarize the significanttrade terms and conditions agreed uponby the parties.

� Master agreements contain terms thatapply to broad classes of transactions,expressions of market practice andconvention, and terms for netting, termi-nation, and liquidation.2

� Standard settlement instructions providefor the exchange of payment instructionsin a standardized, secure, and authenti-cated format.

Each institution is responsible for ensuringthat it has the capacity to enter into a trans-action, as well as to monitor and enforcecompliance with its internal proceduresregarding any limitations there may be on the

trading authority of its employees or thirdparties acting on its behalf. Thus, providing todealing firms documentation that includes anumber of investment limitations and restric-tions affecting a participant’s ability to trade andinvest is not consistent with best marketpractice.3

Before executing a master agreement with acounterparty, an institution should alsoestablish a policy on whether or not it willtrade and in what circumstances. It should alsobe noted that electronic trading often requiresadditional or different documentation.Specifically, customer and user identificationprocedures, as well as security procedures,should be documented.

Nondealer participants should be aware thatdealers are likely to be subject to statutory,regulatory, and supervisory requirements for“knowing” their customers. Dealers need toknow the identity of their counterparties, theactivities they intend to undertake with thedealer, and why they are undertaking thoseactivities. While each dealer may havedifferent procedures for implementing theserequirements, nondealer participants shouldcooperate in providing the information thatallows dealers to fulfill these obligations.

17FOREIGN EXCHANGE TRANSACTION PROCESSING

2 The Financial Markets Lawyers Group (FMLG), an industry organization of lawyers representing major financial institutions sponsored bythe Federal Reserve Bank of New York, has helped draft documentation for FX activities, including the International Foreign ExchangeMaster Agreement, the International Foreign Exchange and Options Master Agreement, the International Currency Options MarketMaster Agreement, and the International Foreign Exchange and Currency Options Master Agreement. These documents, endorsed bythe Committee, are available on the FMLG’s and the Committee’s websites, <www.newyorkfed.org/fmlg> and<www.newyorkfed.org/fxc>, respectively.

3 For related guidance on this issue, see the letter to market participants on the Committee’s website.

Trade Executionand Capture

Process DescriptionThe trade execution and capture function isthe second phase of the FX processing flow.Deals may be transacted directly over arecorded phone line or through Internet-based systems (for example, proprietary tradingsystems or multidealer trading platforms).Trade information captured typically includestrade date, time of execution, settlementdate, counterparty, financial instrument traded,amount transacted, price or rate, and mayalso include settlement instructions.

Recommendation No. 4:Establish Appropriate TradingPolicies and ProceduresFirms should endeavor to execute transactions in amanner that reduces the possibility of misunder-standings, errors, or unauthorized dealing. Oncecompleted, FX trades constitute binding obligationsfor both parties. Although subsequent processingsteps (for example, confirmation) may uncoverproblems, the best protection from unanticipatedloss is to avoid problems from the outset.

Transactions should be executed only byinternally authorized staff who are fullyconversant with market practice andterminology. Firms should avoid the use ofobscure market jargon that may lead toconfusion or miscommunication. Whentrades are verbally executed, traders should

carefully reconfirm key terms with thecounterparty before ending the call.

Firms should ensure that all trading isconducted at current market rates. Tradesexecuted at off-market rates can conceallosses, facilitate accounting misstatements, ormask other illegitimate activities. Off-markettrades also involve the extension of creditfrom one party to the other. Nondealerparticipants should establish controls todetect off-market dealing, such as comparingactual trade rates against daily market rangesand reviewing position revaluation results forunreasonable gains or losses.

In certain cases, valid business purposesmay exist for completing off-market trades.Firms intending to complete off-market trades,including historical rate rollovers, shouldprovide counterparties such additionalinformation as is necessary to establish anunderlying business purpose, as well asevidence that such dealing has been reportedto and approved by senior management.4

Responsibilities regarding monitoring andreporting off-market transactions should beclearly defined.

Firms electing to leave orders with FXdealers should establish a clear mutualunderstanding of how such orders will behandled, particularly with respect to fast ordiscontinuous markets or more seriousmarket disruptions. Firms should clearly agreeon the specific terms of the order, particularly

18 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT

4 The Committee’s letter on historical rate rollovers, first published in December 1991, continues to offer sound advice to those who needto execute these transactions. The letter, reprinted in the Committee’s 1995 Annual Report, is available on the Committee’s website,<www.newyorkfed.org/fxc>.

when such orders are activated, canceled, ormodified by the occurrence of subsequentevents. If certain aspects of an order arecontingent upon the achievement of specificmarket levels, firms should agree in advanceupon the rate or price sources to be used insuch determination.

Given the twenty-four-hour nature of theFX market, nondealer participants shouldhave a clear policy on dealing off thepremises or during off-hours. Firms allowingsuch activity should consider institutingprocedures to ensure that trades executedduring off-hours are promptly reported toothers in a prearranged manner (for example,e-mail, voicemail).

Recommendation No. 5:Clearly Identify CounterpartiesAll participants should clearly identify the legalentity on whose behalf they are undertaking atransaction. Trading on an unnamed basis iscontrary to best market practice.

Each counterparty to a transaction shouldensure that its organization recognizes theimportance of clearly and accurately identifyingthe legal entities involved in the transaction.Additionally, firms should encourage staff toprovide their names and affiliation in allcounterparty communication. The benefits ofclear counterparty identification are particularlyevident when:

� the organization has multiple legal entities(subsidiaries, branches, offices, and affili-ates) that are trading in the FX market;

� the organization has been involved inacquisition, divestiture, or restructuringactivity that has led to name changes; and

� participants are transacting in an agencycapacity.

Identification failure raises a number ofpotential risks, including:

� incorrect assessment of counterparty per-formance risk;

� erroneous bookings and/or misdirectedsettlements, creating potential losses foreither counterparty to the transaction;

� misallocation of collateral; or

� disclosure of transaction information toincorrect entities.

The practice of trading FX on an unnamedbasis—also referred to as undisclosed principaltrading—presents an adverse risk to bothindividual market participants and thebroader financial market. Such practicesconstrain a dealer’s ability to assess thecreditworthiness of its counterparties and tocomply with “know your customer” and anti-money-laundering rules and regulations—exposing dealers to clear and significant legal,compliance, credit, and reputational risks aswell as heightening the risk of fraud. It isrecommended that investment advisors anddealers alike implement measures toeliminate the practice of trading on anunnamed basis. Specifically, investmentadvisors and FX intermediaries should developa process to disclose client names to a dealer’scredit, legal, and compliance functions beforethe execution of FX trades.

19FOREIGN EXCHANGE TRANSACTION PROCESSING

Recommendation No. 6:Establish and Control System AccessAs alternative technologies continue to emerge inthe FX trading and processing environments,rigorous controls need to be implemented andmonitored to ensure that data integrity and securityare not undermined. Each system should haveaccess controls that allow only authorized individ-uals to alter the system and/or gain user access.

The use of electronic interfaces among FXmarket participants—such as electroniccommunications networks (ECNs) andautomated trading systems (ATSs)—hasincreased significantly in recent years. Useof robust electronic interfaces is encouragedas it reduces trading- and operations-relatederrors, particularly when trade data flowdirectly from the electronic trading platformto the front-end trading system and to theoperations system books and records in orderto achieve straight-through processing.

To maximize the benefits of thesedevelopments, access to production systemsshould be allowed only for those individualswho require such access to perform their jobfunction. Lack of adequate access controlsand related monitoring can result inunauthorized trading activity. Without properaccess control, the flow of data between theelectronic trading platform and the tradingsystems or back-office books and records canbe altered, compromising data integrity andsubjecting the firm to the risk of financial loss.

System access and entitlements should beperiodically reviewed, and users who nolonger require access to a system should have

their access revoked. Under no circumstanceshould operations or trading functions havethe ability to modify a production system ifthey are not authorized.

Recommendation No. 7:Enter Trades in a Timely MannerAll trades should be entered immediately intoappropriate systems and be accessible for bothtrading and operations processing as soon asthey are executed.

It is crucial that all trades are entered imme-diately so that all systems and processes havetimely, updated information. Front-end systemsthat capture deal information may interfacewith other systems that monitor and updatecredit limit usage, intraday profit and loss (P&L),trader positions, confirmation status, settle-ment instructions, and general ledger activity.

An institution’s ability to manage risk may beadversely affected if it does not have accuratetransaction updates in each of the above-mentioned areas. The failure to recordtrades promptly misrepresents contractualpositions and can result in:

� inaccurate accounting records,

� mismanagement of market risk,

� misdirected or failed settlement, and

� the failure of a trade to be booked at all.

20 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT

Confirmation

Process DescriptionThe transaction confirmation is evidence ofthe terms of an FX or a currency derivativetransaction. Therefore, proper management ofthe confirmation process is an essential control.This process is handled in many ways within FXmarkets. For spot, forward FX, or vanilla cur-rency option transactions, counterpartiesexchange electronic or paper confirmationsthat identify transaction details and provideother relevant information. For structured andnonstandard transactions (for example, non-deliverable forwards [NDFs] and exotic cur-rency option transactions), documents areprepared and 1) exchanged and matched byboth counterparties, in the case of most dealers,or 2) signed and returned in the case of certaincounterparties.5

All confirmations should be subject eitherto the 1998 FX and Currency Option Definitionsissued by the Committee, EMTA, and the Inter-national Swaps and Derivatives Association(ISDA) or to other appropriate guidelines.

Recommendation No. 8:Confirm Trades in a Timely MannerBoth parties should make every effort to sendconfirmations or positively affirm trades withintwo hours after execution and in no event laterthan the end of the day.

Prompt confirmations are key to theorderly functioning of the marketplacebecause they reduce market risk andminimize losses due to settlement errors. In

the absence of timely confirmation, tradediscrepancies may go undetected, which canlead to disputes, disrupting the settlementprocess and increasing processing costs. Suchdiscrepancies can also result in failed tradesor inaccurate accounting records and canadversely affect any underlying securitysettlement. The incidence of error tends toincrease when non-automated or verbalconfirmations are not followed up withwritten or electronic confirmation. Given thesignificance of the confirmation process, it isimportant that the process is handledindependently of the trading function.

Counterparties should have an under-standing regarding confirmation practices,that is, whether they will both send out theirown confirmations, or whether one counter-party will sign and return (affirm) incomingconfirmations. It is not recommended thateither party simply accept receipt of thecounterparty confirmation as completion ofthe confirmation process.

Confirmations should be transmitted in asecure manner whenever possible. In themost developed markets, confirmations aregenerally sent via electronic message througha secure network. Automated confirmationmatches one party’s trade details to itscounterparty’s trade details. It minimizesmanual error and is the most timely andefficient method because it requires nosubsequent confirmation or manual check.

While a significant number of transactionconfirmations are also sent via mail, e-mail, or

21FOREIGN EXCHANGE TRANSACTION PROCESSING

5 Typically, the price maker prepares the confirmation and the price taker signs the confirmation.

fax, it is important to note that when theseopen communication methods are usedthere is a greater risk of human error orfraudulent correspondence. When sendingconfirmations by fax or e-mail, or whenconfirming by telephone, counterparties mayagree to take additional steps to ensure receiptby the correct counterparty. Telephoneconfirmations should be used when no othermethod is available. Following the telephoneconfirmation, both parties should exchangeand match written or electronic confirmations.With verbal confirmations, most dealersemploy recorded telephone lines. Non-dealer participants may want to consideradopting this practice.

Data included in the confirmation shouldcontain the following: the counterparty to theFX transaction, the office through which it isacting, the transaction date (or trade date),the value date (or settlement date), the amountsof the currencies being bought and sold, thebuying and selling parties, and settlementinstructions. Amended confirmations shouldbe sent promptly when necessary. Settle-ment instructions for forward transactionsshould be reconfirmed two days before thesettlement date.

Once a trade between counterparties hasbeen confirmed, such trades may be thesubject of novation or other similar agreements,which should be confirmed in a similarlyvigorous manner.

Recommendation No. 9:Block Trades Should Be Confirmed ina Timely MannerThe full amount of block trades transacted byagents should be confirmed as soon as possible,but always within two hours of the trade execution.

Investment managers or others acting as anagent may undertake “block” or “bundled”trades on behalf of multiple counterparties.Such trades are subsequently split into smalleramounts and apportioned to specific under-lying funds or counterparties. The failure toallocate a block trade on a timely basis couldresult in increased credit, legal, and operationalrisk. Specifically, a delay in allocation hampersthe allocation and management of creditexposure. Trade confirmation will also bedelayed, which in turn may interrupt thesettlement process and, in extreme cases, causepayment failures.

The full amount of block trades should beconfirmed as soon as possible but always withintwo hours of trade execution. Allocations andconfirmations to individual obligor accountsshould be completed within four hours andno later than the end of the day on the tradedate. To minimize errors caused by manualintervention, trade allocations should, ifpossible, be provided to the counterpartyelectronically, either through a securenetwork or through authenticated means.

Recommendation No. 10:Resolve Confirmation Discrepanciesin a Timely MannerDiscrepancies between a confirmation receivedfrom a counterparty and a firm’s own recordsshould be brought to the counterparty’s attention

22 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT

immediately. Escalation procedures should beestablished to resolve any unconfirmed or dis-puted deals.

When trade discrepancies exist,unintended exposure to market risk mayarise. Trade discrepancies may also lead toincreased processing costs, inaccurateaccounting records, failed settlements(including underlying transactions), andfinancial loss. Unconfirmed trades may resultfrom simple trade entry errors or more seriousdisagreements between counterparties withrespect to the agreed-upon transaction terms.

To mitigate this risk, confirmation discre-pancies should be brought to the counterparty’sattention immediately and resolved as quicklyas possible. Additionally, procedures should beestablished to escalate unresolved discre-pancies to increasingly higher levels ofmanagement within established time frames.Automated trade confirmation systems arestrongly recommended; these systems canhighlight discrepancies and mitigate potentialproblems. Processes should be in place todetect chronic discrepancies.

Recommendation No. 11:Unique Features of Foreign ExchangeOptionsMarket participants should establish clear policiesand procedures for the confirmation, exercise, andsettlement of FX options and familiarize staff withthe additional terms and conditions associatedwith options.

FX options are more complex productsthan spot and forward transactions. Optionsincorporate additional and often complex

contract terms (such as strike price, call or putindicator, premium price, and expiry date andtime). Their value is determined not only byspot and forward exchange rates but also byimplied volatilities and time remaining untilexpiration. Option values may change rapidlyand in a nonlinear manner. Those optionspossessing intrinsic value at expiration (strikerate more favorable than current market orindex rate) must be properly exercised if suchvalue is to be realized. The exercise of anoption generally creates a new position in theunderlying instrument (for example, spotdollar-yen) requiring further processing andsettlement.

Special attention should be paid to the saleof options (short positions), which generallyentail significantly higher levels of market risk.Similarly, management should be aware that“deep-in-the-money” option transactions bytheir nature involve unusual funding require-ments and related credit exposure. There maybe legitimate reasons for the sale of suchoptions—for example, the “sell back” of anoption or the implied delta within a separatederivatives product. However, it should berecognized that the sale of deep-in-the-moneyoptions can be used to exploit weaknesses in acounterparty’s revaluation or accountingprocess that could create erroneous results.Procedures should ensure an appropriate levelof review—if necessary, by senior tradingmanagement or risk management outside thesales and trading area—to guard againstpotential legal, reputational, and other risks.

Management should clearly define rolesand responsibilities to ensure that the higherinherent risk of options is well controlled.

23FOREIGN EXCHANGE TRANSACTION PROCESSING

Operations staff should be fully versed inoptions terminology, contract provisions, andmarket practice. Transaction terms should beelectronically, or at least verbally, confirmedon the trade date and both parties should signa detailed confirmation. Certain exoticoptions may also require the collection ofadditional information or rates, depending onthe product.

Premium settlements should be closelymonitored to reduce the potential for out-trades.

Clear policies and procedures related tothe exercise of options should be establishedand, where possible, documents and systemsshould be designed to auto-exercise expiringin-the-money options. It is recommendedthat, whether or not auto-exercise applies,both parties independently monitor theiroption positions for internal market andoperational risk management purposes.

Recommendation No. 12:Unique Features of Non-deliverableForwardsMarket participants should establish clear policiesand procedures for the confirmation and set-tlement of FX NDFs and familiarize staff withthe additional terms and conditions associatedwith NDFs in order to reduce operational risk.

NDFs are cash-settled FX instruments thatrequire a rate fixing to determine the amount

and direction of the cash settlement. NDFs,like options, have additional trade terms andrequire additional handling and processing.In addition, they may be more susceptible tomarket disruptions.

Counterparties should confirm NDFtransaction terms electronically, or at leastverbally, on the trade date. In addition to thestandard transaction details (such as thecounterparties and the offices through whichthey are acting, the transaction date, thenotional amount of the currencies, andsettlement instructions), NDFs involveadditional trade terms that requireconfirmation, such as fixing source and date.Following telephone confirmation, bothparties must validate, review, sign, and returnthe long-form confirmation to cover allnonfinancial information. Confirmationsshould be reviewed on the trade date todetermine the fixing source, and transactionsshould be reviewed daily thereafter to ensurethat fixings are obtained as required in theconfirmation language.

When possible, counterparties are encour-aged to use an addendum to an existing masteragreement, indicating a set fixing rate for eachcurrency.6 On the fixing date, fixing advicesthat reflect the fixing rate and cash settlementamount should be generated and exchangedelectronically (when possible).

24 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT

6 The Master Agreement Addendum for Non-deliverable Forwards is available online at the Committee’s public website.

Netting and Settlement

Process DescriptionSettlement is the exchange of payments betweencounterparties on the value date of the transaction.Bilateral settlement netting is the practice ofcombining all trades between two counterpartiesdue on a particular settlement date and calcu-lating a single net payment in each currency. Forexample, if an institution executes twenty-fivedollar-yen trades with the same counterparty, allof which settle on the same day, bilateral settle-ment netting will enable the institution to makeonly one or two netted payments.7 These nettedpayments will generally be much smaller thanthe gross settlement amount due. The establish-ment of settlement netting agreements betweencounterparties can thus reduce settlement risk,operational risk, and clearing costs.

Various market utilities support multilateralsettlement netting, which involves combiningall trades between multiple counterpartiesand calculating a single net payment in eachcurrency.

For counterparties that do not settle on anet basis, payment instructions are sent tonostro banks for all the amounts owed—aswell as for expected receipts. Settlementinstructions are sent one day before settle-ment, or on the settlement date, dependingon the currency’s settlement requirements. Ifa settlement error occurs in the process, it is

typically quite costly. If a company fails tomake a payment, it must compensate itscounterparty, thus generating additionalexpense. Settlement errors may also cause aninstitution’s cash position to be different thanexpected.

In addition, settlement risk—the risk that acompany makes its payment but does notreceive the payment it expects—can cause alarge, even catastrophic, loss. This risk arises inFX trading because payment and receipt ofpayment often do not occur simultaneously. Aproperly managed settlement function reducesthis risk. Settlement risk is measured as the fullamount of the currency purchased and ispresent from the time a payment instruction forthe currency sold becomes irrevocable untilthe time the final receipt of the currencypurchased is confirmed.8 Sources of this riskinclude internal procedures, intramarketpayment patterns, finality rules of localpayments systems, and operating hours of thelocal payments systems when a counterpartydefaults.

Recommendation No. 13:Net Payments and Confirm BilateralAmountsTransaction payments should be netted wheneverpossible. Legal agreements should provide for set-tlement netting as well as “close-out” netting in theevent transactions are terminated before maturity.

25FOREIGN EXCHANGE TRANSACTION PROCESSING

7 Participants may also conduct “novational netting,” which nets trades across currency pairs. For example, a dollar-yen trade and a euro-dollar trade may be netted for a single dollar payment.

8 For additional information on settlement risk, see Foreign Exchange Committee, “Defining and Measuring FX Settlement Exposure,” inForeign Exchange Committee 1995 Annual Report (New York: Federal Reserve Bank of New York, 1996), and Foreign Exchange Committee,“Reducing FX Settlement Risk,” in Foreign Exchange Committee 1994 Annual Report (New York: Federal Reserve Bank of New York, 1995).

Settlement on a gross basis not onlyincreases the actual number of settlements thatare necessary but also increases the probabilityof settlement errors. An enforceable settlementnetting agreement has the benefit of entitlingparties to reduce the number and size ofpayments between themselves.

The operational process of settlementnetting should be supported by a legalagreement. Such an agreement may be a briefdocument that only supports settlementnetting or a settlement netting provision that isincluded in a master agreement. Thefollowing master agreements have beendeveloped as industry standard forms. Eachform includes provisions for settlementnetting (included as an optional term) andclose-out netting:

� International Swaps and DerivativesAssociation (ISDA) Master Agreement,

� International Foreign Exchange MasterAgreement (IFEMA) covering spot andforward currency transactions,

� International Currency Options MarketMaster Agreement (ICOM) covering cur-rency options, and

� International Foreign Exchange andOptions Master Agreement (FEOMA)covering spot and forward currency trans-actions and currency options.

Correct calculations of netted paymentsare important to ensure accurate settlementamounts and enhance the efficiency ofoperations. All market participants areencouraged to automate the actual nettingcalculation so that errors introduced by

manual calculation are reduced. To protectagainst an improper settlement of a netamount, counterparties should confirm thenet payment amount with each other at somepredetermined cutoff time before settlement.Parties should establish the latest possiblecutoff time for confirming bilateral nettedamounts. Such a deadline will ensure that theparties agree on the transactions included inthe net amounts.

In addition to settlement netting, masteragreements may provide for close-outnetting. Close-out netting clauses provide for1) appropriate events of default, includingdefault upon insolvency or bankruptcy;2) close-out of all covered transactions;and 3) the calculation of a single netobligation from unrealized gains and losses.Close-out netting provisions providesignificant risk management benefits to bothparties to a master agreement by providing forthe netting of all outstanding transactionsunder an agreement. Master agreements withlegally enforceable close-out netting receivebankruptcy and insolvency law protection toensure that the defaulting counterpartyremains responsible for all existing contractsand transactions under the agreement andnot just those it chooses. Thus, close-outnetting provisions provide the legal basis forparties to measure counterparty exposure ona net rather than a gross basis.

Recommendation No. 14:Provide Accurate and CompleteSettlement InstructionsMarket participants should always provide com-plete and accurate settlement instructions in atimely manner.

26 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT

Settlement instructions should clearlyreference the following information:

� the recipient’s account name, accountaddress, and account number;

� the name of the receiving bank, a SWIFT/ISO address, and a branch identifier; and

� the identity of any intermediary bank usedby the recipient.

Incomplete or inaccurate settlementinstructions heighten the risk of a disruptedsettlement process, thus inflating processingand compensation costs. Failed FX settlementsmay also disrupt completion of an underlyingtransaction.

Recommendation No. 15:Use Standing Settlement InstructionsStanding settlement instructions (SSIs) should beexchanged whenever possible. Market partici-pants should issue new SSIs, as well as changesto SSIs, in a secure manner.

SSIs allow for complete trade details to beentered quickly so that the confirmationprocess can begin as soon as possible aftertrade execution. By removing the need toexchange settlement instructions solely on atrade-by-trade basis, SSIs minimize thepotential that incorrect or incompletesettlement instructions will be exchanged. SSIsalso contribute to improved risk managementand greater efficiency because the repeatedmanual inputting, formatting, and confirming ofsettlement instructions increases the cost oftrade processing and heightens the opportunityfor errors in settlement.

Market participants should exchangestanding settlement instructions as soon aspossible. When an institution changes its SSIs,it should provide as much lead time aspossible—a minimum of two weeks’ notice—to its counterparties to allow them to updatetheir records before the new SSIs becomeeffective. Institutions should update theirrecords promptly when changes to SSIs arereceived from their counterparties.

All standing settlement instructions shouldbe delivered electronically, if possible, andpreferably through authenticated mediabecause electronic delivery minimizesmanual error and is the timeliest method ofdelivery. In addition, authenticated mediareduce the potential for fraud. Changes toSSIs that cannot be delivered electronicallyshould be delivered in writing and signed byan authorized individual.

Although SSIs are preferred, they are notalways available and may not be appropriatefor all trades. When SSIs are not used, thesettlement instructions may be recorded atthe time of trade execution. These exceptionsettlement instructions should be deliveredby the close of business on the trade date (ifspot) or at least one day before settlement (ifforward).

Recommendation No. 16:Understand Risks Associated withThird-Party PaymentsIn cases where a dealer agrees to process a third-party payment, nondealer participants shouldprovide the information necessary for the dealerto internally approve and accurately make thepayment.

27FOREIGN EXCHANGE TRANSACTION PROCESSING

Third-party payments are the transfer ofsettlement funds for an FX transaction to theaccount of an entity other than the counter-party to the transaction. Third-party paymentsraise important issues that should beconsidered carefully by a firm requesting sucha practice.

Participants should recognize that third-partypayments may significantly increase operationalrisk and potentially expose all involved tomoney laundering or other fraudulent activity.The practice also heightens the risk of financialloss; if the third-party payment is directed to anincorrect beneficiary, the payment may bedelayed or even lost. Third-party payments mayalso create potential legal liability to the dealermaking the payment.

Both nondealers and dealers should beaware of the risks involved with thesetransactions and should establish clearprocedures beforehand for validating boththe authenticity and correctness of suchrequests. In addition, nondealer participantsshould provide dealers with any writteninformation required to screen, internallyreview and approve, and accurately make thethird-party payment. For example, writteninformation may include the third party’sreceiving bank name and address; the thirdparty’s account name, address, and number;and the nature of the third party’s affiliationwith the nondealer participant.

Also, third-party payment instructionsshould be provided via authenticated means.Instructions otherwise provided—for example,by phone or fax—should be reconfirmed bystaff independent of those providing suchinstructions.

Account Reconciliation

Process DescriptionAccount reconciliation occurs at the end ofthe trade settlement process to ensure that atrade has settled properly and that all expectedcash flows have occurred. An institutionshould begin reconciliation as soon as itreceives notification from its bank that pay-ments are received. If possible, reconciliationshould be performed before the paymentsystem associated with each currency closes.Early reconciliation enables an institution todetect any problems in cash settlement andresolve them on the settlement date.

Recommendation No. 17:Perform Timely AccountReconciliationAccount reconciliation—the process of comparingexpected and actual cash movements—should beperformed as early as possible.

The main objective of the accountreconciliation function is to ensure thatexpected cash movements agree with theactual cash movements in a firm’s currencyaccounts. The cause for the difference might bethat wrong settlement or trade information wascaptured or that a payment error occurred.

Failure to reconcile expected and actual cashmovements could result in the inability torecognize the underfunding of a transactionand/or an overdraft to the cash account. Whencash is used to overfund a position, opportunitycosts arise because cash often cannot beinvested. When positions are underfunded,overdraft charges may be imposedunknowingly. Account reconciliation also

28 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT

serves as a main line of defense in detectingfraudulent activity.

All market participants are encouraged toreconcile expected cash flows against actualcash flows in a timely manner. The soonerreconciliations are performed, the sooner aninstitution can take appropriate actions toensure that its accounts are properly funded.

Recommendation No. 18:Identify Nonreceipt of Payments andSubmit Compensation Claims in aTimely MannerManagement should establish procedures fordetecting nonreceipt of payments and for notify-ing appropriate parties of these occurrences.Escalation procedures should be in place fordealing with counterparties that fail to makepayments. Parties that have failed to make a pay-ment on a settlement date should arrange for theproper value to be applied and pay compensa-tion costs promptly.

An institution should attempt to identify, asearly in the process as possible, any expectedpayments that are not received. Failure tonotify counterparties of problems in a timelymanner may lead them to dismiss claims thatare over a certain age, causing the institutionto absorb overdraft costs.

All instances of nonreceipt of paymentshould be reported immediately to thecounterparty’s operations and/or tradingunits. When necessary, escalation proceduresshould be followed. Management may wishto consider a limited dealing relationship withcounterparties that have a history of settle-ment problems. The counterparty that has not

received payment generally incurs the costsassociated with nonreceipt, including thoseassociated with obtaining alternative fundingon the settlement date, processing theexception, and administering payment. As aresult, the counterparty may commence legalaction to recover these costs. Compensationclaims for nonreceipt or late receipt ofpayment should be agreed upon and paidexpeditiously.

Accounting and Control

Process DescriptionThe accounting function ensures that FXtransactions are properly recorded on thebalance sheet and income statement. Iftransaction information is not recorded cor-rectly, a company’s reputation may be tarnishedif material restatements of financial accountsare necessary.

Accounting entries are first bookedfollowing the initiation of a trade. At the endof each trade day, all sub-ledger accountsflow through to the general ledger. Anydiscrepancies should be investigated as soonas possible to ensure that the institution’sbooks and records reflect accurate infor-mation. The accounting area should ensurethat outstanding positions are continuallymarked to market until close-out—afterwhich realized gains and losses arecalculated and reported.

Cash flow movements that take place onsettlement date are also posted to the generalledger in accordance with accepted accountingprocedures. The receipt and payment of

29FOREIGN EXCHANGE TRANSACTION PROCESSING

expected cash flows at settlement arecalculated in an institution’s operations system.

Recommendation No. 19:Conduct Daily General Ledger,Position, and P&L ReconciliationSystematic reconciliations of both the generalledger to the operations system and the tradingsystems to the operations systems should bedone daily.

Timely reconciliations will allow for promptdetection of errors in the general ledgerand/or sub-ledgers and should minimizeaccounting and reporting problems. Thisreconciliation will ensure that the generalledger presents an accurate picture of aninstitution’s market position. When problemsare detected, they should be resolved as soonas possible. Senior management should benotified of accounting discrepancies toreview and update control procedures asneeded.

Position reconciliations allow an institutionto ensure that all managed positions are thesame as those settled by operations. Thiscontrol is imperative when all deal entries andadjustments are not passed electronicallybetween trading and operations. Whenstraight-through processing is in place, thereconciliation ensures that all deals weresuccessfully processed from trading tooperations, along with all amendments.Because a discrepancy in P&L between tradingand operations can indicate a difference inpositions or market parameters (that is, rates orprices) all differences should be reported,investigated, and resolved in a timely manner.

Recommendation No. 20:Conduct Daily Position ValuationUsing independent price sources, staff independentof the trading function should revalue outstand-ing positions to market daily. This is particularlyimportant for market participants that are activein less liquid forward markets or in exotic optionsmarkets. Both trading and operations staffshould be familiar with the procedures used forposition valuation.

The daily revaluation of outstandingpositions is an integral part of the controlprocess. The end-of-day rates and prices thatare used to create the position valuationsshould be periodically checked by anindependent source. Staff independent of thetrading function should ensure that the ratesand prices used for end-of-day valuationrepresent market rates. Position valuationsshould be verified using independent sourcessuch as market rate screens or broker/dealerquotations.

Illiquid markets present additional risk toan institution because illiquid instruments aretraded infrequently, making them difficult toprice. Often, it is difficult to obtain marketquotes, thereby preventing timely andconsistent position monitoring. Valuations maybe distorted, causing improper managementof risk. In such instances, a company shouldseek to obtain quotes from other counter-parties active in the market. Managementshould be aware of these procedures so that itmay effectively manage and evaluate illiquidmarket positions. These procedures allow aninstitution to mark to market its positions andto evaluate associated risks.

30 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT

Marking to market reflects the current valueof FX cash flows to be managed and providesinformation about market risk.9 Seniormanagement will be able to better manage andevaluate market positions when it knowspositions are accurately valued on a daily basis.

Other

Recommendation No. 21:Develop and Test Contingency PlansParticipants should develop plans for operatingin the event of an emergency. Contingency plansshould be periodically reviewed, updated, andtested.

In the event of a major disaster, a marketparticipant may not be able to meet itsobligation to monitor its market positions. Itmay also fail to meet its obligation to settleand confirm transactions. Inability to trade orsettle transactions could subject the marketparticipant to severe financial and reputationalrepercussions.

Firms should identify various types ofpotential disasters and examine how they maydisrupt the participant’s ability to satisfy itsobligations (that is, issuing and receivingconfirmations, performing settlements, andcompleting daily trading). Disaster recoveryplans should identify requisite systems andprocedural backups, management objectives,staffing plans, and the methodology fordealing with each type of disaster. Plansshould be reviewed and tested periodically.

Backup sites that can accommodate theessential staff and systems should be estab-lished, maintained, and tested on a regularbasis. Particularly for operations, marketparticipants should consider developing abackup site that relies on a separate infra-structure (electricity, telecommunications, andso forth).

Additionally, all market participants shouldidentify alternative methods of confirmationand settlement communication and practicethese methods with counterparties. Suchmethods may require the use of fax or telex toensure proper processing. During a disaster, afirm should notify its counterparties ofpotential processing changes. It should alsoprovide counterparties with current contactinformation for key personnel to ensure thatcounterparties can contact the firm in anemergency.

Recommendation No. 22:Ensure Service OutsourcingConforms to Best PracticesIf an institution chooses to outsource a portion orall of its operational functions, it should ensurethat its internal controls and industry standardsare met. A firm that outsources should have ade-quate operational controls in place to monitorthe outsourcer and to ensure that functions arebeing performed according to agreed-uponstandards and industry best practices.

An institution may choose to outsourcesome or all of its operations functions.However, outsourcing should neither

31FOREIGN EXCHANGE TRANSACTION PROCESSING

9 Group of Thirty, Global Derivatives Study Group, Derivatives: Practices and Principles (Group of Thirty, 1993), p. 19.

32 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT

compromise a firm’s internal standards forconfirmations, settlement, and payments nordiminish the responsibility of the firm toensure settlement performance.

Controls should be in place to monitorvendors to ensure that internal standards aremet. For example, trades should still beconfirmed in a timely manner and properescalation and notification procedures muststill be followed.

Participants should establish procedures toperiodically monitor service providers toensure that they are performing functionsaccording to agreed-upon standards andindustry best practices. A service levelagreement should be in place to clearlyidentify responsibility in case of failure tomeet obligations.

33FOREIGN EXCHANGE TRANSACTION PROCESSING

Charles LeBrunBank One

Philip ScottBank of New York

Kathryn WheadonBank of America

AcknowledgmentsThis document was originally prepared in 1998 by a task force composed of members of the ForeignExchange Committee and the Operations Managers Working Group. The task force included:

The task force for the 2004 revision included:

Joe DemetrioBank of New York

Laura HuiziFederal Reserve Bankof New York

Sandra GalarzaBank of New York

Barry McCarraherHSBC

Keith McDonaldCSFB

Michael NelsonFederal Reserve Bankof New York

Nancy RiyadHSBC

Richard RuaMellon Bank

Daniel RupertoGoldman Sachs & Co.

Robert ToomeyFederal Reserve Bankof New York

Diane VirzeraFederal Reserve Bankof New York

34 FOREIGN EXCHANGE COMMITTEE 2004 ANNUAL REPORT

Bank for International Settlements. TriennialCentral Bank Survey of Foreign Exchange andDerivatives Market Activity 2004. Basel: Bank forInternational Settlements, 2004.

Emerging Markets Traders Association, ForeignExchange Committee, International Swaps andDerivatives Association, New York ClearingHouse Association, Public Securities Association,and Securities Industry Association. “Principlesand Practices of Wholesale Financial MarketTransactions.” 1995.

Foreign Exchange Committee. “Defining andMeasuring FX Settlement Exposure.” In ForeignExchange Committee 1995 Annual Report. NewYork: Federal Reserve Bank of New York, 1996.

———. “Guidelines for FX Settlement Netting.” InForeign Exchange Committee 1996 Annual Report.New York: Federal Reserve Bank of New York,1997.

———. “Guidelines for the Management of FX TradingActivities.” In Foreign Exchange Committee 2000Annual Report. New York: Federal Reserve Bankof New York, 2001.

———. “Management of Operational Risk in ForeignExchange.” In Foreign Exchange Committee 2003Annual Report. New York: Federal Reserve Bank ofNew York, 2004.

———. “Reducing FX Settlement Risk.” In ForeignExchange Committee 1994 Annual Report. NewYork: Federal Reserve Bank of New York, 1995.

———. “Standardizing the Confirmation Process.”In Foreign Exchange Committee 1995 AnnualReport. New York: Federal Reserve Bank of NewYork, 1996.

———. “Supplementary Guidance on ElectronicValidations and Confirmation Messaging.” InForeign Exchange Committee 2001 Annual Report.New York: Federal Reserve Bank of New York,2002.

Foreign Exchange Committee and FinancialMarkets Lawyers Group. “Guide for TransactionsInvolving Intermediaries.” 1998.

Recommended Readings