forestry commission: timber harvesting and marketing · forestry commission: timber harvesting and...

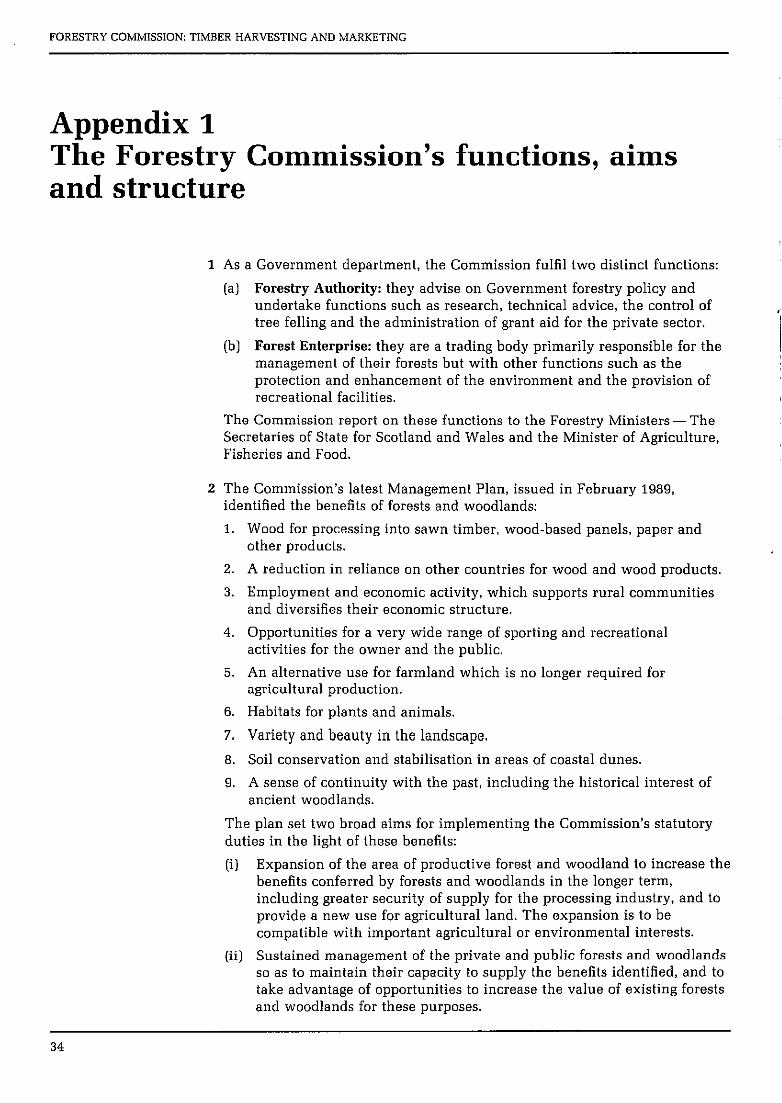

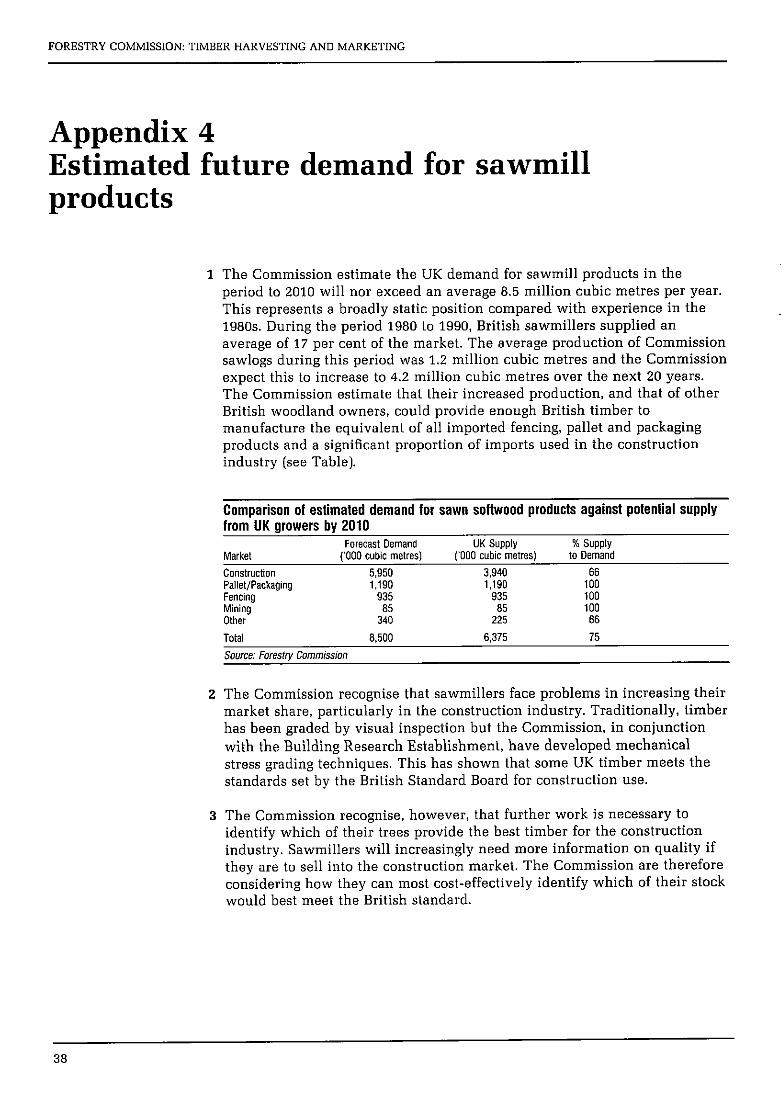

TRANSCRIPT

NATIONAL AUDIT OFFICE

REPORT BY THE

COMPTROLLER AND

AUDITOR GENERAL

Forestry Commission: Timber Harvesting And Marketing

ORDERED BY THE HOUSE OF COMMONS TO BE PRINTED 1 MARCH 1993

LONDON: HMSO 526 f8.15 NET

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

This report has been prepared under Section 6 of the National Audit Act, 1983 for presentation to the House of Commons in accordance with Section 9 of the Act.

John Bourn Comptroller and Auditor General

National Audit Office 24 February 1993

The Comptroller and Auditor General is the head of the National Audit Office employing some 900 staff. He, and the NAO, are totally independent of Government. He certifies the accounts of all Government departments and a wide range of other public sector bodies; and he has statutory authority to report to Parliament on the economy, efficiency and effectiveness with which departments and other bodies have used their resources.

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

Contents

Page

Summary and conclusions 1

Part I: Introduction 6

Part 2: Planning timber production 9

Part 3: Timber harvesting 19

Part 4: Marketing 26

Part 5: The effects of harvesting and marketing on the forest asset 32

Appendices

1. The Forestry Commission’s functions, aims and structure

2. The age structure and species of the forestry Commission’s forests

3. Comparison of the types of information included in the Commission’s and other forestry organisations’ forest inventories

4. Estimated future demand for sawmill products

34

36

37

38

The Forestry Commission manage 900,000 hectares of forest valued at f2.8 billion

FORESTRY COMMISSION: TlMBER HARVESTING AN,, MARKETING

Summary and conclusions

1 The Forestry Commission are a Government department responsible for forestry throughout Great Britain. They report to Forestry Ministers and are responsible for promoting the interests of forestry, establishing and maintaining adequate reserves of growing timber, and producing timber; and for achieving a balance between the needs of forestry and the environment. Although the Commission’s forest operations are small compared with major overseas timber producers they are the largest UK timber producer and manage 900,000 hectares of forest estate with an expected value of f2.8 billion. In 1991-92 the cost of harvesting and marketing timber was E46 million and the Commission’s timber sales yielded income of D3 million. Production is expected to double to 7 million cubic metres of timber by the year 2010.

2 The Commission’s forests and forestry estate supply timber to the wood using industries, provide opportunities for recreation, enhance nature conservation and the forest environment and contribute to the conservation of Britain’s woodland heritage. In planning the harvesting of timber the Commission take account of Ministerial statements made in 1988 on the benefits of restructuring uniform aged forests. They also seek a balanced approach to attaining their wider objectives while optimising the financial return from the production of timber. The Commission draw together information from across their operations on tree growth, prices, timber stocks, market needs, financial targets, landscaping and conservation considerations to provide a production plan of the areas of forest to be felled and a forecast of how much timber this will produce for the market. This plan is translated at local forest level into a production programme detailing which forest areas are to be cut down. Finally, trees are felled and the timber is sold.

3 Against this background the National Audit Office examined how the Commission determine the level of timber to harvest; whether they have identified the most economic and efficient methods of harvesting and how successfully the methods are applied and how they identify markets for, and sell, their timber products. The National Audit Office employed Jaakko Payry - a firm of Finnish-based international forestry consultants-to provide advice on forestry matters. In view of the international nature of the forestry industry and the Forestry Commission’s unique position within the United Kingdom, the National Audit Office drew on published information on Canadian forests and also visited forestry organisations overseas; ie the Irish Forestry Board (Coillte Teoranta), the Swedish Board of Forestry, Domanverket (Swedish Forest Enterprise), Stora (Sweden and Europe’s largest commercial forestry organisation), and Uppsala Stift [a Swedish municipal forest authority). The main findings and conclusions are presented in the following paragraphs.

Planning timber production

4 Most of the Commission’s forests were planted in the last 50 years and have not yet reached maturity. The Commission have developed a production planning system which combines information on the crop growth, timber

1

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

prices and growing stock levels, in order to forecast the volume and source of timber available for harvesting. The Commission’s production plan consists of a 20-year forecast of timber production and forest areas which are to be felled.

5 The Commission assess the age at which the theoretical maximum economic return will be achieved for different trees using a yield modelling methodology which is recognised within the forest industry. Yield models are designed to enable the Commission to forecast yield on sites that have not previously carried trees, and are constructed from information collected from permanent sample plots. Although the Commission have reviewed their modelling data gathered from the sample plots since the 1960s for changes in trends, they have not found it necessary to review the existing models. In 1989 the Commission began to develop a new methodology for calculating and validating models. Yield models are now being revised and will incorporate all the data collected since the last major revision.

6 Details of the Commission’s growing stock are held in a forest inventory. This was originally established to support their production planning system and has evolved into a wider management information system. The inventory currently contains information to assess the volume of timber expected from the growing stock but some overseas forestry organisations hold more detailed information in their inventory. This is partly due to the different approaches to forest planning but the Commission accept the case for considering cost-effective additions to their inventory to improve the operation of their planning system.

7 Production plans are refined by forest managers to reflect the local effect of wind damage, environmental considerations and differences between actual and recorded stock levels. The Commission consider that it is not possible to manage forests in accordance with multi-purpose objectives and achieve the theoretical maximum economic return on timber production. They produce general guidance on adjustments to be made to refine plans and have also issued instructions on environmental requirements and the consequent costs managers might incur. Because of the difficulty of identifying non-financial benefits they rely on management judgement to provide assurance that forests are being managed economically and efficiently.

8 The National Audit Office found that monitoring arrangements did not always provide cost analysis or other evidence to support local decisions. A National Audit Office analysis of 2,300 forest areas revealed that as a result of such changes by local management 49 per cent of trees were being felled on average more than five years before or after their age of theoretical maximum economic return. As the Commission had not calculated the consequent overall effect of environmental and other factors on their revenue, ihe National Audit Office made an asssessment which indicated that decisions to alter production plans could represent E5.6 million a year in notional income foregone, or 8 per cent of the value of timber harvested.

9 By continuing to refine their yield models and considering additions to their inventory of growing stocks the Commission could improve their production plans. They also need a better basis for monitoring local decision which alter production plans to judge whether the benefits are commensurate with the level of income foregone.

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

Timber harvesting 10 Circumstances can change after production plans are completed due to market conditions, wind damage, and the need to deal with differences between estimated production from forest areas and the volume and mix of timber actually available. A National Audit Office comparison of 1991-92 district production programmes against the latest production plans showed that, on average, 50 per cent of the timber intended for harvesting in local progammas was to be obtained from forest areas not scheduled for harvesting in the first five years of the Commission’s plans. Although the Commission expected circumstances to change, they have not been consistently monitoring or analysing variations between plans and local programmes. The National Audit Office found it was not possible to identify the full extent of variations between production plans and actual production but they compared the ages of trees planned to produce timber during 1990-91 with the ages of trees actually harvested. This showed that, on average, the trees felled were three to five years younger than those planned to be harvested. This could have represented income foregone of E5.2 million in that year in addition to the income foregone at the planning stage.

11 A Commission analysis of estimated and actual output in a selection of forest areas concluded that actual output was within IO per cent of the volume expected. But this was an average which masked variations of 40 per cent between expected and actual output in many individual forest areas. The National Audit Office consider that, without a formal system to monitor variations which occur between sources and volume of timber harvested and those planned, the Commission do not have an adequate basis to determine the reasons for and benefits derived from the changes in planned production and to achieve the optimum balance between wood production and their other objectives.

12 Since 1980 the Commission have reduced the unit cost of timber harvesting by 42 per cent in a period when timber production doubled. This has been achieved through the development of improved working systems, increased use of contractors and the introduction of more advanced mechanised harvesting. The Commission have been particularly innovative in adapting Scandinavian equipment to meet British conditions and modifying standard construction equipment as a less costly alternative to specialist machinery.

Marketing and sales methods

13 The Commission have a statutory responsibility to develop the wood processing industry and during the 1970’s and 1980’s they were involved in studies to identify the type of wood processing best suited to timber produced in Britain and how wood processing industries might be attracted to this country. The Commission have identified the need to provide a secure supply of wood to that industry and consequently their marketing strategy is based on a general commitment that the volume of timber in the production forecast will be offered to the market at prevailing prices. Unlike some overseas forest organisations, the Commission are not directly involved in the wood processing industry but, by negotiating long-term contracts for supply, the Commission have successfully encouraged the timber processing industry to develop to match increased Commission and private sector production. The marketing strategy has therefore been successful and, despite two major recessions in the last 20 years, they have produced and sold the volume of timber forecast. The development of export markets in the early 1980’s and the attraction of El billion of new investments in wood processing during that period were notable successes.

3

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

14 The Commission sell their timber by auction, competitive tender and negotiation. Timber is offered to the market as standing trees (to be harvested by the customer), or as logs felled and cut by the Commission for roadside collection. Over the last 10 years the Commission have achieved the best profits from standing sales and have set an objective to increase the proportion of timber sold in this way.

15 The Commission’s volume based market strategy has encouraged the industry to develop. However, as timber prices fluctuate there can be difficulty in pursuing specific targets for financial return. While their market strategy has been flexible in response to significant changes in market conditions during the past decade it is equally important to consider how future plans to increase production will be responsive to changes in trading conditions. Early completion of the market audit would be a first step in this process. The Commission should also continue to monitor the relative advantage of different methods of sale and consider developing a more stable relationship between expected production and forward sales through longer-term contracts.

Effects on the forest asset

16 The Commission face a major challenge in reconciling the demands of financial and non-financial objectives. Managing and harvesting their forests and marketing timber provide considerable national benefits, but they are difficult to quantify. The Commission are required to achieve a three per cent rate of return on the 50-60 year life cycle of the timber crop. They show the extent to which they expect to meet the target through triennial revaluations of their forests. Because of the difficulties inherent in recording all costs associated with individual forest areas over the life of the crops, the Commission regard it as impacticable to evaluate the rate of return actually achieved in forest areas which have been harvested.

17 Although operational targets are being achieved, local level changes, which the Commission consider reflect their wider objectives, have led to timber being produced by felling trees before and after their age of economic maturity and from areas outside their harvesting plans. The Commission’s strategic planning system is not intended to provide an exact forecast of available timber in individual forest areas and does not therefore provide a sufficiently reliable picture of timber volume for operational planning. The Commission nevertheless agreed that there was a need to improve the relationship between plans and actual production. It is important that these factors are controlled more closely to ensure that the longer term management of the Commission’s forest assets achieves the right balance between its economic and environmental potential. The Commission accept that monitoring and control of the source and volume of timber harvested should be improved to take full account of the longer term interests of the forest asset and to demonstrate whether it is being maintained at its required level.

18 The Commission’s marketing strategy has led to a commitment to provide forecast volumes of timber to the market, which they have met. The National Audit Office consider that improvements to the system of production forecasting are necessary to reduce the level of variation between the strategic forecast of production and the timber actually

4

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

General conclusion

harvested. Attention to this will ensure that the potential for timber income, in so far as it is consistent with other objectives, will be optimised and the Commission can then demonstrate that the forest asset is managed to its full economic and environmental potential.

19 The Commission’s harvesting and marketing activities make major contribution to the achievement of their overall forestry and other objectives. They have achieved significant economies over recent years in the cost of producing timber. But in the longer term interest of the forest asset, attention must be given to reducing the disparity between timber production plans and the sources of timber actually harvested. Planned increases in timber production could accentuate this problem. The Commission therefore need to address these questions while they increase output from the forests as they intend over the next decade.

5

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

Part 1: Introduction

Background to the Forestry Commission

1.1 The Forestry Commission were established in 1919 to provide the United Kingdom with a strategic reserve of growing timber and have, over the years, acquired additional commercial, social and environmental objectives. Under legislation now consolidated mainly in the Forestry Act 1967. the Commission are responsible for promoting the interests of forestry, establishing and maintaining adequate reserves of growing trees and producing timber. The Act was amended by the Wildlife and Countryside [Amendment) Act 1985 to provide the Commission with an additional statutory duty to seek to achieve a balance, in carrying out their functions, between the needs of forestry and the environment. The Commission’s functions, aims and structure are set out at Appendix 1.

Harvesting and marketing

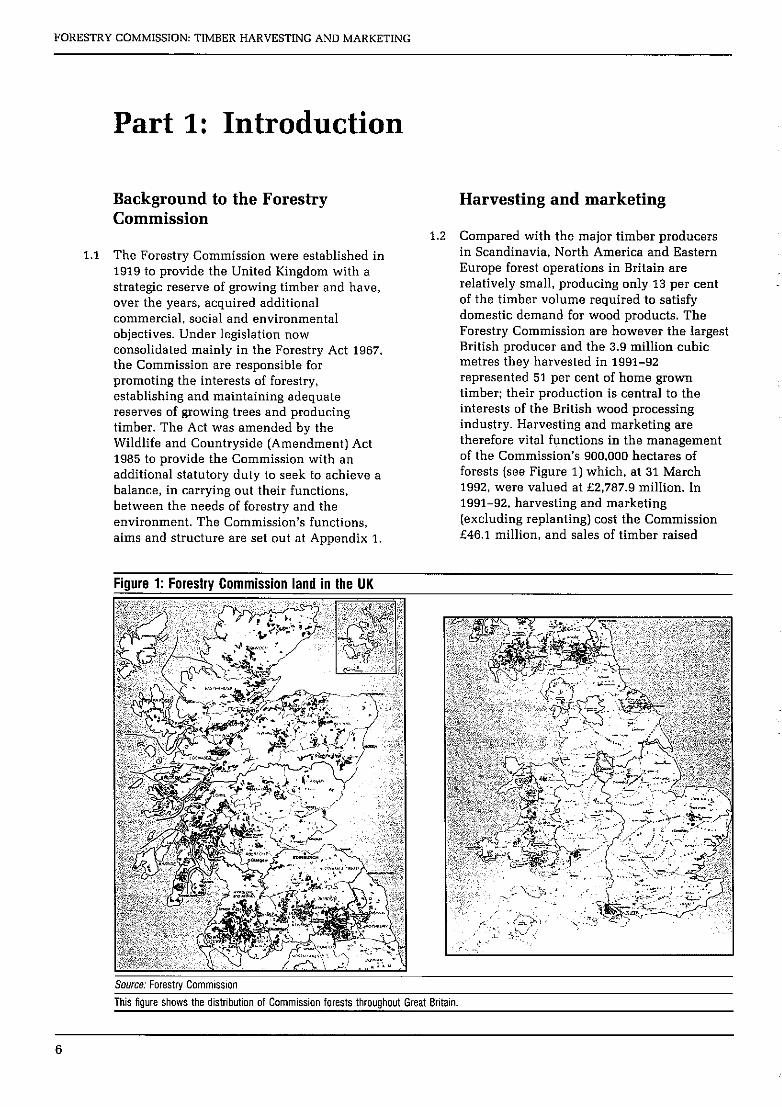

1.2 Compared with the major timber producers in Scandinavia, North America and Eastern Europe forest operations in Britain are relatively small, producing only 13 per cent of the timber volume required to satisfy domestic demand for wood products. The Forestry Commission are however the largest British producer and the 3.9 million cubic metres they harvested in 1991-92 represented 51 per cent of home grown timber; their production is central to the interests of the British wood processing industry. Harvesting and marketing are therefore vital functions in the management of the Commission’s 900,000 hectares of forests (see Figure 1) which, at 31 March 1992, were valued at f&787.9 million. In 1991-92. harvesting and marketing [excluding replanting) cost the Commission 646.1 million, and sales of timber raised

Figure 1: Forestry Commission land in the UK

Source: Forestry Commission

This figure shows the distribution of Commission forests throughout Great Britain.

6

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

7273.3 million of the Commission’s total operating income of f83.3 million.

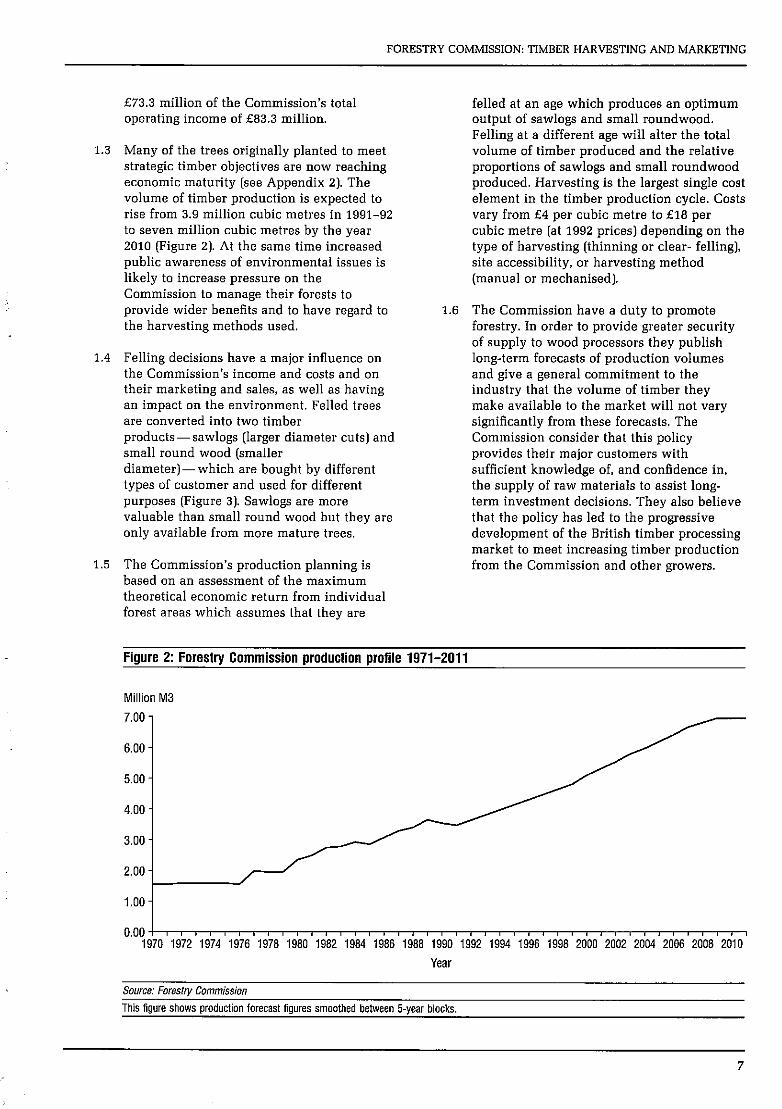

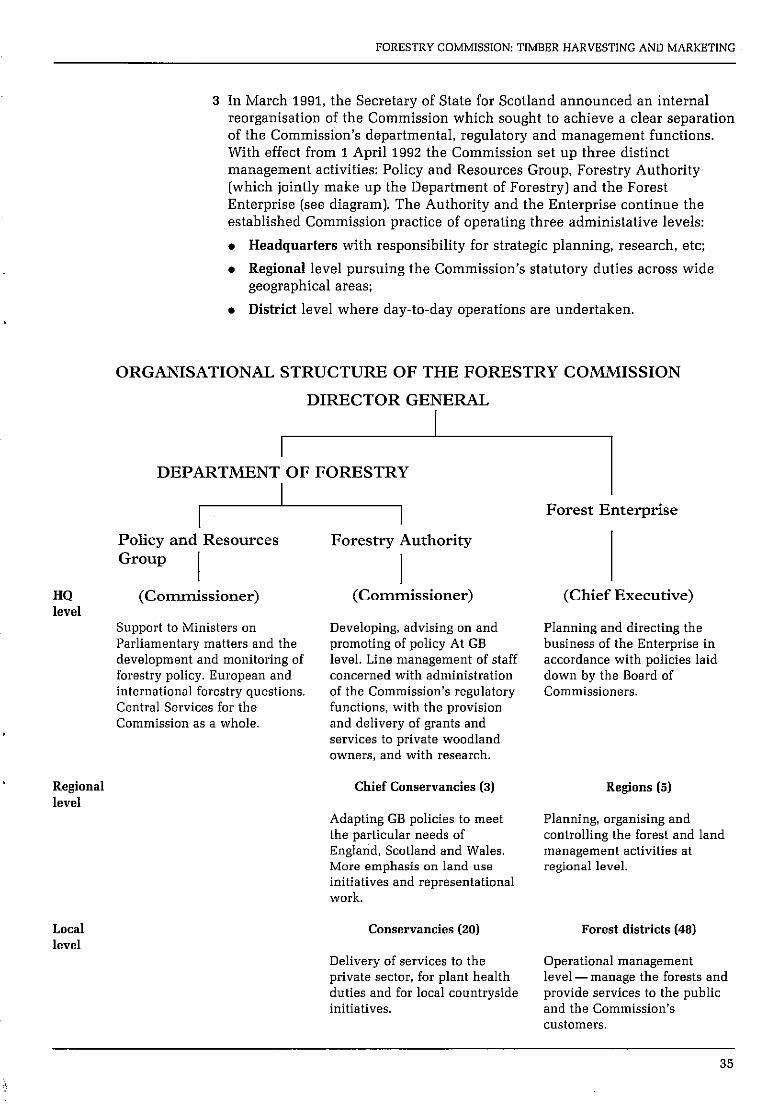

1.3 Many of the trees originally planted to meet strategic timber objectives are now reaching economic maturity (see Appendix 2). The volume of timber production is expected to rise from 3.9 million cubic metres in 1991-92 to seven million cubic metres by the year 2010 (Figure 2). At the same time increased public awareness of environmental issues is likely to increase pressure on the Commission to manage their forests to provide wider benefits and to have regard to 1.6 the harvesting methods used.

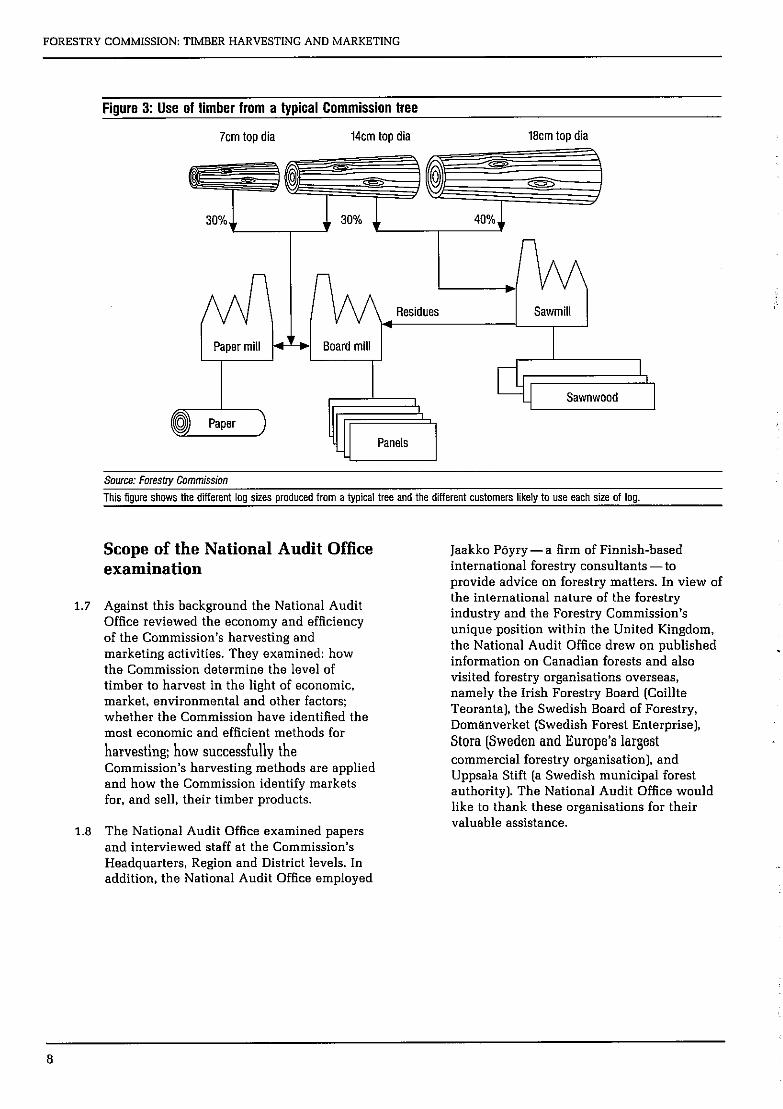

1.4 Felling decisions have a major influence on the Commission’s income and costs and on their marketing and sales, as well as having an impact on the environment. Felled trees are converted into two timber products-ssawlogs (larger diameter cuts) and small round wood (smaller diameter)-which are bought by different types of customer and used for different purposes (Figure 3). Sawlogs are more valuable than small round wood but they are only available from more mature trees.

1.5 The Commission’s production planning is based on an assessment of the maximum theoretical economic return from individual forest areas which assumes that they are

felled at an age which produces an optimum output of sawlogs and small roundwood. Felling at a different age will alter the total volume of timber produced and the relative proportions of sawlogs and small roundwood produced. Harvesting is the largest single cost element in the timber production cycle. Costs vary from f4 per cubic metre to 618 per cubic metre [at 1992 prices) depending on the type of harvesting (thinning or clear- felling), site accessibility, or harvesting method (manual or mechanised).

The Commission have a duty to promote forestry. In order to provide greater security of supply to wood processors they publish long-term forecasts of production volumes and give a general commitment to the industry that the volume of timber they make available to the market will not vary significantly from these forecasts. The Commission consider that this policy provides their major customers with sufficient knowledge of, and confidence in, the supply of raw materials to assist long- term investment decisions. They also believe that the policy has led to the progressive development of the British timber processing market to meet increasing timber production from the Commission and other growers.

Figure 2: Forestry Commission production profile 1971-2011

Million M3

7.00 -

6.00

5.00

4.00

3.00

2.00

1 .oo i

0.00-I I8 I I I I I I I I I I I I I I I I I I I I I I I I a I I

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Year

Source: Forestry Commission

This figure shows production forecast figures smoothed between 5.year blocks.

7

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

1.7

1.8

Figure 3: Use of timber from a typical Commission tree

7cm top dia 14cm top dia 18cm top dia

I

Residues

Y v

Sawmill

Source: Fore&y Commission This figure shows the different log sizes produced from a typical tree and the different customers likely to use each size of log.

Scope of the National Audit Office examination

Against this background the National Audit Office reviewed the economy and efficiency of the Commission’s harvesting and marketing activities. They examined: how the Commission determine the level of timber to harvest in the light of economic, market, environmental and other factors; whether the Commission have identified the most economic and efficient methods for

harvesting: how successfully the Commission’s harvesting methods are applied and how the Commission identify markets for, and sell, their timber products.

The National Audit Office examined papers and interviewed staff at the Commission’s Headquarters, Region and District levels. In addition, the National Audit Office employed

Jaakko Pdyry--a firm of Finnish-based international forestry consultants-to provide advice on forestry matters. In view of the international nature of the forestry industry and the Forestry Commission’s unique position within the United Kingdom, the National Audit Office drew on published information on Canadian forests and also visited forestry organisations overseas, namely the Irish Forestry Board (Coillte Teoranta), the Swedish Board of Forestry, Dominverket (Swedish Forest Enterprise), Stora [Sweden and Europe’s largest commercial forestry organisation), and Uppsala Stift (a Swedish municipal forest authority]. The National Audit Office would like to thank these organisations for their valuable assistance.

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

Part 2: Planning timber production

2.1 Trees are a unique biological raw material with a natural life span (for conifers growing in Britain) of over 100 years although in order to maximise the investment return, trees in managed forests are normally harvested when they are 50 to 60 years old. Effective forest management requires a clear understanding of overall forestry objectives, based on a sound knowledge of the growing crop and its potential value, to identify when particular forest areas should be felled. Trees may be harvested by thinning young crops (ie removing trees from a plantation to encourage growth and quality in the remainder of the crop) or clear felling of forest areas (removal of all trees).

2.2 Most modern forests are managed to meet multi-purpose objectives comprising a financial return from timber production and non-financial objectives such as conservation and the environment. In addition, a range of external factors arising from the cultural and economic importance of forestry in different countries can influence which timber is harvested. For example, Swedish and Finnish forest owners are required to operate within statutory constraints designed to limit the volume and age of timber felled in any year to ensure a permanent yield of timber from the forest asset which is high in both quantity and quality. Thus, objectives in those countries for financial return, conservation and the environment are constrained by the limits on the volume of timber which the law allows to be felled.

2.3 The Commission do not operate in such a restricted environment; there are no statutory constraints cm the volume of timber which they may harvest. Subject to their duty to seek a balance between timber production and the environment the Commission decide the priorities between individual forestry objectives.

The production planning system

2.4 Managing forests in Britain presents special problems. The Commission are required. for their own forests, to achieve a specific

financial return on the asset whilst meeting other non-financial objectives. However, most of the Commission’s forests were planted in the last 50 years and have not yet reached maturity. Consequently, the Commission have no complete coverage of growth patterns upon which to base predictions of future yields from the timber crop. The Commission have therefore developed a production planning system based upon the information available from permanent plots established up to 70 years ago. This system combines information on crop growth, timber prices and stocking levels. in order to indicate the volume and source of timber available for harvesting. This production planning system forms the basis of the Commission’s strategic and operational planning.

2.5 The Commission’s production planning system is intended to inform felling decisions in the light of their overall objectives. This system produces a production plan of the individual forest areas to be felled in each five year period of a rolling ZO-year production plan. The areas range in size from less than one hectare to uver 20 hectares and the plan is accompanied by a forecast of timber production in each five-year period. The Commission produce forecasts of average annual timber production which they publish in summary form for the benefit of the timber trade.

2.6 The three primary components of the production planning system are: a series of yield models characterising tree growth: historic information on prices which, when applied to yield models, indicates when trees should be felled; and an inventory of the growing timber stock. This information is combined to produce an initial theoretical forecast of optimum production which is refined at three further stages to produce production plans (schedules of areas to be felled in individual forests) and the production forecast (Figure 4). The Commission use the refinements in stages 2-4 of the planning system to take account of their financial and non-financial objectives and the outcome of stage 4 should provide a

9

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

Figure 4: Forestry Commission harvesting planning system

Stage 1 -Theoretical forecast of optimum production A computer program compares information in an inventory of growing trees against models the Commission have developed to assess the age at which different categories of trees will produce the maximum economic return and assessment of the potential wind damage based on the

nature and location of the trees to produce a theoretical forecast of optimum production

Stage Z-local crop management refinements Provides for local district level managers to amend the standard models to better reflect local conditions and plans ongoing from previous

forecasts. This stage is frequently used to change thinning prescriptions which have arisen from landscape and conservation plans.

Stage 3-Local reffnements to felling proposals Provides local managers with the opportunity to refine further felling proposals

Stage 4-Marketing reffnements Takes account of the effect of marketing constraints on the forecast. These are most likely to arise because forecasts revised at Stages 2 and 3 may prevent the Commission fulfilling commitments given to the market in earlier, published forecasts. This stage may also reflect specific market information (eg the opening of a large pulp mill would have a significant influence an the overall market demand for Smaller diameter

logs).

The Production Plan at all management levels analyses the total volume forecast by species, volume, assortment, period, thinning/felling and type of model used. In addition, it provides data on the area felled and in the case of district level reports schedules stands due in each period for

thinning. first thinning or felling.

I Published Production Forecast

Aggregates total available volume. Used by the Commission to give the timber industry a commitment as to future

production levels

I I

Harvesting programme Using the schedules from the Production Plan

local data from crop measurements and operational plans the local managers build up

harvesting programmes which satisfy operational efficiency and sales commitments

Source: Forestrv Commission

This figure shows the four stages of production planning which lead to the Production Forecast. the Production Plans and Harvesting Plans.

strategic overview of production as well as a framework of information for detailed operational planning.

National Audit Office examination

2.7 The production plan and production forecast provide the Commission with management information for valuing their forest estate; informing their market planning; planning the efficient use of harvesting resources; and appraising the management of their forests. Development of the plan and forecast relies upon a range of information and assumptions on crop behaviour and the National Audit Office therefore examined the adequacy of the information used in preparing this vital stage in the timber harvesting and marketing p*ClCiXS.

Yield modelling

2.8 As trees grow the volume of timber they are capable of producing increases but the rate of growth slows down as trees become older. For a given discount rate, the maximum economic return is achieved if trees are

felled when the discounted revenue obtainable from the volume of timber available ceases to increase despite extra volume gained by further growth.

2.9 The Commission assess the age of maximum economic return for different trees using a yield modelling system. They categorise trees in terms of species, growth rate and forest management treatments which have been applied to them. The Commission have developed tables which predict the volume of timber expected from each category of tree at different felling ages. They apply this information to the estimated discounted price for the volume and mix of timber produced to establish the value expected from trees in

10

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

2.10

2.11

Figure 5: Discounted value curve for a typical Forestry Commission conifer crop

Pounds (f)

3500 4 35 40 45 50 55 60 65 70

Age

Source: Forestrv Commission

This figure shows the net discounted value of one hectare of 35 year old Sitka Spruce Non-thin Yield class 12 in Scotland using a 6% discount rate: the age of maximum discounted revenue is 50 years.

each category at different ages. The age at which discounted value ceases to increase is regarded as the point of maximum economic return (except for trees planned to be felled earlier to avoid wind damage). Stage 1 of the production planning system indicates when each forest area should theoretically be felled to achieve maximum economic return (Figure 5).

The National Audit Office found that the Commission’s use of age, volume and price data to assess the maximum economic return was a recognised methodology within the forest industry. Research in Sweden is seeking to introduce price probability into the methodology. The Commission have confidence in their historical price records and do not regard the Swedish research as sufficiently conclusive for them to consider changes to their system.

The Commissions most recent yield tables were drawn up during the 1960s from detailed statistical analysis of information on crop behaviour gathered from 1,500 sample forest areas and they published a full set of tables for all categories of commercial softwood trees in 1977. They maintain smne 800 of the sample plots to provide further information on crop behaviour to inform and enhance their models. Although the Commission have reviewed their modelling

2.12

2.13

data gathered from sample plots since 1966 for changes in trends, they have not found it necessary to revise the existing models. In 1989, the Commission launched a project to develop new methodologies for constructing and validating yield models “sing more advanced statistical techniques and available computer technology. Yield models are now being revised to incorporate data collected since the last major revision.

The Yield tables generally assume specific management treatment of crops-either that trees have been thinned in accordance with specified timetables or that no thinning has taken place. But during the 1970s and 1980s marketing difficulties for the small round wood produced by thinning caused the Commission to cancel or delay thinning in many areas. Consequently, some forest areas do not fit into the standard yield models which they have developed. It is therefore important that local managers identify such forest areas and make appropriate adjustments to yield assumptions.

The Treasury set the Commission a 3 per cent real rate of return target on their plantations. They also provide guidance on the test discount rates for public sector bodies’ investment appraisals, but leave the Commission to determine the rate of return for assessing optimum felling ages. In 1972

11

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

2.14

2.15

2.16

the Commission adopted a 5 per cent discount rate for this purpose based on the Treasury guidance at the time. Since then the Treasury rate has varied significantly hut the Commission have maintained their 5 per cent rate because fluctuations would in their view result in short-term changes to felling ages which are not conducive to good long-term forest management or the sustained supply of timber to the wood processing industry.

Forestry inventory

In 1974 the Commission computerised the record of their growing stock. This record was developed to provide information on growth potential in individual forest areas to compile strategic production forecasts and as a management information system for operational planning.

The Commission’s central inventory details the growing timber stock in all their forests across scune 200,000 individual geographical units, though the information may vary for each geographical unit. The inventory record provides key data on individual groups of trees (such es age, species, and growth rate) and optional data on site conditions (such es soil type and the risk of wind damage). The record is updated annually from returns made by district managers of changes resulting from clear-felling and planting. Changes may also result from field surveys conducted on a 15 year cycle. The surveys are intended to confirm species and age and give an early indication of growth rate (for trees up to 15 years old); provide a check on growth rate and indications of factors likely to affect production volume (for trees aged

from 15 to 30 years): and give a final reliable estimate of growth rate prior to inclusion of the crop in the 20 year production forecast [for trees Over 30 years).

The National Audit Office found that forest inventories maintained by the werseas organisations visited contained mnre detailed information than the Commission’s inventory. This was because the Commission used their yield models to forecast growth rates in their maturing forests whereas the other organisations sought to identify timber available from their forests from the

2.17

2.16

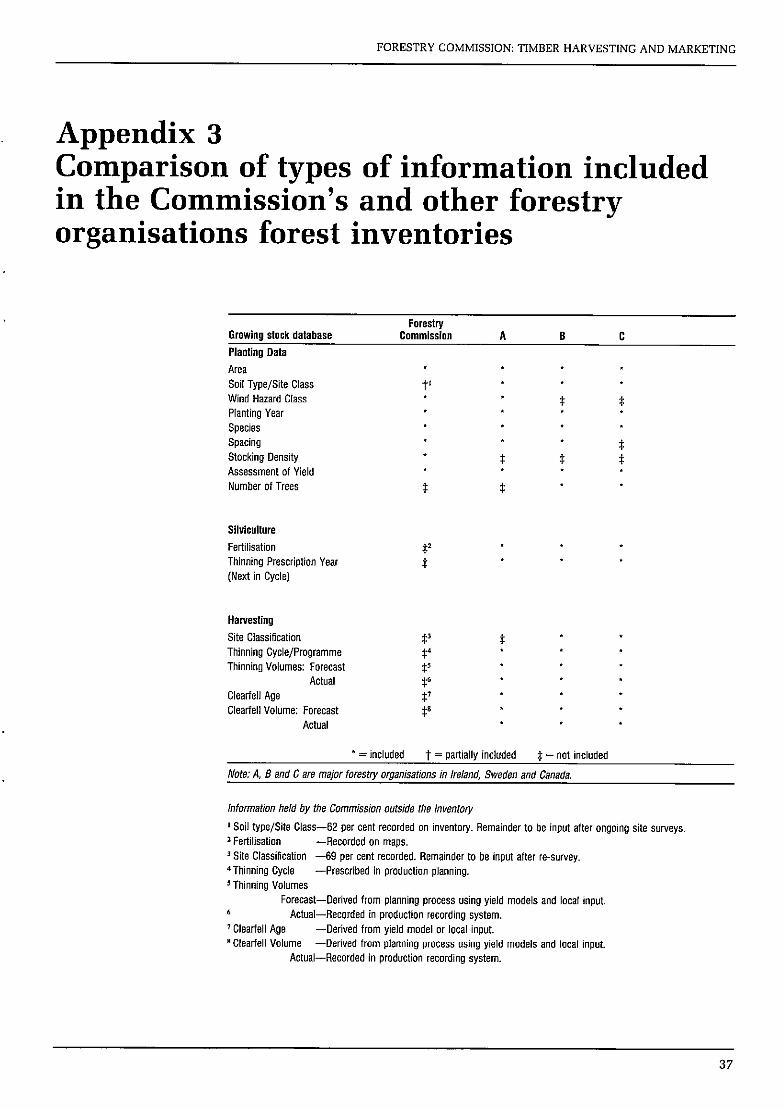

inventory. The overseas inventories included, for each forest area, measurements of the volume of growing timber, the number and height of trees, and the volume and number of trees removed. This additional information reflected the need for mnre accurate information of expected production volumes imposed on Scandinavia in planning to meet statutory felling limits. But the National Audit Office considered that sane of the additional information might be necessary to the Commission for effective operation of their planning system. An analysis of the information held by the Forestry Commission and by other organisations is at Appendix 3. The Commission accept the case for considering cost-effective additions to their inventory to improve the operation of their planning system.

The Commission’s 15 year survey cycle is longer than that applied in most countries with slower growing trees. The Commission cycle of three or four surveys in the 50 to 60 year life-span of their trees was established mainly on cost grounds. In Sweden, where most trees felled are river 100 years old, surveys are conducted on average every 10 years to provide the detailed forest inventory they require. A similar level of accuracy in forecast timber output in Britain would probably require surveys at less than 10 year intervals.

The Commission told the National Audit Office that their survey cycle reflects their different planning methodology and that their system is suited to the particular circumstances of a maturing forest resource in Britain. Whilst the Swedish system required accurate assessments of volume

available to meet statutory limits on harvesting, the Commission’s strategic assessment of volume did not require that level of detail. Their modelling system provided strategic assessment of likely output and, although the production plan was intended to form a framework for operational planning, they recognised that the actual volume available at forest area level would vary. They expected forest managers to inspect the areas listed for timber production before taking final decisions on felling to ensure that the forecast volume of timber was actuallv available.

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

2.19

Maps

Maps are essential for the efficient and effective management of forests. The Commission maintain a large number of forest maps which they update manually to reflect management decisions. The overseas organisations visited by the National Audit Office had invested in computer generated mapping equipment which they judged to be nmre efficient than manual mapping. Computerised mapping can also be linked to the computcriscd forest inventory and be automatically updated to reflect changes in forests. The Commission had considered the introduction of computerised mapping scnne years ago but had rejected it because they considered the technology available at that time was neither efficient nor cost effective. They have now recognised the recent advances in technology and are therefore reconsidering the benefits which might be available.

Effects of windblow

Source: Forestry Commission

Forest hillside which has suffered windblow.

2.20

2.21

2.22

2.23

Planning for potential wind damage

When today’s mature forests were planted some 40 to 60 years ago to meet strategic timber reserve objectives, much of the land available to the Commission for new forests was on exposed upland areas in the north and west of England, Scotland and Wales. These areas have soils which, while generally fertile, are frequently water-logged or shallow and thus prevent development of strong rwx systems. The combination of soil limitations, high altitude and exposure to high winds, make trees in these areas vulnerable to being blown over as they grow higher. They are not expected to reach the same height as trees grown in nmre favourable conditions and their age of economic maturity is therefore assessed as being earlier.

The Commission have heen researching the effects of wind in forest areas for sxne 40 years. They have devised a system (the Windthrow Hazard Classification) for assessing the risk of wind damage to trees on the basis of four specific site factors: the general trend for wind in the geographic area; height above sea level: exposure to prevailing winds and soil conditions. They then categorise individual forest locations into six bands, according to the assessed risk of wind damage.

The Commission consider the risk and cost of damage in the highest wind risk categories justifies some anticipatory felling. The production planning system therefore assumes that trees at most risk from wind will be felled at a height-known as terminal height -at which the Commission estimate some 40 per cent of the crop in the locality are likely to have been blown down. The Commission have placed scme 55 per cent of their forest area in these high wind risk categories.

The wind hazard classification system is a broad means of classifying forest areas according to their inherent vulnerability to wind and of predicting the tree height at which damage is expected to occur. The Commission recognise that damage occurs in individual forest areas which does not accord with wind risk predictions. The actual effect of wind on trees may deviate from the Commission’s predictions because of

13

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

inadequate or revised data on which sites are classified; the uncertain and unpredictable nature of winds in upland Britain; and the degree to which the terminal heights may vary regionally. The Commission’s research in eight wind monitoring areas indicated that the actual degree of damage matched their predictions in 51 per cent of cases.

2.24 The scale of forest area susceptible to wind damage presents the Commission with special problems. They therefore recognise the importance of continuing research to improve their ability to forecast terminal heights. The Commission’s on-going research into wind hazard is intended to identify predictable risk from normal wind against which management can take precautions. It does not address abnormal gales [such as that experienced by South-East England in October 1987) for which it is impossible to plan. The Commission analyse information from eight wind monitoring areas and, using data from crop surveys, reappraise terminal heights.

2.25

2.26

The National Audit Office noted that historic records of windblow at forest or district level are rare and considered that there may be a need for more reliable data on how wind damage progresses through individual forest areas in order to devise more flexible guidance for forecasting. Figure 6 shows the difference in value between crops felled at lower heights because of their susceptibility to wind damage, and the value of those felled at a greater height and age. Better records of the development of wind damage would assist local managers in establishing evidence to improve decisions on changes to predicted terminal heights.

Local management input to production plans

The Commission issue guidance to managers on how to make adjustments to stage 1 of the planning system and those factors which might influence adjustments. Some regional managers supplement this guidance with

Figure 6: Comparison of the discounted value of a typical Commission crop at heights specified for felling to avoid wind damage and at maximum economic return

Height (metres)

25 - f556 fS97

Risk of wind : Hiohest damage -

Felling age (371

f942

1471

Insignificant risk, can attain age of maximum economic return

Source: National Audit Office

This figure shows the discounted value of trees felled early to avoid wind damage.

14

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

2.27

2.28

more detailed instructions to forest district managers on specific issues likely to affect their areas. Forest district managers make adjustments to the system directly, and where appropriate are expected to consult regional offices. The adjustments made at each stage of the planning system are reviewed by regional and Headquarters staff.

The National Audit Office examined the contribution to the harvesting planning process made by six of the Commission’s 48 forest districts. The results of the examination indicated that the main reasons for local level adjustments to the Commission Headquarter’s initial [Stage 1) plans were: re- assessment of terminal heights for wind damage; the effect of catastrophic wind blow; changes to felling ages for environmental reasons; refinements to reflect differences between actual and recorded local levels of timber stocks: and changes intended to improve the management of forests and to create felling areas which are operationally efficient. The National Audit Office noted that discussion had taken place between districts and other levels of the Commission in the context of these changes, but that the monitoring arrangements were not applied consistently and that decisions to adjust production plans were not always supported by cost analysis or other evidence. The National Audit Office therefore examined the major factors which had influenced adjustments to the harvesting plans.

Wind hazard

Local managers frequently adjusted harvesting plan assumptions on tree height for high wind risk crops. The National Audit Office calculated that, of 430,000 hectares in high wind-risk areas, local adjustments had led to some 230,000 hectares being planned for felling at stages other than predicted terminal height. Of these areas, some 112,000 hectares were planned to be felled after the trees would reach terminal heights. Local managers were therefore accepting the risk of wind damage well beyond the age contained in guidance issued by the Commission. In some forest districts this was supported by limited research. The Commission told the National Audit Office that guidance on windthrow hazard classification is based on the best available information but cannot be regarded as absolute. They consider that

2.29

2.30

2.31

local managers should recommend changes to terminal height where crops are observed to stand beyond the level of predicted damage implicit in the windthrow classification system. Decisions to extend terminal heights are normally taken after discussion with senior management and Research Division.

Environment

Changes to production plans for environmental reasons fell into three general categories:

Landscaping reflected a commitment by the Commission to enhance the natural beauty of forest landscapes. The effect this work can have depends on the sensitivity of the landscape and the visual impact of harvesting activity.

Restructuring is carried out to convert uniform age forests into more attractive and varied landscapes in accordance with Ministerial requirements. It also helps to smooth peaks and troughs in production when large forest areas reach economic maturity age at the same time.

Conservation reflects the Commission’s concern to maintain a varied selection of wildlife in the forests and areas of other interest such as archaeological sites.

The Commission have published statements stressing their statutory and other environmental responsibilities. In 1977 and in 1985 they issued instructions to forest managers on environmental requirements and the consequent costs they might incur. The instructions gave no guidance, however, on the priority to be afforded to environmental and other objectives in local circumstances.

In 1988, Ministerial statements highlighted the benefits of restructuring uniform age forests but set no timetable or target for the cost to be incurred. Forests can be restructured by advancing tree felling ages or by delaying replanting in felled areas. Since revenue may be foregone by advancing felling ages this method could prove less cost-effective, but more immediate. The Commission have recognised that the pace of restructuring in any forest area will vary depandanl 011 ils anvirormwnlal ssnsilivily and issued revised guidance on this in November 1992.

15

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

Forestry Commission restructuring proposals for a large hillside

Fwsen, landscape Felling panern

Replanting Landscape at 2008 Source: Forestry Commission

These photographs show the transitional Stages from the present str~~f~re to the proposed landscape in 2008

2.32 The National Audit Office noted that in four forest districts where restructuring plans had been produced the costs had all been within the general limits applied in the earlier

environmental circulars but the method of calculating cost in these cases was not always consistent. One of the Commission’s regional offices now requires local managers to produce monitoring plans for their forests. These plans are to be costed, in terms of revenue foregone compared with production forecast, and in terms of acceptable costs to reflect the sensitivity of different forest areas.

Local stock levels

2.33 Local managers changed the plan if they knew that the stock of trees on the ground was different from that forecast by the Commission’s production planning system.

These differences can be due to trees growing faster or slower than expected, biological constraints changing the expected number of trees, and unrecorded changes in

forest management treatments such as thinning.

2.34 Two of the six forest districts visited by the National Audit Office had recently experienced production difficulties. One forest had been affected by unexpected growth patterns which reduced the number of larger diameter logs. As a consequence more trees than planned were being cut and a surplus of smaller logs produced. In the other case, as the areas planned to be cut had not been thinned as intended, they contained more, thinner trees. This made it difficult for managers to meet their targets for the mixture of large and small logs.

16

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

2.35

2.36

Marketing adjustments

Demand for sawlogs and small roundwood fluctuates and, consequently, the Commission may modify production forecasts to respond to market conditions. During the last decade the Commission have been required to make major marketing adjustments because of a lack of demand for small round wood and to take account of surplus supply resulting from the catastrophic wind damage in 1987 and 1990.

Costs of amendments in production planning system

The Commission do not assess the overall cost of adjustments made during production planning. They consider that is is not possible to manage forests in accordance with their multi-purpose objectives and achieve the theoretical maximum economic return on timber production. Because they believe that the methods for assessing non-financial benefits are still in their infancy, they see little purpose in routinely analysing the cost of variation from the maximum. They prefer to rely on management analysis of the general trends in production volumes to provide assurance that forests are being managed economically and efficiently.

2.37

2.38

The National Audit Office analysed a sample of 2,300 forest areas identified for felling in the latest production plan. This revealed that in these forest areas trees were to be harvested, on average, five years before the age of maximum economic return. A more detailed analysis (Figure 7) showed that plans actually provided for only 51 per cent of trees to be harvested within five years of their age of maximum economic return. A further 37

per cent were planned to be felled nmre than five years before that age, and the remaining 12 per cent were to be harvested more than five years after.

Felling trees at a stage before or after the age of maximum economic return will reduce the potential income from timber. The National Audit Office therefore compared the planned felling ages for all forest areas identified for harvesting in production plans in 1991-92 with their ages of maximum economic return and assessed the level of notional income foregone which represented the cost of adjustments to plans. This indicated some 8 per cent of the value of the harvested timber was foregone which, at prevailing volume and price levels, is equivalent to some f5.6 million each year.

37% More than tiy”,y;;

51% Within plus or minus

five years

Source: Forest,y Commission

The figure shows that only 51% of forest areas were planned to be felled within five years of the age of maximum economic return.

17

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETLNG

2.39

2.40

Conclusions

Production plans should provide a reliable indication of which forest areas ought to be felled to accord with the Commission’s financial and non-financial objectives, The Commission provide forest managers with production plans based on analytical assessment of available crops, likely crop behaviour patterns and expected value refined to meet local circumstances.

The National Audit Office’s examination of the production planning system suggests that the information used could be refined. Further analysis should be undertaken of information collected from the Commission’s sample plots to ensure that yield models are accurate and representative. The information held on the forest inventory could be enhanced to aid the prediction of expected production volumes, to assist strategic planning and to underpin operational planning. The Commission should re- consider the costs and benefits of their

2.41

survey cycle and should continue their research into the damage caused by wind in their forests, particularly at local level.

The Commission would benefit from greater information on the changes to production plans introduced at local forest district levels. Many of these changes are necessary to bring the production plan into line with actual forest stock, to meet environmental and other objectives. and to recognise the valuable input which local managers can make to the planning process. However, the National Audit Office analysis suggests that although local decisions to alter production plans may represent over f5 million per annum in notional income forgone, evidence to support the decisions taken is limited. Scope therefore exists for the Commission to improve the basis upon which to judge whether the benefits derived from local decisions are commensurate with the level of income foregone as a result.

18

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

3.1

3.2

Part 3: Timber harvesting

The Commission’s timber production plan forms the basis of annual production programmes for each forest district. These programmes are essential prerequisites to the efficient planning, implementation and control of all harvesting activity. The programmes also inform the Commission’s annual sales plans and provide the basis on which annual resource budgets for local managers are determined.

Preparation of production programmes

The production programme for a forest district specifies the areas to be harvested and the volume of timber expected from each area. Programmes identify forest areas to be thinned or clear-felled and reflect production levels which will deliver the annual volumes forecast for the five year period.

3.3 In practice, since circumstances change after production plans are finalised, the production programme can vary from the plan. Generally changes reflect variations in marketing conditions but they may also be necessary to take account of wind damage, or differences between expected production and the volume and mix of timber actually available in forest areas. .

3.4 The forest district manager is responsible for preparing and updating the production programme to conform with the plan and regional office guidance on changes, as well as any additional information gathered during site inspections on potential sources of timber and expected volume. The programme acts as a basis of production control in the district office and summaries of the volumes of different types of timber product and proposed harvesting methods are approved by the regional office. As harvesting

Clearfell operations

Source: Forestry Commission

A site where clearfell is takino date

19

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

3.5

3.6

3.7

operations progress the actual source and volume of timber produced is recorded so that the volume of timber obtained from each hectare of harvested land can be monitored.

Annual sales plans

Regions are required to produce an annual sales plan giving detailed analysis by product and price. The volume of timber for sale must accord with the production forecast. The regions are advised by Headquarters on the timber price and quantity required to meet long-term contracts and by districts on their detailed operational proposals. After Headquarters approval, regional sales plans are sub-divided to form District sales plans which provide local managers with target volumes of different types of logs to be produced during the year. Forest managers regard sales plans as their prime operational targets.

Cost budgets

Operational programmes are the responsibility of forest district managers. They draw up detailed harvesting programmes and cost budgets from the approved sales plan and the production plan. Budgets are used to provide financial control over locally incurred expenditure on directly-employed labour, contract labour, machine hire and construction and maintenance of forest roads. In each forest area. the manager decides, on the basis of cost, terrain, availability of resources and general efficiency, which of a number of harvesting methods to use. The Commission

have issued guidance to managers on the consideration of comparative operational costs.

National Audit Office examination

The Commission manage and control timber production through harvesting programmes. Programmes should conform to production plans unless important changes such as new sales commitments or wind damage have occurred since the plans were drawn up. The National Audit Office therefore examined the production programmes in six forest districts in order to establish to what extent

3.6

3.9

programmes were consistent with plans, whether plans were consistent with actual production, and how control was exercised over timber harvesting through sales plans and cost budgets.

Compilation of harvesting programmes

During visits to forest districts the National Audit Office compared district harvesting programmes for 1991-92 with the latest production plans, and found significant variations in each district. On average, 50 per cent of the volume of timber intended to be harvested in the production programme was / to be obtained from forest areas not planned to be harvested within the five year period arising from the production planning system. In some districts the proportion exceeded 80 per cent. The Commission told the National Audit Office that because of changing circumstances and the fact that yield models ,

were not intended to provide accurate / assessments of volume production for individual forest areas, they would normally i expect forest managers to produce programmes which vary to some extent from the forecast. The level of change was, however, dependent on local circumstances and consultation between district and regional management. The Commission had introduced arrangements which should identify the extent to which programmes varied from the first five year period of the plan but these were not applied consistently to monitor differences. The Commission did not seek to undertake any central analysis of changes between plan and programme.

Local managers did not adequately document the reasnn for changes between the plan and their programmes, and the Commission considered that to do so would require additional staff and not be cost effective. They relied on dialogue between managers as a mechanism for considering changes but this did not provide cost analyses of the effects of changes. In a selection of cases where the National Audit Office sought details of the reason for changes, forest managers provided explanations, but could not provide supporting evidence. Generally managers attributed changes to: inadequate inventory information, wind damage, and updates to environmental plans.

20

FORESTRY COMMISSION: TlMBER HARVESTING AND MARKETING

3.10

3.11

3.12

Source of actual production 3.13

The National Audit Office sought to compare actual timber production with production plans and programmes. The Commission aggregate forest areas to be harvested into felling blocks and operate a job costing system which allocates job numbers to each block but this does not always show how much timber was produced by any individual forest area. There is therefore no clear link between the Commision’s production plans and actual production and it was not possible to identify the full extent of variations between planned, programmed and actual forest areas supplying production volumes. In contrast, overseas forest organisations regard this link as an essential tool in managing their forests. Those organisations visited had generally installed computer systems which provided full integration of information from their operational plans to actual production.

3.14

Costs of changes in harvesting programmes

Forest district managers are required to meet targets for production volumes and sales. The National Audit Office found that most forest districts achieved their required volume and sales but that these targets were exclusively concerned with the volume of timber to be produced with little reference to the source of production. There is, therefore, no routine mechanism which compares the actual source of timber harvested with areas identified in production plans and programmes to assess the effect of production decisions on longer-term management of the forest.

3.15

In order to assess the effects of delegated decisions on forest management the National Audit Office compared the ages of trees intended to be felled in the 1990-91 production plan with the ages of trees reported by forest managers as harvested during that year. The comparison showed that, on average, trees were felled between three and five years earlier than the age planned (see Figures 8(i) and (ii)). The National Audit Office estimated that, because younger trees had not reached economic maturity, this could have represented income foregone of E5.2 million in that year in addition to that already foregone in preparing the plans (paragraph 2.38).

3.16

The Commission consider that appraisal of all changes between plans and actual production could be administratively costly. As a result of the National Audit Office’s examination, however, they have undertaken to review their existing appraisal procedures and to set limits on the degree of variation from production plans made at District and Regional levels.

Monitoring actual volumes

The Commission’s production plans are based on yield model information which predicts volume per hectare for different categories of tree. The production from any individual forest area may vary from the model for a variety of reasons. Production plans need to be reliable, however, because they are fundamental to the budgetary planning process, to the calculation of the Commission’s input to the Public Expenditure Survey requirements and to the overall performance of the Commission. It is therefore essential for the Commission to review regularly the accuracy of their predictions in order to validate the results of the yield model and to inform and improve the basis of volume predictions.

In view of the importance of validating production planning and programming information the Commission’s procedures require forest managers to record details of the actual volume of timber produced. But there is no clear guidance on the use to be made of the information and in many cases forest managers have not been following the procedures. Also. the Commission do not require districts to pass information on the relationship between expected and actual timber volumes to regions or Headquarters. Consequently, there is no on-going assessment of this important area beyond individual district level. The National Audit Office noted that overseas organisations did collect information on actual timber volumes harvested as part of their overall forest management.

The Commission have, however, undertaken some limited comparisons of expected and actual volumes. Since 1989 forest managers have been required to report to Headquarters measurements of the volume of timber sold for harvesting by the buyer (standing sales). The Commission have analysed this

21

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

information and have concluded that, on a UK average, the volume of timber actually produced by the areas of forest sold in this way was within 10 per cent of the volume expected.

3.17 Further analysis by the National Audit Office showed that averaging masked a 40 per cent variation above or below the planned timber

volume between expected and actual output in most forest areas (Figure 9). The Commission explained that volume estimates in the production forecast were not designed to be accurate to individual forest area level. The National Audit Office considered that because the Commission’s forecast relies heavily on the choice, modification to or availability of an appropriate yield model, the

Figure 8(i): Comparison of optimum and actual felling ages for crops in high wind risk areas

. .--- ---___

35 a 10 12 14 16 18

Assessed Yield

I Optimum - - - - - Actual 1

Figure 8(ii): Comparison of optimum and actual felling ages of crops on low wind risk areas

Age 55 1

12 14 16 18 Assessed Yield

I ODtimum -----Actual 1

Source: Jaakko Poyry These figures show that the Forestry Commission are felling crops in advance of plans.

22

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

scale of variations warrants further investigation by the Commission. The accumulated data at forest district level also showed significant deviation in 36 out of 45 districts where variation had been measured. This too could be more fully investigated by the Commission.

Control of costs

3.18 The cost of harvesting timber can vary significantly depending on the methods employed. Forest managers decide for each harvesting job whether to use mechanical harvesters or manual felling (using chain saws etc). The manager must then decide whether to use the Commission’s own workforce or to employ contractors, although in practice the choice is often limited by the difficulty of the terrain and the availability of machines and contractors.

3.19 Since 1960, the Commission have reduced the unit costs of timber harvesting by 42 per cent in real terms (Figure 10). This has been achieved by the development of improved harvesting systems based on Scandinavian experience adapted to British conditions, increasing the employment of contractors and investments in mechanised systems. The reduction in unit cost has also been influenced by changes in work patterns. During the period the proportion of timber produced from clear-felling (at an average

cost f10 per cubic metre) as opposed to thinning (average cost f15 per cubic metre) rose from nearly 50 per cent to nearly 75 per cent of total production.

Labour costs

3.20 The Commission require district managers to compare costs of in-house resources with those available from contractors for at least 20 per cent of their harvesting jobs. In 1991 some 60 per cent of the Commission’s harvesting work was undertaken by contractors, which the Commission estimate costs about 16 per cent less than using their own work-force. The benefits of using contractors are diminishing, however. as new working practices (particularly mechanisation) are progressively introduced. Where costs of using contractors consistently undercut in-house costs by 15 per cent or more, the local manager is required to review the need to maintain the level of the Commission workforce in his district.

3.21 The number of contractors available has generally increased in line with the Commission’s increased timber production but availability varies between locations. The Commission generally invite tenders on a job-by-job basis. The size of the contracts they offer varies but seldom provides enough work for more than four to eight months and contractors consequently have no assurance

Figure 9: Analysis of deviation between forecast and actual production in felled forest areas

Number of forest areas

25.00

20.00

15.00 I

(Negative) Variation from forecast (Positive)

Source: Jaakko Poyry This figure shows the number of forest areas varying from forecast production IewIs.

23

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

Figure 10: Harvesting cost reductions 1980/81-1990/91

f Per M3 25 -

20 -

15.

lo-

5-

0-l 1980-81 1981-82 1982-83 1983-84 1984-85 1985-86 1986-87 1987-88 1988-89 1989-90 1990-91 :

Source: Forestry Commission This figure shows the Forestry Commission’s harvesting CDS& expressed in f 1990-91~

Mechanised harvesting (1)

Source: Foresfrv Comm~sss,on

This photograph shows a harvester felling a tree.

of continuity of work. The Commission are

therefore considering the scope for increasing the amount of work included in tender offers. Longer term work should make it easier for the contractor to finance the expensive machinery necessary to carry out the work efficiently.

Mechanised harvesting

3.22 Harvesting machines fell trees, strip the branches then cut the trees into logs. Such machines are highly sophisticated and cost between f140,000-f200.000 each but they can achieve significant cost savings. An average harvesting machine (with an hourly cost rate including labour of some f65) can

24

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

3.23

Mechanised harvesting (2)

Source: Forestry Commission

This photograph shows a harvester cutting a tree to specified dimensions.

cut trees equivalent to 10 cubic metres of timber per hour, which would cost f80 per hour if done manually. Similar savings can be achieved using machines to carry logs to the roadside rather than hauling them across the ground. The Commission have gradually increased their fleet of machines (from six harvesters in 1982 to 37 in 1991), employing them initially in labour-intensive areas where they considered the greatest cost savings were likely.

3.24

The Commission have been particularly innovative in the use of harvesting machines. Much of the specialist equipment available was of Scandinavian origin and designed to operate on flatter, firmer ground than that frequently found in the Commission’s forests. Their engineers have had to adapt the models available to allow them to work beyond manufacturer’s specifications. The Commission have also adapted standard construction equipment such as excavators to provide a lower cost alternative to specialist Scandinavian forest machinery. The Commission recognise the scope for further mechanisation and are assessing the possibilities for mechanising the more expensive initial thinning of trees.

3.25

Conclusions

The Commission’s production planning system is intended to provide a sound base upon which to identify the source of timber to be harvested to meet target production volumes. The plan provides a volume target to which forest managers operate, but the Commission have no mechanism for readily identifying the source and volume of timber produced against the areas shown in the plan and do not consider it necessary to regulate production in this way. The National Audit Office found significant differences between planned and actual sources and volumes of timber production which may have cost the Commission scme f5.2 million in 1990-91. This suggests that by improving the management of production, the Commission would have a better basis to determine the reasons for and benefits derived from the changes in planned production and to achieve the optimum balance between wood production and their other objectives.

The Commission have made significant progress in reducing the real cost of harvesting timber. They have successfully pursued the potential for savings through the use of contractors and increased mechanisation and are continuing to explore the scope for further savings in both areas.

25

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

4.1

4.2

4.3

4.4

Part 4: Marketing and sales methods

Marketing

The Commission aim to maximise income from the volume of timber harvested from their forests. They seek to ensure that the specifications of the wood supply meet the needs of the wood processing industry. They also maintain a close liaison with the industry to keep supply and demand under continuous review so that increases in wood supplies are matched by the expansion of industrial capacity.

On the basis of legal opinion and in accordance with prevailing Government policy, the Commission do not process the timber they produce into other wood products. They sell the timber on the open market to pulp mills, sawmills and wood panel ma”“fact”rers.

Marketing strategy

The Commission have a statutory responsibility to develop the wood industry, and during the 1970s and 1980s they were involved in studies to identify the types of wood processing best suited to the timber produced in Britain and how wood processing industries might be attracted to this country. This is important against a background of significant increases in timber production when it is necessary to encourage existing customers and to attract new investment. The studies concluded that the Commission’s markets were restricted to larger logs for sawmills and smaller logs for pulp and panel mills and recognised that both market sectors required a commitment from forest owners to make viable volumes of wood available.

Consequently, the Commission have developed a marketing strategy which is based on offering volumes of timber for sale and recognises the need to provide a secure source of timber for the market. The Commission therefore publish their production forecasts and make a commitment to offer predicted volumes of timber to the

4.5

4.6

4.7

market. They also enter more specific commitments, through long-term supply contracts, with major processors who are making large scale investments. They honour commitments under contract and to the open market and will generally sell timber whenever they can obtain income in line with market prices.

During the 1980s the Commission produced a series of corporate and management plans which outlined marketing policies and sales targets. But the Commission have not produced formal marketing plans. In 1991, the Commission began work on a full market plan by undertaking a market audit. This was designed to establish the potential for the Commission to increase timber production in the light of world wood market developments and to inform this future strategy in the various sectors of the wood industry. The Commission expect the market audit to be completed by early 1993.

NAO examination of marketing strategy

The Commission’s market strategy is based on the recommendations of specific studies of the British wood industry and reflects both their statutory responsibilities and their position as market leader. The National Audit Office therefore examined the went to which the Commission had adopted earlier recommendations. the cost of the strategy adopted and whether it had been successful.

Study recommendations

Three major studies provide the basis of the Commission’s strategy: a 1974 review which they initiated of British forest products and industrial development alternatives: a 1980 report into market possibilities for British timber, particularly smaller diameter logs, which they also initiated: and a 1984 review of long-term strategy for the Scottish forest products industry commissioned by the Scottish development agencies. Most of the recommendations emerging from these

26

FORESTRY COMMISSION: TIMBER HARVESTING AND MARKETING

4.8

4.9

4.10

studies were directed at the wood processing industry in general although certain themes emerged which had a direct bearing on the Commission’s activity. These included the need for forecasts of wood availability, the benefits of sales to larger sawmills and pulp processors and the need to provide incentives to the developing industry.

The Commission have published forecasts of timber production since 1972 and introduced in 1977 a general commitment to provide forecast volumes in the immediate five-year period. Since the cost of hauling timber over long distances generally restricts the catchment area in which sawmillers will buy wood, the studies recommended that the Commission should present localised market forecasts. The Commission have responded by producing separate forecasts for England, Scotland and Wales and they are content. on the basis of their regular discussion with the industry, that the timber trade are satisfied with this arrangement.