franchise bidding in the water industry ... - isu.uzh.ch file2 1. introduction due to extensive...

TRANSCRIPT

Institute for Strategy and Business Economics

University of Zurich

Working Paper Series ISSN 1660-1157

Working Paper No. 33

Franchise Bidding in the Water Industry-

Auction Schemes and Investment Incentives

Urs Meister

April 2005

1

Franchise Bidding in the Water Industry Franchise Bidding in the Water Industry Franchise Bidding in the Water Industry Franchise Bidding in the Water Industry

Auction Schemes and Investment IncentivesAuction Schemes and Investment IncentivesAuction Schemes and Investment IncentivesAuction Schemes and Investment Incentives

Urs Meister*

April 18, 2005

Abstract

The periodical re-auction of a water monopoly concession causes the danger of underinvestment. If the life-time of specific assets such as water pipes exceeds the contract length and transferring the ownership of assets is difficult, the incumbent franchisee faces a hold-up problem. Using a simple auction model that considers the specifics of the piped water sector this paper shows that investment incentives may vary depending on the applied auction scheme. The model is designed as a two stage game, where the franchisee decides about investment on the first and competes with a potential market entrant on the second stage. Investment tends to be higher in sealed bid auctions than in an English auction, since the incumbent benefits from an information advantage. Additionally investment may vary in a first- and a second-price sealed bid auction depending on several factors such as costs or effectiveness of investment. The analysis is extended by a vertical separation.

Key Words: Water, Networks, Franchise Bidding, Investment JEL Classification: L95, L43, D21, Q25

* University of Zurich, Institute for Strategy and Business Economics, Plattenstrasse 14, CH-8032 Zürich, Tel: +41-1-634 29 62, Fax: +41-1-634-43 48, email: [email protected]. ** Thanks to Men-Andri Benz from the University of Zurich and Reto Foellmi MIT, Department of Economics, Cambridge MA for helpful comments.

2

1. Introduction Due to extensive shares of fixed costs network industries such as electricity, gas, railways or water are widely seen as natural monopolies. In such case it is cost minimising and therefore socially wanted when only one single firm serves the entire market. Usually these services are rendered by public enterprises or strongly regulated private companies. Harold Demsetz (1968) proposed franchise bidding as an alternative to regulation. He argued that auctioning the rights to a natural monopoly would lead to a similar outcome as regulation, but at lower costs. In fact franchise bidding has often been used in practice. But there is only some experience in the water sector mainly from France. The success of the auctioning model in the French water sector is assessed ambivalent since competition at the re-auctioning stage is only minor intensive. However, in theory the main criticism of Demsetz proposal rather concerns investment incentives than competition intensity. It was Oliver Williamson (1976) who pointed out the problem of long-term specific investments. If the life-time of specific assets exceeds the contract length and transferring the ownership of assets is difficult the franchisee faces a serious hold-up problem. As a result re-auctioning a natural monopoly undermines investment incentives. The hold-up problem tends to be stronger in sectors where investment is very specific, long term oriented and hardly to evaluate by a third party. One can assume that investment in the capital-intensive water sector exactly corresponds to these characteristics. Water pipes have technological lifetimes up to 100 years and they can not be dug out and used elsewhere. Additionally investment into the underground network can hardly be monitored by a third party. However, if an incumbent franchisee is able to pretend higher investment and to receive higher compensation in case of loosing the re-auction process he has an advantage in the re-auctioning stage. Armstrong et al. (1994, p, 129) follow: If Investment in specific assets is important, as in major parts of the utilities there is a serious danger either of underinvestment or of

3

ineffective competition for franchise. And they conclude that franchise bidding is not useful for capital-intensive natural monopolies. One should have in mind that investment into the pipe network plays an important role in the capital-intensive water industry. Up to 90 percent of total costs in the piped water industry concerns investment into the network. However, in many European countries investment has been widely neglected due to the municipalitys financial restrictions. As a result water losses in different networks amount up to 50 percent of total water production.

After discussing the background of specific investment in procurement auctions and some auction theory in Section 2, we introduce a simple model which examines investment incentives in an auctioned water monopoly. The model presented in this paper basically examines an incumbent franchisees investment incentives. The model assumes that investment into the pipe network reduces water losses in a pipe network and therefore total costs of water production. Additionally investment is i) long term oriented, ii) very specific and iii) not verifiable. Section 4.2 varies the duration of the concession contract. Obviously investment incentives are stronger in a long term contract, since the hold-up problem tends to be less intensive. Section 4.3 introduces a re-auctioning procedure and investigates investment depending on different auction schemes such as a first-price sealed bid auction, second-price sealed bid auction and the English auction. Such analysis uses a game theoretic approach. On a first stage of the model the incumbent player decides about the amount of investment, on the second stage the incumbent competes with a potential market entrant in the auctioning procedure. The model can be solved by backwards induction. Using a common value auction scheme where the incumbent has superior information about its past investment and therefore future production cost one can show that investment incentives differ in these auction schemes. However, investment tends to be the lowest in the English auction scheme, where the concurrent bidder is able to observe the incumbents bidding behaviour. In Section 4.4 the model is extended by assuming vertical

4

separation. And Section 5 investigates additional aspects which are relevant in different auction schemes. Such aspects concern political sustainability, the hazard of the winners curse and opportunities of collusion amongst bidding firms.

Some literature examines investment incentives in procurement auctions. One main paper was written by Tan (1992) who analysed R&D investment. He showed that in case of simultaneous investment and ex-ante symmetric firms investment incentives are equal for all participants. Furthermore firms investment incentives do not differ in first and second price auctions. Laffont and Tirole (1993) analyse investment in repeated auctions and show that investment can be improved by giving preference to the incumbent in the re-auction. The case of heterogeneous firms was investigated by Arozamena and Cantillon (2000). In their model firms invest in pre-auction investment in order to improve their relative position in the procurement auction. They show that in the first price sealed bid auction firms tend to underinvest since they anticipate stronger competition afterwards. Tolga Yuret (2004) examines the auction design problem when bidders invest before the auctioning process in order to increase the expected valuation. He shows that in equilibrium none of the bidders invests when the auctioneer is not able to commit to an auction scheme before the bidders invest. However, our model applies basic auction theory to the water sectors specific problems. In contrast to most papers above, there is only one bidder the incumbent investing before the auction takes place.

2 Theoretical background

2.1 Franchise Bidding and specific investment According to Demsetzs proposal in his famous article Why Regulate Utilities (1968) firms bidding for a natural monopoly do not specify the

5

purchase price they are willing to pay. Instead they are required to define the per-unit price they would charge for the relevant product or service at given performance parameters. The company promising the lowest price gets the exclusive right to serve customers in the defined area. With enough bidders it is expected that a bidder reveals his minimum costs and offers a price, which differs insignificantly from the per-unit cost (Demsetz 1968, p. 64). Such average cost price is expected to be lower than the profit-maximising monopoly price1. Demsetz pointed out that the resulting prices from the auction procedure are a result of the competition at the auctioning stage instead of regulation. In a world of perfect information and efficient contracts the role of the government can be reduced to the organisation of the auction ex post price regulation would not be necessary. However, in practice both information and contracts are fairly incomplete. One might conclude that franchise bidding is expected to be less efficient than predicted by Demsetz. It was in particular Oliver E. Williamson (1976) who pointed out the problem of specific investments in long term franchising contracts. It is supposable that the actual terms of a franchising contract do not count for all possible states in the future. Contractors are not able to anticipate all circumstances that require a modification of the original terms such as the relevant per unit price. In order to prevent unwanted welfare impairments the governmental authorities can re-auction the monopoly periodically2. However, Williamson indicates that re-auctions combined with shorter holding periods undermine the incumbents incentives to invest in durable specific assets. Due to their specificity assets cannot be used elsewhere and are hardly tradable. Williamson argues that in order to maintain investment

1 Lester Telser (1969) objected that the maximisation of social welfare requires marginal cost pricing. Average cost pricing induces only a second-best solution. However, such solution assures that the winning firm does not need subsidies to cover entire costs. In order to enforce a first-best solution, bidders could alternatively be required to offer a two-part tariff. The regulator chooses the firm which maximises social welfare. However, to choose such first-best solution the regulator would need exact information about demand (see Viscusi et al. 1998, p. 418). 2 Of course such problem could basically be solved by the renegotiation of the contractual terms. However, Richard A. Posner (1972, p. 115) argues that a regulator is not expected to represent consumers interest in such renegotiations adequately. He rather recommends re-auctioning the monopoly periodically.

6

incentives some method of transferring assets from existing franchisees to successor firms plainly needs to be worked out (Williamson 1976, p 85). A basic rule was already proposed by Richard A. Posner (1972, p. 116): An incumbent franchisee is required to sell his plant (included improvements) to the latter at its original costs as depreciated. Williamson argued that Posner declines to supply the troublesome details of such rule. In order to use such rule in practice, sufficient accounting data must be available and physical depreciation must be measured adequately. But due to asymmetric information an incumbent firm may be able to manipulate such data: While the franchisee itself is able to evaluate its assets accurately, outsiders such as competitors or regulators can not observe and verify past investment behaviour properly. Furthermore Williamson remarks the hazard of inflated equipment prices when a franchisee is integrated backwards into equipment supply or when kickbacks are paid. The more informed incumbent firm may successfully pretend an oversized investment level and obtain a significant advantage at the contract renewal interval. Re-auctioning the monopoly therefore causes not only the danger of underinvestment but also the hazard of lacking competition at the auctioning stage.

Based on Williamsons critique Jean-Jacques Laffont and Jean Tirole (1993) developed a theory regarding optimal re-auctions in case of specific but transferable assets. They assume that the incumbents specific investments can not be observed and verified by a regulator. In order to maintain the incumbents investment incentives Laffont and Tirole recommend a re-bidding scheme that gives preference to the incumbent. However, such rule implies a break with the principle of bidders parity in auctions. One might concern about the practical implementation of such rule, since a regulator should assess the relevant preference for the incumbent. Michael Klein (1998/b, p. 3) recommends an auction scheme that restricts the regulators discretion. The regulator should define before the auction that another bidder wins only if it underbids the incumbents offered per-unit price by for example more than 10 percent. Yet in

7

practice such discount-rule has been used in several auctions in particular in water concession auctions in France. Klein (1998/b, p. 4) complains that such rules usually meant that water concessions are just re-awarded to the incumbent.

2.2 Auction schemes Before examining the relation between auction schemes and investment incentives in the water industry in section 4 it is useful to give a brief survey of auction schemes that can be used for franchise bidding procedures. Such survey is given by several authors such as McAfee and McMillan (1987), Milgrom and Weber (1982), Engelbrecht-Wiggans (1980), Milgrom (1989), Rothkopf and Harstad (1994) or Becker (2001). Auction theory suggests four basic schemes3: The English auction, the Dutch auction, the first-price sealed-bid auction and the second-price sealed bid auction. Both the English and the Dutch auction are open auctions. Bidders traditionally gather at one place to bid, whereby they are able to observe others bidding behaviour. In the English auction scheme the auctioneer raises the price incrementally. Bidders decide if they are still willing to pay the actual price and continue participating in the auction. The auctioneer stops raising the price when only one bidder remains. The winner has just to outbid the second highest bid. In case of infinite small incremental price steps, the price to be paid equals the second highest valuation. The Dutch auction is organised reverse: The auctioneer reduces an initially defined price incrementally. The first bidder who signals willingness to pay receives the auctioned good the price equals its own bid. Sealed bid auctions do not offer participants to observe their concurrent bidders. In the first-price sealed bid auction bidders submit sealed bids. The highest bidder is awarded the item for the price he bid. The second-price sealed bid auction is basically organised similar. But the price 3 All of these auction schemes give preference to the bidder with the highest willingness to pay, e.g. the one who offers the highest price for a good. Of course these schemes can easily be transformed into an auction scheme that gives preference to the bidder that offers the lowest per-unit price.

8

to be paid equals the second highest bid. Such rule was proposed by William Vickrey (1961).

First-price Second-price

Open Dutch English

Sealed First-price sealed bid

Second-price sealed bid

Table 1: Auction rules

The bidders strategies may differ depending on the available information about the value of an auctioned good and on the information about other bidders valuation of the good. Standard models in auction theory assume independent private values where each bidder knows exclusively his own value for the good and the bidders valuations are statistically independent. In such setting the bidders strategies in the English and the second-price sealed bid auction are equivalent: competing up to the maximum valuation is a dominant strategy for all bidders. Furthermore bidders strategies in the Dutch and the first-price sealed bid auction are equivalent: bidders face a trade off between losing the auction against the profitability of winning. Bidders will therefore not reveal their maximum valuation (see Rothkopf and Harstad 1994).

In real auctions it might be necessary to weaken the assumptions regarding independent valuation. Common value models assume one true value of a good. Bidders estimate this value based on similar common random factors they observe. One can therefore assume that valuations must be positively correlated. Milgrom (1989, p. 13) points out, that such setting is applicable especially in auction models for oil and gas drilling rights or for wine and art. In these cases bidders face a common uncertainty about the value. Milgrom and Weber (1982) introduced a model with affiliated values. Their model has independent private values as one polar

9

case and common values as another. They showed that open auctions offer bidders to gather more information about the value since they allow to observe others bidding behaviour. As a result the English and second-price auctions are not equivalent. Due to the additional information bidders tend to be more aggressive in the English auction. However, the Dutch and the first-price auctions are still strategically equivalent.

3 The piped water industry

3.1 The role of investment The distribution network is the main cost driver in the piped water industry. Up to 90 percent of water utilitys total costs are related to network investment and maintenance (see Skarda 1998, p. 867). Water pipes have a technological life-time that ranges from 50 to 100 years depending on their material. Main pipe damages are caused by corrosion since the largest part of the network consists of cast iron pipes. In order to maintain the network and to minimise water leakage utilities are required to renew their network continuously. The International Water Service Association (IWSA) recommends a yearly turnover rate of 1.5 percent which means utilities are required to replace 1.5 percent of their network. In fact turnover rates are far lower and amount to an international average of about 0.6 percent (see Skarda 1998, p. 867). As a result water leakage rates in the network systems are significant and amount up to 50 percent of total water production in some areas. In Spain the average leakage rate amounts to 30 percent, in England and Wales to 29 percent, in France to 25 percent, in Germany to 9 percent and in the Netherlands to 3 percent (see EEB 2002, p. 29). The cost of water leakage equals the relevant water production costs, since water has to be treated before introducing it into the pipe network. Costs therefore depend on the quality of used raw waters and the relevant

10

treatment requirements. As a result water leakage tends to be less expensive in regions with high quality raw water resources such as spring or ground water. It is more expensive in regions where surface water is used, which has to be treated more extensive and therefore costly (see Dwr Cymru Welsh Water 1999, p. 9). On a quantitative basis the extent of water leakage for a given pipe length and time period is determined by two factors: the consistency of the pipe network on the one side and water pressure in the pipe network on the other side. Water utilities can influence the pipe consistency by network investment. A higher renewal rate increases network consistency and reduces water leakage. Water pressure in the pipe network is given by factors such as topography, network extension or the location of water treatment and storage facilities. Utilities have to ensure a permanent minimal operating pressure in order to satisfy customer needs.

A further role for investment is the extension of supply capacities. Such investment may concern treatment and storage facilities on the one side and pipe networks on the other side. However, in practice capacity extensions today play a minor role in many developed countries since per capita water consumption significantly declined during the last 15 years mainly due to technical inventions and changed industrial structures. In Germany for instance per capita consumption declined about 13 percent between 1990 and 2001. At the same time water utilities extended their capacities significantly during the seventies and eighties in exception of an increasing demand. Prognoses assumed a daily per capita household consumption of 219 litres in 2000. In fact consumption amounts to 136 litres (see BGW 2004). Similar trend occurred in other European countries, e.g. Switzerland. Daily household consumption amounted to 162 litres in 2003 in 1982 it was 182 litres. Within the same period total per capita consumption declined from 500 to 391 litres (see SVGW 2003, p. 1).

Investment into the water pipe network is assumed to be very specific. Michael Klein (1998/b, p. 1) emphasises that water pipes normally cannot be dug out and used elsewhere economically. Since water pipes can

11

not be used alternatively the relevant costs can be assumed to be sunk (see Furrer 2004, p. 24). Furthermore it is obvious that a fair and true evaluation of a water utilitys network assets must be difficult. Since pipelines are in the ground, it is not possible to assess the quality of the water pipelines (see Klein 1998/b, p. 2). Even when exact data about the age and the structures of the network are available, it would be difficult to assess the consistency and therefore the value of the network assets. The technological life-time of pipes vary significantly and depends on several factors such as material of pipes, soil conditions, parasitic current or other external impacts (see Skarda 1998, p. 871).

3.2 Franchise bidding in the water industry evidence from France Obviously network investment in the piped water industry is highly specific and very long term oriented. In a re-bidding procedure for a franchised water monopoly one can expect a serious hold-up problem as described in section 2.1. Since investment into underground assets can not be observed and verified exactly by a third party, there is a serious danger of underinvestment or ineffective competition. Michael Klein (1998/b, p. 3) follows, that re-bidding for a water concession will remain the toughest challenge since underground pipes are the hardest to inspect. Nevertheless, many water sector reforms in practice used franchise bidding as a way of introducing privatisation and competition into the piped water industry. Major experience in auctioning water monopolies has been made in France. At the beginning of the 19th century large cities such as Paris, Marseille or Lyon already called private companies to make infrastructure investments in exchange for the right to manage them. The process of delegation and privatisation strongly continued in the second half of the 20th century. Today more than 75 percent of total population in France is served by private

12

water companies (see Clark and Mondello 2000, p. 326 and Hemmer et. al. 2002, p. 12).4

The extent of private involvement in water supply varies significantly between municipalities. Elnaboulsi (2001) differentiates four basic types of delegation: Management Contracts (Gérance), Régie Interessé, Leasing (Affermage) and Franchise (Concession). This paper focuses Leasing and Franchise where the entire water supply is delegated to one company5. Under the Leasing contract the private company is responsible at its own risk for provision of the water service, including operating and maintaining the infrastructure and charging water fees to customers. But investments into pipe network and treatment facilities are rendered and financed exclusively by the municipality; the private company pays a fee for using the infrastructure. Under the Franchise contract the private company is additionally responsible for financing and carrying out the investments that are required to meet the relevant obligations fixed in the contract or defined by a regulator. At the end of the contract period the incumbent can be compensated if investment is not fully amortised.

Leasing Franchise

Financing operations

Private Private

Financing investment

Public Private

Duration of concession

20 years 10 12 years

Table 2: Delegation contracts (see Elnaboulsi 2001, p. 536)

4 Since recent years franchise bidding has also been applied in other countries such as Italy, Hungary, Argentina, Bolivia, Manila, Morocco, Colombia, or Senegal. 5 Both Management Contracts and Régie Interessé use a relative low level of private sector involvement, where a private company operates only specified parts of the water supply system. Under the Management Contract the company charges a fixed fee for its service, under the Régie Interessé the relevant fees depend on efficiency.

13

In both delegation models the municipality auctions the right to serve water supply to a private company. Usually the auction procedure contains two major steps. In a first step the auctioneer evaluates financial and technical capabilities of potential bidders. Firms that meet the auctioneers requirements are allowed to make concrete tenders in the second step, where the main evaluation criterion is the offered per-unit price. The second step basically refers to a first price sealed bid auction. However, municipal authorities are free to negotiate with bidders and to choose the preferred company based on several criteria beside per-unit price (see Furrer 2003, p. 216). The success of franchise bidding in the French water sector is assessed ambivalent. One main criticism is the lack of competition at the auctioning respectively the re-auctioning stage. In its 1997 report the French national audit court (Cour des Comptes 1997) identified a lack of competition, a lack of transparency and excess pricing. The report emphasised in particular the repeated use of the negotiated procedure, nearly always with the same companies and a tendency to extend existing contracts without subjecting them to tender. Additionally cases of bribery and corruption occurred. Municipalities awarded concessions to companies that paid entry fees. Municipal authorities used these payments to improve their budget situation.6 Additionally the audit court stated the widespread renegotiation of original contract terms. Incumbent firms often renegotiate franchising contracts ex post in their favour. Asymmetric information and costs of re-awarding the monopoly to another firm give the incumbents significant bargaining power in this process (Cour Des Comptes, 1997, p 125). Water tariffs vary significantly between French municipalities. On average prices are 30 percent higher in case of private supply. However, higher prices are not only a result of lacking competition. Private companies tend to supply more problematic and therefore costly areas. Additionally 6 One main example is Grenoble, where the private company Cogese paid entry fees worth FF 226 millions. Cogese recovered these costs through charging higher tariffs to water users (see Hall and Lobina 2001, p. 6)

14

investment into infrastructure tends to be more continuous than in public served areas (see BMWi 2000, p. 16).

Since recently the French government tries to improve the degree of competition in the water industry. As some major steps it limited the duration of franchising contracts and forbid the practice of entry fees (see Furrer 2003, p. 208). Obviously such measures tend to limit the market power of incumbent franchisees. However, increased competition undermines the incumbents incentives to invest in specific assets. One can expect that in the near future the French water industry will increasingly face the trade off between competition and investment incentives.

4 A simple model

4.1 The models design Since investment into the pipe network can not be observed and verified properly by third parties contracts between the public body and a private franchisee concerning the amount of investment are expected to fail. Sufficient investment can not be guaranteed by a contract or regulation. In this case the public body has to consider a franchisees investment incentives when arranging a franchise bidding procedure and writing the relevant franchise contract. The following model basically assumes a Franchise contract between a private franchisee and the public body, where the private firm is responsible for carrying out and financing the investment. We extend the model in Section 4.4 by introducing vertical separation of infrastructure investment and infrastructure operations. The time frame of the model consists of two periods. In the first period water supply and network investment is carried out by an incumbent firm A. The chosen investment determines the consistency of the pipe network and therefore water leakage in the first and the second period since investment is assumed to be long-

15

term oriented. In the second period water supply is provided by the incumbent firm A again, or by an entrant B. In our analysis we focus the incumbents investment behaviour in the first period investment in the second period is not of interest and can be ignored. Figure 1 outlines the basic design of the model:

Figure 1 : Time frame of the model

In order to keep the analysis simple, the model assumes a fixed demand for treated water in both periods. Elasticity of demand is therefore assumed to be zero in the relevant range. Such assumption might be appropriate, since effective demand elasticity in the urban piped water sector tends to be very inelastic.7 There is a common knowledge about market demand q1 respectively q2. The quantities q1 and q2 can be different.

A water suppliers costs consist of treatment costs C on the one side and investment costs K on the other side. We omit further administrative costs since they are not relevant in our analysis. Water treatment costs are increasing in the production quantity, which is determined by sold water and water leakage. As explained in section 3, the amount of water leakage for a given pipe length and time period depends on the consistency of the pipe network on the one side and water pressure in the pipe system on the other side. In this model water pressure is exogenous. The consistency of the

7 Dalhuisen et. al. (2000) analysed 70 studies, which contain 241 estimates on water demand. According to their meta-analysis the distribution of estimated price elasticities has a mean of -0.51 and a median of -0,41. About 15 percent of the estimates have a price elasticity of about 0.

PeriodPeriodPeriodPeriod 1111 PeriodPeriodPeriodPeriod 2222

ReReReRe----auctionauctionauctionauctionIncumbent Aruns themonopolyand invests I1

Incumbent Aor entrant Bruns themonopoly

PeriodPeriodPeriodPeriod 1111 PeriodPeriodPeriodPeriod 2222

ReReReRe----auctionauctionauctionauctionIncumbent Aruns themonopolyand invests I1

Incumbent Aor entrant Bruns themonopoly

16

pipe network depends on the extent of investment. Water treatment costs in period one can be defined as follows:

( ))( 11111 ILqCC += (1)

C1 stands for total treatment costs in period one, q1 for the quantity of billed water, L1 for the amount of water losses in period one and I1 for investment in period one. Since investment into the pipe network can not be observed and verified by a third party, the franchisee can not expect to be compensated adequately in case of loosing the re-bedding procedure. Costs of investment are therefore sunk.8 It is reasonable to assume, that the life time of network assets exceed the Franchise contract length.9 One can therefore assume that water leakage and therefore treatment costs in the second period are as well affected by first-period investment:

( ))( 12222 ILqCC += (2)

Since any supplier would use the same infrastructure in the second period, both suppliers A and B would face similar treatment costs C2. Water treatment costs increase in production quantity. Since both billed water and water losses have to be treated before introduced into the pipe network, we can define 0// >∂∂=∂∂ iiii LCqC where i ∈ 1, 2 . Obviously the investment

tends to reduce water leakage stronger in the first period than in the second period the older the assets, the higher the leakage. Therefore:

0// 1211 <∂∂<∂∂ ILIL . As a result water treatment costs are decreasing in

investment, 0/ 1 <∂∂ ICi . Additionally we can assume that 0/)( 211

2 <∂∂ IICi .

8 One could alternatively assume that the incumbent and a regulator negotiate about the compensation. However, in such case the resulting compensation would rather reflect bargaining power than actual worth of investment. The compensation is then assumed to be exogenous since it is not explained by the model. Such assumption would not change any results. 9 In France the duration of Franchise contracts amounts to a maximum of 30 years. The technical lifetime of network assets varies between 50 and 100 years.

17

Beside treatment costs the water supplier A faces costs of investment in the first period. We define such costs as follows:

)( 111 IKK = (3)

Costs of investment are increasing in the amount of Investment, 0/ 11 >∂∂ IK .

Additionally we assume that investment costs increase at an increasing rate, 0/ 2

112 >∂∂ IK . In the following sections we examine As investment

incentives in the first period. In section 4.2 we analyse the influence of the contract length. In 4.3 we introduce a re-auction procedure after the first period and compare investment incentives in different auction schemes. In Section 4.4 we analyse the players participation incentives in the auctioning stage and in 4.5 we extend the model by allowing for firm specific efficiency differentials. Section 4.6 extends the model by assuming vertical separation of operations and investment according to a Leasing contract.

4.2 Long-term versus short-term contracts Investing into the pipe network allows the incumbent A to reduce the extent of water leakage and therefore production costs in the first and the second period, since investment into the pipe network can be assumed to be long-term oriented. A therefore faces a hold-up problem when the relevant contract period is short term. As profit maximising problem from running the water monopoly only in the first period can be defined as follows:

)())((max 111111111

IKILqCqp AI−+− (4)

where p1A denotes As per-unit price in period one. The price can be seen as exogenous because it results from the initial franchise bidding procedure at the beginning of period one. Since we assumed that costs of investment

18

K1(I1) are sunk, A is not compensated for its past investment at the end of the contract period. One can easily derive the optimal investment level by using the first order condition:

∂∂

∂⋅∂−=

∂∂

1

1

1

1

1

1 )(IL

LC

IK (5)

A equals marginal costs and marginal benefits from investment. Such benefits arise due to a reduction in total treatment costs in period one. Benefits of the investment are denoted by the left hand side of equation (4). However, the incumbent A does not take into account any positive effects from cost-reducing investment in period two. A welfare-maximising regulator would rather require the equalisation of marginal costs and total marginal benefits from both periods. A profit maximising firm that runs the monopoly in both periods would meet such requirement:

[ ]))(()())((max 122222111111111

ILqCqpIKILqCqp AAI+−+−+− δ (6)

where δ denotes the discount factor. Again one can derive the optimal investment level by using the first order condition:

∂∂

∂⋅∂+

∂∂

∂⋅∂−=

∂∂

1

2

2

2

1

1

1

1

1

1 )()(IL

LC

IL

LC

IK δ (7)

It is easy to show that direct investment incentives are higher in the two-period monopoly, since the right hand side of equation (7) exceeds the right hand side of equation (5). Obviously the hold-up problem can be removed by exceeding the contract period. However, as mentioned in section 2.1 the regulator faces a trade off between keeping direct investment incentives and degree of competition. Exceeding the contract period and leaving the re-

19

auctioning stage remove competition and therefore the potential for price reductions. Net-welfare effects of a longer contract period can be negative if technical progress or other external effects reduce production cost. Nevertheless, since demand is assumed not to be varying in retail prices, the amount of investment always corresponds to the social optimum. Since we focus investment behaviour, we can use the resulting investment incentives given by equation (7) as a benchmark in the following.

4.3 Re-auctioning the monopoly In order to limit the incumbents potential market power the regulator can re-auction the monopoly after the first period. The re-auction of the concession can basically be designed as a two stage game. In a first stage an incumbent franchisee chooses the amount of investment which determines actual and future water leakage. In the second stage a regulator re-auctions the water monopoly. The model assumes two risk-neutral bidders, the incumbent company A and a potential market entrant B. In order to define their bidding strategies in the re-auction process both the incumbent A and the entrant B need to forecast average treatment cost C2/q2 = c2 in the second period. 10 As mentioned above, both water suppliers A and B would use the same pipe network in the second period. As a result they would face similar treatment cost c2 after winning the re-auction if we abstract from firm specific efficiency differentials. However, the model assumes asymmetric information about the investment level and therefore about water leakage and treatment costs in the second period. Obviously the incumbent firm A faces an information advantage, since it knows the extent of its past investment exactly. In our model we assume a perfectly informed incumbent A that assesses average production cost in period two exactly at c2. However, the less informed player B can not observe c2. Therefore B is 10 In their tenders bidders have to define the per-unit price they would charge to customers. Since bidders do not want to generate losses, they compare the per-unit price with average costs. An optimal bidding strategy requires a per-unit price which is increasing in average costs.

20

not aware of true costs. In order to prepare its price bid in the auction process, B makes a cost estimate c2B. From the incumbents perspective Bs cost estimation is a random variable c2B with a uniform distribution on

[ c,0 ] as presented in Figure 2. We assume that actual costs c2 in the second

period are in the range of 0 and c . The cost maximum c would result at zero investments in period one. The distribution is not assumed to be common knowledge among both bidders.

Figure 2 : The distribution of Bs average cost estimation

One might complain that using a backwards induction could allow B to anticipate As optimal investment level I1* and therefore actual average production costs. However, we assume that B does not have any information about the relevant starting point: B does not know about the pipe networks initial consistence and therefore about As true treatment costs at the beginning of period one. In such case B is not able to anticipate As investment behaviour and therefore the average production cost in period two. In addition there might be other sources of uncertainty: Costs may differ between A and B due to different labour productivity. However, the model represents a reduced form and abstracts from such additional sources of uncertainty. We summarise that A does expect that B is not able to observe or to anticipate I*.

prob (c2B)

c2B

c0

c1

222 / qCcprob B <

2

2

qC

prob (c2B)

c2B

c0

c1

222 / qCcprob B <

2

2

qC

21

In the following sections we analyse As auctioning and investment behaviour under different auction regimes. For this purpose we assume As and Bs participation in the auctioning procedure as exogenously given. Such assumption is useful, since up to this point we did not allow for firm specific efficiency differentials. However, we extend the analysis in section 4.4 where we make the participation decision endogenous and when we allow for firm specific efficiency differentials.

4.3.1 First-price sealed bid auction For concessions it is the standard to use a first-price sealed bid auction (see Klein 1998/a, p. 1). Bidders submit a sealed envelope to the regulator. The monopoly is awarded to the bidder with the lowest per-unit price. In order to examine the incumbents investment incentives we solve the model by backwards induction. In the second stage of the model A and B compete in the re-auctioning process. Therefore we firstly analyse their competitive behaviour which determines the relevant per-unit price in the second period on the one side and the probability of winning the auction on the other side. Afterwards we analyse the first stage of the model where the incumbent decides about its investment into the pipe network.

The incumbent A wins the first-price sealed bid auction when the offered price p2A is lower than p2B offered by entrant B et vice versa. In a first-price sealed bid auction both bidders face a trade off between maximising the probability of winning the auction and maximising the relevant profit margin (see Becker 2001, p. 6). Obviously the bidders lowest possible bids equal forecasted average costs c2 respectively c2B otherwise the outside option is more attractive. Bidding a price equal to average costs maximises the bidders probability of winning the auction. However, a price above average costs increases the payoff when winning. Since the offered price is expected to increases in average costs, we can define the bidders price strategies as )( 222 cpp AA = respectively )( 222 BBB cpp = . We follow

22

Rothkopf (1969) and simplify the exposition by assuming that players only choose multiplicative strategies. Such strategies are defined as follows:

22 cp AA α= and BBB cp 22 α= , where αi ≥ 1 is the mark-up multiplier. Now we

can write the necessary condition for winning the auction. The incumbent firm A wins the auction when p2A < αA c2B or

BB

A

B

A ccp2

22 <=α

αα

(8)

Firm A therefore faces the following maximisation problem:

<− B

B

AA ccprobccE

A2

222 )(max

ααα

α (9)

When maximising the expected profit bidder A not only take its own costs into account. Obviously A considers Bs mark-up multiplier and therefore Bs cost forecast. From equation (9) we know that the rivals cost forecast c2B affects the probability of winning the auction. A believes that c2B is

uniformly distributed on [ c,0 ]. The incumbent A faces therefore the

following maximisation problem for a given mark-up multiplier αB* in Bs strategy.

−−

ccccE

B

AA

A*

222 1)(max

ααα

α (10),

Using the first order condition for As maximisation problem we can define As optimal strategy.

( )cccp BAA*

22**

2 21 αα +== (11)

23

From equations (11) one can follow that A offers a higher price when Bs mark-up multiplier αB* increases. In addition A offers a higher per-unit price when Bs uncertainty about true costs increases. Such uncertainty increases

when c increases. Due to the trade off between mark-up and probability of winning the minimum offered price amounts to cB

*2/1 α . And we know

02/12/1 * >≥ ccBα . In order to derive an explicit Nash equilibrium in the first

stage of the game, we would have to consider Bs optimal price strategy in equation (11). However, due to the assumed information asymmetry defining an explicit Nash equilibrium in the second stage of our model is not only expected to be complex, in addition it requires extended rationality from A. In order to ease our analysis we omit defining such equilibrium. Instead we analyse As investment behaviour given Bs strategy αB*. Such procedure corresponds to a decision theoretic approach, where the case of only one strategic bidder is analysed (see Engelbrecht-Wiggans, p. 124)11. Since our analysis is focused on As investment behaviour, it is appropriate to use such approach. Using αB* and As price strategy from (11) we can define As maximisation problem at the first stage of the game as follows:

+−

+−+−+−

2*

122212222

*1111111 2

))((21))((

21

21)())((max

1 qcILqCILqCqcIKILqCqp

BBAI α

αδ (12)

Since we assumed Bs strategy as given and since B can not observe or anticipate As investment behaviour in the first stage, the actual amount of investment is not expected to have an impact on Bs mark-up strategy:

0/ 1* =∂∂ IBα . In addition we know that αB* ≥ 1. Using the first order condition

11 Other bidders are assumed to be non-strategic. In such setting the strategic bidder defines its optimal bidding strategy given the others bidding behaviour. Such behaviour can be assumed to be random. In our model the strategic bidder has believes about the other bidders cost forecasts c2B. Therefore Bs offered per-unit price p2B = α2B c2B is random from As point of view. Of course one could extend the model by introducing an additional distribution function F(·) from which A derives its estimation of Bs mark-up multiplier α2B. In order to ease the analysis we assume that A assesses α2B at α2B*.

24

regarding I1 allows us to derive the optimal level of investment into the pipe network in the first period.

+−

∂∂

⋅∂∂+

∂∂

⋅∂∂−=

∂∂

2*

1222

1

22

1

11

1

1

2))((

21

)()()(

qcILqC

ILC

ILC

IIK

B

A

αδ (13)

Obviously the first term of the right hand side of equation (13) denotes As direct investment incentives from period one. Higher investment reduces water leakage and therefore costs in the first period. Investment therefore increases profit in the first period directly. The second term is related to the second period. The marginal benefit of additional investment amounts to the marginal cost reduction multiplied with the probability of winning the auction. Such result is not surprising and follows from two effects. On the one side investment reduces treatment costs and increases the probability of winning the auction. On the other side the cost reduction directly increase profit in the second period. One can easily show that in our model both effects have the same size. Adding the effects leads to the second term in equation (13). Such result is intuitive: basically the marginal benefit of an investment amounts to the marginal cost reduction in the second period. However, the incumbent profits from such cost reduction only with a certain probability. Such probability is higher at higher levels of I1, since lower per-unit costs would cause a lower offered per-unit price in equilibrium.

From equation (13) we can follow that As investment incentives are increasing in αB*. A higher αB* increases As probability of winning the auction on the one side and allows A to increase the own offered per-unit price p2A on the other side. Investment into the pipe network gets more attractive, since the hazard of the hold-up decreases. In addition investment increases when Bs uncertainty about the true costs increases. Again, the increased uncertainty increases the probability of winning the re-auction and allows A to bid a higher per-unit price. Additionally investment increases in the discount factor δ.

25

4.3.2 Second-price sealed bid auction

A regulator could alternatively use a second price sealed bid auction. Such rule was proposed by William Vickrey (1961). In practice such auction scheme is less common for concessions than first-price auctions. However, second-price auctions have been used as well. New Zealand, for example, applied second-price sealed bids to auction licenses for radio spectrum (see Klein 1998/a, p. 1). In a second-price sealed bid auction the bidder with the lowest per-unit price bid wins the auction. The actual price that the winner can charge to customers equals the second lowest bid. Again we solve our model by backwards induction. At the second stage of the game the participants of the auction define their per-unit price offers. Obviously we can define the players strategies more easily than in the first price auction. In the second-price auction both bidders A and B have strong incentives to bid a per-unit price that equals the own average treatment costs in period two. Since the actual price is independent of the own bid, the bidder maximise expected profit only by maximising the probability of winning the auction. Obviously bidding average costs is a dominant strategy for both. Such result is not surprising and is very well known in auction theory (see Becker 2001, p. 8). In our model we assumed a common value auction, where winning the auction has the same value for both bidders. However, such assumption does not change their strategies, since the second-price sealed bid auction with only two bidders does not allow any bidder to gather any information about the others cost forecast.

Since both players have a dominant strategy that is independent from the others strategy we can easily define a Nash Equilibrium in the first stage of the game. As equilibrium strategy is defined as 22

*2 )( ccp A = , the

entrant Bs strategy as BB ccp 22*2 )( = .12 However, A can not observe c2B.

12 One may concern that it is rather optimal for B to make a price bid equal to zero. In such case B would win the auction with certainty, the actual retail price would equal c2, the relevant margin is zero. Then, A

26

Instead A has a believe about it which is based on the uniform distribution

[ ]c,0 . Since A wins the auction when *2

*2 BA pp < respectively when Bcc 22 < we

can define As perceived probability of winning the auction as follows:

+−=cq

ILqCwinningprob2

1222 ))((1)( (14)

And the estimated price given A wins the auction can be written as follows:

( )

++=<2

1222222

))((21

qILqCcccpE B (15)

We can use (14) and (15) in As maximisation problem in the first stage of the game:

+−

+−+−+−

cqILqCILqCqcIKILqCqp AI

2

1222122221111111

))((1))((21

21)())((max

1

δ (16)

Using the first order condition regarding I1 allows us to derive the optimal level of investment into the pipe network in the first period.

+−

∂∂

⋅∂∂+

∂∂

⋅∂∂−=

∂∂

cqILqC

ILC

ILC

IIK

2

1222

1

22

1

11

1

1 ))((1)()(

)( δ (17)

The result is not very surprising. Again, the first term of the right hand side of equation (17) denotes As direct investment incentives from period one.

would lose the auction with certainty and, hence, A would not have incentives to take part in the auction. However, if B considers the possibility that A foregoes to file an offer in the sealed-bid auction, it can not be optimal to make a bid equal to zero, since it would result in a loss in the second period. Additionally, if assuming that B does not know about the actual number of bidders, it can not be optimal for B to choose p2B = 0, otherwise it faces the danger of a loss in period 2. We summarise that it must be optimal for both parties to make a bid which is equal to their cost estimation.

27

Investment increases profit in the first period directly. The second term is related to the second period. The marginal benefit of additional investment amounts to the marginal cost reduction multiplied with the probability of winning the auction. Such result exactly corresponds to the one in the first price sealed-bid auction in section 4.3.1. However, the relevant probability of winning the auction is defined different since As bidding strategy in the two auction schemes varies.

4.3.3 English auction In open auctions such as Dutch or English auctions bidders gather at one place. Such schemes allow bidders to observe others bidding behaviour. Open auctions are less common for concessions than sealed bid auctions. Dutch auctions are often used for selling fast perishable goods such as flowers or food. English auctions are very common for selling unique goods such as art or antiques (see Becker 2001, p. 3). Traditional auction theory predicts similar bidding strategies in first-price sealed bid and Dutch auctions respectively second-price sealed bid and English auctions. However, such result requires independent private values: each bidder knows its valuation for a good exactly and knows that such value is statistically independent from others valuations. Bidding strategies are expected to be different in models assuming statistical dependence among bidders value estimates. Milgrom and Weber (1982) analysed bidding behaviour in a general auction model with independent private values and common values as polar cases. They show that in contrast to the model with independent private values the second-price sealed bid auction and the English auction are not equivalent. Instead the English auction leads to larger expected prices (respectively to lower expected per-unit retail prices in our auction scheme) than the second price auction. The English auction therefore influences the degree of competition positively, since bidders tend to bid more aggressively. However, they show that bidding strategies in the Dutch

28

and the first-price sealed bid auction are still equivalent just as they are in private value models (see Milgrom and Weber 1982, p. 1095).

Our model is based on statistical dependence among bidders value estimates. We assume a polar case with only one common value for the concession. Such value is determined by true average costs cB. Bidders have different estimates about costs in the second period and therefore about the common value. Due to the assumed asymmetry the incumbent A has superior information about true costs: As cost estimate equals c2. B only has an estimate c2B about it. Since B knows about As information advantage, one can follow that Bs estimate must be perfectly correlated with As cost forecast. In the following we focus the English auction scheme, since bidding strategies in Dutch and first-price sealed-bid auction are expected to be equivalent. Again we solve our model by backwards induction.

First, we analyse the players bidding strategies in the auction stage. In the English auction scheme the auctioneer reduce the per-unit price p2 incrementally. Bidders decide if they are still willing to participate in the auction at the actual price level or if they want to leave the auction. The auctioneer stops reducing the per-unit price when only one bidder remains. One can easily derive the bidders strategies. The incumbent A is willing to participate in the auction as long as the auction price p2 exceeds c2. At a level of p2 = c2 A is indifferent since profit would be zero in the second period. A therefore signals to leave the auction exactly when p2 = c2 since a lower per-unit price would cause a negative profit. One can follow that A has a dominant bidding strategy: participating in the auction as long as p2 > c2, leaving the auction at p2 = c2. Now we can define Bs strategy as a best response to As dominant strategy. The English auction scheme allows B to observe As bidding behaviour and therefore to gather information about true costs c2: as long as A decides to participate in the auction, p2 exceeds c2. Obviously it would not be rational for B to leave the auction procedure before A, since treatment costs are the same for both utilities in the second period. The rational player B knows about As dominant strategy to leave

29

the auction at p2 = c2. There is only one best response: waiting until A stops bidding and gathering the concession at p2 = c2 since the auctioneer stops reducing the price when the other bidder signals to leave the auction. Considering both players strategies we can derive the Nash equilibrium. The resulting price level amounts to p2 = c2, the expected profit from period two amounts to zero. Additionally the entrant B can expect to win the auction definitely. One can easily define As maximisation problem at the first stage of the game, where it decides about optimal investment:

)())((max 11111111

IKILqCqp AI−+− (18)

Using the first order condition regarding I1 allows us to derive the optimal level of investment into the pipe network in the first period.

∂∂

∂⋅∂−=

∂∂

1

1

1

1

1

1 )(IL

LC

IK (19)

Equation (19) exactly corresponds to equation (5). As investment incentives in the English auction equal the investment incentives of a one-period monopoly. Obviously there is no marginal benefit of the investment related to the second period. Every cost reduction caused by investment would only reduce the second period per-unit price to the same extension. The result basically corresponds to Milgroms and Webers findings. They show that players tend to bid more aggressively in the English auction than in a second-price sealed bid auction. As a result, competition at the re-auctioning stage is higher and the expected per-unit price tends to be lower. Since we assumed a polar case where Bs cost estimation is perfectly correlated with As cost forecast, the resulting per-unit price equals c2.

30

4.3.4 Evaluating the auction schemes In sections 4.3.2 to 4.3.3 we applied different schemes for the re-auction of a water monopoly considering the information asymmetries in a piped water market. In this section we evaluate and compare these schemes regarding the incumbents incentives to invest in the first period of our model. It is obvious that the introduction of any auction scheme lowers As investment incentives compared to the benchmark case, where the incumbent runs the monopoly both periods with certainty. Increasing competition lowers As probability to win the auction and therefore increases the hold-up problem. However, an incumbent still has positive investment incentives which are related to the second period, since investment can influence the probability of winning the re-auction on the one side and the profit margin in the second period on the other side. In order to compare the above described auction schemes regarding the incumbents investment incentives, we have to analyse the impact of investment on profit margin and probability of winning.

It is easy to show that based on our model the hold-up problem is the strongest in the English auction. From equation (18) we know that A can not expect a marginal benefit in the second period from investing in the first period, since the probability of winning the re-auction amounts to zero at any investment level. Comparing equation (19) with equations (13) and (17) one can easily show that equilibrium investment in the English auction is lower than in sealed bid auctions. However, the English auction assures the highest degree of competition, since the expected per-unit price equals true average treatment costs in the second period. The high degree of competition is a result of the open auction scheme which offers B to observe As bidding behaviour and therefore to anticipate true average treatment costs c2. Since A loses its information advantage, competition basically refers to a situation with two players facing similar costs. Such strong competition in the re-auctioning stage undermines investment incentives.

31

Sealed bid auctions in contrast offer the incumbent A to use its information advantage since B has no opportunity to observe or anticipate true average treatment costs. Obviously such information advantage lowers As perceived degree of competition at the re-auctioning stage and increases the probability to win. A can use such advantage by defining its bidding strategy in a way that maximises expected profit in the second period. Since bidding strategies in the first- and the second-price sealed bid auction schemes vary, one can expect different investment incentives in these two auction schemes. Using equations (12) and (16), one can easily show that the impact of an additional amount of investment on the profit margin in period two is equal in both schemes. Higher investment causes lower treatment costs on the one side but a lower (expected) per-unit price on the other side. Potential differences in investment incentives are therefore caused by the impact on the probability of winning the re-auction. In fact we know from equations (13) and (17) that in equilibrium investment incentives in these two auction schemes vary with the probability of winning. In both schemes the marginal costs of investment equal the marginal cost reduction in the first period plus marginal cost reduction in the second period multiplied with the probability of winning the re-auction. Since the probability of winning the re-auction is defined different, the equilibrium investment may differ in the two schemes. In order to derive the equilibrium investment incentives in the first- and the second-price auction graphically, we define

)( 1IΩ as the probability of winning in the first price auction, )( 1IΦ as the

probability in the second price auction. Since demand is assumed to be

constant we can use q2 = 1 and therefore C2 = c2. )( 1IΩ and )( 1IΦ are

defined as follows:

+−=Ωc

ILqCIB*

12221 2

))((21)(

α and

+−=Φc

ILqCI ))((1)( 12221 .

32

Both functions are increasing in c and increasing in I1, since a higher I1 lowers average costs c2 in the second period. However, a higher I1 raises the probability of winning in the second price auction stronger than in the first price auction, since the marginal effect of an additional investment tends to be stronger in the second price auction:

1

1

1

1 )()(0II

II

∂Φ∂<

∂Ω∂<

Additionally we know that 0/)( 211

2 <∂Ω∂ II and 0/)( 211

2 <∂Φ∂ II since

0/)( 211

2 >∂∂ IIC . In the second price auction the probability of winning

amounts to a maximum of 1 in case of very high investment respectively very low costs C2. In the first-price auction the probability of winning amounts to a maximum level of only 1/2. Such result is not surprising: since A faces a trade off between maximising the probability of winning and maximising the profit margin the offered per-unit price amounts to a minimum of c2/1 . However, one can not follow that the probability of

winning is always higher in the second-price auction. At very low equilibrium levels of I1 respectively at very high cost levels where c2 converges to c the value of )( 1IΩ may exceed )( 1IΦ . Such case requires

12 *

*

2 −>

B

B ccαα (20)

Obviously this condition is only fulfilled for a sufficient high level of αB*. In case of very intensive competition where αB* = 1 the values of both

)( 1IΩ and )( 1IΦ amount to zero at I1 = 0 respectively at c2 = c ; )( 1IΦ always

exceeds )( 1IΩ at positive investment levels. In order to derive the

33

equilibrium investment we have to consider the additional terms in equations (13) and (17).13 We define:

1

22

1

1

1

)(

)(

)(

ILC

IIK

IA

∂∂

⋅∂∂−

∂∂

=Ψδ

>0

where )( 1IΨ is positive since 0/ 12 >∂∂− IC A and 0/ 11 >∂∂ IK . Additionally

0/)( 11 >∂Ψ∂ II since 0/)( 211

2 >∂∂− IIC and 0/ 211

2 >∂∂ IK .14 Figure 3 shows

)( 1IΩ , )( 1IΦ and )('' 1IΨ > )(' 1IΨ .

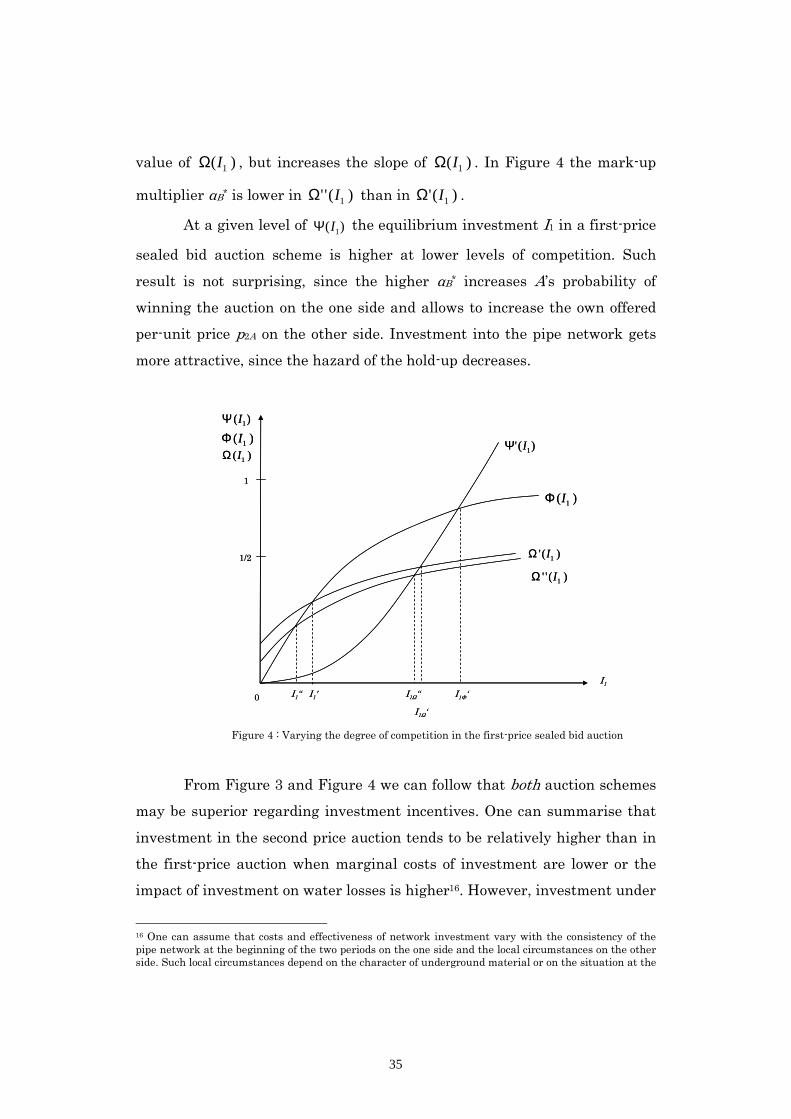

In both auction schemes equilibrium investment tends to be higher at a lower levels of )( 1IΨ , where )( 1IΨ = )(' 1IΨ . Lower levels of )( 1IΨ are caused

by a lower value of 11 / IK ∂∂ or an increased value of )/( 12 IC ∂−∂ . Obviously

investment gets less expensive and therefore more attractive. From Figure 3 one can follow that investment in second-price auctions tends to be relatively higher at lower levels of )( 1IΨ where marginal costs of investment

are low or the impact of additional investment on treatment costs is high. At very low levels of )( 1IΨ investment incentives in the second price auction

scheme converge to the investment level in our benchmark case, where the incumbent runs the monopoly in both periods with certainty. Increasing marginal costs of investment weakens the second-price auctions relative performance. The first-price auction gets relatively more attractive. At a sufficient low level of )( 1IΨ equilibrium investment ''

1ΩI in the first-price

auction may even exceed investment ''1ΦI in the second price auction

provided )( 1IΩ exceeds )( 1IΦ at very low levels of I1. Since the resulting I1 in

equilibrium tends to be very low in both auction schemes, A expects high

13 Since investment incentives related to the first period are similar in both schemes, we can ignore them. Therefore we set the first terms of the equations (13) and (17) equal to zero. 14 The second deviation of )( 1IΨ can be assumed to be positive when assuming all third deviations as zero.

34

average costs in the second period. In this case the probability of winning the re-auction tends to be higher in the first-price auction: since A expects B charging a positive mark-up as well, A perceives a positive probability of winning the re-auction even when its investment is very low and costs in period two are high.15 As a result investment incentives are higher in the first-price auction, where the hazard of hold-up is lower.

Figure 3 : Investment incentives in the first- and the second-price auction schemes

Additionally the relative performance of the first-price auction can be

altered by varying the perceived degree of competition. Competition is basically determined by αB* As assessment of Bs mark-up multiplier. A higher level of competition is associated with a lower level of αB*, since player B bids more aggressively. Obviously a lower value of αB* reduces the

15 Obviously A can expect a (small) positive probability of winning the re-auction even when actual marginal cost in the second period are close to c since B might offer a price that exceeds c as well. However, in the second-price auction scheme the probability of winning amounts to zero when cc =2 .

I1

0

1

)( 1IΩ

)( 1IΦ

)(' 1IΨ

I1'

)('' 1IΨ

)( 1IΩ)( 1IΦ)( 1IΨ

I1Ω'I1Ω I1ΦI1Φ

1/2

I1

0

1

)( 1IΩ

)( 1IΦ

)(' 1IΨ

I1'

)('' 1IΨ

)( 1IΩ)( 1IΦ)( 1IΨ

I1Ω'I1Ω I1ΦI1Φ

1/2

35

value of )( 1IΩ , but increases the slope of )( 1IΩ . In Figure 4 the mark-up

multiplier αB* is lower in )('' 1IΩ than in )(' 1IΩ .

At a given level of )( 1IΨ the equilibrium investment I1 in a first-price

sealed bid auction scheme is higher at lower levels of competition. Such result is not surprising, since the higher αB* increases As probability of winning the auction on the one side and allows to increase the own offered per-unit price p2A on the other side. Investment into the pipe network gets more attractive, since the hazard of the hold-up decreases.

Figure 4 : Varying the degree of competition in the first-price sealed bid auction

From Figure 3 and Figure 4 we can follow that both auction schemes

may be superior regarding investment incentives. One can summarise that investment in the second price auction tends to be relatively higher than in the first-price auction when marginal costs of investment are lower or the impact of investment on water losses is higher16. However, investment under

16 One can assume that costs and effectiveness of network investment vary with the consistency of the pipe network at the beginning of the two periods on the one side and the local circumstances on the other side. Such local circumstances depend on the character of underground material or on the situation at the

I1

0

1

)( 1IΦ

)(' 1IΨ

I1'

)( 1IΩ)( 1IΦ)( 1IΨ

I1Φ

1/2 )(' 1IΩ

)('' 1IΩ

I1

I1Ω

I1ΩI1

0

1

)( 1IΦ

)(' 1IΨ

I1'

)( 1IΩ)( 1IΦ)( 1IΨ

I1Φ

1/2 )(' 1IΩ

)('' 1IΩ

I1

I1Ω

I1Ω

36

the first-price auction scheme becomes relatively more attractive when investment into the pipe network is very costly and less efficient and competition is assumed to be weak. Therefore a regulator would need extensive information about costs and productivity of investment and therefore about the actual and future consistence of the pipe network and about the expected degree of competition in order to choose the sealed bid auction scheme that maximises the incumbents investment incentives. However, it is assumable that the regulators information about all these aspects is rather imperfect. The optimal decision is therefore expected to be very complex in practice. Additionally the regulator needs to be credible in order to achieve the desired investment behaviour of the incumbent utility. Obviously a regulator could have incentives for opportunistic behaviour. After announcing a sealed bid auction scheme at the beginning of period one he could rather use an English auction in order to maximise competition at the re-auctioning stage while keeping investment incentives. Of course the hazard of opportunistic behaviour increases the incumbents hold-up problem and undermines its investment incentives.

4.4 Endogenous participation So far the model assumed that each player A and B takes part with certainty in the auction procedure. We ignored their incentives to participate in the auction procedure and assumed the inexistence of any participation costs. In this section we extend the model by making the participation decision endogenous. Obviously any potential market entrant faces a significant risk due to lacking information about the networks consistence and therefore about actual future treatment costs. Making an obligatory per-unit price offer which does not cover average costs could end up in losses and finally in bankruptcy. As a result the participation in the re-auctioning

surface. Obviously investment tends to be more expensive in urban than in rural areas, since construction works tend to be more complex and therefore costly.

37

procedure of a water monopoly concession tends not to be very attractive for any third party that has less information than the incumbent. To some extend this finding may explain the low degree of competition in the French water sector, where re-auctions are usually won by the incumbent or where re-auctions do not take place, since the concession is just re-awarded to the incumbent without any auctioning procedure.

Considering the model above, participation of the two parties is not for sure, since winning the auction does not necessarily brings a positive profit. In the second-price sealed bid auction, only the incumbent may have a positive profit when winning the auction, since the relevant retail price amounts to Bs price offer. If B wins the auction, the relevant retail price amounts to c2, which is not profitable. Hence, B may forego to participate in the auction. In such case, A wins the re-auction with certainty, the relevant investment incentives increase. Obviously, in the first-price sealed bid auction the result is different. Now, both parties have positive probabilities to win the auction with profit. Hence, both have incentives to take part in the procedure. Figure 5 compares the relevant investment incentives in a first- and a second-price sealed bid auction.

Figure 5 : Considering participation incentives

I1

0

1

)( 1IΩ

)( 1IΦ

)( 1IΨ)( 1IΩ

)( 1IΦ

)( 1IΨ

I1Ω I1Φ

1/2

I1

0

1

)( 1IΩ

)( 1IΦ

)( 1IΨ)( 1IΩ

)( 1IΦ

)( 1IΨ

I1Ω I1Φ

1/2

38

In the English auction, participation is not very attractive for both

parties. A expects to loose the auction, B expects to win the auction, but with zero profit. Actually, both would forego to take part in the auction process. However, considering such idea, it would be optimal for a party to take part hoping that the other party foregoes to participate in the English Auction. To overcome such puzzling results, we should allow for firm-specific efficiency differentials. Such differentials support the assumption above, that each party has incentives to take part in the auction process..

4.5 Firm specific efficiency differentials Water utilities costs are mainly determined by factors such as quality of used raw waters, pipe networks consistence or production capacity. These parameters are not firm specific and can be seen as exogenously given for any market entrant B. Nevertheless there is some minor potential for firm specific efficiency differentials, mainly related to operational activities. Cost differentials between A and B are for instance caused by differences in organisational terms, employment contracts or technical skills. However, it is straightforward to show that allowing for efficiency differentials does not change the results from section 4.3 fundamentally.

The model can be extended by introducing a firm specific efficiency parameter θi into the cost function: ( )ijjjj ILqCC θ),( 1+= , where j denotes the

relevant period, j ∈ 1, 2 , i denotes the firm, i ∈ A, B and 0/ >∂∂ ijC θ .

One can assume that each player knows his own θi but not the others. The introduction of θi increases As uncertainty about Bs cost estimation from As point of view the range of potential c2B values increases depending on the assumed distribution of θB. We forbear to model this extension explicitly. However, we know that θB increases the values of c2B at the upper end when As assumes that θB tends to be higher than θA. A fears less competition at

39

the re-auctioning stage, investment increases in the first- and the second-price sealed bid auction schemes. Additionally investment increases in both schemes at relatively lower levels of θA, since As perceived probability to win the re-auction increases. As a result, the introduction of θi may change the level of investment in both schemes, but it does not change their relative investment performance. But we gain additional information about Bs participation in the second-price sealed bid and the English auction: B does only participate when expecting θB ≤ θA.

4.6 Vertical separation Investment incentives may be different in a franchising model that assumes the vertical separation of operations from investment. In fact the Leasing contract is the most common used delegation contract in the French water industry (see Furrer 2004, p. 212)17. Under a Leasing contract (see Table 2) the franchisee is only responsible for operating the infrastructure including treatment of raw water and charging water fees to customers. Investment into the pipe and treatment facilities is excluded from the (re-) auctioning procedure. The municipal body or a strongly regulated infrastructure company owns the pipe and treatment facilities and is responsible for the entire investment. Financing the investment can be assured by charging utilization fees to the operating company that uses the infrastructure. In such Leasing approach only the operation of network and treatment facilities can be (re-) auctioned, the investment is excluded from the re-auctioning process. As a result the franchisees hold-up problem is expected to be removed. However, vertical separation does not necessarily guarantee an optimal investment level. Obviously one has to consider investment incentives of the infrastructure company.

17 Full vertical separation has applied used as well in several other liberalisation processes, for example in the U.S. telecommunications industry or the British railway industry.

40

In this section we investigate investment incentives of a separated infrastructure company. For this reason we assume an independent upstream company U that owns the network infrastructure in both periods. Similar to the analysis above, we focus network investment and do not consider additional infrastructure such as treatment and storage facilities. One can assume U as a strongly regulated but profit-maximising private company.18 Us revenues consist of utilization fees charged to a downstream company D which uses the network to render its water services. U charges a fee that depends on the amount of water transported through its network. Such fee is assumed to be linear and similar in both periods. In order to restrict Us monopoly power a public regulator is required to restrict Us freedom to determine the utilization fee by defining a price cap aU. In our model aU can be seen as exogenous. Us costs are determined by investment costs K(I1) in period one. Since not relevant in our analysis we omit from further administrative costs. The upstream companys profit maximisation problem can therefore be defined as follows:

211 )(max1

qaIKqa UUIδ+− (21)

One can easily show that the infrastructure company U does not face any incentives to invest into the pipe network since additional investment only causes higher costs at constant revenues. Obviously U does not face any voluntary investment incentives since the resulting costs caused by water losses are not relevant in its income statement. As a result the regulator should not only regulate the utilization fee, in addition he is required to regulate and monitor Us investment behaviour in order to ensure welfare maximisation. But as stated in Section 3.1 the regulation and monitoring of