from enron to worldcom and beyond: life and … enron to worldcom and beyond: life and crime after...

TRANSCRIPT

Washington University Law ReviewVolume 81Issue 2 After the Sarbanes-Oxley Act: The Future of the Mandatory Disclosure System

2003

From Enron to Worldcom and Beyond: Life andCrime After Sarbanes-OxleyKathleen F. Brickey

Follow this and additional works at: http://openscholarship.wustl.edu/law_lawreview

Part of the Securities Law Commons

This F. Hodge O'Neal Corporate and Securities Law Symposium is brought to you for free and open access by the Law School at WashingtonUniversity Open Scholarship. It has been accepted for inclusion in Washington University Law Review by an authorized administrator of WashingtonUniversity Open Scholarship. For more information, please contact [email protected].

Recommended CitationKathleen F. Brickey, From Enron to Worldcom and Beyond: Life and Crime After Sarbanes-Oxley, 81 Wash. U. L. Q. 357 (2003).Available at: http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

FROM ENRON TO WORLDCOM AND BEYOND: LIFE AND CRIME AFTER SARBANES-OXLEY†

KATHLEEN F. BRICKEY*

It all began with Enron. On October 16, 2001, Enron stunned Wall Street by announcing that it had a $618 million net loss for the third quarter and would reduce shareholder equity by $1.2 billion. October 16 was a Tuesday. On Wednesday, the SEC opened an inquiry and made a written request for information from Enron officials. Friday, Enron notified its auditor, Arthur Andersen, that the SEC had initiated an inquiry into Enron’s financial accounting practices. Four days after that, Andersen’s Enron engagement team began wholesale destruction of Enron-related documents.

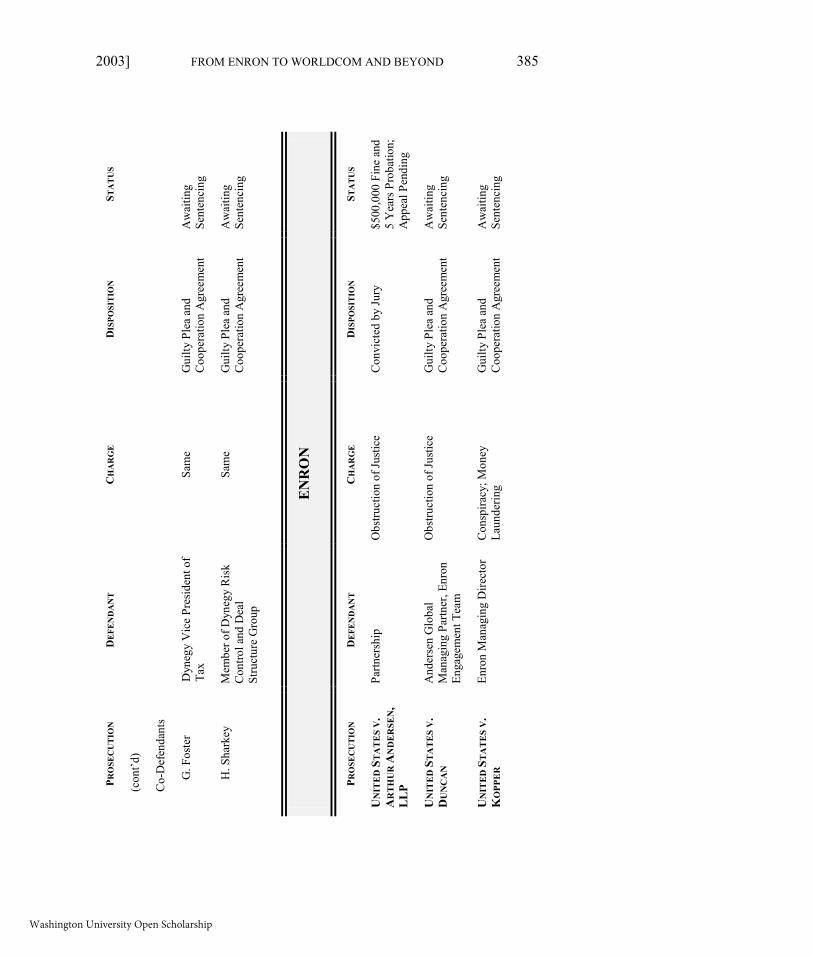

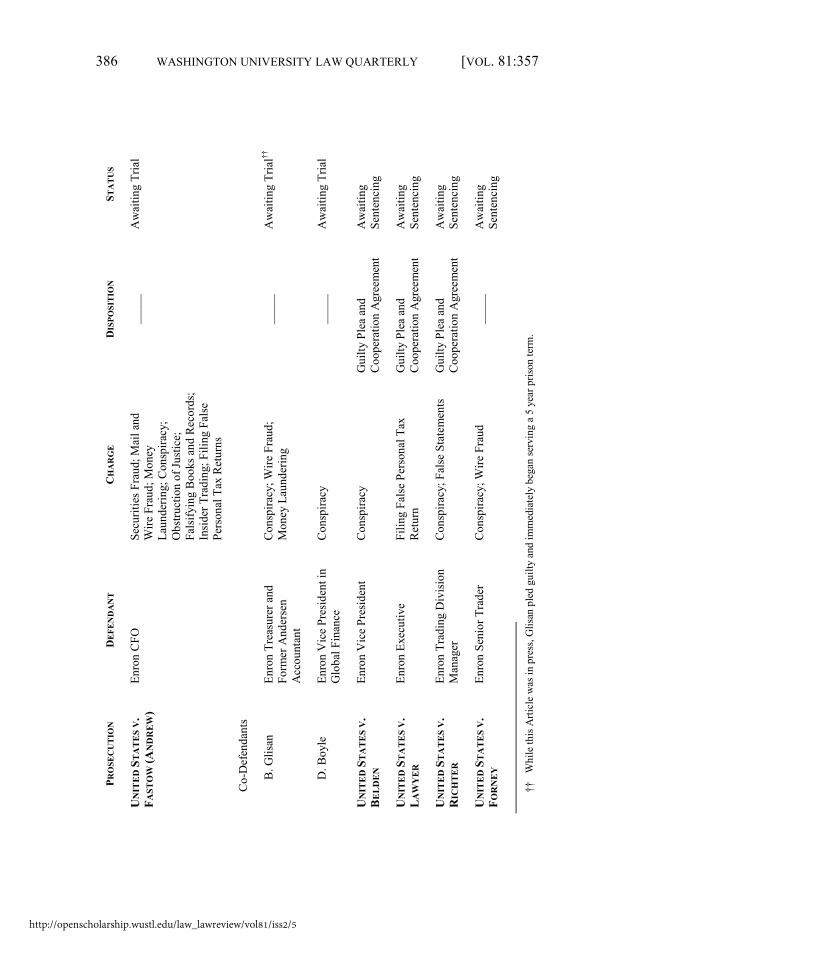

Andersen and its lead partner on the Enron audit team now stand convicted of obstruction of justice,1 four former Enron executives have pled guilty to fraud charges,2 Enron’s Chief Financial Officer is under indictment and awaiting trial on ninety-eight counts of fraud and related offenses,3 Enron is bankrupt, and civil and criminal investigations

† Copyright 2003 by Kathleen F. Brickey. All rights reserved. * James Carr Professor of Criminal Jurisprudence and Israel Treiman Faculty Fellow, Washington University in St. Louis. My sincere thanks to Jim Brickey, Steve Cutler, Troy Paredes and other participants in the F. Hodge O’Neal Corporate and Securities Law Conference for their insightful comments and suggestions, and to Jonathan Linas and Christine Knickmeyer for their invaluable research assistance. 1. United States v. Duncan, CRH-02-209 (S.D. Tex. Apr. 9, 2002) (Information) (charging Andersen’s lead partner on the Enron engagement team with one count of obstruction of justice); United States v. Andersen, CRH 02-121 (S.D. Tex. Mar. 7, 2002) (Indictment) (charging Arthur Andersen with one count of obstruction of justice) (both on file with author). Mr. Duncan pled guilty, and Andersen was convicted after a six-week jury trial. For an analysis of the legal strategy Andersen pursued to avoid criminal prosecution, see Kathleen F. Brickey, Andersen’s Fall From Grace, 81:4 WASH. U. L.Q. (2004) (forthcoming). 2. See United States v. Richter, CR-03-0026-MJJ (N.D. Cal. Feb. 4, 2003) (Plea Agreement) (pleading guilty to conspiracy to commit wire fraud and to violating federal false statements statute); United States v. Lawyer, CRH 02-705 (S.D. Tex. Nov. 26, 2002) (Information) (charging former Enron executive with tax fraud); United States v. Kopper, CRH 02-0560 (S.D. Tex. Aug. 20, 2002) (Information) (charging Enron’s Managing Director for Global Finance with conspiracy to commit wire fraud and to commit money laundering); United States v. Belden, CR 02-0313 MJJ (N.D. Cal. Oct. 17, 2002) (Information) (charging Enron former Vice President and Managing Director of Energy Trading with conspiracy to commit wire fraud) (all on file with author). 3. See United States v. Fastow, CRH-02-0665 (S.D. Tex. Apr. 30, 2003) (Superseding Indictment) (charging former Enron CFO with securities fraud, wire fraud, money laundering, obstruction of justice, tax fraud, and conspiracy; also charging former Enron Treasurer and former Enron Vice President in Global Finance with conspiracy, wire fraud, and money laundering). See also United States v. Fastow, CRH-03-150 (S.D. Tex. Apr. 30, 2003) (Indictment) (charging wife of former Enron CFO with conspiracy to defraud, money laundering conspiracy, and tax fraud); United States v. Rice, CRH-03-93-01 (S.D. Tex. Apr. 29, 2003) (Superseding Indictment) (charging seven broadband

357

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 358 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

continue to examine Enron’s complex accounting practices and byzantine financial schemes.

Fascinating in its own right, the Enron-Andersen saga enjoyed prominent front page coverage in major papers for an extended period of time. In the beginning, it was widely assumed that the Enron scandal was an anomaly. But it soon became clear that this was anything but an isolated case of financial accounting fraud at a major corporation. Enron’s record largest bankruptcy in United States history was soon eclipsed by WorldCom, whose less sophisticated accounting fraud led to a larger restatement of earnings, a larger bankruptcy filing, and equally far-reaching civil and criminal investigations.4

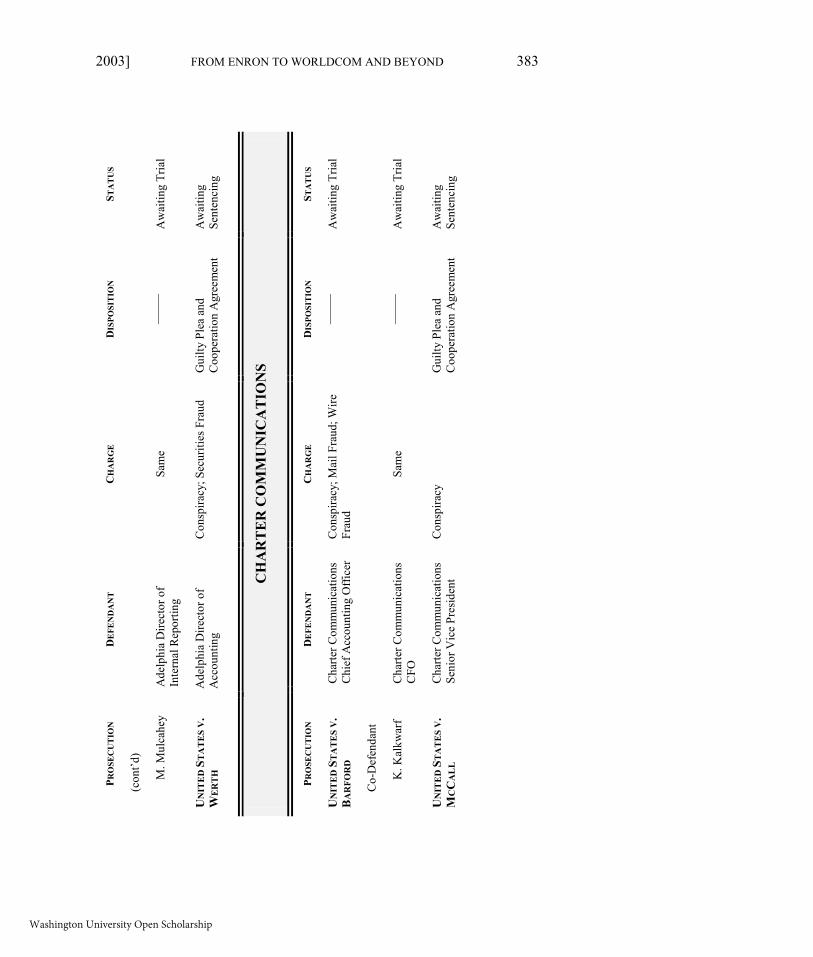

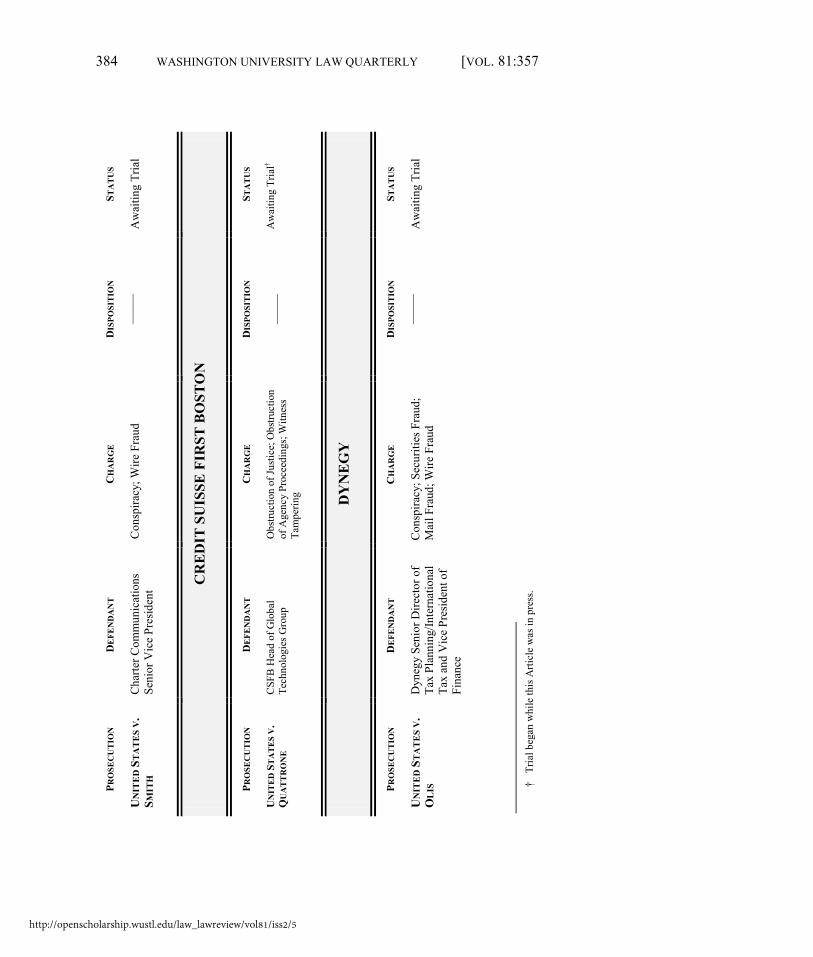

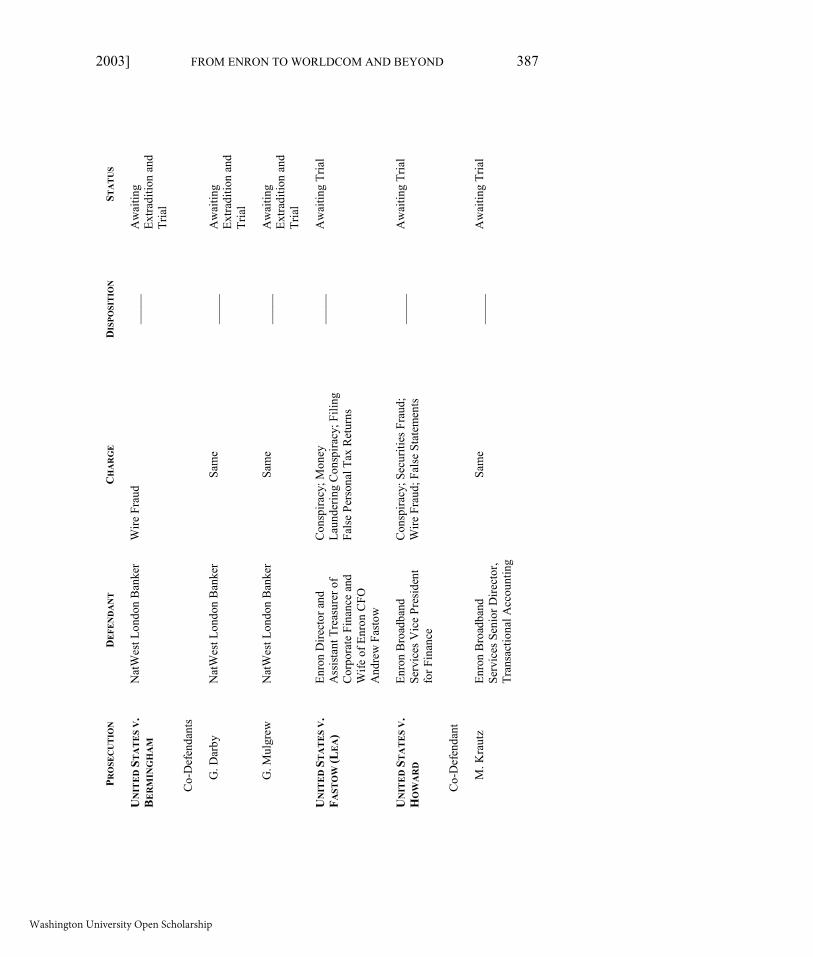

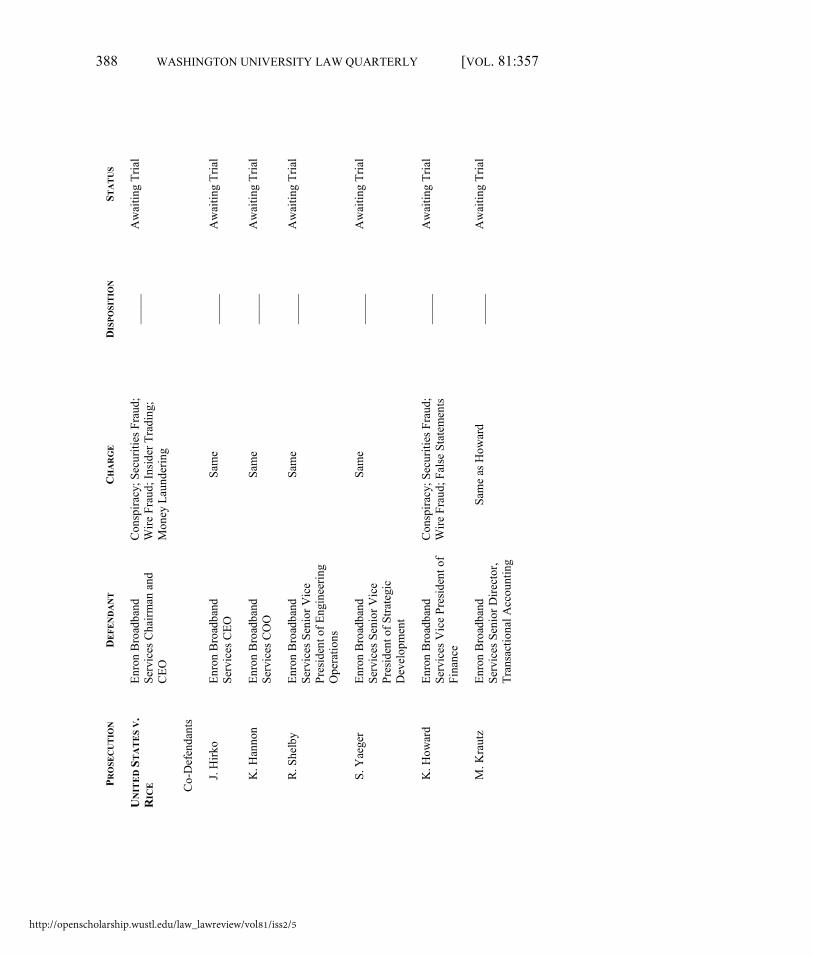

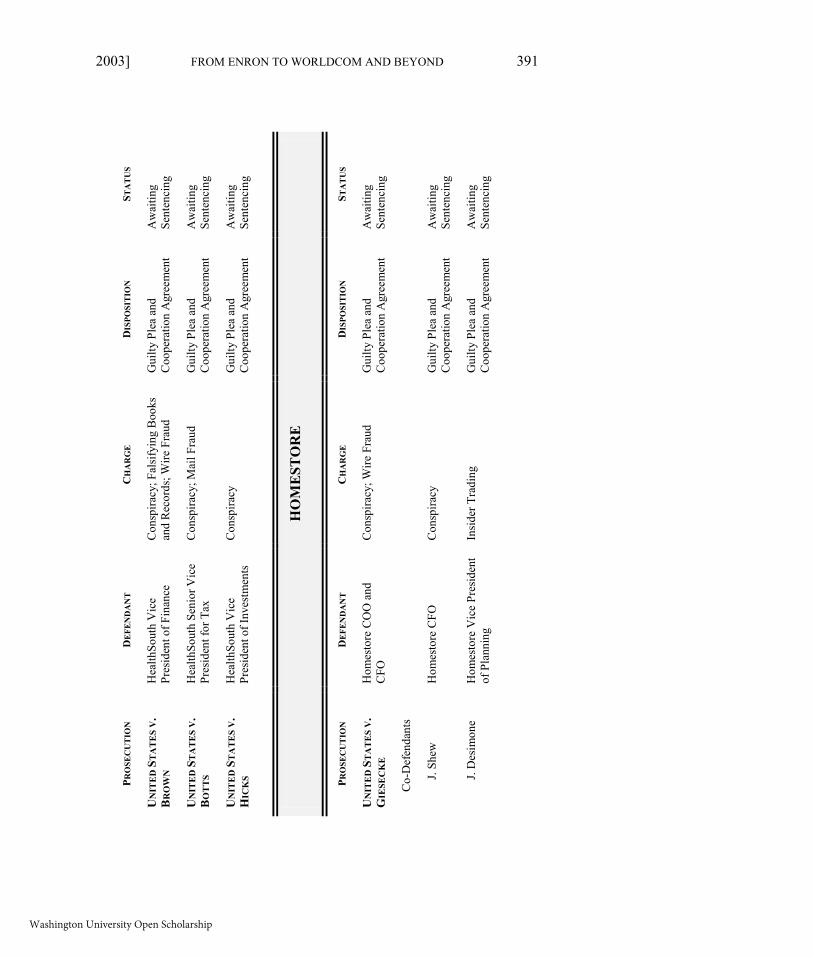

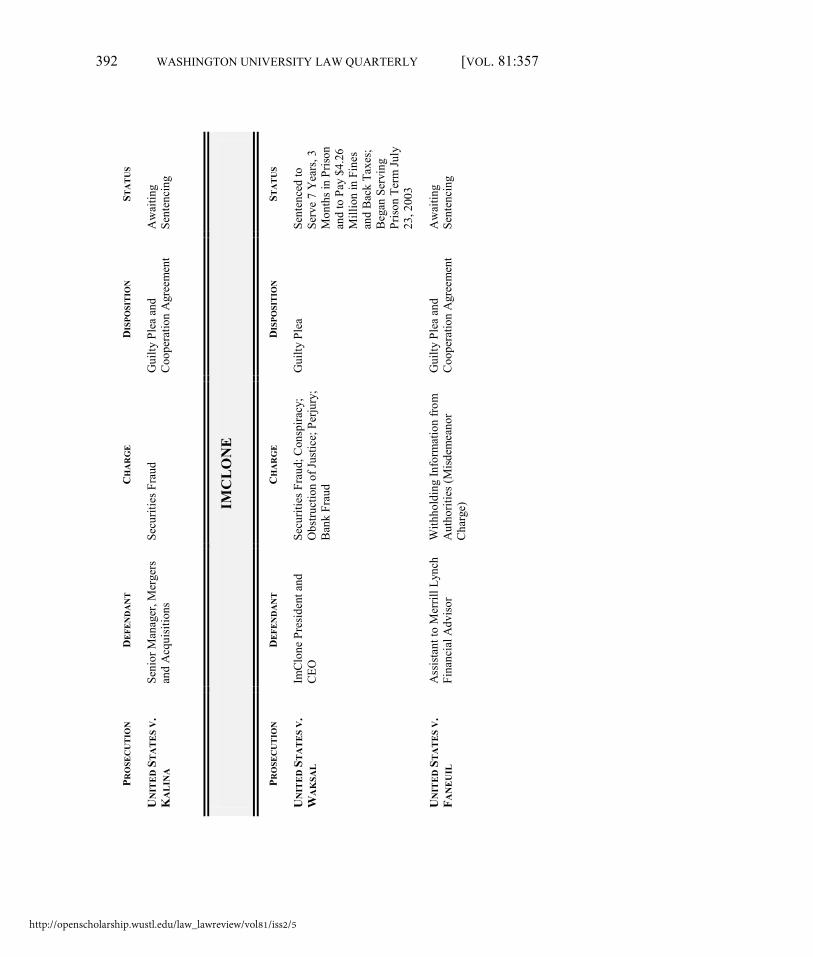

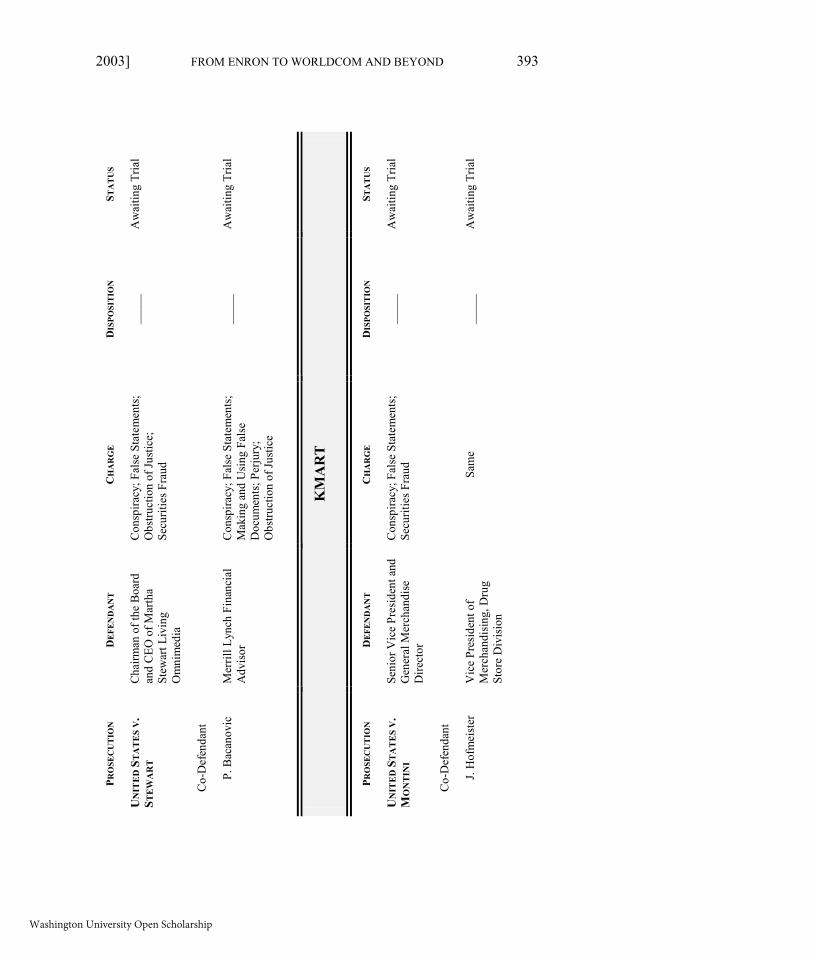

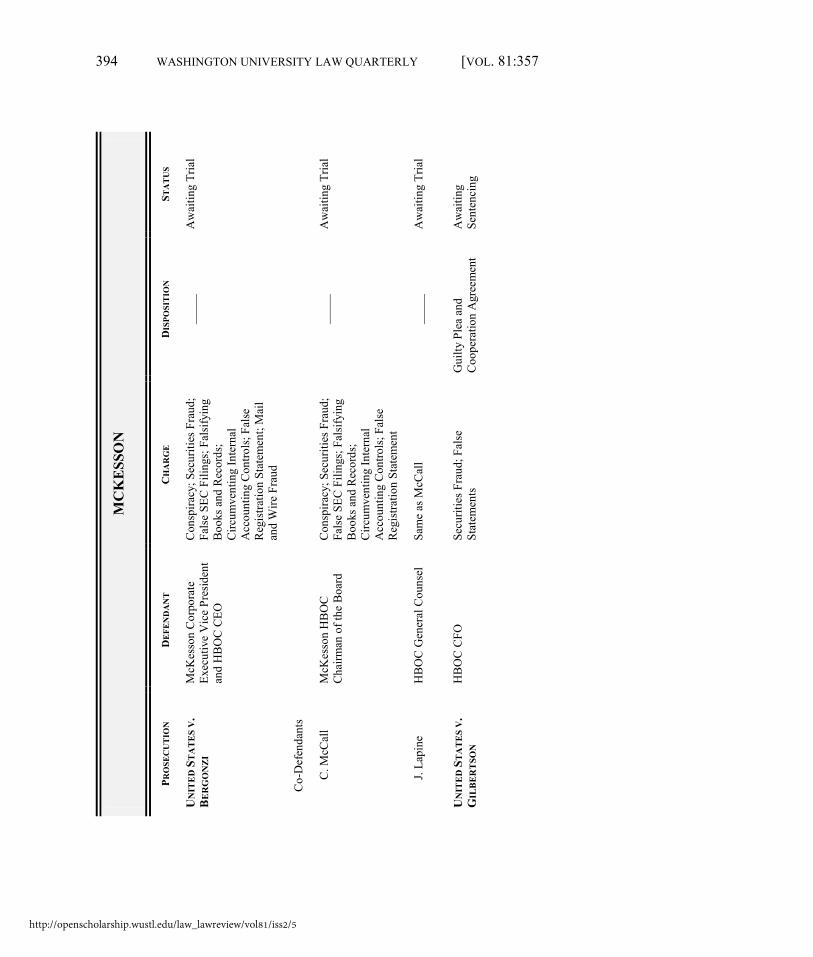

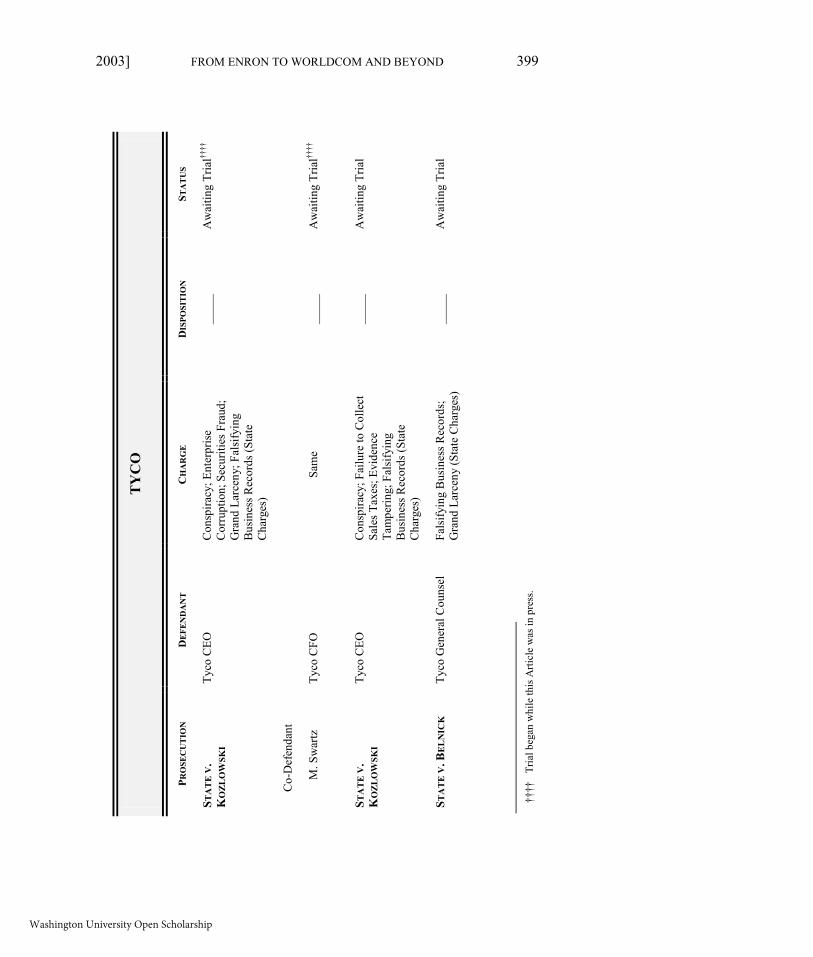

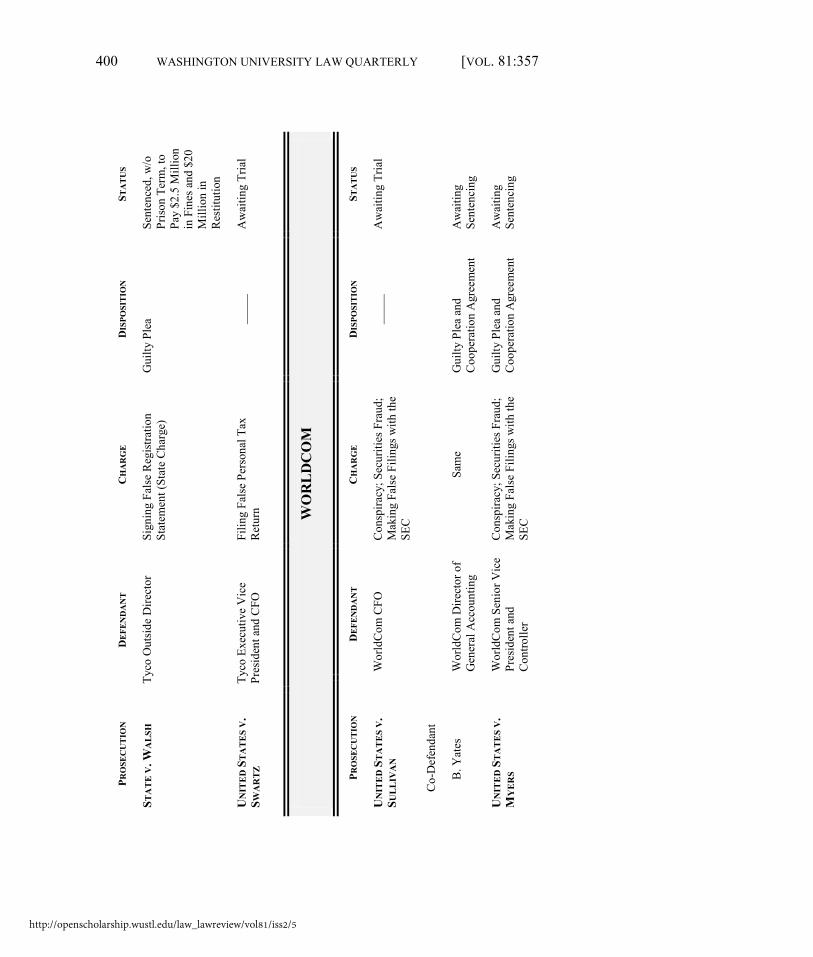

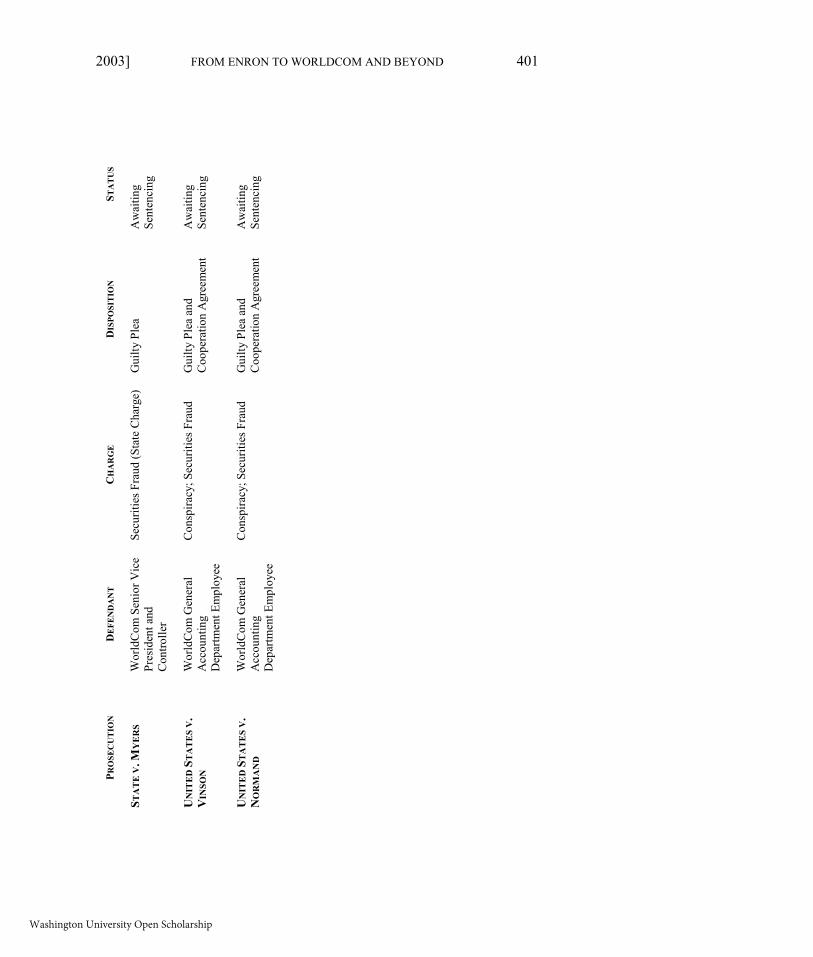

Federal and state regulators have since initiated fraud investigations involving dozens of corporations, including Adelphia, HealthSouth, McKesson, Tyco, and Qwest. To date, some ninety corporate owners, executives, and employees have been criminally charged, and the investigations are ongoing.5 The enforcement net has also expanded to include detailed scrutiny of how investment banks and investment advisers may have contributed to these scandals, and the SEC and the Justice

executives with securities fraud, false statements, wire fraud, conspiracy, and money laundering); United States v. Bermingham, CRH 02-0597 (S.D. Tex. Sept. 12, 2002) (Indictment) (charging three London bankers with wire fraud in scheme with two Enron executives to defraud a British bank) (all on file with author). As of August, 2003, eighteen Enron executives and three British bankers had been criminally charged in connection with the fraud. See infra APPENDIX A, MAJOR CORPORATE FRAUD PROSECUTIONS, March 2002 - August 2003. 4. When this Article went to press, five WorldCom executives and employees had been criminally charged in federal court. See United States v. Sullivan (indictment filed in United States District Court for the Southern District of New York) (Aug. 28, 2002) (charging Scott Sullivan, WorldCom’s CFO, and Buford Yates, WorldCom’s Director of General Accounting, with conspiracy, securities fraud, and making false SEC filings); United States v. Myers, 02-CR-1261 (S.D.N.Y. Sept. 25, 2002) (Information) (charging WorldCom Senior Vice President and Controller David Myers with conspiracy, securities fraud, and making false SEC filings); United States v. Vinson, 02-CR-1349 (S.D.N.Y. Oct. 10, 2002) (Information) (charging employee with conspiracy and securities fraud); United States v. Normand (information filed in United States District Court for the Southern District of New York) (S.D.N.Y. Oct. 10, 2002) (charging employee with conspiracy and securities fraud) (all on file with author). With the exception of Scott Sullivan, all of these defendants pled guilty. See infra text accompanying notes 66-73. Six months after his initial indictment, prosecutors added bank fraud to the list of charges against Mr. Sullivan. Kurt Eichenwald, New Charges Against Ex-WorldCom Executive, N.Y. TIMES, Apr. 17, 2003, at C2. While this Article was in press, the Oklahoma Attorney General filed a fifteen count felony information in state court charging WorldCom and its former CEO, Bernard Ebbers, with criminal violations of state securities laws. The information also charged Sullivan, Myers, Vinson, and Normand with committing the same crimes. State v. WorldCom, Inc. (felony information filed in District Court of Oklahoma County, Oklahoma) (Aug. 27, 2003) (on file with author). As of this writing, no federal criminal charges have been brought against WorldCom or Ebbers. 5. See infra APPENDIX A, MAJOR CORPORATE FRAUD PROSECUTIONS, March 2002 - August 2003.

http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

p357 Brickey book pages.doc10/24/03 12:46 PM 2003] FROM ENRON TO WORLDCOM AND BEYOND 359

Department have begun to examine the role of lawyers and other professionals who may have turned a blind eye to obvious fraud. Enron was, quite simply, the opening chapter in a series of sordid tales about corporate governance run amuck.

It was against this backdrop that zeal for corporate governance reform gained unexpected momentum and resulted in the surprisingly quick enactment of the Sarbanes-Oxley Act to correct systemic weaknesses in corporate governance structures. Sarbanes-Oxley’s goals include improving accounting oversight, strengthening auditor independence, requiring more transparency in corporate financial matters, eliminating analyst conflicts of interest, and requiring greater accountability from corporate officials. But Sarbanes-Oxley also augments prosecutorial tools available in major fraud cases by expanding statutory prohibitions against fraud and obstruction of justice, increasing criminal penalties for traditional fraud and cover-up crimes, and strengthening sentencing guidelines applicable to high-end frauds.

Sarbanes-Oxley’s criminal provisions have not been particularly well received. Critics complain that they are needlessly redundant, rely too heavily on enhanced criminal penalties to achieve their goals, and attach far too much importance to filling minor gaps in the coverage of existing laws.6 Thus, some critics conclude that “[t]he significance of the new crimes and higher penalties is vastly overstated”7 and that Sarbanes-Oxley’s criminal provisions are “more an expression of symbolic political outrage than they are a reasoned response to a public policy question.”8

This Article presents the alternative view that the Act’s criminal provisions make significant strides toward piercing the veil of corporate silence. Part I of the article focuses on corporate whistleblowers and the important role they played in bringing the Enron and WorldCom scandals to light. On this front, Sarbanes-Oxley strengthens the legal protections accorded whistleblowers by extending existing criminal prohibitions against witness retaliation to include retaliatory acts that occur in the workplace setting. Part II looks at how federal prosecutors are building

6. See, e.g., Michael A. Perino, Enron’s Legislative Aftermath: Some Reflections on the Deterrence Aspects of the Sarbanes-Oxley Act of 2002, 76 ST. JOHN’S L. REV. 671, 676-89 (2002) (arguing that the Act’s new obstruction of justice and securities fraud crimes largely extend to conduct that was already criminal and that its increased penalties will have little deterrent effect) [hereinafter Perino]. 7. Joseph F. Savage, Jr. & Stephanie R. Pratt, Sarbanes-Oxley: New Ways to Solve Old Crimes, 9 BUS. CRIMES BULL. No. 11, at 1 (Dec. 2002). 8. Id. See also Perino, supra note 6, at 673 (calling Sarbanes-Oxley’s criminal provisions “little more than political grandstanding”).

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 360 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

criminal fraud cases arising from the current corporate scandals and the crucial role that cooperating witnesses play. Part II also explores why Sarbanes-Oxley’s enhanced criminal penalties and the corresponding revisions to the federal sentencing guidelines are likely to provide powerful incentives for targets of criminal fraud investigations to help prosecutors build cases against other participants in the fraud.

I. CORPORATE WHISTLEBLOWERS

A. Enron

1. Sherron Watkins

“I am incredibly nervous that we will implode in a wave of accounting scandals.”9 Thus began Sherron Watkins’ odyssey from an obscure corporate whistleblower to one of Time Magazine’s Persons of the Year.10 She voiced her concern about accounting irregularities in an anonymous memo to Enron’s Chairman, Ken Lay. The memo followed on the heels of the abrupt and puzzling departure of CEO Jeff Skilling for “personal reasons” after only six months on the job.11 Wall Street reacted badly to Skilling’s resignation, and Enron stock fell more than six percent, continuing a trend that had marked his brief tenure as CEO.12

As rumors quickly spread among Enron employees and Wall Street analysts, Mr. Lay invited employees to submit their concerns in a comment box shortly after Skilling resigned.13 It was in response to these

9. Anonymous Memorandum from Sherron Watkins, Vice President of Corporate Development, Enron, to Kenneth Lay, Chairman, Enron (Aug. 15, 2001) (on file with author) [hereinafter Anonymous Watkins Memorandum]. 10. Ms. Watkins shared the cover of Time with two other whistleblowers, including WorldCom’s Cynthia Cooper. 11. ROBERT BRYCE, PIPE DREAMS: GREED, EGO, AND THE DEATH OF ENRON 293 (2002) [hereinafter PIPE DREAMS]. 12. Id. at 294. Enron’s stock declined by almost half during Skilling’s tenure as CEO. 13. Jodie Morse & Amanda Bower, The Party Crasher, TIME, Dec. 30, 2002/Jan. 6, 2003, 53, at 55 [hereinafter The Party Crasher]. Mr. Lay solicited questions to address at an upcoming all-employee meeting to discuss Skilling’s departure. The Financial Collapse of Enron—Part 3: Hearing Before the Subcomm. on Oversight and Investigations of the House Comm. on Energy and Commerce, 107th Cong. 15-16 (2003) (testimony of Sherron Watkins) [hereinafter House Hearing]. Mr. Lay joined Enron as its CEO in 1984. PETER C. FUSARO & ROSS M. MILLER, WHAT WENT WRONG AT ENRON 1 (2002) [hereinafter WHAT WENT WRONG]. He stepped down in February of 2001 when Skilling assumed the post, but Lay remained Chairman of the Board. Id. at 174. After Skilling’s abrupt resignation, Lay assumed the CEO post again. Id. at 176. Lay resigned on January 23, 2002, following Enron’s bankruptcy, the initiation of a Justice Department criminal investigation into Enron, and the sale of Enron’s energy trading business for a song. Id. at 178.

http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

p357 Brickey book pages.doc10/24/03 12:46 PM 2003] FROM ENRON TO WORLDCOM AND BEYOND 361

events that Sherron Watkins—an Enron Vice-President who reported to CFO Andy Fastow—warned Ken Lay about “an elaborate accounting hoax.”14 By then Watkins knew that Enron’s assets were artificially inflated. She also thought that Skilling knew the accounting problems could not be fixed and that he “would rather abandon ship now than resign in shame in two years.”15

Shortly after sending the memo, Watkins met with Ken Lay. At that meeting, she provided five new memos that both detailed problems with Enron’s off-book partnerships and special purpose entities and suggested a strategy for disclosing the accounting irregularities, restating third quarter earnings, and rebuilding investor confidence.16 She also encouraged Lay to engage an independent law firm to conduct a preliminary investigation into the accounting problems17 and urged him not to retain Vinson & Elkins because it had helped structure some of the questionable deals.18 He agreed to investigate her concerns19 but gave Vinson & Elkins the nod.20 The law firm conducted a brief and limited investigation into the allegations21 and—to no one’s surprise—reported that the special purpose entity transactions were not problematic.22 Ironically, the report came just

14. Anonymous Watkins Memorandum, supra note 9. Ms. Watkins, Enron’s Vice President of Corporate Development and a CPA, began her career as an auditor at Arthur Andersen. House Hearing, supra note 13, at 14-15. 15. House Hearing, supra note 13, at 14-15; PIPE DREAMS, supra note 11, at 294. 16. Memorandum from Sherron Watkins, Vice President of Corporate Development, Enron, to Kenneth Lay, Chairman, Enron (Aug. 22, 2001) (on file with author) [hereinafter Watkins Strategy Memorandum]; House Hearing, supra note 13, at 16. 17. Watkins Strategy Memorandum, supra note 16; House Hearing, supra note 13, at 19-20. 18. House Hearing, supra note 13, at 19-20; PIPE DREAMS, supra note 11, at 298. Vinson & Elkins, the law firm that did much of Enron’s work over the years, billed the corporation $30 million—or seven percent of the firm’s total billings—in 2001. PIPE DREAMS, supra note 11, at 298. 19. House Hearing, supra note 13, at 16. 20. PIPE DREAMS, supra note 11, at 298; The Party Crasher, supra note 13, at 55. Ms. Watkins would later call Mr. Lay’s reliance on Vinson & Elkins and Arthur Andersen to review their own work a serious mistake. Memorandum from Sherron Watkins, Vice President of Corporate Development, Enron, to Elizabeth Tilney, Senior Vice President for Advertising, Communications and Organization Development, Enron (Oct. 30, 2001) (on file with author). 21. The law firm’s report states that Enron’s General Counsel had limited the investigation by instructing Vinson & Elkins not to second guess Arthur Andersen’s treatment of underlying accounting issues, not to do a detailed analysis of the transactions in question, and not to conduct a discovery-style investigation. House Hearing, supra note 13, at 20. See also Letter from Mark Hendrick III, Partner, Vinson & Elkins L.L.P., to James V. Derrick, Jr., Executive Vice President and General Counsel, Enron, Re: Preliminary Investigation of Allegations of an Anonymous Employee 1-2 (Oct. 15, 2001), reprinted in id. at 142-43 [hereinafter Vinson & Elkins Report]. The report also stated that contrary to Watkins’ recommendation, Enron’s General Counsel had decided not to hire an independent accountant. Id. 22. House Hearing, supra note 13, at 20; Vinson & Elkins Report, supra note 21, at 8-9, reprinted in House Hearing, at 149-50. The report characterized any potential concerns with the transactions as primarily “bad cosmetics.” Vinson & Elkins Report, supra note 21, at 9, reprinted in

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 362 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

days before Enron announced its third quarter loss of more than $500 million and its $1 billion write-down in shareholder equity.23 Three months later, Enron filed for bankruptcy.

Sherron Watkins never brought her concerns to Enron’s board or the SEC,24 but she provided devastating testimony at congressional hearings that probed into Enron’s collapse.25 During a pre-hearing review of subpoenaed Enron documents, she came across a telling e-mail from a Vinson & Elkins lawyer to Enron’s Assistant General Counsel. Bearing the subject line “Confidential Employee Matter,” the message read in pertinent part:

Per your request the following are some bullet thoughts on how to manage the case with the employee who made the sensitive report.

. . . .

You . . . asked that I include in this communication a summary of the possible risks associated with discharging (or constructively discharging) employees who report allegations of improper accounting practices:

1. Texas law does not currently protect corporate whistle-blowers. The Supreme Court has twice declined to create a cause of action for whistle-blowers who are discharged.

. . . .

4. In addition to the risk of a wrongful discharge claim, there is the risk that the discharged employee will seek to convince some government oversight agency (e.g., IRS, SEC, etc.) that the corporation has engaged in materially misleading reporting or is otherwise non-compliant. As with wrongful discharge claims, this

House Hearing, at 150. 23. E-mail from Carl Jordan, Attorney and Member, Vinson & Elkins, to Sharon Butcher, Staff Attorney, Enron, Re: Confidential Employee Matter (Aug. 24, 2001) [hereinafter Jordan E-mail] (on file with author); PIPE DREAMS, supra note 11, at 298; House Hearing, supra note 13, at 64. 24. She later regretted her naiveté in believing that reporting the fraud to top management would resolve the crisis and wished she had brought her concerns to higher authority. The Party Crasher, supra note 13, at 54. From the perspective of her staunchest critics, her efforts were flawed not only because she failed to inform federal regulators about the fraud, but also because she failed to confront Skilling and Fastow or even to go to Enron’s board. Wendy Zellner, Was Sherron Watkins Really So Selfless?, BUS. WEEK, Dec. 16, 2002, at 110; WHAT WENT WRONG, supra note 13, at 142. 25. See House Hearing, supra note 13, at 14-67.

http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

p357 Brickey book pages.doc10/24/03 12:46 PM 2003] FROM ENRON TO WORLDCOM AND BEYOND 363

can create problems even tho [sic] the allegations have no merit whatsoever.26

The message was dated just two days after Watkins met with Ken Lay. The e-mail served as a stark reminder that, as a general matter,

whistleblowers are underappreciated by corporate managers.27 Bearing that observation out, Andy Fastow was furious that Watkins had talked to Ken Lay. Upon learning that she had, he told Watkins’ direct supervisor that he wanted Watkins “out of here tonight” and seized the laptop computer from her desk.28 Despite the heated rhetoric, Watkins remained an Enron Vice-President. But she was reassigned from her executive suite to a starkly furnished office 33 floors below and relegated to performing make-work tasks.29 The environment was so tense that she even sought

26. Jordan E-mail, supra note 23; The Party Crasher, supra note 13, at 53. 27. As Senator Charles Grassley (a Sherron Watkins fan) quipped, a corporate employee who blows the whistle is as about as welcome “as a skunk at a picnic.” Paula Dwyer & Dan Carrey, Year of the Whistleblower, BUS. WK., Dec. 16, 2002, 107, at 108 [hereinafter Whistleblower] (quoting Senator Charles Grassley). The current dispute over the credibility of James Krutchen, a former employee of Onvoy, is another case in point. Krutchen was the whistleblower who alleged that MCI and other telecom companies committed fraud by improperly routing phone calls to avoid access fees they owed other phone companies. Janice Aune, Onvoy’s President and CEO, attacked Krutchen’s credibility and publicly released his personnel record to discredit him. She portrayed him as a disgruntled employee who was fired because of his poor performance record and justified the release of personnel information on the ground that Onvoy had become “the victim of corporate terrorism.” Stephen Labaton, Credibility of Witness is Challenged in MCI Inquiry, N.Y. TIMES, Aug. 2, 2003, at B1. See also Yochi J. Dreazen, Views Diverge on Credibility of MCI Informer, WALL ST. J., Aug. 4, 2003, at B1. 28. PIPE DREAMS, supra note 11, at 298. Several executives were alarmed by Mr. Fastow’s reaction. House Hearing, supra note 13, at 18-19. Although he seized her computer, another superior promptly replaced it and allowed Watkins to transfer files from the hard drive of the confiscated laptop. Id. at 19. 29. Richard Lacayo & Amanda Ripley, Persons of the Year, TIME, Dec. 30, 2002/Jan. 6, 2003, 30, at 33. See also MIMI SWARTZ, POWER FAILURE 300-01, 321-25 (2003) [hereinafter POWER FAILURE]. Ms. Watkins was transferred from the corporate development group to the human resources group. House Hearing, supra note 13, at 15. She testified that she asked to be transferred because she was no longer comfortable reporting directly to Fastow. Id. at 16. See also Jordan E-mail, supra note 23 (memorandum from outside lawyer stating that Ms. Watkins’ request for reassignment was “a positive”). Ms. Watkins later wrote that “I haven’t really had a real job since my first meeting with Ken re: these matters in late August.” Memorandum from Sherron Watkins to Elizabeth Tilney, Senior Vice President for Advertising, Communications and Organization Development, Enron (Oct. 30, 2001) (on file with author) (offering to assist in devising a viable public relations strategy to deal with Enron’s crisis). Sherron Watkins was not the only employee whose skepticism about Enron’s finances resulted in de facto demotion. Keith Power was an Enron manager who monitored the Enron stock held in JEDI, a special purpose entity, and supervised JEDI’s routine debt administration. After an executive told him about a negative Enron story posted on a Web site, Power delved more deeply and discovered that the story was based on a longer proprietary report prepared by a highly respected stock analyst. Power

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 364 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

advice from Enron security personnel.30 Fastow’s angry reaction and Vinson & Elkins’ e-mail clearly

demonstrate that Enron managers did not welcome the opportunity to take corrective action. They knew they had a big problem, and they wanted it to go away. But the “it” was less the accounting issues than it was the vice-president who brought them to light.

2. Sarbanes-Oxley

Because she had an insider’s perspective into Enron’s labyrinthine accounting maneuvers, Sherron Watkins was able to provide a roadmap for a highly complex financial fraud investigation.31 But it takes courage to do that.32 Whistleblowers have historically been at risk of being labeled

called the analyst, who faxed him the 30 page report and gave him permission to show it around the company. The upshot of the report was that the analyst thought that Enron stock was overvalued, that he questioned the quality of earnings, and that he was troubled that senior Enron executives were selling their Enron stock. The report confirmed what Power already suspected, and he gave copies to several executives he worked with. Two days later, Power’s boss told him that he “shouldn’t have distributed” the report, not to give it to anyone else, and to forget that he ever saw it. POWER FAILURE, supra note 29, at 257-59. Three days later, Power was transferred to another group with a less desirable assignment. He was snubbed by his superiors, given relatively little meaningful work, and was ultimately demoted despite high marks from his peers. Id. at 307-08. 30. The Party Crasher, supra note 13, at 53. See also House Hearing, supra note 13, at 49-50, 62. Although she had not been threatened with physical harm, she was concerned that her superiors might be vindictive and that she had very little support. “I did feel like I was a little bit of a lone fish swimming upstream, and so it starts to wear on you that it’s you against them. . . .” Id. at 62. Perhaps the underlying assumption was that if you make life unpleasant enough for the whistleblower, you may not have to fire her. She may leave on her own volition. 31. Whistleblower, supra note 27, at 107. While working for Fastow, Watkins’ responsibilities included reviewing and valuing all assets that Enron considered selling. In the course of doing this, she learned that hedged losses incurred by one of the special purpose entities were transferred to Enron. She was “alarmed” by the explanations she received and found them contrary to her understanding of accounting principles. But despite her efforts to clarify the situation, she found no reassuring answers. House Hearing, supra note 13, at 15. Despite her central role in revealing the fraud, the Powers Committee—a special committee of the Enron Board charged with conducting an internal investigation—did not contact Ms. Watkins until late December, when the Committee’s work was almost done. House Hearing, supra note 13, at 51. Although she and her newly retained lawyer met with the Committee a week after the Committee’s request, they told the Committee they would need to reschedule so her lawyer could get up to speed. Id. Apart from references in the Committee’s report that described the time line of Ms. Watkins’s revelation of the fraud, the only reference to her is a footnote statement that “Watkins, through her counsel, declined to be interviewed by us.” Report of Investigation by the Special Investigative Committee of the Board of Directors of Enron Corporation 172 n.81 (Feb., 1, 2002), available at http://news.findlaw.com/legz/news/lit/enron/. Taken out of context, the report disingenuously implies a lack of cooperation on her part. 32. Representative John Dingell called Watkins “an extraordinary, courageous woman, who has been a bright spot in an otherwise sorry and outrageous saga.” WHAT WENT WRONG, supra note 13, at 142. See also House Hearing, supra note 13, at 55 (remarks of Representative Gene Green)

http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

p357 Brickey book pages.doc10/24/03 12:46 PM 2003] FROM ENRON TO WORLDCOM AND BEYOND 365

troublemakers. Even the House Subcommittee that so eagerly sought her testimony gave the term “whistleblower” a negative connotation. “Ms. Watkins is not a whistleblower in the conventional sense. She was and is a loyal company employee.”33 The implication, of course, is that most whistleblowers are not.

Apart from the very real risk of being shunned by co-workers as disloyal tattletales, whistleblowers are often demoted, fired, or even blackballed by an entire industry.34 A random review of 200 whistleblower complaints filed with the National Whistleblower Center in 2002 found that about half of the complainants said they were fired after they reported misconduct.35 The remaining complainants had been subjected to other retaliatory action such as on-the-job harassment or discipline. A survey by another watchdog group, the Government Accountability Project, found that about ninety percent of whistleblowers are subjected to reprisals or threats.36

In recognition of the crucial role that corporate whistleblowers play,37 Sarbanes-Oxley endeavors to reverse this trend by providing them significant legal protection.38 In addition to creating civil remedies for

(expressing respect and admiration for Watkins’ courage in putting her job on the line by reporting her concerns to the CEO). 33. House Hearing, supra note 13, at 3 (remarks of Representative James Greenwood). 34. Whistleblower, supra note 27, at 108. Indeed, Ms. Watkins said she believed that confronting either Mr. Skilling or Mr. Fastow would have been a “job terminating move.” House Hearing, supra note 13, at 15. Cf. id. at 52 (cautioning Ms. Watkins that if her cooperation with the Committee’s investigation had adverse repercussions at Enron, she should let the Committee know); id. at 61 (asking Ms. Watkins to inform the Committee promptly of any threatened retaliation resulting from her testimony or her reporting the fraud to Ken Lay). 35. National Whistleblower Center, The National Status of Whistleblower Protection on Labor Day, 2002 (Sept. 2, 2002) (unpaginated) (on file with author). Of these 200 cases, the largest category of wrongdoing the whistleblowers reported consisted of fraud or other criminal misconduct. The whistleblowers’ employment status ran the gamut from corporate executives to maintenance employees. This study does not purport to be scientific. It is a random survey of cases in which individual whistleblowers had complained about retaliatory treatment. Thus, while the self-selection bias inherent in the study would not pass scientific muster, it nonetheless sheds anecdotal light on the perils of whistleblowing. 36. Gail Russell Chaddock, Enron Changes Climate for Whistle-Blowers, THE CHRISTIAN SCIENCE MONITOR, Mar. 1, 2002, at 5 [hereinafter Enron Changes Climate]. 37. “We learned from Sherron Watkins of Enron that these corporate insiders are the key witnesses that need to be encouraged to report fraud and help prove it in court.” The Truth Is Out There, LEGAL WK. (Aug. 20, 2002), at http://www.legalweek.net/ViewItem.asp?id=10241 (quoting Senator Patrick Leahy). According to a recent study, thirty-six percent of frauds and other economic crimes against businesses are reported by whistleblowers. Jonathan D. Glater, Survey Finds Fraud’s Reach in Big Business, N.Y. TIMES, July 8, 2003, at C3. 38. Unlike Sarbanes-Oxley’s civil whistleblowing provisions, which only protect employees of publicly traded companies, the criminal provision applies to harmful retaliatory acts toward any

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 366 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

employee retaliation in fraud cases,39 Sarbanes-Oxley makes it a felony to take any action that is harmful to any person in retaliation for providing information about a federal crime to law enforcement officials.40 The “harm” element includes, but is not limited to, interference with another’s lawful employment or livelihood.41 Thus, a retaliatory firing or demotion

witness or informant. 39. The civil whistleblower provision forbids publicly traded companies and their officers and agents from discharging, demoting, suspending, threatening, harassing, or otherwise discriminating against an employee in retaliation for the employee’s providing information about securities fraud, mail and wire fraud, or bank fraud to a federal regulator or investigator, to members of Congress, to a corporate supervisor, or to anyone working for the corporation who has the authority to investigate or terminate misconduct. 18 U.S.C.A. § 1514A(a) (West Supp. 2003). The civil statute also prohibits retaliating because the employee participated or assisted in a proceeding relating to securities fraud, mail and wire fraud, or bank fraud. 18 U.S.C.A. § 1514A(b) (West Supp. 2003). A whistleblower may seek relief by filing a complaint with the Secretary of Labor within 90 days of the retaliatory act and may file suit in federal court if the Secretary does not issue a final decision within 180 days after the complaint is filed. 18 U.S.C.A. § 1514A(c) (West Supp. 2003). The statute authorizes recovery of compensatory damages including reinstatement, back pay, and special damages such as the cost of litigating the claim, expert witness fees, and reasonable attorneys’ fees. 18 U.S.C.A. § 1514A(d) (West Supp. 2003). The Labor Department received more than 110 whistleblower complaints in the first 14 months after this provision became law. Laurie P. Cohen, Quattrone Trial: New Template?, WALL ST. J., Sept. 30, 2003, at C1. Another civil provision requires audit committees of public companies to establish procedures for handling employee complaints about auditing and internal accounting issues. Among other things, the committee must protect whistleblowers by establishing procedures for the submission of confidential, anonymous concerns about such matters. 15 U.S.C.A. § 78j-1(m)(4) (West Supp. 2003). Rejecting a “one size fits all” approach, SEC regulations implementing this provision give audit committees discretion to adopt procedures they deem appropriate in light of the particular circumstances or needs of the company. Standards Relating to Listed Company Audit Committees, 68 Fed. Reg. 50,379 (Apr. 16, 2003) (to be codified at 17 C.F.R. pts. 228, 229, 240, 249, 274). 40. 18 U.S.C.A. § 1513(e) (West Supp. 2003). The term “law enforcement officer” means federal officers and employees who are legally authorized to investigate or prosecute an offense. 18 U.S.C.A. § 1515(a)(4) (West Supp. 2003). Section 1513(e) is an amendment to a witness retaliation provision in the Victim and Witness Protection Act that punishes the use or threat of violence against person or property in retaliation for another person’s cooperation with federal law enforcement officials. 18 U.S.C.A. § 1513(a) (West 2000 & Supp. 2003); 18 U.S.C.A. § 1513(b) (West Supp. 2003). The criminal statute applies whenever the whistleblower reports evidence of any federal crime, 18 U.S.C.A. § 1513(e) (West Supp. 2003), while the protections of the civil whistleblower statute are triggered only when the employee reports possible securities fraud, mail and wire fraud, or bank fraud. 18 U.S.C.A. § 1514A(a)(1) (West Supp. 2003). See supra note 39. 41. The statute is not a model of clarity. Unlike its counterparts in subsections (a) and (b), the whistleblower protection provision is ambiguous on the question whether it protects against retaliatory actions that harm third persons. Compare 18 U.S.C.A. § 1513(a) (West 2000 & Supp. 2003) and 18 U.S.C.A. § 1513(b) (West Supp. 2003) (prohibiting causing, attempting to cause, or threatening to cause death, bodily injury, or property damage to another person with intent to retaliate against any person for his cooperation as a witness or informant) with 18 U.S.C.A. § 1513(e) (West Supp. 2003) (prohibiting taking action that is harmful to any person with intent to retaliate for providing truthful information to law enforcement officers but failing to specify toward whom the retaliatory intent must be directed). See 3 KATHLEEN F. BRICKEY, CORPORATE CRIMINAL LIABILITY § 12:23 (2d ed. Supp. 2002).

http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

p357 Brickey book pages.doc10/24/03 12:46 PM 2003] FROM ENRON TO WORLDCOM AND BEYOND 367

would constitute a crime.42 The statute prohibits retaliating against those who voluntarily come

forward to report suspected criminal activity as well as those who are sought out by federal investigators. Thus, regardless of whether someone like Sherron Watkins contacted the SEC about Enron’s accounting fraud or whether SEC investigators contacted her as part of an ongoing probe, any harmful act in retaliation for her cooperation would be felonious.

This provision fills a major loophole in the Victim and Witness Protection Act, whose witness retaliation prohibitions previously applied only to violence or threats of violence.43 By extending the prohibition to any harmful act, Sarbanes-Oxley significantly strengthens the legal protections accorded federal witnesses and informants.44 That said, it is nonetheless important to recognize the statute’s inherent limitations.

Sherron Watkins reported what she knew to Enron’s Chairman. The Vinson & Elkins e-mail about managing the “confidential employee matter” made it clear that within two days after she met with Ken Lay, Enron executives were considering all available options. If they had fired her on the spot, they would not have violated the witness retaliation statute because she had yet to tell law enforcement officials what she knew.45 Thus, even though Sarbanes-Oxley fills an important gap in the criminal law, Sherron Watkins’ whistleblowing had not gone far enough to trigger

42. Other means of wrongfully interfering with the whistleblower’s livelihood could include reorganizing the company to eliminate her job, spreading false rumors that impair her reputation, causing the denial or revocation of an essential business or professional license, blacklisting her in the industry, or falsely accusing her of a crime. But the statute is not limited to retaliation that causes economic harm. In consequence, it is possible that intentionally inflicting intangible harms like emotional distress could be prohibited as well. This is in marked contrast with the civil whistleblower provision, which is limited to discrimination against the employee “in terms and conditions of employment.” 18 U.S.C.A. § 1514A(a) (West Supp. 2003). See supra note 39. 43. See 18 U.S.C.A. § 1513(a) (West 2000 & Supp. 2003); 18 U.S.C.A. § 1513(b) (West Supp. 2003) (punishing, respectively, killing or attempting to kill a witness or informant to prevent him from participating in an official proceeding, and using or threatening to use intimidation or physical force to prevent a witness or informant from participating in an official proceeding). 44. The witness retaliation statute, § 1513, is one of dozens of federal offenses enumerated as RICO predicate crimes. See 18 U.S.C.A. § 1961(1) (West Supp. 2003). Because the whistleblower provision amends § 1513, retaliation against a corporate whistleblower can be part of a RICO pattern of racketeering activity in a criminal prosecution or a civil RICO suit brought by private litigants. See 18 U.S.C.A. § 1961(5), § 1963, § 1964(c) (West 2000). Section 1513 is also a predicate crime under the money laundering statutes. See 18 U.S.C.A. §§ 1956(a)(1) (West 2000); 18 U.S.C.A. § 1956(c)(7) (West Supp. 2003); 18 U.S.C.A. §§ 1957 (a), (f)(3) (West 2000). 45. In contrast, the civil whistleblower provision more broadly protects not only employees who report fraud to federal regulators and investigators but also extends its protections to employees who report to a corporate supervisor, assist members of Congress, or participate or assist in a legal proceeding. 18 U.S.C.A. § 1514A(a) (West Supp. 2003). See supra note 39.

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 368 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

its protections.46 It was only after she was subpoenaed that she told outsiders what she knew.47

But there is another lingering question as well. After Sarbanes-Oxley, would Sherron Watkins have been more likely to bypass the corporate chain of command and report the fraud directly to the SEC? It is not so clear that she would. It is understandable that she would bring Enron’s accounting problems to the attention of her superiors before going to the SEC.48 First, she feared that public disclosure of her concerns would hasten Enron’s demise.49 She worried that if she went outside the corporate chain of command, management would lose the opportunity to thoroughly examine the problem and “try to fix it calmly.”50 Second, she believed Ken Lay was “a man of integrity.”51 She might reasonably expect that if she gave him evidence of massive fraud, he would do whatever it took to clean it up. Indeed, she believed that by going to Ken Lay she would hand him “his leadership moment.”52 But that was not to be. His efforts to address Ms. Watkins’ concerns—however sincere—were lukewarm and ineffective at best.53

Thus, it is far from clear that Sarbanes-Oxley’s prohibition against witness retaliation would induce a Sherron Watkins to take action that she feared would doom the corporation and put the livelihoods of thousands of

46. She would have been protected under the civil whistleblower provision, which extends to corporate employees who report suspected wrongdoing to a supervisor. 18 U.S.C.A. § 1514A(a)(1)(C) (West Supp. 2003). See supra note 39. 47. The first week in January she received an SEC subpoena ordering her to produce, within seven days, three years worth of Enron bank records and all Enron records and stock records. The SEC also wanted to interview her during that same time frame. POWER FAILURE, supra note 29, at 344. 48. Ironically, her chain of command approach was consistent with the approach taken by the Private Securities Litigation Reform Act of 1995, which—among other things—specifically addressed how independent public auditors should initially respond if they detect possible illegal acts while performing a required audit of an issuer’s financial statements. See 15 U.S.C.A. § 78j-1(b)(1)(B) (West Supp. 2003) (requiring the auditor, as soon as is practicable, to “inform the appropriate level of the management” and to assure that the audit committee or the board of directors is also informed unless the illegal act is “inconsequential”). 49. House Hearing, supra note 13, at 50-51. 50. Id. at 51. 51. Id. at 49. 52. The Party Crasher, supra note 13, at 54. 53. Ms. Watkins believed that Ken Lay and the board had been “dupe[d]” by Skilling and Fastow, House Hearing, supra note 13, at 21, and that Mr. Lay should not bear full responsibility for the accounting mess. Memorandum from Sherron Watkins to Elizabeth Tilney, Senior Vice President for Advertising, Communications and Organization Development, Enron (Oct. 30, 2001) (attachment) (on file with author) (stating that if Mr. Lay did not act to clean up the mess, the worst would happen, and he would bear a disproportionate share of the blame). Ms. Watkins also testified that even after she informed Mr. Lay of the special purpose entity problem, he did not fully understand the seriousness of the issue. House Hearing, supra note 13, at 23.

http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

p357 Brickey book pages.doc10/24/03 12:46 PM 2003] FROM ENRON TO WORLDCOM AND BEYOND 369

people at risk.54 She reported her concerns to Ken Lay because he was the one person in authority whom she thought she could trust.55 Lay had the power to take corrective action, and he assured her that he would.

But there is also another dynamic at work. During Ms. Watkins’ meeting with Ken Lay, he inquired whether she had talked to the SEC or the press. When she said she had not, he asked her to refrain from going public until he had time to investigate.56 A reasonable request? Presumably so, and she readily agreed. After all, Ms. Watkins had achieved what she had boldly set out to accomplish—or so she was led to believe.

B. WorldCom

1. Cynthia Cooper

The circumstances under which WorldCom’s fraud was brought to light are dishearteningly similar to Sherron Watkins’ tale. Like Ms. Watkins, Cynthia Cooper—WorldCom’s Vice President for Internal Auditing—also sought to expose and correct a massive accounting fraud. Her suspicions arose when a concerned official in the wireless division told her the accounting department had taken $400 million from his reserve account and used it to inflate WorldCom’s income. She first raised the issue with Arthur Andersen, WorldCom’s accounting firm. Although Andersen insisted that everything was fine, she continued to press on—notwithstanding that her boss, CFO Scott Sullivan, angrily told her to back off.57

Concerned by Sullivan’s hostility and worried about the reliability of Andersen’s audits, Cooper and her accounting team secretly conducted an extensive review of the books, working at night and copying data to a CD to prevent it from being destroyed. Within a few months they learned that in 2001, billions of dollars in ordinary operating costs had been improperly recorded as capital expenditures, thus disguising a $662 million loss as a $2.4 billion profit.58 When Scott Sullivan discovered that Cooper’s team was auditing Andersen’s work, he asked her to suspend the review. But Cooper refused to yield.59

54. House Hearing, supra note 13, at 50. 55. Ms. Watkins testified that she believed she could bring her concerns to him, but not to Jeff Skilling. Id. at 49. 56. Id. at 50-51. 57. Amanda Ripley, The Night Detective, TIME, Dec. 30, 2002/Jan. 6, 2003, 44, at 46-47. 58. Id. at 47. 59. Id.

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 370 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

Instead, she went to the head of the board’s audit committee the following day. To its credit, the committee did the right thing. Within little more than a week, the audit committee convened a meeting in which all sides of the issue were fully aired. When all was said and done, the committee found Sullivan’s explanation of the unorthodox accounting practices unpersuasive and concluded that they could not be justified. The committee then told Sullivan and Controller David Myers that if they did not resign, the board would fire them the next day.60

2. Sarbanes-Oxley

Why didn’t Cynthia Cooper go to the SEC? It must be hard to blow the whistle on your mentors. It must be harder still to report that they might have committed crimes. And up until the last minute, Cynthia Cooper had hoped that someone could provide a reasonable explanation for the accounting errors she had found.61

Thus, as with Enron, it remains to be seen whether Sarbanes-Oxley’s whistleblower protections would provide a sufficient incentive to cause a Cynthia Cooper—a “loyal corporate employee”—to bypass the normal chain of command. Yet even if no one came forward on their own, the whistleblower statute could lead to felony penalties for firing or demoting any corporate employee interviewed by the SEC, the FBI, or the Justice Department in retaliation for providing information regarding criminal wrongdoing in the organization. That is a significant change in the law.

II. COOPERATING WITNESSES

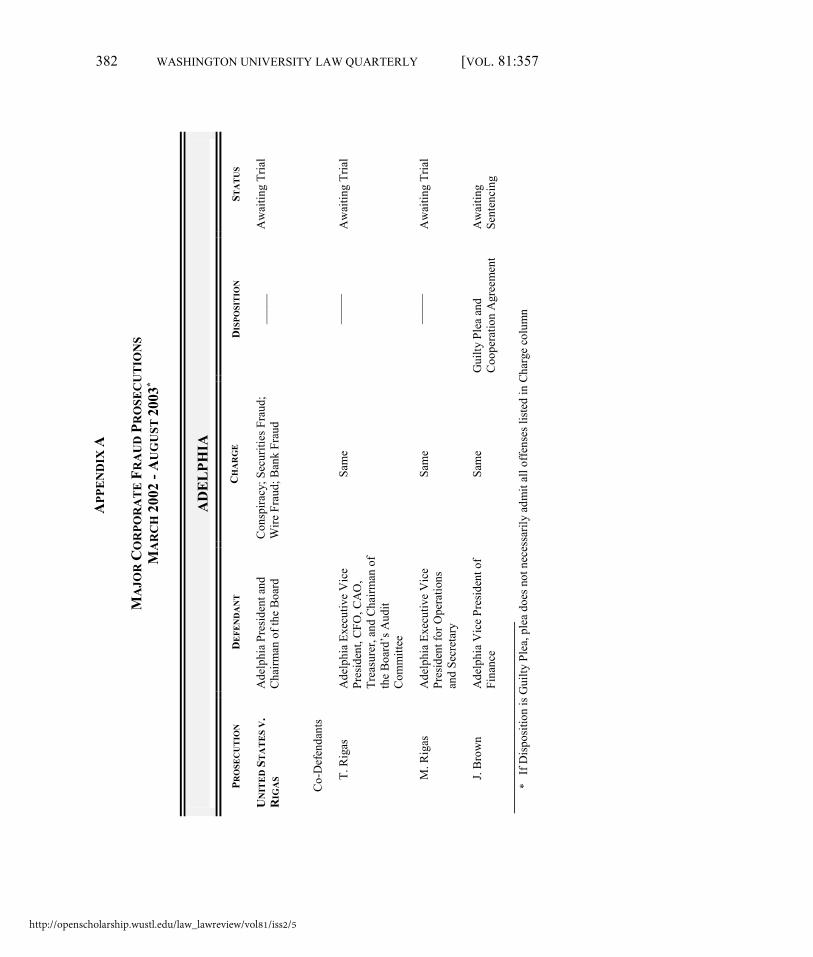

A. Adelphia Communications

“I deeply regret my participation in this fraud. . . . I knew at that time that what I was doing was wrong, and that I should have walked out rather than agree to participate.”62 These are the words of Timothy Werth, Adelphia’s Director of Accounting. He spoke them in federal court as he pled guilty to conspiracy and securities fraud charges arising out of a $2.5

60. Myers resigned but Sullivan did not, so the board dismissed him as promised. Id. at 49. Myers has since pled guilty to conspiracy, securities fraud, and filing false statements with the SEC. As of this writing, Sullivan is awaiting trial on similar criminal charges. 61. After going to the audit committee, she and her audit team remained hopeful that they could find something they might have missed that would explain the unorthodox accounting. But Cooper’s hopes were dashed when she confronted WorldCom Controller David Meyers, who conceded that the entries could not be justified. Id. at 47.

62. Former Adelphia Executive Enters a Guilty Plea, N.Y. TIMES, Jan. 11, 2003, at E3.

http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

p357 Brickey book pages.doc10/24/03 12:46 PM 2003] FROM ENRON TO WORLDCOM AND BEYOND 371

billion accounting scandal that led to Adelphia’s bankruptcy. The plea hearing marked the beginning of his formal participation as a cooperating witness in the Adelphia criminal investigation. Two months earlier, James Brown, Adelphia’s Vice President for Finance, also pled guilty to fraud and conspiracy and agreed to help the government build its case.63

Werth’s and Brown’s agreements to become cooperating witnesses are significant because four other Adelphia executives had already been indicted and were then awaiting trial. Notably, at least three of the four were far bigger fish than either Werth or Brown. They included John Rigas, the President and Chairman of the Board; Timothy Rigas, the Chief Financial Officer and Chairman of the Board’s Audit Committee; Michael Rigas, the Executive Vice President for Operations; and Michael Mulcahey, the Director of Internal Reporting. The indictment charged the four with conspiracy, securities fraud, wire fraud, and bank fraud.64 It alleged that the President had looted the company on a “massive scale” and that he and his family had used Adelphia as their “personal piggy bank.”65

Mr. Brown’s plea implicated all four of the executives in criminal wrongdoing, and Mr. Werth admitted that he conspired with the CFO and others. Their cooperation will thus provide invaluable assistance to the government in building its case against the other four executives, both during the investigation and at their trial. But it is equally important that Werth and Brown may also be poised to provide the government with leads about other possible participants in the fraud.

B. WorldCom

The WorldCom investigation also yielded important cooperating witnesses. The government first indicted Scott Sullivan—a CPA and WorldCom’s CFO, Treasurer, and Secretary—and Buford Yates, also a CPA and WorldCom’s Director of General Accounting.66 The indictment

63. Benjamin Weiser, Ex-Executive Pleads Guilty and Accuses Adelphia’s Founder, N.Y. TIMES, Nov. 15, 2002, at C7. Mr. Brown pled guilty to conspiracy, bank fraud and securities fraud charges. 64. United States v. Rigas (indictment filed in United States District Court for the Southern District of New York) (Sept. 23, 2002) (on file with author). The substance of the allegations is that the four executives engaged in a scheme to deprive Adelphia and its shareholders of the right to the honest services of its directors and officers, to violate fiduciary duties to the company and its shareholders, and to fraudulently obtain Adelphia’s money or property. Id. at 13. The bank fraud counts allege false representations made in credit agreements involving more than $4 billion. 65. Id. 66. United States v. Sullivan (indictment filed in United States District Court for the Southern District of New York) (Aug. 28, 2002) (on file with author).

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 372 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

charged them with conspiring to inflate WorldCom’s earnings, committing securities fraud, and making false filings with the SEC. Mr. Yates later pled guilty to the conspiracy and securities fraud charges and agreed to cooperate with the investigation. At his plea hearing, he said he committed the crimes on orders from the “highest levels” of senior management.67

The Sullivan indictment also named three unindicted co-conspirators as participants in the scheme. They were: David Myers, a CPA and WorldCom’s Senior Vice President and Controller, and Betty Vinson and Troy Normand, both WorldCom accounting officials who worked under Yates’ supervision. After Yates entered his guilty plea, Myers, Vinson, and Normand were charged in separate prosecutions with conspiracy and securities fraud.68 Myers was also charged with submitting false SEC filings.

In contrast with the prosecution of Sullivan and Yates, the cases against Myers, Vinson, and Normand were initiated by the filing of a criminal information rather than an indictment.69 All three pled guilty on the day the information was filed, and in each case a cooperation agreement was part of the plea bargain. At separate plea hearings, Vinson and Normand stated that they were obeying orders from their supervisors—including Scott Sullivan—to cook WorldCom’s books.70 At his plea hearing, Myers informed the court that he was told by “senior management” to falsify WorldCom’s books to inflate reported earnings.71

The potential value of these plea agreements is obvious. All four cooperating defendants implicated Scott Sullivan in the fraud and can be called to testify at his trial. The prospect that Myers might provide damaging testimony against his former boss puts enormous pressure on Sullivan.72 But the plea agreements are important in the continuing

67. Robert F. Worth, Ex-Official Of WorldCom Pleads Guilty To Fraud, N.Y. TIMES, Oct. 8, 2002, at C9; Jerry Markon, WorldCom’s Yates Pleads Guilty, WALL ST. J., Oct. 8, 2002, at A3. 68. United States v. Myers, 02-CR-1261 (S.D.N.Y. Aug. 25, 2002) (Information); United States v. Vinson, 02 CR-1349 (S.D.N.Y. Oct. 10, 2002) (Information); United States v. Normand (information filed in United States District Court for the Southern District of New York) (Oct. 10, 2002) (all on file with author); 2 Ex-Officials of WorldCom Plead Guilty, N.Y. TIMES, Oct. 11, 2002, at C10. 69. The filing of a criminal information is a less formal way to proceed than presenting the case to a grand jury and seeking the return of an indictment. In federal court, the Constitution prohibits bringing a defendant to trial for a felony offense without an indictment unless the defendant waives the right to a grand jury proceeding. U.S. CONST., Amend. V. 70. 2 Ex-Officials of WorldCom Plead Guilty, N.Y. TIMES, Oct. 11, 2002, at C10. 71. Former Controller of WorldCom Pleads Guilty to Fraud Charges, N.Y. TIMES, Sept. 27, 2002, at C2; Deborah Solomon, WorldCom’s Ex-Controller Pleads Guilty to Fraud, WALL ST. J., Sept. 27, 2002, at A3. 72. Deborah Solomon, WorldCom’s Ex-Controller Pleads Guilty to Fraud, WALL ST. J., Sept.

http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

p357 Brickey book pages.doc10/24/03 12:46 PM 2003] FROM ENRON TO WORLDCOM AND BEYOND 373

investigation as well. The cooperation of these witnesses is likely to intensify the government’s scrutiny of other senior managers to determine who among them may have participated in or approved the plan to crudely inflate WorldCom’s revenues.73 Thus, by the time all is said and done, it is possible that criminal charges will be filed against other WorldCom officials as well.

C. Cooperation Agreements

Like whistleblowers, cooperating witnesses play essential roles in investigations and prosecutions arising out of the corporate accounting fraud scandals, in part due to the nature of the underlying crimes. Enron, WorldCom, and Adelphia involve highly complex fraud investigations. Massive accounting frauds that artificially inflate corporate revenues to the tune of billions of dollars are crimes involving elaborate efforts to conceal. Corporate officials hid debt and manufactured revenue by making false entries, creating special purpose entities, and using other unorthodox accounting techniques.

With the aid of Wall Street lawyers, accountants, and investment banks, Enron also devised tax shelters that enabled the corporation to avoid paying any taxes over a period of years, even though it booked billions of dollars of profits.74 The transactions were so complex that even the IRS did not understand them. Effective investigation of these transactions thus requires an enormous investment of time, money, and personnel, including forensic experts. To sort the intricacies out, investigators need the benefit of insiders’ knowledge of the corporate chain of command, the inner workings of the organization’s accounting system, and the day-to-day interactions among key players.

27, 2002, at A3. Indeed, there were reports that plea negotiations between Mr. Sullivan and Justice Department lawyers broke down when the prosecutors insisted that he serve at least ten years in prison. Deborah Solomon, Jerry Markon & Susan Pulliam, Sullivan Indictment May Be Near, WALL ST. J., Aug. 28, 2002, at A3; Mike Claffey, Feds Indict WorldCom Executive, N.Y. DAILY NEWS, Aug. 29, 2002, News Section, at 9. Later reports suggested that plea negotiations may have resumed, but as of the date of this writing, there is no solid evidence that they have. 73. Former Controller of WorldCom Pleads Guilty to Fraud Charges, N.Y. TIMES, Sept. 27, 2002, at C2; 2 Ex-Officials of WorldCom Plead Guilty, N.Y. TIMES, Oct. 11, 2002, at C10. See infra text accompanying notes 76-78. 74. David Cay Johnston, Wall St. Firms Are Faulted in Report on Enron’s Taxes, N.Y. TIMES, Feb. 14, 2003, at C1. According to a staff report issued by the Joint Committee on Taxation, Enron’s tax department functioned like a corporate business unit and had annual revenue targets. The tax shelter schemes were so aggressive that the front page of one deal known as the Steele Project bore the title “Show Me the Money!” Id.

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 374 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

As a practical matter, large-scale corporate accounting frauds require cooperative efforts among managers and their subordinates. Yet notwithstanding that high-level executives may have engineered the fraud, there will rarely be a paper trail that leads to the top. Just as the Enron and WorldCom whistleblowers went up the chain of command in reporting the fraud, corporate officials can use layers of bureaucracy to distance themselves from the acts of subordinates and keep their hands clean.75

WorldCom is a case in point. Prosecutors are reportedly trying to determine whether CEO Bernard Ebbers had any role in the fraud.76 They hoped to obtain productive leads from the cooperating witnesses, all of whom said they falsified the company’s books on orders from high-level managers.77 But just how far up the line responsibility goes may be hard to resolve. According to WorldCom insiders, Ebbers delegated virtually everything. And notwithstanding that he was in charge of one of the world’s largest Internet companies, he was widely reputed to be a technophobe. He did not use e-mail, never took notes, and rarely used a computer. As one executive said, “[i]f people had questions for him, they’d fax them to his secretary and he’d call them back or scribble a reply.”78 He met mainly with top executives, and no minutes or records of meetings were kept. Thus, with no paper trail to follow, investigators face an uphill battle in their quest to learn “what did Ebbers know and when did he know it?”79

This provides prosecutors an incentive to begin farther down the line. Because mid-level managers are most likely to be “hands on” when it comes to implementing the fraud, they are most likely to leave a traceable trail and are most vulnerable to criminal prosecution. Thus, without the

75. And while the Board of Directors may give unorthodox accounting methods a wink and a nod, their winks and nods will not be recorded in the corporate minutes. Cf. Commonwealth v. Beneficial Finance Co., 275 N.E.2d 33, 82 (Mass. 1971) (“Criminal acts are not usually made the subject of votes of authorization or ratification by corporate Boards of Directors . . . . ”). 76. Former Controller of WorldCom Pleads Guilty to Fraud Charges, N.Y. TIMES, Sept. 27, 2002, at C2; 2 Ex-Officials of WorldCom Plead Guilty, N.Y. TIMES, Oct. 11, 2002, at C10. 77. See supra text accompanying notes 66-71. 78. Jessica Hall, Ebbers Left Little Evidence; WorldCom CEO Always Low-Tech, HOUS. CHRON., Oct. 15, 2002, Business Section, at 4. But cf. Report of Investigation by the Special Investigative Committee of the Board of Directors of WorldCom, Inc. (March 31, 2003) (finding, inter alia, clear evidence that Ebbers knew that WorldCom’s reported revenues were inflated through financial gimmickry). 79. While this article was in press, the Oklahoma Attorney General filed criminal charges against Ebbers, alleging that he violated state securities laws. The information also charged WorldCom, Sullivan, Myers, Vinson, and Normand with the same crimes. State v. WorldCom, Inc. (felony information filed in District Court of Oklahoma County, Oklahoma) (Aug. 27, 2003) (on file with author). As of this writing, no federal criminal charges have been brought against Ebbers or WorldCom.

http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

p357 Brickey book pages.doc10/24/03 12:46 PM 2003] FROM ENRON TO WORLDCOM AND BEYOND 375

assistance of insiders to help connect the dots, the middle managers may end up as scapegoats while the higher-ups remain unscathed.

D. Sarbanes-Oxley

An offer of leniency can provide a strong incentive to become a cooperating witness. In exchange for a witness’s cooperation in the investigation, the prosecutor may agree not to prosecute the witness or another party,80 to reduce pending charges or charge fewer crimes,81 to

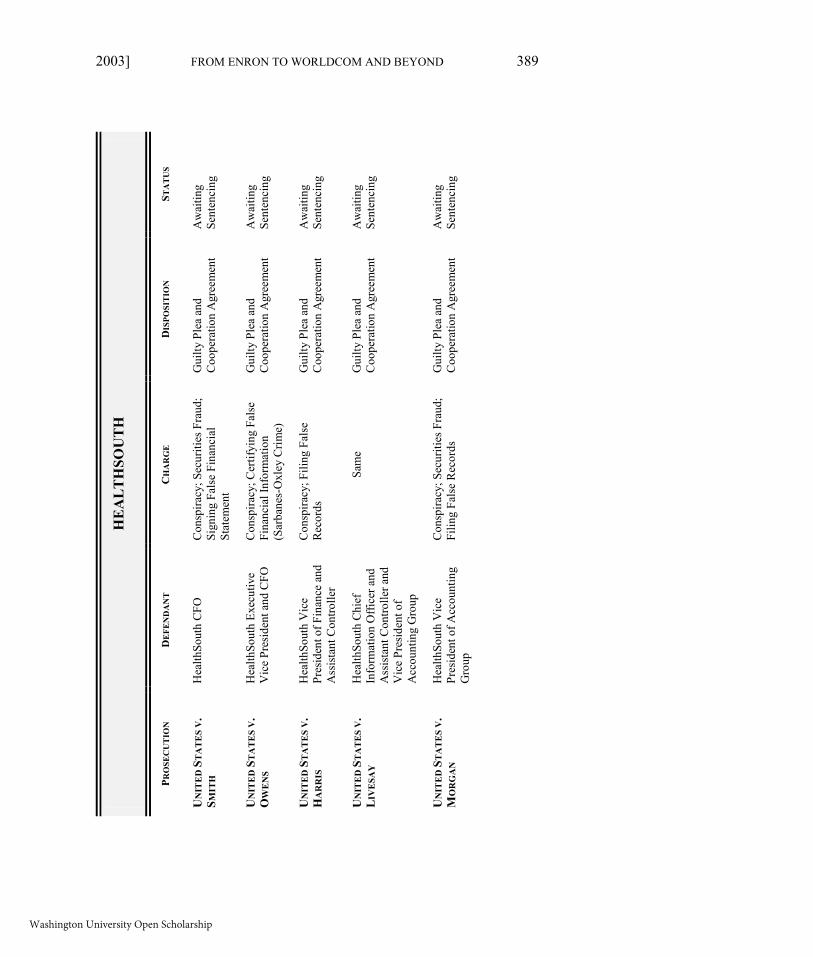

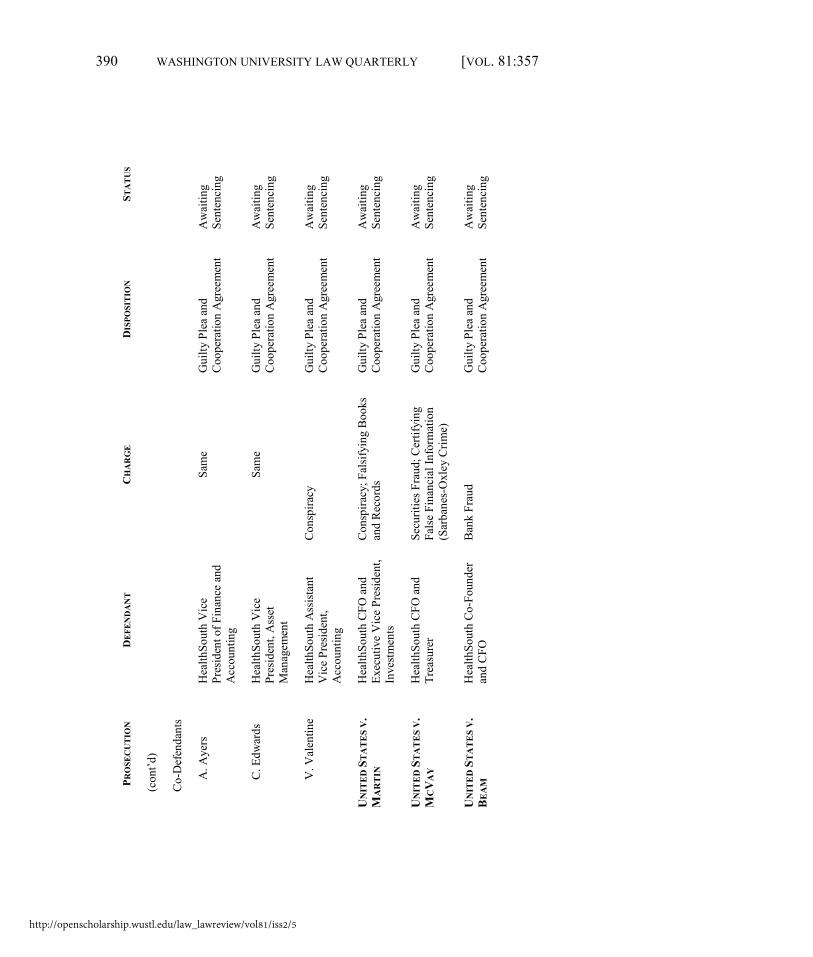

80. According to conventional wisdom, in his plea negotiations ImClone CEO Sam Waksal sought in vain to obtain the prosecutor’s agreement not to prosecute his father and daughter, or alternatively, not to seek prison sentences if they were criminally charged. They were implicated in the indictment as having conspired with Waksal and having lied under oath to the SEC. Andrew Pollack, U.S. Adds Charges Against Ex-Chief of Drug Company, N.Y. TIMES, Aug. 8, 2002, at A1; Jerry Markon, Waksal’s Plea Talks Continue After Latest Deadline Extension, WALL ST. J., July 29, 2002, at B9. Although he eventually pled guilty to conspiracy, securities fraud, perjury, obstruction of justice and bank fraud charges, Waksal’s plea was not part of a negotiated agreement with the prosecutors, and he did not become a cooperating witness. Constance L. Hays, Ex-ImClone Chief Admits Some U.S. Charges, N.Y. TIMES, Oct. 16, 2002, at C1; Laurie P. Cohen & Jerry Markon, Waksal Plea Could Backfire, Lead to Hearing, WALL ST. J., Oct. 18, 2002, at C1. As of the date of this writing, no charges have been filed against the father or daughter. 81. For example, the prosecutor might agree to limit the number of counts charged against the defendant or to forego charging additional related crimes like filing false reports with the SEC. This may have been the case in the WorldCom prosecutions. David Myers, Betty Vinson, and James Brown were each charged in a criminal information with one count of conspiracy and one count of securities fraud, and Myers was charged with one count of false filings with the SEC. In contrast, while Scott Sullivan and Buford Yates were also charged with one count of conspiracy and one count of securities fraud, they were each charged with five counts of filing false statements with the SEC. United States v. Sullivan (indictment filed in United States District Court for the Southern District of New York) (Aug. 28, 2002) (on file with author). Yates later struck a plea agreement under which he pled guilty to reduced charges that did not include the false filing counts. See supra text accompanying notes 66-71. Prosecutors are sometimes publicly explicit about these matters. In the HealthSouth investigation, for example, the prosecutor’s pursuit of real-time prosecutions led to eleven guilty pleas by HealthSouth executives—including all five former CFO’s—in the short span of two months. Former Executive at HealthSouth Pleads Guilty, N.Y. TIMES, May 6, 2003, at C8. When the second guilty plea was announced, the prosecutor emphasized that it was important that other HealthSouth employees come forward soon. “People who do not cooperate will not see the small number of counts that are being charged against these individuals,” she said. Noting that the fraud continued for years, she cautioned that separate counts of wire fraud and false certification charges could be filed for each quarter in which false financial figures were used in SEC reports. Suspended HealthSouth Officer Pleads Guilty to Fraud, nbc13.com, Mar. 26, 2003, available at http://www.nbc13.com/ news/2065461/detail.html (on file with author). “We’re moving as swiftly as could be expected,” she said. “There’s a hole over at HealthSouth and you can climb deeper in it or you can do what you can to pull yourself out.” Simon Romero & Riva D. Atlas, New Charges Are Expected at HealthSouth, N.Y. TIMES, Mar. 25, 2003, at C2. When the third guilty plea was announced, she again publicly encouraged other employees who were privy to the fraud to contact her office “to discuss how they can best ‘help themselves’” and noted that the investigation was expanding beyond HealthSouth’s finance department. Press Release, U.S. Attorney’s Office, Northern District Alabama, HealthSouth Officer Charged with Conspiracy to Commit Wire & Securities Fraud (Mar. 31, 2003), available at http://www.usdoj.gov/usao/aln/pages/newsreleseasesmain.html (on file with author). As of August,

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 376 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

charge crimes that carry less severe punishment,82 or to recommend leniency in sentencing.83 Moreover, once the cooperation is complete, the prosecutor may ask the court for a downward departure from the applicable sentencing guideline if the witness has provided substantial assistance in the case.84

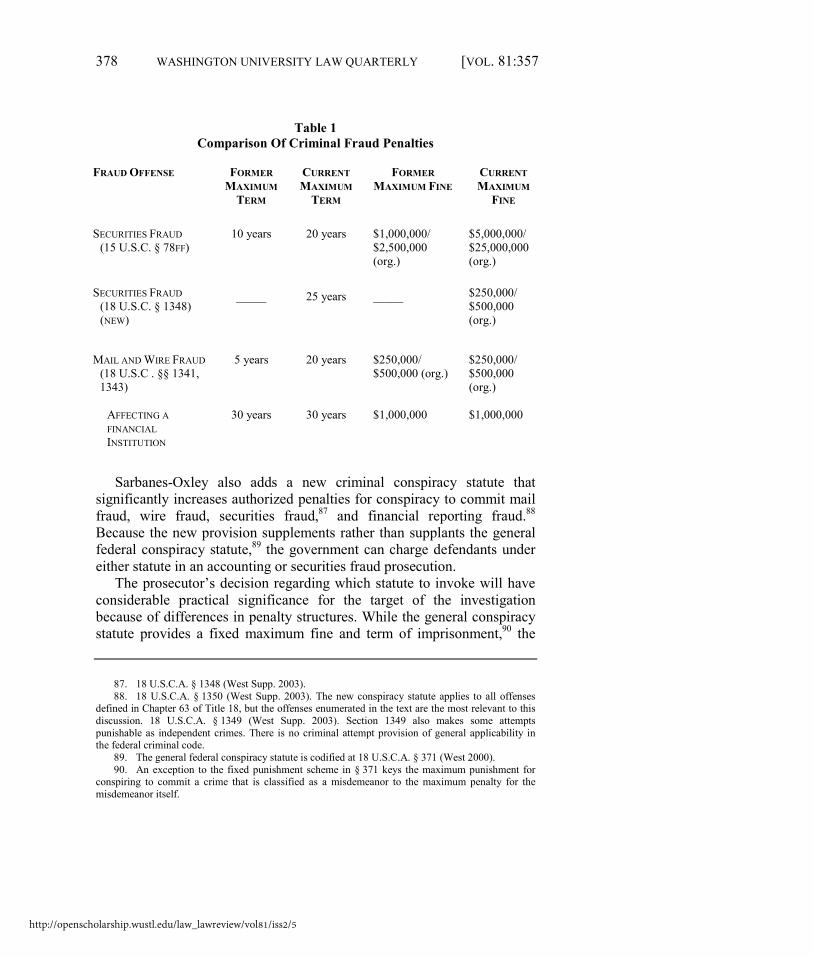

That brings us back to Sarbanes-Oxley, which enhances criminal fraud penalties and directs the United States Sentencing Commission to revise the sentencing guidelines to require longer sentences for high-end fraud.85 As shown in Table 1, Sarbanes-Oxley doubles the maximum prison term for securities fraud, quadruples the maximum term for mail and wire

2003, fourteen HealthSouth executives had pled guilty, including the Senior Vice President for Tax and the Vice President of Investments. Another Guilty Plea in HealthSouth Case, N.Y. TIMES, Aug. 29, 2003, at C2; HealthSouth Executive Admits to Falsifying Taxes, N.Y. TIMES, Aug. 28, 2003, at C7. See infra APPENDIX A, MAJOR CORPORATE FRAUD PROSECUTIONS, March 2002 - August 2003. While this Article was in press, a fifteenth executive pled guilty and became a cooperating witness. Ex-Health South Official Agrees to Plea Deal in Massive Fraud, WALL ST. J. ONLINE, Sept. 26, 2003 (on file with author). 82. In the ImClone case, for example, an assistant to a financial advisor at Merrill Lynch allegedly passed inside information relating to sales of ImClone stock to the financial advisor’s client. The client then sold nearly 4,000 shares of ImClone stock on the basis of the information. The assistant also lied to the SEC about whether he knew the reasons for the client’s sales. These facts, which are alleged in a one-count information charging the assistant, could have resulted in felony charges for insider trading and violating the false statements statute. As a cooperating witness, however, he was charged with and pled guilty to a misdemeanor for accepting money in consideration for withholding the truth from the SEC, in violation of 18 U.S.C.A. § 873. United States v. Faneuil, 02-CR-1287 (S.D.N.Y. Oct. 2, 2002) (Misdemeanor Information) (on file with author). 83. See generally U.S. ATTORNEY’S MANUAL § 9-27.400 (2002). 84. U.S. SENTENCING GUIDELINES MANUAL § 5K1.1 (2002). The court considers a downward departure for providing substantial assistance independently of other mitigating factors such as acceptance of responsibility. Id. at Application Note 2. Providing substantial assistance to authorities is one of a very limited number of grounds on which the sentencing judge may reduce the sentence below the statutorily prescribed minimum and can only be considered upon the government’s motion. 85. Sarbanes-Oxley gave the Commission authority to exercise its emergency powers to adopt temporary amendments and imposed a six-month deadline for the Commission to act. The Commission adopted temporary amendments that became effective January 25, 2003 and will expire November 1, 2003, when permanent amendments come into place. The Commission submitted the permanent amendments for congressional review on May 1, 2003. U.S. Sentencing Commission, Amendments to the Sentencing Guidelines, Part B: Submitted to Congress May 1, 2003.

http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

p357 Brickey book pages.doc10/24/03 12:46 PM 2003] FROM ENRON TO WORLDCOM AND BEYOND 377

fraud, and creates a new securities fraud offense authorizing an even longer maximum term.86

86. 18 U.S.C.A. § 1348 (West Supp. 2003). Section 1348, which is modeled on the mail fraud statute, is “more general and less technical” than the anti-fraud provisions in the securities laws and “should not be read to require proof of technical elements from the securities laws.” 148 CONG. REC. S7421 (daily ed. July 26, 2002). Critics of Sarbanes-Oxley see its reliance on increased penalties as perhaps the weakest link in the chain. They reason that if corporate executives are not deterred by the prospect of five or ten years in prison, the threat of imprisonment will have little or no practical effect no matter what the maximum is. See, e.g., Perino, supra note 6, at 685, 687 (stating that economic analysis of crime and punishment suggests that Sarbanes-Oxley’s enhanced penalties are unlikely to deter corporate crime). Putting aside the question whether it is possible to deter greed, the ill-founded assumption is that Sarbanes-Oxlely’s higher penalties are only about deterrence. But that is surely not the case. Enron and WorldCom involve egregious frauds that are literally off the charts. The fraud in these two cases alone caused billions of dollars in shareholder losses, including employee pensions funded with now-worthless stock. The fraud precipitated the two largest corporate bankruptcies in our nation’s history, caused the loss of tens of thousands of jobs, harmed the economy, and destroyed investor confidence. In view of the magnitude of the harm and the lack of justification for bringing it about, the architects of Sarbanes-Oxley might reasonably have concluded that higher authorized penalties are needed to reflect the gravity of egregious high-end fraud. Fraud on this scale provokes moral outrage that is often expressed by the enactment of new laws that condemn it. In response to the Savings and Loan scandals of the 1990’s, for example, Congress increased the maximum penalty for mail and wire fraud to thirty years in prison and a $1 million fine if the fraud affected a financial institution, 18 U.S.C.A. §§ 1341, 1343 (West Supp. 2003), and enacted a bank fraud statute authorizing the same severe punishment. 18 U.S.C.A. § 1344 (West 2000). Section 1344 is modeled on the mail fraud statute. Congress also enacted special statutes that: (1) punish obstructing the examination or investigation of a financial institution, 18 U.S.C.A. § 1510(b)(1) (West 2000) and 18 U.S.C.A. § 1517 (West 2000); (2) made financial institution fraud a RICO predicate crime, 18 U.S.C.A. § 1961 (West 2000 & Supp. 2003); (3) enacted a continuing financial crimes enterprise statute based on the drug kingpin law, compare 18 U.S.C.A. § 225 (West 2000) (continuing financial crimes enterprise statute) with 21 U.S.C.A. § 848(c) (West 1999) (continuing criminal enterprise statute); and (4) authorized civil and criminal forfeitures for some financial institution crimes. See 18 U.S.C.A. § 981(a)(1)(C)-(E) (West Supp. 2003); 18 U.S.C.A. § 982(a)(2)-(4) (West 2000). See generally 2 KATHLEEN F. BRICKEY, CORPORATE CRIMINAL LIABILITY Chapter 8A (2d ed. 1992). As is true of Sarbanes-Oxley’s criminal provisions, the financial institution crimes enacted in the wake of the Savings and Loan scandals ensure the availability of meaningful criminal penalties for the truly egregious case and, as a practical matter, can significantly influence pre-indictment strategies adopted by those who may become targets of a criminal investigation.

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 378 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

Table 1 Comparison Of Criminal Fraud Penalties

FRAUD OFFENSE FORMER MAXIMUM

TERM

CURRENT MAXIMUM

TERM

FORMER MAXIMUM FINE

CURRENT MAXIMUM

FINE

SECURITIES FRAUD (15 U.S.C. § 78FF)

10 years

20 years

$1,000,000/ $2,500,000 (org.)

$5,000,000/ $25,000,000 (org.)

SECURITIES FRAUD (18 U.S.C. § 1348) (NEW)

_____

25 years

_____

$250,000/ $500,000 (org.)

MAIL AND WIRE FRAUD (18 U.S.C . §§ 1341, 1343) AFFECTING A FINANCIAL INSTITUTION

5 years

30 years

20 years

30 years

$250,000/ $500,000 (org.) $1,000,000

$250,000/ $500,000 (org.) $1,000,000

Sarbanes-Oxley also adds a new criminal conspiracy statute that

significantly increases authorized penalties for conspiracy to commit mail fraud, wire fraud, securities fraud,87 and financial reporting fraud.88 Because the new provision supplements rather than supplants the general federal conspiracy statute,89 the government can charge defendants under either statute in an accounting or securities fraud prosecution.

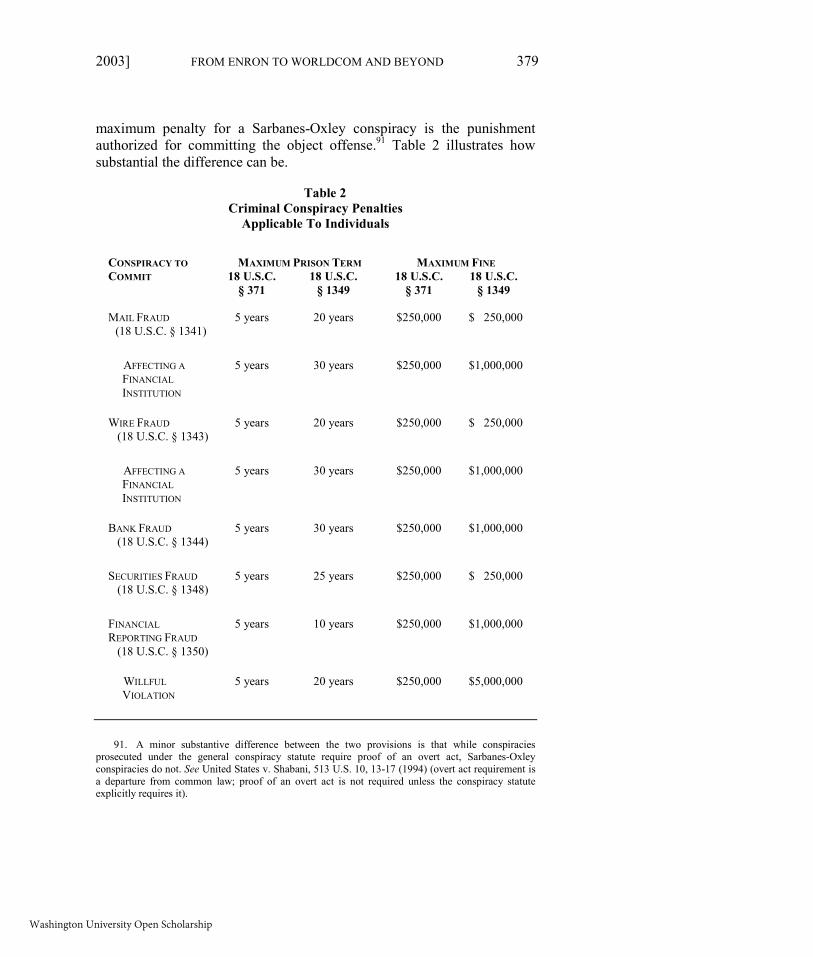

The prosecutor’s decision regarding which statute to invoke will have considerable practical significance for the target of the investigation because of differences in penalty structures. While the general conspiracy statute provides a fixed maximum fine and term of imprisonment,90 the

87. 18 U.S.C.A. § 1348 (West Supp. 2003). 88. 18 U.S.C.A. § 1350 (West Supp. 2003). The new conspiracy statute applies to all offenses defined in Chapter 63 of Title 18, but the offenses enumerated in the text are the most relevant to this discussion. 18 U.S.C.A. § 1349 (West Supp. 2003). Section 1349 also makes some attempts punishable as independent crimes. There is no criminal attempt provision of general applicability in the federal criminal code. 89. The general federal conspiracy statute is codified at 18 U.S.C.A. § 371 (West 2000). 90. An exception to the fixed punishment scheme in § 371 keys the maximum punishment for conspiring to commit a crime that is classified as a misdemeanor to the maximum penalty for the misdemeanor itself.

http://openscholarship.wustl.edu/law_lawreview/vol81/iss2/5

p357 Brickey book pages.doc10/24/03 12:46 PM 2003] FROM ENRON TO WORLDCOM AND BEYOND 379

maximum penalty for a Sarbanes-Oxley conspiracy is the punishment authorized for committing the object offense.91 Table 2 illustrates how substantial the difference can be.

Table 2 Criminal Conspiracy Penalties

Applicable To Individuals

CONSPIRACY TO MAXIMUM PRISON TERM MAXIMUM FINE COMMIT 18 U.S.C.

§ 371 18 U.S.C.

§ 1349 18 U.S.C.

§ 371 18 U.S.C.

§ 1349

MAIL FRAUD (18 U.S.C. § 1341)

5 years 20 years $250,000 $ 250,000

AFFECTING A FINANCIAL INSTITUTION

5 years 30 years $250,000 $1,000,000

WIRE FRAUD (18 U.S.C. § 1343)

5 years 20 years $250,000 $ 250,000

AFFECTING A FINANCIAL INSTITUTION

5 years 30 years $250,000 $1,000,000

BANK FRAUD (18 U.S.C. § 1344)

5 years 30 years $250,000 $1,000,000

SECURITIES FRAUD (18 U.S.C. § 1348)

5 years 25 years $250,000 $ 250,000

FINANCIAL REPORTING FRAUD (18 U.S.C. § 1350)

5 years 10 years $250,000 $1,000,000

WILLFUL VIOLATION

5 years 20 years $250,000 $5,000,000

91. A minor substantive difference between the two provisions is that while conspiracies prosecuted under the general conspiracy statute require proof of an overt act, Sarbanes-Oxley conspiracies do not. See United States v. Shabani, 513 U.S. 10, 13-17 (1994) (overt act requirement is a departure from common law; proof of an overt act is not required unless the conspiracy statute explicitly requires it).

Washington University Open Scholarship

p357 Brickey book pages.doc10/24/03 12:46 PM 380 WASHINGTON UNIVERSITY LAW QUARTERLY [VOL. 81:357

Contrary to popular lore,92 Sarbanes-Oxley’s increased penalties will result in the imposition of substantially longer prison terms because of corresponding changes in the federal sentencing guidelines:93

�� A mandatory six level enhancement for any fraud offense that affects 250 or more victims will increase the minimum sentence for major fraud by about 25%.94

�� Substantial enhancements in the sentence imposed for fraud offenses that endanger the solvency or financial security of a substantial number of victims or a publicly traded company can as much as triple the guideline sentence.95

�� The sentence for officers or directors of publicly traded companies who are convicted of securities violations will increase by about 50% based solely on their status as fiduciaries.96 If the offense also endangers the financial security of the company or economically harms a substantial number of victims, an additional increase in the guideline sentence will be imposed.