frost & sullivan global mobile vpn products market

Post on 17-Oct-2014

3.473 views

DESCRIPTION

Frost & Sullivan Global Mobile VPN Products Market: Meeting the Wireless Security Challenge with an Emerging VPN for the Remote WorkerTRANSCRIPT

Global Mobile VPN Products Market:Meeting the Wireless Security Challenge with an Emerging VPN

for the Remote Worker

Global

N9B3-74September 2011

2<N9B3-74>

Research Team

Martha VazquezIndustry Analyst, Network Security

(001) 210-247-3864

Jennifer BatesDirector of Consulting & Network Security

(001) 940-455-7475

Alpa ShahVice President of Research, ICT

(001) 650-475-4556

3<N9B3-74>

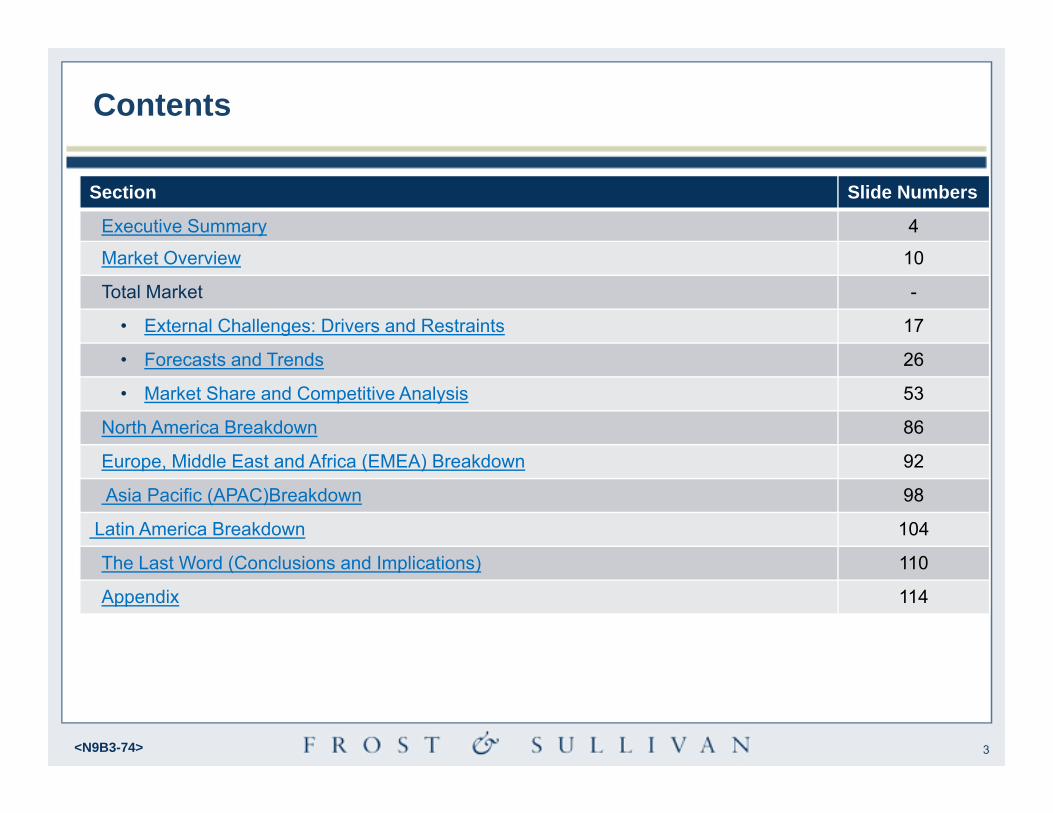

Contents

Section Slide Numbers

Executive Summary 4

Market Overview 10

Total Market -

• External Challenges: Drivers and Restraints 17

• Forecasts and Trends 26

• Market Share and Competitive Analysis 53

North America Breakdown 86

Europe, Middle East and Africa (EMEA) Breakdown 92

Asia Pacific (APAC)Breakdown 98

Latin America Breakdown 104

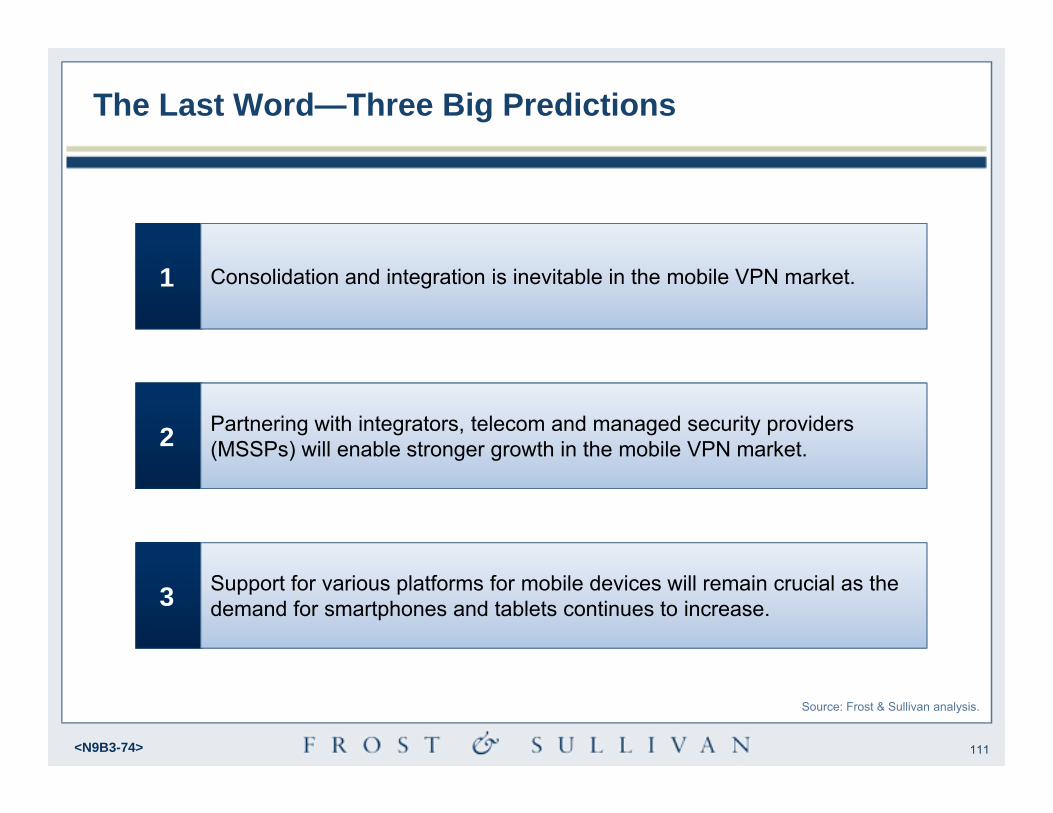

The Last Word (Conclusions and Implications) 110

Appendix 114

4<N9B3-74>

Executive Summary

5<N9B3-74>

Executive Summary

• Wireless Internet connectivity has become ubiquitous during the last five years. Driven primarily by lower cost access and integrated connectivity in devices, such as laptops, tablets, and smartphones, wireless Internet has become a viable option for remote employees.

• As a result, many businesses and government entities have built remote Internet capabilities into their operating fabrics.

• Employees are utilizing mobile devices to perform transactions directly at customer worksites. Protecting these transactions and providing secure connectivity back to the central office is a critical concern.

• While many mobile security technologies exist, mobile virtual private network (VPN) technology allows organizations to enhance productivity and operate more effectively and efficiently by providing secure and persistent connections for remote workers.

• The mobile VPN products market is an emerging market. The Mobile VPN market is gaining traction because of the explosive growth of mobile devices and the increasingly stringent regulatory requirements facing organizations.

Source: Frost & Sullivan analysis.

6<N9B3-74>

Executive Summary (continued)

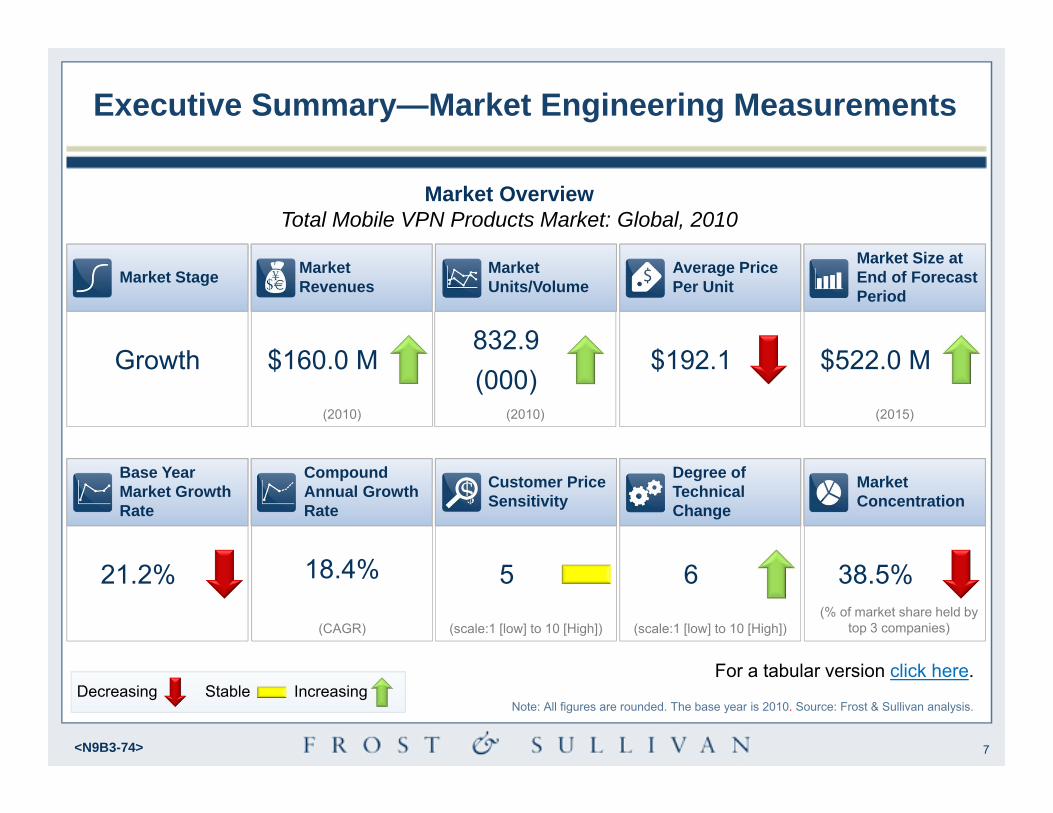

• In 2010, the global mobile VPN products market was valued at $160 million in revenue, with a compound annual growth rate (CAGR) of 18.4 percent. The North American region represents the highest percentage of the global market, at 79 percent and $126.9 million in total revenue.

• In 2010, the top two vertical markets for mobile VPN products were the telecommunications segment and the government segment. Both of these verticals have a large number of remote employees with access to sensitive information and large field service teams.

• The mobile VPN market is forecasted to show solid growth throughout the forecast period. The market consists of a wide variety of vendors ranging from dedicated software vendors, such as NetMotion Wireless and Columbitech, to large vendors that offer a breadth of networking products, such as Cisco and Juniper.

\Source: Frost & Sullivan analysis.

7<N9B3-74>

Executive Summary—Market Engineering Measurements

Market Stage

Growth

Market Revenues

$160.0 M

(2010)

Market Units/Volume

832.9 (000)

(2010)

Average Price Per Unit

$192.1

Market Size at End of Forecast Period

$522.0 M

(2015)

Base Year Market Growth Rate

21.2%

Compound Annual Growth Rate

18.4%

(CAGR)

Customer Price Sensitivity

5

(scale:1 [low] to 10 [High])

Market Concentration

38.5%

Degree of Technical Change

6

(scale:1 [low] to 10 [High])

Market OverviewTotal Mobile VPN Products Market: Global, 2010

For a tabular version click here.Stable IncreasingDecreasing

(% of market share held by top 3 companies)

Note: All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis.

8<N9B3-74>

Number of Companies that Exited*

0

(2010)

Number of Companies that Entered*

0

(2010)

Number of Competitors

19(active market competitors in

base year)

Attachment Rate

1(current number of units per

user - Base Year)

Executive Summary—Market Engineering Measurements (continued)

Competitor Overview

Stable IncreasingDecreasing

Total Addressable Market

Replacement Rate

18 Months(average period of unit

replacement)

Current Potential Users

3.1 M(Revenue/ Average Sales

Price)

Total Addressable Market

Industry AdvancementMarketing Spend as a Percent of Market Revenue

5.5%

Average R&D Spend by Product

$5.5M

Maximum Attachment Rate

2(maximum potential number

of units per user)

•Companies with revenue > $1M revenue. Note: All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis.

Average Product Development Time

15 Months

9<N9B3-74>

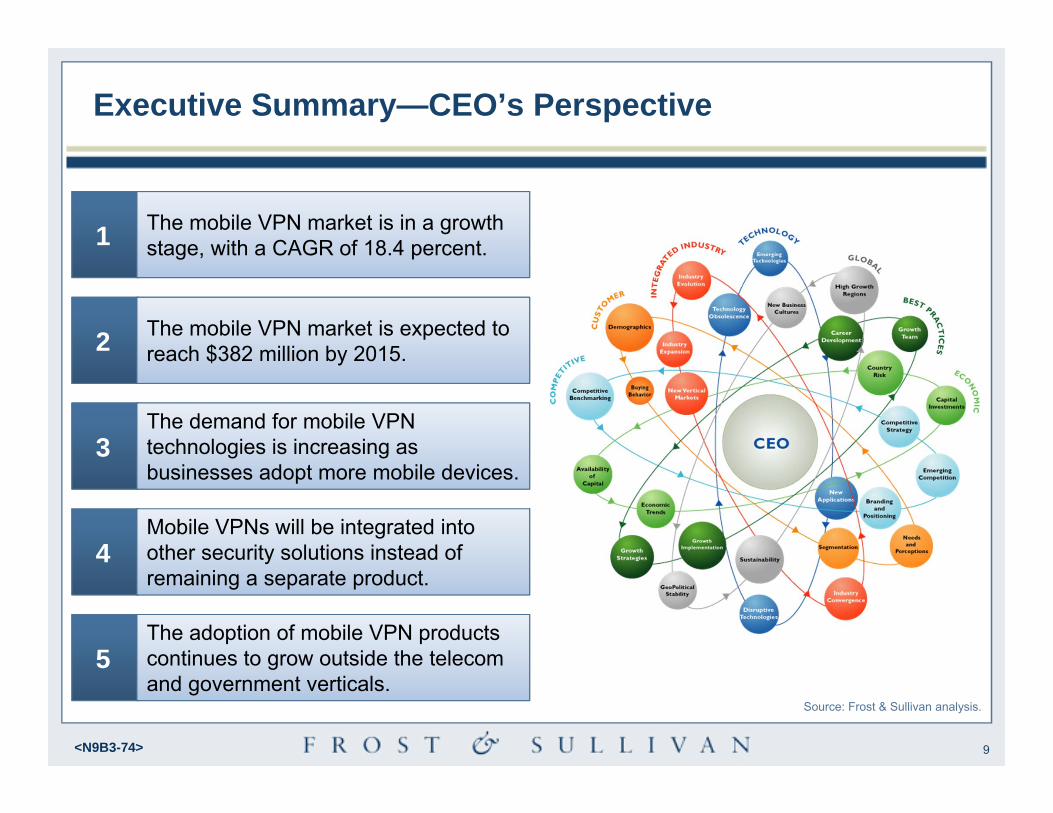

Executive Summary—CEO’s Perspective

2 The mobile VPN market is expected to reach $382 million by 2015.

3The demand for mobile VPN technologies is increasing as businesses adopt more mobile devices.

4Mobile VPNs will be integrated into other security solutions instead of remaining a separate product.

5The adoption of mobile VPN products continues to grow outside the telecom and government verticals.

1 The mobile VPN market is in a growth stage, with a CAGR of 18.4 percent.

Source: Frost & Sullivan analysis.

10<N9B3-74>

Market Overview

11<N9B3-74>

Market Overview—Definitions

• A mobile VPN is a VPN with specific features designed to provide secure connectivity and persistence over wireless networks. While other technologies, such as mobile Internet protocol (IP), IPSec, or Secure Sockets Layer (SSL) VPNs, provide similar functionality, mobile VPNs unify persistence and security features into a single product built for wireless coverage.

• A mobile VPN allows devices to work across a variety of public or private networks, wired or wireless. These networks include wired local area networks (LAN), Wi-Fi networks, hotspots, and many varieties of wireless wide area networks (WANs) provided by different wireless carriers and satellite networks.

• A mobile VPN solution may also include additional reporting, management, and control features. Frost & Sullivan also sees many traditional network access control (NAC) vendors partnering with vendors in this space, and some mobile VPN vendors have developed their own NAC solutions.

• Frost & Sullivan requires the following features to be present in a mobile VPN solution for inclusion in this study:

o Session Persistence - Traditional VPN users lose connectivity once they roam into different wireless networks, whereas mobile VPN users do not. The virtual IP address for each mobile VPN client remains the same, even when the IP address changes. The network connection is always on through a persistent IP address.

Source: Frost & Sullivan analysis.

12<N9B3-74>

Market Overview –Definitions (continued)

• Application persistence - As mobile VPNs pass through different networks, the application sessions are sustained, even when connectivity is lost.

• Traditional VPNs lose application sessions, which causes data loss and forces users to restart applications.

• Network transparency - When switching networks, the mobile VPN is transparent to the user and does not compromise security or privacy. The application interface remains the same.

• Bandwidth optimization - Mobile VPNs use a variety of optimization features to reduce network consumption and to lower bandwidth constraints thus lowering costs for organizations.

Source: Frost & Sullivan analysis.

13<N9B3-74>

Market Overview—Definitions (continued)

• North America refers to the United States and Canada.

• Europe, the Middle East, and Africa (EMEA) includes countries in Europe, including Eastern European countries and countries in Western Asia, and countries in Africa.

• Asia-Pacific (APAC) refers to countries in East and Southeast Asia, including Japan and Australia.

• Latin America (LATAM) refers to Mexico, Central and South America.

• This research service/study defines a unit as a single license per user sold by a mobile VPN vendor to a customer either directly or indirectly through a reseller or a channel partner.

• The average unit price is calculated by dividing the total product revenue by the number of licenses sold.

• Revenue is based on original vendor product sales and does not include resale revenue or products sold by original equipment manufacturer (OEM) partners.

Source: Frost & Sullivan analysis.

14<N9B3-74>

Market Overview—Definitions (continued)

Source: Frost & Sullivan analysis.

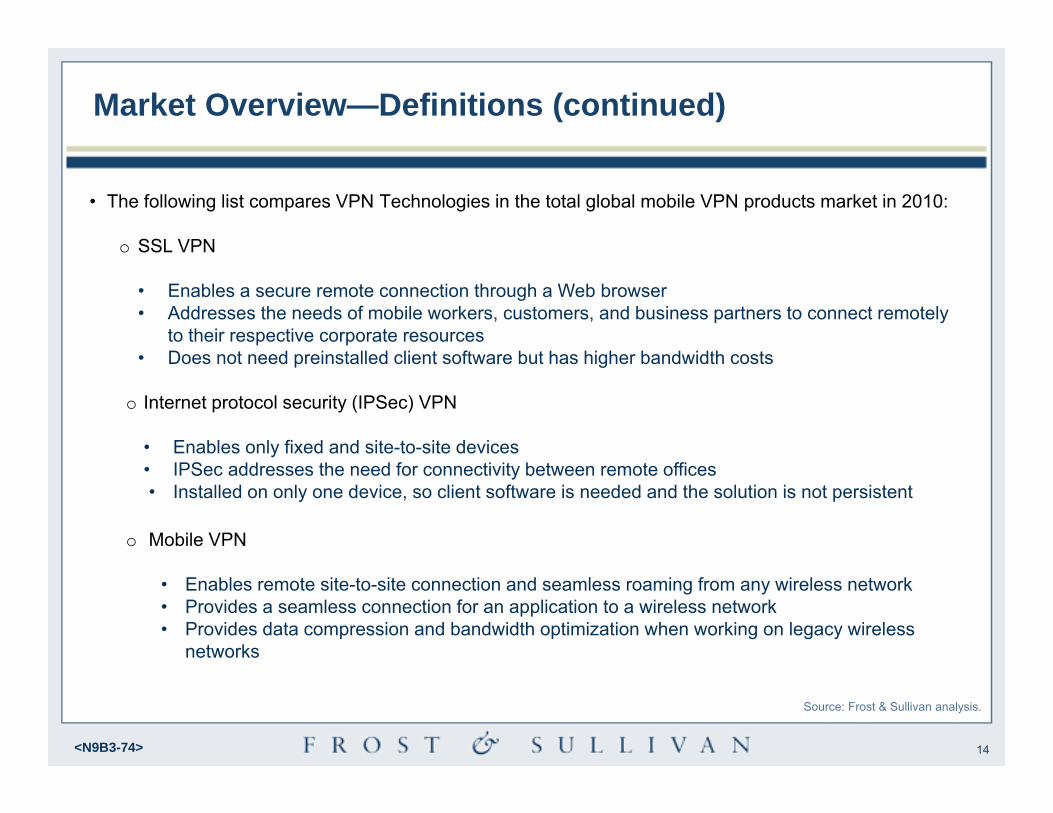

• The following list compares VPN Technologies in the total global mobile VPN products market in 2010:

o SSL VPN

• Enables a secure remote connection through a Web browser• Addresses the needs of mobile workers, customers, and business partners to connect remotely

to their respective corporate resources• Does not need preinstalled client software but has higher bandwidth costs

o Internet protocol security (IPSec) VPN

• Enables only fixed and site-to-site devices• IPSec addresses the need for connectivity between remote offices • Installed on only one device, so client software is needed and the solution is not persistent

o Mobile VPN

• Enables remote site-to-site connection and seamless roaming from any wireless network• Provides a seamless connection for an application to a wireless network• Provides data compression and bandwidth optimization when working on legacy wireless

networks

15<N9B3-74>

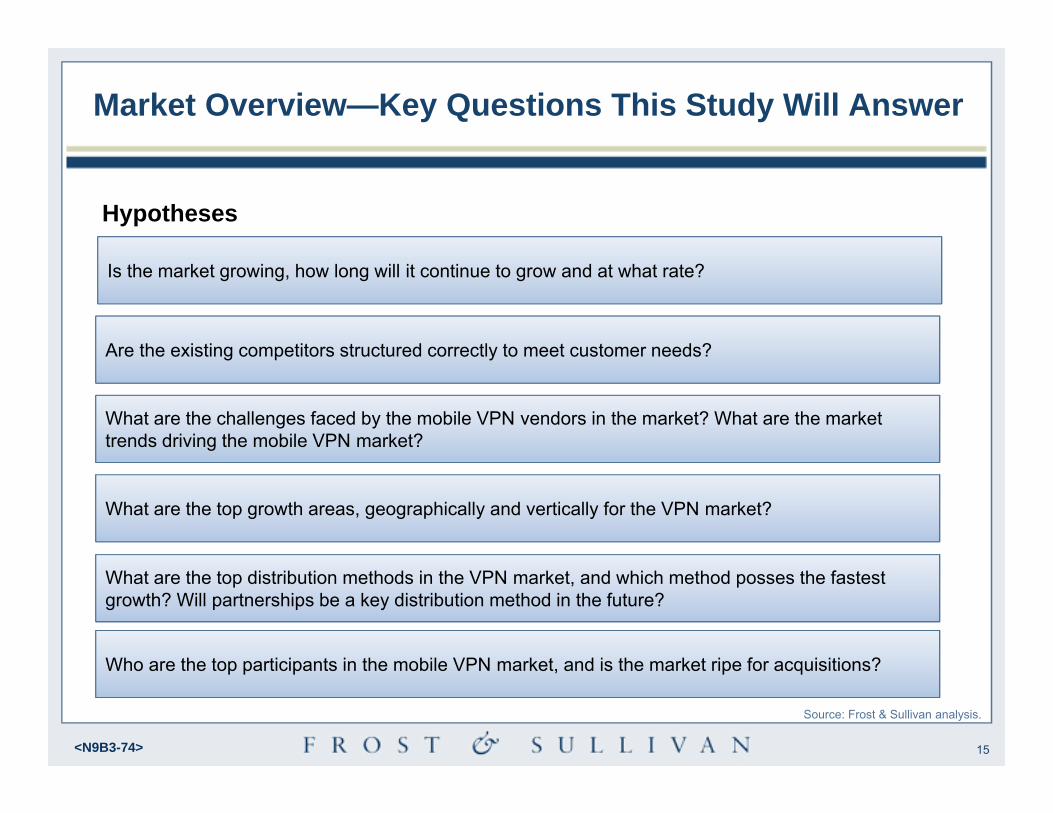

Is the market growing, how long will it continue to grow and at what rate?

Hypotheses

Market Overview—Key Questions This Study Will Answer

Are the existing competitors structured correctly to meet customer needs?

What are the challenges faced by the mobile VPN vendors in the market? What are the market trends driving the mobile VPN market?

What are the top growth areas, geographically and vertically for the VPN market?

What are the top distribution methods in the VPN market, and which method posses the fastest growth? Will partnerships be a key distribution method in the future?

Source: Frost & Sullivan analysis.

Who are the top participants in the mobile VPN market, and is the market ripe for acquisitions?

16<N9B3-74>

Market Overview—Distribution Channels

Market VPN vendors

End Customer

Partnerships

VARs

Total Mobile VPN Products Market: Distribution Channel Analysis, Global, 2010

Key: VARs: value-added resellersSource: Frost & Sullivan analysis.

Key Takeaway: Partnerships and value-added resellers (VARs) are preferred sources of market VPN products because of their ability to provide trusted technical guidance.

OnlineDirect Sales

10.0%

17<N9B3-74>

External Challenges: Drivers and Restraints—Total Mobile VPN Products Market

18<N9B3-74>

Drivers and RestraintsM

arke

t Driv

ers

Mar

ket R

estr

aint

s

1-2 years 3-5 years 6-10 yearsIncrease in advanced and complex threats drives demand for Mobile VPN solutions in order to address security on wireless devices

Compliance regulations require organizations to implement additional security

Budget Concerns because of the current economic situation slows the purchase of mobile VPN solutions

Explosion of mobile and wireless devices within organizations drives the demand for Mobile VPN solutions

Need to support multiple operating systems slows down mobile VPN development and sales

Need for remote accessibility drives the need for secure and continuous access to critical data

Costumer confusion about importance of mobile security solutions delays spending on products, such as mobile VPNs

Impact: High Medium Low

Total Mobile VPN Products Market: Key Market Drivers and Restraints: Global, 2011-2020

Source: Frost & Sullivan analysis.

19<N9B3-74>

Drivers Explained

• Increase in advanced and complex threats drives demand for Mobile VPN solutions in order to address security on wireless devices

o The Internet has become a universal platform for conducting business. As a result, attackers have zeroed in on the Internet for conducting theft and fraud. Mobile devices are not immune from this trend and both consumers and organizations are looking for products to secure transactions conducted on Internet from outside the organization.

o Even though mobility allows workers to demonstrate improved productivity, organizations have become increasingly concerned with hackers accessing corporate networks by posing as remote employees. Cybercriminals have shown they can easily take advantage of users connecting through hot spots or through unsecured connections, and organizations have little defense against these kinds of attacks.

o Hackers are constantly looking for new vulnerabilities to exploit, and enterprises need to be prepared for these zero-day attacks. Using encrypted sessions and enforcing organizational policies on the mobile endpoint will help to prevent these attacks.

Source: Frost & Sullivan analysis.

20<N9B3-74>

Drivers Explained (continued)

• Explosion of mobile and wireless devices within organizations drives the demand for mobile VPN solutions

o Lowered prices and higher speeds for mobile Internet drive mobile devices into the hands of businesses and consumers.

o Organizations are leveraging the use of personal mobile devices in the workplace. Today, most employees can access any business application and can connect to their corporate networks from anywhere through mobile applications, such as smartphones, laptops, tablets, and netbooks.

o Because more and more work transactions are processed through mobile devices, security is a heighted concern. Mobile VPN technology and other mobile security products will be a crucial component as more mobile devices enter the workplace.

Source: Frost & Sullivan analysis.

21<N9B3-74>

Drivers Explained (continued)

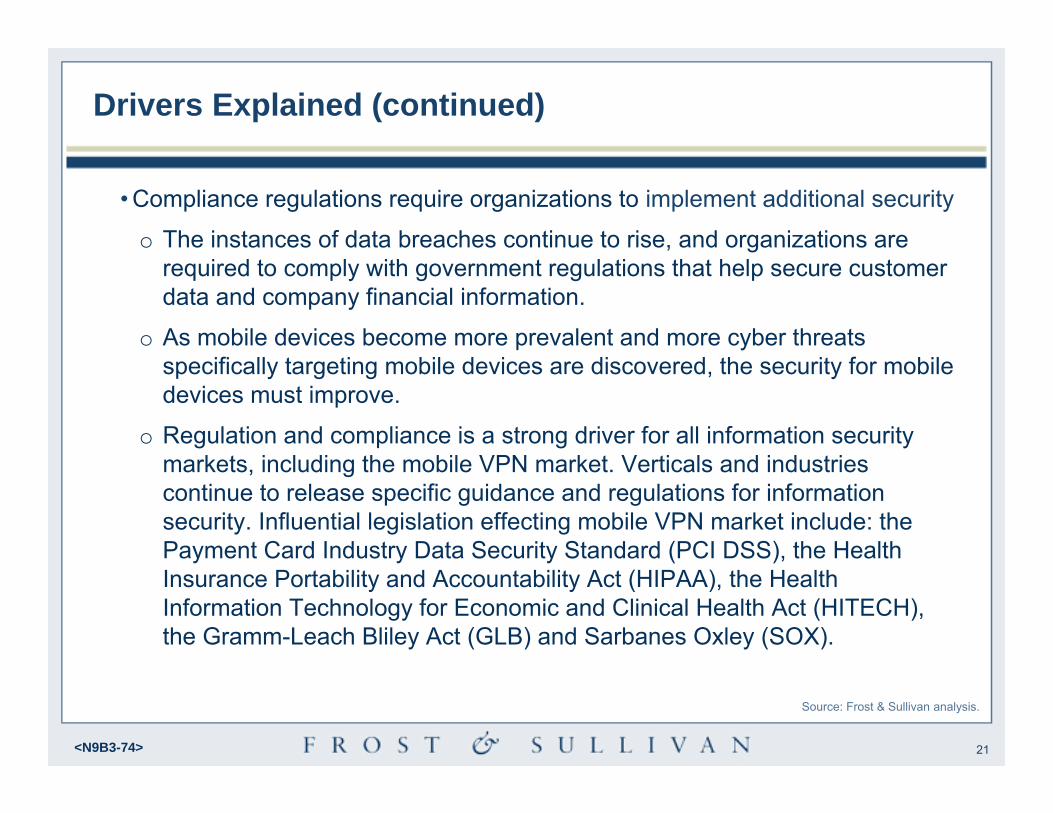

• Compliance regulations require organizations to implement additional security

o The instances of data breaches continue to rise, and organizations are required to comply with government regulations that help secure customer data and company financial information.

o As mobile devices become more prevalent and more cyber threats specifically targeting mobile devices are discovered, the security for mobile devices must improve.

o Regulation and compliance is a strong driver for all information security markets, including the mobile VPN market. Verticals and industries continue to release specific guidance and regulations for information security. Influential legislation effecting mobile VPN market include: the Payment Card Industry Data Security Standard (PCI DSS), the Health Insurance Portability and Accountability Act (HIPAA), the Health Information Technology for Economic and Clinical Health Act (HITECH), the Gramm-Leach Bliley Act (GLB) and Sarbanes Oxley (SOX).

Source: Frost & Sullivan analysis.

22<N9B3-74>

Drivers Explained (continued)

• Need for remote accessibility drives the need for secure and continuous access to critical data

o For remote employees, the ability to access data at all times is critical. Businesses now expect their employees to be able to log on from any location. The ability to access the Internet through enhanced wireless technologies has allowed for applications to be downloaded onto mobile devices. Employees are using more applications than originally intended. As more applications are available for mobile or wireless devices, enterprises are utilizing these applications to increase efficiency and to enhance productivity.

o Furthermore, falling prices for consumer devices and data plans have driven organizations to adopt more mobile devices into the workplace. Because businesses financially benefit from constant employee mobility, keeping connections secure and persistent is a necessity.

Source: Frost & Sullivan analysis.

23<N9B3-74>

Restraints Explained (continued)

• Budget concerns because of the current economic situation slows the purchase of mobile VPN solutions

o Since 2008, the global economy has experienced slow growth, causing many businesses to cut spending. In a majority of organizations, IT has bee hit hard by spending cuts. As a result, sales cycles have slowed, which has slowed growth in the overall information security market and for new security products, specifically.

o Starting in 2010, the economy started to recover, but IT administrators remain cautious about spending on new security technologies. Frost & Sullivan believes that the need for mobile device security will outpace the current hesitation and this market will show steady growth through the forecast period.

Source: Frost & Sullivan analysis.

24<N9B3-74>

Restraints Explained (continued)

• Need to support multiple operating systems slows down mobile VPN development and sales

o Mobile devices of the past were Windows laptops and personal digital assistants (PDAs), but the recent mobile-device market explosion has resulted in an array of mobile devices. Employees are no longer limited to Windows devices, but are using Macs, iPhones, Androids, Blackberries, and Symbian devices to connect to corporate networks.

o Mobile VPN vendors are now scurrying to offer solutions for these broad-based platforms. This restraint will decrease as mobile VPN vendors offer a larger portfolio for these diverse operating systems. Many mobile VPN vendors have support on the roadmap or in development for these platforms, and this restraint will lessen over the next 18 months as development and product releases catch up with demand.

Source: Frost & Sullivan analysis.

25<N9B3-74>

Restraints Explained

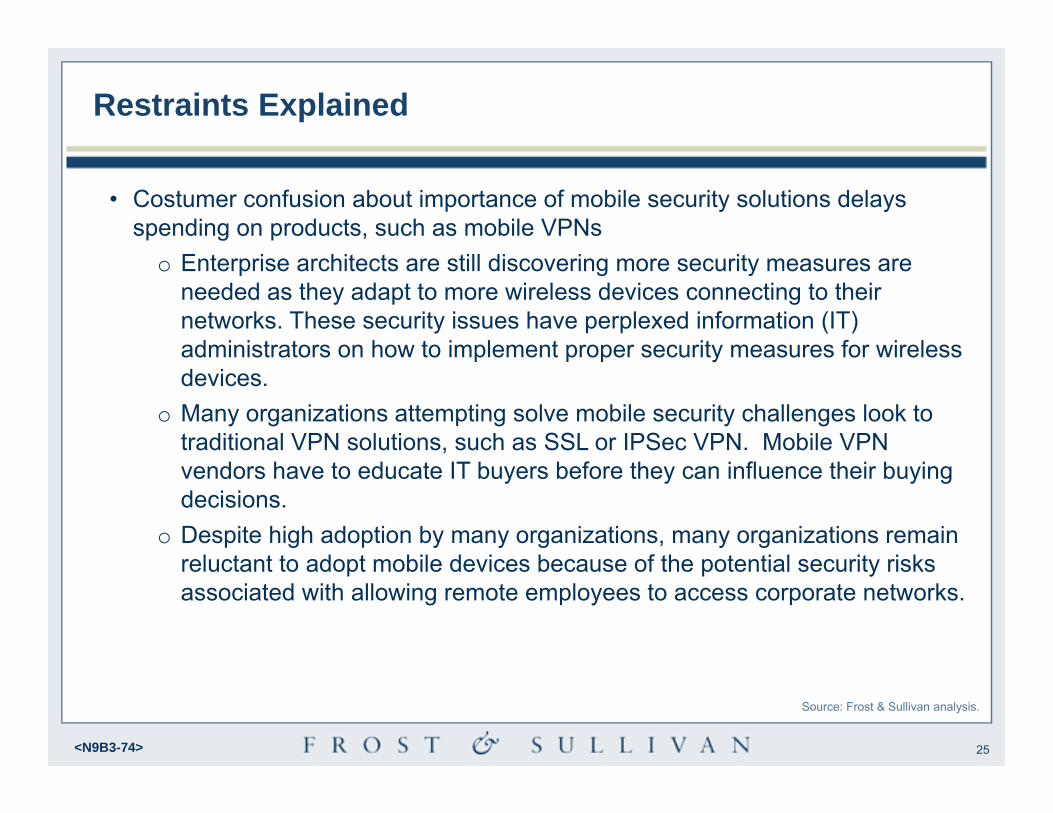

• Costumer confusion about importance of mobile security solutions delays spending on products, such as mobile VPNs

o Enterprise architects are still discovering more security measures are needed as they adapt to more wireless devices connecting to their networks. These security issues have perplexed information (IT) administrators on how to implement proper security measures for wireless devices.

o Many organizations attempting solve mobile security challenges look to traditional VPN solutions, such as SSL or IPSec VPN. Mobile VPN vendors have to educate IT buyers before they can influence their buying decisions.

o Despite high adoption by many organizations, many organizations remain reluctant to adopt mobile devices because of the potential security risks associated with allowing remote employees to access corporate networks.

Source: Frost & Sullivan analysis.

26<N9B3-74>

Forecasts and Trends—Total Mobile VPN Products Market

27<N9B3-74>

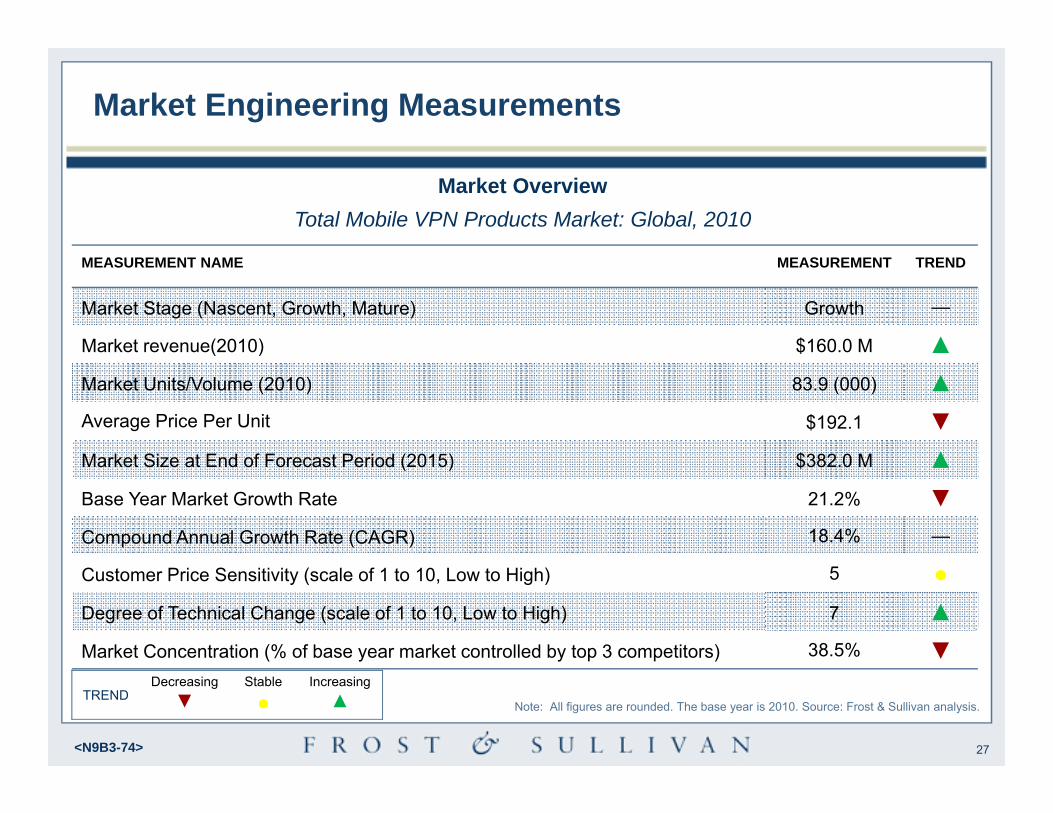

MEASUREMENT NAME MEASUREMENT TREND

Market Stage (Nascent, Growth, Mature) Growth —

Market revenue(2010) $160.0 M ▲Market Units/Volume (2010) 83.9 (000) ▲Average Price Per Unit $192.1 ▼Market Size at End of Forecast Period (2015) $382.0 M ▲Base Year Market Growth Rate 21.2% ▼Compound Annual Growth Rate (CAGR) 18.4% —

Customer Price Sensitivity (scale of 1 to 10, Low to High) 5 ●Degree of Technical Change (scale of 1 to 10, Low to High) 7 ▲Market Concentration (% of base year market controlled by top 3 competitors) 38.5% ▼

Market Engineering Measurements

Note: All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis.TREND

Decreasing Stable Increasing▼ ● ▲

Market OverviewTotal Mobile VPN Products Market: Global, 2010

28<N9B3-74>

Replacement Rate (average period of unit replacement) 18 Months ●

Attachment Rate (current number of units per user - 2010) 1 ●Maximum Attachment Rate (maximum potential number of units per user - 2010) 2 ●

Base Year 2010 (Potential Users or Addressable Market) 3.1 M ●

MEASUREMENT NAME MEASUREMENT TREND

Number of Competitors (active market competitors in base year) 19 ●

Number of Companies that Exited in Base Year* 0 ●Number of Companies that Entered in Base Year* 0 ●

Market Engineering Measurements (continued)

Competitor Overview

Total Addressable Market

Note: All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis.* Companies with >$1M revenue.

TRENDDecreasing Stable Increasing

▼ ● ▲

29<N9B3-74>

MEASUREMENT NAME MEASUREMENT TREND

Average Product Development Time 15 Months ●

Average R&D Spend by Product $5.5 M ▲Marketing Spend as a Percent of Market Revenue 5.5% ●

Market Engineering Measurements (continued)

TRENDDecreasing Stable Increasing

▼ ● ▲

Industry Advancement

Note: All figures are rounded; base year is 2010. Source: Frost & Sullivan analysis.

30<N9B3-74>

Forecast Assumptions

The forecast for mobile VPN market revenue and unit shipment prices are based on numerous assumptions, including the following factors:

• New cyber security requirements and legislation to be released in 2012 and 2013

• Continued product development and new features expected between 2010 and 2013

• Continued cyber terrorism and data-security breaches throughout the forecast period

• A significant increase in number mobile devices entering organizations through 2015

• Continued concerns around unsecure mobile devices entering enterprise space

• Increased competition from traditional VPN security solutions from 2011 to 2015

• The integration and consolidation of VPN clients onto new mobile devices

Source: Frost & Sullivan analysis.

31<N9B3-74>

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.

Total Mobile VPN Market Unit Shipment and Revenue Forecast

Key Takeaway: An increase in using wireless devices will fuel revenuegrowth through 2015.

2007 2008 2009 2010 2011 2012 2013 2014 2015Revenue 90.0 110.0 132.0 160.0 193.0 230.0 275.0 325.0 382.0Units 441.4 550.3 673.6 832.9 1025.1 1246.6 1520.9 1834.2 2199.9

0.0

500.0

1000.0

1500.0

2000.0

2500.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

Uni

ts (0

00s)

Rev

enue

($M

illio

n)

Year

Total Mobile VPN Products Market Unit Shipment and Revenue Forecast, Global, 2007-2015

CAGR = 18.4%

32<N9B3-74>

Unit Shipment and Revenue Forecast Discussion

• The global mobile VPN market was in a growth stage in 2010, with an estimated $160 million in revenue. The market is expected to grow at a CAGR of 18.4 percent throughout the forecast period. The base year growth was 21.2 percent in 2010. The market is expected to generate $382 million in revenue by 2015.

• High growth was expected for the mobile VPN market in a 2008 study; however, actual growth was slower than forecasted because of the competition increase and the popularity of a variety of operating systems in the device market. Most mobile VPN vendors have been slow in offering broader platforms and have focused on the Windows platform. As a result, growth during the forecast period is expected to be approximately 18.4 percent healthy but lower than many other security markets.

• The number of units represents the number of users purchasing mobile VPN solutions. In 2010, the number of units was estimated at 832.9 thousand and was predicted to reach 3.1 million users by 2015. The average sales price used to determine the number of units was estimated to be $192.1 per user. The price is expected to reach $173.60 per user by 2015 and is expected to decline as more competitors begin offering similar solutions and the demand increases because of the number of various endpoints entering the business market.

Source: Frost & Sullivan analysis.

33<N9B3-74>

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.

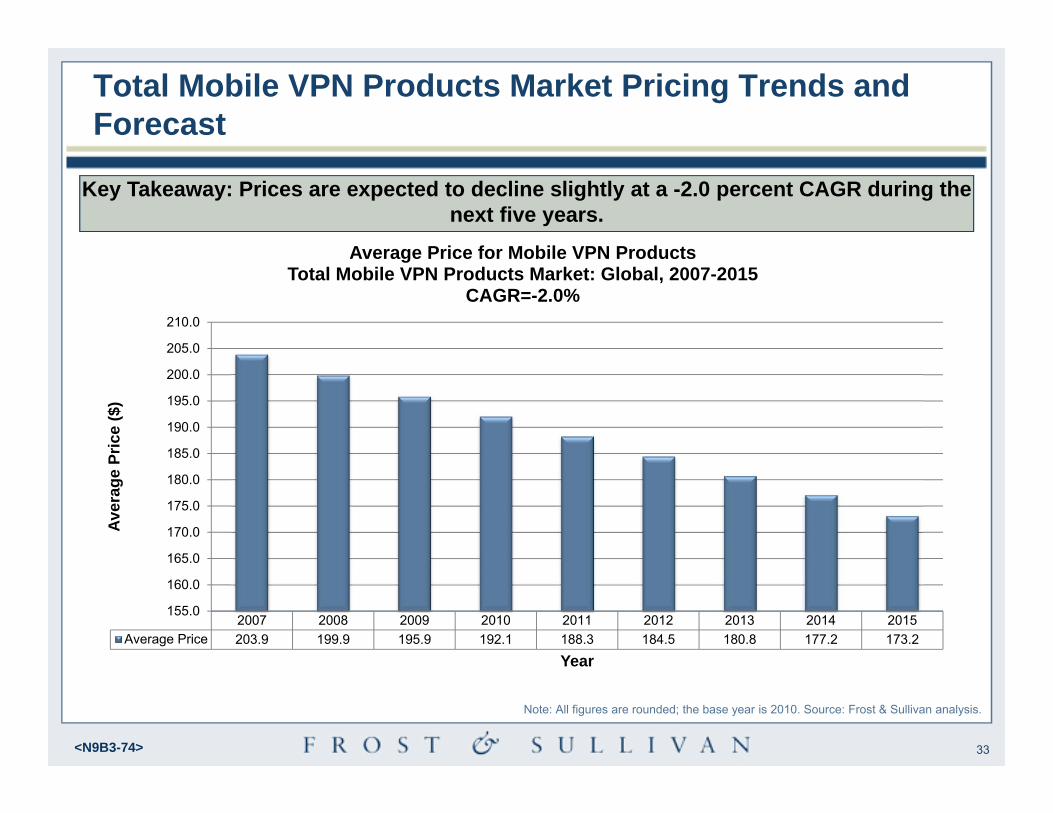

Total Mobile VPN Products Market Pricing Trends and Forecast

Key Takeaway: Prices are expected to decline slightly at a -2.0 percent CAGR during the next five years.

2007 2008 2009 2010 2011 2012 2013 2014 2015Average Price 203.9 199.9 195.9 192.1 188.3 184.5 180.8 177.2 173.2

155.0

160.0

165.0

170.0

175.0

180.0

185.0

190.0

195.0

200.0

205.0

210.0

Aver

age

Pric

e ($

)

Year

Average Price for Mobile VPN ProductsTotal Mobile VPN Products Market: Global, 2007-2015

CAGR=-2.0%

34<N9B3-74>

Pricing Trends and Forecast Discussion

• The pricing for the mobile VPN market differs somewhat from the traditional SSL or IPSec VPN vendors who charge for the number of deployed users. Mobile VPN vendors have a variety of sales models. Some vendors may sell a clients to a company and then include the server for free. Other vendors may place the client for free within the device and make up the revenue from hardware or support services.

• The average sales price in 2010 was $192.1 per user. The average sales price is expected to reach $173.2 per user by 2015. Prices are expected to decline as more competitors begin offering similar solutions increasing competition. Not included in this pricing are annual maintenance fees that range from 20 to 30 percent of the cost.

• Mobile VPN pricing can vary, depending on the featured set or solution and the contract size. The pricing can also change, depending on the service or the maintenance model the client chooses. Dedicated mobile VPN vendors are experiencing increased competition from traditional network equipment vendors, such as Juniper and Cisco. Cisco, for example, has a solution that includes many of the benefits of a mobile VPN, such as seamless roaming and application persistence. Stand-alone mobile VPN vendors continue to add separate modules into the mobile VPN solution as a means to differentiate themselves from other traditional SSL VPN vendors.

Source: Frost & Sullivan analysis.

35<N9B3-74>

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.

Total Mobile VPN Market Percent Revenue Forecast by Region

Key Takeaway: The North American market will remain the key adopter for newer technologies.

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015Latin America 5.0 4.9 5.0 5.0 5.1 5.2 5.3 5.5 5.7APAC 5.0 5.2 5.4 5.5 5.6 5.8 6.0 6.1 6.2EMEA 9.9 10.2 10.1 10.2 10.3 10.4 10.6 10.8 11.1North America 80.1 79.7 79.5 79.3 79.0 78.6 78.1 77.6 77.0

% R

even

ue

Year

Total Mobile VPN Products Market Percent Revenue Forecast by Region, 2007–2015

36<N9B3-74>

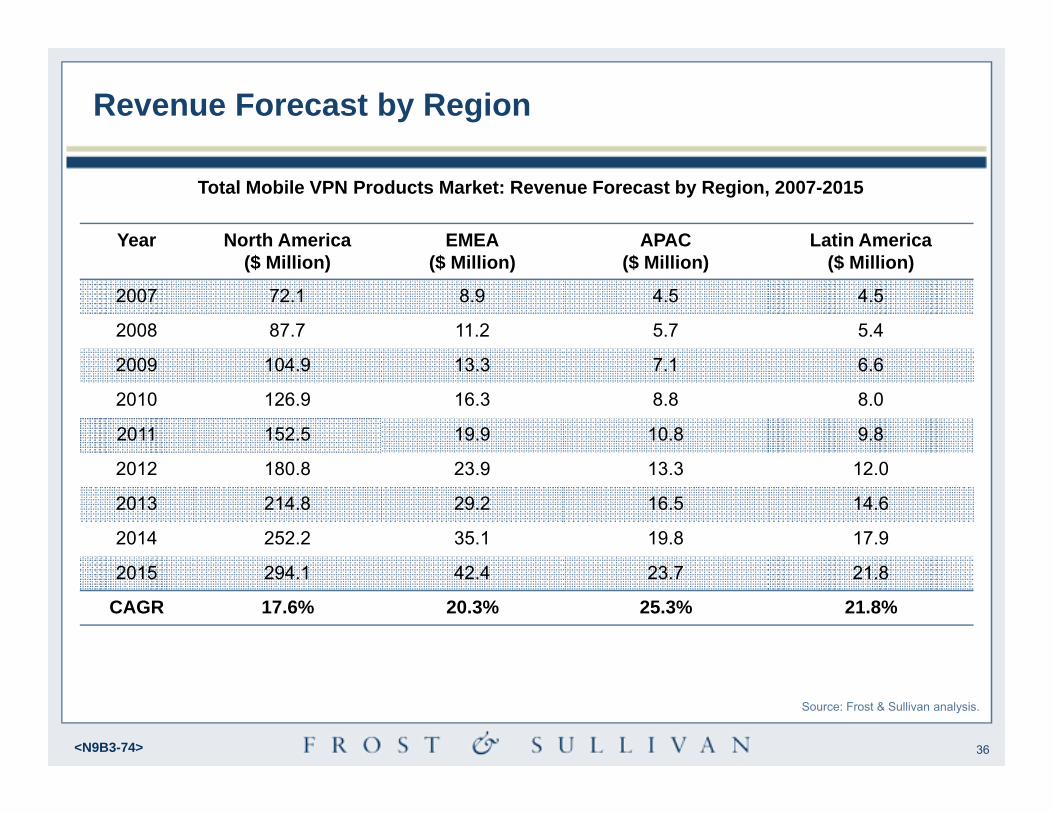

Revenue Forecast by Region

Total Mobile VPN Products Market: Revenue Forecast by Region, 2007-2015

Year North America($ Million)

EMEA($ Million)

APAC($ Million)

Latin America($ Million)

2007 72.1 8.9 4.5 4.5

2008 87.7 11.2 5.7 5.4

2009 104.9 13.3 7.1 6.6

2010 126.9 16.3 8.8 8.0

2011 152.5 19.9 10.8 9.8

2012 180.8 23.9 13.3 12.0

2013 214.8 29.2 16.5 14.6

2014 252.2 35.1 19.8 17.9

2015 294.1 42.4 23.7 21.8

CAGR 17.6% 20.3% 25.3% 21.8%

Source: Frost & Sullivan analysis.

37<N9B3-74>

Regional Revenue Forecast Discussion

• North America remained the leading geographic market for mobile VPN products, with approximately $126.9 million in revenue and 79.3 percent of the market in 2010. North America provides solid market opportunity because of its heavily regulated business environment and early adopter mentality for security solutions.

• In 2010, EMEA generated $16.3 million in revenue, representing 10.2 percent of the global mobile VPN market. Mobile VPN products are beginning to gain more traction in EMEA. The small revenue amount represents the nascent nature of this market combined with the broader acceptance of mobile technologies in EMEA lead Frost & Sullivan to believe the potential for high levels of competition in EMEA.

• In 2010, the APAC and Latin America markets combined totaled $16.8 million in revenue. For the APAC region, the market represented a CAGR of 25.3 percent and represented 5.6 percent of the Global VPN market. Latin America regions had a CAGR of 21.8 percent and represented 5.1 percent of the global mobile VPN market.

Source: Frost & Sullivan analysis.

38<N9B3-74>

Product and Technology Trends

Management tools: analytics/policy tools• Businesses today are looking for solutions that offer more than just secure tunnels—

they are also looking for better management tools. The increase in multiple devices and remote employees has driven the need for better visibility in managing these devices. In addition, the remote user can now log in to many different networks, making it difficult for IT management to centrally manage these devices. In addition to managing these devices, businesses want to view mobile workers’ activities on wireless connections.

Network Access Control (NAC)• Companies such as NetMotion Wireless and Birdstep have implemented NAC

solutions into their portfolios. The NAC feature allows users to connect to the corporate network only if it complies with security policies. Although this functionality has appeared as important in the past, its adaption has been slow. Control in policies and management is becoming increasingly more important than the NAC feature.

Source: Frost & Sullivan analysis.

39<N9B3-74>

Product and Technology Trends (continued)

Increasing number and types of mobile devices and operating systems• As the number of remote workers increases, the multitude of new wireless devices

and operating systems is also causing challenges for businesses. In the past few years, the market has experienced an influx in new operating systems besides Windows. Many traditional mobile VPN participants only support Windows and Symbian, and the addition of support for new platforms is a critical competitive factor moving forward.

Integration/consolidation• Organizations continue to demand a one-stop-shop for security products to reduce

complexity and the amount of support contracts. In the information security market, integration and consolidation of vendors continues to rise. Vendors, such as Cisco and Juniper, are partnering with other mobile vendors to increase the value proposition of their solutions. It is likely that pure-play mobile VPN vendors will need to create tighter integration and partnerships with other mobile vendors, or they will be acquired by larger, more comprehensive security providers.

Source: Frost & Sullivan analysis.

40<N9B3-74>

Legislative Trends

Payment Card Industry (PCI) Data Security Standard (DSS) • The PCI DSS set a minimum baseline in the marketplace to protect a cardholder’s

sensitive account and transaction information. On 1 October 2008, PCI DSS 1.2 was implemented. The main purpose for the update was to clarify existing requirements and provide flexibility in the standard’s interpretation. Within the mobile VPN market, legislation has stirred the retail market and businesses that have access to remote credit card transactions. The need for encryption and protecting data in motion continues to drive the market for mobile security.

HIPAA and HITECH• The Health Insurance Portability and Accountability Act (HIPAA) was signed into law

on August 21, 1996, causing a host of security solutions to be evaluated and implemented by hospitals, doctors, pharmacies, and insurance companies. The Health Information Technology for Economic and Clinical Health Act (HITECH) responds to the criticisms of HIPAA and builds on HIPAA and broadens HIPPA’s scope by increasing the rigor for compliance. As the healthcare market adopts wireless technologies, the need for remote access will increase. In addition, organizations will need to secure any mobile or wireless device that is accessing the corporate network to reduce the possibility of threats.

Source: Frost & Sullivan analysis.

41<N9B3-74>

Legislative Trends (continued)

Gramm-Leach-Bliley Act• The Gramm-Leach-Bliley Act (GLB) targets the financial markets, banks, securities

firms, and insurance companies. This act addresses the privacy of consumer data and its exchange. Given the sensitivity of financial information, the financial sector required little convincing of the need for securing their communications. Financial institutions were early adopters of security technologies because of the size of their networks and budgets and the sensitivity of their data.

Sarbanes-Oxley Act• The Sarbanes-Oxley Act (SOX) set and enforced standards for corporate financial

accountability. Intended to reduce fraud and conflicts of interest, SOX mandates that CEOs, CFOs, and auditing firms attest to the validity of financial records and audits. It establishes management's responsibility for internal control and financial reporting; it also requires organizations to report material changes in financial conditions or operations on a rapid and current basis.

Source: Frost & Sullivan analysis.

42<N9B3-74>

Total Mobile VPN Products Market Percent of Revenue Distribution by Vertical Market

Telecommunications 30.0%

Government 20.0%Healthcare

10.0%

Utilities 10.0%

Financial 7.0%

*Other23.0%

Percent Sales BreakdownTotal Mobile VPN Products Market: Global, 2010

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.*Other Verticals include: Retail, Media, Transportation, Hospitality, Manufacturing , and Entertainment

43<N9B3-74>

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.

Total Mobile VPN Products Market Revenue Forecast by Vertical Market (continued)

yKey Takeaway: Telecommunications will provide strong growth opportunities during

next 5 years.

*Other Verticals include: Retail, Media, Transportation, Hospitality, Manufacturing , and Entertainment

2007 2008 2009 2010 2011 2012 2013 2014 2015Other 24.5 28.2 32.0 36.8 42.1 48.2 53.8 60.6 65.7Utilities 8.3 10.5 12.9 16.0 19.9 24.2 30.0 35.8 43.5Financial 5.7 7.2 8.8 11.2 13.7 16.8 20.6 24.7 29.8Healthcare 7.9 10.0 12.5 16.0 20.1 24.4 30.3 37.4 45.5Telecommunications 26.5 32.6 39.3 48.0 58.3 69.7 83.9 99.5 117.7Government 17.2 21.5 26.1 32.0 39.0 46.7 56.4 67.0 79.8Revenue Growth Rate (%) 22.2 20.0 21.2 20.6 19.2 19.6 18.2 17.5

0.0

5.0

10.0

15.0

20.0

25.0

0.050.0

100.0150.0200.0250.0300.0350.0400.0450.0

Grow

th Rate (%

)Rev

enue

($ M

illio

n)

Year

Total Mobile VPN Products Market Revenue Forecast by Vertical Market , 2007-2015, Global

44<N9B3-74>

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.

Total Mobile VPN Products Market Unit Shipment and Revenue Forecast for Telecommunications Vertical

Key Takeaway: Wireless carriers and other telecom carriers will continue to drive the sales of mobile VPNs from integrated devices

2007 2008 2009 2010 2011 2012 2013 2014 2015Revenue 26.5 32.6 39.3 48.0 58.3 69.7 83.9 99.5 117.7Units 129.7 162.9 200.7 249.8 309.6 377.7 463.9 561.2 677.5

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

Uni

ts (1

000s

)

Rev

enue

($ M

illio

n)

Year

Total Mobile VPN Products Market, Unit Shipment and Revenue Forecast for Telecommunications Vertical

Global, 2007–2015CAGR = 19.1%

45<N9B3-74>

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.

Total Mobile VPN Products Market Unit Shipment and Revenue Forecast for Government Vertical

Key Takeaway: State and emergency response workers will drive the government market.

2007 2008 2009 2010 2011 2012 2013 2014 2015Revenue 17.2 21.5 26.1 32.0 39.0 46.7 56.4 67.0 79.8Units 84.2 107.3 133.3 166.5 207.0 253.0 311.8 377.8 459.7

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

500.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Uni

ts (1

000s

)

Rev

enue

($ M

illio

n)

Year

Total Mobile VPN Products Market Unit Shipment and Revenue Forecast for Government Vertical

Global, 2007–2015CAGR = 19.4%

46<N9B3-74>

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.

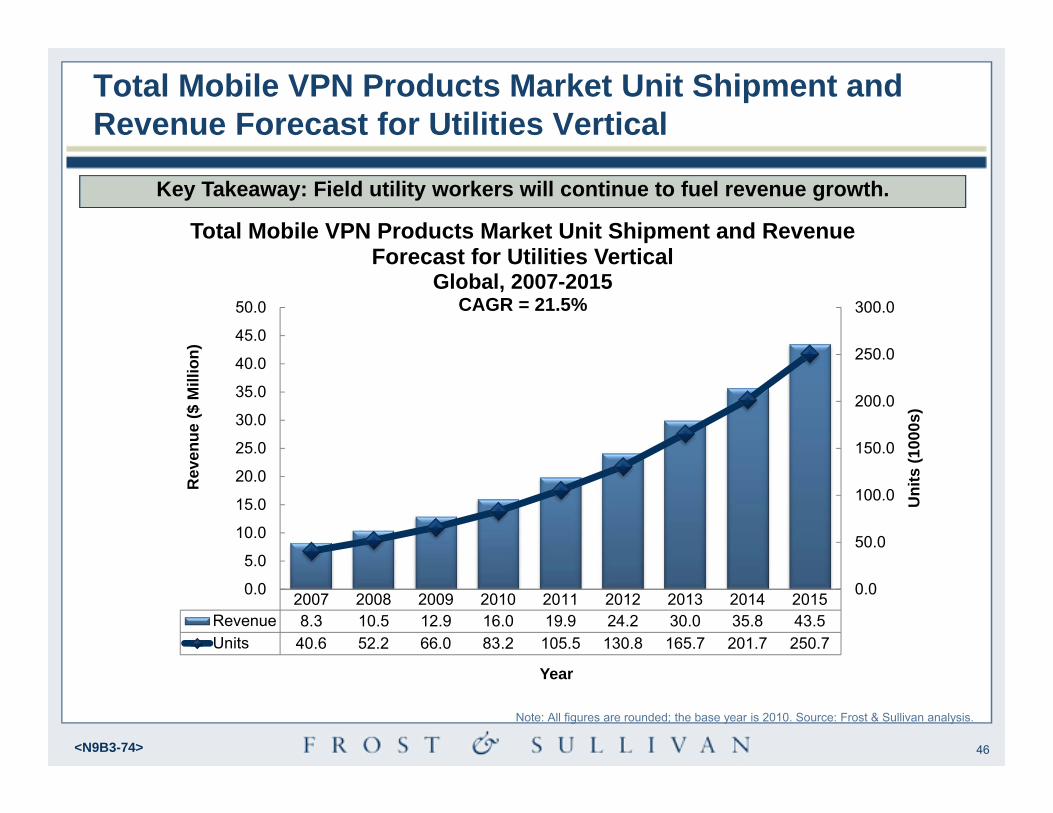

Total Mobile VPN Products Market Unit Shipment and Revenue Forecast for Utilities Vertical

Key Takeaway: Field utility workers will continue to fuel revenue growth.

2007 2008 2009 2010 2011 2012 2013 2014 2015Revenue 8.3 10.5 12.9 16.0 19.9 24.2 30.0 35.8 43.5Units 40.6 52.2 66.0 83.2 105.5 130.8 165.7 201.7 250.7

0.0

50.0

100.0

150.0

200.0

250.0

300.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Uni

ts (1

000s

)

Rev

enue

($ M

illio

n)

Year

Total Mobile VPN Products Market Unit Shipment and Revenue Forecast for Utilities Vertical

Global, 2007-2015CAGR = 21.5%

47<N9B3-74>

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.

Total Mobile VPN Products Market Unit Shipment and Revenue Forecast for Healthcare Vertical

Key Takeaway: Field workers in the healthcare market will fuel revenue growth

2007 2008 2009 2010 2011 2012 2013 2014 2015Revenue 7.9 10.0 12.5 16.0 20.1 24.4 30.3 37.4 45.5Units 38.8 50.0 63.9 83.2 106.6 132.1 167.3 210.9 261.7

0.0

50.0

100.0

150.0

200.0

250.0

300.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Uni

ts (1

000s

)

Rev

enue

($ M

illio

n)

Year

Total Mobile VPN Products Market Unit Shipment and Revenue Forecast for Healthcare Vertical

Global, 2007-2015CAGR = 22.6%

48<N9B3-74>

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.

Total Mobile VPN Products Market Unit Shipment and Revenue Forecast for Financial Vertical

Key Takeaway: The financial market is more inclined to purchase traditional SSL VPN solutions, but will be inclined to try new technologies.

2007 2008 2009 2010 2011 2012 2013 2014 2015Revenue 5.7 7.2 8.8 11.2 13.7 16.8 20.6 24.7 29.8Units 27.8 35.7 45.1 58.3 72.7 91.0 114.0 139.4 171.5

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Uni

ts (1

000s

)

Rev

enue

($ M

illio

n)

Year

Total Mobile VPN Products Market Unit Shipment and Revenue Forecast for Financial Vertical

Global, 2007–2015CAGR = 21.1%

49<N9B3-74>

Vertical Market Revenue Forecast Discussion

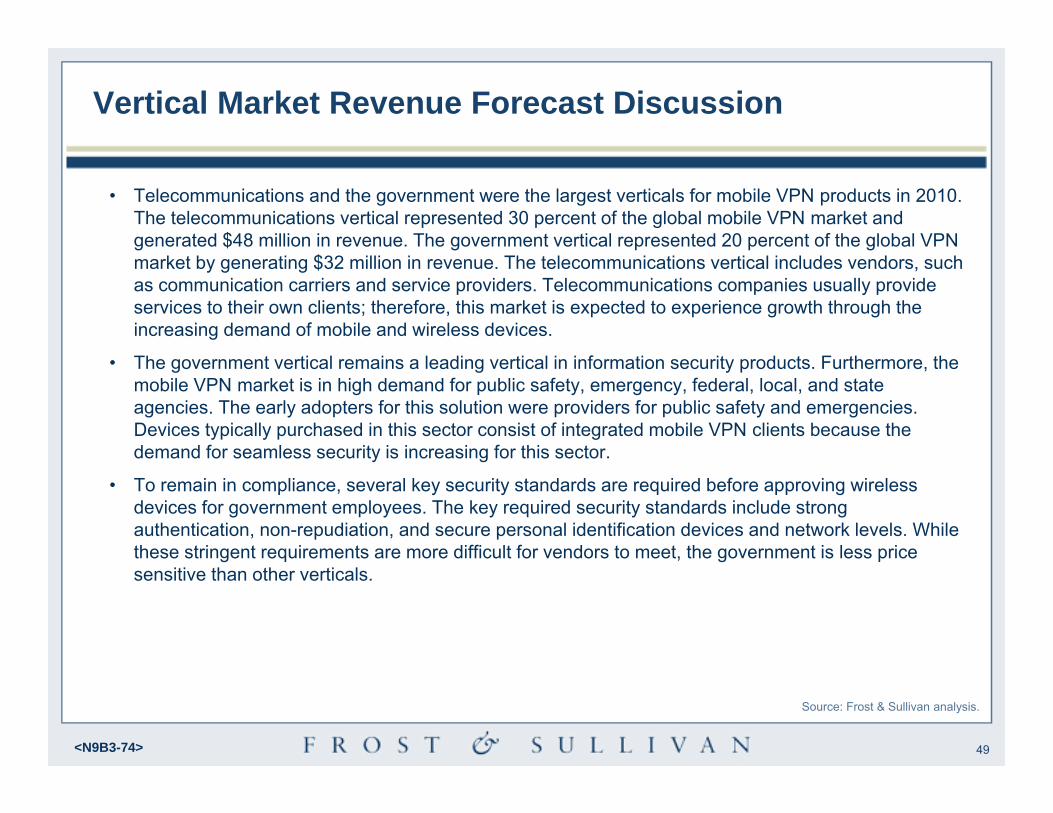

• Telecommunications and the government were the largest verticals for mobile VPN products in 2010. The telecommunications vertical represented 30 percent of the global mobile VPN market and generated $48 million in revenue. The government vertical represented 20 percent of the global VPN market by generating $32 million in revenue. The telecommunications vertical includes vendors, such as communication carriers and service providers. Telecommunications companies usually provide services to their own clients; therefore, this market is expected to experience growth through the increasing demand of mobile and wireless devices.

• The government vertical remains a leading vertical in information security products. Furthermore, the mobile VPN market is in high demand for public safety, emergency, federal, local, and state agencies. The early adopters for this solution were providers for public safety and emergencies. Devices typically purchased in this sector consist of integrated mobile VPN clients because the demand for seamless security is increasing for this sector.

• To remain in compliance, several key security standards are required before approving wireless devices for government employees. The key required security standards include strong authentication, non-repudiation, and secure personal identification devices and network levels. While these stringent requirements are more difficult for vendors to meet, the government is less price sensitive than other verticals.

Source: Frost & Sullivan analysis.

50<N9B3-74>

Vertical Market Revenue Forecast Discussion(continued)

. • The healthcare vertical generated $16 million in revenue in the total global mobile VPN market. In 2010, this segment represented 10 percent of the global mobile VPN market. The healthcare vertical is made of hospitals and other healthcare facilities.

• The healthcare vertical has been a key adopter of SSL VPNs and Virtual Desktop Infrastructure (VDI). Meeting HIPAA compliance has increased the need to secure data on mobile devices—the effort to meet these compliance regulations will create strong traction for this market globally.

• Field workers, physicians, and medical staff are being given more access to confidential medical records and other healthcare applications through wireless networks; therefore, the need to protect this data in transit will help spur the growth of the healthcare vertical. Home healthcare and telemedicine is driving the addition of more wireless devices and with required compliance legislations, such as HIPAA and HITech, mobile-device security be at the forefront of deployments.

• The utilities vertical is comprised of gas, electric, and energy companies. The utilities segment has adopted mobile VPN solutions in order to provide continuous application sessions and seamless roaming capabilities to field service workers. Field service workers within the utilities vertical are also utilizing this solution to process orders and respond to service inquires more efficiently and effectively.

Source: Frost & Sullivan analysis.

51<N9B3-74>

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan analysis.

Total Mobile VPN Products Market Percent Revenue Forecast by Distribution Channel

Key Takeaway: Partner channels will remain the most influential channel in 2011; the VARs channel will also continue to grow throughout 2015.

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015Web 3.1 3.5 3.6 3.0 2.9 2.7 2.5 2.4 2.1Partners 43.6 44.1 44.5 45.0 45.3 45.7 46.0 46.2 46.4Direct Sales 12.0 11.0 10.1 10.0 9.5 9.1 8.7 8.3 7.8VARS 41.3 41.4 41.8 42.0 42.3 42.5 42.8 43.1 43.7

% R

even

ue

Year

Total Mobile VPN Products Market Percent Revenue Forecast by Distribution Channel

Global, 2007-2015

52<N9B3-74>

Distribution Channel Revenue Forecast Discussion

• Key distribution channels for mobile VPN products include: partnerships with telecom companies, integrators, and handset manufacturers. VARs are also an important distribution channel for mobile VPN products. In 2010, partnerships accounted for $72 million in revenue and 45 percent of mobile VPN market. Partnerships are expected to continue to be a key driver in the future, generating $177.2 million in revenue or 46.3 percent of the market by 2015. Carriers such as AT&T, Sprint, and Verizon Wireless have been instrumental in selling mobile VPN solutions to their customers. Adding security to the wireless portfolio has been important in the sales process for wireless solutions.

• VARs generated $67.2 million in revenue in 2010. VARs remains a key channel distributer for mobile VPN vendors. VARs are expected to remain a top distribution point for mobile VPN providers and are expected to contribute $166.9 million in revenue by 2015.

• Managed security service providers are also hosting mobile VPN services. Enterprises have found that mobile deployments may be confusing and complex; therefore, enterprises are turning to MSSPs to host this service. MSSPs are expected to become a more important channel in the next 3 to 5 years.

Source: Frost & Sullivan analysis.

53<N9B3-74>

Market Share and Competitive Analysis—Total Mobile VPN Products Market

54<N9B3-74>

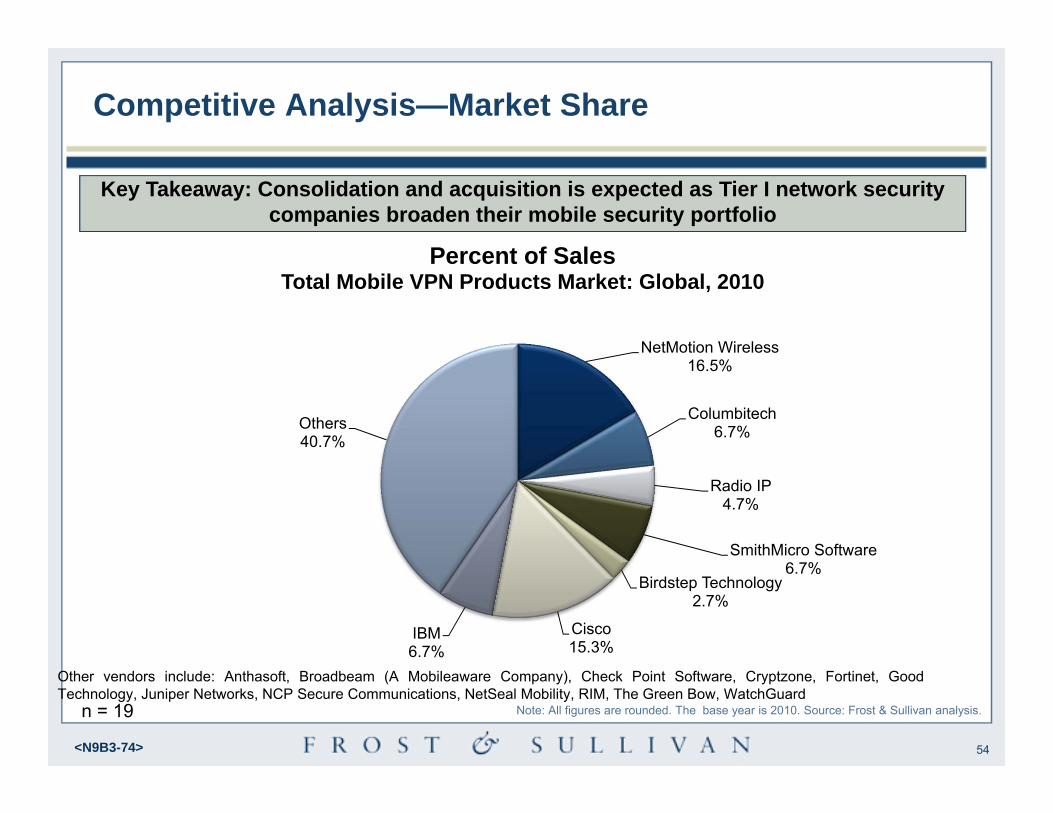

Competitive Analysis—Market Share

Note: All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis.

Key Takeaway: Consolidation and acquisition is expected as Tier I network security companies broaden their mobile security portfolio

NetMotion Wireless 16.5%

Columbitech 6.7%

Radio IP4.7%

SmithMicro Software6.7%

Birdstep Technology 2.7%

Cisco 15.3%

IBM6.7%

Others40.7%

Percent of SalesTotal Mobile VPN Products Market: Global, 2010

Other vendors include: Anthasoft, Broadbeam (A Mobileaware Company), Check Point Software, Cryptzone, Fortinet, GoodTechnology, Juniper Networks, NCP Secure Communications, NetSeal Mobility, RIM, The Green Bow, WatchGuard

n = 19

55<N9B3-74>

Market Share Analysis

The top five mobile participants contributed 55.1 percent of total market revenue. NetMotion Wireless leads the competition in 2010 with 16.5 percent of revenue. NetMotion Wireless developed relationships with wireless carriers early in the market, and these relationships have proven to be favorable for the company. In addition to existing partnerships, NetMotion’s early market entrance has also enabled the company’s success in the mobile VPN market.

Cisco is a top integrator in the market, and its always on approach for remote access has enabled the company to gain a strong market entrance in the enterprise market. Cisco ranked second next to NetMotion with $23 million in revenue for 2010.

Companies Revenue (%)

NetMotion Wireless 16.5

Cisco 15.3

Columbitech 6.7

SmithMicro Software 6.7

IBM. 6.7

Radio IP 4.7

Birdstep Technology 2.7

Others 40.7

Total 100.0

* A list of “Other” companies can be found at link to slide in appendix. Note: All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis.

Mobile VPN Products Market: Company Market Share Analysis of Top Participants Global, 2010

56<N9B3-74>

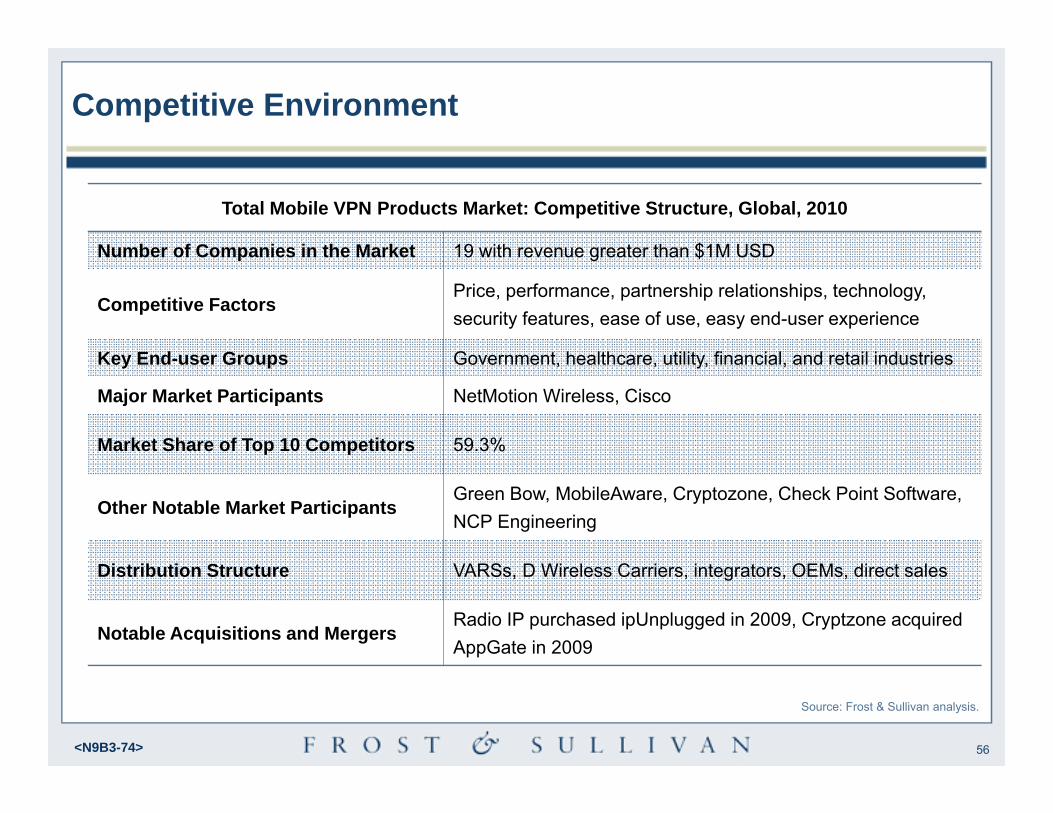

Competitive Environment

Source: Frost & Sullivan analysis.

Total Mobile VPN Products Market: Competitive Structure, Global, 2010

Number of Companies in the Market 19 with revenue greater than $1M USD

Competitive FactorsPrice, performance, partnership relationships, technology, security features, ease of use, easy end-user experience

Key End-user Groups Government, healthcare, utility, financial, and retail industries

Major Market Participants NetMotion Wireless, Cisco

Market Share of Top 10 Competitors 59.3%

Other Notable Market ParticipantsGreen Bow, MobileAware, Cryptozone, Check Point Software, NCP Engineering

Distribution Structure VARSs, D Wireless Carriers, integrators, OEMs, direct sales

Notable Acquisitions and MergersRadio IP purchased ipUnplugged in 2009, Cryptzone acquired AppGate in 2009

57<N9B3-74>

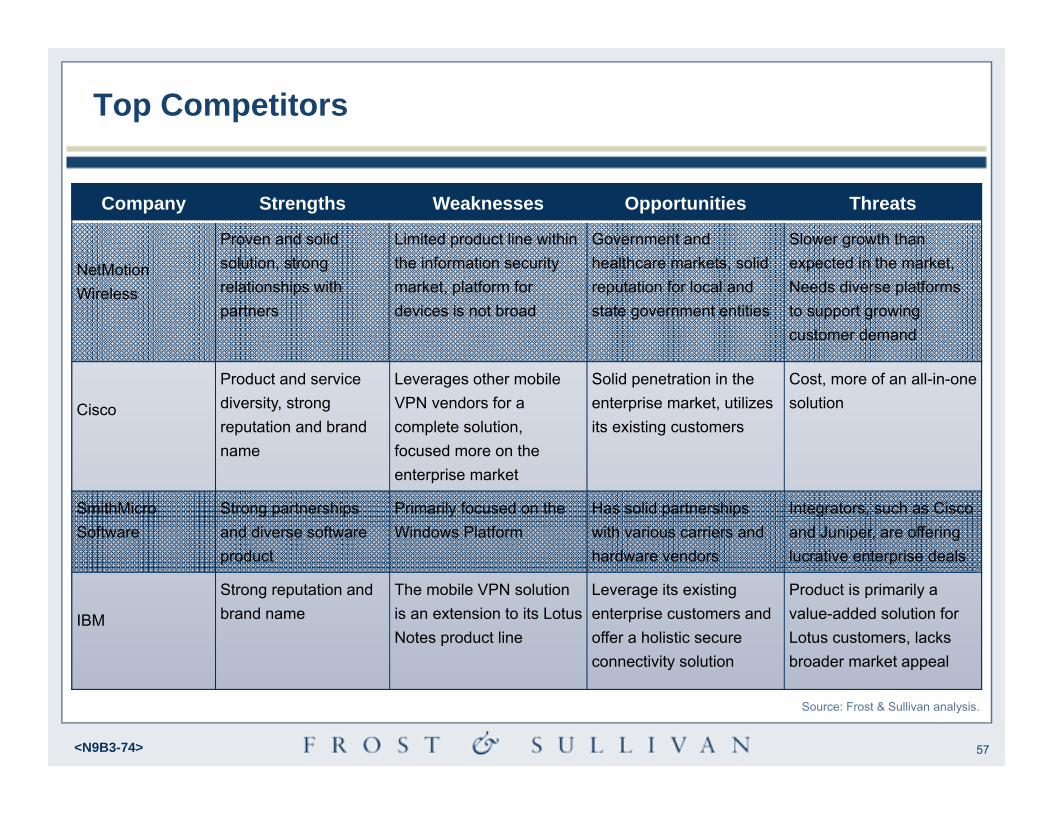

Top Competitors

Company Strengths Weaknesses Opportunities Threats

NetMotionWireless

Proven and solid solution, strong relationships with partners

Limited product line within the information security market, platform for devices is not broad

Government and healthcare markets, solid reputation for local and state government entities

Slower growth than expected in the market, Needs diverse platforms to support growing customer demand

Cisco

Product and service diversity, strong reputation and brand name

Leverages other mobile VPN vendors for a complete solution, focused more on the enterprise market

Solid penetration in the enterprise market, utilizes its existing customers

Cost, more of an all-in-one solution

SmithMicroSoftware

Strong partnerships and diverse software product

Primarily focused on the Windows Platform

Has solid partnerships with various carriers and hardware vendors

Integrators, such as Cisco and Juniper, are offering lucrative enterprise deals

IBM

Strong reputation and brand name

The mobile VPN solution is an extension to its Lotus Notes product line

Leverage its existing enterprise customers and offer a holistic secure connectivity solution

Product is primarily a value-added solution for Lotus customers, lacks broader market appeal

Source: Frost & Sullivan analysis.

58<N9B3-74>

Top Competitors (continued)

Company Strengths Weaknesses Opportunities Threats

Columbitech Solid mobile VPN product, works well for integration, supports Android platform

Low penetration in North America

Wireless carriers, value-added resellers in North America

Slow growth because of economic restraints, focuses less on enterprise markets

Radio IP

Product and service diversity

Limited market penetration globally

Government and global expansion markets

The need to remarket brand name after purchase of ipUnplugged

BirdstepTechnologies

Solid product offering and relationships

Small penetration in the enterprise market, low brand awareness

North America penetration, building more partnerships

Low growth due to economic issues

Cryptzone Solid security portfolio and SSL VPN provider

Building reputation in mobile VPN market

North America and building strong distribution channels

Low brand name and reputation in VPN market

NCP Engineering Solid SSL VPN solution and hybrid offering, strong relationships

Strong brand name outside Germany, offering is for large enterprises

North America penetration, offers a managed service for penetrating SMB markets

Competitive market from large networking companies such as Cisco

Source: Frost & Sullivan analysis.

59<N9B3-74>

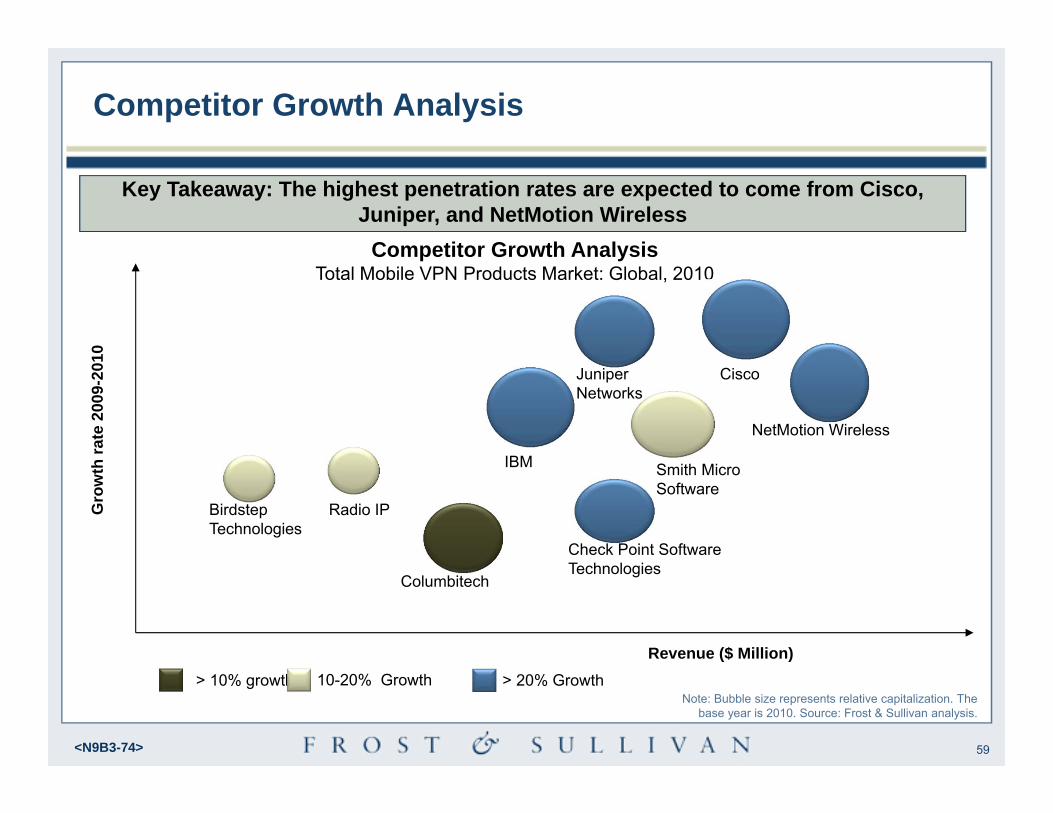

Competitor Growth AnalysisG

row

th ra

te 2

009-

2010

NetMotion Wireless

Revenue ($ Million)

Cisco

BirdstepTechnologies

Smith Micro Software

Columbitech

> 10% growth 10-20% Growth > 20% Growth

Key Takeaway: The highest penetration rates are expected to come from Cisco, Juniper, and NetMotion Wireless

Competitor Growth AnalysisTotal Mobile VPN Products Market: Global, 2010

IBM

Check Point Software Technologies

Radio IP

Juniper Networks

Note: Bubble size represents relative capitalization. The base year is 2010. Source: Frost & Sullivan analysis.

60<N9B3-74>

Competitive Factors and Assessment

Source: Frost & Sullivan analysis.

Tier Analysis

Birdstep Technologies, Radio IP, NCP Engineering, Cryptzone

Columbitech, Smith Micro,IBM, Check Point Software

NetMotion Wireless, Cisco

Tier III

Tier II

Tier I

Company Tier AnalysisCompany Tier Analysis• There are three tiers of competitors in the global

mobile VPN security market. • NetMotion Wireless and Cisco were the Tier I

market competitors that dominated the market, with a combined share of 42.5 percent in 2010.

• Tier II companies, including Columbitech , IBM, Check Point Software were considered challengers or contenders, with a strong presence in the market.

• Tier III companies had a smaller presence in the market, primarily niche markets.

61<N9B3-74>

Inno

vatio

n

Strategy Implementation

Check Point

Columbitech

Source: Frost & Sullivan analysis.

Cisco

NetMotion

Wireless

Juniper

Networks

Total Mobile VPN Products Market: Strategy Implementation and Innovation by Vendor Global, 2010

Competitive Analysis (continued)Competitive Factors and Assessment (continued)

RadioIP

Birdstep Technologies

IBM

Cryptzone

NCP Engineering

62<N9B3-74>

Competitive Factors and Assessment (continued)

Source: Frost & Sullivan analysis.

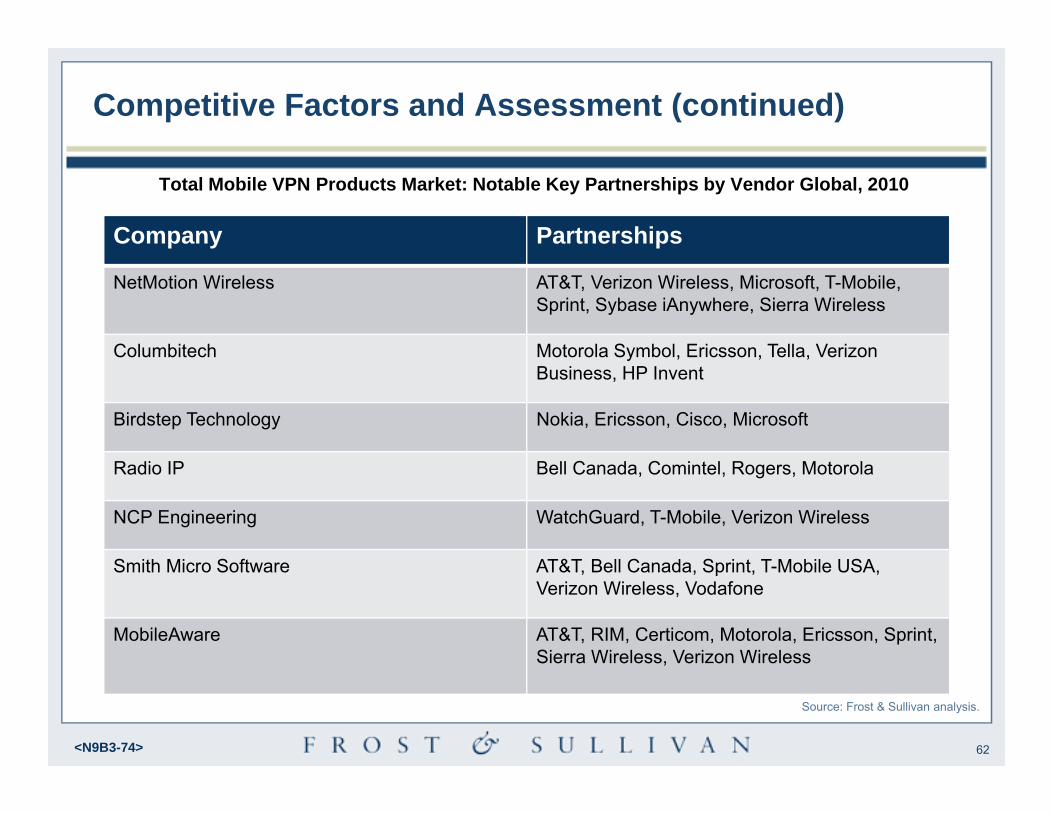

Company Partnerships

NetMotion Wireless AT&T, Verizon Wireless, Microsoft, T-Mobile, Sprint, Sybase iAnywhere, Sierra Wireless

Columbitech Motorola Symbol, Ericsson, Tella, Verizon Business, HP Invent

Birdstep Technology Nokia, Ericsson, Cisco, Microsoft

Radio IP Bell Canada, Comintel, Rogers, Motorola

NCP Engineering WatchGuard, T-Mobile, Verizon Wireless

Smith Micro Software AT&T, Bell Canada, Sprint, T-Mobile USA, Verizon Wireless, Vodafone

MobileAware AT&T, RIM, Certicom, Motorola, Ericsson, Sprint, Sierra Wireless, Verizon Wireless

Total Mobile VPN Products Market: Notable Key Partnerships by Vendor Global, 2010

63<N9B3-74>

Competitive Factors and Assessment (continued)

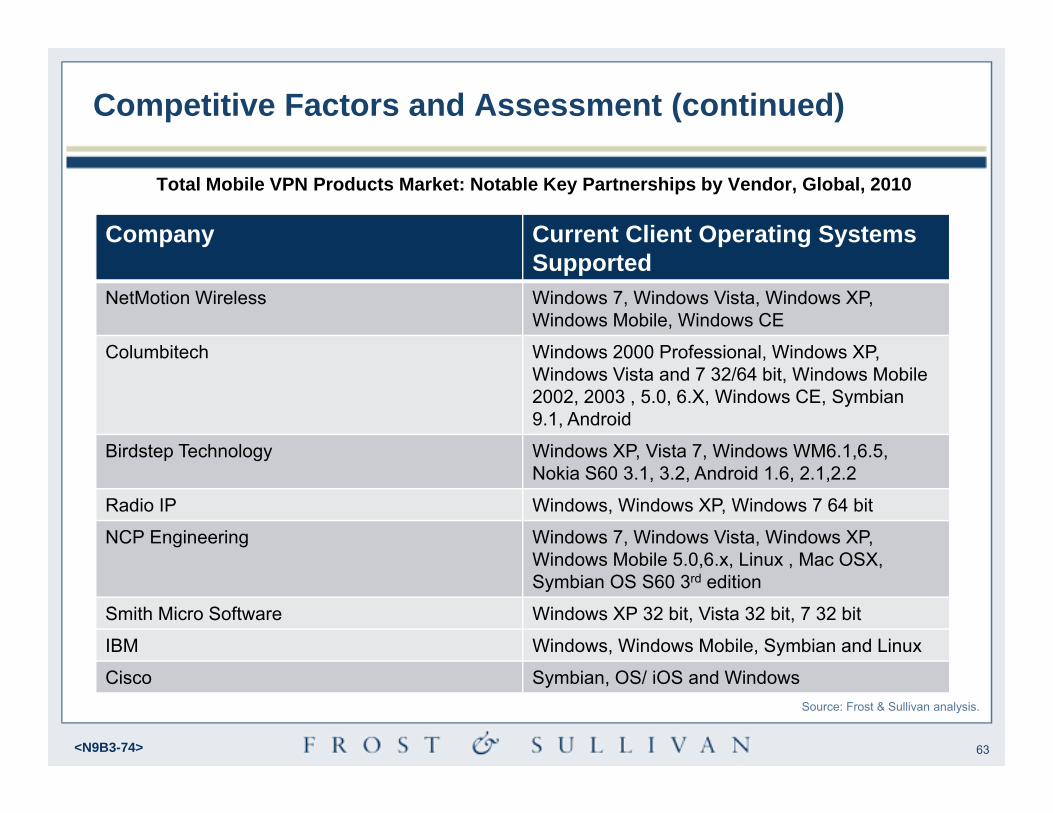

Source: Frost & Sullivan analysis.

Company Current Client Operating Systems Supported

NetMotion Wireless Windows 7, Windows Vista, Windows XP, Windows Mobile, Windows CE

Columbitech Windows 2000 Professional, Windows XP, Windows Vista and 7 32/64 bit, Windows Mobile 2002, 2003 , 5.0, 6.X, Windows CE, Symbian 9.1, Android

Birdstep Technology Windows XP, Vista 7, Windows WM6.1,6.5, Nokia S60 3.1, 3.2, Android 1.6, 2.1,2.2

Radio IP Windows, Windows XP, Windows 7 64 bit

NCP Engineering Windows 7, Windows Vista, Windows XP, Windows Mobile 5.0,6.x, Linux , Mac OSX, Symbian OS S60 3rd edition

Smith Micro Software Windows XP 32 bit, Vista 32 bit, 7 32 bit

IBM Windows, Windows Mobile, Symbian and Linux

Cisco Symbian, OS/ iOS and Windows

Total Mobile VPN Products Market: Notable Key Partnerships by Vendor, Global, 2010

64<N9B3-74>

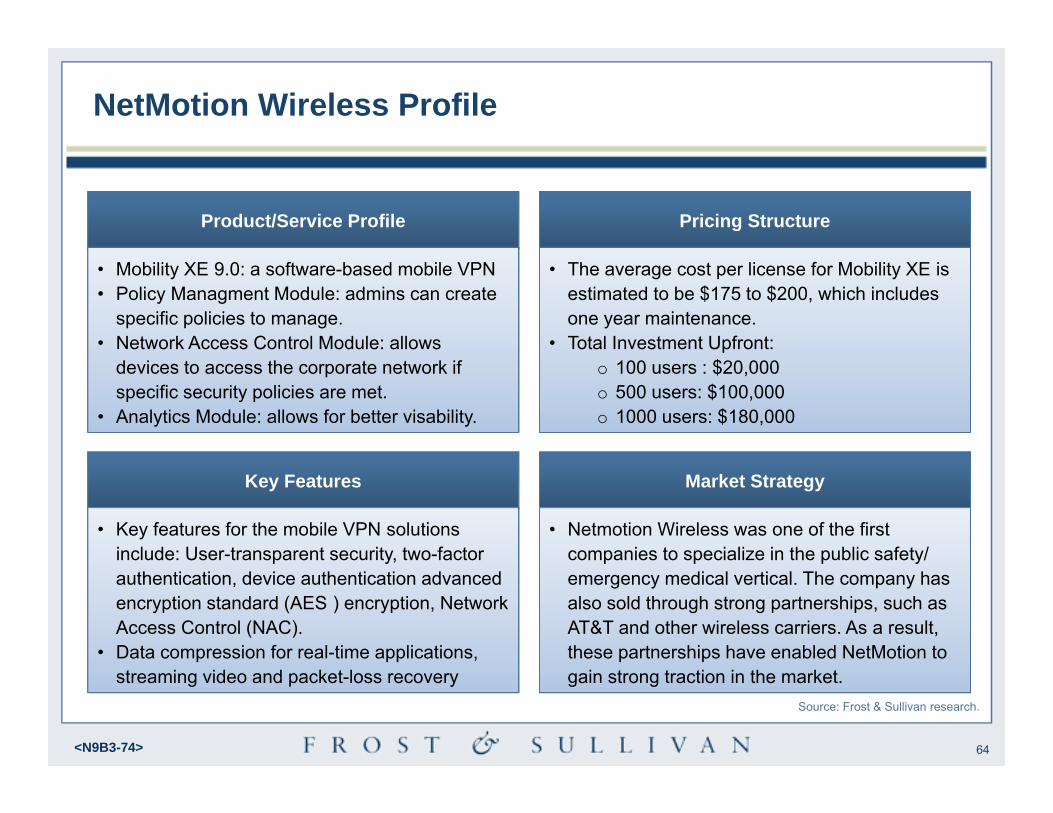

NetMotion Wireless Profile

Product/Service Profile Pricing Structure

Key Features Market Strategy

• Mobility XE 9.0: a software-based mobile VPN• Policy Managment Module: admins can create

specific policies to manage. • Network Access Control Module: allows

devices to access the corporate network if specific security policies are met.

• Analytics Module: allows for better visability.

• The average cost per license for Mobility XE is estimated to be $175 to $200, which includes one year maintenance.

• Total Investment Upfront:o 100 users : $20,000o 500 users: $100,000o 1000 users: $180,000

• Key features for the mobile VPN solutions include: User-transparent security, two-factor authentication, device authentication advanced encryption standard (AES ) encryption, Network Access Control (NAC).

• Data compression for real-time applications, streaming video and packet-loss recovery

• Netmotion Wireless was one of the first companies to specialize in the public safety/ emergency medical vertical. The company has also sold through strong partnerships, such as AT&T and other wireless carriers. As a result, these partnerships have enabled NetMotion to gain strong traction in the market.

Source: Frost & Sullivan research.

65<N9B3-74>

Competitor Opportunities• NetMotion is a solid competitor, but it

lacks visibility into other geographic areas.

• NetMotion is a strong competitor in the government sector, but it does not have a large presence in the enterprise market.

• The company’s product is restricted to the Windows operating system; therefore, the company needs to focus on expanding to support more operating systems, such as the Android and Apple platforms.

NetMotion Wireless Strengths• NetMotion Wireless already has a strong

presence in the North American market and is making an entrance into the European market.

• NetMotion Wireless has expanded its product line to include a detailed policy management and network access control (NAC) module.

• Frost & Sullivan believes that NetMotionWireless will continue to have a strong position in the mobile VPN market.

NetMotion Wireless Profile (continued)

Source: Frost & Sullivan analysis.

66<N9B3-74>

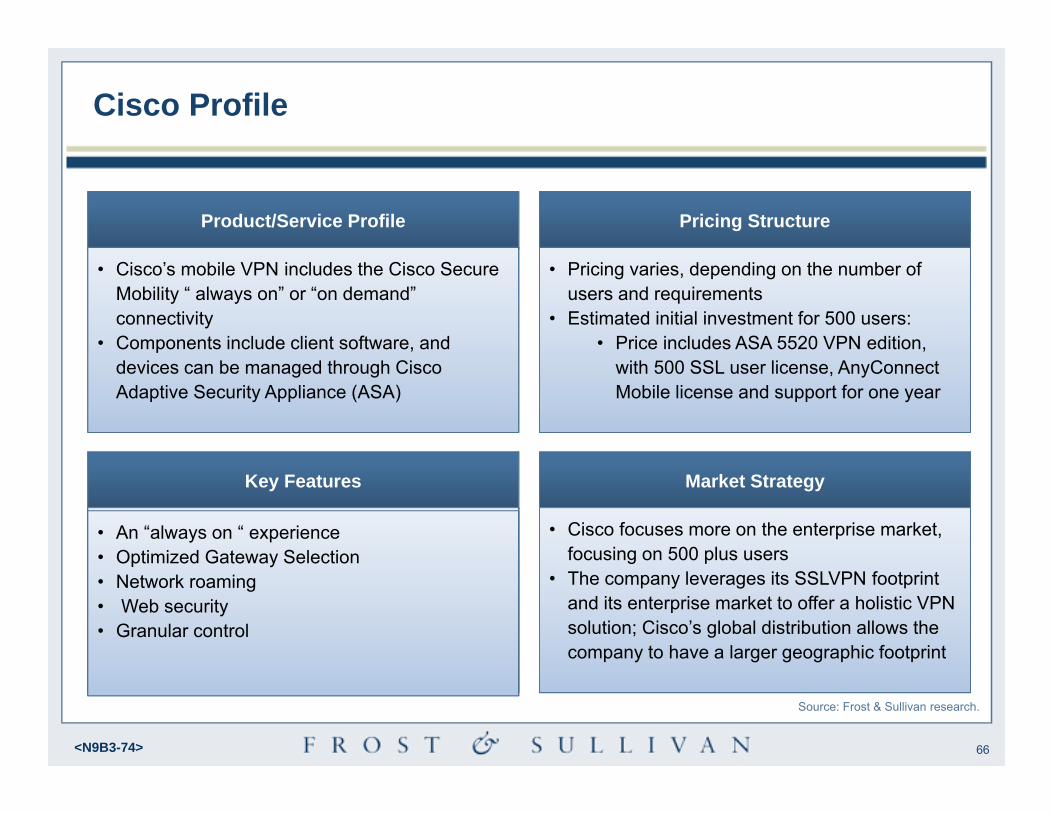

Cisco Profile

Product/Service Profile Pricing Structure

Key Features Market Strategy

• Cisco’s mobile VPN includes the Cisco Secure Mobility “ always on” or “on demand” connectivity

• Components include client software, and devices can be managed through Cisco Adaptive Security Appliance (ASA)

• Pricing varies, depending on the number of users and requirements

• Estimated initial investment for 500 users: • Price includes ASA 5520 VPN edition,

with 500 SSL user license, AnyConnectMobile license and support for one year

• The solution offers an “always on “ experience • In addition, the VPN offers an optimized

gateway selection Other additional features include: • Web secuirty • Granular control

• Cisco focuses more on the enterprise market, focusing on 500 plus users

• The company leverages its SSLVPN footprint and its enterprise market to offer a holistic VPN solution; Cisco’s global distribution allows the company to have a larger geographic footprint

Source: Frost & Sullivan research.

• An “always on “ experience • Optimized Gateway Selection • Network roaming • Web security • Granular control

67<N9B3-74>

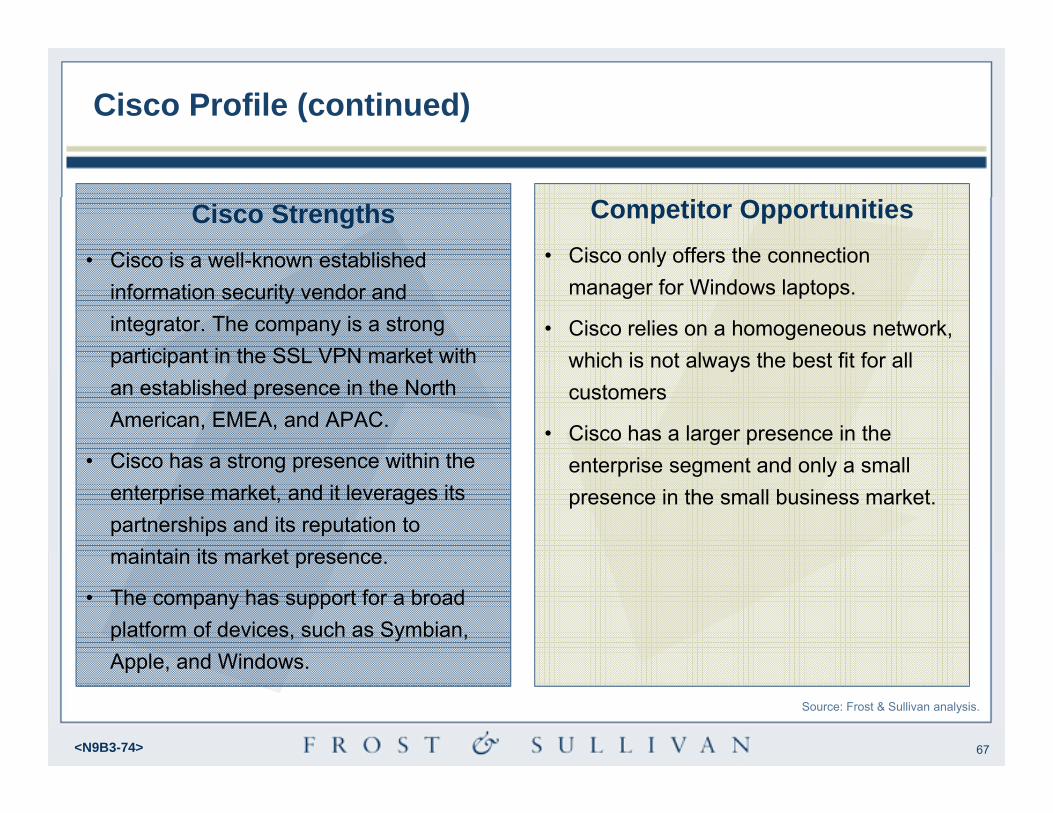

Cisco Strengths• Cisco is a well-known established

information security vendor and integrator. The company is a strong participant in the SSL VPN market with an established presence in the North American, EMEA, and APAC.

• Cisco has a strong presence within the enterprise market, and it leverages its partnerships and its reputation to maintain its market presence.

• The company has support for a broad platform of devices, such as Symbian, Apple, and Windows.

Cisco Profile (continued)

Source: Frost & Sullivan analysis.

Competitor Opportunities• Cisco only offers the connection

manager for Windows laptops.

• Cisco relies on a homogeneous network, which is not always the best fit for all customers

• Cisco has a larger presence in the enterprise segment and only a small presence in the small business market.

68<N9B3-74>

SmithMicro Software Profile

Product/Service Profile Pricing Structure

Key Features Market Strategy

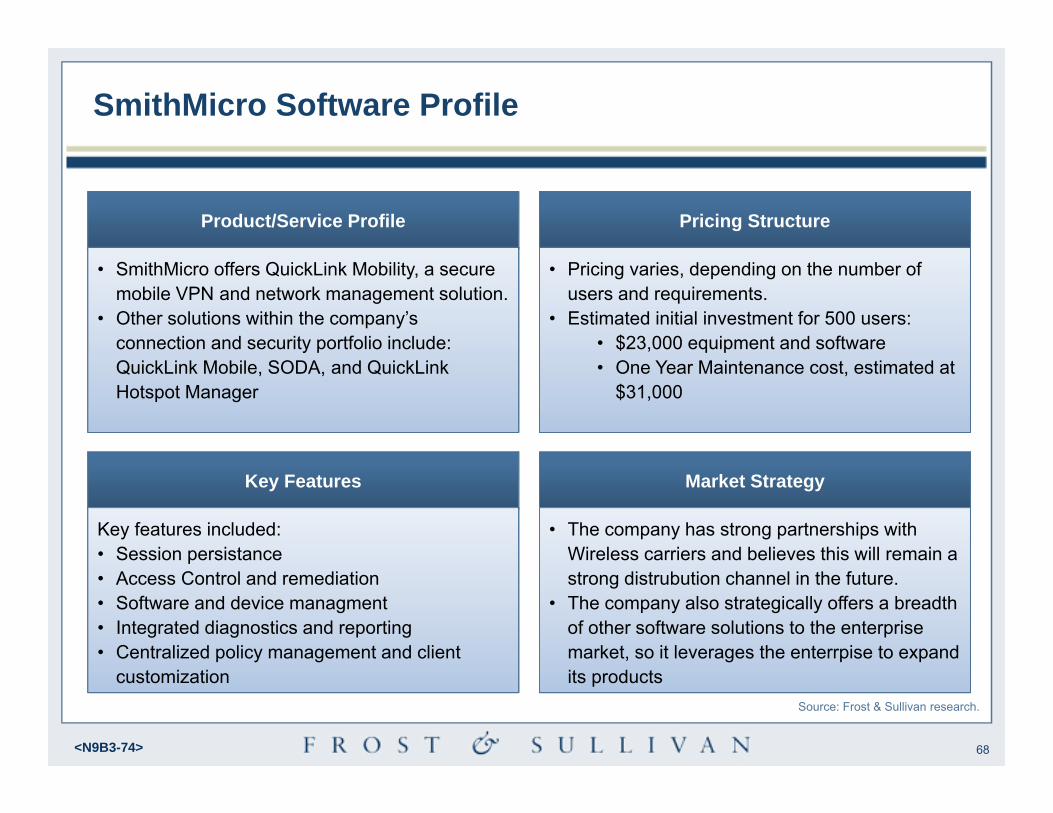

• SmithMicro offers QuickLink Mobility, a secure mobile VPN and network management solution.

• Other solutions within the company’s connection and security portfolio include: QuickLink Mobile, SODA, and QuickLink Hotspot Manager

• Pricing varies, depending on the number of users and requirements.

• Estimated initial investment for 500 users: • $23,000 equipment and software• One Year Maintenance cost, estimated at

$31,000

Key features included: • Session persistance • Access Control and remediation• Software and device managment • Integrated diagnostics and reporting • Centralized policy management and client

customization

• The company has strong partnerships with Wireless carriers and believes this will remain a strong distrubution channel in the future.

• The company also strategically offers a breadth of other software solutions to the enterprise market, so it leverages the enterrpise to expand its products

Source: Frost & Sullivan research.

69<N9B3-74>

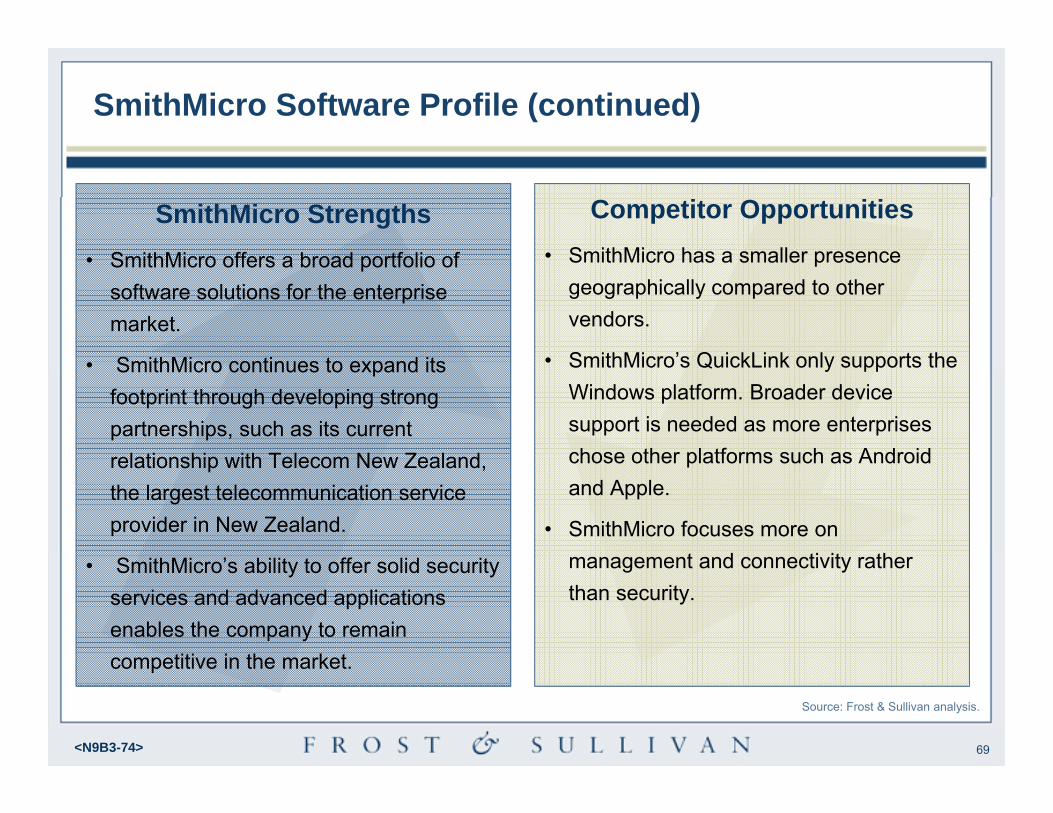

SmithMicro Strengths• SmithMicro offers a broad portfolio of

software solutions for the enterprise market.

• SmithMicro continues to expand its footprint through developing strong partnerships, such as its current relationship with Telecom New Zealand, the largest telecommunication service provider in New Zealand.

• SmithMicro’s ability to offer solid security services and advanced applications enables the company to remain competitive in the market.

SmithMicro Software Profile (continued)

Source: Frost & Sullivan analysis.

Competitor Opportunities• SmithMicro has a smaller presence

geographically compared to other vendors.

• SmithMicro’s QuickLink only supports the Windows platform. Broader device support is needed as more enterprises chose other platforms such as Android and Apple.

• SmithMicro focuses more on management and connectivity rather than security.

70<N9B3-74>

Columbitech Profile

Product/Service Profile Pricing Structure

Key Features Market Strategy

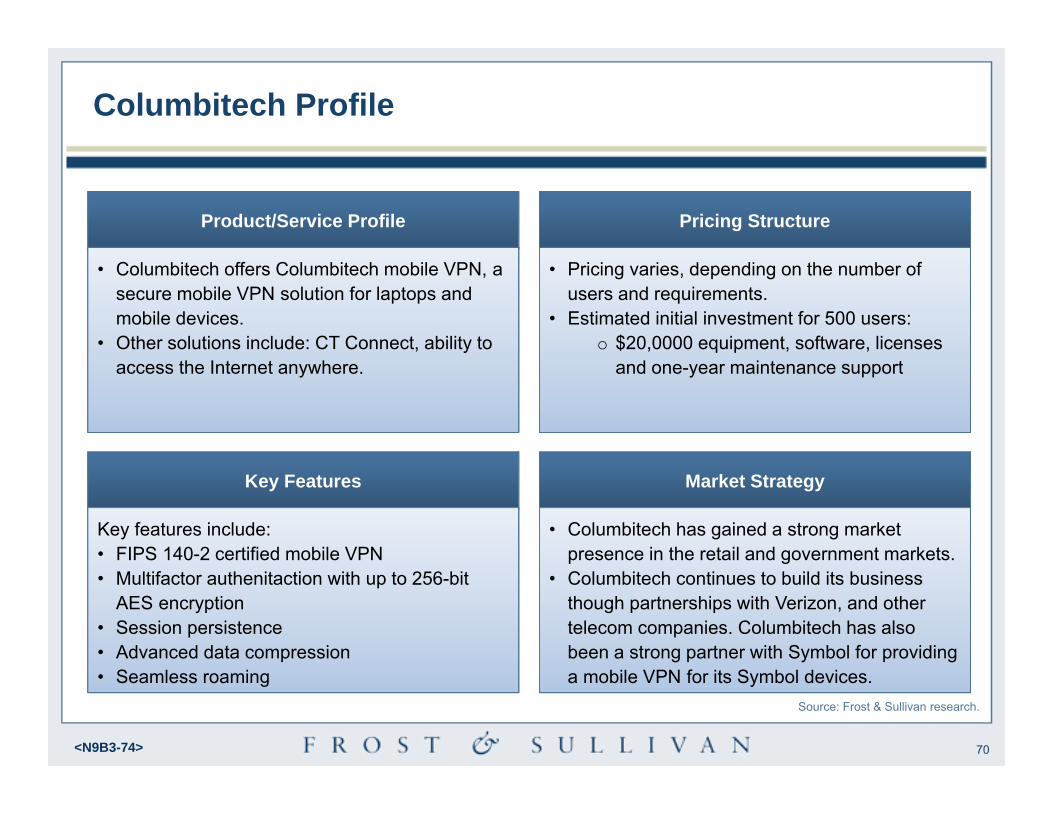

• Columbitech offers Columbitech mobile VPN, a secure mobile VPN solution for laptops and mobile devices.

• Other solutions include: CT Connect, ability to access the Internet anywhere.

• Pricing varies, depending on the number of users and requirements.

• Estimated initial investment for 500 users: o $20,0000 equipment, software, licenses

and one-year maintenance support

Key features include:• FIPS 140-2 certified mobile VPN• Multifactor authenitaction with up to 256-bit

AES encryption • Session persistence• Advanced data compression• Seamless roaming

• Columbitech has gained a strong market presence in the retail and government markets.

• Columbitech continues to build its business though partnerships with Verizon, and other telecom companies. Columbitech has also been a strong partner with Symbol for providing a mobile VPN for its Symbol devices.

Source: Frost & Sullivan research.

71<N9B3-74>

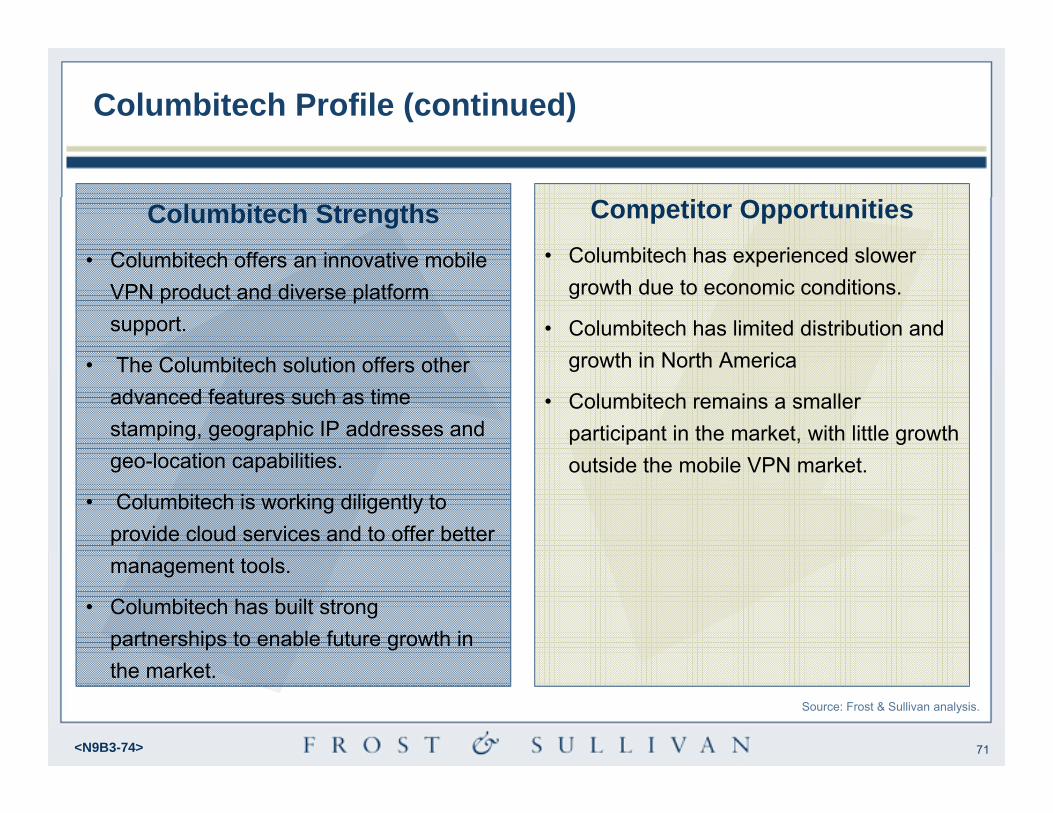

Columbitech Strengths• Columbitech offers an innovative mobile

VPN product and diverse platform support.

• The Columbitech solution offers other advanced features such as time stamping, geographic IP addresses and geo-location capabilities.

• Columbitech is working diligently to provide cloud services and to offer better management tools.

• Columbitech has built strong partnerships to enable future growth in the market.

Columbitech Profile (continued)

Source: Frost & Sullivan analysis.

Competitor Opportunities• Columbitech has experienced slower

growth due to economic conditions.

• Columbitech has limited distribution and growth in North America

• Columbitech remains a smaller participant in the market, with little growth outside the mobile VPN market.

72<N9B3-74>

IBM Profile

Product/Service Profile Pricing Structure

Key Features Market Strategy

• IBM offers its IBM Lotus Mobile Connect solution.

• IBM’s Lotus Mobile Connect works in conjuction with its other products, such as IBM Lotus Sametime software, Web Conferencing, IBM WebSphere Portal, IBM Lotus Notes, and IBM Lotus Expeditor.

• Pricing varies, depending on the number of users, feature sets and deal sizes.

• The pricing for the Lotus Mobile Connect is part of a total solution for IBM’s collaboration a solution. A server is typically $5,700 for 100 users. Client access is typically $100 per user.

• IBM includes its mobile connect solution as a feature to its other IBM Lotus products.

• IBM is a well-known security, software, and hardware solutions vendor that focuses on the enterprise segment, with more than 5,000 plus employees.

Source: Frost & Sullivan research.

Key features include: • Session Persistence• Data Optimization• Anytime, anywhere access to collaboration and

enterrpise applications• FIPS 140-2

73<N9B3-74>

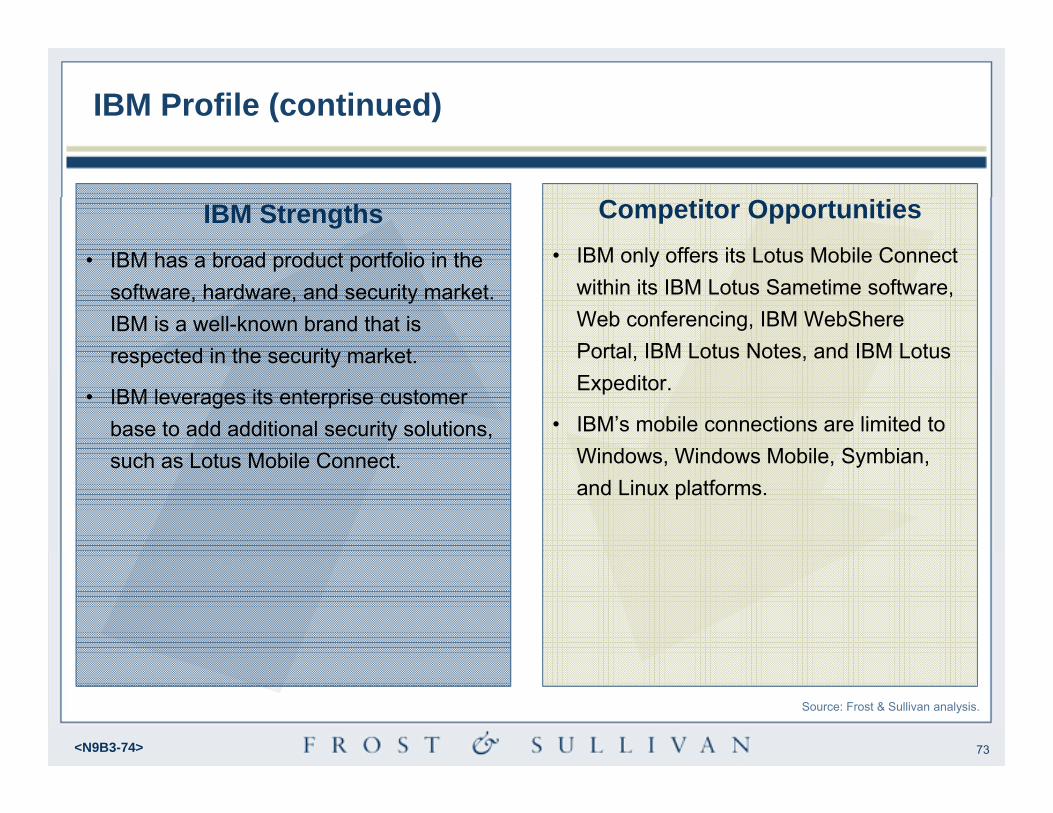

IBM Strengths• IBM has a broad product portfolio in the

software, hardware, and security market. IBM is a well-known brand that is respected in the security market.

• IBM leverages its enterprise customer base to add additional security solutions, such as Lotus Mobile Connect.

IBM Profile (continued)

Source: Frost & Sullivan analysis.

Competitor Opportunities• IBM only offers its Lotus Mobile Connect

within its IBM Lotus Sametime software, Web conferencing, IBM WebSherePortal, IBM Lotus Notes, and IBM Lotus Expeditor.

• IBM’s mobile connections are limited to Windows, Windows Mobile, Symbian, and Linux platforms.

74<N9B3-74>

Radio IP Profile

Product/Service Profile Pricing Structure

Key Features Market Strategy

• Radio IP offers two types of mobile VPN solutions, Radio IP MTG, ipUnplugged, and Mult IP.

• Radio IP MTG is tailored for the public safety (government) and utility sectors.

• Mult IP is focused other enterprises, such as the healthcare and financial sectors.

• Pricing varies, depending on the number of users , feature sets, and deal sizes.

• Estimated initial investment for 500 users: o $100,000 software licenses and one-year

maintenance supporto $200 per-user license

• Constant connectivity across multiple-IP and non-IP wireless networks

• Bandwidth Optimization

• FIPS 140-2 compliant

• Single sign on authentication

• Two-factor authentication

• Access Defender• Secure Guest Access

• Radio IP has focused on governement and utilites segments. The company purchased ipUnplugged in 2009 and is now slowly gaining traction in the enterprise market.

• Radio IP plans to strengthen its position by offering support to a broader number of mobile device platforms.

Source: Frost & Sullivan research.

75<N9B3-74>

Radio IP Strengths• Radio IP has experienced large

deployments in verticals, such as in the government and utilities segments.

• Radio IP’s solution offers seamless connectivity to legacy networks that may not be supported by other mobile VPN providers. In addition, the solutions have a solid group-policy management control system.

• Radio IP can work on Windows platforms, but plans exist for expanding to Windows Mobile and Android devices.

Radio IP Profile (continued)

Source: Frost & Sullivan analysis.

Competitor Opportunities• Radio IP is heavily distributed in North

America and has limited international presence.

• Radio IP acquired ipUnplugged to compliment Radio IP’s existing solution and to penetrate European markets, but the company lacks a strong brand name and reputation in the enterprise market.

76<N9B3-74>

Birdstep Technology Profile

Product/Service Profile Pricing Structure

Key Features Market Strategy

• Birdstep offers, SafeMove, a mobile VPN software

• Other software solutions within its profolio include:

o EasyConnect o SmartConnect

• Pricing varies, depending on the number of users, feature sets, and deal size

• Estimated initial investment for 500 users: o $100,000 software licenses and one-year

maintenance support o $200.00 per-user license

Key features include: • Network Access Control-like feature• FIPS 140-2 Encryption • Session persistence• Seamless roaming• Zero- Click connectivity • Data and VOIP optimization

• Birdstep has a strong direct channel though its partnerships.The company maintains strong partnerships with other companies, such as Ericsson and Cisco.

• Birstep continues to provide a strong innovative solution, along with a mulitude of platforms to support.

Source: Frost & Sullivan research.

77<N9B3-74>

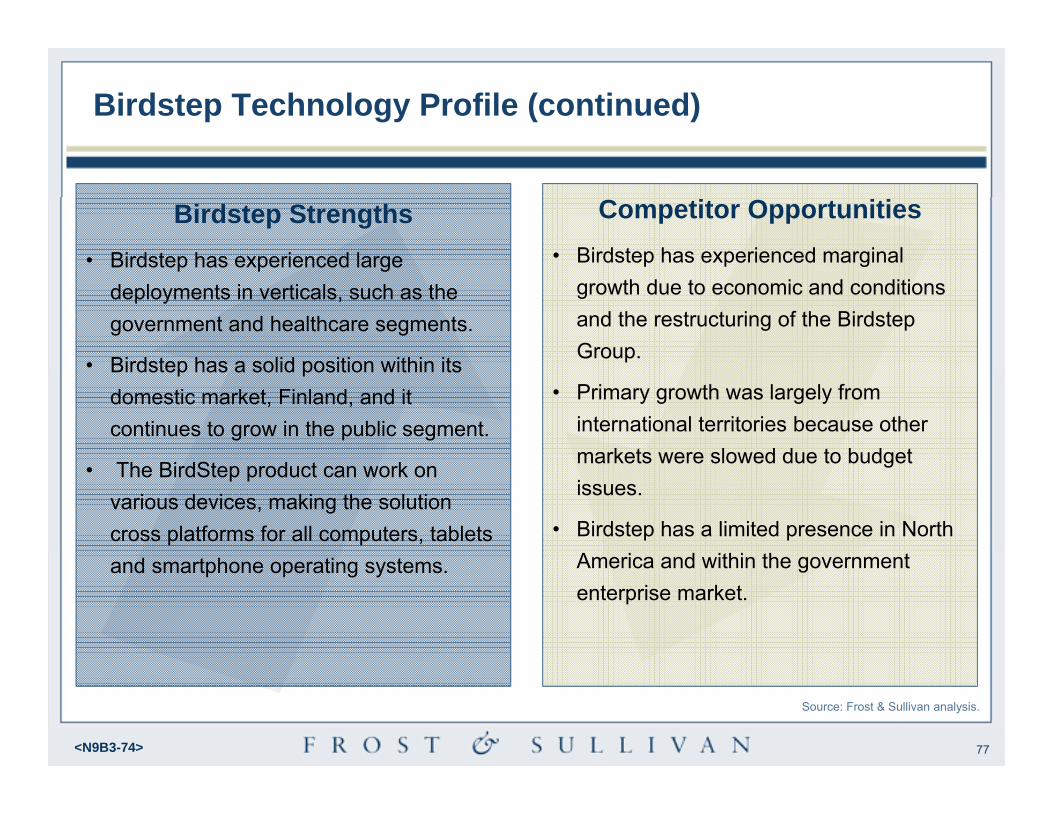

Birdstep Strengths• Birdstep has experienced large

deployments in verticals, such as the government and healthcare segments.

• Birdstep has a solid position within its domestic market, Finland, and it continues to grow in the public segment.

• The BirdStep product can work on various devices, making the solution cross platforms for all computers, tablets and smartphone operating systems.

Birdstep Technology Profile (continued)

Source: Frost & Sullivan analysis.

Competitor Opportunities• Birdstep has experienced marginal

growth due to economic and conditions and the restructuring of the BirdstepGroup.

• Primary growth was largely from international territories because other markets were slowed due to budget issues.

• Birdstep has a limited presence in North America and within the government enterprise market.

78<N9B3-74>

Cryptzone Profile

Product/Service Profile Pricing Structure

Key Features Market Strategy

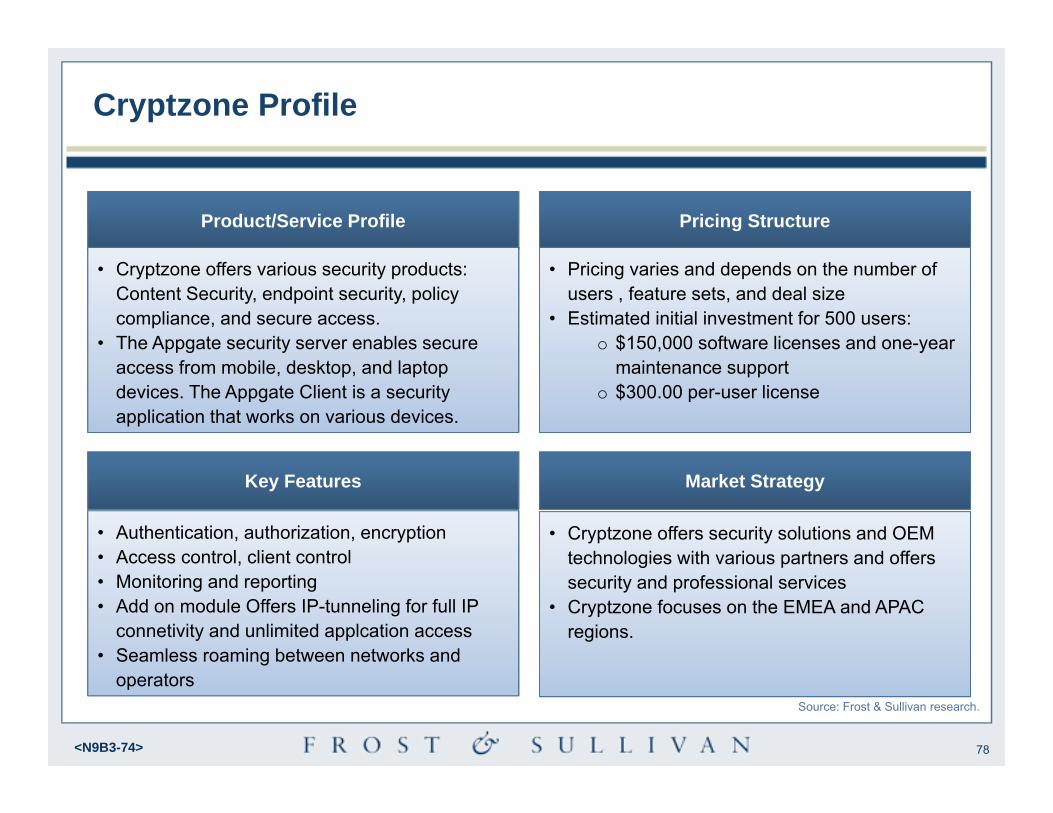

• Cryptzone offers various security products: Content Security, endpoint security, policy compliance, and secure access.

• The Appgate security server enables secure access from mobile, desktop, and laptop devices. The Appgate Client is a security application that works on various devices.

• Pricing varies and depends on the number of users , feature sets, and deal size

• Estimated initial investment for 500 users: o $150,000 software licenses and one-year

maintenance support o $300.00 per-user license

• Cryptzone offers security solutions and OEM technologies with various partners and offers security and professional services

• Cryptzone focuses on the EMEA and APAC regions.

Source: Frost & Sullivan research.

• Authentication, authorization, encryption• Access control, client control• Monitoring and reporting• Add on module Offers IP-tunneling for full IP

connetivity and unlimited applcation access• Seamless roaming between networks and

operators

79<N9B3-74>

Crtyptzone Strengths• Cryptzone has a broad product portfolio

in the network security market, offering more than just mobile VPN solutions.

• Cryptzone has a number of partners OEMing their technologies within the European market.

• The Cryptzone Appgate client includes a mobile VPN that will log the user on automatically when switching networks, and supports the Windows and Symbianplatform.

Cryptzone Profile (continued)

Source: Frost & Sullivan analysis.

Competitor Opportunities• Cryptzone has a limited presence in the

North American market.

• Cryptzone is not as well known as other security companies, such as Cisco or Juniper.

• The Cryptzone Appgate client needs to add support for Apple and Android devices in order to remain competitve.

80<N9B3-74>

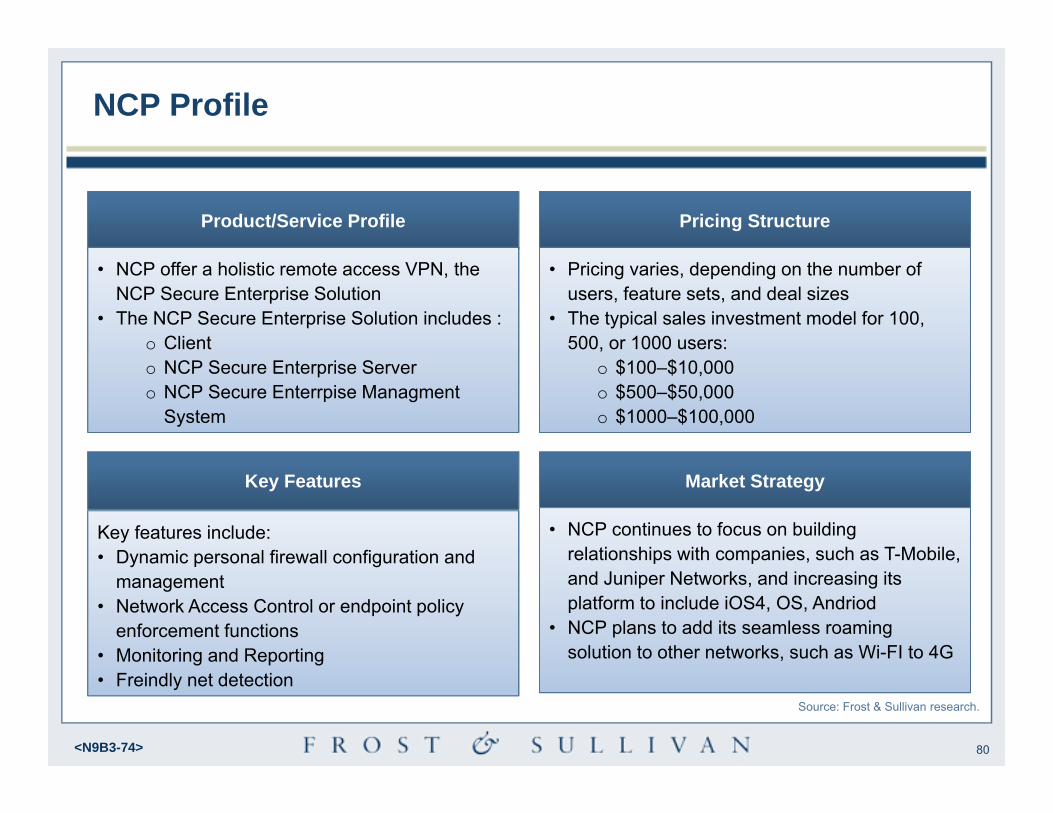

NCP Profile

Product/Service Profile Pricing Structure

Key Features Market Strategy

• NCP offer a holistic remote access VPN, the NCP Secure Enterprise Solution

• The NCP Secure Enterprise Solution includes :o Client o NCP Secure Enterprise Server o NCP Secure Enterrpise Managment

System

• Pricing varies, depending on the number of users, feature sets, and deal sizes

• The typical sales investment model for 100, 500, or 1000 users:

o $100–$10,000o $500–$50,000o $1000–$100,000

• NCP continues to focus on building relationships with companies, such as T-Mobile, and Juniper Networks, and increasing its platform to include iOS4, OS, Andriod

• NCP plans to add its seamless roaming solution to other networks, such as Wi-FI to 4G

Source: Frost & Sullivan research.

Key features include:• Dynamic personal firewall configuration and

management • Network Access Control or endpoint policy

enforcement functions• Monitoring and Reporting• Freindly net detection

81<N9B3-74>

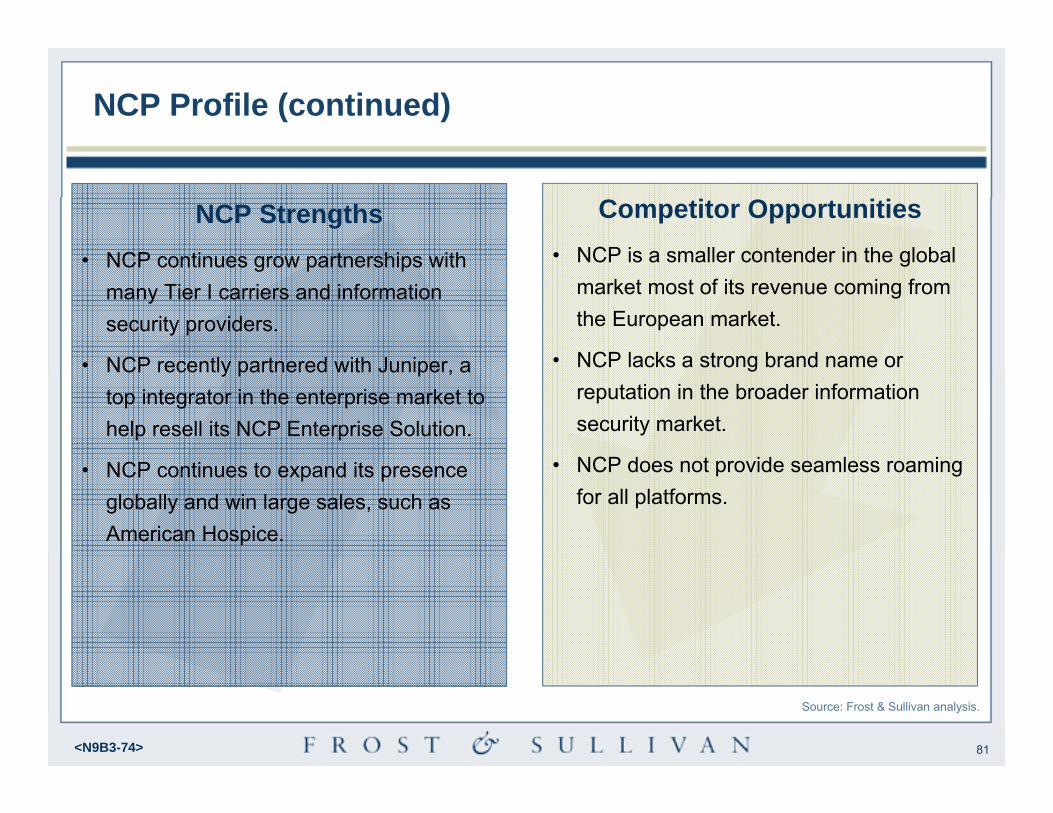

NCP Strengths• NCP continues grow partnerships with

many Tier I carriers and information security providers.

• NCP recently partnered with Juniper, a top integrator in the enterprise market to help resell its NCP Enterprise Solution.

• NCP continues to expand its presence globally and win large sales, such as American Hospice.

NCP Profile (continued)

Source: Frost & Sullivan analysis.

Competitor Opportunities• NCP is a smaller contender in the global

market most of its revenue coming from the European market.

• NCP lacks a strong brand name or reputation in the broader information security market.

• NCP does not provide seamless roaming for all platforms.

82<N9B3-74>

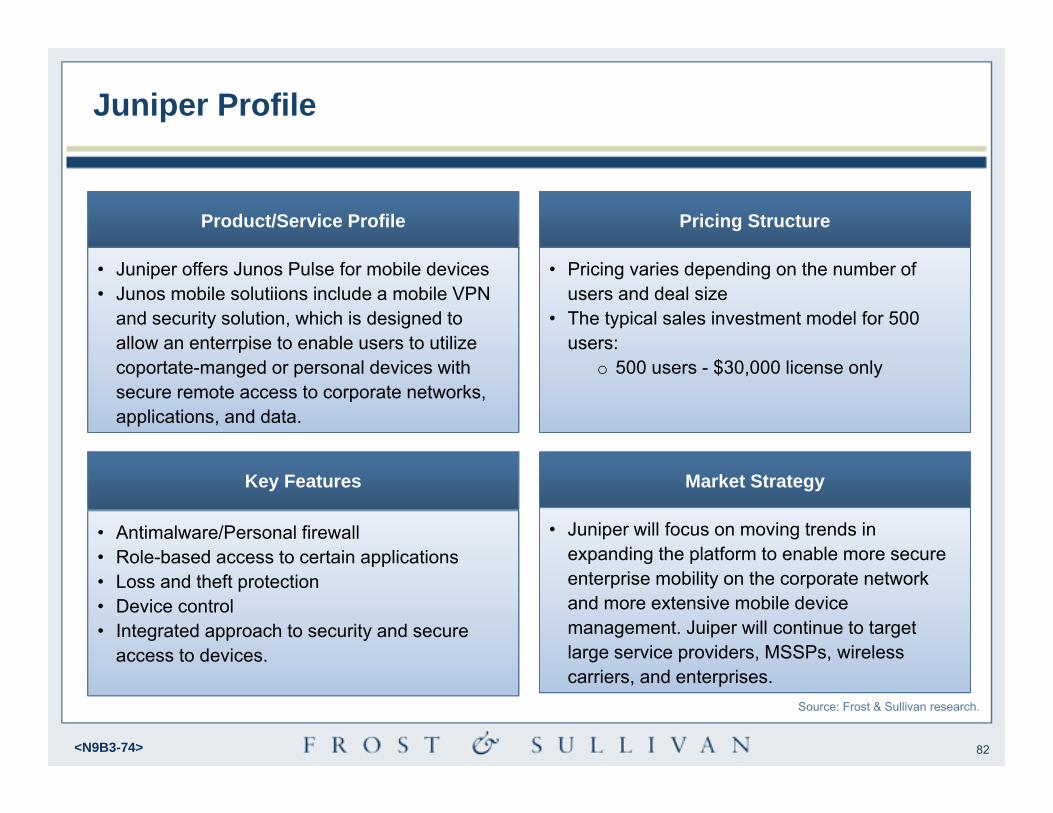

Juniper Profile

Product/Service Profile Pricing Structure

Key Features Market Strategy

• Juniper offers Junos Pulse for mobile devices • Junos mobile solutiions include a mobile VPN

and security solution, which is designed to allow an enterrpise to enable users to utilize coportate-manged or personal devices with secure remote access to corporate networks, applications, and data.

• Pricing varies depending on the number of users and deal size

• The typical sales investment model for 500 users:

o 500 users - $30,000 license only

• Juniper will focus on moving trends in expanding the platform to enable more secure enterprise mobility on the corporate network and more extensive mobile device management. Juiper will continue to target large service providers, MSSPs, wireless carriers, and enterprises.

Source: Frost & Sullivan research.

• Antimalware/Personal firewall • Role-based access to certain applications • Loss and theft protection • Device control • Integrated approach to security and secure

access to devices.

83<N9B3-74>

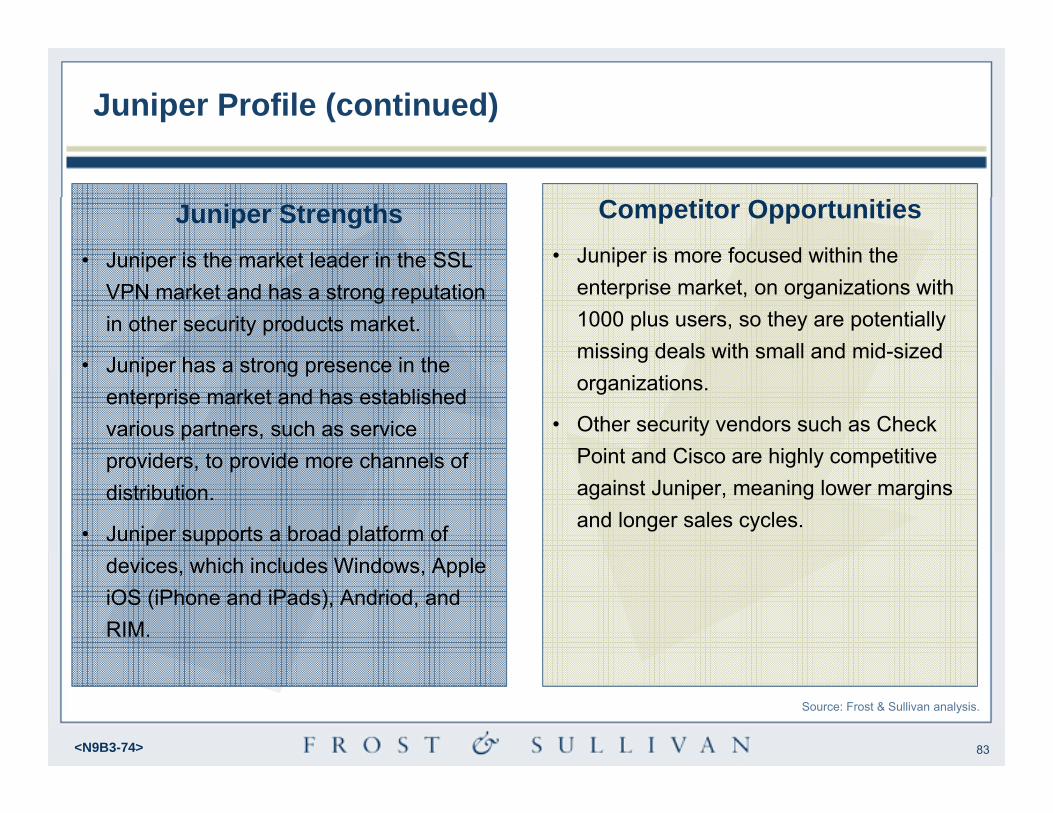

Competitor Opportunities• Juniper is more focused within the

enterprise market, on organizations with 1000 plus users, so they are potentially missing deals with small and mid-sized organizations.

• Other security vendors such as Check Point and Cisco are highly competitive against Juniper, meaning lower margins and longer sales cycles.

Juniper Strengths• Juniper is the market leader in the SSL

VPN market and has a strong reputation in other security products market.

• Juniper has a strong presence in the enterprise market and has established various partners, such as service providers, to provide more channels of distribution.

• Juniper supports a broad platform of devices, which includes Windows, Apple iOS (iPhone and iPads), Andriod, and RIM.

Juniper Profile (continued)

Source: Frost & Sullivan analysis.

84<N9B3-74>

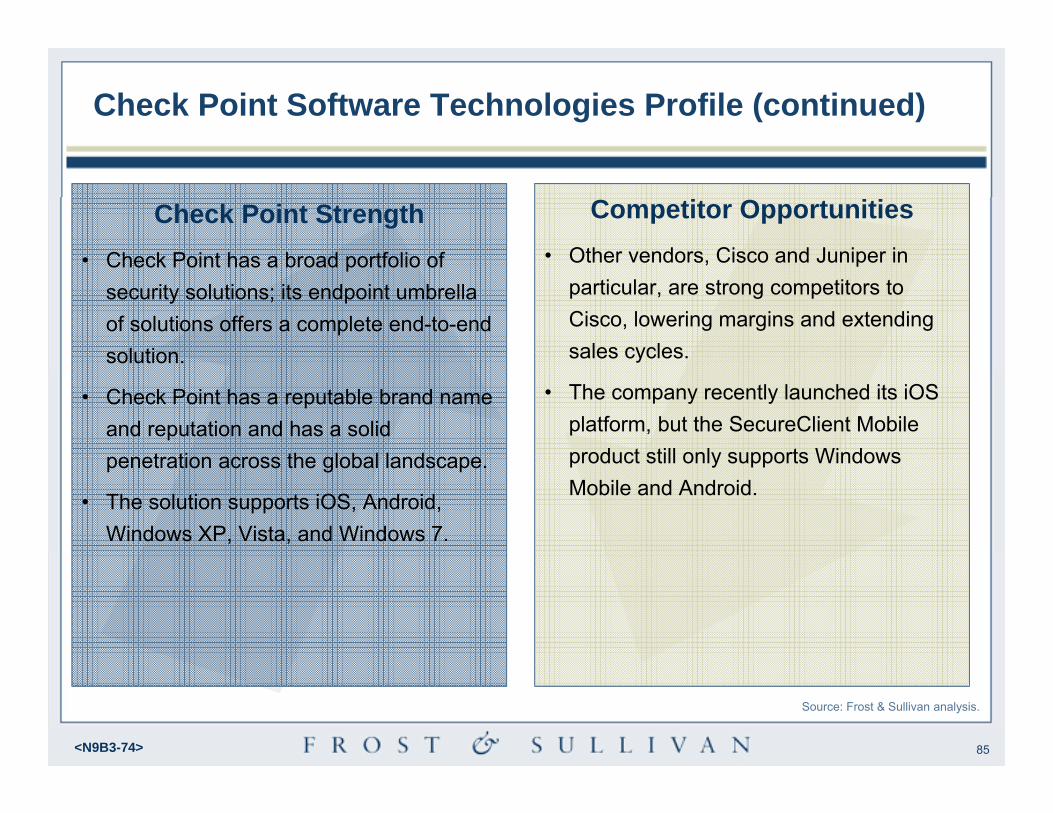

Check Point Software Technologies Profile

Product Profile Pricing Structure

Key Features Market Strategy

• As part of Check Point’s endpoint security portfolio, Check Point offers Mobile Access Software Blade

• The solution offers mobile VPN access to the corporate netwok email, and business applications

• Pricing varies, depending on the number of users and deal size

• The typical sales investment model for 1000 users:

o 1000 users is $40,000 license

• Check Point is 100 percent indirect channel and consists of various OEM partnerships.

• Most of the enterprise market is sold through Check Point, standard partners, and endpoint security solution providers.

Source: Frost & Sullivan research.

Key features include: • Personal firewall• Port control • Seamless roaming accross wireless networks• Managedment through SmartCenter and

Provider-1

85<N9B3-74>

Check Point Strength• Check Point has a broad portfolio of

security solutions; its endpoint umbrella of solutions offers a complete end-to-end solution.

• Check Point has a reputable brand name and reputation and has a solid penetration across the global landscape.

• The solution supports iOS, Android, Windows XP, Vista, and Windows 7.

Check Point Software Technologies Profile (continued)

Source: Frost & Sullivan analysis.

Competitor Opportunities• Other vendors, Cisco and Juniper in

particular, are strong competitors to Cisco, lowering margins and extending sales cycles.

• The company recently launched its iOSplatform, but the SecureClient Mobile product still only supports Windows Mobile and Android.

86<N9B3-74>

North America Breakdown

87<N9B3-74>

North America Breakdown

• North America refers to the United States and Canada.

• The North American region has the highest mobile VPN market revenue.

• Mobile VPN sales in North America accounted for 79.3 percent of the total market revenue.

• The higher market penetration of mobile VPN products could also be attributed to the number of large wireless carriers in the market.

Source: Frost & Sullivan analysis.

88<N9B3-74>

Note: All figures are rounded. The base year is 2010. Source: Frost & Sullivan analysis.

2007 2008 2009 2010 2011 2012 2013 2014 2015Revenue 72.1 87.7 104.9 126.9 152.5 180.8 214.8 252.2 294.1Units 353.6 438.6 535.5 660.4 809.8 979.8 1,187.8 1,423.3 1,693.9

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Uni

ts (1

,000

s)

Rev

enue

($ M

illio

n)

Year

Mobile VPN Products Market Unit Shipment and Revenue Forecast, North America,

2007-2015CAGR = 17.6%

North America Market Unit Shipment and Revenue Forecast

Key Takeaway: Revenue growth is fueled by new subscribers from 2009 to 2011.

89<N9B3-74>

North America Unit Shipment and Revenue Forecast Discussion

• The North American market remains the leading geography for mobile VPN sales. The North American market generated approximately $126.9 million in revenue and accounted for 79.3 percent of total sales in 2010.

• North America remains a key market for mobile VPN vendors because of the early adoption of North American organizations. In addition, higher market penetration is attributed to many large wireless carriers in the market.