ftac personal financial briefing · personal financial readiness appointments ... and retirement...

TRANSCRIPT

CONTENTS: SERVICES PROVIDED YOUR LES PAY TABLES FREE OIL CHANGE PERSONAL FINANCIAL READINESS APPOINTMENTS CREDIT REPORTS SERVICEMEMBERS CIVIL RIGHTS ACT THRIFT SAVINGS PLAN DOD SAVINGS DEPOSIT PLAN

FTAC Personal Financial Briefing

1000 Ellsworth Street Suite 1500 Ellsworth AFB, South Dakota 57706

Phone: 605-385-4663 Fax: 605-385-6322 www.ellsworthafrc.org www.facebook.com/ellsworthafrc www.twitter.com/ellsworthafrc

Version: June 2013

Airman & Family Readiness Center

What Financial Services are Provided at the Airman & Family Readiness Center?

Personal financial assessments and plans

Educational programs on financial issues

Investment and retirement education

Off-base housing assessments

Credit counseling advice and referrals

Home purchasing and car purchasing tutorials

All services are

free of charge to you!

http://ellsworthafrc.org

Why do we Offer These Services?

Air Force Instruction 36-2906 7.1 Military members will pay their just financial obligations in a proper and

timely manner 7.2 Will provide adequate financial support of a spouse or child or any other

relative for which the member receives additional allowances for support. Members will also comply with the financial support provisions of a court order or written support agreement.

7.3 Will comply with the requirements imposed by this instruction, including the

requirement to respond to applications for involuntary allotments of pay within suspense dates established by DFAS or the commander

7.4 Will comply with rules concerning the government travel charge card

program.

Disciplinary Actions and Consequences

Forfeiture of pay (7 days to one month)

60 days restriction

30 days arrest in quarters or correctional custody

Reduction in rank (E4-E1 max)

45 days extra duty Total Possible Financial penalty: $15,000 in lost income

Or

In these days of cutbacks, discharge from the Air Force

The Leave and Earning Statement (LES) Dilemma

1. Responsibility for the accuracy of your LES is yours!

2. Common pay problems that we see are:

Overpayment of BAH after moving on base BAS received while on meal card State income tax declaration is wrong Allotments don’t stop when requested Debt owed on travel cards/TDY Basic Pay is incorrect based upon rank

When in doubt, go to Finance – DON’T WAIT!

How to read an active duty Air Force Leave and Earning Statement

Your pay is your responsibility.

This is a guide to help you understand your Leave and Earnings Statement (LES). The LES is a comprehensive statement of a member's leave and earnings showing your entitlements, deductions, allotments (fields not used for Reserve and National Guard members), leave information, tax withholding information, and Thrift Savings Plan (TSP) information. Your most recent LES can be found 24 hours a day on myPay.

If members receive Career Sea Pay, the Sea Service Counter will still be displayed in the remark portion of the LES. The LES remains one page in length.

Verify and keep your LES each month. If your pay varies significantly and you don't understand why, or if you have any questions after reading this publication, consult with your disbursing/finance office.

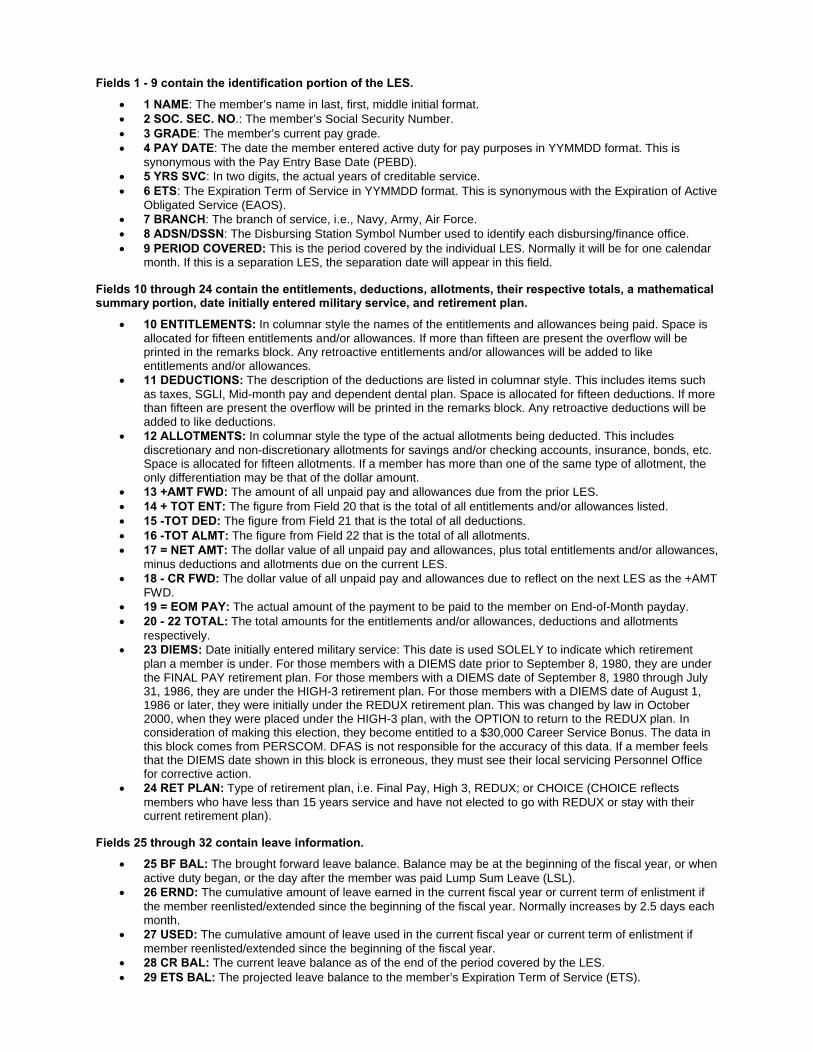

Fields 1 - 9 contain the identification portion of the LES.

1 NAME: The member’s name in last, first, middle initial format. 2 SOC. SEC. NO.: The member’s Social Security Number. 3 GRADE: The member’s current pay grade. 4 PAY DATE: The date the member entered active duty for pay purposes in YYMMDD format. This is

synonymous with the Pay Entry Base Date (PEBD). 5 YRS SVC: In two digits, the actual years of creditable service. 6 ETS: The Expiration Term of Service in YYMMDD format. This is synonymous with the Expiration of Active

Obligated Service (EAOS). 7 BRANCH: The branch of service, i.e., Navy, Army, Air Force. 8 ADSN/DSSN: The Disbursing Station Symbol Number used to identify each disbursing/finance office. 9 PERIOD COVERED: This is the period covered by the individual LES. Normally it will be for one calendar

month. If this is a separation LES, the separation date will appear in this field.

Fields 10 through 24 contain the entitlements, deductions, allotments, their respective totals, a mathematical summary portion, date initially entered military service, and retirement plan.

10 ENTITLEMENTS: In columnar style the names of the entitlements and allowances being paid. Space is allocated for fifteen entitlements and/or allowances. If more than fifteen are present the overflow will be printed in the remarks block. Any retroactive entitlements and/or allowances will be added to like entitlements and/or allowances.

11 DEDUCTIONS: The description of the deductions are listed in columnar style. This includes items such as taxes, SGLI, Mid-month pay and dependent dental plan. Space is allocated for fifteen deductions. If more than fifteen are present the overflow will be printed in the remarks block. Any retroactive deductions will be added to like deductions.

12 ALLOTMENTS: In columnar style the type of the actual allotments being deducted. This includes discretionary and non-discretionary allotments for savings and/or checking accounts, insurance, bonds, etc. Space is allocated for fifteen allotments. If a member has more than one of the same type of allotment, the only differentiation may be that of the dollar amount.

13 +AMT FWD: The amount of all unpaid pay and allowances due from the prior LES. 14 + TOT ENT: The figure from Field 20 that is the total of all entitlements and/or allowances listed. 15 -TOT DED: The figure from Field 21 that is the total of all deductions. 16 -TOT ALMT: The figure from Field 22 that is the total of all allotments. 17 = NET AMT: The dollar value of all unpaid pay and allowances, plus total entitlements and/or allowances,

minus deductions and allotments due on the current LES. 18 - CR FWD: The dollar value of all unpaid pay and allowances due to reflect on the next LES as the +AMT

FWD. 19 = EOM PAY: The actual amount of the payment to be paid to the member on End-of-Month payday. 20 - 22 TOTAL: The total amounts for the entitlements and/or allowances, deductions and allotments

respectively. 23 DIEMS: Date initially entered military service: This date is used SOLELY to indicate which retirement

plan a member is under. For those members with a DIEMS date prior to September 8, 1980, they are under the FINAL PAY retirement plan. For those members with a DIEMS date of September 8, 1980 through July 31, 1986, they are under the HIGH-3 retirement plan. For those members with a DIEMS date of August 1, 1986 or later, they were initially under the REDUX retirement plan. This was changed by law in October 2000, when they were placed under the HIGH-3 plan, with the OPTION to return to the REDUX plan. In consideration of making this election, they become entitled to a $30,000 Career Service Bonus. The data in this block comes from PERSCOM. DFAS is not responsible for the accuracy of this data. If a member feels that the DIEMS date shown in this block is erroneous, they must see their local servicing Personnel Office for corrective action.

24 RET PLAN: Type of retirement plan, i.e. Final Pay, High 3, REDUX; or CHOICE (CHOICE reflects members who have less than 15 years service and have not elected to go with REDUX or stay with their current retirement plan).

Fields 25 through 32 contain leave information.

25 BF BAL: The brought forward leave balance. Balance may be at the beginning of the fiscal year, or when active duty began, or the day after the member was paid Lump Sum Leave (LSL).

26 ERND: The cumulative amount of leave earned in the current fiscal year or current term of enlistment if the member reenlisted/extended since the beginning of the fiscal year. Normally increases by 2.5 days each month.

27 USED: The cumulative amount of leave used in the current fiscal year or current term of enlistment if member reenlisted/extended since the beginning of the fiscal year.

28 CR BAL: The current leave balance as of the end of the period covered by the LES. 29 ETS BAL: The projected leave balance to the member’s Expiration Term of Service (ETS).

30 LV LOST: The number of days of leave that has been lost. 31 LV PAID: The number of days of leave paid to date. 32 USE/LOSE: The projected number of days of leave that will be lost if not taken in the current fiscal year

on a monthly basis. The number of days of leave in this block will decrease with any leave usage.

Fields 33 through 38 contain Federal Tax withholding information.

33 WAGE PERIOD: The amount of money earned this LES period that is subject to Federal Income Tax Withholding (FITW).

34 WAGE YTD: The money earned year-to-date that is subject to FITW. Field 35 M/S. The marital status used to compute the FITW.

36 EX: The number of exemptions used to compute the FITW. 37 ADD’L TAX: The member specified additional dollar amount to be withheld in addition to the amount

computed by the Marital Status and Exemptions. 38 TAX YTD: The cumulative total of FITW withheld throughout the calendar year.

Fields 39 through 43 contain Federal Insurance Contributions Act (FICA) information.

39 WAGE PERIOD: The amount of money earned this LES period that is subject to FICA. 40 SOC WAGE YTD: The wages earned year-to-date that are subject to FICA. 41 SOC TAX YTD: Cumulative total of FICA withheld throughout the calendar year. 42 MED WAGE YTD: The wages earned year-to-date that are subject to Medicare. 43 MED TAX YTD: Cumulative total of Medicare taxes paid year-to-date.

Fields 44 through 49 contain State Tax information.

44 ST: The two digit postal abbreviation for the state the member elected. 45 WAGE PERIOD: The amount of money earned this LES period that is subject to State Income Tax

Withholding (SITW). 46 WAGE YTD: The money earned year-to-date that is subject to SITW. Field 47 M/S. The marital status

used to compute the SITW. 48 EX: The number of exemptions used to compute the SITW. 49 TAX YTD: The cumulative total of SITW withheld throughout the calendar year.

Fields 50 through 62 contain additional Pay Data.

50 BAQ TYPE: The type of Basic Allowance for Quarters being paid. 51 BAQ DEPN: A code that indicates the type of dependent. A - Spouse C -Child D - Parent G

Grandfathered I -Member married to member/own right K - Ward of the court L - Parents in Law R - Own right S - Student (age 21-22) T - Handicapped child over age 21 W - Member married to member, child under 21

52 VHA ZIP: The zip code used in the computation of Variable Housing Allowance (VHA) if entitlement exists.

53 RENT AMT: The amount of rent paid for housing if applicable. 54 SHARE: The number of people with which the member shares housing costs. 55 STAT: The VHA status; i.e., accompanied or unaccompanied. 56 JFTR: The Joint Federal Travel Regulation (JFTR) code based on the location of the member for Cost of

Living Allowance (COLA) purposes. 57 DEPNS: The number of dependents the member has for VHA purposes. 58 2D JFTR: The JFTR code based on the location of the member’s dependents for COLA purposes. 59 BAS TYPE: An alpha code that indicates the type of Basic Allowance for Subsistence (BAS) the member

is receiving, if applicable. This field will be blank for officers. o B - Separate Rations o C - TDY/PCS/Proceed Time o H - Rations-in-kind not available o K - Rations under emergency conditions

60 CHARITY YTD: The cumulative amount of charitable contributions for the calendar year. 61 TPC: This field is not used by the active component of any branch of service. 62 PACIDN: The activity Unit Identification Code (UIC). This field is currently used by Army only.

Fields 63 through 75 contain Thrift Savings Plan (TSP) information/data.

63 BASE PAY RATE: The percentage of base pay elected for TSP contributions. 64 BASE PAY CURRENT: Reserved for future use. 65 SPECIAL PAY RATE: The percentage of Specialty Pay elected for TSP

contribution.

66 SPECIAL PAY CURRENT: Reserved for future use. 67 INCENTIVE PAY RATE: Percentage of Incentive Pay elected for TSP contribution. 68 INCENTIVE PAY CURRENT: Reserved for future use. 69 BONUS PAY RATE: The percentage of Bonus Pay elected towards TSP contribution. 70 BONUS PAY CURRENT: Reserved for future use. 71 Reserved for future use. 72 TSP YTD DEDUCTION (TSP YEAR TO DATE DEDUCTION): Dollar amount of TSP contributions

deducted for the year. 73 DEFERRED: Total dollar amount of TSP contributions that are deferred for tax purposes. 74 EXEMPT: Dollar amount of TSP contributions that are reported as tax exempt to the Internal Revenue

Service (IRS). 75 Reserved for future use

76 REMARKS: This area is used to provide you with general notices from varying levels of command, as well as the literal explanation of starts, stops, and changes to pay items in the entries within the “ENTITLEMENTS”, “DEDUCTIONS”, and “ALLOTMENTS” fields.

77 YTD ENTITLE: The cumulative total of all entitlements for the calendar year.

78 YTD DEDUCT: The cumulative total of all deductions for the calendar year.

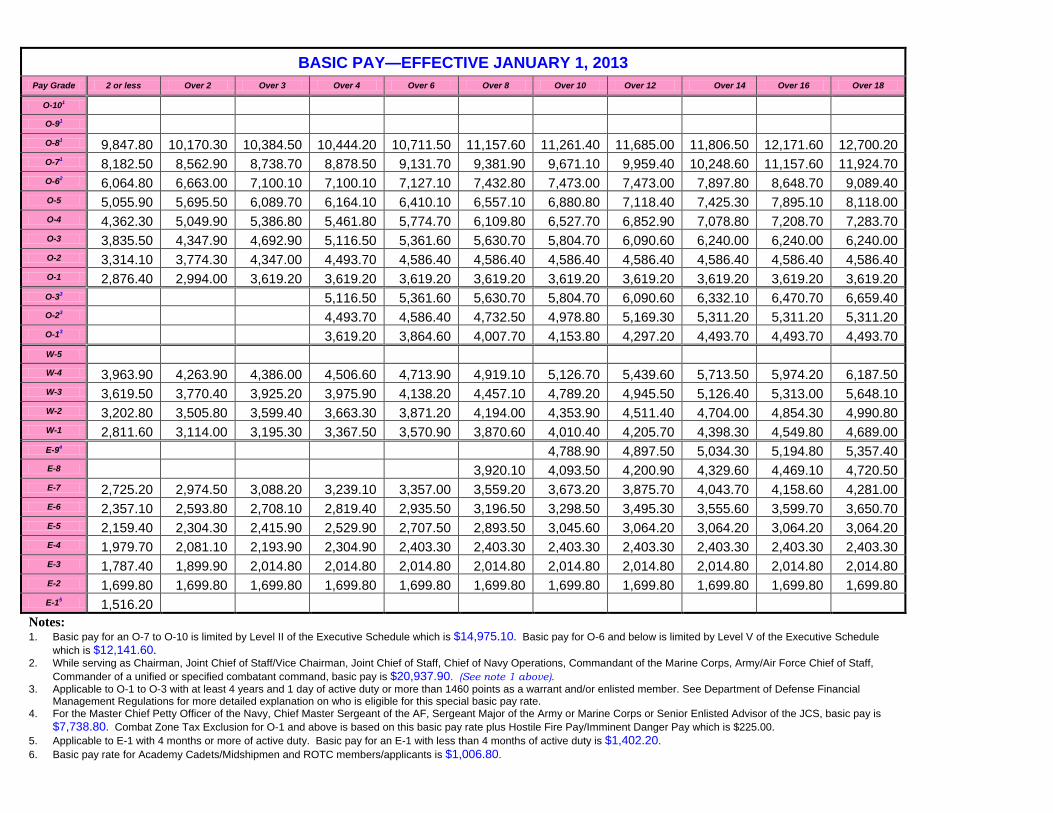

BASIC PAY—EFFECTIVE JANUARY 1, 2013 Pay Grade 2 or less Over 2 Over 3 Over 4 Over 6 Over 8 Over 10 Over 12 Over 14 Over 16 Over 18

O-101

O-91

O-81 9,847.80 10,170.30 10,384.50 10,444.20 10,711.50 11,157.60 11,261.40 11,685.00 11,806.50 12,171.60 12,700.20 O-71 8,182.50 8,562.90 8,738.70 8,878.50 9,131.70 9,381.90 9,671.10 9,959.40 10,248.60 11,157.60 11,924.70 O-62 6,064.80 6,663.00 7,100.10 7,100.10 7,127.10 7,432.80 7,473.00 7,473.00 7,897.80 8,648.70 9,089.40 O-5 5,055.90 5,695.50 6,089.70 6,164.10 6,410.10 6,557.10 6,880.80 7,118.40 7,425.30 7,895.10 8,118.00 O-4 4,362.30 5,049.90 5,386.80 5,461.80 5,774.70 6,109.80 6,527.70 6,852.90 7,078.80 7,208.70 7,283.70 O-3 3,835.50 4,347.90 4,692.90 5,116.50 5,361.60 5,630.70 5,804.70 6,090.60 6,240.00 6,240.00 6,240.00 O-2 3,314.10 3,774.30 4,347.00 4,493.70 4,586.40 4,586.40 4,586.40 4,586.40 4,586.40 4,586.40 4,586.40 O-1 2,876.40 2,994.00 3,619.20 3,619.20 3,619.20 3,619.20 3,619.20 3,619.20 3,619.20 3,619.20 3,619.20 O-33 5,116.50 5,361.60 5,630.70 5,804.70 6,090.60 6,332.10 6,470.70 6,659.40 O-23 4,493.70 4,586.40 4,732.50 4,978.80 5,169.30 5,311.20 5,311.20 5,311.20 O-13 3,619.20 3,864.60 4,007.70 4,153.80 4,297.20 4,493.70 4,493.70 4,493.70 W-5 W-4 3,963.90 4,263.90 4,386.00 4,506.60 4,713.90 4,919.10 5,126.70 5,439.60 5,713.50 5,974.20 6,187.50 W-3 3,619.50 3,770.40 3,925.20 3,975.90 4,138.20 4,457.10 4,789.20 4,945.50 5,126.40 5,313.00 5,648.10 W-2 3,202.80 3,505.80 3,599.40 3,663.30 3,871.20 4,194.00 4,353.90 4,511.40 4,704.00 4,854.30 4,990.80 W-1 2,811.60 3,114.00 3,195.30 3,367.50 3,570.90 3,870.60 4,010.40 4,205.70 4,398.30 4,549.80 4,689.00 E-94 4,788.90 4,897.50 5,034.30 5,194.80 5,357.40 E-8 3,920.10 4,093.50 4,200.90 4,329.60 4,469.10 4,720.50 E-7 2,725.20 2,974.50 3,088.20 3,239.10 3,357.00 3,559.20 3,673.20 3,875.70 4,043.70 4,158.60 4,281.00 E-6 2,357.10 2,593.80 2,708.10 2,819.40 2,935.50 3,196.50 3,298.50 3,495.30 3,555.60 3,599.70 3,650.70 E-5 2,159.40 2,304.30 2,415.90 2,529.90 2,707.50 2,893.50 3,045.60 3,064.20 3,064.20 3,064.20 3,064.20 E-4 1,979.70 2,081.10 2,193.90 2,304.90 2,403.30 2,403.30 2,403.30 2,403.30 2,403.30 2,403.30 2,403.30 E-3 1,787.40 1,899.90 2,014.80 2,014.80 2,014.80 2,014.80 2,014.80 2,014.80 2,014.80 2,014.80 2,014.80 E-2 1,699.80 1,699.80 1,699.80 1,699.80 1,699.80 1,699.80 1,699.80 1,699.80 1,699.80 1,699.80 1,699.80 E-15 1,516.20

Notes: 1. Basic pay for an O-7 to O-10 is limited by Level II of the Executive Schedule which is $14,975.10. Basic pay for O-6 and below is limited by Level V of the Executive Schedule

which is $12,141.60. 2. While serving as Chairman, Joint Chief of Staff/Vice Chairman, Joint Chief of Staff, Chief of Navy Operations, Commandant of the Marine Corps, Army/Air Force Chief of Staff,

Commander of a unified or specified combatant command, basic pay is $20,937.90. (See note 1 above). 3. Applicable to O-1 to O-3 with at least 4 years and 1 day of active duty or more than 1460 points as a warrant and/or enlisted member. See Department of Defense Financial

Management Regulations for more detailed explanation on who is eligible for this special basic pay rate. 4. For the Master Chief Petty Officer of the Navy, Chief Master Sergeant of the AF, Sergeant Major of the Army or Marine Corps or Senior Enlisted Advisor of the JCS, basic pay is

$7,738.80. Combat Zone Tax Exclusion for O-1 and above is based on this basic pay rate plus Hostile Fire Pay/Imminent Danger Pay which is $225.00. 5. Applicable to E-1 with 4 months or more of active duty. Basic pay for an E-1 with less than 4 months of active duty is $1,402.20. 6. Basic pay rate for Academy Cadets/Midshipmen and ROTC members/applicants is $1,006.80.

ALLOWANCES Basic Allowance for Housing RC/Transient

(January 1, 2013) Family Separation Allowance

Pay Grade Partial Without

Dependent With

Dependent Differential All Pay Grades: $250

0-10 $ 50.70 $ 1,481.70 $ 1,822.50 $ 330.30 Basic Allowance for Subsistence (Effective January 1, 2013)

Family Subsistence Supplemental Allowance (Effective October 1, 2010) 0-9 $ 50.70 $ 1,481.70 $ 1,822.50 $ 330.30

0-8 $ 50.70 $ 1,481.70 $ 1,822.50 $ 330.30 Officers: $242.60 All Pay Grades 0-7 $ 50.70 $ 1,481.70 $ 1,822.50 $ 330.30 Enlisted: $352.27 Not to Exceed $1100.00 0-6 $ 39.60 $ 1,358.70 $ 1,640.70 $ 273.60 Clothing Allowances (Effective October 1, 2012) 0-5 $ 33.00 $ 1,308.30 $ 1,581.60 $ 264.30 0-4 $ 26.70 $ 1,212.00 $ 1,394.10 $ 175.80 Standard Initial Clothing Allowance (Enlisted Members Only) 0-3 $ 22.20 $ 972.00 $ 1,153.50 $ 175.80 Army Navy Air Force Marine Corps 0-2 $ 17.70 $ 770.40 $ 984.30 $ 207.30 Male Female Male Female Male Female Male Female 0-1 $ 13.20 $ 660.90 $ 881.10 $ 224.10 1533.95 1756.94 1811.61 2031.69 1464.04 1667.36 1758.70 1803.50 03E $ 22.20 $ 1,049.10 $ 1,239.90 $ 184.20 Cash Clothing Replacement Allowance (Enlisted Members Only) 02E $ 17.70 $ 891.90 $ 1,118.70 $ 220.20 Army Navy Air Force Marine Corps OlE $ 13.20 $ 775.80 $ 1,034.10 $ 258.30 Male Female Male Female Male Female Male Female W-5 $ 25.20 $ 1,231.80 $ 1,346.40 $ 109.80 Basic 327.60 367.20 327.60 331.20 237.60 241.20 414.00 428.40 W-4 $ 25.20 $ 1,093.50 $ 1,233.90 $ 135.30 Standard 469.35 522.00 468.00 471.60 338.40 342.00 594.00 612.00 W-3 $ 20.70 $ 919.80 $ 1,131.30 $ 204.30 Special 0 0 640.80 630.00 0 0 0 0 W-2 $ 15.90 $ 816.00 $ 1,039.50 $ 216.00 Civilian Clothing Allowance W-1 $ 13.80 $ 684.30 $ 899.70 $ 209.10 Type of Duty Initial Replacement 15 days in 30 days period 30 days in 36 month period E-9 $ 18.60 $ 897.90 $ 1,184.10 $ 276.00 Permanent 970.56 323.52 0 0 E-8 $ 15.30 $ 825.00 $ 1,092.30 $ 258.60 Temporary 0 0 323.52 647.04 E-7 $ 12.00 $ 760.50 $ 1,013.70 $ 299.40 Personal Money Allowance (Monthly Amount) E-6 $ 9.90 $ 702.90 $ 936.60 $ 289.20 1. While serving as Chairman or Vice Chairman of the JCS,

or Army or Air Force CS, CNO, or CMC $333.33 E-5 $ 8.70 $ 632.10 $ 842.70 $ 246.30 E-4 $ 8.10 $ 549.60 $ 732.33 $ 213.00 2. Senior Member of the Military Staff Committee of the U.N. $225.00 E-3 $ 7.80 $ 511.20 $ 681.00 $ 174.30 3. General or Admiral $183.33 E-2 $ 7.20 $ 487.20 $ 649.20 $ 233.10 4. Lieutenant General Vice Admiral $41.67 E-1 $ 6.90 $ 487.20 $ 649.20 $ 276.00 5. Senior Enlisted Member of a Military Service $166.67 For other pays or specific requirements for the pay cited in this table, go to the web at: http://www.dtic.mil/comptroller/fmr/07a/index.html

INCENTIVE AND SPECIAL PAYS Aviation Career Incentive Pay

Years of Aviation Service 2 or less

Over 2 Over 3 Over 4 Over 6 Over 14 Over 22 Over 23 Over 24 Over 25

125.00 156.00 188.00 206.00 650.00 840.00 585.00 495.00 385.00 250.00 Career Enlisted Flyer Incentive Pay

Years of Aviation Service 4 or less Over 4 Over 8 Over 14 150.00 225.00 350.00 400.00

Hazardous Duty Incentive Pay (Crew Member- Non-AWAC) Pay Grade Amount Pay

Grade Amount Pay

Grade Amount Pay

Grade Amount Pay

Grade Amount

O-10 150.00 O-5 250.00 W-5 250.00 E-9 240.00 E-4 165.00 O-9 150.00 O-4 225.00 W-4 250.00 E-8 240.00 E-3 150.00 O-8 150.00 O-3 175.00 W-3 175.00 E-7 240.00 E-2 150.00 O-7 150.00 O-2 150.00 W-2 150.00 E-6 215.00 E-1 150.00 O-6 250.00 O-1 150.00 W-1 150.00 E-5 190.00

Hazardous Duty Incentive Pay (Non-Crew Member)

Imminent Danger Pay/Hostile Fire Pay

ALL GRADES – 150.00 ALL GRADES – 225.00

Diving Pay HDIP (Parachute, Flight Deck, Demolition, & Others)

Officers – 240.00 (Max) Enlisted – 340.00 (Max) All Grades – 150.00 (Member qualified for HALO Pay – 225.00).

COMBAT ZONE TAX EXCLUSION For other pays or specific requirements for the pays cited in

this table, go to the web at: http://www.dtic.mil/comptroller/fmr/07a/index.html

Basic pay for the MCPO of the Navy, CMSgt of the AF, Sergeant Major of the Army or Marine Corps, basic pay is $7,738.80. Combat Zone Tax Exclusion for O-1 and above is based on this basic pay rate plus HFP/IDP ($225).

E1 E2 E3 E4 E5 E6 E7 E8 E9

Full 759.00$ 759.00$ 759.00$ 759.00$ 852.00$ 951.00$ 1,041.00$ 1,152.00$ 1,230.00$

Partial 6.90$ 7.20$ 7.80$ 8.10$ 8.70$ 9.90$ 12.00$ 15.30$ 18.60$

WO1 WO2 WO3 WO4 WO5 O1E O2E O3E

Full 969.00$ 1,149.00$ 1,233.00$ 1,299.00$ 1,416.00$ 1,119.00$ 1,185.00$ 1,269.00$

Partial 13.80$ 15.90$ 20.70$ 25.20$ 25.20$ 13.20$ 17.70$ 22.20$

O1 O2 O3 O4 O5 O6 O7+

Full 900.00$ 1,083.00$ 1,236.00$ 1,401.00$ 1,476.00$ 1,596.00$ 1,629.00$

Partial 13.20$ 17.70$ 22.20$ 26.70$ 33.00$ 39.60$ 50.70$

E1 E2 E3 E4 E5 E6 E7 E8 E9

Full 1,011.00$ 1,011.00$ 1,011.00$ 1,011.00$ 1,119.00$ 1,269.00$ 1,386.00$ 1,515.00$ 1,638.00$

WO1 WO2 WO3 WO4 WO5 O1E O2E O3E

Full 1,272.00$ 1,440.00$ 1,596.00$ 1,653.00$ 1,719.00$ 1,413.00$ 1,575.00$ 1,665.00$

O1 O2 O3 O4 O5 O6 O7+

Full 1,137.00$ 1,266.00$ 1,590.00$ 1,746.00$ 1,854.00$ 1,872.00$ 1,890.00$

WITH DEPENDENTS

WITHOUT DEPENDENTS

MILITARY HOUSING AREA: (SD264) Ellsworth AFB, South Dakota 57706

2013 BAH RATES

Do you want a FREE Oil Change? Courtesy of the Air Force Aid Society

FTAC students can receive a FREE oil change by scheduling and completing a Personal Financial Readiness budget appointment with the Airman & Family Readiness Center. Once you have completed the appointment, you will receive a certificate for a FREE oil change at the Auto Repair Shop on Ellsworth AFB (Valued up to $50.00).

To schedule the appointment, follow the instructions on the next page by completing and sending the budget spreadsheet to [email protected].

If you don’t have a computer with Microsoft Excel to complete the spreadsheet, use the spreadsheet pages attached in this booklet to complete your budget and then send an email as directed above.

Please note to gather the required paperwork to bring to the appointment. Without the documents, we can’t complete a budget and the appointment will need to be rescheduled.

Ellsworth AFB Airman & Family Readiness Center 1000 Ellsworth Street, Ellsworth AFB, South Dakota 57706

Setting Up a Personal Financial Readiness Appointment

We're glad you have reached out for assistance!

To help you, we need to get a snapshot of where you are at.

Go to www.ellsworthafrc.org on the internet and click on the image of money that says “Set‐up a Personal Financial Appointment.”

Download the Budget Worksheet and save the spreadsheet to your computer. Save the file as your last name (for example: Smith.xls or Jones.xls).

Open the spreadsheet and complete it to the best of your ability. The worksheet should take no longer than 30 – 45 minutes to accomplish. You may need to review your bank statement to calculate your monthly ex‐penditures. Please don’t worry about having exact numbers; we need a starting point. Be sure to save the file after entering all your information.

Email the saved, completed spreadsheet, as an attachment, to this address: [email protected].

In your email, please be sure to state what your purpose of the appointment request is and let us know if you were referred to us by someone in your chain of command. In turn, we will get back with you to schedule you for an appointment.

Please allow at least 2 full business days for us to reply to your appointment request.

Please plan on bringing the following items to your appointment. We will need to see:

1. All copies of your: a. Bills b. Statements c. Contracts d. Loans e. Terms of agreement and disclosures for your cell phone, cable/satellite, internet, home phone, water, gas, electric, car payment, auto insurance, and all credit cards

2. Your last End of Month Leave and Earning Statement 3. Any other statements of family income 4. The last three bank statements for all accounts 5. If your bills are paid electronically, please download your statements/terms of agreements and

bring these with you to your appointment

Without these documents, we can't be much help to you, and the appointment will need to be rescheduled.

We look forward to assisting you!

Current $ Projected $ Due Date Current $ Projected $

Current $ Projected $

Current $ Projected $

Current $ Projected $

FICA-Soc Security 4.20%FICA-Medicare 1.45%

State Income Tax State: Due Date Current $ Projected $

Due Date Current $ Projected $

Current $ Projected $

Current $ Projected $

Child Support/Alimony

CLOTHING RELATED (Monthly)

Postage/Shipping

Entertainment Food (BBQ, Parties, etc.)

Fuel and Oil

Savings Other (House, Vacation, etc)Education FundInvestmentsNon-Service Retirement Plan

Self

Church Tithes/CharityVideos/DVDs (Including On-Line CDs/Music (Including On-Line Newspapers/Magazines

Tobacco Products

HaircutsBeauty Care

Pets

Checking/ATM FeesEntertainment (Movies, Bowling, Spending Money

GroceriesLunches (Self)Lunches (Spouse)Lunches (Children)Meals Out

Quick Stops (Coffee, Soda & Snacks)

Spouse Education (Books, Tuition, Fees, Gifts (Birthdays, Graduation, etc.)

Thrift Savings Plan (TSP)

House Repair/Yard Maintenance

Rent Payment

Pagers

TRANSPORTATION (Monthly)

Auto Insurance

Hobbies

PERSONAL (Monthly)

Alcoholic Beverages

Tolls/ParkingBus/Subway/Car PoolCar WashAuto Repairs

Child Toys, AllowanceAdditional Life Insurance

Home/Renters Insurance Second Mortgage PaymentMortgage Payment

Water

Storage

Spending Plan Financial Intake Worksheet

Hostile Fire Pay/Imminent Danger PayRefund Debt

Special Pay

Children

COLA

VA BenefitsRental Home IncomeMilitary Retirement PayOther Job Take Home PayJump PaySpouse Earnings (Net)

Sewer

Internet FeesTelevision/Cable/Satellite

Personal Digital Assistant (PDA)

Family Separation AllowanceForeign Language Proficiency Pay

SAVINGS / INVESTMENTS (Monthly)

HOUSING RELATED (Monthly)

LaundryDry Cleaning

Gas

Clothing Allowance

Flight Duty PayHazardous Duty Pay

ElectricityOHABAHBASBase Pay

FOOD (Monthly)

Cleaning Supplies

Cell PhoneTelephone Long DistanceTelephone Land LineGarbage

Advance Debt

Federal Income Tax Withheld (FITW)

Family Member (SGLI)

Emergency Funds

Interest/Dividends

Servicemembers Group Life Insurance (SGLI)

Montgomery GI BillAFRH (Air Force Retire Home)

Alterations

DEDUCTIONS (Monthly)

INCOME (Monthly)

Dependent DentalDebt DeductionMeal DeductionCombined Federal Campaign (CFC)Air Force Assistance Fund (AFAF)

Survivor Benefit PlanSocial Security Benefits

OTHER INCOME (Monthly)

Air Force Aid Loan Payment

CHILD CARE (Monthly) Due Date Current $ Projected $ Current $ Projected $

Child CareBabysitterSchool SuppliesSports Events/Activities

HEALTH (Monthly) Due Date Current $ Projected $

Medical Expense Current $ Projected $

Medical InsuranceDental ExpenseDental Insurance (other)Prescriptions/EquipmentVitamins/Supplements/HerbalGlasses/Contacts

CONSUMER DEBT Debt Name (Auto & Other Loans,

Credit Cards, etc.) Balance Remaining Due DateMinimum Payment $

Projected Payment $

OVERDUE PAYMENTS

Account NameDate of Last

PaymentMonths

Late

Vacation

Dues (Professional Org/Club)

SecuritiesVehiclesReal Estate

Debt Type:

Savings/Checking/CashBonds

Holiday GiftsONE-TIME / ANNUAL (Annually)

ASSET VALUE(S) (Total Values)

$ Needed to be current

Spending Plan Financial Intake Worksheet

Debt Type:Orig. Due

Date

License/Tax/Inspection (Auto, Boats, etc…)

Interest Rate

Personal PropertyLump Sum ExpectedThrift Savings Plan (TSP)

This central site allows you to request a FREE credit file disclosure, commonly called a credit report, once every 12 months from each of the

nationwide consumer credit reporting companies: Equifax, TransUnion and Experian.

NOTE: This does not provide you with a credit score, but shows what debt and accounts are associated with you.

AnnualCreditReport.com is the official site to help consumers to obtain their free credit report. If you use any other site, you may be subject to fees and other costs.

Sometimes, if you don’t have a long credit history, you may not be able to receive your credit report online. In this case you should request your credit report by mail using the form on the next page. Once you have completed the form, mail it to:

Annual Credit Report Request Service P.O. Box 105281 Atlanta, GA 30348-5281

If additional information is needed to process your request, the consumer creditreporting company will contact you by mail.

Your request will be processed within 15 days of receipt and then mailed to you.Copyright 2004, Central Source LLC

Equifax

ExperianTransUnion

I want a credit report from (shadeeach that you would like toreceive):

Shade here if, for securityreasons, you want your creditreport to include no more thanthe last four digits of yourSocial Security Number.

Shade Circle Like This >

Not Like This >

Social Security Number:

- -Date of Birth:

/ /Month Day Year

First Name M.I.

Last Name JR, SR, III, etc.

Current Mailing Address:

House Number Street Name

City State ZipCode

ZipCodeStateCity

Apartment Number / Private Mailbox For Puerto Rico Only: Print Urbanization Name

Street NameHouse Number

Previous Mailing Address (complete only if at current mailing address for less than two years):

Fold HereFold Here

Fold HereFold Here

For Puerto Rico Only: Print Urbanization NameApartment Number / Private Mailbox

You have the right to get a free copy of your credit file disclosure, commonly called a credit report, once every 12 months, from each ofthe nationwide consumer credit reporting companies, Equifax, Experian and TransUnion.For instant access to your free credit report, visit www.annualcreditreport.com.

For more information on obtaining your free credit report, visit www.annualcreditreport.com or call 877-322-8228.Use this form if you prefer to write to request your credit report from any, or all, of the nationwide consumer credit reporting companies. The

following information is required to process your request. Omission of any information may delay your request.

Annual Credit Report Request Form

Once complete, fold (do not staple or tape), place into a #10 envelope, affix required postage and mail to: Annual Credit Report Request Service P.O. Box 105281 Atlanta, GA 30348-5281.

Please use a Black or Blue Pen and write your responses in PRINTED CAPITAL LETTERS without touching the sides of the boxes like the examples listed below:

31238

SERVICEMEMBERS CIVIL RELIEF ACT

The Servicemembers Civil Relief Act (SCRA) helps those who have dropped their affairs to answer

their nation’s call and alleviates some of the stress placed on their families. It allows Servicemembers to

suspend or postpone certain civil obligations so they can devote their full attention to their military

duties.

SCRA benefits include the following:

Caps on interest rates

Tax reliefs

Temporary relief from mortgage payments

Termination of residential and automobile leases

Protection from eviction

Stay of judicial proceedings

The SCRA offers protection to the following:

Active duty Servicemembers in all branches of service

Reservists and National Guard Members in active federal Service

Dependents of Servicemembers in active duty (some benefits only)

SCRA RIGHTS AND BENEFITS

The SCRA provides eligible Servicemembers with a variety of rights and benefits, including (but not

limited to) the ones listed in this section. For more information, contact your local Armed Forces Legal

Assistance (AFLA) office.

A 6% Cap on Interest Rates

If the Service affects your ability to meet obligations you had before entering active duty, you can cap

their interest rate at 6%:

The interest rate cap starts on the first day of active duty and lasts for the duration of Service.

The cap can apply to credit cards, mortgages and student loans (excluding Federal Guaranteed

Student Loans).

The excess interest will not be due after your release from active duty. The portion above 6% is

permanently settled.

Your monthly payment must be reduced by the amount of interest saved during the covered

period.

To qualify for the 6% cap, you must demonstrate the following:

You are now on active duty.

The obligation or debt was made prior to entering active duty.

Military Service significantly affects your ability to make payments.

You must provide creditors with a written notice requesting relief under the SCRA and a copy of your

orders showing the date you entered active duty. See the next page for a sample letter to your creditor

requesting reduction of your interest rate.

Residential Lease Termination

You have the right to terminate a housing lease when you receive Permanent Change of Station (PCS)

orders or when you are deployed to a new location for 90 days or more. To qualify, you or your

dependents must occupy the house.

Termination occurs 30 days after the next rental payment’s due date. You must provide the landlord

with written notice and a copy of your orders.

Motor Vehicle Leases

If you are called to active duty for 180 days or more, you can terminate an automobile lease signed

before Service without legal repercussions.

You can also terminate an automobile lease signed during Service if you can demonstrate any of the

following:

You are deployed for 180 days or more.

You have received PCS orders relocating you outside of the Continental U.S.

Source: http://www.benefits.va.gov/homeloans/scraqb.asp

SAMPLE LETTER

Date

Name of Creditor Address City, State Zip RE: Your name as it appears on your statement, account number. Dear Sir or Madam: This letter is to advise you that I have been ordered to active duty service with the United States Armed Forces. As a result of my military service, I have lost my civilian employment income. I incurred the above referenced debt prior to entry on active duty. My entry into military service has substantially affected my ability to make the payments that I agreed to make while a civilian. I entered active duty on ______________ (date), and am presently on active duty assigned to _________________________ (unit), The Servicemembers Civil Relief Act of 2003, 50 U.S.C. Appendix, Section 527, sets a six percent (6%) per annum ceiling on interest charges (including service charges, renewal charges and fees) during the period of a servicemember’s military service for obligations made prior to the date of entry onto active duty when the active duty materially affect the ability to pay. Since entering active duty, I have experienced a decrease in salary, adversely affecting my ability to pay. Thus I am requesting an adjustment of this account to reflect the statutory six percent (6%) rate. This rate became effective upon my entry to active duty on _______________ (date). Please ensure that your records reflect this statutory ceiling and that any excess charge is withdrawn. The interest over 6% must be forgiven, not just deferred and my monthly payments must be reduced by the reduction in the interest rate. Please contact me at _______________________ (phone or address) with a revised payment schedule. Thank you for your understanding and support in this matter. Sincerely, Your Name Rank, Branch of Service

** Be sure to enclose a copy of your current leave and earnings statement and a copy of your orders that (1) brought you from civilian life to boot camp or

(2) activated you as a reservist or guard member. **

TSP Fund Comparison Matrix

The chart below provides a comparison of the available TSP funds.

G Fund F Fund* C Fund* S Fund* I Fund* L Funds**

Description of Investments

Government securities (specially issued to the TSP)

Government, corporate, and mortgage-backed bonds

Stocks of large and medium-sized U.S. companies

Stocks of small to medium-sized U.S. companies (not included in the C Fund)

International stocks of 21 developed countries

Invested in the G, F, C, S, and I Funds

Objective of Fund

Interest income without risk of loss of principal

To match the performance of the Barclays Capital U.S. Aggregate Bond Index

To match the performance of the Standard & Poor's 500 (S&P 500) Index

To match the performance of the Dow Jones U.S. Completion TSM Index

To match the performance of the Morgan Stanley Capital International EAFE (Europe, Australasia, Far East) Index

To provide professionally diversified portfolios based on various time horizons, using the G, F, C, S, and I Funds

Risk Inflation risk

Market risk, Credit risk, Prepayment risk, Inflation risk

Market risk, Inflation risk

Market risk, Inflation risk

Market risk, Currency risk, Inflation risk

Exposed to all of the types of risk to which the individual TSP funds are exposed - but total risk is reduced through diversification among the five individual funds

Volatility Low Low to moderate

Moderate

Moderate to high — historically more volatile than C Fund

Moderate to high — historically more volatile than C Fund

Asset allocation shifts as time horizon approaches to reduce volatility

Types of Earnings***

Interest

Change in market prices Interest

Change in market prices Dividends

Change in market prices Dividends

Change in market prices Change in relative value of currency Dividends

Composite of earnings in the underlying funds

2012 Administrative Expenses****

0.027% 0.027% 0.027% 0.027% 0.027% 0.027%

Inception Date 04/01/87 01/29/88 01/29/88 05/01/01 05/01/01 08/01/05

* The F, C, S, and I Funds also have earnings from securities lending income and from temporary investments in G Fund securities. These amounts represent a very small portion of total earnings.

** Each of the L Funds is invested in the individual TSP funds (G, F, C, S, and I). The proportion of your L Fund balance invested in each of the individual TSP funds depends on the L Fund you choose.

*** Income from interest and dividends is included in the share price calculation. It is not paid directly to participants' accounts.

**** Expenses are offset by the forfeitures of Agency Automatic (1%) contributions of FERS employees who leave Federal Service before they are vested, other forfeitures, and loan fees.

Source: www.tsp.gov

TSP Summary of Returns

Average Annual Returns (As of December 2012)

L

Income L 2020 L 2030 L 2040 L 2050 G Fund F Fund C Fund S Fund I Fund

1-Year 4.77% 10.42% 12.61% 14.27% 15.85% 1.47% 4.29% 16.07% 18.57% 18.62%

3-Year 4.24% 7.03% 8.09% 8.83% - 2.24% 6.29% 10.90% 13.92% 4.13%

5-Year 3.14% 2.44% 2.32% 2.01% - 2.69% 6.06% 1.71% 4.22% (3.30%)

10-Year - - - - - 3.61% 5.25% 7.12% 10.79% 8.39%

Since Inception 4.17% 4.82% 4.95% 5.00% 5.81% 5.69% 7.01% 9.50% 7.12% 4.06%

Inception Date 08/01/05 08/01/05 08/01/05 08/01/05 01/31/11 04/01/87 01/29/88 01/29/88 05/01/01 05/01/01

Calendar Year Returns

L

Income L 2020 L 2030 L 2040 L 2050 G Fund F Fund C Fund S Fund I Fund

2008 (5.09%) (22.77%) (27.50%) (31.53%) - 3.75% 5.45% (36.99%) (38.32%) (42.43%)

2009 8.57% 19.14% 22.48% 25.19% - 2.97% 5.99% 26.68% 34.85% 30.04%

2010 5.74% 10.59% 12.48% 13.89% - 2.81% 6.71% 15.06% 29.06% 7.94%

2011 2.23% 0.41% (0.31%) (0.96%) - 2.45% 7.89% 2.11% (3.38%) (11.81%)

2012 4.77% 10.42% 12.61% 14.27% 15.85% 1.47% 4.29% 16.07% 18.57% 18.62%

YTD 2.99% 7.00% 8.77% 10.08% 11.27% 0.62% (0.76%) 15.38% 16.91% 6.46%

Monthly Returns (Past 12 Months)

L

Income L 2020 L 2030 L 2040 L 2050 G Fund F Fund C Fund S Fund I Fund

2012

Jun 1.04% 2.72% 3.32% 3.77% 4.27% 0.11% 0.05% 4.13% 3.25% 7.08%

Jul 0.37% 0.63% 0.71% 0.75% 0.78% 0.12% 1.38% 1.40% (0.62%) 0.56%

Aug 0.63% 1.57% 1.94% 2.23% 2.51% 0.11% 0.07% 2.25% 3.57% 3.29%

Sep 0.62% 1.52% 1.87% 2.12% 2.38% 0.10% 0.15% 2.57% 2.51% 2.96%

Oct (0.11%) (0.45%) (0.60%) (0.71%) (0.80%) 0.12% 0.20% (1.86%) (1.31%) 0.85%

Nov 0.34% 0.77% 0.93% 1.06% 1.19% 0.11% 0.16% 0.57% 1.53% 2.41%

Dec 0.47% 1.19% 1.48% 1.69% 1.93% 0.12% (0.13%) 0.91% 2.69% 4.02%

2013

Jan 1.10% 2.83% 3.56% 4.11% 4.63% 0.13% (0.56%) 5.18% 6.96% 4.45%

Feb 0.27% 0.41% 0.49% 0.54% 0.56% 0.13% 0.51% 1.36% 1.00% (0.99%)

Mar 0.73% 1.69% 2.12% 2.44% 2.71% 0.13% 0.07% 3.75% 4.69% 0.88%

Apr 0.67% 1.58% 1.91% 2.13% 2.41% 0.12% 1.02% 1.93% 0.65% 5.32%

May 0.19% 0.33% 0.43% 0.51% 0.53% 0.12% (1.78%) 2.34% 2.71% (3.12%)

Last 12 mo 6.50% 15.78% 19.66% 22.59% 25.56% 1.41% 1.11% 27.26% 31.05% 30.96%

Percentages in ( ) are negative.

Source: www.tsp.gov

FEDERAL RETIREMENT THRIFT INVESTMENT BOARD 77 K Street, NE Washington, DC 20002

FOR IMMEDIATE RELEASE April 11, 2012

FEDERAL RETIREMENT THRIFT INVESTMENT BOARD ANNOUNCES

THE LAUNCH DATE FOR NEW ROTH TSP OPTION

Washington, D.C. -- The Federal Retirement Thrift Investment Board announced today at its quarterly inter-agency meeting of Thrift Savings Plan (TSP) coordinators that May 7, 2012 will be the day that the TSP will begin to accept Roth TSP contributions. The Roth TSP was authorized by the Thrift Savings Plan Enhancement Act of 2009, which was enacted on June 22, 2009, and will allow Federal civilian employees and members of the uniformed services to contribute after-tax dollars into the TSP for the first time. Both the contributions and their earnings will be tax-free when withdrawn, as long as IRS requirements are met. According to Greg Long, Executive Director of the Agency, “the Roth TSP option offers an important new tool for Federal civilian employees and uniformed service members in managing their retirement income by providing greater flexibility in the tax treatment of contributions now and in the future.” Long noted that the Agency will continue to provide participants and agencies with educational materials to help them understand this new option but, as with all tax matters, participants should seek the advice of their qualified tax or financial advisers for answers to questions pertaining to their specific tax situation. The Agency has been sharing Roth TSP planning bulletins with agency and service payroll and personnel representatives since December 2010 to provide them with the information they require to be able to program their payroll systems to accept and transmit pre-tax and after-tax money. The Agency is aware that not all agencies or services have completed the technical and programmatic modifications of their payroll systems required to

implement Roth TSP. These agencies or services will require additional time to modify their payroll systems and will be able to begin participation in Roth as soon after May 5, 2012 as they are able. With the addition of the Roth TSP option, participants can choose to invest pre-tax or after-tax dollars in any of the TSP funds, up to the Internal Revenue Code limits. TSP participants can currently invest in ten different funds: the five Lifecycle (L) Funds, the Government Securities (G) Fund, and the four broadly diversified stock and bond funds – the Fixed Income Index Investment (F) Fund, the Common Stock Index Investment (C) Fund, the Small Capitalization Index Investment (S) Fund, the International Stock Index Investment (I) Fund. The TSP is a retirement savings plan for Federal employees; it is similar to the 401(k) plans offered by many private employers. As of March 2012, TSP assets totaled approximately $308 billion, and retirement savings accounts were being maintained for roughly 4.5 million TSP participants. Participants include Federal civilian employees in all branches of Government, employees of the U.S. Postal Service, and members of the uniformed services. Additional information can be found at www.tsp.gov. MEDIA CONTACT: Kim Weaver 202-942-1640

(end)

January/February 2012

IGHLIGHTSH Thrift Savings Plan

(Continued on back)

TSP Website: ThriftLine: 1-TSP-YOU-FRST (1-877-968-3778) TDD: 1-TSP-THRIFT5 www.tsp.gov Outside the U.S. and Canada: 404-233-4400 (1-877-847-4385)

3 3 3

Is Roth for You?The TSP will introduce a feature later this year that will allow active participants to make Roth contributions to their TSP accounts. This new feature will allow you to contribute some or all of your contributions to the Roth TSP. With Roth contributions, you pay taxes now. However, when you withdraw these contributions and their earnings, you will not have to pay taxes on them as long as you are 59½ or older and you have had Roth contribu-tions for five years or more when you receive your distribution.

As we get closer to the date when you can start making Roth contributions, you’ll learn more about this new feature on the TSP website. In the meantime, you may want to start thinking about whether Roth contributions could be to your advantage.

Comparison of Traditional (Pre-tax) and Roth (After-tax) Contributions

2011 TSP Expense RatioThe expense ratio is the amount by which each TSP account is reduced to cover administrative expenses. Fol-lowing are the expense ratios for 2011:

G Fund: .025% F Fund: .024% C Fund: .025% S Fund: .025% I Fund: .025% L Funds: .025%

.025% is equivalent to 2.5 basis points, or 25¢ for every $1,000 in your account.

This pays for:

• managementfees;

• operatingandmaintain-ing the TSP’s record keep-ingsystem;

• providingparticipantservices;and

• printingandmailingnotices, statements, and publications.

Expenses are offset by the forfeitures of Agency Auto-matic (1%) Contributions of FERS employees who leave Federal service before they are vested, other forfeitures, and loan fees.

The Treatment of . . . Traditional TSP Roth TSP

Contributions Pre-tax After-tax1

Your Paycheck Taxes are deferred, so less money is taken out of your paycheck.

Taxes are paid up front, so more money comes out of your paycheck.

Transfers In Transfers allowed from eligible em-ployer plans and traditional IRAs

Transfers allowed from Roth 401(k)s, Roth 403(b)s, and Roth 457(b)s

Transfers Out Transfers allowed to eligible employer plans, traditional IRAs, and Roth IRAs2

Transfers allowed to Roth 401(k)s, Roth 403(b)s, Roth 457(b)s, and Roth IRAs3

Withdrawals Taxable when withdrawn Tax-free earnings if five years have passed since January 1 of the year you made your first Roth contribution, AND you are age 59½ or older, permanently disabled, or deceased

1 Roth contributions are subject to Federal (and, where applicable, state and local) income taxes, while traditional contributions are not taxed until withdrawn. However, both Roth contributions and traditional contributions are included in the amount of wages used to calcu- late payroll taxes (e.g., Social Security taxes). 2 You would have to pay taxes on any pre-tax amount transferred to a Roth IRA. 3 Transfers to a Roth IRA from a Roth TSP are not subject to the income restrictions that apply to Roth IRA contributions.

How should you decide? It all comes down to whether you would be better off paying your taxes now or later (i.e., your marginal tax rate now versus your rate at retirement). Your personal situation will determine whether it is better to have the tax savings of traditional TSP now or the tax-free earnings of Roth TSP later. As you make your Roth decision, think about your income level and tax rate now and what you expect they will be when you retire.

Rates of ReturnL

2050L

2040L

2030L

2020L

IncomeG

FundF

FundC

FundS

FundI

Fund

Monthly 2011

Jan Feb Mar Apr May June July Aug Sept Oct Nov Dec

– 3.28 – 0.15 3.57 – 1.39 – 1.48 – 1.75 – 6.16 – 7.80 9.92 – 0.78 – 0.01

1.75% 2.95 – 0.08 3.20 – 1.15 – 1.30 – 1.49 – 5.37 – 6.85 8.83 – 0.62 0.07

1.57% 2.60 – 0.05 2.83 – 0.97 – 1.10 – 1.25 – 4.63 – 5.92 7.68 – 0.49 0.09

1.35% 2.15 – 0.03 2.37 – 0.74 – 0.84 – 0.94 – 3.69 – 4.73 6.18 – 0.34 0.11

0.63% 0.90 0.17 1.01 – 0.05 – 0.18 – 0.14 – 1.10 – 1.51 2.31 0.02 0.20

0.24% 0.22 0.26 0.25 0.25 0.21 0.22 0.19 0.16 0.14 0.14 0.15

0.13% 0.26 0.06 1.28 1.31 – 0.30 1.59 1.45 0.73 0.11 0.01 1.01

2.37% 3.42 0.04 2.96 – 1.13 – 1.67 – 2.04 – 5.44 – 7.03 10.93 – 0.21 1.04

1.23% 4.52 2.06 2.94 – 1.27 – 2.35 – 3.14 – 8.12 – 10.73 14.09 – 0.51 – 0.04

2.41% 3.33 – 2.23 6.03 – 2.90 – 1.16 – 1.60 – 9.03 – 10.55 9.48 – 2.46 – 2.03

Annual 2002 – 2011

20022003200420052006 2007 20082009 2010 2011

– – – – – – – – – –

––––

16.53 7.36 – 31.53 25.19 13.89 – 0.96

– – – – 15.00 7.14 – 27.50 22.48 12.48 – 0.31

––––

13.72 6.87 – 22.77 19.14 10.59 0.41

––––

7.59 5.56– 5.09

8.57 5.74 2.23

5.00%4.11

4.30 4.49 4.93 4.87

3.75 2.97 2.81 2.45

10.27%4.11

4.30 2.40 4.40 7.09

5.45 5.99 6.71 7.89

– 22.05%28.54

10.82 4.96 15.79 5.54– 36.99 26.68 15.06 2.11

– 18.14%42.92

18.03 10.45 15.30 5.49– 38.32 34.85 29.06 – 3.38

– 15.98%37.94

20.00 13.63 26.32 11.43– 42.43 30.04 7.94 – 11.81

The returns for the TSP funds represent net earnings after deduction of administrative expenses and, in the cases of the F, C, S, I, and L Funds, after deduction of trading costs and investment management fees. Additional information about the TSP funds, the related indexes, and their respective 1-, 3-, 5-, and 10-year returns can be found in the TSP Fund Information sheets on the TSP website.

The Lifecycle funds, which are invested in the individual TSP funds (G, F, C, S, and I)‡,wereimplementedonAugust1,2005;therefore,thefirstannualreturns are for 2006.

‡ TheGovernmentSecuritiesInvestment(G)Fund;theFixedIncomeIndexInvestment(F)Fund;theCommonStockIndexInvestment(C)Fund;theSmallCapitalizationStockIndex(S)Fund;theInternationalStockIndexInvestment(I)Fund

3

Printed on Recycled PaperFPI-PET

Future tax rates play into the Roth decision. Tax rates are a constantly moving target. It’s hard to guess what your future earnings and tax rate will be, or even what the U.S. income tax structure will be in the future. Having a mix of traditional and Roth savings is one way to avoid betting on just one tax scenario. The TSP will provide you the flexibility to make traditional pre-tax and Roth contributions to your account simul-taneously or at different times. You should reassess your decision whenever your tax or income situation changes.

Roth TSP is not a Roth IRA. Unlike a Roth IRA, there are no income restrictions on contributions to the Roth TSP feature. Any participant who is eligible to contribute to the TSP can make Roth contributions.

Also, Roth TSP contributions are subject to different contribution limits than Roth IRAs. In 2012, you can contribute up to $17,000 (plus $5,500 if you are 50 or older) to your Roth TSP,* while you can only contrib-ute $5,000 ($6,000 if you are 50 or older) to a Roth IRA. (If you are eligible to contribute to a Roth IRA, making Roth contributions to your TSP account will not affect your Roth IRA contribution limits.)

The decision is yours. The Roth decision is an indi-vidual one. Later in the year, the TSP will provide more information on the TSP website to help you decide whether making Roth contributions could be benefi-cial for you. You may also wish to consult a qualified financial or tax advisor.

* The combined total of Roth and traditional contributions cannot exceed these limits.

• You will be able to take loans, in-service withdrawals, and partial withdrawals from your account as before. They will come out of your account on a pro rata basis — with a proportional amount from your traditional and Roth balances.

• Whenyouwithdrawyouraccount,youwillbeabletoseparatelytransferanyportionofyourRothandtra-ditionalbalancestoIRAsorothereligibleemployerplans.

How will you sign up?

You will elect to make Roth contributions in the same way as you have always elected traditional contributions — using either the electronic system of your agency or service, or Form TSP-1, Election Form (TSP-U-1 for uniformed services).

If you are eligible for catch-up contributions, you will use your agency or service electronic system or Form TSP-1-C (TSP-U-1-C for uniformed services).

Check with your agency or service to find out whether your TSP elections should be made electronically or by using a TSP form.

Right before the Roth feature is introduced, the TSP will provide more information on the website about the new Roth feature.

YOUR PLAN YOUR FUTURETHRIFT SAVINGS PLAN

Watch the TSP website for announce-ments about Roth in the coming months.

You may want to consult a qualified tax or financial advisor to help you decide if Roth is for you. You should reassess your decision anytime your tax or income situation changes.

Scan above or visit the TSP website for more information about the TSP Roth feature.

www.tsp.gov/roth/index.shtml

www.tsp.gov

TSPLF30 (1/2012)

More Tax Flexibility in the TSP

The TSP will soon begin offering all active Federal employees and members of the uni-formed services the option to designate some or all of their contributions as Roth contribu-tions. The TSP Roth feature will give partici-pants flexibility in the tax treatment of their contributions now and in the future.

How does Roth TSP compare to Traditional TSP?

Roth contributions are taken out of your paycheck after your income is taxed. When you withdraw funds from your Roth balance, you will receive your Roth contributions tax-free since you have already paid taxes on the contributions. You also won’t pay taxes on any earnings, as long as you’re at least age 59½ (or disabled) and your withdrawal is made at least 5 years after the beginning of the year in which you made your first Roth contribution.

Traditional (pre-tax) contributions, which lower your current taxable income, give you a tax break today. They grow in your account tax-deferred, but when you withdraw your money, you pay taxes on both the contribu-tions and their earnings.

Can Roth benefit you?

Everyone’s situation is different. Whether you would be better off making traditional or Roth contributions depends on your income tax rate now and in the future. For example, you might benefit from making Roth TSP contributions if:

• You are in a low tax bracket now, but think your tax rate may be higher in re-tirement. With Roth, your contributions are taxed at your current lower rate, and you avoid paying taxes at the expected higher rate in the future.

• You are not in a low tax bracket now, but anticipate that your marginal Fed-eral tax rate will increase in the coming years.

• You are a uniformed services member making contributions from tax-exempt pay earned in a combat zone. If you elect Roth contributions, you will not pay taxes on either your Roth contri-butions or their earnings (as long as you satisfy the age and 5-year holding requirements mentioned earlier).*

• Youwanttaxdiversificationandseeanadvantageinmakingafter-taxcontri-butionssothatyoucanhavetax-freewithdrawalsinretirement.

• You are age 50 or older and deployed to a combat zone while making catch-up contributions. You will be able to con-tinue these contributions if they are Roth contributions. (You can’t make catch-up contributions to your traditional TSP balance from tax-exempt pay.)

How does Roth TSP work?

• Money already in your account when you begin making Roth contributions will remain part of your traditional balance. You will not be able to convert it to Roth.

• The combined total of your Roth and tax-deferred traditional contributions in 2012 cannot exceed the elective deferral limit of $17,000, or the catch-up contri-bution limit of $5,500.

• Agency contributions will always be part of your traditional (non-Roth) balance.

• Any contribution allocation or interfund transfer will apply to the investment of both your Roth and traditional contri-butions or balances.

• You will be able to transfer Roth 401(k), Roth 403(b), and Roth 457(b) (but not Roth IRA) money into the Roth balance in your TSP account. Pre-tax transfers will continue to be placed in your traditional balance.Electing Roth contributions is not

an all-or-nothing decision. You can contribute to both your Roth and tra-ditional balances. Roth gives you the opportunity to diversify the tax treat-ment of the money in your account.

* Tax-exempt contributions that go into your traditional and Roth balances are subject to the Internal Revenue Code 415(c) limit ($50,000 in 2012). However, only tax-exempt contributions that go into your Roth balance are subject to the elective deferral limit ($17,000 in 2012).

Roth TSP is similar to a Roth 401(k), not a Roth IRA. There are no income limits for Roth TSP contributions.

DoD Savings Deposit Program

The DoD Savings Deposit Program (SDP) was established to provide members of the uniformed services serving in designated combat zones the opportunity to build their financial savings. If you are serving in an SDP-eligible combat zone, you can start your SDP account once you’ve been deployed for a minimum of 30 consecutive days or at least one day in each of three consecutive months, and you must be receiving Hostile Fire Pay. Any military finance office in theater can help you establish an account and assist you in setting up the deposit method most convenient for you. A total of $10,000 may be deposited during each deployment and will earn 10% interest annually. You cannot close your account until you have left the combat zone, although your money will continue to draw interest for 90 days once you’ve returned home or to your permanent duty station. Deposits may be made in cash, by check or through allotment. Once started, allotments may be increased or decreased as your financial situation changes. Your allotment will stop upon your departure from the combat zone. While your account will be closed and all funds returned to you via direct deposit 120 days after leaving the combat zone, there are some guidelines regarding earlier withdrawal you need to know:

Once your account reaches a $10,000 balance, you may withdraw funds over $10,000 on a quarterly basis.

Emergency withdrawal must be approved by your commanding officer who must determine that it is necessary for the health and welfare of you or your family.

If you want your funds before the 120-day period ends, your myPay account provides an automated request option for Savings Deposit Program participants.

You can also send a request including your name, Social Security number and date of departure from the combat zone…

o … via e-mail to [email protected] o …via fax to (216) 522-5060 "Attention: SDP" o …or by mail to DFAS-Cleveland Center (DFAS-CL), ATTN: SDP, Special Claims, 1240

East 9th St., Cleveland , OH 44199-2055 Funds will be transferred electronically to the direct deposit account on record, but may be

deposited in another account you identify or via hard copy check. You must identify how you want funds returned to you. For banking/credit union accounts, provide the bank name, routing number, account number and account type (savings or checking). For hard copy checks, provide a complete mailing address.

Be sure your allotment has been stopped before requesting withdrawal.

Need help with your SDP account? Our staff is ready to help, just contact us at: Toll Free (Stateside Only): 1-888-332-7411 Commercial: 216-522-5096 DSN: 580-5096 Fax: (Attention SDP): 216-522-5060 E-mail: [email protected]

Source: http://www.dfas.mil/militarymembers/payentitlements/sdp.html