future of irish and uk gaap - cima - chartered ... locations docs/ireland...future of irish and uk...

TRANSCRIPT

FUTURE OF IRISH AND UK GAAP Financial Reporting Exposure Drafts (FREDs) 46 to 48

23RD FEBRUARY 2012

Consultative Committee of Accountancy Bodies - Ireland

The Future of UK Financial Reporting Standards

Michelle Sansom & Jennifer Guest,

Project Directors

UK Accounting Standards Board

23 February 2012

Over 290 responses to FREDs 43 and 44

Over 100 responses to FRED 45

The status of ASB deliberations: Responses to FREDs 43, 44 & 45

Oct 2010

Nov 2010

Dec 2010

Jan 2011

Feb 2011

Mar 2011

Apr 2011

May 2011

Jun 2011

FRED 45 issued for public benefit

entities

FREDs 43/44 issued

Extensive outreach programme ends

and comment period closes

Extensive redeliberation and regular published updates on tentative

decisions

FREDs 46/47/48 issued

Jul 2011

Aug 2011

Sep 2011

Oct 2011

Nov 2011

Dec 2011

Jan 2012

3

Key Comments

Acceptance of a need for modernization

Approval of use of IFRS for SME’s

BUT

Should we mandate full IFRS for companies beyond those fully listed?

Why eliminate options currently in UK GAAP and also in full IFRS?

Why not update the FRSSE?

4

Amendments made to IFRS for SMEs in preparing FRED 48

The ASB agreed and updated its guidelines for amending

the IFRS for SMEs:

changes for accounting treatments that exist in current FRSs

and EU-adopted IFRS

changes should normally be consistent with EU-adopted

IFRS

make use, where possible, of existing exemptions in

company law to avoid gold-plating and

Formats simplified.

5

6

Amendments made to IFRS for SMEs in preparing FRED 48

Application of the guidelines re-introduced a number of accounting options for example:

Revaluation of property, plant and equipment

Capitalisation of development expenditure

Capitalisation of borrowing costs

7

What about public accountability?

The concept of public accountability has been eliminated: The costs of applying EU-adopted IFRS, were considered

to outweigh the benefits

Concerns continued to be raised about the practical application of the definition of public accountability.

For some of these entities additional requirements have been included in FRED 48, eg financial institutions

The proposed reporting framework (FRED 46)

A framework based on proportional financial reporting:

In addition, qualifying subsidiaries and ultimate parents may

apply FRED 47 ‘Reduced Disclosure Framework’ – EU-adopted IFRS with reduced disclosures.

FRSSE FRS 102 EU-adopted IFRS

Entities eligible for small companies regime

Entities eligible for the small companies regime

Entities eligible for the small companies regime

Entities not small and not required to apply EU-adopted IFRS

Entities not small and not required to apply EU-adopted IFRS

Entities required to apply EU-adopted IFRS.

8

Key facts about the proposals: How FRED 48 differs from current accounting

Revenue recognition – similar approach but different words: service contracts

construction contracts

contracts with contingent fees

Investment properties - recognised at fair value through profit & loss, rather than through reserves: increased volatility of profit/loss for the year

consider implications for distributable reserves

9

Key facts about the proposals: How FRED 48 differs from current accounting

Intangible assets – could see more recognised as part of future acquisitions

revised definition of intangible assets

Employee benefits – required to accrue for short-term employee benefits (holiday pay)

will need to measure holiday earned, but not taken

might be easier in practice if holiday year coincides with financial year

10

Key facts about the proposals: How FRED 48 differs from current UK accounting

Leases – high level definitions the same, but…

some differences in detailed application

no requirement to split land and buildings

retrospective – may need to restate operating leases as finance leases in opening balance sheet

leases incentives – same principle but period not specified; full IFRS differs from UK accounting standards

no reference to detail of IFRIC 4; presumption that outsourcing arrangements include a lease

11

Key facts about the proposals: How FRED 48 differs from current accounting

Foreign exchange: Not permitted to use contract rate for sales and purchases,

must be spot rate

no change in cash flows but …

if previously used contracted rates, gains and losses from exchange rate movements will now be disclosed separately – for example movement between spot rate and contracted rate

may need systems changes

May now choose a presentation currency other than functional currency

might be useful for subsidiaries of global groups

12

Key facts about the proposals: How FRED 48 differs from current accounting

Equity investments: where fair value is reliably measurable, use fair value

through profit and loss;

little practical impact? but more volatility where applies

Impairment of financial assets: includes ‘bad debt’ provision for trade debtors, no change

must be based on objective evidence

can still include ‘collective’ provision, as long as based on objective evidence

13

Key facts about the proposals: How FRED 48 differs from current accounting

Pensions For defined benefit (final salary) schemes:

Group schemes can no longer recognise surplus/deficit in group accounts only

Where contractual agreement for charging the cost as a whole for the scheme between members - cost recognised

Where no agreement the legal sponsor recognises the full surplus/deficit in its individual accounts

Consider implications for distributable reserves

14

Key facts about the proposals: How FRED 48 differs from current accounting

Pensions For defined benefit schemes presentation requirements are

changed:

Recognised in the period

Profit or loss

Other

comprehensive

income

Service cost

Net Interest Income

Remeasurements

15

Key facts about the proposals: How FRED 48 differs from current accounting

Acquisitions

Goodwill has a finite useful life

amortise on a systematic basis over life

prospective, but in practice, unlikely to need to ‘re-life’ existing goodwill

12 months to make adjustments eg to fair values

16

Key facts about the proposals: How FRED 48 differs from current accounting

Taxation

Not IFRS for SMEs, nor IAS 12, but UK solution

Less complex than IAS 12, but in many cases will lead to same deferred tax

Differences include no discounting

must provide for deferred tax on revaluations

17

Key facts about the proposals: How FRED 48 differs from current accounting

Financial instruments:

Changing requirements for recognition & measurement determine whether financial instruments are ‘basic’

straight-forward accounting for ‘basic’ instruments

Derivatives are not ‘basic’ and are fair valued foreign currency forward contracts.

interest rate swaps

Possible use of hedge accounting more complex than SSAP 20

18

Key facts about the proposals: How FRED 48 differs from current accounting

Proposed additional disclosures for financial

institutions:

ASB tentatively decided that to include additional disclosures for financial institutions

financial instruments central to the business model

necessary to reflect risks arising from financial instruments

19

Key facts about the proposals: Sectors and industries with particular financial reporting issues

Public benefit entities (PBEs) additional PBE requirements worked in to FRED 48

all current SORPs to be retained and updated

Other SORPs

Update or withdraw? SORPs

Retain and update Pension funds

Oil and gas

Limited liability partnerships

Investment companies

Authorised funds

Separate consultation Insurance

Withdraw Leasing

Banking segments

20

Key facts about the proposals: What is FRED 47?

FRED 47 sets out reduced disclosures for qualifying entities that otherwise apply the requirements of EU-adopted IFRS.

A qualifying entity is a subsidiary or an ultimate parent.

21

Key facts about the proposals: What is FRED 47?

Qualifying entities need not disclose: A cash flow statement (IAS 7);

Related party transactions between wholly-owned members of the same group (IAS 24); and

Selected disclosures from IFRS 1, IFRS 2, IFRS 5, IAS 1, IAS 8, IAS 16, IAS 36 and IAS 38

Also, qualifying entities which are not financial institutions need not provide the disclosures required by IFRS 7 and IFRS 13

22

Next steps in the project: Update FRSSE

Current FRSSE

One-stop-shop for accounting and legal

requirements for small entities

Offers some simplifications from full UK accounting standards

23

Next steps in the project: Update FRSSE

Options for revision of FRSSE

Required Consistency with legal requirements

Possible options Non-mandatory guidance on disclosure?

Consistency with draft FRS 102

Update language?

Update accounting requirements?

24

Micro-companies

European agreement to simplify accounting requirements

BIS consultation later in 2012

FRSSE would not be applicable to micro-companies?

25

26

Conclusion

ASB has listened to feedback

Short modern standard suitable for wide range of companies

Firmly rooted in IFRS

Many companies will see little change

Updating under ASB control – normally every 3 years

No change to the FRSSE – yet!

FUTURE OF IRISH AND UK GAAP Financial Reporting Exposure Drafts (FREDs) 46 to 48

23RD FEBRUARY 2012

Consultative Committee of Accountancy Bodies - Ireland

FRED 46 – 48 – CAI/ASB Forum

23 February 2012

A Practitioner Perspective

Liam McQuaid

Managing Partner

28

FRED 46 – 48

Overview of Practitioner Issues

• Introducing – Liam McQuaid

• Congratulations

• Some Issues with the FRED 46 – 48

• Key issues for CASE constituency

• FRSSE changes

• Basic differences to the FRSSE

• Conclusion

FRED 46 – 48 – CAI / ASB Forum 23/02/2012 29

Introducing Liam McQuaid

• Managing Partner - Duignan Carthy O’Neill

• Director AGN International – International

Association of Duignan Carthy O’Neill

• Member of ASB CASE Committee

• Member of Accounting Committee

Chartered Accountants Ireland

FRED 46 – 48 – CAI / ASB Forum 23/02/2012 30

Congratulations

• To ASB on FRED 46/47/48 - Excellent document

However

FRED 46 – 48 – CAI / ASB Forum 23/02/2012 31

Some Issues with FRED 46 – 48

• Simplification opportunity missed

• Now have excellent compendium of FRS/UITF/IFRS

in one document

• Significant changes from FRED 43 – 45 and may be

more

• IAS 39 update

• Related parties

• Merger accounting

• Respondent favourites

FRED 46 – 48 – CAI / ASB Forum 23/02/2012 32

Some Issues with FRED 46 – 48

• Financial instruments - Section 11 & 12 to change

- Fair value measurement

• Not stand alone - Cross reference to IFRS

• Pension funds - Need SORP update

- Exclude actuarial liabilities

• Co-operatives - Fair value investments

• Disclosure exemptions for subsidiaries are welcome

Fred 46 – 48 – CAI / ASB Forum 23/02/2012 33

Key issues for CASE Constituency

FRED 46 – 48 – CAI / ASB Forum 23/02/2012

Two of the following three

Sales Gross Assets Employees

R.O.I. €3.8m €1.9m <50

U.K. Stg£6.5m Stg£3.2m <50

EU Directive Proposal €10.0m €5.0m <50

• Number of UK Entities

• Small Entity not so small

Number %

Small / FRSSE 1,959,000 97.6

Medium 40,000 2.0

Quoted parent & subsidiaries using IFRS

7,200

________

2,006,200

________

0.4

_____

100

_____

• Increase small thresholds in R.O.I.

34

Key Issues for CASE Constituency

• EU Plans for Small Entities - Mandatory limited disclosures

- True and fair accounts

- Micros exempt

• Major revision of FRSSE when directive issues

• Opportunity to simplify accounting for small entities

• Consider strongly move to revised FRSSE if small entity

“All the great things are simple” Winston Churchill

FRED 46 – 48 – CAI / ASB Forum 23/02/2012 35

FRED 48 FRSSE Changes

• Capitalised Goodwill & Intangible - useful life 20 to

5 years

• Asset impairment to be reviewed

• Related Party - Exemption for wholly owned entity

- Close family definition

- Related party definition

FRED 46 – 48 – CAI / ASB Forum 23/02/2012 36

FRSSE & FRED 48 Compared

FRED 46 – 48 – CAI / ASB Forum 23/02/2012

Topic FRSSE FRED 48

Scope Small Entities Entities not required to apply EU -

adopted IFRS and not small

Cash Flow Statement None Required (with exceptions)

Investment Property Market value changes

to STRGL

Fair value changes to P/L account

Listed Investments At cost or fair value At fair value

Deferred Tax No recognition on

revaluations

Recognition on revaluations

Employee Benefit No guidance Recognise holiday pay accrual

Foreign currency

translation

Can use contract rate Cannot use contract rate

Specialised activities Not addressed Addressed

Company Law Included Excluded

37

Conclusion

• FRED 46 – 48 is an excellent compendium of

FRS/UITF and IFRS and not a simplified set of

standards as envisaged by IFRS for SMEs.

• The development of the FRSSE as a standard for small

entities, which is EU compliant, presents a unique

opportunity to simplify accounting for small entities

and is now essential to service the accounting needs of

the CASE constituency.

“The secret of all victory lies in the organisation of the non-obvious”

Marcus Aurelius

FRED 46 – 48 – CAI / ASB Forum 23/02/2012 38

Duignan Carthy O’Neill, Chartered Accountants

84 Northumberland Road, Dublin 4, Ireland.

Contact: Liam McQuaid

(01) 668 2404

Website: www.dcon.ie

FRED 46 – 48 – CAI / ASB Forum 23/02/2012 39

FUTURE OF IRISH AND UK GAAP Financial Reporting Exposure Drafts (FREDs) 46 to 48

23RD FEBRUARY 2012

Consultative Committee of Accountancy Bodies - Ireland

ASB Proposals for the Future of UK and Irish GAAP February 2012

www.pwc.com

PwC

Agenda

• How do the proposals impact Ireland?

• The ASB is listening

Slide 42

February 2012 CCAB-I Presentation

PwC

Fiona Hackett

Senior Manager

PwC

Speaker

Slide 43

February 2012 CCAB-I Presentation

PwC

ASB Proposals

How do the proposals impact Ireland?

Slide 44

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

What makes Ireland famous? Some ideas ….

What makes Ireland famous?

Open and welcoming, tourism

Food and drink, agriculture

Heritage, culture, Island of Saints and Scholars

Leprechauns

Corporation tax rate

Slide 45

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

What makes Ireland famous? How do the proposals impact Ireland?

Opening and welcoming, tourism

Food and drink, agriculture

Heritage, culture, Island of Saints and Scholars

Leprechauns

Corporation tax rate

Slide 46

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

What makes Ireland famous? How do the proposals impact Ireland?

Opening and welcoming, tourism Foreign direct investment – subsidiaries

IFSC & Investment Funds

Food and drink Accounting for biological assets

Heritage, culture, Island of Saints and Scholars

Accounting for heritage assets, accounting by charities

Leprechauns Small company size thresholds

Corporation tax rate New model to calculate deferred tax

Slide 47

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

IFSC & Investments Funds Foreign Direct Investment – Subsidiaries

Accounting for biological assets

Accounting for heritage assets and accounting by charities

Small company size thresholds

New model of calculating deferred tax

Slide 48

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

IFSC & Investments Funds Foreign Direct Investment – Subsidiaries

Slide 49

February 2012 CCAB-I Presentation

PwC

IFSC & Investment Funds

• The Irish funds industry services assets worth over Euro 1.8 trillion held in over 11,000 funds#

• The centre is host to half of the world’s top 50 banks and to half of the top 20 insurance companies*

# Source – Irish Funds Industry Association website

* Source – ifsc.ie

Slide 50

February 2012 CCAB-I Presentation

PwC

IFSC & Investment Funds

• GOOD NEWS for the IFSC and investment funds

• No mandatory transition to IFRS

• Can use the FRS or IFRS.

• The FRS means;

- Less disclosure compared to IFRS (e.g. new IFRSs not yet effective, critical accounting estimates and judgements, share based payments ….)

- Defers mandatory application of new IFRSs, e.g. IFRS 10, IFRS 13

• The FRS has been upgraded to prescribe disclosures for ‘financial institutions’ that are based on IFRS 7

Slide 51

February 2012 CCAB-I Presentation

PwC

IFSC & Investment Funds

Open for Debate

Definition of ‘Financial Institution’ aims to capture

“Entities seeking to generate wealth from financial instruments”, e.g. banks, building societies, insurers, funds, credit unions, friendly

societies.

ASB Question #4

‘Do you agree with the definition of a financial institution?’

Slide 52

February 2012 CCAB-I Presentation

PwC

Foreign Direct Investment - Subsidiaries

• GOOD NEWS for subsidiaries.

• The FREDs develop on the ‘reduced disclosure framework’ of previous proposals.

• Available to a qualifying entity – “member of a group that prepares publicly available financial statements, which give a true and fair view, in which that member is consolidated”.

• Individual accounts only.

• Options available to ‘qualifying entity’;

- Full IFRS

- IFRS group reporting numbers but without full IFRS disclosures

- The FRS

- The FRS with reduced disclosure

Slide 53

February 2012 CCAB-I Presentation

PwC

Foreign Direct Investment - Subsidiaries

“It is envisaged that the provision of these disclosure exemptions could result in cost savings in the preparation of

financial statements of subsidiaries and ultimate parents, without reducing the quality of financial reporting.”

FRED 47, summary para 5

Proposed exemptions include;

• Group share based payment arrangements

• Financial instrument disclosures (unless a ‘financial institution’)

• Cash flow statement …..

Slide 54

February 2012 CCAB-I Presentation

PwC

Foreign Direct Investment - Subsidiaries

What’s not exempted;

• Certain related party disclosures

Slide 55

February 2012 CCAB-I Presentation

PwC

Foreign Direct Investment - Subsidiaries

Open for Debate

Related Party Disclosures

ASB Question #6

‘Do you consider that the related party disclosure requirements in section 33 of FRED 48 are sufficient to meet the needs of preparers and

users?’

Slide 56

February 2012 CCAB-I Presentation

PwC

Foreign Direct Investment - Subsidiaries

What’s not exempted;

• Certain related party disclosures

• Financial instrument disclosures for ‘qualifying entities’ that are ‘financial institutions’

Slide 57

February 2012 CCAB-I Presentation

PwC

Foreign Direct Investment - Subsidiaries

Open for Debate (the FRS only)

Financial instrument disclosures for a ‘qualifying entity’ that is a ‘financial institution’

ASB Question #3

Should a ‘qualifying entity’ that is a ‘financial institution’ have any exemption from the disclosure requirements of IFRS 7 and IFRS 13?

Slide 58

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

IFSC & Investments Funds Foreign Direct Investment – Subsidiaries

Accounting for biological assets

Accounting for heritage assets and accounting by charities

Small company size thresholds

New model of calculating deferred tax

Slide 59

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

Accounting for biological assets

Slide 60

February 2012 CCAB-I Presentation

PwC

Biological Assets

“A biological asset is a living animal or plant.”

Slide 61

February 2012 CCAB-I Presentation

PwC

Biological assets

Examples;

• Standing timber

• Fruit trees

• Livestock

• Plants

• Measured initially and subsequently at

fair value less costs to sell

• Changes in fair value less costs to sell shall

be recognised in profit or loss

Slide 62

February 2012 CCAB-I Presentation

PwC

Biological assets

What does this mean?

• Currently no discrete Irish GAAP accounting standard for biological assets

• More complexity in calculating fair value

• More estimation involved – estimating future cash flows

• More volatility in profit or loss

• Consistent with IFRS

• Fair value reflects the changes brought

about by biological transformation

Slide 63

February 2012 CCAB-I Presentation

PwC

Biological assets

Open for Debate

Is measurement of biological assets at fair value less costs to sell too onerous?

ASB Question #5

“Whether and, if so, why the proposals for agricultural activities are considered unduly arduous? What alternatives should be proposed?”

Slide 64

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

IFSC & Investments Funds Foreign Direct Investment – Subsidiaries

Accounting for biological assets

Accounting for heritage assets and accounting by charities

Small company size thresholds

New model of calculating deferred tax

Slide 65

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

Accounting for heritage assets and accounting by charities

Slide 66

February 2012 CCAB-I Presentation

PwC

Accounting for heritage assets

“An item of property, plant and equipment with historic, artistic,

scientific, technological, geophysical, or environmental qualities that is held and

maintained principally for its contribution to knowledge and culture.”

Slide 67

February 2012 CCAB-I Presentation

PwC

Accounting for heritage assets

• FRS 30 incorporated into the FRS

• Heritage assets presented separately in the balance sheet

• Considered for impairment annually

• Measured at cost or valuation

• How is impairment calculated/measured?

• Is information about cost or value of heritage assets available?

Slide 68

February 2012 CCAB-I Presentation

PwC

Accounting by charities

• FRED 45 – incorporated into the FRS

• Public benefit entity SORPs to be maintained and updated

• Includes guidance on;

- Non-reciprocal transactions

- Social housing

• Compliance with Co Law formats for presentation

• Charities SORP remains a separate document

Slide 69

February 2012 CCAB-I Presentation

PwC

Accounting by charities

Open for Debate

Will the public benefit entity SORPs be updated in time?

ASB Question #8

“Do you agree with the effective date? If not, what alternative date would you prefer and why?”

Slide 70

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

IFSC & Investments Funds Foreign Direct Investment – Subsidiaries

Accounting for biological assets

Accounting for heritage assets and accounting by charities

Small company size thresholds

New model of calculating deferred tax

Slide 71

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

Small company size thresholds

Slide 72

February 2012 CCAB-I Presentation

PwC

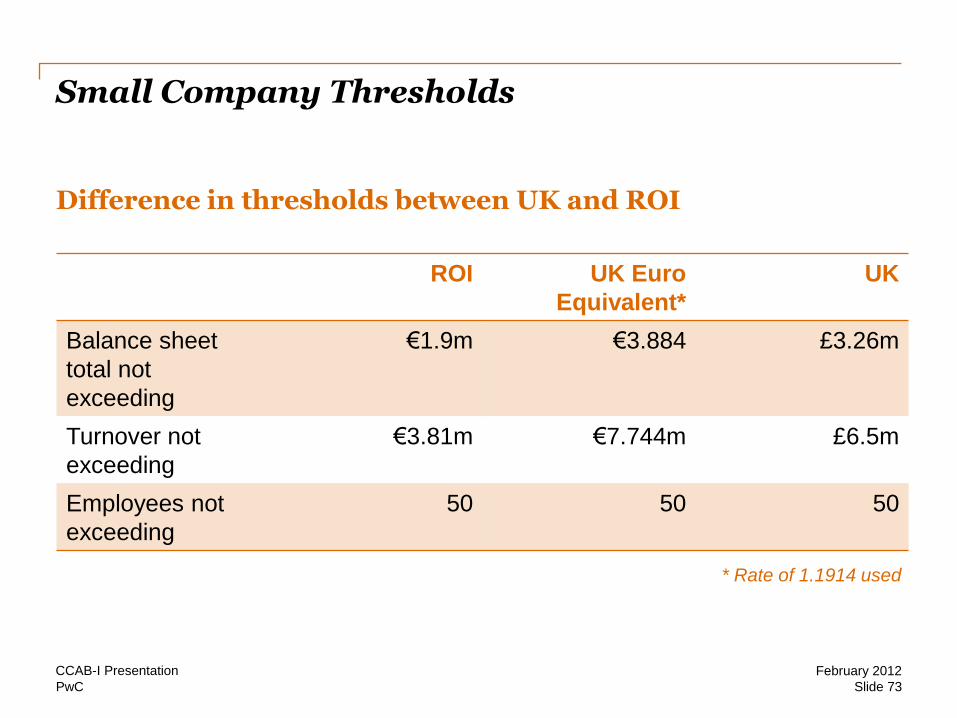

Small Company Thresholds

Difference in thresholds between UK and ROI

ROI UK Euro

Equivalent*

UK

Balance sheet

total not

exceeding

€1.9m €3.884 £3.26m

Turnover not

exceeding

€3.81m €7.744m £6.5m

Employees not

exceeding

50 50 50

* Rate of 1.1914 used

Slide 73

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

IFSC & Investments Funds Foreign Direct Investment – Subsidiaries

Accounting for biological assets

Accounting for heritage assets and accounting by charities

Small company size thresholds

New model of calculating deferred tax

Slide 74

February 2012 CCAB-I Presentation

PwC

How do the proposals impact Ireland?

New model of calculating deferred tax

Slide 75

February 2012 CCAB-I Presentation

PwC

12.5% but New Model for Calculating Deferred Tax

• Timing difference plus approach

• Closer to IFRS than current UK/Irish GAAP

• Deferred tax recognised on;

- Revaluation adjustments

- Fair value adjustments in a business combination

• Measured based on ‘average rate’ expected to apply

Slide 76

February 2012 CCAB-I Presentation

PwC

Agenda

• How do the proposals impact Ireland?

• The ASB is listening

Slide 77

February 2012 CCAB-I Presentation

PwC

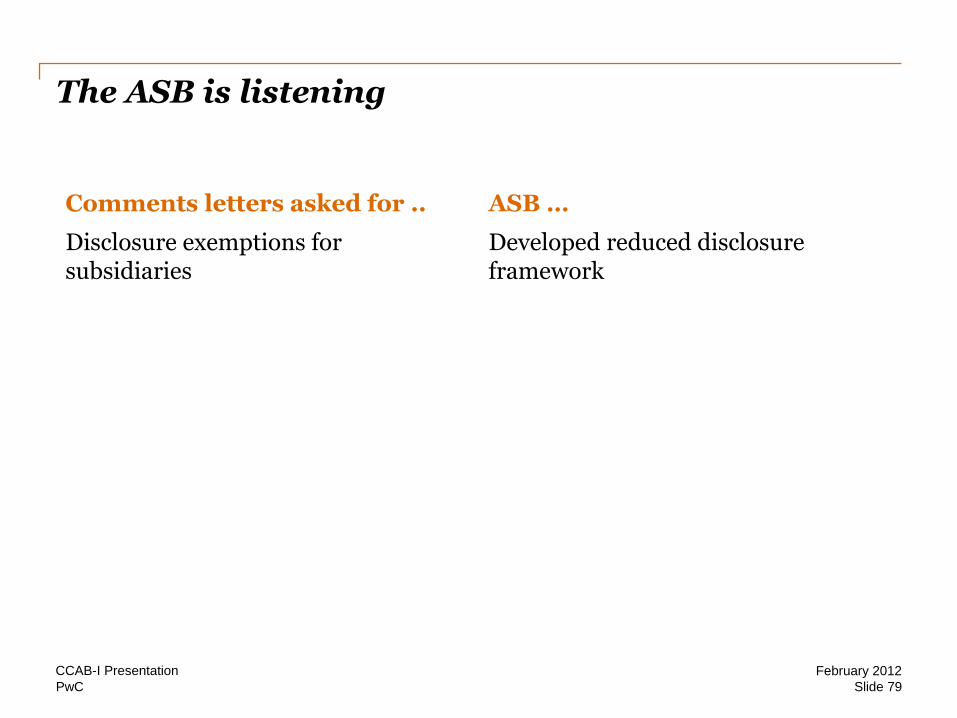

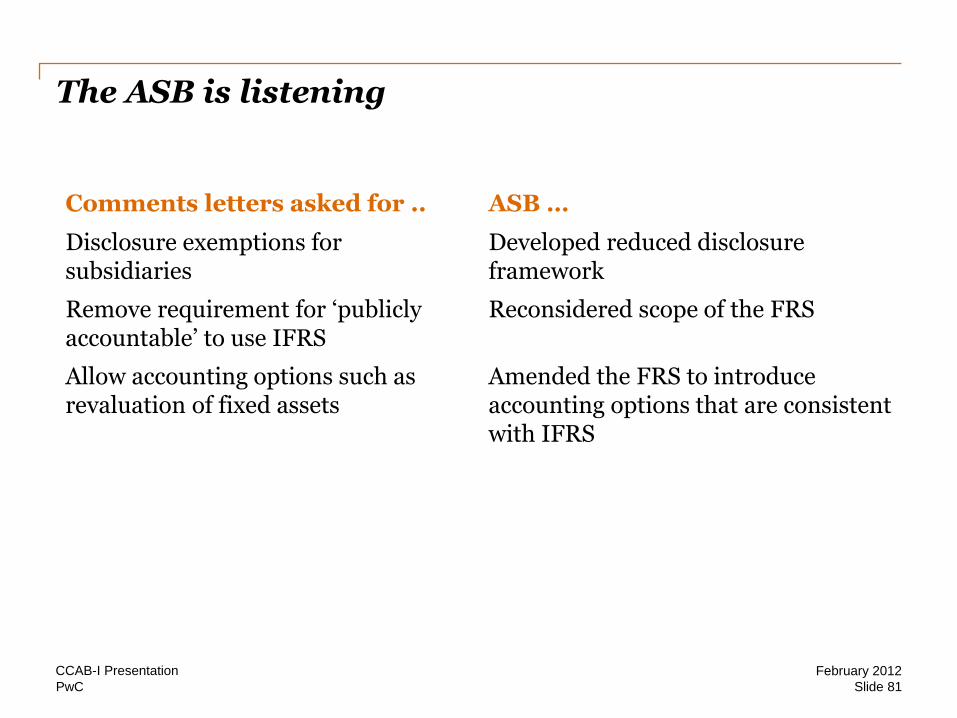

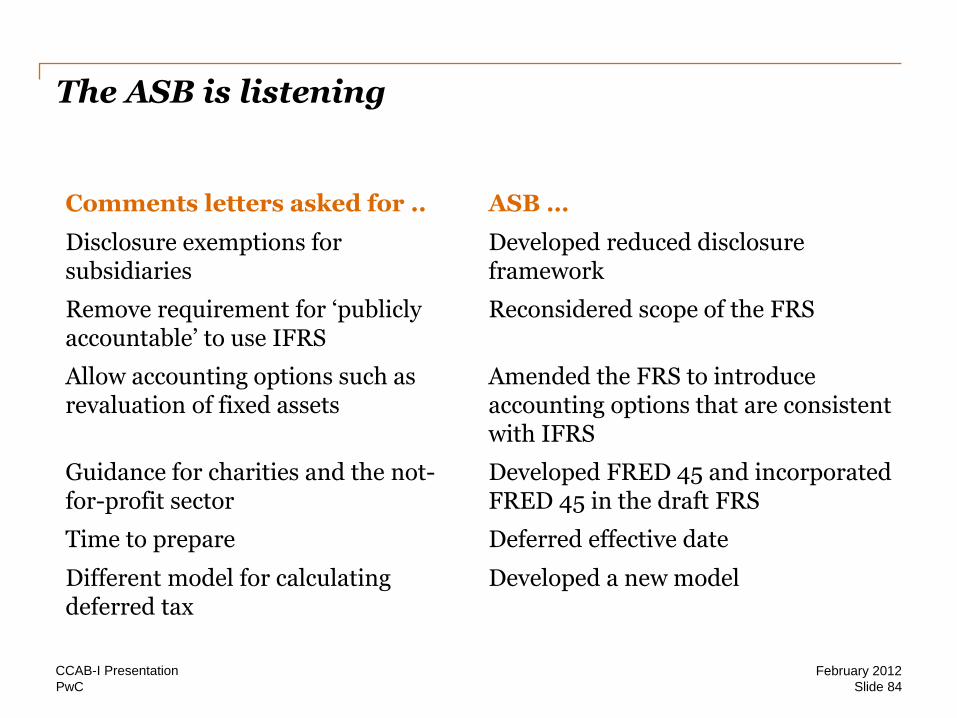

The ASB is listening

Comments letters asked for .. ASB …

Slide 78

February 2012 CCAB-I Presentation

PwC

The ASB is listening

Comments letters asked for .. ASB …

Disclosure exemptions for subsidiaries

Developed reduced disclosure framework

Slide 79

February 2012 CCAB-I Presentation

PwC

The ASB is listening

Comments letters asked for .. ASB …

Disclosure exemptions for subsidiaries

Developed reduced disclosure framework

Remove requirement for ‘publicly accountable’ to use IFRS

Reconsidered scope of the FRS

Slide 80

February 2012 CCAB-I Presentation

PwC

The ASB is listening

Comments letters asked for .. ASB …

Disclosure exemptions for subsidiaries

Developed reduced disclosure framework

Remove requirement for ‘publicly accountable’ to use IFRS

Reconsidered scope of the FRS

Allow accounting options such as revaluation of fixed assets

Amended the FRS to introduce accounting options that are consistent with IFRS

Slide 81

February 2012 CCAB-I Presentation

PwC

The ASB is listening

Comments letters asked for .. ASB …

Disclosure exemptions for subsidiaries

Developed reduced disclosure framework

Remove requirement for ‘publicly accountable’ to use IFRS

Reconsidered scope of the FRS

Allow accounting options such as revaluation of fixed assets

Amended the FRS to introduce accounting options that are consistent with IFRS

Guidance for charities and the not-for-profit sector

Developed FRED 45 and incorporated FRED 45 in the draft FRS

Slide 82

February 2012 CCAB-I Presentation

PwC

The ASB is listening

Comments letters asked for .. ASB …

Disclosure exemptions for subsidiaries

Developed reduced disclosure framework

Remove requirement for ‘publicly accountable’ to use IFRS

Reconsidered scope of the FRS

Allow accounting options such as revaluation of fixed assets

Amended the FRS to introduce accounting options that are consistent with IFRS

Guidance for charities and the not-for-profit sector

Developed FRED 45 and incorporated FRED 45 in the draft FRS

Time to prepare Deferred effective date

Slide 83

February 2012 CCAB-I Presentation

PwC

The ASB is listening

Comments letters asked for .. ASB …

Disclosure exemptions for subsidiaries

Developed reduced disclosure framework

Remove requirement for ‘publicly accountable’ to use IFRS

Reconsidered scope of the FRS

Allow accounting options such as revaluation of fixed assets

Amended the FRS to introduce accounting options that are consistent with IFRS

Guidance for charities and the not-for-profit sector

Developed FRED 45 and incorporated FRED 45 in the draft FRS

Time to prepare Deferred effective date

Different model for calculating deferred tax

Developed a new model

Slide 84

February 2012 CCAB-I Presentation

PwC

Agenda

• How do the proposals impact Ireland?

• The ASB is listening

Slide 85

February 2012 CCAB-I Presentation

PwC

Conclusion

ASB Objective

“The ASB’s objective is to enable users of accounts to receive high-quality understandable financial reporting

proportionate to the size and complexity of the entity and the users’ information needs.”

FRED 46, Summary para 3

Slide 86

February 2012 CCAB-I Presentation

Thank you

© 2012 PricewaterhouseCoopers. All rights reserved.

PwC refers to the Irish member firm, and may sometimes refer to the PwC network. Each

member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

This content is for general information purposes only, and should not be used as a substitute

for consultation with professional advisors.

FUTURE OF IRISH AND UK GAAP Financial Reporting Exposure Drafts (FREDs) 46 to 48

Q & A

Consultative Committee of Accountancy Bodies - Ireland