fy 2009 results - fin

TRANSCRIPT

FY 2009 ResultsFY 2009 Results

2

1.1. TREVI Group at a Glance TREVI Group at a Glance

2. FY 09 Financial Results

3. Foundations Sector

4. Drilling Sector

5. Appendix

3

PETREVEN starts drilling activities in Venezuela (HH Technology)

TREVI Group: TREVI Group: HistoryHistory

1957

1999

1969 1983 1997

2000 2004 2008/2009

WATSON

ASC

GALANTE S.A.

Established PalificazioniGeom. Davide Trevisani, (future TREVI SpA)

Established SOILMEC, part of

the future mechanical division

Pali Trevisani becomes TREVI SPA Acquisition of

TREVI ICOS Corporation (Boston,

Massachusetts

Acquisition of SWISSBORING in

Middle East

Established DRILLMEC.Acquisition of

RODIO, historical world leader in the foundation field

listed at Milan Stock Exchange

completion of 3 acquisitions:

TREVI Group: TREVI Group: MissionMission

4

We plan,We plan,execute execute and offerand offer

technologiestechnologies and and innovative servicesinnovative servicesfor any kind of work for any kind of work

in the field of in the field of foundation engineeringfoundation engineering

TREVI Group: VisionTREVI Group: Vision

55

Becoming the Becoming the main main

technological technological partnerpartner in the in the field of soil field of soil foundation foundation engineering engineering and in the and in the

research and research and development development of water and of water and

energy energy resourcesresources

Well Founded Well Founded

RootsRoots

• Onshore Drilling

• Long term contracts

• Latin America emerging

Player

• Hydraulic Rotary Rigs

• Cranes

• Jet Grouting

• Tunnel Consolidation

• Casing Oscillators

• Extractors

• Drilling Tools

• etc.

• Automatic Rigs

(HH Series)

• Land rigs

• Derricks & Offshore

• Mobile Drilling Rigs

• Hydraulic Top Drives

• Triplex Mud Pumps

• Deep Foundations

• Geotechnical Works

• Marine Works

• Tunnel Consolidation

• Automated Car Parks

• Environment

TREVI GroupTREVI Group

6

SERVICESDivision

MECHANICAL Division

Projects for renewable energy

Special foundation services Oil drilling services Oil drilling rigs Special foundation rigs

UniqueUnique Business Business ModelModel

Technological InnovationProcess Innovation

STRENGTHENING MARKET LEADERSHIPSTRENGTHENING MARKET LEADERSHIP

FOUNDATION EQUIPMENTS AND DRILLING RIGSFOUNDATION AND DRILLING SERVICES

7

8

Based on Not Consolidated Data

Total

Total Revenues

RevenuesFY09:

FY09:

EUR 1.035,8

EUR 1.035,8 m

lnmln

8

AddedAdded ValueValue FY09:FY09:€€ 347,1 347,1 mlnmln

One Group: Two Points of View One Group: Two Points of View

Services Division 53,0%

Mechanical Division47,0%

Foundations Division64,5%

Drilling Division35,5%

Services Divis ion 72,9%

Mechanical Divis ion

27,1%

TREVI Group: Global TREVI Group: Global PresencePresence

SOILMEC Division

DRILLMEC Division

PETREVEN DivisionVenezuela

U.S.A.Boston

Mozambique

Nigeria Oman

GermanyItaly

Hong Kong

Japan

China

Singapore

Italy (Piacenza)

U.S.A.Houston

Argentina

Colombia

New Zealand

France

Peru

UK

Austria

Venezuela

Argentina

Algeria

India

Philippines

Panama

Germany

TREVIDivision

Angola

U.S.A.Dallas

Colombia

U.S.A. Fort Worth

Saudi Arabia

Australia

Libya

45 Operating Companies in 32 Countries – 53 Business Units

9

Brazil

Canada

U.A.E.

Qatar

Italy (Cesena)Italy

10

1. TREVI Group at a Glance

2. FY 09 2. FY 09 Financial ResultsFinancial Results

3. Foundations Sector

4. Drilling Sector

5. Appendix

31/12/2009 % 31/12/2008 %

REVENUES 1.035,8 100,0% 1.069,2 100,0%

EBITDA 181,8 17,6% 166,3 15,6%

EBIT 117,4 11,3% 127,6 11,9%

FINANCIAL COSTS (17,4) -1,7% (17,2) -1,6%

TAXES (20,4) -2,0% (31,8) -3,0%

NET PROFIT 82,2 7,9% 74,7 7,0%

31/12/2009 % 31/12/2008

NET CAPITAL EMPLOYED 759,7 557,4

EQUITY 315,9 235,3

NET FINANCIAL POSITION 443,8 322,1

BACKLOG 780,3 1.109,0

31/12/2009 % 31/12/2008

NFP / EBITDA 2,4X 1,9X

NFP / EQUITY 1,4X 1,4X

31/12/2009 % 31/12/2008

EMPLOYEES 6.064 5.898

Financial Financial HighlightsHighlightsEuro mln

Euro mln

NET PROFIT + 10,0%NET PROFIT + 10,0%

EBIT EBIT -- 8,0%8,0%

REVENUES REVENUES -- 3,1%3,1%

INV. CAP. + 36,3%INV. CAP. + 36,3%

EQUITY + 34,2%EQUITY + 34,2%

NFP + 37,8%NFP + 37,8%

EBITDA + 9,3%EBITDA + 9,3%

BACKLOG BACKLOG –– 29,6%29,6%

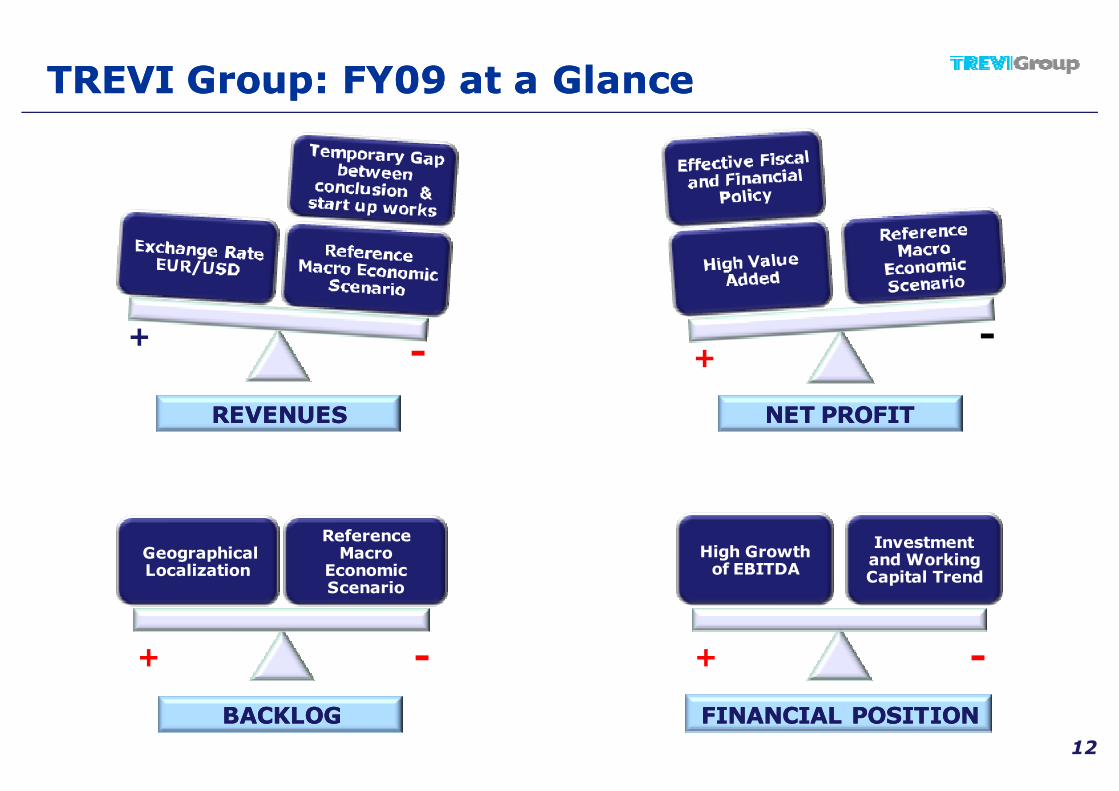

11

+- +

-

+ -

High Growth of EBITDA

Investment and Working Capital Trend

+ -

Geographical Localization

Reference Macro

Economic Scenario

REVENUESREVENUES NET PROFITNET PROFIT

BACKLOGBACKLOG

12

TREVI Group: FY09 at a GlanceTREVI Group: FY09 at a Glance

FINANCIAL POSITIONFINANCIAL POSITION

Total Total RevenuesRevenues and and ValueValue AddedAdded

13

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

263,0304,0

349,7 340,1366,6 366,4

498,0

642,4

841,6

1.069,2 1.035,8

92,9 104,0 105,2 111,0 127,1 123,2149,3

190,3

255,6

313,2347,1

Revenues

Value Added

Eur Mln

FY05 FY06 FY07 FY08 FY09

100,8 109,5 141,4 127,9 131,5

53,884,9

139,1 178,8

55,255,9

89,0

91,091,9

115,648,6

61,9

102,3118,4

121,7

89,1

99,2

126,3

132,3

149,9

114,6

165,3

188,9

364,0

421,5

34,9

32,6

52,5

55,840,3

Far East and Others

Middle East and Asia

Africa

Latin America

U.S.A. and Canada

Europe (Italy excl.)

Italy

Geographical BreakdownGeographical Breakdown

14

498,0

642,4

1.035,8

841,6

1.069,2

Eur mln

EbitdaEbitda MarginMargin

15

498,0

642,4

841,6

1.069,21.035,8

11,1%

13,3%

15,9%15,6%

17,6%

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1.000

1.200

FY05 FY06 FY07 FY08 FY09

Ebitda Margin

Eur mln

Revenues EBITDA Margin

EbitEbit MarginMargin

16

498,0

642,4

841,6

1.069,21.035,8

5,8%

9,0%

12,3% 11,9%11,3%

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1.000

1.200

FY05 FY06 FY07 FY08 FY09

Ebit Margin

Eur mln

Revenues EBIT Margin%

Eur mln FY09 g% YoY FY08

Special Foundation Services (TREVI) 495,2 8,6% 456,1

Drilling Services (PETREVEN) 65,4 0,8% 64,9

Interdivisional Adjustments and Eliminations (6,3) (3,2)

Sub-Total Foundations and Drilling Services 554,2 7,0% 517,8

Machines for Special Foundations (SOILMEC) 187,4 -41,3% 319,2Drilling Rigs (DRILLMEC) 310,5 7,5% 288,8Interdivisional Adjustments and Eliminations (1,4) (0,8)

Sub-Total Mechanical Division 496,4 -18,2% 607,2

Parent Company 15,0 13,5

Interdivisional Eliminations (29,8) (69,4)

TOTAL CONSOLIDATED REVENUES 1.035,8 -3,1% 1.069,2

RevenuesRevenues BeforeBefore and and AfterAfter ConsolidationConsolidation

17

GEOGRAPHICAL AREA Eur mln 31/12/2009 %

Latin America 135,8 17,4%

Middle East and Asia 215,5 27,6%U.S.A. and Canada 204,3 26,2%

Italy 97,3 12,5%

Europe (excl. Italy) 28,3 3,6%Africa 89,7 11,5%

Far East 5,1 0,7%Others 4,4 0,6%

TOTAL 780,3 100%

BacklogBacklog

4%

26%

12%

58%

Euro mln

FY05 FY06 FY07 FY08 FY09

517,0

709,3636,8

1.109,0

780,3

329,0 316,3431,9

700,7

482,6

188,0320,5

277,3

408,2

297,8

18Foundations Sector Drilling Sector

322,1

159,5

20,4

171,1

80,3

17,4 4,7 3,4

443,8

Net Financial PositionNet Financial Position

INVESTMENTS INTERESTS OTHER NFP FY09NFP FY08 EBIT + D&A TAXES ∆WORKING CAPITAL

FREE CASH FLOW

- 112,3 mln Euro

Eur mln

19

EXCHANGE DIFFERENCES

148,0126,0

175,7

142,6

322,1

443,8

3,6x

2,3x2,1x

1,1x

1,9x

2,4x

0,0x

0,5x

1,0x

1,5x

2,0x

2,5x

3,0x

3,5x

4,0x

4,5x

0

50

100

150

200

250

300

350

400

450

PFN PFN / EBITDA

Net Financial PositionNet Financial Position

NFP/EQUITY

FY 05 FY 06 FY 07 FY 08 FY 09

1,4x1,4x0,9x1,4x1,2x

Euro mln

FY 04

1,8x

20EBITDA/NET INTERESTS 10,4x9,7x9,8x8,2x6,2x5,7x

NFP NFP / EBITDA

0

50

100

150

200

250

300

350

400

450

500

2004 2005 2006 2007 2008 2009 2009

EQUITY and NFPEQUITY and NFP

Euro mln

EQUITY NFP

80,9102,1

127,4

163,5

235,3

315,9

443,8

21

77%

23%

Short Term Debt

Long Term Debt

22

Foundations and Drilling ServicesFoundations and Drilling Services

Not Consolidated Data

361,5

401,2

517,8

554,2

9,2%

11,2%

13,3%

15,0%14,2%

16,2%

18,3%

24,7%

7%

12%

17%

22%

27%

90

140

190

240

290

340

390

440

490

540

590

FY06 FY07 FY08 FY09Margin %

Euro m

ln

FY07 FY08

Revenues Ebit% Ebitda%

Italy15%

Europe (excl. Italy)1%

U.S.A. and Canada12%

Latin America21%Africa

24%

Middle East and Asia25%

Far East2%

310,0

464,9

607,2

496,4

10,2%

13,7%

11,4%

7,3%

12,9%

15,5%

12,9%

9,2%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

80

180

280

380

480

580

FY06 FY07 FY08 FY09Margin %

Euro m

ln

23

Mechanical DivisionMechanical Division

Not Consolidated Data

FY07 FY08

Revenues Ebit% Ebitda%

Italy11%

Europe (excl.

Italy)10%

U.S.A. and

Canada10%

Latin America1%

Africa4%

Middle East and Asia

57%

Far East5%

Others

2%

24

1. TREVI Group at a Glance

2. FY 09 Financial Results

3. 3. Foundations SectorFoundations Sector

4. Drilling Sector

5. Appendix

EstimatedEstimated Global Global GDP% inGDP% in 20102010

Estimated Global Estimated Global GDP% GDP% in 2011in 2011

Source: Goldman Sachs 11.01.2010

TREVI Group, in order to catch all businessopportunities coming worldwide will establish newbusiness presences through its Trevi division;starting from 2009 until now SOILMEC hasestablished newbranches:

o SOILMEC WUJIANG (China)o SOILMEC DO BRAZIL (Brazil)o SOILMEC INDIA (India)

Emerging Markets are able to emphasize allindustrial skills and the flexible organization of TREVIGroup.

Tables show estimates related to the globalGDP trend during the period 2010 – 2011.

Major performances in particular (see redline) are referred to China, India and otherEmerging Markets.

All the above mentioned countries will showin the next couple of years a continuousgrowing trend of their GDP especially throughmajor investments in infrastructures.

Outlook: Construction Sector Outlook: Construction Sector

25Source: Goldman Sachs 11.01.2010

TREVI in the WorldTREVI in the World

26

• U.S.A.

• Canada

• Panama

• Santo Domingo

• Colombia

• Argentina

• Perù

• Venezuela

• New Zealand

• Philippines

• Hong Kong

• Thailand

• Saudi Arabia

• Oman

• Qatar

• Other U.A.E.

• Algeria

• Angola

• Libya

• Mozambique

• Nigeria

• Ivory Coast

• Austria

• Italy

• Sweden

Project in SwedenProject in USA

TREVI Group: TREVI Group: UnitedUnited StatesStates

27

WOLF CREEK

AWARD: 2008 in JV 50%

TOT AMOUNT (USD): 341,400,000

C LIENT: CORPS of ENGINEERS

OBJECTIVE: Restoration of the Dam through an installation of a Concrete Wall in the inner part of the Dam located in the county of Russell, Kentucky.

NEW ORLEANS (PHASE I)

AWARD: 2009

TOT AMOUNT (USD): 116,000,000

C LIENT: CORPS of ENGINEERS

OBJECTIVE: Consolidation and embankments’ restoration of the canals in New Orleans (Louisiana) damaged by the Katrina Hurricane.

HERBERT HOOVER (PHASE I)AWARD: 2008

TOT AMOUNT (USD): 39,000,000

C LIENT: CORPS of ENGINEERS

OBJECTIVE: Extraordinary Job of maintenance in the Dam located in the State of Florida through the insertion of a Plastic Impermeable Wall.

LouisianaFlorida

Kentucky

TREVI Group: AfricaTREVI Group: Africa

Project in Nigeria

Project in Algeria

Project in Ivory Coast

The localization of all projects shown hererepresents a sample of areas in which theGroup is working in Africa. In some ofthese areas (Nigeria and Algeria) the Groupis historically present since many years.The experience gained and the formation ofspecialized local manpower founded strongbases for a further development allowingthe Group to award new importantprojects.

Project in Angola

28

TREVI Group: Middle EastTREVI Group: Middle East

29

TREVI Group through its controlled companySWISSBORING Overseas Corporation Ltd., isestablished in the Middle East region since 1973.

The table on side shows estimates related to thevolume of investments for every country includedn the region during the year 2010.

The total value of investments (in $bln) isextremely relevant and includes many projectsrelated to major infrastructures.

Arabia Saudita

Yemen

Oman

UAE

Iraq Iran

Siria

Kuwait

Bahrain

Qatar

Trevi Trevi OverviewOverview

(*) Not Consolidated Data30

FY05 FY06 FY07 FY08 FY09

282,1

338,3357,6

456,1

495,2

DRIVERS THE FUTURE

Strengthening of Strengthening of market leadership market leadership

in existing in existing geographical areasgeographical areas

Focus on “big” Focus on “big” infrastructural and infrastructural and

technological technological projectsprojects

Selective growth in Selective growth in new geographical new geographical

areasareas

Looking for new Looking for new market niches to market niches to

addressaddress

Stimulus Plans Stimulus Plans focused on focused on

infrastructural infrastructural expenditures expenditures

Focusing on project Focusing on project with strong with strong technological technological challengeschallenges

(General Specialty (General Specialty Contractor)Contractor)

Focusing on Focusing on maritime projects maritime projects

REVENUES (*) FY05 – FY09

Eastern

Europe

Ireland

Portugal

Austria

Belgium

Switzerland

Netherlands

Spain

UKItaly

FranceGermany

(10%)

(5%)

5%

10%

(1%) 1% 2% 3%

2009E-2012E GDP CAGR (%)

Outlook: Construction Sector in Europe Outlook: Construction Sector in Europe

Construction Sector and GDPConstruction Sector and GDP Public Financial Resources Public Financial Resources Allocated by CIPEAllocated by CIPE

The table on left side shows estimates of thegrowth of GDP and construction sector announcedby each European country. Considering only majorEuropean countries (Germany, France, UK andItaly) the outlook is quite positive even if it showslow growth rates.

The table above shows in which projects the CIPEhas allocated Public Financial Resources. Themajor part shall be assigned to new projects notyet published (33,2%) and to new projectsalready assigned to General Contractors (47,5%).

31

Source: Note by ANCE on CIPE Plan – 16.03.2010

2009E-2012EConstruction CAGR (%)

= EUR100bn of 2009E Construction Value

Source: Merril Lynch, 12.04.2010

Values in milion of Euro Ammount %

Works in progress 1.051,0 15,8%

Works already assigned to General Contractors 3.166,8 47,5%

New works to be published 2.215,2 33,2%

New works already published 200,1 3,0%

New assigned works 20,2 0,3%

Not Infrastructural works 12,0 0,2%

TOTAL 6.665,3 100%

TREVI: TREVI: ProjectsProjects in Italyin Italy

32

METRO of NAPOLIARCO MIRELLI

CONSOLIDATION of “CAMPANILE PIAZZA SAN MARCO”

33

PROV. of BOLOGNAPORRETTANA

BOLOGNA – TREVI PARK

MORBEGNO – Project in PEDEMONTANA

TREVI: TREVI: ProjectsProjects in Italyin Italy

Soilmec: Extended Global NetworkSoilmec: Extended Global Network

34

Boston

Houston

Dallas

Headquarter CESENA

(Italy)

Sydney

Assembling/ManufacturingNetwork

Germany

SOILMEC WUJIANG China

SOILMEC BRAZIL

Sao Paulo

SOILMEC India

AustraliaAustralia

SR SR SeriesSeriesSRSR--9090

SRSR--9090

Soilmec: Range of ProductsSoilmec: Range of Products

SR 80SR 80

SR 70SR 70

Excadrill 10Excadrill 10

Model 2500Model 2500

PSMPSM--88

Excadrill 5Excadrill 5

PSM PSM --2020

PSMPSM--8B8B

HousingMicropiles

CommercialReal Estate

Major Infrastructures

35

Soilmec: Soilmec: BaumaBauma 2010 2010 –– New ProductsNew Products

SC-65

36

SM-3During the BAUMA 2010 SOILMEC presented

several new products (see pictures).

These equipments for special foundation (low,

medium and high tonnage), meet high standard of

safety and do include new important technologies in

order to develop considerably the drilling performances and the

service offered to clients.

New Cab

SR-30SM-5 Transport Isometric

SC-65

Soilmec: Extended Range of ProductsSoilmec: Extended Range of Products

Housing

Micropiles

Real Estate

Major Infrastructures

37

Commercial

SCSC--6565

SCSC--100 Hydraulic 100 Hydraulic Crawler CraneCrawler Crane

SRSR--3030

SMSM--55

SMSM--33

SMSM--1818 SRSR--90 TTJ90 TTJ

SoilmecSoilmec OverviewOverview

(*) Not Consolidated Data38

FY05 FY06 FY07 FY08 FY09

132,5

190,5

280,9

319,2

187,4

DRIVERS THE FUTURE

Residential Sector Residential Sector (House & (House &

Commercial) Commercial) strongly impacted strongly impacted

by crisisby crisis

Strong Strong InsourcingInsourcingof productionof production

Opening of new Opening of new geographical geographical

markets for the markets for the medium term medium term developmentdevelopment

Launching of new Launching of new products and products and

addressing new addressing new market nichesmarket niches

Stimulus Plans Stimulus Plans often delayed in often delayed in many Countries many Countries

Strengthening of Strengthening of market share in the market share in the existing markets existing markets

REVENUES (*) FY05 – FY09

39

1. TREVI Group at a Glance

2. FY 09 Financial Results

3. Foundations Sector

4. 4. Drilling SectorDrilling Sector

5. Appendix

40

Oil & Gas OutlookOil & Gas Outlook

0

100

200

300

400

500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009e 2010e 2011e 2012e

GLOBAL INVESTMENTS IN GLOBAL INVESTMENTS IN E&PE&P (US$ bln)

Source: Merrill Lynch 20.01.2010

OIL PRICE ESTIMATES

Source: stime UBS

The table on left side showsestimated global investments (inUS$ bln) in E&P.

After the reduction ofinvestments during the year2009, the table shows aprogressive estimated increase ofinvestments for the period 2010to 2012.

This level of investments will besupported by a stable Oil Pricetrend.

4Q09 2009 1Q10 2Q10E 3Q10E 4Q10E 2010E 2011E 2012E 2013E

WTI ($/bbl) 78.00 62.30 75.00 74.00 74.00 77.00 75.00 80.00 80.00 80.00

Brent ($/bbl) 76.00 62.60 74.00 73.00 73.00 76.00 74.00 79.00 79.00 79.00

OGDCL

ONGC

Pet roChina

Pet r onas

PTT

S inopec

Ecopet rol

PDVSA

Pemex

Pet r obr as

Abu Dhabi NOC

Egypt ian Gener al Pet r ol eum

Nat ional Oil Corp

NNPC

PDO

Qatar Pet roleum

Saudi Ar am co

Sonangol

Sonat rach

BP

Chevron

ConocoPhill ips

Exxon Mob il

Royal Dutch/Shel l

Tot al

Gazprom

Gazprom Nef t

Lukoil

Novatek

Rosnef t

Surgutnef tegaz

TNK-BP

BG Gr oup

Eni

OMV

Repsol

Santos

Statoil Hydro

Woodside

Af ren

BowLeven

Cai rn Energy

Dana Dragon

Lundin

Pr emier

Regal

Salamander

Soco Tull ow

Anadarko

Apache

CNR

Cenovus

Chesapeake

Devon

EnCana

EOG Res

Hess

Marathon

Murphy Nexen

Noble

Occidental

Pet rohawk Pl ains Explo

Range Res Suncor

Tal ism an

Wil li ams Cos

(5.0)

0.0

5.0

10.0

15.0

20.0

25.0

(50%) (40%) (30%) (20%) (10%) 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100% 110% 120%

41

Investments of Oil CompaniesInvestments of Oil Companies

Change in % 2010 Capex vs 2009 Capex

2010 Capex($m)

NOCs

Majors

Russia

Altri E&Ps

Euro E&Ps

USA/Canada

INVESTMENTS 2009 vs 2010 FOR A SAMPLE OF OIL COMPANIES INVESTMENTS 2009 vs 2010 FOR A SAMPLE OF OIL COMPANIES

The table above shows the change of investments between 2010 and 2009 and the volume of suchinvestments related to a sample of major Oil Companies .

The major part of such Oil Companies will show higher volumes of investments with an average aggregategrowth in 2010 equal to about 9,4%.

’09-’10

Change

% Capex ’10

of Total

NOC 14.2% 37.9%

� Asian 21.5% 11.1%

� Latam 9.1% 12.0%

� MENA 13.3% 14.9%

Majors (0.5%) 33.0%

US/Canadian Independents

19.2% 14.6%

Russian 19.8% 9.8%

Other E&Ps 1.1% 3.3%

Euro E&Ps 8.9% 1.4%

All 9.4% 100.0%

Source: Merril Lynch 12.04.2010

DrillmecDrillmec: : ExtendedExtended Global NetworkGlobal Network

DRILLMEC Branches

Houston (USA) – OIL&GAS Division

Headquarter PIACENZA (Italy)

OIL&GAS Division

Drillmec Division, in order to improvethe relationship with its customers andto catch all major opportunities comingfrom the market, during last few yearshas extended its global networkestablishing new branches in mainstrategic areas.

During the period 2009/2010 theDivision established a new productionunit in Houston, Texas where will berealized both conventional rigs andhydraulic drilling rigs(series HH).

42

Gorizia (Italy)PUMPS Division

Parma (Italy)WATER Division

In the South American region Drillmec takes

advantage from the local presence of

Different & Complementary TechnologiesDifferent & Complementary Technologies

REDUCTION REDUCTION ofof AREAAREA

REDUCTION REDUCTION ofof COSTSCOSTS

INCREASED PERFORMANCEINCREASED PERFORMANCE

INCREASED SECURITYINCREASED SECURITY

43

RIG RIG -- UP UP in Italyin Italy

Main Advantages for clients are the following:

• Reduction of Costs

• Security of Operating

• Reduction of Risks

DrillmecDrillmec: HH : HH RigsRigs DeliveredDelivered

RUSSIA

AUSTRALIA

ICELAND

EGYPT

LIBYA

SYRIA

ARGENTINA

COLOMBIA

U.S.A

UKRAINE

PERU’

VENEZUELA

UK ITALY

BRAZIL

CHINA

LEBANON

FRANCEGERMANY

NETHERLANDS

CONGO

ROMANIA

KSA

44

45

DrillmecDrillmec: : ConventionalConventional RigsRigs-- KazakhstanKazakhstan

Drillmec S.p.A., has won a contract from Saipem S.p.A. to build and testtwo oil drill rigs each of 3,000 HP.

The two rigs, to be sited on artificial islands in Kazakhstan, as part ofthe development of the Kashagan oil field, are designed to function inthe particular conditions that characterise the northern part of theCaspian Sea, a harsh climate and tight environmental controls.

Project in Kazakhstan

3000 Hp RIG

46

DrillmecDrillmec: Full Products Range : Full Products Range (*)(*)

(*) Sample of Clients

WATER OIL & GAS GEOTHERMAL

Conventional Technology

HydraulicTechnology

Drillmec OverviewDrillmec Overview

(*) Not Consolidated Data47

FY05 FY06 FY07 FY08 FY09

75,4

126,6

194,1

288,8310,5

DRIVERS THE FUTURE

Drilling Drilling AcademyAcademy

Strategic Strategic Partnership Partnership

with clients and with clients and competitorscompetitors

Outsourcing Outsourcing CapabilitiesCapabilities

Widening of Widening of commercial commercial network and network and strengthening strengthening relationshiprelationship

Increasing Increasing production capacity production capacity

HH: Technological HH: Technological InnovationInnovation Widening products Widening products

rangerange

REVENUES (*) FY05 – FY09

PetrevenPetreven: : Operative Operative RigsRigs

2005

4 rigs

2006

8 rigs

2007

9 rigs

ARGENTINA

5 rigs HH100

-Petrobras (2)

-Chevron Texaco (1)

-Repsol YPF (2)

VENEZUELA

1 rig HH300

Petrobras

1 rig HH200

Petrooritupano

COLOMBIA

1 rig HH100

Petrominerales

PERU

2 rig HH100

Petrobras

2008/2009

10 rigs

AWARDS FOR SECURITY

48

Petreven: Rigs Competitive AdvantagePetreven: Rigs Competitive Advantage

VENEZUELA

ARGENTINA

IMPIANTO: HH200–HH300

CLIENTE:

IMPIANTO: H103-H104-H105-H106-H108

CLIENTE:

PERU’

IMPIANTO: H107-H109

CLIENTE:

COLOMBIA

IMPIANTO: G102

CLIENTE:

49

HH Technology

Security

Performance

People

Petreven division is taking advantage of both afavoured access to the HH Hydraulic technologyand its important track record in all referencecountries. The current and expected stability ofthe Oil Price shall increase opportunities for afurther growth.

TREND 2010/2011

Petreven OverviewPetreven Overview

(*) Not Consolidated Data50

FY05 FY06 FY07 FY08 FY09

16,0

25,2

46,6

64,9 65,4

DRIVERS THE FUTURE

Preferential access Preferential access to HH series to HH series technology technology

Historical strong Historical strong presence in Latin presence in Latin

AmericaAmerica

Constant growth Constant growth with “acquisition” with “acquisition”

of new rigsof new rigs

Development of Development of commercial and commercial and technological technological partnerships partnerships

High operating and High operating and safety standardssafety standards

Further Further development of development of

know how know how (especially with (especially with

regard to Hydraulic regard to Hydraulic Rigs)Rigs)

REVENUES (*) FY05 – FY09

51

1. TREVI Group at a Glance

2. FY 09 Financial Results

3. Foundations Sector

4. Drilling Sector

5. 5. AppendixAppendix

INCOME STATEMENT FY09 INCOME STATEMENT FY09 vsvs FY08FY08

52

Eur 000 FY09 FY08 %

TOTAL REVENUES 1.035.815 1.069.155 -3,1%

Changes in inventories of finished and semi-finished products 38.912 82.351

Increase in fixed assets for internal use 20.607 50.278

Other non-ordinary operating revenues 0 0

VALUE OF PRODUCTION 1.095.334 1.201.784 -8,9%

Raw materials and external services 735.642 878.107

Other operating costs 12.553 10.465

VALUE ADDED 347.139 313.212 10,8%

Personnel expenses 165.331 146.904

EBITDA 181.808 166.307 9,3%

% total revenues 17,6% 15,6%

Depreciation 42.161 32.398

Provisions and write-downs 22.287 6.308

EBIT 117.361 127.601 -8,0%

% total revenues 11,3% 11,9%

Financial revenues (expenses) (17.423) (17.176)

Gains/(losses) on exchange rates 4.694 (1.250)

Gains/(losses) on 0 0

EBT 104.631 109.175 -4,2%

Tax 20.427 31.820

Minorities 2.046 2.694

GROUP NET PROFIT 82.158 74.661 10,0%

% total revenues 7,9% 7,0%

BALANCE SHEET: FY 2009BALANCE SHEET: FY 2009

(*) Taking into account IAS 11 53

FY09 FY08 %

Fixed assets

- Tangible fixed assets 319.838 294.464

- Intangible fixed assets 13.695 6.073

- Financial fixed assets 4.588 5.036

Net working capital

- Inventories 356.199 335.551

- Trade receivables 316.215 315.581

- Trade payables (-) (169.979) (340.223)

- Pre-payments (-) (82.733) (67.126)

- Other assets (liabilities) 18.652 23.456

776.475 572.813 36%

(16.799) (15.391)

759.676 557.422 36%

302.225 226.436

13.667 8.903

443.783 322.084

759.676 557.422 36%

Group net shareholders' funds

Minorities' share of net shareholders' funds

Net financial position

TOTAL SOURCES OF FINANCING

Eur 000

Post-employment benefits (-)

Fixed assets plus net working capital

NET INVESTED CAPITAL

Financed by:

TREVI Group: AWARDSTREVI Group: AWARDS

54

DYNAMISM PERFORMANCE

SECURITYQUALITY

AWARD MEDIOBANCA 2009

AWARD LEONARDO 2009

AWARDAT KEARNEY 2009

AWARD MAESTRIA 2009

Award to TREVI Group as Best Dynamic Italian Middle Company

Award to TREVI Group as one of the Best Companies which promote the “Italian Quality” worldwide

Award to TREVI Group for the best combination of growth of revenues and return for shareholders during last 5

years

Award to PETREVEN C.A. (established in Colombia) as Company with the Best Security and Management System

DisclaimerDisclaimer

55

Executive in charge of the preparation of accounting documents “Daniele Forti” declares, pursuant to

paragraph 2 of article 154-Bis of the consolidated law on finance, that the accounting information contained

in this presentation corresponds to the document results, books and accounting records.

This presentation, prepared by TREVI – FINANZIARIA Industriale SPA, contains forward looking information

and statements about the group and in no case may it be interpreted as an offer or an invitation to sell or

purchase any security issued by the company or its subsidiaries.

These statements include financial projections and estimates and their underlying assumptions, statements

regarding plans, objectives and expectations to future operations, products and services, and statements

regarding future performance.

Forward looking statements involve inherent risks and uncertainties are current only at the date they are

made.

However, the management of TREVI – FINANZIARIA Industriale SPA believes that the expectations are

reasonable, but, at the same time, points out to holders and investors that all the information and all the

statements are subject to various risk and many of which are very difficult to predict and to control.

TREVI – FINANZIARIA Industriale SPA does not undertake any obligation to update forward looking

statements to reflect any changes in own expectations with regard thereto or any changes in events.

56

InvestorInvestor Relations TeamRelations Team

Stefano CampanaStefano Campana [email protected]@trevifin.comSimone NanniSimone Nanni [email protected]@trevifin.comMatteo ScarpelliniMatteo Scarpellini [email protected]@trevifin.comCristina TrevisaniCristina Trevisani [email protected]@trevifin.com