fy 2014 departmental change in management audit austin... · fy 2014 departmental change in...

TRANSCRIPT

FY 2014 Departmental Change in Management Audit

Department of Chemistry

July 2015

The University of Texas at Austin Office of Internal Audits

UTA 2.302 (512) 471-7117

The University of Texas at Austin Internal Audit Committee

Mr. William O'Hara, Independent Member, Chair Dr. Gregory L. Fenves, President Dr. Judith Langlois, Executive Vice President and Provost (Interim) Dr. Patricia L. Clubb, Vice President for University Operations Ms. Patricia C. Ohlendorf, Vice President for Legal Affairs Dr. Juan M. Sanchez, Vice President for Research Dr. Gage E. Paine, Vice President for Student Affairs Ms. Mary E. Knight, CPA, Associate Vice President and Interim Chief Financial Officer Mr. Paul Liebman, Chief Compliance Officer, University Compliance Services Mr. Cameron D. Beasley, University Information Security Officer Mr. Tom Carter, Independent Member Ms. Lynn Utter, Independent Member Mr. Michael W. Vandervort, Director, Office oflnternal Audits Mr. J. Michael Peppers, Chief Audit Executive, University of Texas System

Director:

Associate Director

The University of Texas at Austin Office of Internal Audits

Michael Vandervort, CPA

Jeff Treichel, CPA

Assistant Directors: Angela Mccarter, CIA, CRMA *Chris Taylor, CIA, CISA Brandon Morales, CISA, CGAP Audit Manager:

Auditor III:

Auditor II:

Auditor I:

Sr. IT Auditor:

Cynthia Martin-Hajmasy, CPA Ashley Oheim, CPA

*Stephanie Grayson Miranda Pruett, CFE

Jason Boone Bobby Castillo Kerri Jordan

Tod Maxwell, CISA, CISSP

*denotes project members

This report has been distributed to Internal Audit Committee members, the Legislative Budget Board, the State Auditor's Office, the Sunset Advisory Commission, the Governor's Office of Budget and Planning, and The University of Texas System Audit Office for distribution to the Audit, Compliance, and Management Review Committee of the Board of Regents.

FY 2014 Departmental Change in Management Audit: Department of Chemistry Project Number: 14.104

OFFICE OF INTERNAL AUDITS

THE UNIVERSITY OF TEXAS AT AUSTIN

1616 Guadalupe Street, Suite 2.302 ·Austin, TX 78701·(512)471-7117 •FAX (512) 471-8099

July 13, 2015

President Gregory L. F enves The University of Texas at Austin Office of the President P.O. Box T Austin, Texas 78713

Dear President F enves,

We have completed our audit of the Department of Chemistry (Chemistry). Our scope included controls and operations in place for fiscal year 2014.

Based on the procedures performed, we conclude that Chemistry has reasonable to strong controls in place in most of the areas reviewed. However, opportunities for improvement were noted for general department information/organization/activities, account reconciliation, cash and cash equivalent handling, travel, purchasing, and procurement cards. Our audit report provides detailed observations for the areas under review. Suggestions are offered throughout the report for improvements in the existing control structure.

We appreciate the cooperation and assistance of Chemistry throughout the audit and hope that the information presented herein is beneficial.

s~ cu Michael W. Vandervort, CPA Director

cc: Internal Audit Committee Members Ms. Nancy Brazzi!, Deputy to the President and Chief of Staff, Office of the

President Dr. Linda Hicke, Dean, College of Natural Sciences Dr. Stephen Martin, Department of Chemistry Chair (Interim), College of

Natural Sciences Mr. Jeff Treichel, Associate Director, Office of Internal Audits

FY 2014 Departmental Change in Management: Department of Chemistry July 2015

TABLE OF CONTENTS

Executive Summary ............................................................................................................. 1

Background .......................................................................................................................... 2

Scope, Objectives, and Procedures ...................................................................................... 2

Audit Results ........................................................................................................................ 3

Conclusion ........................................................................................................................... 8

Appendix .............................................................................................................................. 9

FY 2014 Departmental Change in Management: Department of Chemistry July 2015

EXECUTIVE SUMMARY

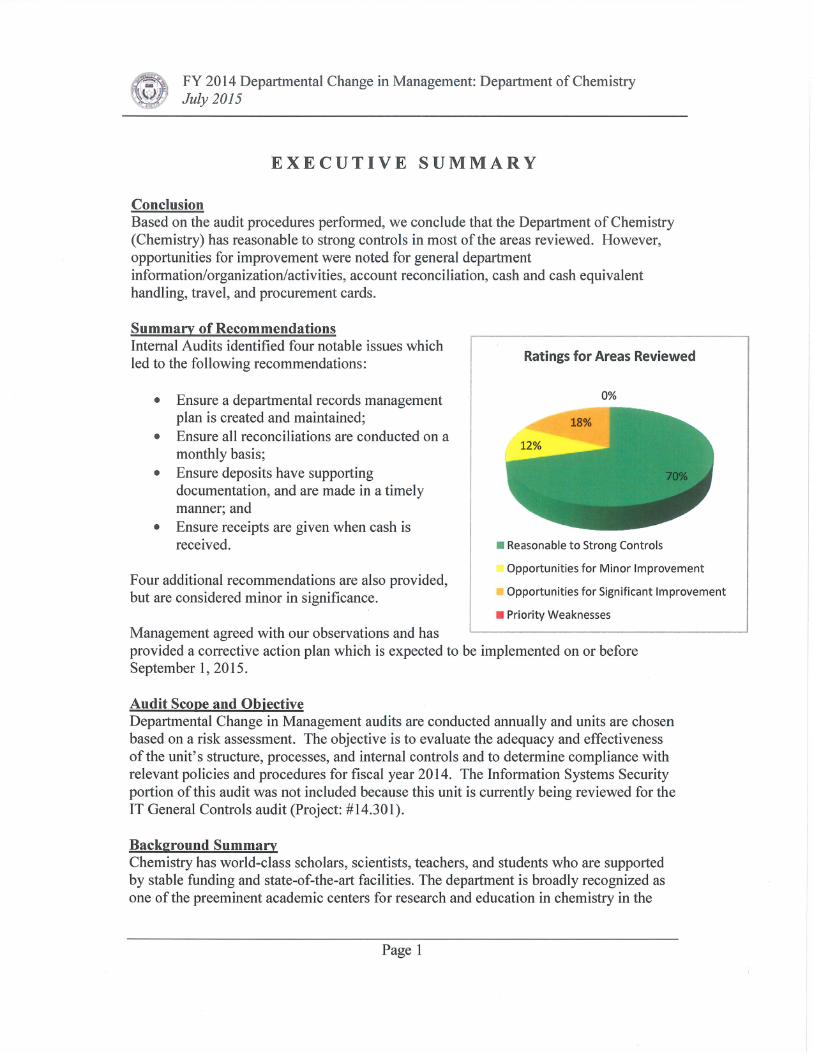

Conclusion Based on the audit procedures performed, we conclude that the Department of Chemistry (Chemistry) has reasonable to strong controls in most of the areas reviewed. However, opportunities for improvement were noted for general department information/organization/activities, account reconciliation, cash and cash equivalent handling, travel, and procurement cards.

Summary of Recommendations Internal Audits identified four notable issues which led to the following recommendations:

• Ensure a departmental records management plan is created and maintained;

• Ensure all reconciliations are conducted on a monthly basis;

• Ensure deposits have supporting documentation, and are made in a timely manner; and

• Ensure receipts are given when cash is received.

Four additional recommendations are also provided, but are considered minor in significance.

Management agreed with our observations and has

Ratings for Areas Reviewed

0%

• Reasonable to Strong Controls

Opportunities for Minor Improvement

Opportunities for Significant Improvement

• Priority Weaknesses

provided a corrective action plan which is expected to be implemented on or before September 1, 2015.

Audit Scope and Objective Departmental Change in Management audits are conducted annually and units are chosen based on a risk assessment. The objective is to evaluate the adequacy and effectiveness of the unit's structure, processes, and internal controls and to determine compliance with relevant policies and procedures for fiscal year 2014. The Information Systems Security portion of this audit was not included because this unit is currently being reviewed for the IT General Controls audit (Project: #14.301).

Background Summary Chemistry has world-class scholars, scientists, teachers, and students who are supported by stable funding and state-of-the-art facilities. The department is broadly recognized as one of the preeminent academic centers for research and education in chemistry in the

Page 1

FY 2014 Departmental Change in Management: Department of Chemistry July 2015

country. Chemistry has a budget of approximately $12.4 million and is a part of the College of Natural Sciences.

BACKGROUND

The Department of Chemistry (Chemistry) has world-class scholars, scientists, teachers, and students who are supported by stable funding and state-of-the-art facilities. The department is broadly recognized as one of the preeminent academic centers for research and education in chemistry in the country.

Chemistry has state-of-the-art mass spectrometry facilities, NMR facilities, X-ray crystallographic facilities and a center for multimedia support. The department has 29 faculty members, many who have received prestigious appointments and awards in their fields. Chemistry conducts research in several areas such as Bioanalytics, Chemical biology, Chemical physics and dynamics, Drug discovery, and Surface chemistry.

Chemistry has responsibility for both undergraduate and graduate programs. In fall 2014, the undergraduate program admitted 634 students and the graduate program admitted 220 students. Chemistry has a budget of approximately $12.4 million and is part of the College of Natural Sciences.

For management ofIT resources, Chemistry uses College of Natural Sciences' Office of Information Technology.

SCOPE, OBJECTIVES, AND PROCEDURES

The scope of this review includes controls and operations of the department currently in place for the fiscal year 2014. Our objectives were to evaluate the adequacy and effectiveness of the unit's structure, processes, and internal controls and to determine compliance with relevant policies and procedures. The Information Systems Security portion of this audit was not included because this unit is currently being reviewed for the IT General Controls audit (Project: #14.301).

To achieve these objectives, Internal Audits:

• Surveyed the unit via a questionnaire to ascertain reported strength in internal controls and compliance with The University of Texas at Austin (UT Austin) rules;

• Reviewed the department's electronic office structure and employees' appointment statuses;

• Conducted limited testing on payroll, account certifications, account reconciliations, cash and cash equivalent handling, inventory, purchasing,

Page2

FY 2014 Departmental Change in Management: Department of Chemistry July 2015

procurement card expenditures, travel expenditures, and entertainment and official occasion expenditures; and

• Clarified follow-up issues through e-mails, meetings, and other correspondence.

This audit was conducted in accordance with the International Standards for the Professional Practice of Internal Auditing and with Government Auditing Standards.

AUDIT RESULTS

We reviewed internal controls in 20 areas regarding departmental operations and financial processes, of which three areas were not applicable to Chemistry. The appendix provides information on the specific areas reviewed. The following were the results:

• 12 (70%) areas had reasonable to strong controls in place, • 2 (12%) areas had opportunities for minor improvements, • 3 (18%) areas had an opportunity for significant improvement, and • 0 (0%) areas have priority weaknesses.

Recommendations were made in areas where opportunities for improvement were noted and are detailed in the remainder of this report.

General Department Information/Organization/Activities - Records Management Plan The unit currently does not have a departmental records management plan. The unit said that due to staff reductions, creating and implementing a departmental plan has been a challenge, and has not been completed. Without having a departmental records management plan in place, there is an increased risk that the department is not following UT Austin's records management policy.

According to Section 20.4.3 of UT Austin's Handbook of Business Procedures, "Each departmental records management contact (DRMC) at The University of Texas at Austin is responsible for creating a records management plan to provide information about how the department will enact university records management policy."

Recommendation 1: Management should ensure that a departmental records management plan is created and maintained.

Management's Corrective Action Plan: A process to comply with the policy will be developed and implemented. Responsible Person: Assistant Director Planned Implementation Date: September 1, 2015

Post Audit Review: Internal Audits will perform its review in September 2015.

Page 3

FY 2014 Departmental Change in Management: Department of Chemistry July 2015

Account Reconciliation - Performance and Documentation The unit does not perform or document account reconciliations. The unit's current practice is to review random transactions using the Expense Certification process. Without conducting account reconciliations, there is an increased risk that financial records may be incorrect.

According to subcertification letter requirements for The University of Texas System Policy 142.1, the department should reconcile all accounts for each of the twelve months in a fiscal year. In addition, the policy also states that, the department head should review and approve all reconciliations, or delegate such review and approval, for the departmental accounts.

Recommendation 2: Management should ensure account reconciliations are being completed on a monthly basis. In addition, management should also ensure that all reconciliations are reviewed, signed, and dated by the unit head or a designated person.

Management's Corrective Action Plan: Effective January 2015, monthly account reconciliation is occurring.

Responsible Person: Assistant Director Planned Implementation Date: Complete as of January 2015

Post Audit Review: Internal Audits is in the process of conducting its post audit review.

Cash and Cash Equivalents Handling - Deposits Three (100%) of three deposits tested were not made in a timely manner. The unit was unaware of the policy regarding cash and check deposits. If deposits are not made in a timely manner, there is an increased risk of lost funds.

According to Section 6.5.B of UT Austin's Handbook of Business Procedures, "Deposits should be made daily if they are equal to or greater than $500. Deposits should be made at least weekly even if the accumulated total is less than $500."

Recommendation 3: Management should ensure that cash and cash equivalents of $500 or more are deposited daily at the Bursar's Office and that all cash and cash equivalents are deposited at least weekly even if the accumulated total is less than $500.

Management's Corrective Action Plan: Effective March 2015, cash on hand is kept at or below $250. Amounts above that are deposited within 5 business days. Responsible Person: Assistant Director Planned Implementation Date: Complete as of March 2015

Page 4

FY 2014 Departmental Change in Management: Department of Chemistry July 2015

Post Audit Review: Internal Audits followed-up on this recommendation and requested that the department modify the corrective action plan to indicate that no cash will be kept on hand, or that the department will work with the Office of Accounting to properly secure the documentation permitting a petty cash fund. The Assistant Director responded on June 5, 2015, and said, "I will submit a petty cash request memo to the office of accounting."

Internal Audits will follow-up to make sure this letter has been obtained.

Cash and Cash Equivalents Handling - Receipts The unit does not provide a receipt when money is collected for sale of department t-shirts. The unit was unaware of the policy regarding the issuance of receipts. Without receipts, cash accepted may not be accurately documented and financial records may be incorrect.

According to Section 6.1.E.1 of UT Austin's Handbook of Business Procedures:

All "over-the-counter" collections of money for The University must be supported by pre-numbered receipts, pre-numbered tickets, or cash register tapes. Computer-generated bills shall also be pre-numbered unless the Office of Internal Audits certifies that other valid means of cash control are in use. The original copies of receipts are to be issued to the payors, and duplicate copies are to be retained for balancing with cash deposits and for audit purposes. The same principle applies to cash register tapesthe original is issued to the payor, and the duplicate (transaction) tape is retained. Departmental records are to be maintained on all event tickets used in accordance with normal procedures available from the Cashier's Office.

Recommendation 4: Management should ensure that pre-numbered receipts are given when cash, or another form of payment, is received for sale of department t-shirts. Management should also ensure that copies of these receipts are maintained for reconciliation and auditing purposes.

Management's Corrective Action Plan: A receipt book has been ordered and will be used immediately upon receipt.

Responsible Person: Assistant Director Planned Implementation Date: May 27, 2015

Post Audit Review: Internal Audits is in the process of conducting its post audit review.

Page 5

FY 2014 Departmental Change in Management: Department of Chemistry July 2015

Travel - Proper Approval One (20%) of the five travel document IDs tested did not have proper approval from an immediate supervisor prior to dates of travel. The unit mentioned that the individual associated with this travel document ID has most of his travel covered by outside sources, which leads to him submitting travel documents after the dates of travel have occurred. Without submission of a Request for Travel Authorization (RTA) to an immediate supervisor, the supervisor may not be aware that an employee is absent from campus for business travel.

According to Section 11.2.A of UT Austin's Handbook of Business Procedures, "Prior approval for all business travel is required for absences of employees from the campus or other designated headquarters for periods of half a day or more during the normal working period, whether or not there is a cost to The University .... Approval is delegated to the immediate supervisor."

Recommendation 5: Management should ensure that travel authorizations are properly approved by an immediate supervisor prior to the dates of travel.

Management's Corrective Action Plan: This occurs only when faculty request an RTA after travel has occurred. We will continue to work with faculty on this.

Responsible Person: Assistant Director Planned Implementation Date: May 27, 2015

Post Audit Review: Internal Audits is in the process of conducting its post audit review.

Procurement Cards - Official Occasion Expense Form Documentation Seven (44%) of the 16 Procurement Card transactions tested did not have proper Official Occasion Expense Form (OOEF) documentation for purchases coded as 1347 (Official Occasion or Administrative/Business Meeting). The OOEF forms were either not created, or were not approved by the dean's office. The unit's current process does not ensure that OOEF documentation is created and approved for these purchases. Without proper documentation, UT Austin funds may be used to pay for disallowed items and events and may necessitate a refund by the department.

According to Procurement Card Program policies and guidelines, "To purchase some items, the cardholder must also obtain the written permission of their Dean or Chairman in advance of the purchase. A special occasions form must be completed for each function where the Procurement Card is used to make purchases such as food for parties, celebrations, etc. that are not routine events."

Page 6

FY 2014 Departmental Change in Management: Department of Chemistry July 2015

Recommendation 6: Management should ensure that for all entertainmentrelated purchases made with Procurement Cards, an OOEF is created and approved by the dean's office.

Management's Corrective Action Plan: Communications to procard holders have been sent. Procard mgr [sic] will ensure compliance.

Responsible Person: Assistant Director Planned Implementation Date: May 27, 2015

Post Audit Review: Internal Audits is in the process of conducting its post audit review.

Procurement Cards - Goods/Services Received Twelve (75%) of the 16 Procurement Card transactions tested did not have documentation providing the verification of receipt of goods. The unit's current practice does not include procurement card purchases having documentation verifying receipt of goods. Without reviewing and documenting the verification of receipt of goods, there is an increased risk that goods purchased with UT Austin funds may not be received or used to conduct UT Austin business.

According to Section 7.8 of UT Austin's Handbook of Business Procedures, Procurement Card Program, "In order to maintain internal controls, an employee other than the cardholder (but in the same department) is responsible for verifying the receipt of the goods or services purchased. Receipt of goods and services must be documentedsome examples of acceptable documentation are noting the date on the associated receipt or retaining the packing slip."

Recommendation 7: Management should ensure that evidence of goods/services received is documented with a signature and date of the responsible individual.

Management's Corrective Action Plan: Receipts for procard purchases will be signed and dated when goods are received.

Responsible Person: Accounting and Procurement Manager Planned Implementation Date: May 27, 2015

Post Audit Review: Internal Audits is in the process of conducting its post audit review.

Procurement Cards - Disallowed Purchases One (6%) of the 16 Procurement Card transactions tested was for a retirement cake, which is a disallowed purchase. The unit was not aware that the cake was a disallowed

Page 7

FY 2014 Departmental Change in Management: Department of Chemistry July 2015

purchase. Without proper review of guidance on disallowed items, UT Austin funds may be used to purchase disallowed items and may necessitate a refund by the department.

According to Section 7.8.C.2 of UT Austin's Handbook of Business Procedures, Procurement Card Program:

The Procard may not be used for some types of purchases. For questions about whether a purchase is allowed, contact the procurement card administrator. Examples of items typically disallowed are:

• alcoholic beverages • entertainment or travel • food (including catering services) • communication design services • consulting services • controlled substances, cylinder gasses, hazardous chemicals,

radioactive material • animals

Recommendation 8: Management should ensure only allowable purchases are made with Procurement Cards.

Management's Corrective Action Plan: A communication to procard holders has been sent. Procard mgr [sic] will ensure compliance.

Responsible Person: Accounting and Procurement Manager Planned Implementation Date: May 27, 2015

Post Audit Review: Internal Audits is in the process of conducting its post audit review.

CONCLUSION Based on the audit procedures performed, we conclude that Chemistry has reasonable to strong controls in most of the areas reviewed. However, opportunities for improvement were noted for general department information/organization/activities, account reconciliation, cash and cash equivalent handling, travel, and procurement cards.

In accordance with directives from The University of Texas System Board of Regents, the Office of Internal Audits will perform follow-up procedures to confirm that audit recommendations have been implemented.

Page 8

FY 2014 Departmental Change in Management: Department of Chemistry July 2015

A PP EN DIX

Electronic Office Structure

General Departmental Information/Organization/Activities

Payroll/HR

Account Reconciliation

Endowed Positions /Gift Administration

Outside Employment/Conflict of Interest

Cash and Cash Equivalent Handling

Cash Registers/Cashiers

Petty Cash

Accounts Receivable

Merchandise for Resale

Inventory

Controlled Items

Purchasing Activities

Authorization for Individual Services

Contracts

Procurement Cards

Travel Expenditures

Entertainment and Official Occasion Expenditures

Information Systems Security

[1] A priority weakness thats ignificantly impacts UT Austin's operations or finances will be

reported to UT System

Page 9