gamuda berhad : field report: tan thang looking to sell like “hot pho” - 8/6/2010

TRANSCRIPT

8/9/2019 Gamuda Berhad : Field Report: Tan Thang Looking To Sell Like “Hot Pho” - 8/6/2010

http://slidepdf.com/reader/full/gamuda-berhad-field-report-tan-thang-looking-to-sell-like-hot-pho 1/7

Page 1 of 7

A comprehensive range of market research reports by award-winning economists and analysts are exclusivelyavailable for download from w w w . r h b i n v e s t . c o m

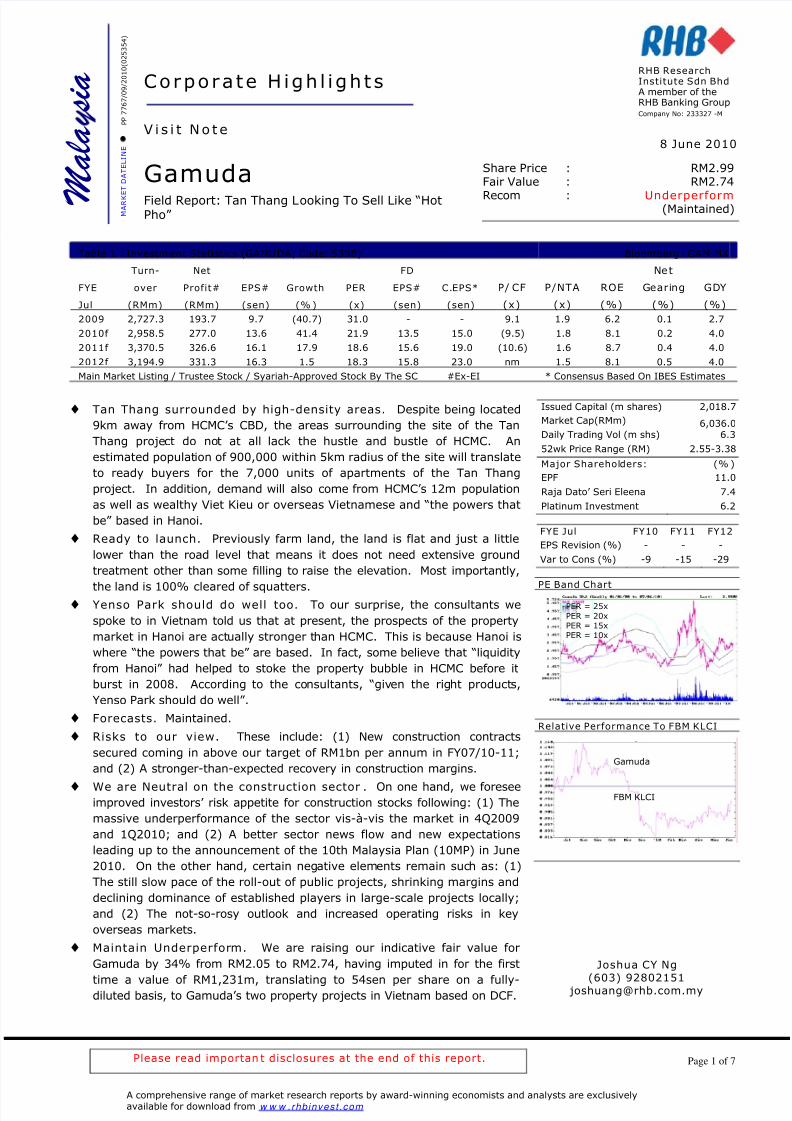

Table 1 : Investment Statistics (GAMUDA; Code: 5398) Bloomberg : GAM MK

Turn- Net FD Net

FYE over Profit# EPS# Growth PER EPS# C.EPS* P/ CF P/NTA ROE Gearing GDY

Jul (RMm) (RMm) (sen) (% ) (x) (sen) (sen) (x) (x) (%) (%) (%)

2009 2,727.3 193.7 9.7 (40.7) 31.0 - - 9.1 1.9 6.2 0.1 2.7

2010f 2,958.5 277.0 13.6 41.4 21.9 13.5 15.0 (9.5) 1.8 8.1 0.2 4.0

2011f 3,370.5 326.6 16.1 17.9 18.6 15.6 19.0 (10.6) 1.6 8.7 0.4 4.0

2012f 3,194.9 331.3 16.3 1.5 18.3 15.8 23.0 nm 1.5 8.1 0.5 4.0

Main Market Listing / Trustee Stock / Syariah-Approved Stock By The SC #Ex-EI * Consensus Based On IBES Estimates

♦ Tan Thang surrounded by high-density areas. Despite being located

9km away from HCMC’s CBD, the areas surrounding the site of the Tan

Thang project do not at all lack the hustle and bustle of HCMC. An

estimated population of 900,000 within 5km radius of the site will translate

to ready buyers for the 7,000 units of apartments of the Tan Thang

project. In addition, demand will also come from HCMC’s 12m population

as well as wealthy Viet Kieu or overseas Vietnamese and “the powers that

be” based in Hanoi.

♦ Ready to launch. Previously farm land, the land is flat and just a little

lower than the road level that means it does not need extensive ground

treatment other than some filling to raise the elevation. Most importantly,

the land is 100% cleared of squatters.♦ Yenso Park should do well too. To our surprise, the consultants we

spoke to in Vietnam told us that at present, the prospects of the property

market in Hanoi are actually stronger than HCMC. This is because Hanoi is

where “the powers that be” are based. In fact, some believe that “liquidity

from Hanoi” had helped to stoke the property bubble in HCMC before it

burst in 2008. According to the consultants, “given the right products,

Yenso Park should do well”.

♦ Forecasts. Maintained.

♦ Risks to our view. These include: (1) New construction contracts

secured coming in above our target of RM1bn per annum in FY07/10-11;

and (2) A stronger-than-expected recovery in construction margins.

♦ We are Neutral on the construction sector . On one hand, we foreseeimproved investors’ risk appetite for construction stocks following: (1) The

massive underperformance of the sector vis-à-vis the market in 4Q2009

and 1Q2010; and (2) A better sector news flow and new expectations

leading up to the announcement of the 10th Malaysia Plan (10MP) in June

2010. On the other hand, certain negative elements remain such as: (1)

The still slow pace of the roll-out of public projects, shrinking margins and

declining dominance of established players in large-scale projects locally;

and (2) The not-so-rosy outlook and increased operating risks in key

overseas markets.

♦ Maintain Underperform. We are raising our indicative fair value for

Gamuda by 34% from RM2.05 to RM2.74, having imputed in for the first

time a value of RM1,231m, translating to 54sen per share on a fully-diluted basis, to Gamuda’s two property projects in Vietnam based on DCF.

Corpora te H igh l ights

V i s i t No t e

GamudaField Report: Tan Thang Looking To Sell Like “HotPho” M

a l a s i a RHB Research

Institute Sdn BhdA member of theRHB Banking GroupCompany No: 233327 -M

8 June 2010

Share Price : RM2.99Fair Value : RM2.74

Recom : Underperform (Maintained)

Issued Capital (m shares) 2,018.7

Market Cap(RMm) 6,036.0Daily Trading Vol (m shs) 6.3

52wk Price Range (RM) 2.55-3.38

Major Shareholders: (% )

EPF 11.0

Raja Dato’ Seri Eleena 7.4

Platinum Investment 6.2

FYE Jul FY10 FY11 FY12

EPS Revision (%) - - -

Var to Cons (%) -9 -15 -29

PE Band Chart

Relative Performance To FBM KLCI

Joshua CY Ng

(603) 92802151 [email protected]

M A R K

E T

D A T E L I N E

P P

7 7 6 7 / 0 9 / 2 0 1 0 ( 0 2 5 3 5 4 )

Please read importan t disclosures at the end of this report.

Gamuda

FBM KLCI

PER = 25x

PER = 20x

PER = 15x

PER = 10x

8/9/2019 Gamuda Berhad : Field Report: Tan Thang Looking To Sell Like “Hot Pho” - 8/6/2010

http://slidepdf.com/reader/full/gamuda-berhad-field-report-tan-thang-looking-to-sell-like-hot-pho 2/7

8 June 2010

Page 2 of 7

A comprehensive range of market research reports by award-winning economists and analysts are exclusivelyavailable for download from w w w . r h b i n v e s t . c o m

Field Report: Tan Thang Looking To Sell Like “Hot Pho”

♦ Highlights. Key takeaways/observations during our recent visit to Ho Chi Minh City (HCMC) including the site

of Gamuda’s RM6bn Tan Thang project in HCMC are:

1. We can confirm that the areas surrounding the site of the Tan Thang project are densely populated. This

dense population base translates to ready buyers for the Tan Thang project; and

2. Our conversation with consultants from the HCMC office of an international property consulting firm gave us

the comfort that Gamuda’s RM10bn Yenso Park in Hanoi should do well too.

Dense population in surround ing areas translates to ready buyers for Tan Thang

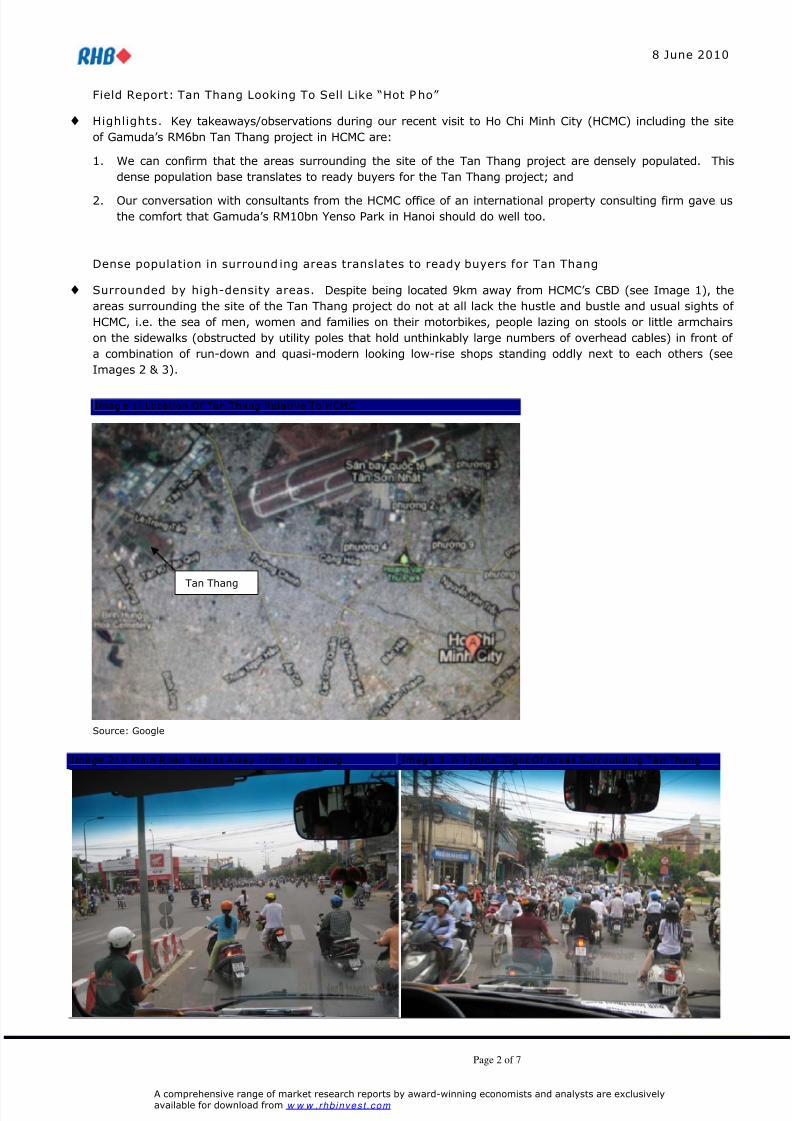

♦ Surrounded by high-density areas. Despite being located 9km away from HCMC’s CBD (see Image 1), the

areas surrounding the site of the Tan Thang project do not at all lack the hustle and bustle and usual sights of

HCMC, i.e. the sea of men, women and families on their motorbikes, people lazing on stools or little armchairs

on the sidewalks (obstructed by utility poles that hold unthinkably large numbers of overhead cables) in front of

a combination of run-down and quasi-modern looking low-rise shops standing oddly next to each others (see

Images 2 & 3).

Image 1: Location Of Tan Thang Relative To HCMC

Source: Google

Image 2: A Main Road Metres Away From Tan Thang Image 3: A Typical Sight Of Areas Surrounding Tan Thang

Tan Thang

8/9/2019 Gamuda Berhad : Field Report: Tan Thang Looking To Sell Like “Hot Pho” - 8/6/2010

http://slidepdf.com/reader/full/gamuda-berhad-field-report-tan-thang-looking-to-sell-like-hot-pho 3/7

8 June 2010

Page 3 of 7

A comprehensive range of market research reports by award-winning economists and analysts are exclusivelyavailable for download from w w w . r h b i n v e s t . c o m

♦ Huge population base. We understand that there is an estimated population of 900,000 within 5km radius of

the site. This 900,000-strong localised population will translate to ready buyers for the 7,000 units of

apartments (comprising 4,500 mid-priced units and 2,500 high-end units) of the Tan Thang project over the

next seven years. In addition, demand will also come from HCMC’s 12m population (including 3m migrant

workers) as well as wealthy Viet Kieu or overseas Vietnamese and “the powers that be” based in Hanoi.

Gamuda intends to price the mid-priced apartments at US$1,100 psm while the high-end apartments at

US$1,700 psm. Our conversation with consultants from the HCMC office of an international property consulting

firm gave us the impression that the pricing for the mid-priced apartments is reasonable, at only 10% premium

to the market rate of US$1,100 psm. We believe the premium is justifiable given the “extras” buyers are getting

including a massive 40-acre park, and various sporting and recreational facilities and amenities within the

development. However, the consultants we spoke to did think US$1,700 psm (for the high-end apartments) is

not quite the price the market is used to paying in that area.

♦ Ready to launch. Previously farm land, the land is flat and just a little lower than the road level that means it

does not need extensive ground treatment other than some filling to raise the elevation. The filling materials

can be partially sourced from excavation for car-park basements for the apartments. Most importantly, the land

is 100% cleared of squatters (see Images 4 & 5).

(

*According to our local tour guide, the sighting of snakes is rare and Vietnamese people believe it will bring good luck

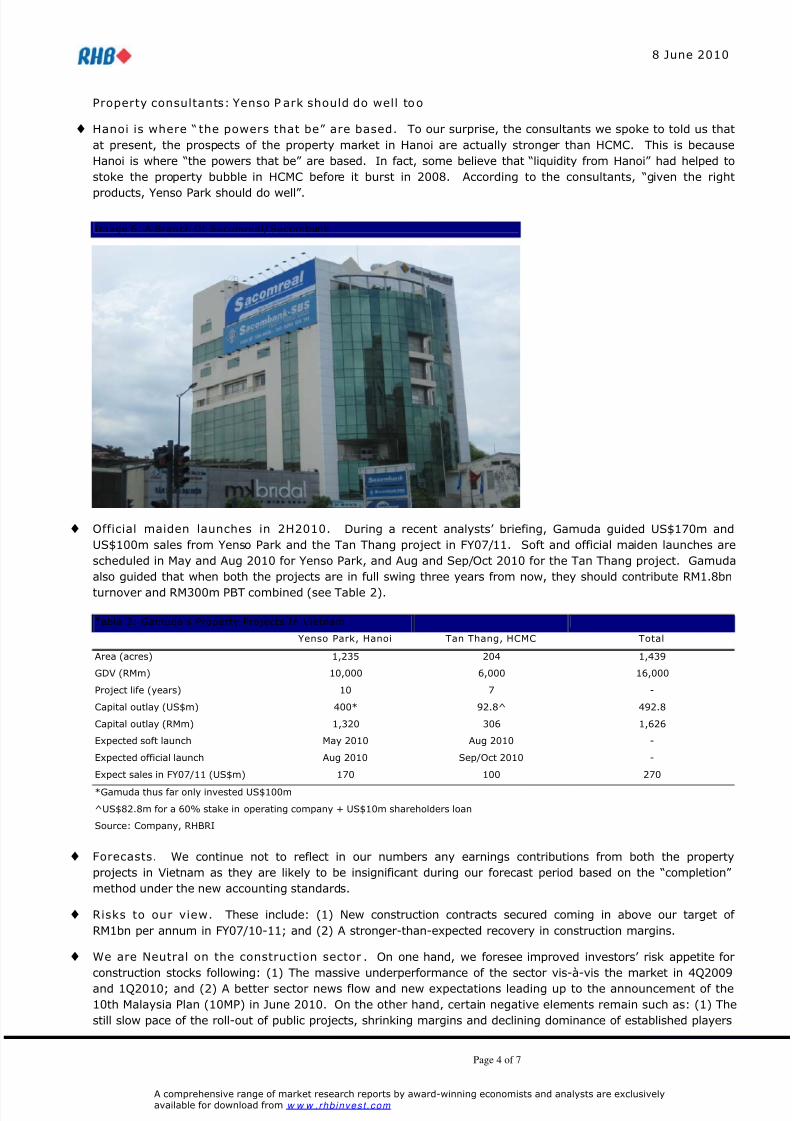

♦ Gamuda has a 60% stake. To recap, Gamuda in Mar 2010 proposed to pay US$82.8m (RM273m) for a 60%

stake in Tan Thang that holds the development rights for a piece of land measuring 204 acres at Son Ky Ward,

Tan Phu District, HCMC, Vietnam (9km from HCMC’s CBD and 3km from HCMC’s international airport). Tan

Thong has secured the key approvals from the authority to develop the land into a township comprising 7,000

apartments, a sports complex and an education centre with a total GDV of RM6bn over seven years. Other

shareholders of Tan Thang are Sacomreal (30%) and an individual (10%). Sacomreal is engaged in the

provision of real estate services and development of high-end apartments. Its sister company Sacombank is thelargest private commercial bank listed in Vietnam with 200 branches nationwide and a market capitalisation of

US$1bn (It was not difficult to find branches of Sacomreal and Sacombank in HCMC, for instance, see Image 6).

Gamuda was approached by Sacomreal about a year ago to become its JV partner for this project as Sacomreal

lacked the experience in township development and was impressed by Gamuda’s first property project in

Vietnam, i.e. Yenso Park in Hanoi.

Image 4: Passers-by Attracted To A “Snake Show” On TheSite*

Image 5: Flat Terrain And Free Of Squatters

8/9/2019 Gamuda Berhad : Field Report: Tan Thang Looking To Sell Like “Hot Pho” - 8/6/2010

http://slidepdf.com/reader/full/gamuda-berhad-field-report-tan-thang-looking-to-sell-like-hot-pho 4/7

8 June 2010

Page 4 of 7

A comprehensive range of market research reports by award-winning economists and analysts are exclusivelyavailable for download from w w w . r h b i n v e s t . c o m

Property consultants: Yenso P ark should do well too

♦ Hanoi is where “ the powers that be” are based. To our surprise, the consultants we spoke to told us that

at present, the prospects of the property market in Hanoi are actually stronger than HCMC. This is because

Hanoi is where “the powers that be” are based. In fact, some believe that “liquidity from Hanoi” had helped to

stoke the property bubble in HCMC before it burst in 2008. According to the consultants, “given the right

products, Yenso Park should do well”.

Image 6: A Branch Of Sacomreal/ Sacombank

♦ Official maiden launches in 2H2010. During a recent analysts’ briefing, Gamuda guided US$170m and

US$100m sales from Yenso Park and the Tan Thang project in FY07/11. Soft and official maiden launches are

scheduled in May and Aug 2010 for Yenso Park, and Aug and Sep/Oct 2010 for the Tan Thang project. Gamuda

also guided that when both the projects are in full swing three years from now, they should contribute RM1.8bn

turnover and RM300m PBT combined (see Table 2).

Table 2: Gamuda’s Property Projects In Vietnam

Yenso Park, Hanoi Tan Thang, HCMC Total

Area (acres) 1,235 204 1,439

GDV (RMm) 10,000 6,000 16,000

Project life (years) 10 7 -

Capital outlay (US$m) 400* 92.8^ 492.8

Capital outlay (RMm) 1,320 306 1,626

Expected soft launch May 2010 Aug 2010 -

Expected official launch Aug 2010 Sep/Oct 2010 -

Expect sales in FY07/11 (US$m) 170 100 270

*Gamuda thus far only invested US$100m

^US$82.8m for a 60% stake in operating company + US$10m shareholders loan

Source: Company, RHBRI

♦ Forecasts. We continue not to reflect in our numbers any earnings contributions from both the property

projects in Vietnam as they are likely to be insignificant during our forecast period based on the “completion”

method under the new accounting standards.

♦ Risks to our view. These include: (1) New construction contracts secured coming in above our target of

RM1bn per annum in FY07/10-11; and (2) A stronger-than-expected recovery in construction margins.

♦ We are Neutral on the construction sector. On one hand, we foresee improved investors’ risk appetite for

construction stocks following: (1) The massive underperformance of the sector vis-à-vis the market in 4Q2009

and 1Q2010; and (2) A better sector news flow and new expectations leading up to the announcement of the

10th Malaysia Plan (10MP) in June 2010. On the other hand, certain negative elements remain such as: (1) The

still slow pace of the roll-out of public projects, shrinking margins and declining dominance of established players

8/9/2019 Gamuda Berhad : Field Report: Tan Thang Looking To Sell Like “Hot Pho” - 8/6/2010

http://slidepdf.com/reader/full/gamuda-berhad-field-report-tan-thang-looking-to-sell-like-hot-pho 5/7

8 June 2010

Page 5 of 7

A comprehensive range of market research reports by award-winning economists and analysts are exclusivelyavailable for download from w w w . r h b i n v e s t . c o m

in large-scale projects locally; and (2) The not-so-rosy outlook and increased operating risks in key overseas

markets (following the Dubai credit crisis, Dong’s devaluation and rising arbitration cases).

♦ Fair value raised to RM2.74. We are raising our indicative fair value for Gamuda by 34% from RM2.05 to

RM2.74, having imputed in for the first time a value of RM1,231m, translating to 54sen per share on a fully-

diluted basis, to Gamuda’s two property projects in Vietnam based on DCF (see Table 3). We have also rolled

forward the base year for valuation purpose from CY10 to fully-diluted CY11 (to reflect 252.3m newly listed

warrants). Despite the upward revision in indicative fair value, Gamuda remains an Underperform as upside in

share price has already been exhausted.

Table 3: Sum-Of-Parts Valu ation

Segment RMm RM/shr Basis

Existing (ex-Vietnam) 5,023 2.20 14x fully-diluted CY11 net profit of RM358.8m or 15.7sen/shr

Vietnam 1,231 0.54 Yenso Park, Hanoi: GDV of RM10bn and project life of 10 yearsTan Thang, HCMC: GDV of RM6bn and project life of 7 yearsPBT margin of 25%, tax rate of 25% and benchmark discount rate of 10% for propertyprojects. A 30% discount to NPV of RM1,759m to reflect country risk

Total 6,254 2.74

Table 4: Outstanding Construction OrderbookProject Balance Of Works (RMbn)

Ipoh – Padang Besar double-tracking project 3.8

Nam Thuen 1 hydroelectric project 1.8

Yenso Park Infrastructure works 0.9

Outstanding works in the Gulf states 0.5

Total 7.0

Source: Company

Table 5: Earnings Forecasts Table 6: Forecast Assumptions

FYE Jul (RMm) FY09a FY10F FY11F FY12F FYE Jul FY10F FY11F FY12F

Turnover 2,727.3 2,958.5 3,370.5 3,194.9 Construction EBIT margin (%) 4.1 7.2 8.8

Turnover growth (%) 13.5 8.5 13.9 -5.2 New orderbook secured (RMbn) 1.0 1.0 2.0

EBITDA 197.9 257.3 363.6 397.1EBITDA margin (%) 7.3 8.7 10.8 12.4

Depreciation -14.1 -14.8 -15.6 -16.4Net Interest -44.8 -38.2 -76.6 -101.7Associates 143.2 176.2 176.2 176.2

EI 0.0 0.0 0.0 0.0

Pretax Profit 282.2 380.4 447.6 455.2

Tax -78.0 -95.1 -111.9 -113.8

PAT 204.2 285.3 335.7 341.4Minorities -10.5 -8.3 -9.2 -10.1Net Profit 193.7 277.0 326.6 331.3Source: Company data, RHBRI estimates

8/9/2019 Gamuda Berhad : Field Report: Tan Thang Looking To Sell Like “Hot Pho” - 8/6/2010

http://slidepdf.com/reader/full/gamuda-berhad-field-report-tan-thang-looking-to-sell-like-hot-pho 6/7

Page 6 of 7

A comprehensive range of market research reports by award-winning economists and analysts are exclusivelyavailable for download from w w w . r h b i n v e s t . c o m

IMP ORTANT DISCLOSURES

This report has been prepared by RHB Research Institute Sdn Bhd (RHBRI) and is for private circulation only to clients of RHBRI and RHB Investment Bank Berhad(previously known as RHB Sakura Merchant Bankers Berhad). It is for distribution only under such circumstances as may be permitted by applicable law. Theopinions and information contained herein are based on generally available data believed to be reliable and are subject to change without notice, and may differ orbe contrary to opinions expressed by other business units within the RHB Group as a result of using different assumptions and criteria. This report is not to beconstrued as an offer, invitation or solicitation to buy or sell the securities covered herein. RHBRI does not warrant the accuracy of anything stated herein in anymanner whatsoever and no reliance upon such statement by anyone shall give rise to any claim whatsoever against RHBRI. RHBRI and/or its associated personsmay from time to time have an interest in the securities mentioned by this report.

This report does not provide individually tailored investment advice. It has been prepared without regard to the individual financial circumstances and objectivesof persons who receive it. The securities discussed in this report may not be suitable for all investors. RHBRI recommends that investors independently evaluateparticular investments and strategies, and encourages investors to seek the advice of a financial adviser. The appropriateness of a particular investment orstrategy will depend on an investor’s individual circumstances and objectives. Neither RHBRI, RHB Group nor any of its affiliates, employees or agents acceptsany liability for any loss or damage arising out of the use of all or any part of this report.

RHBRI and the Connected Persons (the “RHB Group”) are engaged in securities trading, securities brokerage, banking and financing activities as well as providinginvestment banking and financial advisory services. In the ordinary course of its trading, brokerage, banking and financing activities, any member of the RHBGroup may at any time hold positions, and may trade or otherwise effect transactions, for its own account or the accounts of customers, in debt or equitysecurities or loans of any company that may be involved in this transaction.

“Connected Persons” means any holding company of RHBRI, the subsidiaries and subsidiary undertaking of such a holding company and the respective directors,officers, employees and agents of each of them. Investors should assume that the “Connected Persons” are seeking or will seek investment banking or other

services from the companies in which the securities have been discussed/covered by RHBRI in this report or in RHBRI’s previous reports.

This report has been prepared by the research personnel of RHBRI. Facts and views presented in this report have not been reviewed by, and may not reflectinformation known to, professionals in other business areas of the “Connected Persons,” including investment banking personnel.

The research analysts, economists or research associates principally responsible for the preparation of this research report have received compensation basedupon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues.

The recommendation framework for stocks and sectors are as follows : -

Stock Ratings

Outperform = The stock return is expected to exceed the FBM KLCI benchmark by greater than five percentage points over the next 6-12 months.

Trading Buy = Short-term positive development on the stock that could lead to a re-rating in the share price and translate into an absolute return of 15% or moreover a period of three months, but fundamentals are not strong enough to warrant an Outperform call. It is generally for investors who are willing to take onhigher risks.

Market Perform = The stock return is expected to be in line with the FBM KLCI benchmark (+/- five percentage points) over the next 6-12 months.

Underperform = The stock return is expected to underperform the FBM KLCI benchmark by more than five percentage points over the next 6-12 months.

Industry/Sector Ratings

Chart 1: Gamuda Technical View P oint

♦ The share price of Gamuda reached a high of

RM3.44 in Aug 2009, before congesting around

RM3.06 – RM3.33 from Aug to Nov 2009.

♦ In late Nov, volatility increased when the stock

plunged below RM3.06 to a low of RM2.58 in Dec,

near a support of RM2.59.

♦ The stock later staged a recovery, but met a tough

support-turned-resistance level at RM3.06 in Apr

2010.

♦ As a result, it fell again to a low of RM2.70 in late

May.

♦ In recent trading, the stock regained some

momentum and trended closer to RM3.06. It closed

at RM2.99 yesterday.

♦ Recorded with a “bullish engulfing” candle on the

chart, and the upticks on the momentumindicators, it is poised to retest RM3.06 soon.

♦ However, we are of the view that it has yet to

accumulate enough momentum to break through

the heavy resistance. As such, we see limited

upside ahead to RM3.06.

8/9/2019 Gamuda Berhad : Field Report: Tan Thang Looking To Sell Like “Hot Pho” - 8/6/2010

http://slidepdf.com/reader/full/gamuda-berhad-field-report-tan-thang-looking-to-sell-like-hot-pho 7/7

Page 7 of 7

A comprehensive range of market research reports by award winning economists and analysts are exclusively

Overweight = Industry expected to outperform the FBM KLCI benchmark, weighted by market capitalisation, over the next 6-12 months.

Neutral = Industry expected to perform in line with the FBM KLCI benchmark, weighted by market capitalisation, over the next 6-12 months.

Underweight = Industry expected to underperform the FBM KLCI benchmark, weighted by market capitalisation, over the next 6-12 months.

RHBRI is a participant of the CMDF-Bursa Research Scheme and will receive compensation for the participation. Additional information on recommendedsecurities, subject to the duties of confidentiality, will be made available upon request.

This report may not be reproduced or redistributed, in whole or in part, without the written permission of RHBRI and RHBRI accepts no liability whatsoever for theactions of third parties in this respect.