gan direct insurance limited solvency & financial ... · name and legal form of undertaking gan...

TRANSCRIPT

GAN DIRECT INSURANCE LIMITED Solvency & Financial Condition Report (‘’SFCR’’)

2016 (Revised - Audited)

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

2/SFCR

Contents Summary 3 A. Business and Performance 4 A.1 Business 4 A.2 Underwriting Performance 6 A.3 Investment Performance 6 A.4 Performance of other Activities 7 A.5 Any other Information 7

B. System of Governance 8 B.1 General Information of the System of Governance 8 B.2 ‘Fit and Proper’ requirements 10 B.3 Risk Management System 11 B.4 Own Risk and Solvency Assessment (ORSA) 13 B.5 Internal Control System 14 B.6 Internal Audit Function 14 B.7 Actuarial Function 15 B.8 Outsourcing 15 B.9 Any Other Information – Quality Management System 16

C. Risk Profile 18 C.1 Underwriting Risk 18 C.2 Market Risk 20 C.3 Credit Risk/Counterparty Default Risk 23 C.4 Liquidity Risk 24 C.5 Operational Risk 24 C.6 Other Material Risks 25

D. Valuation for Solvency Purposes 26 D.1 Assets 26 D.2 Technical Provisions 27 D.3 Valuation of other liabilities 29 D.4 Alternative Methods 29

E. Capital Management 30 E.1 Own Funds 30 E.2 Solvency Capital Requirement and Minimum Capital Requirement 31 E.3 Any other Information 32

ANNEX: Annual Quantitative Reporting Templates (QRT’s) 33 S.02.01.02 Balance Sheet 34 S.05.01.02 Premiums, claims and expenses by line of business 36 S.05.02.01 Premiums claims and expenses by country 37 S.17.01.02 Non-Life Technical Provisions 39 S.19.01.21 Non-Life Insurance Claims 40 S.23.01.01 Own Funds 42 S.25.01.21 Solvency Capital Requirement – for Undertaking on Standard Formula 44 S.28.01.01 Minimum Capital Requirement – Only Non- Life Insurance or Reinsurance 45

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

3/SFCR

Summary The new, harmonised EU-wide regulatory regime for Insurance Companies, known as Solvency II, came into force with effect from 1 January 2016.The Regime requires new reporting and public disclosure arrangements to be put in place by insurers and some of that is required to be published on the Company’s public website. This document is the first version of the Solvency and Financial Condition Report (‘’SFCR’’) that is required to be published by Gan Direct Insurance Limited (Gan Direct or ‘the Company). This report covers the Business and Performance of the Company, its System of Governance, Risk Profile, Valuation for Solvency Purposes and Capital Management. The ultimate Administrative Body that has the responsibility for these matters is the Company’s Board of Directors (BoD), with the help of various governance and control functions that is has put in place to monitor and manage the business. Gan Direct Insurance Limited was founded in 2000 and is privately owned insurance company licenced in Cyprus. During 2016, it continued writing Non-Life business. Over the past few years, the respective Boards in the Company put in place measures to strengthen the corporate governance framework, including the risk management function, in readiness for Solvency II which was effective from 1 January 2016. The governance and risk frameworks are explained in more detail in this report. On 1 January 2016, the company smoothly transitioned into Solvency II (SII) regime following a lot of preparatory work over the last few years. Solvency II represents a shift to a more risk-based approach to the measurement and monitoring of capital for insurance companies in the European Union. The Company uses the standard formula to calculate its solvency requirement. The Company’s Solvency Capital Requirement at 31 December 2016 is Euro 5.82 million. This is covered by Euro 6.4 million of eligible capital resources providing a Solvency II surplus of Euro 0.58 million and a Solvency II coverage ratio of 110%. Both these metrics are defined to mean the excess of the Company’s total eligible own funds over its solvency capital requirement. The Company’s Financial Year runs to 31December each year and it reports its results in Euro.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

4/SFCR

A: Business and Performance A.1 Business This is the first Solvency and Financial Condition Report provided under European Commission delegated Regulation 2015/35 concerning the business of insurance and reinsurance (Solvency II). There is no summary of material changes as there is no previous report for comparison.

Lines of Business and geographical area Gan Direct Insurance Limited has the following lines of business

• Motor Vehicle liability insurance

• Other Motor Insurance

• Fire and Other Damage to property

• Income protection Insurance

• General Liability Insurance

• Marine, Cargo and Yacht The Company only writes business in Cyprus and remains focused on the individual customer business as it writes its business by maintaining and expanding a direct portfolio. The company specialises in selling insurance products directly to customers by telephone and the internet. The Company also maintains offices in Nicosia, Limassol, Larnaca, Paphos and Paralimni for sales and customer service and support. The Company is very well known in Cyprus for its distinctive logo, an orange telephone, regularly used in its marketing and for the tune of the free telephone line for customer service and support of 800 5 10 15. This business model of direct sales means that there are no intermediaries and therefore no commissions are paid. This saving on the commission expense is then passed onto the customers in terms of lower premiums.

Significant Business or other events over the reporting period There were no significant business or other events having a material impact on the Company.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

5/SFCR

Name and legal form of Undertaking Gan Direct Insurance Limited is a Cyprus registered company (Registration number 113668). The Company is licenced by the Cyprus Regulatory Authorities to carry on most classes of short term (that is, non-life) business and is a private company limited by shares. The registered office address is: Corner of Archbishop Makarios III 220 and Marikkas Kotopoulli, Limassol, Cyprus Tel: 00357 25 885 885 E-mail: [email protected] Fax:25 822 668

Name and contact details of the Supervisory Authority Superintendent of Insurance Cyprus Insurance Companies Control Service Ministry of Finance PO Box 23364,1682 Nicosia Cyprus Tel: 00357 22 602 990 Fax: 00357 22 302 938 E-mail: [email protected]

Name and contact details of external auditors KPMG Limited Esperidon Street 14, 1087 Nicosia P.O Box 21121 1502 Nicosia, Cyprus

Description of the holders of qualifying holdings.

There is only one shareholder who has 100% of the Company’s shares. The name of the shareholder is George Nicolaides.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

6/SFCR

A.2 Underwriting Performance The table below sets out the analysis of the underwriting results of the Company for the year ended 31 December 2016:

Underwriting Performance 2016 €'000

Motor Property Income Protection Other Total

Gross Written Premium 12,052 1,207 266 17 13,542

Net Earned Premium 11,176 448 60 17 11,701

Other Income 43 221 79 1 344

Total Earned Income 11,219 669 139 18 12,045

Net Claims Incurred 7,909 81 55 1 8,046

Expenses 3,402 366 83 4 3,855

Underwriting Profit -92 222 1 13 144 Gross written premium in 2016 was Euro 13.6 million compared to Euro 13.5 million in 2015. Net claims incurred in 2016 were Euro 8.0 million compared to Euro 7.7 million in 2015. Expenses in 2016 were Euro 3.9 million the same as for 2015. The underwriting result for 2016 was Euro 144K compared to 716K in 2015. This decrease in underwriting profit was mainly due to the increase in net claims incurred on Motor business and from the increase in unearned premiums provision resulting from the change in the accounting policy from the method of 24ths to the 365.

A.3 Investment Performance Income and expenses by asset class The table below sets out the major income and expenses by asset class.

Euros '000

2016 2015

Rental Income from properties 23 23

Interest from term deposits with banks 38 63

Change in the fair value of equity shares - -13

Gains recognised directly in Equity

Euros '000

2016 2015

Revaluation of land and buildings (net of deferred tax) 360 158

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

7/SFCR

A.4 Performance of other Activities The Company does not carry out any other activities.

A.5 Any other Information There is no other information to report.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

8/SFCR

B. System of Governance

B.1 General Information on the System of Governance

Board of Directors Gan Direct is managed by its Board of Directors, supported by an audit and risk committee and an Investment committee. The board of the Company is of sufficient size expertise to oversee adequately the operations of the Company. The Board of Directors meets quarterly and is charged with the strategic management of the company.

Audit and Risk Committee

The Audit and Risk Committee meets quarterly. The committee’s objective is to assist the Board of Directors and has the responsibility for three of the four key functions, namely Risk Management, Compliance and Internal Audit. The Committee also oversees the External Audit function.

Description of the main roles and responsibilities of key functions

The Company’s key Control Functions are partially undertaken through the Company’s resources with support of external consultants.

Risk and Compliance Function

The risk management and compliance function is responsible for facilitating the implementation of the Risk Management System of the Company and achieving the efficient and effective management of risk in accordance with the risk appetite of the Company, and ensuring compliance with external regulations and internal policies. Duties included under this function are in relation to the preparation of underwriting and reserving exercises, operational risk management, reinsurance, quantification of risk and capital allocation, and compliance with regulatory regime.

Internal Audit Function

The Internal Audit Function examines and reviews holistically key activities within selected risk areas of the Company and provides recommendations for improvement regarding the proper design and application of control to safeguard against potential loss emerging from probable inefficiencies within those selected areas. The internal audit evaluates and assesses the adequacy, appropriateness and effectiveness of all the Company’s internal control system and offer operations and provides suggestions for possible improvements.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

9/SFCR

Actuarial Function

The Actuarial Function advises the Risk Committee and the Board of Directors on the following:

• Underwriting policy

• Reinsurance arrangements of the company and their adequacy

• Valuation of technical provisions

• Capital adequacy

• Risk Management System The main duties of the Actuarial Function include:

• Coordination of the calculation of technical provisions

• Assess the quality and sufficiency of the data used for the calculation of technical provisions

• Compare best estimates against experience

• Risk modelling of capital requirement calculations

• Stress testing and sensitivity analysis The actuarial function was getting support from external consultants.

Changes in the system of governance

There were no material changes to the system of governance.

Remuneration policy The Company provides a fixed remuneration package and a range of benefits is offered to employees, including 13th salary, medical insurance and paid holiday arrangements, contributions to social insurance fund. The Company also pays a discretionary Easter Bonus in the form of a 14th salary up to one month’s gross salary. The amount paid, is based on a percentage scale depending on the number of years employed by the Company. Employees with over five years’ continuous employment receive a full 14th month salary. Remuneration of non-executive directors considers their attendance to Board of Directors and committee meetings and receive a nominal fee. The executive directors are also on a fixed salary. The Company does not offer any performance-based bonuses or incentives to executive directors. The Company considers that this remuneration practice for executive directors promotes sound and effective risk management and does not encourage excessive risk taking. There is no entitlement for Company options and shares and there is no supplementary pension on earlier retirement for any staff member.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

10/SFCR

B.2 Fit and Proper requirements Skills knowledge and expertise requirements In accordance with Solvency II Directive the Company has specified fit and proper requirements for persons who effectively run the business or hold other key functions. Basically, the persons above are the members of the Board of Directors and holders of the governance functions namely the risk management, compliance, internal audit and actuarial functions. There are however, different requirements for the members of the Board and different requirements for holders of other key functions.

Members of the Board of Directors To ensure that the members if the Board are fit for the position there are requirements which include a level of expertise and experience in the following areas:

• Insurance and financial markets

• Business strategy and business model

• Solvency II requirements for the system of governance

• Financial and actuarial analyses, and

• Regulatory frameworks and requirements

The Company applies the principle of collective professional skills, qualifications and experience. This means that not every member of the Board will meet all the above requirements but that the Board collectively meets the above requirements. This knowledge and experience is required to have a sound and prudent management. To ensure that the members of the Board are proper persons, the Company has the following requirements:

• no criminal record

• no breaches of legislation or regulations

• good personal conduct, reputation, financial integrity and honesty.

Process for assessing fitness and propriety

The Company has a policy to ensure that persons appointed to relevant roles are ‘’Fit and Proper’’. As part of that policy, various checks and procedures are listed which may be carried out before appointing an individual to a key position or to a position involving oversight of key functions. Those checks include:

• the completion by the applicant of a ‘’fit and proper’’ Declaration Form;

• the undertaking of credit checks to determine the status of the person’s credit record;

• undertaking of qualification checks to determine the authenticity of the person’s qualifications

• undertaking checks with any regulatory body tasked with administering any legislation;

• undertaking of checks to confirm the work experience that the person claims to have;

• undertaking of checks via the internet for any adverse information relating to the person.

A person will only be deemed fit and proper if it can be shown that:

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

11/SFCR

• it can reasonably be concluded that the person possesses the competence, character, diligence, honesty, integrity and judgement to properly perform their duties;

• the person is disqualified from acting in their position or performing their duties in terms of any legislation.

Holders of key function. Requirements to ensure that holders of key functions are fit persons include:

• appropriate level of qualifications necessary for the function

• technical knowledge and experience required for the function.

For the key functions that are also requirements to ensure that these individuals are proper persons which include:

• no criminal offences

• no breaches of legislation

• good personal conduct, reputation, financial integrity and honesty.

B.3 Risk Management System The risk management system is an integral part of the governance system. Its purpose is to identify, evaluate, manage and report the risks that Gan Direct is exposed to.

Risk management Process The risk management process provides information on risk situations and helps top management to place controls to ensure that the strategic objectives are achieved. This process addresses all the risks relevant to Gan Direct and which include the following risks:

• Insurance (undertaking) risk

• Market risk

• Concentration risk

• Counterparty default risk

• Credit risk

• Liquidity risk

• Operational risk

• Reputational risk

• Strategic risk

• Emerging risk

For all the significant risks identified above, the risk management process at Gan Direct identifies, measures, manages, monitors and reports.

Risk Identification Risk identification is the first stage in the risk management process during which the Company’s management identify and record all material risk exposures that arise in the course of business. The process is performed annually using a Risk Register, which includes all the risks inherent to the Company’s functions and operations, that could potentially have an adverse effect on the Company’s performance. The Risk Register is updated with new risks, as they arise.

Measurement and assessment

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

12/SFCR

After the risks have been identified there is a series of qualitative and/or quantitative assessments of these risks to estimate the probability of occurrence and the potential impact. In measuring and assessment of the risks we use methods such as:

• Sensitivity analysis

• Scenario analysis

• Expert judgments Materiality has been defined in terms of the maximum potential loss occurring from an event taking place The company uses a range of materiality thresholds based on the impact or risks on Solvency, earnings, liquidity and reputation. During the risk mapping exercise, the materiality of each risk within the risk universe was assessed against the materiality thresholds.

Managing - Risk mitigation and transfer The resulting material risks to the Company are managed by using a number of strategies:

• Mitigate Risk mitigation involves the mitigation of the risk likelihood and or impact

• Avoid Risks avoidance is the elimination of activities that cause the risk

• Transfer Risk transference is transferring the impact of the risk to a third part

• Accept Risk acceptance means accepting that a risk might have an impact, and no mitigating measures are taken.

The risk management strategies are selected in such a way to ensure that the risks remain wilting the risk appetite tolerance limits set by the company.

Monitoring and Reporting The risk monitoring and reporting are required to ensure they reflect changes to the environment and conditions. This means that it is possible that risk management strategies may have to be adapted in accordance with risk appetite tolerance levels and limits.

Risk Management Implementation and Integration

The way the risk management system including the risk management function are implemented and integrated into the organisation structure and decision-making process of the Company is set below. The company has a risk appetite statement approved by both the audit and risk committee, and the Board of Directors. The risk appetite statement is supported by a risk indicators and tolerance document which seeks to sets out in practical terms how the Company measures whether its performance remains within the approved appetite for risk. The risk indicators and tolerance document is used to generate key risk indicators which are reported on twice a year and are reviewed by both the audit and risk committee and the Board of Directors. The risk register is maintained by the risk function and is subject to an annual review at a minimum. The risk register tabulates all the perceived risks to the business as well as any

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

13/SFCR

emerging risks. Those risks are assessed as to their impact on the business both in terms of percentage likelihood and in financial terms, where applicable (not all risks have financial consequences). Once reviewed, the updated risk register is presented to the audit and risk committee for review, and to the Board of Directors. Both the audit and risk committee and the Board of Directors consider the adequacy of the controls in place and the financial impact of the risk occurring. The audit and risk committee has responsibility for overseeing the implementation of any additional controls that might be deemed necessary. In this way, the governance bodies charged with managing the company’s exposure to risk are kept updated and informed as to the risks faced by the business, and through the key risk indicators, the current level of exposure to each risk.

B.4 Own Risk and Solvency Assessment (ORSA) The EC Directive in Article 45 requires that insurers, as part of their risk management system, to perform an Own Risk and Solvency Assessment (ORSA). The assessment requires the Company to properly determine its overall solvency needs to cover both short and long- term risks. The risk based approach requires amongst other things, that the Company hold an amount of capital that is commensurate with the risks to which it may be exposed, and therefore the ORSA assists the Company in better understanding of its risks, solvency needs and own funds held. Gan Direct produces an ‘’ORSA’’ at least once in each calendar year. Additional ORSAs may be produced in response to material changes to risks faced by the Company. The Company uses ORSA as a management tool to enhance risk awareness in its culture and decisions making processes, forming an integral part of the overall business strategy and assists in having a practical understanding of the risks it has. The ORSA process includes an assessment of our capital requirement over the next 12 months. The level of economic capital required is also delivered using stress scenarios whereby the capital, available is recalculated under the different risk scenarios. The process of producing the ORSA is a cyclical one. The inputs include:

• Board’s policies

• The Board strategy for the business

• Output from the standard model Pillar 1 process

• Actuarial function output

• The Company’s Enterprise Risk Management system The ORSA is then produced by management in conjunction with the actuarial and risk management function. The ORSA is presented to the audit and risk committee for comment and review; and if approved, to the Board of Directors for their consideration. The result of the Board’s consideration forms the basis for the future strategy of the business, which forms the basis for the following year’s ORSA.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

14/SFCR

B.5 Internal Control System The Company’s Internal Control System (ICS) is the aggregate of control mechanisms and procedures which covers, on an ongoing basis, every single activity of the Company and contributes towards the Company’s efficient and sound operation. The Company applies five lines of defence in dealing with its Internal Controls. They are:

• The Control Environment, whereby the culture of internal control is set from the Board of Directors, down to employees. The Company promotes the importance of appropriate internal controls by ensuring that all personnel are aware of their role in the internal control system.

• Risk Assessment, whereby all risks are assessed and compiled into a Risk Register reviewed twice a year

• Control Activities-Those controls integrated in the routine operations of the Company

• Information & Communication – whereby the results of the Control activities are communicated across the company, and

• Monitoring Activities – whereby the system of internal control is reviewed by independent staff that have no operational responsibilities.

Gan Directs’ compliance mission is to:

• Protect the Company’s reputation and manage compliance risk

• Show its commitment to establishing high ethical standards in conducting its business

• Ensure compliance with regularly bodies and authorities. There is continuous monitoring of trends and changes in regulations in order to manage reputational and compliance risks.

The Compliance function engages in a number of methods and activities in order to identify control and suggest measures to mitigate compliance risk.

B.6 Internal Audit Function As part of the system of internal controls, The Company has a team of independent staff that have no operational responsibilities and aims to the verification of the adequacy and effectiveness of controls including quality assurance. The team look into whatever matter as an internal audit team feel they require to review, and any matters referred to them by the audit and risk committee of the Company. The internal Audit’s activities are designed to provide advice to management in improving the internal control system and monitors the implementation of management’s remedial actions.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

15/SFCR

B.7 Actuarial Function The actuarial function is responsible amongst other things, for

• Calculating the technical provisions including:

Ensuring the appropriateness of the methodologies and assumptions

Assessing the adequacy and quality of data used

• Analysing the movement in technical provisions

• Comparison of the best estimates against experience

• Providing an opinion on the underwriting policy

• Providing an opinion on the adequacy of the reinsurance arrangements

• Contributing to enhance the risk management system

• Contributing to the ORSA process Each of these activities are carried out at least on annual basis. The Actuarial Function is getting support from external consultants.

B.8 Outsourcing To manage the risks related to outsourcing, Gan Direct has a policy to safeguard its business operations.

General requirements for outsourcing The outsourcing policy sets out the procedures for the assessment of outsourcing as outlined below:

• Risk assessment is required for important activities, whereby concentration of risk, competition risk and possible conflicts of interest are examined.

• Confidentiality, quality of service and continuity are crucial to ensure the service provider is competent and reliable

• Compliance with law and regulations is also essential element of the assessment. When choosing a supplier, consideration is given as to how the risks identified can be mitigated. Furthermore, the procedures for the selection of the supplier, consider matters such as the supplier’s experience, reputation, its organisation and employees. In the selection process, it is ensured that the supplier has the ability and capacity to be able to perform the task and can fulfil the requirement of any applicable legislation. Where important or critical activities are to be outsourced there must be in place a written agreement to ensure the interests of the Company are protected and comply with any legal and regulatory requirements. All important, or critical outsourcing require the approval of the Managing Director. Gan Direct remains fully responsible for the activities outsourced.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

16/SFCR

Requirements for the outsourcing of critical or key functions or activities In addition to the above, for outsourcing an important or key function or activity, Gan Direct has also set the following requirements:

Due diligence A due diligence exercise must be carried out to ensure that:

• Service provider can perform the outsourced function or activity

• Service provider has the technical ability required

• The employees of the service provider that will be involved in providing the outsourced function have sufficient qualifications

• Service provider has the authorisations required by law to provide the required function or activity.

Written authorisation to the supervisory authority Gan Direct is obliged to notify the supervisory authority in a timely manner prior to the outsourcing of critical or key functions.

Outsourcing Key Functions For the outsourcing of a key function, the Company must also fulfil the following requirements:

• Designation of the responsible person within Gan Direct, that will have overall responsibility for the outsourced key function, who is fit and proper and possesses sufficient knowledge and experience regarding the outsourced key function to be able to challenge the performance and result of the service provided.

• Assessment of the person responsible for the outsourced key function and any relevant persons at the service provider.

• Notification to the supervisory authority of the responsible person

• Monitor and review to be able to assess if the service provider delivers according to the written agreement.

Gan Direct has outsourced some of its operational activities. The Company did not outsource any of its key functions in 2016. The Company did however use external consultants in areas relating to the implementation and compliance with Solvency II requirements. Main Gan Direct activities outsourced during 2016 are as follows:

Outsourced Function or Activity Jurisdiction of service provider

Accident and Road Assistance Cyprus

Networking and Security Cyprus

Loss Estimators/ Adjusters Cyprus

Servers and Systems Cyprus

Medical Assistance Abroad Greece

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

17/SFCR

B.9 Any Other Information

Quality Management System

Gan Direct maintains a Quality Management System and is accredited with the international standard of ISO 9001 since May 2002. A Quality Management System (QMS) is a set of policies, processes and procedures required for planning and execution (production/development/service) in the core business area of an organization. (i.e. areas that can impact the organization's ability to meet customer requirements.) ISO 9001 is the international standard that specifies requirements for a quality management system (QMS). Organizations use the standard to demonstrate the ability to consistently provide products and services that meet customer and regulatory requirements. The Management and the staff of the Company are fully committed to work consistently, having the customer satisfaction as their top priority, to offer quality non-life insurance products that will meet customer expectations when the need arises, to minimize customer complaints, with the aim towards improving the effectiveness of the Quality Management System. The Quality Management System implemented within the Company is reviewed on a systematic basis

• to ensure continual improvement on customer satisfaction and service quality

• to safeguard that all the processes needed for non-life insurance cover is in accordance with the relevant requirements

• to make sure that the Company’s Quality Management continues to be operative so as to control the requirements of the ISO 9001 Standard

• and that the customer requirements are fully met in a competitive way. The renewal of the ISO certificate is subject to an annual external audit by the British Standards Institute (BSI).

Assessment of the adequacy of the System of Governance.

Overall the Company’s Management System is considered appropriate and effective given the nature, size and complexity of the risks inherent in the business. The main risks inherent in the Company’s business are discussed further in section C of this report. The Company will however continue with the strengthening of its governance system in response to new business demands and regulatory requirements.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

18/SFCR

C. Risk Profile Overview of the Risk Profile The Solvency capital requirement of Gan Direct is calculated using the Solvency II standard formula and is the sum of the following three components:

• Basic Solvency capital requirement (BSCR)

• Capital requirement for operational risks

• Adjustments for risk – mitigating effects The BSCR in calculated by the sum of the different risk modules and sub-modules with due regard to correlation effects. The following table shows the risk profile and composition of SCR as at 31 December 2016 for Gan Direct.

Type of Risk 31/12/2016 €’000

Market risk Counterparty default risk Health underwriting risk Non-Life underwriting risk Diversification

3,255 559 16

3,971 -1,776

Basic Solvency Capital Requirement Operational Risk Adjustment for the LAC of TP and deferred taxes

6,025 396

(600)

Solvency Capital Requirement 5,821

As can be seen clearly from the table above the biggest risk drivers for Gan Direct are Non-life underwriting risk and Market risk. These two risk modules account for over 90% of the total BSCR. The detailed composition of these two risk modules are analysed further down in this report.

C.1 Underwriting Risk Underwriting risk is generally defined as the risk of loss or of the detrimental changes in terms of the value of insurance liabilities. This basically is the risk that premium and/or investment income will not be sufficient to cover current or future payment obligations, due to inaccurate pricing and provisioning assumptions. Underwriting risk is an industry specific risk, and comprised of:

• Premium and Reserve risk

• Non-Life Catastrophe risk

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

19/SFCR

For the purposes of the SCR model, the underwriting module is divided into sub-modules as shown in the following table:

Risk sub-module Definition

Premium risk Premium risk only relates to future claims (excluding) IBNR and IBNER, and originates from claim sizes being greater than expected, and differences in timing of claim payments from expected, and differences in claims frequency from those expected. In summary, it is the risk of loss resulting from an increase in claims costs in the next year which could be because of a higher claims frequency or higher level of average claims cost than expected.

Reserve risk Reserve risk only relates to incurred claims, i.e. existing claims (including IBNR and IBNER), and originates from claim sizes being greater than expected, and differences in timing of claims payments from expected and differences in claims frequency from those expected. This basically means the risk of loss through adverse development in claims settlement.

Catastrophe risk Catastrophe risk is the risk that a single event, or a series of events, of major magnitude, leads to a significant deviation in actual claims from the total expected claims. This is basically the risk of damage from natural disasters or individual major damage in the next year.

Based on the Pillar 1 result for year 2016 the total diversified Non- Life underwriting is Euro 3.97 million out of which Euro 3.86 million derives from Premium and Reserve Risk and Euro 0.38 million derive from Catastrophe Risk) including the diversification effect of Euro 0.26 million.

Non-Life Catastrophe Risk The company’s exposure to Catastrophe risk stems from extreme or irregular events that are not sufficiently captured by the capital requirements for premium and reserve risk. The total diversified gross catastrophe risk consists of Natural Catastrophes and Man-made Catastrophes. In Cyprus, the only peril with regards to natural catastrophes is earthquake. Based on the Pillar 1 results for year 2016 the total diversified catastrophe risk is Euro 37.05 million out of which approximately Euro 36.4 million are covered by the reinsurers of the Company. The total retained diversified catastrophe risk, after reinsurance is approximately Euro 0.38 million.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

20/SFCR

Mitigating Steps Reinsurance The main risk mitigation the Company employs is reinsurance. There are a number and a mix of reinsurance arrangements to ensure adequate protection for the Company. For example, the Company transfers its exposure to major events involving damage to building and contents so that the potential loss to the Company is limited to its retention. The Company has also taken out reinsurance of the risk of large claims occurring with large sums insured. To mitigate its exposure to Insurance Risk to less material levels, the Company consults with external professionals who review and reserves and claims provisions, taking into consideration the Company’s risk profile, policies and procedures. In addition, underwriting procedures including measurement and pricing of insurance policies, is performed based on strict policies and guidelines, and after considering the Company’s strategy and other macroeconomic factors, including the level of economic activity and competition in the industry.

Stress testing sensitivity analysis Stress testing and sensitivity analysis, included for example, the effect of a percentage shock to the technical provisions of motor business. Another stress test used, is a major flood event damaging motor vehicles and buildings.

C.2 Market Risk Description of the risk Market risk is the risk of potential losses due to adverse movements in financial market variables. Exposure to market risk is measured by the impact of movements in financial variables such as property prices, equity prices and interest rates. Under Solvency II, the market risk reflects the sensitivity of assets, liabilities and financial instruments values to change in the following factors:

• Currency risk

• Interest rate risk

• Spread risk

• Equity risk

• Property risk

• Concentration risk

Currency Risk Currency risk relates to the sensitivity of the values of assets, liabilities and financial instruments to changes in the level or in the volatility of currency exchange rates.

Interest Rate Risk Interest Rate Risk relates to the sensitivity of the values of assets, liabilities and financial instruments to changes in the term structure of interest rates, or in the volatility of interest rates.

Spread Risk

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

21/SFCR

Spread Risk relates to the sensitivity of the values of assets, liabilities and financial instruments to changes in the level or in the volatility of credit spreads over the risk-free interest rate term structure.

Equity Risk Equity Risk relates to the sensitivity of the values of assets, liabilities, and financial instruments to changes in the level or in the volatility of market prices of equities.

Property Risk Property Risk relates to the sensitivity of the values of assets, liabilities, and financial instruments to changes in the level or in the volatility of market prices of real estate.

Concentration Risk Concentration Risk may arise with respect to investments in geographical area, economic sector, or individual investments in a geographical area, economic sector, or individual investments or due to a concentration of business written within a geographical area, of a policy type or of underlying risks covered.

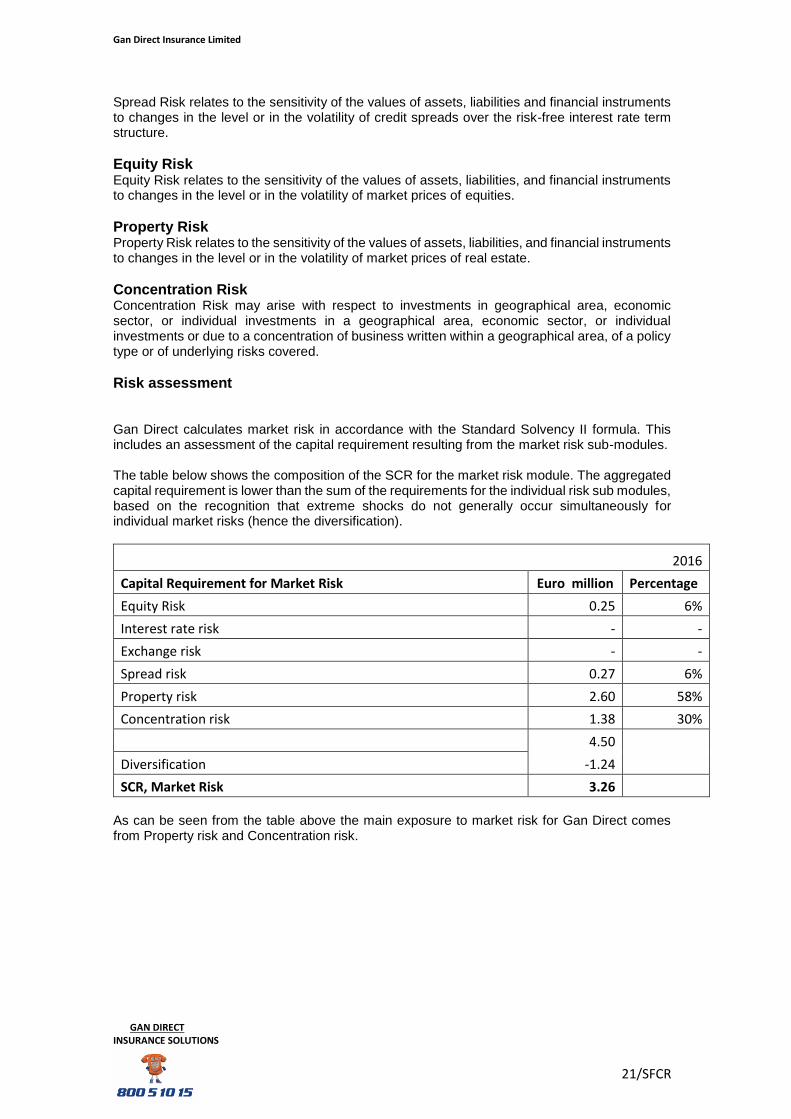

Risk assessment Gan Direct calculates market risk in accordance with the Standard Solvency II formula. This includes an assessment of the capital requirement resulting from the market risk sub-modules. The table below shows the composition of the SCR for the market risk module. The aggregated capital requirement is lower than the sum of the requirements for the individual risk sub modules, based on the recognition that extreme shocks do not generally occur simultaneously for individual market risks (hence the diversification).

2016

Capital Requirement for Market Risk Euro million Percentage

Equity Risk 0.25 6%

Interest rate risk - -

Exchange risk - -

Spread risk 0.27 6%

Property risk 2.60 58%

Concentration risk 1.38 30%

4.50

Diversification -1.24

SCR, Market Risk 3.26 As can be seen from the table above the main exposure to market risk for Gan Direct comes from Property risk and Concentration risk.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

22/SFCR

Property risk exposure The calculation of the capital requirement for the property risk equates to the loss of basic own funds with a direct 25% fall in the values of land and buildings. Gan Directs’ SCR property risk amounts to Euro 2.6 million and represents 58% of the undiversified Market SCR. Property risk arises from the Company’s exposure to properties in Nicosia, Limassol, Larnaca and Paphos. A big part of this property risk relates to the Company’s Head Office in Limassol.

Concentration risk exposure Gan Directs’ SCR concentration risk amounts to Euro 1.38 million and represents 30% of the undiversified market SCR. Gan Direct is exposed to concentration risk due to large individual exposures in its deposits which two Cyprus Banks. The one bank is unrated and the other one has a low credit rating and this results in the relatively high capital requirement on concentration risk. Part of the concentration risk capital requirement also comes from the Company’s Head Office in Limassol.

Equity risk and spread risk exposure Gan Direct does not have material exposure to equity and spread risk.

Mitigating Steps Transfer of risk For property risk to be lower, the Company’s management is considering restructuring options which include scenarios to transfer properties ownership to different entity and reduce the direct Company’s exposure to property risk. Risk mitigation from deferred tax The use of deferred tax is a general risk mitigation technique that can be applied in certain cases. When deferred taxes are used as a risk mitigation technique, it is assumed that in the event that an extreme scenario occurs which reduces the value of the relevant asset, part of the impact can be absorbed, because the existing and recognised deferred tax liability will no longer be due following the occurrence of the scenario. This reduces the overall influence of the scenario. In the case of Gan Direct the overall impact of the scenario regarding properties could be reduced by approximately 20% which is the rate for Capital Gains Tax on Properties already provided for in the IFRS statements.

Diversification - Counterparties As mentioned above Gan Direct is exposed to concentration risk due to large individual deposits will two Cyprus banks. Measures were taken by management to reduce both concentration risk and counterparty risk by opening bank accounts outside Cyprus (elsewhere Europe) with banks with a good credit rating.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

23/SFCR

Despite these management measures the Company is still exposed to concentration risk as shown by the Pillar 1 results for 2016. This matter is constantly under review by the management.

Stress testing and sensitivity analysis Stress testing included for example, a scenario where it was assumed, that the value of properties the Company holds, will decline by 10% next year and by a further 5% in the following year.

Application of the ‘’Prudent Person Principle’’ to Investments. Gan Direct has an Investment Management Policy which sets out the framework in which it may set investment mandates and manage its assets/liability management activities. This includes:

• Defining the investment objectives and benchmarks;

• Documenting and communicating the investment philosophy;

• Provide a framework for the approval, and monitoring the performance of investment decisions;

• Specifying the requirements for asset liability management; and

• Ensuring compliance with all regulatory requirements. The Company’s major investments consists of land and building (appx Euro 10.4 million) and term deposits placed with different banks both in Cyprus and elsewhere in Europe. (appx Euro 8.4 million) These two asset classes represent appx 84% of the Company’s total assets and these are basically the only classes were the Company is presently investing. The Company’s investments in hand and Buildings was done long before Solvency II came into effect. The world economy is still fragile with a lot of uncertainties and therefore the Board that takes all the ultimate decisions about investments is very risk averse under the present economic situation in Cyprus, Europe and the world economy in general. The emphasis at present is placed on capital preservation rather than return on investments. This however is constantly under review.

C.3 Credit Risk/Counterparty Default Risk Credit risk is the risk of loss, or of adverse change in the financial situation, resulting from fluctuations in the credit standing of issuers of securities, counterparties and any debtors to which insurance and reinsurance undertakings are exposed to. Counterparty risk includes the exposures with the Company’s:

• Reinsurance Providers

• Other debtors (term and cash deposits with banks and other balances)

The company uses the Direct Channel of sales and does NOT allow any credit and therefore does not have any exposure to amounts due from policyholders or intermediaries.

• For year 2016 based on the results of the Pillar 1, the total diversified Counterparty Risk under Solvency II is estimated to be Euro 0.56 million.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

24/SFCR

• The Company’s exposure to counterparty risk for year 2016 comes mainly from reinsurance recoverable.

• Counterparty exposures are usually monitored taking into consideration the credit rating of each counterparty

Mitigating Steps Overall the company has adopted the following policies and controls set by management, to mitigate its exposure to credit counterparty risk, and ensure compliance with the Company’s risk appetite:

• Engagement only with reinsurers with minimum credit rating of A

• In the Company’s agreements with reinsurers, there is a build-in clause which states that in the event where the reinsurance providers credit rating deteriorates, the Company has the option to immediately replace them

• Changes in credit rating or solvency ratio of reinsurance and other counterparties are monitored regularly and the list of approved counterparties is updated accordingly.

• Term deposits are placed with banking institutions with a good credit rating wherever possible.

Stress testing and sensitivity analysis Stress testing included for example the default of the Company’s biggest financial counterparty are Cyprus Banks and a 20% write off from the Company’s term deposits and current accounts.

C.4 Liquidity Risk Liquidity risk is the risk that Gan Direct would not be able to meet its financial obligations as they fall due. Gan Direct is averse to liquidity risk and holds sufficient cash balances to pay at least 6 months claims and expenses at any one time. In fact, the total deposits and cash equivalent balances as at 31st December 2016 amounted to Euro 8.66 million and can settle immediately over 70% of the total net claim provisions as at 31st December 2016.

C.5 Operational Risk Operational risk is the risk of loss caused by inadequacies or failure in internal processes, employees or systems, or by external events. Operational risk does not include reputational or strategic risk. Gan Direct assesses operational risks in accordance with the standard Solvency II formula. The capital requirement for operational risk as at 31st December 2016 was Euro 0.4 million and represents appx 6.8% of the standard formula SCR.

Risk Exposure

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

25/SFCR

Gan Direct is exposed to a high number of operational risks. These risks have been catalogued in the Company Risk Register. The following risks have been judged to be the material ones:

• Litigation risk, particularly in relation to settlement of claims.

• IT risks (including Cyber risk)

• Business interruption risk

• Claims and external fraud

• Employee risk (staff shortage, etc)

• Claims and internal fraud

C.6 Other Material Risks A part of the regular ORSA process, the overall risk profile and associated solvency capital needs are assessed against Gan Directs’ actual solvency position, taking into account identified risks that are not incorporated into the standard formula. The following rules have been recognised by Gan Direct as being potentially material:

• Regulatory risk

• Strategic risk

• Reputational risk

• Legal environment risk

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

26/SFCR

D. VALUATION FOR SOLVENCY PURPOSES D.1 Assets All assets and liabilities, listed in the table below are valued in accordance with Solvency II Principle and are compared to theirs IFRS valuation. Assets and liabilities are valued on the assumption that the Company will pursue the business as a going concern. No changes in the valuations methods occurred during the year under review. The Company does not have any off-balance sheet assets or liabilities. The table below summarises the assets as ta 31 December 2016. The material difference between the financial statements and the Solvency II balance sheet relates to the bases which are used to value the assets. For the financial statements, the reinsurance receivables relating to the reinsurer share of unearned premiums are valued at fair value whereas for the Solvency II balance sheet, the premium provision is used resulting from the reinsurer share in the premium provisions. The table below shows the Assets Valuations - IFRS vs Solvency II

Euro '000

IFRS Solvency II

Assets 2016 2016

Property, plant and equipment held for own use 10,733 10,733

Investment Property 191 191

Intangible Assets 1 0

Long term bank deposits 7,705 7,705

Reinsurance share of TP 861 624

Insurance and other receivables 1,355 1,355

Deferred Acquisition Costs (DAC) 774 -

Cash and Cash equivalents 763 763

Deferred Tax Assets 17 17

22,400 21,388

Bases, methods and main assumptions used for valuation for Solvency II. Property, plant and equipment held for own use. Properties for own use are initially measured at cost, is then subsequently carried at fair value representing open market value as determined annually by independent qualified valuer’s. Plant and equipment is valued at cost less accumulated depreciation which provides a close approximation of fair value. There are no differences between IFRS valuation and Solvency II valuation.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

27/SFCR

Investment Properties Investment properties are valued at fair value determined annually by external valuers or by virtue of a Director’s valuation. Long term Deposits

Deposits other than cash equivalents are valued at fair value. Insurance and other receivables

The Company does not allow credit to Policyholders and does not use any intermediaries. The value of insurance and other receivables is the same in both the IFRS and the Solvency II Balance Sheet. Cash and Cash Equivalents

Cash and cash equivalents includes cash in hand and deposits in bank current accounts.

Assets Valuation Differences - IFRS vs Solvency II There are differences for intangibles, Deferred Acquisition Costs and Reinsurance recoverables as explained further below: Intangible assets

Intangible assets are not recognised in Solvency II. Therefore, there is a difference between IFRS and Solvency II of Euro 1K. Deferred Acquisition Costs

There is no concept of Deferred Acquisition Costs in Solvency II. Therefore, there is a difference between IFRS and Solvency II of Euro 774K. Reinsurance recoverable

Reinsurance recoverable are the difference between the gross and net provisions under Solvency II, these are valued on a best estimate basis. This difference in the valuation methods means there is a difference between IFRS and Solvency II of Euro 237K.

D.2 Technical Provisions Valuation of technical provisions under Solvency II are the sum of the best estimate and the risk margin. The table below shows the technical provisions by line of business

Line of Business Gross €'000 Net €'000

Motor 12,851 12,457

Property 341 154

Income Protection 76 33

Other 2 2

13,270 12,646

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

28/SFCR

Bases, Methods and Main Assumptions for the valuation of Technical Provisions Best Estimate The best estimate of the premium provision relates to all future cashflows relating mainly to cashflows of future claims, expenses and reinsurance costs. The provisions for claims outstanding includes claims that have already been incurred regardless, whether these claims have been reported or not. Therefore, the claims provision would include the outstanding claims estimates the IBNER and claims expenses! The cashflow are discounted to allow for the time value of money using the risk-free interest rates prescribed under Solvency II. Risk Margin The risk margin is added to the best estimate liability. This margin is calculated in accordance with Article 37 of the Commission Delegated Regulation (EU) 2015/35 whereby an additional margin is added to the best estimate liability to ensure that the technical provisions as a whole are equivalent to the amount that an insurance undertaking would be expected to require in order to take over the insurance obligations, assuming a cost of capital a rate of 6%. Level of uncertainty and the value of technical provisions The level of uncertainty basically relates as to how future actual experience will differ from the best estimate assumptions used to calculate the technical provision. The calculation of the claims provisions is inherently uncertain with respect to the amount and timing of future cash flows and requires the use of judgement. Therefore, the Company’s actual liability for losses may therefore be subject to positive or negative deviations relative to the initially estimated claims provisions. Comparison between the IFRS valuation and Solvency II The comparison between the IFRS valuation and Solvency II valuation of technical provisions is shown in the table below:

Euro ‘000 2016

IFRS Solvency II

Technical Provisions 2016 2016

Premium Provisions Gross 5,303 3,974

Claims Provisions Gross Risk Margin

8,561 -

8,646 650

Best Estimates Gross 13,864 13,270

Premium Provisions Net 5,098 3,854

Claim Provisions Net Risk Margin

8,142 -

8,142 650

Best Estimates Net 13,240 12,646

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

29/SFCR

Under Solvency II, the technical provisions are calculated using a different method compared to IFRS. The main differences between IFRS and Solvency II are described below:

• Different method for the risk margin. Under Solvency II valuation of technical reserves include the Risk Margin. There is no concept of risk margin under the IFRS methodology

• In IFRS there is no expected profit taken into account

• Different methods are used for determining best estimate premium liabilities

• Different curve used to calculate the best estimate

D.3 Valuation of Other liabilities The value of other liabilities is set out in the table below:

Euro '000

IFRS Solvency II

Liabilities 2016 2016

Reinsurance payables 214 214

Trade Creditors and other account payable (not insurance) 412 412

Taxation 30 30

Deffered Income 205 205

861 861

Deferred Tax Liability 859 859

1720 1720

Reinsurance payables The Balance due to reinsurers as at 31st December 2016 amounted to Euro 0.2 million and are calculated in occurrence with the reinsurance agreement. No adjustments are required for these balances. These payables relate to balances owed in respect of services and assets acquired by the Company and no adjustments are required for those balances.

Deferred Tax Liability Deferred tax liabilities are recognised in relation to temporary timing differences between accounting and tax values of assets and liabilities and is calculated using the applicable tax rates.

D.4 Alternative Methods for Valuation No other alternative methods for valuation are used.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

30/SFCR

E. CAPITAL MANAGEMENT

E.1 Own Funds The objective of managing the company’s own funds is to ensure that there are sufficient own funds to meet the capital requirement under Solvency II at all times with a prudent buffer to ensure its financial capacity under more difficult economic conditions. The overall solvency of the Company is subject to a quarterly review of the coverage of the capital requirements in Pillar 1. Furthermore, as part of the ORSA process, the Company prepares a three-year business projection which will also result in a three-year projection of the capital requirements. This helps the Board of Directors in ensuring that there are available own funds in the line with its business plan and objectives.

Structure, Amount and Quality of Own Funds The total amount of own funds is as follows:

Euros '000

2016 2015

Ordinary Share Capital 1,505 1,505

Surplus Funds 5,316 4,923

Reconciliation Reserve -418 -234

Total Basic Own Funds 6,403 6,194 The eligible amount of own funds to cover the Solvency Capital Requirement and the Minimum Capital Requirement is Euro 6.4 million. This is comprised entirely of Tier 1 Basic Own Funds and is available to cover the MCR and SCR. IFRS Equity vs Own Funds The table below shows the comparison and movement in the IFRS and Solvency II valuation of assets, liabilities and own funds.

Euro '000

31 December 2016 IFRS Euro Solvency II Movement

Total Assets 22,401 21,389 -1,012

Total Liabilities 15,580 14,986 474

Total Own Funds 6,821 6,403 -418

The movement in valuation of assets and liabilities arises from the differences in the valuation of IFRS and Solvency II Standards, as set out below:

• Intangibles (not included under Solvency II)

• Deferred Acquisition cost (not included under Solvency II)

• Differences in gross technical provisions and reinsurance recoverable (as explained in Section D)

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

31/SFCR

Basic own-fund item subject to transitional arrangement None

Ancillary Own Funds None

Deductions from Own Funds None

E.2 Solvency Capital Requirement and Minimum Capital Requirement The Solvency capital requirement (‘’SCR’’) is calculated using the standard formula of Pillar 1. As at 31 December 2016 the SCR amounted to Euro 5.82 million. The table below shows the components of the SCR (using the Standard Formula) at 31 December 2016:

Type of Risk 31/12/2016 €’000

Market risk Counterparty default risk Health underwriting risk Non-Life underwriting risk Diversification

3,255 559 16

3,971 -1,776

Basic Solvency Capital Requirement Operational Risk Adjustment for the LAC of TP and deferred taxes

6,025 396

(600)

Solvency Capital Requirement 5,821

The Company uses EIOPA’s Solvency II Standard Formula. It does not use Company specific parameters and does not use simplified calculations in its computation. The Minimum Capital requirement at 31 December 2016 is Euro 3,7 million which is the absolute floor.

Information on the inputs used to calculate the MCR

31/12/2016 €’000

Linear MCR 2,038

SCR 5,821

MCR cap (45% of SCR) 2,619

MCR floor (25% of SCR) 1,455

MCR absolute floor 3,700

MCR 3,700

Material changes to the SCR and MCR over the reporting period No material changes

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

32/SFCR

Use of the duration – based equity risk sub-module for the calculation of the Solvency Capital Requirement N/A

Differences between the standard formula and any internal model used N/A

Non – compliance with the Minimum Capital Requirement or significant non – compliance with the Solvency Capital Requirement There was no breach of the Solvency Capital Requirement or the Minimum Capital Requirement over the reporting period.

E.3 Any Other Information None.

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

33/SFCR

ANNEX: Annual Quantitative Reporting Templates (QRT’s) The following QRTs are required for the SFCR S.02.01.02 Balance Sheet S.05.01.02 Premiums, claims and expenses by line of business S.05.02.01 Premiums claims and expenses by country S.17.01.02 Non-Life Technical Provisions S.19.01.21 Non-Life Insurance Claims S.23.01.01 Own Funds S.25.01.21 Solvency Capital Requirement – for Undertaking on Standard Formula S.28.01.01 Minimum Capital Requirement – Only Non- Life Insurance or Reinsurance

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

34/SFCR

Annex I S.02.01.02 Balance Sheet

Solvency II value

Assets C0010

Intangible assets R0030

Deferred tax assets R0040 17,286

Pension benefit surplus R0050 0

Property, plant & equipment held for own use R0060 10,732,392

Investments (other than assets held for index-linked and unit-linked contracts) R0070 7,897,451

Property (other than for own use) R0080 191,363

Holdings in related undertakings, including participations R0090 0

Equities R0100 1,342

Equities - listed R0110 1,342

Equities - unlisted R0120 0

Bonds R0130 0

Government Bonds R0140 0

Corporate Bonds R0150 0

Structured notes R0160 0

Collateralised securities R0170 0

Collective Investments Undertakings R0180 0

Derivatives R0190 0

Deposits other than cash equivalents R0200 7,704,746

Other investments R0210 0

Assets held for index-linked and unit-linked contracts R0220 0

Loans and mortgages R0230 0

Loans on policies R0240 0

Loans and mortgages to individuals R0250 0

Other loans and mortgages R0260 0

Reinsurance recoverables from: R0270 624,450

Non-life and health similar to non-life R0280 624,450

Non-life excluding health R0290 581,410

Health similar to non-life R0300 43,040

Life and health similar to life, excluding health and index-linked and unit-linked R0310 0

Health similar to life R0320 0

Life excluding health and index-linked and unit-linked R0330 0

Life index-linked and unit-linked R0340 0

Deposits to cedants R0350 0

Insurance and intermediaries receivables R0360 818,415

Reinsurance receivables R0370 127,897

Receivables (trade, not insurance) R0380 275,327

Own shares (held directly) R0390 0

Amounts due in respect of own fund items or initial fund called up but not yet

paid inR0400 0

Cash and cash equivalents R0410 762,781

Any other assets, not elsewhere shown R0420 132,972

Total assets R0500 21,388,971

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

35/SFCR

Annex I S.02.01.02 Balance Sheet

Solvency II value

Liabilities C0010

Technical provisions – non-life R0510 13,270,268

Technical provisions – non-life (excluding health) R0520 13,194,504

Technical provisions calculated as a whole R0530 0

Best Estimate R0540 12,547,066

Risk margin R0550 647,438

Technical provisions - health (similar to non-life) R0560 75,763

Technical provisions calculated as a whole R0570 0

Best Estimate R0580 73,290

Risk margin R0590 2,473

Technical provisions - life (excluding index-linked and unit-linked) R0600 0

Technical provisions - health (similar to life) R0610 0

Technical provisions calculated as a whole R0620 0

Best Estimate R0630 0

Risk margin R0640 0

Technical provisions – life (excluding health and index-linked and unit-linked) R0650 0

Technical provisions calculated as a whole R0660 0

Best Estimate R0670 0

Risk margin R0680 0

Technical provisions – index-linked and unit-linked R0690 0

Technical provisions calculated as a whole R0700 0

Best Estimate R0710 0

Risk margin R0720 0

Contingent liabilities R0740 0

Provisions other than technical provisions R0750 0

Pension benefit obligations R0760 0

Deposits from reinsurers R0770 0

Deferred tax liabilities R0780 859,239

Derivatives R0790 0

Debts owed to credit institutions R0800 25,454

Financial liabilities other than debts owed to credit institutions R0810 0

Insurance & intermediaries payables R0820 119,887

Reinsurance payables R0830 214,149

Payables (trade, not insurance) R0840 291,405

Subordinated liabilities R0850 0

Subordinated liabilities not in Basic Own Funds R0860 0

Subordinated liabilities in Basic Own Funds R0870 0

Any other liabilities, not elsewhere shown R0880 205,702

Total liabilities R0900 14,986,104

Excess of assets over liabilities R1000 6,402,867

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

36/SFCR

Annex I S.05.01.02 Premiums, claims and expenses by line of business

Medical

expense

insurance

Income

protection

insurance

Workers'

compensation

insurance

Motor

vehicle

liability

insurance

Other motor

insurance

Marine, aviation

and transport

insurance

Fire and

other damage

to property

insurance

General

liability

insurance

Credit and

suretyship

insurance

Legal

expenses

insurance

Assista

nce

Miscellaneo

us financial

loss

Health Casualty

Marine,

aviation,

transport

Property

C0010 C0020 C0030 C0040 C0050 C0060 C0070 C0080 C0090 C0100 C0110 C0120 C0130 C0140 C0150 C0160 C0200

Premiums written

Gross - Direct Business R0110 265.663 0 8.276.500 3.775.703 2.043 1.206.877 15.187 0 0 0 0 13.541.973

Gross - Proportional

reinsurance accepted R0120 0

Gross - Non-proportional

reinsurance accepted R0130 0

Reinsurers' share R0140 201.839 482.586 129.320 1.457 757.270 1.572.472

Net R0200 63.824 0 7.793.914 3.646.383 586 449.607 15.187 0 0 0 0 0 0 0 0 11.969.501

Premiums earned 0

Gross - Direct Business R0210 245.406 0 8.072.798 3.714.736 2.043 1.145.055 15.995 0 0 0 0 13.196.033

Gross - Proportional

reinsurance accepted R0220 0

Gross - Non-proportional

reinsurance accepted R0230 0

Reinsurers' share R0240 185.633 482.586 129.320 1.457 696.882 1.495.878

Net R0300 59.773 0 7.590.212 3.585.416 586 448.173 15.995 0 0 0 0 0 0 0 0 11.700.155

Claims incurred 0

Gross - Direct Business R0310 178.077 5.352.305 2.824.195 4.000 335.666 8.694.243

Gross - Proportional

reinsurance accepted R0320 0

Gross - Non-proportional

reinsurance accepted R0330 0

Reinsurers' share R0340 123.409 267.898 3.200 254.180 648.687

Net R0400 54.668 0 5.084.407 2.824.195 800 81.486 0 0 0 0 0 0 0 0 0 8.045.556

Changes in other technical

provisions0

Gross - Direct Business R0410 0

Gross - Proportional

reinsurance acceptedR0420 0

Gross - Non- proportional

reinsurance acceptedR0430 0

Reinsurers' share R0440 0

Net R0500 0

Expenses incurred R0550 83.276 2.336.500 1.065.241 0 366.035 3.960 3.855.012

Other expenses R1200

Total expenses R1300 3.855.012

Line of Business for: non-life insurance and reinsurance obligations (direct business and accepted proportional reinsurance)Line of Business for:

accepted non-proportional reinsurance

Total

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

37/SFCR

Annex I S.05.02.01

Premiums claims and expenses by country.

Home

CountryTotal Top 5 and home country

C0010 C0020 C0030 C0040 C0050 C0060 C0070

R0010

C0080 C0090 C0100 C0110 C0120 C0130 C0140

Premiums written

Gross - Direct Business R0110 13.541.973 13.541.973

Gross - Proportional reinsurance accepted R0120

Gross - Non-proportional reinsurance accepted R0130

Reinsurers' share R0140 1.572.472 1.572.472

Net R0200 11.969.501 11.969.501

Premiums earned

Gross - Direct Business R0210 13.196.033 13.196.033

Gross - Proportional reinsurance accepted R0220

Gross - Non-proportional reinsurance accepted R0230

Reinsurers' share R0240 1.495.878 1.495.878

Net R0300 11.700.155 11.700.155

Claims incurred

Gross - Direct Business R0310 8.694.243 8.694.243

Gross - Proportional reinsurance accepted R0320

Gross - Non-proportional reinsurance accepted R0330

Reinsurers' share R0340 648.687 648.687

Net R0400 8.045.556 8.045.556

Changes in other technical provisions

Gross - Direct Business R0410

Gross - Proportional reinsurance accepted R0420

Gross - Non- proportional reinsurance accepted R0430

Reinsurers' share R0440

Net R0500

Expenses incurred R0550 3.855.012 3.855.012

Other expenses R1200

Total expenses R1300 3.855.012

Top 5 countries (by amount of gross premiums written)

- non-life obligations

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

38/SFCR

Annex I S.05.02.01

Premiums claims and expenses by country.

Home

CountryTotal Top 5 and home country

C0150 C0160 C0170 C0180 C0190 C0200 C0210

R1400

C0220 C0230 C0240 C0250 C0260 C0270 C0280

Premiums written

Gross R1410

Reinsurers' share R1420

Net R1500

Premiums earned

Gross R1510

Reinsurers' share R1520

Net R1600

Claims incurred

Gross R1610

Reinsurers' share R1620

Net R1700

Changes in other technical provisions

Gross R1710

Reinsurers' share R1720

Net R1800

Expenses incurred R1900

Other expenses R2500

Total expenses R2600

Top 5 countries (by amount of gross premiums written)

- life obligations

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

39/SFCR

Annex I S.17.01.02 Non-Life Technical Provisions

Medical

expense

insuranc

e

Income

protection

insurance

Workers'

compens

ation

insuranc

e

Motor

vehicle

liability

insurance

Other

motor

insurance

Marine,

aviation

and

transport

insurance

Fire and other

damage to

property

insurance

General

liability

insuranc

e

Credit

and

suretys

hip

insuran

ce

Legal

expenses

insurance

Assista

nce

Miscella

neous

financial

loss

Non-

proporti

onal

health

reinsur

ance

Non-

proportion

al casualty

reinsuranc

e

Non-

proport

ional

marine

,

aviatio

n and

transpo

Non-

proporti

onal

property

reinsura

nce

C0020 C0030 C0040 C0050 C0060 C0070 C0080 C0090 C0100 C0110 C0120 C0130 C0140 C0150 C0160 C0170 C0180

Technical provisions calculated as a whole R0010 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Total Recoverables from reinsurance/SPV and

Finite Re after the adjustment for expected R0050

Technical provisions calculated as a sum of

Best estimate

Premium provisions

Gross R0060 68,848 0 2,516,607 1,271,476 0 116,759 0 0 0 0 0 0 0 0 0 3,974,125

Total recoverable from reinsurance/SPV and

Finite Re after the adjustment for expected R0140

0 39,836 0 29,707 15,009 - 35,681 - 0 0 0 0 0 0 0 0 120,233

Net Best Estimate of Premium Provisions R0150 0 29,012 0 2,486,901 1,256,467 0 81,078 434 0 0 0 0 0 0 0 0 3,853,892

Claims provisions

Gross R0160 0 4,442 0 6,577,996 1,857,116 527 206,073 77 0 0 0 - 0 0 0 0 8,646,231

Total recoverable from reinsurance/SPV and

Finite Re after the adjustment for expected R0240

0 3,203 0 348,965 - 210 151,761 77 0 0 0 0 0 0 0 0 504,217

Net Best Estimate of Claims Provisions R0250 0 1,238 0 6,229,031 1,857,116 316 54,312 0 0 0 0 0 0 0 0 0 8,142,014

Total Best estimate - gross R0260 0 73,290 0 9,094,604 3,128,592 527 322,832 511 0 0 0 0 0 0 0 0 12,620,356

Total Best estimate - net R0270 0 30,250 0 8,715,932 3,113,583 316 135,390 434 0 0 0 0 0 0 0 0 11,995,906

Risk margin R0280 0 2,473 0 456,430 171,232 86 18,803 888 0 0 0 0 0 0 0 0 649,912

Amount of the transitional on Technical

Technical Provisions calculated as a whole R0290

Best estimate R0300

Risk margin R0310

Technical provisions - total

Technical provisions - total R0320 0 75,763 0 9,551,034 3,299,824 613 341,635 1,399 0 0 0 0 0 0 0 0 13,270,268

Recoverable from reinsurance contract/SPV and

Finite Re after the adjustment for expected R0330

0 43,040 0 378,672 15,009 210 187,442 77 0 0 0 0 0 0 0 0 624,450

Technical provisions minus recoverables from R0340 0 32,724 0 9,172,362 3,284,815 403 154,192 1,322 0 0 0 0 0 0 0 0 12,645,818

Direct business and accepted proportional reinsurance Accepted non-proportional reinsurance

Total Non-

Life

obligation

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

40/SFCR

Annex I S.19.01.21 Non-Life Insurance Claims

Total Non-Life Business

Accident year / Underwriting year Z0010

Gross Claims Paid (non-cumulative)

(absolute amount)

Year 0 1 2 3 4 5 6 7 8 9 10&+

In

Current

year

Sum of

years

(cumulative)

C0010 C0020 C0030 C0040 C0050 C0060 C0070 C0080 C0090 C0100 C0110 C0170 C0180

Prior R0100 0 R0100

N-9 R0160 1,757,896 405,379 68,523 350 0 0 12,000 0 10650 0 R0160 2,254,798

N-8 R0170 2,399,650 599,053 73,756 57,363 34,000 88,000 117,000 3,000 8,000 R0170 8,000 3,379,822

N-7 R0180 2,735,222 679,905 222,000 44,050 197,000 33,000 455,000 57,000 R0180 57,000 4,423,177

N-6 R0190 3,003,065 1,066,811 241,615 247,306 122,000 265,000 59,000 R0190 59,000 5,004,797

N-5 R0200 3,420,912 1,231,445 269,600 231,000 469,000 196,000 R0200 196,000 5,817,957

N-4 R0210 4,166,485 1,272,285 217,000 174,000 103,000 R0210 103,000 5,932,770

N-3 R0220 4,430,403 1,022,784 291,461 144,000 R0220 144,000 5,888,648

N-2 R0230 4,819,613 1,053,494 363,123 R0230 363,123 6,236,230

N-1 R0240 4,774,210 1,186,016 R0240 1,186,016 5,960,226

N R0250 4,755,442 R0250 4,755,442 4,755,442

Total R0260 6,871,581 49,653,867

Development year

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

41/SFCR

Annex I S.19.01.21

Non-Life Insurance Claims

Gross undiscounted Best Estimate Claims Provisions

(absolute amount)

Year 0 1 2 3 4 5 6 7 8 9 10&+

Year end

(discounte

d data)

C0200 C0210 C0220 C0230 C0240 C0250 C0260 C0270 C0280 C0290 C0300 C0360

Prior R0100 0 R0100 0

N-9 R0160 0 R0160 0

N-8 R0170 10,013 R0170 10,012

N-7 R0180 221,215 R0180 221,149

N-6 R0190 157,891 R0190 157,864

N-5 R0200 191,329 R0200 191,271

N-4 R0210 581,712 R0210 581,538

N-3 R0220 1,239,570 R0220 1,236,201

N-2 R0230 1,113,237 R0230 1,112,981

N-1 R0240 1,709,702 R0240 1,709,187

N R0250 3,426,384 R0250 3,426,027

Total R0260 8,646,231

Development year

Gan Direct Insurance Limited

GAN DIRECT INSURANCE SOLUTIONS

42/SFCR

Annex I S.23.01.01 Own Funds

TotalTier 1 -

unrestricted

Tier 1 -

restricted Tier 2 Tier 3

C0010 C0020 C0030 C0040 C0050

Basic own funds before deduction for participations in other financial sector as foreseen

in article 68 of Delegated Regulation 2015/35

Ordinary share capital (gross of own shares) R0010 1,504,800 1,504,800

Share premium account related to ordinary share capital R0030

Iinitial funds, members' contributions or the equivalent basic own - fund item for mutual and

mutual-type undertakings R0040

Subordinated mutual member accounts R0050

Surplus funds R0070 5,316,073 5,316,073

Preference shares R0090

Share premium account related to preference shares R0110

Reconciliation reserve R0130 -418,006 -418,006

Subordinated liabilities R0140

An amount equal to the value of net deferred tax assets R0160

Other own fund items approved by the supervisory authority as basic own funds not specified

above R0180

Own funds from the financial statements that should not be represented by the

reconciliation reserve and do not meet the criteria to be classified as Solvency II own

funds

Own funds from the financial statements that should not be represented by the reconciliation

reserve and do not meet the criteria to be classified as Solvency II own fundsR0220

Deductions

Deductions for participations in financial and credit institutions R0230

Total basic own funds after deductions R0290 6,402,867 6,402,867

Ancillary own funds

Unpaid and uncalled ordinary share capital callable on demand R0300