gap inc. equity valuation and analysis valued at...

TRANSCRIPT

1

Gap Inc. Equity Valuation and Analysis Valued at November 1, 2006

Brian Vance: [email protected] Jonathan Applegate: [email protected]

Kyle Reynolds: [email protected] Chance Baucum: [email protected]

Matt Loyd: [email protected]

2

Table of Contents

Executive Summary…………………………………………………6

Industry Overview and Analysis…………………………………8

Company Overview………………………………………………….8

Competitive Advantage Analysis…………………………………15

Accounting Flexibility………………………………………………..23

Accounting Strategy Evaluation…………………………………..24

Quality of disclosure…………………………………………………………………………………..25

Potential “Red flags”………………………………………………………………………………...26

3

Ratio Analysis and Forecast Financials…………………………28

Liquidity Analysis……………………………………………………..29

Profitability Analysis…………………………………………………30

Capital Structure Analysis………………………………………….31

Benchmark Analysis………………………………………………....31

Liquidity…………………………………………………………………………………………………...32

Profitability ………………………………………………………………………………………………35

Capital structure………………………………………………………………………………………..38

Financial Statement Forecasting…………………………………39

Valuation Analysis……………………………………………………42

Method of comparables Valuation…………………………………………………………….43

Cost of Capital Estimation………………………………………………………………………..44

Summary of Valuations…………………………………………….45

Altman’s Z-Score……………………………………………………..49

References…………………………………………………………….51

Appendices…………………………………………………………….52

4

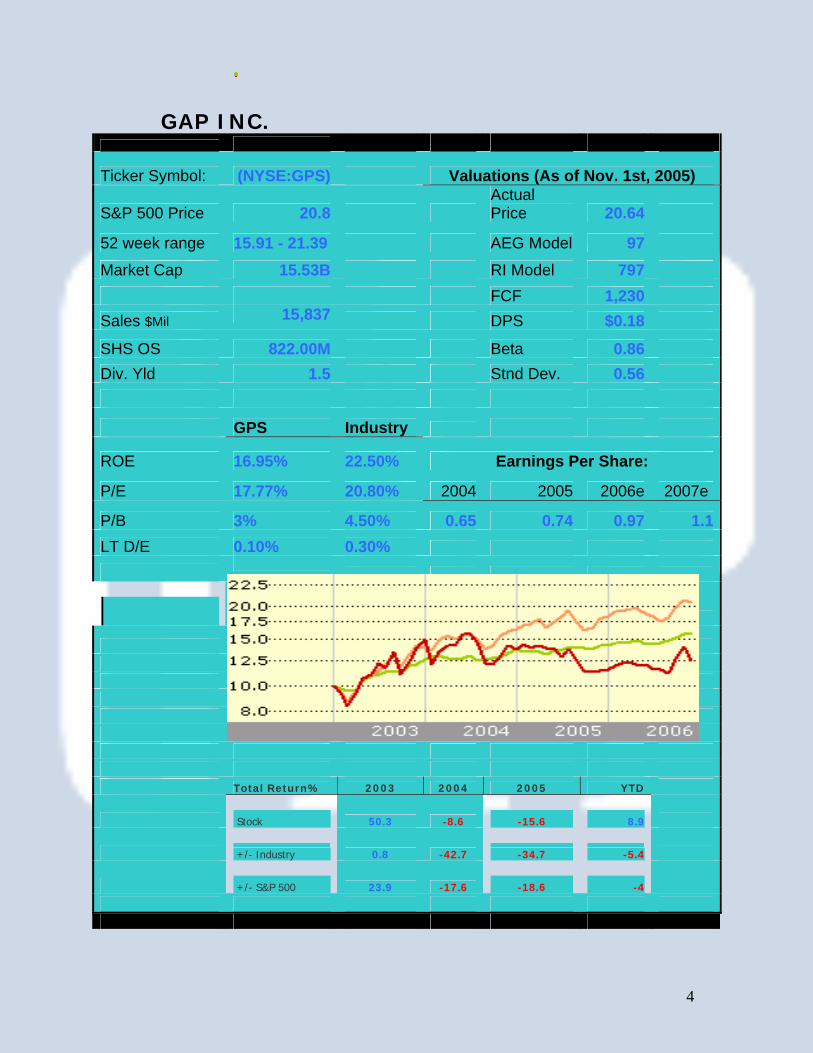

GAP INC.

Ticker Symbol: (NYSE:GPS) Valuations (As of Nov. 1st, 2005)

S&P 500 Price 20.8 Actual Price 20.64

52 week range 15.91 - 21.39 AEG Model 97

Market Cap 15.53B RI Model 797 FCF 1,230 Sales $Mil 15,837 DPS $0.18

SHS OS 822.00M Beta 0.86 Div. Yld 1.5 Stnd Dev. 0.56

GPS Industry

ROE 16.95% 22.50% Earnings Per Share:

P/E 17.77% 20.80% 2004 2005 2006e 2007e

P/B 3% 4.50% 0.65 0.74 0.97 1.1LT D/E 0.10% 0.30%

Total Return% 2003 2004 2005 YTD

Stock 50.3 -8.6

-15.6

8.9

+/- Industry 0.8 -42.7

-34.7

-5.4

+/- S&P 500 23.9 -17.6

-18.6

-4

5

Executive Summary Recommendation: Overvalued firm

Through detailed research and valuation, we have concluded that we are

a selling opportunity. The clothing retail industry is very competitive with a high

number of competitors. This large number of competitors creates strong

earnings potential compared to other industries. The industry is characterized by

emphasizing differentiation and not cost leadership, which results in the firms not

having to have a price war. Along with differentiation, most of the competitors

within this industry tend to rely on their brand image. The biggest firms within

the industry also tend to create subsidiaries in order to compete with rival firms.

The threat of new competitors is relatively low due to the high start up costs of

entering the market. Since Gap Inc. and other firms in this industry tend to have

a high quality brand image, most firms have power over their suppliers, due to

manufacturers competing for business.

After analysis, Gap’s accounting practices and policies were found to be

fairly aggressive. However, their disclosure and reporting of relevant material is

seemingly very transparent. Gap discloses all accounting methods concerning

everything from leases and pension plans to inventory and tax methods. They

also outline all accounting statements and opinions affecting their business. We

found no distortions or discrepancies in their accounting.

6

After computing our firm’s core ratios, we felt we were able to grasp Gap’s

overall performance as compared to its competitors within the industry.

Inventory turnover tended to be lower while gross profit was high throughout

the industry. This is most likely due to the fact that most firms in our industry

compete with differentiation and brand name.

To understand what the future holds for Gap Inc., we forecasted the

company’s financial statements through 2015. By analyzing trends, we have

concluded that Gap will continue to grow at a current rate; much like the firm

has been doing the last 3 years without any unforeseen abnormalities. It was

extremely important that our forecasts be calculated as accurately as possible

due to the fact that forecasting was the base upon which all valuation methods

rested.

After thorough evaluation, we have found that Gap Inc. is overvalued in

the market. All of our valuation models showed Gap Inc.’s stock to be

considerably overvalued. The most accurate valuation model for us was the free

cash flows valuation. Using our free cash flow model, we found an estimated

price per share at the end of 2005 to be $15.72 while our actual price per share

was $17.64. The only model which we considered to be unreliable was the

discounted dividend valuation. We feel this was due to our low dividend payout

rate in forecasted years. The discounted dividends valuation model is flawed

because it values companies based on what they pay per dividend, and many

companies pay little or no dividends at all. Based on this all-inclusive, in-depth

7

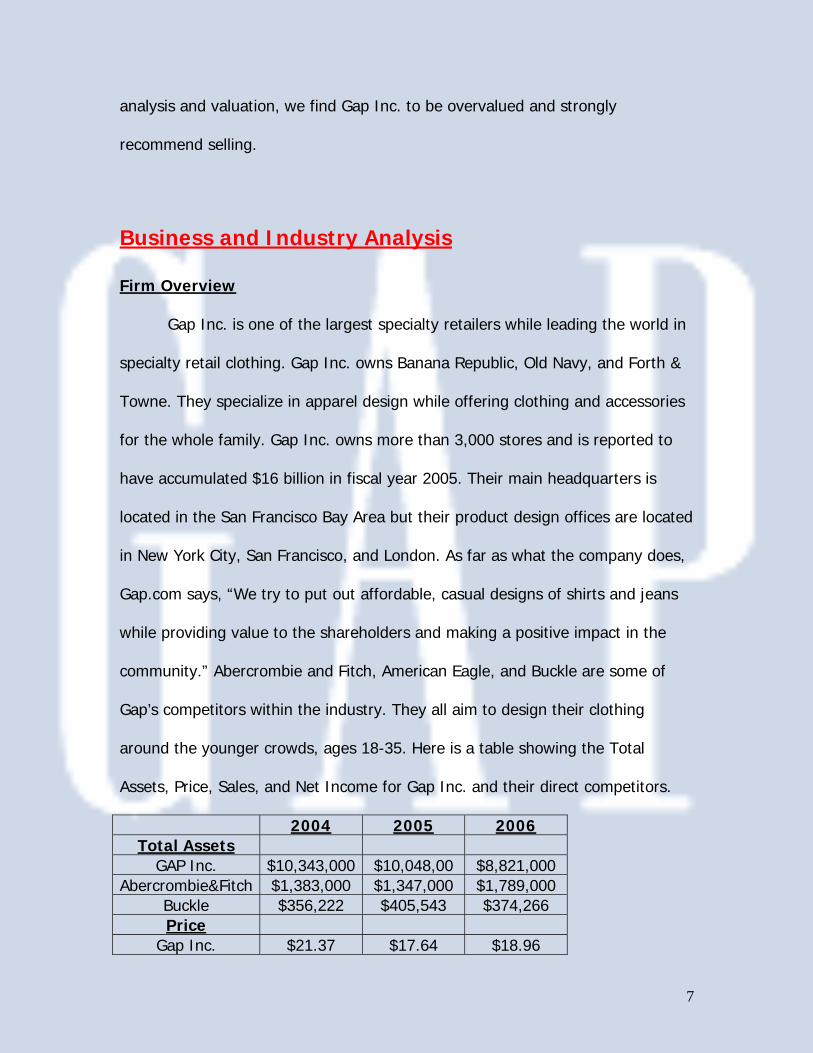

analysis and valuation, we find Gap Inc. to be overvalued and strongly

recommend selling.

Business and Industry Analysis

Firm Overview

Gap Inc. is one of the largest specialty retailers while leading the world in

specialty retail clothing. Gap Inc. owns Banana Republic, Old Navy, and Forth &

Towne. They specialize in apparel design while offering clothing and accessories

for the whole family. Gap Inc. owns more than 3,000 stores and is reported to

have accumulated $16 billion in fiscal year 2005. Their main headquarters is

located in the San Francisco Bay Area but their product design offices are located

in New York City, San Francisco, and London. As far as what the company does,

Gap.com says, “We try to put out affordable, casual designs of shirts and jeans

while providing value to the shareholders and making a positive impact in the

community.” Abercrombie and Fitch, American Eagle, and Buckle are some of

Gap’s competitors within the industry. They all aim to design their clothing

around the younger crowds, ages 18-35. Here is a table showing the Total

Assets, Price, Sales, and Net Income for Gap Inc. and their direct competitors.

2004 2005 2006 Total Assets

GAP Inc. $10,343,000 $10,048,00 $8,821,000 Abercrombie&Fitch $1,383,000 $1,347,000 $1,789,000

Buckle $356,222 $405,543 $374,266 Price

Gap Inc. $21.37 $17.64 $18.96

8

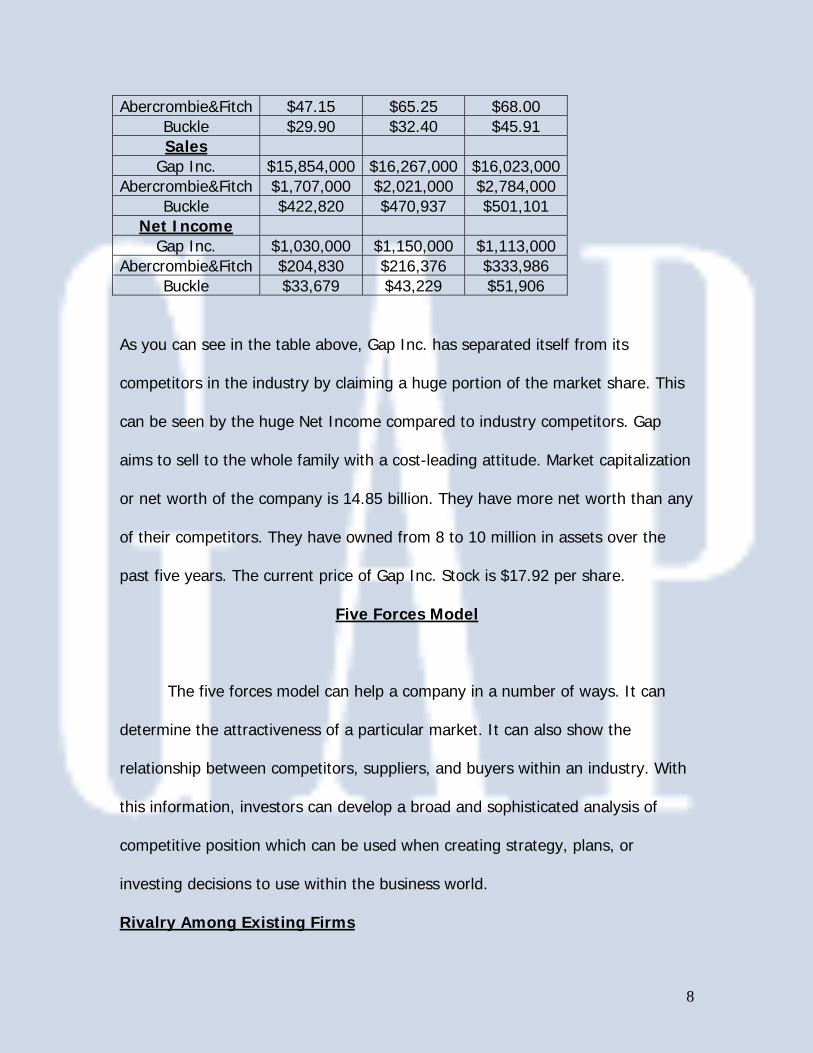

Abercrombie&Fitch $47.15 $65.25 $68.00 Buckle $29.90 $32.40 $45.91 Sales

Gap Inc. $15,854,000 $16,267,000 $16,023,000Abercrombie&Fitch $1,707,000 $2,021,000 $2,784,000

Buckle $422,820 $470,937 $501,101 Net Income

Gap Inc. $1,030,000 $1,150,000 $1,113,000 Abercrombie&Fitch $204,830 $216,376 $333,986

Buckle $33,679 $43,229 $51,906

As you can see in the table above, Gap Inc. has separated itself from its

competitors in the industry by claiming a huge portion of the market share. This

can be seen by the huge Net Income compared to industry competitors. Gap

aims to sell to the whole family with a cost-leading attitude. Market capitalization

or net worth of the company is 14.85 billion. They have more net worth than any

of their competitors. They have owned from 8 to 10 million in assets over the

past five years. The current price of Gap Inc. Stock is $17.92 per share.

Five Forces Model

The five forces model can help a company in a number of ways. It can

determine the attractiveness of a particular market. It can also show the

relationship between competitors, suppliers, and buyers within an industry. With

this information, investors can develop a broad and sophisticated analysis of

competitive position which can be used when creating strategy, plans, or

investing decisions to use within the business world.

Rivalry Among Existing Firms

9

Some aspects of rivalry among firms that make this model so important

would be the number and size of firms, industry size and trends, product/service

range, and differentiation and strategy. The clothing stores industry, which has

done extremely well over the last 5-10 years, has a large number of competitors.

A few of the competing companies include American Eagle, Abercrombie & Fitch,

and TJ Maxx. This large number of competitors creates strong earnings potential

compared to other industries. In the clothing store industry there is room to

grow, but start up costs can be high. While Gap is definitely looking to gain a

larger share of the market, switching costs for consumers is low. This is

especially true with one of Gap’s top competitors TJ Maxx. TJ Maxx competes

solely on price. In response, Gap is looking to reestablish a larger core of

consumers who are brand loyalists. To compete with all these different

competitors in the market, Gap Inc. created such higher end clothing lines as

Banana Republic, Old Navy, and Forth & Towne. In an industry where the right

mix of product differentiation and price play a key role, these three brands allow

them to be competitive.

Threat of New Entrants

Some important factors surrounding the threat of new entrants section of

the five forces model include: barriers to entry, brand equity, switching costs,

access to distribution and government policies. Understanding these concepts

will help a firm understand the industry at a higher level. The popularity of the

internet has brought more sales opportunities for all companies within this

10

industry, which in turn, has increased the development of online marketing.

While Gap and its competitors compete in the clothing store industry, they also

have a number of competitors in the fashion industry which includes brands such

as Polo, Tommy Hilfiger, and Lacoste. These industries differ slightly because

these fashion companies sell their clothing to department stores like Dillard’s,

while Gap Inc. operates their own stores. They compete with these companies

because switching costs are so low. However, within their own industry, start up

costs can be high. Even though there is room to grow within the industry, the

threat of new entrants is relatively low. This is largely due to large economies of

scale in this industry in which new entrants will initially suffer from a cost

disadvantage from existing firms such as GAP Inc. The risk of investing so much

to start up deters most new entrants. In conclusion, there will always be the

threat of new entrants, but it will be extremely hard and expensive to match

Gap’s share in the market.

Threat of Substitute Products

Some key concepts that go along with the threat of substitute products

are buyer propensity to substitute, relative price performance of substitutes,

buyer switching cost, and perceived level of product differentiation.

Understanding this section will allow a firm to know how to handle any substitute

products that is thrown at them by competitors. The threat of substitute

products for Gap is very real. This is the main reason they are trying to

reestablish a larger group of brand loyalists with their “back to basics” simplistic

11

style that consumers had known and loved. Another way Gap Inc. can overcome

this problem is with their other brands, especially Old Navy. Brand loyalists will

generally buy a particular brand regardless of the price. However, consumers

who are not brand loyal tend to seek out substitute products largely because of

high prices. This is where Old Navy is able to tap into the industry. Old Navy

offers trendier styles with a lower cost, which lessens the threat of substitute

products. In an industry as diverse as the clothing industry, every move you

make determines when and how many substitute products could possibly enter

your market. This is why having more than one line of clothing, an online shop,

and sales in more than just the United States is so important.

Bargaining Power of Buyers/Customers

Understanding the bargaining power of your customers will help a firm

decide on the price it wants to sell its products for. Since our industry is, on

average, not a price competitive industry, this section is not as important as

others in the five forces model. Simply due to the low switching costs of the

industry, buyers do have some power. Price sensitivity plays a small role but the

majority of buyers are willing to pay for Gap’s moderately priced clothing. Sales

at retail locations tend to attract customers with less spending power, but

customers generally know what to expect with regard to prices in the industry.

On the average, Gap Inc.’s prices are lower than both Abercrombie & Fitch, and

Buckle. The Gap brand or Banana Republic may lose a few customers due to

prices, but Old Navy was created to appease the price shoppers. In this market,

12

it is important to compete on both quality and brand name, as well as price. This

is why, for example, Abercrombie & Fitch launched Abercrombie Kids, Hollister

Co., and RUEHL 925 campaigns. In conclusion, the customers do not have much

bargaining power within this industry. An example of an industry that would have

high bargaining power of customers would be lower quality outlets such as K-

mart, Payless, and Wal-Mart.

Bargaining Power of Suppliers

Bargaining power of suppliers is an extremely important aspect of our

firm, and the industry in general. If not properly calculated, excess cost and high

inventory can occur. There are numerous suppliers of fabrics and other materials

like cotton to choose from. Most firms actually shop for manufacturers of clothes

and hand their designs over to them. Since the firms in our industry have a high

quality brand image, most have real power over their suppliers, due to

manufacturer’s vying for their business.

In conclusion, there is an extremely high degree of competition within this

clothing retail industry. Since these brands rely on the latest fashions, quarterly

changes in seasonal products must happen as much as possible. Technology,

including online shopping, must be up to date. Branching out to places other

than the United States is important. Overall, these firms are relying on brand

image and differentiation to gain as much market share as possible.

Key Success Factors

13

Every firm in America has to decide, when it first starts, how it wants to

position itself in the industry. Our firm, Gap Inc., is no different. Gap had to

make the decision of how it wanted to gain a competitive advantage over other

firms in its field. There are two strategies a firm can follow. It can either choose

a cost leadership plan or a differentiation plan. Cost leadership is essentially just

competing with other firms only on cost. A cost leader can offer the same

product as a competitor, only at a lower price. Differentiation on the other hand

is competing by offering a product that is different in some way. These plans are

important because a firm can gain an advantage over its competitors based on

either of these strategies. It is also important that a firm choose one or the other

and not get stuck in the middle. Not taking one side or the other can cause a

firm to earn low profits.

The objective of product differentiation is to develop a position that

potential customers will understand to be unique. There are two mechanisms for

which differentiation affects performance. First, differentiation will reduce price

sensitivity. This means that consumers might be willing to pay a higher price for

the differentiating factor(s). Second, differentiation should reduce directness of

competition. This can be defined by stating that the more your product differs

from the industry’s products, categorization becomes more difficult thus your

product draws fewer comparisons to competition.

At the market level, differentiation can be defined as improving the quality

of goods over time due to innovation. In an evolutionary sense, differentiation is

14

more of a strategy that is important in adapting to a moving environment and its

social groups. Since almost all the firms in our industry have name recognition,

success in this market must be achieved by adapting to a moving environment

that is obsessed with the latest trends, while producing comfortable and casual

styles of dress.

Competitive Analysis

Gap Inc. is in the highly competitive, ever changing, clothing retail

industry. The Gap is implementing technology into its stores which contain

certain intrinsic competitive advantages which give the corporation a head up on

the competition. Not only does this new technology allow for more cost effective

distribution, but it also offers a more time-efficient experience for both the

consumer and the employee. Instead of spending large amounts of money yearly

by manually taking inventory, The GAP will now be able to access inventory data

quickly and easily through a handheld device. If there is a situation where

merchandise is out of stock at a particular location, it can be dealt with quickly

and effectively, by communicating with other GAP stores to replenish the missing

units.

These measures taken to provide technological advantages over other

companies will pay off, simply because it is a more convenient way of shopping.

It literally bridges inventories from multiple stores in a region, giving the

customer a larger selection of sizes and styles. This allows for customers to try

15

on clothing at the store, as well as offer the large inventory the internet has

been able to offer for many years. These new ways of business improves The

GAP with an entirely different shopping experience. This experience in time will

increase customer retention and rapport, generating profits. The Gap Web

advancements will provide the base for more company expansion. If the GAP can

hold their customer base through outstanding customer satisfaction, then people

will be drawn to the unique shopping experience.

Gap Inc. has chosen a differentiation strategy. “Know who you are and be

it. Celebrate your uniqueness with passion and conviction.” That phrase has been

the philosophy that has driven GAP for the last three decades. Gap’s purpose has

been to appeal to people of all ages, not just teens and young adults in their

twenties. This process starts with Gap designers who travel to such fashion and

cultural capitals as New York, Paris, London, Milan, and Tokyo. Here, the

designers partake in fashion shows and get a feeling for what the target

audience’s preferences are. Once these concepts have been developed, the

merchants and designers work extremely close together to translate this

inspiration into reality. This process of creativity and innovation is very much

necessary to differentiate The Gap’s clothing line from such top competitors as

Abercrombie & Fitch and American Eagle.

Investment in brand image has had a huge impact on GAP Inc. For

around thirty years, GAP specialized in basic clothing and had a consistent core

group of customers. Around 2000, GAP launched a new campaign to start

16

making a newer, trendier style of clothing. GAP also created flashy commercials

that included choreographed dance numbers and singing. This change alienated

many of Gap’s core customers and as a result, the company lost a sufficient

amount of money. Around 2002, then CEP Millard Drexler launched a “back to

basic” campaign. This campaign consisted of going back to Gap’s roots and

specializing in items such as denim, T-shirts, hooded sweaters, and basic pants.

This has improved sales, but it has been an uphill battle. Essentially, Gap’s brand

image tries to differentiate itself from competitors by offering very high quality,

basic, casual clothing.

Differentiation companies require heavy investments in research and

development. At GAP Inc., each item is sold and then registered for analysis by

planners and distribution analysts. These analysts monitor weekly sales trend

reports and determine which stores need to be stocked with what products.

These “replenishment shipments” usually occur one to three times per week.

This process continues until the season ends. At this point, all customer

feedback, performance notes, and suggested improvements are analyzed so GAP

is ready to being this cycle again.

As far as differentiation goes, Gap’s investment in brand image is by far

the most important aspect of value chain management. A bad decision, such as

the one made in 2000, can cripple a company. GAP is just now recovering and it

has been a slow process. In order to achieve and sustain competitive advantage,

17

GAP Inc. needs to stick to its roots and structure its supply chain in a way that is

consistent.

Even with The Gap implementing a polished product differentiation

strategy, with strong focus on brand development and unique advertisement, it

is still not at the top of the market. Population groups like the baby boomers are

not tailored to by Gap Inc. or any of its subsidiaries. Expansion of Gap Inc. would

open up a whole new, highly lucrative, market share.

Although The Gap has gone from being a corner shop in California, to a

worldwide corporation, they have experienced many peaks and valleys. The

company has learned many lessons. First, when creating marketing campaigns,

they learned to create their own image and not rely on celebrity status. Second,

they have learned how to create their own image. Their image is broad, but

specific. It adheres strictly to high quality, basic, casual clothing. Third, The Gap

has learned to create sub-brands to tailor to various classifications of people.

Fourth, The Gap realizes that they operate within a niche where customers care

about fashion but only so long as it can be delivered at a moderate price. The

Gap has also learned early that they have to outsource labor in order to keep

costs down and remain competitive. The Gap’s commitment to customer

satisfaction and ability to reinvent themselves in the volatile fashion industry

provides for an expected strong future for the company.

18

Accounting Analysis

In the section we analyzed Gap Inc.’s accounting quality by six steps.

First, by identifying the key accounting policies that are used. Then, Assess

Accounting Flexibility for the firm, and evaluating the accounting strategy. Next,

we had to evaluate how easy or less easy managers made it analyst to look at

it’s financial statements, and point out any potential “red flags”. Finally, based on

this analyzes; we felt that there was no accounting distortions to undo. Gap Inc.

has disclosed all of its material very well, and we feel that their accounting

practices are not misleading or distorted based off of the ratio analyzes of Gap

Inc.’s financial results.

Key Accounting Policies

The Gap’s key success factors are attributed to their strict accounting

polices which coordinate with each other to create the present and future

financial performance of the company. The financial statements are consolidated

to include the accounts of the company and all its subsidiaries. All inter-company

transactions and balances have been eliminated. Translation adjustments result

from translating foreign subsidiaries’ financial statements into U.S. dollars.

Balance sheet accounts are translated at exchange rates in effect at the balance

sheet date. Income statement accounts are translated at average exchange rates

during the year. The resulting translation adjustments are included in

accumulated other comprehensive earnings in the Consolidated Statements of

Shareholders’ Equity (Gap 10-K).

19

Fiscal year for Gap Inc. ends on the Saturday closest to January 31. The

last three years have consisted of 52 weeks while fiscal 2006 will consist of 53

weeks.

Revenue and the related cost of goods sold (including shipping costs) is

recognized at the time the products are received by the customers in

compliance with the rules of Staff Accounting Bulletin No. (“SAB”) 101, “Revenue

Recognition in Financial Statements” as amended by SAB 104 (Gap 10-K). The

point at which the customer receives and pays for the merchandise is when the

revenue is accounted for by means of either cash or credit card. The Gap is in

the retail clothing sales industry where transactions are processed very rapidly

and easily, explaining their non-reporting of Accounts Receivable. Amounts

related to shipping and handling that are billed to customers are reflected in net

sales and the related costs are shown in cost of goods sold and occupancy

expenses. The Gap uses the historical return gross profit patterns to record its

allowances for estimated returns.

Cash and equivalents represent cash and short-term, highly liquid

investments with original maturities of three months or less. Cash and

equivalents are accumulated by finding all accounts in-transit from banks for

customer credit card, debit card and electronic transfer transactions that go

through or clear in less than a week, which are then classified as cash and

equivalents in the Consolidated Balance Sheets. Checks outstanding are classified

in accounts payable on the Consolidated Balance Sheets. The restricted cash

account serves as collateral for the insurance obligations and recently in 2005

held $55 million (Gap 10-K).

Property and equipment are stated at cost. Depreciation and amortization

are computed using the straight-line method over the estimated useful lives of

the related assets. The cost of assets sold or rendered useless and the

20

accumulated depreciation or amortization are removed from the accounts with

any records of gain or loss shown in net earnings.

The Statement of Financial Accounting Standards No. (“SFAS”) 133,

“Accounting for Derivative Instruments and Hedging Activities,” establishes the

accounting and reporting principles for hedging activities and derivative

instruments (Gap 10-K). Gap measures all derivative instruments at fair value

and distinguishes them as either other current assets or accrued expenses and

additional current liabilities in their Consolidated Balance Sheets.

Merchandise inventory is calculated using the first-in, first-out method

(“FIFO”) to determine cost. By means of the cost method the inventory is valued

at the lower of the actual cost or market. They also estimate and accrue

shortage for the period between the last physical inventory count and the

balance sheet date.

Gap inc. leases most of their store premises and some headquarter

facilities and distribution centers. These operating leases expire at various dates

through 2033. Most store leases are for a five year base period and include

options that allow Gap to extend the lease term beyond the initial base period,

subject to terms agreed to at lease birth. Some leases also include early

termination options, which can be exercised under specific conditions. Gap inc.

recognizes the related rental expense on a straight-line basis and records the

difference between the recognized rental expense and amounts payable under

the leases as deferred rent liability. Deferred rent liability was approximately

$342 million at January 28, 2006 and $361 million at January 29, 2005. As stated

in the initial terms of the lease, the minimal lease payment has no dependency

on factors such as future sales volume and contingent rentals. Future payments

for maintenance, insurance and taxes to which the Company is obligated are

excluded from minimum lease payments.

21

Gap Inc. has acquired three different pension plans for its employees, all

with different types of defined benefit or defined contribution plans. The First,

“GapShare,” is a qualified defined contribution plan, available to employees who

meet certain age and service requirements. This plan allows employees to make

contributions up to a maximum limit and Gap matches the contribution total

amount or a portion of it according to a predetermined formula. Gaps’

contributions to this plan averaged $30 million over the last three years.

Another pension plan of Gap is known as the (“Plan”). This is a non-

qualified executive deferred compensation plan. It allows eligible employees to

defer compensation up to a maximum amount. Gap does not match any

contributions under this plan. Established on January 1, 1999, the asset and

liability concerning the Plan was approximately $24 million and $30 million,

respectively. As of December 31, 2005 the plan was frozen for additional

contributions.

In January of 2006 a nonqualified Supplemental Deferred Compensation

Plan replaced the (“Plan”).This new nonqualified Supplemental Deferred

Compensation Plan now allows for employees and non-employees on the Board

of Directors to defer compensation up to a limit. However under this new plan

the employee members on the Board of Directors will have their contributions

matched under a predetermined formula.

Accrued expenses and other current liabilities consist of payroll and

related benefits, deferred rent liability and other current liabilities. They use a

combination of insurance and self-insurance for a number of risk management

activities including workers’ compensation, general liability,

automobile liability and employee-related health care benefits, some of which is

paid by their employees (GPS 2005 Annual Report).

22

Income taxes are recorded using the asset and liability method in

compliance with SFAS 109 “Accounting for Income Taxes” (Gap 10-K). Deferred

income taxes come from temporary differences between the tax part of assets

plus the liabilities under this method. The reported amounts from the calculations

are then shown in the Consolidated Financial Statements.

Accounting Flexibility

Gap Inc has a significant amount of flexibility in choosing their key

accounting policies. Gap Inc. prepares financial statements in accordance with

accounting principles commonly accepted in the United States of America.

Management is required to use accounting policies in order to make significant

judgments and estimates to develop amounts reflected and disclosed in the

financial statements. Gap Inc. has shown accounting flexibility in many areas on

the financial statements.

Merchandise Inventory is valued using the cost method. Cost method

values inventory at the lower of the actual cost or market. Gap Inc. determines

cost using FIFO method, and the market cost is estimated by the net realizable

value. Also, depreciation and amortization are calculated using straight-line

method. Cost of assets sold or retired and related accumulated depreciation or

amortization are removed from the accounts with any resulting gain or loss

included in net earnings. Under Financial Accounting Standards No.133,

“Accounting Instruments and Hedging Activities”, establishes the accounting and

reporting standards for derivative instruments and hedging activities. Gap Inc.

recognizes all derivatives instruments as either other current assets or accrued

expenses and other current liabilities in Gap’s Consolidated Balance Sheets and

measures those instruments at fair value.

23

Gap Inc.’s accounting reports seem to have a lot of flexibility for

managers.

Accounting Strategy Evaluation

Gap’s preparation of financial statements is in conformity with accounting

principles generally accepted in the U.S. Managements is responsible to make

estimates and assumptions that affect the reported amounts of assets and

liabilities. Gap Inc. reports any accounting methods they use or any areas in their

consolidated statements that might seem unclear to investors in the footnotes.

For example, during the fiscal year of 2005, Gap Inc. accounted for stock-based

awards to employees and directors using the intrinsic value method of

accounting required by APM, Accounting Principles Board Opinion. Under this

method when price of employee stock options equals the market price of the

stock on the day it was issued, no compensation expense is recognized in the

Consolidated Statements of Operations. Stock options that are less than fair

market value are amortized to operating expenses over the vesting period of the

stock award, using the straight-line method.

In the clothing retail industry, they all record Gift cards at different times.

For example, American Eagle, one of Gap Inc.’s competitors, records a gift card

as a current liability upon purchase and recognized when the gift card is

redeemed for merchandise. AE gives customers 24 months to redeem the gift

card or the Company assesses the holder of the card a one dollar per month

service fee, which is deducted from the value of the gift card. The fee is

recorded in selling, general and administrative expenses. Unlike Gap Inc., who

treats gift certificates or gift cards as a liability and income is recorded as net

sales upon redemption or as other income, but up to sixty months. After sixty

24

months is up, the redemption is remote, and the liability for gift cards and gift

certificates is recorded in accounts payable on the consolidated balance sheets.

Quality of Disclosure throughout Financial Statements

Every manager in a firm has the discretion to disclose information.

Accounting rules require a certain amount of disclosure, but beyond that it is up

to the manager how much information the firm will disclose. Quality of

disclosure is very important to an investor. A manager can make it easy for an

analyst to gain an insight into the firm by disclosing a lot of information. On the

other hand they can make it quite difficult to assess the business reality by only

disclosing the minimum amount required. As an investor you want as much

disclosure as possible without threatening the firm’s competitive advantage. If

you disclose too much information the competitors will be able to look through

the glass and see your strengths and weaknesses, of which they can then turn

around and use against you or copy your strengths and gain a profit like yours.

GAP does a good job of disclosing its’ business strategy. In the Letter to

Shareholders they do not try to sugar coat their performance. They are quite

liberal in disclosing bad news. Paul Pressler, CEO of GAP, makes no attempt to

explain the drop in Net Sales for 2005. Instead of excuses he clearly lays out a

plan to return to growing sales and to regain Gap Inc.’s competitive position.

One criticism of disclosure is that there is no real explanation of Gap Inc.’s

performance from 2005. Their net sales were down 2% from 2004. Gap Inc.

did not try to explain this decrease to any reason. They basically just said they

can do better and have a plan in place to return to its’ increased earnings.

Another good quality of Gap Inc.’s disclosure is that they break up their

finances by different companies. Gap Inc. owns Banana Republic, Old Navy, and

Forth and Towne. In their annual report they separate these businesses out so

25

all their performances aren’t lumped together. This can show the investor or

analyst which companies are doing well and which aren’t.

Gap Inc. is also very good with disclosing numbers that they think are

important. Free cash flow is a subject they spend a lot of time on in their

financial report. They believe that free cash flow is important because it

represents how much cash a company has after the deduction of capital

expenditures. Gap Inc. goes above and beyond disclosure for their cash flows to

show the analyst how important they feel these cash flows are. They also

explain in their footnotes all the forward looking statements that they include in

their annual report. In Gap Inc.’s report they use numbers and strategies with

forward looking statements that basically anticipate future effects on cash flows,

dividend payouts, cash balances vs. cash flows, and new store openings. They

explain how they came to these numbers, which makes it easier for the analyst

to determine if these numbers are accurate.

In conclusion, Gap Inc. does a great job of disclosing information for an

analyst or investor. This level of disclosure makes it very easy to determine the

reality of Gap Inc.’s position in the industry and to forecast future financial

results

Identification of Potential “ Red Flags”

As far as identifying red flags, we were unable to find any flags in GAP

Inc.’s financials statements. Even when performance was down, there were no

unexplained changes in the accounting process. There were no unexplained

transactions to boost profits. There were no unusual increases in accounts

receivable with respect to sales increases. There were no large fourth-quarter

adjustments. Inventories did not increase in relation to an increase in sales. After

26

analysis, GAP Inc.’s accounting is legitimate with no questionable accounting

quality.

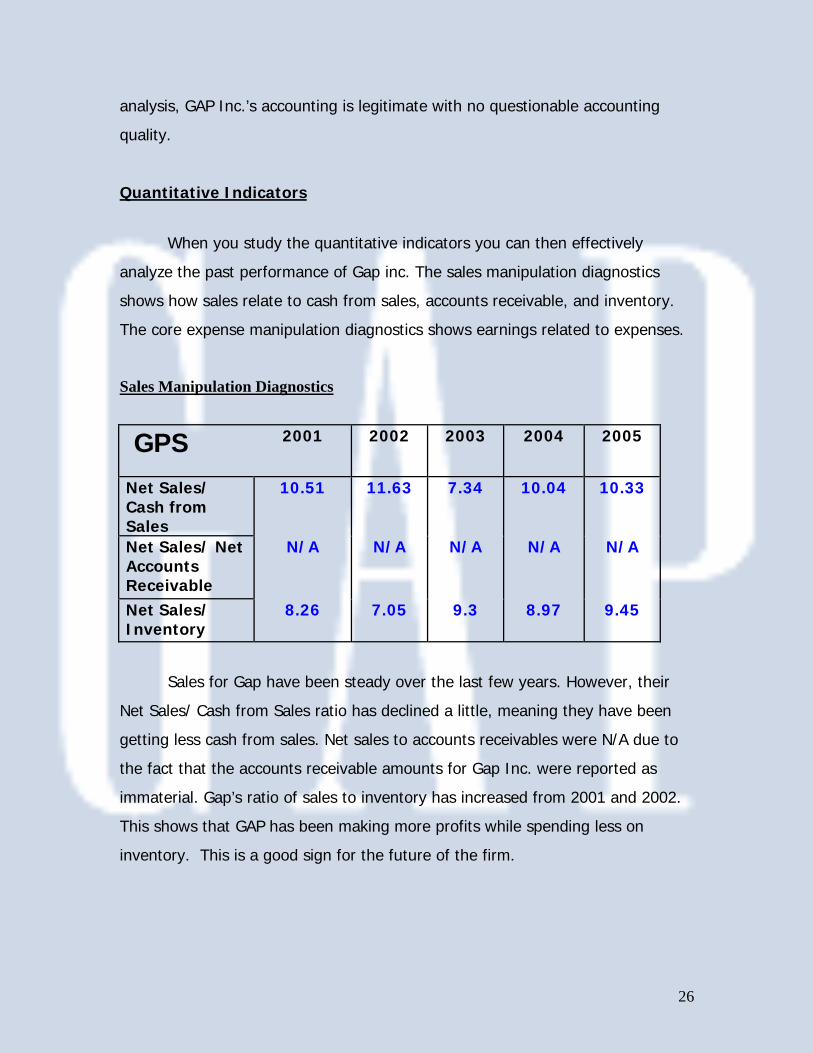

Quantitative Indicators

When you study the quantitative indicators you can then effectively

analyze the past performance of Gap inc. The sales manipulation diagnostics

shows how sales relate to cash from sales, accounts receivable, and inventory.

The core expense manipulation diagnostics shows earnings related to expenses.

Sales Manipulation Diagnostics

GPS 2001 2002 2003 2004 2005

Net Sales/ Cash from Sales

10.51 11.63 7.34 10.04 10.33

Net Sales/ Net Accounts Receivable

N/A N/A N/A N/A N/A

Net Sales/ Inventory

8.26 7.05 9.3 8.97 9.45

Sales for Gap have been steady over the last few years. However, their

Net Sales/ Cash from Sales ratio has declined a little, meaning they have been

getting less cash from sales. Net sales to accounts receivables were N/A due to

the fact that the accounts receivable amounts for Gap Inc. were reported as

immaterial. Gap’s ratio of sales to inventory has increased from 2001 and 2002.

This shows that GAP has been making more profits while spending less on

inventory. This is a good sign for the future of the firm.

27

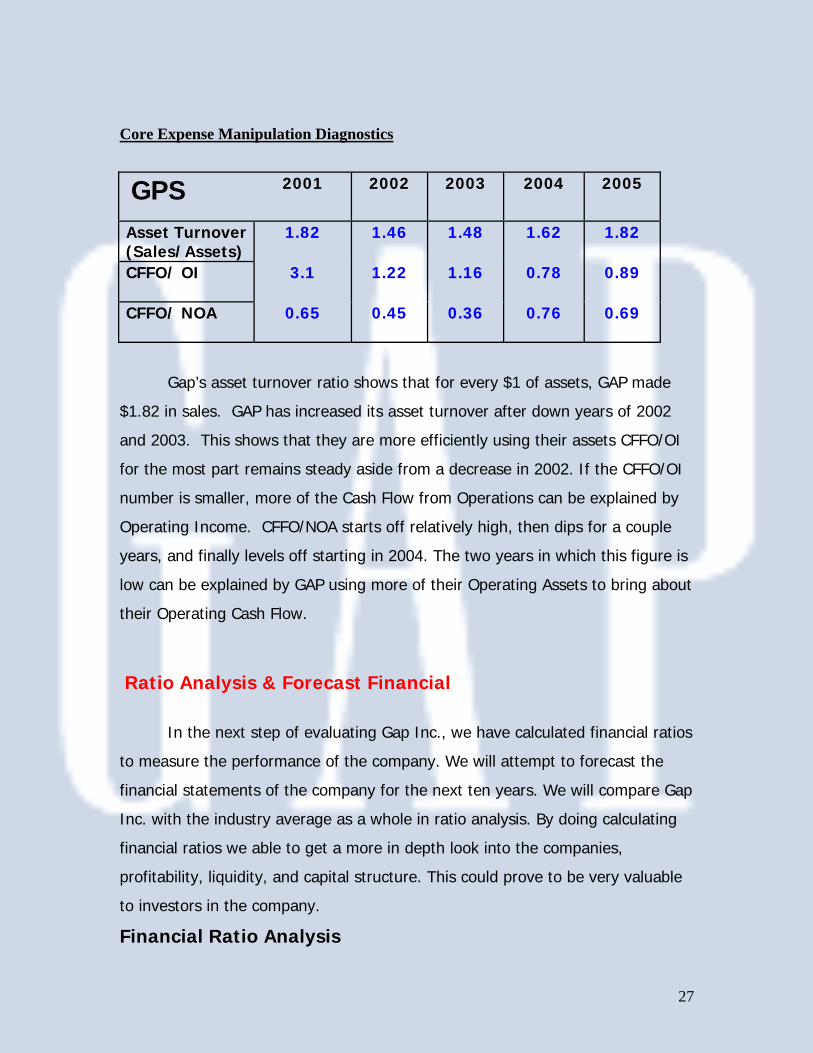

Core Expense Manipulation Diagnostics

GPS 2001 2002 2003 2004 2005

Asset Turnover (Sales/Assets)

1.82 1.46 1.48 1.62 1.82

CFFO/ OI 3.1 1.22 1.16 0.78 0.89

CFFO/ NOA 0.65 0.45 0.36 0.76 0.69

Gap’s asset turnover ratio shows that for every $1 of assets, GAP made

$1.82 in sales. GAP has increased its asset turnover after down years of 2002

and 2003. This shows that they are more efficiently using their assets CFFO/OI

for the most part remains steady aside from a decrease in 2002. If the CFFO/OI

number is smaller, more of the Cash Flow from Operations can be explained by

Operating Income. CFFO/NOA starts off relatively high, then dips for a couple

years, and finally levels off starting in 2004. The two years in which this figure is

low can be explained by GAP using more of their Operating Assets to bring about

their Operating Cash Flow.

Ratio Analysis & Forecast Financial

In the next step of evaluating Gap Inc., we have calculated financial ratios

to measure the performance of the company. We will attempt to forecast the

financial statements of the company for the next ten years. We will compare Gap

Inc. with the industry average as a whole in ratio analysis. By doing calculating

financial ratios we able to get a more in depth look into the companies,

profitability, liquidity, and capital structure. This could prove to be very valuable

to investors in the company.

Financial Ratio Analysis

28

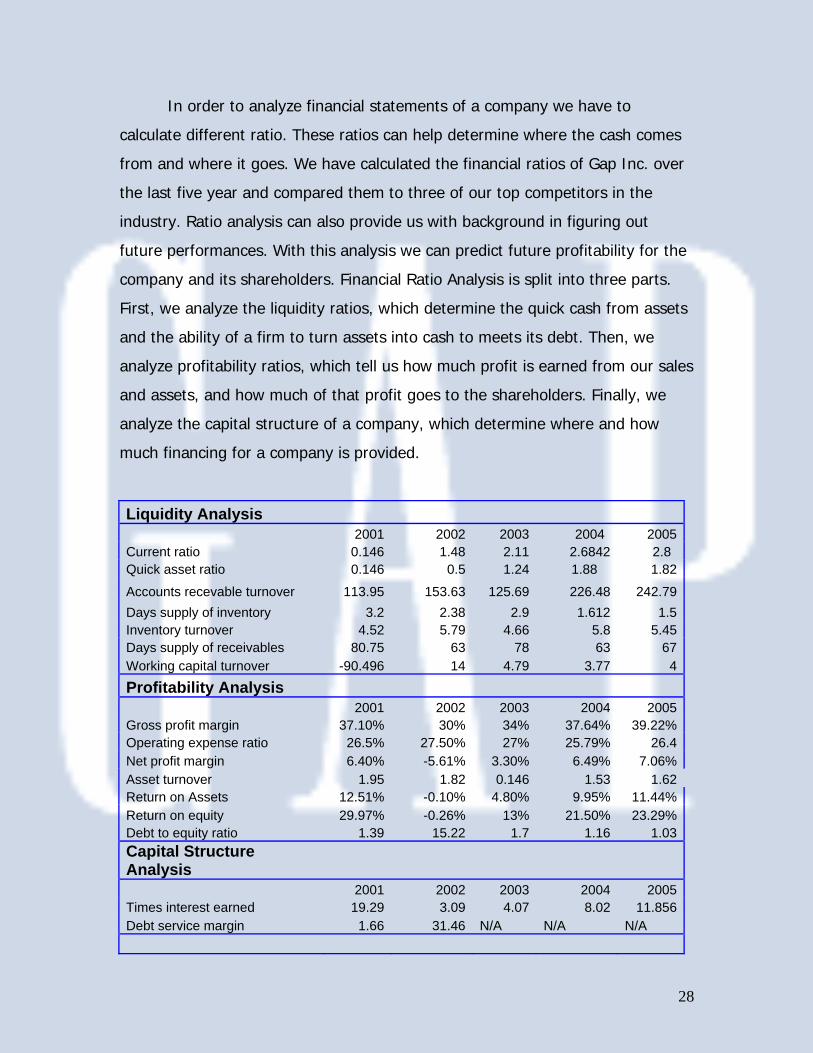

In order to analyze financial statements of a company we have to

calculate different ratio. These ratios can help determine where the cash comes

from and where it goes. We have calculated the financial ratios of Gap Inc. over

the last five year and compared them to three of our top competitors in the

industry. Ratio analysis can also provide us with background in figuring out

future performances. With this analysis we can predict future profitability for the

company and its shareholders. Financial Ratio Analysis is split into three parts.

First, we analyze the liquidity ratios, which determine the quick cash from assets

and the ability of a firm to turn assets into cash to meets its debt. Then, we

analyze profitability ratios, which tell us how much profit is earned from our sales

and assets, and how much of that profit goes to the shareholders. Finally, we

analyze the capital structure of a company, which determine where and how

much financing for a company is provided.

Liquidity Analysis 2001 2002 2003 2004 2005Current ratio 0.146 1.48 2.11 2.6842 2.8 Quick asset ratio 0.146 0.5 1.24 1.88 1.82

Accounts recevable turnover 113.95 153.63 125.69 226.48 242.79Days supply of inventory 3.2 2.38 2.9 1.612 1.5Inventory turnover 4.52 5.79 4.66 5.8 5.45Days supply of receivables 80.75 63 78 63 67Working capital turnover -90.496 14 4.79 3.77 4

Profitability Analysis 2001 2002 2003 2004 2005Gross profit margin 37.10% 30% 34% 37.64% 39.22%Operating expense ratio 26.5% 27.50% 27% 25.79% 26.4Net profit margin 6.40% -5.61% 3.30% 6.49% 7.06%Asset turnover 1.95 1.82 0.146 1.53 1.62Return on Assets 12.51% -0.10% 4.80% 9.95% 11.44%Return on equity 29.97% -0.26% 13% 21.50% 23.29%Debt to equity ratio 1.39 15.22 1.7 1.16 1.03Capital Structure Analysis 2001 2002 2003 2004 2005Times interest earned 19.29 3.09 4.07 8.02 11.856Debt service margin 1.66 31.46 N/A N/A N/A

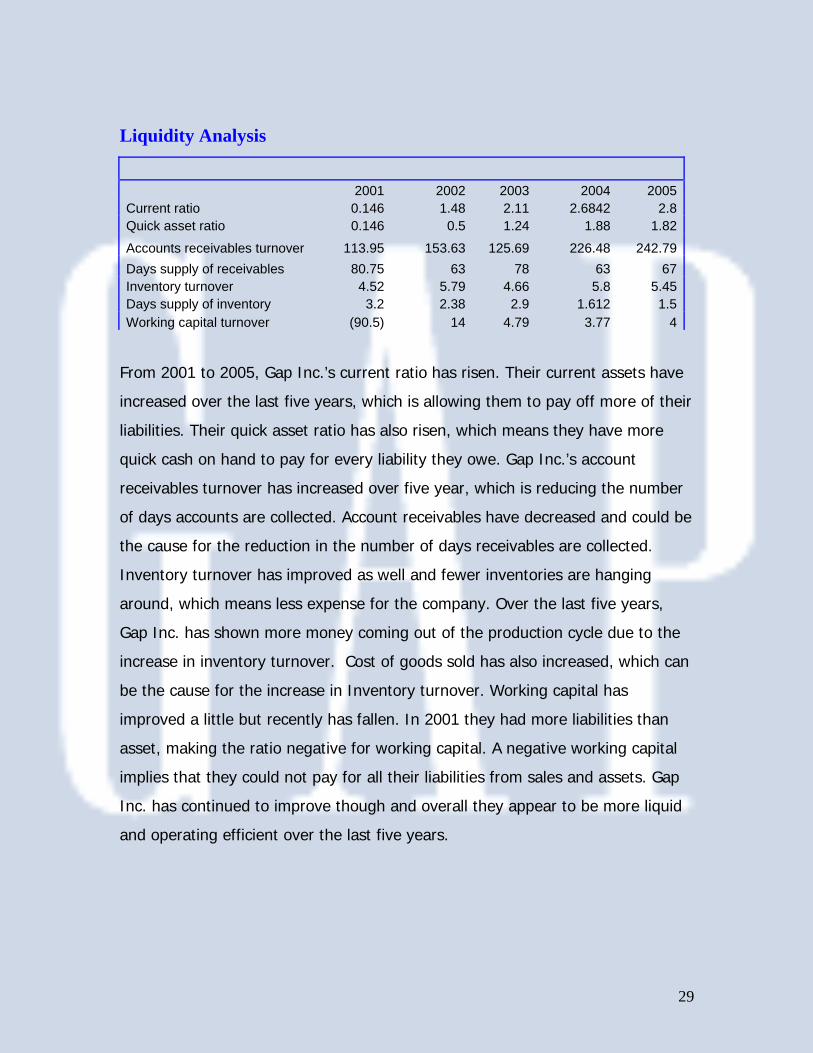

29

Liquidity Analysis

2001 2002 2003 2004 2005Current ratio 0.146 1.48 2.11 2.6842 2.8Quick asset ratio 0.146 0.5 1.24 1.88 1.82

Accounts receivables turnover 113.95 153.63 125.69 226.48 242.79Days supply of receivables 80.75 63 78 63 67Inventory turnover 4.52 5.79 4.66 5.8 5.45Days supply of inventory 3.2 2.38 2.9 1.612 1.5Working capital turnover (90.5) 14 4.79 3.77 4

From 2001 to 2005, Gap Inc.’s current ratio has risen. Their current assets have

increased over the last five years, which is allowing them to pay off more of their

liabilities. Their quick asset ratio has also risen, which means they have more

quick cash on hand to pay for every liability they owe. Gap Inc.’s account

receivables turnover has increased over five year, which is reducing the number

of days accounts are collected. Account receivables have decreased and could be

the cause for the reduction in the number of days receivables are collected.

Inventory turnover has improved as well and fewer inventories are hanging

around, which means less expense for the company. Over the last five years,

Gap Inc. has shown more money coming out of the production cycle due to the

increase in inventory turnover. Cost of goods sold has also increased, which can

be the cause for the increase in Inventory turnover. Working capital has

improved a little but recently has fallen. In 2001 they had more liabilities than

asset, making the ratio negative for working capital. A negative working capital

implies that they could not pay for all their liabilities from sales and assets. Gap

Inc. has continued to improve though and overall they appear to be more liquid

and operating efficient over the last five years.

30

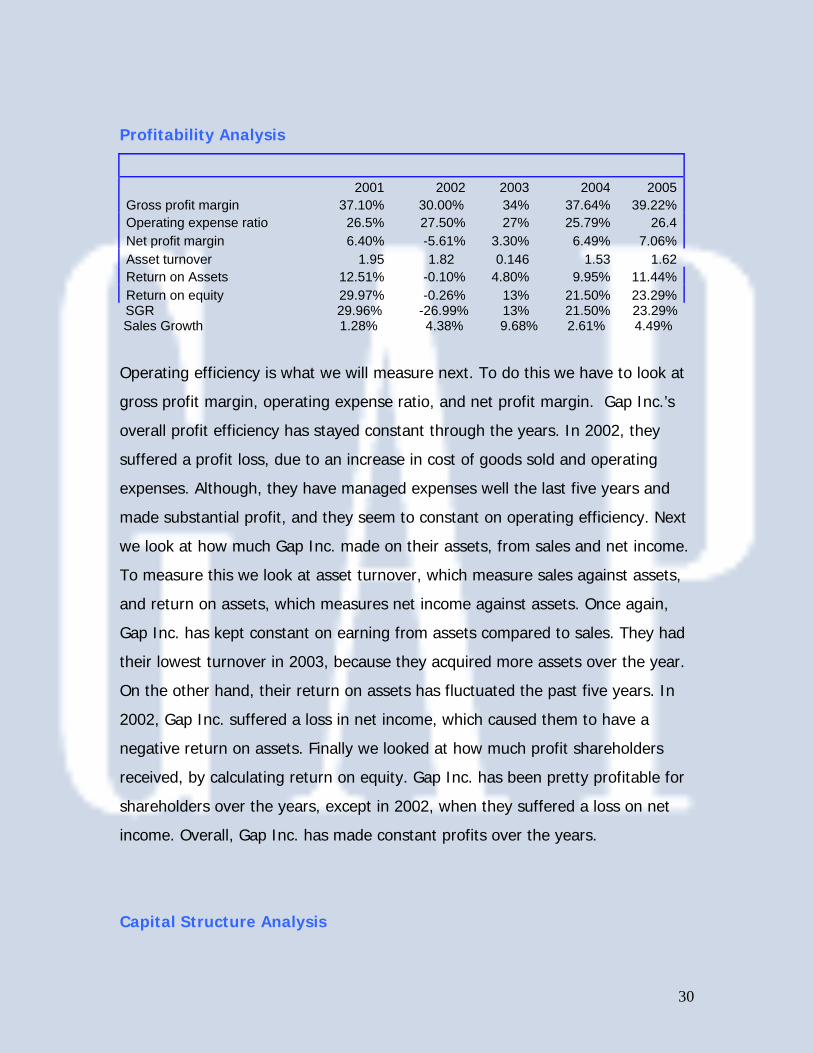

Profitability Analysis

2001 2002 2003 2004 2005Gross profit margin 37.10% 30.00% 34% 37.64% 39.22%Operating expense ratio 26.5% 27.50% 27% 25.79% 26.4Net profit margin 6.40% -5.61% 3.30% 6.49% 7.06%Asset turnover 1.95 1.82 0.146 1.53 1.62Return on Assets 12.51% -0.10% 4.80% 9.95% 11.44%Return on equity 29.97% -0.26% 13% 21.50% 23.29%

SGR 29.96% -26.99% 13% 21.50% 23.29% Sales Growth 1.28% 4.38% 9.68% 2.61% 4.49%

Operating efficiency is what we will measure next. To do this we have to look at

gross profit margin, operating expense ratio, and net profit margin. Gap Inc.’s

overall profit efficiency has stayed constant through the years. In 2002, they

suffered a profit loss, due to an increase in cost of goods sold and operating

expenses. Although, they have managed expenses well the last five years and

made substantial profit, and they seem to constant on operating efficiency. Next

we look at how much Gap Inc. made on their assets, from sales and net income.

To measure this we look at asset turnover, which measure sales against assets,

and return on assets, which measures net income against assets. Once again,

Gap Inc. has kept constant on earning from assets compared to sales. They had

their lowest turnover in 2003, because they acquired more assets over the year.

On the other hand, their return on assets has fluctuated the past five years. In

2002, Gap Inc. suffered a loss in net income, which caused them to have a

negative return on assets. Finally we looked at how much profit shareholders

received, by calculating return on equity. Gap Inc. has been pretty profitable for

shareholders over the years, except in 2002, when they suffered a loss on net

income. Overall, Gap Inc. has made constant profits over the years.

Capital Structure Analysis

31

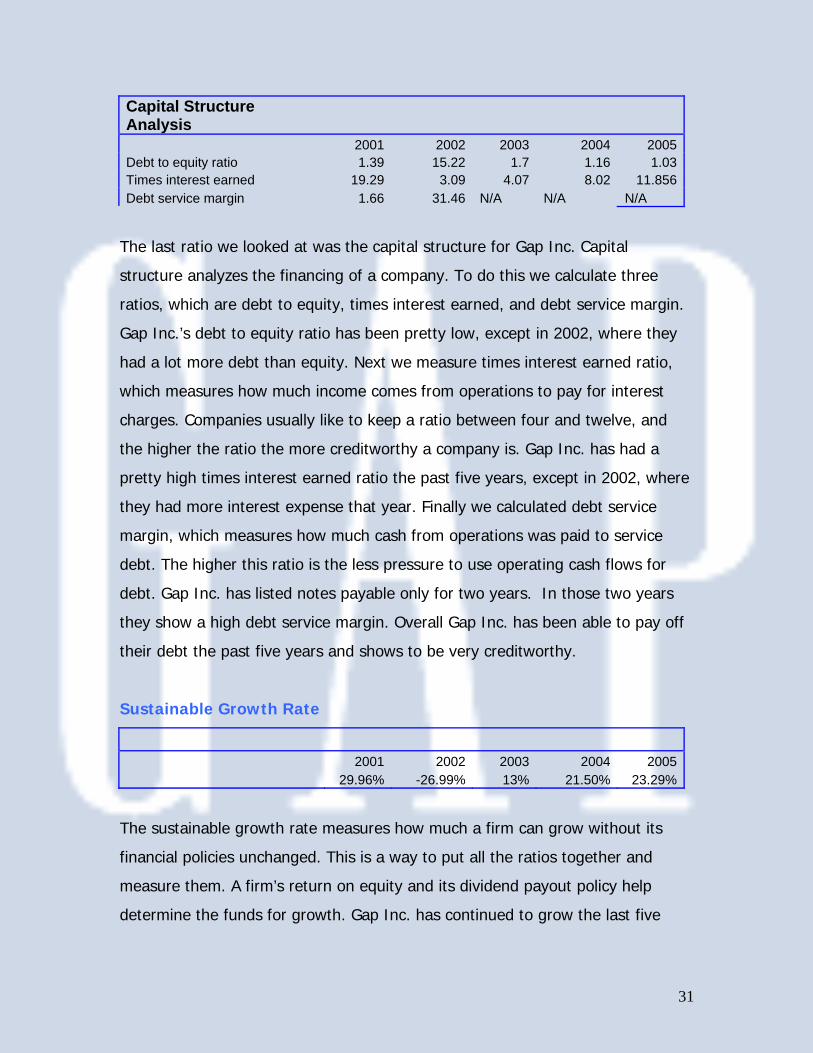

Capital Structure Analysis 2001 2002 2003 2004 2005Debt to equity ratio 1.39 15.22 1.7 1.16 1.03Times interest earned 19.29 3.09 4.07 8.02 11.856Debt service margin 1.66 31.46 N/A N/A N/A

The last ratio we looked at was the capital structure for Gap Inc. Capital

structure analyzes the financing of a company. To do this we calculate three

ratios, which are debt to equity, times interest earned, and debt service margin.

Gap Inc.’s debt to equity ratio has been pretty low, except in 2002, where they

had a lot more debt than equity. Next we measure times interest earned ratio,

which measures how much income comes from operations to pay for interest

charges. Companies usually like to keep a ratio between four and twelve, and

the higher the ratio the more creditworthy a company is. Gap Inc. has had a

pretty high times interest earned ratio the past five years, except in 2002, where

they had more interest expense that year. Finally we calculated debt service

margin, which measures how much cash from operations was paid to service

debt. The higher this ratio is the less pressure to use operating cash flows for

debt. Gap Inc. has listed notes payable only for two years. In those two years

they show a high debt service margin. Overall Gap Inc. has been able to pay off

their debt the past five years and shows to be very creditworthy.

Sustainable Growth Rate

2001 2002 2003 2004 2005 29.96% -26.99% 13% 21.50% 23.29%

The sustainable growth rate measures how much a firm can grow without its

financial policies unchanged. This is a way to put all the ratios together and

measure them. A firm’s return on equity and its dividend payout policy help

determine the funds for growth. Gap Inc. has continued to grow the last five

32

years. They suffered a loss in 2002, which caused them to not grow. Overall they

have kept a constant growth rate around 20 % each year.

Benchmark Analysis

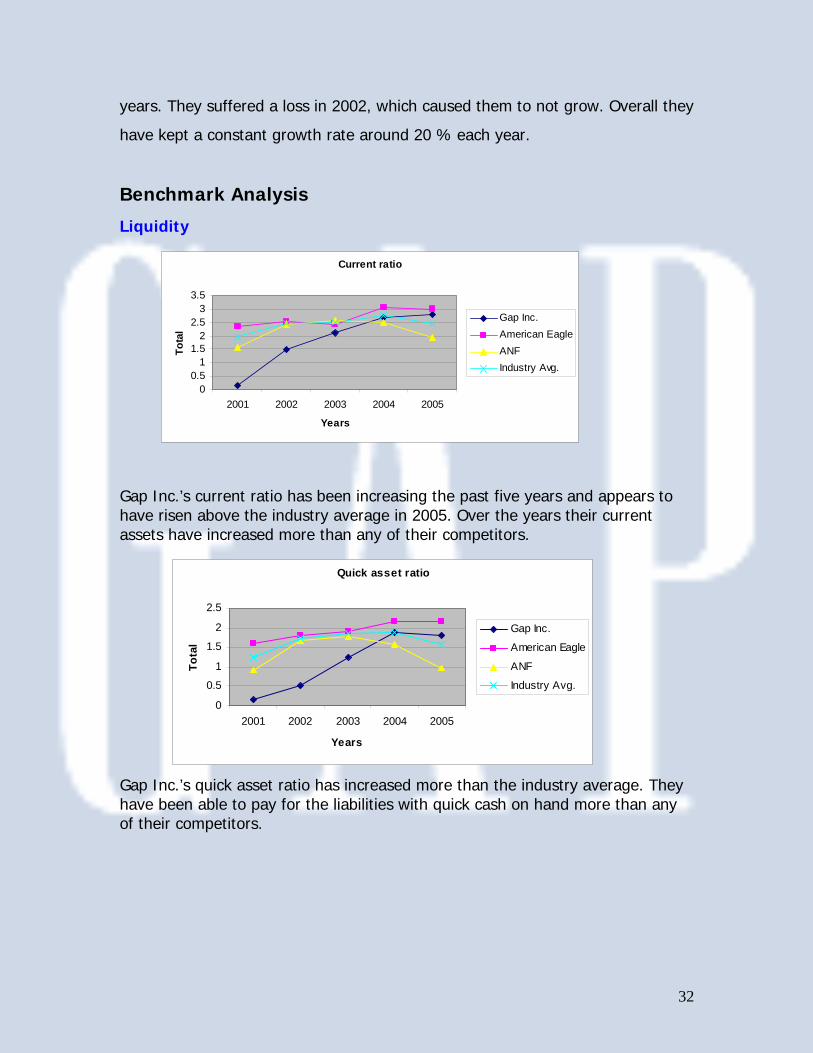

Liquidity

Gap Inc.’s current ratio has been increasing the past five years and appears to have risen above the industry average in 2005. Over the years their current assets have increased more than any of their competitors. Gap Inc.’s quick asset ratio has increased more than the industry average. They have been able to pay for the liabilities with quick cash on hand more than any of their competitors.

Current ratio

00.5

11.5

22.5

33.5

2001 2002 2003 2004 2005

Years

Tota

l

Gap Inc.American EagleANFIndustry Avg.

Quick asset ratio

0

0.5

1

1.5

2

2.5

2001 2002 2003 2004 2005

Years

Tota

l

Gap Inc.

American Eagle

ANF

Industry Avg.

33

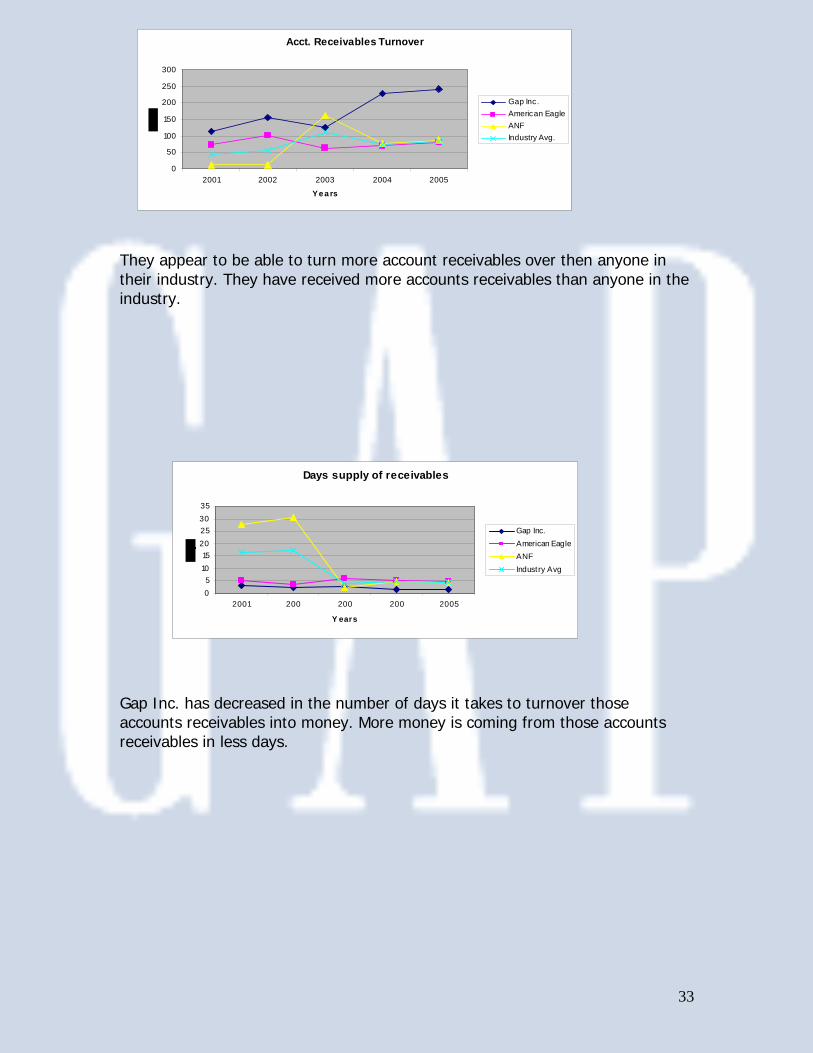

They appear to be able to turn more account receivables over then anyone in their industry. They have received more accounts receivables than anyone in the industry. Gap Inc. has decreased in the number of days it takes to turnover those accounts receivables into money. More money is coming from those accounts receivables in less days.

Acct. Receivables Turnover

0

50

100

150

200

250

300

2001 2002 2003 2004 2005

Ye a rs

Gap Inc.American EagleANFIndustry Avg.

Days supply of receivables

05

1015

20253035

2001 200 200 200 2005

Y ears

Gap Inc.American EagleANFIndustry Avg

34

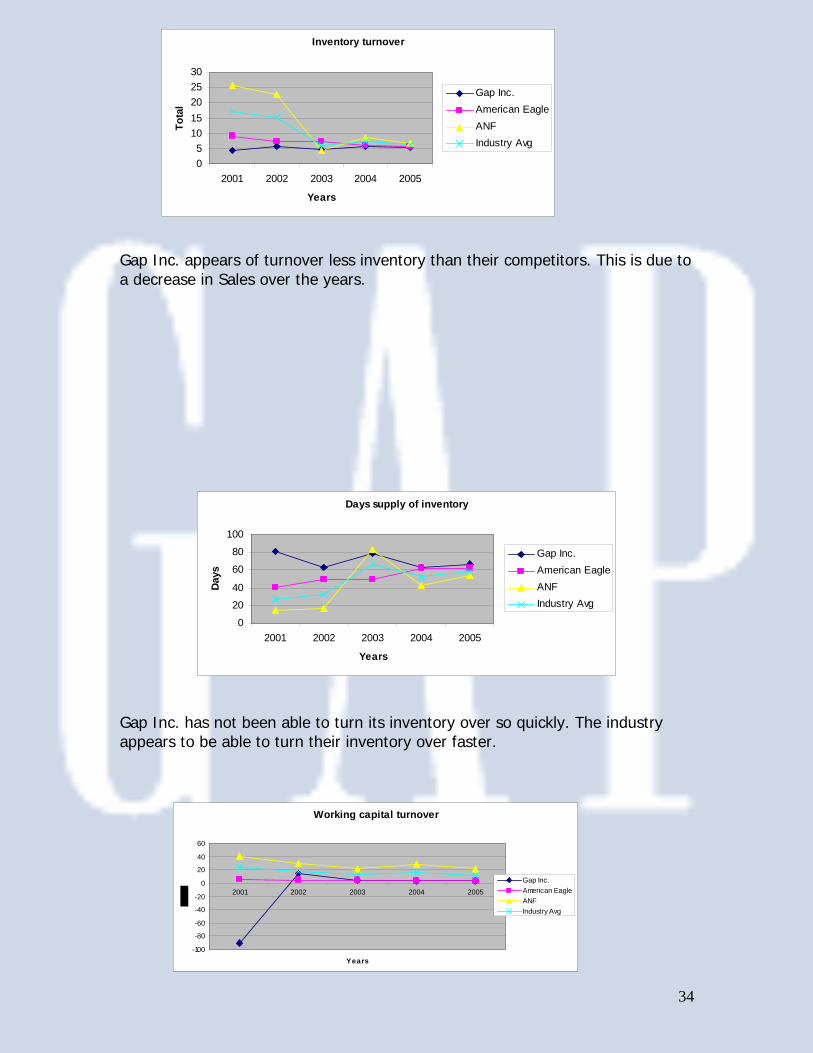

Gap Inc. appears of turnover less inventory than their competitors. This is due to a decrease in Sales over the years. Gap Inc. has not been able to turn its inventory over so quickly. The industry appears to be able to turn their inventory over faster.

Inventory turnover

05

1015202530

2001 2002 2003 2004 2005

Years

Tota

l

Gap Inc.American EagleANFIndustry Avg

Days supply of inventory

0

20

40

60

80

100

2001 2002 2003 2004 2005

Years

Days

Gap Inc.American EagleANFIndustry Avg

Working capital turnover

-100

-80

-60

-40

-20

0

20

40

60

2001 2002 2003 2004 2005

Years

Gap Inc.American EagleANFIndustry Avg

35

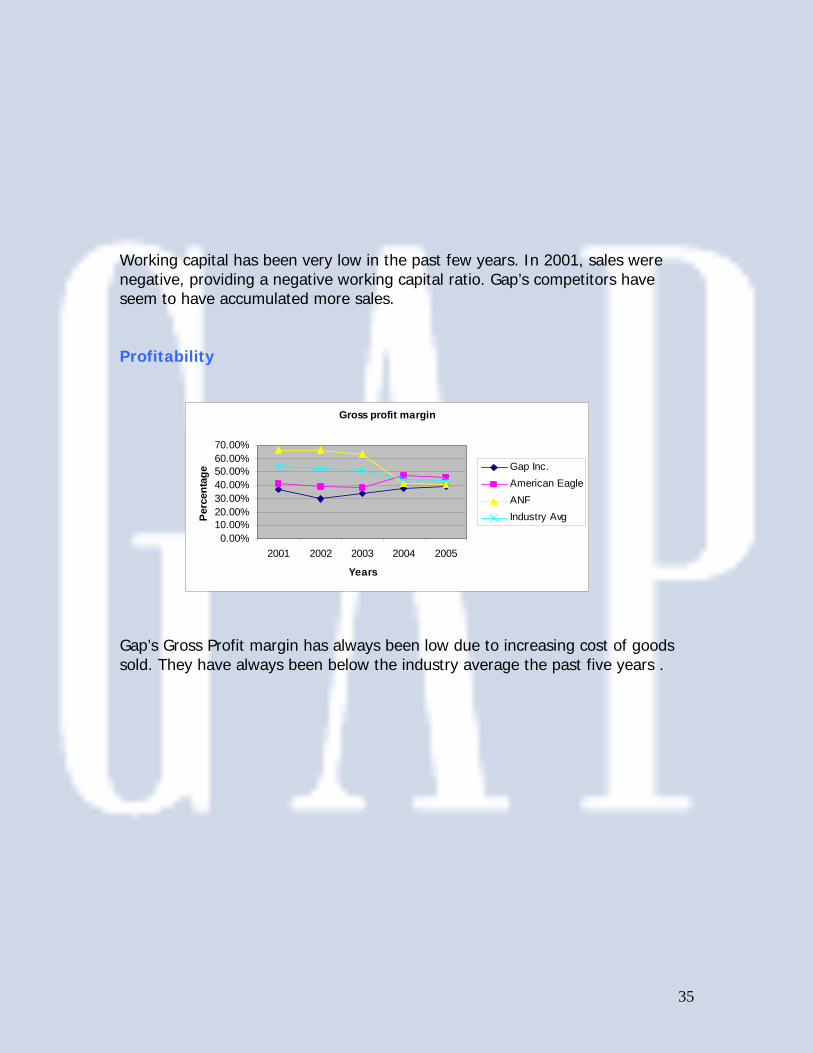

Working capital has been very low in the past few years. In 2001, sales were negative, providing a negative working capital ratio. Gap’s competitors have seem to have accumulated more sales. Profitability Gap’s Gross Profit margin has always been low due to increasing cost of goods sold. They have always been below the industry average the past five years .

Gross profit margin

0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%

2001 2002 2003 2004 2005

Years

Perc

enta

ge

Gap Inc.American EagleANFIndustry Avg

36

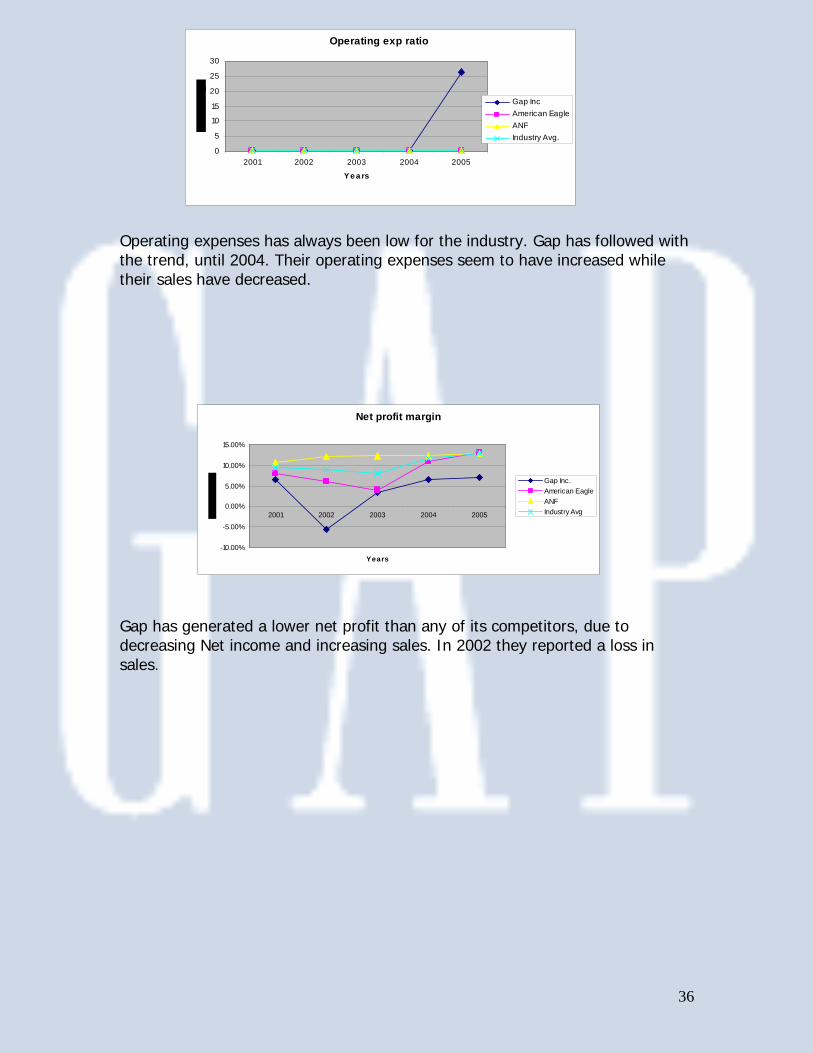

Operating expenses has always been low for the industry. Gap has followed with the trend, until 2004. Their operating expenses seem to have increased while their sales have decreased. Gap has generated a lower net profit than any of its competitors, due to decreasing Net income and increasing sales. In 2002 they reported a loss in sales.

Operating exp ratio

0

5

10

15

20

25

30

2001 2002 2003 2004 2005

Ye a rs

Gap IncAmerican EagleANFIndustry Avg.

Net profit margin

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

2001 2002 2003 2004 2005

Years

Gap Inc.American EagleANFIndustry Avg

37

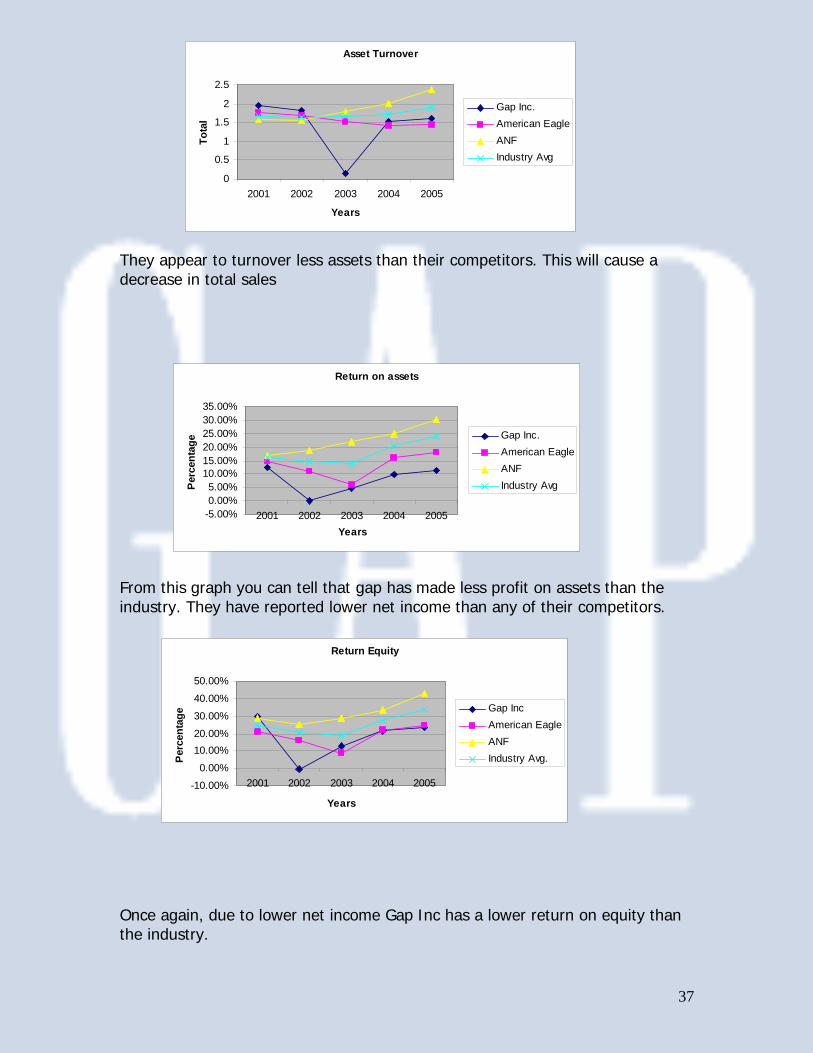

They appear to turnover less assets than their competitors. This will cause a decrease in total sales From this graph you can tell that gap has made less profit on assets than the industry. They have reported lower net income than any of their competitors. Once again, due to lower net income Gap Inc has a lower return on equity than the industry.

Asset Turnover

0

0.5

1

1.5

2

2.5

2001 2002 2003 2004 2005

Years To

tal

Gap Inc.American EagleANFIndustry Avg

Return on assets

-5.00%0.00%5.00%

10.00%15.00%20.00%25.00%30.00%35.00%

2001 2002 2003 2004 2005Years

Perc

enta

ge

Gap Inc.American EagleANFIndustry Avg

Return Equity

-10.00%

0.00%

10.00%20.00%

30.00%

40.00%

50.00%

2001 2002 2003 2004 2005

Years

Perc

enta

ge

Gap IncAmerican EagleANFIndustry Avg.

38

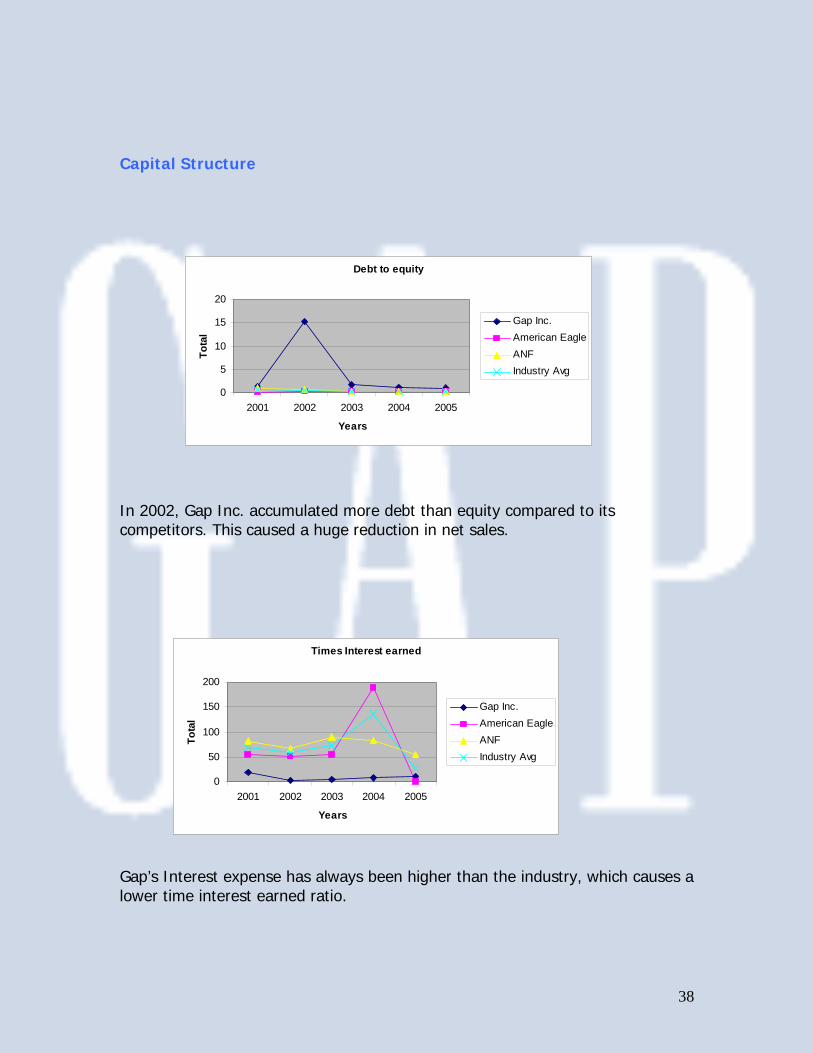

Capital Structure In 2002, Gap Inc. accumulated more debt than equity compared to its competitors. This caused a huge reduction in net sales. Gap’s Interest expense has always been higher than the industry, which causes a lower time interest earned ratio.

Debt to equity

0

5

10

15

20

2001 2002 2003 2004 2005

Years

Tota

l

Gap Inc.American EagleANFIndustry Avg

Times Interest earned

0

50

100

150

200

2001 2002 2003 2004 2005

Years

Tota

l

Gap Inc.American EagleANFIndustry Avg

39

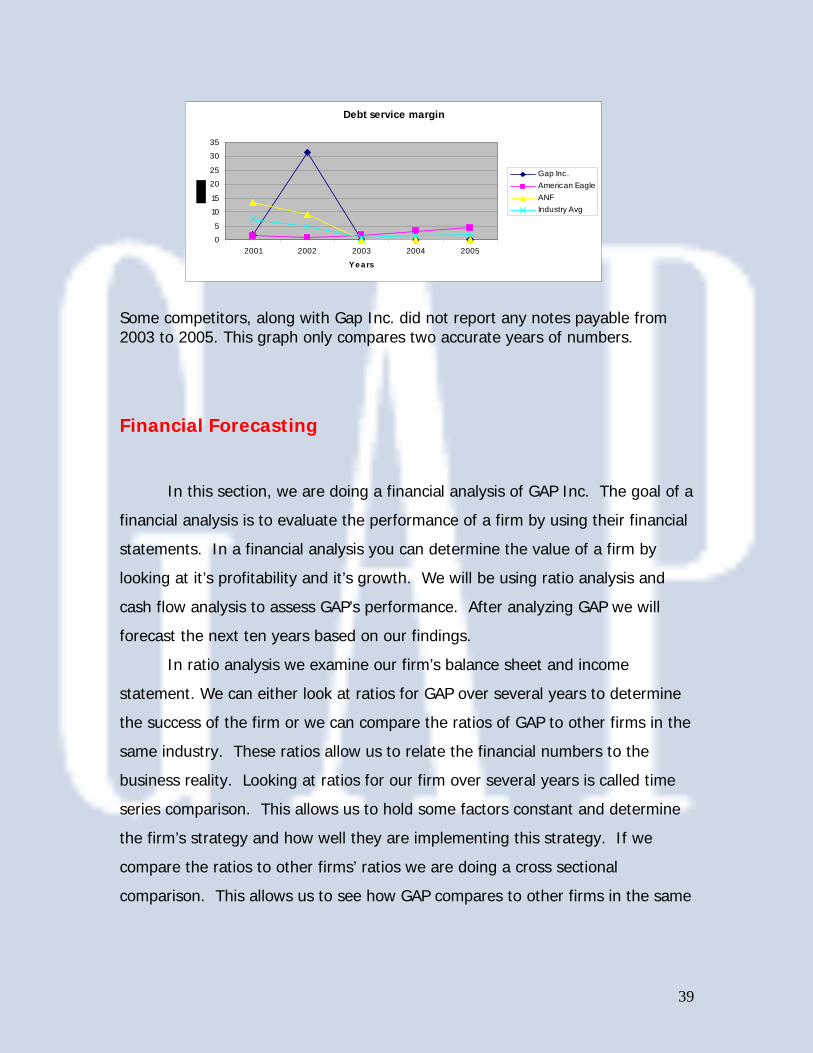

Some competitors, along with Gap Inc. did not report any notes payable from 2003 to 2005. This graph only compares two accurate years of numbers. Financial Forecasting In this section, we are doing a financial analysis of GAP Inc. The goal of a

financial analysis is to evaluate the performance of a firm by using their financial

statements. In a financial analysis you can determine the value of a firm by

looking at it’s profitability and it’s growth. We will be using ratio analysis and

cash flow analysis to assess GAP’s performance. After analyzing GAP we will

forecast the next ten years based on our findings.

In ratio analysis we examine our firm’s balance sheet and income

statement. We can either look at ratios for GAP over several years to determine

the success of the firm or we can compare the ratios of GAP to other firms in the

same industry. These ratios allow us to relate the financial numbers to the

business reality. Looking at ratios for our firm over several years is called time

series comparison. This allows us to hold some factors constant and determine

the firm’s strategy and how well they are implementing this strategy. If we

compare the ratios to other firms’ ratios we are doing a cross sectional

comparison. This allows us to see how GAP compares to other firms in the same

Debt service margin

0

5

10

15

20

25

30

35

2001 2002 2003 2004 2005

Ye a rs

Gap Inc.American EagleANFIndustry Avg

40

industry. This lets us determine in what areas they are lacking and what areas

they are excelling in compared to firms in the same industry.

In cash flow analysis we study the firm’s cash flow statements to get

further insights into the firm’s policies. By looking at the cash flow we can find a

number of things that are important to valuing our firm. We can see if our firm

has the ability to pay its interest and long term debt payments from the cash

generated from operations. We can also find if GAP is making a cash surplus

from operations or making enough cash to invest in long term growth. These

things can give us a better idea of the risk of our firm.

Finally after analyzing GAP’s financial statements, we can forecast the

future for the firm. It is important to forecast so we can determine the future of

the firm and if the firm is currently undervalued or overvalued. We can use a

number of methods to determine our forecasting values. You can average past

performances of the firm and assume this past performance will continue.

Sometimes this can provide inaccurate numbers. So values are mean-reverting,

which means that over time they go back to the industry average.

Our financial analysis and forecast of GAP should provide a clearer picture

of the performance of GAP then just scanning their financial statement. This will

allow us to determine the success that GAP has had in implementing strategies

and gaining profitability and growth.

Balance Sheet Forecasting

The accounts on the balance sheet that we feel are the most important to

forecast are accounts payable, total current liabilities, total liabilities, common

stock, total shareholder’s equity, and sales growth. Accounts payable, current

liabilities, and total liabilities show us our debt. Common stock, and total

shareholder’s equity shows us how we are financing our firm through equity.

Sales growth is important because it is what drives our firm. We need a high

41

sales growth to continue creating value for our shareholders. We took the

averages of values off the common size balance sheet to forecast for our actual

balance sheet. The only account forecasted using another method was the total

current liabilities. For this account, we used the current ratio to forecast. While

these projections can prove to be extremely helpful, we realize that these

numbers may not be 100% accurate. If there are any major changes within the

company, the forecasts will deviate from the projections made when forecasted.

Even with the weaknesses in our forecasting method, we feel that the methods

used were the most appropriate for GAP Inc.( Refer to Exhibit B)

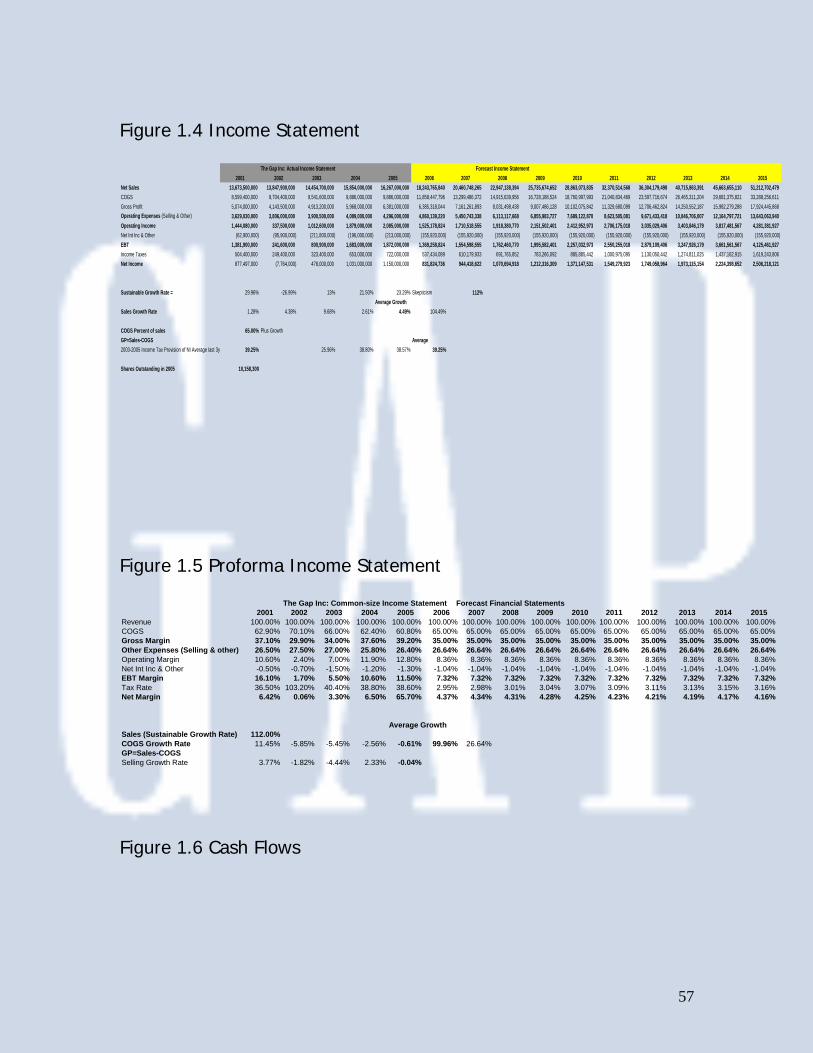

Income Statement Forecasting We were able to forecast every account in our income statement. The

most important ones for GAP are net sales, Cost of Goods Sold, Operating

Expenses, and Net Income. Net sales show us how much GAP is selling

throughout its many stores. Cost of Goods sold and operating expenses give us

an overview of the cost of doing business for GAP. We can analyze this and see

where their costs are too high. Net income is also important because it gives us

our final dollar amount that we earned for the year. All of the accounts were

forecasted by taking the average off the common size income statement. As

always the case with forecasting these numbers could be changed by any

change in GAP’s operations.

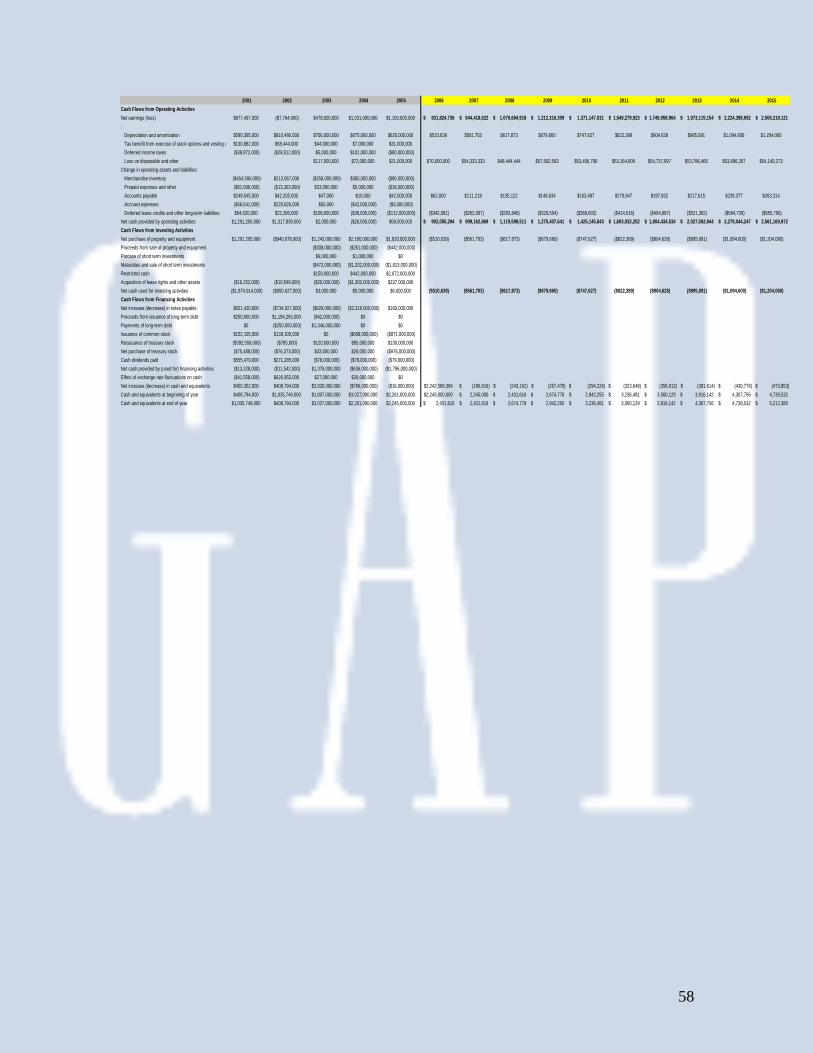

Cash Flow Forecasting The accounts used in forecasting some of Gap’s Cash Flows were net

earnings, depreciation and amortization, loss on disposable and other, accounts

payable, deferred lease credits and other long term liabilities, net cash provided

by operating activities, net purchase of property and equipment, net cash used

for investing activities, net increase/ decrease in cash and equivalents, and cash

and equivalents for beginning and year end. The majority of the values derived

42

upon forecasting cash flows come simply from the balance sheet and income

statements; either through subtraction of the trailing year, or an average of the

percentage change multiplied by a corresponding number in the balance sheet or

income statement. However, the loss on disposable and other account was

derived through and average of the trailing three years for each year forecasted.

Just as the methods used to forecast the balance sheet, the methods used to

forecast the cash flows can be helpful for figuring ballpark numbers and aid in

decision making. However this forecasting method is based mainly on recent

information and is not always a good predictor to future performance.

Valuation Analysis

So far we have calculated the financial ratios and forecasted financial

statements for the next ten years, which was the first stage of prospective

analysis. In this is section we will complete prospective analysis by valuing Gap

Inc. through different methods. Valuation is important because we can price an

initial public offering and be able to inform parties involved with Gap Inc. on their

actual sales, credit and other business concerns. In order to evaluate a company

we use many different methods, because one method alone cannot provide a

sound basis for a firm valuation. Intrinsic methods along with comparable ratios

must be calculated for the firm in order to get a true picture of what the

company is worth. Also, we need to create a sensitivity analysis which will make

sure that miscalculated costs of capital and growth rates will not give us bad

results. The cost of capital and equity will give us a weighted average cost of

43

capital, which is used in many of our intrinsic valuation models. The following

sections will demonstrate how we use each intrinsic valuation method to value

Gap Inc.

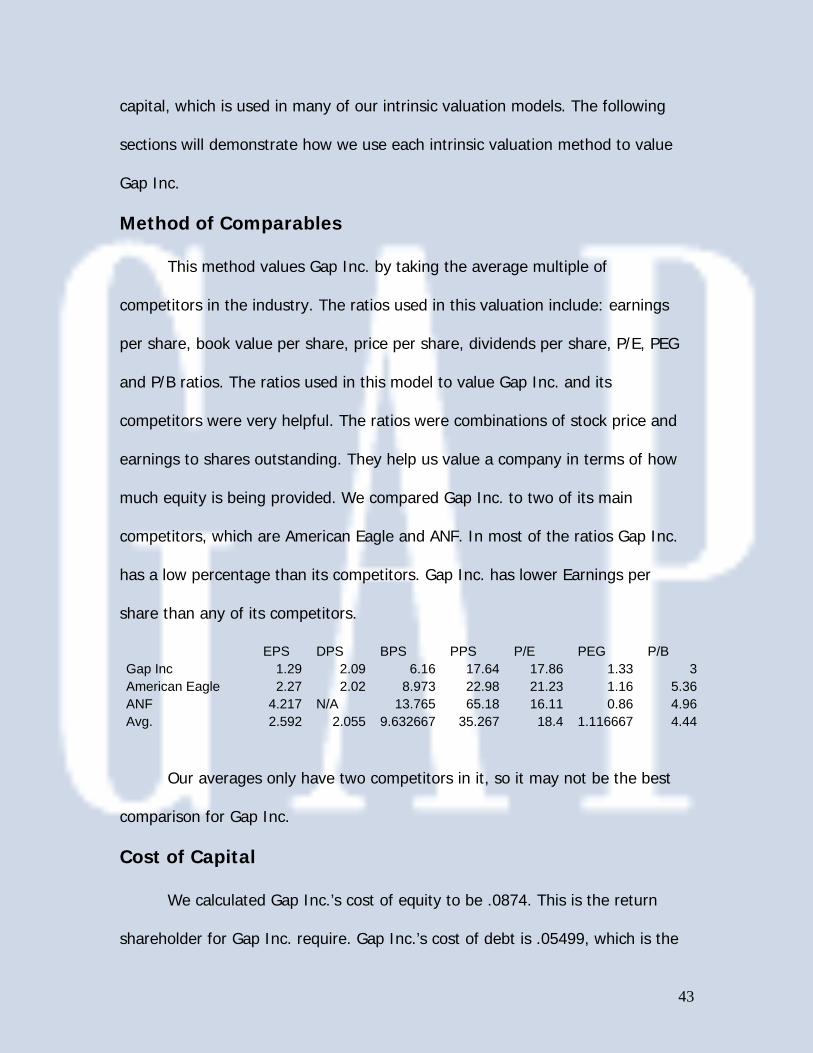

Method of Comparables

This method values Gap Inc. by taking the average multiple of

competitors in the industry. The ratios used in this valuation include: earnings

per share, book value per share, price per share, dividends per share, P/E, PEG

and P/B ratios. The ratios used in this model to value Gap Inc. and its

competitors were very helpful. The ratios were combinations of stock price and

earnings to shares outstanding. They help us value a company in terms of how

much equity is being provided. We compared Gap Inc. to two of its main

competitors, which are American Eagle and ANF. In most of the ratios Gap Inc.

has a low percentage than its competitors. Gap Inc. has lower Earnings per

share than any of its competitors.

EPS DPS BPS PPS P/E PEG P/B Gap Inc 1.29 2.09 6.16 17.64 17.86 1.33 3American Eagle 2.27 2.02 8.973 22.98 21.23 1.16 5.36ANF 4.217 N/A 13.765 65.18 16.11 0.86 4.96Avg. 2.592 2.055 9.632667 35.267 18.4 1.116667 4.44

Our averages only have two competitors in it, so it may not be the best

comparison for Gap Inc.

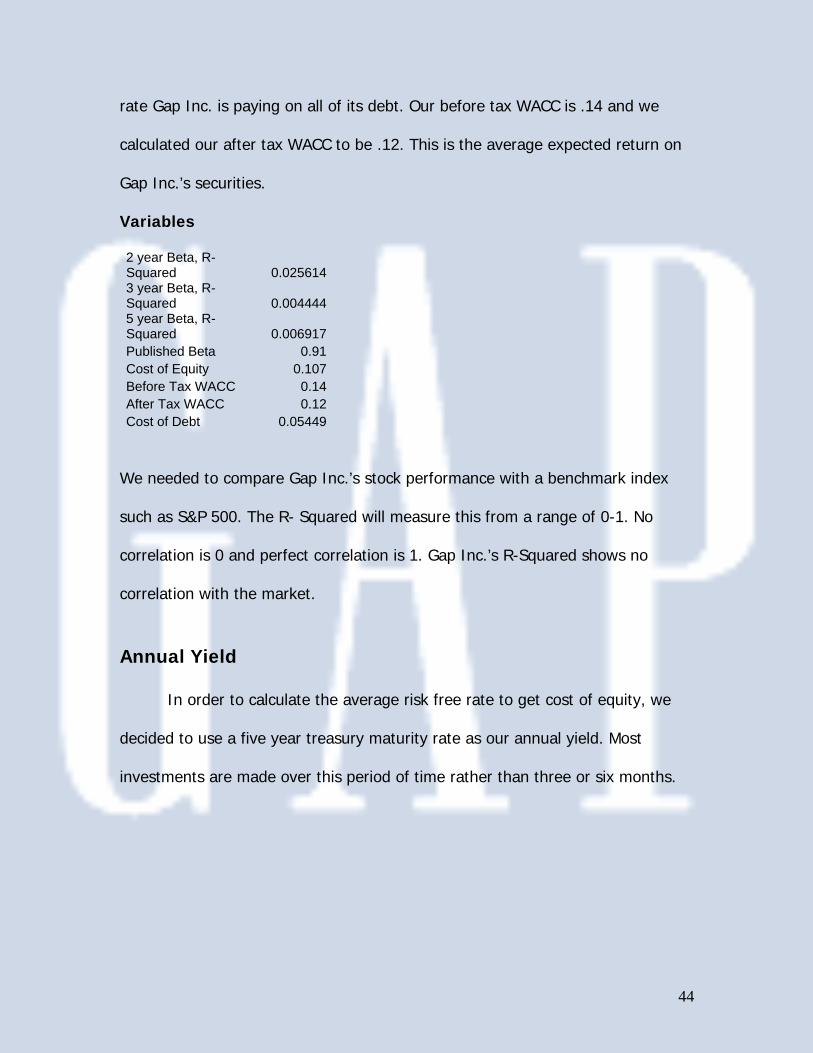

Cost of Capital

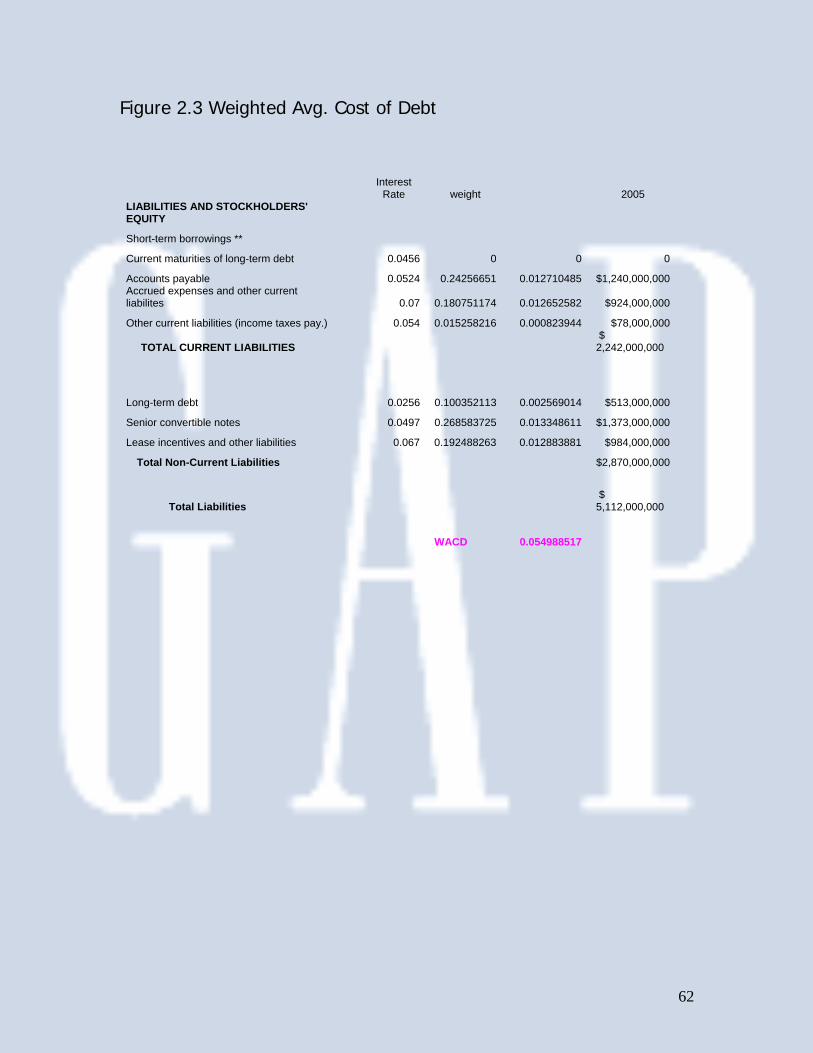

We calculated Gap Inc.’s cost of equity to be .0874. This is the return

shareholder for Gap Inc. require. Gap Inc.’s cost of debt is .05499, which is the

44

rate Gap Inc. is paying on all of its debt. Our before tax WACC is .14 and we

calculated our after tax WACC to be .12. This is the average expected return on

Gap Inc.’s securities.

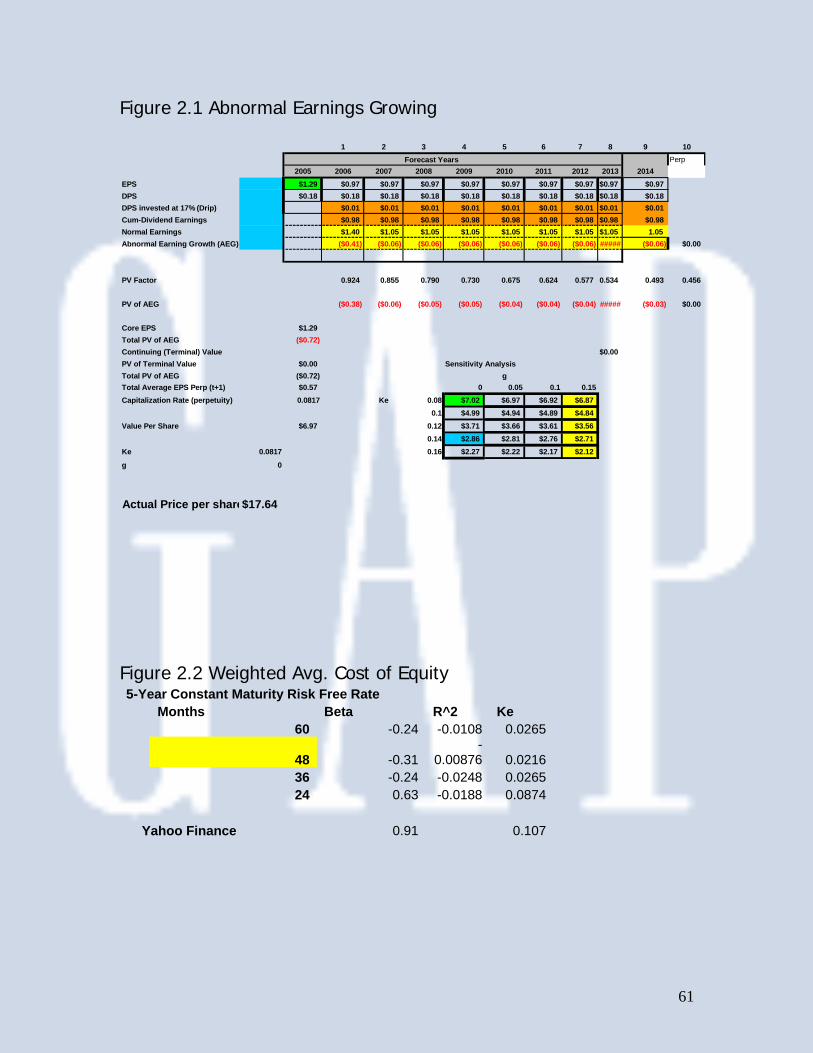

Variables

2 year Beta, R-Squared 0.025614 3 year Beta, R-Squared 0.004444 5 year Beta, R-Squared 0.006917 Published Beta 0.91 Cost of Equity 0.107 Before Tax WACC 0.14 After Tax WACC 0.12 Cost of Debt 0.05449

We needed to compare Gap Inc.’s stock performance with a benchmark index

such as S&P 500. The R- Squared will measure this from a range of 0-1. No

correlation is 0 and perfect correlation is 1. Gap Inc.’s R-Squared shows no

correlation with the market.

Annual Yield In order to calculate the average risk free rate to get cost of equity, we

decided to use a five year treasury maturity rate as our annual yield. Most

investments are made over this period of time rather than three or six months.

45

Intrinsic Valuation Methods

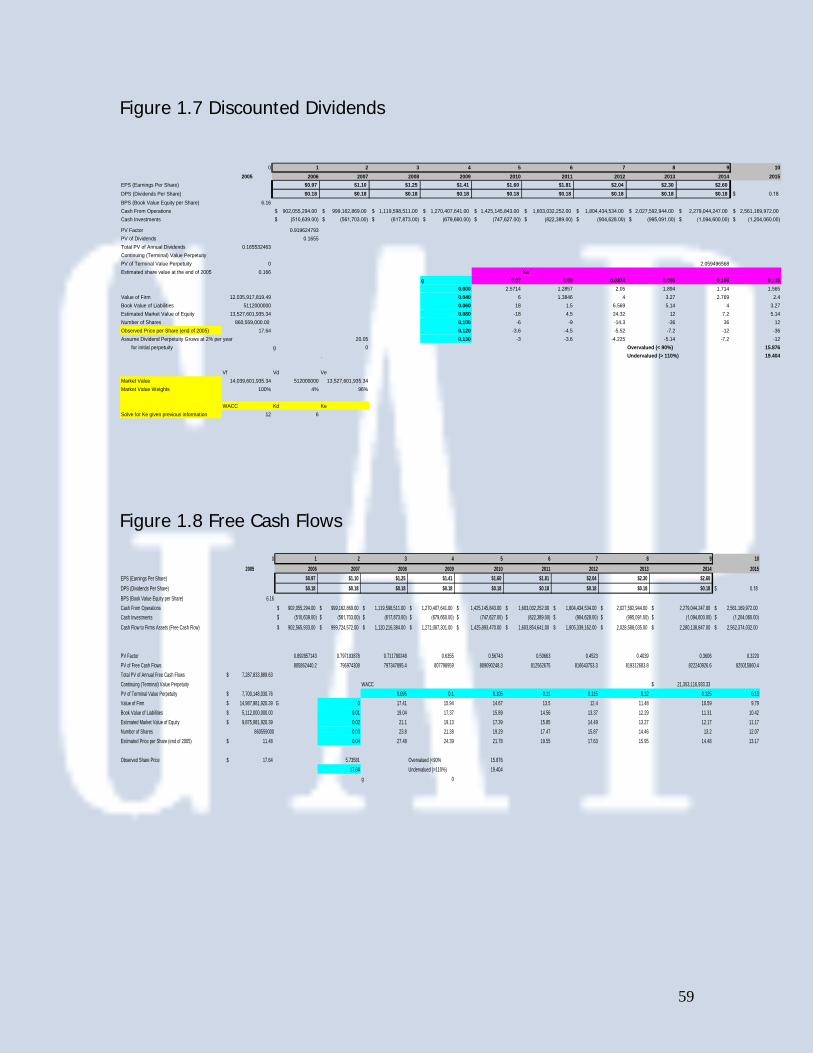

Free Cash Flow

Free cash flows will give us an estimated share price for the firm. This

model uses the WACC based on a flow of free cash flows. We calculated the free

cash flows by adding the cash flow from operations and investing activities. We

discounted are WACC back to 2005. We calculated the total present value of

annual free cash flows to be $ 6,971,364,299.14. Next, we had to find the

present value of the continuing terminal value, and with no growth we found it

to be $ 19,710,569,476.92. To find the value of the firm we added the present

value of the annual cash flows and the present value of terminal value

perpetuity. We found the value of the firm for 2005 to be $ 13,532,713,935.34.

Finally, we needed to find the estimated price per share at the end of 2005. To

do this we first needed to find the market value of equity, which is calculated by

subtracting the estimated value of the firm by the liabilities. Our estimated

market value of equity came out to be $ 13,527,601,935.34. Finally, divide our

estimated market value of Equity by the number of outstanding shares, to find

an estimated price per share at the end of 2005 to be $15.72. Gap Inc.’s

observed share price at the end of 2005 was 17.64, which tells us that Gap Inc.

was slightly overvalued. (Refer to 1.8)

46

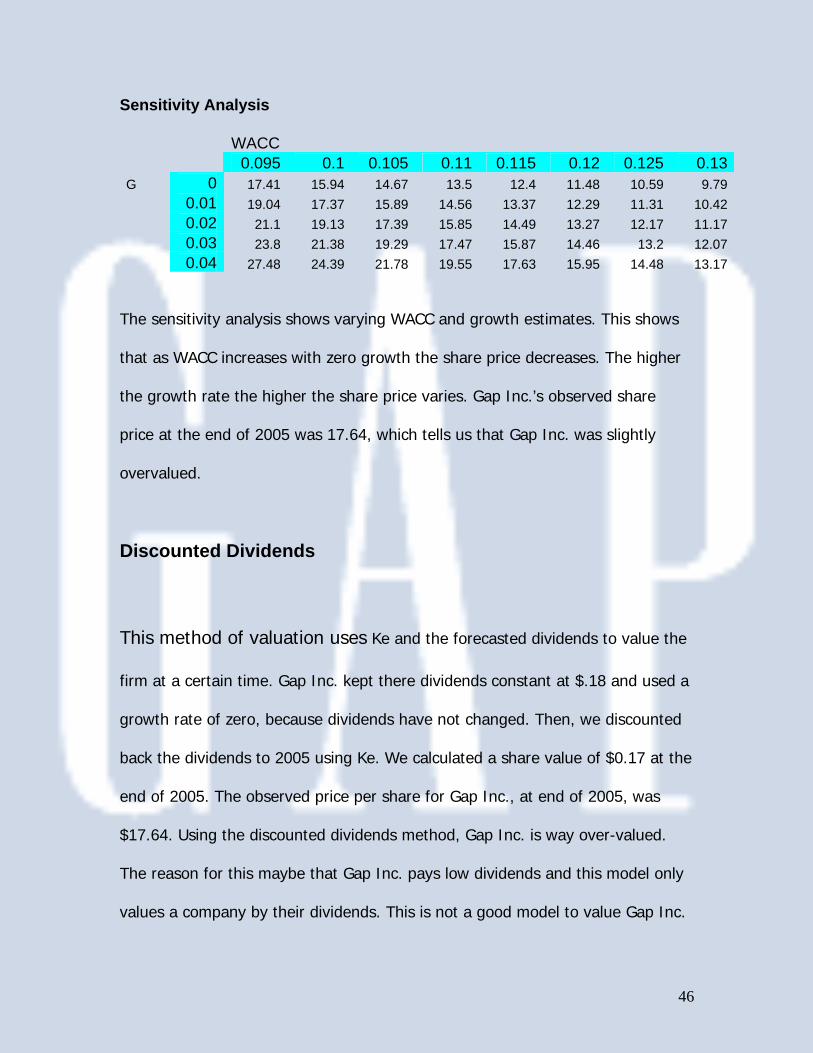

Sensitivity Analysis

WACC 0.095 0.1 0.105 0.11 0.115 0.12 0.125 0.13G 0 17.41 15.94 14.67 13.5 12.4 11.48 10.59 9.79 0.01 19.04 17.37 15.89 14.56 13.37 12.29 11.31 10.42 0.02 21.1 19.13 17.39 15.85 14.49 13.27 12.17 11.17 0.03 23.8 21.38 19.29 17.47 15.87 14.46 13.2 12.07 0.04 27.48 24.39 21.78 19.55 17.63 15.95 14.48 13.17

The sensitivity analysis shows varying WACC and growth estimates. This shows

that as WACC increases with zero growth the share price decreases. The higher

the growth rate the higher the share price varies. Gap Inc.’s observed share

price at the end of 2005 was 17.64, which tells us that Gap Inc. was slightly

overvalued.

Discounted Dividends

This method of valuation uses Ke and the forecasted dividends to value the

firm at a certain time. Gap Inc. kept there dividends constant at $.18 and used a

growth rate of zero, because dividends have not changed. Then, we discounted

back the dividends to 2005 using Ke. We calculated a share value of $0.17 at the

end of 2005. The observed price per share for Gap Inc., at end of 2005, was

$17.64. Using the discounted dividends method, Gap Inc. is way over-valued.

The reason for this maybe that Gap Inc. pays low dividends and this model only

values a company by their dividends. This is not a good model to value Gap Inc.

47

From the sensitivity analysis you can see the growth rate cannot be very high.

Just to get to price per share, the growth rate would have to be than 1 %. This

model is not very accurate in valuing Gap Inc., and should not be considered in

the final valuing of this company. (Refer to 1.7)

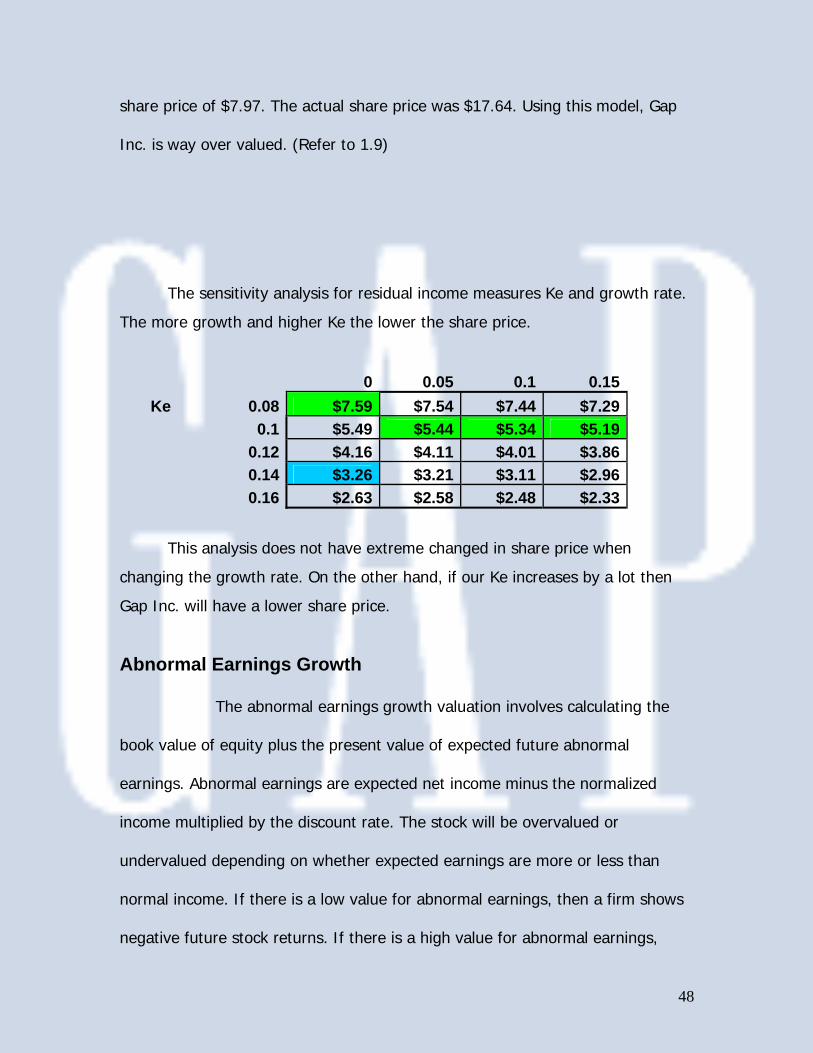

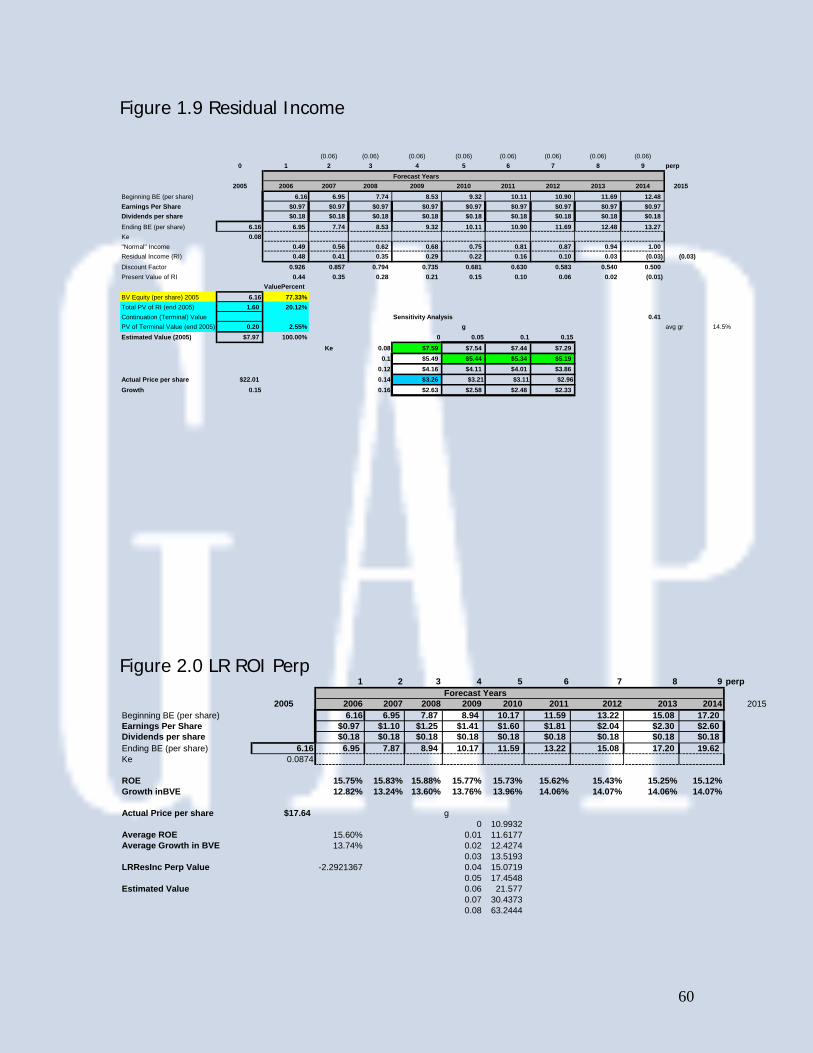

Residual Income

In this model we calculated a stream of residual incomes for the next 10

years, including a terminal value, and then discounted all the numbers back to

the present time. First we had to find the ending book value of equity which we

found by adding the book value of equity with the earning per share, then

subtracting the dividends per share. Then we needed to find the normal income,

which we did by multiplying Ke with the beginning book value of equity from the

previous years. The difference between earnings per share and normal income is

the residual income. We then discounted the residual income from forecast and

found present value of residual income. Adding the book value of equity, present

value of RI, and present value of terminal value at the end 2005 we estimated a

Ke g 0.07 0.08 0.0874 0.095 0.105 0.1150.000 2.5714 1.2857 2.05 1.894 1.714 1.5650.040 6 1.3846 4 3.27 2.769 2.40.060 18 1.5 6.569 5.14 4 3.270.080 -18 4.5 24.32 12 7.2 5.140.100 -6 -9 -14.3 -36 36 120.120 -3.6 -4.5 -5.52 -7.2 -12 -360.130 -3 -3.6 -4.225 -5.14 -7.2 -12

48

share price of $7.97. The actual share price was $17.64. Using this model, Gap

Inc. is way over valued. (Refer to 1.9)

The sensitivity analysis for residual income measures Ke and growth rate.

The more growth and higher Ke the lower the share price.

0 0.05 0.1 0.15 Ke 0.08 $7.59 $7.54 $7.44 $7.29

0.1 $5.49 $5.44 $5.34 $5.19 0.12 $4.16 $4.11 $4.01 $3.86 0.14 $3.26 $3.21 $3.11 $2.96 0.16 $2.63 $2.58 $2.48 $2.33

This analysis does not have extreme changed in share price when

changing the growth rate. On the other hand, if our Ke increases by a lot then

Gap Inc. will have a lower share price.

Abnormal Earnings Growth

The abnormal earnings growth valuation involves calculating the

book value of equity plus the present value of expected future abnormal

earnings. Abnormal earnings are expected net income minus the normalized

income multiplied by the discount rate. The stock will be overvalued or

undervalued depending on whether expected earnings are more or less than

normal income. If there is a low value for abnormal earnings, then a firm shows

negative future stock returns. If there is a high value for abnormal earnings,

49

then the complete opposite, positive future stock returns, occurs. In our case,

GAP Inc. has a low value for AEG; therefore we can predict that there will be

negative future stock returns. ( Refer to 2.1)

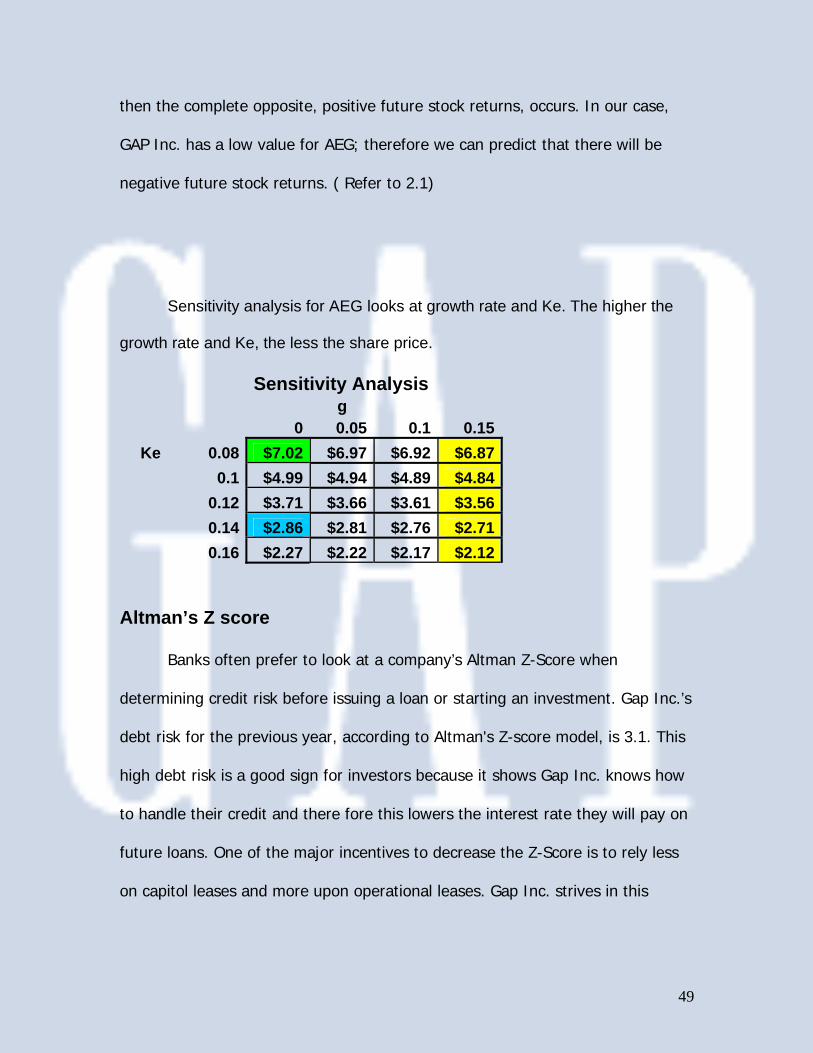

Sensitivity analysis for AEG looks at growth rate and Ke. The higher the

growth rate and Ke, the less the share price.

Sensitivity Analysis g 0 0.05 0.1 0.15

Ke 0.08 $7.02 $6.97 $6.92 $6.87 0.1 $4.99 $4.94 $4.89 $4.84 0.12 $3.71 $3.66 $3.61 $3.56 0.14 $2.86 $2.81 $2.76 $2.71 0.16 $2.27 $2.22 $2.17 $2.12

Altman’s Z score

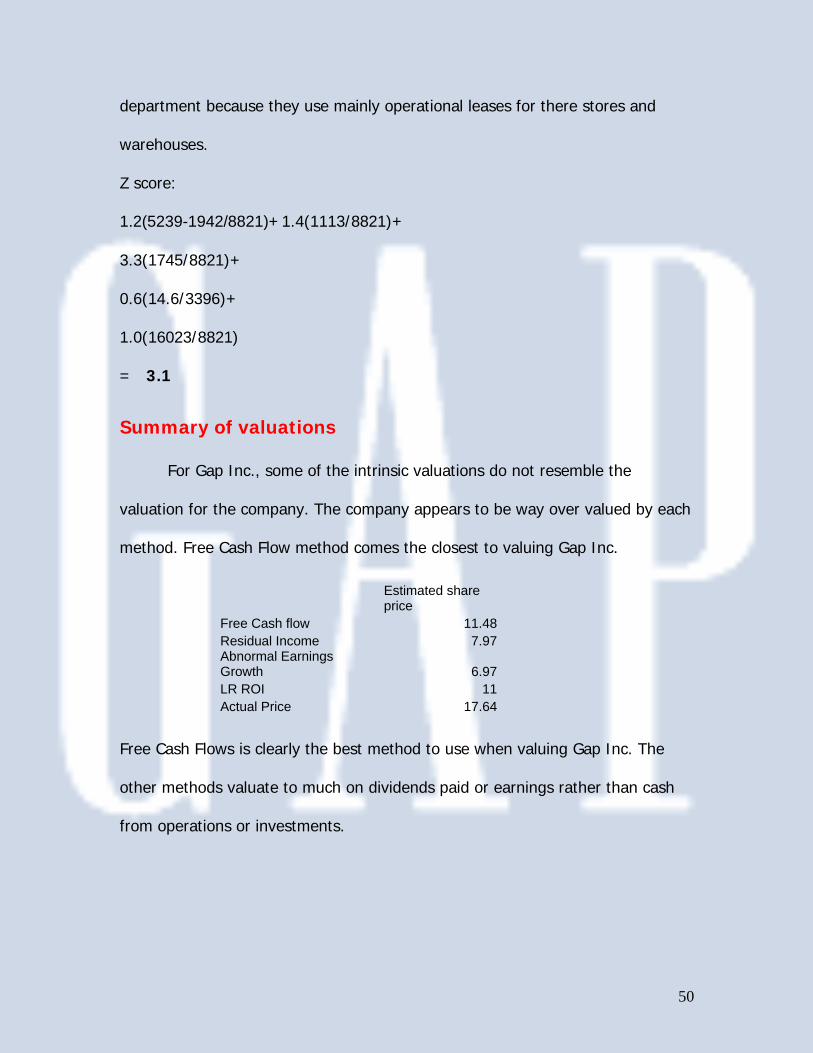

Banks often prefer to look at a company’s Altman Z-Score when

determining credit risk before issuing a loan or starting an investment. Gap Inc.’s

debt risk for the previous year, according to Altman's Z-score model, is 3.1. This

high debt risk is a good sign for investors because it shows Gap Inc. knows how

to handle their credit and there fore this lowers the interest rate they will pay on

future loans. One of the major incentives to decrease the Z-Score is to rely less

on capitol leases and more upon operational leases. Gap Inc. strives in this

50

department because they use mainly operational leases for there stores and

warehouses.

Z score:

1.2(5239-1942/8821)+ 1.4(1113/8821)+ 3.3(1745/8821)+ 0.6(14.6/3396)+ 1.0(16023/8821) = 3.1

Summary of valuations

For Gap Inc., some of the intrinsic valuations do not resemble the

valuation for the company. The company appears to be way over valued by each

method. Free Cash Flow method comes the closest to valuing Gap Inc.

Free Cash Flows is clearly the best method to use when valuing Gap Inc. The

other methods valuate to much on dividends paid or earnings rather than cash

from operations or investments.

Estimated share price

Free Cash flow 11.48Residual Income 7.97Abnormal Earnings Growth 6.97LR ROI 11Actual Price 17.64

51

References 1. www.finance .yahoo.com 2. www.morngstar.com 3. www.edgarscan.pwcglobal.com 4. www.gapinc.com/public/Investors/investors.shtml

52

Appendix 1.1 Ratio Forecast 1.2 Balance Sheet 1.3 Proforma Balance Sheet 1.4 Income Statement 1.5 Proforma Income Statement 1.6 Cash Flows 1.7 Discounted Dividends 1.8 Free Cash Flows 1.9 Residual Income 2.0 LR ROI 2.1 AEG 2.2 Weighted Avg. cost of equity 2.3 Weighted Avg. cost of debt

53

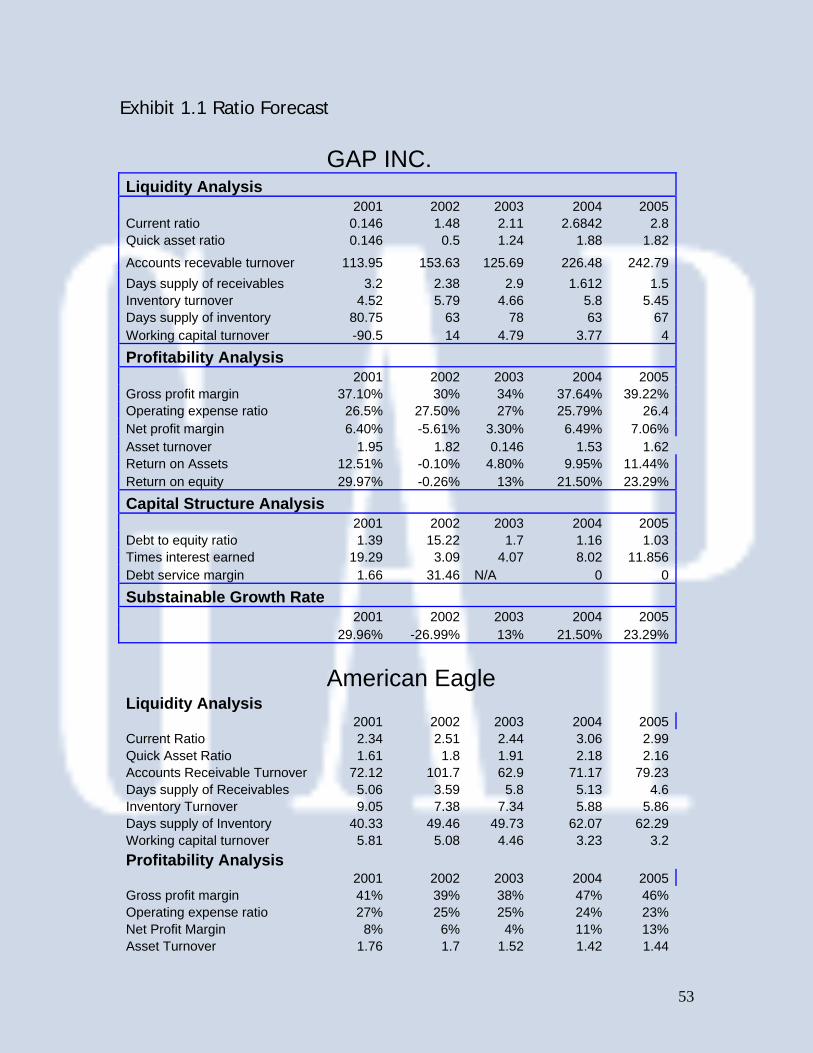

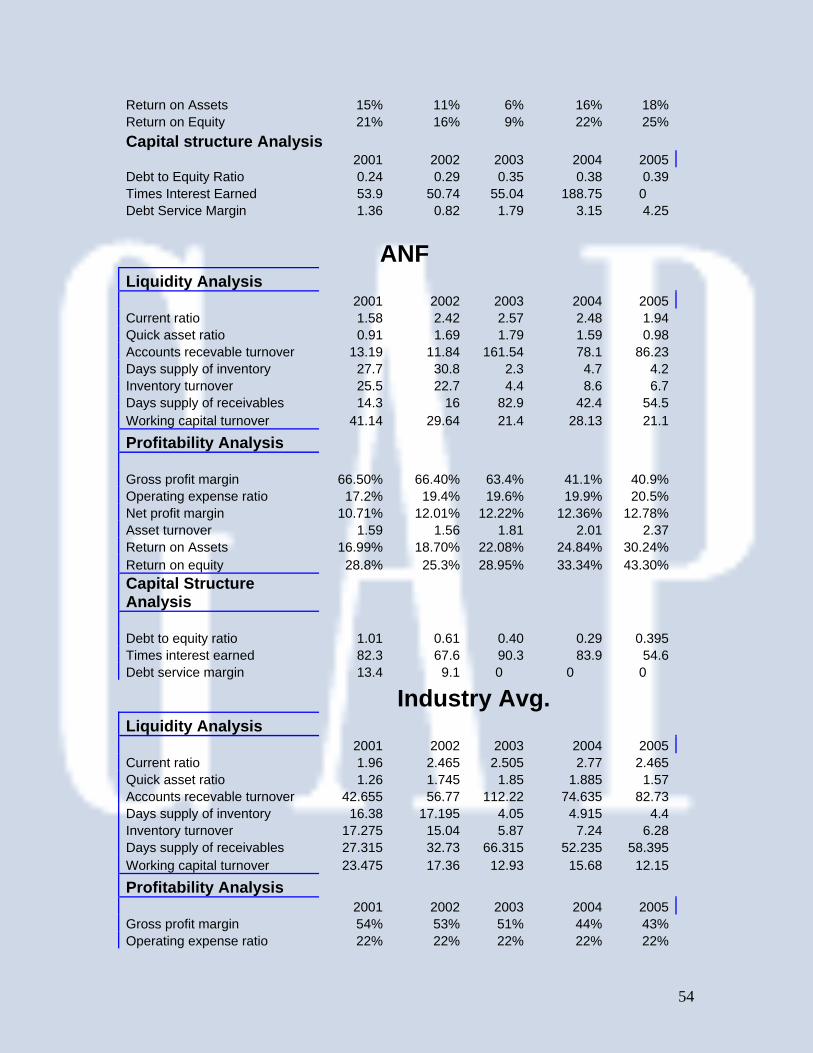

Exhibit 1.1 Ratio Forecast

GAP INC.

Liquidity Analysis 2001 2002 2003 2004 2005Current ratio 0.146 1.48 2.11 2.6842 2.8Quick asset ratio 0.146 0.5 1.24 1.88 1.82

Accounts recevable turnover 113.95 153.63 125.69 226.48 242.79Days supply of receivables 3.2 2.38 2.9 1.612 1.5Inventory turnover 4.52 5.79 4.66 5.8 5.45Days supply of inventory 80.75 63 78 63 67Working capital turnover -90.5 14 4.79 3.77 4

Profitability Analysis 2001 2002 2003 2004 2005Gross profit margin 37.10% 30% 34% 37.64% 39.22%Operating expense ratio 26.5% 27.50% 27% 25.79% 26.4Net profit margin 6.40% -5.61% 3.30% 6.49% 7.06%Asset turnover 1.95 1.82 0.146 1.53 1.62Return on Assets 12.51% -0.10% 4.80% 9.95% 11.44%Return on equity 29.97% -0.26% 13% 21.50% 23.29%

Capital Structure Analysis 2001 2002 2003 2004 2005Debt to equity ratio 1.39 15.22 1.7 1.16 1.03Times interest earned 19.29 3.09 4.07 8.02 11.856Debt service margin 1.66 31.46 N/A 0 0

Substainable Growth Rate 2001 2002 2003 2004 2005 29.96% -26.99% 13% 21.50% 23.29%

American Eagle Liquidity Analysis 2001 2002 2003 2004 2005Current Ratio 2.34 2.51 2.44 3.06 2.99Quick Asset Ratio 1.61 1.8 1.91 2.18 2.16Accounts Receivable Turnover 72.12 101.7 62.9 71.17 79.23Days supply of Receivables 5.06 3.59 5.8 5.13 4.6Inventory Turnover 9.05 7.38 7.34 5.88 5.86Days supply of Inventory 40.33 49.46 49.73 62.07 62.29Working capital turnover 5.81 5.08 4.46 3.23 3.2Profitability Analysis 2001 2002 2003 2004 2005Gross profit margin 41% 39% 38% 47% 46%Operating expense ratio 27% 25% 25% 24% 23%Net Profit Margin 8% 6% 4% 11% 13%Asset Turnover 1.76 1.7 1.52 1.42 1.44

54

Return on Assets 15% 11% 6% 16% 18%Return on Equity 21% 16% 9% 22% 25%Capital structure Analysis 2001 2002 2003 2004 2005Debt to Equity Ratio 0.24 0.29 0.35 0.38 0.39Times Interest Earned 53.9 50.74 55.04 188.75 0 Debt Service Margin 1.36 0.82 1.79 3.15 4.25

ANF

Liquidity Analysis 2001 2002 2003 2004 2005Current ratio 1.58 2.42 2.57 2.48 1.94Quick asset ratio 0.91 1.69 1.79 1.59 0.98Accounts recevable turnover 13.19 11.84 161.54 78.1 86.23Days supply of inventory 27.7 30.8 2.3 4.7 4.2Inventory turnover 25.5 22.7 4.4 8.6 6.7Days supply of receivables 14.3 16 82.9 42.4 54.5Working capital turnover 41.14 29.64 21.4 28.13 21.1

Profitability Analysis Gross profit margin 66.50% 66.40% 63.4% 41.1% 40.9%Operating expense ratio 17.2% 19.4% 19.6% 19.9% 20.5%Net profit margin 10.71% 12.01% 12.22% 12.36% 12.78%Asset turnover 1.59 1.56 1.81 2.01 2.37Return on Assets 16.99% 18.70% 22.08% 24.84% 30.24%Return on equity 28.8% 25.3% 28.95% 33.34% 43.30%Capital Structure Analysis Debt to equity ratio 1.01 0.61 0.40 0.29 0.395Times interest earned 82.3 67.6 90.3 83.9 54.6Debt service margin 13.4 9.1 0 0 0

Industry Avg.

Liquidity Analysis 2001 2002 2003 2004 2005Current ratio 1.96 2.465 2.505 2.77 2.465Quick asset ratio 1.26 1.745 1.85 1.885 1.57Accounts recevable turnover 42.655 56.77 112.22 74.635 82.73Days supply of inventory 16.38 17.195 4.05 4.915 4.4Inventory turnover 17.275 15.04 5.87 7.24 6.28Days supply of receivables 27.315 32.73 66.315 52.235 58.395Working capital turnover 23.475 17.36 12.93 15.68 12.15

Profitability Analysis 2001 2002 2003 2004 2005Gross profit margin 54% 53% 51% 44% 43%Operating expense ratio 22% 22% 22% 22% 22%

55

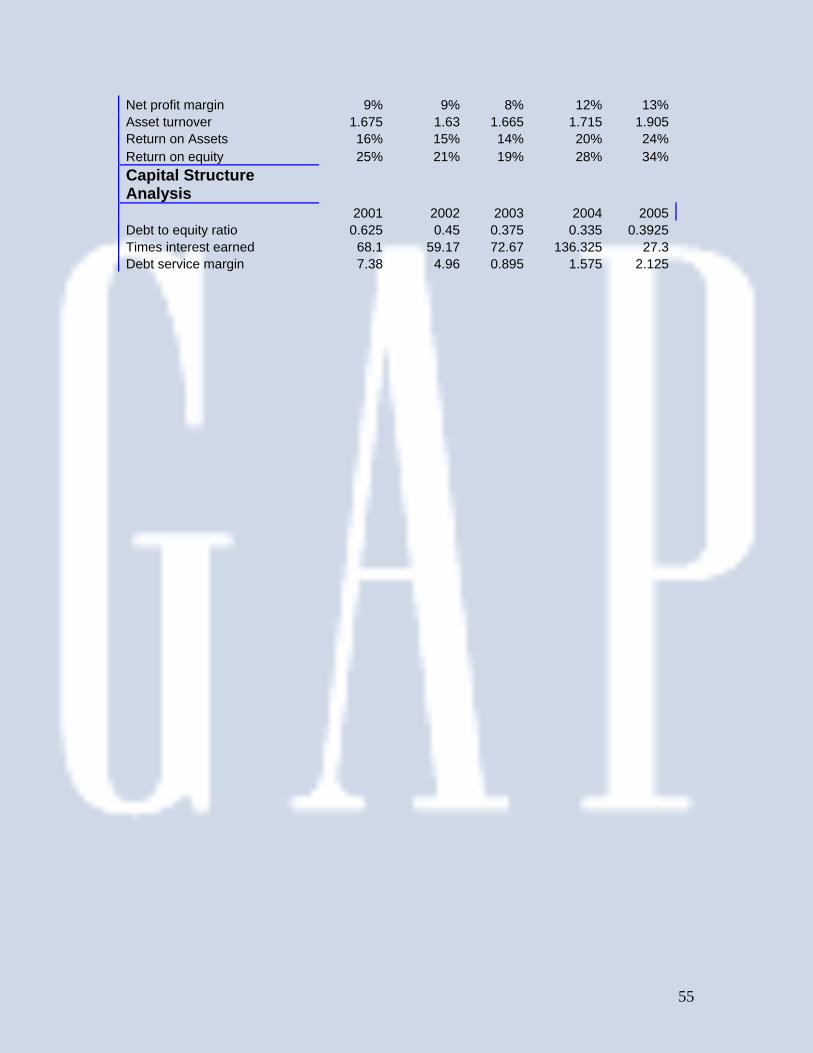

Net profit margin 9% 9% 8% 12% 13%Asset turnover 1.675 1.63 1.665 1.715 1.905Return on Assets 16% 15% 14% 20% 24%Return on equity 25% 21% 19% 28% 34%Capital Structure Analysis 2001 2002 2003 2004 2005Debt to equity ratio 0.625 0.45 0.375 0.335 0.3925Times interest earned 68.1 59.17 72.67 136.325 27.3Debt service margin 7.38 4.96 0.895 1.575 2.125

56

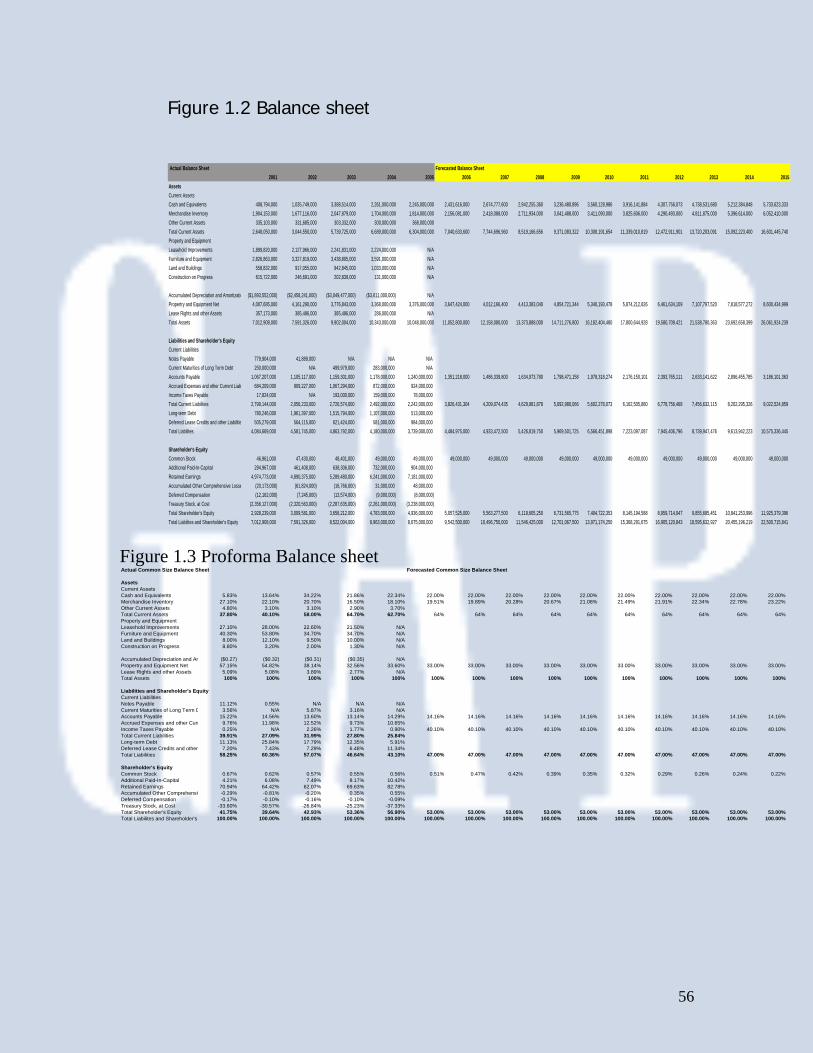

Figure 1.2 Balance sheet Actual Balance Sheet Forecasted Balance Sheet

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015AssetsCurrent AssetsCash and Equivalents 408,794,000 1,035,749,000 3,388,514,000 2,261,000,000 2,245,000,000 2,431,616,000 2,674,777,600 2,942,255,360 3,236,480,896 3,560,128,986 3,916,141,884 4,307,756,073 4,738,531,680 5,212,384,848 5,733,623,333 Merchandise Inventory 1,904,153,000 1,677,116,000 2,047,879,000 1,704,000,000 1,814,000,000 2,156,081,000 2,418,088,000 2,711,934,000 3,041,488,000 3,411,090,000 3,825,606,000 4,290,493,000 4,811,875,000 5,396,614,000 6,052,410,000 Other Current Assets 335,103,000 331,685,000 303,332,000 300,000,000 368,000,000Total Current Assets 2,648,050,000 3,044,550,000 5,739,725,000 6,689,000,000 6,304,000,000 7,040,633,600 7,744,696,960 8,519,166,656 9,371,083,322 10,308,191,654 11,339,010,819 12,472,911,901 13,720,203,091 15,092,223,400 16,601,445,740 Property and EquipmentLeasehold Improvements 1,899,820,000 2,127,966,000 2,241,831,000 2,224,000,000 N/AFurniture and Equipment 2,826,863,000 3,327,819,000 3,438,805,000 3,591,000,000 N/ALand and Buildings 558,832,000 917,055,000 942,845,000 1,033,000,000 N/AConstruction on Progress 615,722,000 246,691,000 202,839,000 131,000,000 N/A

Accumulated Depreciation and Amortizatio ($1,893,552,000) ($2,458,241,000) ($3,049,477,000) ($3,611,000,000) N/APropertry and Equipment Net 4,007,685,000 4,161,290,000 3,776,843,000 3,368,000,000 3,376,000,000 3,647,424,000 4,012,166,400 4,413,383,040 4,854,721,344 5,340,193,478 5,874,212,826 6,461,634,109 7,107,797,520 7,818,577,272 8,600,434,999 Lease Rights and other Assets 357,173,000 385,486,000 385,486,000 286,000,000 N/ATotal Assets 7,012,908,000 7,591,326,000 9,902,004,000 10,343,000,000 10,048,000,000 11,052,800,000 12,158,080,000 13,373,888,000 14,711,276,800 16,182,404,480 17,800,644,928 19,580,709,421 21,538,780,363 23,692,658,399 26,061,924,239