gas: asia’s confounding challenge - the lantau group asia’s confounding challenge. ... gmr 800...

TRANSCRIPT

The Lantau Group Confidential and Proprietary

Gas: Asia’s Confounding Challenge

The Lantau Group Confidential and Proprietary

Who we are

Office/Presence

Senior Advisors

Offerings:

• Strategic, commercial, and regulatory support

• Ability to connect the dots between fuel markets and power

• Analysis-based recommendations

• Highly relevant international experience

• Accessible experts focussed on the region

1

Economic and commercial consultants with expertise in regulatory economics, market development,

commercial transaction support, and strategy

TLG is the result of a

management buy-out of the

Asia Pacific energy practice of,

a US-based global

consultancy.

TLG is an independent

company with experts and

affiliates throughout the Asia

Pacific region.

Decisions Support Analysis

Asset Valuation

Strategy and Advanced Analytics

Competition, Markets, Regulation, Policy

Disputes

Market Analysis

Focussed on Energy

The Lantau Group Confidential and Proprietary

In the 1970s, oil prices shot up, creating a “coal window”

2

Oil

Coal

Up to that point, many Asian countries were using oil for power generation

The Lantau Group Confidential and Proprietary

Almost all of Asia shifted away from oil

3

It was a simple world from something expensive towards something cheaper

Almost everyone

moved away from oil

If you had no other choices, you

moved quickly towards coal

0

20

40

60

80

100

1978 1980 1982 1984 1986 1988

Hong Kong Malaysia

Thailand Philippines

Indonesia

Percent

0

20

40

60

80

100

1978 1980 1982 1984 1986 1988

Hong Kong Malaysia

Thailand Philippines

Indonesia

Percent

Hong Kong

Source: World Bank

The Lantau Group Confidential and Proprietary

The opening and closing of the coal window was followed by a period of growth

in use of natural gas

4

1991 Discovery of

Malampaya gas

field

1997 NPC/FirstGen sign GSPAs

with SPEX/OXY

2001 Commission of

Malampaya

2006 Singapore

commits to

LNG imports

1995 Hong Kong

first gas unit

commissioned

Decisions are easy when the same choice gives you: “green”, “cheaper”, and “local”

1993 Malaysia;s first

gas unit

commissioned

Thailand gas &

oil

development

Malaysia

gas and oil

development

Coal

Window #1

1992 Singapore’s

first gas unit

commissioned

The Lantau Group Confidential and Proprietary 5

Up to then….life was pretty straightforward….

Core generation

technologies

Keep up with

growth

Few

complicating

issues

Respond to

fuel

availability

and cost

The Lantau Group Confidential and Proprietary

Around 2005, a second Asian coal window opened…

6

0

5

10

15

20

25

30

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006 2010 2014 2018

Fu

el

Pri

ce

(U

SD

/mm

btu

)

And so here we are….much of that gas is linked to the price of oil

Notes: Coal: 1970 to 2022: Australian Newcastle FOB coal. Historic from World Bank, futures from ICE.

Oil: 1970 to 1997: Dubai crude adjusted to approximate Brent. 1997 to 2022: Brent. Historic from World Bank, futures from ICE.

Coal window #1 Coal window #2

The Lantau Group Confidential and Proprietary

Oil-linked natural gas prices in Asia have fallen

7

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Mar-

09

May-0

9

Jul-0

9

Sep-0

9

Nov-0

9

Jan-1

0

Mar-

10

May-1

0

Jul-1

0

Sep-1

0

Nov-1

0

Jan-1

1

Mar-

11

May-1

1

Jul-1

1

Sep-1

1

Nov-1

1

Jan-1

2

Mar-

12

May-1

2

Jul-1

2

Sep-1

2

Nov-1

2

Jan-1

3

Mar-

13

May-1

3

Jul-1

3

Sep-1

3

Nov-1

3

Jan-1

4

Mar-

14

May-1

4

Jul-1

4

Sep-1

4

Nov-1

4

Jan-1

5

US

D/m

mb

tu

Proxy long term Asian LNG price (slope at 0.135 with constant 0.8/mmbtu)

The Lantau Group Confidential and Proprietary

But so, too, have coal prices

• The Newcastle FOB coal price and

the FOB Indonesian coal reference

(HBA) price track each other

closely in terms of USD per tonne

• Also, as the calorific values are

very similar, the price per energy

unit (mmbtu) also exhibit a close

correlation

• In order to have a basis for a

forward price for Indonesian coal,

we have used forward prices for

Newcastle coal as a proxy

8

0

1

2

3

4

5

6

2009 2010 2011 2012 2013 2014 2015 (toMarch)

Co

al p

ric

e (

US

D/m

mb

tu)

FOB Newcastle

FOB Indonesian CoalReference Price

Sources: World Bank, Ministry of Energy and Mineral Resources

The Lantau Group Confidential and Proprietary

Before oil price drop in June 2014

9

To be economic -- every mmBtu of gas has to cover the cost of its spread vs coal

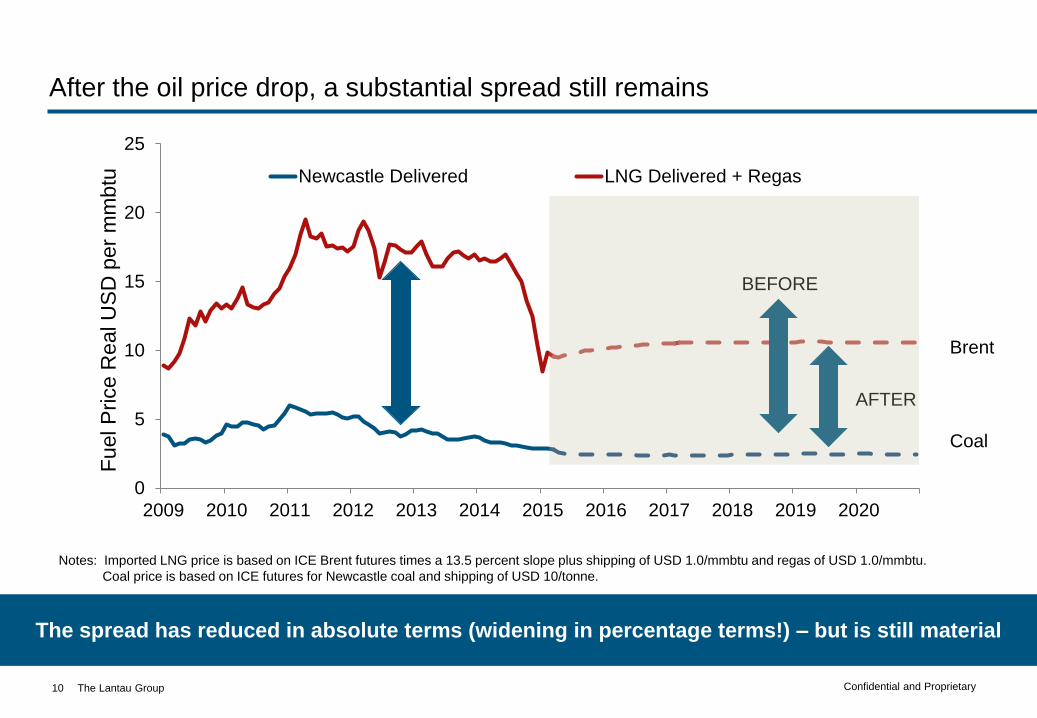

Notes: Imported LNG price is based on ICE Brent futures times a 13.5 percent slope plus shipping of USD 1.0/mmbtu and regas of USD 1.0/mmbtu.

Coal price is based on ICE futures for Newcastle coal and shipping of USD 10/tonne.

0

5

10

15

20

25

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Fu

el P

rice

Re

al U

SD

per

mm

btu

Newcastle Delivered LNG Delivered + Regas

Futures

Coal

Brent

The Lantau Group Confidential and Proprietary

After the oil price drop, a substantial spread still remains

10

The spread has reduced in absolute terms (widening in percentage terms!) – but is still material

0

5

10

15

20

25

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Fu

el P

rice

Re

al U

SD

per

mm

btu

Newcastle Delivered LNG Delivered + Regas

Notes: Imported LNG price is based on ICE Brent futures times a 13.5 percent slope plus shipping of USD 1.0/mmbtu and regas of USD 1.0/mmbtu.

Coal price is based on ICE futures for Newcastle coal and shipping of USD 10/tonne.

AFTER

BEFORE

Coal

Brent

The Lantau Group Confidential and Proprietary

Over time, the spreads remain a significant risk factor

11

Note: 2000 to present. Brent and Newcastle Coal from ICE.

LNG assumes 13.5 slope and shipping of USD 1/mmbtu and

regas of USD 1.0/mmbtu. Coal assumes shipping of USD

10/tonne.

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

0 20 40 60 80 100 120 140 160 180 200

Spread between gas and coal in Asia since 1/1/2000

Count

Current range (2015)

The Lantau Group Confidential and Proprietary

Did the Asian LNG price premium really disappear in the blink of an eye?

Forever?

12

0

5

10

15

20

25

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Gas P

rice

(U

SD

/mm

btu

)

Henry Hub

NBP

Asia LNG price

(assuming 13.5

slope and USD 0.8

constant) JKM

Source: ICE, CME, Platts, TLG analysis

The Lantau Group Confidential and Proprietary

Not yet clear – oil futures still point to an Asian penalty unless contracting

changes

13

0

5

10

15

20

25

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Gas P

rice

(U

SD

/mm

btu

)

Asian oil-indexed LNG prices

based on oil forward curve

Source: ICE, CME, Platts, TLG analysis

The Lantau Group Confidential and Proprietary

However, spot and short-term LNG trading clearly have increased, possibly

making regional gas prices become more correlated in the future

14

R² = 0.7461

0.0

5.0

10.0

15.0

20.0

25.0

0.0 5.0 10.0 15.0

JK

M p

ric

e (

As

ian

sp

ot

LN

G p

ric

e),

U

SD

/mm

btu

NBP price, USD/mmbtu

R² = 0.0481

0.0

5.0

10.0

15.0

20.0

25.0

0.0 2.0 4.0 6.0 8.0

JK

M p

ric

e (

As

ian

sp

ot

LN

G p

ric

e),

U

SD

/mm

btu

Henry hub, USD/mmbtu

Asian spot LNG prices correlated to UK gas prices but not the US gas price

Economic law of one price in action

Two markets – unable to converge due to

insufficient interconnection infrastructure

The Lantau Group Confidential and Proprietary

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

Time of day

MW

A typical generation day has a variety of requirements that typically support

generation technologies with different cost and performance characteristics

15

We divide demand into

three categories

• Baseload: always on

at full output

• Intermediate: often

on, generally for

extended periods of

time, though usually at

varying output levels

• Peaking: needed

sometimes, for varying

amounts. Often must

start and stop on short

notice`

Baseload or “always on”

Swing or Intermediate

Peaking

Source: PEMC

A typical daily load profile [electricity demand in Luzon on an illustrative day

(Friday, 10th January 2014)]

Evening peak Day peak

The Lantau Group Confidential and Proprietary

A stylised Asian example

16

Terminal

• Coal plants are very expensive to build but

relatively cheap to run.

Coal is a good baseload option for

Philippines even if LNG is imported.

• Gas plants are relatively lower cost to build

(even taking into account an LNG terminal

needed too) but expensive to run (in Asia)

Gas fits well into a mid-merit role. It

also provides flexibility for changes

in demand due to outages of other

fuels; hydro fluctuations; changes in

demand etc.

• Diesel and OCGT plants are lower cost to

build but expensive to run.

Displacing diesel for baseload and

peaking is value-adding; assuming

that “no diesel is good for the

system” is not.

The right mix is a blend of baseload, mid-merit and peaking plants to give overall least

system cost

Fixed costs - $/kW per year Variable costs - $/MWh

0

20

40

60

80

100

120

140

160

180

Oil Gas Coal

Fuel

Variable O&M

0

50

100

150

200

250

300

Oil Gas Coal

Capital

Fixed O&M

The Lantau Group Confidential and Proprietary

The value of flexibility and the role of gas:

examples

17

The Lantau Group Confidential and Proprietary

Gas demand, particularly for power, depends on price and availability of

alternatives

• Peninsular Malaysia sells gas to the

power sector at a price that is

approximately equal to coal in terms of

RM/GJ

• The market-price of gas, (whether

measured as the replacement cost, the

regional LNG price or the price paid by

the non-power sector or Singapore) is

much higher

• As Peninsular Malaysia moves to market-

priced gas, the ratio of gas price to coal

price will increase, changing the

economics of gas-fired power generation

from baseload to peaking duty

• Coal becomes the least-cost source of

baseload power supply

Reliance on gas-fired capacity for baseload power is expensive relative to coal

18

The Lantau Group

0

1

2

3

4

5

6

0% 20% 40% 60% 80% 100%

Market

Prices

Optimum Gas-Unit Capacity Factor

Regulated

Prices

“Today’s

Market Prices”

Gas/Coal Price Ratio

MALAYSIA EXAMPLE

GAS IS PREFERRED

COAL IS PREFERRED

The Lantau Group Confidential and Proprietary

As Singapore outgrew its available gas supplies, it sought to build an LNG

terminal to enhance energy security

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

PNG supply

disruption

and partial

blackout

EMA launches

LNG terminal

feasibility study

Singapore

commits to

import LNG

EMA limits

PNG imports

Gas Act

amended

EMA appoints

PowerGas as

LNG terminal

developer

BG selected as

LNG Aggregator

Gas

market

formed

EMA takes

over LNG

terminal

EMA announces

LNG Vesting

Gencos

commit

to LNG

contracts

Terminal

breaks

ground

Terminal

begins

operation

CCGTs with new LNG

contracts come online

Keppel

840 MW

Senoko

860 MW

Tuas

406 MW

GMR

800 MW

Sembcorp

400 MW

Meanwhile…the gas vs coal price spread tripled….

The terminal provided security: but over-contracting for gas resulted in higher cost

19

Gas Price

Coal Price

SINGAPORE EXAMPLE

The Lantau Group Confidential and Proprietary

In this section, we consider an example based on Indonesia

• My intent is to identify the least-cost mix of Indonesian resources, based on fuel price

expectations as of June 2014

• In order to simplify presentation, I will focus on a “first-year” analysis of units coming

on line in 2018

• A key issue involves the determination of gas value, since there are three distinctly

different sources of gas in Indonesia:

– Piped gas. This gas is priced via existing contracts, whereby prices escalate with inflation

and defined indices

– Imported LNG. Prices for imported and exported LNG are largely tied to crude prices

(particularly Brent)

– Domestic market obligation (DMO) LNG. By law, gas producers seeking to export LNG

must set aside at least 25 percent of production for the domestic market, at prices that

represent roughly a 15 percent discount to imported LNG

• While the marginal source of gas for PLN is probably the DMO LNG, I argue that

imported LNG sets the opportunity cost of gas for Indonesia.

20

INDONESIA EXAMPLE

The Lantau Group Confidential and Proprietary

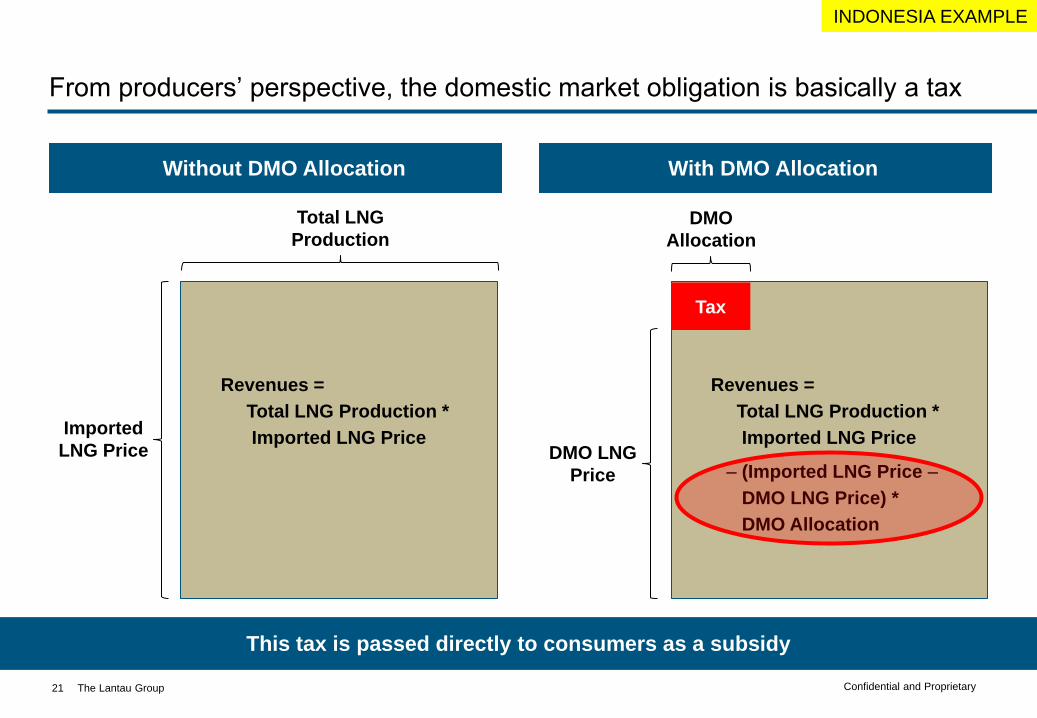

From producers’ perspective, the domestic market obligation is basically a tax

21

Without DMO Allocation With DMO Allocation

Imported

LNG Price

Total LNG

Production

Revenues =

Total LNG Production *

Imported LNG Price DMO LNG

Price

DMO

Allocation

Revenues =

Total LNG Production *

Imported LNG Price

Tax

– (Imported LNG Price –

DMO LNG Price) *

DMO Allocation

This tax is passed directly to consumers as a subsidy

INDONESIA EXAMPLE

The Lantau Group Confidential and Proprietary

Screening curve analysis is based on fixed and variable cost components for

each technology (using real dollars)

22

Plant Type Gas CCGT Greenfield Coal Geothermal

Capital Cost

Generic Cost (USD/kW) 900 1,600 3,475

Construction Time (years) 2.5 3.5 7.0

Total Cost (USD/kW) 976 1,832 5,754

Economic Life (years) 25 30 30

Station-Own Consumption (percent) 1.5 4.0 4.0

Annualized Capital Cost (USD/kW-year) 118 .220 999

Fixed Cost

Fixed O&M (USD/kW-year) 13 25 160

Fuel Costs

Gross Fuel Cost (HHV) (USD/mmbtu) 13.40 3.55

Heat Rate (mmbtu/MWh) 7.0 9.0 0.0

Variable Costs

Variable O&M (USD/MWh) 2 4 1

INDONESIA EXAMPLE

The Lantau Group Confidential and Proprietary

Given the fixed and variable cost components, the total cost of generation is

proportional to capacity factor

• Our analysis assumes a 2018 start date

for new plant

• We used the forward curve for Newcastle

coal plus delivery to approximate the

Indonesian Reference Coal Price, yielding

a real price of 3.55 USD/mmbtu in 2018

• We assumed that the imported LNG price

equals the Brent forward price times a

slope of 12.5 percent, plus shipping of

1.00 USD/mmbtu and regas cost of 0.70

USD/mmbtu, yielding a real gas price of

13.40 USD/mmbtu

23

Source: TLG analysis

0

200

400

600

800

1,000

1,200

1,400

0 10 20 30 40 50 60 70 80 90 100

To

tal C

ost

(US

D/k

W-y

ear)

Capacity Factor (percent)

Geothermal

CCGT

Coal

INDONESIA EXAMPLE

The Lantau Group Confidential and Proprietary

We can also express the results directly in terms of USD/MWh energy cost

• Coal-fired plant is clearly the

least expensive base load

option

• CCGTs are the least

expensive option for capacity

factors below 21-22 percent

• At our assumed costs

(consistent with breakeven

operation at the lower end of

the geothermal FiT),

geothermal is simply not

economic

24

Source: TLG analysis

Coal

0

40

80

120

160

200

240

280

320

0 10 20 30 40 50 60 70 80 90 100

Co

st

(US

D/M

Wh

)

Capacity Factor (percent)

Geothermal

CCGT

CCGT Coal

INDONESIA EXAMPLE

The Lantau Group Confidential and Proprietary

Even with CO2 priced at 50 USD/tonne, the optimal mix does not shift – but the

breakeven CCGT capacity factors rise to about 40 percent

25

Source: TLG analysis

0

40

80

120

160

200

240

280

320

0 10 20 30 40 50 60 70 80 90 100

Co

st

(US

D/M

Wh

)

Capacity Factor (percent)

Breakeven

Capacity Factor

Geothermal

CCGT

Coal

0

200

400

600

800

1,000

1,200

1,400

0 10 20 30 40 50 60 70 80 90 100

To

tal

Co

st

(US

D/k

W-y

ea

r)

Capacity Factor (percent)

Breakeven

Capacity Factor

Geothermal

CCGT

Coal

INDONESIA EXAMPLE

The Lantau Group Confidential and Proprietary

There was a time when the gas to coal spread supported higher utilisation

26

0

10

20

30

40

50

60

70

80

90

0.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00

00-01

02-03

Simple Difference Between Gas and Coal Prices ($/mmBtu)

Gas Plant Capacity Factor (Optimal)

The Lantau Group Confidential and Proprietary

Some years, like 2008 and 2009 – are hugely variable

27

0

10

20

30

40

50

60

70

80

90

0.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00

08-09

Simple Difference Between Gas and Coal Prices ($/mmBtu)

Gas Plant Capacity Factor (Optimal)

The Lantau Group Confidential and Proprietary

More recent experience is at the opposite end

28

0

10

20

30

40

50

60

70

80

90

0.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00

12-13

14-15

Simple Difference Between Gas and Coal Prices ($/mmBtu)

Gas Plant Capacity Factor (Optimal)

The Lantau Group Confidential and Proprietary

Overall picture

29

0

10

20

30

40

50

60

70

80

90

0.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00

00-01

02-03

04-05

06-07

08-09

10-11

12-13

14-15

Simple Difference Between Gas and Coal Prices ($/mmBtu)

Gas Plant Capacity Factor (Optimal)

The Lantau Group Confidential and Proprietary

Gas infrastructure is needed – but the operating regime is highly variable

• Variable operating profile

• Seasonality

• Responsiveness to outages or demand variation

• Long-period variation (El Nino vs La Nina)

30

The value of gas to the power sector in Asia is greatest (by far) when the arrangements for accessing it are highly flexible

The Lantau Group Confidential and Proprietary

It’s All About Uncertainty and Flexibility

31

The Lantau Group Confidential and Proprietary

Base Case

• Standard size FSRU running at less than ten

percent capacity factor or 30 percent at peak

times with all cost assigned to a power plant.

• Might be able to get by on only need five

deliveries a year – or more, smaller deliveries

at slightly higher cost

• An 800 MW gas fired plant could run at 30

percent capacity factor to serve mid merit

load.

32

Item Units

Terminal storage size 155,000 m3

Terminal capex USD 300 m

Max send out 500 mmscfd

Terminal charge USD 2.8/mmbtu

Shipping charge USD 0.5/mmbtu

Levelised Real LNG FOB USD 7.9/mmbtu

Regasified LNG USD 11.2/mmbtu

0

10

20

30

40

50

60

70

80

90

100

0

100

200

300

400

500

600

700

0 10 20 30 40 50 60 70 80 90 100

Lo

ad

as P

erc

en

t o

f P

eak

US

D M

Wh

Capacity Factor (Percent)

Standard FSRU Scenario

The Lantau Group Confidential and Proprietary

0

10

20

30

40

50

60

70

80

90

100

0

100

200

300

400

500

600

700

0 10 20 30 40 50 60 70 80 90 100

Lo

ad

as P

erc

en

t o

f P

eak

US

D M

Wh

Capacity Factor (Percent)

Base Case (plus $20 carbon charge)

• Standard size FSRU running at less than fifteen ten percent capacity factor or 30 percent at peak times with all cost assigned to a power plant.

• Might be able to get by on only need six deliveries a year – or more, smaller deliveries at slightly higher cost

• An 800 MW gas fired plant could run at 40 percent capacity factor to serve mid merit load.

33

Item Units

Terminal storage size 155,000 m3

Terminal capex USD 300 m

Max send out 500 mmscfd

Terminal charge USD 2.1/mmbtu

Shipping charge USD 0.4/mmbtu

Levelised Real LNG FOB USD 7.9/mmbtu

Regasified LNG USD 10.4/mmbtu

Standard FSRU Scenario

Significant rise in

capacity factor

The Lantau Group Confidential and Proprietary

Base Case with Smaller (Lower Cost) FSRU

• Reduced terminal size would lower the

terminal charge by about one USD per

mmbtu. But that would most likely mean

more partial cargos and higher shipping

costs

• An 800 MW CCGT plant could run at 32

percent capacity to serve mid merit load.

Not a lot of extra demand for LNG, but a

loss of flexibility

34

Item Units

Terminal storage size 80,000 m3

Terminal capex USD 200 m

Max send out 250 mmscfd

Terminal charge USD 1.9/mmbtu

Shipping charge USD 0.8/mmbtu

Levelised Real LNG FOB USD 7.9/mmbtu

Regasified LNG USD 10.6/mmbtu

0

10

20

30

40

50

60

70

80

90

100

0

100

200

300

400

500

600

700

0 10 20 30 40 50 60 70 80 90 100

Lo

ad

as P

erc

en

t o

f P

eak

US

D M

Wh

Capacity Factor (Percent)

Slight rise in

capacity factor

Smaller FSRU Scenario

The Lantau Group Confidential and Proprietary

Smaller FSRU means more trips for refilling higher cost & less flexibility

• As the size of the FSRU is scaled down the

greater the number of delivery trips, by

whatever size of carrier.

• If the shipping is by dedicated smaller LNG

carriers, this might increase the risk of an

interruption to deliveries. That is unless the

LNG supplier or LNG vessel charter can use

an alternative vessel temporarily.

• The number of days of inventory falls as the

FSRU gets smaller which means regular top

ups are required.

• If demand for peaking power suddenly picks

up then it is easier to call on LNG from the

spot market in more standard sized LNG

carriers.

35

0

5

10

15

20

0

50

100

150

200

1 2 3 4 5 6 7 8 9

Num

ber

of T

rips

FS

RU

Siz

e (

thousand m

3)

FSRU Size Number of Trips

0

20

40

60

80

100

0

50

100

150

200

1 2 3 4 5 6 7 8 9

Days o

f in

vento

ry

FS

RU

Siz

e (

thousand m

3)

FSRU Size Inventory

The Lantau Group Confidential and Proprietary

Being able to accommodate a wider range of (up-to) full-sized carriers cargoes

increases flexibility when sourcing short-term or spot

0

50

100

150

200

250

300

0 50 100 150 200 250 300 350

Th

ou

sa

nd

cu

bic

metr

es

36

Cumulative number of ships

Clear sweetspot of carrier size:

125,000m3 – 170,000m3

(56kt – 76kt)

Source: TLG research

Number of LNG carriers by size

The Lantau Group Confidential and Proprietary

55

14

1

28

1

0

10

20

30

40

50

60

70

80

90

100

1

Perc

ent

of to

tal le

velis

ed c

ost

Power Plant Opex

Power Plant Capex

Terminal Opex

Terminal Capex

Fuel

The terminal is the key source of flexibility – and its contribution to total cost is

comparatively small

37

• The main driver of changes in overall busbar

power cost are changes in the price of LNG.

• Size of the FSRU terminal does not have that

great an impact on costs.

• Dispatch against versus coal fired plants is

also mostly driven by the relative pricing of

LNG against coal.

The Lantau Group Confidential and Proprietary

What are the implications of mid-merit LNG-fired generation on associated

infrastructure investment

• Mid-merit LNG-fired generation will be subject to daily load variation, seasonal swings,

and long-term capacity factor uncertainty

– Cannot support high load factor for LNG terminals

– Costly to be constrained by inflexible, take-or-pay commitments

– Cannot sign bankable long-term supply contracts

• Fuel margins matter and vary widely over time

• Asian LNG terminals need to be able to recover their costs primarily via capacity

reservation charges, rather than throughput charges

– Throughput capacity will vary with circumstances

– Sizing of terminal storage capability will be the key design variable

– Break-bulk shipping and LNG trucking – both inherently more flexible – will supplant gas pipelines

• Needed: a new set of commercial and regulatory arrangements to enable decoupling of

capacity and usage….in Asia

38

The Lantau Group Confidential and Proprietary

Thank You

Contact

Mike Thomas [email protected]

By phone +852 2521 5501 (office)

By mail 4602-4606 Tower 1, Metroplaza

223 Hing Fong Road,

Kwai Fong, Hong Kong

Online www.lantaugroup.com

Rigour

Value

Insight

Energy Power Utilities

39