gasb 67 and gasb 68 implementation questions –part 2 implementation... · gasb 67 and gasb 68...

TRANSCRIPT

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP

GASB 67 and GASB 68 Implementation Questions – Part 2

October 28, 2015

The webinar will begin promptly at noon eastern.

WebEx technical support can be reached at 800.508.8758.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 6

Today’s Speakers

Christine Torres, CPAPartner

Kevin Smith, CPAPartner

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 7

Agenda

Highlights from AICPA Audit Guide

Journal Entries

AICPA Released Guidance

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 8

Polling Question

GASB 68 Implementation:

a) Makes me jump up and down with excitement.b) Liked the challenge of implementation.c) Gave me an overall headache.d) Was like being in a torture chamber.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 9

AICPA Audit Guide

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 10

Procedures – Cost Sharing Plans

Obtain the actuarial valuation report used to measure the collective total pension liability for the plan as of the measurement date based on GASB #68. Evaluate the professional qualifications of the actuary, including his or

her competence, capabilities, and objectivity. Read the actuarial certification for potential exclusions from the scope

of the actuary’s work or qualifications on the actuary’s certification relating to actuarial methods, actuarial assumptions, or census data. Determine whether the actuarial valuation was performed as of a date

no more than 30 months and 1 day of the employer’s fiscal year-end. Evaluate whether the methods and assumptions used in determining

the total pension liability are in accordance with GASB #68 and Actuarial Standards of Practice and are the same as those used by the plan.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 11

Procedures – Cost Sharing Plans

Obtain the audited schedule of employer allocations and compare and recalculate amounts specific to the employer to the employer’s records.Obtain the audited schedule of pension amounts and recalculate the

allocated pension amounts for the employer by multiplying the collective pension amounts for the plan by the employer’s proportionate share (allocation percentage). Evaluate whether the plan auditor’s report on the schedule of employer

allocations and the schedule of pension amounts is adequate and appropriate for the employer auditor’s purposes. Evaluate whether the plan auditor has the necessary competence and

objectivity for the employer auditor’s purposes.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 12

Procedures – Cost Sharing Plans

Obtain the audited plan financial statements and perform the following: Agree or reconcile net pension liability reported in the schedule of pension amounts to

the net pension liability disclosed in the notes to the plan financial statements Agree the fiduciary net position component of the net pension liability disclosed in the

notes to the plan financial statements to that reported in the plan statement of fiduciary net position

Obtain a detailed schedule of employer-specific deferred outflows of resources and deferred inflows of resources by type and by period and perform the following: Test contributions made after the measurement and before the employer’s year-end

and compare to amount reported as deferred outflows of resources Agree amortization schedules and amortization periods for prior period deferral

amounts to prior year working papers and audited financial statements Recalculate the current year gross incremental deferrals for changes in proportion and

differences between the employer’s actual contributions and its proportionate share of total employer contributions

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 13

Procedures – Cost Sharing Plans

Obtain a detailed schedule of employer-specific deferred outflows of resources and deferred inflows of resources by type and by period and perform the following: Recalculate the amortization amount for the current period incremental deferrals for

changes in proportion and differences between the employer’s actual contributions and its proportionate share of total employer contributions

Recalculate the mathematical accuracy of the total deferred outflows of resources and deferred inflows of resource by type as of the measurement date and the total amortization for the measurement period based on the components tested. Recalculate pension expense based on the employer’s specific pension

expense in the schedule of pension amounts plus the amortization amount of employer-specific deferred outflows of resources and deferred inflows of resources.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 14

Census Data Procedures – Cost Sharing Plans

Identify the payroll registers and payroll cycles for all reporting units of the governmentObtain the population of employer (payroll) transmission reports

submitted to the plan during the year and performing the following: Evaluate whether the population of employer (payroll) transmission reports received is

complete based on an understanding of the employer’s payroll registers and cycles Select a sample of employer (payroll) transmission reports to verify the mathematical

accuracy of reports and whether the correct contribution rates were used

Obtain a list of new employees hired during the year from the employer and perform the following procedures: Select a sample to determine that eligible new employees were appropriately enrolled

in the plan and properly included in the employer (payroll) transmission reports For each employee selected, verify accuracy of the significant elements of census data

reported to the plan upon enrollment to the payroll and personnel records (for example, name, Social Security number, date of birth, gender, date of hire, marital status, and position or job code)

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 15

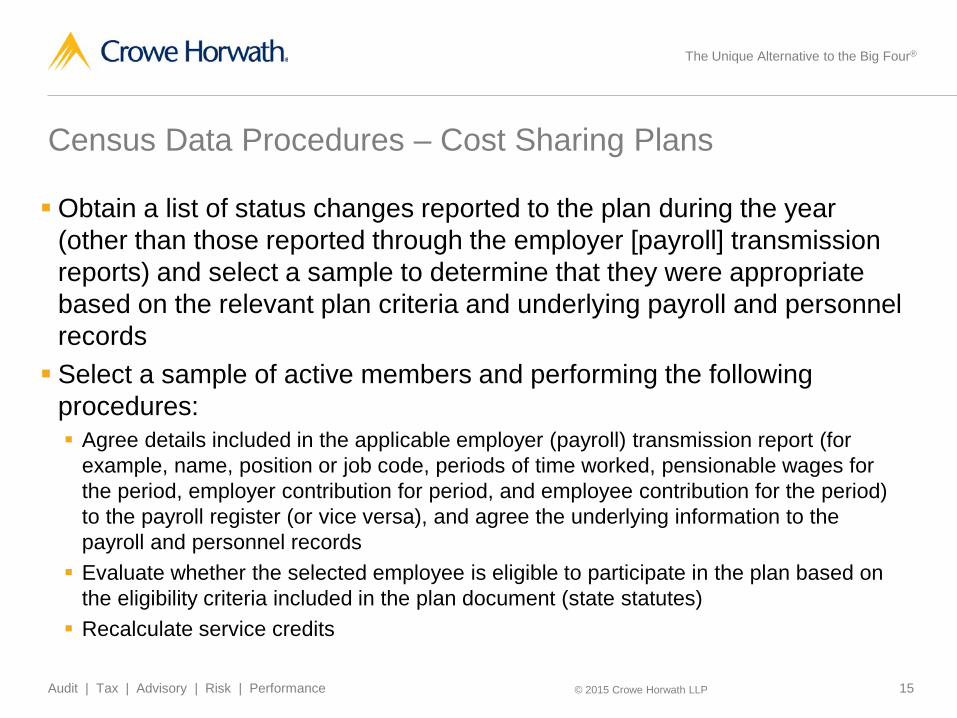

Census Data Procedures – Cost Sharing Plans

Obtain a list of status changes reported to the plan during the year (other than those reported through the employer [payroll] transmission reports) and select a sample to determine that they were appropriate based on the relevant plan criteria and underlying payroll and personnel records Select a sample of active members and performing the following

procedures: Agree details included in the applicable employer (payroll) transmission report (for

example, name, position or job code, periods of time worked, pensionable wages for the period, employer contribution for period, and employee contribution for the period) to the payroll register (or vice versa), and agree the underlying information to the payroll and personnel records Evaluate whether the selected employee is eligible to participate in the plan based on

the eligibility criteria included in the plan document (state statutes) Recalculate service credits

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 16

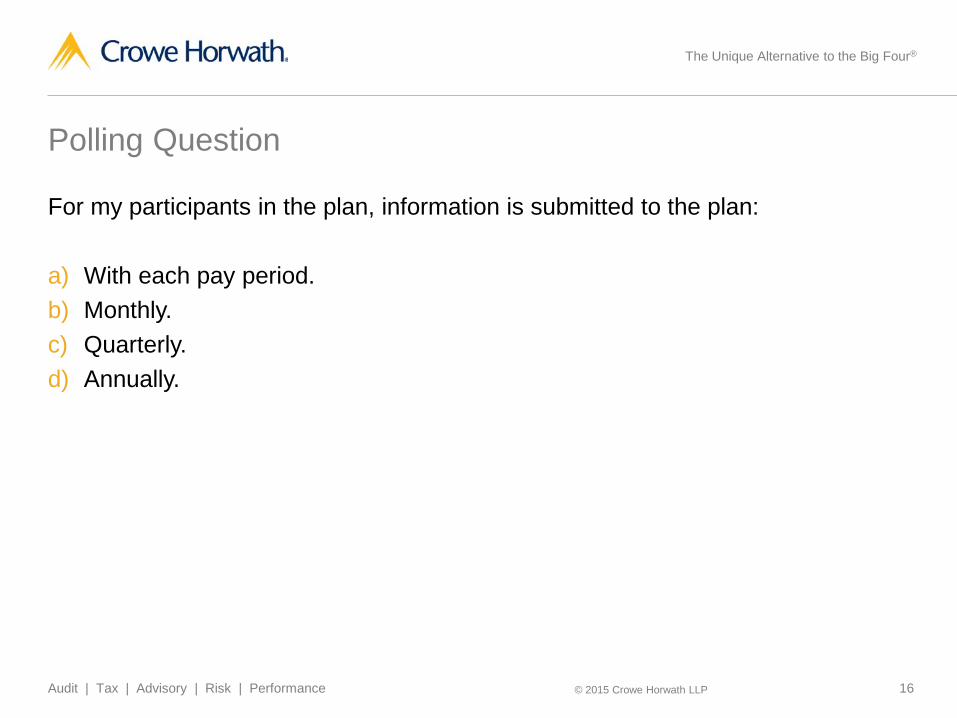

Polling Question

For my participants in the plan, information is submitted to the plan:

a) With each pay period.b) Monthly.c) Quarterly.d) Annually.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 17

Journal Entries

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 18

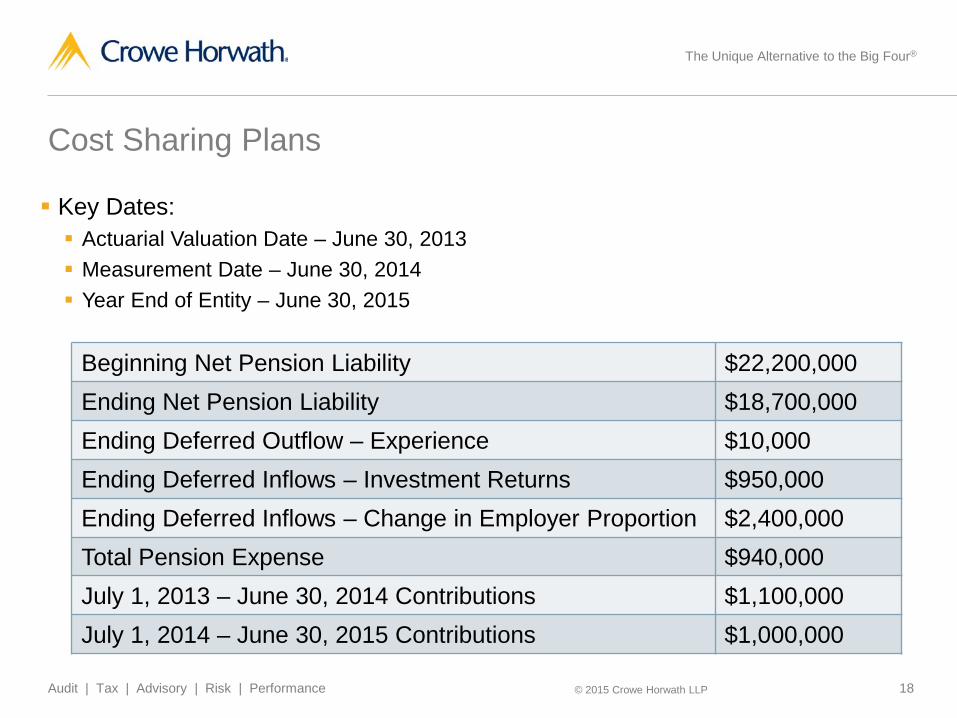

Cost Sharing Plans

Key Dates: Actuarial Valuation Date – June 30, 2013 Measurement Date – June 30, 2014 Year End of Entity – June 30, 2015

Beginning Net Pension Liability $22,200,000Ending Net Pension Liability $18,700,000Ending Deferred Outflow – Experience $10,000Ending Deferred Inflows – Investment Returns $950,000Ending Deferred Inflows – Change in Employer Proportion $2,400,000Total Pension Expense $940,000July 1, 2013 – June 30, 2014 Contributions $1,100,000July 1, 2014 – June 30, 2015 Contributions $1,000,000

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 19

Cost Sharing Plans

1. Record prior period adjustment to record beginning balances for Net Pension Liability and Deferred Outflows – Employer Contributions

Account Debit CreditNet Position $21,100,000Net Pension Liability $22,200,000Deferred Outflow – Employer Contributions

$1,100,000

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 20

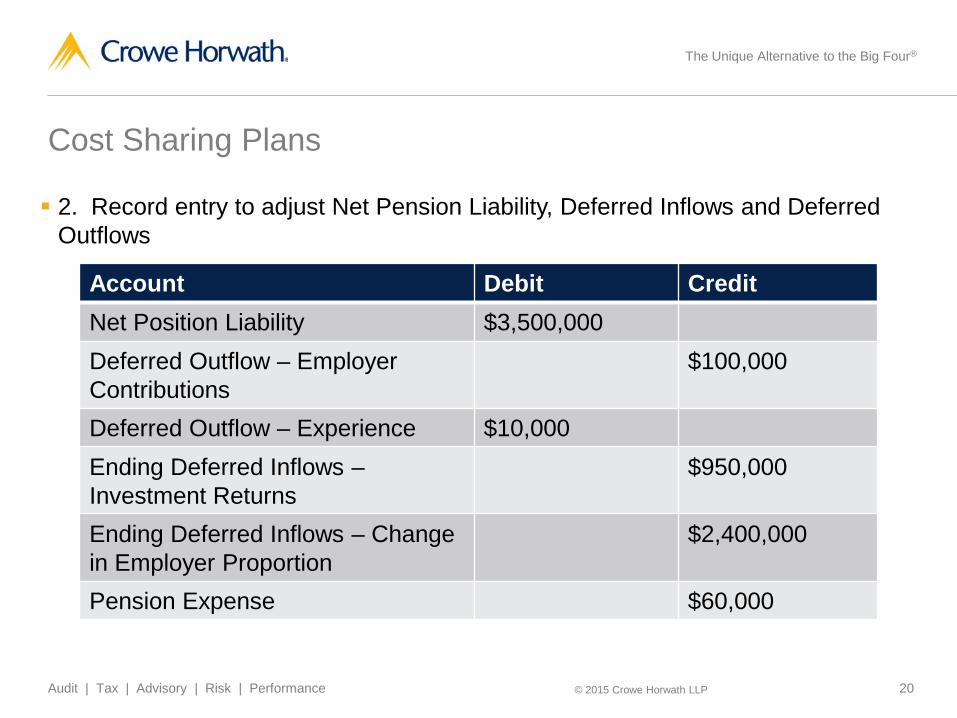

Cost Sharing Plans

2. Record entry to adjust Net Pension Liability, Deferred Inflows and Deferred Outflows

Account Debit CreditNet Position Liability $3,500,000Deferred Outflow – Employer Contributions

$100,000

Deferred Outflow – Experience $10,000Ending Deferred Inflows –Investment Returns

$950,000

Ending Deferred Inflows – Change in Employer Proportion

$2,400,000

Pension Expense $60,000

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 21

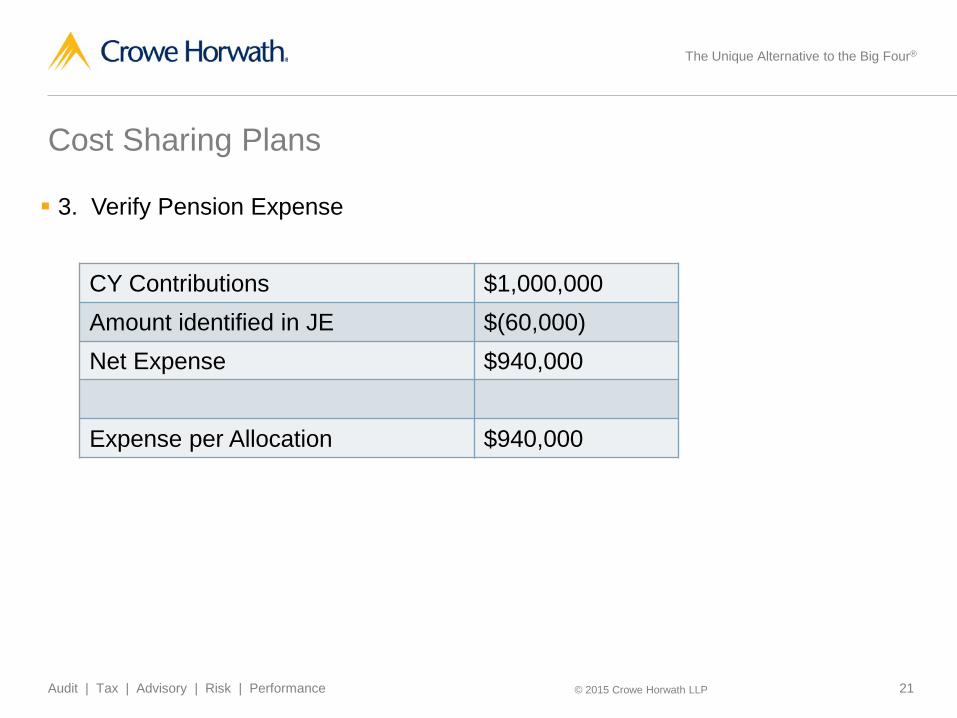

Cost Sharing Plans

3. Verify Pension Expense

CY Contributions $1,000,000Amount identified in JE $(60,000)Net Expense $940,000

Expense per Allocation $940,000

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 22

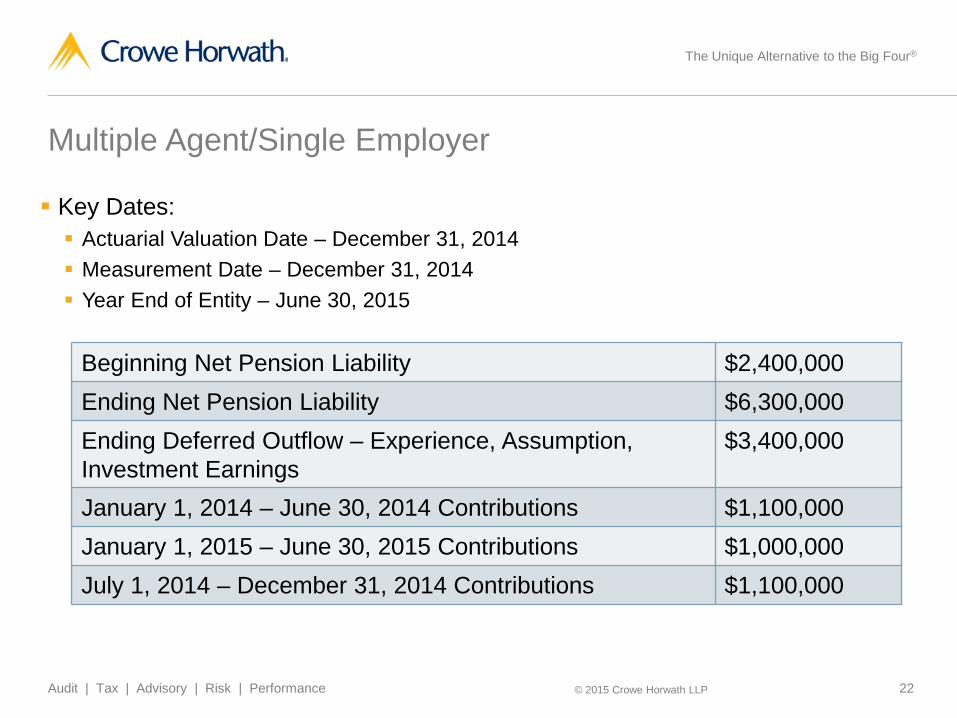

Multiple Agent/Single Employer

Key Dates: Actuarial Valuation Date – December 31, 2014 Measurement Date – December 31, 2014 Year End of Entity – June 30, 2015

Beginning Net Pension Liability $2,400,000Ending Net Pension Liability $6,300,000Ending Deferred Outflow – Experience, Assumption,Investment Earnings

$3,400,000

January 1, 2014 – June 30, 2014 Contributions $1,100,000January 1, 2015 – June 30, 2015 Contributions $1,000,000July 1, 2014 – December 31, 2014 Contributions $1,100,000

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 23

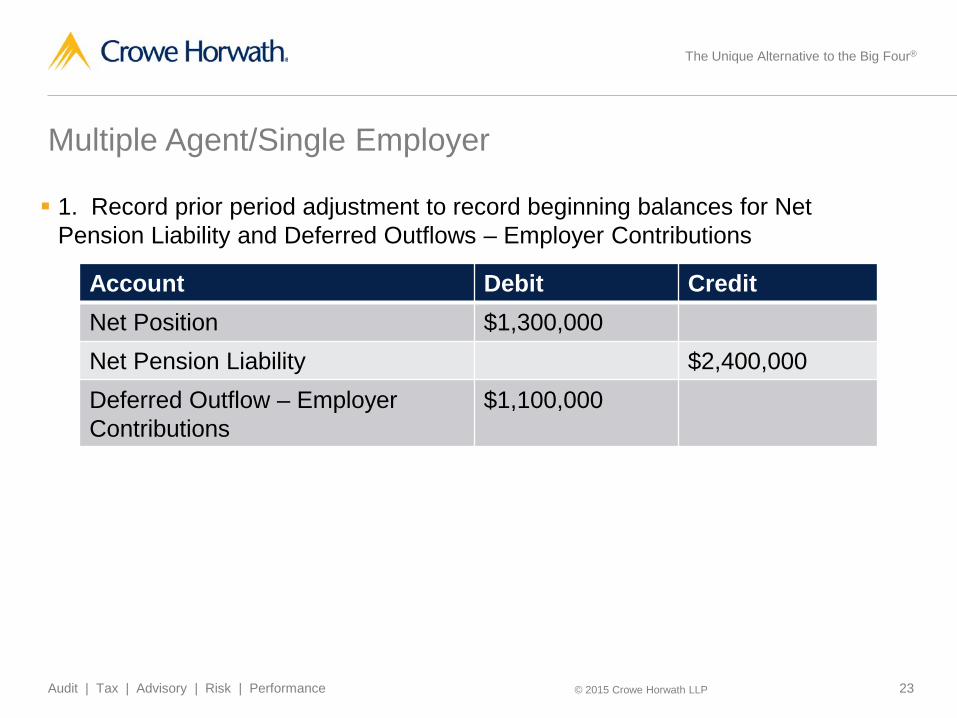

Multiple Agent/Single Employer

1. Record prior period adjustment to record beginning balances for Net Pension Liability and Deferred Outflows – Employer Contributions

Account Debit CreditNet Position $1,300,000Net Pension Liability $2,400,000Deferred Outflow – Employer Contributions

$1,100,000

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 24

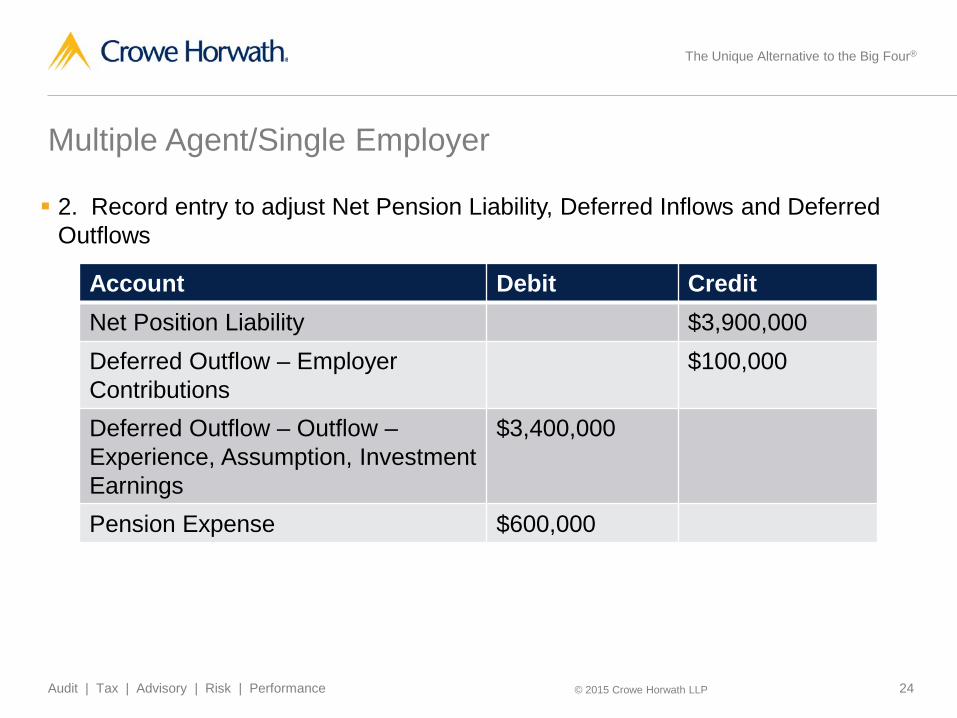

Multiple Agent/Single Employer

2. Record entry to adjust Net Pension Liability, Deferred Inflows and Deferred Outflows

Account Debit CreditNet Position Liability $3,900,000Deferred Outflow – Employer Contributions

$100,000

Deferred Outflow – Outflow –Experience, Assumption, Investment Earnings

$3,400,000

Pension Expense $600,000

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 25

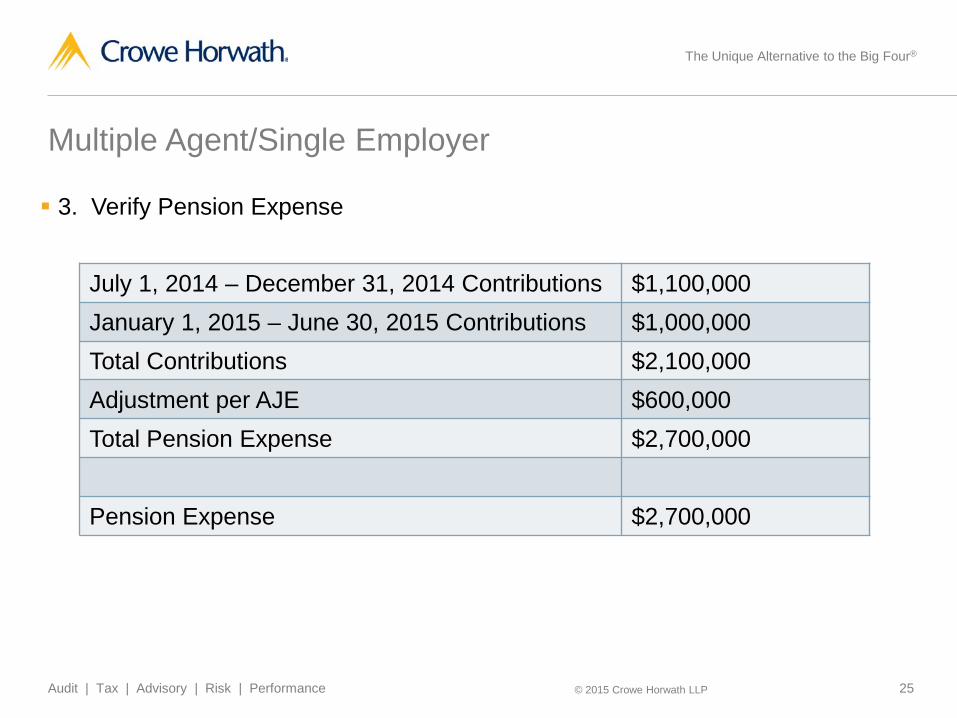

Multiple Agent/Single Employer

3. Verify Pension Expense

July 1, 2014 – December 31, 2014 Contributions $1,100,000January 1, 2015 – June 30, 2015 Contributions $1,000,000Total Contributions $2,100,000Adjustment per AJE $600,000Total Pension Expense $2,700,000

Pension Expense $2,700,000

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 26

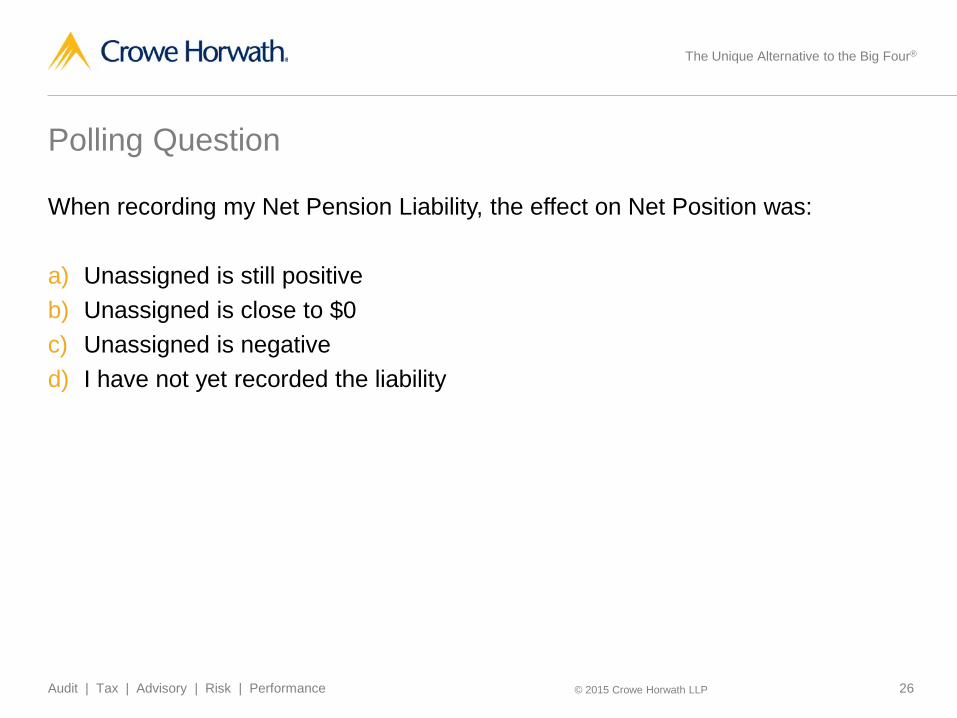

Polling Question

When recording my Net Pension Liability, the effect on Net Position was:

a) Unassigned is still positiveb) Unassigned is close to $0c) Unassigned is negatived) I have not yet recorded the liability

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 27

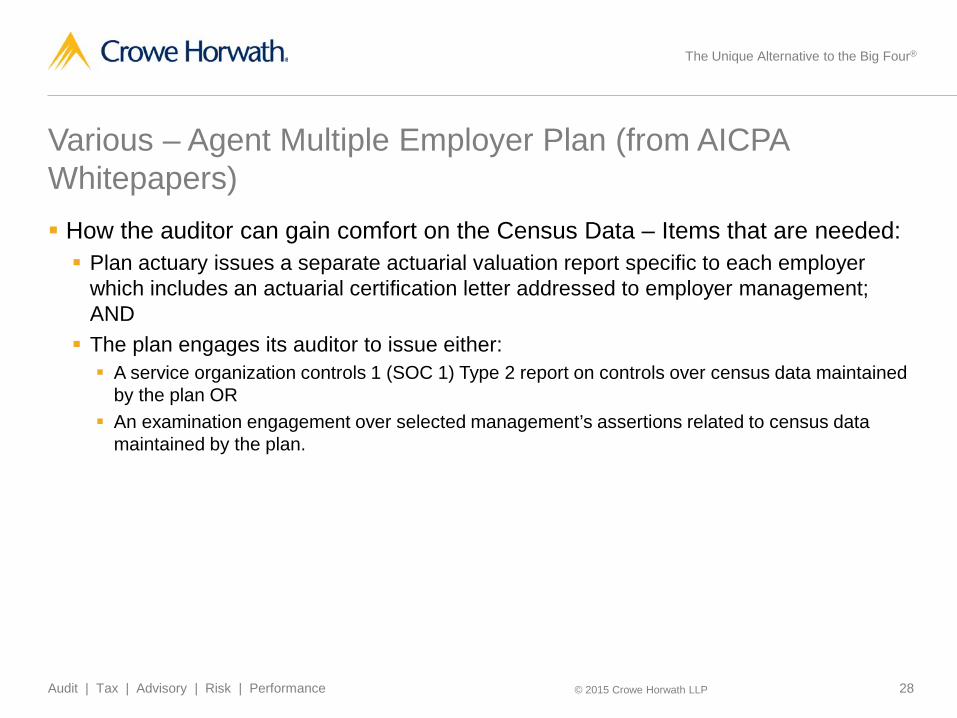

Various – Agent Multiple Employer Plan (from AICPA Whitepapers) How the auditor can gain comfort on the Census Data – Items that are needed: Plan actuary issues a separate actuarial valuation report specific to each employer

which includes an actuarial certification letter addressed to employer management; AND The plan engages its auditor to issue either: A service organization controls 1 (SOC 1) Type 2 report on controls over census data maintained

by the plan OR An examination engagement over selected management’s assertions related to census data

maintained by the plan.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 28

Various – Agent Multiple Employer Plan (from AICPA Whitepapers) How the auditor can gain comfort on the Census Data – Items that are needed: Plan actuary issues a separate actuarial valuation report specific to each employer

which includes an actuarial certification letter addressed to employer management; AND The plan engages its auditor to issue either: A service organization controls 1 (SOC 1) Type 2 report on controls over census data maintained

by the plan OR An examination engagement over selected management’s assertions related to census data

maintained by the plan.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 29

Various – Agent Multiple Employer Plan (from AICPA Whitepapers) How the auditor can gain comfort on the fiduciary net position component of the

net pension liability – Items that are needed: Plan prepares a schedule of changes in fiduciary net position by employer and related

notes to the schedule; AND The plan engages its auditor to opine on the schedule of fiduciary net position by

employer by either: An opinion on the schedule as a whole combined with SOC 1 Type 2 report on the controls over

the calculation and allocation of additions and deductions to employer accounts OR An opinion on each employer column in the schedule.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 30

Various – Agent Multiple Employer Plan (from AICPA Whitepapers) If Best Practice Solutions Not Adopted: If an agent plan issues audited financial statements, but does not implement

the best practice solutions, it is unlikely that employer auditors will be able to accumulate sufficient appropriate audit evidence necessary to provide unmodified opinions on the opinion units of the government financial reporting entity that have material pension amounts. Unaudited information provided by the plan to its employers to support

specific pension amounts that have not been subjected to further audit procedures would not constitute sufficient appropriate audit evidence upon which employer auditors could base their opinions.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 31

Various – Cost Sharing Multiple Employer Plan (from AICPA Whitepapers) Methods of allocation: Basis of an employer’s allocation of the collective pension amounts should be

consistent with the manner in which contributions to the plan are determined. GASB 68 does not specify which party (plan or employer) is responsible for calculating

the allocation percentage, it is recommended that the plan calculate each employer’s allocation percentage and collective pension amounts. Items that are needed: An opinion on the schedule of employer allocations and related notes to the schedule (not in-

relation) An opinion on the schedule of pension amounts by employer and related notes to the schedule

(not in-relation). This includes Total Pension Liability, Total Deferred Outflows of Resources, Total Deferred Inflows of Resources and Total Pension Expense

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 32

Various – Cost Sharing Multiple Employer Plan (from AICPA Whitepapers) If Best Practice Solutions Not Adopted: If a cost sharing plan issues audited financial statements, but does not

implement the best practice solutions, it is unlikely that employer auditorswill be able to accumulate sufficient appropriate audit evidence necessary to provide unmodified opinions on the opinion units of the government financial reporting entity that have material pension amounts. Unaudited information provided by the plan to its employers to support

specific pension amounts that have not been subjected to further audit procedures would not constitute sufficient appropriate audit evidence upon which employer auditors could base their opinions.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 33

Various – Audit Evidence on Beginning Net Pension Liability in the Implementation Year – AICPA Article Requires cost sharing employers, for the first time, to report net pension liability Plans prepare an additional schedule of employer allocations and a schedule of

net pension liability as of the plan’s prior year end. Deferred inflows, deferred outflows and pension expense would not need to be

included. Plan can add an additional column to the current year schedule of pension amounts

that includes the net pension liability as of the end of the prior year.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 34

Various – Effect of Employer Paid Member Contributions –AICPA Article Employer-paid member contributions may affect the classification of

contributions by the plan in the statement of changes in fiduciary net position. If the employer-paid member contribution is recognized by an employer as

salary expense, the contributions relative to that employer should be classified as member contributions. If the employer-paid member contribution is treated by the employer as salary

expense, the contributions would be reported as salary expense and excluded from the employer’s pension expense. If the employer-paid member contribution is recognized by an employer as

other than salary expense, the contributions relative to that employer should be classified as employer contributions. If the employer-paid member contribution is treated by the employer as other

than salary expense, the contributions would be considered additional employer pension expense.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 35

Various – Effect of Employer Paid Member Contributions –AICPA Article In situations in which the employer-paid member contributions meet the criteria

to be classified as pension expense : Employer-paid member contributions made to the plan during the measurement

period should be reflected in pension expense. Employer-paid member contributions made to the plan subsequent to the

measurement date and before the employer year end should be reported by the employer as deferred outflows of resources.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 36

Various – Audit Evidence on Intra-Entity Allocations – AICPA Article In situations where a primary government allocates pension amounts to

components (i.e., funds, departments, or component units) that issue separate financial statements that are audited by other auditors, component auditors are advised that additional audit evidence may be needed to support the allocations. Cost Sharing: If the allocation basis used by the plan for the schedule of employer allocations

is the same that was used for the intra-entity allocation, component auditors would likely not need additional assurance from the auditor of the primary government on the intra-entity allocations. If the allocation basis used by the plan for the schedule of employer allocations

is different that was used for the intra-entity allocation, component auditors would likely need additional assurance (i.e., an opinion) from the auditor of the primary government on the intra-entity allocations.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 37

Various – Audit Evidence on Intra-Entity Allocations – AICPA Article Single Employers and Agent Employers: If other auditors are not involved in component audits, additional assurance from

the auditor of the primary government on the intra-entity allocations would not be necessary as the auditor of the primary government is the auditor of the financial reporting entity and would have access to the books and records of the components suitable for testing the various allocations. If other auditors are involved in component audits, component auditors would likely

need additional assurance (i.e., an opinion) from the auditor of the primary government on the intra-entity allocations and on the pension amounts to which the allocation is applied. It is recommended that either the primary government or plan prepare a schedule of pension amounts and engage the auditor of the primary government or plan to obtain reasonable assurance and report on total net pension liability, total deferred outflows of resources, total deferred inflows of resources, and total pension expense for the sum of all participating components included in this schedule.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 38

Polling Question

Which best describes your organization:

a) I have a component unit that will be allocated part of the NPLb) I don’t have any component units that will be allocated part of the NPLc) I don’t have any component units

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 39

Common Questions

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 40

Can I still Present Comparative Financial Statements?

Yes!

Changes made to comply with the standards should be treated as an adjustment of prior periods if “practical”, resulting in restatement of those periods Employers should not report beginning balances of deferred

outflows/inflows of resources if not practical to determine Not required to restate comparative information in MD&A

Need to explain why prior periods are not restated in the Notes.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 41

My Financial Statements are on a Cash Basis, what do I need to do?

Liability is not reported on the Financial Statements

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 42

How does my Organization Pay-Off the Liability?

The Pension Liability is not expected to be paid off on a current basis. The liability is reduced over time through the contribution rates. If part of a cost-sharing plan, since the liability itself is a shared liability,

individual reporting units can’t “pay off” their proportionate share.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 43

Can the Pension Liability be Allocated?

No specific requirements for allocation of the net pension liability or other pension-related amounts to individual funds or departments in GASB 68 Question 36 of GASB Guide to Implementation of GASB Statement 68 states For proprietary and fiduciary funds, consideration should be given to National Council

on Governmental Accounting (NCGA) Statement 1, Governmental Accounting and Financial Reporting Principles, paragraph 42, as amended, which requires that long-term liabilities that are "directly related to, and expected to be paid from" those funds be reported in the statement of net position or statement of fiduciary net position, respectively.

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 44

Questions?

The Unique Alternative to the Big Four®

Audit | Tax | Advisory | Risk | Performance © 2015 Crowe Horwath LLP 45

For more information, contact:

Christine TorresDirect [email protected]

Kevin W. SmithDirect [email protected]

Crowe Horwath LLP is an independent member of Crowe Horwath International, a Swiss verein. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLP and its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2015 Crowe Horwath LLP