gatwick airport limited · gatwick airport limited . ... gate each year across europe •gatwick...

TRANSCRIPT

RESULTS FOR THE SIX MONTHS ENDED 30 SEPTEMBER 2013

GATWICK AIRPORT LIMITED

OPERATIONAL AND FINANCIAL PERFORMANCE

Traffic growth from existing carriers with new routes, fuller planes and increased flight frequencies

Additional traffic from new airlines joining Gatwick

Investment programme delivering new and improved facilities that transform the passenger and airline experience

Continuing trend of improvement in operational performance is delivering near record levels of customer service

Robust financial performance reflecting passenger growth, increased income per passenger and careful cost management

+ 3.5%

UNDERLYING TRAFFIC GROWTH *

+ 14.4%

EBITDA GROWTH

£105m

CAPITAL EXPENDITURE

£2,453m

RAB**

£1,474m

SENIOR NET DEBT**

* Underlying traffic growth is 3.5% as Olympics reduced traffic by an estimated 170k passengers in 2012. Actual traffic growth was 4.4%

**All figures are for the six months ended 30 September 2013 except RAB, Senior Net Debt and Senior RAR which are shown as at 30 September 2013

HIGHLIGHTS

2

0.60x

SENIOR RAR **

OUR AMBITION & STRATEGY, CONSISTENTLY APPLIED

3

RECORD SERVICE AND SATISFACTION LEVELS

Service quality at record levels Consistently high on-time departures performance

Security queuing beats targets

4

change of ownership

Sustained passenger ratings at near 12/13 record levels

4.06

4.07 4.08

4.16 `

4.23

Average

50%

60%

70%

80%

90%

100%

08/09 09/10 10/11 11/12 12/13 13/14

% Measures Failed % Measures Passed

75%

80%

85%

90%

95%

100%

08/09 09/10 10/11 11/12 12/13 13/14

North Terminal Average <5 min South Terminal Average <5 min Target

55.0%

60.0%

65.0%

70.0%

75.0%

10/11 11/12 12/13 13/14

Peak months are June, July & August

3.9

4.0

4.1

4.2

4.3

08/09 09/10 10/11 11/12 12/13 13/14

Overall QSM Target

4.21

RECORD SERVICE LEVEL RANKINGS (ASQ)

5

0.0

1.0

2.0

3.0

4.0

5.0

1 2 3 4 5 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Benchmarking Q3 2013

Average LGW

0.0

1.0

2.0

3.0

4.0

5.0

1 2 3 4 5 6 7 8 9 10 11 13 14 15 16 17 18 19 20 21

Benchmarking Q4 2009

Average LGW

12th of 21 in

Q4 2009

6th of 23 in

Q3 2013

• Results of ASQ rankings from data collected from multiple European airports

• Over 100,000 passengers interviewed at gate each year across Europe

• Gatwick now achieving both a record score and also a record highest position, in an increasing survey size

INCUMBENT…

Announcements indicate increasingly diversified route mix

European market continues to be Gatwick’s largest and grew by 5.2%

Norwegian launched 12 new routes, Vietnam & Turkish increasing

frequencies

Growth in long haul leisure complemented by growth in

business (Dubai, Moscow, China)

BA basing new 777 & Emirates expecting A380 at Gatwick in 2014

Announced new routes to New York, Los Angeles and Paris

More new airlines attracted to Gatwick, in competition with other

London airports

Vueling 14 flights per week to Barcelona

Air Arabia 3 per week to North Africa

WOWair 14 per week to Iceland

Garuda launch delayed to May 14 as Jakarta runway needs remedial

work. 3 flights per week, rising to 5 in Sep 14 – the UK’s only direct

connection

6

and NEW AIRLINES

TRAFFIC GROWTH FROM…

DELIVERING AIRPORT TRANSFORMATION PROGRAMME

DELIVERY OF INVESTMENT PROGRAMME ON SCHEDULE

£105m invested in H1 2013/14

£1,089m invested since start of Q5 (April 2008)

£1,172m total projected investment in Q5

PROJECTS COMPLETED IN LAST 6 MONTHS

Second phase of ST IDL refurbishment – 11 new stores (£11m)

Pier 5 Phase 1 reconfiguration (£23m)

Flood alleviation (£4m)

Redevelopment of UKBF Arrivals area (£3m)

PROJECTS ONGOING IN 2013/14

Pier 5 Phase 2 reconfiguration (£45m)

Pier 1 redevelopment (£42m)

New crew reporting facility (£20m)

Review of capital programme for the period beyond March 2014

7

LARGEST RETAIL DEVELOPMENT IN GATWICK’S HISTORY

GATWICK RETAIL IS CHANGING…

- 23 retail redevelopment projects in last year in NT alone

- Summer 13 saw a record number of new store openings in the ST in one day, including a new 6,000ft2 Harrods department store

- ST development completes in Dec13 when new brands launching include Victoria’s Secret, Zara, Joules, Superdry, Snow & Rock, Ted Baker and Fat Face

8

…AND PASSENGERS LOVE IT! Customer satisfaction is at a record high

- in Oct13, 81.5% of passengers rated retail outlets as ‘excellent’ or ‘good’ - Catering was at 85% on the same basis and has received 2 awards for ‘best in class’ in the last 3 months

INCREASED MOVEMENTS, INCREASED SIZE AND FULLER PLANES…

9

…results in higher capacity from Gatwick’s most limiting resource – a single runway

2012 H1 2013 H1 Change %

ATMs (k) 135.3 139.0 +2.7%

Seats per ATM 174.7 174.9 +0.1%

Load factors 84.3% 85.6% +1.3% pts

Passengers (m) 19.9 20.8 +4.4%

CONTINUED TREND OF STEADY TRAFFIC GROWTH

Recent growth • 2013 H1 total traffic has increased by +4.4% • Underlying 2013 H1 growth +3.5% (Olympics reduced traffic by an estimated 170k passengers in 2012) • 12 month trailing traffic at 35.2m, by end October 2013; 3.3% higher than the equivalent period last year

10

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%Jun-0

8

Aug-0

8

Oct-

08

De

c-0

8

Feb

-09

Apr-

09

Jun-0

9

Aug-0

9

Oct-

09

De

c-0

9

Feb

-10

Apr-

10

Jun-1

0

Aug-1

0

Oct-

10

De

c-1

0

Feb

-11

Apr-

11

Jun-1

1

Aug-1

1

Oct-

11

De

c-1

1

Feb

-12

Apr-

12

Jun-1

2

Aug-1

2

Oct-

12

De

c-1

2

Feb

-13

Apr-

13

Jun-1

3

Aug-1

3

Movin

g A

vera

ge T

ota

l

Month

ly y

ear-

on-y

ear

traff

ic g

row

th (

%)

YOY Growth by month (%)

Moving Average Total

GATWICK HEATHROW STANSTED LUTON

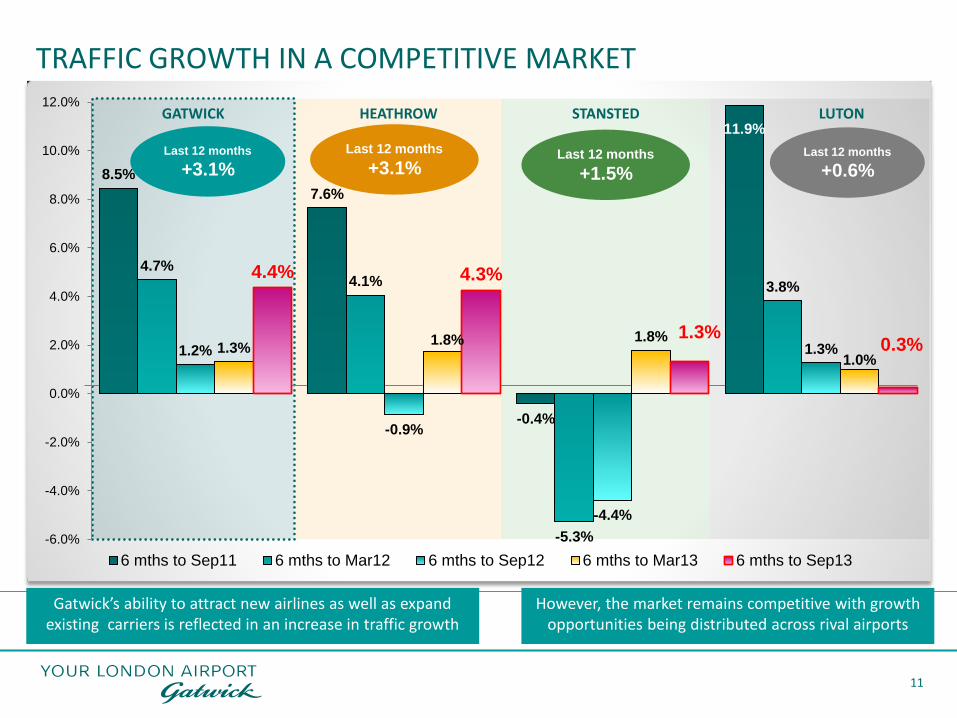

TRAFFIC GROWTH IN A COMPETITIVE MARKET

Gatwick’s ability to attract new airlines as well as expand existing carriers is reflected in an increase in traffic growth

However, the market remains competitive with growth opportunities being distributed across rival airports

11

Last 12 months

+3.1% Last 12 months

+1.5%

Last 12 months

+0.6% 8.5%

7.6%

-0.4%

11.9%

4.7% 4.1%

-5.3%

3.8%

1.2%

-0.9%

-4.4%

1.3% 1.3% 1.8% 1.8%

1.0%

4.4% 4.3%

1.3% 0.3%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

6 mths to Sep11 6 mths to Mar12 6 mths to Sep12 6 mths to Mar13 6 mths to Sep13

Last 12 months

+3.1%

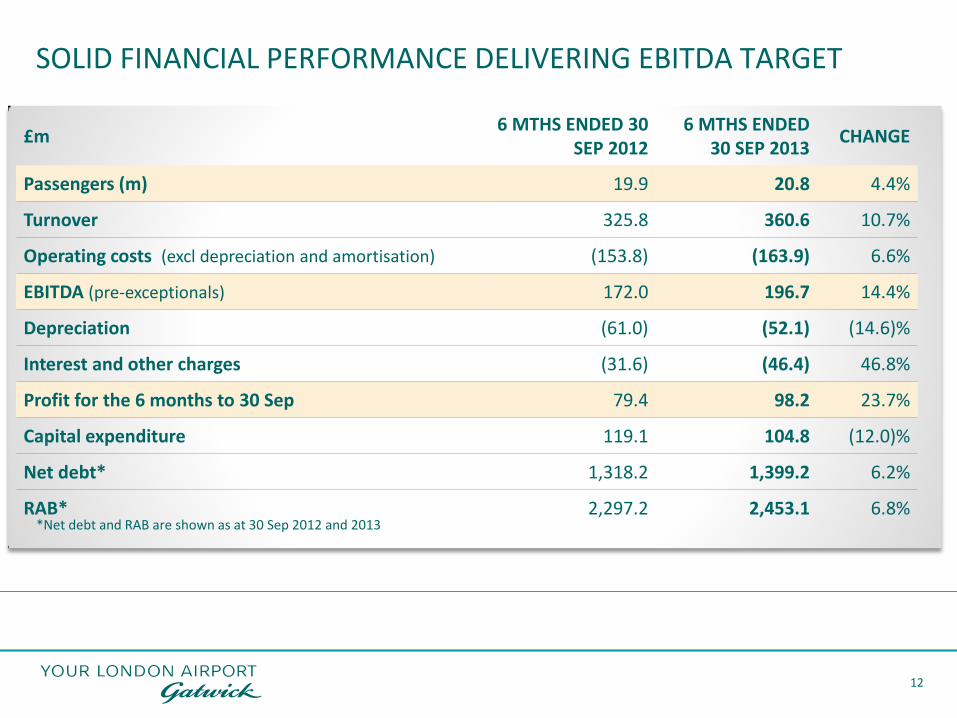

SOLID FINANCIAL PERFORMANCE DELIVERING EBITDA TARGET

£m 6 MTHS ENDED 30

SEP 2012 6 MTHS ENDED

30 SEP 2013 CHANGE

Passengers (m) 19.9 20.8 4.4%

Turnover 325.8 360.6 10.7%

Operating costs (excl depreciation and amortisation) (153.8) (163.9) 6.6%

EBITDA (pre-exceptionals) 172.0 196.7 14.4%

Depreciation (61.0) (52.1) (14.6)%

Interest and other charges (31.6) (46.4) 46.8%

Profit for the 6 months to 30 Sep 79.4 98.2 23.7%

Capital expenditure 119.1 104.8 (12.0)%

Net debt* 1,318.2 1,399.2 6.2%

RAB* 2,297.2 2,453.1 6.8% *Net debt and RAB are shown as at 30 Sep 2012 and 2013

12

10.7% INCREASE IN TURNOVER REFLECTING TRAFFIC GROWTH AND HIGHER SPEND PER PASSENGER

Turnover analysis

TOTAL £325.8m £360.6m +10.7% Aeronautical revenues increased by 11.6%, half of which is due to capex trigger payments in 2012

Net retail income per passenger increased by 2.0% to £3.55 as new stores and rejuvenated IDL drive higher spending • 23 projects in NT in last 12 months • 11 new stores in H1 2013 in ST • Includes new 6,000ft2 Harrods store

Net car parking revenue per passenger increased by 15.7% to £1.47 • Improved yield management in peak

season • Increased premium products eg valet • New offers eg hotel park and stay

13

37.2 39.6

33.5 39.5

69.7 74.6

185.4 206.9

2012 H1 2013 H1

Aeronautical Retail Car parking Other income

+11.6%

+7.0%

+17.9%

+6.5%

6.6% INCREASE IN COSTS TO SUPPORT SERVICE LEVELS, INCREASE EFFICIENCY AND REGULATORY WORK

Staff costs increase driven by • Increase in security staff to support

improved service levels • 2% increase in average salaries • Pension costs up £1.7m • Severance costs £1.0m

General expenses reflects • Increased consultancy cost to support

Q6 regulatory and R2 work • Contract savings

Rates costs increase as Capital Programme returns more assets to operational status

14

Operating costs analysis

TOTAL £153.8m £163.9m +6.6%

Note: operating costs excluding depreciation and amortisation

18.2 19.4

26.7 27.1

46.4 47.9

62.5 69.5

2012 H1 2013 H1

Staff Costs (net) General + Other Expenses

Rates + Utilities Maintenance + IT

+11.2%

+3.2%

+1.5%

+6.6%

Maintenance & IT costs increase due to reprioritisation and rephasing of maintenance spend

NET DEBT 31 MARCH 2013 TO 30 SEPTEMBER 2013

15

178.6 113.9

8.5

50.0

1.9

1,403.5 1,399.2

1,100.0

1,150.0

1,200.0

1,250.0

1,300.0

1,350.0

1,400.0

1,450.0

1,500.0

1,550.0

Opening Capitalexpenditure

Net interest Cash flow fromops

Restrictedpayment

Other Closing

£m

Note: net interest includes £5.5m capitalised interest

FUNDING PLATFORM ESTABLISHED – BANK REFINANCING WITHIN NEXT YEAR

FINANCIAL RATIO

12 MONTHS ENDED 30 SEPTEMBER 2012

12 MONTHS ENDED 30 SEPTEMBER 2013

Cash flow (per covenant) £180.1m £220.4m

Total interest (net) £36.5m £70.9m

Senior ICR 4.93x 3.11x

Trigger <1.50x <1.50x

Senior Net Debt (per covenant) £1,382.7m £1,474.4m

RAB £2,297.2m £2,453.1m

Senior RAR 0.60x 0.60x

Trigger >0.70x >0.70x

DEBT MATURITY PROFILE REDUCES REFINANCING RISK

STRONG LIQUIDITY POSITION TO FUND REMAINING Q5 INVESTMENT PROGRAMME OF £82m :

£300m 2041/43 Class A Bond

£300m 2037/39 Class A Bond

£300m 2026/28 Class A Bond

£300m 2024/26 Class A Bond

£222m Dec-14 Bank Facilities (drawn)

Annual cash flow from operations £269m for the 12 months ended 30 September 2013

Undrawn bank commitments £234m as at 30 September 2013

Restricted payment proposed £55m December 2013

16

REGULATORY UPDATE

17

CAA published Q6 Final Proposals on 3 October, 2013

• CAA will “introduce a new regulatory approach for GAL based on the airport’s commitments to airlines and underpinned by a CAA licence”

• Commitments are a 7 year, legally binding contractual undertaking between GAL and its airlines, embedded in the airport's Conditions of Use

Regulatory timetable

• 30 day consultation on Q6 Final Proposal, ended 4 November 2013

• CAA publishes market power determination & proposed licence January 2014

• CAA grants licence February 2014

• Appeal (if any) of market power determination or licence terms March 2014

• Airport Commitments & licence come into force 1 April 2014

• Appeal hearings (if any) with CAT or CMA Spring/Summer 2014

THE AIRPORTS COMMISSION - TIMELINE

28 Feb

2013 15 Mar

2013 15 Mar

2013

17 May

2013 19 Jul

2013 Spring

2014 Summer

2014 11 July

2013 6 Sept

2013

27 Sept

2013

Summer

2015 Dec

2013

18

Gatwick delivers the increased connectivity that the UK needs

True competition leads to passenger choice, better service and lower fares

Economic benefits spread more

widely across the south east

More certainty of delivery

Great resilience to disruption

Less environmental impact

Supported by County Councils around Gatwick

LONDON GATWICK …THE BEST SOLUTION

19

LONDON GATWICK: THE DELIVERABLE SOLUTION

LONDON GATWICK BAA Heathrow

Connectivity Legacy Charter Low Cost Legacy Charter Low Cost

Noise

Lden (55-60 dBA)

2011

3,700 – 13,800 households

affected 256,000 households affected

Air Quality Complies with legal standards Breaches legal standards today

Cost £5bn+ Up to £18bn

Speed Open 2025 Open earliest 2030

Surface Access Manageable

Minimal funding

Congested

£billion public contribution

Resilience HIGH LOW

Consumer choice Grows Shrinks

Economy Distributed Concentrated

20

• Despite the ongoing tough economic conditions in key European markets, traffic growth has continued through incumbent and new airlines and routes

• Robust financial performance in line with expectations, reflecting passenger growth, new retail and car parking products delivering increased income per passenger, and careful cost management

• All service quality measures achieved for all but one month and significant improvements in customer survey scores and overall airport ranking

• Investment programme on track, delivering new, improved and innovative facilities

• Continuing to state London Gatwick’s case as the obvious choice for further expansion of airport capacity

CONCLUSION

Full details of today’s announcement at: gatwickairport.com/investor

21

DISCLAIMER

This material contains certain tables and other statistical analyses (the “Statistical Information”) which have been prepared in reliance on publicly available information and may be subject to rounding. Numerous assumptions were used in preparing the Statistical Information, which may or may not be reflected herein. Actual events may differ from those assumed and changes to any assumptions may have a material impact on the position or results shown by the Statistical Information. As such, no assurance can be given as to the Statistical Information’s accuracy, appropriateness or completeness in any particular context; nor as to whether the Statistical Information and/or the assumptions upon which it is based reflect present market conditions or future market performance. The Statistical Information should not be construed as either projections or predictions nor should any information herein be relied upon as legal, tax, financial or accounting advice. Gatwick Airport Limited (“GAL”) does not make any representation or warranty as to the accuracy or completeness of the Statistical Information.

These materials contain statements that are not purely historical in nature, but are “forward-looking statements”. These include, among other things, projections, forecasts, estimates of income, yield and return, and future performance targets. These forward-looking statements are based upon certain assumptions, not all of which are stated. Future events are difficult to predict and are beyond GAL’s control. Actual future events may differ from those assumed. All forward-looking statements are based on information available on the date hereof and neither GAL nor any of its affiliates or advisers assumes any duty to update any forward-looking statements. Accordingly, there can be no assurance that estimated returns or projections will be realised, that forward-looking statements will materialise or that actual returns or results will not be materially lower that those presented.

This material should not be construed as an offer or solicitation to buy or sell any securities, or any interest in any securities, and nothing herein should be construed as a recommendation or advice to invest in any securities.

This document has been sent to you in electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of electronic transmission and consequently neither GAL nor any person who controls it (nor any director, officer, employee not agent of it or affiliate or adviser of such person) accepts any liability or responsibility whatsoever in respect of the difference between the document sent to you in electronic format and the hard copy version available to you upon request from GAL.

Any reference to “GAL” will include any of its affiliated associated companies and their respective directors, representatives or employees and/or any persons connected with them.

22

QUESTIONS