gender differences in financial reporting decision- making: evidence from accounting conservatism...

TRANSCRIPT

Gender Differences in Financial Reporting Decision-Making: Evidence from Accounting Conservatism

Bill Francis , Iftekhar Hasan , Jong Chool Parka, Qiang Wu *

Lally School of Management and Technology, Rensselaer Polytechnic Institute, Troy, NY 12180, USA

報告人 : 佘濰任

Abstract

※This paper investigates the effect of gender on corporate financial reporting decision-making.

※By focusing on firms that experience changes of CFO from male to female, we compare the firms’ degree of reporting conservatism between pre- and posttransition period.

Gender Differences in Financial Reporting Decision-Making

Section1: Introduction Section2: Relevant research and hypothesisSection3: Introduces the measures of conservatism in our analysisSection4 :Sample selectionSection5 : The results of multivariate tests

Introduction

• Gender differences in attitudes towards risk and in risk related behavior have long been studied in the sociology, psychology and economics literatures

• We examine whether female CFOs follow a more conservative approach in their financial reporting compared to their alecounterparts.

Literature Review

• Watts (2003a) summarizes that accounting conservatism is an efficient mechanism to reduce information asymmetry and mitigate interest conflicts between management and various contracting parties, and reduce potential litigations by outside parties, especially shareholders.

Literature Review

• Prior studies also find that CEO/CFO turnover rate is relatively higher around financial

restatements, especially due to the use of aggressive accounting

(e.g., Desai et al. (2006) and Hennes et al. (2008)

Literature Review

• Jiang et al. (2008) document that earnings management increase more in the CFO’s equity incentives than in the CEO’s equity incentives

• Chava and Purnanandam (2007) find that a firm’s debt structure is mostly influenced by

the CFO’s incentive

Data

• S&P 1,500 companies from 1988-2007

(1)market to book ratio [Beaver and Ryan (2000)]

(2)accrual measure[Givoly and Hayn (2000)]

(3)skewness measure[Givoly and Hayn (2000) and Zhang (2008)]

Method

• We examine the impact of endogeneity on our results

• Fama-French Three-Factor Model

• CFO change(male to female) stock return volatility and cost of bank loans

• The market reacts to the quarterly earnings announcements differently

2. Conservative Financial Reporting and Gender Differences in Risk Attitudes

※ 2.1 Information asymmetry, risk and accounting conservatism

Conservatism has long been an important convention in financial reporting.

Basu (1997) interprets conservatism as “the accountant’s tendency to require a higher degree of verification to recognize good news as gains than to recognize bad news as losses.”

2. Conservative Financial Reporting and Gender Differences in Risk Attitudes

• 2.2 Gender differences in risk attitudes

※In psychology and sociology literature the women are more risk-averse than men.

Levin et al. (1988) 、 Eckel and Grossman (2003) ※ Bernasek and Shwiff (2001) also find that women allocate their pension more conservatively than men ※ Johnson and Powell (1994) study betting decisions on horse and dog races

2. Conservative Financial Reporting and Gender Differences in Risk Attitudes

• 2.2 Gender differences in risk attitudes

※ Jianakoplos and Bernasek (1998) find single women are more risk-averse than single men in household holdings investment decisions ※ Huang and Kingen (2008) investigate how gender differences of CFOs affect various corporate financial decisions

◎To summarize, most of the evidence in the literature points to gender differences in risk attitudes, with females being more risk-averse

3. Measurement of Accounting Conservatism

Because there is no single general accepted

measure of conservatism in the accounting literature, we use three different individual measures: a market-value-based measure (CON_MTB) and two earnings-based measures (CON_ACCRUAL and CON_SKEWNESS)

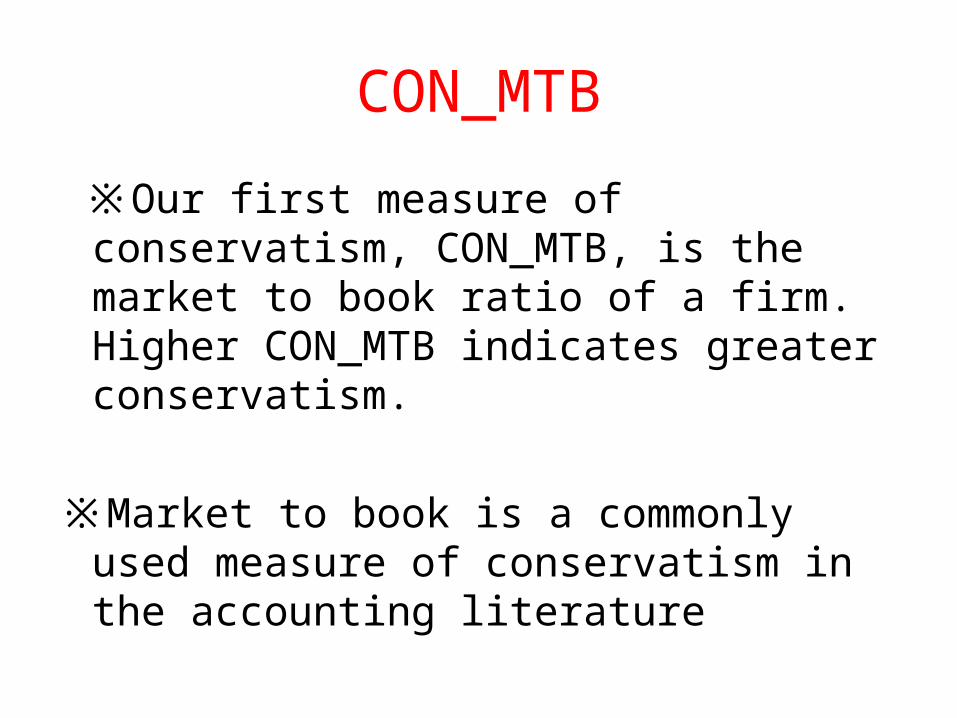

CON_MTB

※Our first measure of conservatism, CON_MTB, is the market to book ratio of a firm. Higher CON_MTB indicates greater conservatism.

※Market to book is a commonly used measure of conservatism in the accounting literature

CON_ACCRUAL

• Our second measure of conservatism, CON_ACCRUAL, is the cumulative nonoperating accruals deflated by cumulative total assets, and multiplied by -1.

• Positive values of CON_ACCRUAL indicate greater conservatism

CON_SKEWNESS

• Our third measure of conservatism, CON_SKEWNESS, is the time-series skewness of earnings

• We also multiply it by -1 to make the results easy to interpret

4. Data

• Our primary research design is to compare accounting conservatism between the pre-transition period and the post-transition period for male to female CFO turnover firms.

• Robustness tests: 1. male to male CFO transition sample 2. female to male CFO transition sample

4. Data

• The gender information is mainly from ExecuComp database which covers most S&P 1500 public companies.

• S&P 1500 includes S&P 500, S&P Midcap 400, and S&P SmallCap 600, and it covers about 85% of the US equities market.

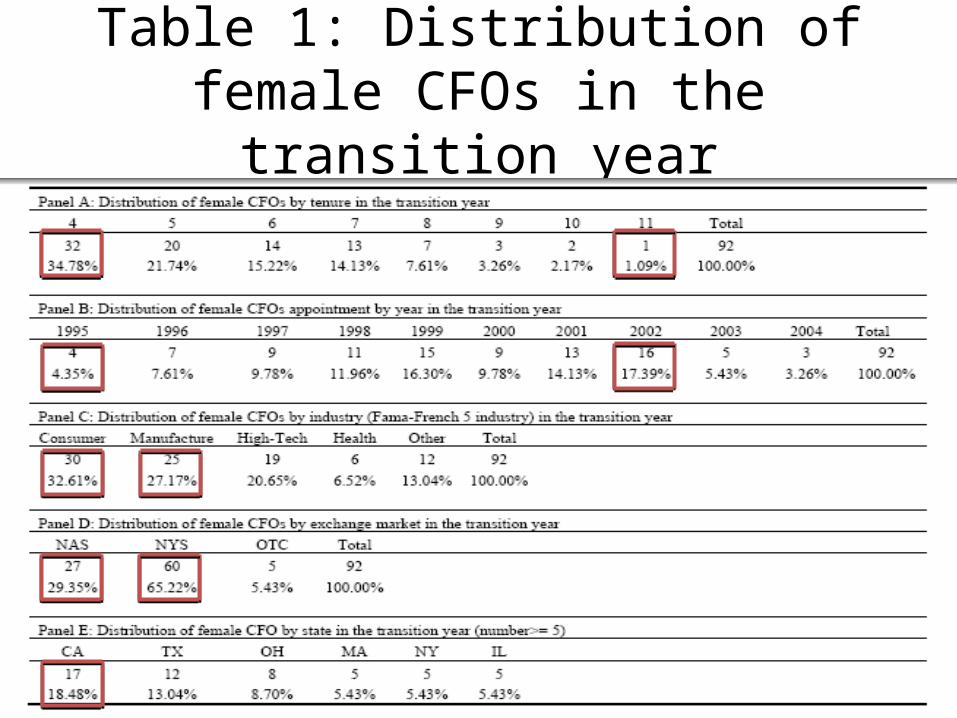

Table 1: Distribution of female CFOs in the transition year

Table 2: Summary statistics and univariate comparison

Table 3: Probit regression of hiring a female CFO

Table 4: Male to Female CFO Change and Accounting Conservatism

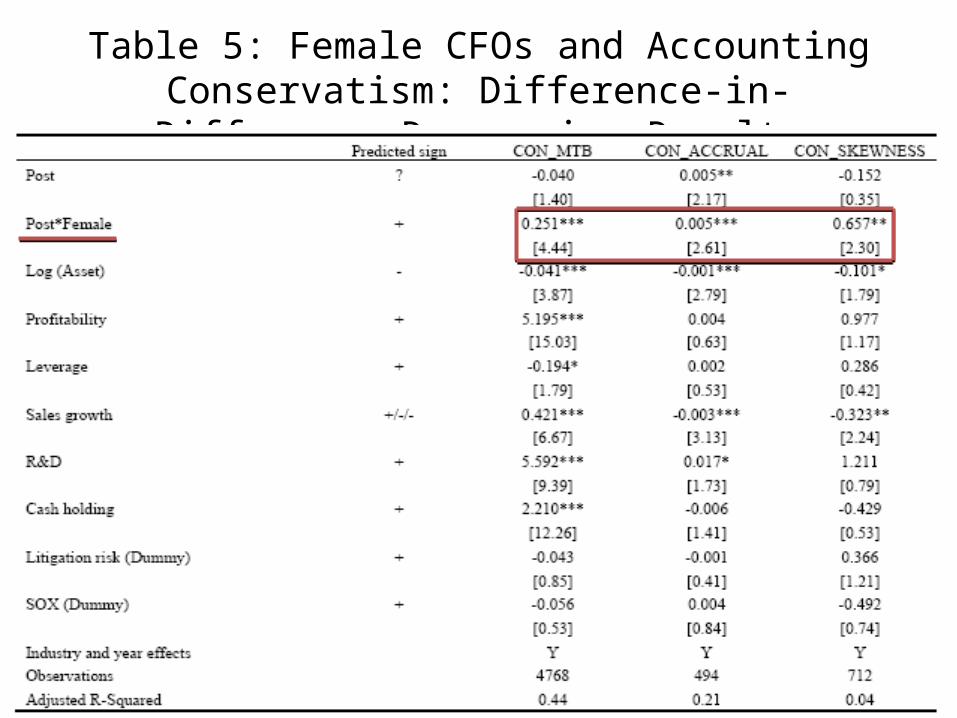

Table 5: Female CFOs and Accounting Conservatism: Difference-in-Difference Regression Results

Table 6: Female CFOs and Accounting Conservatism: Propensity Score Match Results

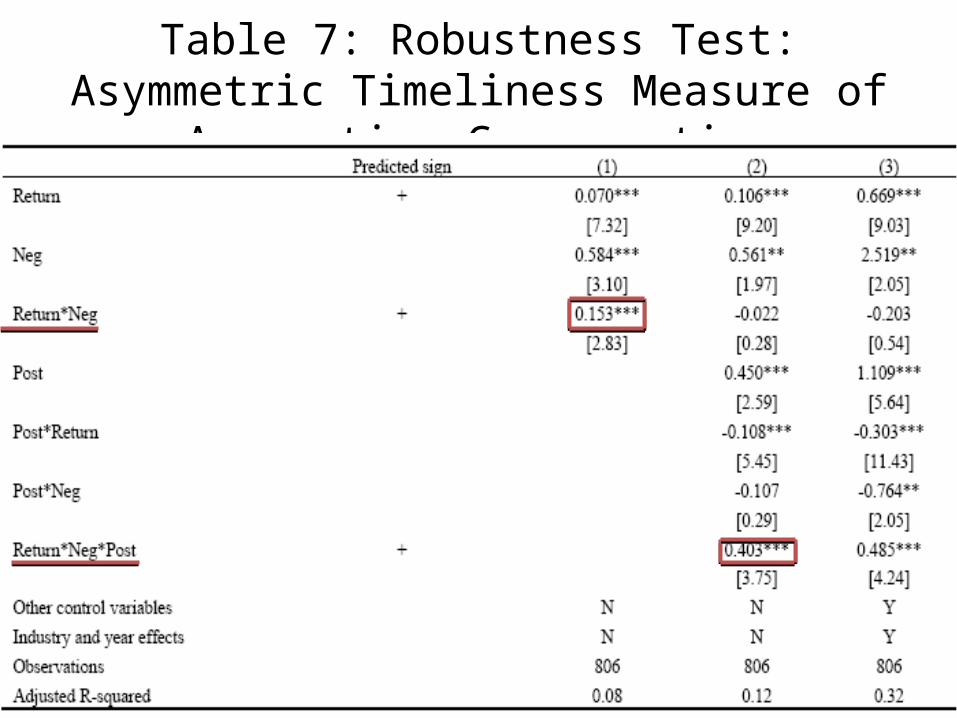

Table 7: Robustness Test: Asymmetric Timeliness Measure of Accounting Conservatism

Table 8: Robustness Test: Are Results Driven by Corporate Governance?

Table 9: Robustness Test: Are Results Driven by CFO Ownership?

Table 10: Robustness Test: Are Results Driven by Simultaneous Changes of CFO and CEO?

Table 11: Robustness Test: Female to Male CFO Transition and Accounting Conservatism

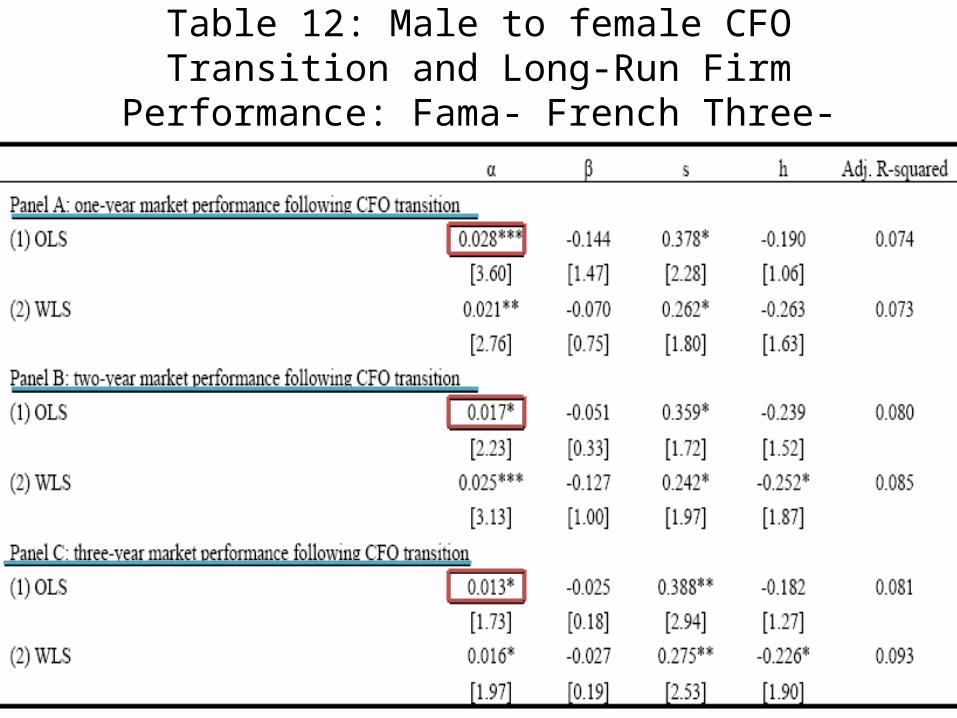

Table 12: Male to female CFO Transition and Long-Run Firm Performance: Fama- French Three-Factor Model

Table 13: Market Reactions to Earnings Announcements before and after Male to Female CFO

Transitions

Table 14: Male to Female CFO Transition, Analyst Forecast, Stock Return Volatility and Cost of Debt

6 Conclusions

We find that subsequent to the hiring of a

female CFO there is a significant increase in the degree of accounting conservatism compared to that of their male predecessors.