general comments - cima docs/2010 syllabus docs/p1... · for those topics from the new areas of the...

TRANSCRIPT

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 1

General Comments This was the second sitting of the new P1 syllabus and candidate performance was generally better than that achieved in the May diet. There were however still core areas of the syllabus where candidates demonstrated a lack of understanding and preparation. It is essential that candidates revise the entire syllabus rather than relying on particular topic areas being included in the paper. As stated in the May 2010 Post Exam Guide, an integral part of the revision process should be practising questions from past P1, P2 and P7 papers, including a comparison of the candidate’s answer to the examiner’s suggested answers. It was apparent however that many candidates had not taken this advice, even to the extent of reviewing the May 2010 exam paper, the examiner’s answers and Post Exam Guide. The answers given by many candidates in this sitting continued to demonstrate poor exam preparation, particularly for those topics from the new areas of the syllabus. The layouts for numerical answers once again fell short of the standard required. Candidates place themselves at a disadvantage if they do not provide a clear layout for their workings in numeric questions. The quality of answers to discursive questions varied considerably between questions. Many candidates demonstrated a clear understanding of zero based budgeting but few appeared to understand what backflush cost accounting involves and were therefore unable to explain why this system would be more appropriate in a JIT environment. In some questions candidates did not provide sufficiently detailed explanations of points made; however in other questions full explanations were given even though candidates were asked to ‘state’ rather than ‘explain’. It is essential that candidates consider the verb used in the question. The list of verbs and their definitions is printed in every CIMA examination paper. Candidates are again reminded of the importance of time management. The exam allows 1.8 minutes per mark and candidates should relate the time they spend on each question to the marks available. Spending a disproportionate amount of time on sections A and B to the detriment of section C is not effective time management. Full use should be made of the 20 minutes reading time at the beginning of the examination.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 2

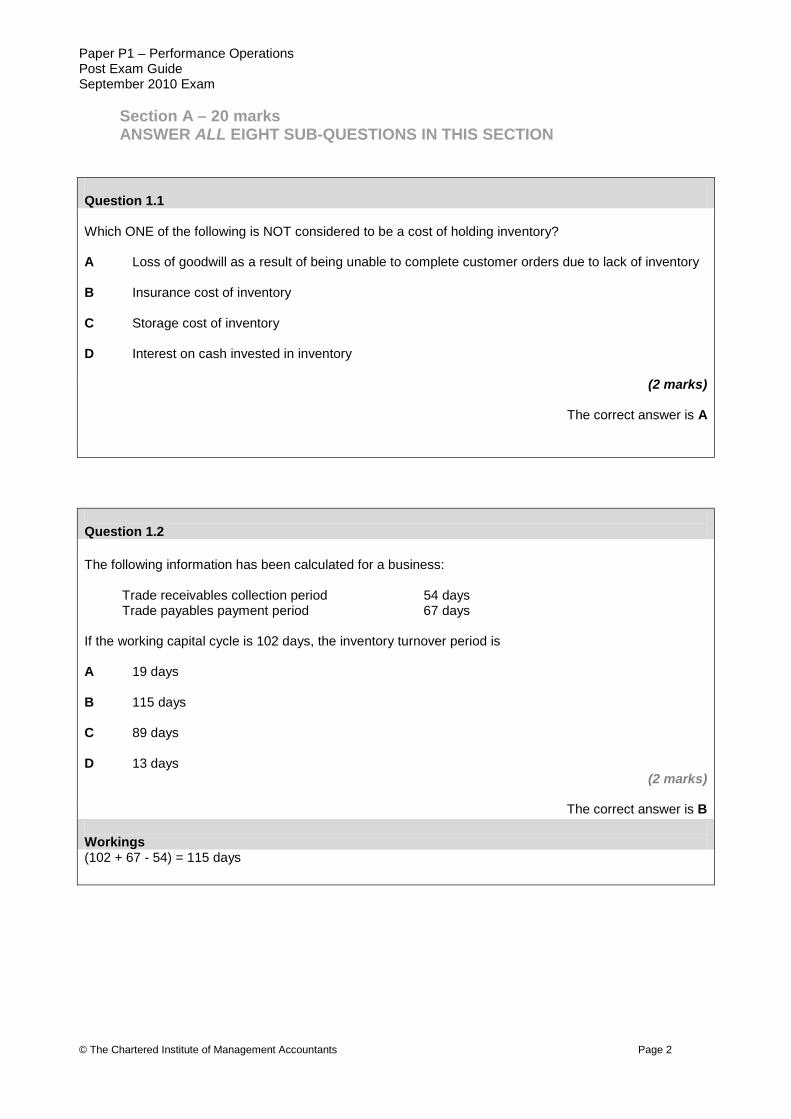

Section A – 20 marks ANSWER ALL EIGHT SUB-QUESTIONS IN THIS SECTION

Question 1.1 Which ONE of the following is NOT considered to be a cost of holding inventory?

A Loss of goodwill as a result of being unable to complete customer orders due to lack of inventory B Insurance cost of inventory C Storage cost of inventory D Interest on cash invested in inventory

(2 marks)

The correct answer is A Question 1.2 The following information has been calculated for a business:

Trade receivables collection period 54 days Trade payables payment period 67 days

If the working capital cycle is 102 days, the inventory turnover period is A 19 days B 115 days

C 89 days

D 13 days (2 marks)

The correct answer is B

Workings (102 + 67 - 54) = 115 days

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 3

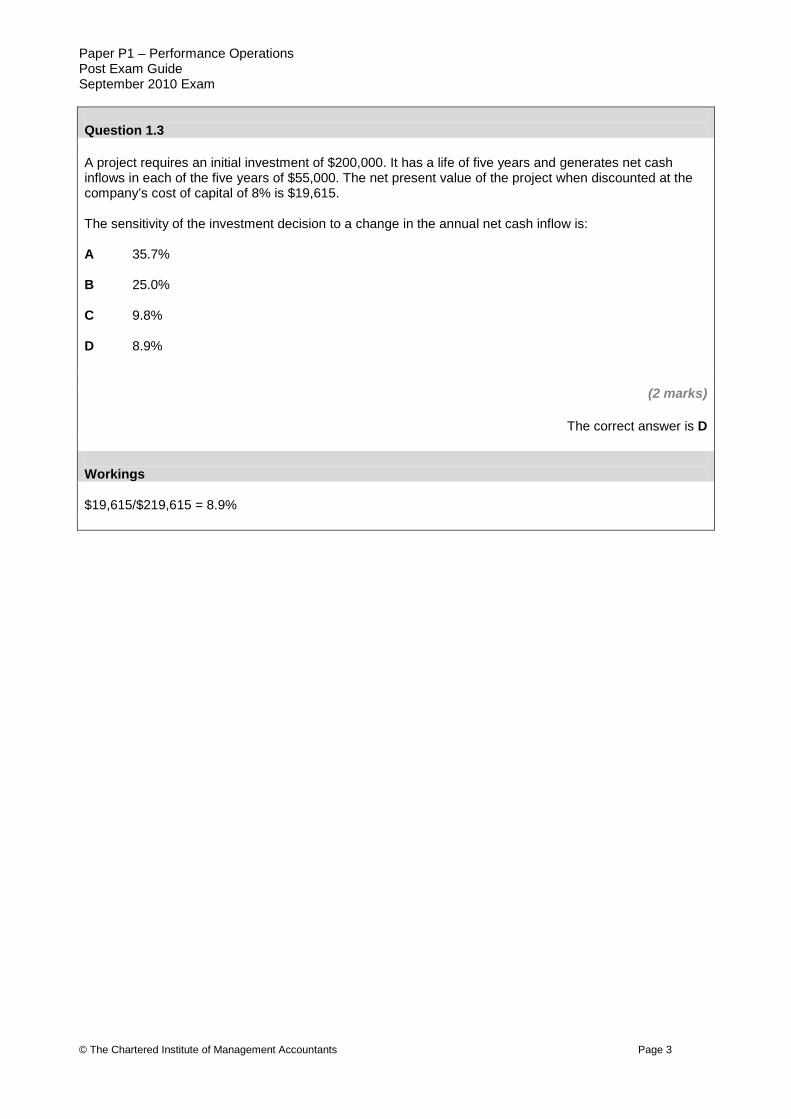

Question 1.3 A project requires an initial investment of $200,000. It has a life of five years and generates net cash inflows in each of the five years of $55,000. The net present value of the project when discounted at the company’s cost of capital of 8% is $19,615. The sensitivity of the investment decision to a change in the annual net cash inflow is:

A 35.7% B 25.0% C 9.8%

D 8.9%

(2 marks)

The correct answer is D Workings $19,615/$219,615 = 8.9%

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 4

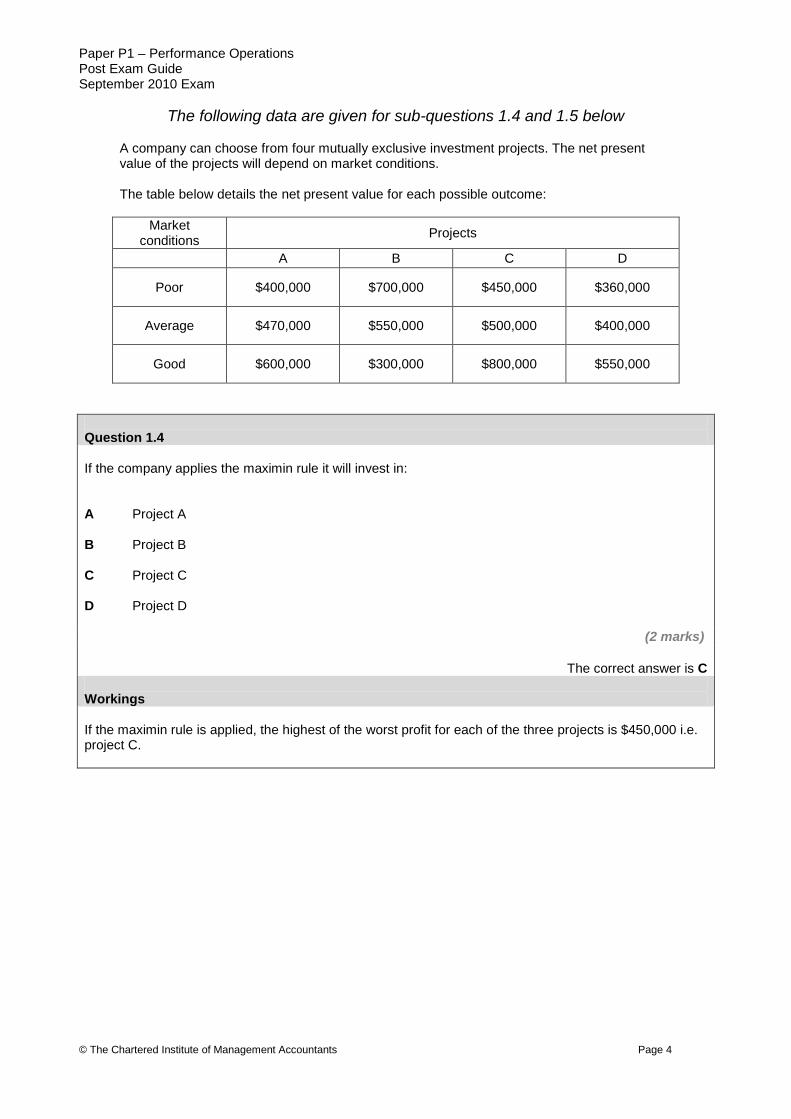

The following data are given for sub-questions 1.4 and 1.5 below A company can choose from four mutually exclusive investment projects. The net present value of the projects will depend on market conditions. The table below details the net present value for each possible outcome:

Market conditions Projects

A B C D

Poor $400,000 $700,000 $450,000 $360,000

Average $470,000 $550,000 $500,000 $400,000

Good $600,000 $300,000 $800,000 $550,000

Question 1.4 If the company applies the maximin rule it will invest in: A Project A B Project B C Project C

D Project D

(2 marks)

The correct answer is C Workings If the maximin rule is applied, the highest of the worst profit for each of the three projects is $450,000 i.e. project C.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 5

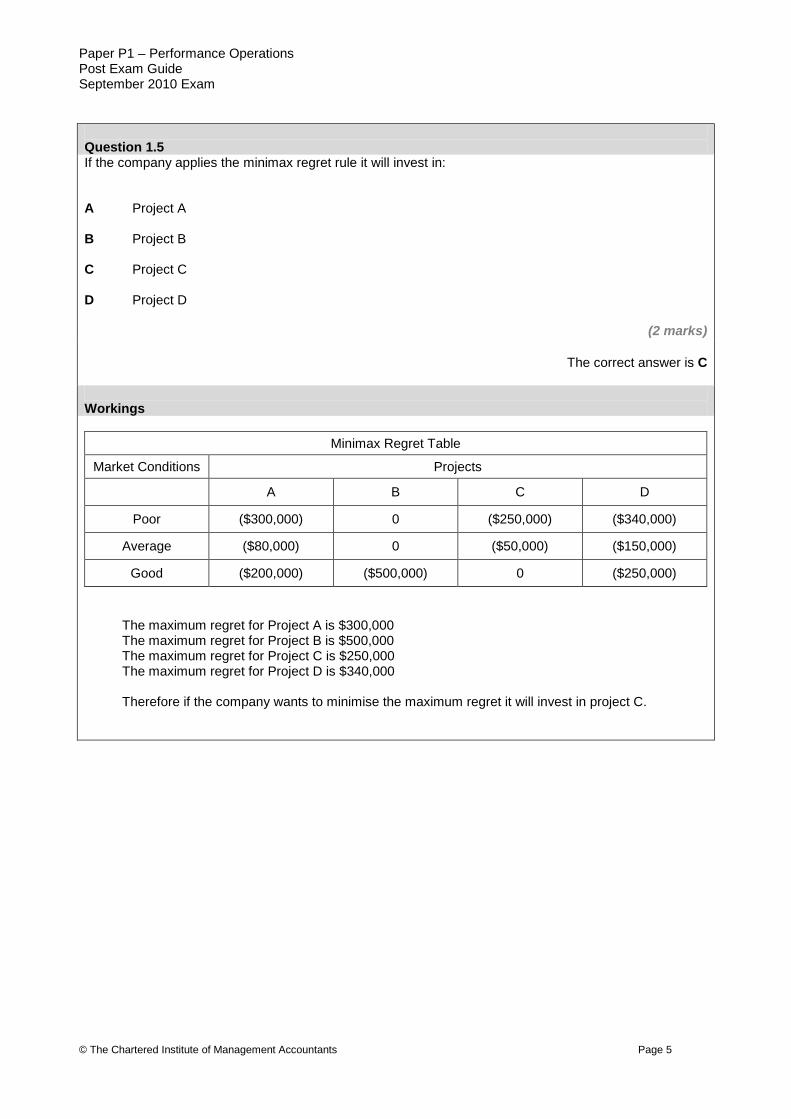

Question 1.5 If the company applies the minimax regret rule it will invest in: A Project A B Project B C Project C

D Project D

(2 marks)

The correct answer is C

Workings

Minimax Regret Table

Market Conditions Projects

A B C D

Poor ($300,000) 0 ($250,000) ($340,000)

Average ($80,000) 0 ($50,000) ($150,000)

Good ($200,000) ($500,000) 0 ($250,000)

The maximum regret for Project A is $300,000 The maximum regret for Project B is $500,000 The maximum regret for Project C is $250,000 The maximum regret for Project D is $340,000

Therefore if the company wants to minimise the maximum regret it will invest in project C.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 6

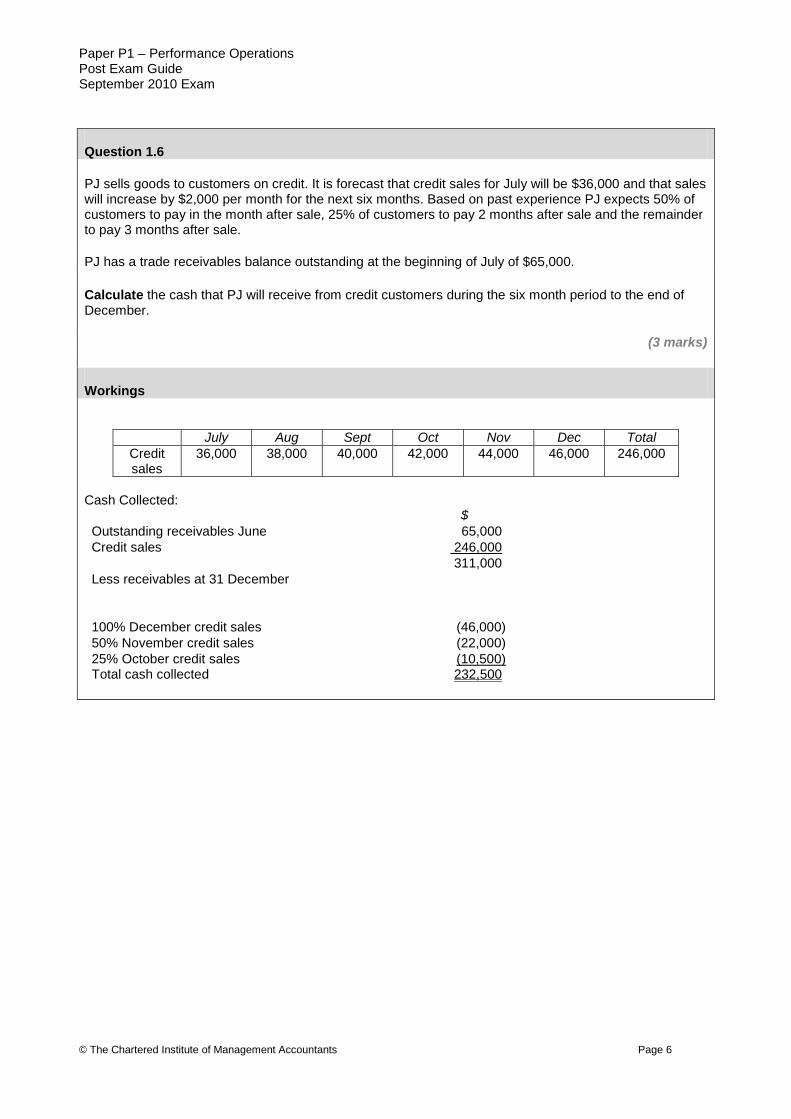

Question 1.6 PJ sells goods to customers on credit. It is forecast that credit sales for July will be $36,000 and that sales will increase by $2,000 per month for the next six months. Based on past experience PJ expects 50% of customers to pay in the month after sale, 25% of customers to pay 2 months after sale and the remainder to pay 3 months after sale. PJ has a trade receivables balance outstanding at the beginning of July of $65,000. Calculate the cash that PJ will receive from credit customers during the six month period to the end of December.

(3 marks) Workings

July Aug Sept Oct Nov Dec Total Credit sales

36,000 38,000 40,000 42,000 44,000 46,000 246,000

Cash Collected: $ Outstanding receivables June 65,000 Credit sales

246,000 311,000

Less receivables at 31 December

100% December credit sales (46,000) 50% November credit sales (22,000) 25% October credit sales Total cash collected

(10,500) 232,500

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 7

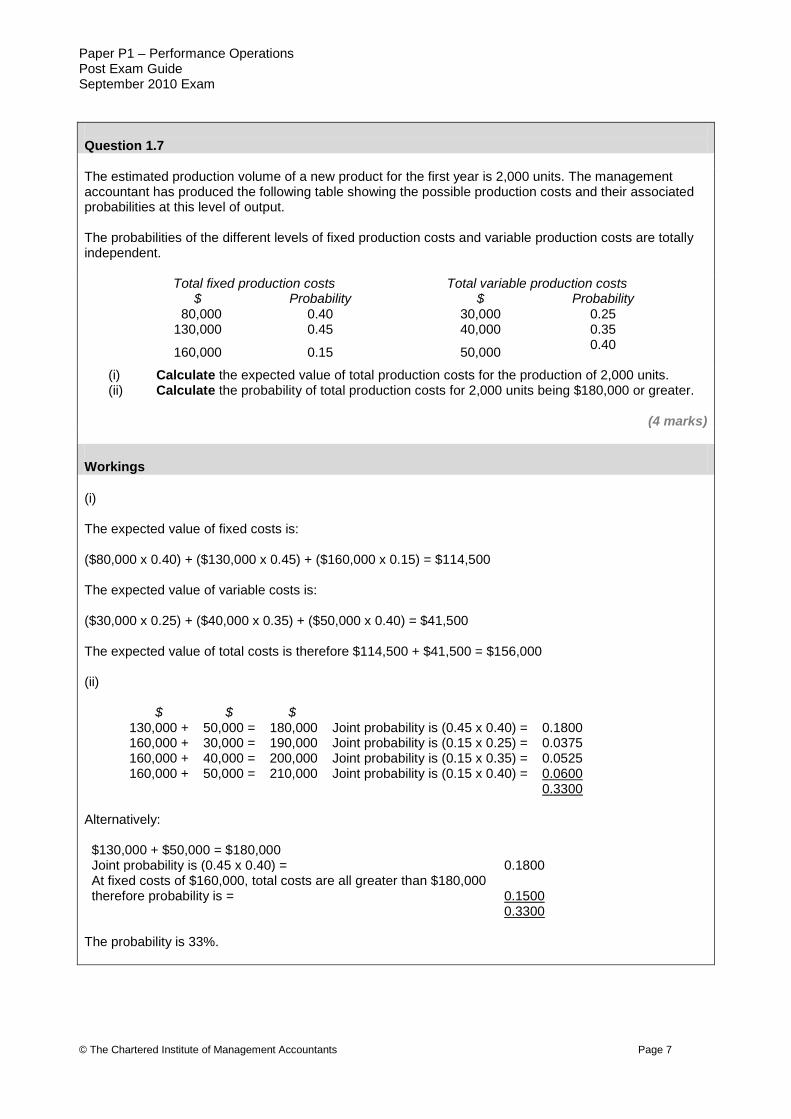

Question 1.7 The estimated production volume of a new product for the first year is 2,000 units. The management accountant has produced the following table showing the possible production costs and their associated probabilities at this level of output. The probabilities of the different levels of fixed production costs and variable production costs are totally independent.

Total fixed production costs Total variable production costs $ Probability $ Probability

80,000 0.40 30,000 0.25 130,000 0.45 40,000 0.35

160,000 0.15 50,000 0.40

(i) Calculate the expected value of total production costs for the production of 2,000 units. (ii) Calculate the probability of total production costs for 2,000 units being $180,000 or greater.

(4 marks)

Workings (i) The expected value of fixed costs is: ($80,000 x 0.40) + ($130,000 x 0.45) + ($160,000 x 0.15) = $114,500 The expected value of variable costs is: ($30,000 x 0.25) + ($40,000 x 0.35) + ($50,000 x 0.40) = $41,500 The expected value of total costs is therefore $114,500 + $41,500 = $156,000 (ii)

$ $ $ 130,000 + 50,000 = 180,000 Joint probability is (0.45 x 0.40) = 0.1800 160,000 + 30,000 = 190,000 Joint probability is (0.15 x 0.25) = 0.0375 160,000 + 40,000 = 200,000 Joint probability is (0.15 x 0.35) = 0.0525 160,000 + 50,000 = 210,000 Joint probability is (0.15 x 0.40) =

0.0600

0.3300

Alternatively: $130,000 + $50,000 = $180,000 Joint probability is (0.45 x 0.40) =

0.1800

At fixed costs of $160,000, total costs are all greater than $180,000 therefore probability is =

0.1500

0.3300

The probability is 33%.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 8

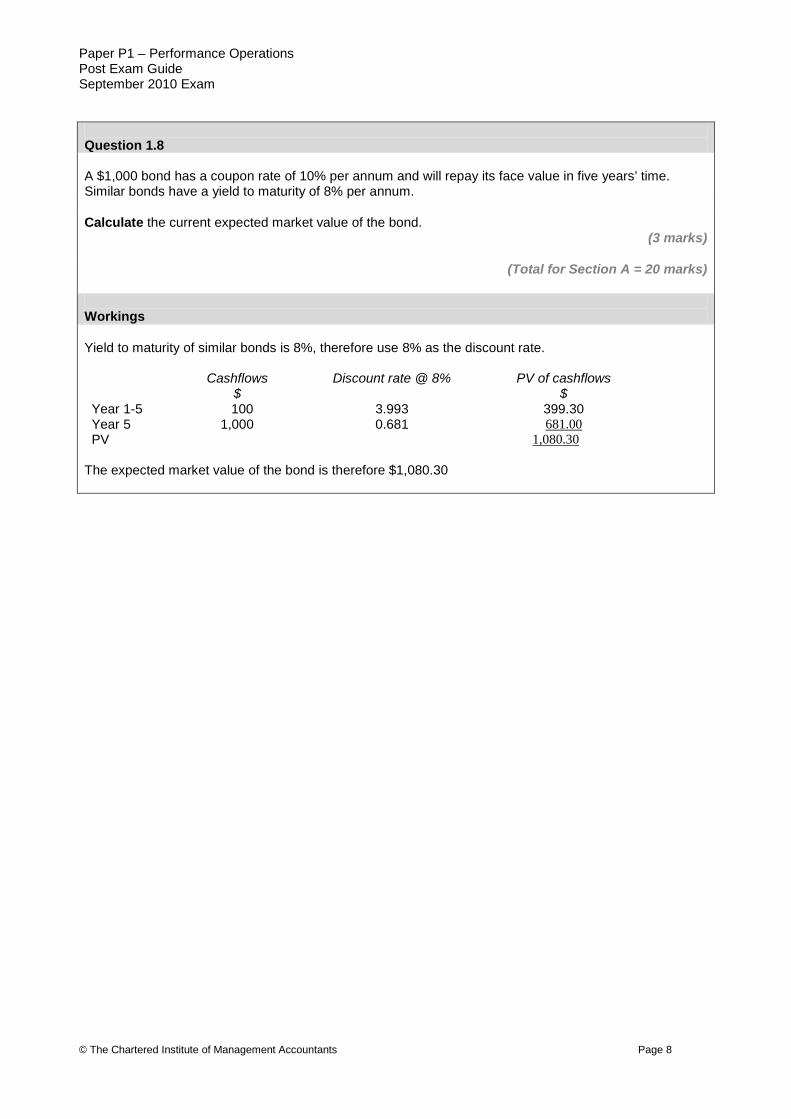

Question 1.8 A $1,000 bond has a coupon rate of 10% per annum and will repay its face value in five years’ time. Similar bonds have a yield to maturity of 8% per annum. Calculate the current expected market value of the bond.

(3 marks)

(Total for Section A = 20 marks) Workings

Yield to maturity of similar bonds is 8%, therefore use 8% as the discount rate. Cashflows

$ Discount rate @ 8% PV of cashflows

$ Year 1-5 100 3.993 399.30 Year 5 1,000 0.681 PV

681.00

1,080.30

The expected market value of the bond is therefore $1,080.30

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 9

Section B – 30 marks ANSWER ALL SIX SUB-QUESTIONS. YOU SHOULD SHOW YOUR WORKINGS AS MARKS ARE AVAILABLE FOR THE METHOD YOU USE

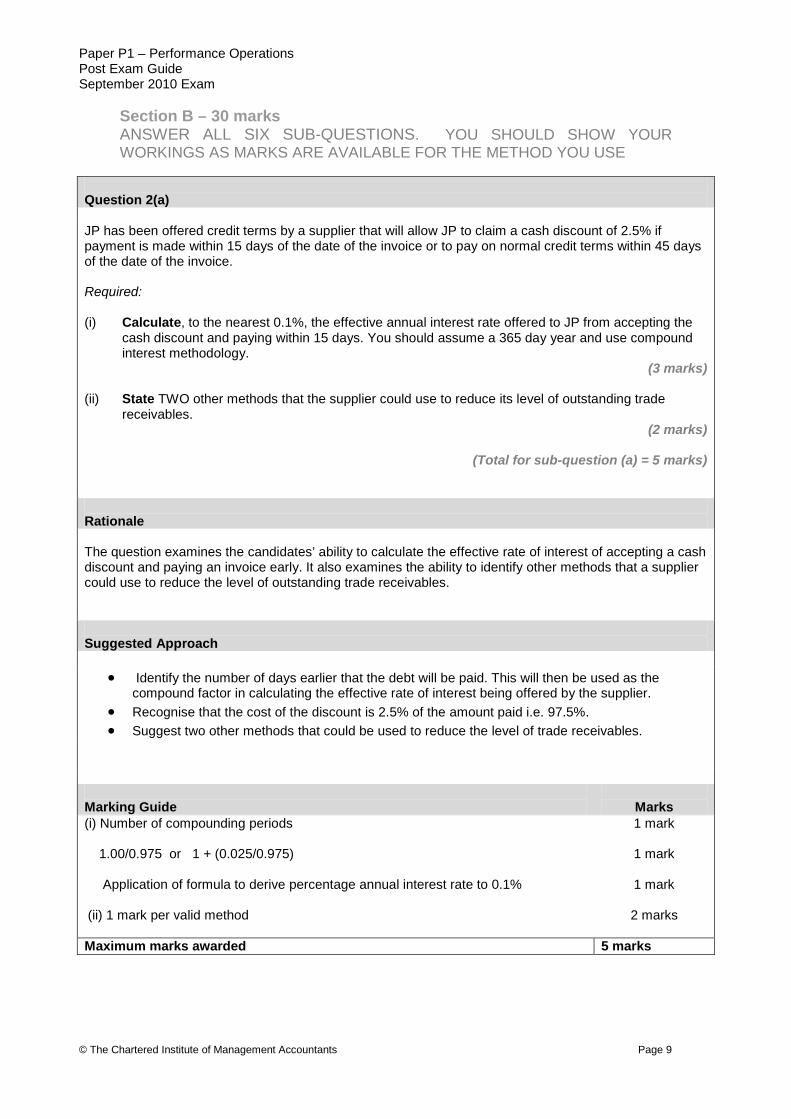

Question 2(a) JP has been offered credit terms by a supplier that will allow JP to claim a cash discount of 2.5% if payment is made within 15 days of the date of the invoice or to pay on normal credit terms within 45 days of the date of the invoice. Required: (i) Calculate, to the nearest 0.1%, the effective annual interest rate offered to JP from accepting the

cash discount and paying within 15 days. You should assume a 365 day year and use compound interest methodology.

(3 marks)

(ii) State TWO other methods that the supplier could use to reduce its level of outstanding trade receivables.

(2 marks)

(Total for sub-question (a) = 5 marks)

Rationale The question examines the candidates’ ability to calculate the effective rate of interest of accepting a cash discount and paying an invoice early. It also examines the ability to identify other methods that a supplier could use to reduce the level of outstanding trade receivables. Suggested Approach

• Identify the number of days earlier that the debt will be paid. This will then be used as the compound factor in calculating the effective rate of interest being offered by the supplier.

• Recognise that the cost of the discount is 2.5% of the amount paid i.e. 97.5%. • Suggest two other methods that could be used to reduce the level of trade receivables.

Marking Guide

Marks

(i) Number of compounding periods 1.00/0.975 or 1 + (0.025/0.975) Application of formula to derive percentage annual interest rate to 0.1% (ii) 1 mark per valid method

1 mark

1 mark

1 mark

2 marks

Maximum marks awarded 5 marks

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 10

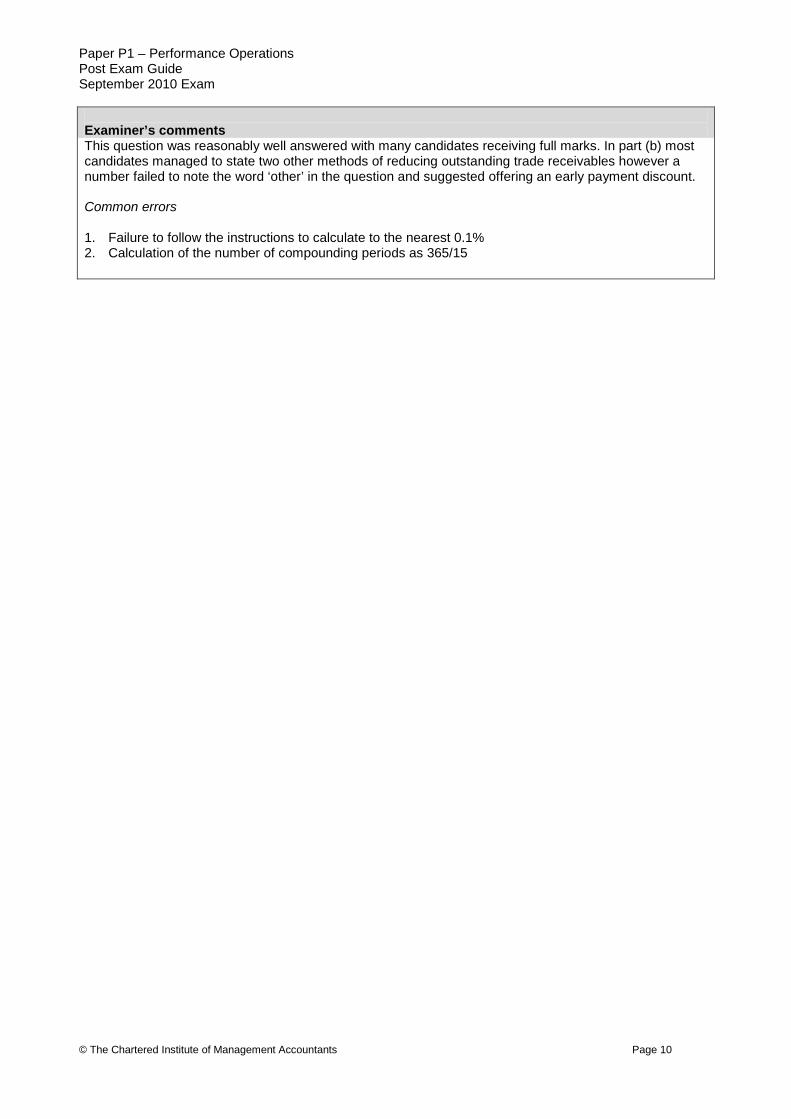

Examiner’s comments This question was reasonably well answered with many candidates receiving full marks. In part (b) most candidates managed to state two other methods of reducing outstanding trade receivables however a number failed to note the word ‘other’ in the question and suggested offering an early payment discount. Common errors 1. Failure to follow the instructions to calculate to the nearest 0.1% 2. Calculation of the number of compounding periods as 365/15

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 11

Question 2(b) BB manufactures a range of electronic products. The supplier of component Y has informed BB that it will offer a quantity discount of 1.0% if BB places an order of 10,000 components or more at any one time.

Details of component Y are as follows: Cost per component before discount $2.00 Annual purchases 150,000 components Ordering costs $360 per order Holding costs $3.00 per component per annum

Required:

(i) Calculate the total annual cost of holding and ordering inventory of component Y using the economic order quantity and ignoring the quantity discount.

(2 marks)

(ii) Calculate whether there is a financial benefit to BB from increasing the order size to 10,000 components in order to qualify for the 1.0% quantity discount.

(3 marks)

(Total for sub-question (b) = 5 marks) Rationale The question examines candidates’ ability to apply the EOQ formula and to calculate the cost of holding and ordering the suggested level of inventory. The question then requires candidates to consider whether it is worth accepting a bulk quantity discount for placing an order greater than the EOQ. Suggested Approach

• Calculate the EOQ and then apply this figure to calculate the cost of holding and ordering inventory.

• Calculate the cost of holding and ordering inventory at the higher order level • Compare the incremental cost to the incremental benefit from the quantity discount.

Marking Guide

Marks

(i) EOQ 1 mark Holding costs ½ mark Ordering costs ½ mark (ii) Holding costs ½ mark Ordering costs

Value of discount Evaluation of financial benefit

½ mark 1 mark 1 mark

Maximum marks awarded 5 marks

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 12

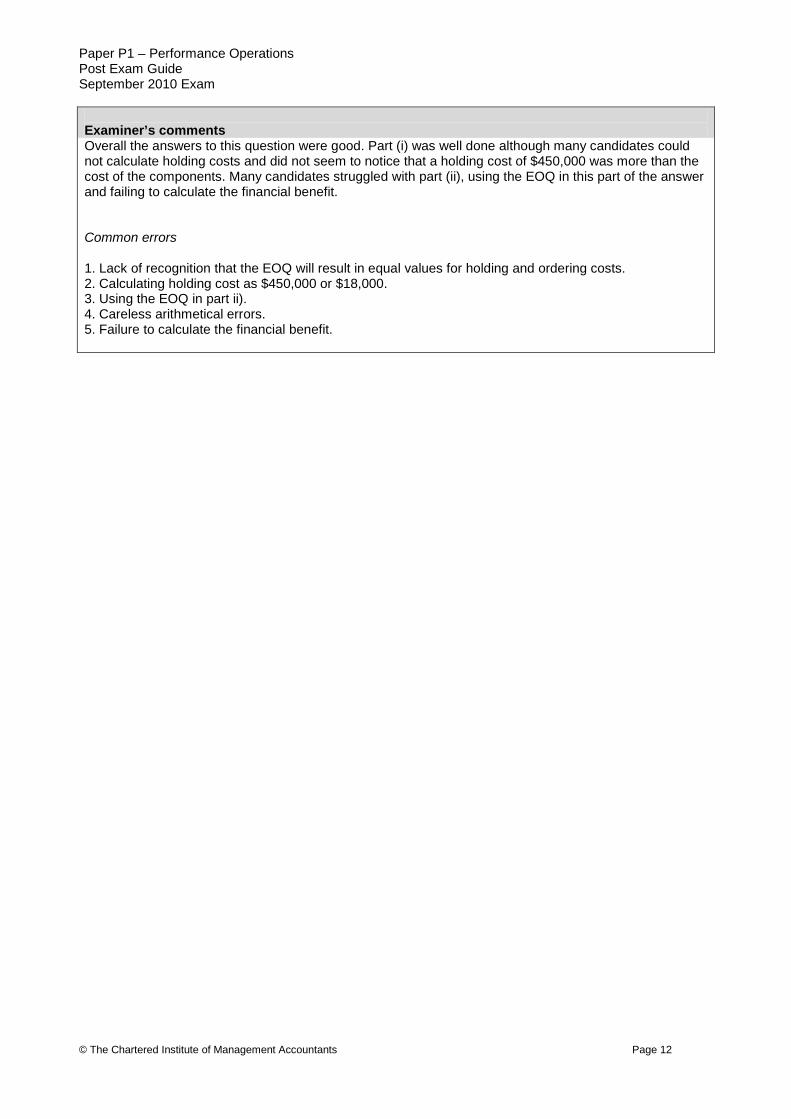

Examiner’s comments Overall the answers to this question were good. Part (i) was well done although many candidates could not calculate holding costs and did not seem to notice that a holding cost of $450,000 was more than the cost of the components. Many candidates struggled with part (ii), using the EOQ in this part of the answer and failing to calculate the financial benefit. Common errors 1. Lack of recognition that the EOQ will result in equal values for holding and ordering costs. 2. Calculating holding cost as $450,000 or $18,000. 3. Using the EOQ in part ii). 4. Careless arithmetical errors. 5. Failure to calculate the financial benefit.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 13

Question 2(c) Explain why a backflush cost accounting system may be considered more appropriate than a traditional cost accounting system, in a company that operates a just-in-time production and purchasing system.

(5 marks)

Rationale The question examines candidates’ ability to explain the benefits of using backflush cost accounting compared to a traditional cost accounting system in a company that operates just in time production and purchasing. Suggested Approach

• Explain how a traditional cost accounting system operates. • Explain what a backflush cost accounting system is and how it operates. • Explain the benefits of using backflush cost accounting when just in time purchasing and

production is being used A good answer will clearly identify and explain why a backflush cost accounting system is more appropriate than a traditional cost accounting system where JIT purchasing and production is being used. A weak answer will explain backflush costing but will not explain how this differs from a traditional costing system and why it would be preferable where JIT purchasing and production is in operation. Marking Guide

Marks

Up to 2 marks per valid point Max 5 marks

Maximum marks awarded 5 marks Examiner’s comments This question was particularly badly answered. Many candidates explained what a JIT environment involves but were unable to explain backflush cost accounting and why it would be more appropriate than a traditional costing system in a JIT environment. Common errors 1. Failure to answer the question that was asked. 2. Providing general statements rather than explaining specific points.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 14

Question 2(d) XY, a not-for-profit charity organisation which is funded by public donations, is concerned that it is not making the best use of its available funds. It has carried out a review of its budgeting system and is considering replacing the current system with a zero-based budgeting system. Explain the potential advantages AND disadvantages for the charity of a zero-based budgeting system.

(5 marks) Rationale The question examines candidates’ ability to identify and explain the advantages and disadvantages of zero based budgeting. Suggested Approach A good answer will clearly identify and explain why zero based budgeting results in a more accurate budget while recognising the difficulties inherent in a zero based budgeting system. A weak answer will not clearly identify the advantages of zero based budgeting and/or not recognise the difficulties in its implementation. Marking Guide

Marks

Up to 2 marks per valid point

Max 5 marks

Maximum marks awarded 5 marks Examiner’s comments This question was fairly straight forward and was well answered with many candidates achieving full marks. Common errors

1. Providing general statements rather than explaining specific points. 2. Lack of detail in the answers. 3. Repetition of the same point a number of times.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 15

Question 2(e) QR uses an activity based budgeting (ABB) system to budget product costs. It manufactures two products, product Q and product R. The budget details for these two products for the forthcoming period are as follows:

Product Q Product R Budgeted production (units) 80,000 120,000 Number of machine set ups per batch 4 2 Batch size (units) 5,000 4,000

The total budgeted cost of setting up the machines is $74,400.

Required:

(i) Calculate the budgeted machine set up cost per unit of product Q.

(3 marks)

(ii) State TWO potential benefits of using an activity based budgeting system.

(2 marks)

(Total for sub-question (e) = 5 marks)

Rationale The question examines candidates’ ability to apply activity based budgeting to calculate budgeted product costs. Suggested Approach

• Calculate the cost driver rate i.e. the budgeted cost per set up. • Apply this rate to product Q to calculate the total set up cost for product Q. • Calculate the set up costs per unit by dividing the total set up cost for product Q by the number of

units of product Q. Marking Guide

Marks

(i) Number of batches for each product

½ mark

Total number of set ups ½ mark Budgeted cost per set up ½ mark Total budgeted set up costs Budget set up costs per unit

½ mark 1 mark

(ii) 1 mark for each valid benefit

2 marks

Maximum marks awarded 5 marks

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 16

Examiner’s comments The performance in this question was particularly poor. Activity based costing is a core part of the P1 syllabus and the failure of many candidates to demonstrate the ability to apply activity based costing techniques to a simple budgeting question was very concerning. In part (i) candidates failed to recognise the need to calculate the cost driver rate for the whole company and then apply this to product Q. In part (ii) most candidates related their answer to activity based costing. Common errors 1. Calculation of cost driver rate using either the number of batches or the number of set ups per batch. 2. Calculation of budgeted set up costs per batch rather than per unit. 3. Failure to calculate the cost driver rate for the whole company. 4. Poor layout of workings. 5. Relating the answer to ABC rather than ABB.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 17

Question 2(f) (f) A university is trying to decide whether or not to advertise a new post-graduate degree

programme. The number of students starting the programme is dependent on economic conditions. If conditions are poor it is expected that the programme will attract 40 students without advertising. There is a 60% chance that economic conditions will be poor. If economic conditions are good it is expected that the programme will attract only 20 students without advertising. There is a 40% chance that economic conditions will be good.

If the programme is advertised and economic conditions are poor, there is a 65% chance that the advertising will stimulate further demand and student numbers will increase to 50. If economic conditions are good there is a 25% chance the advertising will stimulate further demand and numbers will increase to 25 students.

The profit expected, before deducting the cost of advertising, at different levels of student numbers are as follows:

Number of students

Profit $

15 (10,000) 20 15,000 25 40,000 30 65,000 35 90,000 40 115,000 45 140,000 50 165,000

The cost of advertising the programme will be $15,000.

Required:

Demonstrate, using a decision tree, whether the programme should be advertised.

(5 marks)

Rationale The question examines candidates’ ability to use decision trees to evaluate a decision where there is uncertainty regarding expected cash flows. Suggested Approach

• Establish the decision that has to be made • Draw the decision tree showing each of the possible outcomes. • Calculate the expected value of each of the possible outcomes.

A good answer will provide a clearly constructed decision tree showing the expected payoffs for each possible outcome.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 18

Marking Guide

Marks

½ mark per payoff 3 marks 1 mark 1 mark

Decision tree format Decision Maximum marks awarded 5 marks Examiner’s comments

This question clearly separated those candidates who had worked on the May exam paper from those who had not. The question was very similar to the one asked in May and yet it was badly answered by many candidates and a large number omitted it altogether. Many candidates seemed to think that the decision was what the economic conditions were going to be. Other candidates misread the question and ended up with a decision tree with only five branches instead of six and wrote a note to the examiner that the question was incorrect. Some candidates drew the decision tree but did not calculate any figures. Common errors 1. Drawing the decision tree on the basis that the decision was to determine the economic conditions. 2. Producing a decision tree with four or five branches rather than six. 3. Giving no figures for the decision tree. 4. Failing to state the final decision. 5. Making computational errors.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 19

Section C – 50 marks ANSWER BOTH THE TWO QUESTIONS

Question 3

(a) Produce a statement that reconciles the budgeted and actual gross profit for product RG for July showing the variances in as much detail as possible.

(13 marks)

(b) Calculate the following materials variances for August:

(i) The total materials cost variance. (ii) The planning variance for materials price. (iii) The operational variances for materials price and materials usage.

(6 marks)

(c) Discuss THREE advantages of using a standard costing system that identifies both planning and operational variances.

(6 marks)

(Total for Question Three = 25 marks)

Rationale The question examines candidates’ ability to calculate variances including both planning and operational variances and to prepare a statement reconciling the budget and actual gross profit. The advantages of identifying both planning and operational variances are also examined. Suggested Approach

• Calculate each of the individual variances, clearly identifying whether they are adverse or favourable

• Calculate the actual profit for the period. • Produce a statement showing the budgeted profit and the individual variances reconciling to the

actual profit. • Calculate the planning and operational variances in part (b) • Explain the benefits of calculating these figures in part (c).

A good answer will calculate the variances and actual profit correctly and will produce a clear reconciliation statement. A weak answer will contain errors in the calculation of variances, will not identify correctly whether the variances are adverse or favourable, will not calculate the actual profit separately and will not produce a clear reconciliation statement.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 20

Marking Guide

Marks

Part (a) Budgeted gross profit

1 mark

Sales variances 3 marks Material variances 2 marks Labour variances 2 marks Variable overhead variances Fixed overhead variances Actual gross profit

1 mark 3 marks 1 marks

Part (b) (i) Materials cost variance

1 mark

(ii) Material price planning variance (iii) Material price operational variance Material usage operational variance Part (c) Up to 2 marks per reason

2 marks 1 mark 2 marks 6 marks

Maximum marks awarded 25 marks Examiner’s comments

Part (a) Candidates performed fairly well in this part of the question. The variances which caused difficulty were the sales volume profit variance and the fixed overhead volume variance. Some candidates provided the total fixed overhead variance rather than analysing this further to show the expenditure variance and the volume variance. Part (b) This part was less well answered. Few candidates were able to calculate a materials cost variance and many calculated a price variance instead. The planning variance was seldom calculated correctly and the operational usage variance caused a lot of difficulty. Overall there was evidence of a lack of knowledge in this area. Part (c) This part was poorly answered. Most candidates discussed standard costing systems without reference to planning and operational variances. When planning and operational variances were considered there was a lack of detail in the points made. Common errors Part (a) 1. Incorrect labelling of variances. 2. Confusion over the calculation and labelling of the fixed overhead variances. 3. Use of incorrect variance signs (adverse/favourable) for the direction of variances, especially with the fixed overhead variances. 4. Incorrect calculation of the sales volume profit variance. 5. Not providing a reconciliation statement. Part (b) 1. Calculation of a material price variance rather than a materials cost variance. 2. Calculation of the material planning variance using actual quantity. 3. Incorrect calculation of the material usage variance. Part (c) 1. Not answering the question that was asked. Lack of detail in the answers.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 21

Question 4

(a) Calculate the net present value (NPV) of the gymnasium and spa project.

(16 marks)

(b) Calculate the post-tax money cost of capital at which the hotel would be indifferent to accepting / rejecting the project.

(4 marks)

(c) Discuss an alternative method for the treatment of inflation that would result in the same NPV.

Your answer should consider the potential difficulties in using this method when taxation is involved in the project appraisal.

(5 marks)

(Total for Question Four = 25 marks)

Rationale Part (a) of the question examines candidates’ ability to calculate the net present value of a project involving the identification of relevant costs and the calculation of the effect of inflation and taxation. Part (b) examines candidates’ ability to calculate the IRR of a project. Part (c) examines the candidates’ understanding of the treatment of inflation in investment appraisal. Suggested Approach

• In part (a) firstly identify the incremental cash flows of the project then calculate the tax effect of the cash flows taking account of the timing of the tax payments.

• Discount the resultant net cash flows at the company’s cost of capital. • In part (b) calculate the IRR of the project. • In part (c) calculate the real discount rate which could be applied to cash flows that were not

adjusted for inflation. • Also demonstrate appreciation of the problem involved with this approach where there are tax

implications of the appraisal.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 22

Marking Guide

Marks

Part (a) Current revenue Future projected revenue Incremental revenue Employee costs Overhead costs Adjusting net cash flows for inflation Residual value Tax calculations and phasing of cash flows Discounting cash flows Part (b) Recognising need for an IRR calculation Calculating NPV at higher/lower discount rate Calculating IRR Part (c) Explanation of alternative approach Formula to calculate real cost of capital Calculation of real cost of capital Explanation of problems where taxation is involved

3 marks 2 marks 1 mark 1 mark 1 mark 1 mark 1 mark 4 marks 2 marks 1 mark 2 marks 1 mark 1 mark 1 mark 1 mark Up to 2 marks

Examiner’s comments Part (a) This part of the question was reasonably well answered although many candidates did not seem to recognise that only the incremental revenue was relevant. Similarly many candidates included the absorbed fixed overheads as a relevant cash flow. Most candidates were able to calculate the tax depreciation for years 1-3 but often calculated the balancing figure for year 4 incorrectly. Part (b) Candidates that recognised the need for an IRR calculation scored well in this part of the question but many candidates did not understand what was required. Some candidates gave the answer to part c) instead. Part (c) This part of the question was omitted by many candidates. Those who did attempt it were usually able to give the formula to calculate the real cost of capital but many did not then go on to calculate it. Explanations given for the difficulties in using this method when taxation is involved were vague and did not demonstrate any clear understanding. Common errors Part (a) 1. Failure to calculate incremental revenue. 2. Inclusion of non-relevant costs in the cash flows. 3. Omission of the residual value from the cash flows. 4. Use of 365 days in the calculation of revenue. 5. Incorrect calculation of Year 4 tax depreciation. 6. Incorrect phasing of the benefit from the tax depreciation. Part (b) 1. Failure to recognise the need to calculate the project IRR.

Paper P1 – Performance Operations Post Exam Guide September 2010 Exam

© The Chartered Institute of Management Accountants Page 23

Part (c) 1. Lack of knowledge of the topic area. 2. General statements that did not demonstrate a clear understanding.