geopolitical risks assess the ever-changing challenges handouts/rims 16/emr010/emr010... ·...

TRANSCRIPT

Geopolitical RisksAssess the Ever-Changing Challenges

(SESSION CODE EMR010)

Speakers:

• Eliane Rodrigues Abrantes, Global Risk Manager, Magnesita Refratários S.A.

• Paul Bassett, Managing Director Crisis Management, Arthur J. Gallagher Specialty

• Christof Bentele, Head of Global Crisis Management, Allianz Global Corporate & Specialty

Learning Objectives

At the end of this session, you will:

• Rate the top geopolitical risks that affect your organization’s operations

• Anticipate developments in geopolitical unrest

• Identify insurance industry solutions that help manage geopolitical risks

Europe

• The migrant crisis and terrorism threat present a compounded dilemma for the EU, as both topics are seen to feed into each other.

• The primary concern is that increased migration elevates the terrorism risk as militants are crossing into Europe with legitimate asylum seekers.

• As the 28 member states continue to debate ways in which to address the crisis, at ground level, nationalistic sentiment has reignited latent extremism in individual states, as evidenced by the growing and intensifying anti-immigrant sentiment within some EU states.

• Attacks in Paris and Brussels clearly show the growing terrorist threat in Europe

• There is a risk of disruption in states with pending EU membership. Russia has already done so in Ukraine and may increase agitation in Moldova and Georgia

• Concern about Russian military involvement on the side of Al-Assad

Europe

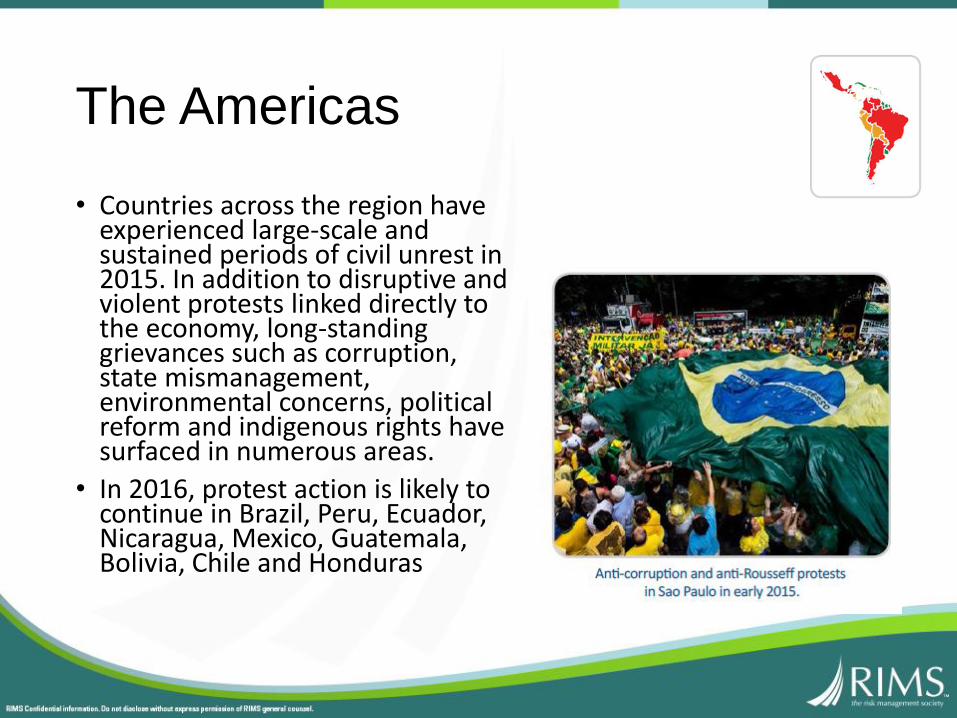

• Countries across the region have experienced large-scale and sustained periods of civil unrest in 2015. In addition to disruptive and violent protests linked directly to the economy, long-standing grievances such as corruption, state mismanagement, environmental concerns, political reform and indigenous rights have surfaced in numerous areas.

• In 2016, protest action is likely to continue in Brazil, Peru, Ecuador, Nicaragua, Mexico, Guatemala, Bolivia, Chile and Honduras

The Americas

• In Ecuador and Bolivia, attempts by the current regimes to extend the term limits of incumbent presidents will likely pass and could serve as the basis for greater political challenges from respective opposition groupings in 2016.

• The impact of these challenges is likely to accelerate should the economic downturn continue.

The Americas

• Number of traditional kidnapping cases is dropping

• Short-term express kidnappings to evolve into a longer-term kidnap for ransom incidents

• Mexico and Venezuela still hotspots in 2016, but Colombia and Brazil catching up due to economic downturn and political instability

The Americas

• Syrian conflict remains the key proxy battleground between Saudi Arabia and Iran, each side seeking to undermine each other

• Sectarian violence increasing and spreading

• Islamic State and the emergence of various IS affiliates or provinces across the region and the globe

MENA

MENA

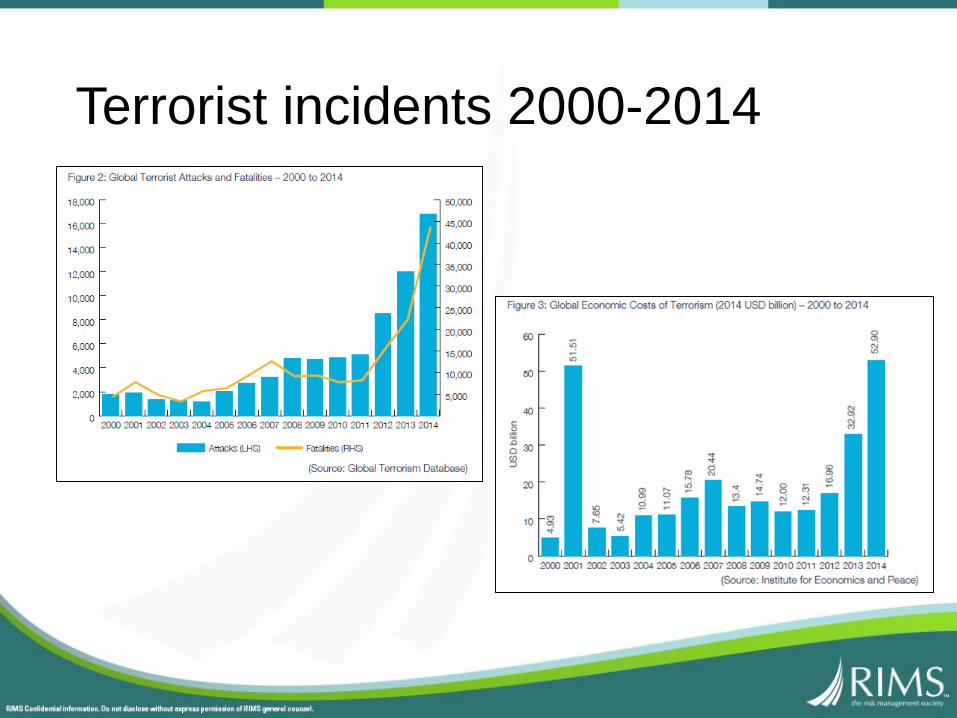

Terrorist incidents 2000-2014

Africa

• Constitutional amendments leading to civil unrest

• Fuelling political instability

• Leading to fertile ‘hunting ground’ for extremist or terrorist groups to recruit followers

Africa

Asia

• Islamic State contagion in Afghanistan and spill over to neighbouring states

• IS-linked groupings in South and South-East Asia

• Accelerated counter terrorism programmes and operations throughout region

• Non-traditional kidnappings on the rise in India, the Philippines, Thailand and Malaysia

Changing Global Terrorism Threat

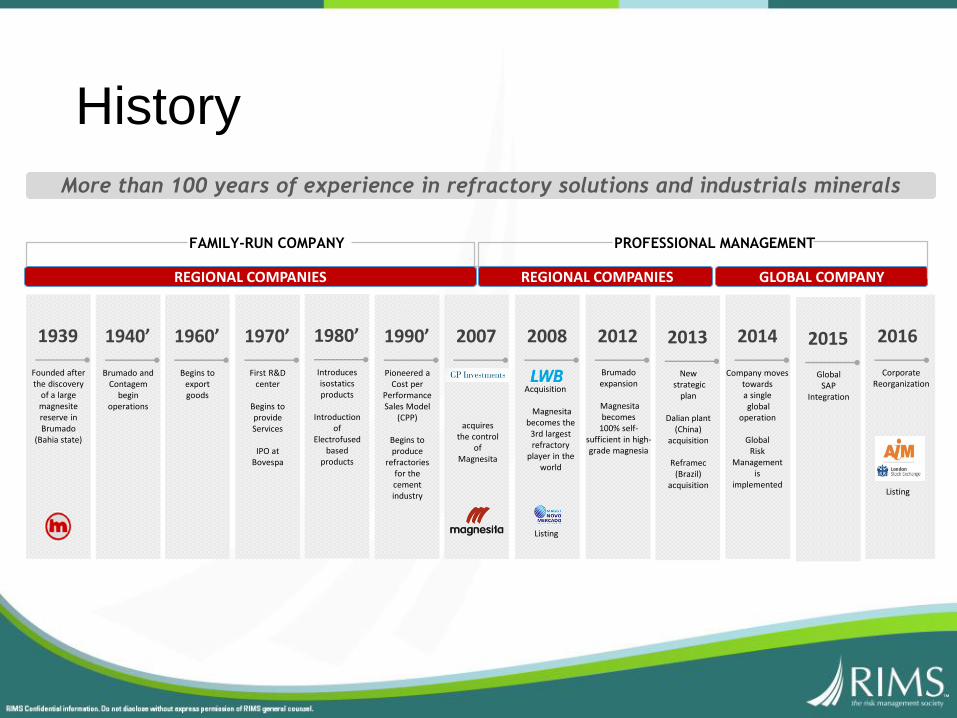

Company Overview

More than 100 years of experience in refractory solutions and industrials minerals

Founded after the discovery

of a large magnesite reserve in Brumado

(Bahia state)

1939

FAMILY-RUN COMPANY PROFESSIONAL MANAGEMENT

REGIONAL COMPANIES REGIONAL COMPANIES GLOBAL COMPANY

Brumado and Contagem

beginoperations

1940’

Begins to export goods

1960’

First R&D center

Begins to provide Services

IPO at Bovespa

1970’

Introduces isostatics products

Introduction of

Electrofused based

products

1980’

Pioneered a Cost per

Performance Sales Model

(CPP)

Begins to produce

refractories for the cement industry

1990’ 2007

acquires the control

of Magnesita

2008

Acquisition

Magnesita becomes the

3rd largest refractory

player in the world

Listing

2012

Brumado expansion

Magnesita becomes

100% self-sufficient in high-grade magnesia

2013

Newstrategic

plan

Dalian plant (China)

acquisition

Reframec (Brazil)

acquisition

2014

Company moves towards a singleglobal

operation

GlobalRisk

Managementis

implemented

2015

Global SAP

Integration

2016

CorporateReorganization

Listing

History

Sales Offices and Sales Representative

Production Units

Mines

Headquarters

Sinterco Dolomite JV (BEL)

Talc Mine (Brumado - BRA)

Magnesite Mine(Brumado – BRA)

Contagem Production Unit (BRA)

York Production Unit (USA)

Hagen-Halden, Oberhausen and Kruft Production Units (DEU)

Dalian Production Unit (CHN)

San NicolásProduction Unit

Valenciennes and Flaumont Production

Units (FRA)

Taiwan JV Production Unit (CHN)

3rd largest refractory producer and the most vertically integrated player in the world

#1 in South America (with 65% market share in steel; 60% in cement)

#1 in dolomite products in North America and Western Europe

Revenues of US$ 1.1 billion in Set/15 LTM¹, with sales to more than 1,000 clients in ~100 countries

Largest and lowest-cost magnesite mine in the world, outside China, with the highest quality magnesite

Global player with 27 facilities in 8 countries representing an annual production capacity of 1.3 million tons

Magnesita at a Glance

19

Global player with a unique footprintLTM=Last Twelve Months

Refractory Industry Overview

Refractories are materials resistant to high

temperatures, consumed in industrial processes

Custom-made products developed according to client

specification (>10,000 SKU’s)

Crucial, but represents only ~3% of COGS in steel

manufacturing and less than 1% in cement

Refractories are consumables: ~10-15Kg per ton of

steel; ~0.6Kg per ton of cement

Raw material are minerals with high melting points.

The main are: magnesite, dolomite and alumina.

Refractories are crucial consumables for high temperatures manufacturing processes

20

Source: The Freedonia Group estimates 2013

~15%Non-ferrous (aluminum,

copper, nickel, silver, zinc)

~10%Other (pulp & paper,

petrochemical, ceramic, other)

Industry overview Main end Markets

~60%Steel

~15%Nonmetallic

(cement, glass, lime)

Types of Refractories

BricksMonolithic

Lin

ing

Ladle bottom

Pre

-cas

tab

le

Flo

w

con

tro

l Valves, slide gates

MiningRefractory

manufacturing

Unique Business Model

21

Cost advantage through vertical integration

Magnesite mine – Brumado, Brazil

Best magnesite mine in the world

One of the largest mines in the world

Dolomite mine – York, USA

Only refractory grade dolomite mine in

N.America

+45 years of reserves

80% vertical integration - highest in the industry

Magnesita is 100% self-sufficient in magnesite and dolomite

Other relevant mines

Dolomite – Belgium (JV);

Dolomite – China

Chromite, clays, pyrophyllite, kyanite – Brazil

Magnesita leverages its competitive advantages throughout the whole value chain

Services Full performance based solution

MiningRefractory

manufacturing

22

Competitive advantage through a distinctive service offering with focus on client performance

Magnesita leverages its competitive advantages throughout the whole value chain

Services Full performance based solution

Cost per performance “CPP”: A win-win model3 levels of service

Clients

Reduced downtime

Lower refractory

consumption

Lower energy and other

raw materials consumption

Higher productivity

Magnesita

Higher market share

Higher client loyalty

Lower competition

Longer contracts

Tech. Assistance

- High level technical training team

- Development of high performance products

- Tailor-made performance-based applied R&D

Other Services

- Installation

- Maintenance

- Recycling

- Engineering

CPP

- On-site technical support- Customized solutions- Enhancement of clients’ productivity

Focus on client performance

Unique Business Model

Vertically integrated low-cost producer

Continuous investments in R&D and technology

Specialized technical assistance

Logistic advantages derived from strategic locations

Captive CPP contracts with long-term alignment of

interests

Brand recognition and historical leadership

Long standing relationship with blue-chip customers

Sustained Leadership in Established Markets

South America

Dolomite products in

North America

Dolomite products in Western Europe

Magnesita’s Top blue-chip customers

~50% in stainless steel~25% in mini-mills

~25% in cement

Market share in established markets¹

~60% in stainless steel~15% in mini-mills

~65% in steel~60% in cement

¹Company estimates

23

Competitive advantages

Magnesita’s unmatched competitive advantages ensure its leadership in established markets

Attractive Opportunity in Selected Growth Markets

Pursue long term growth opportunities in select markets where we can deliver superior value

24

Estimated refractory market size¹ (in USD)

Integrated steel

mills:~USD700 mln

USASteel:~USD 430 mln

Eastern Europe + CIS (ex-Russia)

Addressable markets are ~4x to 5x larger than Magnesita’s established markets

Steel:~USD270

mln

Cement:~USD40

mln

Mexico

Steel:~USD130mlnCement:~USD80 mln

LatAm ex-Brazil

Steel:~USD 2.2 bln

Cement: ~USD280 mln

Asia + Oceania (ex-China & Japan)

Steel: ~USD 800 mln

Cement: USD80 mln

Middle East & Africa

~USD 200 mln

Global non-ferrousmarket

Government

Interference

Political Risk & PRI

Captives

[may include:

Expropriation

Political Violence

Currency Inconvertibility

Sovereign Default

& other specific perils]

Contract Frustration (for trade transactions)

Confiscation Insurance (mobile assets)

Investment Risk Insurance (fixed assets/ equity

interest & Lenders’ Form)

Security Risks

Political Violence (inc. Terrorism, War/Civil War, Riots,

Property Damage and Business Interruption)

Kidnap & Ransom

The insurance market can help investors, traders and financiers with bespoke insurance

solutions which support international trade and investment

Off-the-shelf and Bespoke Insurance Solutions

Off the Shelf Bespoke - Trends

Government Action/Inaction PRI products : may include:

Expropriation

Political Violence

Currency Inconvertibility

Sovereign Default

Arbitration Award Default

& other specific perils

Variations of Off the Shelf

Specific to sector

Specific to Stakeholders’ concerns

Specific to host country Systemic risks

Captives

Security Risk Kidnap & Ransom Terrorism & Political

Violence (war, civil war, insurrection riots,

strikes, civil commotion, terrorism, sabotage,

vandalism etc.)

Variations of Off the Shelf

Family Extensions

Key Man

Contagion Risk

Supply Chain Risks

Urban Violence

Balance Sheet Protection

P & L protection

BI & Contingent BI protection

Large Self Insured Retentions

Captives

Contract Risk Credit Insurance, Contract Frustration, Non-

Honoring Arbitration Award

Variations of Off the Shelf

Large Self Insured Retentions

Specific to Arbitration Laws & Venue

Home court advantage? Not always.

Off-the-shelf and Bespoke Insurance Solutions

We may be operating in one of the most volatile global risk environments seen in decades, but the Credit & Political Risk insurance market is expanding…

• Active public sector coupled with a growing commercial global market for class especially in Lloyd’s.

• The market is maturing post-financial crisis and new participants joined in 2014; increasing to over 50 specialist (re)insurers.

• The market’s reliability was robustly proven during the financial crisis.

• Soft market conditions set to continue as more capital enters the market.

• The number of enquiries from established users and new buyers increases as Political Risk Insurance (PRI) risks hit the headlines.

The CPS Market

Evolution of the Market

The Private Insurance Market

• Approximately 50 private insurers in the market, largely London based, to write Political and Structured Credit Risk, able to accept risk on a stand-alone or subscription / syndicated basis.

• The market is now bigger than at any time before - theoretical capacity now in excess of USD 2bn for some risks.

Tenor

Potential Private Market Capacity

Contract Frustration (USDm)Comprehensive Credit

(USDm)Political Risks (USDm)

Up to 1 year approx. 2,239 approx. 1,877 approx. 2,370

1 to 3 years approx. 2,289 approx. 1,824 approx. 2,370

3 to 5 years approx. 2,263 approx. 1,470 approx. 2,350

5 to 7 years approx. 1,948 approx. 1,163 approx. 2,040

7 to 10 years approx. 1,462 approx. 502 approx. 1,625

10 to 15 years approx. 750 approx. 50 approx. 800

Growth of Market; Capacity

• Obtain consulting services that utilize their own analysis and robust technology.

• Focus on understanding risk. Obtain expertise in quantifying and qualifying political risk, political violence, cyber risk, kidnap and travel safety.

• Look for ground-breaking modelling and rating tools, consultants should help clients anticipate, prevent, respond and where necessary recover from a crisis.

Quantifying and Qualifying Risk

• Clients should use a system to alert employees both up and down communication cascades from C-Suite to local teams, or vice versa.

• Clients can also use a system’s communications logging tool to keep all relevant decision-makers informed and restrict access where appropriate. User groups can be set up in advance to restrict access where appropriate. Where applicable, employees should receive the system’s email and SMS alerts, or be able to ‘reply’ back to the system.

* Consultant should help migrate your existing Crisis Management plans onto technology, to create clear crisis workflows before an incident occurs.

Incident and Crisis Management

The role of the broker is not to sell insurance, but to add value to clients’ operations through our knowledge, in maximising efficiency and continually evolving new and innovative solutions to manage and distribute risk.

1. Analysis: standalone Analytics & Consultancy team can deliver on-demand support and solutions to help identify, understand and mitigate risks to contracts, assets and personnel.

2. Broking: transactional analysis and management of individual contracts or project requirements for credit and political risk insurance.

3. Claims and Recoveries: ensuring timely payment by insurers and that our clients’ commercial interests are best addressed in any recovery action.

Objective is to become a long-term, strategic partner; to understand, structure and distribute clients’ risks into the insurance market and to build client ‘brands’ in the market over time.

A Broker and Consultant’s Job

• To protect balance sheets when trading in high risk / high reward territories.

• To allow expansion of business into a spread of new emerging markets while offsetting the higher country risk with first class insurers.

• To obtain finance from banks, allowing the banks to leverage their participation on the back of Basel II/III compliant insurance covering political risk and non payment/default by the obligor.

• Allows Export Credit Agencies to continue to write large and complex risks.

• To reduce the overall cost of finance / funds using the insurance as security.

• Removal of entry barriers.

• Increase of confidence.

Why use Credit and Political Risks Insurance

• Protection of physical assets due to deteriorating security environment and political acts.

• Comprehensive, non-cancellable coverage as opposed to ‘add on’ within all risks policy.

• To meet lender requirements and secure financial backing for a project.

• Should a claim occur, a comprehensive PV program will cause less opportunity for underwriters to query a loss on account of definitions.

• We can arrange custom built Delay in Start-Up (DSU) / BI coverage for principals and banks for Construction projects.

Why use Political Violence Insurance

• Applicable to:• Any business with employees who travel internationally

• Tailored policy wording• Policies can be tailored to meet the needs of businesses or

individuals / families

• Named perils include• Kidnap (incl. Express Kidnap)

• Unlimited coverage for dedicated response consultants

• Extortion (incl. Product Extortion)

• Illegal detention

• Hijack

• Disappearance

• Hostage crisis

• Optional extensions include: emergency political repatriation, express threat, loss of earnings

• Tenor can be up to 5 years• Cover can also be trip or project specific

Kidnap & Ransom (K&R) Insurance

• Duty of Care / Corporate Governance- There is an increased obligation now for companies to address this issue.

• Protection against corporate reputational damage

• Risks in any country can change overnight and therefore a company has to be well equipped to respond to unforeseen security incidents. Pre-incident planning, country risk & resilience reviews as well as employee/ expat travel tracker can mitigate the impact of such risks.

• Increased criminal and ideological threat around the world- any representative of a company, be it director or employee, can become a target.

• Increased complexity of incidents around the world e.g. sanctions. We are equipped to deal with such complexities and have experience in handling sensitive issues such as these.

• Access to experienced response consultants paid for by Insurers who can assist and advise the company and victim’s family. The response team will remain on the case until they secure the safe and timely release of the victim.

• Between 10-20% of the annual premium can be contributed towards the services of the consultants or information services to assist in risk mitigation.

37

Why use K&R Insurance