geordan murray - housing industry australia - what are the opportunities in building and...

TRANSCRIPT

What are the opportunities in

building and construction?Geordan Murray, HIA Economist

PVC Australia ConferenceMelbourne, May 2016

Global economic conditions

• World economic recovery has stumbled a bit – particularly emerging markets

• The collapse in oil prices has hurt some – but benefitted most

• US interest rates increased late last year and may move again soon

• China risks still weigh most heavily on Australia

• Several geopolitical risks

– ‘Brexit’ vote in June

– Syrian refugee migration to Europe

– President Trump?

• The shadow of debt still looms large globally

Australia’s economy

• GDP grew surprisingly quickly during the final quarter of 2015

– Growth drivers: Household consumption, residential building

– Growth detractor: Engineering construction

• Inflationary pressures are very muted

• The door is open for a further rate cut

• The weaker Australian dollar is making the economy’s traded sectors more

competitive – mining output, but also tourism, education and high skill services

• Residential building is propping growth up…

• …but non-residential construction is still relatively weak

More new homes than ever before

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Num

ber

Total Dwelling Starts – AustraliaSource: ABS 8752

Seasonally Adjusted Trend

The mix of dwelling types has changed

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Dec

-198

6

Dec

-198

7

Dec

-198

8

Dec

-198

9

Dec

-199

0

Dec

-199

1

Dec

-199

2

Dec

-199

3

Dec

-199

4

Dec

-199

5

Dec

-199

6

Dec

-199

7

Dec

-199

8

Dec

-199

9

Dec

-200

0

Dec

-200

1

Dec

-200

2

Dec

-200

3

Dec

-200

4

Dec

-200

5

Dec

-200

6

Dec

-200

7

Dec

-200

8

Dec

-200

9

Dec

-201

0

Dec

-201

1

Dec

-201

2

Dec

-201

3

Dec

-201

4

Dec

-201

5

Mov

ing

Ann

ual T

otal

Dwelling Commencements and Long Term Trends Source: HIA Economics, ABS

Other dwellings (MAT) Detached dwellings (MAT) Other dwellings (long term trend) Detached dwellings (long term trend)

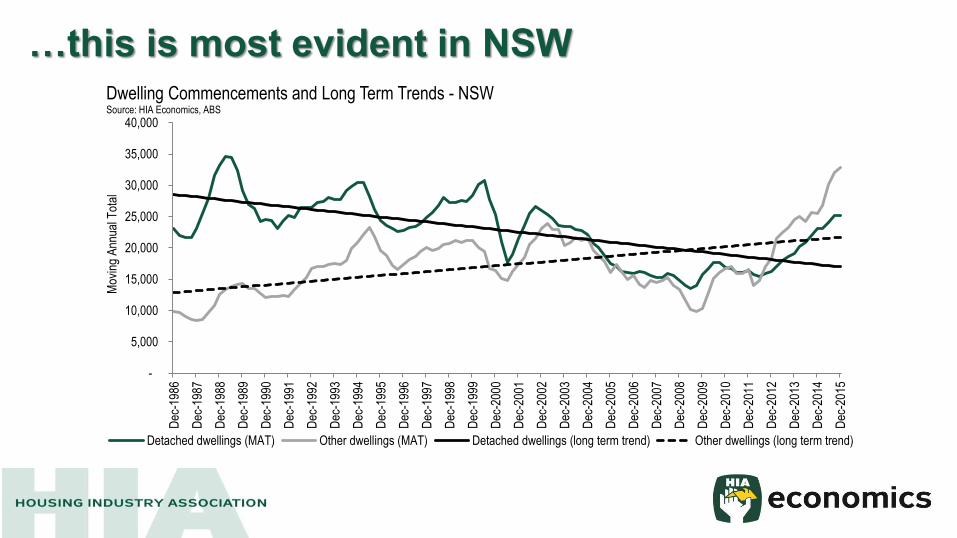

…this is most evident in NSW

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Dec

-198

6

Dec

-198

7

Dec

-198

8

Dec

-198

9

Dec

-199

0

Dec

-199

1

Dec

-199

2

Dec

-199

3

Dec

-199

4

Dec

-199

5

Dec

-199

6

Dec

-199

7

Dec

-199

8

Dec

-199

9

Dec

-200

0

Dec

-200

1

Dec

-200

2

Dec

-200

3

Dec

-200

4

Dec

-200

5

Dec

-200

6

Dec

-200

7

Dec

-200

8

Dec

-200

9

Dec

-201

0

Dec

-201

1

Dec

-201

2

Dec

-201

3

Dec

-201

4

Dec

-201

5

Mov

ing

Ann

ual T

otal

Dwelling Commencements and Long Term Trends - NSWSource: HIA Economics, ABS

Detached dwellings (MAT) Other dwellings (MAT) Detached dwellings (long term trend) Other dwellings (long term trend)

There is a loaded pipeline of multi-unit activity

-

20,000

40,000

60,000

80,000

100,000

120,000

-

5,000

10,000

15,000

20,000

25,000

Mar

-05

Mar

-06

Mar

-07

Mar

-08

Mar

-09

Mar

-10

Mar

-11

Mar

-12

Mar

-13

Mar

-14

Mar

-15

Mar

-16

Snapshot of the Building Activity Pipeline - Flats, units and apartmentsSource: HIA Economics, ABS 8752.0, ABS 8731.0

Under construction (RHS) Approved (1 month lag) Commenced Completed

…and there are more waiting in the wings

-

5,000

10,000

15,000

20,000

25,000

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

Dec

-12

Dec

-13

Dec

-14

Dec

-15

Dwellings Approved but Not Yet CommencedSource: HIA Economics, ABS

Houses Semi-detached, row or terrace houses, townhouses Flats units or apartments

Key risks for residential building:

Key risks for residential building:

– Interest rates

– Labour market

– Foreign investment

– Population growth

– Settlement risk

– Tax ‘reform’

– External shock

What are the possibilities?

187.1 181.3

220.0

174.8

160.8

145.0

114.0

100

120

140

160

180

200

220

240

1994 Peak 2013/14 Level 2015 Record Peak Moderate Cycle Average Cycle Shock Cycle Major Shock

Cyclical Peaks Potential Cyclical Troughs

Dw

ellin

g st

arts

('0

00)

The New Home Building CycleSource: HIA Economics; ABS 8752.0

Outlook for residential building

93.0

115.

8

100.

5

89.6 93

.4

104.

9 113.

9

111.

8

104.

0

97.2

39.6

56.8 61

.9

55.4

69.5 76

.3

100.

4

104.

3

84.9

67.0

0

20

40

60

80

100

120

140

2008/09 (a) 2009/10 (a) 2010/11 (a) 2011/12 (a) 2012/13 (a) 2013/14 (a) 2014/15 (a) 2015/16 2016/17 2017/18

Dw

ellin

g st

arts

('0

00)

Dwelling Commencements Forecast by Dwelling TypeSource: HIA Economics

Detached Houses Multi-unit dwellings

Forecast

Residential building forecasts

Basic forecasts are freely available from the HIA website

– By state

– Detached house, other dwellings, and renovations

– Number of dwellings and value of work

– Five year forecast horizon

Detailed forecasts are available via subscription

– Sub-state regional markets

– Disaggregated across six different dwelling types

– Longer term projections

– Customised forecasts by request

Please contact [email protected] or visit www.hia.com.au

Australian Construction Insights

Australian Construction Insights (ACI) - powered by HIA Economics, is the most reliable place to obtain market research and forecasts, in-depth analysis, and expert presentations regarding the Building and Construction Industry.

ACI is backed by a wealth of experience through our expert team of economists. ACI produces comprehensive and unique insights into the construction industry which can be tailored to your organisation’s needs.

• Specialists in all components of Australia’s construction industry

• Forecasting

• Market Research

• In Depth Analysis

Please contact [email protected] or visit www.aciresearch.com.au

Non-residential building work is easing

0

5,000

10,000

15,000

20,000

25,000

30,000

Jun-

2006

Sep

-200

6

Dec

-200

6

Mar

-200

7

Jun-

2007

Sep

-200

7

Dec

-200

7

Mar

-200

8

Jun-

2008

Sep

-200

8

Dec

-200

8

Mar

-200

9

Jun-

2009

Sep

-200

9

Dec

-200

9

Mar

-201

0

Jun-

2010

Sep

-201

0

Dec

-201

0

Mar

-201

1

Jun-

2011

Sep

-201

1

Dec

-201

1

Mar

-201

2

Jun-

2012

Sep

-201

2

Dec

-201

2

Mar

-201

3

Jun-

2013

Sep

-201

3

Dec

-201

3

Mar

-201

4

Jun-

2014

Sep

-201

4

Dec

-201

4

Mar

-201

5

Jun-

2015

Sep

-201

5

Dec

-201

5

Mar

-201

6

$ m

illio

ns

Work yet to be done Work approved Work done Work commenced

TOTAL NON-RESIDENTIAL BUILDING WORK

Sou

rce:

AC

I, A

BS

873

1.0,

875

2.0

…but not across all sectors

Strengthening:– Factories and other secondary production buildings

– Agricultural and aquacultural buildings

– Entertainment and recreation buildings

– Short term accommodation buildings

– Aged care buildings

Neutral:– Offices

– Retail and wholesale trade buildings

– Health buildings

– Education buildings

– Warehouses

Weakening:– Transport buildings

Engineering work post mining boom

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Dec

200

5

Mar

200

6

Jun

2006

Sep

200

6

Dec

200

6

Mar

200

7

Jun

2007

Sep

200

7

Dec

200

7

Mar

200

8

Jun

2008

Sep

200

8

Dec

200

8

Mar

200

9

Jun

2009

Sep

200

9

Dec

200

9

Mar

201

0

Jun

2010

Sep

201

0

Dec

201

0

Mar

201

1

Jun

2011

Sep

201

1

Dec

201

1

Mar

201

2

Jun

2012

Sep

201

2

Dec

201

2

Mar

201

3

Jun

2013

Sep

201

3

Dec

201

3

Mar

201

4

Jun

2014

Sep

201

4

Dec

201

4

Mar

201

5

Jun

2015

Sep

201

5

Dec

201

5

Value of work yet to be done Value of work done Value of work commenced

LABOUR MARKET CONDITIONS - AUS

Sou

rce:

AC

I, A

BS

876

2

TOTAL ENGINEERING CONSTRUCTION $

mill

ions

…but it isn’t all negative

Strengthening:

– Roads, highways and subdivisions

Neutral:

– Water storage and supply, sewerage and drainage

– Telecommunications

Weakening:

– Heavy industry

– Bridges, railways and harbours

– Electricity generation, transmission etc. and pipelines

– Recreation and other

Outlook for non-res and engineering

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2005/0

6 (

a)

2006/0

7 (

a)

2007/0

8 (

a)

2008/0

9 (

a)

2009/1

0 (

a)

2010/1

1 (

a)

2011/1

2 (

a)

2012/1

3 (

a)

2013/1

4 (

a)

2014/1

5 (

a)

2015/1

6

2016/1

7

2017/1

8

va

lue o

f w

ork

don

e (

$m

illio

n)

Engineering construction Non-residential building Total

AUSTRALIAN CONSTRUCTION ACTIVITY OUTLOOK

Source: ACI

Forecast

Summing up

• Household consumption has driven growth

…partly attributable to the wealth effect of rising home prices;

• The peak of the residential building cycle is here;

• We are well into the post-peak contraction in mining investment;

• Non-mining engineering construction demand should be bolstered by public

infrastructure investment;

• Non-mining business investment remains at an ebb;

• In time we’ll see business investment return and this will reignite the latent

sectors of non-residential building construction.

THANK YOU FOR YOUR TIME

Geordan Murray, HIA Economist

economics.hia.com.au