getting started with planned giving

TRANSCRIPT

Getting Started With Planned Giving

6/25/15 1pm Eastern

The presentation will begin shortly.

Before We Get Started3

This presentation is being recorded!

The recording and slides will be emailed to you later this afternoon.

Please chat in any questions for our guest. We will answer them in the formal Q&A session

at the end of the presentation.

3

3

Our guest presenter »Judi Smith, MA, CFRE

Judi Smith, MA, CFRE, caps a career of more than three decades in development by working with the Arizona Community Foundation in Sedona as a Regional Senior Philanthropic Advisor. She has been an independent consultant to nonprofits, an executive director and staff leader in higher education, arts organizations, and a national foundation. A sought-after speaker and trainer, Judi considers teaching others about topics in our field to be a special talent. A huge believer in planned giving and endowments, Judi loves to talk with individual donors and nonprofits about the planned gifts that build secure futures for nonprofit missions.

GETTING STARTED WITH PLANNED GIVING A WEBINAR FOR BLOOMERANG

JUDI SMITH, MA, CFRE

THE PRO’S AND CON’S OF STARTING PLANNED GIVING

PRO’S

• Positions your organization for the future

• Invites donors to consider significant gifts

• May offer donors income, capital gains, or estate tax advantages

• Creates opportunities to build endowment

• Creates opportunities for planning professionals to affiliate with your organization

• Receiving larger gifts advances your mission and the programs that support it.

PRO’S

• Great opportunity for planned giving

• About 2/3 of Americans have a will or trust

• Less than 10% age 55+ have a charitable bequest

• 2007 Campbell & Company study

• 1 in 3 would consider a charitable bequest if asked

• Intergenerational wealth transfer

• 10,000 Americans turn 65 every day for the next few years

CON’S

• Like any fundraising program, it costs money and takes time.

• Depending upon how deeply you dive, there can be lots to

learn.

• Documentation and paperwork is more stringent than for cash

gifts.

• You should maintain currency with legislation that affects

charitable taxation opportunities.

CON’S

• The type of organization you are may be a detriment

• New organization (not affiliated with a long-established organization)

• An organization that derives most of its funding from government

sources

IF YOU DECIDE TO GO FOR IT, WHAT IS “IT”?

PLANNED GIFTS TO PROMOTE FOR A NEW PROGRAM: BEQUESTS

• Bequest giving

• Consistently about 8% of gift dollars given

• Consistently about 75% of all planned gifts

If you do nothing else, ask your closest friends

to remember you in their will or trust.

MORE ON BEQUESTS

• Remember that bequests can be

• Specific – amount or asset

• Percentage of the estate after bills are paid and specific bequests made

• Remainder

• Contingent

PLANNED GIFTS TO PROMOTE FOR A NEW PROGRAM: BENEFICIARY DESIGNATIONS

• Beneficiary Designations

• Assets that transfer at death

• Usually by a simple form obtained by the custodian of the asset

• Can be the entire final balance or a percentage of the final balance

• Examples

• Life insurance policies

• Pension accounts

PLANNED GIFTS TO PROMOTE FOR A NEW PROGRAM CHARITABLE LIFE INSURANCE

• Charitable Life Insurance -- some thoughts

• Better to let donors work with their own agents rather than to adopt a

program from one company trying to sell your donors

• You will probably want to accept as gifts only policies that build and

maintain cash value.

• However, for recognition purposes, you could choose to recognize term life.

• Be aware that the PPA 2006 requires appraisal standards for life insurance

gifts

• Excellent guideline for evaluating charitable life insurance from PPP

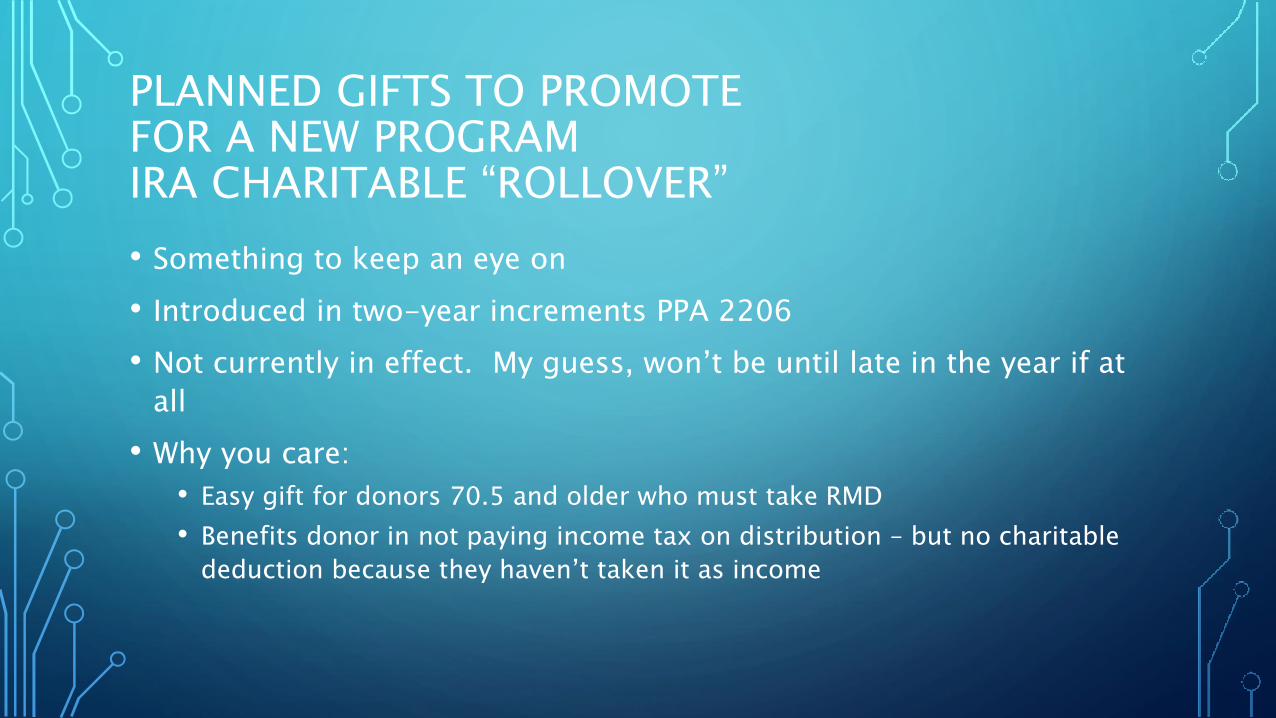

PLANNED GIFTS TO PROMOTE FOR A NEW PROGRAM IRA CHARITABLE “ROLLOVER”

• Something to keep an eye on

• Introduced in two-year increments PPA 2206

• Not currently in effect. My guess, won’t be until late in the year if at

all

• Why you care:

• Easy gift for donors 70.5 and older who must take RMD

• Benefits donor in not paying income tax on distribution – but no charitable

deduction because they haven’t taken it as income

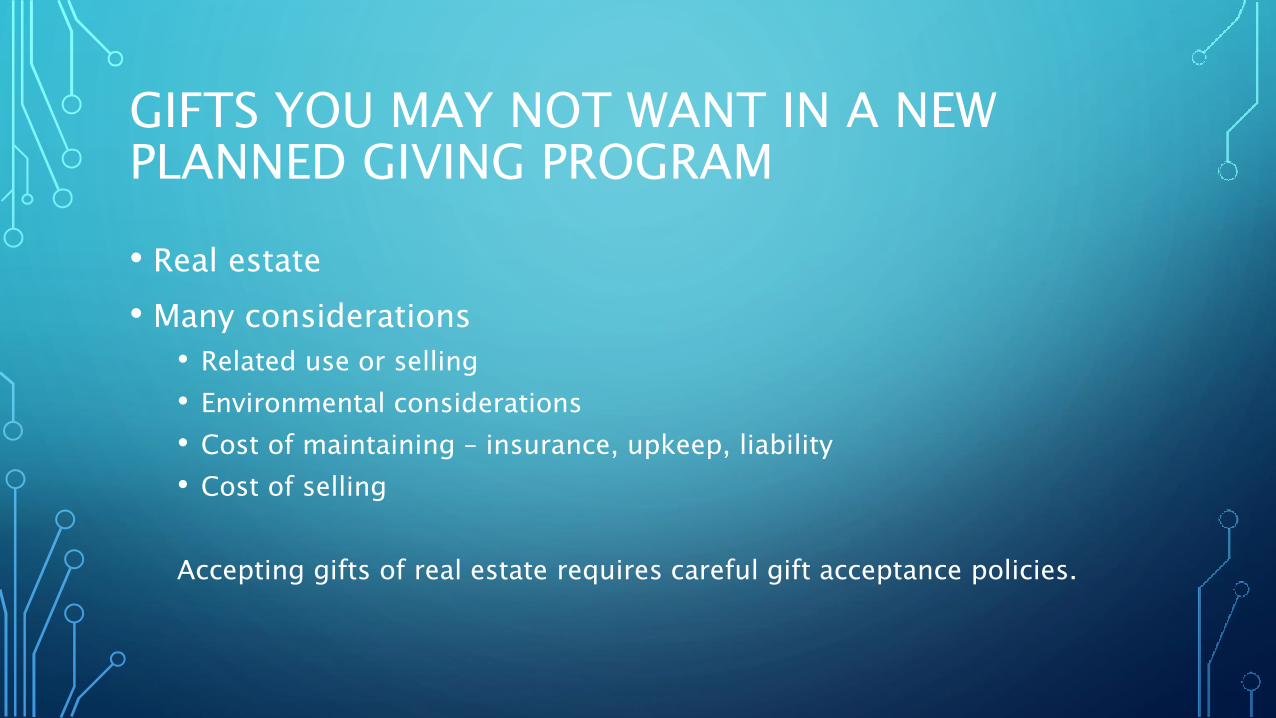

GIFTS YOU MAY NOT WANT IN A NEW PLANNED GIVING PROGRAM

• Real estate

• Many considerations

• Related use or selling

• Environmental considerations

• Cost of maintaining – insurance, upkeep, liability

• Cost of selling

Accepting gifts of real estate requires careful gift acceptance policies.

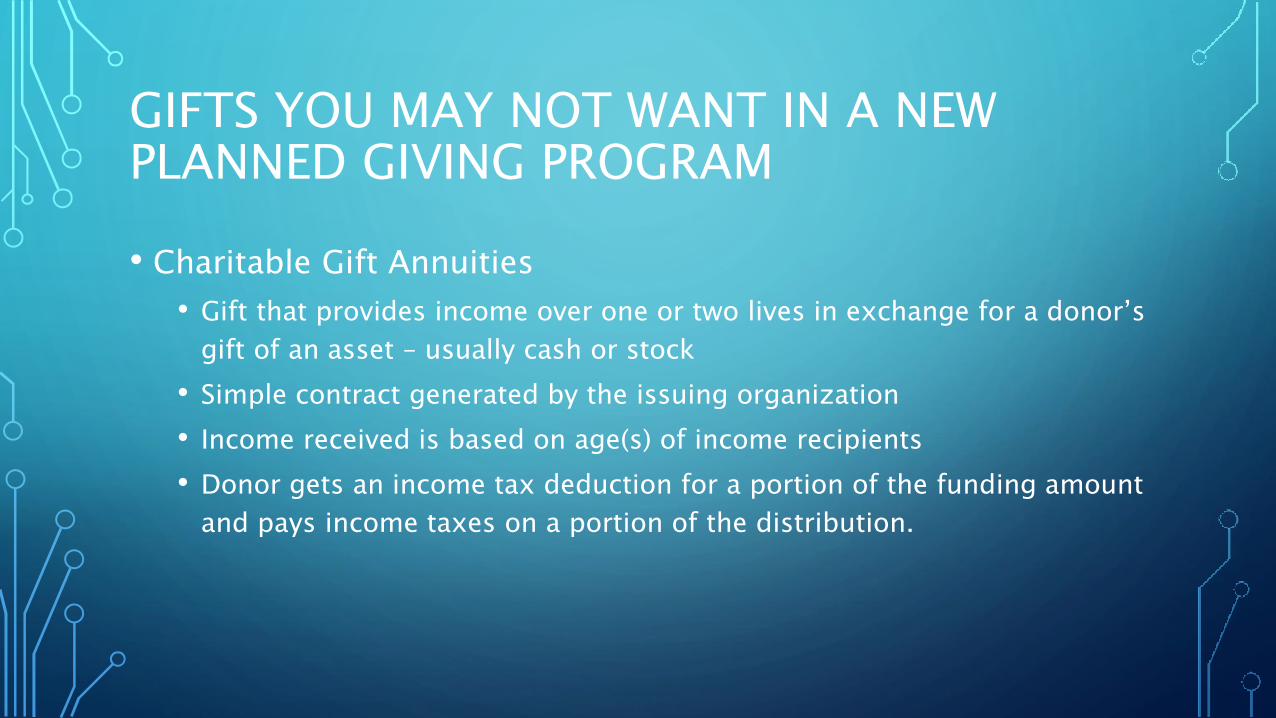

GIFTS YOU MAY NOT WANT IN A NEW PLANNED GIVING PROGRAM

• Charitable Gift Annuities

• Gift that provides income over one or two lives in exchange for a donor’s

gift of an asset – usually cash or stock

• Simple contract generated by the issuing organization

• Income received is based on age(s) of income recipients

• Donor gets an income tax deduction for a portion of the funding amount

and pays income taxes on a portion of the distribution.

GIFTS YOU MAY NOT WANT IN A NEW PLANNED GIVING PROGRAM

• Charitable Gift Annuities – Some important considerations

• Some state regulations are onerous

• All assets of the issuing charity are pledged to support annuities

• Will need software or a contractor

• There are investment considerations

• Great for repeat gifts

• Many donors are women

• Great resource: www.acga-web.org

RECAP OF POSSIBLE GIFTS

• Relatively easy to facilitate:

• Bequests

• Payable on Death transfers

• Life Insurance (some caveats)

• Requires more stringent oversight and involvement:

• Real estate

• Charitable Gift Annuities

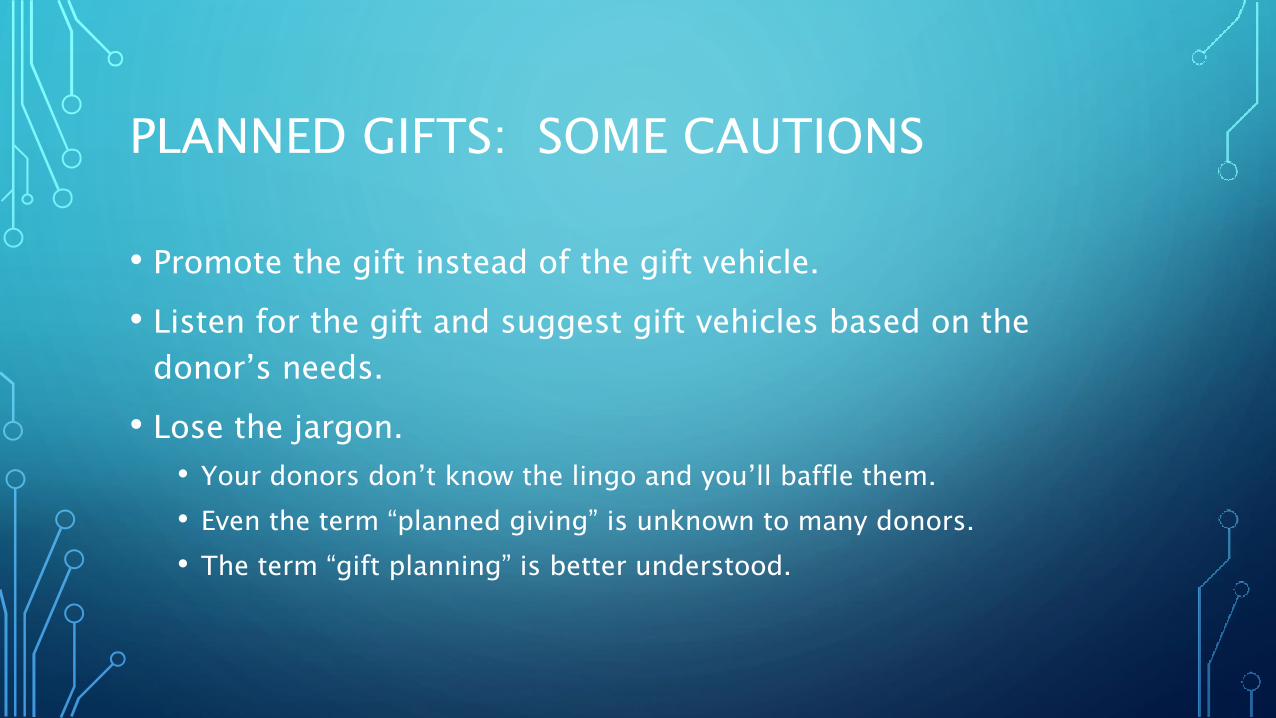

PLANNED GIFTS: SOME CAUTIONS

• Promote the gift instead of the gift vehicle.

• Listen for the gift and suggest gift vehicles based on the

donor’s needs.

• Lose the jargon.

• Your donors don’t know the lingo and you’ll baffle them.

• Even the term “planned giving” is unknown to many donors.

• The term “gift planning” is better understood.

WHO ARE YOUR POTENTIAL PLANNED GIFT DONORS?

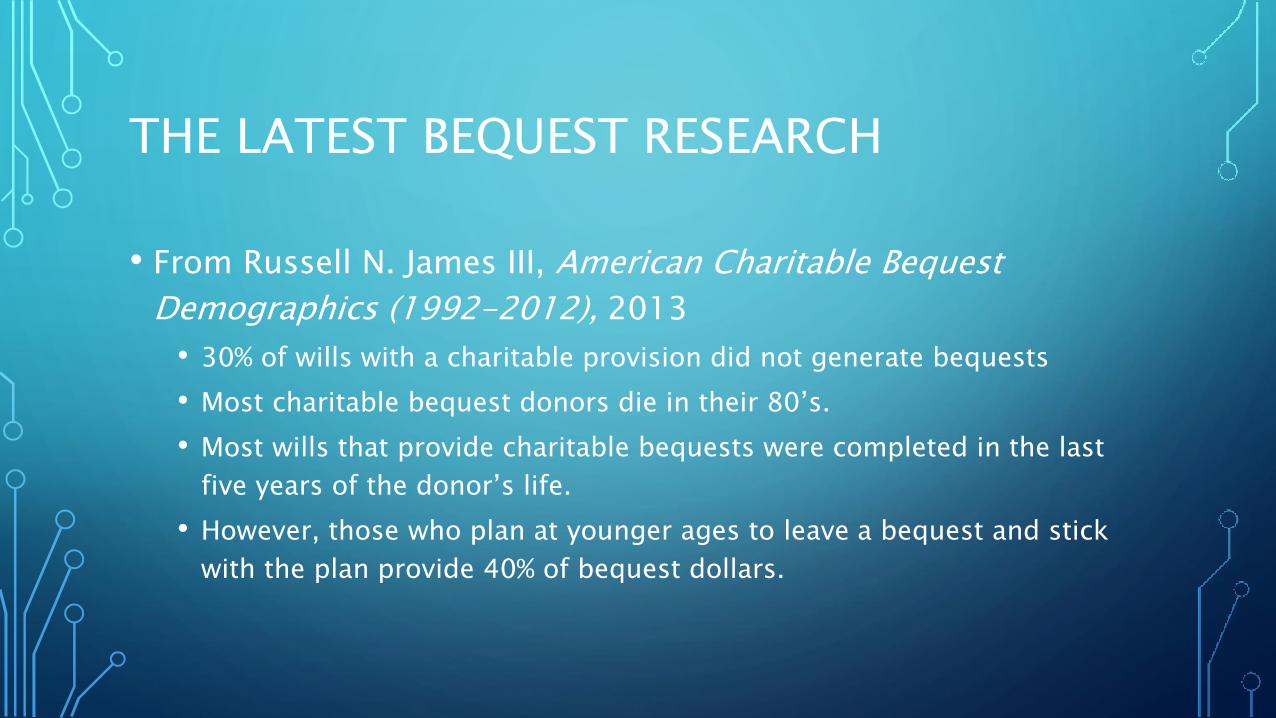

THE LATEST BEQUEST RESEARCH

• From Russell N. James III, American Charitable Bequest

Demographics (1992-2012), 2013

• 30% of wills with a charitable provision did not generate bequests

• Most charitable bequest donors die in their 80’s.

• Most wills that provide charitable bequests were completed in the last

five years of the donor’s life.

• However, those who plan at younger ages to leave a bequest and stick

with the plan provide 40% of bequest dollars.

MORE RUSSELL JAMES

• Once a charitable estate provision has been made, 55% retain

the charitable provision over time.

• An older age at death and having no surviving spouse is

associated with larger bequests.

• 2/3 by number

• 71% by dollar amount

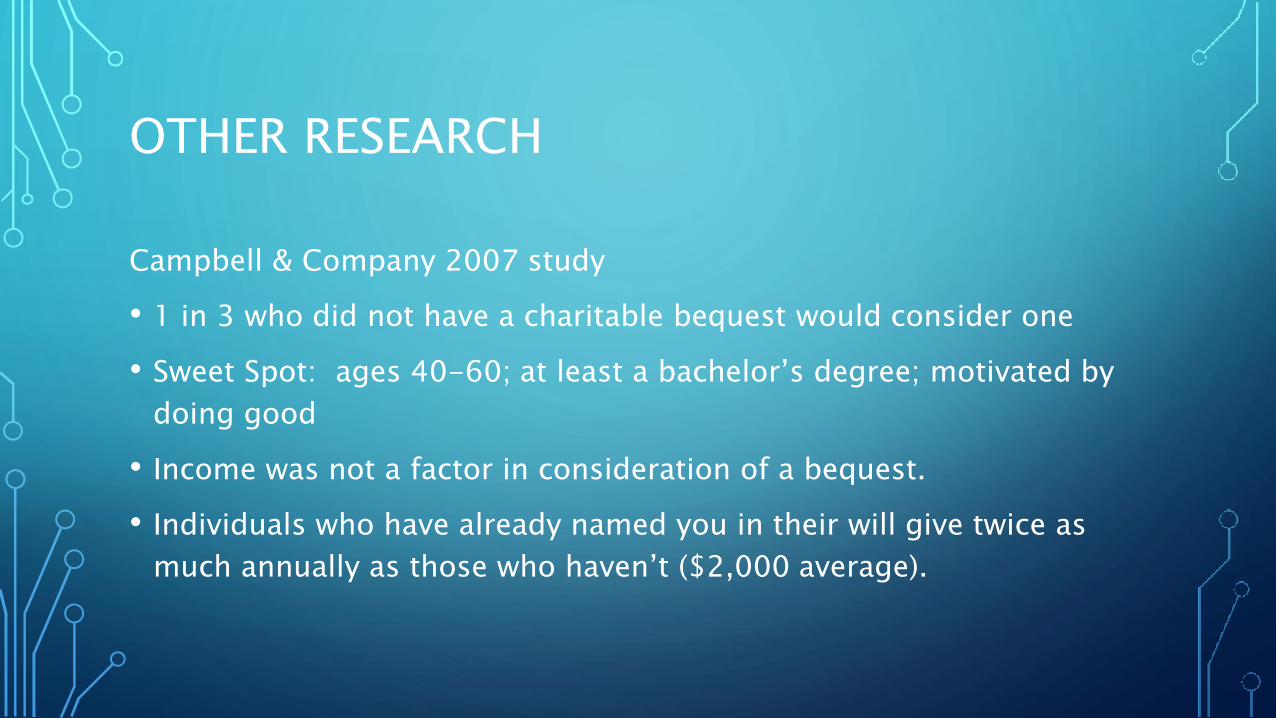

OTHER RESEARCH

Campbell & Company 2007 study

• 1 in 3 who did not have a charitable bequest would consider one

• Sweet Spot: ages 40-60; at least a bachelor’s degree; motivated by

doing good

• Income was not a factor in consideration of a bequest.

• Individuals who have already named you in their will give twice as

much annually as those who haven’t ($2,000 average).

FREQUENCYregular smaller

SINGLE widowed Volunteer 9.4%

Single Volunteer

Childless 10,000 attend

college educated longtime

Relationship Loyalty 78 FREQUENCY

$500 annual gift regular smaller gifts

Will/Trust/POD 9.4%

CONVENTIONAL WISDOM

• It’s not the size of the gift.

• It’s not necessarily the recency of the gift.

• It’s the frequency of giving.

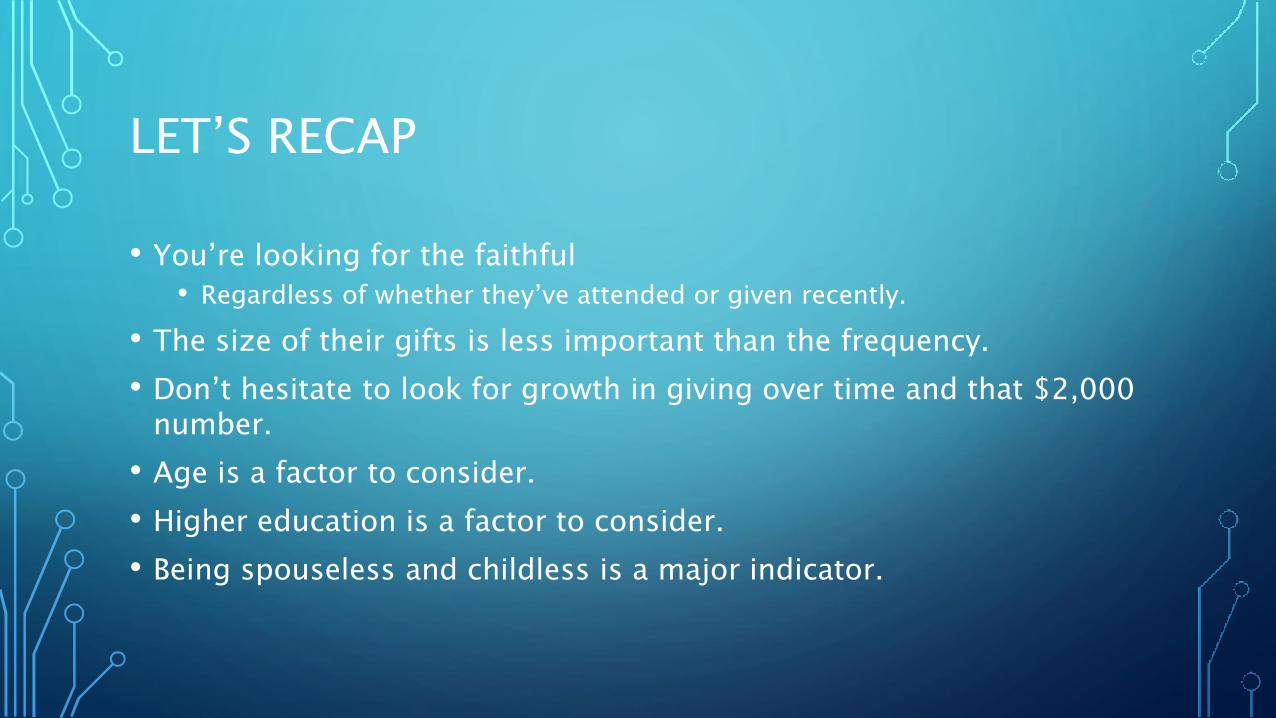

LET’S RECAP

• You’re looking for the faithful

• Regardless of whether they’ve attended or given recently.

• The size of their gifts is less important than the frequency.

• Don’t hesitate to look for growth in giving over time and that $2,000 number.

• Age is a factor to consider.

• Higher education is a factor to consider.

• Being spouseless and childless is a major indicator.

GETTING STARTED

INTERNAL PROCESSES

• ED / CEO must be on board with you. A planned giving

program will touch every facet of your operation.

• Update gift acceptance policies.

• Talk with your finance team or auditor about appropriate

booking and investing of planned gifts.

• Learn what your software will allow you to track and set

procedures for tracking planned gifts.

INTERNAL PROCESSES

• Your public relations team will need to help promote the

program on the website, in newsletters, in specialized

communication.

• Your receptionist must be prepared to appropriately direct

calls.

INTERNAL PROCESSES

• Determine your budget

• There is a plethora of existing off-the-shelf material

• Customized websites

• Customizable brochures and newsletters

• Utilize existing staff or hire a specialist?

• In 2012 the mean salary for a planned giving officer was $90,166

• Expect to add $ for CFRE, JD, years of experience, years with the org

• Other factors – area of the country; metropolitan vs. rural

INTERNAL PROCESSES

• Other budgetary considerations

• Attend to continuing professional education for appropriate staff

• Membership in the Partnership for Philanthropic Planning and local or

regional planned giving and/or estate planning councils

• Allocate funds for travel, even if it’s mostly local, there is still mileage

and entertaining.

• Provide planned giving staff the technological resources they need to do

their jobs, from the laptop to necessary software to remote access to

your database.

INTERNAL TO EXTERNAL

• Follow your approval process to begin involving volunteers.

• Board should be invited to become charter members of your

legacy or heritage society

• Possible names

• Qualifying gifts

• Documentation

• Benefits

INTERNAL TO EXTERNAL

• Professional Advisors are vital to your program

• Plan how you will engage them and inform them

• Will you have an advisory council?

• Will you send them a newsletter?

• Will you recognize them in some way?

• Will you offer seminars that help them attain continuing education

credits?

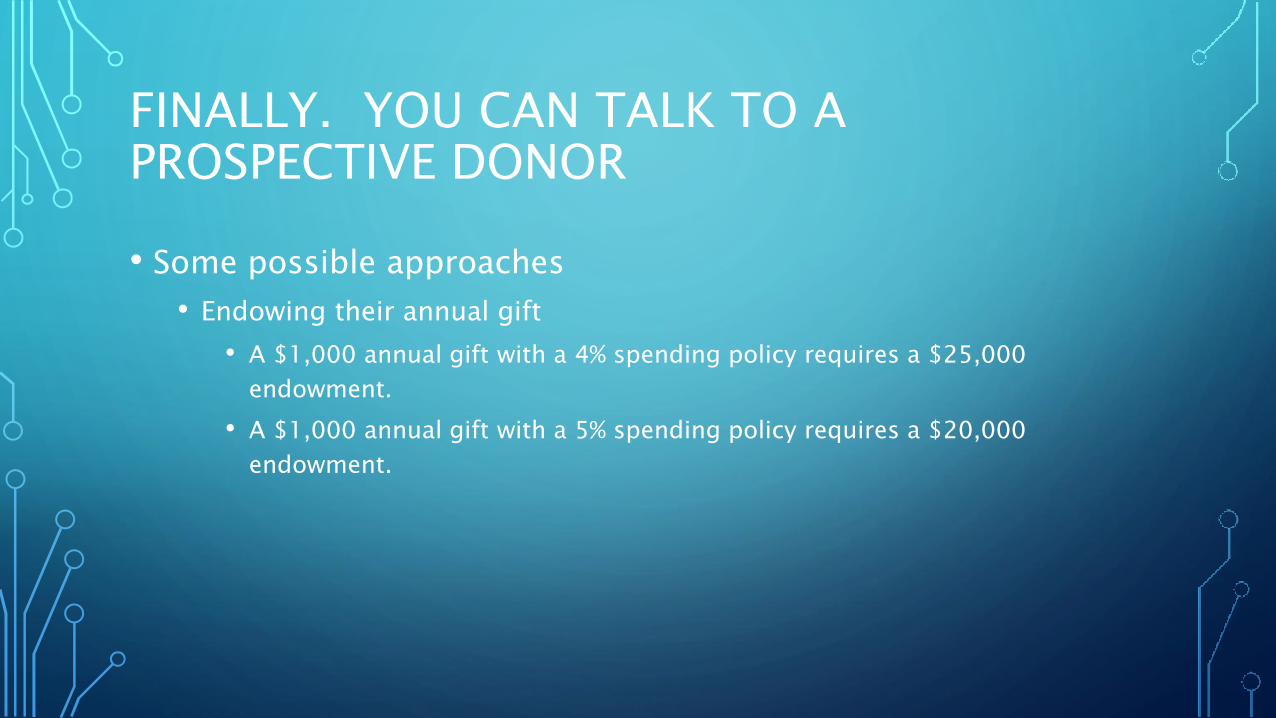

FINALLY. YOU CAN TALK TO A PROSPECTIVE DONOR

• Some possible approaches

• Endowing their annual gift

• A $1,000 annual gift with a 4% spending policy requires a $25,000

endowment.

• A $1,000 annual gift with a 5% spending policy requires a $20,000

endowment.

OTHER APPROACHES

• Make your charities one of your “children.”

• If there are three children, would each child really miss 3 1/3% ?

• That gives the donor 10% to continue taking care of those charities they

cared so much about and supported during their lifetime.

OTHER APPROACHES

• Create a deadline

• Open charter membership in your heritage society for at least 18 months

for people to get their plans in place.

• The deadline will push actions.

• If you list or invite heritage society members, those deadlines can

encourage finalizing documentation.

OTHER APPROACHES

• Help them create their legacy.

• People care deeply about how they will be remembered.

• Why do think that 4 of 5 won’t even tell you you’re in the will?

OTHER APPROACHES

• Help them effect tax-wise giving through their planning

professionals.

• Everyone wants to be “smart” about their financial decisions.

• Help them work with their planning professionals to accomplish their

charitable goals.

legacy D E A T H permanence impact organizational stability

I L L N E S S immortality memorial travel

YOU DO HAVE TO EDUCATE AND ASK

• This is not checkbook giving. This is lifetime asset giving.

• Your organization must be deemed worthy.

• Worthy or not, your donors must know you are “in the

business” of accepting charitable gifts.

• I encourage you to move your organization forward along the

path of promoting planned giving. You will never regret it.

Questions?

Free educational resources »

https://bloomerang.co/resources

•Daily blog post •Weekly webinars •Downloadables •Nonprofit Wrap-‐Up •Bloomerang TV •Bloomies

Upcoming webinar »

https://bloomerang.co/resources/webinars/

Create and Run Your First Really Big Fundraising Campaign w/ Sandy Rees 7/8 1:00pm Eastern