gild cfa presentation version 1.1

TRANSCRIPT

CALIFORNIA STATE UNIVERSITY (EAST BAY) GROUP 2

CFA INSTITUTE RESEARCH REPORT 2015

MARCH 5, 2015

RANDY ACOSTA ▪ ETIENNE BOWIE ▪ DEEPIKA KARNIK ▪ MATTHEW PHILLIPS ▪ BOHDAN STRYUK

Market Profile

52-Wk Price Range $63.25 - $116.83

Avg. Daily Vol. 17,196,000

Beta 0.91

Stock Price Growth 25.5% (2014)

Market Cap. 183 Billion

Shares Outstanding 1.5 Billion

EPS 7.35

P/E 13.91

ROE 87%

EBITDA $16.17 Billion

Profit Margin 65%

Institutional Holdings

94%

Source: Team Estimates, Yahoo Finance

2

Investment Summary Product Portfolio IO AND CP Investment Risk Financial Analysis Sensitivity Analysis Conclusion

Key Performance Indicators

Company Fiscal Gross EBITDA EBIT Pretax Net

Name Period Margin Margin Margin Margin Margin

Gilead Sciences 09/30/2014 82.5% 63.4% 59.1% 56.5% 45.3%

Industry Average 73.0% 33.5% 26.2% 20.6% 16.2%

GlaxoSmithKline 09/30/2014 68.6% 29.3% 25.5% 20.9% 17.6%

Pfizer 09/28/2014 72.9% 42.5% 30.9% 27.0% 20.9%

Roche Hldg DR 12/31/2014 72.4% 34.1% 28.6% 26.4% 19.7%

AstraZeneca 09/30/2014 73.8% 27.4% 16.1% 3.9% 3.6%

AbbVie 09/30/2014 77.1% 34.2% 30.1% 24.7% 18.9%

Source: Gilead Sciences Reports

46%

48%

5% 1%

Gilead Sales by Disease HIV

Hep C

Cardiovascular

Other

Source: Team Research

3

Investment Summary Product Portfolio IO AND CP Investment Risk Financial Analysis Sensitivity Analysis Conclusion

TICKER: GILD NASDAQ

Industry: Biotechnology Headquarters: Foster City, CA

30

50

70

90

110

Jan-

10

May

-10

Sep-

10

Jan-

11

May

-11

Sep-

11

Jan-

12

May

-12

Sep-

12

Jan-

13

May

-13

Sep-

13

Jan-

14

May

-14

Sep-

14

Jan-

15

GILD Historical Prices 2010-2015

Closing PriceCurrent PriceTarget Price

11.86% upside

$114.78

$102.61

TARGET PRICE $114.78

CURRENT PRICE $102.61

Gilead Sciences Inc.

BUY Recommendation

11.86% UPSIDE

Market Leader in HIV Sector

Market Leader in Hepatitis Sector

Best in Class Regimens

Best in class pharmaceutical regimens

Robust pipeline of upcoming drugs

Globally increasing demand for life-threatening diseases

(focusing on HIV, Hepatitis, Oncology)

Sound financial position

COMPANY FACTS

MAIN GROWTH DRIVERS

4

Investment Summary Product Portfolio IO AND CP Investment Risk Financial Analysis Sensitivity Analysis Conclusion

1987

1992

1996

2015

Establishment of Gilead Sciences

IPO on NYSE

Change in Management

and Corporate Strategy

What is happening now and will be next?

� 14 Mergers and Acquisitions Since 1999 � Diversification of Portfolio of Drugs � International Expansion

Management Team

John C. Martin PhD

Chairman & CEO

John C. Milligan PhD President &

COO

John HcHutchison MD

Clinical Research

Norbert W. Bischofberger

VP R&D CSO

Robin L. Washington

Vice President CFO

Gregg H. Alton Vice President Corporate and Medical Affairs

Andrew Cheng MD PhD

HIV Therapeutics and Dev Ops

Paul R. Carter Vice President

Commercial Operations

FDA Approval

5

HIV PORTFOLIO

IO AND CP Investment Risk Financial Analysis Sensitivity Analysis Conclusion

Atripla

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

FDA Approval

Truvada

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

FDA Approval

Complera

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

Patent Expiration Date:

Patent Expiration Date:

Patent Expiration Date:

Investment Summary Product Portfolio

FDA Approval

Striblid

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage Patent Expiration Date:

Sales of Product (2015)E Millions

FDA Approval

Viread

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage Patent Expiration Date:

$3,301

$3,540

$1,427

$1,375

$1,122

42.02%

Percent Overall Sales 2014 (%) Atripla Truvada Complera Striblid Viread

14.17% 13.65% 5.01% 4.89% 4.30%

2019

2019

2020

2018

2018

FDA Approval

6

HIV PORTFOLIO

IO AND CP Investment Risk Financial Analysis Sensitivity Analysis Conclusion

Tybost

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

FDA Approval

Vitekta

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

Patent Expiration Date:

Patent Expiration Date:

Investment Summary Product Portfolio

$10.1

$8.2

Both HIV drugs were approved in Q3 2014

2029

2024

Sales of Product

(2015) E Millions

30.61%

32.83%

13.23%

12.76%

10.40%

0.09% 0.08%

Sales HIV Products 2015E

Atripla

Truvada

Complera

Striblid

Viread

Tybost

Vitekta

Expected Sales

from HIV portfolio:

$10,783 M (2015)E

7

HEPATITIS PORTFOLIO

FDA Approval

Sovaldi

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

FDA Approval

Harvoni

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

Patent Expiration Date:

Patent Expiration Date:

$6,996

$11,627

IO AND CP Investment Risk Financial Analysis Sensitivity Analysis Conclusion Investment Summary Product Portfolio

Expected Sales

from HEP portfolio:

$18,623 M (2015)E

All Other Portfolios

Harvoni

2028

2029

Sales of Product

(2015) E Millions

Sovaldi Highlights • Record Sales • Cure Rate • Interferon/Ribavirin Complements Harvoni Highlights • Lowered Treatment Time • Higher Cure Rate • No Complements

43%

9%

48%

2014

Sovaldi

22%

37%

41%

2015E

8

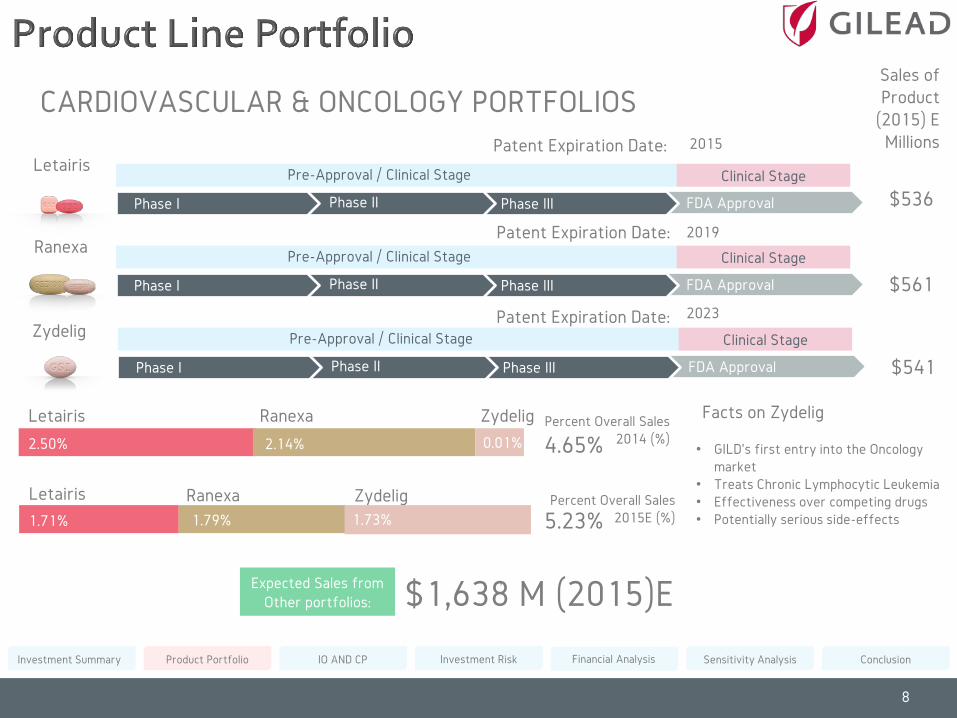

CARDIOVASCULAR & ONCOLOGY PORTFOLIOS

FDA Approval

Letairis

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

FDA Approval

Ranexa

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

FDA Approval

Zydelig

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

Patent Expiration Date:

Patent Expiration Date:

Patent Expiration Date:

$536

$561

$541

2015

2019

2023

Sales of Product

(2015) E Millions

IO AND CP Investment Risk Financial Analysis Sensitivity Analysis Conclusion Investment Summary Product Portfolio

4.65% Percent Overall Sales

2014 (%)

Letairis Ranexa Zydelig

2.50% 2.14% 0.01%

5.23% Percent Overall Sales

2015E (%)

Letairis Ranexa Zydelig 1.71% 1.79% 1.73%

• GILD’s first entry into the Oncology market

• Treats Chronic Lymphocytic Leukemia • Effectiveness over competing drugs • Potentially serious side-effects

Facts on Zydelig

Expected Sales from Other portfolios: $1,638 M (2015)E

9

IO AND CP Investment Risk Financial Analysis Sensitivity Analysis Conclusion Investment Summary Product Portfolio

Pipeline Products

Vedroprevir

GS-4774

GS-9620

Tenofovir Alafenamide

Simtuzumab

Entospletinib

Momelotinib

Idelalisib

GS-4059

GS-4997

GS-6615

Simtuzumab

GS-5806

Gilead Pipeline Products Phase III Phase II

FDA Approval TAF

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

FDA Approval Simtuzmab

Phase I Phase II Phase III

Pre-Approval / Clinical Stage Clinical Stage

Expected Approval:

Expected Approval:

$300

Q3 2015

3 year window

Sales of Product

(2015) E Millions

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

P1 to P2 P2 to P3 P3 toNDA/BLA

NDA/BLA toApproval

Industry Phase LOA

Gilead Phase LOA

Industry Phase Success

Gilead Phase Success

10

Product Portfolio Investment Risk Financial Analysis Sensitivity Analysis Conclusion

Main Competitive Forces from the Industry

New and Superior Drugs Entering The Markets

Rival Drugs Eroding Gilead’s

Profits

Bargaining Power of Consumers

Improved and Efficient R&D

Across the Industry

Increasing Diversification Into

Biologics Throughout the Industry

Competitive Environment

Of Gilead Sciences Inc.

Investment Summary IO AND CP

11

Product Portfolio Investment Risk Financial Analysis Sensitivity Analysis Conclusion Investment Summary IO AND CP

Demand for Pharmaceuticals Demand Analysis

Country Population HBV HCV HIV GDP Per Capita

United States 320,334,000 1,601,670 5,766,012 1,922,004 53,041.98

Canada 35,675,834 178,379 35,676 107,028 51,958.38

Japan 127,020,000 2,540,400 2,921,460 127,020 36,654.00

European Union 507,416,607 7,103,832 2,537,083 2,943,016 35,438.49

South Korea 50,423,955 6,050,875 857,207 50,424 33,791.00

Russia 146,270,033 7,313,502 2,925,401 1,462,700 14,611.70

Brazil 203,836,000 4,076,720 5,299,736 6,115,080 11,208.08

Mexico 121,005,815 1,210,058 847,041 242,012 10,307.28

China 1,368,040,000 164,164,800 41,041,200 1,368,040 6,807.43

India 1,266,430,000 37,992,900 22,795,740 3,799,290 1,498.87

Africa (Developed)** 359,865,000 7,197,300 7,197,300 2,159,190 1,722.92

TOTALS / AVGs 4,506,317,244 239,430,436 92,223,855 20,295,804

World Bank, IMF, CIA** This includes Libya, Mauritus, Seychelles, Tunisia, Algeria, Botsw ana, Egypt, Gabon, South Africa, Cape Verde, Namibia, Morocco, Ghana, Democratic Republic of Congo, Zambia, Sao Tome and Principe, Equatorial Guinea

Infected Population

12

Product Portfolio Financial Analysis Sensitivity Analysis Conclusion Investment Summary

1. Risk in HCV Portfolio 2. Patent Expirations 3. Risks Associated with R&D 4. Risks with Foreign

Currency Exchange Rates 5. Litigation 6. Intellectual Property Risks

Prob

abili

ty

HIG

H

MID

LO

W

LOW MID HIGH

Impact

Investment Risk Matrix

1

2

3

4

5

6

IO AND CP Investment Risk

13

Product Portfolio IO AND CP Investment Risk Sensitivity Analysis Conclusion Financial Analysis Investment Summary

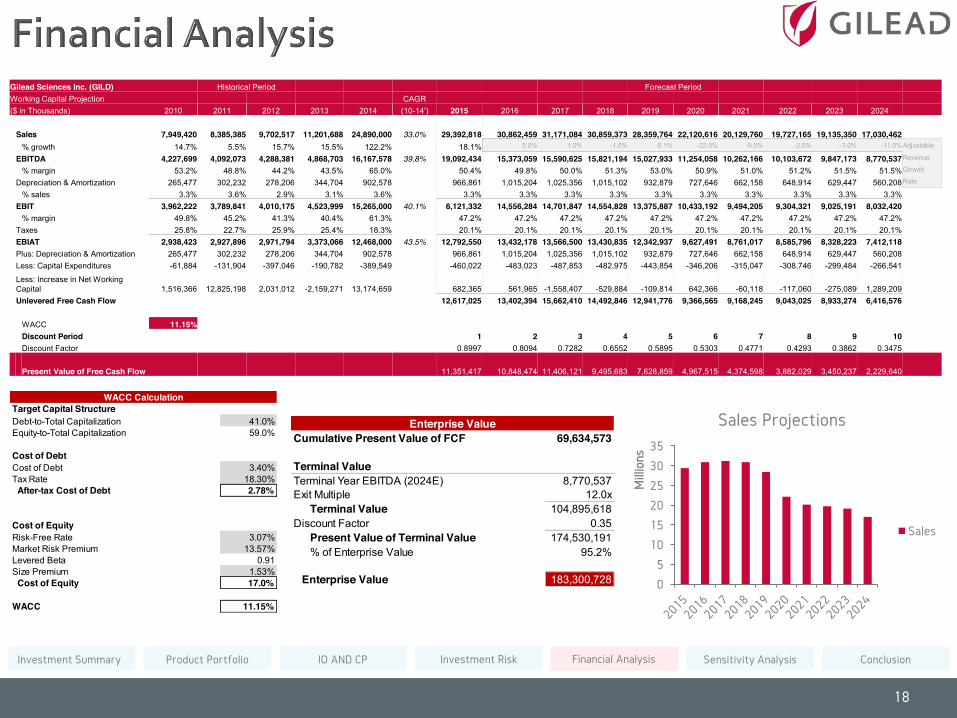

Gilead Sciences Inc. (GILD)Income Statement (Actual and Forecasted)Figures in USD Thousands 2010 2011 2012 2013 2014 2015 F 2016 F 2017 F 2018 F 2019 F 2020 F 2021 F 2022 F 2023 F 2024 F

Gilead SEC 10-K & Q: 2012, 2013, 2014Revenue:

Product sales 7,389,921 8,102,359 9,398,371 10,803,695 24,474,000 28,901,560 30,346,638 30,650,105 30,343,604 27,885,772 26,212,625 24,901,994 23,656,894 22,474,050 21,350,347Royalty revenues 545,970 268,827 290,523 383,849 401,216 473,800 497,490 502,464 497,440 457,147 429,718 408,232 387,821 368,430 350,008Contract and other 13,529 14,199 13,623 14,144 14,784 17,458 18,331 18,515 18,330 16,845 15,834 15,042 14,290 13,576 12,897

Total revenues 7,949,420 8,385,385 9,702,517 11,201,688 24,890,000 29,392,818 30,862,459 31,171,084 30,859,373 28,359,764 26,658,178 25,325,269 24,059,006 22,856,055 21,713,253

Cost and Expenses:Cost of goods sold 1,869,876 2,124,410 2,471,363 2,858,502 3,788,000 7,348,205 7,715,615 7,792,771 7,714,843 7,089,941 6,664,544 6,331,317 6,014,751 5,714,014 5,428,313Research and development expenses 1,072,930 1,229,151 1,759,945 2,119,756 2,854,000 3,300,000 3,816,988 4,416,256 5,109,608 5,911,816 6,839,971 7,913,847 9,156,321 10,593,863 12,257,100Selling, general, and administrative expenses 1,044,392 1,241,983 1,461,034 1,699,431 2,983,000 4,268,195 4,481,605 4,526,421 4,481,157 4,118,183 3,871,092 3,677,537 3,493,661 3,318,978 3,153,029

Total costs and expenses 3,987,198 4,595,544 5,692,342 6,677,689 9,625,000 14,916,400 16,014,208 16,735,447 17,305,608 17,119,940 17,375,608 17,922,702 18,664,733 19,626,854 20,838,441

(EBIT) Income from operations 3,962,222 3,789,841 4,010,175 4,523,999 15,265,000 13,863,128 14,556,284 14,701,847 14,554,828 13,375,887 12,573,334 11,944,667 11,347,434 10,780,062 10,241,059Interest expense -108,961 -205,418 -360,916 -306,894 -412,000 - - - - - - - - - - Other income (expense), net 60,287 66,581 37,279 8,886 3,000 - - - - - - - - - - (EBT) Income before provision for income taxes 3,913,548 3,651,004 3,686,538 4,225,991 14,856,000 13,863,128 14,556,284 14,701,847 14,554,828 13,375,887 12,573,334 11,944,667 11,347,434 10,780,062 10,241,059

Provision for income taxes 1,023,799 861,945 1,038,381 1,150,933 2,797,000 2,701,861 2,836,954 2,865,324 2,836,670 2,606,900 2,450,486 2,327,962 2,211,564 2,100,986 1,995,936Net income 2,889,749 2,789,059 2,648,157 3,075,058 12,059,000 11,161,266 11,719,330 11,836,523 11,718,158 10,768,987 10,122,848 9,616,705 9,135,870 8,679,077 8,245,123

Net loss attributable to noncontrolling interest 11,508 14,578 17,967 17,522 42,000 51,172 53,731 54,268 53,725 49,374 46,411 44,091 41,886 39,792 37,802

Net income attributable to Gilead 2,901,257 2,803,637 2,666,124 3,092,580 12,101,000 11,212,438 11,773,060 11,890,791 11,771,883 10,818,361 10,169,259 9,660,796 9,177,756 8,718,868 8,282,925Net income per share attributable to Gilead common stockholders---basic 1.69 1.81 1.76 2.02 7.95 7.17 7.67 7.76 7.66 7.03 6.60 6.29 5.97 5.67 5.38Shares used in per share calculation---basic 1,712,120 1,549,806 1,514,621 1,528,620 1,522,000 1,563,745 1,535,650 1,532,835 1,536,503 1,538,085 1,541,322 1,536,877 1,537,122 1,537,981 1,538,277Net income per share attributable to Gilead common stockholders---diluted 1.66 1.77 1.68 1.82 7.35 6.80 7.22 7.25 7.13 6.58 6.19 5.88 5.58 5.30 5.04Shares used in per share calculation---diluted 1,746,792 1,580,236 1,582,549 1,694,747 1,647,000 1,649,012 1,630,123 1,640,287 1,652,085 1,643,683 1,643,020 1,641,824 1,644,175 1,644,953 1,643,531

Depreciation and amortization expense 265,477 302,232 278,206 344,704 902,578 803,496 811,428 815,872 827,980 840,268 852,738 865,393 878,236 891,269 904,496(EBITDA) Income from operations before interest, D & A 4,227,699 4,092,073 4,288,381 4,868,703 16,167,578 15,121,474 17,221,605 19,392,771 21,698,303 23,809,845 24,222,991 25,756,177 27,456,326 29,269,874 31,075,625

Historical Data Forecasts Data

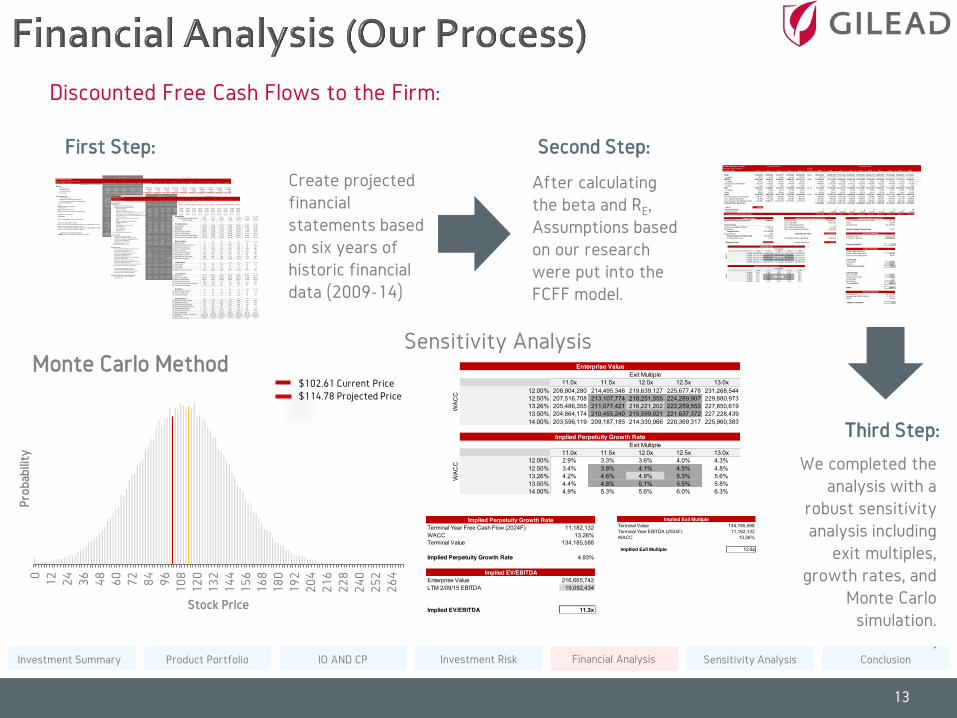

Discounted Free Cash Flows to the Firm:

First Step:

Gilead Sciences Inc. (GILD)Cash Flow StatementFigures in USD Thousands 2010 2011 2012 2013 2014 2015 F 2016 F 2017 F 2018 F 2019 F 2020 F 2021 F 2022 F 2023 F 2024 F

Gilead SEC 10-K: 2012, 2013, 2014Operating Activities:

Net income 2,889,749 2,789,059 2,573,599 3,057,286 8,597,335 10,794,144 12,423,075 13,925,133 15,191,049 16,116,317 17,097,941 18,139,355 19,244,200 20,416,340 21,659,874Adjustments to reconcile net income tonet cash provided by operating activities:

Depreciation expense 67,240 72,187 82,847 102,644 93,669 179,519 176,799 174,532 165,784 155,405 177,032 177,040 177,417 177,999 180,548Amortization expense 198,237 230,045 195,359 242,060 680,950 588,877 592,471 590,784 603,246 616,725 622,441 631,167 640,390 650,801 660,753Stock-based compensation expense 200,041 192,378 208,725 251,984 264,583 251,984 251,984 251,984 251,984 251,984 251,984 251,984 251,984 251,984 251,984In-process research and development impairment charges 136,000 26,630 - - - - - - - - - - - - - Excess tax benefits from stock-based compensation -81,620 -40,848 -114,236 -278,773 -357,928 -174,681 -193,293 -223,782 -245,691 -239,075 -215,305 -223,429 -229,457 -230,591 -227,571Tax benefits from exercise and vesting of stock-based awards 82,086 37,231 112,629 284,655 360,336 252,540 299,177 304,018 285,245 296,147 295,136 292,176 294,486 293,933 293,532Deferred income taxes 12,152 64,061 -39,393 -98,181 -67,061 -25,684 -33,252 -52,714 -55,378 -46,818 -42,769 -46,186 -48,773 -47,985 -46,506Change in fair value of contingent consideration - - - 58,700 -4,119 -4,119 -4,119 -4,119 -4,119 -4,119 -4,119 -4,119 -4,119 -4,119 -4,119Other 10,408 47,931 -1,878 47,289 54,791 10,408 47,931 -1,878 47,289 54,791 10,408 47,931 -1,878 47,289 54,791Changes in operating assets and liab ilities: Accounts receivable, net -348,875 -375,736 197,986 -315,299 -826,970 -740,230 -851,937 -954,944 -1,041,757 -1,105,209 -1,172,525 -1,243,942 -1,319,709 -1,400,091 -1,485,369Inventories -161,190 -200,793 -349,924 -343,143 100,828 -349,924 -402,731 -451,424 -492,463 -522,458 -554,280 -588,041 -623,857 -661,856 -702,169Prepaid expenses and other assets -70,466 -13,959 -129,318 -170,355 -428,969 -299,662 -364,316 -331,989 -348,152 -340,070 -344,111 -342,091 -343,101 -342,596 -342,849Accounts payable -4,453 428,944 117,485 -97,673 -74,599 -86,136 -80,368 -83,252 -81,810 -82,531 -82,170 -82,350 -82,260 -82,305 -82,283Income taxes payable -185,733 110,771 -68,473 30,021 135,672 4,452 42,489 28,832 48,293 51,947 35,203 41,353 41,126 43,584 42,642Accrued liabilities 120,065 300,593 386,063 311,628 1,256,505 1,124,712 1,294,440 1,450,949 1,582,853 1,679,263 1,781,545 1,890,056 2,005,177 2,127,310 2,256,882Deferred revenues -29,728 -29,484 23,245 22,145 12,310 19,233 17,896 16,480 17,870 17,415 17,255 17,513 17,394 17,388 17,432

Net cash provided by operating activities 2,833,913 3,639,010 3,194,716 3,104,988 9,797,333 11,545,432 13,216,248 14,638,610 15,924,243 16,899,715 17,873,664 18,958,416 20,019,020 21,257,084 22,527,572

Investing Activities:Purchases of marketable securities -5,502,687 -5,127,790 -1,244,898 -256,700 -1,532,426 -2,732,900 -2,178,943 -1,589,173 -1,658,028 -1,938,294 -2,019,468 -1,876,781 -1,816,349 -1,861,784 -1,902,535Proceeds from sales of marketable securities 3,033,893 8,649,752 527,712 494,117 477,152 2,636,525 2,557,052 1,338,512 1,500,671 1,701,982 1,946,948 1,809,033 1,659,429 1,723,613 1,768,201Proceeds from maturities of marketable securities 683,927 788,395 44,813 77,655 26,582 324,274 252,344 145,134 165,198 182,706 213,931 191,863 179,766 186,693 190,992Purchases of other investments - - -25,000 - - - - - - - - - - - - Acquisitions, net of cash acquired -91,000 -588,608 -10,751,635 -378,645 - - - - - - - - - - - Capital expenditures -61,884 -131,904 -397,046 -190,782 -389,549 -460,022 -483,023 -487,853 -482,975 -443,854 -417,222 -396,361 -376,543 -357,716 -339,830

Net cash used in investing activities -1,937,751 3,589,845 -11,846,054 -254,355 -1,418,241 -232,122 147,430 -593,381 -475,134 -497,459 -275,811 -272,247 -353,697 -309,194 -283,172

Financing Activities:Proceeds from debt financing, net of issuance costs 2,962,500 4,660,702 2,144,733 - 3,965,446 2,746,676 2,703,511 2,312,073 2,345,541 2,814,650 2,584,490 2,552,053 2,521,762 2,563,699 2,607,331Proceeds from convertible note hedges - 36,148 213,856 2,774,402 1,629,483 930,778 1,116,933 1,333,090 1,556,937 1,313,444 1,250,237 1,314,128 1,353,567 1,357,663 1,317,808Proceeds from sale of warrants 155,425 - - - - - - - - - - - - - - Proceeds from issuances of common stock 221,223 211,737 466,283 313,079 275,074 297,479 312,730 332,929 306,258 304,894 310,858 313,534 313,695 309,848 310,566Purchases of convertible note hedges -362,622 - - - -26,249 - - - - - - - - - - Repurchases of common stock -4,022,593 -2,383,132 -667,041 -582,358 -3,348,477 -2,200,720 -1,836,346 -1,726,988 -1,938,978 -2,210,302 -1,982,667 -1,939,056 -1,959,598 -2,006,120 -2,019,549Repayments of debt and other long-term obligations -500,000 -686,135 -1,837,139 -4,439,891 -2,859,872 -2,064,607 -2,377,529 -2,715,808 -2,891,541 -2,581,871 -2,526,271 -2,618,604 -2,666,819 -2,657,022 -2,610,118Payments to settle warrants - - - -1,039,695 -4,092,758 -1,026,491 -1,231,789 -1,478,146 -1,773,776 -1,920,592 -1,486,159 -1,578,092 -1,647,353 -1,681,194 -1,662,678Repayments of other long-term obligations -5,786 -1,562 -2,186 -77 - -1,922 -1,149 -1,067 -843 -996 -1,196 -1,050 -1,030 -1,023 -1,059Excess tax benefits from stock-based compensation 81,620 40,848 114,236 278,773 357,928 174,681 193,293 223,782 245,691 239,075 215,305 223,429 229,457 230,591 227,571Payment of contingent consideration - - - - -98,346 - - - - - - - - - - Contributions from (distributions to) noncontrolling interest 131,523 -115,037 130,604 151,826 -61,105 47,562 30,770 59,931 45,797 24,591 41,730 40,564 42,523 39,041 37,690

Net cash provided by (used in) financing activities -1,338,710 1,763,569 563,346 -2,543,941 -4,258,876 -1,096,564 -1,089,574 -1,660,203 -2,104,913 -2,017,107 -1,593,672 -1,693,094 -1,813,798 -1,844,517 -1,792,437

Effect of exchange rate changes on cash 77,469 -16,526 7,909 2,420 -23,962 9,462 -4,139 -1,662 -3,576 -4,776 -938 -3,018 -2,794 -3,021 -2,909Cash and cash equivalents at end of period -365,079 8,975,898 -8,080,083 309,112 4,096,254 10,226,207 12,269,964 12,383,363 13,340,620 14,380,373 16,003,244 16,990,057 17,848,732 19,100,353 20,449,052Cash and cash equivalents at beginning of period 1,272,958 907,879 9,883,777 1,803,694 2,112,806 7,685,878 10,342,623 12,333,710 12,454,501 13,424,268 14,478,147 16,092,072 17,073,657 17,936,538 19,191,559Net change in cash and cash equivalents 907,879 9,883,777 1,803,694 2,112,806 6,209,060 2,540,329 1,927,341 49,653 886,119 956,105 1,525,097 897,985 775,075 1,163,814 1,257,493

Supplemental disclosure of cash flow information:Interest paid, net of amounts capitalized 15,748 62,180 249,358 238,325 - - - - - - - - - - - Income taxes paid 1,129,577 621,025 1,101,241 1,050,588 - - - - - - - - - - -

Historical Data Forecasts Data

Growth Rates: 2010 2011 2012 2013 2014 Geo Mean Arth. Mean1 One-Year Growth Rate (Sales) 6.6% 9.6% 16.0% 15.0% 126.5% 18.1% 34.8%2 CAGR (5-years) 27.0% 18.9% 15.9% 12.8% 33.3% 18.9% 21.6%

Profitability Ratios: 2010 2011 2012 2013 2014 Geo Mean Arth. Mean3 Gross Margin 76.5% 74.7% 74.5% 74.5% 84.8% 76.9% 77.0%4 EBIT Margin 49.8% 46.8% 41.3% 40.4% 61.3% 47.4% 47.9%5 Net Margin 36.4% 33.3% 27.3% 27.5% 48.4% 33.8% 34.6%6 Return on Assets (ROA) 20.6% 15.3% 13.7% 11.7% 35.2% 17.8% 19.3%7 Return on Equity (ROE) 47.2% 40.6% 27.8% 26.2% 87.0% 41.4% 45.8%8 Return on Invested Capital (ROIC) 32.3% 19.8% 17.5% 21.0% 54.8% 26.4% 29.1%9 Pre-Tax Return on Invested Capital 43.6% 25.7% 23.6% 28.1% 67.1% 34.6% 37.6%

Efficiency Ratios: 2010 2011 2012 2013 2014 Geo Mean Arth. Mean10 Asset Turnover 1.3 0.6 0.5 0.5 0.8 0.7 0.711 Net Working Capital Turnover 11.1 1.1 1.3 -168.5 4.4 2.5 -30.112 Fixed Assets Turnover 10.5 10.5 8.5 9.3 14.6 10.5 10.713 Days in Inventory (Days) 117.6 222.8 231.5 242.7 165.8 189.5 196.114 Inventory Turnover 2.9 1.6 1.6 1.5 2.2 1.9 2.015 Collection Period (Days) 31.0 57.3 51.2 46.3 35.8 43.2 44.316 Receivables Turnover 8.4 4.5 5.1 5.6 7.3 6.0 6.217 Days' Sales in Cash (Days) 44.8 445.3 70.0 71.4 171.9 111.4 160.718 Payable Period (Days) 156.8 207.2 196.0 160.4 114.0 163.4 166.9

Liquidity Ratios: 2010 2011 2012 2013 2014 Geo Mean Arth. Mean19 Current Ratio 2.3 5.5 1.5 1.1 3.2 2.3 2.720 Quick Ratio 0.9 4.5 0.8 0.7 2.1 1.4 1.821 Cash Ratio 0.4 3.9 0.4 0.3 1.9 0.8 1.422 Defensive Interval Measure 231.6 940.0 228.0 230.3 612.9 370.7 448.5

Leverage Ratios: 2010 2011 2012 2013 2014 Geo Mean Arth. Mean23 Debt Ratio 31.7% 52.6% 42.5% 25.1% 36.4% 36.5% 37.7%24 Debt to Equity Ratio 46.4% 110.8% 73.9% 33.5% 57.2% 59.2% 64.4%25 Equity to Assets Ratio 52.8% 39.7% 44.9% 52.2% 39.1% 45.4% 45.7%26 Times-Interest Earned 36.4 18.4 11.1 14.7 37.1 21.0 23.527 Times-Interest Earned (Cash Flow) 38.8 19.9 11.9 15.9 39.2 22.5 25.128 Times-Burden Covered 5.2 18.3 2.6 1.5 8.1 5.0 7.2

Risk Ratios: 2010 2011 2012 2013 2014 Geo Mean Arth. Mean29 Fixed to Variable Costs 1.1 1.2 1.3 1.3 1.5 1.3 1.330 Sales to Fixed Costs 3.1 3.3 2.9 2.8 4.2 3.2 3.331 Contribution Margin 0.7 0.7 0.7 0.7 0.8 0.7 0.7

Valuation Ratios: 2010 2011 2012 2013 2014 Geo Mean Arth. Mean32 Earnings Per Share (EPS) 1.80 1.55 1.46 1.65 6.54 2.13 2.6033 Dividend Per Share 0.00 0.00 0.00 0.00 0.00 0.00 0.0034 Price/Earnings (P/E) Ratio 10.1 13.2 25.2 45.5 14.4 18.6 21.735 Price/Book Value (P/B) Ratio 5.0 4.6 6.0 10.1 10.4 6.8 7.236 Dividend Payout Ratio 0.0 0.0 0.0 0.0 0.0 0.0 0.037 Stock Price (Year-end) 18.12 20.47 36.72 75.10 94.26 39.52 48.9338 Stock Price Growth -16.3% 13.0% 79.4% 104.5% 25.5% 40.7% 41.2%39 Average # of Shares Outstanding 1,603,996 1,506,212 1,519,163 1,534,414 1,499,000 1,532,102 1,532,55740 Book Value 5,863,729 6,738,856 9,309,739 11,369,067 13,564,709 8,928,255 9,369,22041 Book Value Per Share 3.66 4.47 6.13 7.41 9.05 5.83 6.14

Create projected financial statements based on six years of historic financial data (2009-14)

Gilead Sciences Inc. (GILD)Working Capital Projection CAGR($ in Thousands) 2010 2011 2012 2013 2014 (10-14') 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Sales 7,949,420 8,385,385 9,702,517 11,201,688 24,890,000 33.0% 29,392,818 30,862,459 31,171,084 30,859,373 28,359,764 26,658,178 25,325,269 24,059,006 22,856,055 21,713,253% growth 14.7% 5.5% 15.7% 15.5% 122.2% 18.1% 5.0% 1.0% -1.0% -8.1% -6.0% -5.0% -5.0% -5.0% -5.0% Adjustible

EBITDA 4,227,699 4,092,073 4,288,381 4,868,703 16,167,578 39.8% 19,092,434 15,373,059 15,590,625 15,821,194 15,027,933 13,562,583 12,910,840 12,322,313 11,761,871 11,182,132 Revenue

% margin 53.2% 48.8% 44.2% 43.5% 65.0% 50.4% 49.8% 50.0% 51.3% 53.0% 50.9% 51.0% 51.2% 51.5% 51.5% Growth

Depreciation & Amortization 265,477 302,232 278,206 344,704 902,578 966,861 1,015,204 1,025,356 1,015,102 932,879 876,906 833,061 791,408 751,838 714,246 Rate

% sales 3.3% 3.6% 2.9% 3.1% 3.6% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3%EBIT 3,962,222 3,789,841 4,010,175 4,523,999 15,265,000 40.1% 6,121,332 14,556,284 14,701,847 14,554,828 13,375,887 12,573,334 11,944,667 11,347,434 10,780,062 10,241,059

% margin 49.8% 45.2% 41.3% 40.4% 61.3% 47.2% 47.2% 47.2% 47.2% 47.2% 47.2% 47.2% 47.2% 47.2% 47.2%Taxes 25.8% 22.7% 25.9% 25.4% 18.3% 20.1% 20.1% 20.1% 20.1% 20.1% 20.1% 20.1% 20.1% 20.1% 20.1%EBIAT 2,938,423 2,927,896 2,971,794 3,373,066 12,468,000 43.5% 12,792,550 13,432,178 13,566,500 13,430,835 12,342,937 11,602,361 11,022,243 10,471,131 9,947,574 9,450,195Plus: Depreciation & Amortization 265,477 302,232 278,206 344,704 902,578 966,861 803,496 1,025,356 1,015,102 932,879 876,906 833,061 791,408 751,838 714,246Less: Capital Expenditures -61,884 -131,904 -397,046 -190,782 -389,549 -460,022 -483,023 811,428 -482,975 -443,854 -417,222 -396,361 -376,543 -357,716 -339,830Less: Increase in Net Working Capital -1,562,923 14,388,121 -12,357,109 10,197,838 -2,115,974 624,097 411,193 -1,645,539 -592,092 -183,108 485,663 -162,559 -183,474 -344,258 1,192,235Unlevered Free Cash Flow 13,923,486 14,163,844 13,757,745 13,370,870 12,648,854 12,547,708 11,296,383 10,702,521 9,997,438 11,016,845

WACC 13.26%Discount Period 1 2 3 4 5 6 7 8 9 10Discount Factor 0.8829 0.7795 0.6883 0.6077 0.5365 0.4737 0.4182 0.3693 0.3260 0.2879Present Value of Free Cash Flow 12,293,269 11,041,293 11,734,177 8,844,871 6,983,025 5,483,897 4,860,692 4,087,729 3,484,079 2,484,989

Cumulative Present Value of FCF 71,298,022 Enterprise Value 216,665,742 Terminal Year Free Cash Flow (2024F) 11,182,132Less: Total Debt 7,933,040 WACC 13.26%

Terminal Value Less: Preferred Securities 0 Terminal Value 134,185,588Terminal Year EBITDA (2024E) 11,182,132 Less: Noncontrolling Interest 51,172Exit Multiple 12.0x Plus: Cash and Cash Equivalents 7,685,878 Implied Perpetuity Growth Rate 4.93%

Terminal Value 134,185,588Discount Factor 0.29 Implied Equity Value 216,367,408

Present Value of Terminal Value 205,483,610 Enterprise Value 216,665,742% of Enterprise Value 94.8% Fully Diluted Shares Outstanding 1,635,005 LTM 2/09/15 EBITDA 19,092,434

Enterprise Value 216,665,742 Implied Share Price 132.33 Implied EV/EBITDA 11.3x

216,665,742 11.0x 11.5x 12.0x 12.5x 13.0x Target Capital Structure12.00% 208,904,280 214,495,346 219,639,127 225,677,478 231,268,544 Debt-to-Total Capitalization 41.0%12.50% 207,516,708 213,107,774 218,251,555 224,289,907 229,880,973 Equity-to-Total Capitalization 59.0%13.26% 205,486,355 211,077,421 216,221,202 222,259,553 227,850,61913.50% 204,864,174 210,455,240 215,599,021 221,637,372 227,228,439 Cost of Debt14.00% 203,596,119 209,187,185 214,330,966 220,369,317 225,960,383 Cost of Debt 3.40%

Tax Rate 18.30%After-tax Cost of Debt 2.78%

4.93% 11.0x 11.5x 12.0x 12.5x 13.0x12.00% 2.9% 3.3% 3.6% 4.0% 4.3% Cost of Equity12.50% 3.4% 3.8% 4.1% 4.5% 4.8% Risk-Free Rate 3.07%13.26% 4.2% 4.6% 4.9% 5.3% 5.6% Market Risk Premium 17.49%13.50% 4.4% 4.8% 5.1% 5.5% 5.8% Levered Beta 0.9114.00% 4.9% 5.3% 5.6% 6.0% 6.3% Size Premium 1.53%

Cost of Equity 20.55%

WACC 13.26%

Terminal Value 134,185,588Terminal Year EBITDA (2024F) 11,182,132WACC 13.26%

Impllied Exit Multiple 12.8x

Historical Period Forecast Period

Enterprise Value Implied Equity Value and Share Price Implied Perpetuity Growth Rate

Implied Exit Multiple

Implied Perpetuity Growth RateExit Multiple

WA

CC

Implied EV/EBITDA

WA

CC

Exit MultipleEnterprise Value

WACC Calculation

Second Step:

After calculating the beta and RE, Assumptions based on our research were put into the FCFF model.

Third Step:

We completed the analysis with a

robust sensitivity analysis including

exit multiples, growth rates, and

Monte Carlo simulation.

.

216,665,742 11.0x 11.5x 12.0x 12.5x 13.0x12.00% 208,904,280 214,495,346 219,639,127 225,677,478 231,268,54412.50% 207,516,708 213,107,774 218,251,555 224,289,907 229,880,97313.26% 205,486,355 211,077,421 216,221,202 222,259,553 227,850,61913.50% 204,864,174 210,455,240 215,599,021 221,637,372 227,228,43914.00% 203,596,119 209,187,185 214,330,966 220,369,317 225,960,383

4.93% 11.0x 11.5x 12.0x 12.5x 13.0x12.00% 2.9% 3.3% 3.6% 4.0% 4.3%12.50% 3.4% 3.8% 4.1% 4.5% 4.8%13.26% 4.2% 4.6% 4.9% 5.3% 5.6%13.50% 4.4% 4.8% 5.1% 5.5% 5.8%14.00% 4.9% 5.3% 5.6% 6.0% 6.3%

Implied Perpetuity Growth RateExit Multiple

WA

CC

WA

CC

Exit MultipleEnterprise Value

Sensitivity Analysis

Terminal Year Free Cash Flow (2024F) 11,182,132WACC 13.26%Terminal Value 134,185,588

Implied Perpetuity Growth Rate 4.93%

Enterprise Value 216,665,742LTM 2/09/15 EBITDA 19,092,434

Implied EV/EBITDA 11.3x

Implied Perpetuity Growth Rate

Implied EV/EBITDA

Terminal Value 134,185,588Terminal Year EBITDA (2024F) 11,182,132WACC 13.26%

Impllied Exit Multiple 12.8x

Implied Exit Multiple

0 12 24 36 48 60 72 84 96 108

120

132

144

156

168

180

192

204

216

228

240

252

264

Prob

abili

ty

Stock Price

Monte Carlo Method $102.61 Current Price $114.78 Projected Price

14

Product Portfolio IO AND CP Investment Risk Sensitivity Analysis Conclusion Financial Analysis Investment Summary

Important Updates (in millions $000) Jan 2014 Jan 2013 Change (%)

Net Product Revenues 24,474 10,804 127%

Antiviral Products 22,791 9,342 144%

HCV 12,410 139 99%

HIV and Other Antiviral 10,381 9,203 13%

Other Products 1,683 1,462 15%

Cost and Expenses 8,306 6,214 32%

Cost of Goods Sold (COGS) 2,964 2,709 9%

Product Gross Margin 88% 75%

R&D 2,585 1,948 33%

SG&A 2,757 1,557 77%

EBIT (Operating) Margin 67% 45%

Net Income $13,314 $3451 286%

Diluted EPS $8.09 $2.04 297%

15

Product Portfolio IO AND CP Investment Risk Sensitivity Analysis Conclusion Financial Analysis Investment Summary

Forecasted Changes (in millions $000) Jan 2015 E Jan 2014 Change (%)

Net Product Revenues 31,344 24,474 28%

Antiviral Products 29,706 22,791 30%

HCV 18,623 12,410 50%

HIV and Other Antiviral 11,083 10,381 7%

Other Products 1,638 1,683 Δ < 1%

Cost and Expenses 14,916 8,306 79%

Cost of Goods Sold (COGS) 7,348 2,964 148%

Product Gross Margin 75% 88%

R&D 3,300 2,585 27%

SG&A 4,268 2,757 68%

EBIT (Operating) Margin 47% 67%

Net Income $11,161 $13,314 -16%

Diluted EPS $6.78 $8.09 -16%

16

Product Portfolio IO AND CP Investment Risk Sensitivity Analysis Conclusion Financial Analysis Investment Summary

Products Price 2014 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E NPV

Atripla $24,960 3,470 3,301 3,103 2,885 2,698 2,496 - - - - - 13,035

Viread $ 9,500 1,058 1,121 1,043 1,012 971 - - - - - - 3,790

Ranexa N/A 510 561 606 630 635 600 - - - - - 2,711

TAF $ 9,000-10,000 300 966 1,140 1,277 1,430 1,559 1,668 1,784 1,856 1,930 11,002

Sovaldi $ 84,000 10,283 6,996 7,031 6,423 6,339 6,206 6,014 5,773 5,600 5,376 5,107 50,390

Harvoni $ 94,500 2,127 11,627 12,429 12,462 12,699 12,737 12,610 12,231 11,803 11,331 10,821 103,682

Striblid $16,650 1,197 1,375 1,512 1,616 1,679 - - - - - - 5,619

Truvada $14,000 3,340 3,540 3,682 3,792 3,830 3,792 - - - - - 16,666

Tybost $15,000 - 10 20 44 75 109 125 138 151 163 173 778

Vitekta $26,000 - 8 16 36 62 89 103 113 124 136 150 644

Complera N/A 1,228 1,426 1,568 1,676 1,741 1,776 1,794 - - - - 8,736

Zydelig $ 86,400 23 541 964 1,070 1,167 1,248 1,323 1,403 1,487 1,576 - 8,783

NPV of sales $ 225,833

stock price (based of gross margins) $ 123.91

17

Product Portfolio IO AND CP Investment Risk Sensitivity Analysis Conclusion Financial Analysis Investment Summary

βf = 0.907

βr = 0.906 22 years

Historical Data Jan1992 - Jan2015

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

-0.20 -0.10 0.00 0.10 0.20 0.30Gile

ad R

isk

Prem

ium

Market Risk Premium

Market Risk Premium Line Fit Plot

Gilead RiskPremium

PredictedGilead RiskPremium

Beta Calculations

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

2010 2011 2012 2013 2014

Gross Margin EBIT Margin Net Margin

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

2010 2011 2012 2013 2014

CAGR (5-years) One-Year Growth Rate (Sales)

18

Product Portfolio IO AND CP Investment Risk Sensitivity Analysis Conclusion Financial Analysis Investment Summary

Gilead Sciences Inc. (GILD) Historical Period Forecast Period Working Capital Projection CAGR ($ in Thousands) 2010 2011 2012 2013 2014 (10-14') 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 Sales 7,949,420 8,385,385 9,702,517 11,201,688 24,890,000 33.0% 29,392,818 30,862,459 31,171,084 30,859,373 28,359,764 22,120,616 20,129,760 19,727,165 19,135,350 17,030,462 % growth 14.7% 5.5% 15.7% 15.5% 122.2% 18.1% 5.0% 1.0% -1.0% -8.1% -22.0% -9.0% -2.0% -3.0% -11.0% Adjustable

EBITDA 4,227,699 4,092,073 4,288,381 4,868,703 16,167,578 39.8% 19,092,434 15,373,059 15,590,625 15,821,194 15,027,933 11,254,058 10,262,166 10,103,672 9,847,173 8,770,537 Revenue

% margin 53.2% 48.8% 44.2% 43.5% 65.0% 50.4% 49.8% 50.0% 51.3% 53.0% 50.9% 51.0% 51.2% 51.5% 51.5% Growth

Depreciation & Amortization 265,477 302,232 278,206 344,704 902,578 966,861 1,015,204 1,025,356 1,015,102 932,879 727,646 662,158 648,914 629,447 560,208 Rate

% sales 3.3% 3.6% 2.9% 3.1% 3.6% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3% 3.3% EBIT 3,962,222 3,789,841 4,010,175 4,523,999 15,265,000 40.1% 6,121,332 14,556,284 14,701,847 14,554,828 13,375,887 10,433,192 9,494,205 9,304,321 9,025,191 8,032,420 % margin 49.8% 45.2% 41.3% 40.4% 61.3% 47.2% 47.2% 47.2% 47.2% 47.2% 47.2% 47.2% 47.2% 47.2% 47.2% Taxes 25.8% 22.7% 25.9% 25.4% 18.3% 20.1% 20.1% 20.1% 20.1% 20.1% 20.1% 20.1% 20.1% 20.1% 20.1% EBIAT 2,938,423 2,927,896 2,971,794 3,373,066 12,468,000 43.5% 12,792,550 13,432,178 13,566,500 13,430,835 12,342,937 9,627,491 8,761,017 8,585,796 8,328,223 7,412,118 Plus: Depreciation & Amortization 265,477 302,232 278,206 344,704 902,578 966,861 1,015,204 1,025,356 1,015,102 932,879 727,646 662,158 648,914 629,447 560,208 Less: Capital Expenditures -61,884 -131,904 -397,046 -190,782 -389,549 -460,022 -483,023 -487,853 -482,975 -443,854 -346,206 -315,047 -308,746 -299,484 -266,541

Less: Increase in Net Working Capital 1,516,366 12,825,198 2,031,012 -2,159,271 13,174,659 682,365 561,965 -1,558,407 -529,884 -109,814 642,366 -60,118 -117,060 -275,089 1,289,209

Unlevered Free Cash Flow 12,617,025 13,402,394 15,662,410 14,492,846 12,941,776 9,366,565 9,168,245 9,043,025 8,933,274 6,416,576 WACC 11.15% Discount Period 1 2 3 4 5 6 7 8 9 10 Discount Factor 0.8997 0.8094 0.7282 0.6552 0.5895 0.5303 0.4771 0.4293 0.3862 0.3475

Present Value of Free Cash Flow 11,351,417 10,848,474 11,406,121 9,495,683 7,628,859 4,967,515 4,374,598 3,882,029 3,450,237 2,229,640

Target Capital StructureDebt-to-Total Capitalization 41.0%Equity-to-Total Capitalization 59.0%

Cost of DebtCost of Debt 3.40%Tax Rate 18.30%

After-tax Cost of Debt 2.78%

Cost of EquityRisk-Free Rate 3.07%Market Risk Premium 13.57%Levered Beta 0.91Size Premium 1.53%

Cost of Equity 17.0%

WACC 11.15%

WACC Calculation

Cumulative Present Value of FCF 69,634,573

Terminal ValueTerminal Year EBITDA (2024E) 8,770,537Exit Multiple 12.0x

Terminal Value 104,895,618Discount Factor 0.35

Present Value of Terminal Value 174,530,191% of Enterprise Value 95.2%

Enterprise Value 183,300,728

Enterprise Value

0

5

10

15

20

25

30

35

Mill

ions

Sales Projections

Sales

19

Product Portfolio Investment Risk Financial Analysis Conclusion Investment Summary IO AND CP Sensitivity Analysis

Terminal Value 104,895,618Terminal Year EBITDA (2024F) 8,770,537WACC 11.1%

Impllied Exit Multiple 12.6x

Implied Exit Multiple

Terminal Year Free Cash Flow (2024F) 8,770,537WACC 11.1%Terminal Value 104,895,618

Implied Perpetuity Growth Rate 2.8%

Implied Perpetuity Growth Rate

Enterprise Value 183,300,728LTM 2/09/15 EBITDA 19,092,434

Implied EV/EBITDA 9.6x

Implied EV/EBITDA

20

Product Portfolio Investment Risk Financial Analysis Conclusion Investment Summary IO AND CP Sensitivity Analysis

2.79% 11.0x 11.5x 12.0x 12.5x 13.0x10.00% 0.9% 1.3% 1.6% 2.0% 2.3%10.50% 1.4% 1.8% 2.1% 2.5% 2.8%11.15% 2.1% 2.5% 2.8% 3.1% 3.5%11.50% 2.4% 2.8% 3.1% 3.5% 3.8%12.00% 2.9% 3.3% 3.6% 4.0% 4.3%

WA

CC

Implied Perpetuity Growth RateExit Multiple

183,300,728 11.0x 11.5x 12.0x 12.5x 13.0x10.00% 177,967,881 182,353,149 186,387,596 191,123,686 195,508,95410.50% 176,598,366 180,983,635 185,018,082 189,754,171 194,139,44011.15% 174,879,285 179,264,553 183,299,000 188,035,090 192,420,35811.50% 173,981,215 178,366,484 182,400,930 187,137,020 191,522,28912.00% 172,730,479 177,115,747 181,150,194 185,886,284 190,271,552

Enterprise ValueExit Multiple

WA

CC

21

Product Portfolio Investment Risk Financial Analysis Conclusion Investment Summary IO AND CP Sensitivity Analysis

0 8 16 24 32 40 48 56 64 72 80 88 96 104

112

120

128

136

144

152

160

168

176

184

192

200

208

216

224

232

240

248

256

264

Mor

e

Prob

abili

ty

Stock Price

Monte Carlo Method $102.61 Current Price $114.78 Projected Price

Mean $109.50 Standard Error 11.0%

Standard Deviation $34.79

Price Frequency 2500/100000

This gives our price chance:

65.5%

22

Product Portfolio Investment Risk Financial Analysis Sensitivity Analysis Investment Summary IO AND CP Conclusion

Target Price $114.78

Upside Potential 11.86%

Keep in Mind: • Possible increase in

competition • Litigation outcomes • Market risks

associated with healthcare reform

• Possible intellectual property issues

Best in class drugs (HIV, HEP, Oncology)

Robust Pipeline of Upcoming drugs

Globally increasing demand for life-threating

diseases

Sound financial positioning

RANDY ACOSTA ▪ ETIENNE BOWIE ▪ DEEPIKA KARNIK ▪ MATTHEW PHILLIPS ▪ BOHDAN STRYUK

THANK YOU

24

Product Portfolio IO AND CP Investment Risk Sensitivity Analysis Conclusion Financial Analysis Investment Summary