glancy binkow & goldberg llp lionel z. glancy · 2015-01-16 · glancy binkow & goldberg...

TRANSCRIPT

CLASS ACTION COMPLAINT

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

GLANCY BINKOW & GOLDBERG LLP

Lionel Z. Glancy

Michael Goldberg

Robert V. Prongay

Casey E. Sadler

1925 Century Park East, Suite 2100

Los Angeles, California 90067

Telephone: (310) 201-9150

Facsimile: (310) 201-9160

LAW OFFICES OF HOWARD G. SMITH

Howard G. Smith

3070 Bristol Pike, Suite 112

Bensalem, PA 19020

Telephone: (215) 638-4847

Facsimile: (215) 638-4867

Attorneys for Plaintiff

UNITED STATES DISTRICT COURT

CENTRAL DISTRICT OF CALIFORNIA

PLAINTIFF, Individually and on Behalf of

All Others Similarly Situated,

Plaintiff,

v.

CALAVO GROWERS, INC., LECIL E.

COLE, and ARTHUR J. BRUNO,

Defendants.

Case No.: DRAFT

CLASS ACTION COMPLAINT FOR

VIOLATIONS OF THE FEDERAL

SECURITIES LAWS

JURY TRIAL DEMANDED

CLASS ACTION COMPLAINT

1

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Plaintiff (“Plaintiff”), by and through his attorneys, alleges the following upon

information and belief, except as to those allegations concerning Plaintiff, which are alleged

upon personal knowledge. Plaintiff’s information and belief is based upon, among other things,

his counsel’s investigation, which includes without limitation: (a) review and analysis of

regulatory filings made by CALAVO GROWERS, INC. (“Calavo” or the “Company”), with the

United States Securities and Exchange Commission (“SEC”); (b) review and analysis of press

releases and media reports issued by and disseminated by Calavo; and (c) review of other

publicly available information concerning Calavo.

NATURE OF THE ACTION AND OVERVIEW

1. This is a class action on behalf of those who purchased or otherwise acquired

Calavo’s securities between March 5, 2012 and January 14, 2015 inclusive (the “Class Period”),

seeking to pursue remedies under the Securities Exchange Act of 1934 (the “Exchange Act”).

2. Calavo is a global avocado distributer and an expanding provider of value-added

fresh food. The Company’s purported expertise in marketing and distributing avocados, prepared

avocados, and other perishable foods allows it to deliver a wide array of fresh and prepared food

products to food distributors, produce wholesalers, supermarkets, and restaurants on a worldwide

basis.

3. On January 15, 2014, Calavo revealed that the Audit Committee of the

Company’s Board of Directors had determined that the Company’s annual financial statements

filed with the SEC for the fiscal years ended October 31, 2012 and October 31, 2013 and the

quarterly financial statements therein, as well as the quarterly financial statements filed with the

SEC the quarters ended January 31, 2014, April 30, 2014 and July 31, 2014 should no longer be

relied upon. Additionally, the Company stated that its outside auditors, Ernst & Young’s (“EY”)

CLASS ACTION COMPLAINT

2

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

reports on the consolidated financial statements, including EY’s opinion on the effectiveness of

internal control over financial reporting, should no longer be relied upon as well. According to

the Company, a non-cash misstatement in its historical consolidated financial statements related

to its treatment of contingent consideration in the acquisition of Renaissance Food Group, LLC

(“RFG”) in June 2011 was identified. In accordance with the earn-out provisions in the RFG

acquisition agreement, if RFG’s operating results exceeded defined thresholds, additional

purchase price was required to be paid by the Company, subject to a ceiling. RFG’s results

substantially exceeded defined thresholds and expectations and, accordingly, RFG’s former

owners received the maximum earn-out payment permitted pursuant to the acquisition

agreement. The Company stated that the total estimated cumulative amount of non-cash

operating expense, entirely related to the revaluation of RFG earn-out liability, that should have

been recorded was approximately $54 million, net of tax, spread over the period from the date of

acquisition of RFG (i.e. June 1, 2011) through the period ended October 31, 2014. Initially, the

Company recorded the contingent consideration, which was settleable in common stock, as an

equity instrument and did not record expense based on the changes in fair value of the contingent

consideration. According to the Company, the contingent consideration should have been

accounted for as a liability requiring re-measurement to fair value and expense recognition at

each reporting period subsequent to the acquisition.

4. On this news, shares of Calavo declined $4.72 per share, nearly 10%, to close on

January 15, 2014, at $43.07 per share, on unusually heavy volume.

5. Throughout the Class Period, Defendants made false and/or misleading

statements, as well as failed to disclose material adverse facts about the Company’s business,

operations, and prospects. Specifically, Defendants made false and/or misleading statements

CLASS ACTION COMPLAINT

3

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

and/or failed to disclose: (1) that the Company had improperly recorded the RFG earn-out

payment; (2) that, as a result, the Company’s expenses and financial results were misstated; (3)

that, as such, the Company’s financial statements were not prepared in accordance with

Generally Accepted Accounting Principles (“GAAP”); (4) that the Company lacked adequate

internal and financial controls; and (5) that, as a result of the foregoing, the Company’s financial

statements were materially false and misleading at all relevant times.

6. As a result of Defendants’ wrongful acts and omissions, and the precipitous

decline in the market value of the Company’s securities, Plaintiff and other Class members have

suffered significant losses and damages.

JURISDICTION AND VENUE

7. The claims asserted herein arise under Sections 10(b) and 20(a) of the Exchange

Act (15 U.S.C. §§ 78j(b) and 78t(a)) and Rule 10b-5 promulgated thereunder by the SEC (17

C.F.R. § 240.10b-5).

8. This Court has jurisdiction over the subject matter of this action pursuant to 28

U.S.C. § 1331 and Section 27 of the Exchange Act (15 U.S.C. § 78aa).

9. Venue is proper in this Judicial District pursuant to 28 U.S.C. § 1391(b) and

Section 27 of the Exchange Act (15 U.S.C. § 78aa(c)). Substantial acts in furtherance of the

alleged fraud or the effects of the fraud have occurred in this Judicial District. Many of the acts

charged herein, including the preparation and dissemination of materially false and/or misleading

information, occurred in substantial part in this Judicial District. Additionally, Calavo’s

principal executive offices are located within this Judicial District.

10. In connection with the acts, transactions, and conduct alleged herein, Defendants

directly and indirectly used the means and instrumentalities of interstate commerce, including the

CLASS ACTION COMPLAINT

4

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

United States mail, interstate telephone communications, and the facilities of a national securities

exchange.

PARTIES

11. Plaintiff, as set forth in the accompanying certification, incorporated by reference

herein, purchased or otherwise acquired Calavo’s securities, including call options during the

Class Period, and suffered damages as a result of the federal securities law violations and false

and/or misleading statements and/or material omissions alleged herein.

12. Defendant Calavo is a California corporation with its principal executive offices

located at 1141-A Cummings Road, Santa Paula, California 93060.

13. Defendant Lecil E. Cole (“Cole”) was, at all relevant times, Chief Executive

Officer (“CEO”) and a director of Calavo.

14. Defendant Arthur J. Bruno (“Bruno”) was, at all relevant times, Chief Financial

Officer (“CFO”) of Calavo.

15. Defendants Cole and Bruno are collectively referred to hereinafter as the

“Individual Defendants.” The Individual Defendants, because of their positions with the

Company, possessed the power and authority to control the contents of Calavo’s reports to the

SEC, press releases and presentations to securities analysts, money and portfolio managers and

institutional investors, i.e., the market. Each defendant was provided with copies of the

Company’s reports and press releases alleged herein to be misleading prior to, or shortly after,

their issuance and had the ability and opportunity to prevent their issuance or cause them to be

corrected. Because of their positions and access to material non-public information available to

them, each of these defendants knew that the adverse facts specified herein had not been

disclosed to, and were being concealed from, the public, and that the positive representations

CLASS ACTION COMPLAINT

5

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

which were being made were then materially false and/or misleading. The Individual

Defendants are liable for the false statements pleaded herein, as those statements were each

“group-published” information, the result of the collective actions of the Individual Defendants.

SUBSTANTIVE ALLEGATIONS

Background

16. Calavo is a global avocado distributer and an expanding provider of value-added

fresh food. The Company’s purported expertise in marketing and distributing avocados, prepared

avocados, and other perishable foods allows it to deliver a wide array of fresh and prepared food

products to food distributors, produce wholesalers, supermarkets, and restaurants on a worldwide

basis.

Materially False and Misleading

Statements Issued During the Class Period

17. The Class Period begins on March 5, 2012. On this day, Calavo issued a press

release entitled, “Calavo Growers, Inc. Announces Increased Fiscal 2012 First Quarter Operating

Results.” Therein, the Company, in relevant part, stated:

Highlights Include:

Revenues Grow 29 Percent to $117.4 Million (Including $35.0 Million

from Renaissance Food Group) Versus $91.3 Million in First Quarter of

Fiscal 2011

Net Income Climbs 16 Percent to $2.7 Million, or $0.18 Per Diluted

Share, from $2.3 Million, or $0.16 Per Diluted Share, Last Year

RFG Acquisition Success Increases Contingent Consideration Expense by

$118,000, or Approximately $0.01 Per Diluted Share

Total Gross Margin Expands 80 Basis Points: 10.3 Percent Versus 9.5

Percent

CEO Cole Reiterates Expectation for Record Fiscal 2012

Calavo Growers, Inc. (Nasdaq-GS: CVGW), a global avocado-industry leader and

an expanding provider of value-added fresh food, today reported higher revenues

and net income for the fiscal 2012 first quarter.

CLASS ACTION COMPLAINT

6

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Operating results for the most-recent quarter include those of Renaissance Food

Group, LLC (RFG), which became part of the company on June 1, 2011. RFG’s

results are included in the company’s Calavo Foods business segment.

Net income for the three months ended January 31, 2012 rose 16 percent to $2.7

million, or $0.18 per diluted share, from $2.3 million, equal to $0.16 per diluted

share, in the fiscal 2011 first quarter. Revenues advanced 29 percent to $117.4

million from $91.3 million one year earlier.

Gross margin in the most recent quarter grew to $12.0 million, equal to 10.3

percent of total revenues, from $8.7 million, or 9.5 percent of total revenues, in

last year’s initial period. First quarter operating income expanded 21 percent to

$4.4 million from $3.7 million in the corresponding fiscal 2011 period.

Chairman, President and Chief Executive Officer Lee E. Cole stated: “Calavo

turned in a very solid operating performance during the fiscal 2012 first quarter. A

shortfall in fresh tomato unit volume in the fiscal 2012 first quarter, which we

anticipate being offset by increased volume in the second quarter, impacted gross

margin and tempered results during an otherwise solid initial period. In our core

fresh avocado business, specifically, the company did an excellent job sourcing

and managing costs on fruit from Mexico to offset the lack of supply from

California—a hangover from last year’s cyclically small crop. This strong supply

from Mexico also is benefiting our prepared avocado business, where we are

seeing an improving gross-margin picture following several quarters of being

impacted by high fruit costs.

“Looking at the Calavo Foods business segment on the whole, our RFG

subsidiary performed well in its historically slowest quarter, which we believe

bodes well for the coming periods. By all indicators, we anticipate a strengthening

performance picture across the company—both our Fresh and Calavo Foods

business units—as the fiscal year progresses.”

In Calavo’s Fresh business segment, first quarter revenues totaled $71.1 million, a

decrease of 12 percent from $80.7 million in the corresponding period last year.

While fresh avocado unit volume was substantially unchanged, the decline in

segment revenues is principally attributable to lower sales prices, which continue

to decrease from last year’s unusually high levels. Total Fresh segment volume,

including other diversified produce items, declined approximately nine percent to

nearly 3.2 million units from about 3.5 million total units in the fiscal 2011 first

quarter. First-quarter segment gross margin totaled $6.1 million, or 8.6 percent of

sales, versus $6.1 million, or 7.6 percent of sales in the like period one year ago.

Calavo Foods business segment revenues jumped 334 percent to $46.3 million

from $10.7 million in the fiscal 2011 first quarter. Approximately $35.0 million of

the increase in revenues is attributable to the recently acquired RFG. Excluding

contributions to sales by RFG, Calavo Foods legacy revenues increased

CLASS ACTION COMPLAINT

7

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

approximately $600,000 to $11.3 million. Segment gross margin dollars in the

most recent quarter benefited from the addition of $2.5 million in gross margin

from RFG and rose to approximately $5.9 million in total, or 12.8 percent of

Calavo Foods revenues, offset by fewer pounds of prepared avocados sold and

residual impact from high fruit costs. This compares with gross margin in the

Calavo Foods business segment last year of $2.6 million, equal to 23.9 percent of

sales.

Pursuant to the terms of its RFG acquisition, which triggered certain accounting

treatment, Calavo performs a quarterly review of the related contingent

consideration liability account and revalues this contingent consideration

obligation to its estimated fair value. As a result of its most recent review, the

company recorded a $118,000 expense, equal to about $0.01 per diluted share,

during the first quarter of fiscal 2012 in selling, general and administration

(SG&A) expenses. The first-quarter SG&A expense reflects an increase in the

probability of future performance-based earn-out payments by Calavo to RFG’s

former owners owing to the success of the transaction. Increases or decreases in

the fair value of this contingent consideration obligation can result from factors

such as changes in the assumed timing and amount of revenue and expense

estimates or changes in assumed discount periods and rates.

The Outlook Ahead

Turning to the fiscal 2012 second quarter and beyond, CEO Cole said that he

foresees “a strengthening operating performance picture, paced by higher

revenues and net income,” as the year progresses.

He said: “I am extremely optimistic about the outlook for Calavo during the

current year—and beyond. The 2012 fresh avocado market forecast of 1.4 billion

total pounds remains a precursor of good things for us. We are encouraged by the

first-quarter showing in Mexico where volumes and fruit prices are aligning

favorably. Calavo saw accelerating Mexican fruit volume at the close of the first

quarter and that velocity is anticipated to continue, or even pick up additional

pace. Furthermore, an anticipated significantly larger California fruit harvest will

bring production efficiencies to our domestic packing operations that last year’s

cyclically smaller crop did not allow. Those two aforementioned factors alone

will afford incremental gross margin contribution.

“Diversified fresh produce will be paced by higher tomato volumes in the second

and, potentially, third quarters. Papayas and pineapples are expected to contribute

incrementally to Fresh segment unit volumes and margin. As indication of

synergies, we will also begin directly sourcing pineapple to be used in the RFG

processing facilities.

“With respect to the Calavo Foods business segment, RFG is on pace for

continued rapid top-line growth and strong profitability as we start to enter their

CLASS ACTION COMPLAINT

8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

historically stronger months and quarters. Additionally, the subsidiary’s pace of

product innovation and speed-to-market are energizing the segment overall.

Turning to legacy Calavo Foods products, the lower fresh fruit prices are expected

to translate to higher gross margin in our prepared avocado business that will

accelerate as the year moves forward and we anticipate reaching record levels—a

strong turnaround from 2011.

“Finally, we are making capital investments to accommodate the expected growth

of our core avocado business. To that end, we are currently doubling the capacity

of our packinghouse in Uruapan, Michoacán—the epicenter of the Mexican

avocado industry. When completed in July 2012, Calavo will possess the

capability to pack 600 million pounds of fruit at its California and Mexico

facilities. We intend not only to maintain but substantially grow our industry

leadership position.

“With the company performing extremely well across multiple business

platforms, I am confident that fiscal 2012 will be a record year for Calavo,

exceeding the company’s historical earnings per share record of $1.22,” Cole

concluded.

18. On March 9, 2012, Calavo filed its Quarterly Report with the SEC on Form 10-Q

for the 2012 fiscal first quarter. The Company’s Form 10-Q was signed by Defendants Cole and

Bruno, and reaffirmed the Company’s statements previously announced March 5, 2012. The

Form 10-Q also contained required Sarbanes-Oxley certifications, signed by Defendants Cole

and Bruno, who certified:

1. I have reviewed this quarterly report on Form 10-Q of Calavo Growers,

Inc.;

2. Based on my knowledge, this report does not contain any untrue statement

of a material fact or omit to state a material fact necessary to make the

statements made, in light of the circumstances under which such

statements were made, not misleading with respect to the period covered

by this report;

3. Based on my knowledge, the financial statements and other financial

information included in this report, fairly present, in all material respects,

the financial condition, results of operations, and cash flows of the

registrant as of, and for, the periods presented in this report;

4. The registrant’s other certifying officer and I are responsible for

establishing and maintaining disclosure controls and procedures (as

CLASS ACTION COMPLAINT

9

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal

control over financial reporting (as defined in Exchange Act Rules 13a-

15(f) and 15d-15(f)) for the registrant and have:

(a) Designed such disclosure controls and procedures, or caused such

disclosure controls and procedures to be designed under our

supervision, to ensure that material information relating to the

registrant, including its consolidated subsidiaries, is made known

to us by others within those entities, particularly during the period

in which this report is being prepared;

(b) Designed such internal control over financial reporting, or caused

such internal control over financial reporting to be designed under

our supervision, to provide reasonable assurance regarding the

reliability of financial reporting and the preparation of the financial

statements for external purposes in accordance with generally

accepted accounting principles;

(c) Evaluated the effectiveness of the registrant’s disclosure controls

and procedures and presented in this report our conclusions about

the effectiveness of the disclosure controls and procedures, as of

the end of the period covered by this report based on such

evaluation; and

(d) Disclosed in this report any change in the registrant’s internal

control over financial reporting that occurred during the

registrant’s most recent fiscal quarter that has materially affected,

or is reasonably likely to materially affect, the registrant’s internal

control over financial reporting; and

5. The registrant’s other certifying officer and I have disclosed, based on our

most recent evaluation of internal control over financial reporting, to the

registrant’s auditors and the audit committee of the registrant’s Board of

Directors:

(a) All significant deficiencies and material weaknesses in the design

or operation of internal control over financial reporting which are

reasonably likely to adversely affect the registrant’s ability to

record, process, summarize, and report financial information; and

(b) Any fraud, whether or not material, that involves management or

other employees who have a significant role in the registrant’s

internal control over financial reporting.

CLASS ACTION COMPLAINT

10

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

19. On January 3, 2013, Calavo issued a press release entitled, “Calavo Growers, Inc.

Announces Fiscal 2012 Fourth Quarter and Full-Year Results.” Therein, the Company, in

relevant part, stated:

Fourth Quarter Highlights Include:

Net Income Climbs 69 Percent to a Quarterly Record of $6.2 Million from

$3.6 Million Last Year

Diluted EPS Equals $0.42 Versus $0.25 in Fiscal 2011 Final Quarter

Operating Results Paced by Strong Avocado Volumes—900,000 More

Units Packed from Year-Earlier Fourth Quarter

Gross Margin Jumps to a Quarterly Record of $17.9 Million, a 35 Percent

Increase from $13.2 Million in Year-Earlier Fourth Quarter

Full-Year Highlights Include:

Net Income Reaches New All-Time High of $18.9 Million before Effect

of $1.8 Million Mexican Tax Charge Which Reduced Net Income to $17.1

Million, a 54 Percent Increase from $11.1 Million Last Year

Diluted EPS of $1.27 before $0.12 Effect of Mexican Tax Item Which

Reduced Diluted EPS to $1.15 as Compared to $0.75 in Fiscal 2011

Gross Margin Soars 43 Percent to Record $60.7 Million from $42.3

Million

Revenues Grow to a New High of $551.1 Million from $522.5 Million

Last Year

Fiscal 2013 Outlook:

Company Announces Expectation for Record Operating Results

CEO Cole Reiterates Industry Avocado Forecast of 1.65 Billion Pounds

Calavo Foods Segment Anticipates Record Gross Profit on Guacamole

Revenue Growth

Calavo Growers, Inc. (Nasdaq-GS: CVGW), a global avocado-industry leader and

expanding provider of value-added fresh foods, today reported that fiscal 2012

fourth-quarter net income rose 69 percent to the highest quarterly net income in

company history from the fourth quarter last year. These results, which drove up

annual net income by 54 percent over prior year, were paced by “continued

operating strength across all three of Calavo’s business segments.”

Current-year, three-month and annual results for the company’s Renaissance Food

Group, LLC (RFG) business segment are now reported separately from the legacy

Calavo Foods business segment.

CLASS ACTION COMPLAINT

11

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

For the three months ended Oct. 31, 2012, net income advanced to a record $6.2

million, equal to $0.42 per diluted share, from $3.6 million, or $0.25 per diluted

share in the fiscal 2011 fourth quarter. Revenues totaled $141.6 million versus

$147.3 million in the fiscal 2011 fourth quarter, owing primarily to the decline in

fresh avocados prices which has resulted from the significantly larger current-year

fruit supply.

Gross margin in the final quarter advanced 35 percent to a record $17.9 million,

equal to 12.6 percent of total revenues, from $13.2 million, or 9.0 percent of total

revenues, in the corresponding quarter one year ago. Operating income increased

to $7.6 million, a 19 percent jump from $6.4 million in the fourth quarter of fiscal

2011.

Fourth-quarter selling, general and administrative (SG&A) expenses totaled $10.3

million, equal to 7.2 percent of revenues, versus $6.8 million, or 4.6 percent of

revenues, in the same quarter last year. The increased SG&A in the most-recent

quarter is principally attributable to costs associated with Calavo’s management-

incentive plan for surpassing earnings targets. SG&A as a percentage of gross

margin increased to 57.4 percent in the most recent quarter from 51.6 percent in

the year-earlier fourth quarter.

Chairman, President and CEO Lee E. Cole stated: “Calavo registered the single-

highest net income for any period in its history during the final quarter, enabling

us to post results for fiscal 2012 that are among its best ever, including revenues

and gross margin which shattered previous record highs. We benefited from

strong showings in each of our three business segments and this operating

momentum continues to validate the strategic blueprint we established for the

company—all indicators are trending favorably.”

Cole continued: “A substantially larger avocado harvest in California resulted in

Calavo packing nearly 900,000 more cartons of fruit in the final quarter than a

year earlier and approximately 2.4 million more units for the whole of fiscal 2012,

bringing to more than 12 million the total number packed. The significantly larger

crop paced volume through our unit-driven packinghouses and benefited Fresh

business segment and overall gross margin. As anticipated, our legacy Calavo

Foods business posted outstanding results for the quarter and full year,

capitalizing on higher sales and favorable fruit costs owing to a larger supply in

the marketplace which, in turn, fueled strong gross margins. And RFG, which

completed its initial full fiscal year as part of Calavo, performed to our

expectations and provided excellent incremental contribution to the company’s

top line.”

Cole added that the strength of Calavo’s operating results enabled it to return to

shareholders more than $9.6 million subsequent to fiscal-year end in the form of

the company’s annual cash dividend, which was increased by 18 percent from the

CLASS ACTION COMPLAINT

12

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

prior year to $0.65 per share. As point of note, since 2002 Calavo’s annual cash

dividend has risen consistently from $0.20 per share to its current payout level.

Net income for the fiscal year ended Oct. 31, 2012 climbed to $17.1 million,

equal to $1.15 per diluted share, from $11.1 million, or $0.75 per diluted share,

one year earlier. Fiscal 2012 results include the effect of a $1.8 million income tax

expense recorded in the second quarter related to an unfavorable ruling in a

disputed matter with Mexico’s tax authority’s examination of the 2004 tax year.

Net income for fiscal 2012 before the Mexican tax item was $18.9 million, equal

to $1.27 per diluted share.

Revenues for the most-recent year rose five percent to $551.1 million, a new

historic high, from $522.5 million in fiscal 2011. Annual gross margin climbed 43

percent to a record $60.7 million from $42.3 million in fiscal 2011 and eclipsing

the prior high of $51.5 million established two years earlier. Operating income

vaulted to $27.5 million in fiscal 2012, an increase of 50 percent from $18.3

million in the corresponding period one year ago.

In Calavo’s Fresh business segment, final-quarter revenues totaled $91.0 million,

down from $102.3 million in last year’s fourth quarter. The year-to-year decline

in segment revenues is indicative of the aforementioned, significantly larger

supply of avocados in the marketplace, as compared to fiscal 2011, which resulted

in substantially lower prices during the current year for the quarter. Total Fresh

segment volume totaled 3.7 million units in the most-recent quarter, increasing 29

percent from 2.9 million units shipped in the fourth quarter of fiscal 2011. Fresh

segment gross margin advanced to $11.4 million, or 12.5 percent of segment

sales, from $7.7 million, approximating 7.5 percent of segment sales, in last

year’s fourth quarter.

Revenues in the Calavo Foods business segment edged upward in the final quarter

to $11.6 million from $11.2 million in the fiscal 2011 fourth quarter. The business

unit—encompassing the company’s legacy products, including prepared

avocados, salsa and tortilla chips—continued to benefit from the aforementioned

larger supply of fruit in the marketplace and, to a less significant extent, improved

pricing. These factors proved beneficial to Calavo Foods’ gross margins in the

most recent quarter, which rose to $3.2 million, or 27.5 percent of that business

unit’s sales, from $2.7 million, or 23.9 percent of segment sales, one year ago.

RFG business segment revenues jumped 15 percent to $39.0 million from $33.9

million in the fourth quarter of fiscal 2011. RFG gross margin in the most-recent

quarter totaled $3.3 million, or 8.4 percent of segment sales, versus $2.9 million,

or 8.5 percent of segment sales, in the fiscal 2011 fourth quarter.

Outlook

CLASS ACTION COMPLAINT

13

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Calavo CEO Cole stated that “the company begins fiscal 2013 with considerable

operating momentum at its back. The same factors which powered our strong

performance in the recently concluded year continue unabated and, in fact, are

even showing early signs of accelerating. As a result of the growing velocity in

our businesses, I am confident that Calavo will register record net income and

per-share results in fiscal 2013.”

Cole continued, “This optimism is extremely well-founded. Early estimates for

the 2013 avocado supply are pegged to be at least 1.65 billion pounds, up from

about 1.4 billion pounds in the recently concluded year and 1.1 billion pounds in

2011. Calavo’s avocado market position places the company in the sweet spot of

an industry that’s booming around us. The surging supply, including a projected

increased harvest in California, should result in larger volume pouring into our

packinghouses which drive operating efficiencies and, by extension, gross

margins.

“Augmenting avocados, we anticipate larger tomato volume at higher prices

during the current year in the Fresh segment, which will be further bolstered by

our other diversified-produce offerings,” the CEO said.

“Our Calavo Foods business segment is increasingly a picture of strength,” Cole

continued, “with a growing pipeline of orders from customers for our prepared

avocado lineup. With continued favorable pricing of fruit, we expect to register

record gross profit in the Calavo Foods segment, building upon the gross-margin

performance which characterized fiscal 2012. We recently launched our latest

ultra-high-pressure product, avocado halves, which are attracting considerable

interest and attention among customers. This convenience product will be rolled

out broadly during the current year and we are genuinely excited about its

prospects.”

The CEO said, “RFG proceeds on plan with market penetration into the retail

grocery channel, as well as expanding consumer demand for its products from

consumers. The business unit’s robust product-development pipeline—as well as

its rapid order-fulfillment and just-in-time distribution of fresh, convenient and

healthful offerings—remain cornerstones of the RFG strategic blueprint.

“With so many platforms driving Calavo’s revenue and profit engines—all

performing exceptionally well—the company begins fiscal 2013 in an enviable

position and I look forward to a very successful year ahead,” Cole concluded.

20. On January 14, 2013, Calavo filed its Annual Report with the SEC on Form 10-K

for the 2012 fiscal year. The Company’s Form 10-K was signed by Defendants Cole and Brumo,

and reaffirmed the Company’s statements previously announced on January 3, 2013.

CLASS ACTION COMPLAINT

14

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

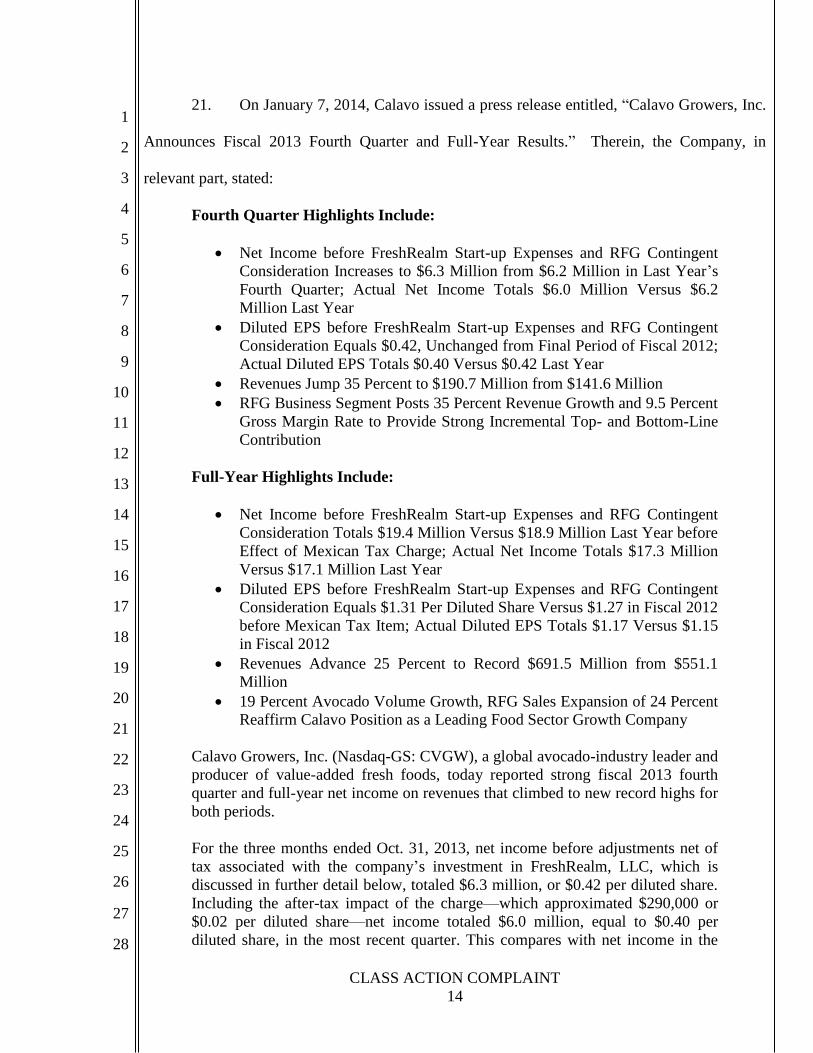

21. On January 7, 2014, Calavo issued a press release entitled, “Calavo Growers, Inc.

Announces Fiscal 2013 Fourth Quarter and Full-Year Results.” Therein, the Company, in

relevant part, stated:

Fourth Quarter Highlights Include:

Net Income before FreshRealm Start-up Expenses and RFG Contingent

Consideration Increases to $6.3 Million from $6.2 Million in Last Year’s

Fourth Quarter; Actual Net Income Totals $6.0 Million Versus $6.2

Million Last Year

Diluted EPS before FreshRealm Start-up Expenses and RFG Contingent

Consideration Equals $0.42, Unchanged from Final Period of Fiscal 2012;

Actual Diluted EPS Totals $0.40 Versus $0.42 Last Year

Revenues Jump 35 Percent to $190.7 Million from $141.6 Million

RFG Business Segment Posts 35 Percent Revenue Growth and 9.5 Percent

Gross Margin Rate to Provide Strong Incremental Top- and Bottom-Line

Contribution

Full-Year Highlights Include:

Net Income before FreshRealm Start-up Expenses and RFG Contingent

Consideration Totals $19.4 Million Versus $18.9 Million Last Year before

Effect of Mexican Tax Charge; Actual Net Income Totals $17.3 Million

Versus $17.1 Million Last Year

Diluted EPS before FreshRealm Start-up Expenses and RFG Contingent

Consideration Equals $1.31 Per Diluted Share Versus $1.27 in Fiscal 2012

before Mexican Tax Item; Actual Diluted EPS Totals $1.17 Versus $1.15

in Fiscal 2012

Revenues Advance 25 Percent to Record $691.5 Million from $551.1

Million

19 Percent Avocado Volume Growth, RFG Sales Expansion of 24 Percent

Reaffirm Calavo Position as a Leading Food Sector Growth Company

Calavo Growers, Inc. (Nasdaq-GS: CVGW), a global avocado-industry leader and

producer of value-added fresh foods, today reported strong fiscal 2013 fourth

quarter and full-year net income on revenues that climbed to new record highs for

both periods.

For the three months ended Oct. 31, 2013, net income before adjustments net of

tax associated with the company’s investment in FreshRealm, LLC, which is

discussed in further detail below, totaled $6.3 million, or $0.42 per diluted share.

Including the after-tax impact of the charge—which approximated $290,000 or

$0.02 per diluted share—net income totaled $6.0 million, equal to $0.40 per

diluted share, in the most recent quarter. This compares with net income in the

CLASS ACTION COMPLAINT

15

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

fiscal 2012 fourth quarter of $6.2 million, or $0.42 per diluted share. Fourth-

quarter revenues climbed 35 percent to reach $190.7 million from $141.6 million

in final period last year.

Gross margin equaled $17.4 million in the fiscal 2013 fourth quarter, which

compares with $17.9 million in the year-earlier like period. Operating income

edged higher to $8.1 million in the most recent quarter from $7.6 million in the

like period one year ago.

Chairman, President and Chief Executive Officer Lee E. Cole: “We completed

another successful year punctuated by a final quarter during which each of

Calavo’s three business segments continued to register outstanding revenue

growth and strong profitability—matching the fourth quarter record for net

income before giving effect to the FreshRealm investment.”

Cole continued: “Our top-line growth was paced by an ever-quickening expansion

of the avocado industry, which we continue to lead and innovate. We packed 2.3

million more fresh avocado cartons last year over fiscal 2012, almost 14.4 million

units in total, indicative of overall industry growth which reached nearly 1.7

billion pounds in 2013 as we had predicted. Demand continues to grow stronger

each year as avocados more and more become a staple in American diets. As the

company’s revenue acceleration indicates, Calavo is ideally situated to benefit

from the strong avocado trend. Beyond fresh avocados, we enjoyed double-digit

revenue growth for the quarter and the year in our other two business segments—

Calavo Foods and Renaissance Food Group, LLC (RFG)— further moving the

sales needle upward.

“And, while growing revenues and profit year over year—indicative of the

enduring strength of the Calavo business model—we remained committed to

delivering return to our shareholders. The company’s substantial profitability

enabled us to return more than $11.0 million to shareholders through Calavo’s

annual common stock cash dividend. Enviably, the 70 cent per share payout was a

7.7 percent increase from the prior year and a 250 percent rise since the company

became publicly traded in 2002,” Cole stated.

Net income for the fiscal-year-ended Oct. 31, 2013 totaled $17.3 million, equal to

$1.17 per diluted share, which compares with $17.1 million, or $1.15 per diluted

share, one year earlier. Results for the most recent year reflect an after-tax impact

approximating $2.1 million, equal to $0.14 per diluted share, associated with

FreshRealm-related investment ($0.9 million or $0.06 per diluted share) and

contingent consideration for the company’s earlier purchase of RFG ($1.2 million

or $0.08 per diluted share). The after-tax impact of these charges had the effect of

reducing fiscal 2013 net income from about $19.4 million or $1.31 per diluted

share. This compares with full-year net income in fiscal 2012 of $18.9 million,

equal to $1.27 per diluted share, before giving effect to a $1.8 million income tax

CLASS ACTION COMPLAINT

16

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

expense related to an unfavorable ruling with Mexico’s tax authority’s

examination of the 2004 tax year.

Full-year revenues climbed 25 percent to a record $691.5 million from $551.1

million in fiscal 2012. Gross margin was substantially unchanged, standing at

$60.1 million in the most-recent year versus $60.7 million in fiscal 2012.

Operating income declined to $25.1 million in fiscal 2013 from a year-earlier total

of $27.5 million.

Revenues in Calavo’s Fresh business segment surged 38 percent in the fourth

quarter to $125.2 million from $91.0 million in the corresponding period last year

driven by volume growth and sharply higher prices in the avocado category. Total

Fresh segment volume approximated 3.8 million units in the final period,

unchanged from the fiscal 2012 fourth quarter. Fresh segment gross margin

registered $11.1 million, equal to 8.7 percent of segment sales. This compares

with segment gross margin of $11.4 million, or 12.5 percent of segment sales, in

last year’s fourth quarter.

Calavo Foods business segment revenues rose to $12.9 million, up 12 percent

from $11.6 million in the final quarter of fiscal 2012. Sharply higher fruit costs

for prepared avocado products during the majority of the fourth quarter adversely

impacted segment gross margin for the period. Gross margin declined to $1.3

million, or 10.2 percent of segment sales, from $3.2 million or 27.5 percent of

segment sales, in the final quarter last year.

RFG business segment revenues advanced 35 percent to $52.6 million from $39.0

million in the fiscal 2012 final quarter. Top-line growth in the RFG segment

continued to be propelled by a combination of factors including additional retail

penetration to more sales points and an expanding product lineup, the company

reported. RFG gross margin equaled $5.0 million, or 9.5 percent of segment sales,

a 110 basis point improvement from $3.3 million, or 8.4 percent of segment sales,

in the fourth period last year. RFG segment gross margin growth is attributable to

the continued leveraging of the business unit’s plants and platform, which also

provided incremental contribution to Calavo’s improved overall selling, general

and administrative (SG&A) metrics.

Fourth-quarter SG&A expense totaled $9.3 million, equal to 4.9 percent of

revenues, improving about 230 basis points from $10.3 million, or 7.2 percent of

revenues, in the final period last year. In the most recent period, SG&A dropped

significantly even after $597,000 in pre-tax expenses related to its FreshRealm

investment and while supporting nearly $50 million in additional company sales,

indicative of substantial leveraging of Calavo platforms. As a percentage of gross

margin, SG&A decreased 390 basis points to 53.5 percent from 57.4 percent in

the fourth quarter last year.

Outlook

CLASS ACTION COMPLAINT

17

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

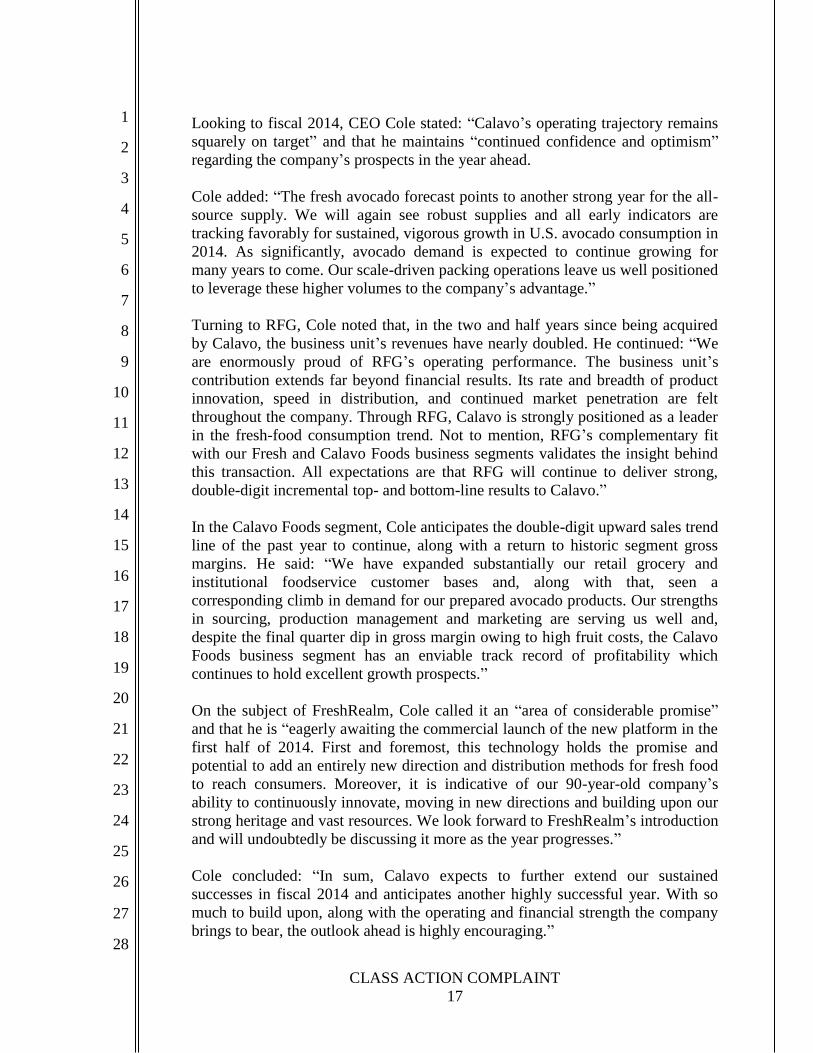

Looking to fiscal 2014, CEO Cole stated: “Calavo’s operating trajectory remains

squarely on target” and that he maintains “continued confidence and optimism”

regarding the company’s prospects in the year ahead.

Cole added: “The fresh avocado forecast points to another strong year for the all-

source supply. We will again see robust supplies and all early indicators are

tracking favorably for sustained, vigorous growth in U.S. avocado consumption in

2014. As significantly, avocado demand is expected to continue growing for

many years to come. Our scale-driven packing operations leave us well positioned

to leverage these higher volumes to the company’s advantage.”

Turning to RFG, Cole noted that, in the two and half years since being acquired

by Calavo, the business unit’s revenues have nearly doubled. He continued: “We

are enormously proud of RFG’s operating performance. The business unit’s

contribution extends far beyond financial results. Its rate and breadth of product

innovation, speed in distribution, and continued market penetration are felt

throughout the company. Through RFG, Calavo is strongly positioned as a leader

in the fresh-food consumption trend. Not to mention, RFG’s complementary fit

with our Fresh and Calavo Foods business segments validates the insight behind

this transaction. All expectations are that RFG will continue to deliver strong,

double-digit incremental top- and bottom-line results to Calavo.”

In the Calavo Foods segment, Cole anticipates the double-digit upward sales trend

line of the past year to continue, along with a return to historic segment gross

margins. He said: “We have expanded substantially our retail grocery and

institutional foodservice customer bases and, along with that, seen a

corresponding climb in demand for our prepared avocado products. Our strengths

in sourcing, production management and marketing are serving us well and,

despite the final quarter dip in gross margin owing to high fruit costs, the Calavo

Foods business segment has an enviable track record of profitability which

continues to hold excellent growth prospects.”

On the subject of FreshRealm, Cole called it an “area of considerable promise”

and that he is “eagerly awaiting the commercial launch of the new platform in the

first half of 2014. First and foremost, this technology holds the promise and

potential to add an entirely new direction and distribution methods for fresh food

to reach consumers. Moreover, it is indicative of our 90-year-old company’s

ability to continuously innovate, moving in new directions and building upon our

strong heritage and vast resources. We look forward to FreshRealm’s introduction

and will undoubtedly be discussing it more as the year progresses.”

Cole concluded: “In sum, Calavo expects to further extend our sustained

successes in fiscal 2014 and anticipates another highly successful year. With so

much to build upon, along with the operating and financial strength the company

brings to bear, the outlook ahead is highly encouraging.”

CLASS ACTION COMPLAINT

18

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

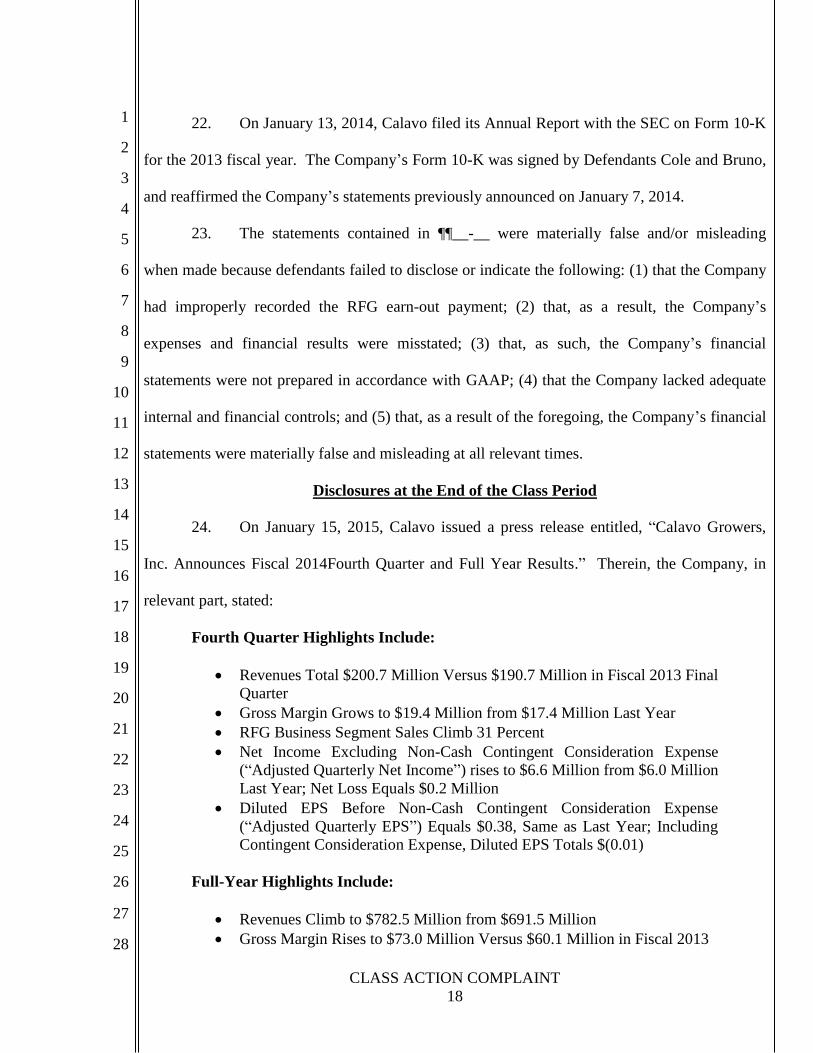

22. On January 13, 2014, Calavo filed its Annual Report with the SEC on Form 10-K

for the 2013 fiscal year. The Company’s Form 10-K was signed by Defendants Cole and Bruno,

and reaffirmed the Company’s statements previously announced on January 7, 2014.

23. The statements contained in ¶¶__-__ were materially false and/or misleading

when made because defendants failed to disclose or indicate the following: (1) that the Company

had improperly recorded the RFG earn-out payment; (2) that, as a result, the Company’s

expenses and financial results were misstated; (3) that, as such, the Company’s financial

statements were not prepared in accordance with GAAP; (4) that the Company lacked adequate

internal and financial controls; and (5) that, as a result of the foregoing, the Company’s financial

statements were materially false and misleading at all relevant times.

Disclosures at the End of the Class Period

24. On January 15, 2015, Calavo issued a press release entitled, “Calavo Growers,

Inc. Announces Fiscal 2014Fourth Quarter and Full Year Results.” Therein, the Company, in

relevant part, stated:

Fourth Quarter Highlights Include:

Revenues Total $200.7 Million Versus $190.7 Million in Fiscal 2013 Final

Quarter

Gross Margin Grows to $19.4 Million from $17.4 Million Last Year

RFG Business Segment Sales Climb 31 Percent

Net Income Excluding Non-Cash Contingent Consideration Expense

(“Adjusted Quarterly Net Income”) rises to $6.6 Million from $6.0 Million

Last Year; Net Loss Equals $0.2 Million

Diluted EPS Before Non-Cash Contingent Consideration Expense

(“Adjusted Quarterly EPS”) Equals $0.38, Same as Last Year; Including

Contingent Consideration Expense, Diluted EPS Totals $(0.01)

Full-Year Highlights Include:

Revenues Climb to $782.5 Million from $691.5 Million

Gross Margin Rises to $73.0 Million Versus $60.1 Million in Fiscal 2013

CLASS ACTION COMPLAINT

19

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

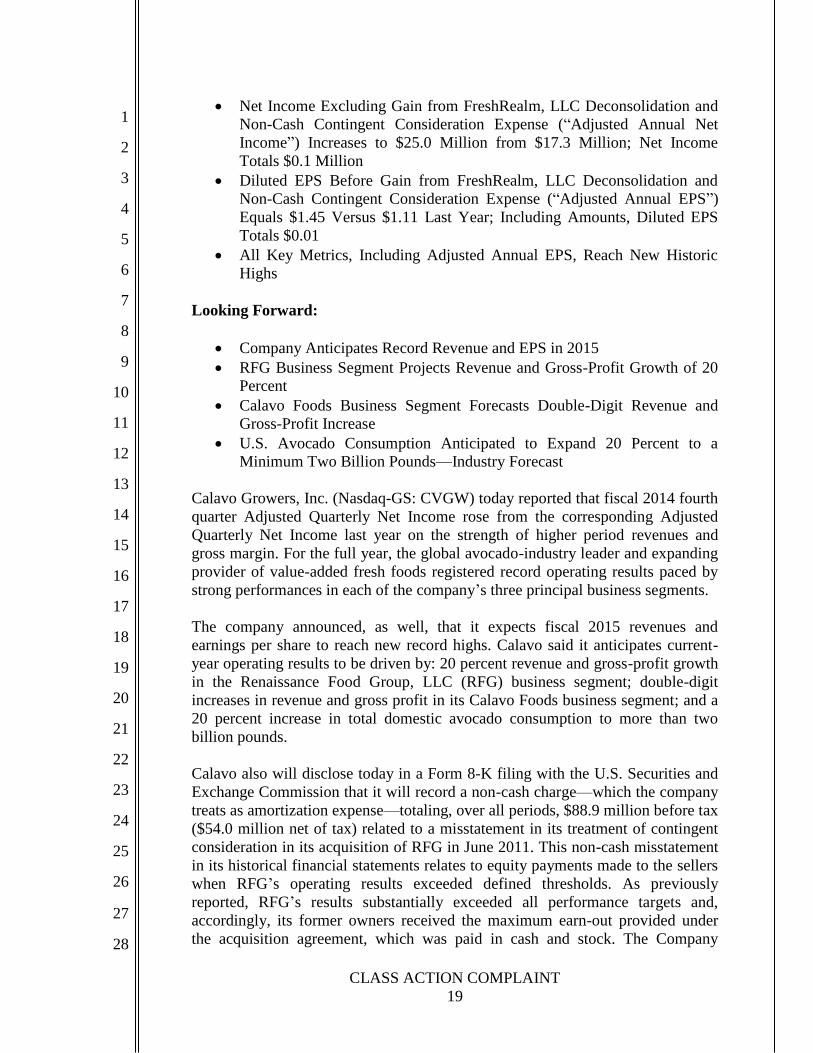

Net Income Excluding Gain from FreshRealm, LLC Deconsolidation and

Non-Cash Contingent Consideration Expense (“Adjusted Annual Net

Income”) Increases to $25.0 Million from $17.3 Million; Net Income

Totals $0.1 Million

Diluted EPS Before Gain from FreshRealm, LLC Deconsolidation and

Non-Cash Contingent Consideration Expense (“Adjusted Annual EPS”)

Equals $1.45 Versus $1.11 Last Year; Including Amounts, Diluted EPS

Totals $0.01

All Key Metrics, Including Adjusted Annual EPS, Reach New Historic

Highs

Looking Forward:

Company Anticipates Record Revenue and EPS in 2015

RFG Business Segment Projects Revenue and Gross-Profit Growth of 20

Percent

Calavo Foods Business Segment Forecasts Double-Digit Revenue and

Gross-Profit Increase

U.S. Avocado Consumption Anticipated to Expand 20 Percent to a

Minimum Two Billion Pounds—Industry Forecast

Calavo Growers, Inc. (Nasdaq-GS: CVGW) today reported that fiscal 2014 fourth

quarter Adjusted Quarterly Net Income rose from the corresponding Adjusted

Quarterly Net Income last year on the strength of higher period revenues and

gross margin. For the full year, the global avocado-industry leader and expanding

provider of value-added fresh foods registered record operating results paced by

strong performances in each of the company’s three principal business segments.

The company announced, as well, that it expects fiscal 2015 revenues and

earnings per share to reach new record highs. Calavo said it anticipates current-

year operating results to be driven by: 20 percent revenue and gross-profit growth

in the Renaissance Food Group, LLC (RFG) business segment; double-digit

increases in revenue and gross profit in its Calavo Foods business segment; and a

20 percent increase in total domestic avocado consumption to more than two

billion pounds.

Calavo also will disclose today in a Form 8-K filing with the U.S. Securities and

Exchange Commission that it will record a non-cash charge—which the company

treats as amortization expense—totaling, over all periods, $88.9 million before tax

($54.0 million net of tax) related to a misstatement in its treatment of contingent

consideration in its acquisition of RFG in June 2011. This non-cash misstatement

in its historical financial statements relates to equity payments made to the sellers

when RFG’s operating results exceeded defined thresholds. As previously

reported, RFG’s results substantially exceeded all performance targets and,

accordingly, its former owners received the maximum earn-out provided under

the acquisition agreement, which was paid in cash and stock. The Company

CLASS ACTION COMPLAINT

20

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

recorded contingent consideration expense related to the acquisition of RFG

totaling $54.0 million for fiscal year 2014, as compared to $32.3 million in fiscal

2013, as well as $12.9 million for the fourth fiscal quarter of 2014, as compared to

$18.8 million for the fourth fiscal quarter of 2013. There will be no further

charges with respect to the RFG acquisition agreement. As point of note, under

Calavo ownership RFG revenues have grown from a fiscal 2011 “run rate” of

$94.1 million to $252.3 million for the fiscal year ended Oct. 31, 2014. In that

same period, RFG EBITDA has risen from $2.6 million to $16.0 million.

Initially, Calavo recorded the contingent consideration, which was settleable in

common stock, as an equity instrument and, therefore, did not record expense

based on the changes in fair value of the contingent consideration. The company

now believes, however, that the contingent consideration should have been

accounted for as a liability, requiring re-measurement to fair value and expense

recognition, which Calavo is treating as amortization expense, at each reporting

period subsequent to the acquisition. Further, all information related to the

specifics of payments of the RFG earn-out payment has been accurately explained

in all of the company’s filings and all payments have been accurately settled.

Addressing the restatement, Chairman, President and Chief Executive Officer Lee

E. Cole stated: “Let me underscore that the contingent consideration liability is a

non-cash charge. It has no impact on Calavo’s cash position whatsoever. Further,

the change does not alter either the company’s historical or current earnings

before interest, taxes, depreciation and amortization (EBITDA) and has no impact

on the company going forward. Furthermore, there will be no additional non-cash

charges, as this transaction is now completed, and all details of the earn-out have

been correctly outlined in all SEC filings over the last three-and-a-half years.”

Cole continued: “It is a unique accounting issue related to structuring the purchase

with a large earn-out component. To that end, we believe that reporting adjusted

annual and quarterly net income and adjusted per-share results for these related

periods—exclusive of the earn-out-specific, non-cash charge as we are doing in

this release—provides the most meaningful way to look at the profitability,

underlying strength and on-going performance of Calavo’s businesses. Finally, it

is important to reiterate that the success of the RFG transaction itself triggered

this charge, and is a reflection of acquiring that business on risk-averse terms.”

For the three months ended Oct. 31, 2014, Adjusted Quarterly Net Income grew

by 8.6 percent to $6.6 million, or $0.38 per diluted share, which compares with

$6.0 million, equal to $0.38 per diluted share, in the final quarter last year. (Note:

the company’s diluted number of shares increased by approximately 1.4 million

shares and 0.7 million shares in the fourth quarter 2014 and 2013, respectively,

related to the issuance of shares to complete the acquisition of RFG.) After giving

effect to the non-cash contingent consideration expense, net loss in the most

recent fourth quarter totaled $0.2 million, or ($0.01) per diluted share. Revenues

CLASS ACTION COMPLAINT

21

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

rose to $200.7 million in the most recent fourth quarter, an increase of 5.3 percent

from $190.7 million in the fiscal 2013 final quarter.

Fourth-quarter gross margin expanded by 11.7 percent, or $2.0 million, to $19.4

million, or 9.7 percent of sales, from $17.4 million, or 9.1 percent of sales, in the

year-earlier final quarter.

CEO Cole stated: “In sum, it was an outstanding final quarter and year for Calavo

as measured by our formidable results from operations. Our company posted

strong final-quarter results to cap a record-breaking fiscal 2014, during which all

important metrics reached new historic highs. Of particular note, Calavo’s

operating performance in the most-recent period reflects the beneficial impact of

sourcing and marketing Mexico-grown avocados, which improved Fresh business

segment gross margin and counterbalanced the cyclically smaller harvest of

California fruit.”

The Calavo CEO continued: “We registered sharply improved gross margin in our

Calavo Foods business segment—a result of favorable fruit and production costs,

as well as significant year-over-year improvement in segment sales—which

further contributed to the uptick in overall company gross margin.

“Finally, sales in the RFG business segment rose by more than 31 percent in the

most-recent quarter. RFG continues to execute impressively—penetrating the

retail grocery channel with its broad line of refrigerated fresh packaged goods. Its

operating performance made significant incremental contribution to Calavo’s top

and bottom lines during fiscal 2014.

“On the strength of Calavo’s record-breaking operating results, we were able to

once again affirm management’s commitment to delivering the highest possible

shareholder returns, increasing the annual cash dividend on our common stock by

seven percent to $0.75 per share,” Cole said.

In addition to the RFG contingent consideration expense, full-year results include

a $12.6 million gain related to Calavo’s previously disclosed deconsolidation of

its FreshRealm, LLC subsidiary last May. Adjusted Annual Net Income for the

fiscal-year-ended Oct. 31, 2014 equaled $25.0 million, or $1.45 per diluted share,

an increase of 44 percent from $17.3 million, or $1.11 per diluted share, in fiscal

2013. Including the gain from the FreshRealm deconsolidation ($0.48 per share)

and RFG contingent consideration expense ($1.44 per share), net income for

fiscal 2014 totaled $0.1 million, equal to $0.01 per diluted share.

Revenues for the most-recent year rose 13.2 percent to $782.5 million, a new

historic high, from $691.5 million in fiscal 2013, which was the previous record.

Gross margin eclipsed last year’s high by climbing $12.9 million, or 21.5 percent,

to reach $73.0 million, equal to 9.3 percent of sales, from $60.1 million, or 8.7

percent of sales in fiscal 2013.

CLASS ACTION COMPLAINT

22

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

Fourth quarter revenues in the Fresh business segment totaled $117.4 million.

This compares with segment revenues of $125.2 million in the like quarter one

year earlier. Fresh gross margin equaled $10.7 million, or 9.1 percent of segment

sales, versus $11.1 million, or 8.9 percent of segment sales in the fiscal 2013

fourth quarter. The company packed 3.6 million total Fresh units in the most-

recent quarter, which compares with about 3.8 million units a year ago. The

modest decline in total units is attributable principally to the aforementioned

smaller California avocado harvest and, to a lesser extent, slightly fewer papaya

and pineapple units packed in the period. This dip in total Fresh units was offset

by a 20-basis-point improvement in segment gross margin owing primarily to

Mexico-grown avocados and papayas.

Calavo Foods business segment revenues in the most recent quarter rose 9.8

percent to $14.2 million from $12.9 million in the like fiscal 2013 quarter. Calavo

Foods gross margin more than doubled to $2.8 million, equal to 19.4 percent of

segment sales, from $1.3 million, or 10.2 percent of segment sales, one year ago.

Margin gains in the business segment are directly attributable to: increased

throughput resulting from higher sales to the retail grocery and foodservice

channels, coupled with the beneficial avocado pricing and improved production

management from the prior year, noted CEO Cole.

RFG business segment revenues grew by 31.5 percent to $69.1 million from

$52.6 million in the fourth quarter of fiscal 2013. RFG gross margin rose by

nearly $1 million to $5.9 million, or 8.6 percent of segment sales, which compares

with $5.0 million, or 9.5 percent of segment sales, in the corresponding quarter

last year. Despite substantially higher RFG business segment revenues, gross

margin in the most-recent period was adversely impacted mainly by higher raw

material costs in the month of October.

Selling, general and administrative (SG&A) expense totaled $9.6 million, or 4.8

percent of revenues, in the most recent quarter. This compares with $9.5 million,

or 5.0 percent of revenues, in the fiscal 2013 fourth quarter. SG&A as a

percentage of gross margin equaled 49.2 percent in this year’s final quarter,

versus 54.8 percent in the corresponding period last year.

Outlook

Calavo begins fiscal 2015 “with all indicators pointing affirmatively,” said Cole.

“By all industry and company expectations, fresh avocado consumption is

expected to resume its upward advance in the coming year after a ‘breather’ in

2014 from the dramatic growth of the past decade. According to industry

forecasts, U.S. fresh avocado consumption, based on the all-source avocado

availability from California, Mexico and South America, is on track to exceed two

billion pounds in the current year.

CLASS ACTION COMPLAINT

23

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

“With our avocado market leadership—strong sourcing capabilities, sales and

distribution expertise, and the vast breadth of resources Calavo brings to bear—

we will be beneficiaries of the upward consumption trendline. The consistently

large Mexico crop, an expected resurgent California avocado harvest, which

adversely affected the all-source fruit supply last year and, most importantly,

strong consumer demand, all point to a brightening picture for fiscal 2015.”

Cole continued: “Under Calavo ownership, RFG has achieved outstanding sales

and profit growth. This fast-growth business unit has exceeded every performance

target set for it, while expanding the company in a meaningful way into the

refrigerated fresh packaged goods segment of the retail grocery channel—one of

the industry’s fastest growing sectors. We believe this category remains poised for

further growth and RFG is well positioned with a great portfolio of offerings,

augmented by formidable product-development capabilities. Its ability to produce

on-demand and strength in ‘just-in-time’ distribution have us optimistic about the

future. Consequently, we expect RFG will continue to be a strong performer and

project revenue and gross-profit growth in this business segment of 20 percent in

fiscal 2015.

“Most significantly, RFG is a testament to this company’s ability to identify

outstanding acquisition targets, complete transactions on competitive terms and

then integrate and grow them within Calavo,” Cole stated.

With respect to Calavo Foods, Cole said that the unit’s operating performance “is

trending strong,” with certain economies of scale and efficiencies resulting from

sales growth, sound production management and beneficial raw ingredient costs.

We are seeing fruit costs moderate and margins returning toward historical levels.

Additionally, the 15 percent increase in segment revenues in fiscal 2014—with

sales climbing in both the retail and foodservice categories—leaves us confident

about prospects for future growth, with revenue and gross profit pegged to expand

by double digits in fiscal 2015.”

Finally, Cole stated that new initiatives, such as Calavo’s 50 percent investment in

FreshRealm, offer growth potential “into related categories with considerable

promise. FreshRealm brings an entirely new dimension to the distribution and

consumption of fresh foods and, while it’s early in the game, we are looking

forward to watching its progress in fiscal 2015,” he said.

“With the momentum of the company’s (adjusted) record-breaking fiscal 2014

squarely at Calavo’s back, we begin the current year in a very strong position.

Calavo will continue to execute its focused strategic agenda and to employ our

disciplined approach to operations that are the cornerstones of the company’s

success. I look forward to another successful year in fiscal 2015 and anticipate

reporting another record year in both revenue and EPS,” Cole concluded.

CLASS ACTION COMPLAINT

24

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

25. On this news, shares of Calavo declined $4.72 per share, nearly 10%, to close on

January 15, 2014, at $43.07 per share, on unusually heavy volume.

CALAVO’S VIOLATION OF GAAP RULES

IN ITS FINANCIAL STATEMENTS

FILED WITH THE SEC

26. These financial statements and the statements about the Company’s financial

results were false and misleading, as such financial information was not prepared in conformity

with GAAP, nor was the financial information a fair presentation of the Company’s operations

due to the Company’s improper recording of the earn-out payment to RFG, in violation of GAAP

rules.

27. GAAP are those principles recognized by the accounting profession as the

conventions, rules and procedures necessary to define accepted accounting practice at a

particular time. Regulation S-X (17 C.F.R. § 210.4-01(a)(1)) states that financial statements

filed with the SEC which are not prepared in compliance with GAAP are presumed to be

misleading and inaccurate. Regulation S-X requires that interim financial statements must also

comply with GAAP, with the exception that interim financial statements need not include

disclosure which would be duplicative of disclosures accompanying annual financial statements.

17 C.F.R. § 210.10-01(a).

28. The fact that Calavo announced that its financial statements will need to be

restated, and informed investors that these financial statements should not be relied upon is an

admission that they were false and misleading when originally issued (APB No.20, 7-13; SFAS

No. 154, 25).

29. Given these accounting irregularities, the Company announced financial results

that were in violation of GAAP and the following principles:

CLASS ACTION COMPLAINT

25

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

(a) The principle that “interim financial reporting should be based upon the

same accounting principles and practices used to prepare annual financial statements” was

violated (APB No. 28, 10);

(b) The principle that “financial reporting should provide information that is

useful to present to potential investors and creditors and other users in making rational

investment, credit, and similar decisions” was violated (FASB Statement of Concepts No. 1, 34);

(c) The principle that “financial reporting should provide information about

the economic resources of Calavo, the claims to those resources, and effects of transactions,

events, and circumstances that change resources and claims to those resources” was violated

(FASB Statement of Concepts No. 1, 40);

(d) The principle that “financial reporting should provide information about

Calavo’s financial performance during a period” was violated (FASB Statement of Concepts No.

1, 42);

(e) The principle that “financial reporting should provide information about

how management of Calavo has discharged its stewardship responsibility to owners

(stockholders) for the use of Calavo resources entrusted to it” was violated (FASB Statement of

Concepts No. 1, 50);

(f) The principle that “financial reporting should be reliable in that it

represents what it purports to represent” was violated (FASB Statement of Concepts No. 2, 58-

59);

(g) The principle that “completeness, meaning that nothing is left out of the

information that may be necessary to insure that it validly represents underlying events and

conditions” was violated (FASB Statement of Concepts No. 2, 79); and

CLASS ACTION COMPLAINT

26

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

(h) The principle that “conservatism be used as a prudent reaction to

uncertainty to try to ensure that uncertainties and risks inherent in business situations are

adequately considered” was violated (FASB Statement of Concepts No. 2, 95).

30. The adverse information concealed by Defendants during the Class Period and

detailed above was in violation of Item 303 of Regulation S-K under the federal securities law

(17 C.F.R. §229.303).

CLASS ACTION ALLEGATIONS

31. Plaintiff brings this action as a class action pursuant to Federal Rule of Civil

Procedure 23(a) and (b)(3) on behalf of a class, consisting of all those who purchased or

otherwise acquired Calavo’s securities between March 5, 2012 and January 14, 2015, inclusive

and who were damaged thereby (the “Class”). Excluded from the Class are Defendants, the

officers and directors of the Company, at all relevant times, members of their immediate families

and their legal representatives, heirs, successors or assigns and any entity in which Defendants

have or had a controlling interest.

32. The members of the Class are so numerous that joinder of all members is

impracticable. Throughout the Class Period, Calavo’s securities were actively traded on the

Nasdaq Stock Market (“NASDAQ”). While the exact number of Class members is unknown to

Plaintiff at this time and can only be ascertained through appropriate discovery, Plaintiff believes

that there are hundreds or thousands of members in the proposed Class. Millions of Calavo

shares were traded publicly during the Class Period on the NASDAQ. As of July 31, 2014,

Calavo had 15,762,405 shares of common stock outstanding. Record owners and other members

of the Class may be identified from records maintained by Calavo or its transfer agent and may

be notified of the pendency of this action by mail, using the form of notice similar to that

CLASS ACTION COMPLAINT

27

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

customarily used in securities class actions.

33. Plaintiff’s claims are typical of the claims of the members of the Class as all

members of the Class are similarly affected by Defendants’ wrongful conduct in violation of

federal law that is complained of herein.

34. Plaintiff will fairly and adequately protect the interests of the members of the

Class and has retained counsel competent and experienced in class and securities litigation.

35. Common questions of law and fact exist as to all members of the Class and

predominate over any questions solely affecting individual members of the Class. Among the

questions of law and fact common to the Class are:

(a) whether the federal securities laws were violated by Defendants’ acts as

alleged herein;

(b) whether statements made by Defendants to the investing public during the

Class Period omitted and/or misrepresented material facts about the business, operations, and

prospects of Calavo; and

(c) to what extent the members of the Class have sustained damages and the

proper measure of damages.

36. A class action is superior to all other available methods for the fair and efficient

adjudication of this controversy since joinder of all members is impracticable. Furthermore, as

the damages suffered by individual Class members may be relatively small, the expense and

burden of individual litigation makes it impossible for members of the Class to individually

redress the wrongs done to them. There will be no difficulty in the management of this action as

a class action.

UNDISCLOSED ADVERSE FACTS

CLASS ACTION COMPLAINT

28

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

37. The market for Calavo’s securities was open, well-developed and efficient at all

relevant times. As a result of these materially false and/or misleading statements, and/or failures

to disclose, Calavo’s securities traded at artificially inflated prices during the Class Period.

Plaintiff and other members of the Class purchased or otherwise acquired Calavo’s securities