global communications gaap summit 2014 - pwc communications gaap summit 2014 eurostars madrid tower,...

TRANSCRIPT

Global Communications GAAP Summit 2014

Eurostars Madrid Tower, Madrid 23-24 June

Paul Barkus Welcome and introduction

PwC

Welcome and introduction

Slide 3

June 2014 Global Communications GAAP Summit

PwC

Navigating change

Global Communications GAAP Summit June 2014

There is nothing wrong with change, if it is in the right direction. Sir Winston Churchill

Slide 4

PwC

Navigating change – what are we seeing?

Global Communications GAAP Summit

Slide 5

June 2014

Consolidation driving an increase in M&A

Convergence of technologies - fixed, mobile, broadcasters

Move from being technology led with customer preferences driving strategies

Innovative financing structures for consumers

New network funding models

Increased activity around accounting standards and regulation

PwC

What’s in the news? (Organic growth)

Slide 6

Global Communications GAAP Summit June 2014

PwC

What’s in the news? (Inorganic growth)

Slide 7

Global Communications GAAP Summit June 2014

PwC

This is your summit...

Slide 8

Global Communications GAAP Summit June 2014

PwC

Global Communications GAAP Summit June 2014

Agenda

Monday 23 June

Time Session

15:00 – 15:45 Registration

15:45 – 16:00 Introduction and welcome

16:00 – 18:00 Navigating change and putting it into practice - how do you tell your story?

18.30 Buses depart for dinner

Today

Slide 9

PwC

Global Communications GAAP Summit June 2014

Agenda

Tuesday 24 June

Time Session

08.00 – 08:15 Introduction

08.15 – 09:00 What’s new in accounting?

09:00 – 09:30 Telefónica market update

09:30 – 10:15 Coffee break

10.15 – 12:15 Workshop 1: Inorganic growth

12.15 – 13.30 Lunch

13.30 - 15.30 Workshop 2: Organic growth

15.30 - 16.00 Closing remarks

Tomorrow

Slide 10

PwC

Administration

Slide 11

Global Communications GAAP Summit June 2014

Global Communications Summit 2014

Navigating change - putting it into practice June 2014

www.pwc.com

PwC

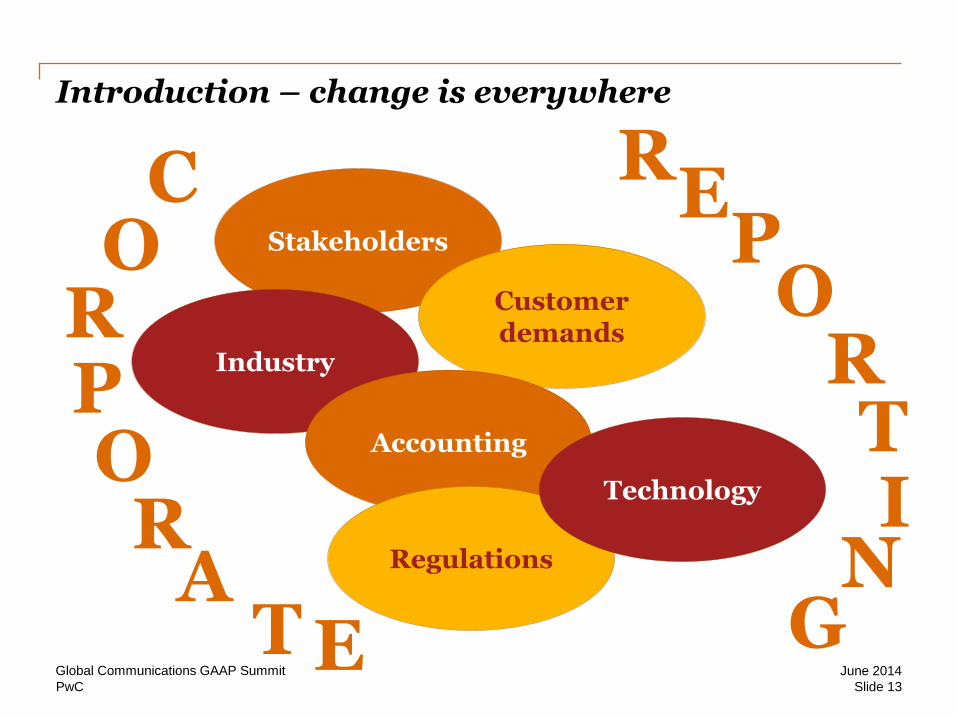

Introduction – change is everywhere

C O

R P O

R A

T E

R E

P O

R T I

N G

Stakeholders

Industry

Customer demands

Accounting

Regulations

Technology

Global Communications GAAP Summit

Slide 13

June 2014

Discussion Panel

The Telco Trends for 2014+

June, 2014 Jose F. Arias / Jose A. Tortosa

VicePresidents (CMT Practice)

Strategy&

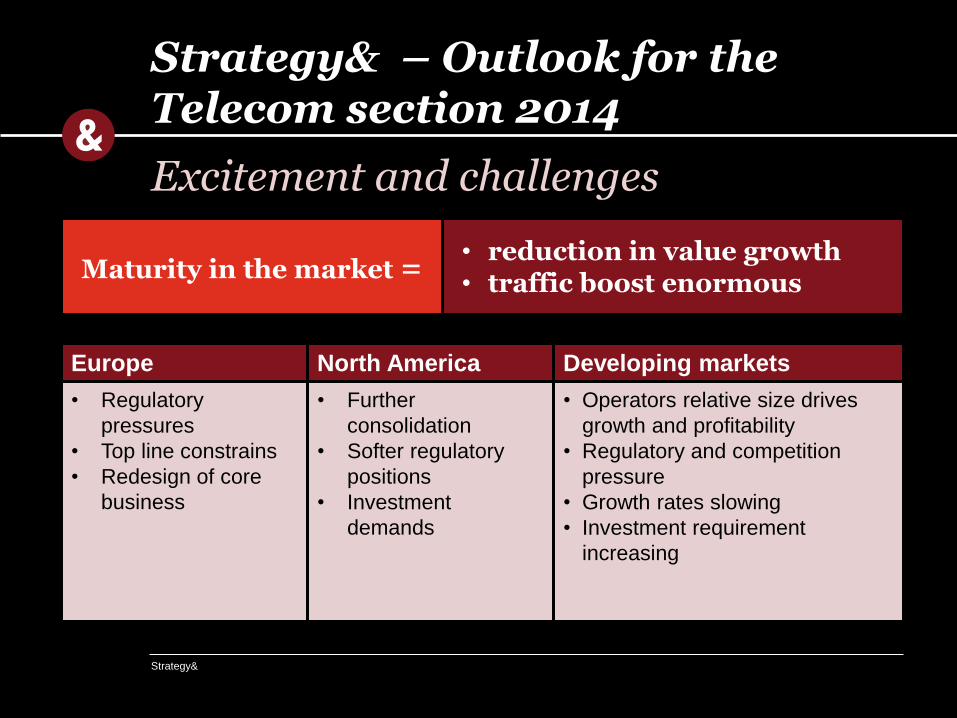

Strategy& – Outlook for the Telecom section 2014

Excitement and challenges

• reduction in value growth • traffic boost enormous

Maturity in the market =

Europe North America Developing markets

• Regulatory

pressures

• Top line constrains

• Redesign of core

business

• Further

consolidation

• Softer regulatory

positions

• Investment

demands

• Operators relative size drives

growth and profitability

• Regulatory and competition

pressure

• Growth rates slowing

• Investment requirement

increasing

Strategy&

Four major industry drivers

Convergence

• 3P/4P becoming the usual offering,…

• …, and buying behavior • Multi-device access

demanded

Competition

• Increasing • Emergence of MVNOs

and arbitrage players • Consolidation of

vendors, device manufacturers

Adjacencies

• OTT • Blurring boundaries

between competitors and collaborators

Regulations

• Stronger quality controls and times

• Decrease of MTRs • Open access • Shift from telecom to

competition law

EU cable players requesting MVNO license to offer 3P/4P

EU incumbents launching 4P in 2012/2013

3P/4P household penetration in Spain in 18 months

10

+40%

+40%

Growth in smartphone adoption cause 4% loss of messaging services to just below $104 Bn

Billion messages a day sent over Whatsapp

Drop in SMS revenues, witnessed by KPN

42%

20%

20

Sector Growth 2005-2013

–# of telecom operators

– Industry revenues

MVNO competition (2013)

–# of MVNOs worldwide

–# of MVNOs in Germany

Million dollar antitrust fine on international telco for abusing dominant position on the Internet market

Countries impose unbundling of copper and fiber

Yearly Drop in MTRs Germany 2007-2013

60

200

+70%

1%

111

1207

-18%

Demand for

investment

(data boost)

Consolidation

of players Digitization

A B C

Strategy&

Convergence

Operator

Bundle

✓ ✓ ✓ ✓ ✓ ✓

✓ ✗ ✓ ✗ ✗ ✓

✓ ✓ ✓ ✗ ✗ ✓

✓ ✗ ✓ ✗ ✓ ✗

✗ ✗ ✓ ✗ ✗ (✓)

✗ ✗ ✓ ✓ ✓ ✓

✗ ✗ ✓ ✓ ✓ ✗

✗ ✗ ✗ (✓) ✓ ✓

Discount

Overview of Bundled Offers of European Incumbents

Strategy&

Competition

MVNOs & Secondary Brands Market Share, 2013 (%)

40% 40%

24%14% 13% 11% 10%5%

MVNOs MNOs

15-20%

Convergent market

Convergent market

Convergent market

45%

convergent

market

Convergent market

60%

convergent

market

10%

convergent

market

Convergent market

Source: Regulatory bodies; Analysis Mason; specialized webs and news

MVNOs in Europe are reaching 15%-20% market share

Strategy&

Regulation

Overview of Bundled Offers of European Incumbents Selected Examples for Antitrust Fines against global Telco operators

(2011-2014)

Telecom Italia, €104 Mn in May 2013

Abuse of dominant position in

network infrastructure

Telekomunikacja Polska S.A,

€127 Mn in June 2011

Abuse of dominant market position

Telefónica and Portugal Telecom,

€79 Mn in Jan 2013

Illegal non-compete contract clause

Telmex (America Movil),

$52 Mn in Feb 2013

Anticompetitive practices

Telecom NZ,

$9 Mn in Apr 2011

Anti-competitive wholesale pricing

KPN, €30 Mn in Jan 2014

Failing to inform competitors on

tariffs in a government tender

Source: Press, Strategy& analysis

2013 2014 2012 2011

Strategy&

Demand for investment A

The Data Traffic Challenge

Higher investments demand

• Fibre as the only solution to address broadband demand

• LTE as the only solution for mid-term data traffic requirement

Need to "re-imagine" the

business model

1

2

Time

Revenues

Traffic

De-coupling/Gap

Costs

~30% of Western

European BB lines >

30MBps in 2Q13;

Cable switching to 120

Mbps; 54% own a

smartphone

Massive Fibre,

Cable, LTE

deployment

ILLUSTRATIVE

Strategy&

Demand for investment A

Core business process re-imagination to respond to Data Traffic challenge

Infrastructure • Fiber and network sharing

• Tower sharing

Network • Pay-per-use models

• Full outsourcing

IT • Greenfield IT

• Full outsourcing

Joint Procurement

• Combining purchasing power

(Digital) Business Processes

• Simplification through adoption of efficiency philosophy

• Exp: “Kaizen” – car manufacturing

Strategy&

Consolidation of players M&A activity: Portfolio rationalization and expansion into adjacencies

B

$21.6 Bn in Jul 2013

$0.7 Bn in Nov 2013

$5.7 Bn in Nov 2013

$2.0 Bn in Jan 2014

$1.6 Bn in Feb 2014

A

B

C

Stake Increase

Cross-Border

In-Market

Acquisition Type

$16 Bn in June 2013

€0.8 Bn in Feb 2014

€7.2 Bn in Mar 2014

€7.7 Bn in Oct 2013€17 Bn in Apr 2014

$45 Bn in Feb 2014

$48.5 Bn in May 2014C

C

C

A

A

A

B

C

A

B

C

Source: Operator announcements, Press, Strategy& analysis

2012 2013 2014

Highlights in M&A´s (2012-2014)

C

Source: Bloomberg, Dealogic; Strategy&

Adjacent Telco´s M&A

Note: Deals > €1 Mn only

$3.1bn in Jan 2011

$80Mn in Apr 2011

$1.4bn in Aug 2011

$1.3bn in Oct 2013

Strategy&

Digitization C

Total

connected

devices

7.6 7.2 6.3

50.0

0.5

12.5

25.0

2020 2003 2010 2015

6.8

0.08 6.58 3.47 1.84

0

40

30

20

50

10

In bn

More Connected Devices than

People

Digital Commerce

eEducation Smart Grid Autonomous Car

Big Data Digital Wallets Mobile Health

3D Printing

From “connecting individuals” to “connecting devices

Source: Ovum, Strategy& analysis

Strategy&

Digitization C

Typical Archetypes of ‘Way to Play’ in Digital Services

Connectivity Play Digital Enabler Digital Life

Provider

Description

EBITDA

Margins

Revenue

Sources

~30-50% ~30-40% ~20-25%

“Become efficient provider

of secure connectivity

related bundled products

and services”

“Build adjacent platforms

that enable Digital services

by partnering with ICT and

OTT players”

“Become a comprehensive

Digital Life Provider with

best-in-class services that

are vertically integrated”

100%

Connectivity

Services

20%

Connectivity

80%

60% Services

Connectivity 40%

Innovation

Focus Defocus/ Partner Enabling platform focus (APIs) Leading-edge services,

global labs

Sample

Operators

Strategy&

Demand for

investment

(data boost)

Consolidation

of players Digitization

A B C

In summary, …

Convergence Competition Adjacencies Regulations

Telling your story

Integrated Reporting

PwC

Integrated Reporting

• An integrated report is a concise communication about how an organization’s strategy, governance, performance and prospects lead to the creation of value over the short, medium and long term

• The International Integrated Reporting Council (IIRC) issued the framework in December 2013.

Global Communications GAAP Summit

Slide 27

June 2014

PwC

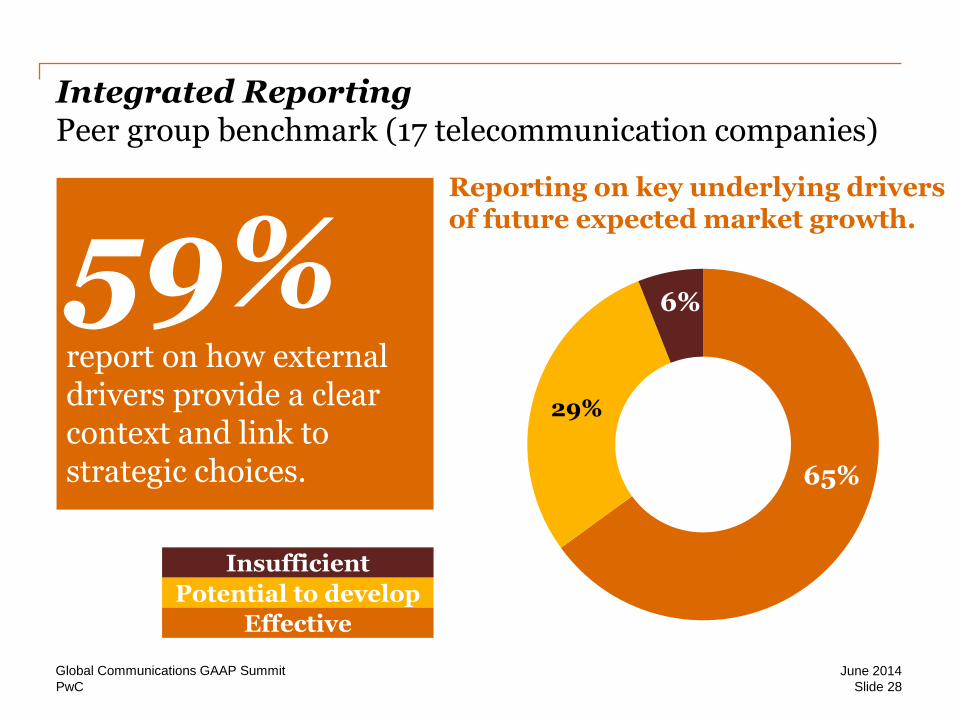

59% report on how external drivers provide a clear context and link to strategic choices.

Integrated Reporting Peer group benchmark (17 telecommunication companies)

Reporting on key underlying drivers of future expected market growth.

29%

6%

65%

Insufficient

Potential to develop

Effective

Global Communications GAAP Summit

Slide 28

June 2014

PwC

12%

Integrated Reporting Peer group benchmark (17 telecommunication companies)

Reporting on the company’s impact on external non-financial capitals.

12% discuss the future availability of material non-financial capitals it uses to create value. 47% 47%

6%

47%

Global Communications GAAP Summit

Insufficient

Potential to develop

Effective

Slide 29

June 2014

PwC

12%

Integrated Reporting Peer group benchmark (17 telecommunication companies)

Are performance measures clearly aligned with strategic priorities? 76%

report consistently on performance between the “front half” reporting and financial statements.

18%

47%

35%

Global Communications GAAP Summit

Insufficient

Potential to develop

Effective

Slide 30

June 2014

Telling your story

Investor views

PwC

Alternative Performance Measures (“APMs”) Investor views

Investor view - Non GAAP measures

Investors discuss how companies can improve Non-GAAP measures in their reporting

http://www.pwc.com/gx/en/audit-services/corporate-reporting/publications/investor-view/index.jhtml

Global Communications GAAP Summit

Slide 32

June 2014

Telefónica

Marta Soto Head of Accounting Policies & Digital Subsidiaries

June 2014

DISCOVER, DISRUPT, DELIVER 34

1. Profile & Strategy: recent developments

DISCOVER, DISRUPT, DELIVER

Telefónica is the result of more than 85 years of anticipation and

transformation especially during the last decade

35

2000 - 2005 2006 - 2008 2009 - 2011 2012 - 2014

• Veronica Operation:

Telefónica de Argentina;

Telefónica del Perú; Telesp

and Tele Sudeste in Brazil

(2000)

• Joint venture of Telefónica and

Portugal Telecom in Brazil:

Vivo (2003)

• Launches Imagenio (2003)

• Acquisition of BellSouth's

assets in Latin America (2004)

• Acquisition of Cesky Telecom

(2005)

• Takes a 5% stake in China

Netcom (2005)

• Acquisition of the O2 assets in

the UK, Germany and Ireland

(2006)

• Mobile license awarded in

Slovakia (2006)

• 51% stake taken in Colombia

Telecom (2006)

• Industrial alliance with

Telecom Italia (10.47% of the

voting rights) (2007)

• Acquisition of Telemig by Vivo

in Brazil (2008)

• Reaches a 5.38% participation

in China Unicom after the CU-

CNC merger (2008)

• Strengthening of the strategic

alliance with China Unicom

(2009)

• Acquisition of Hansenet in

Germany, Jajah in Israel and

Tuenti in Spain (2010)

• Control of Vivo obtained by

buying PT stake out of

Brasilcel (2010)

• Mobile license awarded in

Costa Rica (2011)

• T.Digital and TGR creation

(2011)

• Sale of 4.56% stake in China

Unicom (2012)

• IPO Telefónica Deutschland

(2012)

• Sale of Atento (2012)

• Sale of 40% of Telefónica’s

stake in Centroamérica (2013)

• Sale of Telefónica Ireland

(2013)*

• Acquisition of E-Plus in

Germany (2013)*

• Capital increase in Telco (from

46,18% to 66%) (2013)

• Sale of Telefónica Czech

Republic (2014)**

• New totally customer-centred

organization

* The operations are subject to obtaining the relevant regulatory approval.

** Telefónica holds a 4.9% stake in Telefónica Czech Republic.

DISCOVER, DISRUPT, DELIVER 36

Since the beginning of internationalization, the company has

experienced a significant growth

* Includes Ireland (in a process of divestment), Czech Republic and Slovakia (Telefónica holds a 4.9% stake in Telefónica Czech Republic).

** Data as of FY 2013.

1989 2000 Mar14 1989 – Mar14

Customers (Mn) 12 68 313 x26

Countries * 1 16 24 +23

Team (‘000) 71 149 122 x2

Revenues (Mn €) 4,273 28,482 57,061 ** x13

DISCOVER, DISRUPT, DELIVER 37

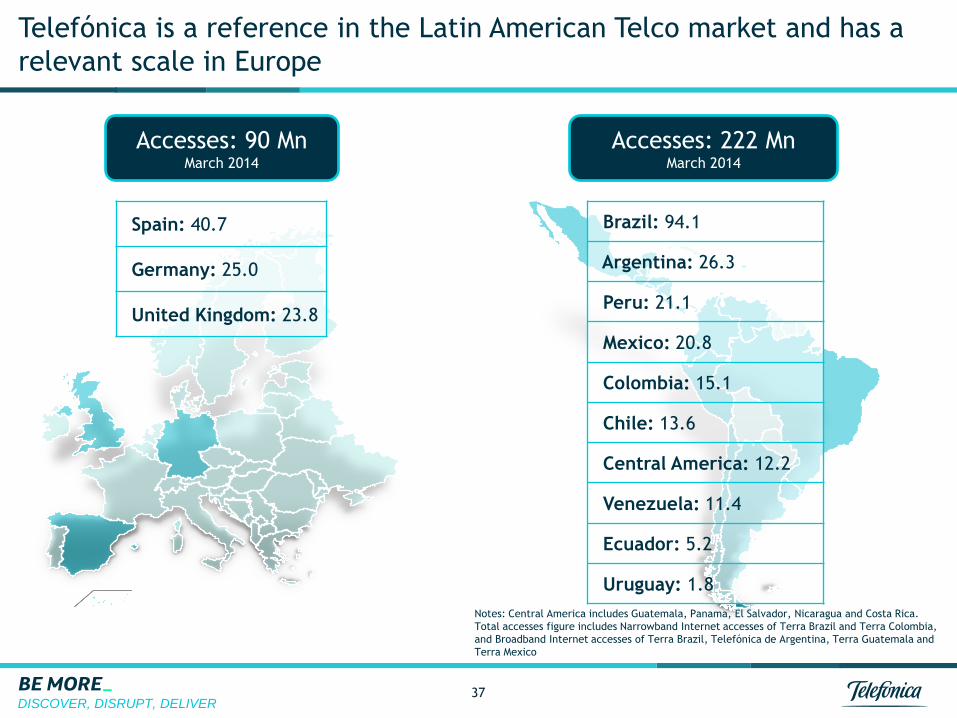

Telefónica is a reference in the Latin American Telco market and has a

relevant scale in Europe

Spain: 40.7

Germany: 25.0

United Kingdom: 23.8

Accesses: 90 Mn March 2014

Accesses: 222 Mn March 2014

Brazil: 94.1

Argentina: 26.3

Peru: 21.1

Mexico: 20.8

Colombia: 15.1

Chile: 13.6

Central America: 12.2

Venezuela: 11.4

Ecuador: 5.2

Uruguay: 1.8

Notes: Central America includes Guatemala, Panama, El Salvador, Nicaragua and Costa Rica.

Total accesses figure includes Narrowband Internet accesses of Terra Brazil and Terra Colombia,

and Broadband Internet accesses of Terra Brazil, Telefónica de Argentina, Terra Guatemala and

Terra Mexico

DISCOVER, DISRUPT, DELIVER

New digital solutions create growth opportunities for the industry...

Cloud Services M2M

Mobile Payment e-Government

Big Data e-Commerce

4%

6%

10%

ICT Total ICT Latam Mobile Data

Global Industry Revenues CAGR 13-17

Source: IDC - Worldwide Black Book (Mar14).

38

DISCOVER, DISRUPT, DELIVER

Telefónica sits on a privileged position to capture that growth potential

39

Traditional Telco Digital Telco From To

“Combines its Telco

with additional digital

assets

to help people to access

and enjoy the best that

technology can offer”

Leverage unique assets (networks/IT & BI/distribution)

• Copper, 2G/3G

• Traditional IT

• Fiber, LTE, Cloud-RAN, virtualisation…

• IT as a Digital enabler

• Physical stores and call centers

• Traditional Business Intelligence

• Digital customer experience

• Customer Insight

+ Capturing growth beyond connectivity

• Communication services • Digital solutions

DISCOVER, DISRUPT, DELIVER

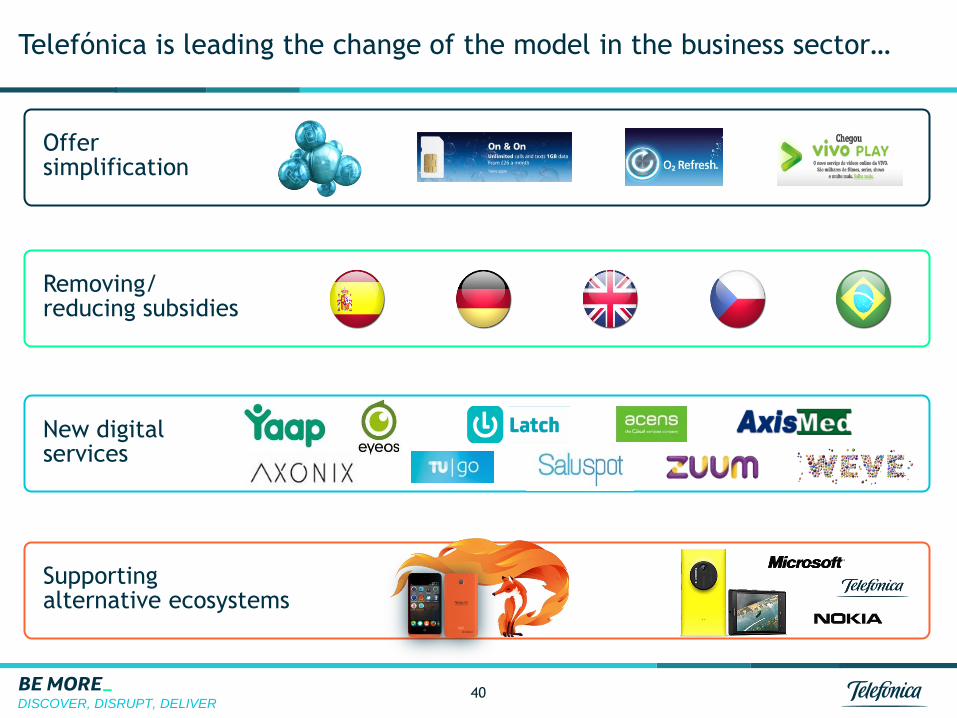

Telefónica is leading the change of the model in the business sector…

Removing/ reducing subsidies

Offer simplification

New digital services

Supporting alternative ecosystems

40

DISCOVER, DISRUPT, DELIVER

…with disruptive initiatives in the way we invest

41

Leading in-market Consolidation

Ireland Czech

The biggest DC in

the World with Tier IV

certificate

Network sharing

Apps and physical

servers reduction

Fibber and LTE

deployment

Server

virtualization

Network virtualization

IT

Network

DISCOVER, DISRUPT, DELIVER

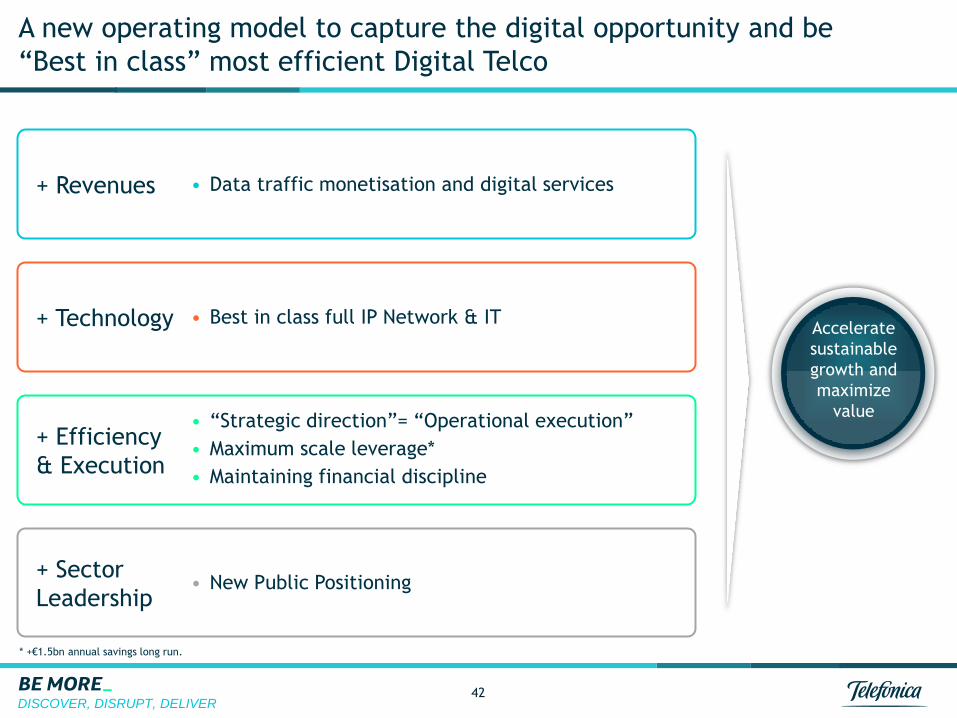

• Data traffic monetisation and digital services

• Best in class full IP Network & IT

• “Strategic direction”= “Operational execution”

• Maximum scale leverage*

• Maintaining financial discipline

• New Public Positioning

42

A new operating model to capture the digital opportunity and be

“Best in class” most efficient Digital Telco

* +€1.5bn annual savings long run.

+ Revenues

+ Technology

+ Efficiency

& Execution

+ Sector

Leadership

Accelerate

sustainable

growth and

maximize

value

DISCOVER, DISRUPT, DELIVER

Enhanced visibility and

report level

43

Closing distances between strategic and operational decisions & increased

visibility of key businesses

LatAm (ex-Bz) Spain Brazil Germany United Kingdom

CGRO (Chief Global

Resources Officer)

CCDO (Chief Commercial

Digital Officer)

Controller

& Planning

Group General

Counsel

Finance & Corp.

Development

Public Affairs and

Regulation

Strategy

Comm. & Media

Chief of Staff

The new organization

COO

Chairman & CEO One single

Corporate

Center

DISCOVER, DISRUPT, DELIVER

Our Vision revolves around our clients

44

Technology should be open

BE MORE_

to everyone so that we can all

DISCOVER, DISRUPT, DELIVER 45

2. Communication

DISCOVER, DISRUPT, DELIVER 46

Our Financial Information…

Our press release,

reflecting our digital

transformation

Our Financial

Statements: simplifying

contents

DISCOVER, DISRUPT, DELIVER 47

Our Integrated Report…

IIRC(*) Pilot

Programme

(*) International Integrated Reporting Council

DISCOVER, DISRUPT, DELIVER 48

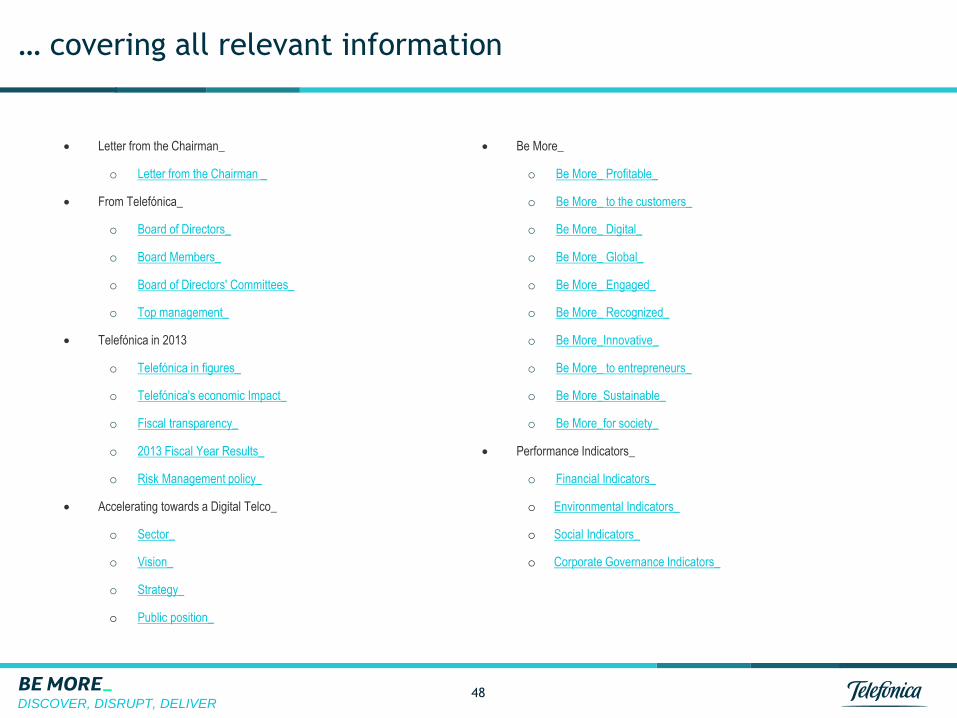

… covering all relevant information

Letter from the Chairman_

o Letter from the Chairman _

From Telefónica_

o Board of Directors_

o Board Members_

o Board of Directors' Committees_

o Top management_

Telefónica in 2013

o Telefónica in figures_

o Telefónica's economic Impact_

o Fiscal transparency_

o 2013 Fiscal Year Results_

o Risk Management policy_

Accelerating towards a Digital Telco_

o Sector_

o Vision_

o Strategy_

o Public position_

Be More_

o Be More_ Profitable_

o Be More_ to the customers_

o Be More_ Digital_

o Be More_ Global_

o Be More_ Engaged_

o Be More_ Recognized_

o Be More_Innovative_

o Be More_ to entrepreneurs_

o Be More_Sustainable_

o Be More_for society_

Performance Indicators_

o Financial Indicators_

o Environmental Indicators_

o Social Indicators_

o Corporate Governance Indicators_

PwC

Telecom Argentina S.A.

Marcelo F. Kozak

Chief Accountant and SOX Compliance Officer

June 2014

Global Communications GAAP Summit

Slide 50

June 2014

PwC

Listed Company (BCBA (*)/ NYSE)

Since 1994

Telecom Italia’s subsidiary

Since 2010

Financial Debt Restructuration

In 2005 (USD 3.2 billion)

Telecom Argentina and its Financial Reporting (“FR”) background

SOX Compliance Since 2002

(Section 404 since 2006)

FINANCIAL REPORTING

RSE Since 2007

(*) BCBA = Buenos Aires Stock Exchange

External & Internal reporting

under IFRS

Global Communications GAAP Summit

Slide 51

June 2014

PwC

Competitors and Market Share

~155% of population

~67% of households2

~45% of households2

MAIN COMPETITORS

ACCESSES

(million)

TELECOM GROUP

PENETRATION

MARKET

SHARE 1Q14 33% 27% 46%

1 Estimated Official GDP, 3Q 2013, Indec. 2 Source: Pyramid Research. Fixed line penetration residential only.

Mobile Broadband Fixed

51 55 57 61

2010 2011 2012 2013

3,9 4,4 4,8 5,1

2010 2011 2012 2013

8,78,8

8,99,0

2010 2011 2012 2013

Integrated operator

Global Communications GAAP Summit

Population 41 million

GDP1 ´13 (billion)

U$S 485.4

GDP1 per capita ´13

U$S 11,824

Slide 52

June 2014

PwC

Our business and our strategy (cont.)

Strategy

Creation of value

to stakeholders in a sustainable way

Global Communications GAAP Summit

Slide 53

June 2014

PwC

Past and current challenges and its impact in FR

Freezing tariffs since 2001 in regulated services (22% of revenues in 2007 to 8% in 1Q 2014)

Strong competition in non-regulated services (data, broadband, mobile )

Greater regulatory and political intervention

Unstable macroeconomic environment (Inflation, devaluation, foreign exchange restrictions, growth/recession periods, etc.)

Management = To manage Risk & Opportunities

Challenges

Evolution of Main Macroeconomic variables -last 2 decades-:

Convertibility

period (1)

Post -convertibility

period (1)

1992-2001 2002-2011 2012 2013 Min Máx

Gross Domestic Product growth ("GDP") 2.7% 5.7% 1.9% 4.9% -10.9% 9.2%

Devaluation ($/U$S) 0.0% 15.7% 14.3% 32.6% -13.1% 237.0%

Consumer Price Index (% variation) 2.6% 11.3% 10.8% 10.9% -1.8% 40.9%

Wholesale Domestic Price Index (% variation) 0.8% 17.6% 13.1% 14.8% -6.3% 118.0%

Unemployment index (% of the economically

active population at the end of year)

15.8% 10.3% 6.9% 6.4% 6.4% 20.9%

GDP per capita (thousand of U$S) 7.6 6.6 11.9 11.8 2.5 11.9

Source: INDEC - Last available variables

(1) Annual average(2) Est imated data

1992-2013 period

(2)

(2)

Global Communications GAAP Summit

Slide 54

June 2014

PwC

Past and current challenges and its impact in FR (cont.)

Impacts in FR:

• High Inflation Analysis / IAS 29 analysis.

• Impairment test / IAS 36.

• Focus on IFRS7 regarding financial risks disclosures.

• Multiples exchange rates / IAS 21.

• “De facto” restrictions to transfer funds abroad.

• Proper disclosure of risks (legal, regulatory, financial, etc.).

Significant Accounting policies (estimations)

Risk Factors (aligned with Risk Mapping)

Global Communications GAAP Summit

Slide 55

June 2014

PwC

How we manage the challenges?

Main grounds of our FR:

Financial

Reporting

High standards regarding Corporate

Governance

Transparency with the market

and comprehensive financial

information

Operational information

Global Communications GAAP Summit

Slide 56

June 2014

PwC

How we manage the challenges? (Cont.)

• Effective communication of our performance results: Through Financial

KPIs (Based on IFRS – Non GAAP measures are not used)

Enterprise Value (USDMM) NFP (USDMM) (market capitalization + net financial debt – fair value)

Global Communications GAAP Summit

Slide 57

June 2014

PwC

How we manage the challenges? (Cont.)

• Effective communication of our performance results: Through Financial

KPIs (Based on IFRS – Non GAAP measures are not used)

Financial performance (AR$MM) Labor Costs

2002 2007 2012 2013 1Q 2014

EBITDA margin 47% 34% 30% 28% 28%

EBIT Margin -5% 18% 18% 17% 18%

CAPEX as % Revenues 7% 16% 15% 18% 14%

ROE N/A 42% 33% 32% 30% Global Communications GAAP Summit

Slide 58

June 2014

PwC

How we manage the challenges? (Cont.)

Clients (Thousands) ARPU (AR$/month)

• Effective communication of our performance results: Through

Operational KPIs

Global Communications GAAP Summit

Slide 59

June 2014

PwC

How we manage the challenges? (Cont.)

Market Share Revenue Share Internet Mobile

These indicators have been published in a consistent manner during the last 10 years.

The Operational KPIs and Macroeconomic indicators are essential for an adequate understanding of FR in a context of high volatility (during growth or recession periods).

• Effective communication of our performance results: Through

Operational KPIs

28.7% 27.5% 26.9%

33.0% 29.3% 28.9%

19.1% 24.3% 25.0%

19.2% 18.9% 19.2%

2007 2012 2013

Telecom Telefónica Cable Other

30.9% 34.3% 34.7%

38.1% 33.6% 34.2%

31.0% 32.1% 31.1%

2007 2012 2013

Telecom Movistar América Movil

Global Communications GAAP Summit

Slide 60

June 2014

PwC

How we manage the challenges? (Cont.)

• Effective and comprehensive disclosure of FR:

Segregation of information

(revenues segregated by type

of service )

Increased bundling

(higher and more complex price estimations to apply relative fair value

allocation of revenues, potential discontinuation of the residual method

in mobile industry).

Non-Gaap measures

(SEC comment: EBITDA & ARPU, key performance measures used by

Telecom Argentina ´s Management )

2013 % 2012 % 2011 %

Voice 10,645 44 9,927 49 9,184 54

Internet 4,879 20 3,395 17 2,411 14

Data 8,488 36 6,767 34 5,316 32

Total services revenues 24,012 100 20,089 100 16,911 100

Annual Variation % 20% 19% 25%

Years ended December 31,

Global Communications GAAP Summit

Slide 61

June 2014

PwC

Next steps in Financial Reporting towards Integrated Reporting

There is an increasing need for an integrated view of the business and value creation for stakeholders. The keys to achieve this are:

Communication with stakeholders,

To use commonly defined KPIs and non-GAAP measures.

In the interim it is key to:

Include detailed disclosures about the policies and criteria used to calculate KPIs and non-GAAP measures.

To include key prospective information (Financial and Operational).

Global Communications GAAP Summit

Slide 62

June 2014

Jenny Harrison, Head of External Reporting, BT Group plc

June 2014

Reporting on our performance

© British Telecommunications plc

65

© British Telecommunications plc

66

Our journey

2001-2003

Rehabilitation

• Reducing debt

• Restructuring

the business

2003-2008

Move to data

• Defend

traditional

• Grow “new

wave”

2008-2013

A better business

• Cost

transformation

• Investing for the

future

2013

A better future

• Further cost

transformation

• Customer

service

improvements

• Delivering on

investments

Cash flow

growth

EBITDA

growth

Profitable

revenue

growth

© British Telecommunications plc

67

Our purpose, goal, strategy and culture

Broaden and deepen our customer relationships

Fibre TV and

content

Mobility

and

future

voice

UK

business

markets

Leading

global

companies

Our strategy

A growing BT: to deliver sustainable profitable revenue growth

Invest for

growth

Our goal

A healthy organisation

Deliver superior

customer service

Transform

our costs

Our purpose To use the power of communications to make a better world

Our culture

© British Telecommunications plc

68

BT Sport – an example of how we explain ourselves

© British Telecommunications plc

69

Q4 2013/14 Change FY 2013/14 Change

Revenue £1,068m 9% £4,019m 4%

EBITDA £269m 5% £833m (14)%

BT Consumer – how our strategy has increased revenue

Consumer YoY revenue growth Q4 revenue up 9%

– broadband and TV up 24%

– improved trend in calls and lines, up 1%

Q4 costs up 10%

– c.£130m BT Sport investment and higher

revenue-related costs

– partly offset by cost transformation activities

Q4 EBITDA up 5%

– reflects better revenue performance

-4%

-2%

0%

2%

4%

6%

8%

10%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012/13 2013/14

© British Telecommunications plc

70

How have we communicated our strategy?

Internal communication – clarity on our strategy. Focus on health of our

organisation.

Externally - strategic reporting in the UK – we have to CONNECT the story

Linking strategy – business model – KPIs – remuneration - financials

The five growth areas in our strategy are used as case studies in this year’s

annual report

The BT Group KPIs

– Adjusted earnings per share

– Normalised free cash flow

– Customer service improvement (non-financial measure)

– And refreshed this year to include Revenue growth (reflects re-emphasis in strategy)

© British Telecommunications plc

71

Our Group KPI disclosure

© British Telecommunications plc

72

How do we measure non-financial value creation?

Our line of business KPIs (published quarterly)

– Order intake (contract businesses)

– Operational measures

– Share of broadband net adds

– Active lines, line loss, physical lines

– Consumer ARPU

Regular disclosure of operational statistics help analysts review the business

– These translate into £ growth

– Importance of trends over time

Organisational health measures (published in annual report)

– Employee engagement

– Volunteering

– Social impact of digital inclusion programmes

© British Telecommunications plc

73

BT Consumer KPIs – how we explain operational performance

Total consumer line loss Broadband net adds1

2012/13 2013/14

‘000s

TV net additions

2012/13 2013/14

‘000s

2012/13 2013/14

BT retail net adds BT share of net adds

‘000s

(250)

(200)

(150)

(100)

(50)

0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

30%

40%

50%

60%

70%

80%

90%

100%

0

30

60

90

120

150

180

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q40

10

20

30

40

50

60

70

80

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Q4 consumer line loss of

49,000, best for >5 years

170,000 retail broadband net

adds in Q4, a 79% market share

Q4 TV net adds of 46,000,

up 15%

1 includes business customers; DSL & fibre, excluding cable

Telling your story

Questions and Answers

PwC

Tonight: Royal Theatre

Meet on floor -1 at 18:30 for a prompt departure

Slide 75

Global Communications GAAP Summit June 2014

Thank you

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2014 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers LLP (a limited liability partnership in the United Kingdom) which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.