global crisis and india - icrier | indian council for …icrier.org/pdf/mathew joseph_new.pdf5...

TRANSCRIPT

1

Global Crisis and IndiaMathew Joseph

Debosree BanerjeePankaj Vashisht

International Conference

Global Economic Downturn: Lessons and Way Forward

New Delhi

9-10 February 2009

2

Roots of Global Crisis• Global macroeconomic imbalances

– Results in huge cross-border capital flows from surplus to deficit countries

– International financial system failed to intermediate these flows properly

• Lending to sub-prime borrowers/ imprudent credit expansion

– Debt crisis of 1980s, East Asian crisis of late 1990s and the present global crisis

– Current one the severest and the impact so vast and widespread

3

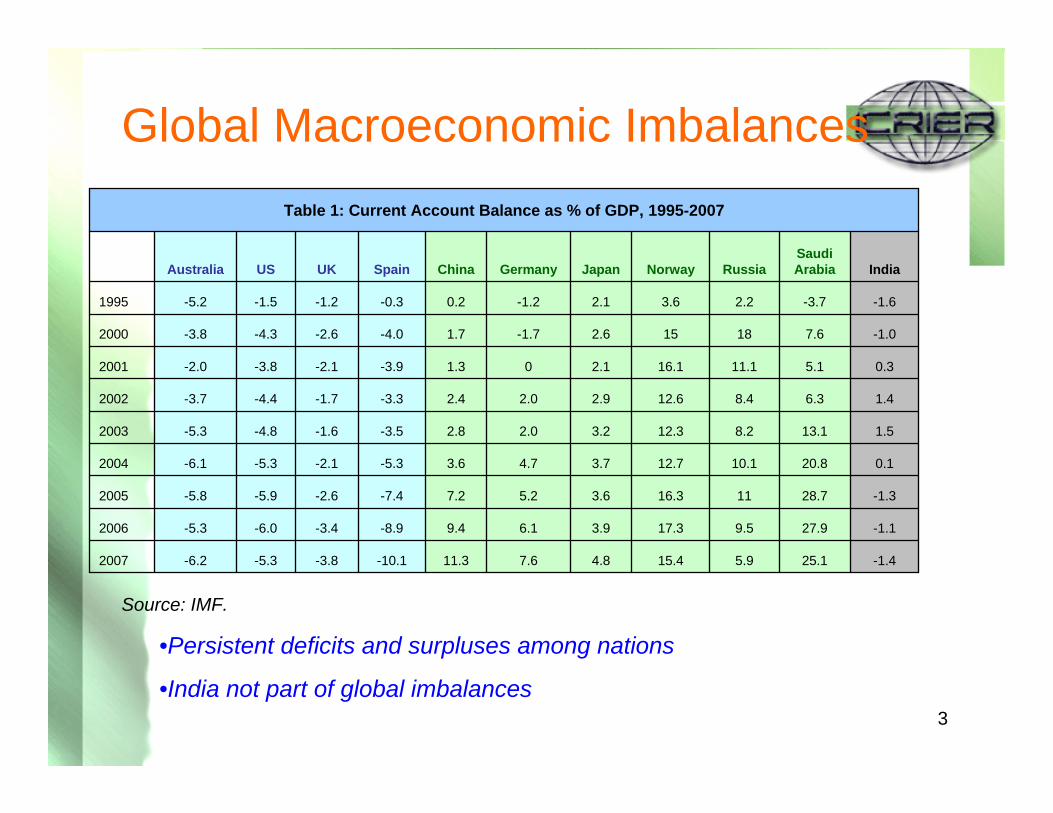

-1.425.15.915.44.87.611.3-10.1-3.8-5.3-6.22007

-1.127.99.517.33.96.19.4-8.9-3.4-6.0-5.32006

-1.328.71116.33.65.27.2-7.4-2.6-5.9-5.82005

0.120.810.112.73.74.73.6-5.3-2.1-5.3-6.12004

1.513.18.212.33.22.02.8-3.5-1.6-4.8-5.32003

1.46.38.412.62.92.02.4-3.3-1.7-4.4-3.72002

0.35.111.116.12.101.3-3.9-2.1-3.8-2.02001

-1.07.618152.6-1.71.7-4.0-2.6-4.3-3.82000

-1.6-3.72.23.62.1-1.20.2-0.3-1.2-1.5-5.21995

IndiaSaudi ArabiaRussiaNorwayJapanGermanyChinaSpainUKUSAustralia

Table 1: Current Account Balance as % of GDP, 1995-2007

•Persistent deficits and surpluses among nations

•India not part of global imbalances

Global Macroeconomic Imbalances

Source: IMF.

4

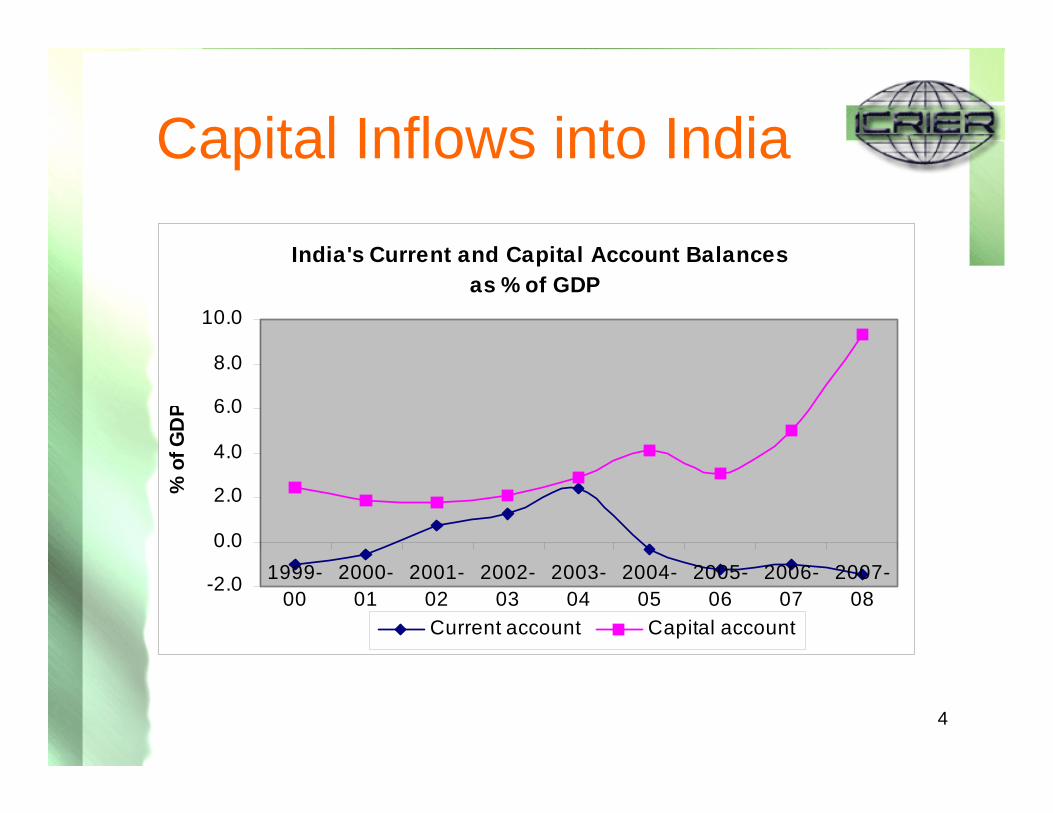

Capital Inflows into India

India's Current and Capital Account Balances as % of GDP

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

% o

f GD

P

Current account Capital account

5

India’s Reserve Build-upInd ia 's Fore ign Ex cha nge Re se rve s (US $ Bill ion )

38.0 42.354.1

76.1

113.0

141.5 151.6

199.2

309.7

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

1999-00 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08

Turned out to be building up a war chest!

6

Huge Stock Market RallyB S E S e n s e x (1 9 7 8 -7 9 = 1 0 0 )

0

5 0 0 0

10 0 0 0

15 0 0 0

2 0 0 0 0

2 5 0 0 0

Stock index rising from an average 5500 during 2004 to over 20,000 in January 2008

7

Remarkable Growth PerformanceGDP Growth Rates, 1997-98 to 2007-08 (Per cent)

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

Lifted to a new high growth trajectory

8

Overheating of Indian Economy

Note: HP filter technique as proposed by Hodrick and Prescott (1997)

GDP growth above potential rate in recent years

Inflation above 5 per cent from 2003-04

9

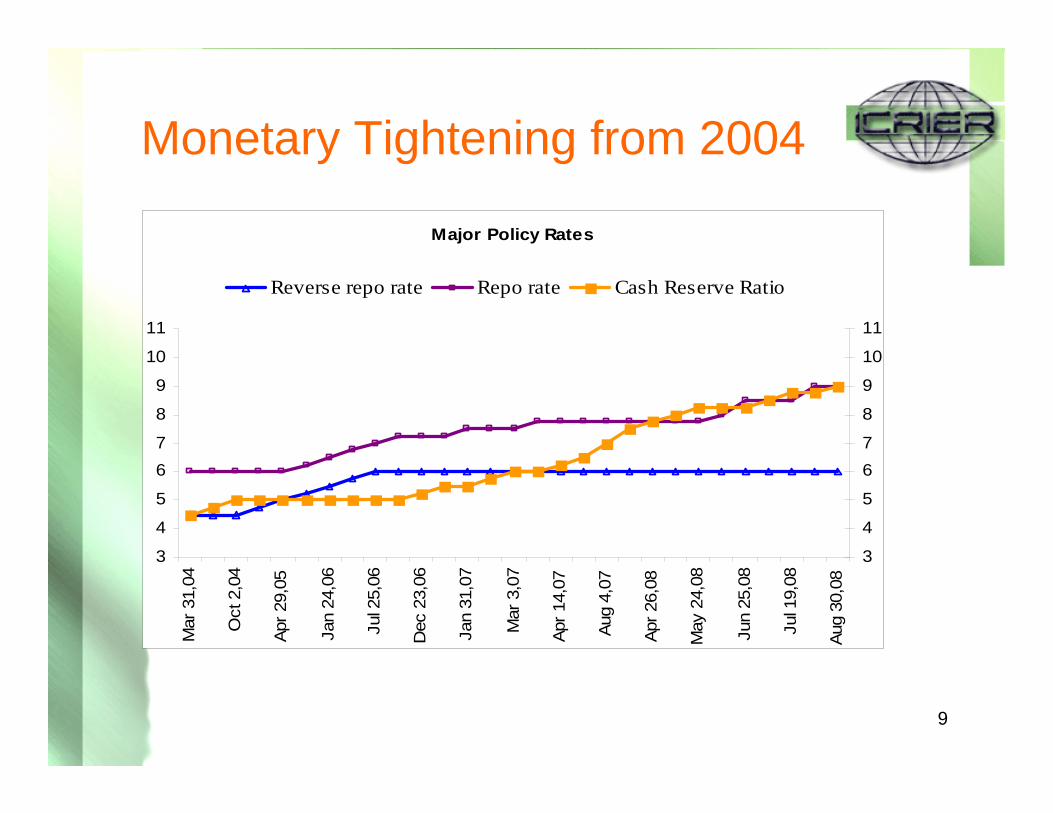

Monetary Tightening from 2004

Major Policy Rates

3

4

5

67

8

9

10

11

Mar

31,

04

Oct

2,0

4

Apr 2

9,05

Jan

24,0

6

Jul 2

5,06

Dec

23,

06

Jan

31,0

7

Mar

3,0

7

Apr 1

4,07

Aug

4,07

Apr 2

6,08

May

24,

08

Jun

25,0

8

Jul 1

9,08

Aug

30,0

8

3

4

5

67

8

9

10

11

Reverse repo rate Repo rate Cash Reserve Ratio

10

Soft-landing of Indian Economy

Cyclical Slowdown of GDP Growth from Q3 2007-08

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09

11

Global Crisis

12

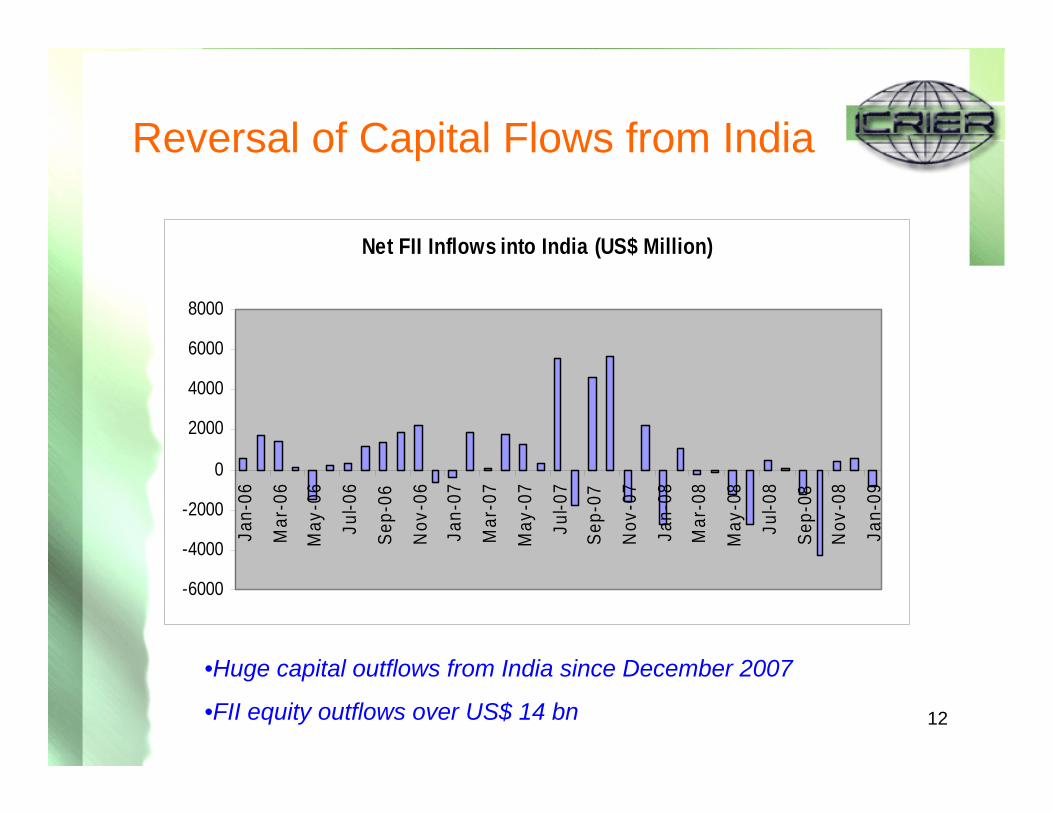

Reversal of Capital Flows from India

•Huge capital outflows from India since December 2007

•FII equity outflows over US$ 14 bn

Net FII Inflows into India (US$ Million)

-6000

-4000

-2000

0

2000

4000

6000

8000

Jan-

06

Mar

-06

May

-06

Jul-0

6

Sep-

06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

09

13

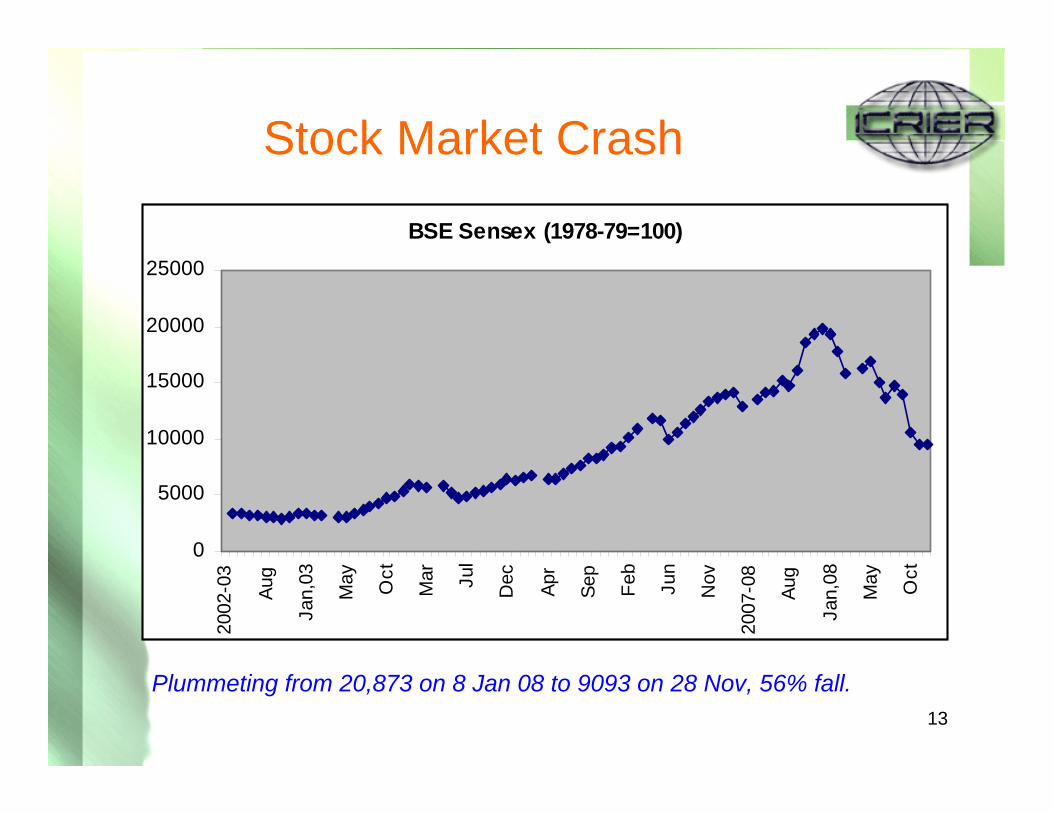

Stock Market Crash

BSE Sensex (1978-79=100)

0

5000

10000

15000

20000

25000

2002

-03

Aug

Jan,

03

May Oct

Mar Ju

l

Dec Apr

Sep

Feb

Jun

Nov

2007

-08

Aug

Jan,

08

May Oct

Plummeting from 20,873 on 8 Jan 08 to 9093 on 28 Nov, 56% fall.

14

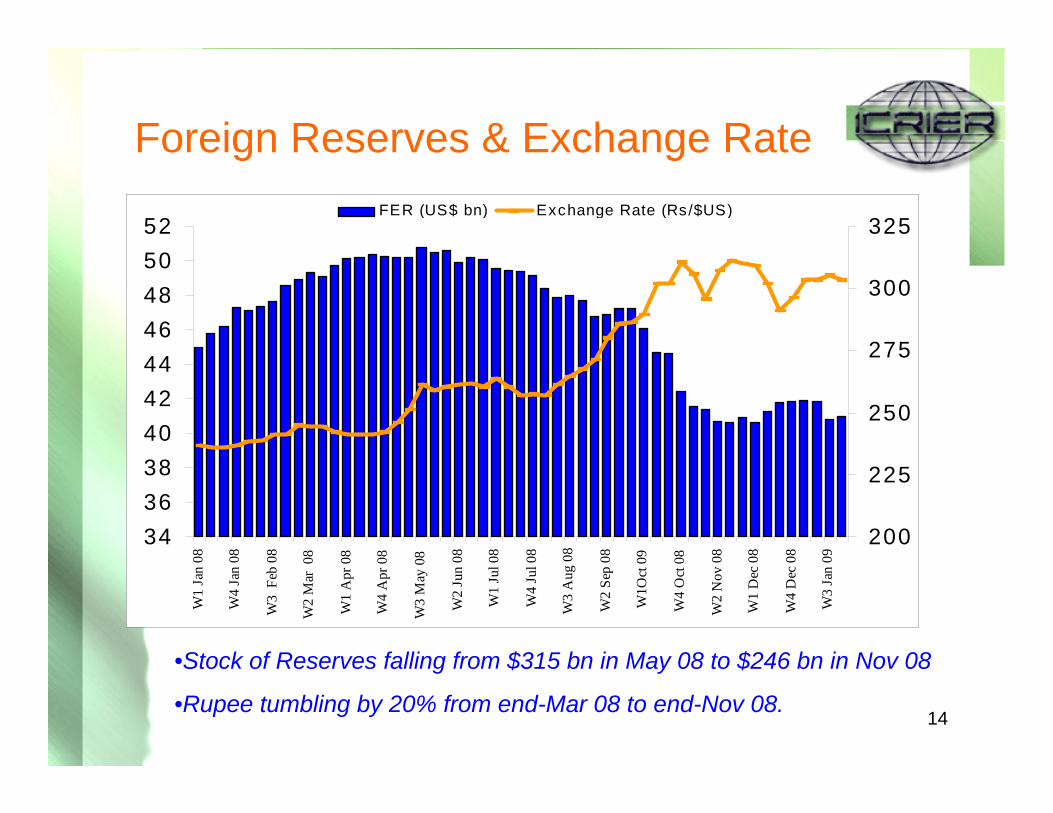

Foreign Reserves & Exchange Rate

•Stock of Reserves falling from $315 bn in May 08 to $246 bn in Nov 08

•Rupee tumbling by 20% from end-Mar 08 to end-Nov 08.

34363840424446485052

W1

Jan

08

W4

Jan

08

W3

Feb

08

W2

Mar

08

W1

Apr

08

W4

Apr

08

W3

May

08

W2

Jun

08

W1

Jul 0

8

W4

Jul 0

8

W3

Aug

08

W2

Sep

08

W1O

ct 0

9

W4

Oct

08

W2

Nov

08

W1

Dec

08

W4

Dec

08

W3

Jan

09

200

225

250

275

300

325FER (US$ bn) Exchange Rate (Rs/$US)

15

Liquidity Crisis

Inter-bank call money rate spiking to 20% in October 08

16

Credit Crunch to Low Credit Demand

•In September and October 08, bank finance (loans & investments) rose to compensate for drying up funds from domestic and foreign capital markets

•In November 08 onwards, bank finance expansion sharply lower as demand has fallen; and bank finance turned negative in Jan 09.

Expansion of Bank Finance to Commercial Sector (Rs crore)

-50000

0

50000

100000

Apr May Jun Jul Aug Sep Oct Nov Dec Mid-Jan

2007-08 2008-09

17

Aggressive Policy Response

• RBI loosening cost and availability of liquidity in a series of steps from mid-September 08

18

RBI Policy Rate ChangesMajor Policy Rates

3

4

5

6

7

8

9

10

11

Apr

14,

07

Aug

4,0

7

Apr

26,

08

May

24,

08

Jun

25,0

8

Jul 1

9,08

Aug

30,

08

Oct

20,

08

Nov

3,0

8

Dec

8,0

8

Jan

17,0

9

3

4

5

6

7

8

9

10

11

Reverse repo rate Repo rate Cash Reserve Ratio

•Cash reserve ratio (CRR) brought down from 9% to 5%•Statutory liquidity ratio (SLR) from 25% to 24%•Repo rate reduced from 9% to 5.5% & reverse repo rate from 6% to 4%•Special window for banks in their lending to mutual funds, NBFCs and housing finance companies•Refinance facility for banks from the central bank & dollar swap arrangements, etc.

19

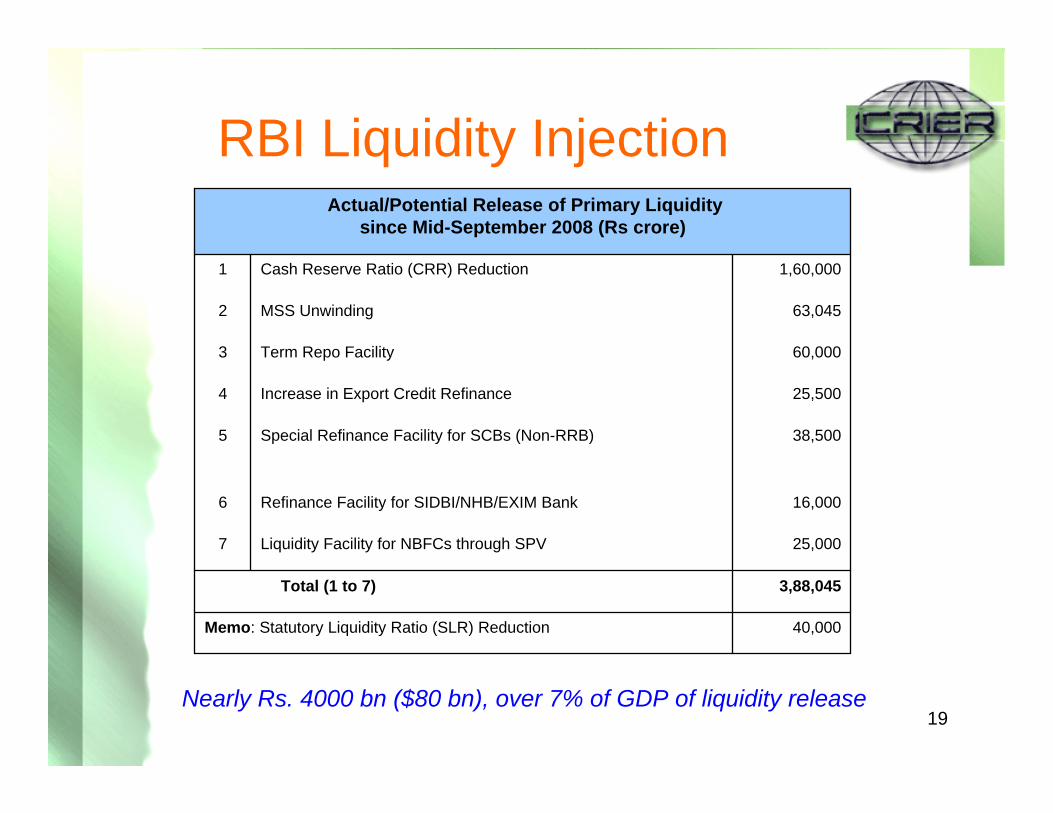

RBI Liquidity Injection

40,000Memo: Statutory Liquidity Ratio (SLR) Reduction

3,88,045Total (1 to 7)

25,000Liquidity Facility for NBFCs through SPV7

16,000Refinance Facility for SIDBI/NHB/EXIM Bank6

38,500Special Refinance Facility for SCBs (Non-RRB)5

25,500Increase in Export Credit Refinance4

60,000Term Repo Facility3

63,045MSS Unwinding2

1,60,000Cash Reserve Ratio (CRR) Reduction1

Actual/Potential Release of Primary Liquidity since Mid-September 2008 (Rs crore)

Nearly Rs. 4000 bn ($80 bn), over 7% of GDP of liquidity release

20

Fiscal Stimulus• Deterioration of the economy leading to Central

government’s two packages of fiscal stimulus in early Dec 08 and early Jan 09– Direct fiscal burden of stimulus just 1.2% of GDP

• Across-the-board excise duty reduction by 4 %age points• Additional plan spending of Rs. 200 billion• State governments allowed additional market borrowing of

Rs 300 billion for plan expenditure• Assistance to export industries

– Fiscal deficit (Central and States combined) rising sharply to cross 10% of GDP in 2008-09

21

Sharp Real Sector deterioration from September 2008

Source: CSO, Ministry of Commerce, CMIE and Economic Times.

(2520 companies)

-25.6-25.44.77.121.2Corporate profit

13.334.631.424.018.5Corporate sales

7.67.98.88.8Real GDP

Q3 08-09Q2 08-09Q1 08-09Q4 07-08Q3 07-08

-18.6-3.5-4.626.025.0Central government tax revenue

-7.7-14.0-0.8Airport passenger traffic

-58.2-48.0-34.9-0.63.9Commercial vehicle sales

-4.6-5.71.18.7Major ports traffic

3.11.3-0.18.28.6Railway freight traffic

-16.18.86.110.643.337.7Imports

-22.3-1.1-9.9-12.110.435.1Exports

2.4-0.35.54.8Industry

Jan-09Dec-08Nov-08Oct-08Sep-08Apr-Aug 08

Growth in Selected Economic Indicators (% Change, Y-O-Y)

22

Growth Prospects: 2008-09 and 2009-10

23

GDP Forecasts

• Methodology:– Use of an index of leading economic

indicators (LEI)– Also a external shock in the form of a dummy

variable

24

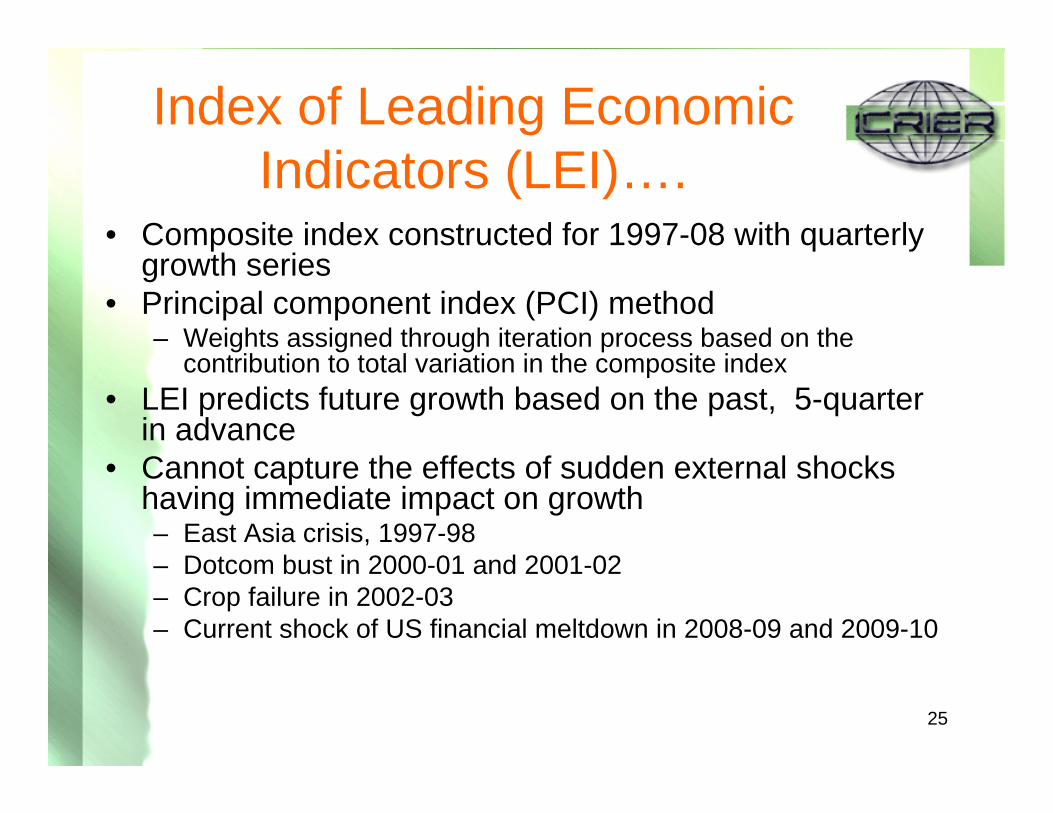

GDP Forecasts…• LEI Consists of:

– (i) production of machinery and equipment– (ii) non-food credit– (iii) railway freight traffic– (iv) cement sales – (v) net sales of the corporate sector – (vi) fuel and metal prices – (vii) real rate of interest – (viii) BSE sensex and – (ix) exports

25

Index of Leading Economic Indicators (LEI)….

• Composite index constructed for 1997-08 with quarterly growth series

• Principal component index (PCI) method– Weights assigned through iteration process based on the

contribution to total variation in the composite index• LEI predicts future growth based on the past, 5-quarter

in advance• Cannot capture the effects of sudden external shocks

having immediate impact on growth– East Asia crisis, 1997-98– Dotcom bust in 2000-01 and 2001-02– Crop failure in 2002-03 – Current shock of US financial meltdown in 2008-09 and 2009-10

26

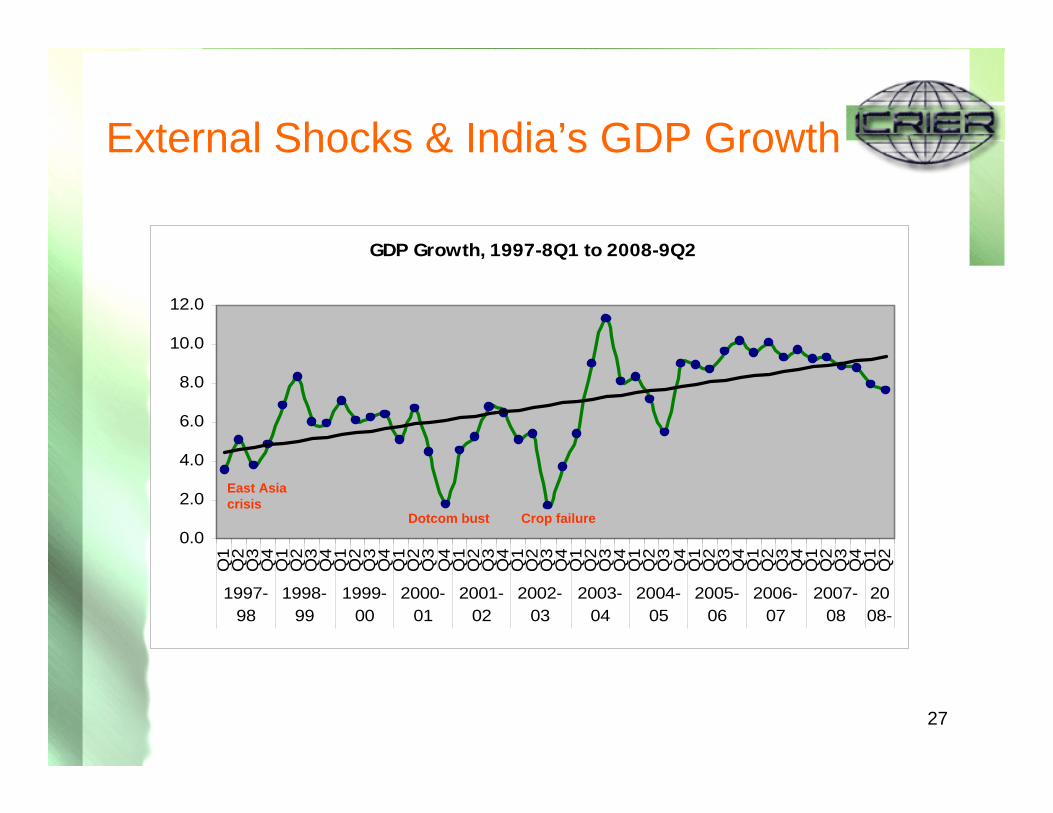

External Shocks & India’s GDP Growth

GDP Growth Rates, 1992-93 to 2007-08 (Per cent)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

GDP 5.4 5.7 6.4 7.3 8.0 4.3 6.7 6.4 4.4 5.8 3.8 8.5 7.5 9.5 9.7 9.0

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

East Asia crisis

Dotcom bust Crop

failure

27

External Shocks & India’s GDP Growth

GDP Growth, 1997-8Q1 to 2008-9Q2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-

East Asia crisis

Dotcom bust Crop failure

28

Projection of Growth Rate through Index of Leading Indicators & a Shock Variable

The estimated equation for GDP growth forecast, given below, is satisfactory with adjusted R-square value of 0.58 and all the co-efficients significant at 99% level.

GrGDP = 7.98 + 1.11 LEI (-5) - 4.15 Dummy(3.36) (-7.26)

Dotcom bust Crop

failure

29

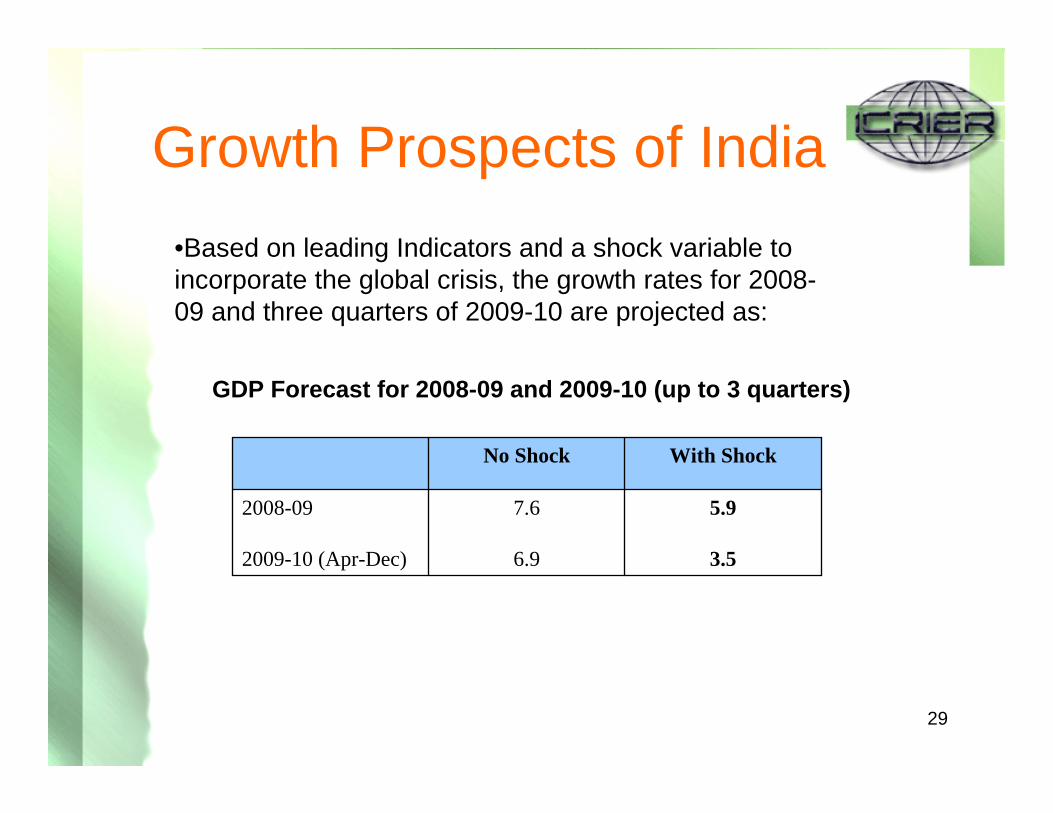

Growth Prospects of India

GDP Forecast for 2008-09 and 2009-10 (up to 3 quarters)

•Based on leading Indicators and a shock variable to incorporate the global crisis, the growth rates for 2008-09 and three quarters of 2009-10 are projected as:

5.9

3.5

7.6

6.9

2008-09

2009-10 (Apr-Dec)

With ShockNo Shock

30

Concluding Remarks• India is seriously affected by the global crisis• Growth to be brought down sharply but not to

the extent of making it below zero• Soundness of banking and cautious capital

account opening has saved the country• Recovery possible in late 2009-10 or early 2010-

11 provided the government is able to push through massive investment in social and physical infrastructure through public-private participation

31

Thank You.

32

Deepening Global Integration(Current Account & Capital Account as % GDP)

•Current account transactions rising from less than 20% of GDP to 50% •Both current and capital account transactions from less than a third of GDP to over 115%