global economic relations the politics of international finance james raymond vreeland school of...

TRANSCRIPT

GLOBAL ECONOMIC RELATIONSThe Politics of International Finance

James Raymond Vreeland

School of Foreign Service

Georgetown University

The questions we will address tonight:

1. Why did we ever invent the International Monetary Fund?

2. What is the IMF and what does it do?

Why was the IMF created?

• To answer this, we need…

• a little historical perspective…

1st: A reminder of

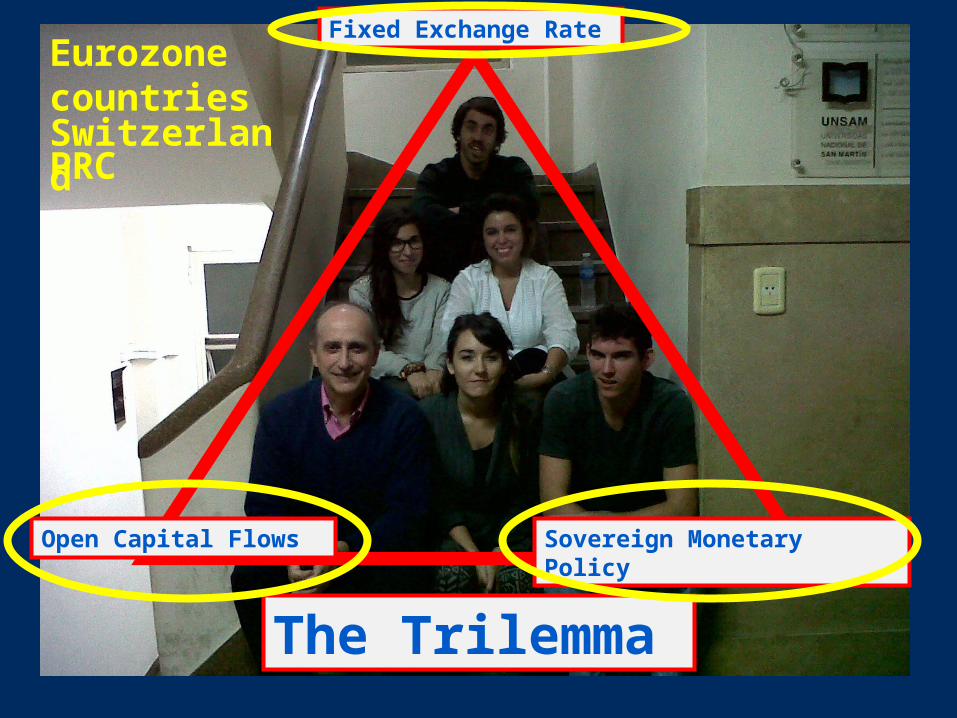

The “Inconsistent” or “Unholy”Trinity

Or“Trilemma”

The Trilemma

Fixed Exchange Rate

Open Capital Flows Sovereign Monetary Policy

Why would you want…

• Free Capital Flow?– Draw on the savings of the rest of the world– Investment opportunities abroad

• Fixed Exchange Rate?– Reduce uncertainty in trade

• Sovereign Monetary Policy?– Address inflation/unemployment

The Trilemma

Fixed Exchange Rate

Open Capital Flows Sovereign Monetary Policy

Eurozone countries SwitzerlandPRC

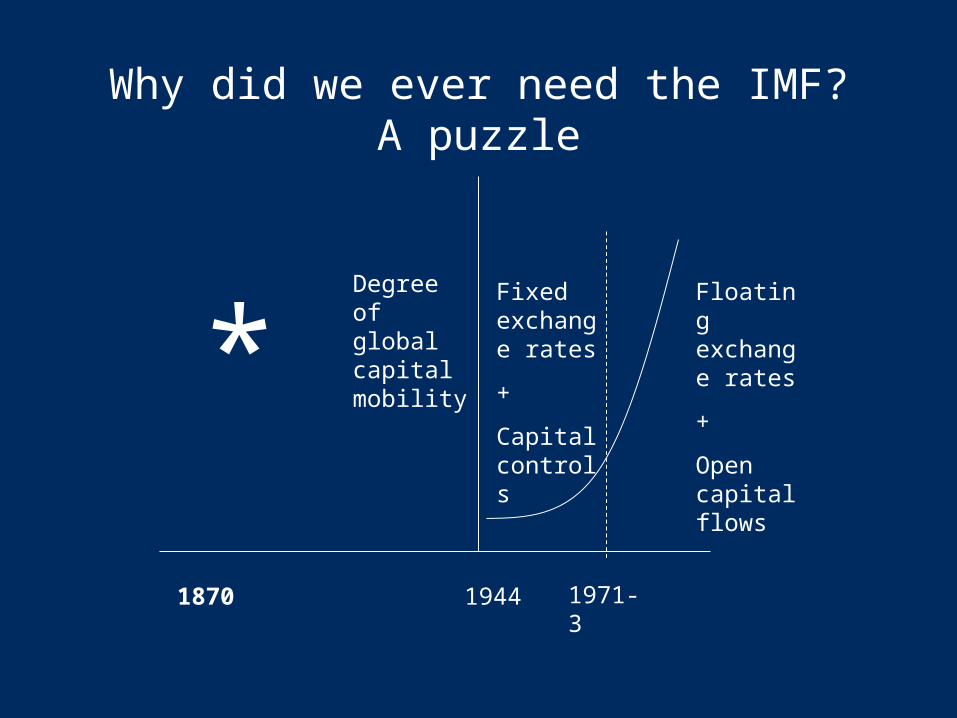

Why did we ever need the IMF?A puzzle

1944

Degree of global capital mobility

1971-3

Fixed exchange rates

+

Capital controls

Floating exchange rates

+

Open capital flows

Conclusion:

Cannot maintain (global) fixed exchange rates in the presence of

high capital mobility…?

Why did we ever need the IMF?A puzzle

1944

Degree of global capital mobility

1971-3

Fixed exchange rates

+

Capital controls

Floating exchange rates

+

Open capital flows

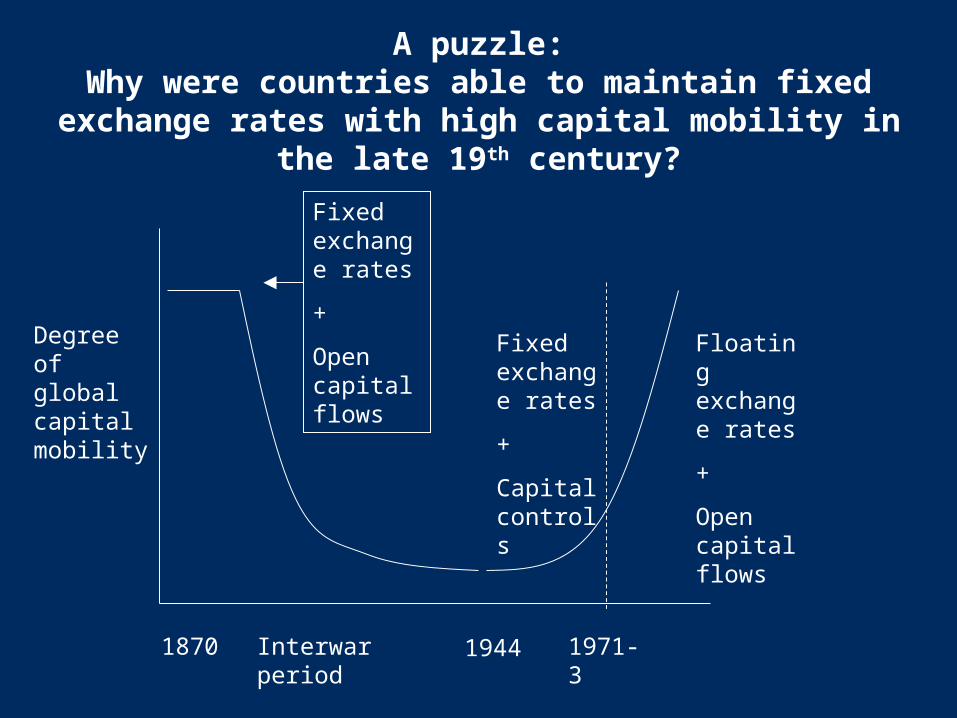

1870

*

A puzzle:Why were countries able to maintain fixed exchange

rates with high capital mobility in the late 19th century?

1944

Degree of global capital mobility

1971-3

Fixed exchange rates

+

Capital controls

Floating exchange rates

+

Open capital flows

1870 Interwar period

Fixed exchange rates

+

Open capital flows

Why?

Discussion…

Answer: Democracy

1944

Degree of global capital mobility

1971-3

Fixed exchange rates

+

Capital controls

Floating exchange rates

+

Open capital flows

1870 Interwar period

Fixed exchange rates

+

Open capital flows

Growing #’s of democraciesFew democracies

Growth of democracy (minimalist definition)

1870 (7): 1884 (8): 1897 (12): 1911 (17):

United States Norway Netherlands Sweden

Canada 1885 (9): 1901 (14): Portugal

France United Kingdom Australia 1912 (18):

Switzerland 1890 (10): Denmark Argentina

Greece Luxemburg 1909 (15):

Orange Free State 1894 (11): Cuba

New Zealand Belgium Chile

(lost OFS – 1902)

Why?

• So, why do fixed exchange rates pose a problem for democracies in the face of highly mobile capital?

Pure gold standard

• Country A imports from Country B

• Gold moves from A to B (re-coined/minted)

• Less money in A lower prices

• More money in B higher prices

Country B imports from Country A

• Balance is restored

With paper money

• Central Banks intervene by adjusting interest rates

• So gold doesn’t actually flow

• Gold Standard strict discipline!

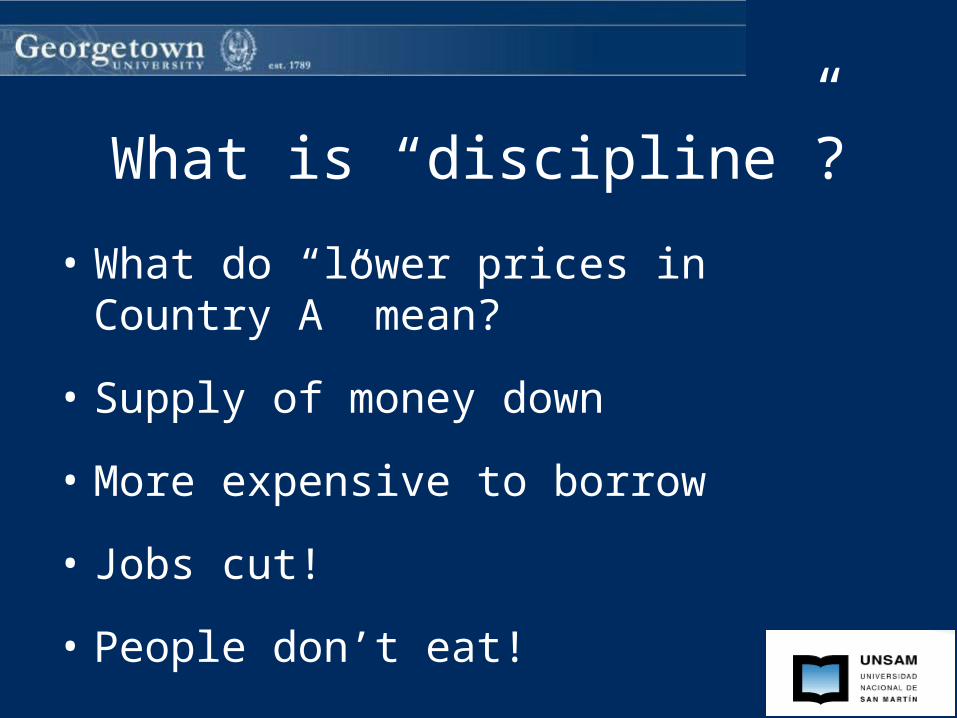

What is “discipline”?

• What do “lower prices in Country A” mean?

• Supply of money down

• More expensive to borrow

• Jobs cut!

• People don’t eat!

People don’t eat

Under authoritarianism:

• Let them eat cake

Under democracy:

• Incumbents lose elections

Hazard Rate over Time for Democracies (Solid Line) & Dictatorships (Dotted Line) – Time in years

2015105

0.625

0.5

0.375

0.25

Time (years)

Hazard Rate

Time (years)

Hazard Rate

Under democracy,

• The “pocketbook voter model”– people vote according to changes in their income– http://www.youtube.com/watch?v=loBe0WXtts8

• Sociotropic model – voters consider macro performance (economic growth, unemployment, inflation)

1956

1960

19641972

1976

1980

1984

1988

1992

1996

20002004

1952

1968

2008

4045

5055

6065

Incu

mb

en

t sh

are

of t

wo

-pa

rty

vote

(%

)

-2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

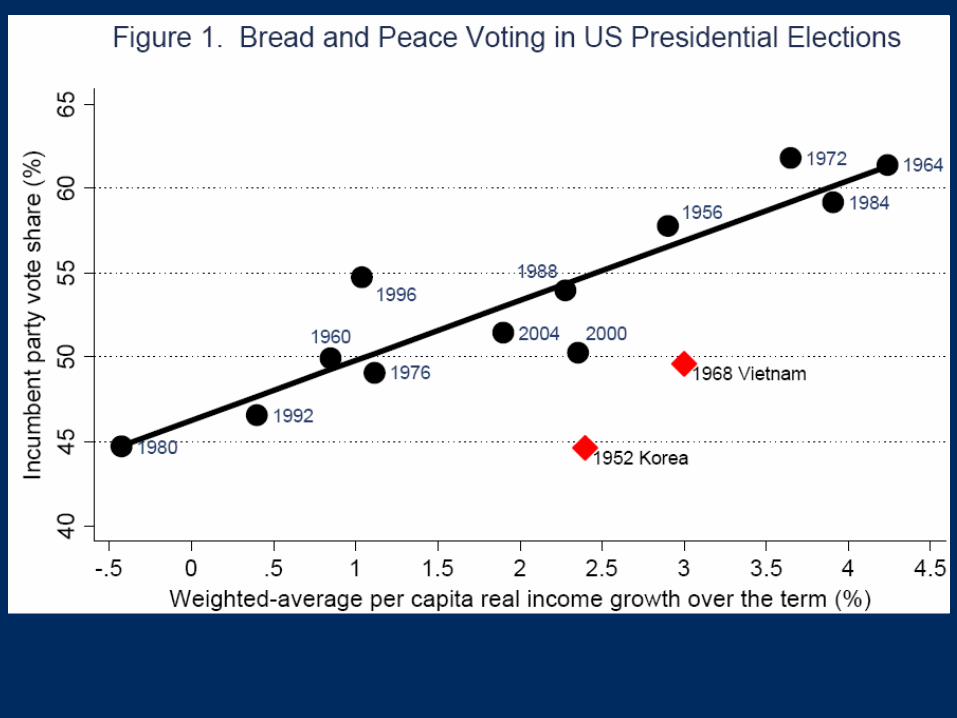

Real income growth and military fatalities combined

Combination of real growth and fatalities weights each variable by its estimated coefficient.Estimated fatalities effects: -0.7% 2008, -7.6% 1968, -9.9% 1952; negligible in 1964, 1976, 2004.Source: www.douglas-hibbs.com

Bread and Peace Voting in US Presidential Elections 1952-2008

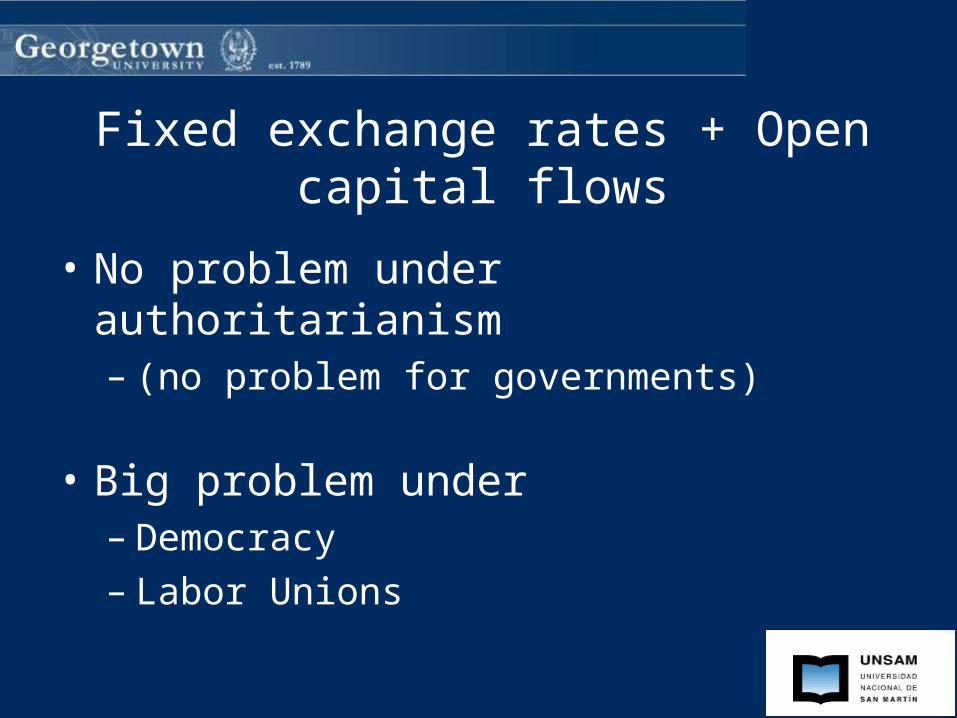

Fixed exchange rates + Open capital flows

• No problem under authoritarianism– (no problem for governments)

• Big problem under– Democracy– Labor Unions

What was the IMF supposed to do?

• Soften the blow

• Lend to “Country A” deficit-countries so that adjustment can be gradual

Problem• Keynes Plan called for contributions totaling $26 billion

(with $23 billion from the US)

• The White Plan called for only $5 billion (with $2 billion from the US)

• Compromise:– $8.8 billion, with just $2.75 billion from the US

• The US would only provide Marshall Plan assistance to countries that did not seek additional assistance from the IMF

• On the eve of the current crisis:– instead of having reserves approximating half of the value of

global imports, the IMF holds on reserve a total of less than 2 percent of global imports

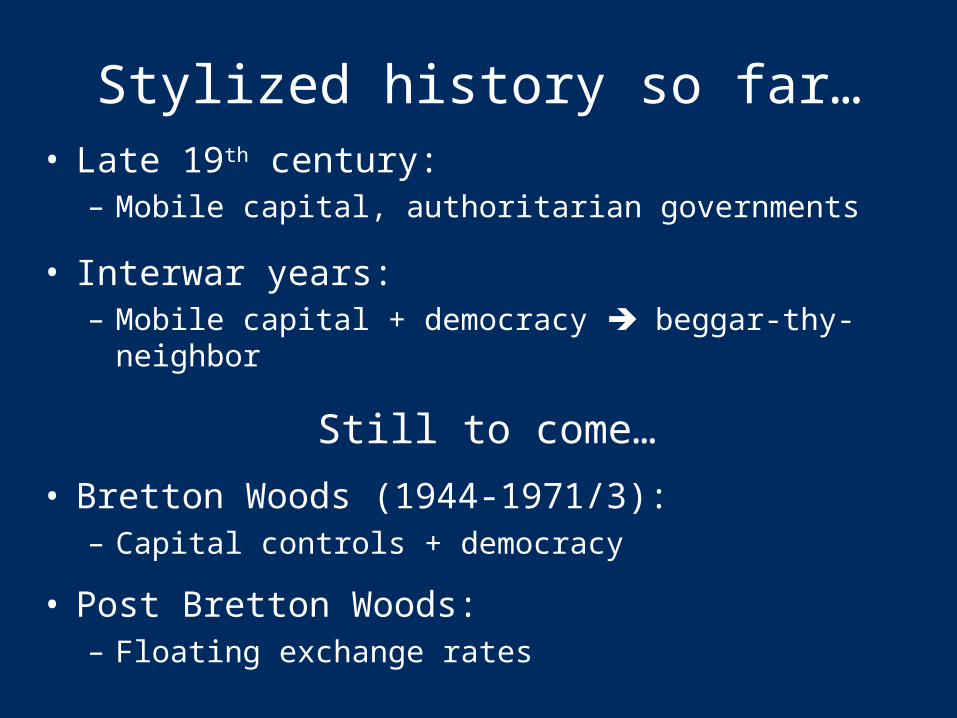

Stylized history so far…• Late 19th century:

– Mobile capital, authoritarian governments

• Interwar years:– Mobile capital + democracy beggar-thy-neighbor

Still to come…

• Bretton Woods (1944-1971/3):– Capital controls + democracy

• Post Bretton Woods:– Floating exchange rates

What was the IMF supposed to do?

After a 15 minute break

Part 2:

What is the IMF and what does it do?

What is theInternational Monetary Fund?

Based on:

Vreeland, James Raymond, The International Monetary Fund: Politics of Conditional Lending (Routledge, January 2007).

• 1944: 44 countries signed the Bretton Woods agreement

– International Monetary Fund (stability)

– World Bank (development)

• The “Bretton Woods” Institutions.

• http://www.youtube.com/watch?v=GVytOtfPZe8&feature=related

The IMF was given 2 tasks:

1. Surveillance.

2. Lending.

The IMF has mainly focused on the latter function – so we will too…

But I’ll touch on surveillance at the end.

Why lending?• Gold standard – each currency’s value

was ultimately backed up by gold.

• A balance of payments deficit could lead to a depletion of gold reserves

• Lowered confidence that the government can really back up the value of the currency

• Run on the currency… hyperinflation, breakdown of economic order!

• Governments close up trading!

A run:

http://www.youtube.com/watch?v=qu2uJWSZkck&feature=related

http://www.youtube.com/watch?v=EOzMdEwYmDU&feature=related

37

Sweeping the pengő inflation banknotes after the introduction of the forint in August 1946

Zimbabwe

Stepping back:

• Who is the IMF?

• Where does it get its resources from?

• How are decisions made?

Who is the IMF?

• Currently 187 members.

• Who’s not a member?– Andorra, Liechtenstein, Nauru, Taiwan, Cuba,

and North Korea

• Members have “votes” according to the size of their subscription to the IMF…

Where do the resources for “loans” come from?

• Members provide a contribution called the member’s quota (held on reserve).

• The size of the quota is a function of the country’s economy:

• GDP

• current account transactions

• official reserves

Largest: USA (SDR 37,149.3 million). Smallest: Palau (SDR 3.1 million).

Who controls the IMF?IMF vote shares have been “out of whack” with reality

• Top 5 members:

– United States (16.8%)

– Japan (6.0%)

– Germany (5.9%)

– France (4.9%)

– UK (4.9%)

• Other important members:

– China (3.7%)

– Saudi Arabia (3.2%)

– Russia (2.7%)

– Italy? (3.2%)

– Belgium? (2.1%)

– Brazil? (1.4%)

– India? (1.9%)

– Turkey? (0.55%)

Who controls the IMF? (2010)

• Top 5 members:

– United States (16.7%)

– Japan (6.0%)

– Germany (5.9%)

– France (4.85%)

– UK (4.85%)

• Other important members:

– Italy? (3.19)

– Saudi Arabia? (3.2%)

– Canada? (2.9%)

– Russia (2.7%)

– Belgium? (2.1%)

– China (3.65%)

– India? (1.9%)

– Spain? (1.4%)

– Brazil? (1.4%)

– Korea? (1.3%)

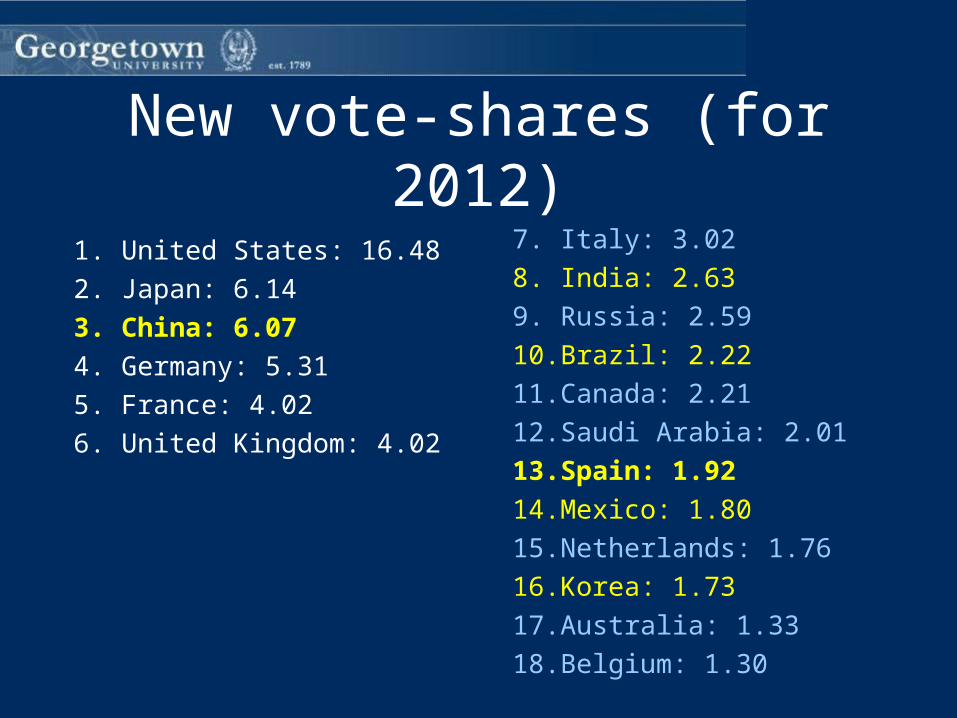

New vote-shares (for 2012)

1. United States: 16.48

2. Japan: 6.14

3. China: 6.07

4. Germany: 5.31

5. France: 4.02

6. United Kingdom: 4.02

7. Italy: 3.02

8. India: 2.63

9. Russia: 2.59

10. Brazil: 2.22

11. Canada: 2.21

12. Saudi Arabia: 2.01

13. Spain: 1.92

14. Mexico: 1.80

15. Netherlands: 1.76

16. Korea: 1.73

17. Australia: 1.33

18. Belgium: 1.30

But real distortions also occur in the elections for the Executive Board

• Recall:

– IMF Board of Governor votes: 53%

– IMF Executive Board votes: 61%

Appointed & Elected Directors• Appointed:

– US, Japan, Germany, France, UK

• Elected:– China, Saudi Arabia, Russia

• Regionally elected (ad-hoc)– Australia

• South Pacific, New Zealand, Korea, Uzbekistan

– Brazil• Latin American countries

– Togo• African countries

– Iran• Afghanistan, Algeria, Ghana, Morocco, Pakistan, Tunisia

Really ad-hoc elected Directors:

• Italy– Greece, Malta, Portugal, San Marino, Albania, & Timor-

Leste

• Belgium– Austria, Luxembourg, Belarus, Czech Republic,

Hungary, Kosovo, Slovak Republic, Slovenia, & Turkey

• Netherlands– Armenia, Bosnia and Herzegovina, Bulgaria, Croatia,

Cyprus, Georgia, Israel, Macedonia, Moldova, Montenegro, Romania, & Ukraine

• Switzerland– Azerbaijan, Kazakhstan, Kyrgyz Republic, Poland,

Serbia, Tajikistan, & Turkmenistan

Figure 1: Seats around the IMF Executive Board (by Director's total vote share, 2010)

United States, 16.7%

Japan, 6.0%

Germany, 5.9%

France, 4.9%

United Kingdom, 4.9%

Belgium, 5.1%

Netherlands, 4.8%Spain, 4.4%Italy, 4.1%

China, 3.7%

Canada, 3.6%

Thailand, 3.5%

Korea, 3.4%

Denmark, 3.4%

Egypt, 3.2%

Saudi Arabia, 3.2%

Sierra Leone, 3.0%

Switzerland, 2.8%

Russia, 2.7%

Iran, 2.4%

Brazil, 2.4%

India, 2.4%

Argentina, 2.0%

Rwanda, 1.3%

How do they do it?

• Foreign aid?

Buying Bretton Woods James Raymond Vreeland

Georgetown [email protected]

Paper prepared for presentation at the AidData Conference, University College, Oxford, March

22-25, 2010

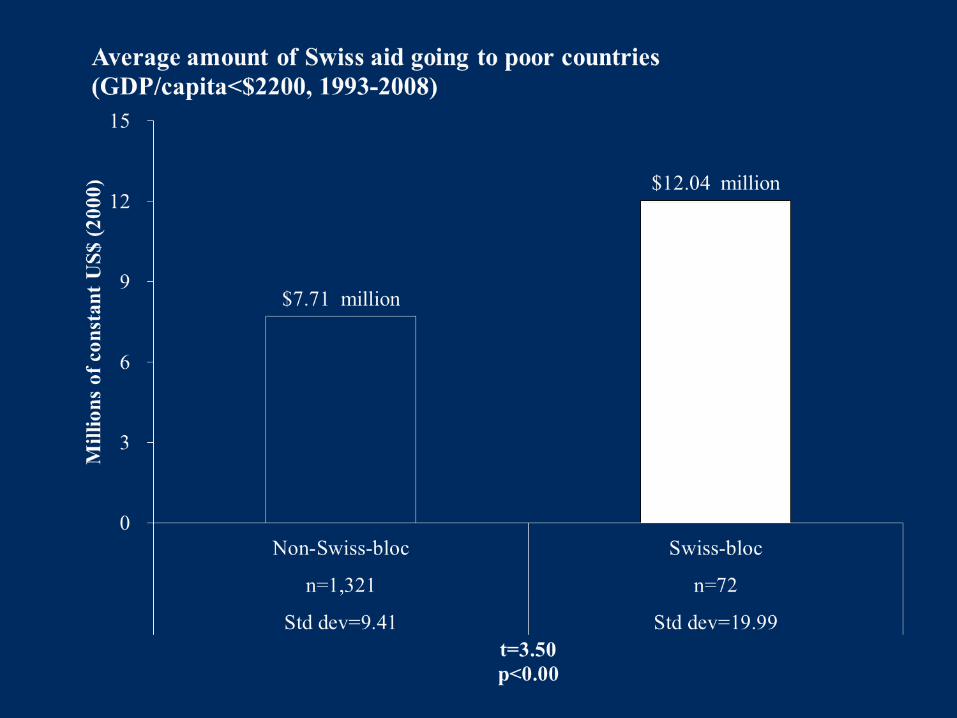

Switzerland?

• New IMF member (1992)– Bloc does not have deep historical ties other

than joining around the same time– Data for the entire period are available

• Switzerland has added incentives– Out of the EU, out of the G20

THE EXECUTIVE BOARD MAKES LENDING DECISIONS

Suffice to say:

IMF lending as insurance

• A loan from the IMF enables a country to survive a temporary balance of payments deficit.

So…as an international lender,

• If a country gets into a balance of payments crisis, or for whatever reason, has a shortfall in its foreign reserves,

• The IMF can provide a loan (lest this country enter into destructive policies).

• Problem: This “bailing out” option lowers the incentive to pursue sound policy.

“Moral Hazard.”

How do we deal with moral hazard?

• Automobile insurance?

• Too big to fail?

• The IMF?

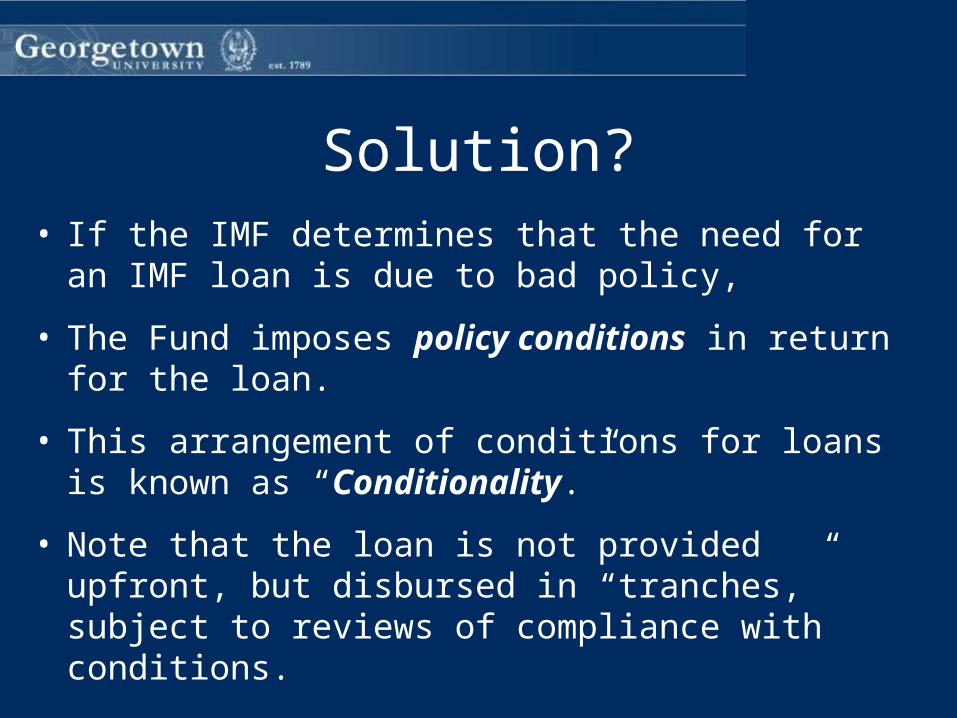

Solution?• If the IMF determines that the need for an IMF loan

is due to bad policy,

• The Fund imposes policy conditions in return for the loan.

• This arrangement of conditions for loans is known as “Conditionality.”

• Note that the loan is not provided upfront, but disbursed in “tranches,” subject to reviews of compliance with conditions.

Policy conditions have traditionally entailed:

• Fiscal austerity– cutting government services and increasing taxes

• Tight monetary policy– raising interest rates and reducing credit creation

• Sometimes currency devaluation

• What are the goals of IMF programs?

– Economic stability

– Economic growth

La loi• LETTER OF INTENT

• Drafted (by whom?)… signed by finance minister, central bank president, and/or chief executive

• Sent to the Executive Board for approval

• 1st “tranche” of loan released

• Ya want another tranche?– Conditionality (goodfellas)

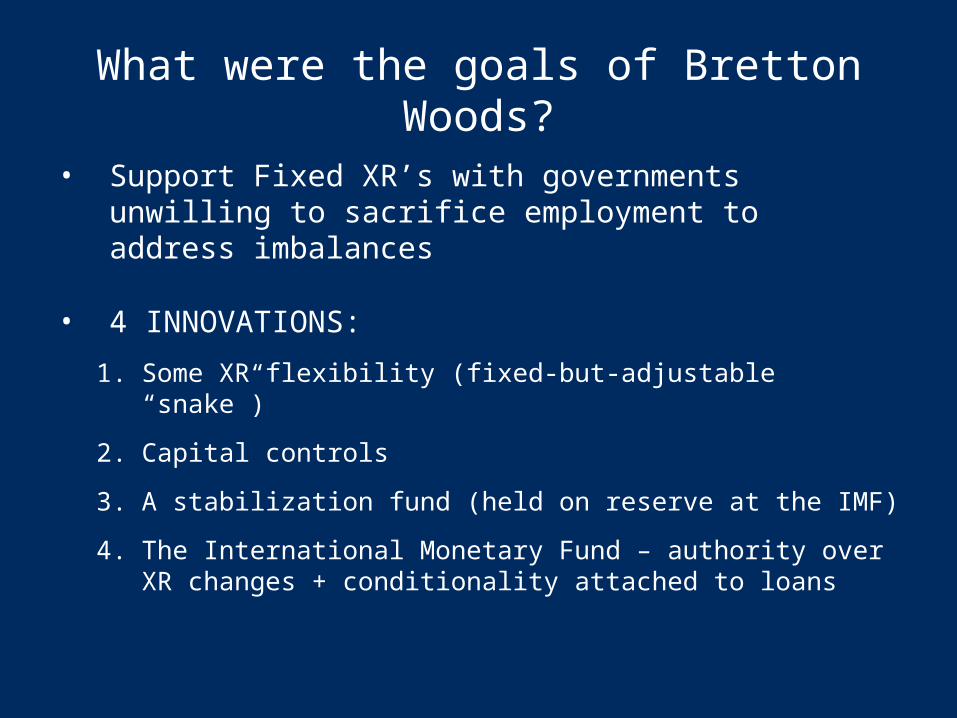

What were the goals of Bretton Woods?

• Support Fixed XR’s with governments unwilling to sacrifice employment to address imbalances

• 4 INNOVATIONS:

1. Some XR flexibility (fixed-but-adjustable “snake”)

2. Capital controls

3. A stabilization fund (held on reserve at the IMF)

4. The International Monetary Fund – authority over XR changes + conditionality attached to loans

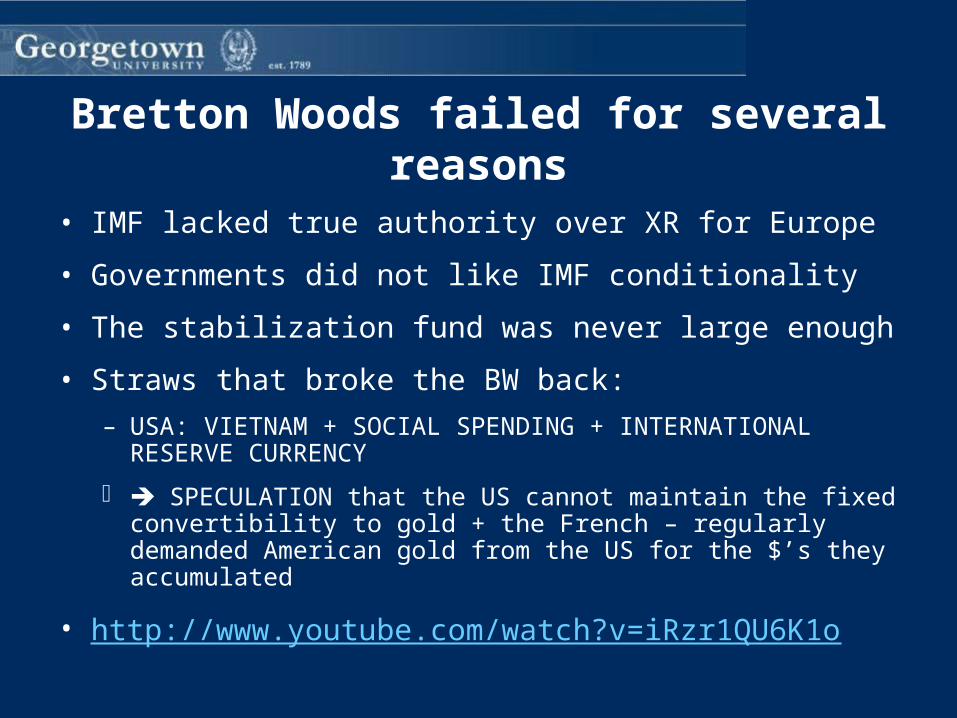

Bretton Woods failed for several reasons

• IMF lacked true authority over XR for Europe

• Governments did not like IMF conditionality

• The stabilization fund was never large enough

• Straws that broke the BW back:

– USA: VIETNAM + SOCIAL SPENDING + INTERNATIONAL RESERVE CURRENCY

SPECULATION that the US cannot maintain the fixed convertibility to gold + the French – regularly demanded American gold from the US for the $’s they accumulated

• http://www.youtube.com/watch?v=iRzr1QU6K1o

• The world shifted away from the Bretton Woods-gold standard in the 1970s

• The old exchange system collapsed.

• The IMF faced a crisis of purpose.

• But the IMF was already involved in the developing world.

• Expanded this role – not just lending for stability, but also to promote development.

The shift?

Was there really a shift?

Figure 1.1: Percentage of countries participating in IMF programs

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

1946

1949

1952

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

Year

Per

cen

t

Western Europe, US and Japan Rest of the world

Europe takes up a new path

• The European Monetary System – 1979

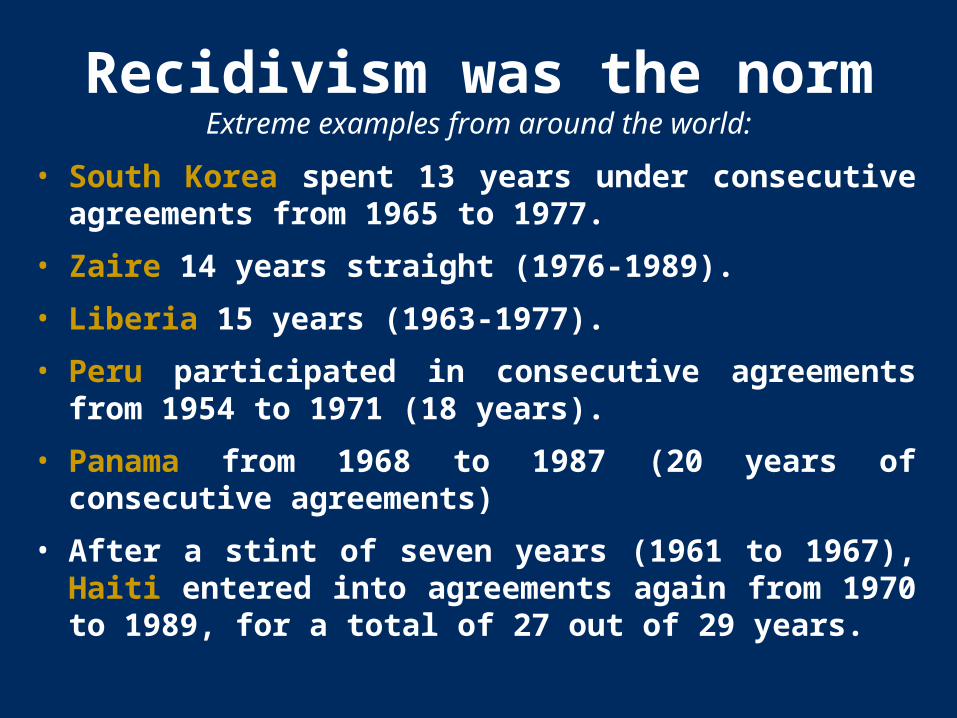

Recidivism was the norm Extreme examples from around the world:

• South Korea spent 13 years under consecutive agreements from 1965 to 1977.

• Zaire 14 years straight (1976-1989).

• Liberia 15 years (1963-1977).

• Peru participated in consecutive agreements from 1954 to 1971 (18 years).

• Panama from 1968 to 1987 (20 years of consecutive agreements)

• After a stint of seven years (1961 to 1967), Haiti entered into agreements again from 1970 to 1989, for a total of 27 out of 29 years.

One last question:

• Why do governments participate in IMF programs?

– Domestic politics stories…

– International politics stories…

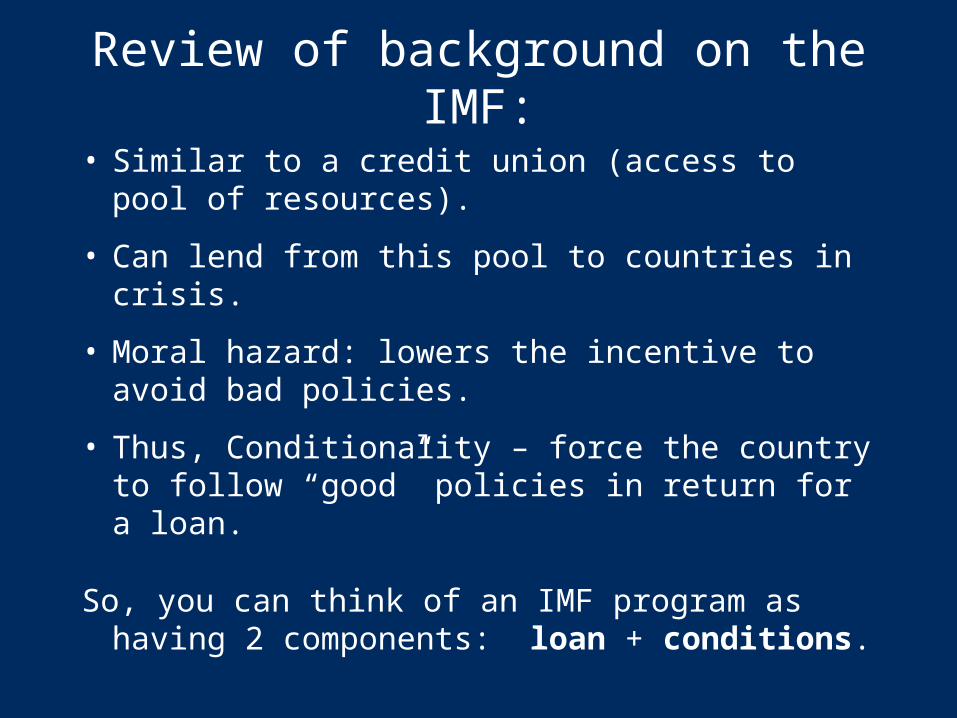

Review of background on the IMF:

• Similar to a credit union (access to pool of resources).

• Can lend from this pool to countries in crisis.

• Moral hazard: lowers the incentive to avoid bad policies.

• Thus, Conditionality – force the country to follow “good” policies in return for a loan.

So, you can think of an IMF program as having 2 components: loan + conditions.

Thank youWE ARE GLOBAL GEORGETOWN!