global economy: its impact on turkey and mediterranean region

TRANSCRIPT

Republic of Turkey Prime Ministry

Investment Support & Promotion Agency of Turkey (ISPAT)

Global Economy: Its Impact on

and Mediterranean

Necmettin KAYMAZ

Chief Project Director

Turkey 2nd Polyolefins Conference, 28 April 2015, Gaziantep

AGENDA

Overview of Global Economy

Recent Developments’ Impact on Global Economy

Impact on the Mediterranean Economies

Impact on Turkish Economy

Investment Support & Promotion Agency of Turkey

Established in 2006 to increase & attract direct investment

Attached to the Prime Ministry & directly report to the PM

Private sector approach with public sector capabilities

ONE STOP SHOP approach

Providing extensive services:

Coordination with relevant governmental institutions

Market information and analyses

Site selection

Matchmaking potential partners

Facilitating legal procedures, such as:

-Company set-up; incentive applications; work permits

Investment Support & Promotion Agency of Turkey

The International Network

Overview of Global Economy

Source: IMF

Global economy has been on constant growth since 1980 despite volatile growth rates and the global financial crisis which almost brought it to a halt in 2009..

Global economy expanded 3,4% in

2014 and is expected to grow

3,5% in 2015

100

150

200

250

300

350

400

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15

20

20

World Economy, Real GDP Index (1980=100)

forecast

0%

1%

2%

3%

4%

5%

6%

1980 1985 1990 1995 2000 2005 2010 2015 2020

World Economy, Real GDP Growth Rates (%)

2016-2020:

3.9% CAGR

Source: IMF

World economy is expected to reach almost $150 trillion by 2020, up from $108 trillion in 2014..

13

14

15

17

18

19

20

21

23

25

27

28

32

34

35

38

40

42

44

46

49

51

54

57

62

67

72

78

82

83

88

94

98

10

3 10

8 11

3 1

18

12

5 1

33

14

1

14

9

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150World GDP

(PPP, $Trillion)

f o r e c a s t

Source: IMF

Emerging and developing markets have been and will continue to be the main source of growth in the world economy despite slowdown…

61,7

107,9

149,4

33,0

29,3

13,2

12,2

-10

10

30

50

70

90

110

130

150

2004 2005-2014 2014 2015-2020 2020

Emerging & Developing Economies Advanced Economies

World Economy, GDP at PPP ($ Trillion)

Over the next 6 years, world output will

increase $41,5 trillion, more than 70% of

growth will come from emerging & developing

economies

Source: IMF

f o r e c a s t

25%

50%

75%

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Emerging & Developing economies

Advanced economies

57%

43%

61%

39%

The gravity of global economy has been shifting towards emerging & developing economies whose share in the world economy has been gradually increasing….

Breakdown of World Economy, GDP at PPP, %

Source: BBVA Research, IMF and Quah D., 2011, “The Global Economy’s Shifting Centre of Gravity”.

Shifting the economic center of gravity from the Atlantic to the Pacific area

Global growth will be concentrated in the Asia-Pacific region, which will account for 76.5% of the increase in GDP between 2014 and 2024..

Recent Developments’ Impact

on

Global Economy

World economy will be affected by various developments…

Source: IMF

Source: IMF

The sharp fall in oil prices will spur global growth, but not enough to offset other

negative factors..

Source: IMF

Oil prices have drastically decreased in recent months and are expected to rebound over the next couple of years..

58

74

0

10

20

30

40

50

60

70

80

90

100

110

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Annual Oil Price* (US$ per barrel) F o r e c a s t

Source: IMF, *Crude Oil (petroleum), simple average of three spot prices; Dated Brent, West Texas Intermediate, and the Dubai Fateh

CAVEAT: Oil prices may rebound sooner than expected…

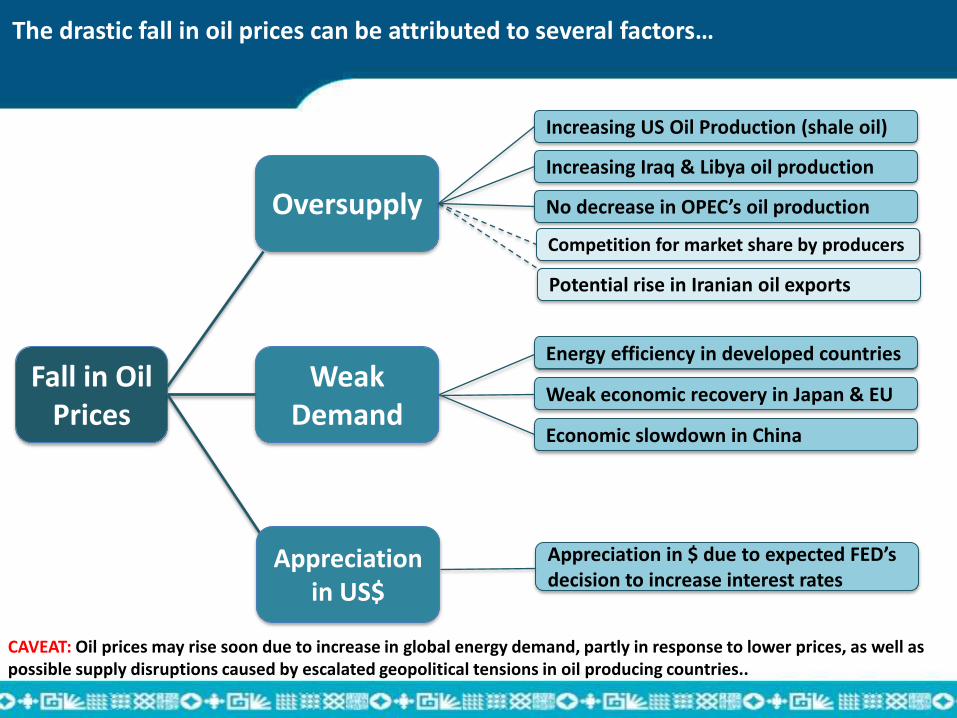

The drastic fall in oil prices can be attributed to several factors…

CAVEAT: Oil prices may rise soon due to increase in global energy demand, partly in response to lower prices, as well as possible supply disruptions caused by escalated geopolitical tensions in oil producing countries..

Fall in Oil Prices

Oversupply

Weak Demand

Increasing US Oil Production (shale oil)

Increasing Iraq & Libya oil production

No decrease in OPEC’s oil production

Energy efficiency in developed countries

Weak economic recovery in Japan & EU

Economic slowdown in China

Appreciation in $ due to expected FED’s decision to increase interest rates

Competition for market share by producers

Potential rise in Iranian oil exports

Appreciation in US$

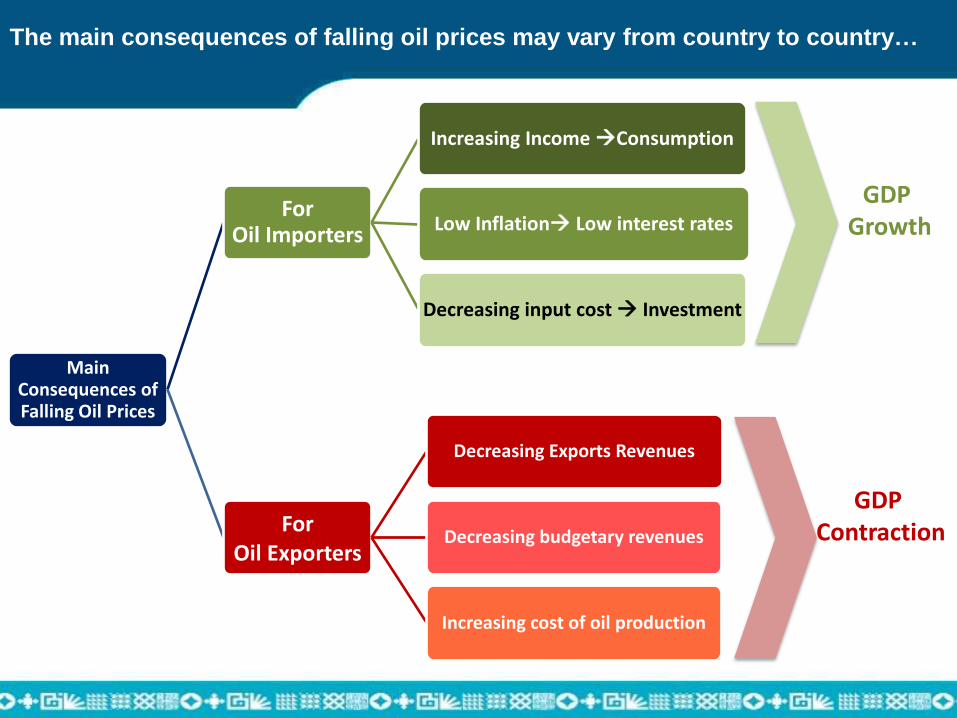

The main consequences of falling oil prices may vary from country to country…

Main Consequences of Falling Oil Prices

For Oil Importers

Increasing Income Consumption

Low Inflation Low interest rates

Decreasing input cost Investment

For Oil Exporters

Decreasing Exports Revenues

Decreasing budgetary revenues

Increasing cost of oil production

GDP Growth

GDP Contraction

The falling oil prices will have both negative and positive impact on economies across the world with varying degrees according to the level of their dependency on oil…

Energy dependency, Oil imports/exports* as % of GDP 2010-13 average

Source: UNCTAD, The Economist *Including petroleum products such as refined oil or kerosene, †Net imports/exports of less than 0.1% of GDP

Source: Oxford Economics / Haver Analytics

The impact of falling oil prices on GDP growth could be somewhere between 0.4% and 0.7%...

The low oil prices will have positive and negative impacts on various sectors across the world..

STRONG

NEGATIVE

MILD

NEGATIVE

NO

EFFECT

MILD

PORSITIVE

MODERATE

POSITIVE

STRONG

POSITIVE

Building Materials

(Proppant) Aerospace

Refining &

marketing

Paper/Forest

products Autos Airlines

Exploration &

Production

Regulated

utilities & power

producers (Europe)

Regulated

utilities & power

producers (Asia)

Regulated

utilities & power

producers (US)

Building Materials

(ex proppant) Protein / Food

Oilfield Services Gaming (Asia) Gaming (US) Chemicals Shipping

Steel

(oil country

tubular goods)

Steel

(ex oil country

tubular goods)

Mining

(Base Metals &

Coal)

Consumer

Durables

Lodging Cruise

Manufacturing Restaurants

Surface

Transportation

Homebuilding

(US)

Theme Parks

(US) Retail

Overall impact of low oil prices on global corporate sectors

Source: Moody’s Investors Service

Impact on the Mediterranean Economies

Developing countries in the Mediterranean region will have robust economic growth, while the developed economies in the region will struggle to sustain growth..

5,1

4,6 4,3

4,2

3,6 3,5 3,4

3,2 3,1 3,1 3,0

2,7

1,9 1,9 1,6 1,6 1,5

1,0

Mo

rocc

o

Egyp

t

Tun

isia

Alb

ania

Alg

eria

Turk

ey

Bo

snia

Leb

ano

n

Isra

el

Mo

nte

neg

ro

Gre

ece

Mal

ta

Spai

n

Slo

ven

ia

Fran

ce

Sou

th C

ypru

s

Cro

atia

Ital

y

Source: IMF

11,9 Li

bya

Average Real GDP Growth (%) in Mediterranean Projection for 2015-2020

Source: International Trade Center

Almost all of Mediterranean economies are net energy importers, hence falling oil prices will have a positive impact for the net importers..

-85.000

-65.000

-45.000

-25.000

-5.000

15.000

35.000

55.000

Fran

ce

Ital

y

Spai

n

Turk

ey

Gib

ralt

ar

Isra

el

Mo

rocc

o

Gre

ece

Leb

ano

n

Cro

atia

Slo

ven

ia

Sou

th C

ypru

s

Pal

esti

ne

Bo

snia

Egyp

t

Tun

isia

Mal

ta

Alb

ania

Syri

a

Lib

ya

Alg

eria

2010-2013 Annual Average Trade Balance in Energy Products ($ Million)

While countries on the north of Mediterranean rim are net oil importers, the ones on the south are mainly net exporters with a few exceptions..

Energy dependency Oil imports/exports* as % of GDP 2010-13 average

Source: UNCTAD, The Economist *Including petroleum products such as refined oil or kerosene, †Net imports/exports of less than 0.1% of GDP

Despite positive impact of falling oil prices, the implications for Med countries are mixed..

Oil producing countries are also significant export markets for the Med countries…

The EU, another major export market for the Med countries, will benefit from low oil prices, despite slow recovery…

While the impact of recent global financial crisis on the Middle East & North African (MENA) countries was limited, MENA is still underperforming pre-crisis level…

7,0

3,7 3,8 3,8

0

1

2

3

4

5

6

7

Pre-Crisis 2003-2007 Crisis 2008-2009 Post-Crisis 2010-2014 Forecast 2015-2020

Growth Outlook for MENA, Average Anuual Real GDP Growth Rates (%)

Pre-crisis level: 7%

Source: IMF

EU is still struggling to recover from the financial and debt crises, growth hasn’t reached pre-crisis levels but outlook seems relatively favorable as the growth is expected to double over the next 6 years.

2,7

-1,8

1,0

1,9

-2,0

-1,5

-1,0

-0,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

Pre-Crisis 2003-2007 Crisis 2008-2009 Post-Crisis 2010-2014 Forecast 2015-2020

Growth Outlook for the EU, Average Anuual Real GDP Growth Rates (%)

Pre-crisis level: 2,7%

Source: IMF

Despite cautious optimistic growth outlook, Med countries may benefit from increasing trade volume in the region..

129

145

100

105

110

115

120

125

130

135

140

145

150

2014 2015 2016 2017 2018 2019 2020

Estimated Volume of Imports of Goods (Index: 2014 = 100)

MENA

Euro Area

Source: IMF

Impact on the Turkish Economy

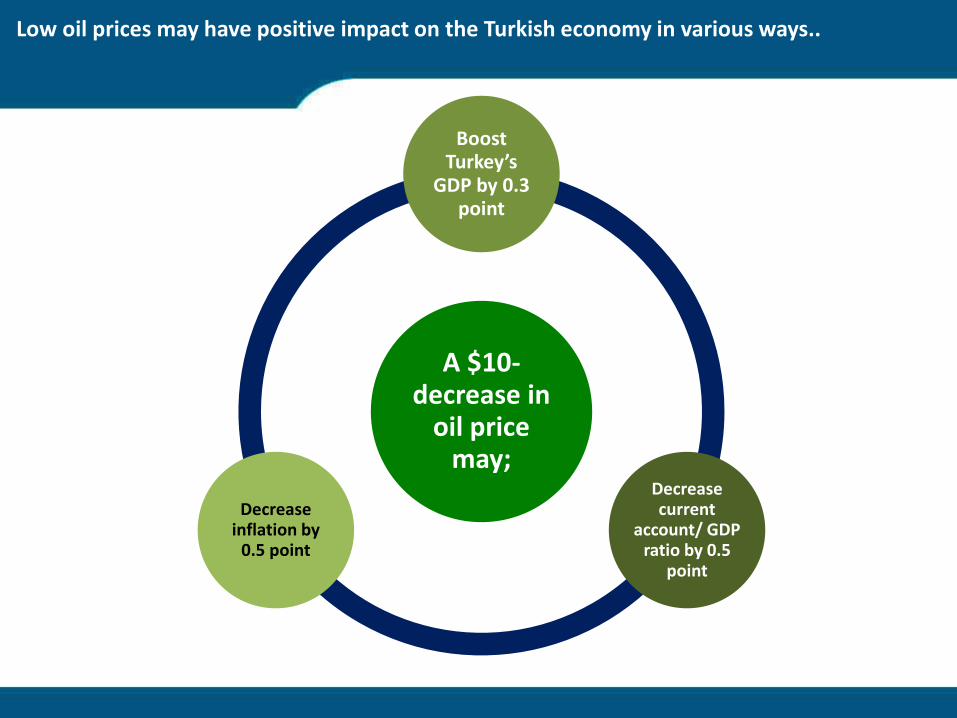

Low oil prices may have positive impact on the Turkish economy in various ways..

A $10-decrease in

oil price may;

Boost Turkey’s

GDP by 0.3 point

Decrease current

account/ GDP ratio by 0.5

point

Decrease inflation by

0.5 point

Source: TurkStat, Treasury

Considering Turkey’s dependence on oil import, it will surely benefit from falling oil prices …

Impact of Energy Prices to Imports of Energy Products ($Billion)

41,7 44,5 43,8

46,2

12,5

15,6 12,1 8,7

38,5

54,2

60,1

55,9 54,9

0

15

30

45

60

2010 2011 2012 2013 2014

Price Effect

Energy Importsfixed to 2010 prices

Actual EnergyImport

Source: TURKSTAT *Coach ticket, airline ticket, intracity transportation, courier services

Considering the oil-related components of the CPI in Turkey, low oil prices may lower inflation as well, but may be offset by pass-through as a result of $$$ appreciation..

Gasoline, Diesel, LPG; 6%

Natural Gas, Electricity; 5% Other

Transportation*; 10%

Others; 79%

Breakdown of CPI (Inflation) Basket in Turkey

Source: TURKSTAT

Export Diversification

Over the past 12 years, Turkey has successfully managed to diversify its exports market and products, hence been able to adjust and make up for the loss during crises in a one of the export markets..

2002 2014

Number of export products with over $1 billion 9 37

Number of export markets with over $1 billion 8 34

Share of top 5 countries (%) 47 31

Share of MENA (%) 13 28,6

Share of North America (%) 10 4,6

Share of EU (%) 57 43

Source: IMF World Economic Outlook April 2014, Eurostat, OECD, TurkStat, OECD Economic Outlook No.95, May 2014

0,8 1,0 1,1 1,1

1,4 1,6 1,6 1,7 1,9

2,5 2,5

3,1 3,2

3,7 3,9 4,0 4,0

4,7

0

1

2

3

4

5

Japan

Fra

nce

Germ

any

EU

28

Hungary UK

Slo

venia

Irela

nd

US

Czech R

ep.

Mexic

o

South

Afr

ica

Bra

zil

Kore

a

Pola

nd

Russia

Slo

vakia

Turk

ey

Average Annual Real GDP Growth (%) 2002-2014 Strong record, bright future

Regardless of the price of oil, Turkey continues to sustain its economic growth trajectory over the next 15 years with robust economic performance..

1,1 1,1

1,4 1,5 1,5

1,6 1,7 1,7 1,9

2,0 2,0 2,1 2,2 2,2 2,2 2,2 2,3 2,4

2,6 2,6 2,6 2,6 2,7 2,9 2,9 2,9

4,2

0

1

2

3

4

Ge

rman

y

Jap

an

Po

rtu

gal

Spai

n

Ital

y

Den

mar

k

Euro

Are

a

Hu

nga

ry

Au

stri

a

Bel

giu

m

Fin

lan

d

Can

ada

Fran

ce

Po

lan

d

OEC

D

Gre

ece

Irel

and

US

Swed

en UK

Slo

vaki

a

Bra

zil

Ru

ssia

Cze

ch R

ep.

Mex

ico

Ko

rea

Turk

ey

Potential Real GDP Growth 2014-2030 (Average Annual, %)

D i s c o v e r t h e P o t e n t i a l

Togetherness

Both East & West

World

Meeting

Harmony

Innovation

Synergy

Growth