global space industry dynamics … · web viewglobal space industry dynamics. ... china, europe,...

TRANSCRIPT

Global Space Industry DynamicsResearch Paper for Australian Government, Department of Industry, Innovation and Science by Bryce Space and Technology, LLC

The goal of this paper is to assist Australian Government in a review to of Australia’s space industry capability to enable the nation to capitalise

on the increasing opportunities within the global space sector.

Contents

Executive Overview

1Elements and Attributes of the Global Space Industry

3Government Space Programs

3Commercial Space Activities

5Geography of the Space Ecosystem

8

Trends and Industry Dynamics

11Opportunities for Australia

12Mature Space Sectors

12Emerging Markets

14

Appendix: Core Technologies

17Launch Vehicles

17Satellites

17Exploration/Government Programs

19

Appendix: Selected Space Terms and Acronyms

20About Bryce Space and Technology

23Endnotes

25

This page intentionally left blank

Executive Overview

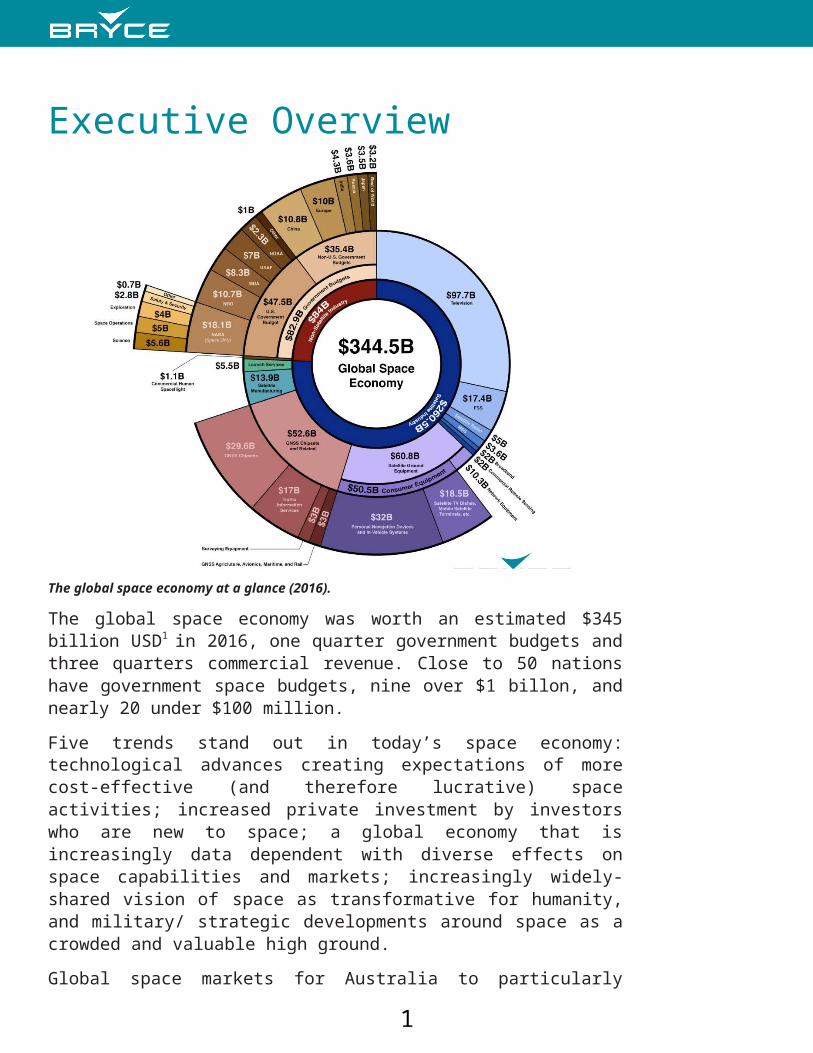

The global space economy at a glance (2016).

The global space economy was worth an estimated $345 billion USD1 in 2016, one quarter government budgets and three quarters commercial revenue. Close to 50 nations have government space budgets, nine over $1 billon, and nearly 20 under $100 million.Five trends stand out in today’s space economy: technological advances creating expectations of more cost-effective (and therefore lucrative) space activities; increased private investment by investors who are new to space; a global economy that is increasingly data dependent with diverse effects on space capabilities and markets; increasingly widely-shared vision of space as transformative for humanity, and military/ strategic developments around space as a crowded and valuable high ground.Global space markets for Australia to particularly consider, based on future growth, Australia’s capabilities, and barriers to entry:

• Consumer broadband• Managed services

1

• Earth observation-driven data analytics• Satellite radio• Navigation devices and applications• Commercial space situational awareness• Smallsat manufacturing• Possible benefits from launch facility• Space mining

2

3

Elements and Attributes of the Global Space Industry

The global space economy was an estimated $345 billion USD in 2016.2 This total is broadly divided into government budgets (nearly one quarter) and commercial revenue (more than three quarters).3

Government Space ProgramsGovernment space activities include military applications for imagery and communications and civil activities including weather forecasting, science, and human exploration. In addition, governments, particularly those of the United States and Europe, also procure commercial space services, especially launch, satellite imagery and communications, to meet mission requirements. Historically, many governments have taken a role in enabling satellite communication through national postal, telegraph, and telephone (PTT) organisations, which have in many cases been privatised. Governments may also seek to stimulate economic growth through space activities.

Largest Space ActorsNine national space budgets (considering Europe collectively) exceed $1 billion: those of the United States, China, Europe (collectively), Russia, India, Japan, France, Germany, and Italy.

The United States leads in government space spending, with an

4

Composition of Australia’s Space BudgetAustralia’s civil space research and development budget in 2015-16 was roughly $20.5 million ($28.2 Australian at Jan. 1, 2016, exchange rate), but that amount captures only a subset of Australian space activities, which are carried out by different agencies. The Australian Defence Ministry spends up to $1 billion on space related activities, with much of that going toward cooperative programs with the U.S. Department of Defence.

estimated $48 billion spread among 11 agencies and offices.4

China follows at $11 billion, with the budget allocated to the military and civil space agency supported by a single contracting entity called China Aerospace Science and Technology Corporation (CASC).5 The space budget of the European Space Agency (ESA) is about $7 billion.6 ESA receives contributions from 22 member states, each state contributing funds based on its gross domestic product (GDP).7 Russia’s budget experienced a major reduction in 2016 (part of a plan that seeks to reduce multi-year government expenditures in light of dropping

5

oil prices) and is estimated to be nearly $4 billion.8 In 2013, Russia started to consolidate its space industry by bringing space contractors under an umbrella organisation called Roscosmos, completing the process in 2016. The top-tier space powers—the United States, China, Europe, and Russia—are the world’s top geopolitical and, with the exception of Russia, economic powers. They possess the full range of space capabilities necessary to preserve and enhance their military and economic power and prestige.Other space powers like India, Japan, France, Germany, and Italy possess technical capabilities that rival and in some cases surpass those of the top space powers (in areas such as global navigation satellite services, or GNSS, imagery intelligence gathering, and space situational awareness), but their programs are smaller in scale and budget. The space investment drivers for these countries vary. India’s program (with a budget of over $4 billion9) has long reflected its self-sufficiency, economic development, and strategic-military goals, although in recent years India has sought to enhance its international prestige by undertaking missions to the Moon and Mars. For Japan (with a budget of over $3 billion10), scientific and technical achievement traditionally have been the major focus, but the threat of North Korea has prodded Tokyo to pursue programs that are more military in nature.11 Japan and India have their own domestic launch capabilities, while France, Germany, and Italy, with space budgets of $2.4 billion, $1.6 billion, and $1.2 billion respectively,12 are the leading partners in Europe’s ArianeGroup launch consortium.All these nations with $1 billion+ space budgets have human spaceflight programs, indigenous launch capability (noting that France, Germany, and Italy achieve this through their participation in ESA), and significant national security space systems. These capabilities tend to be differentiators between the largest space actors and the next tier. Of the 40 or so nations with space budgets less than $1 billion, five have indigenous launch capability (Israel, South Korea, North Korea, Iran, and, potentially, New Zealand) and none have a human spaceflight program (noting that several European countries and Canada contribute either through NASA or ESA in this regard). Some countries, like Israel and Turkey, have imagery intelligence (IMINT) satellites in operation.

Mid-Tier and Growing Space ActorsOf nations with space agencies below the billion dollar threshold, about half exceed

6

$100 million (to a high value of $600 million, for South Korea) while the remainder allocate at least $20 million per year. Nineteen of these countries are members of ESA but also support separate space activities. In addition, Eumetsat, an intergovernmental agency distinct from ESA set up to share meteorological data for European member states, has an annual budget just under $200 million.Several countries have recently intensified efforts to pursue more robust space programs, including South Korea, Turkey, the UK, and the United Arab Emirates (UAE). All have been expanding their investment in space in pursuit of economic and strategic objectives, with varying emphasis on one or the other. The UK, for example, has long invested in military satellite communications but since 2013 has been accelerating its civil space spending to advance its economic competitiveness.Niche players in the space economy, who contribute funding to support distinct space missions (often as part of a joint or international program) or leverage space

7

applications, include Australia, Canada, Israel, Norway, and Sweden. These countries tend to have small but highly educated populations, industrialised economies, and space capabilities that are world class but concentrated on a few key technologies or markets. Australia, for example, is a key partner in gathering and distributing space situational awareness (SSA) data, leveraging its technical expertise and ground-based assets.Some countries allocate funding for space-related projects without having a dedicated space agency or national security space mission. Luxembourg, for instance, has put aside funding to provide incentives for companies worldwide interested in pursuing new space efforts, particularly the identification, extraction, and processing of non- terrestrial resources. Luxembourg has already pledged nearly $20 million in funding and facilities support to US-based Planetary Resources. Part of this effort aims to challenge, update, and draft related legal tools.Governments also plant their flag in space through ownership and operation of satellites procured on the commercial market. Mexico is among the countries that have taken that route to joining the club of spacefaring nations. Others include Azerbaijan, Belarus, Nigeria, Singapore, and Vietnam.Cooperation among governments is an important feature of the global space landscape. Such cooperation allows countries to pool resources and also serves as a tool of international diplomacy.

Commercial Space ActivitiesThe commercial space economy is dominated by the services and products that satellites provide: television to homes, broadband connections, mobile asset tracking, mobile communications, and data connections for organisations around the world. The mature satellite industry also includes satellite manufacturing, launch, and ground equipment.In addition, new satellite business models and capabilities have emerged in recent years, still largely in the investment and development phase (that is, not yet generating substantial revenue). Several companies and government agencies seek to service satellites on orbit. Dozens of large constellations of small satellites (tens or hundreds of kilograms in size, rather than thousands) designed to provide new global imagery and communications services are in development, as are very small launch vehicles aimed at launching them. Expanded downstream

8

applications relying on advanced data analytics and machine learning seek to exploit new satellite data to provide insight into the terrestrial economy, as well as provide commercial space situational awareness.Beyond the satellite industry, commercial space also includes human spaceflight, platforms, manufacturing, mining and resource utilisation, and other markets. These markets are at a relatively early stage, attracting initial investment and still seeking robust business cases in the face of uncertain demand; typically, they require high capital expenditure. These factors add to their business risk.

RevenueThe commercial space sector accounts for an estimated $262 billion of the annual global space economy, almost entirely satellite industry revenues. Satellite revenues have more than doubled in the last decade,13 although growth has slowed in recent years.

9

Satellite revenue is dominated by two massive satellite markets: direct to home television (DTH, at about $100 billion) and GNSS products and services (about $85 billion, counting stand-alone navigation devices and GNSS chipsets supporting location-based services in mobile devices, traffic systems, aircraft, maritime, surveying, and rail). (Note that the additional downstream GNSS market—that is, the market for integration of and applications using GNSS devices and chipsets—is even larger, estimated to exceed$100 billion.14) These two large markets have many differences (especially: homogenous DTH versus diverse and distributed GNSS ecosystem, and corporate DTH satellites versus government-owned GNSS satellites). They share the attribute of space-based capability integrated with other value added elements: programming, in the case of DTH; and integration into devices that apply the capability to maps, tracking software, weather forecasts, traffic information, and so on, for GNSS.GNSS has lead the way in terms of growth, increasing by 60% over the five-year period ending in 2016, from $53 billion to $85 billion.15 The DTH market grew 11% over the same period, from $88 billion to $98 billion.Other satellite markets include satellite radio (digital audio radio service, or DARS), satellite broadband, transponder leasing, managed network services, and mobile satellite service (MSS), with total revenue of about $28 billion. The fastest growth rates come from the smaller, less mature subsectors like managed network services, which include in-flight internet connectivity (35% growth for the five years ending in 2016), broadband (33%), mobile communications (50%), and Earth observation (EO) (54%). These subsectors currently represent a small portion of the total services market. Broadband is 1.6% of the total, while mobile and EO are 3% and 1.6%, respectively.16

The enabling infrastructure functions of building and launching satellites constitute less than 10% of commercial revenue, with satellite manufacturing revenue of $13.9 billion and launch services revenue of $5.5 billion. (Launch vehicle manufacturing is not tracked separately, as launch providers generally manufacture their own vehicles).Additional revenue is generated by the wide range of applications and businesses that in some way use space capabilities or data. These diverse activities, ranging from advertising-supported weather forecasts, to precision timing for banking transactions, to location-based games and services, to sales of prints and artwork of space images, are difficult to

10

systematically and realistically quantify overall, in part because the varying degree to which their value propositions rely on space is not easily allocable.

InvestmentA number of growing, new commercial activities, which do not yet generate significant revenue, are attracting investment. These activities include satellite servicing, platforms, space mining/resource utilisation, situational awareness, in-space research and manufacturing, and others. Investors are also targeting new telecommunication and EO products and services. Investment in commercial space activities has increased in recent years, with a particular focus on the potential of lower-cost space infrastructure such as smaller, less expensive satellites, and reusable launch vehicles.Telecommunication ventures combining small satellites and large constellations have attracted some of the largest investments. OneWeb and SpaceX, among other firms, have declared plans to deploy so-called mega-constellations for ubiquitous internet

11

connectivity. OneWeb and SpaceX have both seen recent billion dollar investment mega-deals.Three types of investors, with different motivations, are shaping the new commercial space landscape, investing nearly $3 billion in 2016, and nearly $8 billion in the last five years.17

Billionaire advocacy investors, such as Elon Musk, Richard Branson, and Jeff Bezos, are using their brand power and capital to promote commercial space. These advocacy investors are motivated by a desire to generate a transformative human experience. They are largely focused on easing access to space and creating opportunities for human space travel. Their approaches have been different: SpaceX has entered into multiple different launch markets (including government markets), building on success and performance at each stage. Investors and future customers (through deposits) have funded Virgin Galactic’s long development timeframe. Blue Origin has relied almost entirely on the deep pockets of founder Jeff Bezos. This patient, advocacy-driven capital is creating an enhancement of launch capabilities beyond what we would expect to see from typical commercial dynamics and capital markets.Corporate strategic investors invest for a combination of financial returns and other benefits, including platform benefits (building a relationship with a customer, supplier, or partner), brand alignment, and control over disruptive market dynamics. For example, multiple companies invested a total of $500 million in OneWeb in 2015, from Coca-Cola to Qualcomm. Corporations also invest in their own new products and services; a recent example is Orbital ATK’s satellite servicing venture.Financially driven venture investors seek the best returns and are willing to accept a relatively high level of risk. Venture investors in space have been attracted by the potentially lucrative new markets (typically driven by data analytics), combined with improved cost structures, including lower cost satellites, launch vehicles, commercial- off-the-shelf components, robust architectures that allow for reduced cost by accepting higher per-satellite failure, and so on. Typical investments are in the millions or tens of millions of dollars, though some much larger investments have been made.The future performance of these new firms is uncertain. Many venture-funded companies (as many as 3 in 4) fail. Space firms face business case uncertainty arising from providing new products and services to new markets, technological hurdles, and the domino effect of ecosystem interdependence (that is, one space company, like a small launch provider, relies on the

12

success of another space company, like a smallsat operator). In planning, it is important to recognise that the increasingly dynamic space ecosystem will see both successes and failures.

ProfitabilitySpace-enabled services, primarily telecommunications, tend to be more lucrative than the satellite manufacturing and launch services businesses, where profitability is often marginal. Exceptions include large government satellite development and launch vehicle programs, particularly under contracts where the customer assumes most of the programmatic risk (usually cost growth) and incentivises good contractor performance with award fees.Telecommunications satellite operators traditionally have been the most profitable space companies, often recording double-digit margins year after year, though recently

13

there has been price pressure in some markets. Another strong performer has been GNSS equipment, such as devices used in cars, where companies like Garmin have enjoyed double-digit margins. Standalone equipment is seeing a demand slowdown, as integrated chipsets in mobile phones and other devices pick up in that market.The commercial launch services business is particularly challenging from a profitability standpoint. All launch vehicles currently in operation rely on some form of government support.Venture-funded space firms targeting data analytics markets with software products anticipate high margins, dramatic growth, and dropping costs. Large constellations of small telecommunications satellites anticipate the ability to compete effectively with terrestrial alternatives and to gain access to massive, underserved global markets, with resulting strong returns. At this still early stage, it is not clear what the outcomes will be.

Geography of the Space EcosystemAs noted, nearly 50 countries have government space budgets. Organisations in nearly 60 countries have built and/or operated satellites launched into space. Only 12 countries feature launch sites from which orbital launches take place, though many more feature launch sites hosting sounding rockets.18

Considering government budgets by global region, North America has the largest combined government space budget, nearly $50 billion, dominated by a single actor, the United States, with Canada playing a niche role, largely in partnership with the US. Asia Pacific broadly (including China, Japan, India) consists of three large, independent space actors that do not act in concert, as well as a robust community of active space nations with medium budgets (including Australia, Indonesia, Malaysia, Singapore, South Korea, and Taiwan), with total regional space approaching half the level of North America (about $20 billion). European government budgets taken together (including the European Space Agency, European Commission, Eumetsat, and individual national space programs), plus Russia, constitute the third largest regional grouping with combined budgets of about $15 billion. The Middle East, South America, and Africa are not anchored by any particular space power, and combined the budgets total about $1 billion.Considering commercial space activity, global leadership is distributed. While there are over 50 commercial satellite

14

operators in the world, most satellites are operated by a handful of large operators of geosynchronous orbit (GEO) satellites, including SES, Intelsat, Eutelsat, Telesat, and Inmarsat. These companies provide communications services to television/cable operators, businesses, and governments primarily through the leasing of satellite capacity (traditional fixed satellite service, or FSS) business. The world’s top three FSS operators by revenue are all headquartered in Europe, with two in Luxembourg and one in France. Though Luxembourg has a negligible space budget, it is home to the world’s two biggest GEO satellite operators, SES and Intelsat. These two companies operate some 100 satellites combined, more than all but the top-tier national space powers.Satellite DTH is usually provided by regional companies such as DirecTV and DISH Network in the United States and SkyPerfect JSAT in Japan. US companies are the largest regional group, reflecting the size of US markets, accounting for about 40% of

15

global DTH revenues. Note that compared to FSS operators, DTH providers generate more revenue with far fewer satellites.For other satellite services, including mobile services, broadband, and EO, US companies had the largest national market share in 2016, also about 40% of the market.19

Satellite manufacturing is dominated by a few large companies in the US, Europe, and Japan. While there are more than 20 satellite manufacturers worldwide, and even more boutique manufacturers for very small satellites, the major players are: Airbus Defense & Space (headquartered in France), Boeing (US), MELCO (Japan), SSL (US), and Thales Alenia Space (France). Other companies such as Ball Aerospace (US), Orbital ATK (US), and Surrey Satellite Technology (UK, owned by Airbus) have strong markets and focus on smaller satellites and more narrow components of the market. The United States has long been the world leader in satellite manufacturing, followed by Europe. US market share exceeds 60% and is largely the result of high-cost government satellites built for the US government.Launch was for a time dominated by Europe and Russia, after US providers lost market position more than a decade ago. Recently, SpaceX in the United States has gained market share and Russian providers have lost it. Europe’s Arianespace continues to dominate as a commercial launch service provider, with 42% of the commercial launch market from 2012 to 2016. US share (mainly SpaceX) is growing, hitting 26% in 2016, compared to 56% for Arianespace. International Launch Services (ILS), which markets the Russian Proton rocket, has seen a significant drop in launch activity in recent years; its 2016 market share was 11%.Considering ground equipment, GNSS devices and chipsets and television dishes account for most of the revenues. Ground equipment manufacturers for GNSS include Garmin, Trimble (both US), Leica Geosystems (Switzerland), and TomTom (The Netherlands); for telecommunications (enterprise and consumer): Harris, Hughes Network Systems, and ViaSat (all US), Cobham Satcom (UK), Gilat (Israel), Intellian (South Korea), and Huawei (China).New smallsat remote sensing and satellite telecommunications ventures largely target global markets.20 Most funded new ventures are based in the US, including Planet, Spire Global, and BlackSky Global (remote sensing) and OneWeb and the SpaceX system (telecommunications). Non- US funded smallsat ventures include remote sensing systems Axelspace (Japan), ICEYE

16

(Finland), and UrtheCast (Canada). More new satellite telecommunications ventures plan to launch larger, more conventional satellites.Investors in these new space companies are based primarily in the United States, which is home to about two-thirds of the 400+ investors identified around the world. Of the non-US investors, 15% are in the UK, followed by Japan (11%), Israel and Canada (9% each), Spain (7%), and India and China (about 6% each).21

Australian investors have recently made multi-million dollar commitments to Fleet and Gilmour Space Technologies, as well as funding early stage space activities.

Regulatory and Legal RegimesRegulatory and legal regimes governing space activity largely begin with the 1967 Outer Space Treaty, considered the foundation of international space law. Among its main provisions are a ban on weapons of mass destruction in space and national territorial

17

claims to celestial bodies. The treaty also includes the assignment of basic liability for damages that result from space activity.UN-affiliated international bodies for space also exist. The International Telecommunication Union (ITU) coordinates radiofrequency use and orbital locations for communications satellites. The Inter-Agency Space Debris Coordination Committee (IADC) develops guidelines for minimising orbital debris in the course of space activity. Neither organisation has binding legal authority, though the ITU plays a critical role in the satellite industry.At the national level, regulatory and legal regimes for space address functions including R&D/technology, space operations (including communication services, imagery, and navigation-related capabilities for various purposes), economic development, military and intelligence activities, and space exploration. National constructs vary widely.

18

Trends and Industry DynamicsFive trends stand out in today’s space economy: 1) technological advances creating expectations of more cost-effective (and therefore lucrative) space activities, 2) increased private investment by investors who are new to space, 3) a global economy that is increasingly data dependent with diverse effects on space capabilities and markets, 4) an increasingly widely shared vision of space as transformative for humanity, and 5) military/strategic developments around space as a crowded and valuable high ground.Technological advances, particularly from non-space industries, have been incorporated into systems that promise more capability in space at a lower cost. Examples of these technological advances include improved electronics, advanced materials, batteries, and computational and design tools. Companies reduce cost by buying these components, such as battery cells, as commercial, off-the-shelf products. Recently established space companies are also streamlining the manufacturing process through vertical integration, allowing systems and components to be built in-house, often using advanced techniques like additive manufacturing.Innovative small satellite constellation architectures, reusable launch vehicles, and other approaches have attracted new investors into space, from Silicon Valley venture capital firms to national governments seeking to target space industries as a path to economic growth.The data dependent global economy has created massively growing demand for two space products: communications and data. New satellite systems such as Planet, Spire Global, OneWeb, and Australian start-up Fleet have attracted venture capital targeting 10x or 100x returns with plans to provide unique global data sets, tracking capabilities, and integrated global communications. The data economy has also disrupted existing telecommunication markets, including satellite telecommunications, as consumers change their use patterns for television and telephone. This disruption has resulted in price pressure and contraction in some existing markets, in addition to growth in new ones.The vision of space as transformative for humanity is becoming increasingly shared, through the narrative, investment, and activity of high visibility space billionaires and others. Today’s transformative vision of space often encompasses human spaceflight on a large scale, including ambitious destinations

19

such as Mars and the emergence of a diverse, on-orbit economy.Space is increasingly recognised for its strategic and defence value, leading many nations to more actively consider the importance of protecting access to space and space assets for military as well as economic purposes. According to NASA, the number of space objects catalogued by the US Air Force, operator of the world’s most sophisticated space surveillance network, grew from 8,840 as of September 200022 to 18,640 as of April 2017.23 Only a small portion—10% or less—are active satellites; the rest are spent satellites, rocket bodies, and other debris from space activity. The increased congestion, coupled with US concerns about Chinese and Russian threats, have placed a premium on better space surveillance and mechanisms for managing debris, as well as protection of space assets. The US Air Force is investing in a more capable space tracking radar called the Space Fence; Canada has launched its own space surveillance satellite; and a number of private companies are offering space surveillance services and even debris mitigation on a commercial basis.

20

Opportunities for AustraliaAustralia’s competitive attributes include high levels of education; proximity to other nations with space budgets and business-friendly policies; an advantageous geographic location in the Southern Hemisphere for satellite ground stations; world-class capabilities in ground systems, software, and applications; and close strategic alliances with space powers, prominently including the United States. Australia is a key partner in several US- led military space activities, including satellite programs and SSA. In communications, for example, Australia hosts ground facilities for the US Wideband Global Satcom (WGS) and Mobile User Objective System (MUOS) programs. Australia’s SSA role has expanded recently with the relocation of US radar (completed) and optical (underway) space surveillance systems to its territory. This infrastructure not only provides high- tech jobs but also will help nurture domestic capabilities that can be brought to bear in the commercial sector. Australia’s plans to increase defence spending to 2% of gross domestic product by 2020/2021 represent a growth opportunity for its space sector. One Defence Ministry initiative would see billions invested over 10 years in a next- generation satellite and terrestrial communications capability and hundreds of millions to improve the military’s access to high-resolution commercial satellite imagery. Several global space companies, including US aerospace and defence giants Boeing, Lockheed Martin, and Northrop Grumman, maintain a significant presence in Australia.Based on Australia’s current space capabilities and other attributes, the analysis below provides a top-level look at opportunities for Australia to participate significantly in sizable, growing segments of the global space economy, and perhaps even capture a disproportionate share of that growth. This analysis is not meant to be limiting. There are many viable space investment decisions for Australia; niche opportunities will arise across the space economy. Within that range of options, these high-growth or potentially high-growth sectors that can leverage significant existing domestic space capabilities or have low barriers to entry represent particularly good opportunities for Australia to expand its footprint in the global space economy.

Mature Space SectorsTable 1 highlights the commercial industry’s most mature sectors, established markets with relatively well understood growth potential, beginning with satellite manufacturing and launch. Both segments have growth potential, but profit margins

21

typically are thin, entry barriers are high, and Australia possesses no significant capability. Although Australia has the basic tools to enter these markets, the required investment is high relative to the potential payoff.As home to Singtel Optus, Australia already has a significant presence in the satellite DTH and FSS businesses. Satellite DTH is by far the largest sector in the global space economy but is approaching market saturation and experiencing flat growth.One of the fastest growing consumer markets is satellite radio, which in the United States, the only established market, grew at an average annual rate of 10% from 2012 to 2016. Australia, with its vast territory and common language, could be a candidate market for satellite radio, although its relatively low population could challenge the business case, despite dropping costs for launch and satellite manufacturing.

22

Market ExamplesExisting Market

($B)Growth Trend Margins Barrier

to Entry

Significant Current

Activity in Australia?

Prime Australia Growth

Opportunity?Satellite Manufacturing

Boeing, TAS, MELCO, MDA/SSL $14B + $ High N

Launch Services ULA, SpaceX, Ariane Group, MHI $6B + $ High N

Satellite DTH TVDirecTV, Foxtel, Sky, Singtel Optus, SkyPerfect JSAT

$98B = $$$ (declining) Medium Y

Satellite Radio Sirius XM $5B ++ $$$ Medium N Yes

Satellite Broadband

ViaSat, Hughes, Inmarsat,NBN $2B ++ $$ Medium Y Yes

FSS Transponder Leasing

Intelsat, SES, Eutelsat, Singtel Optus, Telesat

$11B – $$$ (declining) Medium Y

FSS Managed Services

Intelsat, SES, ViaSat, Hughes, Inmarsat, NBN, Singtel Optus, Global Eagle

$6B+ ++ $$$ Medium Y Yes

Mobile Communications

Inmarsat, Iridium, Orbcomm, Thuraya $4B + $? High N

Earth ObservationDigitalGlobe, Airbus, Imagesat Intl .

$2B ++ $$ High N

Consumer Ground Equipment

Cisco, Echostar, Huawei, Foxtel $19B = $$ Medium Y

GNSS Devices, Chipsets, and Applications

Garmin, Trimble, Fugro $31B ++ $$$ Medium Y Yes

Network Ground Equipment

Hughes, Gilat, Clearbox Systems $10B + $$ Medium Y Yes

Table 1. Mature space markets.

The global market for consumer broadband services via satellite is far smaller but nonetheless grew at almost 7% annually from 2012 to 2016 and is expected to see continued solid growth. In Australia, this service is provided by NBN Communications, which was created by the government and currently has two satellites in orbit. This market could also be an opportunity for Australian industry to insert itself into the global supply chain.The transponder-leasing portion of the FSS sector is shrinking as terrestrial fibre makes further inroads into its traditional market, and currently high margins are in decline.The other FSS subsector, managed services, which refers to internal networks for businesses and government agencies as well as mobility applications such as Internet service to aircraft passenger cabins, represents a growth opportunity. This market grew at an annual rate of nearly 8% from 2012 to 2016 and will

23

likely continue to grow. This growth could be a boon to Australian suppliers and integrators of the associated ground equipment. Australia has a substantial domestic market for managed services and as a result has significant industrial capability for associated hardware and software.24

Mobile communications (MSS) are currently primarily provided by several existing fleets of low Earth orbiting (LEO) satellites. There is little growth, high barriers

24

to entry, and relatively low margins in this business. EO systems are experiencing relatively high growth in the sale of imagery for an expanding list of applications. Consequently, developing state of the art sensors and deploying them and building the sales organisation required to generate revenues all represent a high barrier to entry that is unlikely to benefit Australia.As previously noted, Australia has significant strengths in ground systems, software, and related applications. One of the more promising areas is GNSS and GNSS- based positioning, navigation, and timing services, where a number of Australian companies are active, developing high-end products and software geared toward specific industries such as mining.25

GNSS, including equipment and applications, is a growing sector of the global space industry. In 2014, there were nearly 4 billion GNSS devices deployed globally, mostly in the form of chipsets embedded in smart phones. By 2023, that number is expected to rise to more than 9 billion, with most of that growth, 11% per year—from 1.7 billion to 4.2 billion devices—coming in the Asia Pacific region, according to a 2015 report by the European Global Navigation Satellite Systems Agency. Related revenues, for component manufacturing, equipment integration, and value- added services, constitute an additional, hundred billion dollar plus growth market.26 Note that international competition, particularly in manufacturing at scale, may be a challenge; software applications and integration services may be better niches.Tightly intertwined with various space services but still noteworthy as a separate category are ground systems, a market where Australia possesses world-class capabilities. In addition to its own systems, Australia hosts ground systems for numerous foreign commercial and government operators—systems used not only to downlink data but to uplink satellite commands.In communications, ground system growth trends track roughly with the managed services side of the business addressed above. Australia also is a magnet for EO satellite ground stations, and the proliferation of these satellites, both government and commercially owned, represents a significant growth opportunity. Numerous countries lacking mature satellite manufacturing industries—Peru, Spain, Turkey the United Arab Emirates, Saudi Arabia, Chile and Kazakhstan, to name a few—have procured their own EO satellites in recent years.

Emerging MarketsEmerging space markets, those in which the companies involved

25

are attracting significant investment but have yet to demonstrate long-term growth and profitability, and in which there is significant uncertainty about business models and markets, are profiled in Table2. Since these markets are new, future growth in these segments is unknown. Table 2 reflects the expected growth potential for these segments considering the underlying market drivers and announced plans. The table captures estimates of the investment required for the different types of systems and characterisation of the barriers to entry. As with the table above, we profile Australia’s current activity and identify prime targets for expanding Australia’s space footprint.Satellite servicing has long attracted government and commercial interest and investment, and now appears to be maturing. The costs to develop and advance the technology are high, even for organisations drawing on a long history of investment, the market is as yet unproven, and concerns over on-orbit security create potential international relations and regulatory complexities.

26

Markets Examples Growth Trend

Required Per Venture Investment

Barrier to Entry

Significant Current Activity

in Australia?

Prime Australia Growth

Opportunity?

Satellite Servicing MDA/SSL, Orbital ATK + ~$500M+ High N

Suborbital Human Spaceflight

Virgin Galactic, Blue Origin + ~$1B+ High N

EO Smallsat Constellations Planet, Spire Global ++ ~$100M+ Low N

EO-Driven Data Analytics

Orbital Insights, HexiGeo, GeoImage

++ ~$10M+ Low Y Yes

Ubiquitous Global Broadband OneWeb, SpaceX, ++ ~$3B+ High N

Commercial SSAAGI, Schafer, EOS, US military infrastructure in Australia

+ ~$10M+ Medium Y Yes

Dedicated Smallsat Launch

Vector, Virgin Orbit, Rocket Lab + ~$100M+ Medium N

Smallsat Manufacturing

Clyde, Pumpkin, Spaceflight Services

+ ~$1M+ Low N Yes

Table 2. Emerging space markets.

Likewise, suborbital human spaceflight is being developed by several dedicated companies who have been working for more than a decade to get a product to market, and is not an attractive entry market for Australia.Multiple companies developing EO smallsat and global broadband constellations have already received significant investments and are in varying stages of development. Given the number of constellations, and their current maturity, and the cost for developing these systems, global broadband constellations are not a likely market target for Australia. The market for data analytics driven by the proliferation of this timely and affordable EO imagery is an emerging market where Australian companies could play a broader role. Data analytics companies already analyse imagery to create actionable information products serving industries including mining, forestry, urban planning and defence. While there are no Australian companies operating their own EO satellites today, this could change in the future as the costs of these systems continues to come down.One of the more intriguing opportunities for Australia is space situational awareness (SSA), which refers to the tracking of space objects as they circle the Earth. SSA is one of the latest space activities moving into the commercial sector after decades of being an exclusively government function. One company in particular, Electro Optics Systems Pty Ltd (EOS), manufactures space surveillance systems and is collaborating with US

27

aerospace giant Lockheed Martin on an Australia-based commercial SSA network called Optical Space Services.27 The growth potential for commercial SSA stems from the orbital congestion issue, and the related desire of commercial satellite operators for better access to this information. In addition, there are growing calls in the United States for transferring part of the US Air Force’s SSA role—providing warnings to civilian and commercial satellite operators of potential on-orbit collisions—to a civilian agency.There are many ventures worldwide seeking to provide dedicated smallsat launchers

28

for the many constellations that are planned for deployment in the next decade. Challenges include the need for significant advancements in process and technology in order to achieve performance at the target prices that will make these vehicles competitive for this market. These barriers are high and are unlikely to provide a good payoff for Australian industry. Developing a launch site to exploit Australia’s geographic advantages would be less costly; however, the success of a launch site depends on the success of the launch providers it is affiliated with. Strong relationships with one or more launch providers predictably conducting launches are necessary to achieve commercial viability.Although space hardware manufacturing represents a tiny segment of Australia’s space economy, the growing popularity of CubeSats could present an opportunity for industry to expand its reach in that sector. Australia’s industrial and university/research sectors provide some capability to build small satellites and instruments. CubeSats are a low cost pathway to conducting space research and are increasingly able to perform operational missions. The opportunity to gain hands-on experience building flight hardware also has significant potential in drawing and retaining students in the science, technology, engineering and math (STEM) disciplines, and provides insight and expertise to aid in development of downstream data applications. For these reasons, combined with the relatively low barriers to entry, a modest increase in investment in space hardware manufacturing capabilities has the potential to pay off.As discussed above, start-ups in less mature/more speculative markets such as orbital human spaceflight, platforms, in-space manufacturing, mining and resource utilisation are attracting investment. The business potential of these markets in the next decade is highly uncertain and the capital expenditure required is high; generally, these markets are likely to be too early stage to attract major commitment as a core part of an economic growth policy aimed at reasonably near-term results. However, the brand value of affiliation with ambitious in-space markets, combined with long- term potential, may warrant some consideration. For example, limited participation in a space mining activity, given Australia’s global leadership in mining, could both aid Australia’s terrestrial industry by providing visibility into its technology capabilities and position Australia as a participant in the longer-term evolution of the LEO economy.

29

Appendix: Core TechnologiesLaunch VehiclesA typical launch vehicle system consists of several basic subsystems, including propulsion; power; guidance, navigation, and control; and payload adapters. Launch vehicles use the same technologies as in the early days of space launch: engines with hydrocarbon and cryogenic propellants or solid fuel boosters for propulsion.Efforts are underway to reduce launch costs via refurbishment/reusability. A typical launch vehicle propulsion system will account for about 70% of the manufacturing cost. If its engines can be recovered and reused, the cost of launch could be dramatically reduced.28 SpaceX and Blue Origin are launching vehicle systems that feature refurbishable elements with the long-term goal of producing and launching entirely reusable systems.In addition, new launch vehicle designs seek to improve manufacturing and operating costs. Several new intermediate- and heavy-class launch vehicles are expected to become available during the next decade. These vehicles include the Ariane 6 being developed by ArianeGroup to replace the Ariane 5 by 2020, the Vulcan being developed by United Launch Alliance (ULA) to replace the Atlas V and Delta IV, and the H3 being developed by Mitsubishi Heavy Industries to replace the H-IIA/B. SpaceX continues to develop its Falcon Heavy vehicle, which is expected to launch for the first time in 2017 or 2018. Blue Origin is pursuing development of the New Glenn family of vehicles, with an anticipated debut of 2020.

SatellitesCore satellite technologies include attitude determination and control; command and data handling; power; propulsion; structures; thermal; telemetry, tracking, and command; and guidance and navigation. The payload subsystem configuration varies depending on the mission, which can be communication, EO, science, technology demonstration, or a combination of these.Communications. The next generation of large, advanced communications satellites, high throughput satellites (HTSs) feature frequency reuse, spot beams, and/or on-board signal processing to maximise efficiency. HTS platforms seek to enable more bandwidth intensive applications including ultra-high-definition television, broadband connectivity for households,

30

businesses, or commercial airline passengers, and connected cars. HTS technology does have the risk of exacerbating the existing bandwidth excess in several markets, leading to a drop in demand for certain types of satellites. HTSs provide at least double the throughput (usually significantly more) compared with traditional FSS satellites, while using the same radio frequency spectrum allocations (C, Ku, and Ka-bands).The ability to reprogram communications satellites on orbit would enable manufacturers to mass-produce homogenous satellites that the operators could then tailor to their specific, changing needs via software uploads. Currently, most GEO communications satellites must be custom built, a feature that adds to their cost. Examples include Anik 2E and 2F, BADR 7, EchoStar XVII, Eutelsat 172B, GSAT 19, HYLAS 2, Inmarsat Global Xpress series, Intelsat Epic series, KA-SAT, NBN Co. 1A, O3b constellation, SES 12 and 14, Spaceway 3, Thaicom 4 (IPSTAR), ViaSat 1 and 2, WINDS, Yahsat 1A and 1B.

31

Increasingly, electric propulsion (EP) systems are being used to deliver communications satellites from geostationary transfer orbit (GTO), where most satellites are dropped off by their launch vehicles, to their final GEO slot. These satellites can save up to 50% of the overall satellite mass by reducing propellant needed for the orbital transition. The use of EP for orbital insertion is an attractive technology for satellite operators aiming to trade propulsion mass for revenue-generating payload mass. The number of EP satellites being built and launched has steadily increased since 2010, with a low of two in 2011 and a high of 10 in 2017, some of them employing EP for both orbit raising and station keeping. Examples include ABS 2A and 3A, Eutelsat 115 West B, Eutelsat 117 West B, Eutelsat 172B, GSAT 9, Hispasat 36W-1, Lisa Pathfinder, and SES 15.Capable constellations of very small satellites (those with masses of 600 kilograms or less), or smallsats, are enabled through advances including improved electronics, advanced materials, batteries, and computational and design tools. Smallsats represent a confluence of proven space capabilities, highly capable microelectronics, miniaturisation, and new precision manufacturing techniques. The disruptive potential of smallsats hangs on lower costs and faster development times, which foster rapid innovation. Smallsat telecommunications constellations, such as OneWeb, tout advantages over GEO systems, including global coverage and low latency, which refers to the lag time between signal transmission and reception via satellite. GEO satellites lose signal effectiveness at extreme latitudes because of their position above the equator, and their high altitude results in signal latency that can disrupt certain types of connectivity applications.Earth Observation. Large EO satellites include platforms used by government agencies to conduct IMINT, meteorology, Earth science, and climate monitoring. Since the launch of SPOT 1 in 1986, companies have also operated large EO satellites to generate revenue. Typically, these satellites feature high-resolution panchromatic optical sensors (0.3-1 metre resolution in black and white) with multispectral (multiple bands within the visible to infrared spectrum) sensors offering about 1 metre resolution. These satellites usually follow a sun-synchronous orbit (SSO) enabling them to pass over any given point of the planet’s surface at the same local solar time—that is, always in sunlight. The satellites typically cover at least 1 million square kilometres per day with revisit times of about 24 to 72 hours. Examples of SSO EO satellites include EROS, Pleiades, Pleaides NG (2020), SPOT, WorldView, and WorldView Legion (2020).Start-up companies like Planet, Spire Global, and many others are building systems with lower resolution, consisting of small

32

satellites in large constellations. These companies see themselves mainly as data analytic service providers that use satellite-based sensors to frequently capture global data. Examples: Astro Digital, AxelSpace, BlackSky Global, HawkEye360, Hera, ICEYE, Planet, Satellogic, Spire Global, UrtheCastSome operators, like GeoOptics and PlanetiQ, are developing satellite constellations designed to detect and characterise the nature of signals transmitted by GNSS satellites as the signals travel through the atmosphere. This capability, called radio occultation, is particularly useful for precision weather forecasting.The data collected by these satellites are being fused with other data—such as PNT information—and analysed using the latest computing technologies, including artificial intelligence. This analysis produces actionable information for corporate and government decision makers. The proliferation of satellite-based EO data has fuelled the growth of data analytics companies specialising in geospatial information.

33

Exploration/Government ProgramsIncreasingly, government space programs rely on technologies from outside industries, not developed for specifically for space. Key areas of global technology (that is, technology not specifically developed for space applications) for use in space exploration and other government space programs are artificial intelligence/machine learning and intelligent systems, autonomy, 3D printing, nanodevices and nanosensors, data analytics, augmented virtual reality, high performance space computing, advanced computing, cyber physical systems (digital twins), batteries, robotics, and IOT. In addition, space-unique technology advances are required in disciplines including nanotechnology, human factors, radiation protection, propulsion, ECLSS, food production, water reclamation, planetary destination systems, and microgravity-unique applications of robotics and related disciplines.

34

Appendix: Selected Space Terms and Acronyms

TermsGeosynchronous orbit (GEO): a circular orbit at an altitude of 35,852 km (22,277 mi) with a low inclination (i.e., near or on the equator). Geostationary orbit (GSO) is a subset of GEO in which a satellite has an orbital period equal to the Earth’s rotational period and thus appears motionless from the groundGeostationary transfer orbit (GTO): an intermediate orbit where a satellite is launched to be further transferred to GEO using its own propulsion or a dedicated booster

Launch vehicle: a rocket used to carry a payload from Earth’s surface into spaceStage (of a launch vehicle or a rocket): in order to lighten the weight of the launch vehicle to achieve orbital velocity, most launchers discard a portion of the vehicle (a stage). Each stage contains its own engines and propellant (fuel)Payload: for orbital launch purposes, a payload can be a satellite, a space probe, an on-orbit vehicle, or a platform that carries humans, animals, or cargo

Orbit: a trajectory of an object, such as the trajectory of a planet about a star or a moon or a satellite around a planet

Space situational awareness (SSA): tracking of space objects as they circle the EarthSpace (or orbital) debris: collection of defunct human-made objects in Earth orbit, such as old satellites, spent rocket stages, and fragments from disintegration, erosion, and collisionsCryogenic propellant (fuel): propellant that requires storage at extremely low temperatures in order to maintain it in a liquid stateSatellite constellation: a number of satellites with coordinated ground coverage, operating together under shared controlRemote sensing: acquisition of information about an object (such as a planet) or phenomenon without making physical contact

35

AcronymsUSD: United States DollarCASC: China Aerospace Science and Technology CorporationESA: European Space AgencyGDP: gross domestic productGNSS: global navigation satellite servicesNASA: National Aeronautics and Space Administration

36

IMINT: imagery intelligenceUK: United KingdomUAE: United Arab Emirates SSA: space situational awareness DTH: direct to home televisionDARS: satellite radio (direct audio radio service)MSS: mobile satellite serviceSpaceX: Space Exploration Technologies SES: Societe Europeenne de Satellite FSS: fixed satellite serviceMELCO: Mitsubishi Electric Corp.UN: United NationsITU: International Telecommunication UnionR&D: research and development WGS: Wideband Global Satcom MUOS: Mobile User Objective SystemMDA: MacDonald, Dettwiler and AssociatesSSL: Space Systems LoralEO: Earth observationAGI: Analytical Graphics Inc.EOS: Electro Optics Systems Pty Ltd.STEM: science, technology, engineering and mathLEO: low Earth orbitGEO: geostationary orbitGTO: geostationary transfer orbit SSO: Sun-synchronous orbit MEO: medium Earth orbit ULA: United Launch Alliance HTS: high

37

throughput satellites EP: electric propulsionIOT: Internet of thingsECLSS: Environmental Control and Life Support System

38

This page intentionally left blank

39

About Bryce Space and Technology

Bryce Space and Technology is an analytic consulting firm serving government and commercial clients. Bryce provides unique, integrated expertise on the space economy.Bryce’s expertise includes market analytics, technology readiness, cyber security, policy and economics, and strategy. Many authoritative data sets characterizing the space industry and sub-segments were originated by our analysts. We understand the interplay of national security, civil, and commercial space programs, capabilities, and markets.Bryce helps clients turn technology into mission and business success. brycetech.com

@brycespacetech

40

This page intentionally left blank

41

Endnotes1 Monetary values are in USD throughout this document unless otherwise noted.2 Bryce Space and Technology, “2017 State of the Satellite Industry Report,” Satellite Industry Association, 2017, https://brycetech.com/reports.html. A note on the term “commercial”: In the U.S., space contractors—firms that execute space activities at the direction of and under thesupervision of the government, for government purposes—are distinct from commercial providers, though in practice this distinction is often blurred. This distinction is important for policy decisions relating to contract terms and conditions. As an obvious example, NASA procured, owned, and operated both the Saturn V and the Space Shuttle, even though for-profit companies built these vehicles under contract. SpaceX and Orbital ATK designed, built, own, and operate assets used to support cargo services to the International Space Station (ISS) under a contract with NASA. This model is similar in Europe and Japan. In China, India, and Russia, the distinction is even more obscure, as in these cases the government is the substantial funder of all space activity, even when it comes to the operation of satellites providing television and data services.3 Some government funds are spent on commercial products and services, notably satellite manufacturing, launch, and a small proportion of the total services market.4 National Aeronautics and Space Administration. “NASA FY 2016 Budget Request [Fact Sheet,” 2016, https://www.nasa.gov/sites/default/files/files/Agency_Fact_Sheet_FY_2016.pdf. See also Pat Towell and Lynn M. Williams, “Defense: FY2017 Budget Request, Authorization, and Appropriations,” Congressional Research Service, June 28, 2017, https://fas.org/sgp/crs/natsec/ R44454.pdf; Mike Gruss, “Leaked Documents Offer Snapshot of NRO Activity,” SpaceNews, August 30, 2013, http://spacenews.com/37021leaked-documents-offer-snapshot-of-nro-activity/;Missile Defense Agency, “Historical Funding for MDA FY85-16,” 2016, https://www.mda.mil/ global/documents/pdf/FY16_histfunds.pdf; and National Aeronautics and Space Administration, “Aeronautics and Space Report of the President: Fiscal Year 2016 Activities,” 2016, https://history. nasa.gov/presrep2016.pdf

5Organisation of Economic Cooperation and Development, Space Economy at a Glance 2014, Paris: OECD Publishing, 2014.

6European Space Agency, “Funding,” http://www.esa.int/About_Us/Welcome_to_ESA/Funding; and Organisation of Economic Cooperation and Development, Space Economy at a Glance 2014, Paris: OECD Publishing, 2014. Excludes the additional budgets of individual space agencies of European countries beyond their contributions to ESA.

7The United Kingdom (UK) has recently voted to exit the European Union (EU), a process not expected to significantly impact its membership in ESA. There are some uncertainties regarding the UK’s

42

participation in the Galileo GNSS system, as this system is managed by the European Commission (EC), an institution within the EU.

8 Ibid.

9Organisation of Economic Cooperation and Development, Space Economy at a Glance 2014, Paris: OECD Publishing, 2014.

10 Ibid

11 Paul Kallender-Umezu, “What’s Behind Japan’s Sudden Thirst for More Spy Satellites,” SpaceNews, November 13, 2015, http://spacenews.com/whats-behind-japan-sudden-thirst-for-more-spy- satellites/.12 Organisation of Economic Cooperation and Development, Space

Economy at a Glance 2014, Paris:13 OECD Publishing, 2014.

43

1 Monetary values are in USD throughout this document unless otherwise noted.2 Bryce Space and Technology, “2017 State of the Satellite Industry Report,” Satellite Industry Association, 2017, https://brycetech.com/reports.html. A note on the term “commercial”: In the U.S., space contractors—firms that execute space activities at the direction of and under thesupervision of the government, for government purposes—are distinct from commercial providers, though in practice this distinction is often blurred. This distinction is important for policy decisions relating to contract terms and conditions. As an obvious example, NASA procured, owned, and operated both the Saturn V and the Space Shuttle, even though for-profit companies built these vehicles under contract. SpaceX and Orbital ATK designed, built, own, and operate assets used to support cargo services to the International Space Station (ISS) under a contract with NASA. This model is similar in Europe and Japan. In China, India, and Russia, the distinction is even more obscure, as in these cases the government is the substantial funder of all space activity, even when it comes to the operation of satellites providing television and data services.3 Some government funds are spent on commercial products and services, notably satellite manufacturing, launch, and a small proportion of the total services market.4 National Aeronautics and Space Administration. “NASA FY 2016 Budget Request [Fact Sheet,” 2016, https://www.nasa.gov/sites/default/files/files/Agency_Fact_Sheet_FY_2016.pdf. See also Pat Towell and Lynn M. Williams, “Defense: FY2017 Budget Request, Authorization, and Appropriations,” Congressional Research Service, June 28, 2017, https://fas.org/sgp/crs/natsec/ R44454.pdf; Mike Gruss, “Leaked Documents Offer Snapshot of NRO Activity,” SpaceNews, August 30, 2013, http://spacenews.com/37021leaked-documents-offer-snapshot-of-nro-activity/;Missile Defense Agency, “Historical Funding for MDA FY85-16,” 2016, https://www.mda.mil/ global/documents/pdf/FY16_histfunds.pdf; and National Aeronautics and Space Administration, “Aeronautics and Space Report of the President: Fiscal Year 2016 Activities,” 2016, https://history. nasa.gov/presrep2016.pdf

5Organisation of Economic Cooperation and Development, Space Economy at a Glance 2014, Paris: OECD Publishing, 2014.

6European Space Agency, “Funding,” http://www.esa.int/About_Us/Welcome_to_ESA/Funding; and Organisation of Economic Cooperation and Development, Space Economy at a Glance 2014, Paris: OECD Publishing, 2014. Excludes the additional budgets of individual space agencies of European countries beyond their contributions to ESA.

7The United Kingdom (UK) has recently voted to exit the European Union (EU), a process not expected to significantly impact its membership in ESA. There are some uncertainties regarding the UK’s participation in the Galileo GNSS system, as this system is managed by the European Commission (EC), an institution within the EU.

8 Ibid.

44

9Organisation of Economic Cooperation and Development, Space Economy at a Glance 2014, Paris: OECD Publishing, 2014.

10 Ibid

11 Paul Kallender-Umezu, “What’s Behind Japan’s Sudden Thirst for More Spy Satellites,” SpaceNews, November 13, 2015, http://spacenews.com/whats-behind-japan-sudden-thirst-for-more-spy- satellites/.

12 Organisation of Economic Cooperation and Development, Space Economy at a Glance 2014, Paris: OECD Publishing, 2014.13 Bryce Space and Technology, “2017 State of the Satellite Industry Report,” Satellite Industry Association, 2017, https://brycetech.com/reports.html.14 Directorate-General for Internal Policies, Space Market Uptake in Europe, 2016,

http://www.

45

europarl.europa.eu/RegData/etudes/STUD/2016/569984/IPOL_STU(2016)569984_EN.pdf15 Bryce Space and Technology, “2017 State of the Satellite Industry Report,” Satellite Industry Association, 2017, https://brycetech.com/reports.html.16 Ibid.17 Bryce Space and Technology, “Start-Up Space: Update on Investment in Commercial Space Ventures,” 2017. Start-up space ventures are defined as space companies that began as angel- and venture capital-backed start-ups.18 In historical order of launch attempt: Soviet Union (Russia), US, Europe (France), Japan, China, India, Israel, North Korea, Iran, South Korea (so far unsuccessfully), and New Zealand (so far unsuccessfully).19 Bryce Space and Technology, “2017 State of the Satellite Industry Report,” Satellite Industry Association, 2017, https://brycetech.com/reports.html.20 The satellite telecommunications ventures tend to use larger satellites than the remote sensing ventures.21 Bryce Space and Technology, “2017 State of the Satellite Industry Report,” Satellite Industry Association, 2017, https://brycetech.com/reports.html.22 “Orbital Box Score,” The Orbital Debris Quarterly News (Houston TX: NASA Johnson Space Center), October 2000, https://www.orbitaldebris.jsc.nasa.gov/quarterly-news/pdfs/odqnv5i4.pdf23 “Satellite Box Score,” The Orbital Debris Quarterly News (Houston TX: NASA Johnson Space Center), August 2017, https://www.orbitaldebris.jsc.nasa.gov/quarterly-news/pdfs/odqnv21i3.pdf24 From data compiled by Bryce from various sources including published reports, government budget tables and industry surveys.25 Asia Pacific Aerospace Consultants Pty Ltd, “A Selective Review of Australian Space Capabilities: Growth Opportunities in Global Supply Chains and Space Enabled Services,” 2015, https://industry. gov.au/industry/IndustrySectors/space/Documents/APAC%20Report%20on%20Australian%20 Space%20Capabilities%20Revised.pdf26 European Global Navigation Satellite System (GNSS) Agency, “GNSS Market Report: Issue 4,” March 2015, https://www.gsa.europa.eu/system/files/reports/GNSS-Market-Report-2015-issue4_0.pdf27 Lockheed Martin, “A Closer Look at Space Debris: Lockheed Martin and Electro Optic Systems Break Ground on Australian Space Tracking Site [Press Release],” December 1, 2015, http://www. lockheedmartin.com/us/news/press-releases/2015/december/121201-ssc-EOS-announcement.html28 E. Clayton Mowry, Carissa Bryce Christensen, and Phil Smith, “The Global Launch Industry: Progress and Evolution,” in Recent Successful Satellite Systems: Visions of the Future, ed. D. K. Sachdev and Ned Allen

46

(Reston, VA: American Institute of Aeronautics and Astronautics, 2017).

47