global trends in energy storage - energy transition...

TRANSCRIPT

Global Trends in Energy StorageLon Huber

September 23, 2016

What is energy storage?

Current state of energy storage (U.S. and globally)

Key trends and drivers

The rise of batteries

“Behind the meter” energy storage

Topics

2

Energy storage is a very broad asset class

3

Electro-Chemical

(Flow battery / Lithium Ion )

Mechanical

(Flywheel)

Bulk Mechanical

Thermal

(Ice / Molten Salt)

Bulk Gravitational

(Pumped Hydro)

Transportation

(Electric Vehicles)

(CAES)

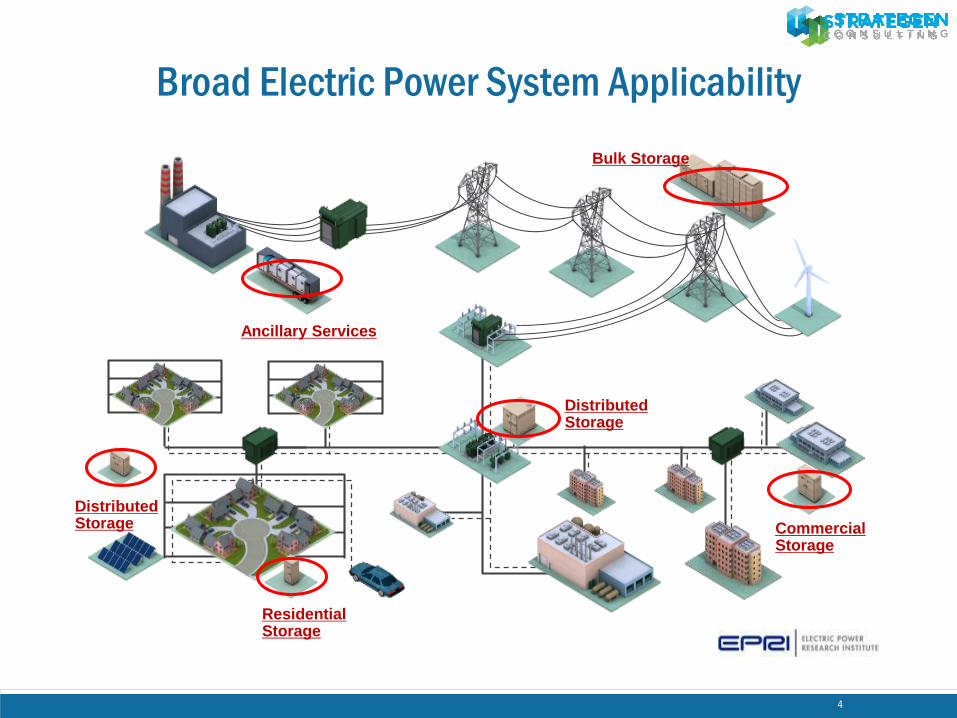

Broad Electric Power System Applicability

4

Bulk Storage

Ancillary Services

DistributedStorage

DistributedStorage Commercial

Storage

ResidentialStorage

SOURCE: HTTP://WWW.RMI.ORG/CONTENT/FILES/RMI-THEECONOMICSOFBATTERYENERGYSTORAGE-FULLREPORT-FINAL.PDF

Storage can provide a range of services

5

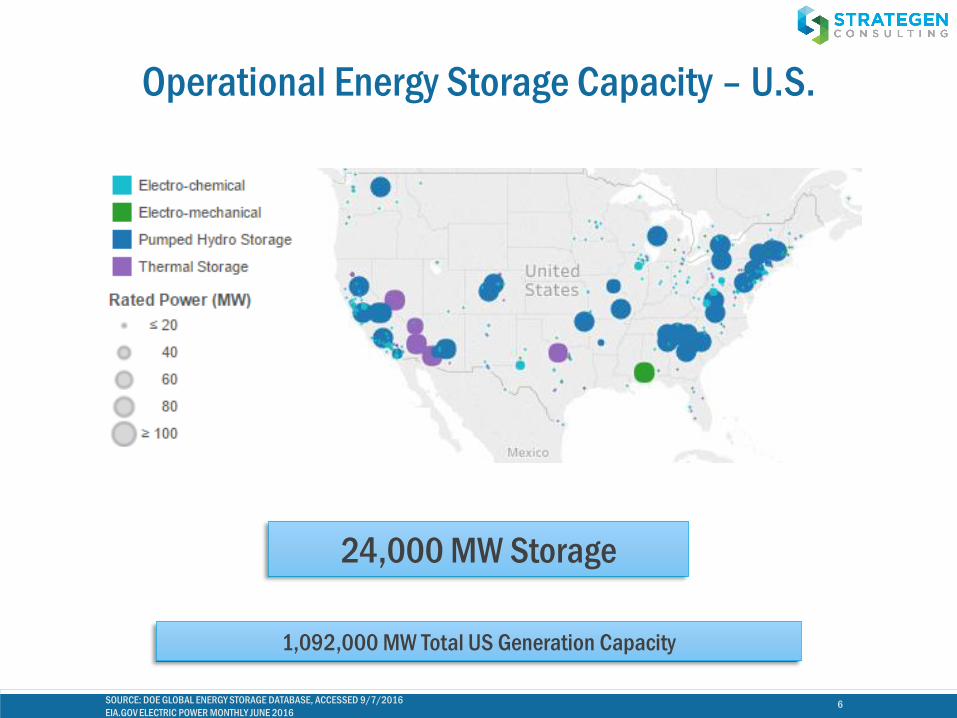

Operational Energy Storage Capacity – U.S.

SOURCE: DOE GLOBAL ENERGY STORAGE DATABASE, ACCESSED 9/7/2016

EIA.GOV ELECTRIC POWER MONTHLY JUNE 20166

24,000 MW Storage

1,092,000 MW Total US Generation Capacity

Chapter 1: Demonstrations

& Pilots(most states are still

here)

Chapter 2:

Niche use case deployment

(some states are here now)

Chapter 3:

Full deployment + Wholesale Market

Opportunities

Widespread adoption and opportunities for wholesale market participation

Special T&D deferral cases, high renewable penetration, load pocket constraints

Many utilities are gaining “real-world” experience with storage deployment

Where are we headed?

7

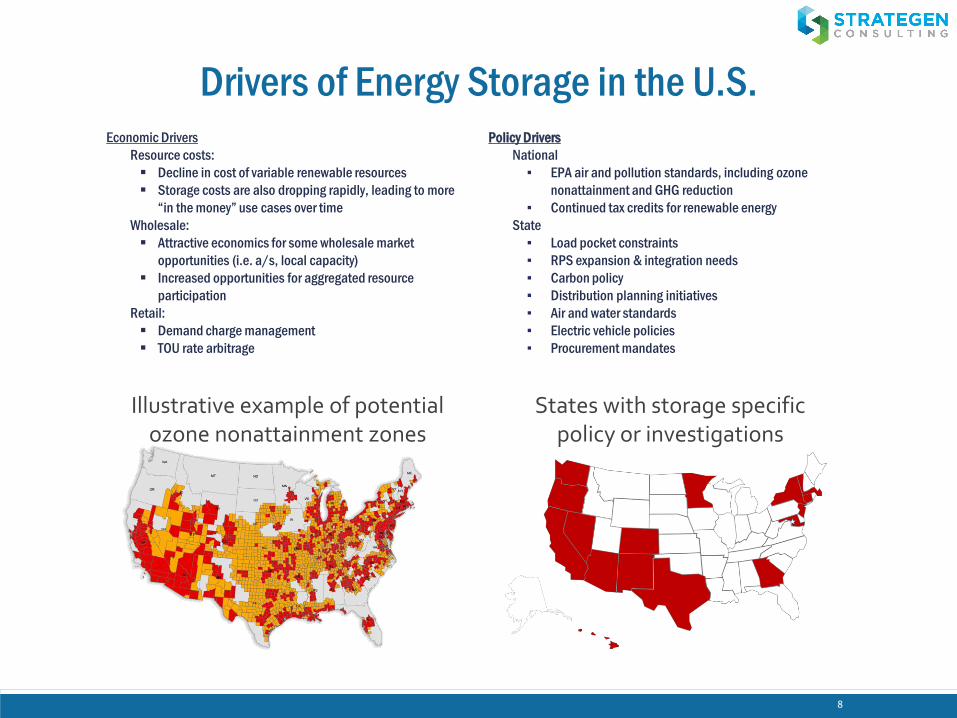

States with storage specific policy or investigations

Drivers of Energy Storage in the U.S.Policy Drivers

National

▪ EPA air and pollution standards, including ozone

nonattainment and GHG reduction

▪ Continued tax credits for renewable energy

State

▪ Load pocket constraints

▪ RPS expansion & integration needs

▪ Carbon policy

▪ Distribution planning initiatives

▪ Air and water standards

▪ Electric vehicle policies

▪ Procurement mandates

Economic Drivers

Resource costs:

Decline in cost of variable renewable resources

Storage costs are also dropping rapidly, leading to more

“in the money” use cases over time

Wholesale:

Attractive economics for some wholesale market

opportunities (i.e. a/s, local capacity)

Increased opportunities for aggregated resource

participation

Retail:

Demand charge management

TOU rate arbitrage

Illustrative example of potential ozone nonattainment zones

8

Utility Investment Priorities

HTTP://WWW.UTILITYDIVE.COM/NEWS/THE-SECTOR-FAVORITE-STORAGE-TOPS-UTILITY-TECH-PICKS-FOR-SECOND-YEAR-

RUNNIN/414304

9

Survey: In which technologies do you think your utility should invest more?

As much as 77% of utility executives are already investing or plan to invest in

storage solutions in the next 10 years.SOURCE: HTTP://SOLARINDUSTRYMAG.COM/UTILITY-EXECS-WEIGH-IN-ON-ENERGY-STORAGE-AND-SOLAR

U.S. Energy Storage Market Forecast

SOURCE: GTM RESEARCH/ESA U.S. ENERGY STORAGE MONITOR 10

• GTM Research forecasts significant growth in the US storage market over the next five years resulting in 1,662 MW annual market by 2020 (26 times the market size in 2014).

Global Battery Storage Market Trends

11

GermanyChileSouth KoreaChinaJapanUnited States

700

600

500

400

300

200

100

0

Rat

ed C

apac

ity

(MW

)

Global Operational Grid-Connected Battery Storage

Japan & South Korea– Ongoing issues with nuclear fleet; large installations

of variable resources– Both countries have storage targets and substantial

development underway

China– Substantial growth in renewables; rapid growth in

storage since 2013– Rapid growth in system capacity needs

EU– Germany leads based on supportive regs, $260 MM

funding, and nuclear decommissioning

Australia– Top global market for distributed storage– Highest retail electricity rates in the Organization for

Economic Cooperation and Development (OECD)

India– Rapid “leapfrogging” of conventional grid with solar

PV for grid electrification– Like other industrializing nations, large opportunity

for solar + storage / microgrids

Battery Technology Costs

Source: Nykvist (2015)

Source: IESA, Walawalkar (2014)

12

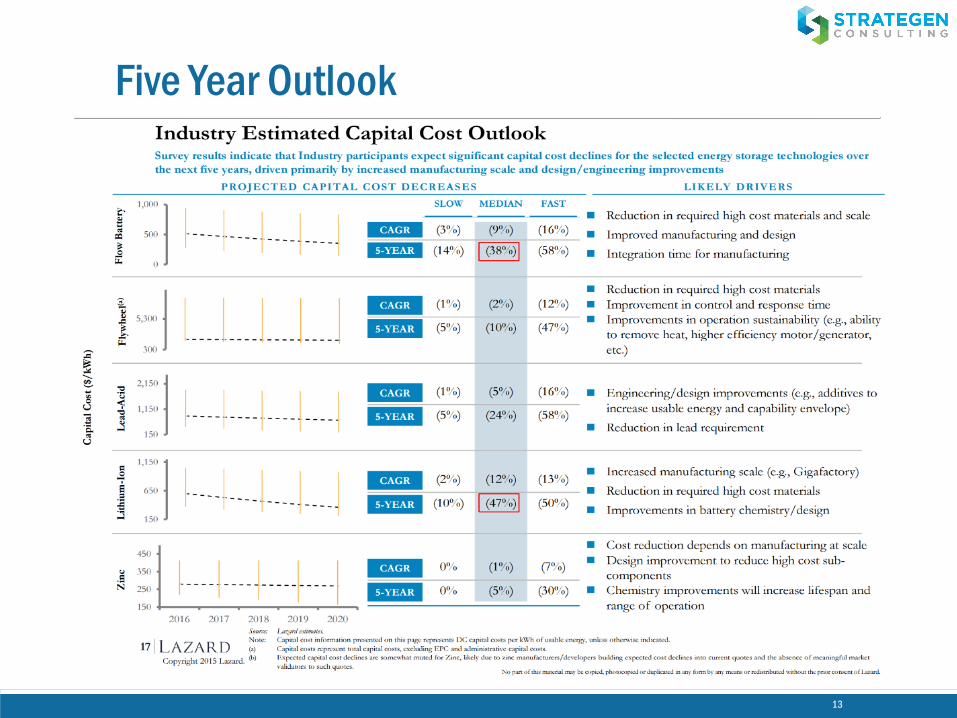

Five Year Outlook

13

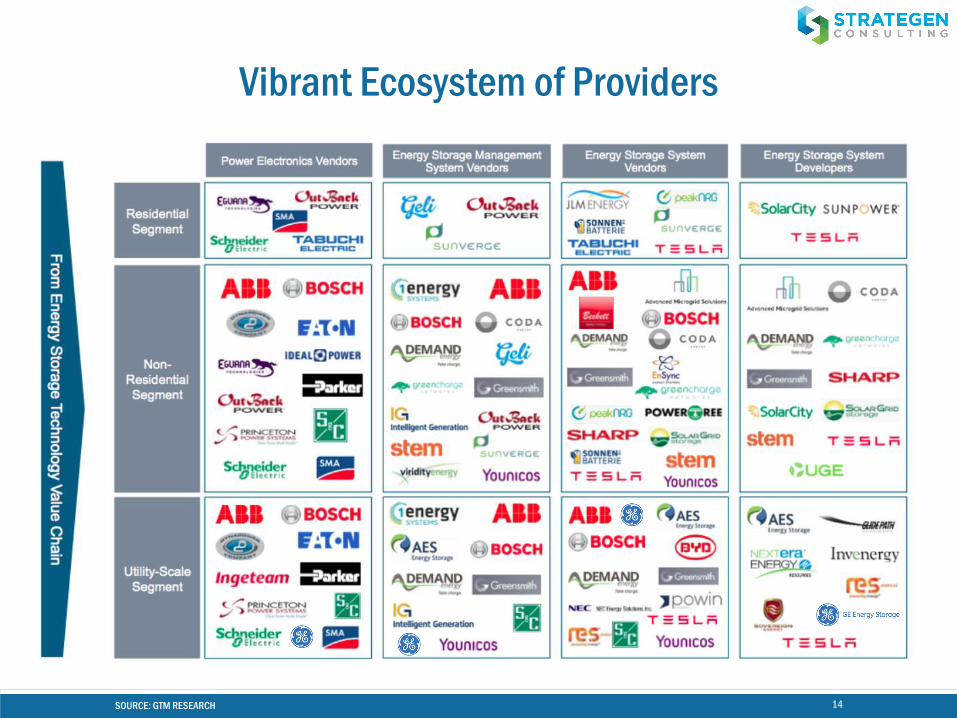

Vibrant Ecosystem of Providers

SOURCE: GTM RESEARCH 14

The Importance of Demand

SOURCE: CEMAC REPORT TO DOE 15

• Modest sales of EV/hybrids can have significant impact on global cell production.

• If just 1 in 10 cars have hybrid/electric capability the demand will be equal to all 2015 global cell demand

• 2015 EV/hybrid demand equates to 2.6 million Powerwalls

• Currently, significant underutilization in global cell production

0

100

200

300

400

500

600

Cu

mu

lati

ve In

stal

led

Cap

acit

y (M

W)

Grid-Connected Battery Storage Projects in the U.S.

SOURCE: DOE GLOBAL ENERGY STORAGE DATABASE ACCESSED 9/7/2016 16

Third-Party Owned

Customer Owned

Utility Owned

BTM Technologies are Merging

Source: GTM Research Q2 2015 U.S, Energy Storage Monitor

Customer-Sited Solar-Plus-Storage Forecasts

17

Emerging “Behind-the-Meter” Storage

Programs and Procurements (Non-MN)

Self-Generation Incentive Program (SGIP)

SGIP & Local Capacity RFO(135 MW Customer-Sited)

SGIP & BYO Storage

Glasgow EPB Infotricity Program (165 homes w/ distributed storage)

Tesla Powerwall(500 unit program)

Demand Mgmt. Program (125 MW overall)Brooklyn-Queens Demand Mgmt. Program (41 MW customer-sited)

Duke Energy partnership with Green Charge Networks and REC Solar through unregulated arm

Solar Innovation Study(25 home pilot)Solar + Storage + Demand Charge (100 home pilot)

Distributed Storage Program (1 MW pilot)

18

Stapleton Project(6 home pilot)

Source: GTM Research

Evolving Wholesale Market Opportunities for Distributed Resources (Non-MISO)

19

“Learning by Doing” State Policy Examples

20

State Measure Summary

California

Assembly Bill 2514 (Passed in 2010)Assembly Bill 2868 Assembly Bill 1637

1.3 GW energy storage procurement mandate for California’s Investor Owned Utilities (PG&E, SCE, and SDG&E) by 2020+ 500 MW in distributed energy storage+ incentives for BTM storage by $249M

OregonHouse Bill 2193(Effective June 10, 2015)

Requires Portland General Electric and PacifiCorp to have procured a minimum of 5 MWh of energy storage by 2020.

Hawaii - Public Utility Commission

Docket No. 2014-019214 (Phase 2) – “DER 2.0”(Current Proceeding)

Proceeding tasked with developing competitive markets for distributed energy resources (DERs) to provide grid-supportive services. Self-supply policy is spurring storage.

New JerseyDocket Nos. QO15040477& QO15121333

$3 million Renewable Electric Storage Initiative for behind-the-meter storage.

WashingtonValuing Energy StorageUE-151069

Inclusion of storage to 2015 IRPs.

ArizonaAPS/RUCO Energy Storage Settlement 14-0292-00169& APS’s 2016 DSM plan

APS agreed to consider technologies other than natural gas for peaker plant upgrade +10 MW of storage + $4 million to develop a residential battery storage program.

Massachusetts

▪ The Massachusetts Department of Energy Resources (DOER) has recommended 600MW of advanced energy storage technologies to be installed on the state grid by 2025, providing over $800 million in cost savings to ratepayers.

▪ Equates to 5 percent of Massachusetts’ peak load, whereas Oregon’s target is 1 percent and California’s is 2 percent.

▪ The top 10 percent of hours of electricity made up 40 percent of ratepayers’ annual electricity bills, to the tune of more than $3 billion.

21

Thank you!Lon HuberDirectorStrategen Consulting, LLC

Email: [email protected] Phone: 928-380-5540

More Information

22