global trends in online shopping - squarespace · asia pacific usa north america germany world ......

TRANSCRIPT

Global Trends in Online Shopping

Keillen Ndlovu

Head of Listed Property Funds

Implications for Listed Property

2

The Rise of Online Shopping

Source: Google

3

Online Shopping in South Africa

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

% Growth year-on-year 15.3% 12.4% 11.7% 4.9% 7.0% 9.1% 8.7% 6.7% 7.4% 7.6% 8.2%

On-line as % of total

retail sales0.17% 0.20% 0.23% 0.29% 0.35% 0.41% 0.50% 0.62% 0.76% 0.88% 0.97%

Source: National Treasury, World Wide Worx, Deutsche Securities March 2017

4

Online shopping as a % of total retail sales across the world

Source: Bank of America Merrill Lynch , Euromonitor June 2016

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0%

ChinaSouth Korea

United KingdomAsia Pacific

USANorth America

GermanyWorld

Western EuropeJapan

FranceAustralia

New ZealandEastern Europe

IndiaRussiaBrazilSpain

ItalyLatin America

CanadaMexico

IndonesiaMiddle East & Africa

5

2016 US Performance by REIT Type

Industrial Outperformed and Malls Underperformed

Source: Deutsche Bank, SNL December 2016

35.0%

30.0%

25.0%

20.0%

15.0%

10.0%

5.0%

0.0%

-5.0%

-10.0

Average

30.6%

27.2%

23.2%

21.6%

17.1%

14.3%

10.7%9.2%

4.9% 4.9%

-4.9%

-7.5%

8.6%

6

Global Online Penetration by Category

0%

5%

10%

15%

20%

25%

30%

35%

Apparel and FootwearSpecialst Retailers

Beauty and PersonalCare Internet Retailing

Electronics andAppliance Specialist

Retailers

Home and GardenSpecialist Retailers

2000

2014

2019E

Source: Bank of America Merrill Lynch , Euromonitor June 2016

7

How Consumers View Internet Versus Physical Shopping for Different Aspects

80.7

73.8

73.1

70.6

67.2

59.2

49.3

29.9

28.9

18.4

18

14.2

6.3

8.1

8.6

14.4

15.9

17.2

33.8

36.9

18.5

44.4

32.1

47.5

0 10 20 30 40 50 60 70 80 90

Easy to compare prices

Price

Range

Convenience

Browsing

Product info

Speed of purchase

Enjoyment

Product quality

Customer service

Trust in Retailer

Refunds

Regular store shopping is better

The internet is better

Source: Bank of Merrill Lynch Real Estate Industry Overview, June 2016

8

Use of Apps to Enhance the Shopping Experience

Source: Wayfair

9

Westfield – One of Largest Retail Landlords Globally Identified 6 Shopper “Tribes” in the UK in 2016

Source: Bank of Merrill Lynch Real Estate Industry Overview, June 2016

10

Move Towards More “Experiential” Retail Means Retailers may Consolidate into Larger Flagship Stores

Source: Westfield Corp October 2016 Presentation

11

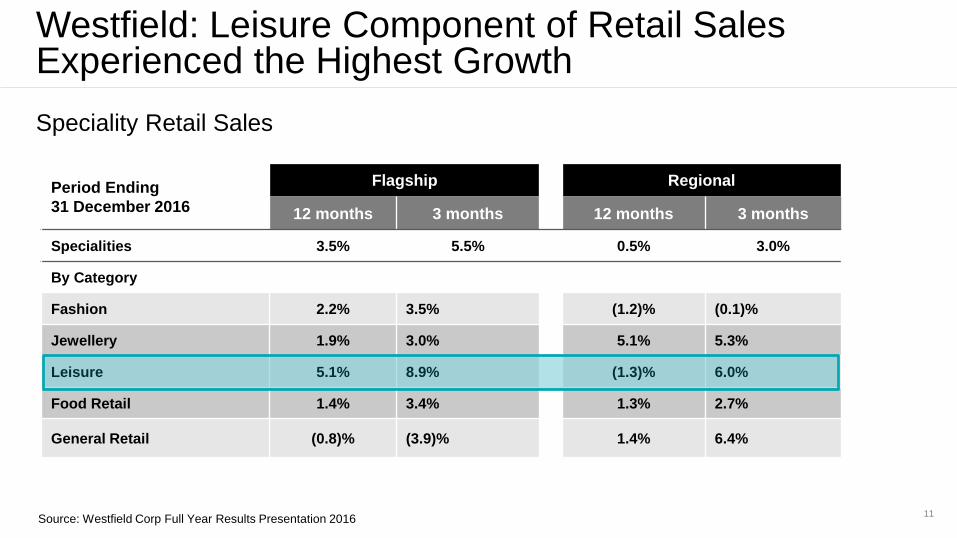

Westfield: Leisure Component of Retail Sales Experienced the Highest Growth

Speciality Retail Sales

Period Ending

31 December 2016

Flagship Regional

12 months 3 months 12 months 3 months

Specialities 3.5% 5.5% 0.5% 3.0%

By Category

Fashion 2.2% 3.5% (1.2)% (0.1)%

Jewellery 1.9% 3.0% 5.1% 5.3%

Leisure 5.1% 8.9% (1.3)% 6.0%

Food Retail 1.4% 3.4% 1.3% 2.7%

General Retail (0.8)% (3.9)% 1.4% 6.4%

Source: Westfield Corp Full Year Results Presentation 2016

12

Unibail: Leisure Component Also Generated the Highest Growth

Source: Unibail Full Year 2016 Results Presentation

Fashion Bags, Footwear

& Accessories

Culture, Media

& Technology

Dining Health & Beauty Entertainment

+0.6%

-1.0%

+0.8%

+4.4%

+5.1%+5.3%

13

Addition of Lifestyle Components to Shopping CentresThis Trend has Started in South Africa

Source: Westfield Corp October 2016 Presentation

14

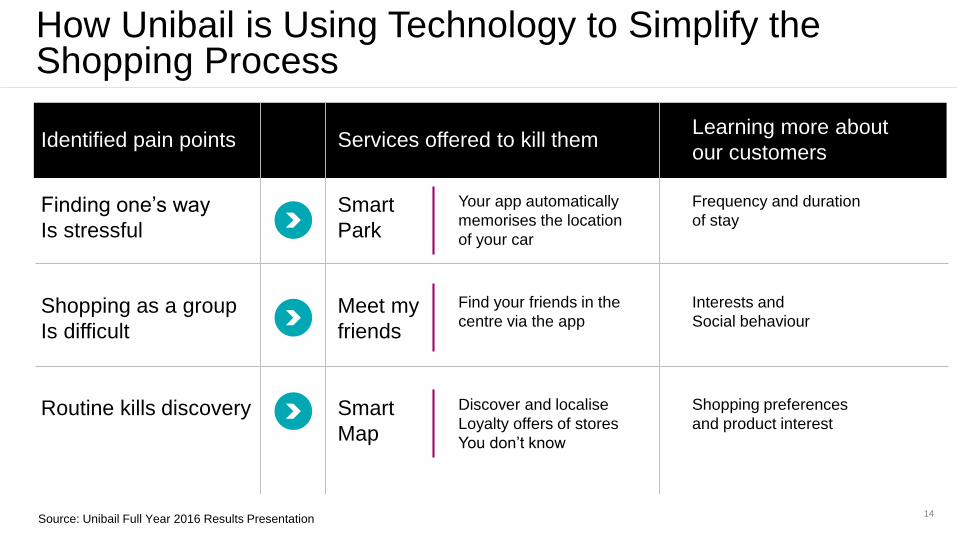

How Unibail is Using Technology to Simplify the Shopping Process

Identified pain points

Source: Unibail Full Year 2016 Results Presentation

Services offered to kill themLearning more about

our customers

Finding one’s way

Is stressful

Shopping as a group

Is difficult

Routine kills discovery

Smart

Park

Meet my

friends

Smart

Map

Your app automatically

memorises the location

of your car

Find your friends in the

centre via the app

Discover and localise

Loyalty offers of stores

You don’t know

Frequency and duration

of stay

Interests and

Social behaviour

Shopping preferences

and product interest

15

Use of Shopping Centre Apps to Target Marketing Material to the Relevant Shopper

Source: CNBC Retail May 2015; Unibail-Rodamco Results Presentation February 2016

Meet My Friends

Smart Map

Smart Park

16

Introducing Electric Car Charging Ports to Parking Lots Attracts consumers and increases centre dwell time

Source: Unibail Full Year 2016 Results Presentation

224electric car

charging stations

4sites with Tesla chargers

20sites targeted in 2017

17

Using Games like Pokemon Go to Attract Footfall Particularly Useful for Attracting Young Adults

Source: Unibail Full Year 2016 Results Presentation

Deploying game features and events in

58 Shopping Centres

Exclusivityin Continental Europe

Footfall

Customer Engagement

Enriching Customer Experience

18

Use of Data Analytics to Fine-Tune Tenant Mix

19

Landlords Taking an Omni-Channel Approach to Enhance the Shopping Centre Experience

Amazon pick up lockers at Drake’s Circus

Shopping Centre in Plymouth (British Land)

Quick check-out handsets at Waitrose, Plymouth

Source: STANLIB Research November 2016

20

Occupancy Rates of Listed Mall Landlords in Key Markets

Source: Bank of Merrill Lynch Research, Company Data, June 2016

100%

90%

80%

70%

60%

50%

2007 2008 2009 2010 2011 2012 2013 2014

Average listed Australia mall operators

Average EU listed mall operators

Average US listed mall operators

Dead mall danger zone

21

Rental Growth for Mall Landlords in Key Markets

0%

1%

2%

3%

4%

5%

6%

7%

Source: Bank of Merrill Lynch Research, Company Data, June 2016

22

Problems Encountered When Buying Online

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Speed of delivery slower than indicated

Technical failure of website during ordering or payment

Wrong or damaged goods delivered

Difficulties in finding information on legal rights

Complaints difficult

Final Costs higher than indicated

Foreign retailer did not sell in my country

Fraud

Source: Eurostat 2016

23

Vast Majority of Retail Sales Should Continue to Occur in Stores

Source: Bank of Merrill Lynch Research, Euromointor, Company Data, June 2016

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2020E

Online Retail Sales

Brick and Mortar Sales

9.6% 10.2% 11.7% 13.2% 14.9%

24.8%

90.4% 89.8% 88.3% 86.8%

85.1%

75.2%

24

Impact of Drone Delivery on Both Retail and Logistics Properties

Source: Bank of Merrill Lynch Real Estate Industry Overview, June 2016

Amazon Prime in action DHL Packstation with SkyPort and Parcelcopter

Manufacturer

Retailer landscape in the past Retailer landscape now

Importer

Regional Distribution Unit

Local Distribution Unit

Retail Stores

Consumers

Manufacturer Importer

National Distribution Unit

Local Distribution Unit

Retail Stores Consumers

Delivery parcel

(returns)

25

Evolving Retailer LandscapeModern supply chain now consumer facing

Source: LondonMetric 2016

26

US Industrial Vacancies at All-Time Lows

Source: Prologis March 2017

350

250

150

50

(50)

(150)

(250)

U.S.Square Feet, Millions

10

9

8

7

6

5

4

3

2

1

0

%

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

07

20

09

20

11

20

13

20

15

20

16

20

17

E

20

18

F

Completions (L) Net Absorption (L) Vacancy Rate (R)

27

Prologis (PLD) – Significant Opportunity to Increase Logistics Space

0.000

1.000

2.000

3.000

4.000

5.000

6.000

US Europe China Japan Other PLDRegions

Additional Modern Stock Required Today

Current Modern Stock

Modern Logistics SpaceSquare Feet, Millions

Source: Prologis March 2017

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2010 2011 2012 2013 2014 2015 2016E 2017F 2018F 2019F 2020F

28

Global E-Commerce Sales Projected to Grow by 162% Between 2015 and 2020

Source: Prologis March 2017

14

12

10

8

6

4

2

0

%Modern Logistics SpaceSquare Feet, Millions

E-Commerce Sales (L) E-Commerce as a % of Total Retail Sales (R)

29

Shopping Centres are the Ultimate Multi-Channel destination

Source: Hammerson Plc February 2017

In-Centre

sales 1 2 3

1. In-store multichannelAdditional click and collect sales,

‘in-store online’ channel and net

effect of online returns +10%

2. Retail haloIncremental market share of online

sales catchment +5%

3. Collection kiosksIntegrate pure online retailers

into centre +1-2%

(1)

(2)

(3)

Productivity of the centre extends by

a further 17%

30

STANLIB Global Property Fund

Top Retail and Industrial Property Holdings

Industrial

• US

– Prologis

• UK and Europe

– Prologis

– LondonMetric

– Segro

• Asia

– Prologis

– Global Logistics Properties

• Australia and New Zealand

– Goodman Group

Retail• UK and Europe

– Hammerson

– Unibail Rodamco

– Westfield

• Asia

– CapitaMall Trust

– Hongkong Land

– Wharf Holdings

• Australia and New Zealand

– Scentre Group

– Westfield

• US

– Westfield

– Simon Property Group

– General Growth Properties

Source: STANLIB February 2017

31

STANLIB Global Property Holdings by Property Sector

Retail REITs, 31.30%

Industrial & Office …

Residential REITs, …

Specialty REITs, 13.76%

Real Estate Holding & Development,

5.99%

Diversified REITs, 4.50%

Hotel & Lodging REITs, 1.61%Cash, 1.50%

Source: STANLIB February 2017

Thank You

33

Disclaimer

Collective Investment Schemes (CIS) in Securities are generally medium to long-term investments. An investment in the participations of

a collective investment scheme in securities is not the same as a deposit with a banking institution. The value of participatory interests

may go down as well as up and past performance is not necessarily a guide to the future. CIS are traded at ruling prices and can engage

in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available on request from STANLIB

Collective Investments (“the Manager”). Commission and incentives may be paid and if so, would be included in the overall costs.

Forward pricing is used. Fluctuations or movements in exchange rates may cause the value of underlying international investments to go

up or down. Liberty is a full member of the Association for Savings & Investment SA (ASISA). The Manager is a member of the Liberty

group of companies.

The information and content of this document are intended to be for information purposes only and STANLIB does not guarantee the

suitability or potential value of any information contained herein. STANLIB Wealth Management Limited does not expressly or by

implication propose that the products or services offered in this document are appropriate to the particular investment objectives or needs

of any existing or prospective client. Potential investors are advised to seek independent advice from an authorised financial adviser in

this regard. STANLIB Wealth Management Limited is an authorised Financial Services Provider in terms of the Financial Advisory and

Intermediary Services Act 37 of 2002 (Licence No. 26/10/590)