globalization, productivity and plant exit - evidence from ... · dp rieti discussion paper series...

TRANSCRIPT

DPRIETI Discussion Paper Series 09-E-048

Globalization, Productivity and Plant Exit- Evidence from Japan -

INUI TomohikoEconomic and Social Research Institute, Cabinet Office and Nihon University

Richard KNELLERNottingham University

MATSUURA ToshiyukiKeio University

Danny McGOWANNottingham University

The Research Institute of Economy, Trade and Industryhttp://www.rieti.go.jp/en/

1

RIETI Discussion Paper Series 09-E -048

Globalization, Productivity and Plant Exit - Evidence from Japan -*

September 2009

Tomohiko Inui (Economic and Social Research Institute, Cabinet Office and Nihon University)

Richard Kneller (Nottingham University) Toshiyuki Matsuura (Keio University)

Danny McGowan (Nottingham University)

Abstract

During the 1980s and 1990s, Japanese manufacturers began to relocate production from sites in

Japan to low-wage East Asian countries such as China, Malaysia and Thailand. Imports of

manufacturing goods increased substantially over the same period. This rapid rise in imports, and

proliferation of globalization, has led to concerns among policymakers that firms and plants may

close. The media portray foreign multinationals as closing down productive Japanese plants and

relocating them elsewhere in Asia. We find that this is not the case. Equally, the plants that are closed

are below average productivity and the exit component contributes a very small fraction to

productivity growth (using both the GR and FHK methods). In short, plant exit has not been the

reason for Japan's low productivity growth in the 1990s. Instead a lack of productivity growth within

plants is identified as being the main cause.

Keywords: Industry Dynamics, Productivity, Exit, Multinational Firms, International Trade

JEL classification: D21, D24, F15, F23, L20, L6

RIETI Discussion Papers Series aims at widely disseminating research results in the form of professional papers, thereby stimulating lively discussion. The views expressed in the papers are solely those of the author(s), and do not present those of the Research Institute of Economy, Trade and Industry.

* We would like to thank Dr. Masahisa Fujita (President and CRO of the Research Institute of Economy, Trade and Industry), Professor Kyoji Fukao (RIETI Faculty Fellow, and Hitotsubashi University), Professor Sadao Nagaoka (RIETI Counselor, and Hitotsubashi University) and participants of the workshop held at RIETI, and at Western Economic Association International conference at Vancouver for helpful comments and suggestions on earlier versions of this paper. This research was partially supported by the Ministry of Education, Science, Sports and Culture, Grant-in Aid for Scientific Research (A), No. 20243021. The views expressed in this paper are those of the authors and should not be attributed to both RIETI and the Economic and Social Research Institute.

2

1. Introduction

The recent empirical studies1, using establishment or firm level data, confirm that

aggregate productivity growth at national level or industry level depends not only on the

productivity gains within the establishments, but also on the shift in the output shares

between the establishments or firms in the different level of productivities (see

Bartelsman and Doms, 2000, Forster et al. 2001 and Hayakawa, Kimura, and Machikita

2009). If the output of the establishments with higher productivities can expand their

production and that of the lower productivity establishments contracts, this change in

the market share also brings improvements in aggregate productivity in the economy.

The productivity improvement through market selection is examined by Disney, Haskel

and Heden (2003) by using UK manufacturing data set. They find the market selection

(entry, exit and the reallocation of market share) accounts for 80-90% of establishment

TFP growth for 1982-92 period in UK. Criscuolo, Haskel and Martin (2004) use more

recent data on UK manufacturing plants and find that the share of productivity growth

accounted for by entry and exit increased from 25 per cent in the 1980s to 50 per cent in

the 1990s.

Increased import penetration may lead to higher domestic market competition and

higher aggregate productivity by forcing the least productive establishments to exit from

the market, as described in the Melitz and Ottaviano (2005) model. Lileeva (2007)

examines the effect of US-Canada Free Trade agreement on the productivity of the

Canadian manufacturing sector. This study finds that the lower tariff rate in Canada

increased exit rates among moderately productive non-exporting plants and lead to the

1 The recent studies on Japanese productivity dynamics using micro data, such as Nishimura, Nakajima and Kiyota (2005) and Fukao and Kwon (2006) confirm the role of “between” effects on the industrial productivity growth.

3

reallocation of the market share to the higher productivity plants in Canadian

manufacturing plants.

Bernard, Jensen and Schott (2006a) find that the probabilities of shut downs are

higher in industries facing increased import competition from low-wage countries,

especially for low-wage and labor-intensive plants within the industries. Bernard,

Jensen and Schott (2006b) examine the effect of the trade cost reduction, such as tariff

and transportation rates, on the reallocation in the US manufacturing sector and find that

low productivity plants in the industry that have relative larger decline in the trade costs

are more likely to die. Bernard and Jensen (2007) show empirical results about the US

manufacturing death that the probability of death is substantially lower for those plants

that are part of multi plant firm and also domestic plants that are owned by US

multinationals. Greenaway, Gullstrand and Kneller (2008) find that the effect of trade

on exit of Swedish firms being strongest when trading partners are other than OECD

countries.

This paper adds to the growing evidence on plant exit and the survival chances of

multinational owned enterprises. Görg and Strobl (2003) address the probability of exit

of majority owned plants in Ireland, and Gibson and Harris (1996), Bernard and Jensen

(2002), Bernard and Sjöholm (2003) look at evidence from New Zealand, the United

States and Indonesia, respectively. The results differ depending upon the country under

inspection. For example, Alvarez and Görg (2009) find that multinationals are more

likely to shut plants in Chile, but only during downturns, while Mata and Portugal

(2004) find that survival probabilities are higher among Portuguese plants when they

are foreign owned.

The reminder of the paper is organized as follows. In the next section, we give a

4

overview of the data and describes the construction of the plant-level, firm-level and

industry-level characteristics. Section 3 investigates differences between plants

depending on their ownership structure by controlling other firm, plat and industry

characteristics. Section 4 investigates whether plant exit has an effect upon Japanese

productivity growth in the recent years. Section 5 concludes.

2. Data

Our primary data sources are the linked longitudinal data sets of the Census of

Manufactures (hereafter called COM) and the Basic Survey of Japanese Business

Structure and Activities (BSJBSA) for the period 1994-2005. The COM data is an

establishment-level data conducted by the Ministry of Economy, Trade and Industry

(METI). The COM data covers all plants located in Japan and it include the information

on plant characteristics, such as, their location, number of employees, tangible assets,

and value of shipments. On the other hand, the BSJBSA is a firm-level survey

conducted by METI. The survey includes all firms with more than 50 employees or over

and with capital of 30 million yen or over. It provides data on corporate characteristics

such as R&D activity, export, import, foreign ownership ratio, foreign direct investment,

and fanatical details. For our analysis, we linked a plant-level data, the COM to a

firm-level survey, the BSJBSA. At first, we constructed a plan-level panel data set,

which covers all the manufacturing plants with more than 3 employees. Since BSJBSA

dose not include firms with less than 50 employees or less than 30 million capital

amounts, we have to exclude small single plants with less than 50 employees in our

sample. In addition, even if plants belong to firms in the BSJBSA, due to the viability of

data on tangible asset, which is indispensable to estimate TFP, those plants with less

than 10 employees are excluded. Information on capital data is also not available for

5

2001, 2002 and 2004 for establishments with less than 29 employees. Therefore, our

linked panel data set covers the years from 1994 to 2000, 2003, and 2005.

For an identification of plant entry and exit, we used using a unique identification

number. An entering plant is deemed to have entered where it is observed at time t but

was not observed in the dataset in previous period, t-1. Equivalently, an exiting plant is

one that was observed at t-1 but not at time t. In this framework, since our plant-level

panel data set is restricted to plants with more than 3 employees, it is not possible to say

whether this is caused by plant death or exit from the sample2. Exit is deemed to refer

specifically to plant closure; industry switching and mergers are not considered within

this framework3.

The percentage of plants which either enter or exit is low, a feature which holds

across industries. Throughout the sample, there are 2,330 instances of entry and 3,392

observations of exit. The exit rate may be affected by the size cut-offs. Throughout the

dataset there are approximately 86,000 observations of single-plant firms. These plants

have at least 50 employees meaning that they are fairly large, and less likely to exit. If

the data permitted inspection of small plants, the exit rate may be higher since such

establishments traditionally face higher probabilities of death.

2 Industry switching is not regarded as plant exit. However, those plants whose industry switches from manufacturing sector to other sector at between t-1 and t, are not observed in our plant-level panel data set at t. Thus these plants are regarded as exiting plants. 3 Switching and M&A activity are found to play an important role in other studies. In Swedish manufacturing industries over the period 1982-1995, Greenaway et al. (2008) find 2.9 percent of exit occurs through switching and 3.9 percent through mergers and acquisitions. Bernard et al. (2006a) find for the United States that in the face of competition from low-wage imports, firms switch towards more capital intensive sectors.

6

Table 1: Annual Rate of Entry and Exit

Percentage of FirmsYear Entering Exiting

Sample Average .01 .02

1994 .01 .011995 .01 .011996 .01 .011997 .01 .021998 .03 .031999 .01 .032000 .01 .032001 .01 .032002 .01 .032003 .01 .022004 .01 .022005 .02 .00

Over the sample, the entry and exit rates are approximately 1 and 2 percent,

respectively. There are some fluctuations around this, notably for the entry rate which

‘spikes’ to 3 percent in 1998. Overall, however, there is little variation with entry and

exit remaining concentrated around the mean. While this may seem to be a fairly low

rate of exit, it is comparable with that of Swedish manufacturers over the period 1982 to

1995 used by Greenaway et al. (2008).

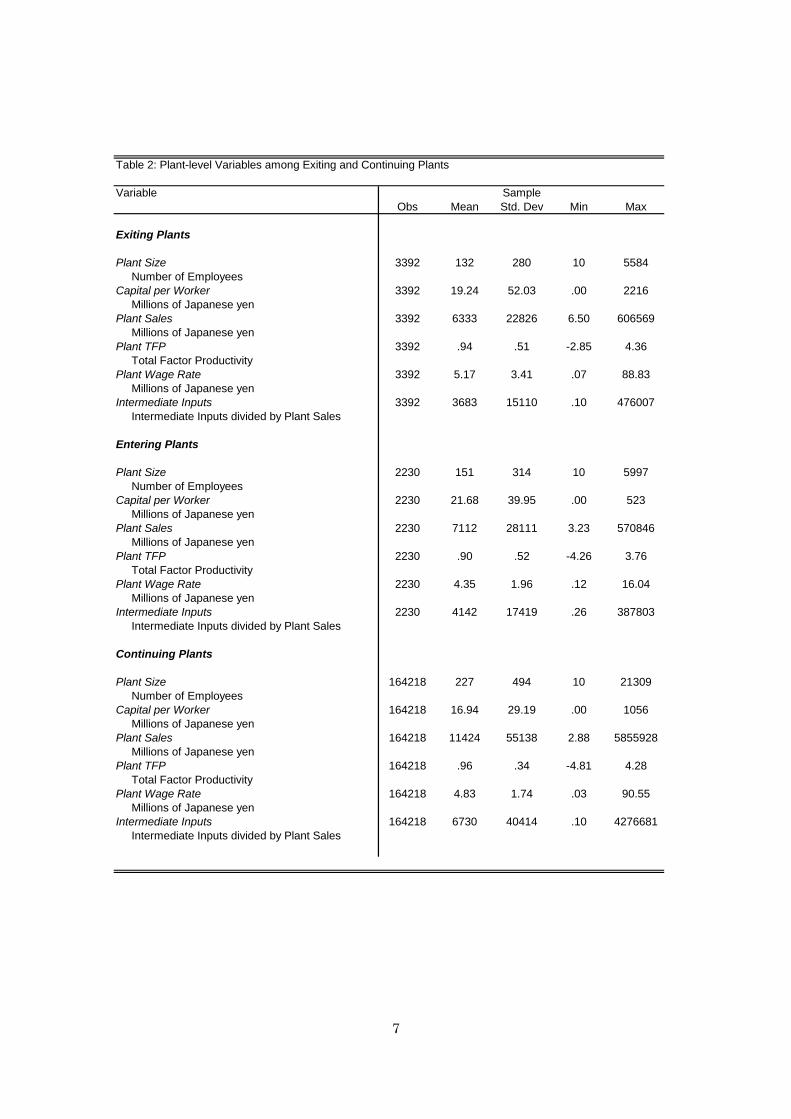

Table 2 shows that the plant variables differ considerably across entering, exiting

and continuing firms. For example, entering and exiting plants tend to be smaller and

have lower sales, productivity and intermediate inputs than continuing plants. On

average, continuing firms have a lower capital-labor ratio relative to entrants and exiting

plants, and, despite paying higher wages than entrants, their wage rate is lower than

what is paid by exiting plants.

7

Table 2: Plant-level Variables among Exiting and Continuing Plants

Variable SampleObs Mean Std. Dev Min Max

Exiting Plants

Plant Size 3392 132 280 10 5584 Number of EmployeesCapital per Worker 3392 19.24 52.03 .00 2216 Millions of Japanese yenPlant Sales 3392 6333 22826 6.50 606569 Millions of Japanese yenPlant TFP 3392 .94 .51 -2.85 4.36 Total Factor ProductivityPlant Wage Rate 3392 5.17 3.41 .07 88.83 Millions of Japanese yenIntermediate Inputs 3392 3683 15110 .10 476007 Intermediate Inputs divided by Plant Sales

Entering Plants

Plant Size 2230 151 314 10 5997 Number of EmployeesCapital per Worker 2230 21.68 39.95 .00 523 Millions of Japanese yenPlant Sales 2230 7112 28111 3.23 570846 Millions of Japanese yenPlant TFP 2230 .90 .52 -4.26 3.76 Total Factor ProductivityPlant Wage Rate 2230 4.35 1.96 .12 16.04 Millions of Japanese yenIntermediate Inputs 2230 4142 17419 .26 387803 Intermediate Inputs divided by Plant Sales

Continuing Plants

Plant Size 164218 227 494 10 21309 Number of EmployeesCapital per Worker 164218 16.94 29.19 .00 1056 Millions of Japanese yenPlant Sales 164218 11424 55138 2.88 5855928 Millions of Japanese yenPlant TFP 164218 .96 .34 -4.81 4.28 Total Factor ProductivityPlant Wage Rate 164218 4.83 1.74 .03 90.55 Millions of Japanese yenIntermediate Inputs 164218 6730 40414 .10 4276681 Intermediate Inputs divided by Plant Sales

8

2.1. Plant-Level Variables

Information is provided on the three-digit industry in which a plant operates4. The

plant-level variables include plant size (measured by the number of employees), capital

per worker, plant sales, plant TFP (measured relative to the industry and in logs), plant

wage rate and the volume of intermediate inputs used by the plant.

Table 3: Plant-level Variables

Variable SampleObs Mean Std. Dev Min Max

Plant Size Number of Employees 169590 225 489 10 21309Capital per Worker Millions of Japanese yen 169590 5119 23240 .07 1052705Plant Sales Millions of Japanese yen 169590 11321.71 54454 2.88 5855928Plant TFP Total Factor Productivity 169590 .96 .35 -4.81 4.36Plant Wage Rate Millions of Japanese yen 169590 4.84 1.79 .03 40.5Intermediate Inputs Intermediate Inputs divided by Plant Sales 169590 6669 39879 .10 4276681

The manufacturing establishments are split into 48 industries and TFP is calculated

for each plant relative to the industry average. Following Caves, Christensen and

Diewert (1982), Caves, Christensen and Tretheway (1983), and Good, Nadiri, Roeller

and Sickles (1983), we define the TFP level of establishment p in year t in a certain

industry in comparison with the TFP level of a hypothetical representative establishment

in year 0 in that industry as follows

4 A list of industries is included in Appendix Table 1

9

( ) ( )( )

( ) ( )( )∑∑∑

∑

= =−−

=−

=

−+−−+

−+−−=

t

s

n

iisisisis

t

sss

itift

n

iitifttftpt

XXSSQQ

XXSSQQTFP

1 111

11

1

lnlnlnln

lnln21lnlnln

where Qft, Sift and Xift denote the gross output of plant f in year t, the cost share of factor

i for establishment p’s input of factor i in year t. Variables with an upper bar denote the

industry average of that variable. We use 1994 as the base year. Capital, labor and real

intermediate inputs are used as factor inputs.

The representative establishment for each industry is defined as a hypothetical

establishment whose gross output as well as input and cost share of all production

factors are identical with the industry average. The first two terms on the right hand side

of the equation denote the gap between plant f’s TFP level in year t and the

representative establishment’s TFP level in year t and the representative establishment’s

TFP level in the base year. lnTFPft in the equation constitutes the gap between

establishment f’s TFP level in year t and the representative establishment’s TFP level in

the base year.

2.2. Firm-Level Variables

In addition to information on each plant, our dataset also includes specific

information on firms. This includes firm age, size, capital-labor ratios, a multi-plant

dummy and information on whether the firm conducts FDI. In the empirical section we

use this to study firm-level variables, such as ownership and exporting status, affect

10

plant exit. Summary statistics of the firm-level variables are shown in Table 4.

Table 4: Firm-level Variables

Variable

Obs Mean Std. Dev Min Max

Age 14033 37.64 15.53 0 150 In monthsSize 14033 459 1918 50 77185 Number of WorkersCapital per Worker 14033 12.79 20.74 .00 1275 Millions of Japanese yenFirm TFP 14033 .93 .15 -3.53 2.39 Total Factor ProductivityForeign Ownership Dummy 14033 .01 .12 0 1 1 if Foreign Firm holds more than 50% of capitalR&D Complexity 6815 -4.94 1.54 -10.71 1.92 log R&D divided by Firm SalesExport Dummy 14033 .26 .44 0 1 1 if the firm exportsImport Dummy 14033 .20 .40 0 1 1 if the firm importsFDI 14033 .15 .36 0 1 1 if outward loans and investment > 0Intermediate Inputs 14033 16208 110875 1 7177500 Millions of Japanese yenMulti-plant Dummy 14033 .23 .42 0 1 1 if the firm has more than one plant

It is apparent from Table 4 that the incidence of foreign ownership in Japanese

firms is low. A firm is adjudged to be foreign owned if a foreign firm holds more than

50 percent of the capital5. Many firms appear to be globally engaged with 26 percent

exporting, 20 percent importing and 15 percent of firms investing abroad. Almost half

of firms own more than one plant.

5 Görg and Strobl (2005) use the same criteria. The International Monetary Fund classifies a firm as being foreign owned if a foreigner holds in excess of 25 percent of the firm’s equity.

11

2.3. Industry-Level Variables

The importance of industry-level variables in determining exit has been firmly

established with Roberts and Tybout (1997) finding sunk costs to be important and

Bernard et al. (2006a) highlighting how import penetration from different regions can

affect exit. With these ideas in mind, we include industry-level variables that capture the

effect globalization may impact on plant exit.

Intra-industry trade is often found to have a positive effect upon firm exit. As

international trade grows firms diversify their product range which may lead them to

enter new industries and exit ones they were once involved in. It has also been

established by Greenaway et al. (2008) that firms do not just closedown their operations,

they switch to new industries too. This is also found by Bernard et al. (2006a) who find

that in the United States, firms which are confronted by low-wage import competition

sometimes switch to more capital intensive sectors.

Our measure of intra-industry trade is constructed using the Grubel-Lloyd (1975)

index.

( )[ ]( )ititititititit MX

MXMXGL+

−−+=100

where GLit is the Grubel-Lloyd index of intra-industry trade in industry i in year t, Xi are

exports in industry i during year t and Mit are imports in industry i during year t.

12

The importance of import competition in affecting plant survival has been

addressed by several authors. As in Bernard et al. (2006a), our dataset allows us to

disaggregate import penetration into low-wage country import penetration and other

country imports6.

The effect of low-wage country imports upon exit is not entirely clear. Differences

in countries’ endowments will have profoundly different effects upon the labor, or

capital, intensity of the goods they produce. According to the factor proportions

framework imports from low-wage countries could be thought to positively affect plant

exit since such imports are likely labor abundant and consequently displace similar, high

wage, Japanese goods. Bernard et al. (2006a) find that for the United States, a one

standard deviation increase in low-wage import penetration increases the probability of

plant exit by 2.2 percentage points. However, it is also possible that the source of import

competition could have little effect on exit. Where industries are already saturated with

imports from low-wage countries, additional imports may do little to affect exit. Exit

may be non-linear in imports with low-wage imports only having an effect upon plant

exit where there is relatively little existing import competition.

The measure of low-wage import competition (LWPEN) is constructed as follows

ititit

LWit

it XYMMLWPEN

−+=

6 Countries are deemed to be low-wage where they have GDP per capita of less than 5 percent that of Japan.

13

where LWPENit represents low-wage country import competition in industry i at time t,

MitLW is the value of imports from low-wage countries in industry i at time t, Mit and Xit

represents the value of total imports and exports in industry i at time t and Yit denotes

output in industry i during year t.

Our second measure of import competition is similar to that used to construct

LWPEN. It embodies imports from all countries that are not deemed to be “low-wage”.

ititit

LWitit

it XYMMMOTHPEN−+

−=

where OTHPENit denotes imports from all countries except low-wage economies.

The industry variables mentioned so far capture the influence of globalization upon

plant exit. We also include a measure of sunk entry costs. The empirical literature has

identified sunk entry costs as being an important factor in shaping exit. For example,

Aw et al. (2002) finds that the nature of sunk costs result in very different productivity

distributions in South Korea and Taiwan. Sunk costs also play a key role in determining

death rates of plants (Dunne, Roberts, and Samuelson, 1988, 1989)

Since exit rates tend to be highly correlated with the sunk costs of entry and exit we

use the same measure as Bernard and Jensen (2002) and Greenaway et al. (2008). For

each industry and year, sunk costs are deemed to be the minimum of either the entry or

exit rate. In steady-state equilibrium, entry and exit rates should be equal. Entry and exit

rates should vary with sunk costs. An increase in sunk costs would mean that the entry

14

rate should fall, in equilibrium. However, to focus solely on entry rates could be

misleading as an industry characterized by high sunk costs could experience a high

entry rate due to high expected profits. By using the minimum of entry or exit, we

circumvent this problem.

Summary statistics for the industry-level variables are provided in Table 5.

Intra-industry trade accounts for approximately half of all trade over the sample. Sunk

costs have an average value of 1 percent, that is, the average of the minimum of the

entry and exit rates in an industry is 1 percent of the total number of operating plants.

The share of low-wage imports accounts for a third of Japanese imports.

Table 5: Industry Variables

Variable Obs Mean Std. Dev Min Max

Grubel-Lloyd Index 157273 .50 .26 .01 1.00 Trade that is Intra-IndustrySunk Costs 169590 .01 .01 0 .05 Minimum of entry and exit rateImport Penetration 131669 .09 .09 .00 .67 Imports divided by apparent consumptionLWPEN 131669 .03 .05 .00 .28 Low wage importsOTHPEN 131669 .06 .06 .00 .55 Imports from all other countries

2.4. Plant Features

2.4.1. Multinational Enterprises

Using the information on foreign direct investment we construct a multinational

15

enterprise (MNE) dummy. A firm is assumed to be a multinational where the outward

loans and investment variable has a positive value. Recently the international trade

literature has found multinational owned plants differ from purely domestic ones.

Japanese plants appear to conform to many of the findings reported elsewhere in the

literature. For example, in Table 6 we observe MNE owned plants (where MNEs are

deemed to include domestic- and foreign-owned multinational plants) to be larger, more

capital intensive, more productive, have higher sales, pay higher wages and use more

intermediate inputs when compared with plants which are non-MNE owned.

Table 6: Differences between MNE and non-MNE Owned Plants

OwnershipVariable MNE non-MNE

Observations 53328 116262

Plant Size 415 138 Number of EmployeesCapital per Worker 25.73 13.07 Millions of Japanese yenPlant Sales 25782 4689 Millions of Japanese yenPlant TFP 1.03 .93 Total Factor ProductivityPlant Wage Rate 5.57 4.51 Millions of Japanese yenIntermediate Inputs 15259 2728 Intermediate Inputs divided by Plant Sales

Simple T-tests reveal that non-MNE owned plants are significantly smaller, less

capital intensive and have lower TFP and wages than MNE owned plants7. Exit rates are

significantly higher among non-MNE owned plants although the difference between the

7 T-tests are computed by subtracting the mean of group j from the mean value of group i to find the difference. A t-test is then run where the null hypothesis is that the differences between the means are zero.

16

mean exit rate of MNE and non-MNE plants is small8. These results are shown in Table

7.

Table 7: T-tests on the differences between MNE and non-MNE Owned Plants

Variable Difference

Exit Rate .00**

Size -.72***

Capital Intensity -.68***

TFP -.10***

Wages -1.07***

The richness of the dataset also permits investigation of how, within firms, exiting

MNE plants differ from those which continue. In Table 8 it is shown that, within firms,

MNE exiting plants are significantly smaller, less capital intensive and pay higher

wages when compared with plants which continue in the same firm. When compared to

continuing plants in the same firm, exiting plants do not appear to have significantly

different productivity.

8 When we compare the differences between the plant-level variables across MNE and non-MNE exiting plants, these features remain.

17

Table 8: Within MNE T-tests

Variable Difference

Size .79***

Capital Intensity .20***

TFP .02

Wages -.61***

2.4.2. Foreign Ownership

As with MNEs, the role of foreign ownership in determining plant exit has been

much discussed with Mata and Portugal (2004), Bernard and Sjöholm (2003) and Girma

and Görg (2004) all touching on the subject. Foreign firms may be more footloose

relative to domestic firms since they can relocate production across countries. However,

it is possible that they may be less likely to close plants because they have incurred sunk

costs to operating abroad which leads to entrenchment and a reduction in the probability

of plant exit. As in the previous section, we use T-tests to examine whether there are

significant differences in exit rates and the plant-level variables between domestic and

foreign owned plants.

In Table 9 we report results of t-tests that deal with differences between domestic

and foreign owned plants. “Domestic plants” refer to all Japanese plants, that is,

irrespective of whether they belong to a multinational or not. The same is true of foreign

owned plants. We find that foreign plants are significantly larger, more capital intensive,

18

productive and pay significantly higher wages than domestic plants. These results

accord with what many other authors, such as Bernard and Sjöholm (2003), have found.

The wage premium paid by foreign plants may be a means of incentivizing workers if

foreign plants are more likely to exit

Table 9: T-tests on the differences between Domestic and Foreign Owned Plants

Variable Difference

Exit Rate .00***

Size -.58***

Capital Intensity -.73***

TFP -.16***

Wages -1.44***

3 Empirical Model and Results of plant shutdowns

In the previous section we observed that plants which exit have, on average,

different attributes compared with continuing firms. Multinational and foreign owned

plants also appeared to differ from domestically owned plants. In this section we

investigate how the plant-, firm- and industry-level variables affect the probability of

plant exit. We address several hypotheses which include whether ownership, export

orientation, and MNE concentration affect plant exit. Regressions are also conducted to

see how plant characteristics within firms affect exit.

The focus of the research is purely upon the determinants of plant exit, that is,

19

shutdown. We do not have information on switching or M&A activity. Hence, we use a

probit estimator of the form

( ) ( )( )ββx

xxyΨ+

Ψ==

1|1Pr

where ( ).Ψ denotes the cumulative normal distribution.

3.1. Plant, Firm and Industry Characteristics

We begin by looking at how the plant, firm and industry variables affect plant exit.

The first model includes import penetration rather than disaggregating it into the

LWPEN and OTHPEN components. The results are reported in Table 109.

From the regression in this specification, we find that plants which exit are more

likely to be small, have low productivity relative to the industry mean, and have lower

capital intensity. A one standard deviation increase in plant size reduces exit by 0.06

percentage points while the effect is a 0.008 and 0.04 percentage point fall in exit

likelihood when plant capital intensity and TFP increase by the same amount. High

wage plants are more likely to exit: a one standard deviation increase raises exit by 0.14

percentage points.

Dunne et al. (1989), Görg and Strobl (2003), Mata and Portugal (2004) and Bernard

9 The reported results are from a probit estimator. We also estimated for the same regressions by a logit model and the results are quite similar to those obtained from probit estimations.

20

and Sjoholm (2003) also find the probability of exit to be decreasing in plant size.

Bernard and Jensen (2007) observe that surviving plants are larger, more productive

than the average plant and are more capital intensive. Bernard and Jensen (2007) also

find that exiting plants pay significantly lower wages than survivors. This is in contrast

to our findings for Japan.

We split the sample into single- and multi-plant firms and run the regressions again

to see whether the probability of exit differs according to whether the plant is part of a

multi-plant firm or not10. The results show that high wage plants are more likely to exit,

regardless of whether the firm is a single-plant or multi-plant business. In addition, it

does not matter whether we split the sample according to whether firms are

multinationals or not, higher wage plants have a greater probability of exit. However,

high wage plants are more likely to exit if they are part of a multi-plant (0.018 versus

0.005) or multinational firm (0.019 versus 0.006). It could be that we are observing the

influence of off shoring, but the positive sign on wages among single-plant and

non-MNE plants may be due to the effect of import competition or the declining

competitiveness of such establishments in the export market. While plants are more

likely to exit if they are high wage and belong to a multinational, the t-tests in Table 8

showed that within multinational firms, exiting plants had significantly lower wages

than continuing plants.

The firm-level exporter and importer dummies are found to significantly increase

the probability of plant exit. A one standard deviation increase causes a 0.02 percentage

10 Results are not reported here.

21

point increase in exit for both variables. This goes against what other scholars have

found. For example, Bernard and Jensen (2007) find that even after controlling for plant

size, productivity, factor intensity and ownership structure, export status reduces the

probability of exit by 15%. Compared with non-exporters, and conditional on plant

variables, they find exporting firms are 6.8 percentage points less likely to close.

However, as we shall see in later regressions, the exporter and importer dummies are

capturing the influence of MNE status.

Theoretically, it could be the case that multi-plant firms could increase the

probability of exit of their plants by relocating production to another subsidiary plant.

Equally, headquarter services, finance and the industry experience of other

establishments within the group may ameliorate the chance of exit for a plant belonging

to a multi-plant firm. While we find a one standard deviation increase in the multi-plant

variable leads to a 0.10 percentage point increase in exit, the results from other studies

often depend on the country under inspection. After controlling for plant features,

Bernard and Jensen (2007) find that there is no difference in the likelihood of exit for

plants owned by a multi-plant firm in the United States. On the other hand, Mata and

Portugal (2004), and Bandick (2007) find the contrary.

22

Table 10: Plant, Firm and Industry Determinants of Exit

Specification1 2 3

Plant-level Variables

Size -.058*** -.058*** -.057***(-23.22) (-23.03) (-23.21)

Capital Intensity -.008*** -.008*** -.008***(-5.90) (-5.81) (-5.75)

TFP -.041*** -.041*** -.040***(-4.65) (-4.63) (-4.57)

Wages .144*** .145*** .146***(8.82) (8.83) (8.91)

Firm-level Variables

Export Dummy .021** .026***(2.47) (4.08)

Import Dummy .017** .022***(2.15) (3.78)

Multi Plant Dummy .100*** .101*** .101***(16.19) (16.34) (16.62)

R&D Intensity .002*** .002*** .003***(2.70) (2.82) (3.18)

Industry-level Variables

Grubel-Lloyd Index .012 .013 .012(.27) (.28) (.26)

Import Penetration -.137 -.136 -.132(-1.51) (-1.51) (-1.46)

Sunk Costs -.001* -.001* -.001*(-1.80) (-1.80) (-1.80)

Industry Dummies Yes Yes YesTime Dummies Yes Yes Yes

Number of Observations 78315 78315 78315Pseudo R2 .14 .13 .13

Standardised coefficients. z-statistics reported in parentheses***, ** and * indicate significance at at least the 1 percent, 5 percent and 10 percent levels

Firm R&D intensity is found to positively affect plant exit, a finding which runs

contrary to other results reported in the literature (Perez at al., 2004). However, the

effect is conditional on plant-level variables. When these are excluded, plants belonging

to firms with high R&D intensities are less likely to exit, although the standardized

23

coefficient is small.

The Grubel-Lloyd index of intra-industry trade and import penetration are both

found to be insignificant. However, industry sunk costs have a negative effect on plant

exit. This arises because in industries with high sunk costs potential entrants must draw

a high productivity so that they may profitably produce (Melitz, 2003). Consequently

there are fewer successful entrants and competition for market share is diminished. The

reduction in competition means that incumbent firms face a lower chance of exit.

Greenaway et al. (2008) find industry sunk costs to be negatively related with plant exit

among Swedish manufacturers (using the same measure of sunk costs). Using an

industry entry cost measure, Bernard and Jensen (2007) find higher industry sunk costs

reduce exit.

The magnitude of the marginal effects is small. This is in part due to the low exit

rate in the sample (2% of firms). Despite this, the marginal effects for closedown

reported by Greenaway et al. (2008) are similar in magnitude. In this context, the

relative size of each variable becomes important. For example, being a large plant is a

more effective means of survival than being capital intensive. Multi-plant ownership

and high plant wages have the same effect upon exit. Plant- and firm-level variables are

considerably more important in the determination of exit than are industry variables.

3.2. Disaggregating Import Penetration

Previously we saw that industry import penetration did not have a significant effect

24

on plant exit. A potential explanation could be that by aggregating together low-wage

and all other country imports, we were obscuring the effect that each component has on

exit. Low-wage country imports may increase the likelihood of exit since these are

goods which tend to be labor intensive and have a competitive advantage when

competing with the same type of (higher wage) products produced in Japan. In contrast,

OTHPEN may represent goods which are complementary to the production process and

hence reduce the chance of exit.

Disaggregating import penetration into LWPEN and OTHPEN does little to affect

the other variables. All variables remain signed as in Table 10 and they are still

significant. Imports from low-wage countries are not found to significantly affect exit,

nor does import competition from all other countries. It could be that exit is non-linear

in import competition. Imports would then only have an impact on plant survival once

they have captured a significant market share. Across all industries and years, imports

from low-wage countries have a market share of just 3 percent while the figure for

OTHPEN is 8 percent. Although there are some instances where the import penetration

measures account for half of production, the statistics suggest that the fairly low level of

competition from abroad is the reason why Japanese manufacturers are less susceptible

to import competition compared with the United States (Bernard et al., 2007).

25

Table 11: Disaggregating Import Penetration

Specification1 2 3

Plant-level Variables

Size -.057*** -.057*** -.057***(-23.30) (-23.31) (-23.27)

Capital Intensity -.008*** -.008*** -.008***(-5.90) (-5.90) (-5.91)

TFP -.041*** -.041*** -.041***(-4.67) (-4.67) (-4.67)

Wages .144*** .143*** .144***(8.81) (8.79) (8.83)

Firm-level Variables

Export Dummy .020** .020** .021**(2.45) (2.43) (2.46)

Import Dummy .017** .017** .016**(2.21) (2.14) (2.13)

Multi Plant Dummy .100*** .100*** .100***(16.21) (16.21) (16.22)

R&D Intensity .002*** .002*** .002***(2.71) (2.71) (2.70)

Industry-level Variables

Grubel-Lloyd Index .005 .002 .009(.12) (.04) (.20)

LWPEN .022 .009(.87) (.37)

OTHPEN -.123 -.095(-1.61) (-1.32)

Sunk Costs -.001* -.001* -.001*(-1.84) (-1.85) (-1.83)

Industry Dummies Yes Yes YesTime Dummies Yes Yes Yes

Number of Observations 78315 78315 78315Pseudo R2 .14 .13 .13

Standardised coefficients.z-statistics reported in parentheses***, ** and * indicate significance at at least the 1 percent, 5 percent and 10 percent levels

3.3. Foreign Ownership

The issue of ownership often been raised as a potential cause of plant and firm exit.

The issue is important since exit and the loss of jobs impacts upon welfare. Foreign, or

26

multinational, owned plants may be less integrated in the local domestic economy

(because of their vertical or horizontal linkages) so may be more likely to exit when

business conditions deteriorate (Flamm, 1984). They are not as familiar with the

domestic market and its modus operandi as domestic firms are which results in foreign

firms incurring greater sunk costs when entering a new market. Negative shocks may

then have less of an impact on the exit decision since the large costs of entry provide an

incentive to remain active and recoup as much of the fixed costs as possible. Girma and

Görg (2004), Taymaz and Ozler (2007) and Bernard and Sjöholm (2003) all address

whether foreign ownership affects establishment survival and growth, while Mata and

Portugal (2004) look at whether new domestic and foreign owned firms differ in their

chances of survival. We investigate whether foreign ownership, as well as multinational

ownership, affects exit in Japan.

Multinational ownership has also been the centre of empirical and theoretical work.

On the empirical side, Alvarez and Görg (2005) look at whether Chilean multinational

owned plants are more likely to exit relative to domestic plants while Görg and Strobl

(2002) examine whether multinationals are more “footloose” than domestic firms in

Irish manufacturing industries. Theoretically, it is difficult to conclusively state whether

multinationals are more or less likely to shut down plants. While it is conceivable that

multinationals could rapidly relocate production across borders, they may not do so

given the large sunk costs they bear from setting up a new plant. The direction of

causality could go either way depending on the nature of foreign direct investment

(FDI). If FDI is horizontal (as in Helpman, Melitz and Yeaple, 2004), then

multinationals may be less likely to close plants since they serve a target market and

27

have been revealed as preferred to exporting. Instead, it may be vertically integrated

firms that are more likely to close plants since they have explicitly set up operations

abroad which are essential to the final production of a good. They may then be more

sensitive to changes in a plant’s costs of production.

Our dataset permits investigation of the role of foreign ownership and its effects on

plant exit. We also explore whether multinational enterprises are more, or less, likely to

close down plants. To investigate these issues, we re-run the regressions used previously,

but now include dummy variables for foreign and multinational ownership. Foreign

ownership is defined as where a foreign firm holds in excess of 50 percent of the

Japanese firm’s share capital. If this is the case the foreign ownership dummy takes a

value of 1 and zero otherwise. The effect of foreign ownership could be either positive

or negative. Foreign firms are able to relocate production across plants in different

countries and are more footloose. Conversely, foreign firms which come to Japan must

wish to produce for the Japanese market. It is unlikely they would use Japan for export

platform FDI. The foreign firms which do locate in Japan would then be more likely to

remain and keep their plants open.

We define a multinational firm as being one which engages in foreign direct

investment (FDI), through investment and outward loans. If the value of FDI is greater

than zero, the MNE dummy takes a value of 1 and zero otherwise. Using this, and the

foreign ownership variable, we construct dummies for domestic and foreign owned

multinationals. If the firm invests in FDI and is foreign owned, then it is deemed to be a

foreign multinational. Throughout the sample we have 623 observations of plants

28

owned by a foreign firm and 53,328 instances of plants being owned by a multinational.

Of the latter, there are only 74 observations where a plant is part of a foreign MNE.

These figures reconcile with anecdotal evidence of low levels of FDI into Japan.

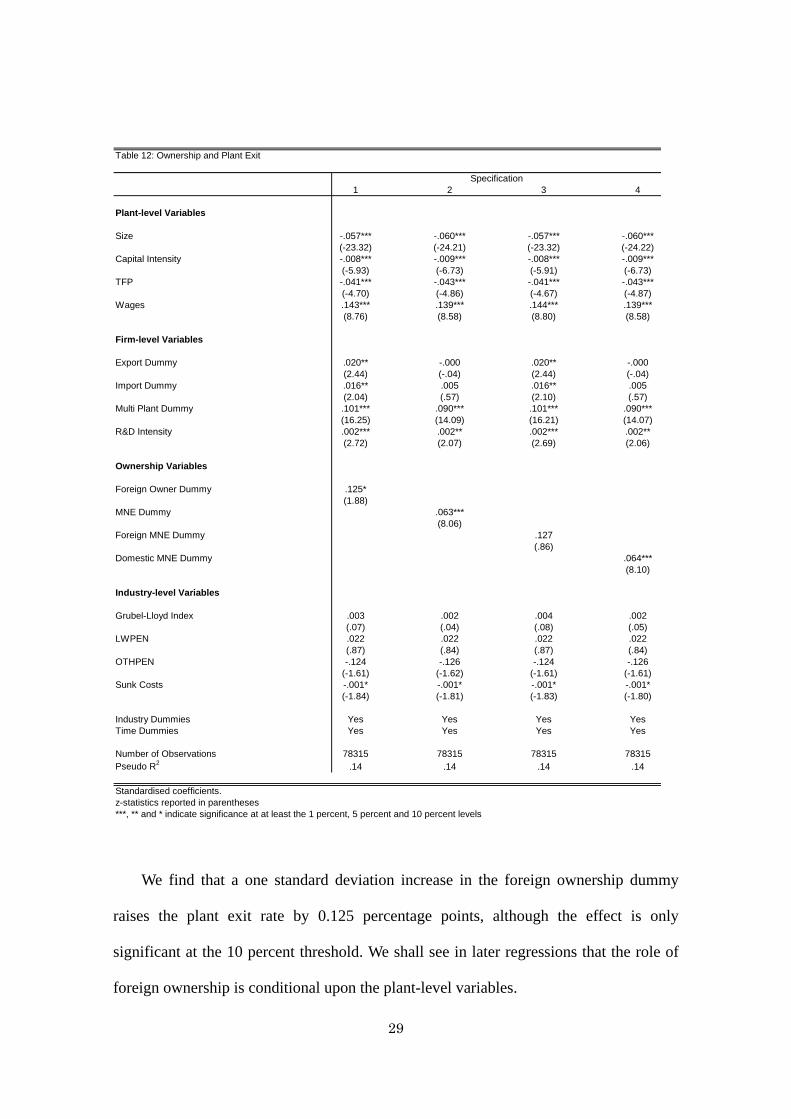

The first column of Table 12 shows the results of the regression when we include

the foreign ownership dummy in the original model. The plant, firm and industry

variables remain identically signed and significant at the same levels as in Table 10.

Foreign ownership is found to be insignificant. This implies that plants with foreign

owners are not footloose and adds weight to the hypothesis that the sunk costs of

entering a foreign market provide an incentive to remain in the face of negative shocks.

29

Table 12: Ownership and Plant Exit

Specification1 2 3 4

Plant-level Variables

Size -.057*** -.060*** -.057*** -.060***(-23.32) (-24.21) (-23.32) (-24.22)

Capital Intensity -.008*** -.009*** -.008*** -.009***(-5.93) (-6.73) (-5.91) (-6.73)

TFP -.041*** -.043*** -.041*** -.043***(-4.70) (-4.86) (-4.67) (-4.87)

Wages .143*** .139*** .144*** .139***(8.76) (8.58) (8.80) (8.58)

Firm-level Variables

Export Dummy .020** -.000 .020** -.000(2.44) (-.04) (2.44) (-.04)

Import Dummy .016** .005 .016** .005(2.04) (.57) (2.10) (.57)

Multi Plant Dummy .101*** .090*** .101*** .090***(16.25) (14.09) (16.21) (14.07)

R&D Intensity .002*** .002** .002*** .002**(2.72) (2.07) (2.69) (2.06)

Ownership Variables

Foreign Owner Dummy .125*(1.88)

MNE Dummy .063***(8.06)

Foreign MNE Dummy .127(.86)

Domestic MNE Dummy .064***(8.10)

Industry-level Variables

Grubel-Lloyd Index .003 .002 .004 .002(.07) (.04) (.08) (.05)

LWPEN .022 .022 .022 .022(.87) (.84) (.87) (.84)

OTHPEN -.124 -.126 -.124 -.126(-1.61) (-1.62) (-1.61) (-1.61)

Sunk Costs -.001* -.001* -.001* -.001*(-1.84) (-1.81) (-1.83) (-1.80)

Industry Dummies Yes Yes Yes YesTime Dummies Yes Yes Yes Yes

Number of Observations 78315 78315 78315 78315Pseudo R2 .14 .14 .14 .14

Standardised coefficients.z-statistics reported in parentheses***, ** and * indicate significance at at least the 1 percent, 5 percent and 10 percent levels

We find that a one standard deviation increase in the foreign ownership dummy

raises the plant exit rate by 0.125 percentage points, although the effect is only

significant at the 10 percent threshold. We shall see in later regressions that the role of

foreign ownership is conditional upon the plant-level variables.

30

Our findings for foreign ownership differ from what has been found in some other

studies. Mata and Portugal (2004) find that once firm characteristics are controlled for,

being foreign does not reduce the chances of exit in Portugal. Taymaz and Ozler (2007)

find that domestic firms have the same survival probability as foreign firms in Turkish

manufacturing industries once establishment characteristics are controlled for (as we

have done through the inclusion of the plant-level variables). Using data on Chilean

manufacturing plants, Alvarez and Görg (2009) find that foreign ownership only has a

positive effect upon plant exit during a significant downturn (the recession in the late

1990s in Chile). On average, they find that foreign ownership does not have a

significant impact upon plant exit.

However, Bernard and Sjohölm (2003) find, for Indonesia, that once the greater

size and labor productivity of foreign plants are controlled for, foreign plants are more

likely to exit. Even when a battery of other variables (such as inputs per employee) is

added to the specification, foreign firms remain 22 to 31 percent more likely to fail than

comparable domestic establishments.

In the specifications of Table 12 we investigate whether multinationals are more

likely to shut down plants. The MNE dummy enters significantly with a one standard

deviation increase raising exit by 0.063 percentage points. That is, if the exit rate was

initially 2 percent, such a change would raise it to 2.063 percent. Our finding indicates

that, in Japan, multinationals are more likely to close plants, even when we condition on

a raft of plant, firm and industry characteristics. Indeed, when we split the MNE dummy

31

into foreign and domestically owned multinationals, we do not find a significant effect

of foreign multinational ownership on plant exit. Rather, it is domestic MNEs which are

more likely to shut down plants with a one standard deviation increase in the domestic

MNE dummy causing 0.064 percentage points more exit.

The results are indicative of foreign MNEs setting up in Japan so they can access

the domestic market. A confounding reason could be that the rules and regulations laid

down by the Japanese government on the production of pharmaceutical products could

be driving the results11. However, the results remain robust to the exclusion of the

pharmaceutical industry from the regression.

Domestic multinationals are significantly more likely to close their Japanese plants.

A potential explanation could be that we are observing off shoring. We shall return to

this hypothesis in a later section when we look at the characteristics of the plants which

multinational-, and domestic-multi-plant, firms shut down.

It has been common throughout the literature to look at the unconditional

probability of exit. That is, are plants more likely to survive, or die, if they belong to a

certain type of firm, regardless of their plant characteristics? We employ two methods to

address this question. We first calculate the probability of exit, depending on ownership

type while holding the plant variables at their means. The figures in Table 13 show that,

for the average plant, which is foreign owned, the probability of exit is 0.0186. Plants

11 In order that a company can sell pharmaceutical goods in Japan, it must produce the drugs within Japan. Foreign firms must then set up production sites in Japan and cannot relocate their operations unless they wish to exit the Japanese market entirely.

32

with multinational owners are relatively more likely to exit than foreign owned plants

with a probability of 0.024. However, since the majority of multinationals in the sample

are Japanese, it is these that drive the result. Domestic multinationals’ plants face an exit

likelihood of 0.024 while for foreign-owned multinational plants the value is lower at

0.014.

The results in Table 13 highlight that once we control for plant characteristics,

domestic multinationals are more likely to close down their plants than foreign

multinationals or foreign owners. However, we are unable to say whether a specific

form of ownership significantly affects exit. To address this we drop the plant-level

variables and run the probit regressions including the ownership dummies. We can then

assess the determinants of exit without conditioning on plant characteristics. Results are

reported in Table 14.

Table 13: Plant Exit Probability and Ownership

Ownership Type

Foreign Owner Probability 95% Conf. Interval

Pr(Exit=1|x) .0186 [0.0100 , 0.0272]Pr(Exit=0|x) .9814 [0.9728 , 0.9900]

Multinational Owner

Pr(Exit=1|x) .0240 [0.0100 , 0.0272]Pr(Exit=0|x) .9760 [0.9728 , 0.9900]

Foreign Multinational Owner

Pr(Exit=1|x) .0140 [0.0038 , 0.0242]Pr(Exit=0|x) .9860 [0.9758 , 0.9962]

Domestic Multinational Owner

Pr(Exit=1|x) .0240 [0.0213 , 0.0267]Pr(Exit=0|x) .9760 [0.9733 , 0.9787]

33

When we omit the plant-level variables, we observe that multi-plant and domestic

MNE firms are more likely to close down their plants, regardless of the characteristics

of their plants. The multi-plant dummy remains positive and significant with a beta

coefficient of 0.091. Unlike in previous regressions, R&D intensity is now negatively

signed which aligns with Perez et al.’s (2004) findings for Spain which shows firms

engaged in R&D to be 57% less likely to fail. Our results point towards R&D playing a

role in attaining, or maintaining, a plant’s competitive edge. Of the ownership variables,

only the domestic multinational dummy has a significant influence on plant survival.

Foreign ownership and the foreign MNE dummy are both found to be insignificant.

34

Table 14: Unconditional Regressions of Ownership on Plant Exit

Specification1 2 3 4

Firm-level Variables

Export Dummy .005 .000 .005 .001(.70) (.03) (.72) (.06)

Import Dummy .002 -.000 .003 .000(.38) (-.01) (.43) (.02)

Multi Plant Dummy .091*** .090*** .090*** .090***(16.77) (15.71) (16.74) (15.76)

R&D Intensity -.001** -.002*** -.002** -.002***(-2.46) (-2.77) (-2.46) (-2.74)

Ownership Variables

Foreign Owner Dummy .082(1.51)

MNE Dummy .014**(2.19)

Foreign MNE Dummy .046(.41)

Domestic MNE Dummy .014**(2.10)

Industry-level Variables

Grubel-Lloyd Index -.006 -.007 -.005 -.006(-.15) (-.16) (-.13) (-.15)

LWPEN .023 .023 .023 .023(1.10) (1.10) (1.11) (1.10)

OTHPEN -.108 -.108 -.108 -.108(-1.56) (-1.56) (-1.56) (-1.55)

Sunk Costs -.001 -.001 -.001 -.001(-1.56) (-1.55) (-1.55) (-1.55)

Industry Dummies Yes Yes Yes YesTime Dummies Yes Yes Yes Yes

Number of Observations 78315 78315 78315 78315Pseudo R2 .06 .06 .06 .06

Standardised coefficients.z-statistics reported in parentheses***, ** and * indicate significance at at least the 1 percent, 5 percent and 10 percent levels

3.4. Firm's Export Orientation

Firms which engage in international trade are perceived to have traits that enable

them to overcome the fixed costs associated with entering a foreign market. Bernard and

Jensen (1995) established that exporting firms in the United States tended to be larger,

more productive and more capital intensive than non-exporters (further evidence is

surveyed in Greenaway and Kneller 2007). In light of these insights we incorporate

35

export status into our regressions since firms which export have ‘better’ characteristics

and may be less likely to close down their plants. We also consider whether plants

belonging to firms that import are less likely to exit. One could imagine that, like

exporting, importing carries sunk costs since a company must make contact with a

supplier abroad, then arrange for the possible customization and transportation of goods.

Importing firms would then be required to have higher productivity, or superior

characteristics, than a domestic firm that does not import.

Given the data available, we are restricted to looking at importing and exporting at

the firm level. We then construct four dummy variables: two-way trader, which takes a

value of 1 if the firm imports and exports, and zero otherwise, export only, which takes

a value of 1 if the firm only exports, import only, which is equal to 1 if the firm only

imports and domestic only which has a value of 1 if the firm neither imports nor exports.

Depending on the type of international trade a firm engages in, its plants are also

assumed to be of that type. We have 44,070 observations of two-way traders, 21580 of

plants which only export, 10,317 for plants that only import and 96,956 observations of

plants which do not trade internationally.

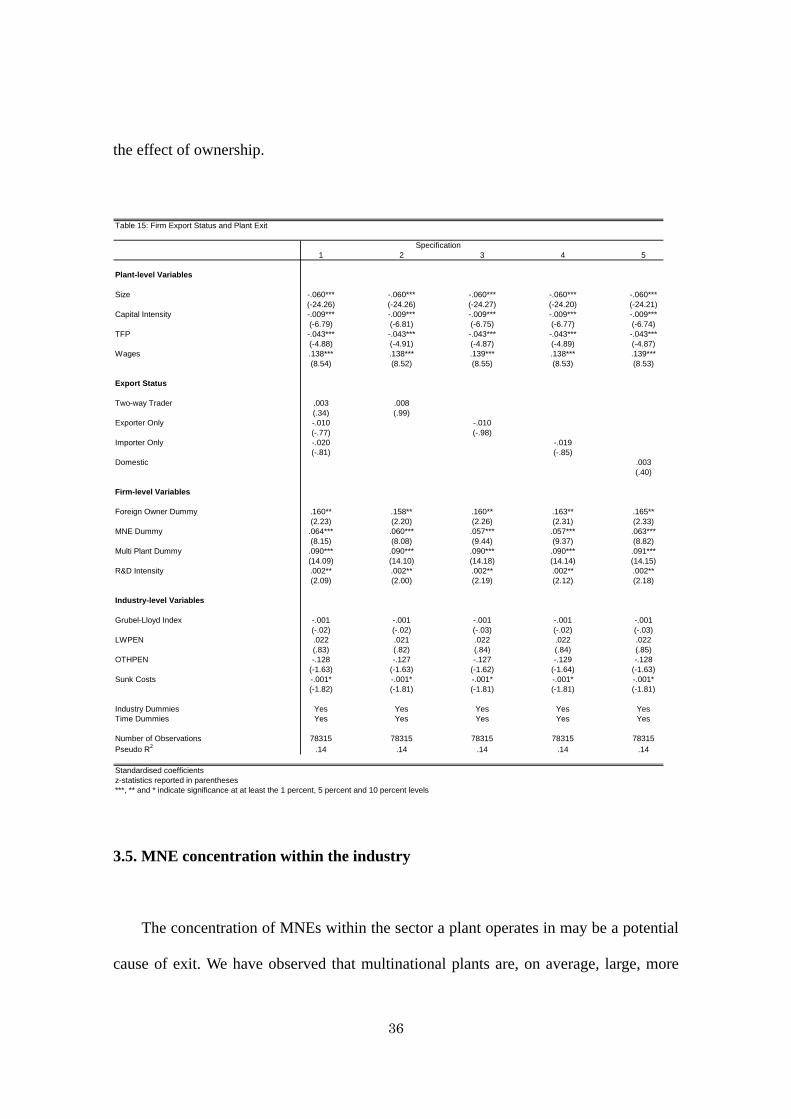

The results in Table 15 show that two-way traders, exporting only and importing

only plants are no less likely to exit than plants which exclusively serve the domestic

market. The plant and firm variables remain the most powerful determinants of exit.

Plants which belong to a multinational, or foreign, owned firm are more likely to exit

but importers or exporters see no difference in exit rates among their plants. The effect

of the firm being an importer, exporter or two-way trader, does not impact on exit above

36

the effect of ownership.

Table 15: Firm Export Status and Plant Exit

Specification1 2 3 4 5

Plant-level Variables

Size -.060*** -.060*** -.060*** -.060*** -.060***(-24.26) (-24.26) (-24.27) (-24.20) (-24.21)

Capital Intensity -.009*** -.009*** -.009*** -.009*** -.009***(-6.79) (-6.81) (-6.75) (-6.77) (-6.74)

TFP -.043*** -.043*** -.043*** -.043*** -.043***(-4.88) (-4.91) (-4.87) (-4.89) (-4.87)

Wages .138*** .138*** .139*** .138*** .139***(8.54) (8.52) (8.55) (8.53) (8.53)

Export Status

Two-way Trader .003 .008(.34) (.99)

Exporter Only -.010 -.010(-.77) (-.98)

Importer Only -.020 -.019(-.81) (-.85)

Domestic .003(.40)

Firm-level Variables

Foreign Owner Dummy .160** .158** .160** .163** .165**(2.23) (2.20) (2.26) (2.31) (2.33)

MNE Dummy .064*** .060*** .057*** .057*** .063***(8.15) (8.08) (9.44) (9.37) (8.82)

Multi Plant Dummy .090*** .090*** .090*** .090*** .091***(14.09) (14.10) (14.18) (14.14) (14.15)

R&D Intensity .002** .002** .002** .002** .002**(2.09) (2.00) (2.19) (2.12) (2.18)

Industry-level Variables

Grubel-Lloyd Index -.001 -.001 -.001 -.001 -.001(-.02) (-.02) (-.03) (-.02) (-.03)

LWPEN .022 .021 .022 .022 .022(.83) (.82) (.84) (.84) (.85)

OTHPEN -.128 -.127 -.127 -.129 -.128(-1.63) (-1.63) (-1.62) (-1.64) (-1.63)

Sunk Costs -.001* -.001* -.001* -.001* -.001*(-1.82) (-1.81) (-1.81) (-1.81) (-1.81)

Industry Dummies Yes Yes Yes Yes YesTime Dummies Yes Yes Yes Yes Yes

Number of Observations 78315 78315 78315 78315 78315Pseudo R2 .14 .14 .14 .14 .14

Standardised coefficientsz-statistics reported in parentheses***, ** and * indicate significance at at least the 1 percent, 5 percent and 10 percent levels

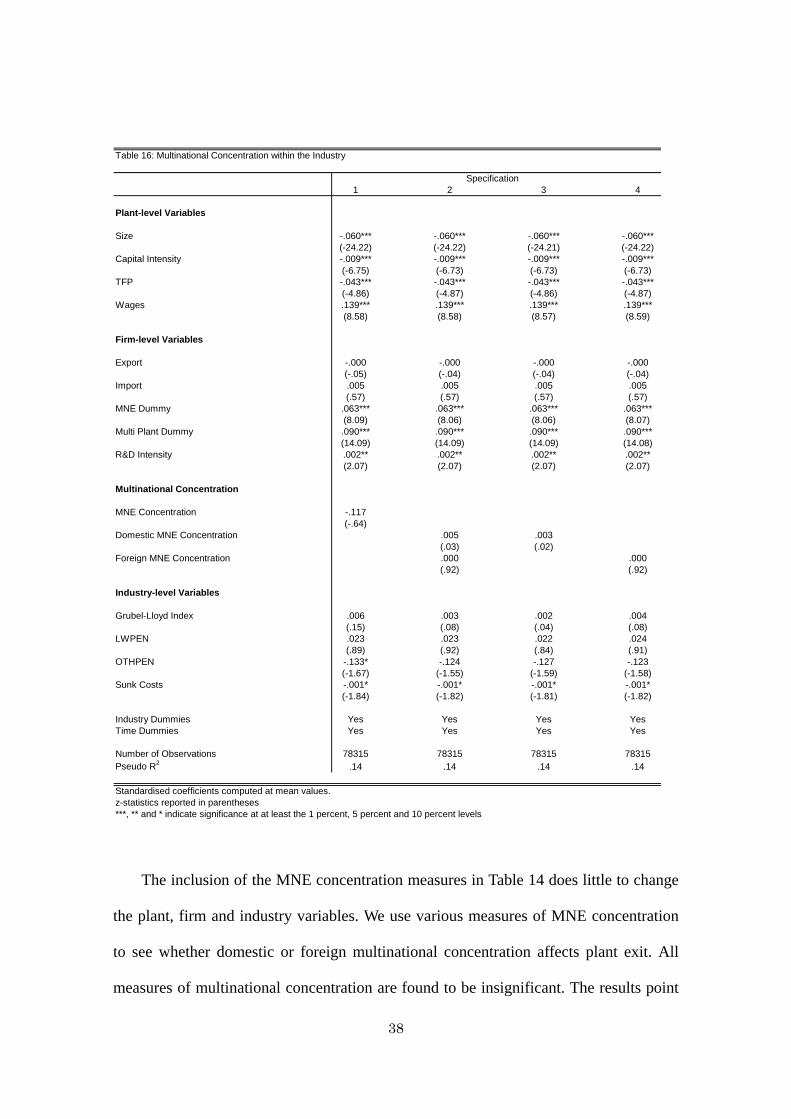

3.5. MNE concentration within the industry

The concentration of MNEs within the sector a plant operates in may be a potential

cause of exit. We have observed that multinational plants are, on average, large, more

37

capital intensive and more productive than domestic plants. They are also backed by a

firm infrastructure which may open new markets and opportunities. Single plant firms

and other non-MNE plants may struggle to survive when confronted by such

competition. To investigate this we include MNE concentration in our regressions using

the following measure

⎟⎟⎠

⎞⎜⎜⎝

⎛=

it

itit EmployeesTotal

EmployeesMNETotalionConcentratMNE_

__log_

where MNE_Concentrationit is the concentration of MNEs in industry i at time t,

Total_MNE_Employeesit denotes the total number of workers employed by

multinationals in industry i at time t and Total_Employeesit denotes the total number of

people employed in industry i at time t.

38

Table 16: Multinational Concentration within the Industry

Specification1 2 3 4

Plant-level Variables

Size -.060*** -.060*** -.060*** -.060***(-24.22) (-24.22) (-24.21) (-24.22)

Capital Intensity -.009*** -.009*** -.009*** -.009***(-6.75) (-6.73) (-6.73) (-6.73)

TFP -.043*** -.043*** -.043*** -.043***(-4.86) (-4.87) (-4.86) (-4.87)

Wages .139*** .139*** .139*** .139***(8.58) (8.58) (8.57) (8.59)

Firm-level Variables

Export -.000 -.000 -.000 -.000(-.05) (-.04) (-.04) (-.04)

Import .005 .005 .005 .005(.57) (.57) (.57) (.57)

MNE Dummy .063*** .063*** .063*** .063***(8.09) (8.06) (8.06) (8.07)

Multi Plant Dummy .090*** .090*** .090*** .090***(14.09) (14.09) (14.09) (14.08)

R&D Intensity .002** .002** .002** .002**(2.07) (2.07) (2.07) (2.07)

Multinational Concentration

MNE Concentration -.117(-.64)

Domestic MNE Concentration .005 .003(.03) (.02)

Foreign MNE Concentration .000 .000(.92) (.92)

Industry-level Variables

Grubel-Lloyd Index .006 .003 .002 .004(.15) (.08) (.04) (.08)

LWPEN .023 .023 .022 .024(.89) (.92) (.84) (.91)

OTHPEN -.133* -.124 -.127 -.123(-1.67) (-1.55) (-1.59) (-1.58)

Sunk Costs -.001* -.001* -.001* -.001*(-1.84) (-1.82) (-1.81) (-1.82)

Industry Dummies Yes Yes Yes YesTime Dummies Yes Yes Yes Yes

Number of Observations 78315 78315 78315 78315Pseudo R2 .14 .14 .14 .14

Standardised coefficients computed at mean values.z-statistics reported in parentheses***, ** and * indicate significance at at least the 1 percent, 5 percent and 10 percent levels

The inclusion of the MNE concentration measures in Table 14 does little to change

the plant, firm and industry variables. We use various measures of MNE concentration

to see whether domestic or foreign multinational concentration affects plant exit. All

measures of multinational concentration are found to be insignificant. The results point

39

towards MNE ownership, and specifically domestic MNE ownership, rather than the

influence of MNEs within the industry being responsible for plant exit.

Non-multinational plants are no more likely to exit when there is an increase in the

concentration of multinationals within the sector they operate.

3.6. Plant Characteristics Relative to the Firm Average

Our dataset matches plant-level information to firm-level data. This allows us to

look within the firm and compare the features of the plants which exit with those that

the firm maintains operational. Specifically, we restrict the sample to multi-plant firms.

We then look at how the plant variables relative to the firm variables differ between

multi-plant MNE and non-MNE firms. Since the plant TFP variable is measured relative

to the sector in which it operates, and firms may have plants in different sectors, we

drop plant TFP from the regressions. The results are reported in Table 17.

Plants that are large relative to the rest of the firm are less likely to exit. The effect

is more pronounced for non-multinational plants. A one standard deviation increase in

the size ratio reduces the likelihood of exit by 0.44 and 0.61 percentage points for MNE

and non-MNE owned plants. In the earlier regressions, plant capital intensity was found

to be a negative determinant of exit. Within multi-plant firms this ceases to be the case.

Relatively more capital intensive plants are less likely to exit, regardless of

multinational status. However, MNE plants that are more capital intensive relative to the

firm are 0.033 percentage points less likely to exit following a standard deviation

increase in the plant-firm capital intensity variable. For non-MNEs the effect is more

40

muted, with a beta coefficient of -0.023.

Previously we had seen that high wage plants were more likely to exit. This

remains true, but only among MNE plants. For a one standard deviation increase in

wages at MNE owned plants relative to the firm, exit rises by 0.12 percentage points.

The same effect is not found among non-MNE multi-plant firms. Plants which pay

relatively higher wages in these businesses are no more likely to exit. The reason for the

differences may be that MNEs can relocate production to low-wage sites abroad and

close their high-wage Japanese plants. Domestic multi-plant firms may relocate workers,

or output, between their plants rather than close them.

41

Table 17: Within Multiplant Firm Exit Regressions

Firm TypeMultinational Non-Multinational

Plant-level Variables

Sizeplant/Sizefirm -.044*** -.061***(-16.53) (-12.32)

Cap Intensityplant/Cap Intensityfirm -.033*** -.023***(8.09) (6.35)

Wagesplant/Wagesfirm .120*** -.026(4.26) (-1.21)

Firm-level Variables

Export Dummy .041 -.051**(1.12) (-2.03)

Import Dummy -.016 -.003(-.80) (-.13)

R&D Intensity -.011*** -.000(-4.05) (-.12)

Industry-level Variables

Grubel-Lloyd Index .021 .112(.18) (.75)

LWPEN .044 .074(.85) (1.07)

OTHPEN -.068 -.781**(-.46) (-2.48)

Sunk Costs -.002* .001(-1.80) (.42)

Industry Dummies Yes YesTime Dummies Yes Yes

Number of Observations 28463 19840Pseudo R2 .12 .11

Standardised coefficients.z-statistics reported in parentheses***, ** and * indicate significance at at least the 1 percent, 5 percent and 10 percent levels

The firm-level variables also reveal that within multi-plant firms, MNE status can

have differing impacts on plant exit. Plants belonging to multi-plant MNE firms which

engage in R&D are less likely to exit. A standard deviation increase in R&D intensity at

the average multi-plant multinational reduces the exit risk by 0.011 percentage points.

R&D intensity does not have a significant effect on plants belonging to

42

non-multinational multi-plant firms.

In earlier regressions we found that the exporter dummy was only ever significant

when the MNE dummy was excluded. Here we find that among non-MNE multi-plant

firms, plant exit is less likely when the firm is an exporter. The result is consistent with

other findings in the literature. Since exporting constitutes domestic firm’s route to the

foreign market, those that export benefit from operating in more markets. They are also

likely more productive relative to firms that only serve the domestic market.

High sunk costs help ameliorate the chance of exit only among MNE plants. This

suggests that MNE plants are established primarily in sectors with higher barriers to

entry, although the effect is only significant at 10 percent. Among domestic multi-plant

firms OTHPEN reduces exit. The same is not true for MNE plants which are unaffected

by this kind of import penetration. Perhaps this is because domestic plants are more

reliant upon imported components while MNE plants can buy components from other

MNE plants within the firm which are located abroad.

3.7. Modeling the Industry Dummies with Industry Variables

So far the industry variables have been picking up within industry variation in

intra-industry trade, import penetration and sunk costs. We now remove the industry

dummies and attempt to model them using industry-level variables. This allows us to

look at how cross-industry variation in the industry variables affects them. In addition to

the four industry variables used previously, we introduce two more: industry capital

43

intensity and industry material intensity.

Industry capital intensity is defined as

( )

( ) ⎟⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜⎜

⎝

⎛

=

∑

∑

=

=N

jijt

N

jijt

it

LabourPlant

CapitalPlantIntensityCapital

1

1

_

_log_

where Capital_Intensityit is the capital intensity of industry i at time t which is

calculated by summing the capital of all plants in industry i during time t divided by the

sum of labor in all plants of industry i during period t.

A measure of industry material (or input) intensity is also included. Material

intensity is defined as

( )

( ) ⎟⎟⎟⎟⎟

⎠

⎞

⎜⎜⎜⎜⎜

⎝

⎛

=

∑

∑

=

=N

jijt

N

jijt

it

SalesPlant

InputsPlantIntensityMaterial

1

1

_

_log_

where Material_Intensityit denotes the input intensity of industry i during time t,

Plant_Inputsijt represents plant j’s inputs at time t in industry i and Plant_Salesijt denotes

plant j’s sales at time t in industry i.

Again we use a probit model and include the plant, firm and all the industry

variables. Seven specifications are run. The first includes all the industry variables while

44

the remaining six include the industry variables one at a time. The plant variables

remain essentially the same as before:

Unlike previously, we now observe that low-wage import penetration has a positive

effect upon exit. This arises from the cross industry variation in LWPEN. The impact is

small with a standard deviation increase raising exit by 0.002 percentage points,

equivalent to about 0.1 percent of the average exit rate. The variable is also only

significant at the 10 percent level when we condition upon the other industry variables.

When LWPEN is included as the sole industry variable in column 3 it becomes highly

significant, but the estimated coefficient remains small at 0.003. In column 4 we see that

across sectors, OTHPEN positively affects exit. Again the effect is due to cross-industry

variation. The result without industry dummies may suggest that exit rises due to the

switching of plants between industries as international trade increases.

45

Table 18: Removing the Industry-level Variables

Specification1 2 3 4 5 6 7

Plant-level Variables

Size -.057*** -.045*** -.057*** -.057*** -.044*** -.045*** -.044***(-20.40) (-19.73) (-19.74) (-19.78) (-19.87) (-19.85) (-20.75)

Capital Intensity -.011*** -.008*** -.011*** -.010*** -.008*** -.008*** -.008***(-7.53) (-7.23) (-8.29) (-8.30) (-7.22) (-6.37) (-6.55)

TFP -.024*** -.017*** -.026*** -.025*** -.017*** -.017*** -.015***(-2.35) (-2.23) (-2.71) (-2.68) (-2.24) (-2.20) (-1.80)

Wages .115*** .083*** .119*** .110*** .082*** .084*** .079***(7.16) (5.51) (7.59) (7.24) (5.49) (5.56) (5.38)

Firm-level Variables

Export Dummy -.004 .005 -.003 -.005 .004 .004 .004(-.48) (.71) (-.38) (-.62) (.60) (.64) (.52)

Import Dummy .010 .006 .009 .009 .006 .005 .007(1.19) (.83) (1.02) (1.10) (.88) (.82) (1.08)

Multi Plant Dummy .090*** .072*** .089*** .090*** .073*** .072*** .072***(13.93) (14.12) (14.09) (14.10) (14.22) (14.22) (14.24)

R&D Intensity .002*** .001** .002** .002* .001* .001** .002**(2.69) (2.08) (2.35) (1.90) (1.94) (1.99) (2.58)

Ownership Variables

Foreign Owner .145** .182*** .140** .136** .181*** .182*** .191***(2.00) (3.18) (2.02) (1.97) (3.19) (3.20) (3.21)

MNE Dummy .060*** .047*** .062*** .063*** .047*** .047*** .045***(7.57) (7.34) (7.79) (8.05) (7.40) (7.31) (6.91)

Industry-level Variables

Grubel-Lloyd Index -.001 .002(-.22) (-.85)

LWPEN .002* .003***(1.82) (3.80)

OTHPEN .002 .005***(1.09) (3.02)

Sunk Costs .000 .001(.21) (.43)

Industry Capital Intensity .002 -.006(.41) (-1.56)

Industry Material Intensity .225*** .211***(3.63) (4.68)

Industry Dummies No No No No No No NoTime Dummies Yes Yes Yes Yes Yes Yes Yes

Number of Observations 78315 78315 78315 78315 78315 78315 78315Pseudo R2 .12 .10 .12 .12 .10 .10 .10

Standardised coefficients.z-statistics reported in parentheses***, ** and * indicate significance at at least the 1 percent, 5 percent and 10 percent levels

Sunk costs and industry capital intensity are found to be insignificant in Table 16.

Each constitutes a measure of the barriers to entry firms face. When industry dummies

were included sunk costs exerted a negative and significant influence upon plant exit. It

appears that sunk costs matter but that they are industry specific. For a one percent

46

increase in industry material intensity exit increases 0.011 percent. Material intensity is

taken to be a proxy for industry profitability. Where more inputs are required in the

production process, the profits firms can make are reduced. The positive coefficient

implies that industries with low profitability see more plants exiting. If we include the

industry dummies, industry material intensity ceases to be significant meaning that the

effect is a cross-, rather than, within-industry result.

4. Productivity Decompositions

So far the analysis has centered upon the determinants of plant exit. We have

established how plant-, firm- and industry-variables affect plant exit. The next step is to

investigate whether plant exit has an effect upon Japanese productivity growth in the

recent years. We specifically ask whether multinational plant exit affects productivity

differently to non-MNE plant exit.

Japanese productivity growth has been notoriously slow in the 1990s. In our sample

we estimate productivity growth across the 51 industries to be 6 percent over the years

1994-2005. A potential explanation of the sluggish productivity growth could be that

firms are off shoring the most productive plants to China and other low-wage East

Asian countries.

To tackle the issue we decompose productivity into four components: within firm

productivity growth, between firm reallocations of market share, entry of new plants

and the exit of existing ones using a modification of the Griliches and Regev (1995)

47

approach. We amend the Griliches and Regev methodology to split the exit component

into MNE and non-MNE parts. The MNE component includes domestic, and foreign,

multinationals. We subsequently decompose the MNE exit component into domestic

and foreign shares. This permits inspection of whether multinationals have been off

shoring their most productive Japanese plants.

Productivity is decomposed using the following method

( ) ( ) ( )

( )∑

∑∑∑∑−−

−−−+−Δ+Δ=Δ

−−

−−

exitMNEnonkitkit

exitMNEkitkit

enrtyitit

betweeniit

withinitit

Pp

PpPpPppP

__

_

θ

θθθθ

where Δ denotes changes over k years interval between the first year (t-k) and the last

year t, itθ is plant i's market share in the given industry at time t, ip is the

productivity of plant i, P is aggregated productivity of the industry and a bar denotes

averaging between (t-k) and t.

The within component represents productivity growth within plants, the between

component constitutes the reallocation of market share across plants in the industry and

the entry component denotes the productivity effect of new plants in the industry. The

exit component is split in two so that we may disentangle the impact of MNE and

non-MNE plant exit on aggregate productivity. Results of the decomposition are

reported in Table 19.

48

Table 19: Griliches and Regev (1995) Productivity Decomposition

Productivity Component Obs Mean

Within Plant 143725 .14

Between Plant 143725 .82

Entry 143725 .01

MNE Plant Exit 143725 .01

Non-MNE Plant Exit 143725 .01

The bulk of productivity growth arose from reallocations of market share from less

productive, to more productive firms. Between firm reallocations of market share

accounted for 82 percent of productivity growth. Productivity growth within plants

accounted for 14 percent of aggregate productivity growth. The entry and exit

components are more modest with values of 1 percent for entry and both forms of plant

exit. The result shows that entering plants enter with above average industry

productivity while exiting plants tend to have below average industry productivity

which points to multinationals closing down less productive plants. This may provide

some evidence that MNEs choose to keep their most efficient Japanese plants open,

rather than move them abroad. Less productive plants are more likely to exit, although

due to the nature of the available data, we cannot say whether they are off shored. Given

that exiting MNE plants account for approximately one third of all exit, we can say that

multinational plant exit has a greater influence on aggregate productivity than non-MNE

exit.

When we classify multinationals as being “domestic” or “foreign” owned, where a

49

plant is deemed to be foreign owned if more than 50 percent of the firm that owns it is

held by foreigners. The results in Table 20 show that it is the exit of Japanese (domestic)

plants which contributes positively to productivity. The exit of foreign plants has

essentially no impact on productivity.

Table 20: Domestic and Foreign MNE Exit

Productivity Component Obs Mean

Within Plant 143725 .14

Between Plant 143725 .82

Entry 143725 .01

Domestic MNE Plant Exit 143725 .01

Foreign MNE Plant Exit 143725 .00

Non-MNE Plant Exit 143725 .01

We elaborate the productivity decompositions in Table 21 and split the within,

between and entry components into MNE and non-MNE parts (the MNE component

again includes all multinationals, domestic and foreign). In general, it is the non-MNE

component of each element of productivity that has a greater bearing on aggregate

productivity. Plant productivity within multinationals is estimated to contribute 4

percent of the growth in productivity while in non-MNEs the contribution is 10 percent.

Likewise, the non-MNE part of the between plant variable accounts for 56 percent of

aggregate productivity growth which is almost double the contribution of the

multinational part.

50

Table 21: Multinational / Non-Multinational Productivity Decomposition

Productivity Component Obs Mean

MNE W ithin Plant 143725 .04

Non-MNE W ithin Plant 143725 .10

MNE Between Plant 143725 .27

Non-MNE Between Plant 143725 .56

MNE Plant Entry 143725 .00

Non-MNE Plant Entry 143725 .01

MNE Plant Exit 143725 .01

Non-MNE Plant Exit 143725 .01

These findings suggest that multinationals may already be more productive than

non-multinational plants (a fact confirmed by t-tests later in the chapter) and that

subsequently, the rate of productivity growth in such plants is slower. It is also evident

from the magnitude of the between plant productivity component that reallocations of

market share across establishments are the prime mechanism which drive productivity

in Japan over the period. However, while reallocations of output towards MNEs are

found to be important, the key effect stems from reallocations of output from less- to

more-productive non-multinational plants. Since multinational plants are, on average,