gold - data.daff.gov.audata.daff.gov.au/brs/data/warehouse/pe_abarebrs99000447/pr11497.pdf · ......

TRANSCRIPT

GOLDAUSTRALIA IN THE WORLD

MARKET

Authors

Chris Allen Taron Brearley Antony Clarke Julie Harman Peter Berry

ABARE Research Report 99.8

© Commonwealth of Australia 1999

This work is copyright. The Copyright Act 1968permits fair dealing forstudy, research, news reporting, criticism or review. Selected passages, tablesor diagrams may be reproduced for such purposes provided acknowledg-ment of the source is included. Major extracts or the entire document maynot be reproduced by any process without the written permission of theExecutive Director, ABARE.

ISSN 1037-8286ISBN 0 642 266 468

Allen, C., Brearley, T., Clarke, A., Harman, J. and Berry, P. 1999, Australiain the World Gold Market, ABARE Research Report 99.8, Canberra.

Australian Bureau of Agricultural and Resource EconomicsGPO Box 1563 Canberra 2601

Telephone +61 2 6272 2000 Facsimile +61 2 6272 2001Internet www.abare.gov.au

ABARE is a professionally independent government economic researchagency.

ABARE project 1527

Foreword

The future direction of the world gold market is of considerable importanceto both the Australian gold industry and the national economy. Gold is nowAustralia’s second largest commodity export, generating nearly $5 billionin annual export revenue and providing an estimated 15 000 direct and 49 000 indirect jobs throughout Australia.

Following substantial falls in world gold prices, ABARE was commissionedby the former Department of Primary Industries and Energy to examine theoutlook for the world gold market in detail, and to focus on other key factorslikely to influence the Australian gold industry over the medium term. Inaddition to developing a medium term outlook for the industry, some esti-mates of the sensitivity of the Australian industry to changes in gold priceshave been developed.

Domestic and international issues — including the nature and scope of bar-riers to international gold trade — that could constrain the Australian goldindustry have been attracting the close attention of policy makers. The scopefor enhancing returns to Australian gold producers by liberalising interna-tional trade in gold and jewellery is examined in this report. In addition, esti-mates of the potential benefits to Australia from removing the main tradebarriers in world markets are provided.

BRIAN S. FISHER

Executive Director

June 1999

iiiAustralia in the world gold market

Acknowledgments

Funding for this project was provided by the Minerals Development Branch,Department of Industry, Science and Resources.

The authors would like to thank their ABARE colleagues who assisted inthe production of this report, particularly Tom Waring for his input to theorganisation and drafting of the report, Nico Klijn for his help with the tariffmodeling and Siobhan Davies for the background analysis of domestic policyissues and exploration trends. Sally Thorpe and Roger Rose also providedhelpful referee comments and suggestions.

The authors also wish to acknowledge officers of the Department of ForeignAffairs and Trade in the main gold importing countries, and the World GoldCouncil who provided up-to-date details on barriers to gold trade. Thanksare also provided to Kamal Naqvi of Macquarie Equities for providing in-sights on the Indian gold market, and to Jessica Cross of Virtual Gold forproviding historical data on the gold leasing market. The authors are alsograteful to the Australian gold producers who provided information abouttheir operations.

iv ABARE research report 99.8

Contents

Summary 1

1 Introduction 5

2 Gold market outlook 7Historical perspective 7Market overview 8Specific market influences 13

3 Australian gold industry outlook 26Industry background 26Factors influencing Australian production 30Australian gold supply projections 39

4 International barriers to gold trade 43Why gold trade barriers exist 43Trade barriers and recent reforms 44Benefits of world gold trade liberalisation 49Other distortions in the world gold market 51Australia’s perspective 52

AppendixesA Projecting Australian gold supply in the medium term 56B Illustrative model – effect on the world gold price of

removing tariffs on gold jewellery imports 69

References 77

vAustralia in the world gold market

Boxes1 Gold stocks and flows 92 Key official sector events with implications for the gold

market 183 Official sector loans and producer hedging 224 Financial liberalisation and gold bullion 46

Figures1 US dollar gold prices 72 Trends in world gold holdings 83 Gold consumption and the mine supply ‘gap’ 104 Net bullion investment and the gold price 155 Composition of official sector gold reserves 176 Net gold sales from the official sector 207 World borrowing and lending of gold 218 Australian gold production, exploration and price 269 World gold production, by region 28

10 Australian exports of gold, by destination, 1996 and 1997 2811 Distribution of major primary gold producers in Australia,

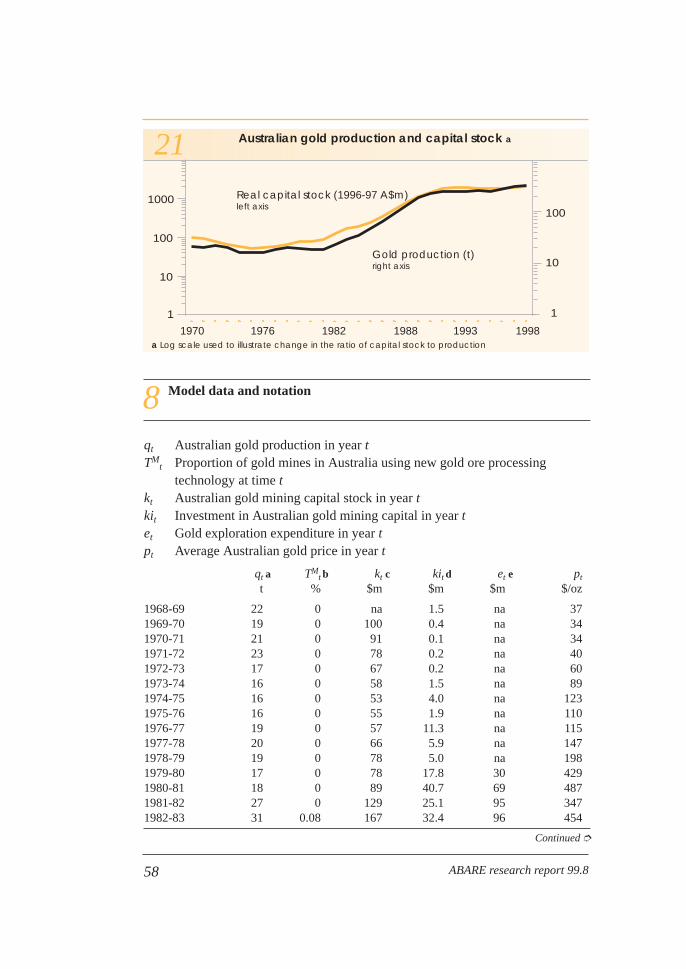

1997 2912 Gold cash margins in Australia 3013 Australian one year forward gold prices 3114 Size and cost structure of the Australian gold industry, 1997 3215 Overseas exploration expenditure by Australian companies 3616 Trends in global gold exploration 3617 Rates of return and effective tax rates for gold mining 3818 Australian gold production – short term 4019 Medium term projections of Australian gold production 4220 Indian gold imports and price premiums 4721 Australian gold production and capital stock 5822 Impact elasticity of a change in the Australian dollar

gold price 6223 Actual and fitted values – production 6524 Actual and fitted values – capital investment 6625 Actual and fitted values – exploration expenditure 67

vi ABARE research report 99.8

Tables1 World gold outlook 112 Gold consumption (per person) in selected countries 133 Economic impacts of Australian gold mining, 1997 294 Major new projects/expansions, 1999–2000 405 Projections of Australian gold production 426 Major international gold import tariffs 457 Estimated changes in the world gold price from the removal

of world gold jewellery import tariffs 548 Model data and notation 589 Diagnostic tests – production 65

10 Diagnostic tests – capital investment 6711 Diagnostic tests – exploration expenditure 6812 Model’s parameter estimates 7313 Model’s initial market conditions 7414 Change in domestic jewellery consumption and prices

following tariff removal 75

viiAustralia in the world gold market

Summary

The global conditions that produced strong growth in the Australian goldindustry during the 1980s have substantially changed. Significantly differentinvestment conditions now face the industry. Rapid growth in the Australiangold sector during the 1980s followed historically unprecedented rises in theprice of gold during the 1970s, and important technological advances in goldore processing in the early 1980s.

A number of factors contributed to the sharp rise in gold prices during the1970s. Most important was the global ‘deregulation’ of the gold market:central banks stopped fixing the price (the gold price was fixed at US$35 anounce from 1934 to 1971) and restrictions on private individuals trading inbullion were largely removed. This freeing up of private gold trade, togetherwith high levels of inflation, led to large increases in private investmentdemand. On the supply side, world mine production began to respond to thehigher prices. Despite gold’s reduced monetary role, central banks generallymaintained their large reserve holdings, allaying fears in the market that theycould become a major source of supply.

After the price increases of the 1970s real prices assumed a declining trendand the structure of the market gradually changed. Jewellery manufacturehas grown to become the overwhelmingly dominant component of golddemand, now accounting for around 90 per cent of annual net gold use. Stronggrowth in jewellery demand and moderate mine production growth haveresulted in an expanding gap between total gold use and mine production —by itself suggesting upward pressure on prices. However, the progressivedecline in real prices in the market largely reflects increasing mine produc-tivity and expanding sales of aboveground gold stocks (from both privateand official sources) to meet this expanding production/use deficit.

The factors underlying the evolution of the gold market over the past twodecades appear set to continue over the medium term. Strong growth injewellery demand over the medium term will continue to reflect rising in-comes associated with sustained economic growth. Mine production contin-ues to be important in the total world supply, but with productivity gainscontinuing, production is expected to respond slowly to easing real prices.As a result, changes in mine production are not expected to be an important

1Australia in the world gold market

influence on the gold price over the medium term. Increasing supply fromcentral banks (through both sales and loans) and private disinvestment areexpected to remain the key supply side price influences into the next decade.

Divestment of official sector gold reserves (through both sales and lendingby central banks) has been a feature of the market over the past two decades,but has accelerated in recent years. Easing real prices for gold, and the avail-ability of higher returns with comparatively low risks from holding basketsof major international currencies, underpin this trend in developed countries.Moreover, recent developments in Europe have resulted in large volumes ofcentral bank reserves that would appear to be ‘earmarked’ for disposal overthe medium and longer term. The likelihood of continued high levels of offi-cial sector sales and low inflation over the medium term underpins ABARE’sassessment that real gold prices will continue their easing trend over mostof the outlook period to 2005.

An important objective in this study was to examine the implications of thisworld market outlook and other factors for the Australian gold industry overthe medium term. In addition to expected world market outcomes, a numberof nonprice factors may affect the Australian industry over the medium term.Qualitative examination of such factors in this study found that they are likelyto be secondary to price in determining the size of the Australian industryover the medium term.

Advances in gold mining and exploration technology have in the past andmay again in the future lead to input cost reductions over the medium term.However, major technological changes are inherently difficult to forecast.Assessments of current research into gold processing suggest that steadyrefinements (resulting in gradual cost reductions) are more likely than majorchanges to the cost structure of the industry over the medium term. Offsettingsuch cost reductions, to some degree, is the likelihood of the average depthof gold mines and the proportion of sulfide ore continuing to increase, therebyraising costs. Other factors influencing the industry in the shorter term includethe hedging behavior of the industry, and the ability of some high cost produ-cers to mine higher grade ore in response to lower prices, tending to increaseoutput in the medium term.

Exploration effort is an important global issue affecting the outlook for theAustralian industry. The risk adjusted returns to gold exploration and miningin Australia compared with available returns in gold exploration investmentelsewhere are under constant review by Australian and overseas companies

2 ABARE research report 99.8

alike. Examination of trends in global exploration suggests that the increas-ing attractiveness of emerging gold producing regions (chiefly South Americaand Africa) has been the major factor behind growing offshore gold invest-ment by gold companies in Australia, the United States and Canada. Thistrend may also reflect the increasing costs and risks of gaining access to landfor exploration and mining in these developed countries, arising from exten-sions to environmental protection and recognition of native title rights.

Although a range of factors will continue to influence investment in Aus-tralia’s gold industry, gold prices are expected to be the major determinantover the medium term. To gain insight into the sensitivity of the Australiangold industry to changes in prices over the medium term, ABARE developedan econometric model of Australian gold supply. This model is based onaggregate historical relationships between gold prices, exploration expend-itures, capital investment in gold mining and gold output. It also incorpo-rates an estimate of the rates at which a new gold processing technology hasbeen adopted in Australia, because this process had a significant effect onindustry output. To develop shorter term industry production forecasts,ABARE undertook a survey of existing gold mines and major planned gold projects.

Both the shorter term surveying and econometric modeling of the Australiangold industry found that Australian gold production is reasonably insensi-tive to changes in the gold price over the shorter term, but that sustainedchanges in the gold price have a substantial effect on production over themedium to longer term. Production in 2010 is projected to be 246 tonnes —around 20 per cent below production in 1998. While major new discoveriesand/or major increases in efficiency may yet sustain output, this projectionlargely reflects the expected continuation of uncertainty in the world marketassociated with the activities of central banks, and industry/investor responsesto the 11 per cent fall in the Australian dollar gold price between 1994 and1998, and a projected further reduction in (nominal) domestic prices of around 18 per cent between 1998 and 2010.

As gold increasingly becomes a widely traded consumer product, the imped-iments to that trade become increasingly important issues for major export-ing countries such as Australia. An important objective in this report is toexamine the potential benefits to Australia from lowering barriers to inter-national gold trade, an issue that the World Gold Council — an organisationrepresenting gold producers worldwide — has raised in the past.

3Australia in the world gold market

Despite gold having one of the more sophisticated commodity markets inthe world, there are a number of restrictions on gold and jewellery trade invarious countries. There are essentially two types of restrictions on inter-national gold trade. First, some countries restrict imports of gold bullion tomaintain additional control over domestic money supply and exchange rates.However, these types of restrictions are not widespread, with most majoreconomies having deregulated their foreign exchange and capital markets.Moreover, as deregulation of foreign exchange and capital markets proceedsaround the world, such restrictions are expected to be progressively removed.

The second major type of gold trade barrier is import restrictions on manufac-tured gold products (mainly jewellery). These are designed to protect domes-tic jewellery manufacturers from world competition. Such restrictions also tendto function as de facto ‘luxury’ taxes on expensive (gold jewellery) imports.

Removal of these barriers to gold trade would produce net economic bene-fits worldwide for all the usual reasons. Liberalisation would enable con-sumers in previously restricted markets to purchase additional gold andjewellery at lower prices, thereby boosting global gold demand. In addition,resources used in protected mining and jewellery manufacturing industriescould be redirected to other more productive uses. Producers of jewelleryand gold in Australia (and throughout the world) would benefit from beingable to provide additional gold to these markets at higher prices.

Although reducing barriers to world gold trade is clearly a worthwhile policyobjective for a major producing country such as Australia, the size of thepotential benefits to gold and jewellery producers may be expected to belimited by the extent to which smuggling currently operates in restrictedmarkets. Another phenomenon that will tend to limit the gains from liberal-isation is the very low value added on jewellery manufacture in some marketsin combination with domestic competition in such manufacturing; this tendsto reduce the effect of tariffs on domestic prices.

ABARE developed an illustrative model of the world gold and jewellerymarket to estimate changes in world gold production and prices that wouldresult from the simultaneous removal of all identified gold jewellery tariffs.It is estimated that removal of all identified import tariffs would result inworld prices increasing by 2–5 per cent, and Australian gold productionincreasing by 4–12 per cent over the long term, other things unchanged.Compared with current levels, this would translate to an additional $230–750million a year in export revenues.

4 ABARE research report 99.8

Introduction

The Australian gold industry has expanded dramatically since 1980. The realvalue (in 1998 dollars) of gold exports increased from $230 million in 1980to $4.0 billion in 1990 and $7.6 billion in 1998. This growth followed higherreal prices of gold in the early 1980s and the development of new gold process-ing technologies (carbon-in-pulp and carbon-in-leach cyanide based process-ing), which increased returns to gold exploration and mining in Australia.The rise in export value also reflects the growing availability of low interestgold loans to Australian producers from central banks since the mid-1980s.

Gold was ranked as Australia’s second largest export sector in 1997-98,accounting for around 11 per cent of Australia’s total commodity exports.The sector also generates significant employment and income throughoutAustralia, accounting for an estimated 15 000 direct and 49 000 indirect jobsin 1997 (ABARE estimate based on Department of Minerals and Energy1997 and Australian Bureau of Statistics 1998b). These benefits generatedby the industry are particularly important to regional areas, where most goldmining operations are located.

However, since the widespread application of new gold processing tech-nologies to Australia during the 1980s, and the introduction of corporatetaxation in 1991, the growth of the Australian gold sector has become increas-ingly affected by world gold prices. The 27 per cent fall in the US dollargold price from January 1996 to January 1998, followed by continuing lowprices, has led to uncertainty about the future direction of the industry —and the wider implications for Australia — if gold prices remain low overthe medium term. The first changes have already occurred, with Australiangold exploration expenditure in 1997-98 seeming to show the first majordownturn for eight years.

As part of the government response to these changes, the former Departmentof Primary Industries and Energy commissioned ABARE to report on keyeconomic factors influencing the outlook for the Australian gold sector overthe medium term. A second requirement was for ABARE to examine thescope for enhancing export markets and returns available to Australian goldproducers through the liberalisation of existing barriers to international goldand jewellery trade.

5

1

Australia in the world gold market

An important objective in this study is therefore to provide a medium termoutlook for both the world gold market and the Australian gold industry. Anoverview of key world gold market influences and recent trends, and mediumterm (to 2005) world gold market projections are presented in chapter 2.Factors influencing Australian gold production and medium term Australiangold supply projections are provided in chapter 3. A simple model of Aus-tralian gold production was developed to examine the sensitivity of futurelevels of Australian gold production to a range of world gold prices, and thushelp the development of medium term projections of Australian gold supply.

Recent attention has focused on barriers to international gold trade (Bannock,Doran and Turnbull 1997). Such barriers may be expected to lower aggre-gate gold demand and thus world prices. There has been no economic analy-sis of the potential effect of international gold trade liberalisation on worldconsumption and the gold price (and thus of the benefits to gold producersworldwide). The nature and extent of impediments to trade, and their impacton global gold trade and export opportunities for Australia, are examined inchapter 4. ABARE constructed an illustrative model of the world gold andjewellery markets to examine the sensitivity of world gold prices to tradeliberalisation, alongside assumptions about the behavior of central banksand private investors.

6 ABARE research report 99.8

Gold market outlook

Historical perspectiveGold is traded globally in relatively unrestricted and competitive markets.However, governments have controlled world gold trade for much of thetwentieth century because gold underpinned mechanisms of internationaltrade. Gold remained linked to the world’s system of international trade until1973 when the major currencies were floated and their link to gold removedfollowing the breakdown of the Bretton Woods System. Reflecting the periodof gold market regulation, the world gold price remained at US$35 an ouncebetween 1934 and 1971.

Following deregulation of the world gold market in the early 1970s, many(mainly developed) countries progressively lifted restrictions on private goldownership. This freeing up of private gold trade, combined with high levelsof inflation, led to rapid growth in gold demand. The apparent ‘freezing’ ofofficial sector reserves increased confidence that the official sector wouldnot become a major source of supply. As a result, gold prices increasedsharply — up from US$42 an ounce in 1973 to over US$600 an ounce in1980 (figure 1).

Average annual gold prices have followed a downward trend since 1980,easing to US$294 an ounce in 1998 (figure 1). This trend reflects gradual

7

2

Australia in the world gold market

US dollar gold prices1

1969 1975 1981 1987 1993 1999 2005

Real (In 1998 dollars)

NominalUS$/oz

600

400

200

800

1000

1200

structural change in the market: on the demand side, the dominance ofjewellery and industrial uses of gold is growing, while on the supply side,substantial gold holdings by central banks and private investors and steadyreductions in average gold production costs are becoming important influ-ences.

Market overview

Recent trendsThe year 1980 is a useful point from which to examine the ‘modern’ goldmarket and apparent trends in the structure of this market. Holdings of goldby the official sector (largely in the form of gold bars) have declined modestlysince that year, while gold use in jewellery fabrication has increased signif-icantly (figure 2). More recently, gold holdings by private investors havealso begun to decline.

An explanation of the different categories of gold stocks, and their influenceon annual flows of gold supply and demand, is provided in box 1.

Declining levels of gold stocks held by investors and the official sector since1980 largely reflect the progressive liberalisation and increased sophistica-tion of world financial markets and, subsequently, lower incentives forgovernments to hold gold as a reserve asset. More recently, this trend hasalso been a response to the associated steady decline in world inflation(Warwick-Ching 1993).

8 ABARE research report 99.8

Trends in world gold holdings2

1980 1983 1986 1989 1992 1995 1998

kt

50

25

75

100

125Other fabricationJewelleryPrivate investment (bullion)Official sector (bullion)

Source: ABARE estimates based on data from Gold Fields Minerals Services (1998), International Monetary Fund (1998) and Warwick-Ching (1993)

9Australia in the world gold market

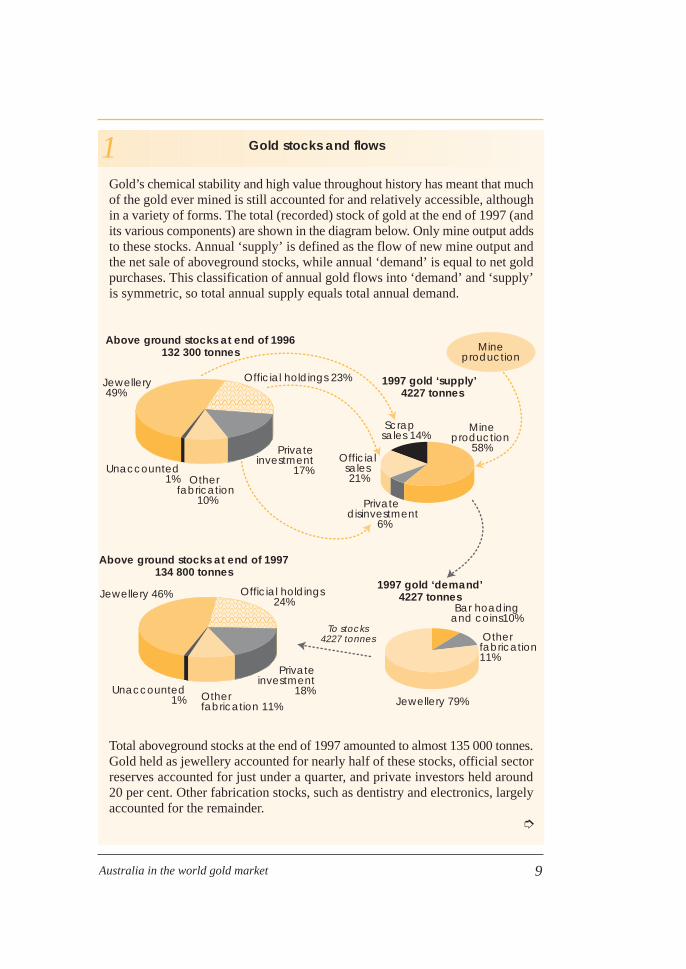

Gold’s chemical stability and high value throughout history has meant that muchof the gold ever mined is still accounted for and relatively accessible, althoughin a variety of forms. The total (recorded) stock of gold at the end of 1997 (andits various components) are shown in the diagram below. Only mine output addsto these stocks. Annual ‘supply’ is defined as the flow of new mine output andthe net sale of aboveground stocks, while annual ‘demand’ is equal to net goldpurchases. This classification of annual gold flows into ‘demand’ and ‘supply’is symmetric, so total annual supply equals total annual demand.

Total aboveground stocks at the end of 1997 amounted to almost 135 000 tonnes.Gold held as jewellery accounted for nearly half of these stocks, official sectorreserves accounted for just under a quarter, and private investors held around20 per cent. Other fabrication stocks, such as dentistry and electronics, largelyaccounted for the remainder.

➮

Official holdings 23%

Private investment

17%

Private investment

18%

Other fabrication

10%

Unaccounted1%

Above ground stocks at end of 1996132 300 tonnes

Above ground stocks at end of 1997134 800 tonnes

Jewellery 46% Official holdings 24%

To stocks4227 tonnes

Other fabrication 11%

Unaccounted1%

Mineproduction

58%

Mineproduction

Private disinvestment

6%

Official sales 21%

Scrap sales 14%

Bar hoading and coins10%

Other fabrication11%

Jewellery 79%

��������yyyyyyyy

Jewellery 49%

����������yyyyyyyyyy

1997 gold ‘demand’4227 tonnes

1997 gold ‘supply’ 4227 tonnes

1 Gold stocks and flows

On the other hand, growth in jewellery demand largely reflects growingpersonal disposable incomes, particularly within developing regions whichtraditionally have high cultural affinities for gold (see Lee 1997). This growthalso reflects progressive gold trade liberalisation (particularly in developingcountries), which has allowed the prospect of owning gold to reach anexpanding number of people, while also bringing domestic gold prices inthese regions closer to the world price. (Chapter 5 contains a detailed over-view of the trend to greater gold trade liberalisation.)

The effect of these trends on the world gold demand–supply balance can begauged from the growing gap between mine supply and total consumption(figure 3). Given the rapid growth in jewellery consumption, world gold

10 ABARE research report 99.8

The ‘mobility’ of gold stocks differs considerably. Stocks of gold held in theform of bullion, such as those held by central banks and private investors, arethe most ‘mobile’ because they can be easily released onto the gold market.Moreover, with the existence of forward markets for gold, the bullion does notnecessarily have to be physically traded. By comparison, stocks of gold held asjewellery are less mobile, as a result of the value added and personal valuesattached to such items, and the costs of recycling jewellery into gold forms thatare tradable in the market. Finally, the least mobile stocks are gold used in otherproducts (such as electronics or dentistry) because there are substantial costsand difficulties with recovery and recycling.

Source: Gold Fields Minerals Services (1998)

Gold consumption and the mine supply ‘gap’3

1987 1990 1993 1996 1999 2002 2005

Total consumption

Mine production

Private disinvestment,scrap and producer

hedging Official sales

t

3000

2000

1000

4000

Source: Historical data from Gold Fields Minerals Services (1998)

1 Gold stocks and flows Continued

consumption over the period 1980–98 increased faster than world gold mineproduction. This implied upward pressure on prices. However, the declinein real gold prices since 1980 suggests that the negative price effect (andassociated expectations) of sales of gold by the official sector and privateinvestors more than offset the positive price influence from strong jewellerydemand.

Medium term outlookThe global macroeconomic assumptions likely to affect the outlook for goldare provided in table 1. In the short term, world economic growth is assumedto decline from a recent high of 4.2 per cent in 1997 to 2.2 per cent in 1999.Over the medium term, world economic growth is assumed to strengthen toaverage 3.4 per cent a year between 2002 and 2005.

11Australia in the world gold market

1 World gold outlook

Unit 1997 1998p 1999 f 2000 z 2001 z 2002 z 2003 z 2004 z 2005 z

Net gold salesMine production t 2 480 2 555 2 560 2 568 2 577 2 577 2 564 2 538 2 508Official sector t 376 412 300 450 600 650 800 900 1 000Scrap t 629 1 098 786 682 753 786 816 841 866Other a t 742 58 215 359 249 300 245 251 263

Net gold purchasesJewellery t 3 342 3 145 3 098 3 272 3 418 3 547 3 658 3 763 3 869Other fabricated

products b t 563 564 574 575 575 576 577 577 578Bullion c t 323 415 190 212 185 190 190 190 190Total sales/

purchases t 4 228 4 123 3 862 4 058 4 178 4 313 4 424 4 530 4 636

Price– nominal US$/oz 331 294 285 285 280 280 280 280 280– real d US$/oz 343 300 285 279 267 259 252 244 237

World growth % 4.2 2.5 2.2 2.9 3.2 3.4 3.4 3.4 3.4

US inflation % 2.4 1.6 2.0 2.0 2.5 3.0 3.0 3.0 3.0

a Includes supply from forward sales, private disinvestment, option hedging and gold loans. b Includes gold used in electronics, dentistry, official coins and medals. c Includes net investmentthrough the physical and paper markets, the repayment of gold loans and net official sector purchases.d In 1999 US dollars. p Preliminary. f ABARE forecast. z ABARE projection.Sources: Gold Fields Minerals Services; ABARE

The changing patterns of gold holding and consumption behavior whichunderpin the easing real price trend since 1980 are expected to continue inthe medium term. (A detailed outlook for the main individual componentsof gold supply and demand are provided in the next section.) To summarise,while the easing trend in real prices is expected to continue over the mediumterm, three important market influences are expected to mitigate substantialreal price falls.

First, the official sectors in developed countries collectively face strong incen-tives to control the rate at which their extensive holdings of monetary goldare sold and replaced with higher yielding alternative reserve assets. Theseincentives stem from the requirements for central banks to maintain inter-national financial stability, and from the prospect of rapid disposal erodingthe prices received and therefore the value of remaining holdings.

Second, consumption of gold for jewellery is expected to continue growingstrongly, in response to lower gold prices and rising incomes in many devel-oping countries that have strong cultural affinities for gold jewellery (notwith-standing the short term financial and economic disruption in Asia).

Third, downward pressure on prices will be moderated to the extent that lowerprices slow the growth of world gold mine output. However, currency depre-ciations in some major gold producing countries and forward sales of gold,together with the gold mining industry’s cost reductions in response to lowerprices, will tend to slow the rate of downward mine supply adjustment.

Overall, a fairly stable flow of mine production, combined with increasingvolumes from official and investment sources, is expected to readily meetforecast strong growth in world demand for gold. However, this outlook ispredicated on substantial and increasing net sales from aboveground sources,particularly from the central banks. For example, ABARE’s projections envis-age net sales by central banks doubling over the next four years, to 800 tonnesa year. A slower rate of disposal, other things being equal, would tend toexert upward pressure on prices.

Periodic market imbalances and shifts in sentiment are likely, resulting inshort term price volatility, but the easing trend in real prices of the past twodecades is expected to be maintained. The real gold price is projected toaverage US$237 an ounce (in 1999 dollars) in 2005, down from US$343 anounce in 1997 and US$300 an ounce in 1998 (table 1).

12 ABARE research report 99.8

13Australia in the world gold market

Specific market influences

The projection of easing real prices is based on expectations that the broadtrends in world gold supply and demand since 1980 will continue over themedium term. The analysis underlying this expectation is detailed below forthe various components of gold supply and demand.

Fabrication demandJewellery fabrication accounts for by far the largest proportion of total worldgold consumption: it comprised around 80 per cent in 1997, up from 56 percent a decade earlier. Jewellery consumption increased at an average annualrate of just over 8 per cent over the past decade. The rapid expansion of therole of the jewellery industry as the dominant user of gold (figures 2 and 3)reflects:

• strong income growth in countries that have high cultural affinities for gold;

• falling real domestic gold prices; and

• the use of gold by consumers as a basic store of value, particularly indeveloping countries.

Other fabrication demand includes the use of gold in electronics, coins andmedals, and dentistry. Combined, these industries used an average 500 tonnesof gold a year over the past decade.However, within this category, theuse of gold in electronics has re-mained fairly stable (at around 200tonnes a year) whereas gold use hasfallen in coin and medal productionand increased in dentistry.

Given differing cultural affinities forgold, income levels, and gold andfinancial market regulations acrosscountries, gold consumption perperson can vary quite significantlybetween countries. Gold consump-tion per person in 1997, for exam-ple, was just 1 gram in the UnitedStates but was 8.2 grams in Italy(table 2).

2 Gold consumption (per person)in selected countries

1985 1990 1995 1997

g g g g

Brazil 0.1 0.1 0.2 0.3China na 0.0 0.2 0.3Egypt 1.2 1.3 1.0 1.2Germany 0.7 1.0 0.9 1.0India 0.2 0.3 0.5 0.8Indonesia 0.2 0.5 0.7 0.7Italy 4.6 6.9 8.0 8.2Turkey 1.5 2.4 2.0 2.5United States 0.8 0.9 0.9 1.0

na Not applicable.Sources: Gold Fields Minerals Services (1998);International Monetary Fund (1998); ABARE.

Fabrication consumption is projected to continue rising to 2005, at an annualaverage rate of 2.6 per cent (table 1). Most of this growth in consumption isexpected as a result of a continuation of recent growth in India and the MiddleEast and, later in the outlook period, growth in a recovering East Asian andSouth East Asia. Consumption in these regions is expected to continueexpanding as incomes grow, particularly if the gold jewellery market is furtherliberalised — such as India’s easing of gold import restrictions at the begin-ning of 1997. (Chapter 5 contains a detailed discussion of gold market liber-alisation and the policy implications for Australia.)

However, currency depreciations in some East Asian and South East Asiancountries have had the effect of increasing the domestic currency prices ofgold. This effect, together with associated lower income growth, is expectedto continue to constrain demand for gold in this region in the first half of theoutlook period. An assumed steady recovery in these economies in the secondhalf of the outlook period, along with the stabilisation of their currencies,will be positive for gold demand.

Investment demand‘Investment demand’ is defined here as net purchases of gold bullion throughboth the physical and paper markets. Purchases of official gold coins andsome jewellery can clearly have investment dimensions, but these productsare not nearly as mobile as bullion because they have intrinsic value (usuallyabove the value of their gold content).

Given that gold bullion is highly mobile, levels of net investment (net bullionpurchases) or disinvestment (net bullion sales) are highly sensitive to changesin the gold price, the strength of the share market, changes in the value ofkey currencies and levels of inflation. Thus levels of bullion investment havefluctuated considerably from year to year. There was no apparent trend inlevels of net investment for 1980–98, although price sometimes appears tohave been linked with levels of such investment (figure 4).

The historical fluctuations in levels of bullion investment suggest that netinvestment demand serves to accentuate changes in the gold price broughtabout through other more fundamental influences, such as changes in levelsof jewellery demand for levels of official sector sales. Thus investmentdemand is not expected to be a major influence on the fundamental trend ingold prices over the medium term. If anything, investment demand isexpected to be a slight net negative influence on the underlying trend in the

14 ABARE research report 99.8

gold price over the outlook period. The assumption of slightly declininginvestment demand is based on the likelihood of low global inflation andinvestor uncertainty about levels of official sales of gold over the mediumterm.

Mine productionThe largest producers of gold are South Africa, the United States, Australia,Canada and China. Over the past decade, these five countries accounted for60–65 per cent of total world gold mine production. However, South Africa’sgold production as a proportion of world output fell over the period — downfrom 35 per cent in 1987 to 20 per cent in 1997 — while Australia’s shareof world gold mine production rose — up from just over 6 per cent to almost13 per cent.

World mine supply accounted for almost 60 per cent of total gold supply in1997, down from an average of 67 per cent in the first half of the 1990s and73 per cent in 1987. This trend reflects lower annual average growth in worldmine production in the 1990s (1.6 per cent) compared with that of the1985–90 period (5.3 per cent) and parallel growth in central bank sales andlending. The slower expansion of gold mining in the 1990s primarily reflectsthe trend in the world price of gold.

Key factors expected to determine future rates of growth in mine supplyinclude trends in gold price and mining costs. Mining profitability and thusthe price of gold will be the main influences on levels of exploration effort.Trends in input costs, improvements in exploration and mining technology,

15Australia in the world gold market

Net bullion investment and the gold price4

1980 1983 1986 1989 1992 1995 1998Investment includes Western investment and bar hoarding in markets outside Europe and the United States (Gold Fields Mineral Services, 1998).

t200

400

600

800

1000

1200

–1001999

US$/oz

100

200

300

400

500Net investmentgold purchases right axis

Gold priceleft axis

and the continuing liberalisation of mining and related laws in developingcountries will also affect the rate of future expansion of gold mining.

However, in aggregate, global mine production is not expected to be a majorinfluence on changes in price over the medium term. This is because a numberof factors are serving to moderate the effect of the recent price falls on worldgold output — for example, world mine supply increased by 4 per cent in1997, despite prices falling by 15 per cent. Over the medium term, worldmine supply growth is projected to continue its easing trend, with gold mineoutput increasing slightly over the next few years before slowly decliningover the later half of the outlook period. World gold mine production in 2005is projected to be around the same level as that in 1998.

The past and expected lagged production response partly reflects scope forhigher cost operators to adjust mine plans to increase average ore grades,lowering per unit costs and raising output (but effectively shortening minelives). It also reflects the significant hedging portfolios held by some keyproducers, and the support of domestic prices received in some producingcountries (such as Australia, Indonesia and South Africa) by currency depre-ciations. Lags have also occurred because operators of higher cost mineshave resisted pressures to incur the disruption and costs of mine closuresuntil they are confident that a significant downturn in gold prices (and theresulting financial losses) will be sustained for a considerable period.

Developing countries, particularly in Asia and South America, are expectedto account for the majority of mine supply growth. The United States,Australia and Canada are projected to maintain gold output at around levelsof the mid-1990s, as output from new and expanded mines offsets produc-tion lost from the closures of depleted and higher cost mines. In contrast,production is projected to ease further in South Africa (still the world’s largestgold producer). That country’s falling gold production, both past andprojected, reflects factors such as progressively lower grades, higher laborcosts and the increasing costs of extraction from deepening mines.

Official sector salesThe pattern of official sector holdings has remained largely unchanged sincethe exchange of gold for US dollars in the official market ceased in 1971(figure 5) (Smeeton 1998). This has occurred despite the gradually declin-ing gold stocks held by governments and other official international organ-isations since 1970. The gradual easing trend in official sector gold holdings

16 ABARE research report 99.8

reflects two opposing factors. First, the incentives for governments to holdgold as a reserve asset have declined considerably in the past two decadesas other reserve asset options have demonstrated their relative attractiveness.Second, despite these incentives, various economic and political constraintsappear to be limiting the pace and extent to which governments lower theirgold holdings.

Gold has had a diminishing role in the world’s international financial systemsince the early 1970s as liberalisation and globalisation of the world’s finan-cial markets have presented governments with a range of strong currenciesto use as reserve assets (Warwick-Ching 1993). These reforms, along withthe increasing economic and political stability of developing nations, havealso lowered the need to hold gold as a ‘war chest’ or ‘asset of last resort’.Further, while the reserve asset options (other than gold) available to centralbanks have been expanding, the value of the banks’ gold holdings has de-clined significantly (in real terms) since 1980. Thus managers of interna-tional currency (and gold) reserves have been under increasing pressure toimprove the returns on their gold holdings (Smeeton 1998).

Lower returns from gold appear to underpin recent growth in official sectorgold sales and lending, but other incentives facing the official sector haveserved to limit the pace and extent of such activity. Perhaps the most power-ful of these influences is the sheer size of official sector holdings in relationto annual supply and demand. Official sector gold holdings equalled around32 000 tonnes in 1997, or equivalent to around thirteen years of annual minesupply. The large volume of official sector gold, along with the market reac-tion to a number of sales in 1997, suggests that the official sector cannot

17Australia in the world gold market

Composition of official sector gold reserves5

1970 1980 1990 1998(September)

kt

15

10

5

20

25

35

30 Other

International organisations

United States

Europe

Source: International Monetary Fund (1998)

18 ABARE research report 99.8

1997

January: The Netherlands announces that it has sold 300 tonnes of its gold inthe previous year.

June: The US Federal Treasury releases a discussion paper analysing the impactsof alternative sales strategies for US Federal Reserve Holdings.

July: Australia and Argentina undertake sales totaling 292 tonnes. Their reservesare exchanged for higher yielding baskets of major currencies.

November: Switzerland and Germany officially enter the gold leasing market.

1998

March: Belgian and Czech central banks announces sales (undertaken on aforward basis) of 299 tonnes and 25 tonnes respectively in late 1997.

May: The Swiss Parliament passes legislation that removes gold backing of theSwiss franc (the last gold backed currency in the world). The Swiss governmentthen proposes to sell around half of the nation’s gold reserves (1300 tonnes). Inearly 1999 Swiss voters approved amendments to the constitution to enable thesesales to proceed.

June: The European Central Bank is formed, leaving around 12 000 tonnes ofgold in EU national central banks with a limited monetary role aside from beinga ‘strategic’ national reserve asset in case of emergencies. It is unclear to whatextent the European Central Bank will regulate any future sales of this surplusby EU national central banks.

1999

March: A former International Monetary Fund proposal to sell 150–300 tonnesof gold to finance debt relief of poor nations (which was rejected in late 1996by Germany) resurfaces, with supportive statements from Germany, France, theUnited Kingdom, the United States and Japan.

May: The UK Treasury announces a plan to sell 415 tonnes (around 60 per cent)of UK gold reserves over the medium term. The Bank of England states thatinitial sales of 125 tonnes over 1999-2000 will be undertaken through a seriesof auctions every two months.

Sources: Macquarie Equities (1997); Gold Fields Minerals Services (1998); World GoldCouncil (1999).

2 Key official sector events with implications for the gold market

quickly dispose of a major proportion of its holdings without pushing downthe gold price received and, equally importantly, the value of its remainingreserves.

Political or even cultural reasons may also underpin government reluctanceto liquidate excess gold holdings. Gold has demonstrated its worth as a usefulreserve asset for governments to hold in times of emergency (such as warand, more recently, the collapse of domestic currencies in Asia) because itsvalue (unlike paper currencies) partly derives from gold’s use as a commod-ity. The United States, which holds the world’s largest stocks of bullion (8200tonnes), continues to maintain a policy of not lending or selling any of thisbullion to the market.

Constraints on official sector activity in the market undoubtedly remain, butthe recent acceleration in gold lending and selling by the official sectorsuggests that overall they are becoming less important. It appears that 1997and early 1998 was a watershed period for defining change in the attitudeand behavior of central banks. This is evidenced by the number and volumeof significant official sector sales and loans, and by other announcements onthe gold policy of the official sector (box 2).

Particularly important were: the Australian and Argentine sales, in whichthe two governments replaced their gold holdings with other governmentsecurities; announcements by the Swiss and German governments of theextent of their gold lending activity; and the release by the US Board ofGovernors of the Federal Reserve System of a discussion paper examiningalternative sales strategies for US gold reserves (Henderson et al. 1997).

More recently, the European Central Bank (established in June 1998) an-nounced that it will hold 15 per cent of its reserves as gold. This representsa share for gold that is well below that generally held by European centralbanks. In effect, it leaves a substantial tonnage notionally ‘surplus’ to therequirements of EU central banks.

The market is presently uncertain about the European Central Bank’s poli-cies for the regulation of gold selling and lending activities by individualcentral banks in the European Union. The nature and strength of these poli-cies are expected to ultimately affect the amount of gold that the EuropeanUnion sells onto the market (in exchange for other monetary assets); theywill probably also affect the manner by and rate at which member countriesconduct such sales.

19Australia in the world gold market

The recent higher rate of official sector net sales (figure 6) is likely to continueover the medium term. This direction is indicated by: the Swiss plan to sellaround 1300 tonnes; the relatively small proportion of gold held in theEuropean Central Bank; the recent proposal by the International MonetaryFund to sell up to 300 tonnes to finance debt relief of poor nations; and therecent announcement by the UK Treasury that it intends to sell 415 tonnes(over half their gold reserves) over the next three years. However, futurelarge scale official sector sales may increasingly occur in a more orderedand transparent fashion, as indicated by the recent UK proposal in which aprogram of future gold auctions was provided to the market (box 2).

Those central banks with the largest holdings of gold appear to have a strongincentive to refrain from major sales over short time periods, but this is notnecessarily the case for central banks with smaller holdings. In 1997 eighteencentral banks had holdings of 100–500 tonnes, accounting for a total of over3200 tonnes (International Monetary Fund 1998). These central banks withsmall to medium sized gold holdings may be less likely than banks withlarger holdings to sell in a gradual and transparent manner. This is becausethey may have a greater chance of obtaining higher prices by pursuing a ‘sellfirst and announce later’ strategy. Thus their future selling behavior is, atbest, a significant uncertainty and, at worst, a negative risk factor facing themarket over the medium term.

Official sector lending and producer hedgingWhile official sector sales have been the focus of popular attention and haveincreased gradually since 1980, official sector lending has increased dramat-

20 ABARE research report 99.8

Net gold sales from the official sector6

1988 1990 1992 19961994 1998

kt

15

10

5

20

25

30

Source: Gold Fields Minerals Services (1998)

ically during the 1990s. From an estimated 600 tonnes at the end of 1988,official sector gold loans to the market increased to over 3800 tonnes by theend of 1997 (figure 7). Most of this increase was effectively borrowed byproducers to finance their gold price hedging transactions.

As with outright sales, the increase in gold lending activity by the officialsector over the 1990s reflects globalisation of the world’s financial marketsand the resulting pressures on central bankers to improve the return on theirgold holdings (Smeeton 1998, p. 255). However, unlike sales, lending enablescentral bankers to derive a return on the asset while retaining ownership.This difference, along with the apparent market and nonmarket constraintsfacing official sector sales (described above), perhaps explains why officialsector lending has increased by far more than official sector sales (figures 6and 7).

As noted above, most gold loaned to the market by the official sector isborrowed by producers to finance hedging transactions (figure 7). Gold pricehedging is the process whereby producers reduce their exposure to the riskof lower gold prices, using mechanisms such as forward sales contracts andoptions. The manner in which borrowed gold (or liquidity) from the officialsector is used to finance forward sales (the most common form of hedgingused by gold producers) is explained in box 3.

A producer effectively borrows gold from the official sector (through anintermediary), then sells the gold to obtain the current spot price and investsthe proceeds in an interest bearing account. The producer subsequently paysback the official sector gold loan (plus interest in the form of additional gold)

21Australia in the world gold market

World borrowing and lending of gold7

1989 1991 19951993 1997Source: Gold Fields Minerals Service (1998)

kt

–5–4–3

–2–1

34

21

��������

����

���

�����

����

���

��

������

����

�������

������

�Borrowing for producer hedgingOther borrowing

Official sector lendingPrivate lending

22 ABARE research report 99.8

The acceleration of producer hedging during the 1990s has been made possibleby the increase in gold lending by the official sector (figure 7). The manner inwhich official sector gold lending (or liquidity) is used to finance a gold forwardsale (the most common form of hedging used by producers) is shown above. Aforward contract provides an agreement between gold producers and the writerof the contract to deliver a certain quantity of gold at an agreed price before aspecified date.

First, gold loaned by the central bank to an intermediary (a bullion bank) for theforward sales is sold onto the spot (immediate delivery) market by the bullionbank, and the proceeds are invested in an interest bearing account. At the endof the transaction, gold from the producer is sold to the bullion bank at thecontracted forward price. The bullion bank then repays the central bank with anamount of gold equal to the amount borrowed plus interest (Gold Fields MineralsServices 1996).

The forward premium over the current spot gold price reflects the differencebetween the rate at which central banks are willing to lend gold to producers forsuch transactions, and the interest rates available on cash deposits, referred to

($)

Source: Gold Fields Minerals Services (1996)

Gold market

delivers gold(Au)

lends gold(Au)(Au)

returns gold(Au + LR)

Central bank

Bullion bank

Producer

Interest earning account closes

account($ + int)

pays producer($ + int – LR – LF)Au = physical gold

$ = cashint = interest earned on cash depositLR = gold leasing rateF = bullion bank fee

= start of forward sale= end of forward sale

3 Official sector loans and producer hedging

from mine production on the delivery date specified by the contract. Theeffective forward price received by the producer derives from the differencebetween the rate at which central banks are prepared to loan gold to produc-ers for such transactions, and the market rate of interest that producers canobtain from investing the proceeds for the duration of the contract (box 3).

The twelve month gold lease rate (representing the market rate at whichcentral banks are willing to lend gold to producers for hedging) averagedaround 1.6 per cent from 1990 to mid-1998, while twelve month world indi-cator borrowing rates (US dollar LIBOR) averaged around 6 per cent (VirtualGold 1998). The substantial difference between leasing rates of gold andborrowing costs of dollars is unusual, because leasing rates for other metalcommodity markets in competitive equilibrium are forced (through arbitrage)

23Australia in the world gold market

as the ‘contango’. The attainable forward price of gold increases with the spotprice of gold, the contango and the duration of the contract.

Producers are not restricted to delivering their mine production against theforward contract, because there are usually mechanisms (depending on the typeof arrangement) by which producers can close out the forward contact and takea profit or loss (Gold Fields Minerals Services 1996).

Another instrument used by producers to hedge against price falls is gold ‘put’or sell options. These provide producers with the right (but not the obligation)to sell a specific quantity of gold at an agreed price before a specified date.However, the grantor of these options (usually a bullion bank) undertakes forwardselling to hedge against the risk of the option being exercised when the strikeprice is above the spot price. This process is referred to as ‘delta hedging’ (Cross1994). Options therefore have an effect similar to that of producer hedging interms of accelerating supply onto the market as forward sales (through thehedging activities of the option counterparties). As reflected in high contangosfor forward prices, the availability of options at ‘low’ prices to producers reflectsincreasing official sector liquidity to finance these transactions.

Hedging through instruments such as forward sales agreements can reduce pricerisk but it will always involve some risk to the producer. If a producer undertakesa forward agreement to deliver a specific quantity of gold for a certain price ata future date, the producer may be unable to benefit from any future rises in theprice of gold (Grieg 1997). Similarly, when producers buy put options, the optionprice includes a premium (above the intrinsic value of the option, were it to beexercised); thus the reduction in downward price risk for the buyer of a putoption comes at a price.

3 Official sector loans and producer hedging Continued

24 ABARE research report 99.8

to a rate around cash interest rates, depending on the change in the lender’scosts of storing and transporting the commodity.

Official sector gold lending has almost exclusively been directed to goldproducers and not to speculators (figure 7). These patterns in lending andthe historically low interest rates for gold lending suggest that the officialsector, in limiting its lending to producers for hedging purposes, has obtaineda below-market rate of return. This low rate of return also reflects the rela-tively small size of demand for nonspeculative forms of borrowing (mainlyhedging by producers and fabricators) relative to the potential size of goldstocks available for lending.

Effect of hedging on the world marketGiven that the gold loaned by the official sector for a producer forward saleis immediately sold on the spot market (then later repaid to the central bankfrom mine production), this activity effectively brings forward mine supplyto the market. However, if in the future the central banks return gold loansto their vaults as they are repaid without undertaking new loans, there wouldbe a relative reduction in supplies to the market (compared with what wouldhave occurred without forward selling).

This ‘drawback’ of official sector loaned gold, in net terms, has not yetoccurred, with net lending to the market for producer hedging increasing inthe 1990s (figure 7). Further, with lending continuing to expand, no signif-icant drawback is envisaged over the medium term.

Another implication of the official sector providing producers with signifi-cant forward price premiums has been that the profitability of gold mininghas increased above the level that would have been achieved given the declinein real gold prices since 1980. Thus, in addition to the direct effect of accel-erating supply described above, the loaning activity of the official sectormay be sustaining higher levels of gold production than would occur other-wise. This also serves to sustain downward pressure on world gold prices.

Outlook for official sector lending and producer hedgingThe supply of official sector gold lending is forecast to continue to increaseto 2005. Both the Swiss and German central banks officially entered theworld gold leasing market in 1997; together, these countries held around5550 tonnes of gold (more than the 3800 tonnes of official sector gold onloan to the market at the end of 1997). Further, if the evolving policies ofthe new European Central Bank tighten the flexibility of the EU central banks

to sell their gold reserves, EU central banks may have further incentive toloan more of their reserves as an alternative to disposal.

Increasing gold lending by the official sector over the medium term isexpected to be associated with sustained producer hedging and, therefore,continued high levels of supply onto the market from that source. Theseeffects will tend to depress prices. However, demand for producer hedgingmay decline in the medium to long term as mine production declines andthus ore reserves available for hedging decrease. On balance, producer hedg-ing is likely to remain a net negative influence on gold prices over the mediumterm, although the size of this influence is expected to decline as world mineproduction falls.

25Australia in the world gold market

Australian gold industry outlook

The gold industry, Australia’s second largest export industry, is consideringthe implications of the substantial falls in the world gold spot price in the pasttwo and a half years and continuing uncertainty in world markets. Given thiscritical period for the market and for the development of the Australian indus-try, it is timely to look at the likely direction of the industry over the next fiveyears and beyond in terms of profitability, exploration and production.

This chapter is divided into three sections: first, a general overview of theAustralian gold industry and recent trends; second, the major factors likelyto affect Australian gold production levels over the medium to longer term(including Australia’s relative attractiveness as a location for gold explo-ration and mining); and finally, projections of Australian gold mining produc-tion.

Industry backgroundThe Australian gold industry has expanded rapidly in the past fifteen years,with the value of exports rising from $270 million in 1983 to $4.91 billionin 1997. This rapid growth followed high real prices of gold during the early1980s (figure 8). Higher gold prices reinforced the positive impact of thedevelopment of new gold processing technologies, the absence of companytaxation on gold mining, and the availability of attractive gold loan facilities.

26

3

ABARE research report 99.8

Australian gold production, exploration and price8

1977 1980 19861983 1989 1992 1995 1998

0

200

400

600

800

1000

1200

t

50

100

150

200

250

300Gold price1998 A$/oz

Exploration1998 A$m

Productionright axis

The advent of carbon-in-pulp and carbon-in-leach cyanide based recoveryprocesses in the early 1980s enabled profitable mining of gold at much lowergrades. Moreover, this technology is particularly well suited to shallowoxidised gold deposits, which are relatively common in Australia as a resultof the extensive weathering of the continent. Thus, with high real prices,new technology, a favorable taxation regime and available development fund-ing, exploration activity and gold production rose significantly in the secondhalf of 1980s.

Following the rapid rise in Australian gold output in the 1980s, growth inthe first half of the 1990s was negligible. The slowing production growthwas linked with a period of declining exploration activity between 1989 and1992 (figure 8). The downturn in exploration activity appears to have partlyreflected the sharp fall in the Australian dollar gold price in the period1988–92. Other significant contributors to the slowdown in industry growthin the early 1990s were the stock market crash of late 1987 (coinciding withthe fall in the world gold price), which reduced the availability of equityfunding for a period, and the introduction of corporate taxation for goldmining companies in 1991.

After 1995, gold production again increased rapidly, with output rising sharplyin 1996, 1997 and the first half of 1998. The recent production increase is alagged response to a modest upturn in the Australian dollar gold price in1993 and sustained high prices until mid-1996. Exploration expenditure rosein response, increasing at an annual average rate of almost 16 per cent in theperiod 1992–97.

The industry todayAustralia is currently the world’s third largest gold producer, after SouthAfrica and the United States (figure 9), and accounted for an estimated 13 per cent (around 314 tonnes) of world gold mine production in 1997.Approximately 342 tonnes of gold were exported in 1997. The differencebetween exports and production reflects re-exporting of gold imported forprocessing (primarily from gold mining operations of Australian firms inthe Asian region and from imports of gold scrap from Asia).

The bulk of Australia’s gold production is exported as bullion, of which mostis shipped to Asian markets (figure 10). However, following the recenteconomic problems in Asia, some output is being diverted to regional marketsin Europe and the Middle East.

27Australia in the world gold market

Given the increase in economic activity in the gold sector, flow-on effectsto the rest of the Australian economy (such as the generation of indirectemployment and output) increased in the 1980s and the second half of the1990s. Using input–output multipliers for the Australian economy (AustralianBureau of Statistics 1997), it is possible to derive estimates of the direct and indirect output and employment effects of the Australian gold industry(table 3).

Most of Australia’s gold mining operations are located in remote areas ofAustralia (figure 11). Thus the industry is indirectly important to regionalincome and employment opportunities in those areas. Also, most ofAustralia’s gold mines (figure 11) are located in Western Australia: in 1997,that state accounted for 76 per cent of Australia’s gold mine output, while

28 ABARE research report 99.8

World gold production, by region9

1988 1989 19911990 1992 1993 1994 1995 1996 1997

t

500

1000

1500

2000

South America

Asia (including China)Australia

South Africa

United States

Other

Source: Gold Fields Minerals Service (1998)

Australian exports of gold, by destination, 1996 and 199710

South Korea

Singapore

1996

1997

HongKong

ThailandMalaysiaOtherJapanSwitzer-land

UnitedKingdom

A$b

1.5

1.0

0.5

2.0

2.5

Queensland, the Northern Territoryand New South Wales accounted for9 per cent, 8 per cent and 4 per centrespectively, and Victoria, Tasmaniaand South Australia combinedaccounted for around 3 per cent.Most of Australia’s gold productioncomes from a relatively small num-ber of large mines, and numeroussmall scale operations contributelittle to total output. Australia’s top20 per cent of mines (by size) pro-duced an estimated 60 per cent ofproduction in 1997, while thebottom 20 per cent of gold minesaccounted for less than 1 per cent(figure 11).

29Australia in the world gold market

3 Economic impacts of Australiangold mining, 1997 a

Gross value of production Employment

Direct s $5 billion 15 000

Indirect $8.5 billion 56 000

a Type IIB full time employment and outputmultipliers from Australian Bureau of Statistics(1997). Input–output multipliers are based onaverage (not marginal) effects, so they tend tooverstate indirect economic effects (AustralianBureau of Statistics 1996, p. 24). Thus the valuesshown here are only indicative, not absolute. sABARE estimate.

Distribution of major primary gold producers in Australia, 1997Based on ounces of gold produced11

Mine

Share of Producer Production Australian quartile range output

% 000' oz/year %20 0–15 140 15–40 660 40–75 1480 75–130 23100 130–680 56

Factors influencing Australian production

Like other major world gold producers, Australia produces an annual outputthat is modest compared with annual global supply (13 per cent) and negli-gible in its share of aboveground bullion stocks. Australia’s relatively modestcontribution to total market global supply means that Australian producers(like their overseas counterparts) have no ‘market power’ over world goldprices (Sjaastad and Scacciavillani 1996, p. 887).

Australian gold producers therefore seek to maximise profits from miningsubject to a number of constraints, including current and expected futureworld prices, mining costs and Australia’s attractiveness for gold miningrelative to other locations.

Returns to gold mining in AustraliaAustralia’s real gold cash margins (real price less real cash costs) have exhib-ited a declining trend in recent years (figure 12). The US dollar gold priceis forecast to remain low in 1999, averaging US$285 an ounce. Reflectingan assumed stable exchange rate in 1999, the Australian gold price is alsoexpected to remain steady across the year, averaging A$437 an ounce.

Over the medium term, the real US dollar gold price is forecast to fall, whilethe Australian dollar is forecast to strengthen against the US dollar. Theseassumptions underpin the projection that the Australian gold price will fallover most of the outlook period to average A$317 an ounce (in 1998 Aus-tralian dollars) in 2005 (figure 12).

30 ABARE research report 99.8

Gold cash margins in Australia12

1985 1990 2005

200

1998A$/oz

800

600

400

1995 2000

Price

Cash cost

Gold revenuesThe Australian dollar price represents the notional price that Australianproducers receive, but the effective price received by producers has gener-ally been somewhat above the prevailing spot price in recent years. This hasresulted from the industry’s extensive use of forward sales and other hedg-ing techniques. Over the period July 1990 to June 1998, the monthly oneyear forward price (that is, the price that producers could contract to deliveragainst in twelve months) was estimated to average A$531 an ounce (figure13). (This forward price was estimated using ‘GOFO’ one year lease ratesas quoted by Reuters [Virtual Gold 1998] and the Reserve Bank of Australiaone year bond rate.) This compares (for each of these months) with an aver-age spot price at maturity of A$489 an ounce.

The existence of this significant premium, along with the extensive use ofhedging by Australian gold producers, has enabled significantly greaterreturns than would have been realised at the prevailing spot prices. Lonergan(1997) estimated that 40 per cent of before-tax profits of Australia’s top 20 gold producers was attributable to hedging activities in 1995, rising to 60 per cent in 1996.

Official sector gold lending at low rates of interest for producer hedging isexpected to continue to expand over the medium term (see chapter 2). Giventhis behavior of the official sector, and the relatively small proportion of goldborrowing in relation to total consumption, the forward premium over spotprices available to producers (as seen over the past decade) is expected tocontinue.

31Australia in the world gold market

Australian one year forward gold pricesMonthly13

July1990

June1991

June1992

June1993

June1998

June1994

June1995

June1996

June1997

Spot

Forward600

500

400

A$/oz

However, the trend in the forward price attainable by producers is alsosubstantially influenced by the price impact of market fundamentals. RealAustralian gold prices are projected to decline by around 18 per cent overthe outlook period to 2005, thus attainable forward prices can also be expectedto decline.

Gold industry costsSpot and forward prices have significantly influenced the cash marginsachieved by Australian gold producers in recent years, but changes in realcosts have played a relatively minor role in determining changes in margins.Having declined modestly over the period (figure 12), real cash costs areexpected to continue an easing trend (in line with real prices over the outlookperiod). However, in addition to responding to pressures from easing realprices, Australian cash costs will also respond to changes in technology, deci-sions on ore grades, and geological conditions.

It is likely that the falling real costs (figure 12) largely reflect continualimprovements in the application of carbon-in-pulp and carbon-in-leach pro-cessing technology since its introduction to Australia in the early 1980s, andthe more recent contraction in Australia’s high cost gold mining activitiesin response to lower real prices. Higher cost mines in Australia tend to besmaller sized operations (figure 14).

This trend is expected to continue over the medium term, with prices fore-cast to remain low. A recent study of the Western Australian gold industry(Greig 1997) found that the top 25 per cent of producers in that state hadaverage reserve–production ratios of eleven years, compared with five years

32 ABARE research report 99.8

Size and cost structure of the Australian gold industry, 199714

100 90 80 70 60Producer decile

50 40 30 20 10

Proportion of total output produced by decile

Production cost of producer decile 25

20

30

15

10

5

250

200

300

150

100

50

%US$/oz

for the rest of the mines. Bigger mines also typically have a larger propor-tion of their anticipated future production sold forward using hedging mech-anisms (such as forward contracts and option strategies). This difference islikely to partly reflect the significant treasury costs involved in building andmaintaining sophisticated hedge portfolios.

The lower hedging levels and smaller reserve–production ratios of smallerproducers, in addition to their higher costs (on average), are likely to resultin faster closures of smaller operations in response to lower prices.

The industry has also reduced costs by amalgamating gold mining opera-tions within close proximity. The Australian gold industry has undergone asignificant degree of ‘regional centralisation’ in recent years, and the numberof companies within specific gold mining regions has decreased sharply.Only two of the previously twenty plus companies still operate within theGolden Mile in Western Australia, for example, and similar reductions haveoccurred in other gold mining regions across Australia (Baker 1997).

Such amalgamations appear to enable companies to tap the synergies ofcentralising several operations within one gold mining region. These bene-fits include the external gains from consolidating exploration within a geolog-ically similar area, as well as the potential cost savings of processing oresfrom different mines at central milling locations.

Further, during the current period of share price weakness (which has partic-ularly affected smaller companies), larger companies have faced increasedincentives to amalgamate with exploration focused ‘juniors’ as a means ofmaintaining access to new resources. Others have noted that ‘juniors’ aregenerally willing to form such alliances in the currently depressed marketso as to obtain necessary exploration support (Hextall and Dixon 1998).

It is assumed for the cash cost projections shown in figure 12, and the supplymodeling in the next section, that no major technological or geoscientificbreakthroughs in the near future will substantially alter the productivity ofgold exploration, processing and mining in Australia. Such productivityincreases have occurred in the past: the introduction of carbon-in-pulp (CIP)and carbon-in-leach (CIL) gold processing technologies to Australia in theearly 1980s dramatically lowered the economic cutoff grades of mining goldore (particularly oxide ores) and thereby provided impetus for the rapidgrowth in the modern gold industry in Australia.

33Australia in the world gold market

Houchin and Staunton (1998) suggest that CIP–CIL based technology islikely to remain the major means of gold ore processing in Australia overthe medium term, given that the process has remained the most economicand reliable of the many alternative processes investigated in recent years.Further, in a period of low prices, the research investment funds availablefor developing new gold processing technologies may be reduced. Processingcost improvements are likely to continue to be derived from refinements ofthe CIP–CIL process, with subsequent savings via reduced reagent consump-tion (mainly cyanide) and higher recovery rates.

However, such cost savings from operational improvements may be offsetby the changing geological and mineralogical conditions facing gold miningand processing in Australia. Many of the shallow oxide deposits in Australiahave been depleted, so the average depth of mining and the proportion ofsecondary (sulfide) ore to be processed have been increasing, thereby rais-ing costs. This trend is expected to continue.

Effect of the changing profitability of Australian goldminingThe decline in returns achieved by the Australian gold mining industry viachanges in prices and other economic conditions will tend to affect produc-tion in two ways. First, gold producers will respond to changed economicconditions by adjusting future production and investment plans (includingexploration). Second, falling profitability often leads, where feasible, to once-off cost cutting through revised mine planning, which can maintain the returnsto the sector in the short term. The likelihood of technological change andimprovements in geoscientific understanding of the magnitude seen in theearly 1980s is assumed to be negligible over the outlook period.

This profitability outlook is expected to result in lower levels of Australiangold production over the medium to longer term. The extent of this reduc-tion and the sensitivity of Australia’s future gold production to alternativeworld price scenarios are examined in more detail in the next section. Butfirst it is useful to consider some influences that will tend to sustain produc-tion in the short term, despite lower profits and increased uncertainty.

Dynamics of Australian gold supplyHistorically, changes in Australian gold production in response to pricechanges (and other factors affecting profits) have been delayed for a numberof reasons. The delay in production increases following sustained price

34 ABARE research report 99.8

increases generally reflects the lead times of exploration and subsequentmine development or expansion. Shutting down or scaling back mine produc-tion in response to price falls usually involves significant adjustment costs,and such decisions are costly to reverse. These adjustment costs also lead toinertia during periods of price uncertainty (such as occurred throughout 1997)as producers wait until prices stabilise or sentiment becomes clearer beforethey fundamentally change production plans (Dixit and Pindyck 1994).