goldman sachs 2019-10-k - learnfrombarryprework

TRANSCRIPT

UNITED STATES SECURITIES AND EXCHANGE COMMISSIONWashington, D.C. 20549

Form 10-KANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019 Commission File Number: 001-14965

The Goldman Sachs Group, Inc.(Exact name of registrant as specified in its charter)

Delaware 13-4019460(State or other jurisdiction of

incorporation or organization)(I.R.S. Employer

Identification No.)

200 West Street 10282New York, N.Y.

(Address of principal executive offices)(Zip Code)

(212) 902-1000(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each classTradingSymbol

Exchangeon whichregistered

Common stock, par value $.01 per share GS NYSEDepositary Shares, Each Representing 1/1,000th Interest in a Share of Floating Rate Non-Cumulative Preferred Stock, Series A GS PrA NYSEDepositary Shares, Each Representing 1/1,000th Interest in a Share of Floating Rate Non-Cumulative Preferred Stock, Series C GS PrC NYSEDepositary Shares, Each Representing 1/1,000th Interest in a Share of Floating Rate Non-Cumulative Preferred Stock, Series D GS PrD NYSEDepositary Shares, Each Representing 1/1,000th Interest in a Share of 5.50% Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series J GS PrJ NYSEDepositary Shares, Each Representing 1/1,000th Interest in a Share of 6.375% Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series K GS PrK NYSEDepositary Shares, Each Representing 1/1,000th Interest in a Share of 6.30% Non-Cumulative Preferred Stock, Series N GS PrN NYSE5.793% Fixed-to-Floating Rate Normal Automatic Preferred Enhanced Capital Securities of Goldman Sachs Capital II GS/43PE NYSEFloating Rate Normal Automatic Preferred Enhanced Capital Securities of Goldman Sachs Capital III GS/43PF NYSEMedium-Term Notes, Series A, Index-Linked Notes due 2037 of GS Finance Corp. GCE NYSE ArcaMedium-Term Notes, Series B, Index-Linked Notes due 2037 GSC NYSE ArcaMedium-Term Notes, Series E, Index-Linked Notes due 2028 of GS Finance Corp. FRLG NYSE Arca

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. È Yes ‘ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. ‘ Yes È No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during thepreceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for thepast 90 days. È Yes ‘ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of RegulationS-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). È Yes ‘ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerginggrowth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2of the Exchange Act.

Large accelerated filer È Accelerated filer ‘ Non-accelerated filer ‘

Smaller reporting company ‘ Emerging growth company ‘

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new orrevised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ‘

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ‘ Yes È No

As of June 30, 2019, the aggregate market value of the common stock of the registrant held by non-affiliates of the registrant was approximately $73.4 billion.

As of February 7, 2020, there were 345,672,769 shares of the registrant’s common stock outstanding.

Documents incorporated by reference: Portions of The Goldman Sachs Group, Inc.’s Proxy Statement for its 2020 Annual Meeting of Shareholders areincorporated by reference in the Annual Report on Form 10-K in response to Part III, Items 10, 11, 12, 13 and 14.

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIESANNUAL REPORT ON FORM 10-K FOR THE FISCAL YEAR ENDED DECEMBER 31, 2019

INDEX

Form 10-K Item Number Page No.

PART I 1

Item 1

Business 1

Introduction 1

Our Business Segments 1

Investment Banking 2

Global Markets 2

Asset Management 4

Consumer & Wealth Management 5

Business Continuity and Information Security 5

Human Capital Management 5

Competition 6

Regulation 7

Information about our Executive Officers 20

Available Information 21

Cautionary Statement Pursuant to the U.S. Private SecuritiesLitigation Reform Act of 1995 21

Item 1A

Risk Factors 23

Item 1B

Unresolved Staff Comments 44

Item 2

Properties 44

Item 3

Legal Proceedings 45

Item 4

Mine Safety Disclosures 45

PART II 45

Item 5

Market for Registrant’s Common Equity, Related StockholderMatters and Issuer Purchases of Equity Securities 45

Item 6

Selected Financial Data 45

Page No.

Item 7

Management’s Discussion and Analysis of Financial Conditionand Results of Operations 46

Introduction 46

Executive Overview 47

Business Environment 47

Critical Accounting Policies 47

Use of Estimates 49

Recent Accounting Developments 50

Results of Operations 50

Balance Sheet and Funding Sources 65

Equity Capital Management and Regulatory Capital 69

Regulatory Matters and Other Developments 73

Off-Balance-Sheet Arrangements and Contractual Obligations 75

Risk Management 77

Overview and Structure of Risk Management 77

Liquidity Risk Management 82

Market Risk Management 88

Credit Risk Management 92

Operational Risk Management 99

Model Risk Management 101

Item 7A

Quantitative and Qualitative Disclosures About Market Risk 102

Goldman Sachs 2019 Form 10-K

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

INDEX

Page No.

Item 8

Financial Statements and Supplementary Data 102

Management’s Report on Internal Control over FinancialReporting 102

Report of Independent Registered Public Accounting Firm 103

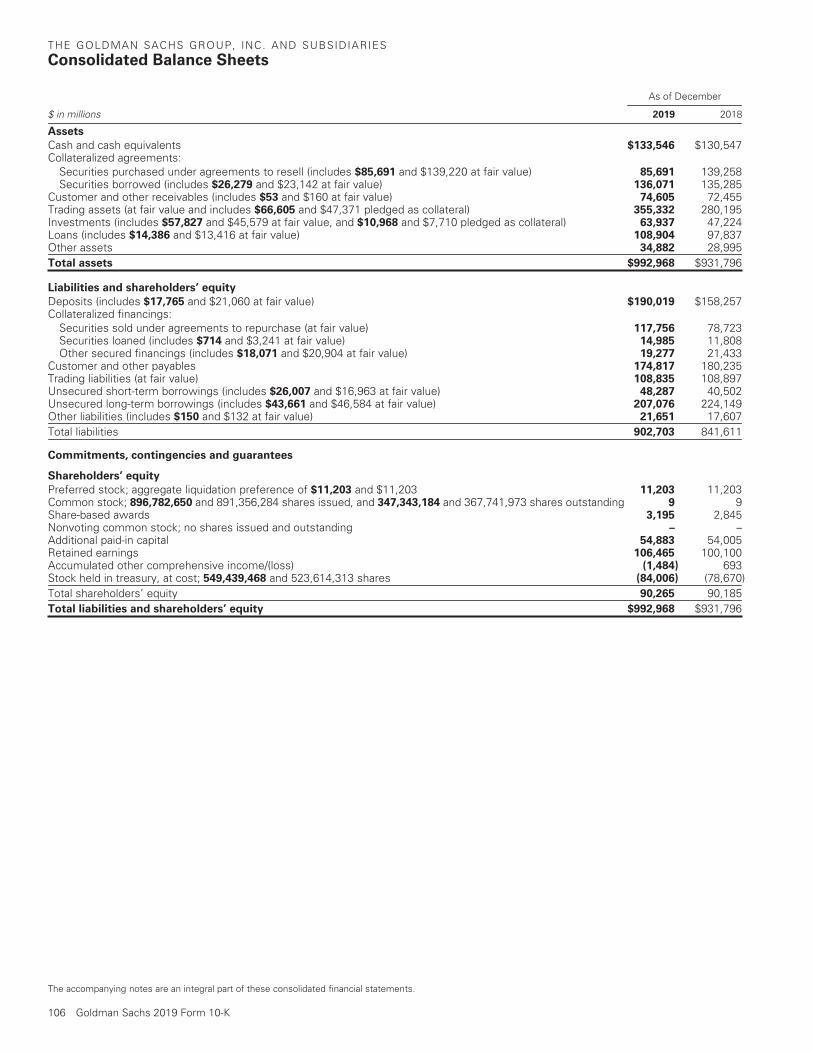

Consolidated Financial Statements 105

Consolidated Statements of Earnings 105

Consolidated Statements of Comprehensive Income 105

Consolidated Balance Sheets 106

Consolidated Statements of Changes in Shareholders’ Equity 107

Consolidated Statements of Cash Flows 108

Notes to Consolidated Financial Statements 109

Note 1. Description of Business 109

Note 2. Basis of Presentation 109

Note 3. Significant Accounting Policies 110

Note 4. Fair Value Measurements 115

Note 5. Trading Assets and Liabilities 120

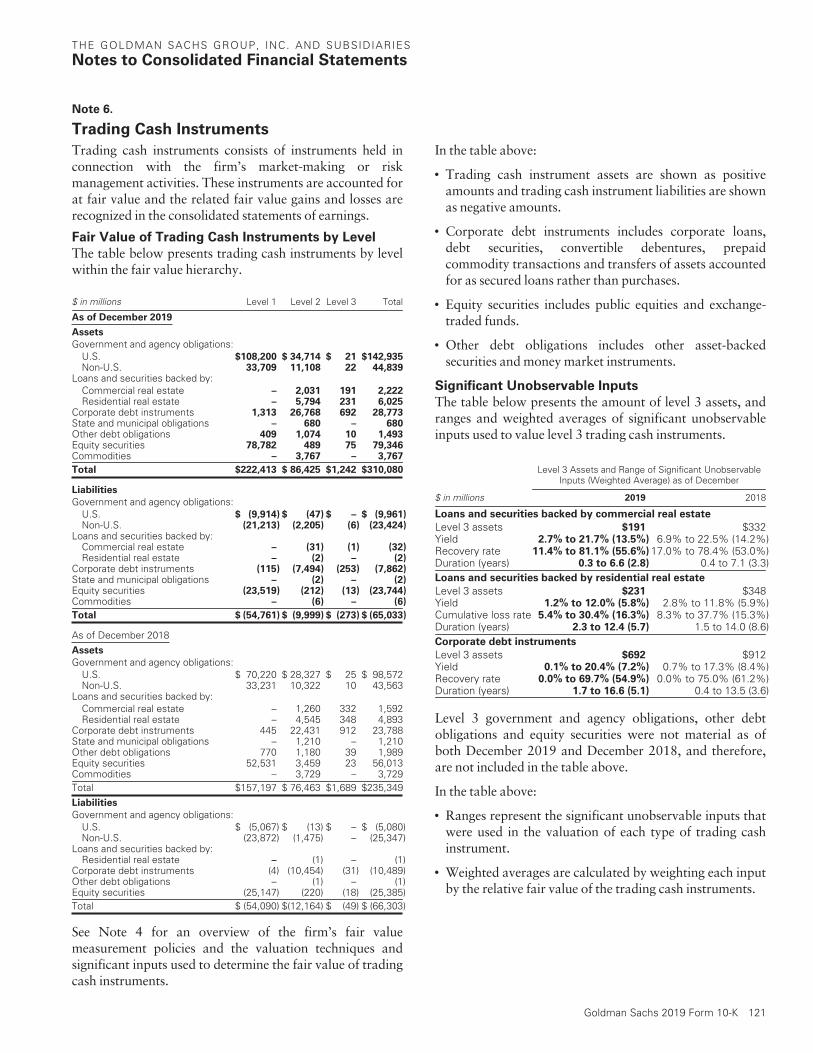

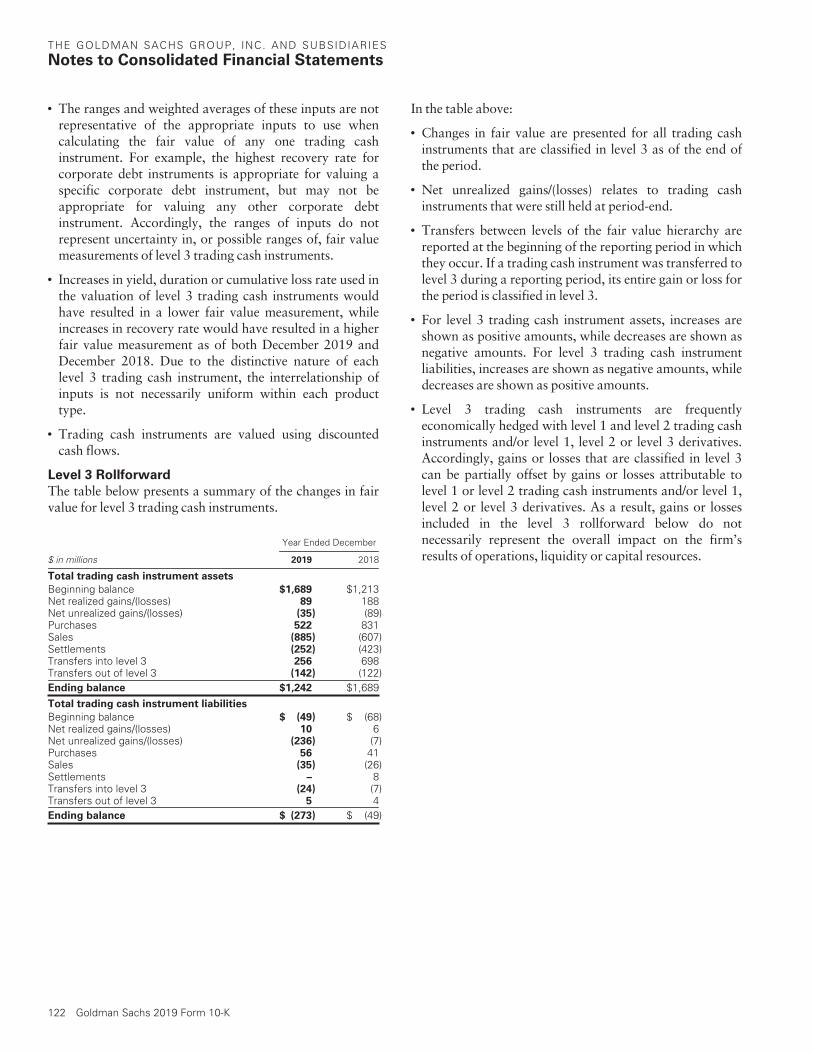

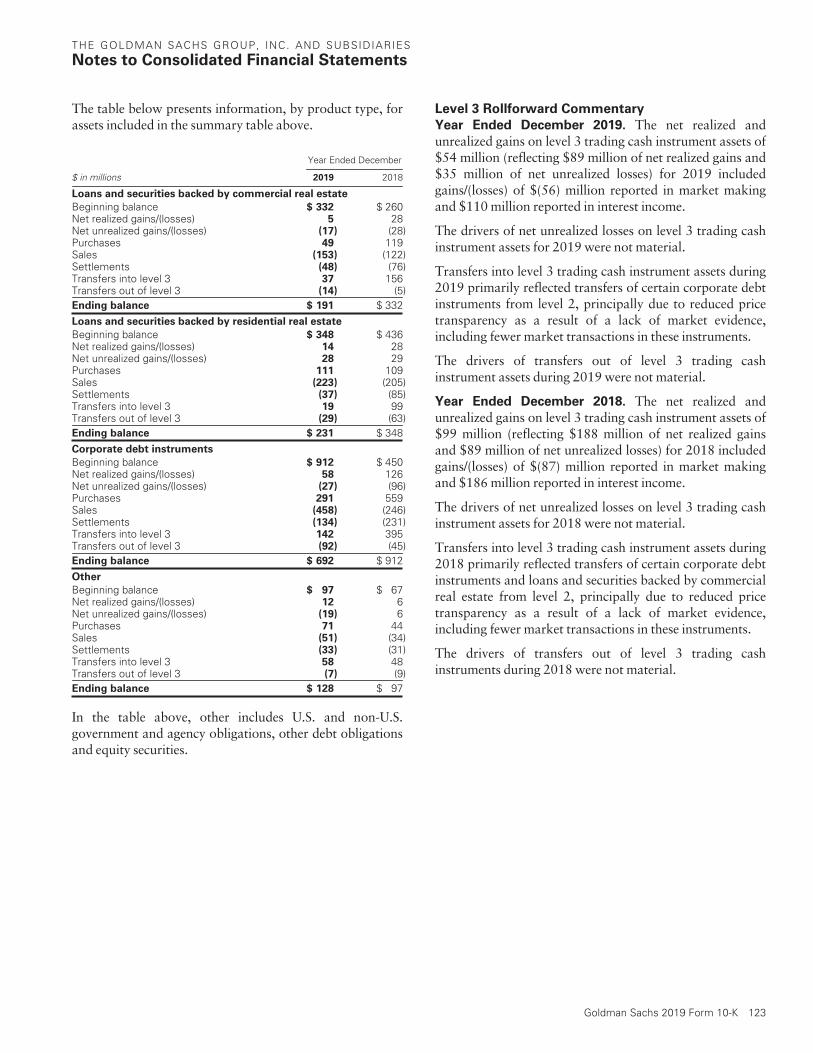

Note 6. Trading Cash Instruments 121

Note 7. Derivatives and Hedging Activities 124

Note 8. Investments 133

Note 9. Loans 138

Note 10. Fair Value Option 144

Note 11. Collateralized Agreements and Financings 149

Note 12. Other Assets 153

Note 13. Deposits 156

Note 14. Unsecured Borrowings 157

Note 15. Other Liabilities 160

Note 16. Securitization Activities 160

Note 17. Variable Interest Entities 162

Note 18. Commitments, Contingencies and Guarantees 165

Note 19. Shareholders’ Equity 169

Note 20. Regulation and Capital Adequacy 172

Note 21. Earnings Per Common Share 179

Note 22. Transactions with Affiliated Funds 179

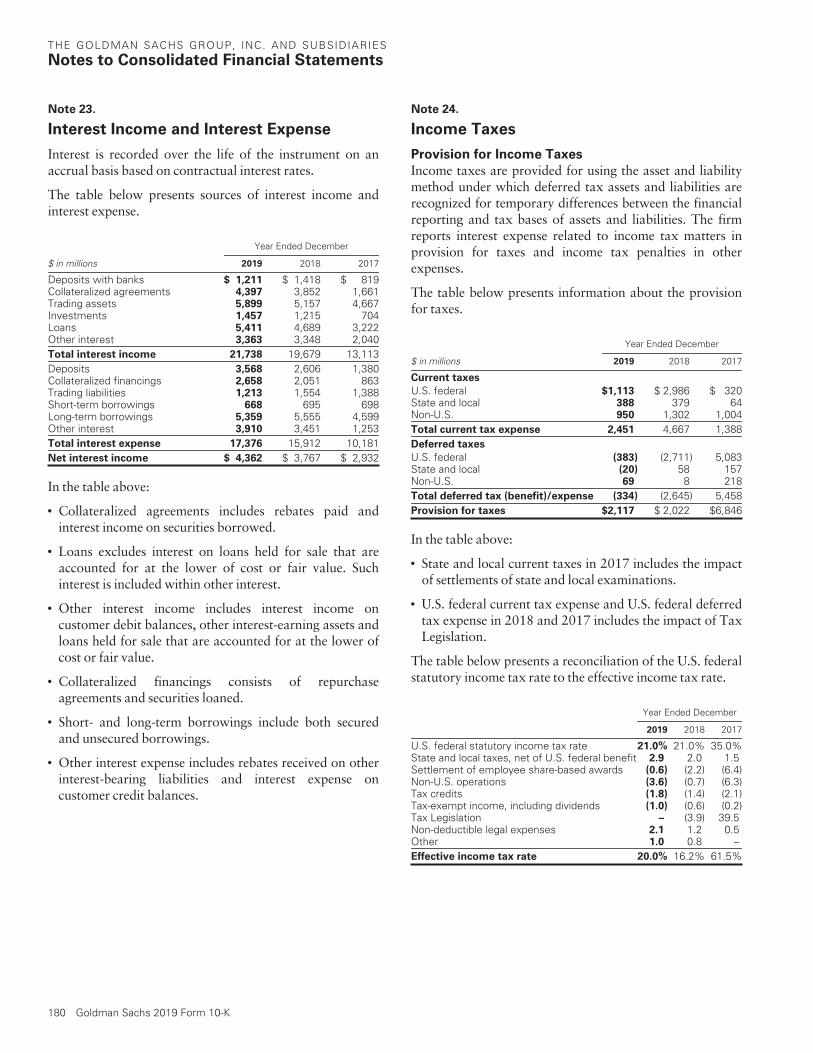

Note 23. Interest Income and Interest Expense 180

Note 24. Income Taxes 180

Note 25. Business Segments 182

Note 26. Credit Concentrations 185

Note 27. Legal Proceedings 185

Note 28. Employee Benefit Plans 194

Note 29. Employee Incentive Plans 194

Note 30. Parent Company 196

Page No.

Supplemental Financial Information 198

Quarterly Results 198

Common Stock Performance 198

Selected Financial Data 199

Statistical Disclosures 199

Item 9

Changes in and Disagreements with Accountants on Accountingand Financial Disclosure 204

Item 9A

Controls and Procedures 204

Item 9B

Other Information 204

PART III 204

Item 10

Directors, Executive Officers and Corporate Governance 204

Item 11

Executive Compensation 204

Item 12

Security Ownership of Certain Beneficial Owners andManagement and Related Stockholder Matters 205

Item 13

Certain Relationships and Related Transactions, and DirectorIndependence 205

Item 14

Principal Accounting Fees and Services 205

PART IV 205

Item 15

Exhibits, Financial Statement Schedules 205

SIGNATURES 210

Goldman Sachs 2019 Form 10-K

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

PART I

Item 1. Business

Introduction

Goldman Sachs is a leading global investment banking,securities and investment management firm that provides awide range of financial services to a substantial anddiversified client base that includes corporations, financialinstitutions, governments and individuals. Our purpose isto advance sustainable economic growth and financialopportunity. Our goal, reflected in our One GoldmanSachs initiative, is to deliver the full range of our servicesand expertise to support our clients in a more accessible,comprehensive and efficient manner, across businesses andproduct areas.

When we use the terms “Goldman Sachs,” “we,” “us” and“our,” we mean The Goldman Sachs Group, Inc. (GroupInc. or parent company), a Delaware corporation, and itsconsolidated subsidiaries. When we use the term “oursubsidiaries,” we mean the consolidated subsidiaries ofGroup Inc. References to “this Form 10-K” are to ourAnnual Report on Form 10-K for the year endedDecember 31, 2019. All references to 2019, 2018 and 2017refer to our years ended, or the dates, as the contextrequires, December 31, 2019, December 31, 2018 andDecember 31, 2017, respectively.

Group Inc. is a bank holding company (BHC) and afinancial holding company (FHC) regulated by the Board ofGovernors of the Federal Reserve System (FRB). Our U.S.depository institution subsidiary, Goldman Sachs BankUSA (GS Bank USA), is a New York State-chartered bank.

As of December 2019, we had offices in over 30 countriesand 46% of our headcount was based outside the Americas.Our clients are located worldwide and we are an activeparticipant in financial markets around the world.

Our Business Segments

We report our activities in four business segments:Investment Banking, Global Markets, Asset Management,and Consumer & Wealth Management. Investment Bankinggenerates revenues from financial advisory, underwriting andcorporate lending activities. Global Markets consists ofFixed Income, Currency and Commodities (FICC) andEquities, and generates revenues from intermediation andfinancing activities. Asset Management generates revenuesfrom management and other fees, incentive fees, equityinvestments and lending. Consumer & Wealth Managementconsists of Wealth management and Consumer banking, andgenerates revenues from management and other fees,incentive fees, private banking and lending, and consumer-oriented activities.

The chart below presents our four business segments andtheir revenue sources.

INVESTMENT BANKING

Financial advisory Management and other fees

Incentive fees Consumer banking

Equity investments

Lending

FICC- FICC intermediation- FICC financing

Underwriting- Equity underwriting- Debt underwriting

Equities- Equities intermediation- Equities financing

Wealth management- Management and other fees- Incentive fees- Private banking and lending

Corporate lending

GLOBAL MARKETS ASSET MANAGEMENT CONSUMER & WEALTHMANAGEMENT

Prior to the fourth quarter of 2019, we reported ouractivities in the following four business segments:Investment Banking, Institutional Client Services,Investing & Lending, and Investment Management. Ournew segments reflect the following changes:

‰ Investing & Lending results are now included across thefour segments as described below.

‰ Investment Banking additionally includes the results fromlending to corporate clients, including middle-marketlending, relationship lending and acquisition financing,previously reported in Investing & Lending.

‰ Institutional Client Services has been renamed GlobalMarkets and additionally includes the results fromproviding warehouse lending and structured financing toinstitutional clients, previously reported in Investing &Lending, and the results from transactions in derivativesrelated to client advisory and underwriting assignments,previously reported in Investment Banking.

‰ Investment Management has been renamed AssetManagement and additionally includes the results frominvestments in equity securities and lending activitiesrelated to our asset management businesses, includinginvestments in debt securities and loans backed by realestate, both previously reported in Investing & Lending.

‰ Consumer & Wealth Management is a new segment thatincludes management and other fees, incentive fees andresults from deposit-taking activities related to our wealthmanagement business, all previously reported inInvestment Management. It also includes the results fromproviding loans through our private bank, providingunsecured loans and accepting deposits through ourdigital platform, Marcus by Goldman Sachs (Marcus),and providing credit cards, all previously reported inInvesting & Lending.

Goldman Sachs 2019 Form 10-K 1

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Investment Banking

Investment Banking serves public and private sector clientsaround the world. We provide financial advisory services,help companies raise capital to strengthen and grow theirbusinesses and provide financing to corporate clients. Weseek to develop and maintain long-term relationships with adiverse global group of institutional clients, includingcorporations, governments, states and municipalities. Ourgoal is to deliver to our institutional clients all of ourresources in a seamless fashion, with investment bankingserving as the main initial point of contact.

Investment Banking generates revenues from the following:

‰ Financial advisory. We are a leader in providingfinancial advisory services, including strategic advisoryassignments with respect to mergers and acquisitions,divestitures, corporate defense activities, restructuringsand spin-offs. In particular, we help clients execute large,complex transactions for which we provide multipleservices, including cross-border structuring expertise. Wealso assist our clients in managing their asset and liabilityexposures and their capital.

‰ Underwriting. We help companies raise capital to fundtheir businesses. As a financial intermediary, our job is tomatch the capital of our investing clients, who aim togrow the savings of millions of people, with the needs ofour public and private sector clients, who need financingto generate growth, create jobs and deliver products andservices. Our underwriting activities include publicofferings and private placements, including local andcross-border transactions and acquisition financing, of awide range of securities and other financial instruments,including loans. Underwriting consists of the following:

Equity underwriting. We underwrite common andpreferred stock and convertible and exchangeablesecurities. We regularly receive mandates for large,complex transactions and have held a leading position inworldwide public common stock offerings andworldwide initial public offerings for many years.

Debt underwriting. We underwrite and originatevarious types of debt instruments, including investment-grade and high-yield debt, bank and bridge loans,including in connection with acquisition financing, andemerging- and growth-market debt, which may be issuedby, among others, corporate, sovereign, municipal andagency issuers. In addition, we underwrite and originatestructured securities, which include mortgage-relatedsecurities and other asset-backed securities.

‰ Corporate lending. We make loans to corporate clients,including middle-market lending, relationship lendingand acquisition financing. The hedges related to thislending and financing activity are reported as part of ourcorporate lending activity. We also provide transactionbanking services to certain of our corporate clients.

Global Markets

Global Markets serves our clients who buy and sellfinancial products, raise funding and manage risk. We dothis by acting as a market maker and offering marketexpertise on a global basis. Global Markets makes marketsand facilitates client transactions in fixed income, equity,currency and commodity products. In addition, we makemarkets in, and clear client transactions on, major stock,options and futures exchanges worldwide.

As a market maker, we provide prices to clients globallyacross thousands of products in all major asset classes andmarkets. At times, we take the other side of transactionsourselves if a buyer or seller is not readily available, and atother times we connect our clients to other parties whowant to transact. Our willingness to make markets, commitcapital and take risk in a broad range of products is crucialto our client relationships. Market makers provide liquidityand play a critical role in price discovery, which contributesto the overall efficiency of the capital markets. Inconnection with our market-making activities, we maintain(i) market-making positions, typically for a short period oftime, in response to, or in anticipation of, client demand,and (ii) positions to actively manage our risk exposures thatarise from these market-making activities (collectively,inventory). We carry our inventory at fair value withchanges in valuation reflected in net revenues.

Our clients are institutions that are primarily professionalmarket participants, including investment entities whoseultimate clients include individual investors investing fortheir retirement, buying insurance or putting aside surpluscash in a deposit account.

2 Goldman Sachs 2019 Form 10-K

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

We execute a high volume of transactions for our clients inlarge, highly liquid markets (such as markets for U.S.Treasury securities, stocks and certain agency mortgagepass-through securities). We also execute transactions forour clients in less liquid markets (such as mid-cap corporatebonds, emerging market currencies and certain non-agencymortgage-backed securities) for spreads and fees that aregenerally somewhat larger than those charged in moreliquid markets. Additionally, we structure and executetransactions involving customized or tailor-made productsthat address our clients’ risk exposures, investmentobjectives or other complex needs (such as a jet fuel hedgefor an airline), as well as derivative transactions related toclient advisory and underwriting activities.

Through our global sales force, we maintain relationshipswith our clients, receiving orders and distributinginvestment research, trading ideas, market information andanalysis. Much of this connectivity between us and ourclients is maintained on technology platforms, includingMarquee, and operates globally where markets are open fortrading. Marquee provides institutional investors withmarket intelligence, risk analytics, proprietary datasets andtrade execution across multiple asset classes.

Global Markets and our other businesses are supported byour Global Investment Research division, which, as ofDecember 2019, provided fundamental research onapproximately 3,000 companies worldwide and more than40 national economies, as well as on industries, currenciesand commodities.

Global Markets activities are organized by asset class andinclude both “cash” and “derivative” instruments. “Cash”refers to trading the underlying instrument (such as a stock,bond or barrel of oil). “Derivative” refers to instrumentsthat derive their value from underlying asset prices, indices,reference rates and other inputs, or a combination of thesefactors (such as an option, which is the right or obligationto buy or sell a certain bond, stock or other asset on aspecified date in the future at a certain price, or an interestrate swap, which is the agreement to convert a fixed rate ofinterest into a floating rate or vice versa).

Global Markets consists of FICC and Equities.

FICC. FICC generates revenues from intermediation andfinancing activities.

‰ FICC intermediation. Includes client execution activitiesrelated to making markets in both trading cash andderivative instruments, as detailed below.

Interest Rate Products. Government bonds (includinginflation-linked securities) across maturities, othergovernment-backed securities, and interest rate swaps,options and other derivatives.

Credit Products. Investment-grade corporate securities,high-yield securities, credit derivatives, exchange-tradedfunds (ETFs), bank and bridge loans, municipalsecurities, emerging market and distressed debt, and tradeclaims.

Mortgages. Commercial mortgage-related securities,loans and derivatives, residential mortgage-relatedsecurities, loans and derivatives (including U.S.government agency-issued collateralized mortgageobligations and other securities and loans), and otherasset-backed securities, loans and derivatives.

Currencies. Currency options, spot/forwards and otherderivatives on G-10 currencies and emerging-marketproducts.

Commodities. Commodity derivatives and, to a lesserextent, physical commodities, involving crude oil andpetroleum products, natural gas, base, precious and othermetals, electricity, coal, agricultural and othercommodity products.

‰ FICC financing. Includes providing financing to ourclients through securities sold under agreements torepurchase (repurchase agreements), as well as throughstructured credit, warehouse lending (includingresidential and commercial mortgage lending) and asset-backed lending, which are typically longer term in nature.

Equities. Equities generates revenues from intermediationand financing activities.

‰ Equities intermediation. We make markets in equitysecurities and equity-related products, including ETFs,convertible securities, options, futures andover-the-counter (OTC) derivative instruments, on aglobal basis. As a principal, we facilitate clienttransactions by providing liquidity to our clients,including with large blocks of stocks or derivatives,requiring the commitment of our capital.

Goldman Sachs 2019 Form 10-K 3

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

We also structure and make markets in derivatives onindices, industry sectors, financial measures andindividual company stocks. We develop strategies andprovide information about portfolio hedging andrestructuring and asset allocation transactions for ourclients. We also work with our clients to create speciallytailored instruments to enable sophisticated investors toestablish or liquidate investment positions or undertakehedging strategies. We are one of the leading participantsin the trading and development of equity derivativeinstruments.

Our exchange-based market-making activities includemaking markets in stocks and ETFs, futures and optionson major exchanges worldwide.

We generate commissions and fees from executing andclearing institutional client transactions on major stock,options and futures exchanges worldwide, as well asOTC transactions. We provide our clients with access to abroad spectrum of equity execution services, includingelectronic “low-touch” access and more complex “high-touch” execution through both traditional and electronicplatforms, including Marquee.

‰ Equities financing. Includes prime brokerage and otherequities financing activities, including securities lending,margin lending and swaps.

We earn fees by providing clearing, settlement andcustody services globally. In addition, we provide ourhedge fund and other clients with a technology platformand reporting that enables them to monitor their securityportfolios and manage risk exposures.

We provide services that principally involve borrowingand lending securities to cover institutional clients’ shortsales and borrowing securities to cover our short sales andotherwise to make deliveries into the market. In addition,we are an active participant in broker-to-broker securitieslending and third-party agency lending activities.

We provide financing to our clients for their securitiestrading activities through margin loans that arecollateralized by securities, cash or other acceptablecollateral. We earn a spread equal to the differencebetween the amount we pay for funds and the amount wereceive from our client.

We execute swap transactions to provide our clients withexposure to securities and indices.

Asset Management

Asset Management provides investment services to helpclients preserve and grow their financial assets. We providethese services to our institutional clients, as well as investorswho primarily access our products through a network ofthird-party distributors around the world.

We manage client assets across a broad range of investmentstrategies and asset classes, including equity, fixed incomeand alternative investments. Alternative investmentsprimarily includes hedge funds, credit funds, private equity,real estate, currencies, commodities and asset allocationstrategies. Our investment offerings include those managedon a fiduciary basis by our portfolio managers, as well asstrategies managed by third-party managers. We offer ourinvestments in a variety of structures, including separatelymanaged accounts, mutual funds, private partnerships andother commingled vehicles.

We also provide customized investment advisory solutionsdesigned to address our clients’ investment needs. Thesesolutions begin with identifying clients’ objectives andcontinue through portfolio construction, ongoing assetallocation and risk management and investment realization.We draw from a variety of third-party managers, as well asour proprietary offerings, to implement solutions forclients.

Asset Management generates revenues from the following:

‰ Management and Other Fees. The majority ofrevenues in management and other fees consists of asset-based fees on client assets that we manage. The fees thatwe charge vary by asset class, distribution channel and thetype of services provided, and are affected by investmentperformance, as well as asset inflows and redemptions.

‰ Incentive Fees. In certain circumstances, we also receiveincentive fees based on a percentage of a fund’s or aseparately managed account’s return, or when the returnexceeds a specified benchmark or other performancetargets. Such fees include overrides, which consist of theincreased share of the income and gains derived primarilyfrom our private equity and credit funds when the returnon a fund’s investments over the life of the fund exceedscertain threshold returns. Incentive fees are recognizedwhen it is probable that a significant reversal of such feeswill not occur.

‰ Equity Investments. Our alternative investing activitiesrelate to public and private equity investments incorporate, real estate and infrastructure entities. We alsomake investments through consolidated investmententities, substantially all of which are engaged in realestate investment activities.

‰ Lending. We provide financing related to our assetmanagement business and invest in debt securities andloans backed by real estate. These activities includeinvestments in mezzanine debt, senior debt and distresseddebt securities.

4 Goldman Sachs 2019 Form 10-K

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Consumer & Wealth Management

Consumer & Wealth Management helps clients achievetheir individual financial goals by providing a broad rangeof wealth advisory and banking services, including financialplanning, investment management, deposit taking, andlending. Services are offered through our global network ofadvisors and via our digital platforms.

Wealth Management. Wealth Management providestailored wealth advisory services to clients across the wealthspectrum. We operate globally serving individuals, families,family offices, and select foundations and endowments.Our relationships are established directly or introducedthrough corporations that sponsor financial wellnessprograms for their employees.

We offer personalized financial planning inclusive ofincome and liability management, compensation andbenefits analysis, trust and estate structuring, taxoptimization, philanthropic giving, and asset protection.We also provide customized investment advisory solutions,and offer structuring and execution capabilities in securityand derivative products across all major global markets.We leverage a broad, open-architecture investmentplatform and our global execution capabilities to helpclients achieve their investment goals. In addition, we offerclients a full range of private banking services, including avariety of deposit alternatives and loans that our clients useto finance investments in both financial and nonfinancialassets, bridge cash flow timing gaps or provide liquidity andflexibility for other needs.

Wealth management generates revenues from thefollowing:

‰ Management and other fees. Includes fees related tomanaging assets, providing investing and wealth advisorysolutions, providing financial planning and counselingservices via our subsidiary, The Ayco Company, L.P. andexecuting brokerage transactions for wealth managementclients.

‰ Incentive fees. In certain circumstances, we also receiveincentive fees based on a percentage of a fund’s return, orwhen the return exceeds a specified benchmark or otherperformance targets. Such fees include overrides, whichconsist of the increased share of the income and gainsderived primarily from our private equity and credit fundswhen the return on a fund’s investments over the life ofthe fund exceeds certain threshold returns. Incentive feesare recognized when it is probable that a significantreversal of such fees will not occur.

‰ Private banking and lending. Includes interest incomeallocated to deposit-taking and net interest income earnedon lending activities for wealth management clients.

Consumer Banking. We engage in consumer-orientedbusinesses. We issue unsecured loans, through Marcus andcredit cards, to finance the purchases of goods or services.We also accept deposits through Marcus, primarily throughGS Bank USA and Goldman Sachs International Bank(GSIB). These deposits include savings and time depositswhich provide us with a diversified source of funding thatreduces our reliance on wholesale funding.

Consumer banking revenues consist of net interest incomeearned on unsecured loans issued to consumers throughMarcus and credit card lending activities, and net interestincome allocated to consumer deposits.

Business Continuity and InformationSecurity

Business continuity and information security, includingcyber security, are high priorities for us. Their importancehas been highlighted by (i) numerous highly publicizedevents in recent years, including cyber attacks againstfinancial institutions, governmental agencies, largeconsumer-based companies and other organizations thatresulted in the unauthorized disclosure of personalinformation and other sensitive or confidentialinformation, the theft and destruction of corporateinformation and requests for ransom payments, and(ii) extreme weather events.

Our Business Continuity & Technology Resilience Programhas been developed to provide reasonable assurance ofbusiness continuity in the event of disruptions at our criticalfacilities or of our systems, and to comply with regulatoryrequirements, including those of FINRA. Because we are aBHC, our Business Continuity & Technology ResilienceProgram is also subject to review by the FRB. The keyelements of the program are crisis management, businesscontinuity, technology resilience, business recovery,assurance and verification, and process improvement. Inthe area of information security, we have developed andimplemented a framework of principles, policies andtechnology designed to protect the information provided tous by our clients and our own information from cyberattacks and other misappropriation, corruption or loss.Safeguards are designed to maintain the confidentiality,integrity and availability of information.

Human Capital Management

We believe that a major strength and principal reason forour success is the quality and dedication of our people andthe shared sense of being part of a team. We strive tomaintain a work environment that fosters professionalism,excellence, diversity, cooperation among our employeesworldwide and high standards of business ethics.

Goldman Sachs 2019 Form 10-K 5

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Instilling our culture in all employees is a continuousprocess, in which training plays an important part. Allemployees are offered the opportunity to participate ineducation and periodic seminars that we sponsor at variouslocations throughout the world. Another important part ofinstilling our culture is our employee review process.Employees are reviewed by supervisors, co-workers andemployees they supervise in a 360-degree review processthat is integral to our team approach, and which includesan evaluation of an employee’s performance with respect torisk management, compliance and diversity. As ofDecember 2019, we had headcount of 38,300.

Competition

The financial services industry and all of our businesses areintensely competitive, and we expect them to remain so.Our competitors are other entities that provide investmentbanking (including transaction banking), market-making,investment management services, and commercial and/orconsumer lending and deposit-taking products, as well asthose entities that make investments in securities,commodities, derivatives, real estate, loans and otherfinancial assets. These entities include brokers and dealers,investment banking firms, commercial banks, credit cardissuers, insurance companies, investment advisers, mutualfunds, hedge funds, private equity funds, merchant banks,consumer finance companies and financial technology andother internet-based companies. We compete with someentities globally and with others on a regional, product orniche basis. We compete based on a number of factors,including transaction execution, products and services,innovation, reputation and price.

We have faced, and expect to continue to face, pressure toretain market share by committing capital to businesses ortransactions on terms that offer returns that may not becommensurate with their risks. In particular, corporateclients seek such commitments (such as agreements toparticipate in their loan facilities) from financial servicesfirms in connection with investment banking and otherassignments.

Consolidation and convergence have significantly increasedthe capital base and geographic reach of some of ourcompetitors, and have also hastened the globalization of thesecurities and other financial services markets. As a result,we have had to commit capital to support our internationaloperations and to execute large global transactions. To takeadvantage of some of our most significant opportunities,we will have to compete successfully with financialinstitutions that are larger and have more capital and thatmay have a stronger local presence and longer operatinghistory outside the U.S.

We also compete with smaller institutions that offer moretargeted services, such as independent advisory firms. Someclients may perceive these firms to be less susceptible topotential conflicts of interest than we are, and, as describedbelow, our ability to effectively compete with them could beaffected by regulations and limitations on activities thatapply to us but may not apply to them.

A number of our businesses are subject to intense pricecompetition. Efforts by our competitors to gain marketshare have resulted in pricing pressure in our investmentbanking, market-making and asset management businesses.For example, the increasing volume of trades executedelectronically, through the internet and through alternativetrading systems, has increased the pressure on tradingcommissions, in that commissions for electronic trading aregenerally lower than those for non-electronic trading. Itappears that this trend toward low-commission trading willcontinue. Price competition has also led to compression inthe difference between the price at which a marketparticipant is willing to sell an instrument and the price atwhich another market participant is willing to buy it (i.e.,bid/offer spread), which has affected our market-makingbusinesses. In addition, we believe that we will continue toexperience competitive pressures in these and other areas inthe future as some of our competitors seek to obtain marketshare by further reducing prices, and as we enter into orexpand our presence in markets that may rely more heavilyon electronic trading and execution.

We also compete on the basis of the types of financialproducts that we and our competitors offer. In somecircumstances, our competitors may offer financialproducts that we do not offer and that our clients mayprefer.

The provisions of the U.S. Dodd-Frank Wall Street Reformand Consumer Protection Act (Dodd-Frank Act), therequirements promulgated by the Basel Committee onBanking Supervision (Basel Committee) and other financialregulations could affect our competitive position to theextent that limitations on activities, increased fees andcompliance costs or other regulatory requirements do notapply, or do not apply equally, to all of our competitors orare not implemented uniformly across differentjurisdictions. For example, the provisions of the Dodd-Frank Act that prohibit proprietary trading and restrictinvestments in certain hedge and private equity fundsdifferentiate between U.S.-based and non-U.S.-basedbanking organizations and give non-U.S.-based bankingorganizations greater flexibility to trade outside of the U.S.and to form and invest in funds outside the U.S.

6 Goldman Sachs 2019 Form 10-K

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Likewise, the obligations with respect to derivativetransactions under Title VII of the Dodd-Frank Act depend,in part, on the location of the counterparties to thetransaction. The impact of the Dodd-Frank Act and otherregulatory developments on our competitive position hasdepended and will continue to depend to a large extent onthe manner in which the required rulemaking andregulatory guidance evolve, the extent of internationalconvergence, and the development of market practice andstructures under the new regulatory regimes, as describedfurther in “Regulation” below.

We also face intense competition in attracting and retainingqualified employees. Our ability to continue to competeeffectively has depended and will continue to depend uponour ability to attract new employees, retain and motivate ourexisting employees and to continue to compensate employeescompetitively amid intense public and regulatory scrutiny onthe compensation practices of large financial institutions.Our pay practices and those of certain of our competitors aresubject to review by, and the standards of, the FRB and otherregulators inside and outside the U.S., including thePrudential Regulation Authority (PRA) and the FinancialConduct Authority (FCA) in the U.K. We also compete foremployees with institutions whose pay practices are notsubject to regulatory oversight. See “Regulation —Compensation Practices” and “Risk Factors — Ourbusinesses may be adversely affected if we are unable to hireand retain qualified employees” in Part I, Item 1A of thisForm 10-K for further information about such regulation.

Regulation

As a participant in the global financial services industry, weare subject to extensive regulation and supervisionworldwide. The regulatory regimes applicable to ouroperations worldwide have recently been, and continue tobe, subject to significant changes. The Basel Committee isthe primary global standard setter for prudential bankregulation; however, its standards do not become effectivein a jurisdiction until the relevant regulators have adoptedrules to implement its standards. The implications of theseregulations for our businesses depend to a large extent ontheir implementation by the relevant regulators globally,and the market practices and structures that develop.

New regulations have been adopted or are being consideredby regulators and policy makers worldwide, as describedbelow. Recent developments have added additionaluncertainty to the implementation, scope and timing ofregulatory reforms and potential for deregulation in someareas. The effects of any changes to the regulations affectingour businesses, including as a result of the proposalsdescribed below, are uncertain and will not be known untilthe changes are finalized and market practices andstructures develop under the revised regulations.

Our principal subsidiaries operating in Europe, GoldmanSachs International (GSI), GSIB and Goldman Sachs AssetManagement International (GSAMI), are incorporated andheadquartered in the U.K. As a result of the U.K.’swithdrawal from the E.U. (Brexit), we expect considerablechange in the regulatory framework that will governtransactions and business undertaken by our U.K.subsidiaries.

The E.U. and the U.K. agreed to a withdrawal agreement(the Withdrawal Agreement), which became effective onJanuary 31, 2020 when the U.K. ceased to be an E.U.member state. The transition period under the WithdrawalAgreement will last until the end of December 2020 and theU.K. Government has stated that it does not intend to agreeto an extension to this period. During the transition period,the U.K. will be treated as if it were a member state of theE.U. and therefore our U.K. subsidiaries will still benefitfrom non-discriminatory access to E.U. clients andinfrastructure. At the end of the transition period, firmsestablished in the U.K., including our U.K. subsidiaries, areexpected to lose their pan-E.U. “passports” and generallyto be treated like entities in countries outside the E.U.,whose access to the E.U. is governed by E.U. and nationallaw and may depend on the making of E.U. equivalencedecisions or on their obtaining licenses or exemptions undernational regimes, subject to any other arrangements such asa free trade agreement. After the end of the transitionperiod, the U.K. will not be required to continue to applyE.U. financial services legislation and may not adopt rulesthat correspond to E.U. legislation not already operative inthe U.K. by then (such as some parts of the 2019 E.U.capital requirements regulation). We have strengthened thecapabilities of our operating subsidiaries in the remainingE.U. countries, particularly Goldman Sachs Bank EuropeSE (GSBE), our German bank subsidiary, and have startedto move certain activities there.

Banking Supervision and Regulation

Group Inc. is a BHC under the U.S. Bank HoldingCompany Act of 1956 (BHC Act) and an FHC underamendments to the BHC Act effected by the U.S. Gramm-Leach-Bliley Act of 1999 (GLB Act), and is subject tosupervision and examination by the FRB, which is ourprimary regulator.

The FRB has a rating system for large financial institutionsthat is intended to align with its supervisory program. Itconsists of component ratings for capital planning andpositions, liquidity risk management and positions, andgovernance and controls. The FRB has proposed guidancefor the governance and controls component.

Goldman Sachs 2019 Form 10-K 7

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Under the system of “functional regulation” establishedunder the BHC Act, the primary regulators of our U.S.non-bank subsidiaries directly regulate the activities ofthose subsidiaries, with the FRB exercising a supervisoryrole. Such “functionally regulated” subsidiaries includebroker-dealers registered with the SEC, such as ourprincipal U.S. broker-dealer, Goldman Sachs & Co. LLC(GS&Co.), entities registered with or regulated by theCFTC with respect to futures-related and swaps-relatedactivities and investment advisers registered with the SECwith respect to their investment advisory activities.

Our principal U.S. bank subsidiary, GS Bank USA, issupervised and regulated by the FRB, the FDIC, the NewYork State Department of Financial Services (NYDFS) andthe Consumer Financial Protection Bureau (CFPB). Anumber of our activities are conducted partially or entirelythrough GS Bank USA and its subsidiaries, including: bankloans (including leveraged lending); personal loans andmortgages; credit cards; interest rate, credit, currency andother derivatives; deposit-taking; and agency lending.

Certain of our subsidiaries are regulated by the banking andsecurities regulatory authorities of the countries in whichthey operate. As described below, our E.U. subsidiaries,including our U.K. subsidiaries during the Brexit transitionperiod, are subject to various European regulations, as wellas national laws, which to some extent implementEuropean directives.

GSI, our U.K. broker-dealer subsidiary and a designatedinvestment firm, and GSIB, our U.K. bank subsidiary, areregulated by the PRA and the FCA. GSI provides broker-dealer services in and from the U.K., and GSIB acts as aprimary dealer for European government bonds and isinvolved in lending (including securities lending) anddeposit-taking activities. GSBE, our German banksubsidiary, is primarily regulated by the ECB within thecontext of the European Single Supervisory Mechanism.Goldman Sachs Paris Inc. et Cie., an investment firmprimarily regulated by the French Prudential Supervisionand Resolution Authority, may, among other activities,conduct activities that GSBE, as a bank subsidiary, isprevented from undertaking.

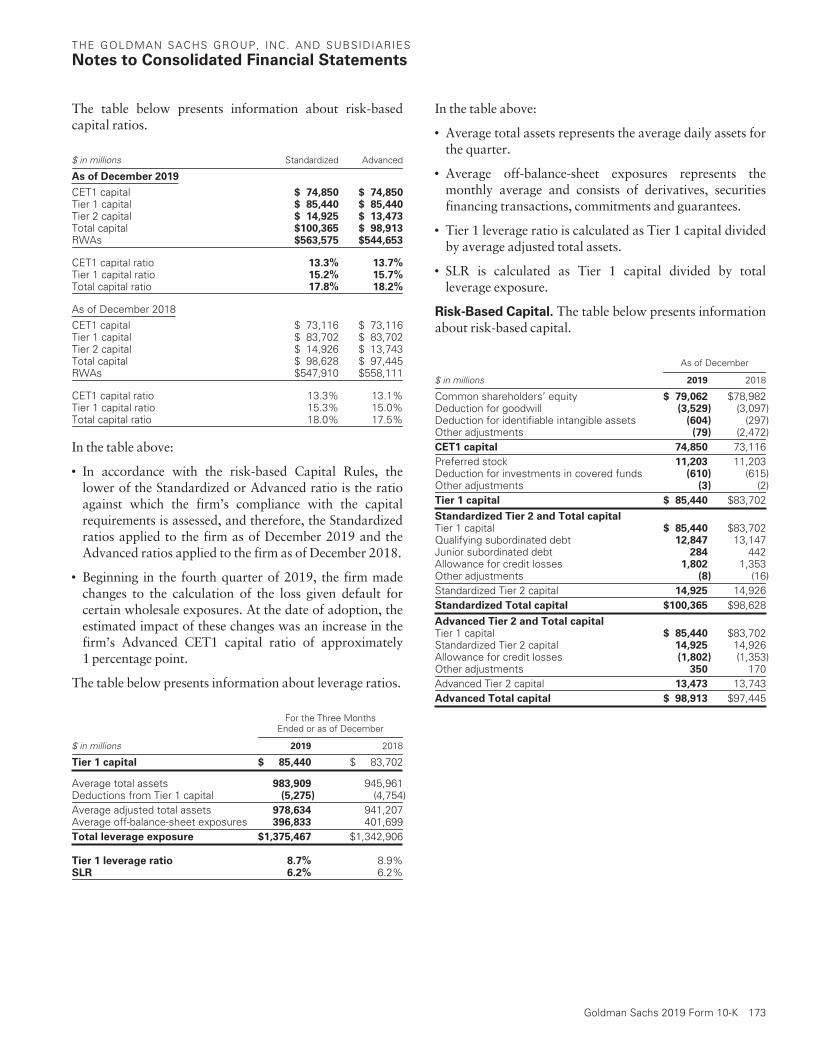

Capital and Liquidity Requirements. We and GS BankUSA are subject to regulatory risk-based capital andleverage requirements that are calculated in accordancewith the regulations of the FRB (Capital Framework). TheCapital Framework is largely based on the BaselCommittee’s framework for strengthening the regulation,supervision and risk management of banks (Basel III) andalso implements certain provisions of the Dodd-Frank Act.Under the tailoring rules adopted by the U.S. federal bankregulatory agencies in October 2019, we and GS Bank USAare subject to “Category I” standards because we have beendesignated as a global systemically important bank (G-SIB).Accordingly, under the Capital Framework, we and GSBank USA are “Advanced approach” bankingorganizations. Under the FRB’s capital adequacyrequirements, we and GS Bank USA must meet specificregulatory capital requirements that involve quantitativemeasures of assets, liabilities and certain off-balance-sheetitems. The sufficiency of our capital levels is also subject toqualitative judgments by regulators. We and GS Bank USAare also subject to liquidity requirements established by theU.S. federal bank regulatory agencies.

GSI and GSIB are subject to capital requirements prescribedin the E.U. Capital Requirements Regulation (CRR) and theE.U. Fourth Capital Requirements Directive (CRD IV),which are largely based on Basel III. GSI and GSIB aresubject to liquidity requirements established by U.K.regulatory authorities that are similar to those applicable toGS Bank USA and us.

Amendments to the CRR and CRD IV (respectively, CRR IIand CRD V) became effective on June 27, 2019. CRR IIwill generally begin to apply in June 2021, and E.U.member states are directed to implement CRD V byDecember 2020.

Risk-Based Capital Ratios. The Capital Frameworkprovides for an additional capital ratio requirement thatincludes three components: (i) for capital conservation(capital conservation buffer), (ii) for countercyclicality(countercyclical capital buffer) and (iii) as a consequence ofour designation as a G-SIB (G-SIB surcharge). Theadditional capital ratio requirement must be satisfiedentirely with capital that qualifies as Common EquityTier 1 (CET1). GS Bank USA is not subject to the G-SIBsurcharge.

The FRB proposed a rule in April 2018 that would, amongother things, replace the capital conservation buffer with astress capital buffer (SCB) requirement for large BHCssubject to the FRB’s Comprehensive Capital Analysis andReview (CCAR). See “Regulation — Banking Supervisionand Regulation — Stress Tests” for further informationabout this proposed rule.

8 Goldman Sachs 2019 Form 10-K

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

The countercyclical capital buffer is designed to counteractsystemic vulnerabilities and currently applies only tobanking organizations subject to Category I, II or IIIstandards, including us. Several other national supervisorsalso require countercyclical capital buffers. The G-SIBsurcharge and countercyclical capital buffer applicable tous could change in the future and, as a result, the minimumcapital ratios to which we are subject could change.

The U.S. federal bank regulatory agencies adopted a rule inDecember 2018 that provides an optional three-yearphase-in period for the day-one regulatory capital effects ofthe adoption of the Current Expected Credit Losses (CECL)accounting standard. The FRB also released a statementindicating that it will not incorporate CECL into thecalculation of the allowance for credit losses in supervisorystress tests through the 2021 stress test cycle. See Note 3 tothe consolidated financial statements in Part II, Item 8 ofthis Form 10-K for further information about CECL.

The U.S. federal bank regulatory agencies adopted a rule inNovember 2019 that will implement the Basel Committee’sstandardized approach for measuring counterparty creditrisk exposures in connection with derivative contracts(SA-CCR). Under the rule, beginning January 1, 2022, butwith the option to adopt starting April 1, 2020, “Advancedapproach” banking organizations will be required to useSA-CCR for purposes of calculating their standardized risk-weighted assets (RWAs) and, with some adjustments, forpurposes of determining their supplementary leverageratios (SLRs) discussed below.

The Basel Committee standards include guidelines forcalculating incremental capital ratio requirements forbanking institutions that are systemically significant from adomestic but not global perspective (D-SIBs). When theseguidelines are implemented by national regulators, theymay apply, among others, to certain subsidiaries of G-SIBs.These guidelines are in addition to the framework forG-SIBs, but are more principles-based. CRD V and CRR IIprovide that institutions that are systemically important atthe E.U. or member state level, known as other systemicallyimportant institutions (O-SIIs), may be subject toadditional capital ratio requirements of up to 3% of CET1,according to their degree of systemic importance (O-SIIbuffers). The designated authority may impose an O-SIIbuffer that is greater than 3% in certain cases. CRD IV andthe CRR currently provide for an additional requirement ofup to 2%. O-SIIs are identified annually, along with theirapplicable buffers. The PRA has identified Goldman SachsGroup UK Limited (GSG UK), the parent company of GSIand GSIB, as an O-SII. GSG UK’s O-SII buffer is currentlyset at zero percent.

The Basel Committee finalized revisions to the frameworkin January 2019 for calculating capital requirements formarket risk, which is expected to increase market riskcapital requirements for most banking organizations. Therevised framework, among other things, revises thestandardized approach and internal models used tocalculate market risk requirements and clarifies the scope ofpositions subject to market risk capital requirements. TheBasel Committee has proposed that national regulatorsimplement the revised framework beginningJanuary 1, 2022. CRR II, which became effective inJune 2019 and establishes a reporting standard, will requireE.U. financial institutions to report their market riskcalculations under the revised framework as early asJanuary 1, 2021. The U.S. federal bank regulatory agencieshave not yet proposed rules implementing the 2019 versionof the revised market risk framework for U.S. financialinstitutions.

The Basel Committee published standards inDecember 2017 that it described as the finalization of theBasel III post-crisis regulatory reforms. These standards seta floor on internally modeled capital requirements at apercentage of the capital requirements under thestandardized approach. They also revise the BaselCommittee’s standardized and model-based approaches forcredit risk, provide a new standardized approach foroperational risk capital and revise the frameworks forcredit valuation adjustment (CVA) risk. The BaselCommittee has proposed that national regulatorsimplement these standards beginning January 1, 2022, andthat the new floor be phased in through January 1, 2027. InNovember 2019, the Basel Committee proposed furtherrevisions to the framework for CVA risk.

The Basel Committee has also published updatedframeworks relating to Pillar 3 disclosure requirements andthe regulatory capital treatment of securitization exposuresand a revised G-SIB assessment methodology. The U.S.federal bank regulatory agencies have not yet proposedrules implementing the December 2017 standards forpurposes of risk-based capital ratios or the BaselCommittee frameworks.

See “Management’s Discussion and Analysis of FinancialCondition and Results of Operations — Equity CapitalManagement and Regulatory Capital” in Part II, Item 7 ofthis Form 10-K and Note 20 to the consolidated financialstatements in Part II, Item 8 of this Form 10-K forinformation about our capital ratios and those of GS BankUSA and GSI.

As described in “Other Restrictions” below, inSeptember 2016, the FRB issued a proposed rule thatwould, among other things, require FHCs to holdadditional capital in connection with covered physicalcommodity activities.

Goldman Sachs 2019 Form 10-K 9

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Leverage Ratios. Under the Capital Framework, we andGS Bank USA are subject to Tier 1 leverage ratios and SLRsestablished by the FRB. In April 2018, the FRB and the OCCissued a proposed rule which would replace the current 2%SLR buffer for G-SIBs, including us, with a buffer equal to50% of their G-SIB surcharge. This proposal, together withthe adopted rule requiring use of SA-CCR for purposes ofcalculating the SLR, would implement certain of therevisions to the leverage ratio framework published by theBasel Committee in December 2017.

The Basel Committee adopted changes in June 2019 to theleverage ratio treatment of client-cleared derivatives andadopted a requirement to publicly disclose daily averagebalances for certain components of leverage ratiocalculations.

The U.S. federal bank regulatory agencies’ November 2019rule implementing SA-CCR similarly allows for greaterrecognition of collateral in the calculation of total leverageexposure relating to client-cleared derivative contracts.

CRR II establishes a 3% minimum leverage ratiorequirement for certain E.U. financial institutions,including GSI and GSIB. This requirement will begin toapply in June 2021.

See “Management’s Discussion and Analysis of FinancialCondition and Results of Operations — Equity CapitalManagement and Regulatory Capital” in Part II, Item 7 ofthis Form 10-K and Note 20 to the consolidated financialstatements in Part II, Item 8 of this Form 10-K forinformation about our and GS Bank USA’s Tier 1 leverageratios and SLRs, and GSI’s leverage ratio.

Liquidity Ratios. The Basel Committee’s framework forliquidity risk measurement, standards and monitoringrequires banking organizations to measure their liquidityagainst two specific liquidity tests: the Liquidity CoverageRatio (LCR) and the Net Stable Funding Ratio (NSFR).

The LCR rule issued by the U.S. federal bank regulatoryagencies and applicable to both us and GS Bank USA isgenerally consistent with the Basel Committee’s frameworkand is designed to ensure that a banking organizationmaintains an adequate level of unencumbered, high-qualityliquid assets equal to or greater than the expected net cashoutflows under an acute short-term liquidity stress scenario.The LCR rule issued by the European Commission andapplicable to GSI and GSIB is also generally consistent withthe Basel Committee’s framework. We are required tomaintain a minimum LCR of 100%. We disclose, on aquarterly basis, our average daily LCR. See “AvailableInformation” below and “Management’s Discussion andAnalysis of Financial Condition and Results of Operations— Equity Capital Management and Regulatory Capital” inPart II, Item 7 of this Form 10-K for information about ouraverage daily LCR.

The NSFR is designed to promote medium- and long-termstable funding of the assets and off-balance-sheet activitiesof banking organizations over a one-year time horizon. TheBasel Committee’s NSFR framework requires bankingorganizations to maintain a minimum NSFR of 100%.

The U.S. federal bank regulatory agencies issued a proposedrule in May 2016 that would implement the NSFR for largeU.S. banking organizations, including us and GS Bank USA,but have not yet released a final rule. CRR II implementsthe NSFR for certain E.U. financial institutions, includingGSG UK, GSI and GSIB during the Brexit transition period.

The FRB’s enhanced prudential standards require BHCswith $100 billion or more in total consolidated assets, tocomply with enhanced liquidity and overall riskmanagement standards, which include maintaining a levelof highly liquid assets based on projected funding needs for30 days, and increased involvement by boards of directorsin liquidity and overall risk management. Although theliquidity requirement under these rules has some similaritiesto the LCR, it is a separate requirement.

See “Management’s Discussion and Analysis of FinancialCondition and Results of Operations — Risk Management —Overview and Structure of Risk Management” and“— Liquidity Risk Management” in Part II, Item 7 of thisForm 10-K for information about the LCR and NSFR, as wellas our risk management practices and liquidity.

Stress Tests. As required by the FRB’s CCAR rules, wesubmit an annual capital plan for review by the FRB. Inaddition, we are required to perform company-run stresstests on an annual basis. As described in “AvailableInformation” below, we publish summaries of our stresstests results on our website.

Our annual stress test submission is incorporated into theannual capital plans that we submit to the FRB as part ofthe CCAR process for large BHCs, which is designed toensure that capital planning processes will permit continuedoperations by such institutions during times of economicand financial stress. As part of CCAR, the FRB evaluates aninstitution’s plan to make capital distributions, such as byrepurchasing or redeeming stock or making dividendpayments, across a range of macroeconomic and company-specific assumptions based on the institution’s and theFRB’s stress tests. If the FRB objects to an institution’scapital plan, the institution is generally prohibited frommaking capital distributions other than those to which theFRB has not objected. In addition, an institution faceslimitations on capital distributions to the extent that actualcapital issuances are less than the amounts indicated in itscapital plan.

10 Goldman Sachs 2019 Form 10-K

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

The FRB issued a proposed rule in April 2018 to establishstress buffer requirements. Under the proposal, the SCBwould replace the static component of the capitalconservation buffer. The SCB, subject to a minimum,would reflect stressed losses in the supervisory severelyadverse scenario of the FRB’s CCAR stress tests and wouldalso include four quarters of planned common stockdividends. The proposal would also introduce a stressleverage buffer requirement, similar to the SCB, whichwould apply to the Tier 1 leverage ratio. In addition, theproposal would require BHCs to reduce their plannedcapital distributions if those distributions would not beconsistent with the applicable capital buffer constraintsbased on the BHCs’ own baseline scenario projections.

Under rules adopted by the U.S. federal bank regulatoryagencies implementing 2018 amendments to the Dodd-Frank Act, depository institutions with total consolidatedassets between $100 billion and $250 billion, such as GSBank USA, are no longer required to conduct annualcompany-run stress tests. They are still required to havetheir own capital planning process. GSI and GSIB have theirown capital planning and stress testing process, whichincorporates internally designed stress tests and thoserequired under the PRA’s Internal Capital AdequacyAssessment Process.

Dividends and Stock Repurchases. Dividend paymentsto our shareholders and our stock repurchases are subjectto the oversight of the FRB.

U.S. federal and state laws impose limitations on thepayment of dividends by U.S. depository institutions, suchas GS Bank USA. In general, the amount of dividends thatmay be paid by GS Bank USA is limited to the lesser of theamounts calculated under a recent earnings test and anundivided profits test. Under the recent earnings test, adividend may not be paid if the total of all dividendsdeclared by the entity in any calendar year is in excess of thecurrent year’s net income combined with the retained netincome of the two preceding years, unless the entity obtainsprior regulatory approval. Under the undivided profits test,a dividend may not be paid in excess of the entity’sundivided profits (generally, accumulated net profits thathave not been paid out as dividends or transferred tosurplus).

The applicable U.S. banking regulators have authority toprohibit or limit the payment of dividends if, in the bankingregulator’s opinion, payment of a dividend wouldconstitute an unsafe or unsound practice in light of thefinancial condition of the banking organization.

Source of Strength. The Dodd-Frank Act requires BHCsto act as a source of strength to their bank subsidiaries andto commit capital and financial resources to support thosesubsidiaries. This support may be required by the FRB attimes when BHCs might otherwise determine not toprovide it. Capital loans by a BHC to a subsidiary bank aresubordinate in right of payment to deposits and to certainother indebtedness of the subsidiary bank. In addition, if aBHC commits to a U.S. federal banking agency that it willmaintain the capital of its bank subsidiary, whether inresponse to the FRB’s invoking its source-of-strengthauthority or in response to other regulatory measures, thatcommitment will be assumed by the bankruptcy trustee forthe BHC and the bank will be entitled to priority paymentin respect of that commitment, ahead of other creditors ofthe BHC.

Transactions between Affiliates. Transactions betweenGS Bank USA or its subsidiaries and Group Inc. or its othersubsidiaries and affiliates are subject to restrictions underthe Federal Reserve Act and regulations issued by the FRB.These laws and regulations generally limit the types andamounts of transactions (such as loans and other creditextensions, including credit exposure arising fromrepurchase and reverse repurchase agreements, securitiesborrowing and derivative transactions, from GS Bank USAor its subsidiaries to Group Inc. or its other subsidiaries andaffiliates and purchases of assets by GS Bank USA or itssubsidiaries from Group Inc. or its other subsidiaries andaffiliates) that may take place and generally require thosetransactions to be on market terms or better to GS BankUSA or its subsidiaries. These laws and regulationsgenerally do not apply to transactions between GS BankUSA and its subsidiaries.

The BHC Act prohibits the FRB from requiring a paymentby a BHC subsidiary to a depository institution if thefunctional regulator of that subsidiary objects to thepayment. In that case, the FRB could instead require thedivestiture of the depository institution and imposeoperating restrictions pending the divestiture.

Goldman Sachs 2019 Form 10-K 11

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

Resolution and Recovery. We are required by the FRBand the FDIC to submit a periodic plan for our rapid andorderly resolution in the event of material financial distressor failure (resolution plan). If the regulators jointlydetermine that an institution has failed to remediateidentified shortcomings in its resolution plan and that itsresolution plan, after any permitted resubmission, is notcredible or would not facilitate an orderly resolution underthe U.S. Bankruptcy Code, the regulators may jointlyimpose more stringent capital, leverage or liquidityrequirements or restrictions on growth, activities oroperations, or may jointly order the institution to divestassets or operations, in order to facilitate orderly resolutionin the event of failure. We submitted our 2019 resolutionplan in June 2019 and the FRB and FDIC did not identifydeficiencies or shortcomings. In October 2019, the FRB andFDIC adopted a rule requiring U.S. G-SIBs to submitresolution plans on a two-year cycle (alternating betweenfull and targeted submissions). Our next requiredsubmission is a targeted submission by July 1, 2021. See“Risk Factors — The application of Group Inc.’s proposedresolution strategy could result in greater losses for GroupInc.’s security holders” in Part I, Item 1A of this Form 10-Kand “Available Information” in Part I, Item 1 of thisForm 10-K for further information about our resolutionplan.

We are also required by the FRB to submit, on a periodicbasis, a global recovery plan that outlines the steps that wecould take to reduce risk, maintain sufficient liquidity, andconserve capital in times of prolonged stress.

The FDIC has issued a rule requiring each insureddepository institution (IDI) with $50 billion or more inassets, such as GS Bank USA, to provide a resolution plan.Our resolution plan for GS Bank USA must, among otherthings, demonstrate that it is adequately protected fromrisks arising from our other entities. GS Bank USA’s mostrecent resolution plan was submitted in June 2018. InApril 2019, the FDIC released an advanced notice ofproposed rulemaking about potential changes to itsresolution planning requirements for IDIs, including GSBank USA, and delayed the next round of IDI resolutionplan submissions until the rulemaking process is complete.

The U.S. federal bank regulatory agencies have adoptedrules imposing restrictions on qualified financial contracts(QFCs) entered into by G-SIBs, which became fully effectiveon January 1, 2020. The rules are intended to facilitate theorderly resolution of a failed G-SIB by limiting the ability ofthe G-SIB to enter into a QFC unless (i) the counterpartywaives certain default rights in such contract arising uponthe entry of the G-SIB or one of its affiliates into resolution,(ii) the contract does not contain enumerated prohibitionson the transfer of such contract and/or any related creditenhancement, and (iii) the counterparty agrees that thecontract will be subject to the special resolution regimes setforth in the Dodd-Frank Act orderly liquidation authority(OLA) and the Federal Deposit Insurance Act of 1950(FDIA), described below. Compliance can be achieved byadhering to the International Swaps and DerivativesAssociation Universal Resolution Stay Protocol (ISDAUniversal Protocol) or International Swaps and DerivativesAssociation 2018 U.S. Resolution Stay Protocol (U.S. ISDAProtocol) described below.

Certain of our subsidiaries, along with those of a number ofother major global banking organizations, adhere to theISDA Universal Protocol, which was developed andupdated in coordination with the Financial Stability Board(FSB), an international body that sets standards andcoordinates the work of national financial authorities andinternational standard-setting bodies. The ISDA UniversalProtocol imposes a stay on certain cross-default and earlytermination rights within standard ISDA derivativecontracts and securities financing transactions betweenadhering parties in the event that one of them is subject toresolution in its home jurisdiction, including a resolutionunder the OLA or the FDIA in the U.S. In addition, certainGroup Inc. subsidiaries adhere to the U.S. ISDA Protocol,which was based on the ISDA Universal Protocol and wascreated to allow market participants to comply with thefinal QFC rules adopted by the federal bank regulatoryagencies.

12 Goldman Sachs 2019 Form 10-K

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

The amended E.U. Bank Recovery and Resolution Directive(BRRD II) establishes a framework for the recovery andresolution of financial institutions in the E.U., such as GSIand GSIB during the Brexit transition period. The BRRD IIprovides national supervisory authorities with tools andpowers to pre-emptively address potential financial crises inorder to promote financial stability and minimizetaxpayers’ exposure to losses, such as the power to imposea temporary stay. The BRRD II requires E.U. member statesto grant “bail-in” powers to E.U. resolution authorities torecapitalize a failing entity by writing down its unsecureddebt or converting its unsecured debt into equity. Financialinstitutions in the E.U. must provide that contractsrecognize those temporary stay and bail-in powers unlessdoing so would be impracticable. Further, certain U.K.financial institutions, including GSI and GSIB, have beenrequired by the PRA to submit solvent wind-down plans onhow they could be wound down in a stressed environment.

Total Loss-Absorbing Capacity (TLAC). The FRB hasissued a rule addressing U.S. implementation of the FSB’sTLAC principles and term sheet on minimum TLACrequirements for G-SIBs. The rule (i) establishes minimumTLAC requirements, (ii) establishes minimum “eligiblelong-term debt” (i.e., debt that is unsecured, has a maturityof at least one year from issuance and satisfies certainadditional criteria) requirements, (iii) prohibits certainparent company transactions and (iv) caps the amount ofparent company liabilities that are not eligible long-termdebt.

The rule also prohibits a BHC that has been designated as aU.S. G-SIB from (i) guaranteeing liabilities of subsidiariesthat are subject to early termination provisions if the BHCenters into an insolvency or receivership proceeding, subjectto an exception for guarantees permitted by rules of the U.S.federal banking agencies imposing restrictions on QFCs;(ii) incurring liabilities guaranteed by subsidiaries;(iii) issuing short-term debt; or (iv) entering into derivativesand certain other financial contracts with externalcounterparties.

Additionally, the rule caps, at 5% of the value of the parentcompany’s eligible TLAC, the amount of unsecurednon-contingent third-party liabilities that are not eligiblelong-term debt that could rank equally with or junior toeligible long-term debt.

The FRB, the OCC and the FDIC issued a proposed rule inApril 2019 that would require “Advanced approach”banking organizations, such as us, to deduct from their ownregulatory capital certain investments above thresholds inunsecured debt instruments issued by G-SIBs, includingthose issued for purposes of satisfying TLAC requirements.

The BRRD II subjects institutions to a minimum requirementfor own funds and eligible liabilities (MREL), which isgenerally consistent with the FSB’s TLAC standard. InJune 2018, the Bank of England published a statement ofpolicy on internal MREL, which requires a material U.K.subsidiary of an overseas banking group, such as GSI, tomeet a minimum internal MREL requirement to facilitate thetransfer of losses to its resolution entity, which for GSI isGroup Inc. The transitional minimum internal MRELrequirement began to phase in from January 1, 2019 and willbecome fully effective on January 1, 2022. In order to complywith the MREL statement of policy, bail-in triggers havebeen provided to the Bank of England over certainintercompany regulatory capital and senior debt instrumentsissued by GSI. These triggers enable the Bank of England towrite down such instruments or convert such instruments toequity. The triggers can be exercised by the Bank of Englandif it determines that GSI has reached the point ofnon-viability and the FRB and the FDIC have not objected tothe bail-in or if Group Inc. enters bankruptcy or similarproceedings.

CRR II and the BRRD II are designed to, among otherthings, implement the FSB’s minimum TLAC requirementfor G-SIBs. For example, CRR II requires subsidiaries of anon-E.U. G-SIB that account for more than 5% of itsRWAs, operating income or leverage exposure, such asGSG UK, to meet 90% of the TLAC requirement applicableto E.U. G-SIBs.

CRD V requires a non-E.U. group with more than€40 billion of assets in the E.U., such as us, to establish anE.U. intermediate holding company (E.U. IHC) if it has twoor more of certain types of E.U. financial institutionsubsidiaries, including broker-dealers and banks. CRR IIrequires E.U. IHCs to satisfy MREL requirements andcertain other prudential requirements. The directives aresubject to implementing rulemakings by E.U. memberstates, which have not yet occurred.

Insolvency of an IDI or a BHC. Under the FDIA, if the FDICis appointed as conservator or receiver for an IDI such as GSBank USA, upon its insolvency or in certain other events, theFDIC has broad powers, including the power:

‰ To transfer any of the IDI’s assets and liabilities to a newobligor, including a newly formed “bridge” bank, withoutthe approval of the depository institution’s creditors;

‰ To enforce the IDI’s contracts pursuant to their termswithout regard to any provisions triggered by theappointment of the FDIC in that capacity; or

‰ To repudiate or disaffirm any contract or lease to whichthe IDI is a party, the performance of which is determinedby the FDIC to be burdensome and the repudiation ordisaffirmance of which is determined by the FDIC topromote the orderly administration of the IDI.

Goldman Sachs 2019 Form 10-K 13

THE GOLDMAN SACHS GROUP, INC. AND SUBSIDIARIES

In addition, the claims of holders of domestic depositliabilities and certain claims for administrative expensesagainst an IDI would be afforded a priority over othergeneral unsecured claims, including deposits at non-U.S.branches and claims of debtholders of the IDI, in the“liquidation or other resolution” of such an institution byany receiver. As a result, whether or not the FDIC eversought to repudiate any debt obligations of GS Bank USA,the debtholders (other than depositors at U.S. branches)would be treated differently from, and could receive, ifanything, substantially less than, the depositors at U.S.branches of GS Bank USA.

The Dodd-Frank Act created a new resolution regime(known as OLA) for BHCs and their affiliates that aresystemically important. Under OLA, the FDIC may beappointed as receiver for the systemically importantinstitution and its failed non-bank subsidiaries if, upon therecommendation of applicable regulators, the U.S.Secretary of the Treasury determines, among other things,that the institution is in default or in danger of default, thatthe institution’s failure would have serious adverse effectson the U.S. financial system and that resolution under OLAwould avoid or mitigate those effects.

If the FDIC is appointed as receiver under OLA, then thepowers of the receiver, and the rights and obligations ofcreditors and other parties who have dealt with theinstitution, would be determined under OLA, and notunder the bankruptcy or insolvency law that wouldotherwise apply. The powers of the receiver under OLAwere generally based on the powers of the FDIC as receiverfor depository institutions under the FDIA.

Substantial differences in the rights of creditors existbetween OLA and the U.S. Bankruptcy Code, including theright of the FDIC under OLA to disregard the strict priorityof creditor claims in some circumstances, the use of anadministrative claims procedure to determine creditors’claims (as opposed to the judicial procedure utilized inbankruptcy proceedings), and the right of the FDIC totransfer claims to a “bridge” entity. In addition, OLA limitsthe ability of creditors to enforce certain contractual cross-defaults against affiliates of the institution in receivership.The FDIC has issued a notice that it would likely resolve afailed FHC by transferring its assets to a “bridge” holdingcompany under its “single point of entry” or “SPOE”strategy pursuant to OLA.

Deposit Insurance. Deposits at GS Bank USA have thebenefit of FDIC insurance up to the applicable limits. TheFDIC’s Deposit Insurance Fund is funded by assessments onIDIs. GS Bank USA’s assessment (subject to adjustment bythe FDIC) is currently based on its average totalconsolidated assets less its average tangible equity duringthe assessment period, its supervisory ratings and specifiedforward-looking financial measures used to calculate theassessment rate. In addition, deposits at GSIB are coveredby the Financial Services Compensation Scheme up to theapplicable limits.

Prompt Corrective Action. The U.S. Federal DepositInsurance Corporation Improvement Act of 1991 (FDICIA)requires the U.S. federal bank regulatory agencies to take“prompt corrective action” in respect of depositoryinstitutions that do not meet specified capital requirements.FDICIA establishes five capital categories for FDIC-insuredbanks, such as GS Bank USA: well-capitalized, adequatelycapitalized, undercapitalized, significantly undercapitalizedand critically undercapitalized.