goldsmith-banking: mutual acceptance and interbanker clearing in restoration london

TRANSCRIPT

Goldsmith-Banking: Mutual Acceptance and InterbankerClearing in Restoration London*

Stephen Quinn

Department of Economics, Texas Christian University

During the second half of the 17th century, London’s goldsmith-bankers formed asystem of banking through mutual debt acceptance and interbanker clearing. Widespreadacceptance of bank notes, orders, and bills created positive externalities for memberbankers and promoted the use of bank supplied media of exchange during the FinancialRevolution in England. Mutual acceptance by goldsmith-bankers arose endogenously as adominant strategy Nash equilibrium. The bilateral clearing of these acceptances producedincentive compatible co-monitoring between goldsmith-bankers. The responsiveness ofco-monitoring is supported by statistical analysis of the accounts of the Restoration eragoldsmith Edward Backwell. Systemic cohesion was further reinforced by the screening ofnew members through apprenticeship.r 1997 Academic Press

By the Restoration of Charles II in 1660, London’s goldsmiths had emerged asa network of bankers.1 The number of goldsmith-bankers has been estimated at 32in 1670, 44 in 1677, and 42 in 1700.2 Some were little more than pawn-brokerswhile others were full service bankers. The story of their system, however, buildson the financial services goldsmiths offered as fractional reserve, note issuingbankers.3 In the 17th century, notes, orders, and bills (collectively called demand-

* I thank Larry Neal, Charles Calomiris, Paul Newbold, Forrest Capie, Eugene White, GeorgeSelgin, Larry White, Jeff Lacker, David Mitchell, David Leblang, Leslie Pressnell, Lynne Kiesling,Joe Mason, three anonymous referees, the Cliometrics Society, the Federal Reserve Bank ofRichmond, the Economic History Seminar at the University of Illinois, and the Centre for Metropoli-tan Studies. Little of the original research herein would have been possible without the generoussupport provided by Alison Turton and Philip Winterbottom, archivists at the Royal Bank of Scotland;the Social Sciences Research Council; and the Institute for Humane Studies.

1 An earlier and less developed working paper on this topic previously appeared as Quinn (1995).2 The 1670 and 1700 estimates are from Hilton-Price (1890, pp. 182, 184–185). The 1677 estimate

is from theLittle London Directory(1677).3 Richards (1929, pp. 23–24) summarizes, ‘‘Interest was paid on deposits; loans were supplied;

bills of exchange, tallies and various types of Treasury-Exchequer payment orders were discounted;promissory notes, which circulated freely, were issued; cheques were used; bullion was bought andsold; foreign coins were changed; systematic accounts were kept in special ledgers.’’

EXPLORATIONS IN ECONOMIC HISTORY34, 411–432 (1997)ARTICLE NO. EH970682

411

0014-4983/97 $25.00Copyrightr 1997 by Academic Press

All rights of reproduction in any form reserved.

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

No. of Pages—22 First page no.—411 Last page no.—432

able debt) acted as media of exchange that spared the costs of moving, protectingand assaying specie (van der Wee, 1977). Merchants then reduced the costs ofrepeatedly creating these paper debts by transferring the ownership of existingdebt.4 London’s goldsmith-bankers specialized in supplying these transferablenotes and bills to the public (Horsefield, 1983, pp. xii–xv). A banking systemdeveloped because goldsmiths accepted the bank notes of rivals. A web ofclearing relationships between the bankers then followed.

The goldsmiths’ banking network was an important advance in the series of17th century developments known as the Financial Revolution because reliableacceptance encouraged note circulation and the adoption by the public of thethen-called ‘‘banking habit’’ (Roseveare, 1991, pp. 19–20). Merchants wereaware that the Dutch had managed to use their public bank in Amsterdam tosupport paper that passed in trade like coin (Dickson, 1967, p. 5). While theEnglish debated the founding of a similar institution, goldsmith-bankers werealready operating a paper-dominated system of payments (Roseveare, 1991, p.83). Additionally, the goldsmiths’ system facilitated tax collection, channeledmoney into the credit market, and ameliorated the declining state of the coinage(Mayhew, 1995; Horsefield, 1983; Quinn, 1994).5 When the Bank of England wasfounded in 1694, its practices were patterned after those of the already well-established goldsmiths (Clapham, 1944, p. 16).6

How did the goldsmiths’ system of banking work? Acceptance and clearingwere not governed by formal rules to overcame coordination problems. Rather, Isuggest this network coalesced endogenously through the rivalrous self-interest ofmembers. Bankers wanted to take business from each other, and acceptance wasan opportunity to do so. Increased circulation was then derived from the actions ofcompetitors, so positive externalities were an emergent characteristic whosefeedback locked-in mutual acceptance.7 The clearing that followed mutual accep-tance brought the additional benefit of acting to discipline bankers. Clearingprovided the information and incentives needed for banker co-monitoring whichalso improved systemic stability. Finally, the goldsmiths knew each other wellbecause of the guild system of apprenticeship. Like clearing, familiarity andreputation improved stability.

The accounts of a London goldsmith-banker, Edward Backwell, providequantitative evidence of the acceptance–clearing system of London’s goldsmith-bankers. Backwell’s ledgers run from March of 1663 until March of 1672.8 His

4 For the development of the legal institutions supporting transferable debt, see Rogers (1995).5 Goldsmiths also supplied intermediation in the credit market similar to Parisian notaries;

however, goldsmith-bankers were fractional reserve bankers (Hoffmanet al.,1995).6 The Bank of England’s fractional reserve banking and note issue were in contrast to the exchange

banks of the European Continent (van Dillen, 1934).7 For an example of lock-in, see David (1985). For an example of emergent properties, see

Krugman (1996).8 Backwell’s ledgers miss three months of records from September through December of 1663 and

nine months from March through December of 1665. The extant ledgers are Ledgers I (March 1663 to

412 STEPHEN QUINN

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

books are the only extant ledgers from a Lombard Street goldsmith-banker priorto the 1690s. While one banker’s clearing accounts with his fellow bankers cannotportray the entire system, Edward Backwell’s accounts do detail his acceptancesfrom the public. Earlier writers have interpreted Backwell’s extensive relationswith other goldsmith-bankers as evidence that the goldsmith-banker was a‘‘banker’s banker.’’ Richards concluded that Edward Backwell:

was undoubtedly both the central or reserve bank and the clearing house of the post-Restoration period. [Backwell’s bank] was the indispensable precursor of the Bank ofEngland, a precursor which was of paramount importance in this outstanding era of Englisheconomic expansion (Richards, 1929, p. 30).

Although the network of goldsmith-bankers was an ‘‘indispensable precursor ofthe Bank of England,’’ Edward Backwell was not a clearing house. At least 19goldsmith-bankers held accounts with Backwell over the decade from 1663 to1672, but they did not clear with each otherthrough Backwell.9 Rather, eachbanker cleared bilaterally with Backwell. Similarly, the ledgers of the small butgrowing West End goldsmith, Sir Francis Child, record regular bilateral clearingactivities with a number of goldsmith-bankers in the 1670s (Mitchell, 1994, p.34).

This paper brings forward a new interpretation of Edward Backwell as animportant member in a system of mutual acceptance and bilateral clearing. Whilethis paper only considers evidence from 1663 to 1672, the story runs much longer.The system’s roots began somewhere in the years of the Protectorate (1648–1660).10 With the Stop of the Exchequer in 1672, a half dozen goldsmith-bankerswho lent large sums to Charles II were forced to suspend payments (Horsefield,1982; Carruthers, 1996). Edward Backwell was one of these ruined bankers, andthis marked the end of his ledgers. Many goldsmith-bankers, however, were notmajor lenders to the Crown and did carry on. Five years after the Stop, 44goldsmith-bankers were listed as keeping running cashes. Despite the plague in1665, the Great Fire in 1666, the Stop of the Exchequer in 1672, a panic in 1682,and the Glorious Revolution of 1688, the system of goldsmith-bankers continuedfunctioning through the foundation of the Bank of England in 1694 and the turn ofthe 18th century.

March 1663/4), K (March 1664 to September 1664), M (September 1664 to March 1664/5), O(January 1665/6 to December 1666), P (January 1666/7 to March 1667/8), Q (March 1668 to March1668/9), R (March 1669 to March 1669/70), S (March 1670 to March 1670/1), T (March 1671 toMarch 1671/2), (EB/1–9). The ledgers are maintained by the Royal Bank of Scotland, London.

9 Backwell also had regular clearing transactions with the money-scrivener firm of Morris andClayton. The money-scriveners were substitute financial intermediaries specializing in mortgages andformal deeds (Melton, 1986). Their accounts with Backwell demonstrate that the scriveners andgoldsmiths both benefited from participating in a system of mutual debt acceptance.

10 For example, the first extant Backwell ledger is labeled letter ‘‘I’’ and begins in January of 1663.Note that there was no Ledger J. If each of the earlier ledgers covered a year, then Backwell’s first bankledger began in 1655.

413GOLDSMITH-BANKING

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

Section I argues that goldsmiths had an incentive to accept rival notes withoutformal coordination, fees, or the maintenance of covering balances. This systemof acceptance created uncleared balances between goldsmith-bankers. Section IIargues that the web of interbanker clearing created by these balances encouragedco-monitoring among bankers similar to the free banking era in the United States(Gorton, 1996). Statistical analysis of a sample of Backwell’s clearing activitiesindicates the goldsmith did respond to potentially abusive behavior by otherbankers, so the system did provide a degree of self-policing. Section III adds theapprenticeship system as another institution that reinforced the goldsmith-banking system. In lacking a formal institutional structure governing acceptanceand clearing, goldsmith-bankers evince how economic incentives, supported byapprenticeship, proximity, and social ties, shaped an early modern bankingnetwork integral to the Financial Revolution.

I. ENDOGENOUS ACCEPTANCES

In the 1660s, Edward Backwell accepted from the public the notes and ordersof his rival bankers. By doing so, Backwell extended credit to other bankers untilthe balance was cleared. The goldsmith did not charge fees for this service.11

Instead, par acceptance of local notes was the norm. Gorton (1996, p. 353) hasfound similar local par acceptance in the American free banking experience. Thissection presents a story within which Backwell, as a representative goldsmith,chose this process of acceptance that generated uncleared balances. This systemof acceptance need not have required a formal set of rules, and researchers knowof no formal institution governing acceptance or clearing. Like a market, theacceptance and clearing network could order itself out of bankers acting in theirown interest. A basic game theoretic characterizes the point that London’s systemof mutual acceptance during the second half of the 17th century can be viewed asendogenous to the self-interest of goldsmiths.

Taken together, London’s goldsmith-bankers averaged negative balances (theyowed Backwell) resulting from the goldsmith’s acceptance of their debts. Figure 1presents the aggregate daily balance of 18 goldsmith-bankers with EdwardBackwell. A few outlier accounts are excluded to highlight the daily acceptancebehavior addressed in this section.12At various times Backwell held both positive

11 At 6% annual interest (the maximum legal interest rate at the time), Backwell’s average dailybalance of2£1,445 from Table 1 cost the goldsmith-banker nearly £700 in forgone interest over the 8years sampled. If the other goldsmiths held similar balances against Backwell, then the net position(his charges against them less their charges against him) would have been smaller still. Even assumingno offsetting balances, the £700 in opportunity costs accounted for less than 1% of Backwell’s £77,279netincome from lending (interest received less interest paid) over the same period.

12 Sundays have been excluded from Fig. 1, and the rare Sunday transaction has been moved to theprior Saturday. The sample includes the earliest generations of goldsmith-bankers: John Colvill, JohnLindsay, John Mawson, Francis Meynell, John Portman, Jeremiah Snow, George Snell, and RobertWelstead. Thomas Cook, John Hinde, Benjamin and Edmund Hinton, Joseph Horneby, ThomasKirwood, Thomas Pardo, Thomas Row, Bernard Turner and Thomas Williams all began accounts with

414 STEPHEN QUINN

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

and negative balances relative to his fellow goldsmith-bankers with a daily meanof 2£1,445 and daily median of2£813 over 2,500 days as reported in Table 1.13

The series had a standard deviation of £4,700. Each goldsmith-banker’s accountwith Backwell was encoded and calculated separately and then summed. Theseaccounts mingled acceptances and clearings with direct loans and other businesstransactions. In a detailed analysis of clearing, Section II separates acceptancesfor a sample of three bankers.

I propose early bankers like Backwell were in a type of game in whichacceptance was the dominant strategy. Instead of charging fees or discounts onacceptances, the story begins with the premise that a competing banker wouldaccept a rival’s note at par in exchange for his own bank debt because, ‘‘If thenotes acquired are redeemed sooner than the notes issued, interest-earning assetscan be purchased and held in the interim (White, 1987, p. 227).’’ Bankersaccepted a rival’s note if the cost of clearing was less than the benefit. The benefitwas from the discounted stream of earnings from investing the acceptance. Thecost would be the shoe leather transaction costs and the risk of a rival’s default.This motivation was not predicated on rivals reciprocating, so the positive

Backwell after March 1663. Only those that have been identified by other sources (Heal, 1935;Hilton-Price, 1890) as goldsmith-bankers have been listed. As yet unknown bankers are not included,so the sample is biased towards exclusion. Figure 1 excludes the Vyners and also excludesextraordinary spikes in the balances of Sir Francis Meynell and Thomas Row. On April 18, 1663,Meynell was credited by Backwell for £34,666:13:4 on behalf of money received by the sale ofDunkirk. In August of 1670, Row deposited over £30,000 in foreign coin with Backwell. In Januaryand February of 1671, Row was repaid by the East India Company for whom Backwell was a banker.

13 The balances from January 1, 1663/4 to March 24, 1664 and from March 25, 1665 to December31, 1665 are not included in the summary statistics.

FIG. 1. Bankers’ balance with Backwell.

415GOLDSMITH-BANKING

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

externalities created by mutual acceptance emerged as a result of each bankerpursuing his best, uncoordinated strategy.

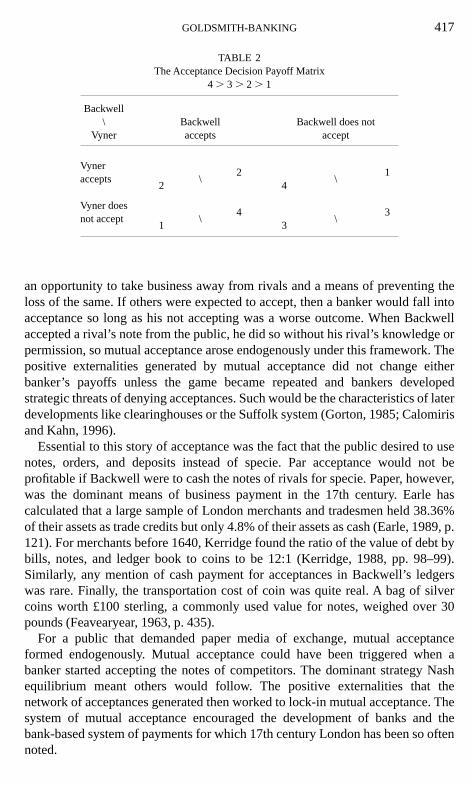

Now consider what happens when a second goldsmith-banker, say RobertVyner, faced the same situation as Backwell. Assume Vyner and Backwell werethe only bankers and had identical shops. Also, assume the public kept all theirspecie in these two bankers’ vaults. These simplifying assumptions made changesin reserves between the two bankers equal but opposite because merchants wouldretain the other banker’s note if denied acceptance. When a merchant presented aVyner note to Backwell, that merchant was shifting a deposit. Such a transferallowed Backwell to expand his lending and forced Vyner to contract his lendingby the same amount. The choice for each banker was to accept and clear theoffered notes or to not accept. This created a four cell payoff matrix in which theresults for each banker could be ranked. Backwell would most prefer to accept(ranked 4 for Backwell) when Vyner did not accept an offsetting note onBackwell. The same situation would be Vyner’s least preferred outcome becauseof the loss of business to Backwell (ranked 1 for Vyner). The reverse situationswitched the rankings to Vyner’s most favored outcome and Backwell’s leastfavored outcome. The other two cells report when both bankers behaved identi-cally. If both bankers did not accept, then neither gained nor lost which placedthem between either extreme (ranked 3). If both did accept, then no change inbalances occurred, but some clearing cost were incurred (ranked 2). Note that therelative ranking of mutual acceptance to mutual nonacceptance did not matter tothe game’s outcome so long as both were better than rank 1 and worse than rank 4.

With these payoffs, the dominant strategy for either banker was to accept. Table2 presents the payoff matrix for Vyner and Backwell with outcomes ranked 4.3 . 2 . 1 from each banker’s perspective. This Nash equilibrium captures whycompetitive bankers would take to accepting each other’s notes. Acceptance was

TABLE 1Distribution of Daily Balances for All Bankers on Edward Backwell

from January 1663 through March of 1672a

By number ofobservations

By value of observations(standard normal distribution)

Minimum 5 2£17,48710% 2£7,731 2£12,34933% 2£2,038 2£3,34050% Median5 2£813 Mean5 2£1,44566% 2£16 £44990% £3,450 £9,459

Maximum5 £17,476

Source.Backwell’s Ledgers (Royal Bank of Scotland: London), EB/1–9.a Distribution excludes missing observations for January through March

1663/4 and March through December 1665.

416 STEPHEN QUINN

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

an opportunity to take business away from rivals and a means of preventing theloss of the same. If others were expected to accept, then a banker would fall intoacceptance so long as his not accepting was a worse outcome. When Backwellaccepted a rival’s note from the public, he did so without his rival’s knowledge orpermission, so mutual acceptance arose endogenously under this framework. Thepositive externalities generated by mutual acceptance did not change eitherbanker’s payoffs unless the game became repeated and bankers developedstrategic threats of denying acceptances. Such would be the characteristics of laterdevelopments like clearinghouses or the Suffolk system (Gorton, 1985; Calomirisand Kahn, 1996).

Essential to this story of acceptance was the fact that the public desired to usenotes, orders, and deposits instead of specie. Par acceptance would not beprofitable if Backwell were to cash the notes of rivals for specie. Paper, however,was the dominant means of business payment in the 17th century. Earle hascalculated that a large sample of London merchants and tradesmen held 38.36%of their assets as trade credits but only 4.8% of their assets as cash (Earle, 1989, p.121). For merchants before 1640, Kerridge found the ratio of the value of debt bybills, notes, and ledger book to coins to be 12:1 (Kerridge, 1988, pp. 98–99).Similarly, any mention of cash payment for acceptances in Backwell’s ledgerswas rare. Finally, the transportation cost of coin was quite real. A bag of silvercoins worth £100 sterling, a commonly used value for notes, weighed over 30pounds (Feavearyear, 1963, p. 435).

For a public that demanded paper media of exchange, mutual acceptanceformed endogenously. Mutual acceptance could have been triggered when abanker started accepting the notes of competitors. The dominant strategy Nashequilibrium meant others would follow. The positive externalities that thenetwork of acceptances generated then worked to lock-in mutual acceptance. Thesystem of mutual acceptance encouraged the development of banks and thebank-based system of payments for which 17th century London has been so oftennoted.

TABLE 2The Acceptance Decision Payoff Matrix

4 . 3 . 2 . 1

Backwell\

VynerBackwellaccepts

Backwell does notaccept

Vyneraccepts

2\

24

\1

Vyner doesnot accept

1\

43

\3

417GOLDSMITH-BANKING

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

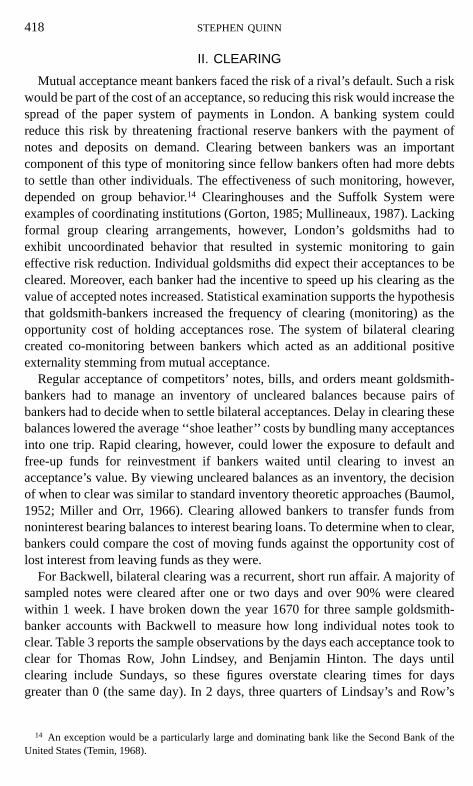

II. CLEARING

Mutual acceptance meant bankers faced the risk of a rival’s default. Such a riskwould be part of the cost of an acceptance, so reducing this risk would increase thespread of the paper system of payments in London. A banking system couldreduce this risk by threatening fractional reserve bankers with the payment ofnotes and deposits on demand. Clearing between bankers was an importantcomponent of this type of monitoring since fellow bankers often had more debtsto settle than other individuals. The effectiveness of such monitoring, however,depended on group behavior.14 Clearinghouses and the Suffolk System wereexamples of coordinating institutions (Gorton, 1985; Mullineaux, 1987). Lackingformal group clearing arrangements, however, London’s goldsmiths had toexhibit uncoordinated behavior that resulted in systemic monitoring to gaineffective risk reduction. Individual goldsmiths did expect their acceptances to becleared. Moreover, each banker had the incentive to speed up his clearing as thevalue of accepted notes increased. Statistical examination supports the hypothesisthat goldsmith-bankers increased the frequency of clearing (monitoring) as theopportunity cost of holding acceptances rose. The system of bilateral clearingcreated co-monitoring between bankers which acted as an additional positiveexternality stemming from mutual acceptance.

Regular acceptance of competitors’ notes, bills, and orders meant goldsmith-bankers had to manage an inventory of uncleared balances because pairs ofbankers had to decide when to settle bilateral acceptances. Delay in clearing thesebalances lowered the average ‘‘shoe leather’’ costs by bundling many acceptancesinto one trip. Rapid clearing, however, could lower the exposure to default andfree-up funds for reinvestment if bankers waited until clearing to invest anacceptance’s value. By viewing uncleared balances as an inventory, the decisionof when to clear was similar to standard inventory theoretic approaches (Baumol,1952; Miller and Orr, 1966). Clearing allowed bankers to transfer funds fromnoninterest bearing balances to interest bearing loans. To determine when to clear,bankers could compare the cost of moving funds against the opportunity cost oflost interest from leaving funds as they were.

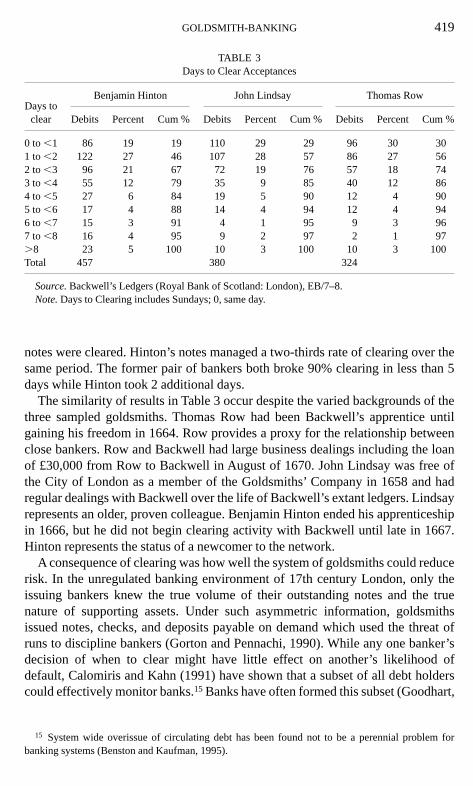

For Backwell, bilateral clearing was a recurrent, short run affair. A majority ofsampled notes were cleared after one or two days and over 90% were clearedwithin 1 week. I have broken down the year 1670 for three sample goldsmith-banker accounts with Backwell to measure how long individual notes took toclear. Table 3 reports the sample observations by the days each acceptance took toclear for Thomas Row, John Lindsey, and Benjamin Hinton. The days untilclearing include Sundays, so these figures overstate clearing times for daysgreater than 0 (the same day). In 2 days, three quarters of Lindsay’s and Row’s

14 An exception would be a particularly large and dominating bank like the Second Bank of theUnited States (Temin, 1968).

418 STEPHEN QUINN

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

notes were cleared. Hinton’s notes managed a two-thirds rate of clearing over thesame period. The former pair of bankers both broke 90% clearing in less than 5days while Hinton took 2 additional days.

The similarity of results in Table 3 occur despite the varied backgrounds of thethree sampled goldsmiths. Thomas Row had been Backwell’s apprentice untilgaining his freedom in 1664. Row provides a proxy for the relationship betweenclose bankers. Row and Backwell had large business dealings including the loanof £30,000 from Row to Backwell in August of 1670. John Lindsay was free ofthe City of London as a member of the Goldsmiths’ Company in 1658 and hadregular dealings with Backwell over the life of Backwell’s extant ledgers. Lindsayrepresents an older, proven colleague. Benjamin Hinton ended his apprenticeshipin 1666, but he did not begin clearing activity with Backwell until late in 1667.Hinton represents the status of a newcomer to the network.

A consequence of clearing was how well the system of goldsmiths could reducerisk. In the unregulated banking environment of 17th century London, only theissuing bankers knew the true volume of their outstanding notes and the truenature of supporting assets. Under such asymmetric information, goldsmithsissued notes, checks, and deposits payable on demand which used the threat ofruns to discipline bankers (Gorton and Pennachi, 1990). While any one banker’sdecision of when to clear might have little effect on another’s likelihood ofdefault, Calomiris and Kahn (1991) have shown that a subset of all debt holderscould effectively monitor banks.15 Banks have often formed this subset (Goodhart,

15 System wide overissue of circulating debt has been found not to be a perennial problem forbanking systems (Benston and Kaufman, 1995).

TABLE 3Days to Clear Acceptances

Days toclear

Benjamin Hinton John Lindsay Thomas Row

Debits Percent Cum % Debits Percent Cum % Debits Percent Cum %

0 to ,1 86 19 19 110 29 29 96 30 301 to ,2 122 27 46 107 28 57 86 27 562 to ,3 96 21 67 72 19 76 57 18 743 to ,4 55 12 79 35 9 85 40 12 864 to ,5 27 6 84 19 5 90 12 4 905 to ,6 17 4 88 14 4 94 12 4 946 to ,7 15 3 91 4 1 95 9 3 967 to ,8 16 4 95 9 2 97 2 1 97.8 23 5 100 10 3 100 10 3 100Total 457 380 324

Source.Backwell’s Ledgers (Royal Bank of Scotland: London), EB/7–8.Note.Days to Clearing includes Sundays; 0, same day.

419GOLDSMITH-BANKING

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

1988, pp. 57–76). Within a clearing system, increased note issue by individualbankers led to more acceptances by rivals and consequently more redemptionswith the issuing banker through interbanker clearing.16 Gorton and Mullineaux(1987) have shown how clearinghouses consolidated this function, but thegoldsmiths did not have such a coordinating institution. London’s monitoringdepended on the incentives of individual bankers to watch their fellow bankers.Because goldsmiths held uncleared balances after acceptances, they had everyincentive to make sure competitors’ notes would be honored, but the ability ofbilateral clearing to discipline bankers also depended on when bankers cleared.Responsiveness to the amount of acceptances created an important additionalmonitoring feature. For pre-American Civil War bank note markets, Gorton hasconcluded that, ‘‘higher-risk banks at a given location are monitoried via morefrequent note redemptions (Gorton, 1996, p. 352).’’ For 17th century goldsmiths,increased public redemption of rival notes meant more acceptances. Additionalacceptances increased inventory costs and encouraged speedier redemption. Suchco-monitoring would improve the stability of the entire banking system becauseclearing that responded to the volume of acceptances disciplined network mem-bers.

The regression analysis tests the hypothesis that Backwell responded toacceptances in a manner consistent with banker co-monitoring. The sampleaccounts of three goldsmith-bankers—Thomas Row, John Lindsay, and BenjaminHinton—have been selected because all three operated on Lombard Street withBackwell and all three had clearing activities of similar sizes. Table 4 provides thesummary statistics for each banker’s distribution of acceptances to be cleared withBackwell in 1670. Although Benjamin Hinton had 50% more acceptances thanThomas Row did, all three bankers had similar flows of notes by the public into

16 The overall effectiveness of co-monitoring via clearing is an ongoing debate (Goodhart, 1988;Dowd, 1993; Selgin and White, 1994).

TABLE 4Characteristics of Backwell Acceptances by Banker in 1670

Benjamin Hinton John Lindsay Thomas Row

Mean £161 £229 £173Median £100 £116 £100Mode £100 £100 £100

(No. of modal observations,% of total observations) (64, 14%) (48, 13%) (33, 10%)

Standard deviation £217 £317 £201Minimum £5.40 £9.95 £6.75Maximum £2,000 £2,911 £1,447Number of observations 457 380 324

Source.Backwell’s Ledgers (Royal Bank of Scotland: London), EB/7–8.

420 STEPHEN QUINN

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

Backwell. All had identical modes £100. Their median note values were also £100except for Lindsay’s median of £116.

Unlike the centralization of a clearinghouse, however, goldsmith-banker moni-toring was conducted in a pair-wise manner, so the quantity of debt accepted by arival banker reduced the rewards to clearing. For example, Backwell’s opportu-nity cost of not clearing was the risk and forgone interest from his expectednetposition. Backwell did not know another banker’s acceptances until clearingoccurred, so when other bankers would choose to initiate clearing could not bepredicted by Backwell’s ledgers. A test of whether Backwell’s acceptances causeda shortening of clearing times thus had a persistent error because the records donot state who initiated clearing. We can, however, predict that when a clearingbalance tended to favor Backwell, his acceptances should affect his clearingbehavior. In contrast, when Backwell regularly faced an adverse clearing position,his acceptances should fail to predict the timing of clearing. Again, whenBackwell owed more in settlement than he was owed, the other goldsmith wouldinitiate most clearing.

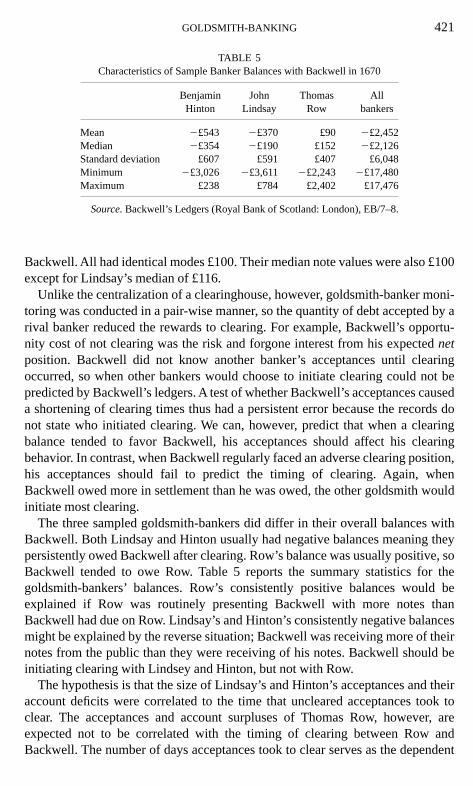

The three sampled goldsmith-bankers did differ in their overall balances withBackwell. Both Lindsay and Hinton usually had negative balances meaning theypersistently owed Backwell after clearing. Row’s balance was usually positive, soBackwell tended to owe Row. Table 5 reports the summary statistics for thegoldsmith-bankers’ balances. Row’s consistently positive balances would beexplained if Row was routinely presenting Backwell with more notes thanBackwell had due on Row. Lindsay’s and Hinton’s consistently negative balancesmight be explained by the reverse situation; Backwell was receiving more of theirnotes from the public than they were receiving of his notes. Backwell should beinitiating clearing with Lindsey and Hinton, but not with Row.

The hypothesis is that the size of Lindsay’s and Hinton’s acceptances and theiraccount deficits were correlated to the time that uncleared acceptances took toclear. The acceptances and account surpluses of Thomas Row, however, areexpected not to be correlated with the timing of clearing between Row andBackwell. The number of days acceptances took to clear serves as the dependent

TABLE 5Characteristics of Sample Banker Balances with Backwell in 1670

BenjaminHinton

JohnLindsay

ThomasRow

Allbankers

Mean 2£543 2£370 £90 2£2,452Median 2£354 2£190 £152 2£2,126Standard deviation £607 £591 £407 £6,048Minimum 2£3,026 2£3,611 2£2,243 2£17,480Maximum £238 £784 £2,402 £17,476

Source.Backwell’s Ledgers (Royal Bank of Scotland: London), EB/7–8.

421GOLDSMITH-BANKING

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

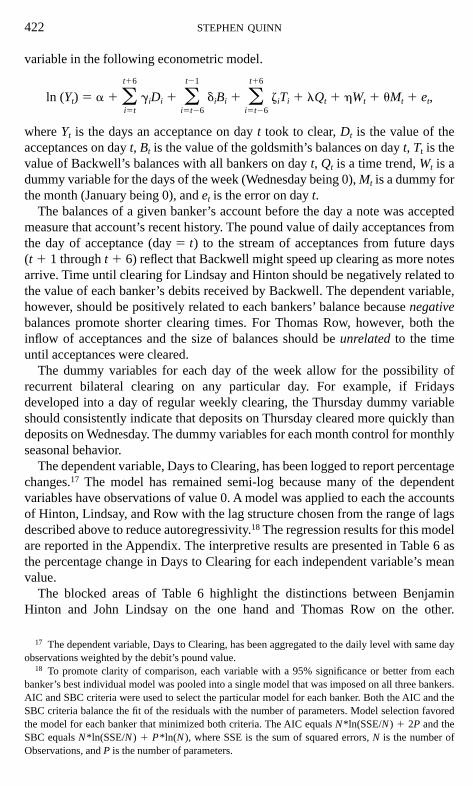

variable in the following econometric model.

ln (Yt) 5 a 1 oi5t

t16

giDi 1 oi5t26

t21

diBi 1 oi5t26

t16

ziTi 1 lQt 1 hWt 1 uMt 1 et,

whereYt is the days an acceptance on dayt took to clear,Dt is the value of theacceptances on dayt, Bt is the value of the goldsmith’s balances on dayt, Tt is thevalue of Backwell’s balances with all bankers on dayt, Qt is a time trend,Wt is adummy variable for the days of the week (Wednesday being 0),Mt is a dummy forthe month (January being 0), andet is the error on dayt.

The balances of a given banker’s account before the day a note was acceptedmeasure that account’s recent history. The pound value of daily acceptances fromthe day of acceptance (day5 t) to the stream of acceptances from future days(t 1 1 throught 1 6) reflect that Backwell might speed up clearing as more notesarrive. Time until clearing for Lindsay and Hinton should be negatively related tothe value of each banker’s debits received by Backwell. The dependent variable,however, should be positively related to each bankers’ balance becausenegativebalances promote shorter clearing times. For Thomas Row, however, both theinflow of acceptances and the size of balances should beunrelatedto the timeuntil acceptances were cleared.

The dummy variables for each day of the week allow for the possibility ofrecurrent bilateral clearing on any particular day. For example, if Fridaysdeveloped into a day of regular weekly clearing, the Thursday dummy variableshould consistently indicate that deposits on Thursday cleared more quickly thandeposits on Wednesday. The dummy variables for each month control for monthlyseasonal behavior.

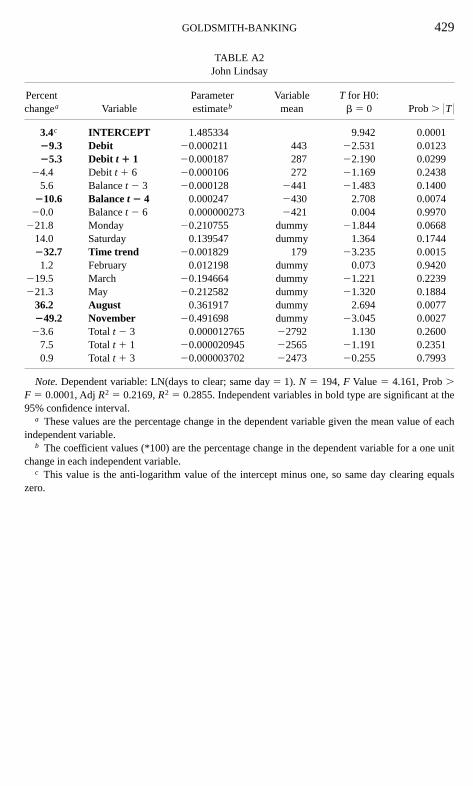

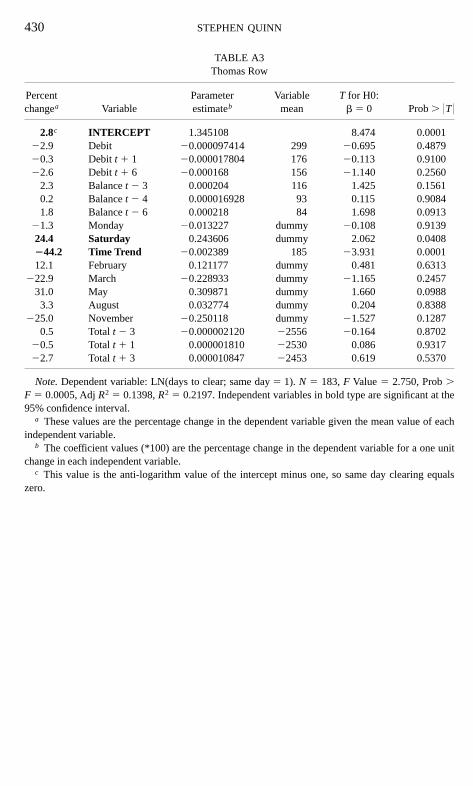

The dependent variable, Days to Clearing, has been logged to report percentagechanges.17 The model has remained semi-log because many of the dependentvariables have observations of value 0. A model was applied to each the accountsof Hinton, Lindsay, and Row with the lag structure chosen from the range of lagsdescribed above to reduce autoregressivity.18 The regression results for this modelare reported in the Appendix. The interpretive results are presented in Table 6 asthe percentage change in Days to Clearing for each independent variable’s meanvalue.

The blocked areas of Table 6 highlight the distinctions between BenjaminHinton and John Lindsay on the one hand and Thomas Row on the other.

17 The dependent variable, Days to Clearing, has been aggregated to the daily level with same dayobservations weighted by the debit’s pound value.

18 To promote clarity of comparison, each variable with a 95% significance or better from eachbanker’s best individual model was pooled into a single model that was imposed on all three bankers.AIC and SBC criteria were used to select the particular model for each banker. Both the AIC and theSBC criteria balance the fit of the residuals with the number of parameters. Model selection favoredthe model for each banker that minimized both criteria. The AIC equalsN*ln(SSE/N) 1 2P and theSBC equalsN*ln(SSE/N) 1 P*ln(N), where SSE is the sum of squared errors,N is the number ofObservations, andP is the number of parameters.

422 STEPHEN QUINN

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

Backwell’s acceptances of Row’s notes at timet andt 1 1 have poor significanceand weak coefficients relative to the estimates for the other two bankers.Lindsay’s variables for acceptances on dayt andt 1 1 are significant with strongnegative values relative to Row. Likewise, Hinton’st 1 1 acceptances aresignificant and negative. The lagged balances of each banker tell a similar butweaker story.

The regression analysis suggests that the acceptances of John Lindsay andBenjamin Hinton, both of whose accounts had negative balances, were beingcleared faster as Backwell accepted more of their debts. This relationship agreeswith the proposal that Backwell initiated clearing when he faced Hinton’s andLindsay’s growing negative balances. Moreover, the acceptances of Thomas Rowdemonstrated no strong relationship with the time acceptances took to clear andsupport the proposal that Backwell had no incentive to clear with Thomas Row inlight of new acceptances. Recall that Backwell accepted similar streams ofLindsay’s, Hinton’s, and Row’s notes from the public. The differences in theirrelationships with Backwell stemmed from the their overall account balances.

Finally, the possibility that clearing occurred consistently on some day or daysof the week for individual bankers or as a group is hard to support. Debits on

TABLE 6Percentage Change in Days to Clearing for Each Independent Variable’s Mean Value

Hinton Lindsay Row

Acceptances t 1.8 29.3 22.9Acceptances t1 1 27.1 25.3 20.3Acceptances t1 6 4.0 24.4 22.6Balance t2 3 0.7 5.6 2.3Balance t2 4 4.3 210.6 0.2Balance t2 6 210.0 20.0 1.8Monday 219.6 221.1 21.3Saturday 23.7 14.0 24.4Time Trend 240.1 232.7 244.2February 264.0 1.2 12.1March 238.8 219.5 222.9May 26.1 221.3 31.0August 2.2 36.2 3.3November 10.9 249.2 225.0Total t 2 3 20.4 23.6 0.5Total t 1 1 3.6 7.5 20.5Total t 1 3 20.2 0.9 22.7

N 5 223 N 5 194 N 5 183F Value5 5.034 F Value5 4.161 F Value5 2.750

Prob. F 5 0.0001 Prob. F 5 0.0001 Prob. F 5 0.0005Adj. R2 5 0.2360 Adj.R2 5 0.2169 Adj.R2 5 0.1398

R2 5 0.2945 R2 5 0.2855 R2 5 0.2197

Source.See Appendix.Note.Bold indicates coefficient significant at the 95% level.

423GOLDSMITH-BANKING

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

Mondays tended to clear more quickly while Saturdays definitely cleared moreslowly, but these results are easily explained by the lack of business on Sundays.Rather, clearing occurred when either banker initiated settlement. If the othergoldsmiths were like Backwell, the system enjoyed incentive compatible co-monitoring that was responsive to potential abuse. Backwell was monitoringLindsay and Hinton while Row monitored Backwell. Bilateral clearing wascreating the positive externality of network monitoring.

III. THE ‘‘GOLD BOYS’’ NETWORK

Along with co-monitoring, the system of goldsmith-banking was buttressed bythe Goldsmiths’ Company. Most new bankers to the clearing network werefiltered by apprenticeship to established goldsmith-bankers. The ‘‘old boy’’ cliqueof goldsmiths did not create an absolute barrier to entry, for the endogenous natureof the system as described above meant that existing players had an incentive totransact with newcomers. No evidence demonstrates that the network had formalrules or acted jointly to punish or exclude, but the connections created byapprenticeships and years of business dealings did create a relative advantage fornetwork members. Trust allowed for increased tolerance of uncleared balancesthat could even extend to support during runs.

Trust between goldsmith-bankers was a function of information and commit-ment. Bankers had to know that their colleagues had more to gain from futurebusiness than from fleeing London with all the bullion they could carry. Unlikethe Maghribi traders story developed by Greif (1989), London’s goldsmith-bankers could not rely on international punishment. A banker that had abscondedwould not be punishable by the group because the goldsmiths were London based.The lack of repeated play after an abuse meant colleagues had to monitor eachother’s business health, assets, and family ties. Proximity and personal historiesinteracted with business relationships to reduce the risk members faced whenholding uncleared balances.

The informal system, however, did have a formal backbone—the Goldsmiths’Company. As one of the oldest and wealthiest of London’s great livery companies,the Goldsmiths’ Company was entrusted with guaranteeing the purity of workedprecious metals. The goldsmith-bankers formed a powerful yet informal subset ofthe larger company, and the goldsmith-bankers used the Goldsmiths’ Company’sformal system of apprenticeship to train new bankers. Throughout London’strades, ‘‘seven years’ ‘genteel servitude’ remained the commonest introduction tothe world of business (Earle, 1989, p. 86).’’ In exchange for 7 years of nonwageskilled labor and often an initial fee, the master taught the apprentice thenecessary banking skills, introduced him to established bankers, and developedthe ground work for a long professional relationship.

Generations of such apprentices-turned-bankers produced lines of goldsmith-bankers related by apprenticeship. Family trees of who was apprenticed to whomemerged. Figure 2 demonstrates how early bankers like Sir Thomas Vynerproduced numerous banking off-spring by apprenticeship. Similar trees of master–

424 STEPHEN QUINN

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

apprentice relationships exist in the records of the Goldsmiths’ Company forRobert Welstead, John Lindsay, John Portman, and others. However, the sameGoldsmiths’ Company records showed that the majority of apprentices did notbecome bankers, so the process did filter potential goldsmith-bankers. Successfulapprentices, like Edward Backwell, often produced more goldsmith-bankers viaapprenticeship. For example, a chain of financiers to the English government ranfrom Sir Thomas Vyner under Cromwell, through Alderman Edward Backwellunder Charles II, and to Sir Charles Duncombe under William III. The extendedfamilies of goldsmith-bankers continued into the 18th century. Not all goldsmith-bankers might have come up through the London apprentice system, but I know ofno Restoration era examples.19

During the years covered by Backwell’s ledgers, a number of apprenticesgained their freedom and set up independent banking shops. Backwell beganclearing accounts with them soon after and sometimes even before their date offreedom. Table 7 lists goldsmith-bankers who gained their freedom of the City ofLondon and then began clearing with Backwell during the years covered by hisledgers. Included in the table is Thomas Cooke who ended his apprenticeshipunder Thomas Row in 1671 and Row himself who gained his own freedom in1664 after having been apprenticed to Edward Backwell.

Apprenticeship allowed the master and the other bankers time and proximity tojudge a newcomer. The relationships built during apprenticeships were important

19 Richard Kent was in partnership with the goldsmith Charles Duncombe, but Kent worked as arevenue officer and had no record of training with the Goldsmiths’ Company.

FIG. 2. Apprentices turned bankers (year of freedom).

425GOLDSMITH-BANKING

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

because no explicit custom or legal statement is known of that delineated who wasin or not in the system. Being a system of bilateral clearing and not a clearinghouse, the arrangements between each banker were different and personalrelationships would became important. Each banker faced no known restrictionsin tailoring his exposure to other bankers. Undoubtedly, apprenticeship generatedinformation and loyalties that supported greater ties and trust. The example inBackwell’s experience was his unique relationship with the shop of his formermaster Sir Thomas Vyner and Sir Thomas’ nephew and heir, Sir Robert Vyner.20

The Vyners occasionally ran balances of over £20,000 and even £30,000. In theextreme, the summer of 1668 saw Vyner’s debt reaching £35,000 by late June.21 In1667, after the disastrous Second Dutch War, depositors ran on Vyner. At thattime, Vyner was owed at least £1,500,000 by the Crown (Clark, 1941, p. 35). In1668, depositors remained uneasy and the Crown pressed for more funds withthreats of withholding interest payments (Roseveare, 1962).22 During that difficultsummer, Backwell appeared to have provided Vyner with substantial credit. Thisrelationship goes well beyond the behavior described in earlier sections. BecauseBackwell was also a heavy lender to the Treasury, Backwell’s support also has anelement of preventing Vyner’s run from becoming a wider panic. Because theledgers of other bankers are not extant, we cannot say if the close ties built duringapprenticeship facilitated a wider system of co-insurance. The potential remains,

20 Sir Robert Vyner assumed full proprietorship of the shop after 1665.21 Both Vyners were men of great importance—Sir Thomas received Oliver Cromwell’s first grant

of knighthood and Sir Robert was a personal friend and financier to Charles II (Clark, 1941).22 An undated letter from Sir Robert Vyner to Arlington reads, ‘‘I have beene by many accidents

much postpon’d soe yt ye money due to mee is soe farre off that I can not possible make it useful tomee. All Credit in London is much Shortened of late. I am attempting a way to enlarge my owne anddoubt not to effect it to his Maties. advantage as well as my owne, if I am (like ye lame dogg) but helptover this style.’’ PRO.SP.29/225, Cal. State Paper, DOM, 1667-8, quoted in Roseveare (1962, p. 113).

TABLE 7Apprentices-Turned-Bankers and Clearing with Edward Backwell

Apprentice MasterDate offreedom

Date of first clearingentry with Backwell

Thomas Cooke Thomas Row 19 January 1671 11 May 1671Benjamin Hinton George Day 29 June 1666 15 November 1667Joseph Horneby Edward Backwell 6 July 1666 20 August 1666Thomas Kirwood John Lindsay 4 October 1668 7 January 1669Thomas Pardo Robert Welstead 17 May 1671 8 April 1671Thomas Row Edward Backwell 15 July 1664 18 April 1664Robert Ryves Robert Welstead 16 August 1671 1 September 1671Bernard Turner Robert Welstead 8 October 1664 15 February 1665Thomas Williams Edmund Hinton 29 September 1669 3 February 1670

Sources.Goldsmiths’ Company (London), Backwell’s Ledgers (Royal Bank of Scotland: London),EB/1–9.

426 STEPHEN QUINN

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

however, that goldsmiths could use the ties of apprenticeship and clearing to aideach other during runs.

CONCLUSION

The goldsmith-banking system of Restoration London promoted the use ofbanks by offering the public mutual acceptance and monitoring. Each goldsmithaccepted rival notes without a formal coordinating institution. Instead, mutualacceptance arose endogenously as a dominant strategy Nash equilibrium. Mutualacceptance also produced positive externalities. Each participating banker en-joyed the increased demand for bank notes, orders, and bills that followed theexpansion of available outlets for those debts. The widespread use of banker-supplied media of exchange became a cornerstone of the Financial Revolutionthat occurred in England from 1660 to 1720. The successful issuance of the firstBank of England notes, for example, relied on the public’s familiarity with the useof bank notes.

The banking system of the goldsmiths was also resilient. The network with-stood fires, the plague, deaths, and a government default because no singlemember or group of bankers was essential for creating or sustaining the network’sactivities. Such systemic stability was supported by interbanker clearing andguild-based relationships. Clearing became an act of monitoring competitors thattook advantage of the acceptance information available to each banker. Statisticalanalysis of Edward Backwell’s behavior finds that the goldsmith indeed wasresponsive to the value of rival notes he accepted. This monitoring by clearingwas incentive compatible because goldsmiths faced personal losses on acceptan-ces should their rivals default. Similarly, apprenticeship within the Goldsmiths’Company tested new members and built lasting relationships.

Through mutual acceptance, bilateral clearing, and apprenticeship the goldsmith-bankers of London created a system of banking in Restoration London that was animportant part of the transition to modern payment systems. Roseveare noted:

that seventeenth century England laboured long to produce a radical tranformation of itsfinancial system which would make it the superior of any of its foreign models, and thatsome of the most important stages in that effort took place in the reign of Charles II(Roseveare, 1991, p. 3).

The goldsmiths and their system of banking were a critical background conditionfor the dramatic innovations in public finance that occurred after the GloriousRevolution of 1688. For example, North and Weingast (1989) have shown howthe constitutional changes helped the English government float more debt, butsuch a large expansion of government debt also required a banking system toconnect savers and the English Treasury. Likewise, the new Bank of Englandenjoyed an established market for bank notes. The goldsmith-bankers created apayments system within which England’s great advances in state finance couldflourish.

427GOLDSMITH-BANKING

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

APPENDIX

TABLE A1Benjamin Hinton

Percentchangea Variable

Parameterestimateb

Variablemean

T for H0:b 5 0 Prob. 0T 0

3.6c INTERCEPT 1.530942 10.992 0.00011.8 Debit 0.000056983 328 0.603 0.547527.1 Debit t 1 1 20.000336 212 23.278 0.00124.0 Debitt 1 6 0.000190 209 1.710 0.08880.7 Balancet 2 3 20.000011142 2603 20.109 0.91354.3 Balancet 2 4 20.000072824 2594 20.695 0.4878

210.0 Balancet 2 6 0.000168 2593 2.053 0.0413219.6 Monday 20.195649 dummy 21.835 0.0679

23.7 Saturday 0.236803 dummy 2.383 0.0181240.1 Time trend 20.002218 181 24.137 0.0001264.0 February 20.640407 dummy 23.721 0.0003238.8 March 20.388370 dummy 22.475 0.014126.1 May 0.261081 dummy 1.771 0.078002.2 August 0.022726 dummy 0.189 0.850410.9 November 0.109468 dummy 0.749 0.4547

20.4 Totalt 2 3 0.000001601 22792 0.146 0.88383.6 Totalt 1 1 20.000013979 22565 20.801 0.4240

20.2 Totalt 1 3 0.000000863 22473 0.061 0.9513

Note.Dependent variable: LN(days to clear; same day5 1). N 5 223,F Value 5 5.034, Prob.F 5 0.0001,R2 5 0.2945, AdjR2 5 0.2360. Independent variables in bold type are significant at the95% confidence interval.

a These values are the percentage change in the dependent variable given the mean value of eachindependent variable.

b The coefficient values (*100) are the percentage change in the dependent variable for a one unitchange in each independent variable.

c This value is the anti-logarithm value of the intercept minus one, so same day clearing equalszero.

428 STEPHEN QUINN

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

TABLE A2John Lindsay

Percentchangea Variable

Parameterestimateb

Variablemean

T for H0:b 5 0 Prob. 0T 0

3.4c INTERCEPT 1.485334 9.942 0.000129.3 Debit 20.000211 443 22.531 0.012325.3 Debit t 1 1 20.000187 287 22.190 0.0299

24.4 Debitt 1 6 20.000106 272 21.169 0.24385.6 Balancet 2 3 20.000128 2441 21.483 0.1400

210.6 Balancet 2 4 0.000247 2430 2.708 0.007420.0 Balancet 2 6 0.000000273 2421 0.004 0.9970

221.8 Monday 20.210755 dummy 21.844 0.066814.0 Saturday 0.139547 dummy 1.364 0.1744232.7 Time trend 20.001829 179 23.235 0.00151.2 February 0.012198 dummy 0.073 0.9420

219.5 March 20.194664 dummy 21.221 0.2239221.3 May 20.212582 dummy 21.320 0.1884

36.2 August 0.361917 dummy 2.694 0.0077249.2 November 20.491698 dummy 23.045 0.0027

23.6 Totalt 2 3 0.000012765 22792 1.130 0.26007.5 Totalt 1 1 20.000020945 22565 21.191 0.23510.9 Totalt 1 3 20.000003702 22473 20.255 0.7993

Note.Dependent variable: LN(days to clear; same day5 1). N 5 194,F Value 5 4.161, Prob.F 5 0.0001, AdjR2 5 0.2169,R2 5 0.2855. Independent variables in bold type are significant at the95% confidence interval.

a These values are the percentage change in the dependent variable given the mean value of eachindependent variable.

b The coefficient values (*100) are the percentage change in the dependent variable for a one unitchange in each independent variable.

c This value is the anti-logarithm value of the intercept minus one, so same day clearing equalszero.

429GOLDSMITH-BANKING

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

TABLE A3Thomas Row

Percentchangea Variable

Parameterestimateb

Variablemean

T for H0:b 5 0 Prob. 0T 0

2.8c INTERCEPT 1.345108 8.474 0.000122.9 Debit 20.000097414 299 20.695 0.487920.3 Debitt 1 1 20.000017804 176 20.113 0.910022.6 Debitt 1 6 20.000168 156 21.140 0.2560

2.3 Balancet 2 3 0.000204 116 1.425 0.15610.2 Balancet 2 4 0.000016928 93 0.115 0.90841.8 Balancet 2 6 0.000218 84 1.698 0.0913

21.3 Monday 20.013227 dummy 20.108 0.913924.4 Saturday 0.243606 dummy 2.062 0.0408244.2 Time Trend 20.002389 185 23.931 0.000112.1 February 0.121177 dummy 0.481 0.6313

222.9 March 20.228933 dummy 21.165 0.245731.0 May 0.309871 dummy 1.660 0.09883.3 August 0.032774 dummy 0.204 0.8388

225.0 November 20.250118 dummy 21.527 0.12870.5 Totalt 2 3 20.000002120 22556 20.164 0.8702

20.5 Totalt 1 1 0.000001810 22530 0.086 0.931722.7 Totalt 1 3 0.000010847 22453 0.619 0.5370

Note.Dependent variable: LN(days to clear; same day5 1). N 5 183,F Value 5 2.750, Prob.F 5 0.0005, AdjR2 5 0.1398,R2 5 0.2197. Independent variables in bold type are significant at the95% confidence interval.

a These values are the percentage change in the dependent variable given the mean value of eachindependent variable.

b The coefficient values (*100) are the percentage change in the dependent variable for a one unitchange in each independent variable.

c This value is the anti-logarithm value of the intercept minus one, so same day clearing equalszero.

430 STEPHEN QUINN

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

REFERENCES

Benston, G., and Kaufman, G. (1995), ‘‘Is the Banking and Payments System Fragile?’’Journal ofFinancial Services Research9, 209–240.

Baumol, W. J. (1952), ‘‘The Transactions Demand for Cash: An Inventory Theoretic Approach.’’Quarterly Journal of EconomicsLXVI, 545–556.

Calomiris, C., and Kahn, C. (1991), ‘‘The Role of Demandable Debt in Restructuring OptimalBanking Arrangements.’’American Economic Review81,497–513.

Calomiris, C., and Kahn, C. (1996), ‘‘The Efficiency of Self-Regulated Payments Systems: Learningfrom the Suffolk System.’’Journal of Money, Credit, and Banking28(2), 766–803.

Carruthers, B. (1996),City of Capital.Princeton: Princeton Univ. Press.Clark, D. K. (1941), ‘‘A Restoration Goldsmith-Banking House: The Vine on Lombard Street.’’ In

Essays in Modern English History,Cambridge, MA: Harvard Univ. Press. Pp. 3–47.Clapham, J. (1970),The Bank of England.Vol. I. Cambridge, UK: Cambridge Univ. Press.David, P. (1985), ‘‘Clio and the Economics of QWERTY.’’American Economic Review75,332–337.Dickson, P. G. M. (1967),The Financial Revolution in England.New York: St. Martins.Dowd, K. (1993),Laissez-Faire Banking.London: Routledge.Earle, P. (1989),The Making of the English Middle Class.London: Methuen.Goodhart, C. (1988),The Evolution of Central Banks.Cambridge, MA: MIT Press.Goodhart, C. (1991), ‘‘Are Central Banks Necessary?’’ In Capie and Woods (Eds.),Unregulated

Banking: Chaos or Order,London: St. Martin’s. Pp. 1–22.Feavearyear, A. (1963),The Pound Sterling.London: Clarendon.Gorton, G. (1985), ‘‘Clearinghouses and the Origin of Central Banking in the United States.’’Journal

of Economic HistoryXLV, 277–284.Gorton, G., and Mullineaux, D. (1987), ‘‘The Joint Production of Confidence: Endogenous Regulation

and Nineteenth Century Commercial-Bank Clearinghouses.’’Journal of Money, Credit, andBanking19,457–468.

Gorton, G. (1996), ‘‘Reputation Formation in Early Bank Note Markets.’’Journal of PoliticalEconomy104,346–397.

Gorton, G., and Pennacchi, G. (1990), ‘‘Financial Intermediaries and Liquidity Creation.’’Journal ofFinanceXLV, 49–71.

Greif, A. (1989), ‘‘Reputation and Coalitions in Medieval Trade: Evidence on the Maghribi Traders.’’Journal of Economic HistoryXLIX, 857–882.

Heal, A. (1935),London Goldsmiths.Cambridge: The University Press.Hilton-Price, F. G. (1890),A Handbook of London Bankers.London: Leadenhall.Hoffman, P., Postel-Vinay, G., and Rosenthal, J. (1995), ‘‘Redistribution and Long-Term Private Debt

in Paris, 1660–1726.’’Journal of Economic History55,256–284.Horsefield, K. (1982), ‘‘The ‘Stop of the Exchequer’ Revisited.’’Economic History Review35,

511–528.Horsefield, K. (1983),British Monetary Experiments, 1650–1710.London: Garland.Kerridge, E. (1988),Trade and Banking in Early Modern England.Manchester: Manchester Univ.

Press.Krugman, P. (1996),The Self-Organizing Economy.Malden: Blackwell.Mayhew, M. J. (1995), ‘‘Population, Money Supply, and the Velocity of Circulation in England,

1300–1700.’’Economic History ReviewXLVIII, 238–257.Melton, F. (1986),Sir Robert Clayton and the Origins of English Deposit Banking, 1658–1685.

Cambridge, UK: Cambridge Univ. Press.Miller, M., and Orr, D. (1966), ‘‘A Model of the Demand for Money by Firms.’’Quarterly Journal of

Economics80,413–435.Mitchell, D. M. (1994), ‘‘ ‘Mr Fowle, Pray Pay the Washwoman’: The Trade of a London Goldsmith-

Banker, 1660–1692.’’Business and Economic History22,27–38.Mullineaux, D. (1987), ‘‘Competitive Moneys and the Suffolk Bank System: A Contractual Perspec-

tive.’’ Southern Economic Journal53,884–897.

431GOLDSMITH-BANKING

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei

North, D., and Weingast, B. (1989), ‘‘Constitutions and Commitment: The Evolution of InstitutionsGoverning Public Choice in Seventeenth-Century England.’’Journal of Economic HistoryXLIX, 803–832.

Quinn, S. (1994), ‘‘Banking before the Bank: London’s Unregulated Goldsmith-Bankers, 1660–1694.’’ Unpublished manuscript, University of Illinois.

Quinn, S. (1995), ‘‘Balances and Goldsmith-Bankers: the Co-ordination and Control of Debt Clearingin Seventeenth-Century London.’’ In D. M. Mitchell (Ed.),Goldsmiths, Silversmiths, andBankers.London: Alan Souton. Pp. 53–76.

Richards, R. D. (1929),The Early History of Banking in England.New York: Augustus M. Kelley.Rogers, J. (1995),The Early History of the Law of Bills and Notes.Cambridge, UK: Cambridge Univ.

Press.Roseveare, H. G. (1962),The Advancement of the King’s Credit 1660–1672.Unpublished manuscript,

Cambridge University.Roseveare, H. G. (1991),The Financial Revolution, 1660–1760.London: Longman.Selgin, G., and White, L. (1994), ‘‘How Would the Invisible Hand Handle Money?’’Journal of

Economic LiteratureXXXII, 1718–1749.Temin, P. (1968), ‘‘The Economic Consequences of the Bank War.’’Journal of Political Economy76,

257–274.van der Wee, H. (1977), ‘‘Monetary, Credit, and Banking Systems.’’ InCambridge Economic History

of Europe, The Economic Organization of Early Modern Europe.Vol. V. Cambridge, UK:Cambridge Univ. Press. Pp. 290–393.

van Dillen, J. G. (1934), ‘‘The Bank of Amsterdam.’’ InHistory of the Principal Public Banks.Dordrecht: Nijhoff. Pp. 79–123.

White, L. (1987), ‘‘Accounting for Non-interest-Bearing Currency: A Critique of the Legal Restric-tions Theory of Money.’’Journal of Money, Credit, and Banking19,448–455.

432 STEPHEN QUINN

EEH 682@xyserv1/disk3/CLS_jrnl/GRP_eehj/JOB_eehj97ps/DIV_240z02 swei