governance manual for community comprehensive schools · governance manual for community &...

TRANSCRIPT

2

0

1

Governance Manual for Community

& Comprehensive

Schools

1

Community and Comprehensive Schools

Governance Manual

Index

Section Page

1. Introduction 3

2. Responsibilities of the Board of Management 5

3. The Protected Disclosures Act 2014 17

4. Registration with the Charities Regulatory Authority 17

5. Energy Management in Schools 18

6. Allocation of Funding and Teaching Resources 19

7. Estimating Funding 23

8. Monitoring of Teacher allocation & Budgets 24

9. Financial Returns 26

10. Audit 30

11. Accounting System 32

12. School Internal Controls 33

13. Purchasing 36

14. Procurement Procedures 39

15. Stock Control 41

16. Control over Assets 42

17. Receipts 43

18. Payments 44

19. Petty Cash 46

20. Bank Accounts 47

21. Banking Arrangements including Bank Overdrafts, Other Borrowing and Leasing 49

22. Payroll 50

23. Travel and Subsistence 52

24. Use of School Facilities by Outside Bodies 53

25. Insurance arrangements for Community & Comprehensive Schools 56

26. Sports Complexes 57

27. Book Grant Scheme 58

28. Book Rental Scheme 60

29. Other Activities including Fund Raising Activities carried on with the approval

of the Board of Management 61

30. Adult Education 64

31. Examination Fees and Repeat Leaving Certificate Fees 65

32. Data Protection Acts 1988 & 2003 and Data storage 67

33. Good Governance Guide to Risk Management 69

34. Health & Safety Risk Management 70

35. Student Enrolment Records 71

2

Schedule of Appendices

Appendix Page

1. Payment of Substitute Teachers employed in Community and 72

Comprehensive Schools

2. School Financial Report 73

3. Sample terms of reference for a Board of Management 85

Finance Committee

4. Circular 43/2006 Tax Clearance Procedures Public Sector Contracts 87

5. Revenue Guidance to Boards of Management on Relevant Contracts 94

Tax / Value Added Tax (revised August 2016)

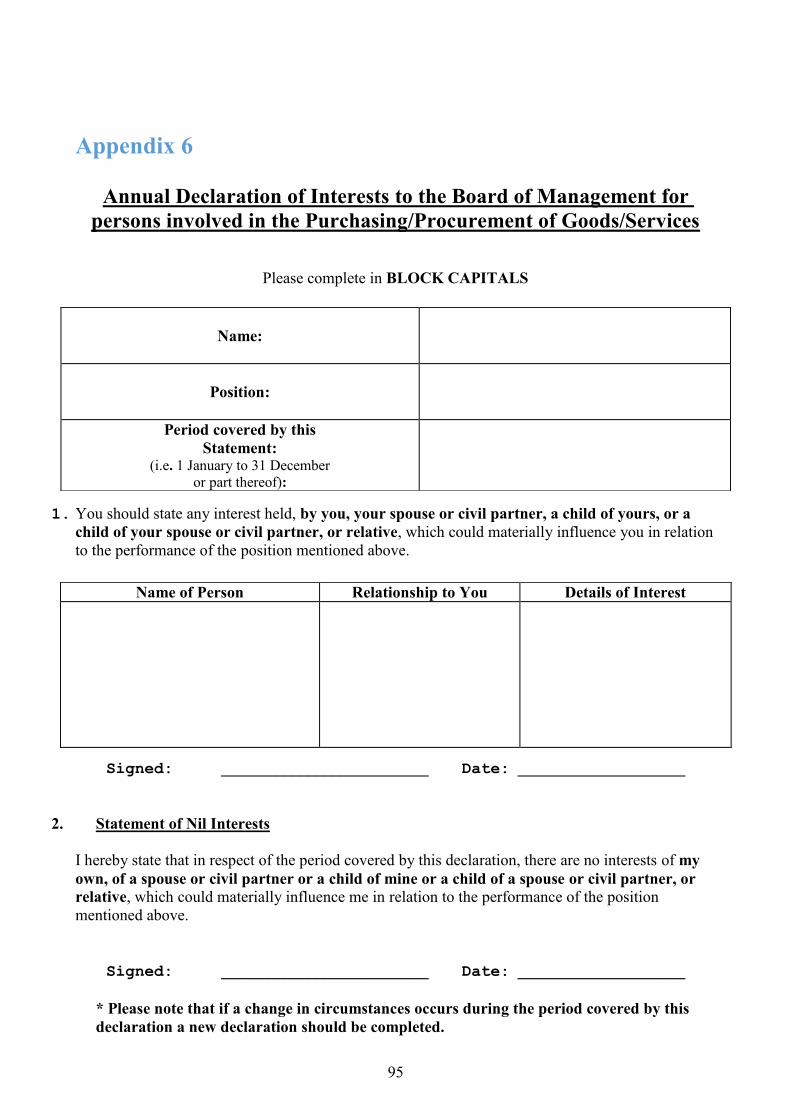

6. Annual Declaration of Interests Form for persons engaged in the purchasing/ 95

procurement of goods/services

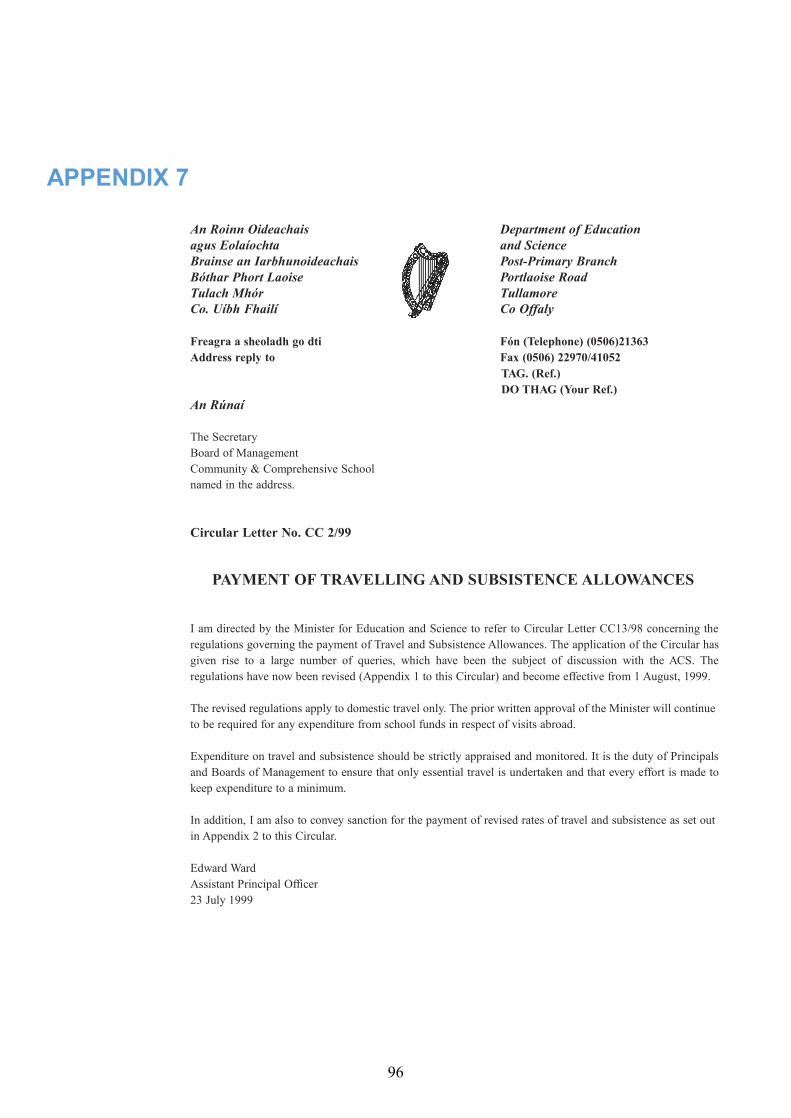

7. Circular CC 2/99 Payment of Travelling and Subsistence Allowances 96

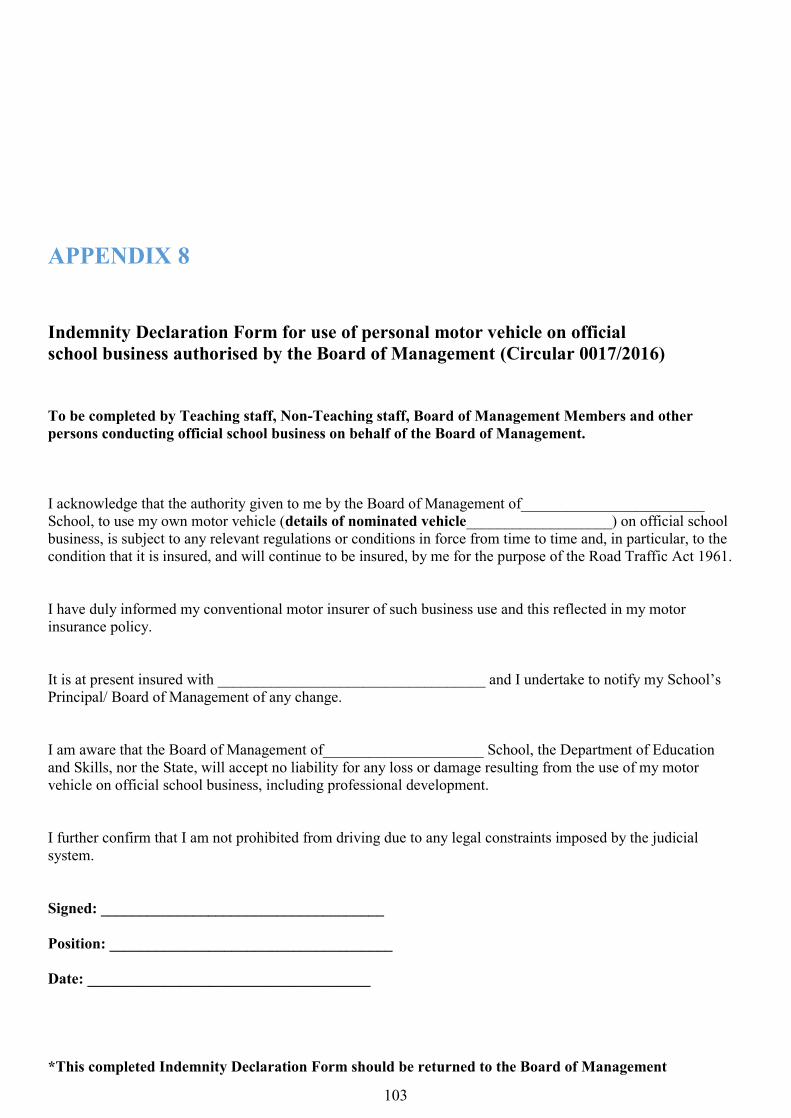

8. Indemnity Declaration form for use of motor vehicle on official school 103

business authorised by the Board of Management, (Circular 0017/2016)

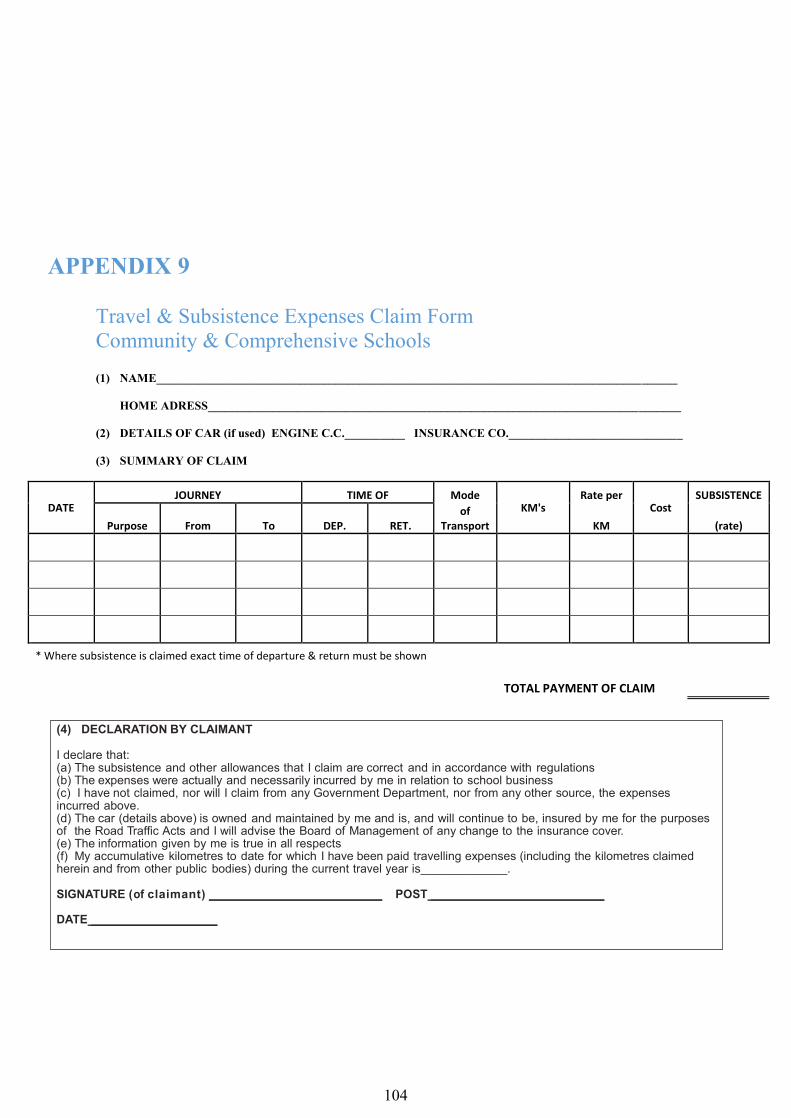

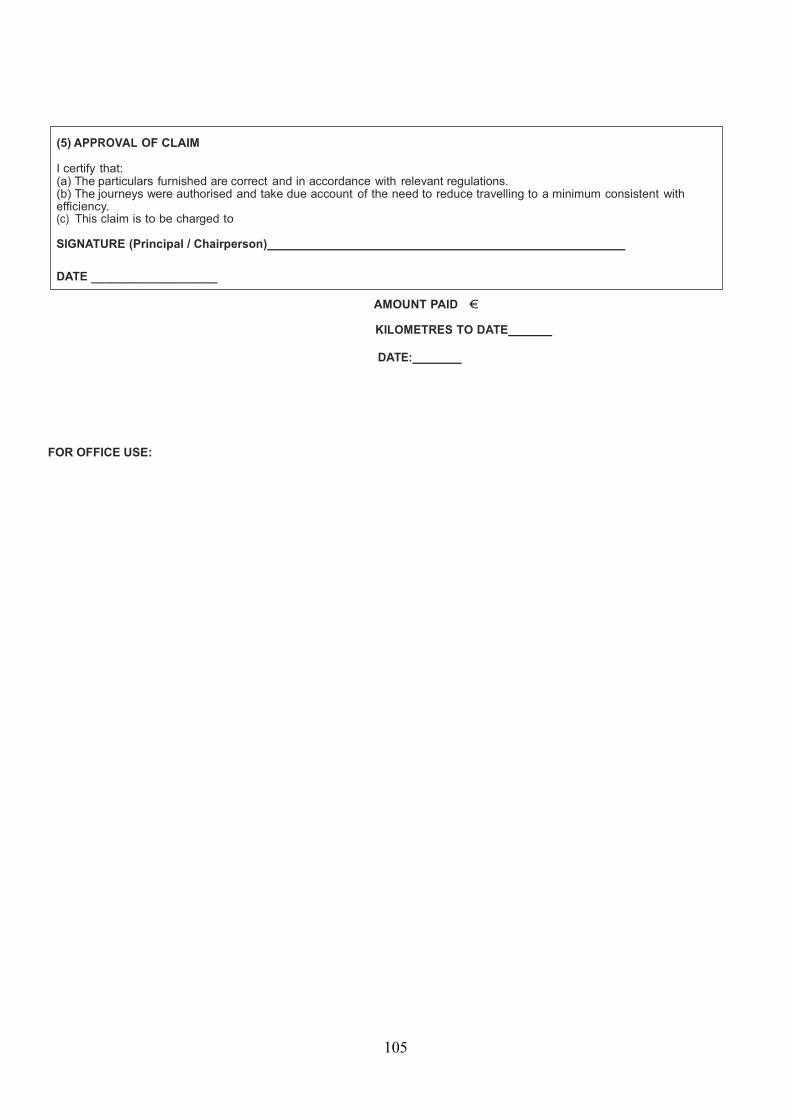

9. Travel and Subsistence Expenses Claim Form 104

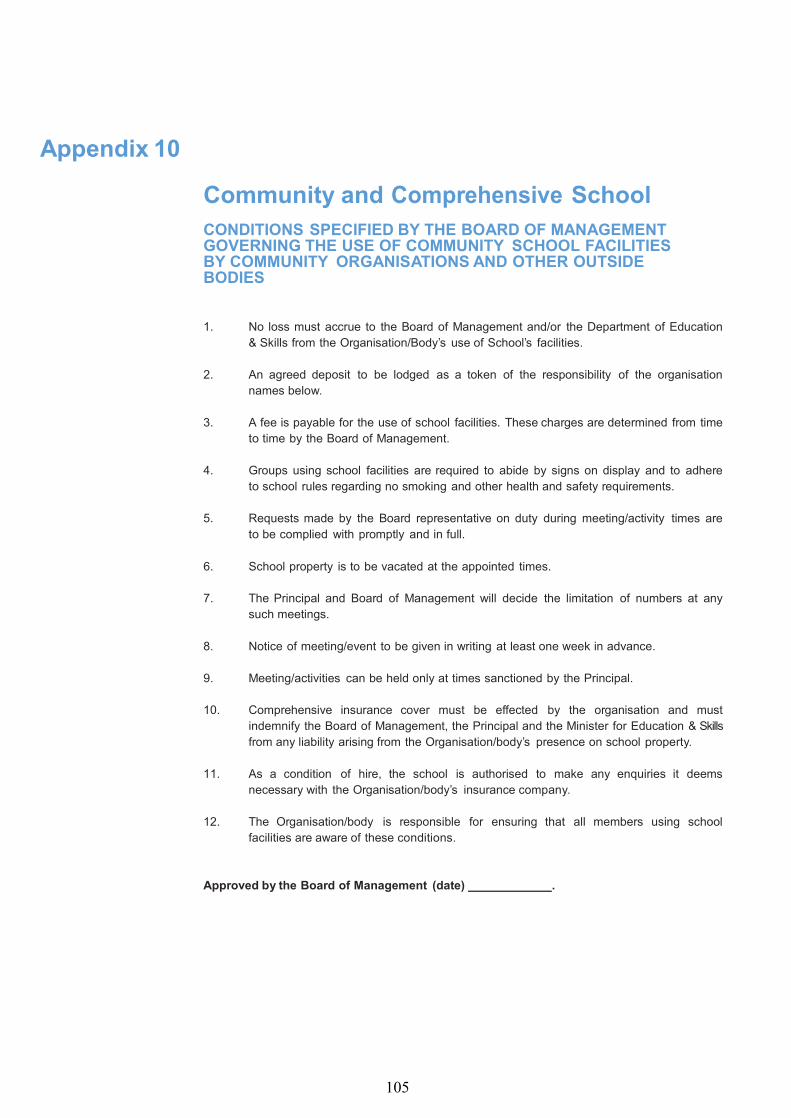

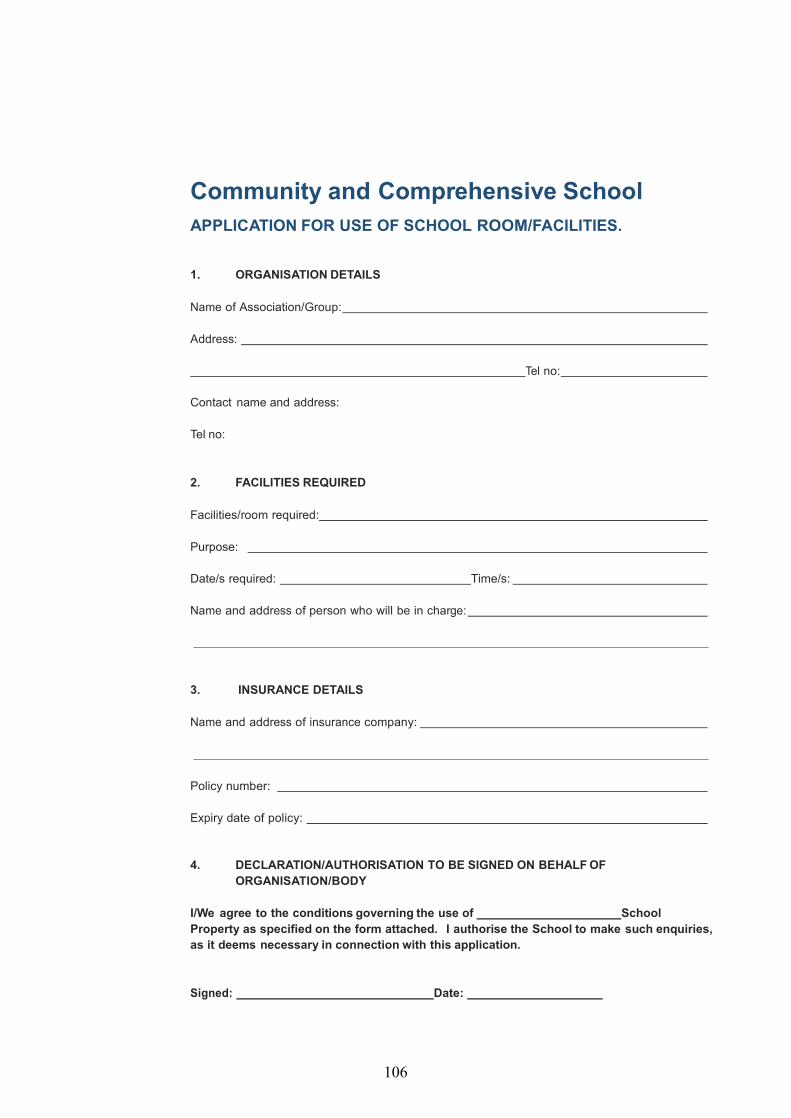

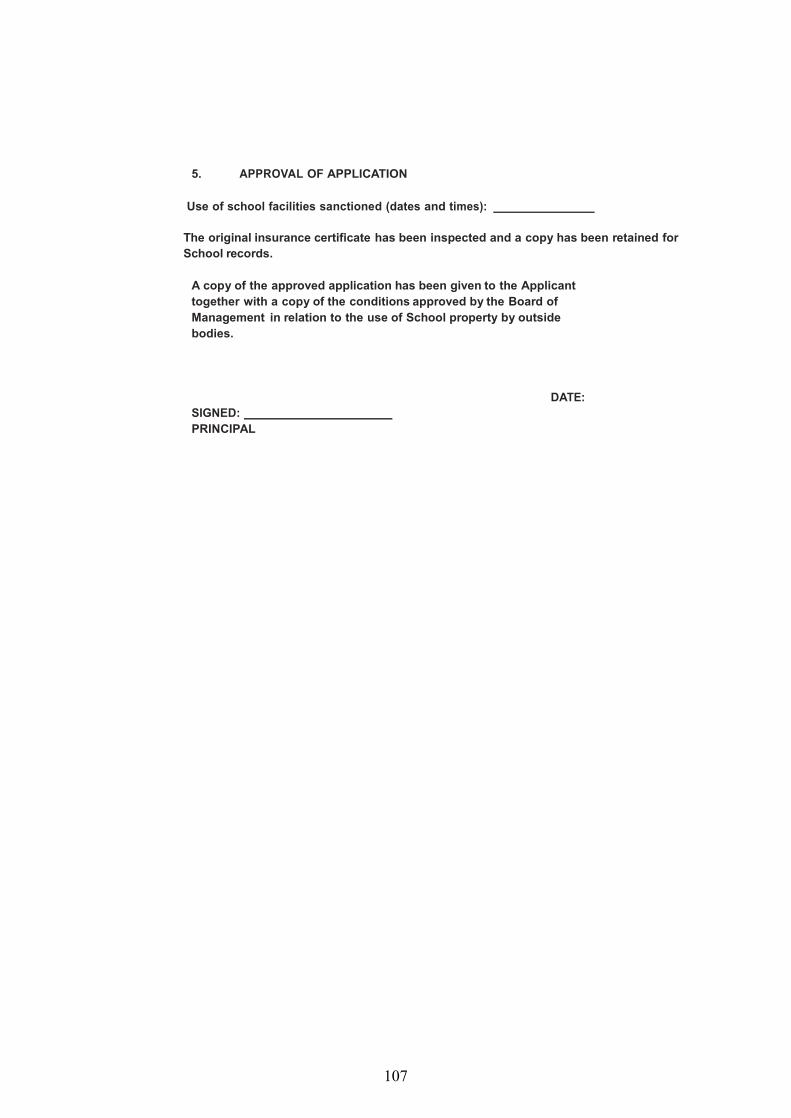

10. Requirements regarding the use of school facilities by outside bodies, 105

Application form and sample conditions

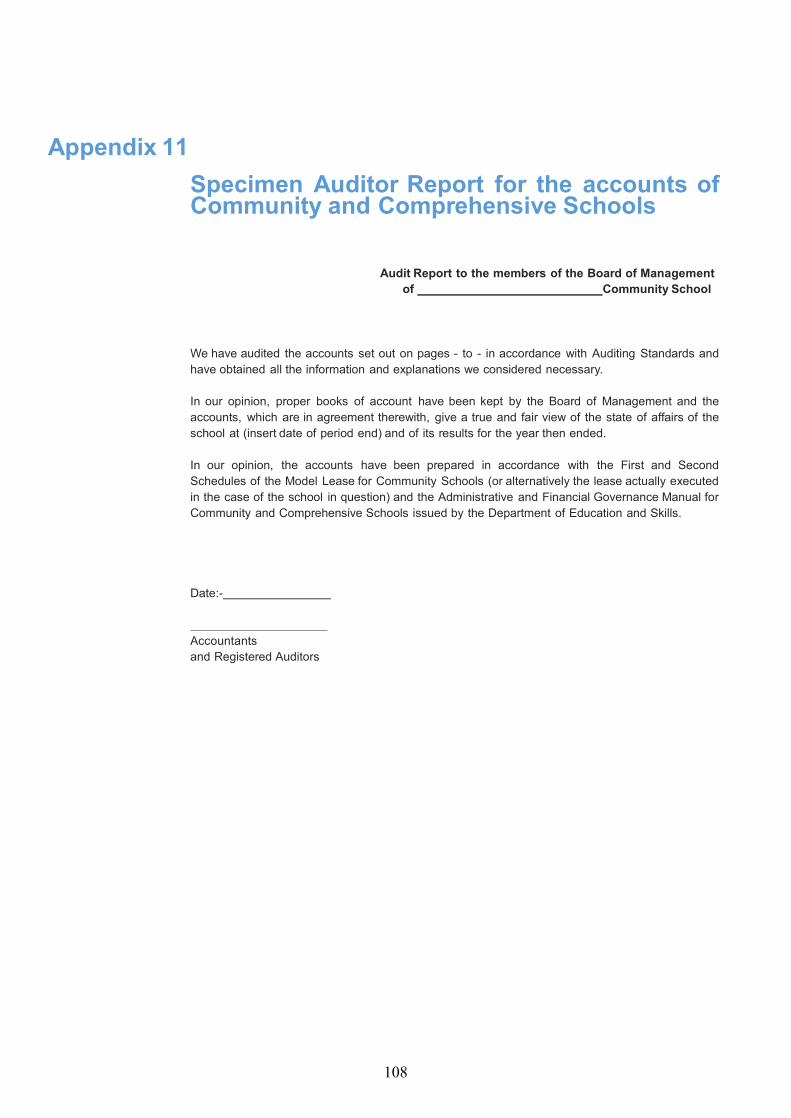

11. Specimen Audit Report in relation to fund raising by school 108

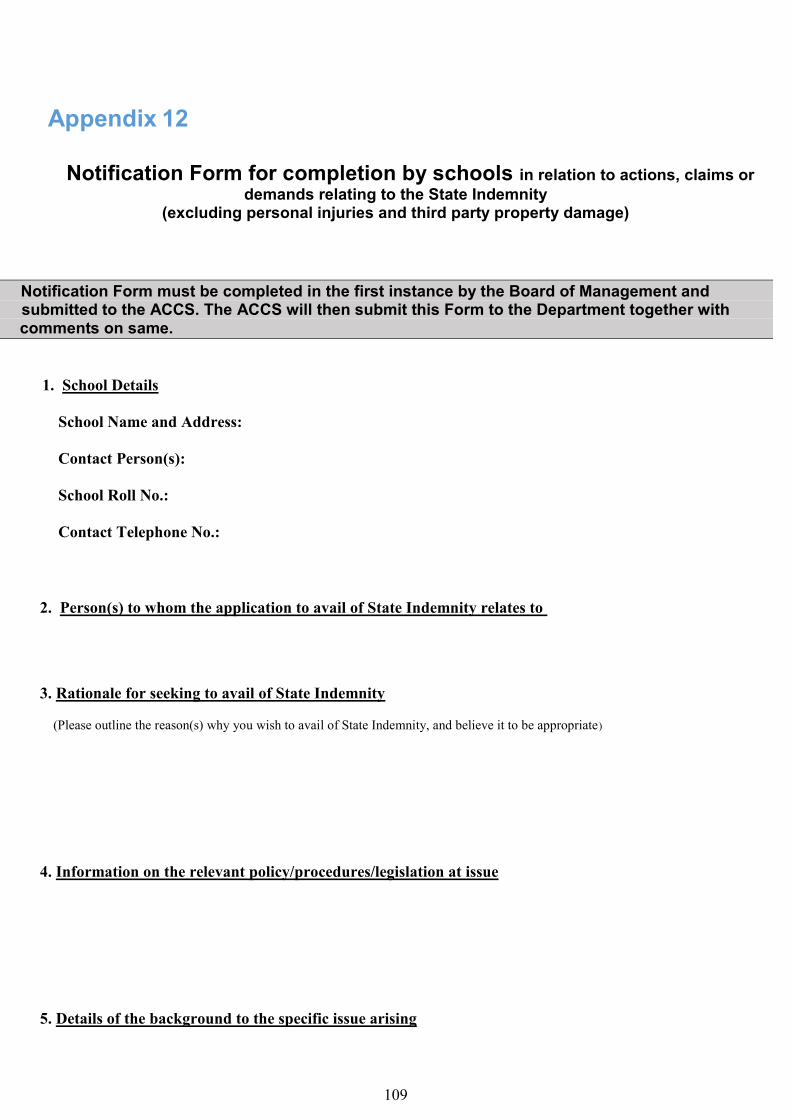

12. Notification Form for completion by schools in relation to actions, claims 109

or demands relating to the State Indemnity

(excluding personal injuries and third party property damage)

13. Procedures for processing actions, claims or demands under the State 113

Indemnity that do not come within the ambit of the State Claims Agency

14. State Claims Agency Claims (SCA) 115

15. Pensions Declaration 121

3

Community and Comprehensive Schools

Governance Manual

1. Introduction

1.1 This governance manual is intended to be read in conjunction with the First and Second

Schedules to the Model Lease for Community Schools, instruments and articles of

management for Comprehensive Schools or the lease actually executed in the case of the

individual school as appropriate.

The First and Second Schedules to the Model Lease for Community Schools are under

review at present.

1.2 It is intended to serve as a manual for Boards of Management and Principals of

Community and Comprehensive Schools as well as for the staff of the Department.

1.3 This Manual is applicable to all areas of the school's operations including activities not

funded by the Department or otherwise within the purview of the Department.

1.4 The operation of this manual will be kept under review with a view to making any

necessary amendments in the light of experience.

1.5 This manual is effective from 1st September 2016.

.

4

Any enquiries in relation to this manual may be forwarded to the address

below. Schools Division Financial Department of Education & Skills Cornamaddy Athlone Co.Westmeath Eircode: N37X659 E-mail [email protected] September 2016

5

2 Responsibilities of the Board of Management

2.1 The Board of Management is responsible for the governance and direction of the school, the use of

school resources and the management of budgetary allocations made to the school by the Minister. To

discharge its duty in this regard, the Board should ensure that there is an adequate system of control,

delegation and accountability in place to ensure the smooth and efficient operation of school services

and school administration. While the Board may delegate many of its responsibilities to the Principal

and in some circumstances to sub committees of the Board, it must remain aware of its responsibilities

and of its accountability to the Minister. Sub committees should be assigned very specific duties,

terms of reference and reporting guidelines.

2.2 The Board of Management is responsible for ensuring that the school maintains such records and

registers as are prescribed from time to time. These include minutes of Board meetings, attendance at

Board meetings, accounting records, asset register, staff attendance, pupil attendance records and

superannuation files.

2.3 The Board must decide the nature and extent of financial and other information required in order to

discharge its functions. At a minimum, the Board must receive separate financial reports at each

meeting for the School Fund and other activities outlining receipts and expenditure for period and year

to date, projected receipts and expenditure for year, calculation of surplus/deficit at year end and

recommendations regarding corrective action where necessary, a list of reconciled bank balances at a

recent date.

2.4 The Board of Management is responsible for ensuring as far as reasonably practicable, the safety and

health at work of their employees and the safety of those who are in any way affected by the work

activities of the school. The Board of Management is responsible for the maintenance, condition and

state of repair of the school premises.

The Board must take reasonable measures to secure the safety of pupils, school staff and visitors to

the school and must establish such procedures as are necessary to ensure that potential hazards are

identified and rectified as soon as possible.

The “Guidelines on Managing Safety and Health in Post-Primary Schools” set out the Board of

Management’s responsibility in maintaining a safe and healthy school environment. This guidance

also provides practical advice and tools to assist schools in planning, organising and managing a safe

and healthy school environment.

2.5 The Board of Management shall make available such reports, returns and other information to

the Minister as s/he may require from time to time.

2.6 Minutes of Board meetings should include particulars of all formal proposals brought before the

Board for decision. One copy of these minutes should be forwarded to Schools Financial Section,

Department of Education and Skills, Cornamaddy, Athlone, Co. Westmeath, N37 X659.

6

2.7 On appointment, new Board members should be apprised of their obligations and

responsibilities as set out in the First and Second Schedules to the Model Lease for

Community Schools or the lease actually executed in the case of the individual

community school as appropriate or otherwise set out by the Department. In particular,

Board members are reminded, inter alia, that:

Board members shall adhere to the requirements as set out in the First Schedule –

Instrument of Management in relation to not having a financial interest in the school.

Board proceedings are confidential and no disclosure may be made without the

authority of the Board.

Disclosures are usually delegated to the Board Chairperson or the Secretary to the Board

as appropriate.

2.8 The Deed of Trust outlines the extent of the general indemnity, which the State provides

to Boards of Management - Section 25 also refers. A Board is fully indemnified from

any claims arising in connection with the carrying out of its duties in the normal way and

in circumstances, which do not disclose a default or wrongful act on the part of the

board.

Similarly, teaching and non teaching staff carrying out their duties in accordance with

the instructions of the Board of Management as conveyed to them in the normal way are

also fully indemnified. The general indemnity does not extend to individual board

members acting in a personal capacity.

2.9 Where an individual Board member has concerns regarding aspects of a school's affairs,

it is incumbent upon that member to bring them before the Board in an appropriate

manner. In circumstances where it can be shown that a member has acted in good faith;

has made a full disclosure of the facts to the Board, in so far as these are known to

him/her at the time; it is reasonable to assume that the member has then discharged

his/her responsibility and the concerns are now the responsibility of the Board.

2.10 Board of Management members should avoid conflicts of interest. Where a situation

arises in which a board member feels that his/her objectivity or independence in relation

to a matter currently before the board is/could be impaired, immediate steps should be

taken to make a full disclosure of the circumstances to the board and the member

concerned should not take any further part in Board’s deliberations in relation to the

matter in question. Board members also should take care to ensure that they are seen to

be acting independently and without personal interest in decisions made by the Board.

2.11 The Board is not permitted to instigate court proceedings without written approval from

the Department.

The Department must be informed if the Board is joined in any court proceedings. The

Secretary of the Board of Management should contact the ACCS for support in this

regard. The State Claims Agency (SCA) should also be informed if the Board is joined

7

in any court proceedings relating to personal injury or third party property damage

claims. See Appendix 14 for further details of claims managed by the SCA.

2.12 The Board and the Patrons

It is the duty of the Board to manage the school on behalf of the Patrons. In carrying

out this duty the board is obliged to consult with and keep the Patrons informed of

decisions and proposals of the board. The Board is also accountable to the Patrons

for upholding the schools characteristic spirit and the Board must publish, in such

manner as the Patrons considers appropriate, the schools admission policy. Patrons have

a specific role in appointing the Board of Management nominating members to interview

boards.

It is essential, therefore that arrangements are in place to ensure that the Patron is

appropriately consulted in relation to Board matters and that any information

required for the Patrons role is made available to the Patron by the board.

Examples of information that must be supplied to the Patron include the Admission

Policy, School Plan, Child Protection Policy, Code of Behaviour/Anti-Bullying

Policy and any major building or refurbishment proposals envisaged at the school.

2.13 The Board as Employer

Under Section 24 of the Education Act, 1998 (as amended by the Education (Amendment) Act,

2012) the Board the Board of Management is the employer of teachers and other staff of the

School. The Board’s role as an employer includes responsibility for the recruitment and dismissal

of teachers and other staff within the school, subject to relevant Department circulars

and employment legislation.

Teachers and other staff proposed for appointment to the school will be remunerated by the

Department of Education and Skills in accordance with the numbers and levels approved by the

Department for such staff. It is the responsibility of the Board to ensure that staff are appointed

to posts in accordance with the relevant procedures and requirements outlined in Department’s

Circulars and in other agreements between the Unions and Management Bodies.

Issues with teacher performance and conduct are addressed under agreements reached

under Section 24(3) of the Education Act, 1998. Procedures in relation to professional competence

issues and general disciplinary matters are set out in Circular 60/2009.

Enquiries in relation to terms and conditions of employment or appointment procedures for

Teachers and Special Need Assistants (SNA’s) may be sent to:

8

General information regarding employers’ responsibilities is contained on

www.workplacerelations.ie

2.14 School Policies

The Board has overall responsibility for school policies. Therefore, there are a range of different

school policies that Boards will, from time to time, be involved in developing, implementing and

reviewing as appropriate. Examples include the Admission (enrolment) Policy, Child Protection

Policy, Code of Behaviour/Anti-Bullying Policy, Complaints Procedures, School Attendance

Strategy, Health and Safety Statement etc.

The extent to which a new Board will need to consider any particular school policy will depend

on the circumstances of the school in question. However, each Board must ensure that the

appropriate and necessary school policies are in place as required.

Further information on the key policy areas of Child Protection and the Code of Behaviour/

Anti-Bullying Policy is set out below.

2.15 Child Protection

Child protection and welfare considerations are relevant to all aspects of school life and the

Board must ensure that such considerations are taken into account in all of the school’s policies,

practices and activities. In particular, the Board must be familiar with and ensure that the Child

Protection Procedures for Primary and Post Primary Schools (issued under Circular 65/2011)

are fully implemented by the school. This includes ensuring that:

the Board has ratified a Child Protection Policy for the school,

a copy of the school’s Child Protection Policy which includes the names of the

Designated Liaison Person (DLP) and Deputy DLP is available to all school personnel

and the Parents’ Association and is readily accessible to parents on request,

the name of the DLP is displayed in a prominent position near the main entrance

to the school,

child protection matters are reported appropriately to the Board in accordance with

the procedures,

an annual review of the Child Protection Policy and its implementation is undertaken

by the Board.

The Child Protection Procedures for Primary and Post Primary Schools are available on the

Department’s website at www.education.ie

A Child Protection Policy template is also available on the Department’s website.

The Children First National Guidelines for the Protection and welfare of Children are available on

the Department of Children and Youth Affairs’ website www.dcya.gov.ie

9

Important Note regarding proposed Children First legislation relevant to schools and teachers.

At the time of publication of these Guidelines, the Department’s requirements in relation to child

protection are set out in the Child Protection Procedures for Primary and Post Primary Schools and

are based on Children First National Guidance for the Protection and Welfare of Children (2011).

The Children First Act, 2015, will put elements of the Children First: National Guidance for the

Protection and Welfare of Children (2011) on a statutory footing.

a) A requirement on organisations providing services to children to keep children safe and to

produce a Child Safeguarding Statement;

b) A requirement on defined categories of persons (who are referred to as “mandated persons” and

which include all registered teachers) to report child protection concerns over a defined threshold

to the Child and Family Agency(the Agency);

c) A requirement on mandated persons to assist the Agency in the assessment of a child protection risk

arising from a mandated report under the Act, if so requested to do so by the Agency;

d) Putting the Children First Interdepartmental Group on a statutory footing.

It is envisaged that the Department of Children and Youth Affairs will review and publish updated

Children First Guidance on foot of the above legislation and other recent legislation relevant to child

protection. This will also trigger some changes to the existing Child Protection Procedures for Primary

and Post-Primary Schools. The Department of Education and Skills will, in due course, consult with the

relevant education partners in this regard. It is therefore important to check the Department’s website

for the up to date position regarding same.

10

2.16 Code of Behaviour /Anti-Bullying Policy The Board must ensure that the school meets its obligations under the Education (Welfare)

Act, 2000 to have in place a Code of Behaviour that has been drawn up in accordance with

the guidelines of TUSLA/ Child and Family Agency http://www.tusla.ie

The Board must also ensure that the school has an Anti-Bullying Policy that fully complies

with the requirements of the Department’s Anti-Bullying Procedures for Primary and Post-

Primary Schools issued under Circular 0045/2013

http://www.education.ie/en/Circulars-and-Forms/Active-Circulars/cl0045_2013.pdf .

A template Anti-Bullying Policy which must be used by all schools for this purpose is provided

in Appendix 1 of the procedures.

The Anti-Bullying Procedures for Primary and Post-Primary Schools and associated Circular

0045/2013 apply to all recognised primary and Post Primary schools. The procedures are

designed to give direction and guidance to the Board and to school personnel in preventing and

tackling school-based bullying behaviour amongst its pupils. The Board and school personnel

are required to adhere to these procedures in dealing with allegations and incidents of bullying.

The Board must ensure that the school’s Anti-Bullying Policy is made available to school

personnel, published on the school website (or where none exists, be otherwise readily

accessible to parents and pupils on request) and provided to the Parents’ Association (where

one exists).

The procedures also include oversight arrangements which require that, at least once in every

school term, the Principal will provide a report to the Board of Management in relation to the

numbers of bullying cases reported to him or her and confirmation that all of these cases have

been, or are being, dealt with in accordance with the school’s Anti-Bullying Policy and the

Anti-Bullying Procedures for Primary and Post-Primary schools.

The oversight arrangements also require that the Board must undertake an annual review

of the school’s Anti-Bullying Policy and its implementation by the school. Written notification

that the review has been completed must be made available to school personnel, published on

the school website (or where none exists, be otherwise readily accessible to parents and

pupils on request) and provided to the Parents’ Association (where one exists).

See Appendix 4, Circular 45/2013

11

2.17 Management of Resources Section 15 of the Education Act, 1998 requires the Board of Management, in carrying out its

functions, to have regard to the efficient use of resources and, in particular, to the efficient use

of State funds. Boards therefore have a statutory duty to ensure that appropriate systems

and procedures are in place to ensure school resources (including grants, staffing and other

resources) are managed appropriately and efficiently and in a manner that provides for

appropriate accountability to the relevant parties.

The Board should also be fully aware of and actively involved in the oversight of the school’s

applications for all resources. The approval of joint Patrons is also required in respect of applications

for building projects.

P-Pod is a central database of Post-Primary student and some school data, which is hosted by the

Department. All Post-Primary Schools can access P-Pod via the Departments secure esinet portal

to maintain their students data. From October 2014, all Post-Primary schools were required to

make their annual return of students known as the October returns via P-Pod. The October returns

data is then used in the allocation of Teaching posts and funding to Post-Primary Schools.

All Post-Primary school authorities are required to submit a completed Certificate of Management

Authority/Principal for the specific school year in question to the Department as part of their

submission of their October returns. This includes a declaration by the school Principal that the

pupil information supplied on the schools October returns, as generated from P-Pod is complete

and accurate in respect of enrolment as at 30th September.

Boards of Management and Principal teachers are reminded about the importance of ensuring

the accuracy of enrolment returns to the Department. They have a responsibility to

immediately notify the Department of any error or irregularity in their enrolment returns. The

Department’s standard policy for cases that involve any deliberate overstatement of

enrolments is to refer them to An Garda Síochána. .

12

2.18 School Leadership

The quality of school leadership in a school is central to setting direction in the school and

achieving the best educational outcomes for pupils. Good leadership increases the overall

effectiveness of the school generally but is particularly important in the context of the effective

delivery of the curriculum, policy development and implementation, school self-evaluation and

the creation of a positive school culture and climate for all pupils and staff.

Boards of Management must be cognisant of the importance of encouraging and facilitating the

Principal and Deputy Principal and others in developing and effectively exercising this leadership

role in the school.

The Department has made considerable investment to build the professional

competence of school leaders through its support services and more recently through the

decision to establish a Centre for School Leadership. The Centre’s responsibilities will cover

the range of leadership development for school leaders, from pre-appointment training and

induction of newly appointed Principals to continuing professional development throughout

their careers.

13

2.19 School Planning

Under the Education Act, 1998 it is the responsibility of the Board to arrange for the

preparation of a School Plan, and to ensure that it is regularly reviewed and updated. The

School Plan sets out the educational philosophy of the school, its aims and how it proposes

to achieve them. Pupil learning needs are at the centre of all planning, and the focus of the

school plan should be the teaching and learning that takes place in the school.

The School Plan is not a static document. It evolves in the light of the changing and developing

needs of the school community. It must be regularly reviewed and updated. One of the first

tasks of any newly appointed Board will therefore be to give careful consideration to the

School Plan. The School Plan serves as a basis for the work of the school as a whole and for

evaluating and reporting on whole school progress and development.

14

2.20 Self-Evaluation/Teaching and Learning

Under the Education Act, 1998 a school is required to establish and maintain systems

whereby the efficiency and effectiveness of its operations can be assessed. Effective Boards

are keenly aware that self-evaluation is central to school improvement and will ensure ongoing

evaluation and review of both the overall effectiveness and efficiency of the school and of the

Board itself.

The Act places a statutory duty on the Board to ensure that an appropriate education is

provided to all of the school’s pupils. In order to effectively carry out this duty, appropriate and

regular oversight by the Board of the teaching and learning in the school should be in place.

Furthermore, the Board, from an oversight and governance perspective, can and should play

a key role in improving standards in the school.

For example, effective Boards will be actively involved in ensuring that appropriate targets are

set for improving learning outcomes, particularly in literacy and numeracy, and in monitoring how

well these targets are being achieved as part of the school’s self-evaluation process.

The Department issued Circular 40/2016, which outlines the requirements in

relation to School Self-Evaluation of teaching and learning. A dedicated website

www.schoolself-evaluation.ie also provides up-to-date information about school self-

evaluation and contains materials and resources to support schools as they engage in the

process.

The Board should ensure that a School Self-Evaluation Report and School Improvement Plan

are prepared each year and that a summary of the School’s Self-Evaluation Report and

School Improvement Plan are provided to the whole school community annually.

The Board is strongly advised to complete a legislative and regulatory checklist and to provide this

to the school community annually to evaluate the extent to which the school is adhering to its

obligations.

The focus of the Board’s considerations in relation to teaching and learning must be on

ensuring the best possible outcomes for the school’s pupils. It is important to ensure that any

such discussions do not breach pupil confidentiality. Likewise, information provided to the Board for

this purpose should be in a format that does not breach pupil confidentiality (e.g. information

aggregated by class or group, as appropriate)

15

2.21 Training for Boards

Board members are strongly advised to access relevant training to assist them in carrying out

their role. In this regard, Boards should contact the ACCS for information in relation to available

training or for advice and guidance in relation to Board matters.

The modules currently covered by such training are as follows:

The Board as a Corporate Entity – Function, Roles and the Board in action

Procedures governing the appointment of staff in schools

Board finances

Legal issues - policies and procedures arising from legislation, guidelines and circulars

Child Protection Procedures

Anti-Bullying Procedures

Data Protection

Given the importance of training in the effective operation of a Board of Management, it is

recommended that Board of Management meetings are used to regularly discuss the training

needs of Board members and available training resources. It is the responsibility of each

Board member to ensure that he or she avails of any Board of Management training that is

made available.

The school Principal and the Chairperson of the Board will normally be the main source of

information for other Board members in relation to general information and in relation to

queries regarding Board matters. Board members will also find that the websites of the ACCS

and the Department are a useful source of general information.

If such general information is not available on the relevant websites then the Board member

may seek it from the ACCS or the Department.

.

2.22 Freedom of Information Acts

A Board of Management established under Section 14 of the Education Act, 1998 other than a Board

of Management of a school established or maintained by an Education and Training Board is currently

exempt under the Freedom of Information Acts.

However, Boards of Management should note that records forwarded to a public body may be subject to

the Provisions of the Freedom of Information Acts

16

2.23 Taxation

The Board must ensure that the school is in compliance with taxation laws and ensure that all tax

liabilities are paid on or before the relevant date due. See Circular 0051/2013

http://www.education.ie/en/Circulars-and-Forms/Active-Circulars/cl0051_2013.pdf

2.24 Remuneration

The Board of Management is reminded that Government pay policy (including procedures and

Systems in relation to travel and subsistence) must be implemented, as expressed from time to time in

relation to Board members and staff and that the arrangements authorised from time to time cover

total remuneration.

The Department should be consulted in good time on any matters which could have

significant implications for general Government pay policy.

Compliance with Government pay policy or with any particular Government decision should not be

effected in ways which cut across public service standards integrity or conduct, or involve unacceptable

practices which result in a loss of tax revenue to the exchequer.

The Board is not empowered in any circumstances to award additional payments

(e.g. “top up payments”, Honoria) to any member of Teaching and non Teaching staff or to any member

of the board.

17

3. The Protected Disclosures Act 2014

The Protected Disclosures Act 2014 became law on 15 July 2014 and places a requirement

on every public body (which includes schools) to establish and maintain procedures for the

making of protected disclosures by workers who are, or were employed, by the public body

and for dealing with such disclosures.

The purpose of this Act is to protect workers from being penalised for whistleblowing about

wrongdoing or potential wrongdoing that has come to their attention in the workplace.

Key provisions in the Protected Disclosures Act 2014 include:

A prohibition on penalising workers who make protected disclosures with a wide

definition of ‘worker’.

A broad range of ‘relevant wrongdoings’ which can be reported including criminal

offences, breaches of legal obligations, where the health and safety of any individual has

been or is likely to be endangered, miscarriage of justice, unlawful or improper use of

public funds or any attempt to conceal information in relation to such wrongdoings.

A ‘stepped disclosure system’ which encourages workers to report to employers in the

first instance.

Each school is required to have appropriate arrangements in place to receive such disclosures

from its workers. It is recommended that all employers i.e. Boards of Management put a

Protected Disclosure Policy in place in addition to establishing the required procedures.

Please see the Template Protected Disclosures Policy developed by ACCS with accompanying Notification Form for a Protected Disclosure at Template Protected Disclosures Policy and Protected Disclosures Notification Form .

4 Registration with the Charities Regulatory Authority (CRA)

Under the Charities Act 2009 there is a requirement for each Board to have its school

registered with the Charities Regulatory Authority (CRA) and to verify this information

once a year.

The Department and the CRA work closely to make the registration process as simple and

straightforward as possible. The CRA can be contacted with queries by email at

18

5 Energy Management in Schools

By managing energy use effectively schools can benefit from increased comfort levels,

reduced costs and better environmental performance.

It has been shown that just by behavioural changes schools can easily save up to 10% of

their energy costs per annum. The Energy in Education programme offers a range of supports

developed by the Sustainable Energy Authority of Ireland (SEAI) in partnership with the

Department of Education and Skills designed to help schools to improve energy management

practices and save money.

The website features short videos, fact sheets and case studies on

specific areas that can be targeted along with a step by step approach on how to get started.

Guidance on energy management and details of the range of supports is available at

www.energyineducation.ie

Statutory Obligation to Monitor and Report Energy Use Annually

All public sector bodies, including schools, have a statutory obligation to report annually on

their energy usage directly to the Sustainable Energy Authority of Ireland (SEAI). All schools

were notified of this requirement in writing in December 2014 by the Department of Communications

Energy& Natural Resources (DCENR).

SEAI and DCENR have developed an on-line energy Monitoring and Reporting (M&R) system to

facilitate schools to report their energy use. As well as enabling schools to report and track energy

data annually, the online system provides:

A scorecard that presents a powerful snapshot of the school’s progress to date.

Online access to annual electricity and natural gas consumption data.

Option to share relevant data with the Office of Government Procurement’s energy

procurement framework.

There is additional information on the reporting process available at

www.seai.ie/your_business/public_sector/reporting

19

6 Allocation of Funding and Teaching Resources

6.1 Allocation in this context is intended to mean the conveyance of the approval of the

Minister for Education & Skills for the use of a certain level of resources by the Board in

meeting its responsibility for the government and direction of the school, as distinct from

any agreement to provide a certain level of exchequer funds for that purpose. These

resources take a number of forms, as indicated in the following paragraphs.

6.2 PAY

6.2.1 Pay savings cannot be used for non-pay purposes and are subject to surrender i.e. they

are taken into account in making the allocation for the following year.

6.2.2 TEACHER PAY

The initial allocation of teaching staff, in wholetime teacher equivalent posts for a

particular school year, is normally made by the Post-Primary Teacher Allocations

Section prior to the 31st of January of the previous school year. The final allocation of

teaching staff will issue in the Summer of the previous school year. Boards of

Management may not employ teachers in excess of this allocation.

The Department meets the pay and PRSI costs of the authorised permanent, CID,

temporary, regular part-time teachers and part-time teachers (Non-RPT) employed as

part of the Approved Allocation of teaching staff for wholetime day courses on behalf of

the Board and charges these payments directly to the appropriate sub heads of the Vote.

The Board may employ substitute teachers in accordance with the arrangements

approved by the Minister from time to time. The current position in regard to the

question of substitution is as outlined in Appendix 1 to the Manual.

Section 30 of the Teaching Council Act 2001 prohibits payment from public funds of

people employed as teachers in recognised schools unless they are registered with the

Teaching Council.

The Department is prohibited by law from paying any person who is employed in a

teaching post in a recognised school unless he or she is registered with the Teaching

Council. See Circulars 0025/2013http://www.education.ie/en/Circulars-and-

Forms/Active-Circulars/Requirement-For-Teachers-In-Recognised-Schools-To-Register-

With-The-Teaching-Council.pdf and 0052/2013 http://www.education.ie/en/Circulars-

and-Forms/Active-Circulars/cl0052_2013.pdf in this regard.

The Board may employ tutors for their self financing evening classes at the rates set out

in the Self-Financing Adult Education Classes Circular 57/2014

20

6.2.3 NON-TEACHER PAY

Secretarial and Maintenance staffing levels are approved by the Department for

Community and Comprehensive schools and are subject to review from time to time.

The prior approval of the Department for the filling of posts that fall vacant must be

obtained.

There has been a Moratorium on Recruitment and Promotions in the Public Service with

effect from the 27 March 2009. No appointments can therefore be made, either

permanent, temporary or by way of an acting appointment.

Any change in these arrangements arising from Delegated Sanction Agreements will be

notified separately to schools.

In exceptional circumstances the necessity to fill such posts may arise but the prior

sanction of the Department of Public Expenditure and Reform must be obtained for the

filling of these posts. See Circular 23/2009 in this regard.

Appointments of staff to permanent pensionable posts are subject to the approval of the

Minister. Recruitment procedures, terms and conditions of service, and remuneration for

non-teaching staff are generally determined in accordance with central agreements and

through central negotiations involving the schools, Government Departments and staff

interests. Recruitment procedures should be adopted by schools in accordance with best

practice and should include arrangements for public advertisement of the post to be

filled, desirable qualification criteria, competitive interview by selection board, ranking

in order of merit of candidates etc. The school must have regard to gender balance,

where appropriate, when establishing a selection committee. Current conditions of

appointment and statement of duties for Secretarial and Caretaking staff must be signed

by an appointee prior to appointment. Any proposals by the school or representations by

staff interests to amend existing provisions should be submitted to the Department at the

earliest opportunity.

The appointment and conditions of service governing the employment of temporary and

part time staff is a function of the Board subject to compliance with relevant legislative

provision and Departmental circular.

6.3. NON-PAY

6.3.1 The allocation for non-pay resources is made in respect of each financial year ending on

December 31. The allocation or budget is designed to cover normal school running costs

and the budget for each school is decided having regard to the total amount of funds

available for the sector in the year in question and estimates submitted by the schools. In

determining the amount of the allocation, account is taken of school enrolments, sports

complexes/halls and other local circumstances.

21

Excluding any additional allocations which may be made for specific programmes (viz.

Post Leaving Certificate Transition Year Programme, Leaving Certificate Applied,

Leaving Certificate Vocational Programme, Junior Certificate School Programme, etc.),

the amount allocated for non-pay represents a limit to expenditure and must not be

exceeded.

The specific sanction of the Department is required where an allocation is required to

meet exceptional needs or where planned expenditure involves a spending commitment

by the school in respect of more than one year. In addition, boards should note that:

(a) Reference to or inclusion of a particular item in the minutes of a board meeting

does not constitute a formal proposal to the Department.

(b) Such reference or inclusion does not relieve the board of the obligation to submit

proposals for sanction formally by way of letter.

6.3.2 The Emergency Works Scheme is available for situations which pose an immediate risk

to health, life, property or the environment, which is sudden, unforeseen and requires

immediate action and if not corrected would prevent the school or part thereof from

opening.

Schools requiring emergency works to be undertaken must apply under this scheme by

completing in full the Emergency Works Application and forwarding same to the School

Planning and Building Unit, Tullamore, Co. Offaly.

See Circular 0018/2011 in this regard. http://www.education.ie/en/Circulars-and-

Forms/Active-Circulars/cl0018_2011.pdf

6.4. CAPITAL

6.4.1. MINOR WORKS

Minor works of a capital nature and replacement of equipment are to be paid from a

specific allocation made to the Board as a part of the Non-Pay Allocation. This

allocation comprises a standard grant plus a per capita grant. No separate application

process is necessary.

It is not permissible except in specific circumstances approved by the Minister to use

funds made available under this heading to finance part of a major capital project or a

series of projects which, when taken together, would constitute a major capital project

and should not therefore be a charge on the School.

22

6.4.2 MAJOR CAPITAL WORKS

The Minister continues to act as client for all major capital projects. The costs of such

projects are charged, as appropriate, directly to the Education and Skills Vote.

Projects of a substantial nature, including major updating of equipment, exceeding 10%

of a school’s Non-Pay allocations (excluding minor works allocation) set out in their

School Budget letter in any year are to be treated as capital works. No commitment in

respect of such works should be entered into without the prior approval of the

Department's Planning and Building Unit. If approved the works will be carried out by

the Building Unit or as directed by them. Payment will be made by the Building Unit on

foot of appropriate vouchers and charged to the Department's capital account. Payments

for such capital items must not be charged to the School Fund.

23

7 Estimating Funding

7.1 TEACHER ALLOCATION

The Board of Management must submit particulars of enrolments as on the 30th

September of a particular year to the Parents Learners & Data Base Section of the

Department in early October in the format as specified by the Department (October

Returns). This information enables the Post-Primary Teacher Allocations Section of the

Department to determine the allocation of teacher resources for wholetime day courses

for the following school year.

7.2 PAY COSTS PAID FROM THE SCHOOL FUND

Pay costs met by the Board from the School Fund includes non-teaching pay and

additional supervision duties.

The Board must submit estimates of its requirements for non teaching pay for the

following financial year by 31st January each year. The Department sets out the precise

content and format of these estimates from time to time. The accounts for the previous

year form a significant part of the supporting information.

The estimate for non-teacher pay must show gross expenditure, anticipated

superannuation receipts, reimbursements to the School Fund for pay costs incurred on

other school activities and net demand from the exchequer. In addition, a schedule is

required showing employees, grades, rates of pay and cost of increments, and indicating

likely changes. Information will also be required on courses and pupil numbers for both

the current school year and the coming school year and on any special circumstances

likely to affect the financial requirements for the coming year.

The Department will take account of any new schools coming on stream within the

financial year and will make any appropriate provision.

7.3 NON-PAY NON-CAPITAL COSTS

The non-pay non-capital estimate excluding minor works of a capital nature, will show

the gross amount sought, anticipated receipts allocated to non-pay and the net amount

sought from the Department's Vote.

7.4 CAPITAL

The Building Unit of the Department includes an appropriate amount in the capital

estimate of the Department in respect of approved projects. The Board must provide

such information for this purpose as the Building Unit may require from time to time.

24

8 Monitoring of Teacher Allocations and Budgets

8.1 TEACHER ALLOCATIONS

Expenditure on authorised permanent, CID, temporary, regular part-time teachers and

part-time teachers(Non-RPT) employed as part of the Approved Allocation of teaching

staff for wholetime day courses on behalf of the Board continues to come within the

Department's own internal control and monitoring procedures.

Under no circumstances should the Approved Allocation of teaching staff be exceeded.

It is the responsibility of the Board of Management to ensure that over utilisation does

not occur.

8.2 NON-TEACHING STAFF

School Division (Athlone) will continue to monitor non-teaching staffing. The regular

completion and submission of the annual census for non-teaching staff is essential in this

regard.

8.2.1 SPECIAL NEEDS ASSISTANT (SNA)

The National Council for Special Education (NCSE) decides on each school’s

requirement for SNAs. This information is conveyed to the Department’s SNA Payroll

Section.

The appointment of Special Needs Assistants (SNAs) is a matter for the individual

school authority, subject to agreed procedures, and must take account of all appropriate

legislation. SNAs are paid from the central DES SNA Payroll section while notification

of claims for substitute SNAs are notified through the OLCS system. Further information

about the terms and conditions of employment for SNAs is available on the DES

website. Circular 21/11 applies.

http://www.education.ie/en/Circulars-and-Forms/Active-Circulars/cl0021_2011.pdf

Schools are required to implement arrangements as per Circular 35/16.

8.3 NON-PAY

In the case of all receipts and payments by the Board, it is the responsibility of the Board

to establish its own system of monitoring to ensure that proper budgetary control

mechanisms and procedures are in place to ensure that expenditure is planned, monitored

and controlled so as to ensure that the approved financial allocation is not exceeded. In

this regard, Boards are advised to draw up a preliminary budget at the commencement of

each year outlining income and expenditure for the year for the school as a whole under

all the various categories. This can be revised in light of final budget figures from the

Department in June of each year.

25

Where individual school departments have particular needs e.g. class materials, budgets

may then be allocated on the basis of projected needs, historical experience and having

regard to available resources. Actual expenditure will be monitored against budget on a

regular basis. Boards are also advised to set aside a contingency fund each year to meet

unforeseen non-pay contingencies, which might arise during the course of the year.

Schools will normally retain end year surpluses on non-pay.

Excesses over approved allocations are not permissible. Where it emerges that the

approved allocation for the year is likely to be exceeded, appropriate measures should be

instituted by the Board to curtail expenditure. The Department reserves the right to

reduce the allocation for subsequent years, if it considers that the circumstances warrant

such a course, or to take other appropriate action where the allocation is exceeded.

8.4 CAPITAL

Capital expenditure met by the Department, will continue to come within the

Department's own internal control and monitoring procedures.

26

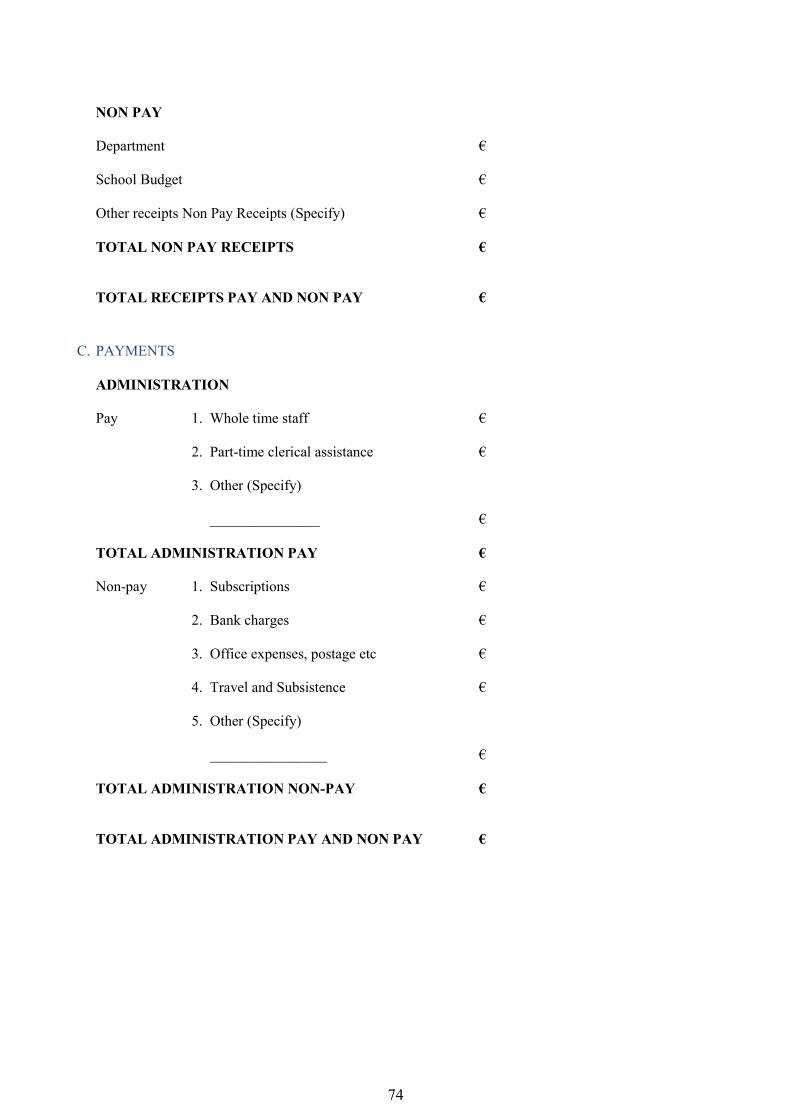

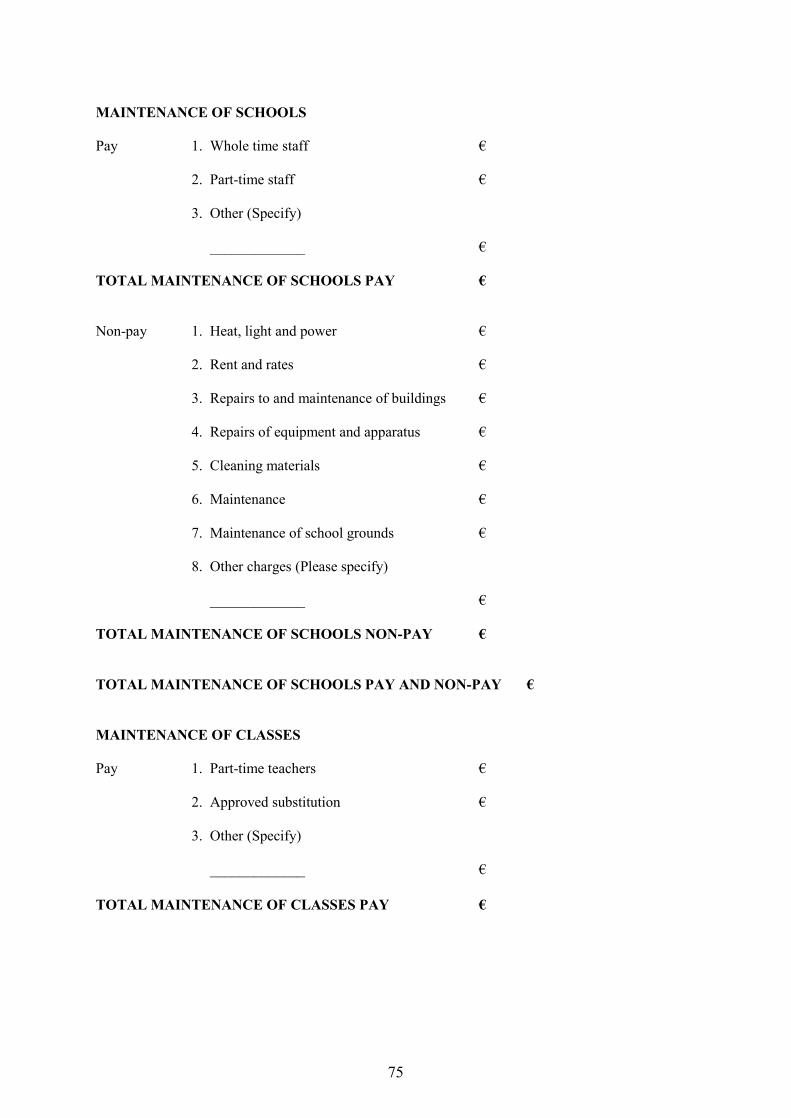

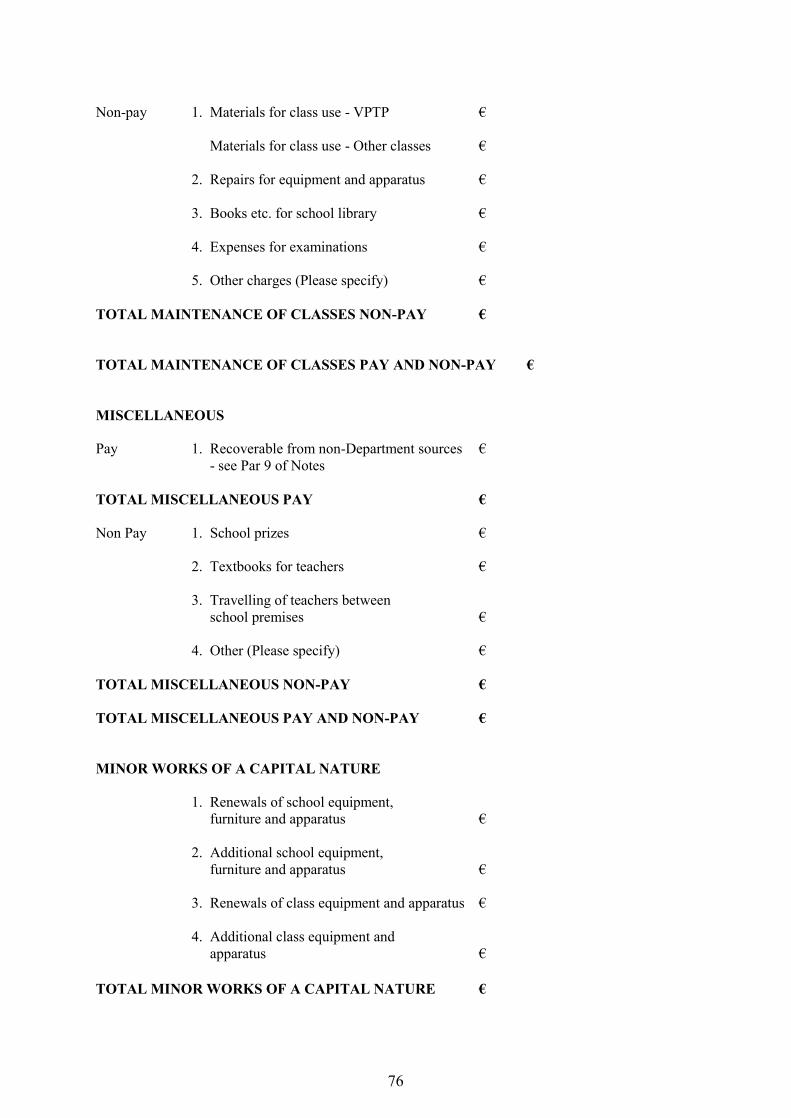

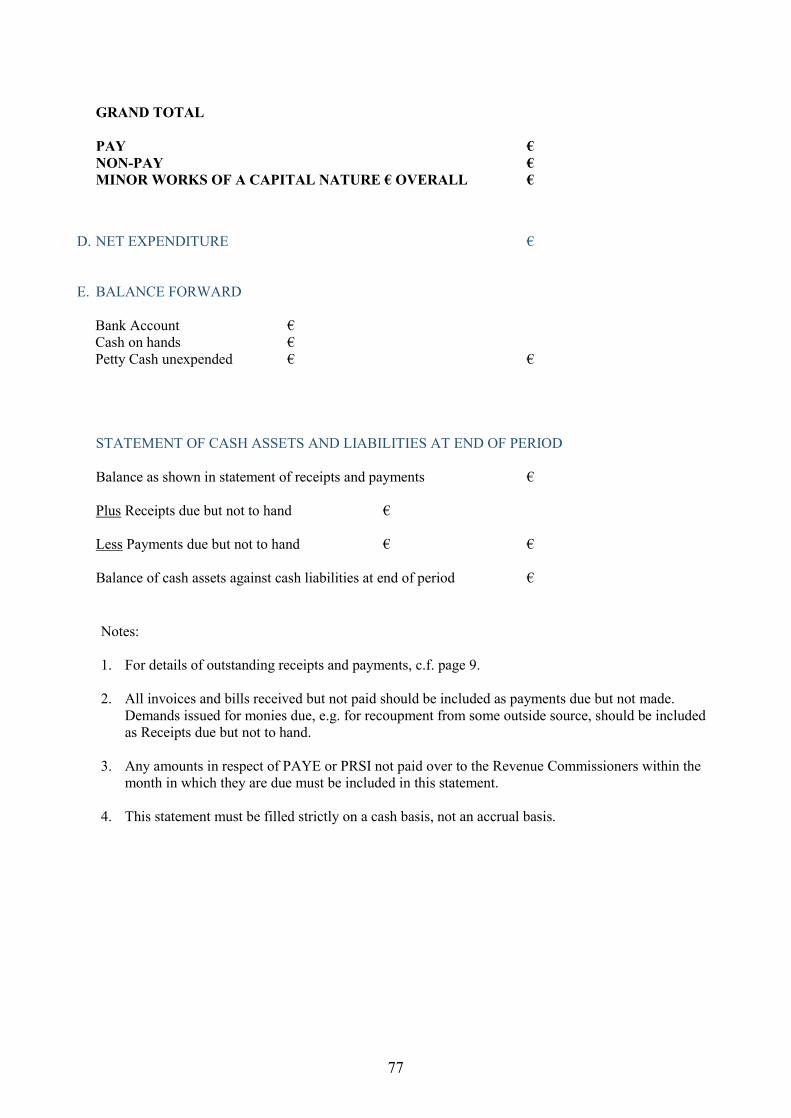

9. Financial Returns

9.1 MONTHLY FINANCIAL RETURNS

In order to facilitate the Department's own monitoring, a profile of anticipated receipts

into and payments from the School Fund, month by month for the financial year, and

agreeing with the approved gross allocation, must be submitted by the Board as soon as

the allocation for the year has been approved. A financial report, as outlined at Appendix

2 to the Manual or on a similar computer-generated form, must be submitted monthly

during the course of the financial year. These reports must show actual receipts and

payments for the month in detail (see notes to Report hereunder). They must include a

budget control statement containing the initial profile, actual receipts and payments to

date and projected receipts and payments to year end. These monthly reports must reach

the Department by the tenth working day of the following month. Copies of these reports

must be tabled at the next following meeting of the Board. A copy of the end of period

bank statement must accompany the reports for the School Fund Account. School

Division Financial Section (Athlone) monitors these returns. Original bank statements

are to be retained by the school for a minimum of seven years.

9.2 ANNUAL FINANCIAL RETURNS

The Board must prepare a financial report, in respect of each financial year ending on 31

December. The December report, as well as being a monthly report may also be used for

the purpose of the annual report. This report, must be formally approved as such by the

Board, and forwarded to the Department by Mid- February following the end of the

financial year. The completed accounts must be accompanied by such other information

as the Minister may require from time to time.

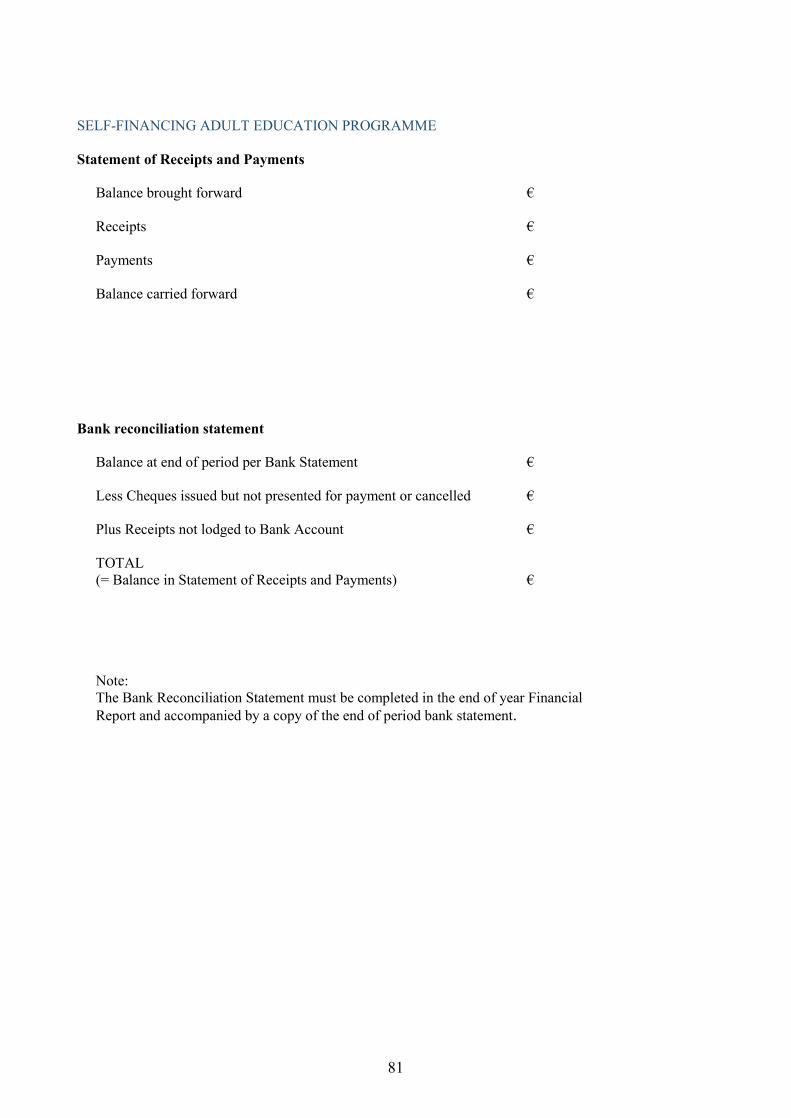

The financial details of the adult education programme must be accounted for separately

from the School Fund to the Board of Management and the Department of Education &

Skills. These details must be submitted to the Department of Education and Skills with

the financial reports.

27

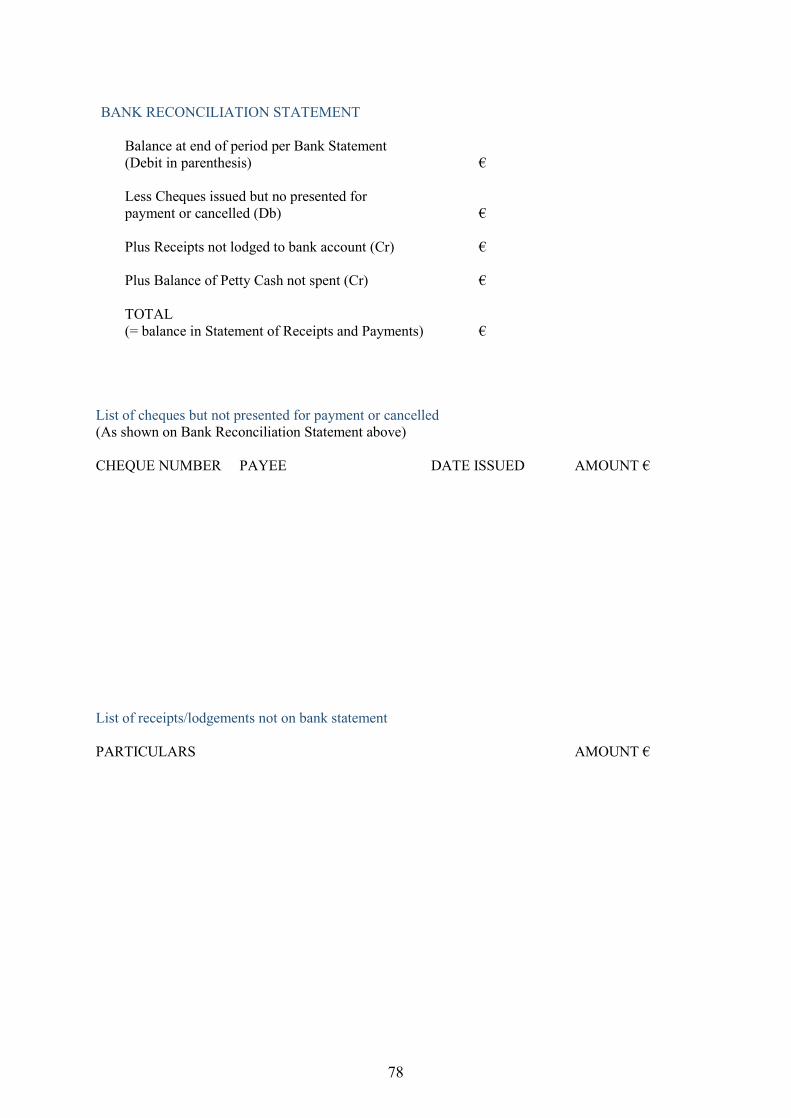

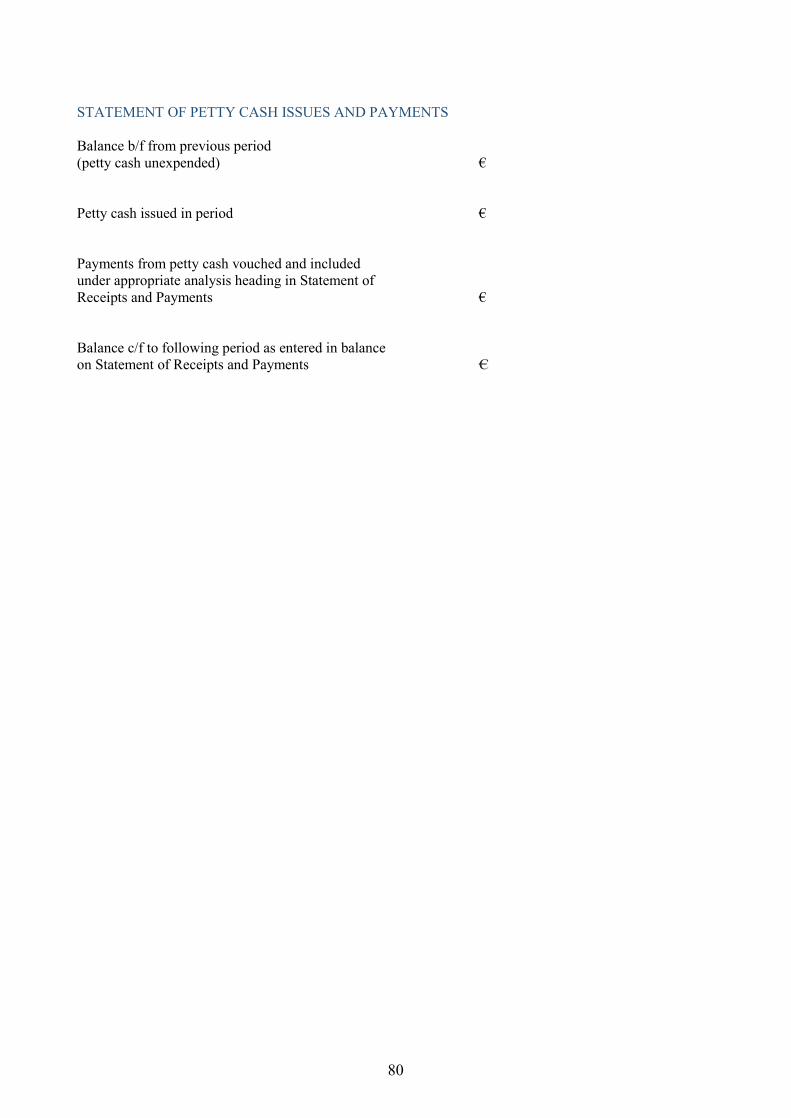

Notes to Monthly/Annual Financial Reports

1. The constituent parts of the monthly/annual financial report are:-

A statement of Receipts and Payments in respect of the School Fund.

A Bank Reconciliation Statement in respect of the School Fund.

A Statement of cash assets and liabilities of the School Fund.

A Petty Cash Statement.

A Statement of Receipts and Payments and Bank Reconciliation Statement in

respect of the self-financing adult education programme.

A School Fund Budget Control statement.

A copy of the end of period bank statement

2. The Report should be completed for each month.

The Report should also be completed for the year as a whole i.e., showing

balance at 1 January, receipts and payments for the whole year, net for year as a

whole and balance at 31 December. This may be used for the purposes of the

Annual Report to be approved by the Board and submitted to the Department.

The various accounts included in the Report are set out in linear format rather

than in double column format. This does not require an understanding of debits

and credits. It also allows them to be entered on any standard computer

spreadsheet.

3. The constituent parts of the Statement of Receipts and Payments are –

Balance at start of period €

Receipts €

Payments €

Net for period €

Balance forward €

28

4. Breakdowns will be given within the broad headings of Receipts and Payments.

These will follow the current division viz.

Administration

Maintenance of School

Maintenance of classes

Miscellaneous.

5. Payments must be analysed into pay and non-pay as at present. Receipts are not

analysed into pay and non-pay.

6. Other sub-divisions will be used to suit local management needs and the Department's

central needs. Some changes in these sub-divisions are proposed from the current

Statement.

7. Payments in the Statement must include cheques issued but not cashed or cancelled.

Receipts in the Statement must include receipts to hand but not lodged to the bank

account.

8. Where activities are undertaken on the basis of recoupment from some external source,

then both receipts and payments relative to this activity and source must be shown to

allow for verification of the recoupment.

9. Cheques issued as petty cash floats must not be shown as payments in the Statement of

Receipts and Payments. Amounts spent from petty cash (as distinct from issues of petty

cash) should be entered under the appropriate payment analysis headings when vouchers

have been received and the payments accepted. The amount of the petty cash issued and

not spent and vouched must be shown as Petty Cash Unexpended in the balance carried

forward in the Statement of Receipts and Payments.

29

10. The Budget Control Statement requires schools to prepare a profile at the beginning of

the year showing how receipts and payments within the budget will fall each month,

under appropriate category headings. It is accepted that estimation on a monthly basis

cannot be done accurately. The Budget report at the end of each month must show actual

receipts and payments for each month to date and an up-to-date estimate for each

succeeding month. The comparison between the two must show the variation from the

budget. Whether variations during the course of the year can be contained within the

total budget for the year as a whole is the most significant question, which the Budget

Report is designed to address.

11. A computer-generated report on the same format may be used instead of the manual

form supplied.

30

10. Audit

10.1 The books and accounts of the Board must be open for inspection by officers of the

Department of Education and Skills and of the Office of the Comptroller and Auditor

General. All financial records and documentation in regard to, tenders, orders, receipts,

invoices and other vouchers requisitions, store records, bank statements and all relevant

supporting documentation must be retained by the Board for a period of 7 years.

This guideline does not extend to pay and related school personnel service records, which

should be retained indefinitely within the school. The Board should ensure that it meets

its obligations in relation to the retention of all documentation.

10.2 Community and Comprehensive schools are subject to audit by the Department’s

Internal Audit Unit.

10.3 The objective of the audit is to examine the effectiveness of the management and control

systems and to assess the current level of assurance which can be attributed to the

systems in place and to make any recommendations considered appropriate. This

includes an assessment of the following:

The soundness, adequacy and application of financial and other management

controls;

The extent to which the school’s assets and interests are accounted for and

safeguarded;

The extent of compliance with, relevance to and financial effect of established

policies, plans and procedures;

The suitability and reliability of financial and other management data developed

within the school.

The audit, which is generally advised in advance, takes place over a number of days in

the school. The audit process involves detailed examination of school accounts and

records by the Department officials, assisted by school personnel having responsibility

for all aspects of the management of school finances including receipt of funds,

authorisation of payments and custody of assets. Such personnel would normally include

the Principal, School Secretary and relevant post holders in the school.

During the actual audit process itself, findings are discussed and agreed with the

Principal and other relevant staff on an ongoing basis. A full presentation of the findings

and recommendations are made to the Principal, and other relevant personnel, if

considered appropriate, at the end of the audit.

A draft audit report together with a table of findings and recommendations will issue to

the Chairperson of the Board of Management, for the Board’s consideration, following

completion of the audit fieldwork; in addition a copy will issue to the Principal and to

the Management of the relevant line section(s) in the Department, for information; or for

a management response in the event of recommendations requiring one. The Chairperson

31

of the Board of Management should respond in writing to Internal Audit Unit by the

specified deadline; having first consulted with the Principal regarding the management

response.

The response must include:

An acceptance or rejection by the Board of each recommendation;

Comments on each of the audit findings;

The Board’s proposed action in relation to each recommendation in the draft audit

report;

A proposed timeframe for implementation of each recommendation. A date must be

specified for each recommendation, even those that may be implemented

immediately.

The response, which must be signed off by the Chairperson of the Board of

Management, will be included in the final audit report. The Chairperson’s signature will

be included electronically on the final audit report as confirmation that the report is

accepted and authorised for issue.

The “final" audit report will be issued to the Department’s Audit Committee for

clearance and then to the Secretary General for approval. The report will then be issued

to the Board of Management, the Principal, the Comptroller and Auditor General and to

relevant management within the Department. It should be noted that audit reports are

subject to Freedom of Information.

As part of its procedures, the Department’s Internal Audit Unit tracks the

implementation of all outstanding recommendations on a quarterly basis. The Secretary

General and the Audit Committee are regularly updated on the implementation of all

recommendations. It is, therefore, vitally important that the most up to date position in

relation to each recommendation is accurately reflected to Internal Audit Unit during the

tracking process.

32

11. Accounting System

11.1 The Board is accountable for all activities carried on under its auspices including those

activities not financed or controlled by the Department.

11.2 The Board must keep such books and accounts as are necessary to ensure good

management, comply with any requirements set down by the Minister from time to time

and satisfy any legal requirements of the Board. These books must be kept on the school

premises and be available for inspection by Department officials and officials from the

Office of the Comptroller and Auditor General.

11.3 The Board requires complete and accurate accounting and other records to help it

manage the school, prepare financial returns and comply with Department requirements.

What constitutes an adequate accounting system depends on the size of the school and

the diversity of its activities. Accounting records must disclose with reasonable accuracy

the financial position of the school and must contain:

entries from day to day of all sums of money received (i.e. cash receipts book) and

expended by the school (i.e. cheque payments and petty cash payments books) for all

activities. These records may be kept on computer.

original supporting documentation in respect of which the receipt and expenditure

takes place

an assets register

record of amounts due to and by the school

wages and other records necessary to comply with Revenue Commissioners'

requirements

original statements for all bank accounts

Board minutes

File of tenders and contracts

student attendance records should be recorded and maintained in a format which can

readily be shared with the TUSLA requirements.

record of attendance for teaching and non-teaching staff paid by the school

Boards should keep records for a minimum period of 7 years or as otherwise

directed.

33

12. School Internal Controls

12.1 Internal controls are defined as the whole system of controls, financial and otherwise,

established by the Board in order to carry on the affairs of the school in an orderly and

efficient manner, to ensure adherence to Board and Department policies, safeguard

school assets and to secure as far as possible the completeness and accuracy of the

school records and returns to the Department.

12.2 It is the responsibility of the Board to decide the extent of the internal control system that

is appropriate to the school.

12.3 The main controls are:

Segregation of duties. This is to ensure that no one individual has complete control

over all aspects of the cash cycle i.e. receipts and payments. This reduces the risk of

intentional manipulation or error.

Physical controls limiting access to assets, school recording systems and bank

accounts.

Authorisation and approval by an appropriate person of all transactions. The limits in

this regard should be specified by the Board.

There should be procedures to ensure that staff members have the capacity to

perform the tasks assigned and receive appropriate training. Staff should also be

formally made aware of their obligations towards the Board, in particular,

maintaining confidentiality in relation to school business and the avoidance of

conflicts of interests in relation to the supply of goods and services to the school.

Job procedures and descriptions for administrative staff in their respective roles

should be fully documented and should be reviewed periodically to bring them up to

date. A contingency arrangement should be put in place for staff absences to

minimise the loss in operational functionality in the school.

The work of school staff should be supervised and checked by a person not directly

involved in a task i.e. the Principal or other nominee of the Board authorised to carry

out an independent check.

The Board should ensure that access to the school office is monitored and all

valuables, including cash and confidential files/documentation are secured

appropriately and accessible by designated staff only.

Boards should set-up and operate a Finance Sub-Committee of the Board of

Management to monitor school systems and school finances more closely.

12.4 It is recognised that schools may find it difficult to maintain a high degree of segregation

of duties. In such circumstances, the most effective form of control is the close

involvement of management in overseeing the financial affairs of the school. The Board

should as a minimum receive and inspect financial reports that show the school’s

34

performance against budget on a regular basis. Material variations should be queried and

explanations furnished.

12.5 A finance committee is a sub committee of the Board of Management established to

carry out the duties assigned to it by the Board within stated terms of reference. Such a

committee can be of major assistance to both the Principal and the Board.

In order to establish a finance committee, the Board needs to formally agree:

terms of reference and functions to be performed by the committee.

membership of the committee – this should ideally comprise the Principal and two

nominees of the Board. On occasions, the Board may also wish to invite a non-Board

member to sit on such a committee.

tenure of office.

reporting arrangements with the Board.

Sample terms of reference are as outlined at Appendix 3 to the Manual. It is not

envisaged that this type of Committee should add significantly to school overheads.

12.6 The Board is responsible for ensuring the integrity of the On Line Claims System

(OLCS) at school level and should formally approve the roles of school personnel

involved in the OLCS.

A short report should be read into the minutes of every Board of Management meeting

listing the names of all substitutes and part-time teachers for whom claims have been

made on the OLCS system since the last board meeting.

Boards should fully comply with the provisions of Circular 24/2013 (Operational

Guidelines for Boards of Management and staff designated to operate the On Line

Claims System in recognised Primary and Post Primary schools).

http://www.education.ie/en/Circulars-and-Forms/Active-Circulars/cl0024_2013.pdf

12.7 The Board of Management should implement a system in the school for recording and

monitoring absences including annual leave and sick leave of non teaching staff. Boards

of Management are responsible for the recording of absences of teachers and special

needs assistants on the OLCS.

12.8 The Board of Management should implement a timesheet or similar electronic system

for recording the hours of attendance of clerical and maintenance staff.

12.9 The Board of Management should note that employers are subject to inspection by the

National Employment Rights Authority and in this regard should be aware of their

obligations to ensure compliance with employment rights legislation. The following

document on the National Employment Rights Authority website will be of assistance.

35

http://www.workplacerelations.ie/en/Publications_Forms/Employers_Guide_to_NERA_

Inspections.pdf

12.10 In the sections which follow, the more important control considerations for each of the

main transaction streams and other matters are outlined.

36

13. Purchasing

13.1 The Board must establish a set of procedures governing purchasing and should set out

the arrangements for buying, receipt of goods and accounting, compliant with public

procurement guidelines, regulation and policy.

13.2 A purchasing policy needs to strike a balance between quality and cost, as the cheapest is

not always the best, and between cost-effective bulk purchasing and inefficient

overstocking. Registers of known suppliers must be built up for frequently required

items but occasional comparative checks must be made with prices of other suppliers.

13.3 Government Procurement: The Office of Government Procurement (OGP) was set up in

2013 to optimise value for money across the public service. This office secures savings

in the purchase of services and materials by public bodies through centralised tendering.

As our schools receive more than 50% of funding from Government we are regarded as

public bodies and subject to Department of Public Expenditure and Reform circulars on

the issue.

Schools will be notified of the relevant information emanating from the OGP pertaining

to Education and schools. The process will be outlined and explained in detail through

DES circulars with additional information on the practical supports needed being

delivered by ACCS e.g. : Photocopying and Multi-Purpose Office Paper Contract. See

Info Bulletin 21/13 on ACCS website. www.accs.ie.

13.4 As an integral strand of the Government’s overall reform programme for public

procurement - the Schools Procurement Unit (SPU) has been established within the JMB

Secretariat of Secondary Schools. The Schools Procurement Unit (SPU) acts as the

central coordinating function for procurement for all schools including schools in the

Community and Comprehensive (C & C) sector. The SPU has responsibility for issue of

guidelines for all schools and will have a central role in communicating procurement

requirements and opportunities to schools, driving and measuring compliance to central

contracts and managing procurement data across the school sectors.

Information on SPU is contained on the JMB website http://www.jmb.ie/school-

procurement.

13.5 For Goods & Services not covered by the OGP, evaluation of proposals from third

parties must take place to establish:

• That the proposal is of clear benefit to the school.

• That the expenditure on the proposal will represent value for money.

• That the proposal does not expose the school to any undue financial or other risk.

• That the third party has the capacity to provide the goods and or/services

concerned. In this regard, thorough and robust due diligence must be undertaken

prior to entering into a contract.

13.6 Boards must take reasonable steps to satisfy themselves that suppliers and contractors

engaged are reputable and competent and are registered with the Revenue authorities in

the State.

37

13.7 In the case of all public sector contracts of a value of €10,000 (inclusive of VAT) or

more within any 12 – month period, the contractor (and agent as appropriate) will be

required either to

• Produce a current tax clearance certificate, or,

• Demonstrate a satisfactory level of subcontractor tax compliance

See links to Revenue website:

Revised procedures for Tax Clearance in respect of Public Service Contracts,

Grants, Subsidies and similar type payments. (Department of Finance Circulars 43/2006)

updated 26th July 2012

http://www.revenue.ie/en/tax/rct/tax-clearance-arrangements.pdf

Guidelines for Tax Clearance (July 2016)

http://www.revenue.ie/en/tax/it/leaflets/guidelines-tax-clearance.html

eTax Clearance FAQs (July 2016)

http://www.revenue.ie/en/online/etax-clearance-faqs.html

See Appendix 4 for further details on Circular 43/2006.

13.8 With effect from January 2012, new requirements were introduced by the Revenue

Commissioners in relation to the operation of Relevant Contracts Tax (RCT). RCT is a

tax regime applicable to construction contracts in which tax is deducted by a principal

contractor from payments due to a contractor for construction operations. School Boards

of Management are regarded as “Principal Contractor”. This means that the Board of

Management undertaking works funded by the Department will be responsible for

complying with RCT requirements and VAT returns when making payments to their

Contractor. All filings and notifications must be done online through the Revenue Online

System (ROS).

A Guidance Note (August 2016) for Boards of Management outlining the responsibilities

of the Board in relation to RCT and VAT is contained on the Revenue Commissioners

web-site. In order to ensure compliance Boards should access the relevant related

information on the following link. (See Appendix 5 also)

Guidance Note Boards of Management -Relevant Contracts Tax/Value Added Tax

13.9 All purchases excluding routine items such as telephone, ESB and petty cash purchases

should be made on foot of an approved order certified by the Principal. Pre-numbered

triplicate order books should be used for this purpose. Purchase orders should be

completed in triplicate and signed off as approved by the Principal in all cases. The

original purchase order should be forwarded to the relevant supplier, the second copy

should be associated with the invoices relating to the goods received and the third should

remain in the purchases order book.

13.10 Competitive tendering procedures as described in Section 14 below should always be

used for the purchase of goods and services.

38

13.11 Tendering procedures must also apply in the case of once off purchases, see Section 14,

paragraph 14.3

13.12 It is accepted that in respect of certain services (e.g. electrical, plumbing) which are

required regularly and often at short notice that it may be more practical to select

one/two contractor(s) whose services are called upon as required without the need to

seek advance quotations for each task. In these cases, periodic comparison of prices and

quality of service between a number of contractors in the area will suffice.

13.13 A file containing evidence of the tendering and quotation procedures actually followed

must be retained for inspection if required.

13.14 Other considerations are:-

• procedures for issuing and authorising orders

• safekeeping of order books

• special requirements in relation to the authorisation of major purchases.

• assignment of responsibilities for checking supplier’s invoices and statements,

goods returned, maintaining records and authorising invoices for payment.

• the need to check individual invoices both as regards quantity and pricing before

being authorised for payment. Checking would involve examination and cross

referencing of the invoice to the purchase order, goods delivery note, evidence as

to quantity and the condition of goods delivered and evidence that service has been

supplied to a satisfactory standard.

13.15 Board members and all other staff with responsibility for purchasing/procurement must

complete an annual Declaration of Interests form Appendix 6. A register of interests

should be maintained by the Board of Management in order to avoid conflicts of interest

arising.

13.16 It is recommended that an overall quotation, rather than an hourly rate, be sought from

any service provider. All payments for travel costs should be calculated on the basis of

distance travelled rather than on time spent.

39

14. Procurement Procedures

14.1 Central frameworks and contracts are available from the Office of Government

Procurement (OGP) and should be used in preference to undertaking individual

procurement exercises. The Schools Procurement Unit is available to support and advise

in procurement matters.

14.2 Competitive tendering should be standard procedure in the procurement process of

schools. The Board should ensure that there is an appropriate focus on good practice in

purchasing and that procedures are in place to ensure compliance with procurement

policy and guidelines.

It is the responsibility of the Board of Management to satisfy itself that the requirements

for public procurement are adhered to and to be fully conversant with the current value

thresholds for the application of EU and national procurement rules.

In this regard, EU directives and national regulations impose legal obligations in regard

to advertising and the use of objective tendering procedures for awarding contracts

above certain value thresholds. See www.procurement.ie or www.etenders.ie for more

information.

Information on procurement policy and general guidance on procurement matters is

published by the Office of Government Procurement. This can be viewed or downloaded

from the national public procurement website www.etenders.gov.ie.

14.3 The thresholds that apply for procurement are as follows (January 2014);

• Less than €5,000 – Informal procedure, obtain at least 2 quotes

• €5,000 to €25,000 – Obtain at least 3 written quotes

• €25,000 to €134,000 – Advertise on e-tenders website

• Above the EU threshold (€134,000) – advertise on e-tenders and on the Official

Journal of the EU

14.4 The Board must determine in advance the tendering procedure to be used in each case. It

is important that no allegation of impropriety arise during the process either in relation to

commercial confidence or fair treatment. The procedure must include the following

features:

• Generally, three tenders must be obtained and more than that sought lest all

invitations to tender are not accepted.

• The invitation to tender may be issued directly to firms which would be capable of

carrying out the contract or supplying the goods and are of good professional

standing.

• The invitation should be standard for all firms invited and contain adequate

information concerning the scope and nature of the contract. Tenders invitations

must be based on adequate specifications which must be in generic terms rather

than in terms of particular brands. It should be clearly indicated that it is a

condition for the award of the contract that a firm or individual must comply with

tax clearance procedures where applicable.

• A date for receipt of tenders must be specified.

40

• All tenders should be opened together at the date and time set for receipt of

tenders. No tender should be opened in advance nor should any tender information

that may have become available through a casual remark from a supplier for